Deep dive explainer on Convex Finance, the Curve yield amplifier and meta-governance layer. Covers CVX, cvxCRV, vlCVX, Curve Wars, bribes, integrations (Resupply, Napier, LlamaLend), risks, and the evolving role of liquid lockers in DeFi.

- x.com28

- convexfinance.medium.com2

- vote.convexfinance.com2

- vxtwitter.com1

- dlnews.com1

- wavey.info1

- curve.convexfinance.com1

+1 sources across the wider coverage universe

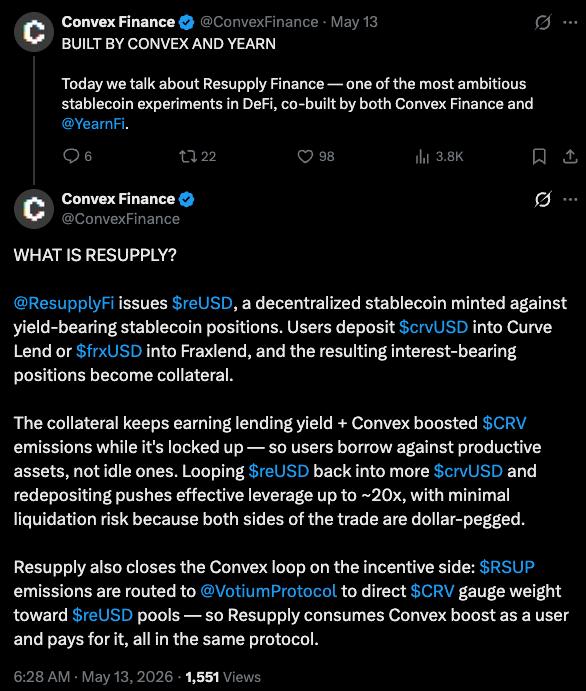

Convex recaps the history of Resupply ($RSUP) and its $reUSD stablecoin backed by yield-bearing positions in Curve Lend and Fraxlend2026-05

Convex recaps the history of Resupply ($RSUP) and its $reUSD stablecoin backed by yield-bearing positions in Curve Lend and Fraxlend2026-05 Convex Finance rose from Curve’s vote-escrow model to dominate the Curve Wars, centralizing veCRV power and reshaping DeFi governance.2026-02

Convex Finance rose from Curve’s vote-escrow model to dominate the Curve Wars, centralizing veCRV power and reshaping DeFi governance.2026-02 Convex Finance turned DeFi governance’s biggest weaknesses—low participation and concentrated power—into a system advantage by optimizing around liquidity coordination and incentive routing rather than idealized voting. By monetizing governance through bribes and veCRV control, Convex built a durable revenue engine that has survived multiple market cycles.2026-01

Convex Finance turned DeFi governance’s biggest weaknesses—low participation and concentrated power—into a system advantage by optimizing around liquidity coordination and incentive routing rather than idealized voting. By monetizing governance through bribes and veCRV control, Convex built a durable revenue engine that has survived multiple market cycles.2026-01 Perry breaks down the Curve War, explaining how veCRV became DeFi’s “Liquidity Stone,” directing emissions, incentives, and power. From StakeDAO and Yearn to Convex’s dominance, control of veCRV ultimately meant control of liquidity flows across Curve.2026-01

Perry breaks down the Curve War, explaining how veCRV became DeFi’s “Liquidity Stone,” directing emissions, incentives, and power. From StakeDAO and Yearn to Convex’s dominance, control of veCRV ultimately meant control of liquidity flows across Curve.2026-01 Convex Finance co-founder Winthorpe suggests an intermediate "stopgap" funding proposal is in the works, following a chilly reception to the 2026 Swiss Stake funding request2025-12

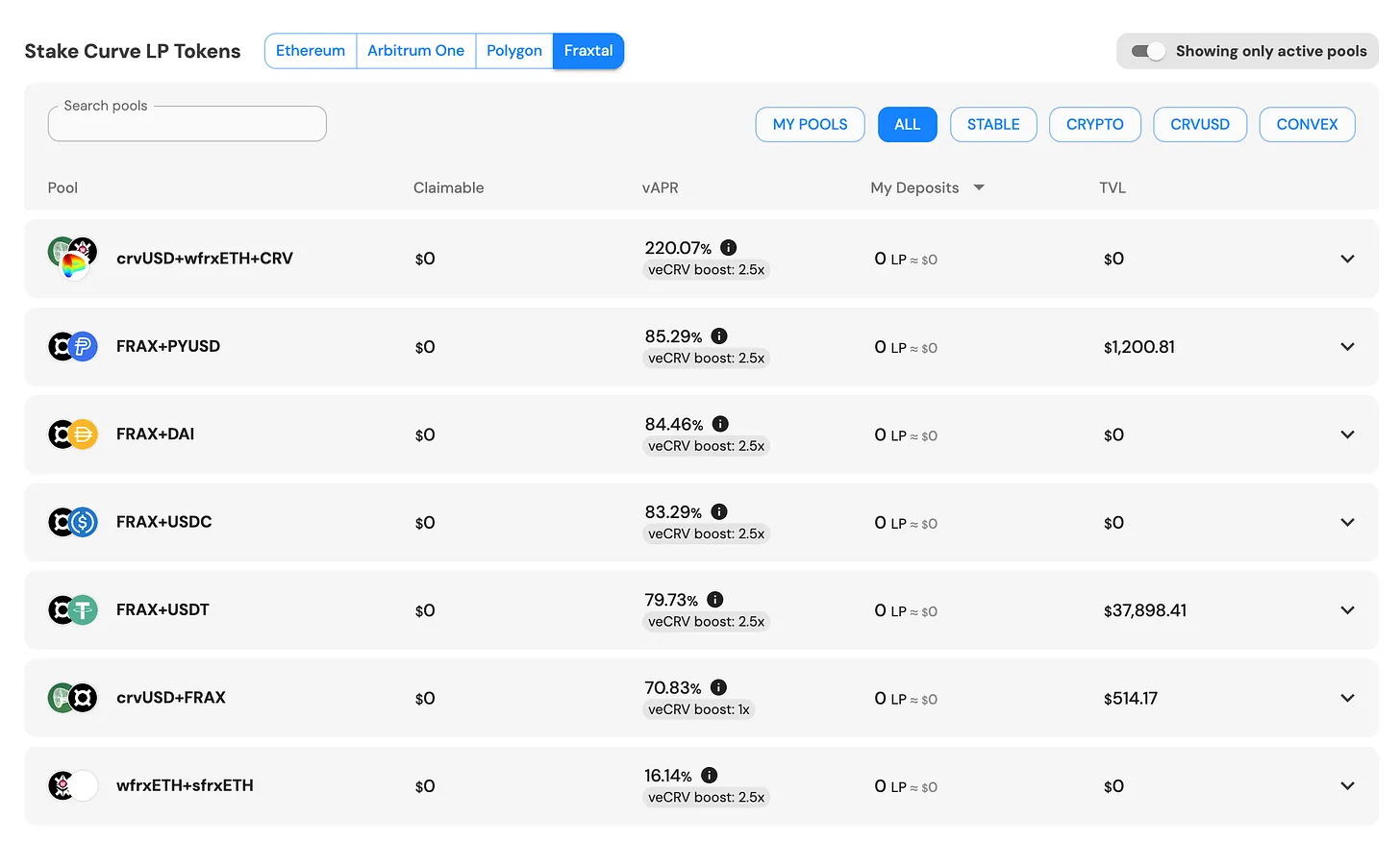

Convex Finance co-founder Winthorpe suggests an intermediate "stopgap" funding proposal is in the works, following a chilly reception to the 2026 Swiss Stake funding request2025-12 Convex adds support for Curve pools on Fraxtal chain, the third sidechain supported after Arbitrum and Polygon2024-03

Convex adds support for Curve pools on Fraxtal chain, the third sidechain supported after Arbitrum and Polygon2024-03

Convex Finance: A Deep Dive into DeFi’s Curve Yield Amplifier and Governance Powerhouse

Convex Finance is a decentralized finance protocol built on top of Curve that aggregates CRV and liquidity provider positions to deliver boosted yields and concentrated governance power, turning Curve’s vote-escrow model into a coordinated, revenue-generating meta-layer for both users and protocols. By pooling veCRV and routing votes via its own governance token, CVX, Convex has become a central actor in the so‑called Curve Wars, reshaping how liquidity, incentives, and political power flow through one of DeFi’s most important stablecoin ecosystems.

Curve, veCRV, and the Coordination Problem Convex Set Out to Solve

Understanding Convex begins with understanding Curve Finance itself. Curve is an automated market maker optimized for low-slippage trading between assets that should trade at near-parity, such as stablecoins or closely correlated assets. Unlike constant-product AMMs, Curve uses a stableswap-style bonding curve that concentrates liquidity around the peg, enabling deep stablecoin liquidity and efficient routing for the broader DeFi ecosystem. As Curve expanded beyond simple stablecoin pairs to include pooled crypto assets and more exotic configurations, it also became a foundational liquidity layer, with countless protocols routing stablecoin, derivative, and LSD liquidity through Curve pools.

Curve’s token, CRV, is at the center of its incentive and governance design. Holders can lock CRV for up to four years to obtain vote-escrowed CRV, or veCRV, which confers three key benefits: boosted CRV rewards on Curve liquidity positions, a share of trading fees, and governance voting power over pool gauges and other protocol parameters. Approximately half of all trading fees across Curve pools flow to veCRV holders, so as Curve’s volume grows, the value of veCRV’s revenue share grows with it. Importantly, the boost a liquidity provider can obtain on CRV emissions depends on how much veCRV they hold relative to the size of their liquidity position, up to a maximum theoretical boost of around 2.5 times the base reward.

This design creates a powerful coordination challenge. For an individual LP, locking enough CRV for four years to achieve a near-maximal boost on a modest liquidity position may be capital-inefficient or simply out of reach. Smaller or newer users may not want to commit to a multi-year lock in order to access full emissions, while still facing competition from large players that can comfortably accumulate veCRV. At the same time, protocols that depend on Curve liquidity, such as algorithmic stablecoins, LSD issuers, or money markets, care deeply about the distribution of CRV emissions because it determines which pools attract sustained liquidity. This mixture of long-dated locks, yield boosts, and governance control is what transformed veCRV into what some analysts have called DeFi’s “Liquidity Stone,” a scarce resource that channels both incentives and political power across the Curve ecosystem.

As Curve grew, a multi-protocol arms race emerged around accumulating veCRV, colloquially known as the Curve Wars. Protocols such as Yearn and StakeDAO began to pool CRV on behalf of users, lock it as veCRV, and then pass on boosted yields and governance exposure through liquid wrappers. These aggregators made it easier for users to benefit from veCRV without individually committing to a four‑year lock, but they also set the stage for a second-order competition: whoever controlled the largest pool of veCRV would effectively steer CRV emissions and, by extension, the flow of liquidity around Curve. It was into this landscape that Convex Finance launched, with a design explicitly tailored to amassing veCRV at scale and optimizing the resulting governance and yield for its users.

Convex recaps the history of Resupply ($RSUP) and its $reUSD stablecoin backed by yield-bearing positions in Curve Lend and Fraxlend

33.1m reUSD outstanding against ~$36.5m Resupply TVL is a pretty tight credit loop, especially with collateral skewed almost entirely to crvUSD (~$35.5m vs <$1m frxUSD). That makes RSUP less of a standalone stablecoin bet and more a levered bid on Curve Lend utilization, Votium incentives, and PegKeeper depth. June 2025 already showed the weak spot: a ~$9.8m wstUSR/empty-vault exploit pushed bad debt into the insurance pool, so this thing lives or dies by oracle hygiene and redemption friction more than by classic liquidation risk.

Readers click Convex most when it reveals new adoption surface — multichain deployment, novel protocol integrations, institutional capital flows — not when it recaps the veCRV dominance thesis they already know, signaling an audience stress-testing whether Convex can sustain relevance beyond its Curve Wars peak.↗

What Convex Finance Is and How It Sits on Top of Curve

Convex Finance is a DeFi protocol that operates as a yield optimizer and governance aggregator for Curve liquidity providers and CRV holders. It is deployed on Ethereum and Arbitrum, and it wraps Curve’s own staking and governance mechanisms in a simpler interface that allows users to deposit Curve LP tokens or CRV and receive boosted yield plus additional incentives without managing veCRV themselves. In effect, Convex exists as an intermediate layer between Curve and its users: Curve handles the automated market making and base rewards, while Convex aggregates veCRV and votes on gauges, then distributes amplified rewards to depositors.

At the heart of Convex’s model is the idea of pooling governance power. Instead of each Curve LP deciding whether to lock CRV and for how long, Convex invites them to deposit either their LP tokens or CRV into its own contracts. The protocol then stakes those assets on Curve or locks CRV as veCRV, thereby accumulating an ever-larger veCRV position. Because Convex aggregates deposits across thousands of users and protocols, it can achieve near-maximal boost levels for its staked Curve positions and then share that boost proportionally with depositors. In practice, this means that an LP who might have earned only base CRV emissions on Curve can earn significantly more by routing their LP tokens through Convex, with no need to hold veCRV themselves.

Convex’s website makes this layered relationship explicit, branding itself as “Convex Boosting for Curve” and highlighting that users deposit Curve, Frax, or f(x) LP tokens into Convex to earn boosted rewards that are applied collectively. Once LP tokens are deposited, Convex stakes them in Curve’s gauges on the user’s behalf and tracks the user’s share of rewards through its own internal accounting tokens. Users can claim rewards at any time and can also withdraw their underlying LP tokens without penalty, even though the CRV that Convex locks as veCRV is committed for long periods at the protocol level. This architecture allows Convex to align long-dated veCRV locks with the shorter-term preferences of yield-seeking LPs.

Convex’s operations are not limited to the Ethereum mainnet. Documentation and integration guides describe Convex as operating across Ethereum and Arbitrum, reflecting Curve’s own expansion into multiple chains. As Curve deploys pools on new networks such as Arbitrum, Polygon, and Fraxtal, Convex has followed by adding support for those Curve pools within its interface, allowing users to capture boosted rewards across multiple chains while still participating in the aggregated governance structure centered on Ethereum-based CRV and veCRV. This multi-chain presence positions Convex as a cross-network coordination layer for Curve liquidity, rather than a single-chain farm.

The Core User Flows: From Curve LP Tokens to Boosted Rewards

From the perspective of a typical Curve liquidity provider, Convex simplifies and automates what would otherwise be a complex set of operations. On Curve itself, the user provides liquidity to a particular pool and receives LP tokens that represent their share of the pool. To earn CRV emissions, they must then stake those LP tokens in the appropriate Curve gauge, and to maximize rewards they would ideally also hold and lock CRV as veCRV. Convex collapses several of these steps into a single workflow: the user simply deposits their Curve LP tokens into a corresponding Convex pool, and the rest happens under the hood.

Technically, when a user deposits LP tokens into Convex, those tokens are sent to a core contract often referred to as the Booster. The Booster then stakes the LP tokens into Curve’s gauge contract and mints Convex deposit tokens that track the depositor’s stake. According to integration notes, depositors can choose whether to simultaneously stake these deposit tokens in a BaseRewardPool, where they begin to accrue CRV, CVX, and any additional incentive tokens, or simply hold the deposit tokens without staking. Staking through the Booster contract and BaseRewardPool is described as the preferred path, because the BaseRewardPool is the component that actually tracks rewards and periodically distributes them to stakers.

Convex exposes view functions such as BaseRewardPool.earned() to allow users or integrating contracts to check how many reward tokens have accrued to a particular staker. For pools with extra incentives beyond CRV and CVX, Convex may deploy additional reward contracts like VirtualBalanceRewardPool instances, whose addresses can be queried via BaseRewardPool.extraRewards(i) and whose earned() function reports extra token rewards. When a user is ready to harvest, they call BaseRewardPool.getReward(user, claimExtras=true), choosing whether to claim those extra tokens at the same time as their main rewards. Withdrawals are handled through functions such as BaseRewardPool.withdrawAndUnwrap(amount, claim=false), which both unstakes the deposit tokens and unwraps them back into the original Curve LP tokens, making it straightforward for the user to exit their liquidity position or move it elsewhere.

From the user’s perspective, the net effect of these behind‑the‑scenes mechanics is that they earn multiple reward streams from a single deposit: base CRV emissions, boosted by Convex’s aggregate veCRV position; CVX tokens that Convex mints as an incentive layer; and any external incentives attached to the Curve gauge, such as protocol-specific rewards or bribe-bought distributions. Convex also supports staking of its own tokens and derivative tokens, such as cvxCRV, in analogous reward pools, enabling users to compound their positions by routing CRV-derived assets back into the system. This layered architecture is what makes Convex both powerful and somewhat complex, motivating the existence of detailed integration guides for developers who want to build on top of it.

To illustrate the basic pattern from a developer standpoint, consider the following simplified Solidity snippet that echoes the flow described in Convex’s integration tips:

```solidity // Deposit Curve LP tokens into Convex and stake IERC20(curveLpToken).approve(booster, amount); IBooster(booster).deposit(poolId, amount, true);

// Later, check rewards uint256 crvEarned = IBaseRewardPool(baseRewardPool).earned(user);

// Withdraw and unwrap back to Curve LP tokens IBaseRewardPool(baseRewardPool).withdrawAndUnwrap(amount, false); ```

While this example omits many safety checks and nuances, it captures the core idea: Convex abstracts away Curve’s gauge staking and veCRV boosting so that both end users and integrating protocols can treat Convex as a higher-level yield source rather than manually orchestrating every step. This abstraction is particularly important for protocols that want to build leveraged or composable strategies on top of Convex positions, such as borrowing against Convex-wrapped LP tokens or bundling them into structured products.

- 01Multichain expansion race↗

The Fraxtal launch story drew the highest click count of any Convex headline, showing readers are watching whether Convex can replicate its Curve-layer dominance on new chains before competitors entrench.

- 02Governance power concentration↗

Stories about vlCVX voting urgency, 51% veCRV control, and fee structure adjustments pulled readers because they expose how a single protocol's governance stance routes billions in DeFi liquidity.

- 03Wrapped-token ecosystem extensions↗

cvxFXN, cvxPRISMA, Resupply, and Napier integrations drove sustained engagement from readers tracking whether Convex's meta-governance model can colonize yield verticals beyond Curve.

- 04Institutional and whale capital flows

Reserve Protocol's $20M governance token purchase and Terraform Labs moving 2MM CVX signaled readers using large-wallet behavior as a proxy for protocol health and governance capture risk.

- 05Stacked yield mechanics and collateral↗

Explainers on liquid lockers, crvUSD MetaMorpho vaults, and Convex LP collateral on FraxLend show readers building a functional mental model of how yield compounds across Convex's protocol stack.

- 06CVX price as governance sentiment proxy↗

A 100%+ single-day spike and a 22% weekend gain attracted clicks from readers treating CVX price as a leading indicator of governance demand rather than a pure speculative trade.

CVX, cvxCRV, and vlCVX: The Token Triptych at the Heart of Convex

Convex’s influence rests not only on its contracts but also on its token design. Three main tokens—CRV derivatives and native governance—define how value and power flow through the system: CVX, cvxCRV, and vlCVX. Each serves a distinct role, and together they transform Curve’s veCRV model into a meta-governance layer that external protocols can target.

CVX is Convex’s native token, used both as an incentive and as a governance asset. The protocol mints CVX pro rata to the amount of CRV that Curve LPs earn through Convex, with a minting ratio that decreases as more CVX enters circulation. Convex’s documentation notes that the CVX-per-CRV mint ratio steps down every 100,000 CVX minted, a mechanism that effectively front‑loads emissions so that early participants receive more CVX per unit of CRV than later ones. The total supply of CVX is capped at 100 million tokens, meaning that over time the emission component of CVX’s tokenomics will asymptotically wind down, and the token’s value proposition will increasingly depend on fee flows and governance rights rather than new issuance.

The cvxCRV token is Convex’s liquid wrapper for staked CRV. Instead of locking CRV themselves on Curve to obtain veCRV, users can deposit CRV into Convex and receive cvxCRV in return. Convex then locks the underlying CRV as veCRV, adding to its collective voting power and boost potential. In exchange, cvxCRV holders receive a bundle of benefits that mirror and enhance the veCRV position: a share of Curve trading fees that would otherwise flow directly to veCRV holders, additional CRV rewards derived from Convex’s boosted position, and CVX token incentives on top. The crucial trade‑off is that the conversion from CRV to cvxCRV is effectively one-way within Convex’s own contracts; users cannot simply redeem cvxCRV for the underlying CRV at par, because the CRV has been permanently locked as veCRV to sustain Convex’s aggregated boost. Instead, liquidity for cvxCRV is provided through external markets, and its price relative to CRV reflects both expected future yield and secondary-market demand.

The third token, vlCVX, represents vote-locked CVX. CVX holders can lock their tokens for fixed 16‑week periods to obtain vlCVX, which is non-transferable and solely used for governance. vlCVX holders collectively determine how Convex’s enormous veCRV position votes on Curve’s gauge weights, effectively making vlCVX a meta-governance token that proxies for a very large veCRV stake. Convex’s governance page provides an interface for vlCVX holders to participate in Convex DAO proposals and voting decisions, including gauge-vote directives, parameter changes, and treasury actions. The protocol has experimented with improved governance UIs and processes, reflecting both the scale of its influence and the need to coordinate a large dispersed voter base around complex, recurring decisions.

The economic significance of vlCVX extends beyond internal Convex matters. Because Convex controls a dominant share of all veCRV—recent figures from the protocol’s own communications highlighted more than 400 million CRV locked, representing just over half of the total veCRV supply—controlling vlCVX effectively means controlling a decisive bloc in Curve’s governance and emissions distribution. This concentration has made vlCVX an attractive target for other protocols that want to direct CRV emissions toward their own pools or strategies. Rather than acquiring CRV, locking it as veCRV, and directly voting in Curve governance, a protocol can instead pay vlCVX holders to vote its way by offering “bribes” that reward voters for supporting particular gauge votes. In this way, Convex’s governance tokens have become a marketplace for directing liquidity across Curve, monetizing what might otherwise have been an underutilized governance process.

Convex Finance rose from Curve’s vote-escrow model to dominate the Curve Wars, centralizing veCRV power and reshaping DeFi governance.

Curve planted veCRV seeds, Convex came along with a giant watering can and claimed the whole garden. DeFi governance wasn't ready for that level of farming efficiency.

Bribes, Liquid Lockers, and the Business of Meta-Governance

The interplay between veCRV, vlCVX, and emission-directed liquidity gave rise to a new class of DeFi business models centered on governance rather than trading spreads or borrowing rates. Convex sits at the nexus of this ecosystem. Protocols that rely on Curve liquidity often prefer to pay vlCVX voters directly through bribes instead of building and maintaining their own large veCRV positions. Curve’s own social channels have described this dynamic as a way to “pay for governance via vlCVX bribes,” outsourcing voting power and accessing CRV emissions without the overhead of acquiring and locking governance assets. Bribe platforms and marketplaces have emerged to structure these payments, standardize vote buying, and compress complex multi-asset incentive flows into a single ROI metric for vlCVX holders.

This model reframes governance from a civic or public-good activity into a yield-bearing strategy. For individual vlCVX holders, participating in bribe markets is a way to monetize their influence, stacking bribe rewards on top of protocol fees and other incentives. For Convex itself, the presence of bribes enhances the value proposition of holding and locking CVX, supporting CVX demand and, indirectly, Convex’s veCRV accumulation. Some critics argue that this dynamic entrenches power in the hands of capital-rich actors and protocols, turning governance into an auction where the highest bidder buys emissions. Others see it as an efficient outcome, in which governance is allocated to those who care most about specific pools and are willing to pay for liquidity direction, while smaller users still benefit from the resulting boosted yields through products like Convex vaults.

Convex is not the only liquid locker or meta-governance protocol in this space. Yearn and StakeDAO both offer liquid veCRV wrappers and associated strategies, pooling CRV and offering boosted yields and governance exposure to their users. Liquid lockers such as these have become the default way for many users to access veCRV’s benefits, while direct veCRV locking remains the tool of choice for a subset of large holders who seek maximum control or bespoke strategies. Over time, this has reshaped Curve governance from a field of individual veCRV voters into a network of DAOs and meta-governance protocols, each representing pooled interests and sometimes negotiating with one another through bribes, partnerships, or shared products.

The competition among lockers has led to further innovation. StakeDAO’s “only-boost” tooling, for example, was audited with explicit references to “Convex Curve” balances and fallback contracts that track CRV rewards, underscoring how closely intertwined these systems have become. More recently, Stake DAO introduced a Vote Optimizer on platforms like Votemarket to maximize returns from both veCRV and vlCVX voting, reflecting the fact that these two meta-governance layers now coexist and can be strategically arbitraged. Meanwhile, initiatives such as OnlyBoost on Curve’s main gauges aim to combine the boosts of Convex and StakeDAO in a way that benefits LPs regardless of which locker they use, illustrating how what began as a competitive Curve War has gradually morphed into a more cooperative, infrastructure-like layer of boost combiners atop Curve.

In this environment, Convex’s business model can be understood as an optimization around liquidity coordination and incentive routing rather than idealized democratic governance. By aligning its tokenomics and incentives with the practical realities of liquidity mining, Convex has turned DeFi governance’s chronic weaknesses—low participation, voter apathy, and concentrated power—into a system advantage. The protocol monetizes governance through bribes, veCRV control, and fee flows, creating a durable revenue engine that has persisted through multiple market cycles, even as token prices and TVL have fluctuated. For better or worse, Convex’s success demonstrates that in DeFi, “governance” can be as much a financial primitive as lending or swapping.

Convex Finance launches on Ethereum mainnet

Convex surpasses Yearn Finance as largest veCRV holder

- 2023-09launch

cvxPRISMA announced in sync with PRISMA locked airdrop distribution

CVX surges 100%+ in 24 hours; Binance CVX/USDT sets single-day volume record near $32M

Convex adds cvxFXN, integrating f(x) Protocol into its wrapped-token ecosystem

Convex announces Resupply ($RSUP) and reUSD stablecoin backed by Curve Lend and Fraxlend yield positions

Convex adds Curve pool support on Fraxtal, its third sidechain after Arbitrum and Polygon

Beyond Curve LPs: Integrations with Lending, Yield Trading, and Stablecoins

Convex’s evolution has increasingly involved integrations that extend beyond plain Curve LP staking, reflecting both the maturation of DeFi and the deepening of the Curve ecosystem. One prominent strand of this evolution is the interaction with lending protocols built around Curve primitives, such as Curve LlamaLend and its crvUSD stablecoin. LlamaLend is structured around three core contracts—a Vault, an AMM called LLAMMA, and a Controller—that together enable overcollateralized borrowing of crvUSD using various collateral types, including Curve LP tokens. A key innovation in crvUSD’s design is its “soft” liquidation mechanism, in which liquidations occur gradually within a liquidation zone rather than at a single fixed price, giving borrowers more time to react to adverse market moves.

As LlamaLend and crvUSD have matured, support for Curve LP tokens as collateral has opened the door to strategies where users can borrow against their LP positions, earn trading fees and CRV emissions, and loop their positions to amplify yield. Convex fits into this picture as an upstream booster of the same LP tokens: by routing Curve LPs through Convex before using them in lending or vault strategies, users can capture boosted CRV emissions and CVX incentives on top of whatever borrowing or looping they execute downstream. Recent integrations, such as Llama Risk’s crvUSD vault on MetaMorpho that allows borrowing crvUSD against Convex-wrapped TriCrypto LPs, illustrate how Convex is becoming a standard building block within more complex structured products.

Another major integration vector involves yield-trading and fixed-income protocols that build on top of Curve. Napier Finance is an example of such a protocol, known for its yield trading strategies that tokenize fixed and variable yields on top of Curve pools. A recent partnership between Convex and Napier introduced a derivative wrapper called cvxNPR, which represents Napier’s NPR governance token locked within Convex’s ecosystem. Under this arrangement, Napier stakeholders can claim liquid cvxNPR on Convex, while the underlying NPR remains locked to preserve long-term value and governance rights. Crucially, these rights are then managed by vlCVX holders, extending Convex’s meta-governance role beyond Curve and into Napier’s own governance process. This deepens the strategic alignment between the two protocols, broadens the utility of the CVX token, and underscores Convex’s ambition to act as a general governance and yield-routing hub, not only a Curve booster.

Stablecoin innovation offers another lens on Convex’s expanding influence. Resupply Finance, for example, has been introduced as an “ambitious stablecoin experiment” co-built by Convex and Yearn, with a focus on a stablecoin called reUSD that is backed by yield-bearing positions in Curve Lend and Fraxlend. In Resupply’s design, users can deposit collateral that is itself yield-bearing, earn yield on that collateral while borrowing reUSD, and receive additional rewards in tokens such as RSUP, CRV, and CVX. This arrangement links Convex’s boosted yield layer, Curve’s lending stack, and Yearn’s strategy automation into a single structured product, positioning Convex not just as a passive booster but as an active co-architect of new stablecoin mechanisms.

As Convex integrates more deeply with lending, yield-trading, and stablecoin protocols, its footprint across DeFi grows more systemic. Protocols such as Convergence Finance have announced plans to integrate Convex via new CVX liquid lockers and deeper Frax integration, suggesting that CVX and vlCVX may become important primitives in their own right for structuring cross-protocol yield flows. These developments reflect a broader trend: Curve’s ecosystem, including Convex, Yearn, Frax, Resupply, and Gearbox, is increasingly viewed as a full-stack DeFi playground, encompassing stablecoin liquidity, lending through products like Curve Lend, and automated yield strategies layered on top. In this stack, Convex often serves as the gateway through which CRV emissions and veCRV governance power are mediated.

UX, Community, and Crypto Twitter as Governance Theatre

Despite its technical sophistication, Convex remains a user-facing product, and its evolution has included significant improvements to user experience and community engagement. The protocol has launched a new frontend with enhanced speed and performance, streamlining navigation across multiple chains and pools and making it easier for users to track their positions and rewards. For a protocol that relies on complex multi-token reward streams, improved UI performance is not merely cosmetic; it reduces cognitive overhead and can help demystify the layered nature of Convex’s yield flows.

Community incentives have also been a consistent feature of Convex’s culture. For its long-standing supporters, the protocol recently announced that OG and Veteran role holders in its Discord would receive 200 CVX as a gesture of appreciation, provided they had claimed those roles. This type of retroactive reward aligns with the broader DeFi practice of acknowledging early adopters and community contributors through token distributions, while also reinforcing the narrative continuity of Convex’s five-year history. Celebrations of its fifth anniversary have highlighted partner shoutouts and community stories, underlining how Convex’s identity is bound up not only with code and tokenomics but also with a persistent set of social relationships across DeFi.

Crypto Twitter, now largely centered on X, has played an outsized role in Convex’s story. It is on X that narratives around the Curve Wars, veCRV, and Convex’s dominance have been publicly debated. Threads such as the widely cited “Curve Wars: how Convex Finance completely screwed everyone” reflect critical perspectives that argue Convex’s veCRV aggregation undermined the spirit of decentralized governance by centralizing control in a single protocol. Conversely, official accounts for Curve and Convex have used X to explain mechanisms like vlCVX bribes, announce integrations such as Napier or Resupply, and rally voters to reach quorum on governance proposals. When a governance vote is “so close to quorum” with only hours left, it is often social media, rather than on-chain interfaces, that serves as the rallying point for vlCVX holders.

Convex’s communications also exhibit a playful, meme-aware side. Cryptic teaser videos, such as hippo-themed clips that hint at upcoming features or partnerships, are shared widely on Crypto Twitter, leveraging the cultural grammar of DeFi memes to maintain attention between major product releases. At the same time, serious governance debates—such as reactions to a Swiss Stake AG grant proposal for funding Curve-related development and Convex co-founder Winthorpe’s suggestion of a “stopgap” alternative—play out across governance forums and X threads. This duality underscores a broader reality in DeFi: the boundary between community marketing, meme culture, and substantive governance deliberation is porous, and protocols like Convex must operate competently in all three domains.

Convex Finance turned DeFi governance’s biggest weaknesses—low participation and concentrated power—into a system advantage by optimizing around liquidity coordination and incentive routing rather than idealized voting. By monetizing governance through bribes and veCRV control, Convex built a durable revenue engine that has survived multiple market cycles.

They are not fixing bad politics ...they are just weaponising it. " Government owns the power , but we have to them" ...as easy as that.

Convex stacks directly on Curve's contracts; a vulnerability in either layer, or in any of the growing family of wrapped tokens (cvxCRV, cvxFXN, cvxPRISMA), would propagate losses across all depositors simultaneously.

Convex controls over 51% of veCRV supply, meaning one protocol's governance stance effectively dictates Curve emission routing and liquidity incentives across the broader DeFi ecosystem.

The bribe economy built around vlCVX voting means governance outcomes can be purchased by well-funded actors, as demonstrated by Reserve Protocol's $20M acquisition of governance tokens across Curve, Convex, and StakeDAO.

CVX and cvxCRV yields depend on sustained Curve fee revenue and CRV emissions; a structural Curve decline or emission model change would directly compress Convex yields without a near-term substitute.

CVX has demonstrated extreme short-term volatility driven by governance event speculation rather than fundamental cash flow changes, creating elevated drawdown risk for holders during governance lulls.

- RegulatoryMedium

The bribe-for-votes model and governance token economics face increasing scrutiny as potential unregistered securities or market coordination mechanisms as global DeFi regulation tightens.

Risks, Critiques, and the Sustainability of Convex’s Model

As with any system that aggregates large amounts of capital and influence, Convex carries risks and has attracted critiques. On the technical side, Convex’s architecture introduces additional smart contract risk relative to staking directly on Curve, since deposits are routed through Convex’s Booster and reward pool contracts. While the protocol and many of its integrations have been audited, and while its multi-year track record without catastrophic exploits is reassuring, the complexity of its layered reward structure and external dependencies cannot be ignored. Tools like StakeDAO’s only-boost system, whose audit documentation explicitly references Convex-related balances and fallback contracts, illustrate how interlinked these ecosystems have become; an unnoticed bug in one layer could propagate unpredictable effects across others.

Beyond code-level risk, governance and concentration risks are more subtle but potentially more far-reaching. By design, Convex has accumulated a majority share of all veCRV, which means that its governance decisions—and the decisions of vlCVX voters—largely determine CRV emission flows and, by extension, liquidity depth across many of DeFi’s most important stablecoin and LSD pools. This centralization contradicts some ideals of decentralized governance, even if it arose organically from users seeking better yields and protocols seeking efficient access to boosts. Critics argue that such concentration makes Curve’s ecosystem vulnerable to governance capture, either by hostile actors accumulating CVX or by misaligned coalitions of vlCVX voters who prioritize short-term bribe income over long-term protocol health.

The bribe-driven governance model itself has also come under scrutiny. While framing bribes as “governance incentives” or “vote markets” softens the language, it does not change the basic fact that votes are often directed by whoever pays the most, not necessarily by who has the best long-term plan for Curve or its integrators. In bull markets, this may lead to over-subsidization of risky or unsustainable pools, as protocols overpay for emissions to gain liquidity at any cost. In bear markets, bribe revenues can shrink, potentially undermining the economic rationale for locking CVX and participating in governance, although fee flows from Curve’s trading volume may provide a stabilizing baseline. Convex’s durability across several market cycles suggests that its revenue engine is more resilient than pure speculative mania, but it does not eliminate the cyclical nature of liquidity mining and governance incentives.

Regulatory uncertainty adds another layer of risk. Governance tokens like CVX, especially when tied to fee flows and bribe revenue, may attract regulatory attention as quasi-equity or yield-bearing securities, depending on jurisdiction and legal interpretation. While no definitive regulatory framework for DeFi governance tokens has yet emerged, protocols that operate as de facto coordination layers for multi-billion-dollar liquidity networks are likely to face heightened scrutiny. Convex’s role in monetizing governance could be framed either as a sophisticated loyalty and coordination mechanism or as a complex financial scheme that blurs the line between user participation and investment contracts. For now, these questions remain largely theoretical, but they may become more pressing as regulators and courts grapple with DeFi’s unique structures.

Finally, sustainability in the ecological sense—namely, whether Convex’s model can maintain relevance in a changing DeFi landscape—is an open question. As new AMMs, ve-tokenomics experiments, and cross-chain architectures emerge, Curve’s primacy as the dominant stablecoin venue could erode, which would directly impact Convex’s core value proposition. On the other hand, Convex’s move to integrate with newer primitives such as LlamaLend’s crvUSD, Napier’s yield markets, and Resupply’s yield-backed stablecoins suggests that the protocol is actively adapting, positioning itself not only as a Curve booster but as a generalized coordinator for ve-style governance and incentive routing.

Comparative Perspective: Direct Curve, Convex, and Alternative Lockers

To ground these dynamics, it is helpful to compare, at a high level, the experience of a user providing liquidity through three different paths: directly on Curve, via Convex, or via an alternative liquid locker. While specifics vary by pool and over time, the structural differences can be summarized as follows.

| Dimension | Direct Curve LP + veCRV | Curve LP via Convex | Curve LP via Other Lockers (e.g., Yearn, StakeDAO) |

|---|---|---|---|

| Need to lock CRV yourself | Yes, to get boost | No, Convex aggregates veCRV | No, locker aggregates veCRV |

| Boost level (typical) | Depends on your veCRV | Near-max due to pooled veCRV | Varies, often competitive |

| Extra token rewards | CRV, sometimes pool incentives | CRV, CVX, bribes, extras | CRV, protocol token, bribes |

| Governance exposure | Direct veCRV voting | Indirect via vlCVX (if you own CVX) | Indirect via locker’s governance |

| Flexibility of exit | Locked veCRV is illiquid | LPs liquid; cvxCRV is liquid but not redeemable | Depends on wrapper liquidity |

| Complexity | Medium (Curve UI + locking) | Higher, but abstracted by Convex UI | Higher, strategy-specific |

This table highlights that Convex’s core value proposition is to offer near-maximal boosts and layered rewards without requiring users to lock CRV themselves, while simultaneously channeling governance through vlCVX as a meta-layer. Alternative lockers provide similar services but may differ in how they share incentives and how much veCRV they control. For sophisticated users, holding both vlCVX and liquid locker tokens can be a way to diversify governance exposure and bribe income across multiple overlapping systems.

Outlook

Looking ahead, Convex’s trajectory will likely be shaped by three interacting forces: the evolution of Curve and its ve-tokenomics, the maturation of DeFi’s lending and yield-trading stacks, and the market’s appetite for meta-governance as a profitable business model. As Curve expands to chains such as Arbitrum, Polygon, and Fraxtal, Convex’s role as a cross-chain coordination and boost layer may become even more important, especially if multi-chain liquidity fragmentation persists. Integrations with LlamaLend, Resupply, and Napier suggest that Convex is already positioning itself at the heart of a multi-protocol stack where stablecoins, lending, and yield derivatives are tightly coupled.

At the same time, the governance landscape around veCRV and vlCVX is still evolving. Tools like StakeDAO’s Vote Optimizer and platforms like Votemarket indicate that sophisticated vote-arbitrage strategies are emerging, which may push governance toward a more explicitly financialized equilibrium. Convex’s ability to maintain active, informed participation from vlCVX holders—rather than purely mercenary bribe chasing—will influence how sustainable its meta-governance model proves to be over the long term. Community engagement, UX improvements, and thoughtful responses to governance controversies, such as debates around external funding proposals, will all play a role in this process.

Finally, the broader regulatory and competitive environment will test whether Convex’s approach to monetizing governance and coordinating liquidity can endure beyond the specific context of Curve. If ve-style models continue to proliferate, Convex’s skill set in aggregating locked governance and routing incentives could be applied more broadly, potentially making CVX and vlCVX key primitives in multiple ecosystems. Conversely, if new forms of AMM design, restaking, or cross-chain liquidity reduce the centrality of Curve, Convex may need to reinvent parts of its model to stay at the center of DeFi’s evolving power grid. In either case, the story of Convex to date has already left a lasting mark on how DeFi thinks about the intersection of yield, governance, and coordination.

Conclusion

Convex Finance began as a specialized tool for boosting Curve yields, but it has grown into a central actor in DeFi’s governance and liquidity infrastructure. By aggregating veCRV at unprecedented scale and routing its influence through the CVX and vlCVX tokens, Convex transformed Curve’s vote-escrow design into a meta-governance engine that monetizes voting power through bribes, fee flows, and complex integrations. This has allowed everyday Curve LPs to access near-maximal boosts without locking CRV themselves, while also giving protocols an efficient way to direct CRV emissions toward their preferred pools.

The same architecture, however, concentrates power and introduces new forms of risk. Convex’s dominance in veCRV makes it a single point of political and economic leverage within the Curve ecosystem, raising questions about governance capture, incentive misalignment, and systemic fragility. At the same time, Convex’s continued adaptation—through integrations with lending protocols like LlamaLend, yield traders like Napier, and stablecoin experiments like Resupply—shows that it is not standing still. It is actively redefining its role from a Curve booster to a broader coordination layer in a dense, multi-protocol DeFi stack.

For users, DAOs, and protocols navigating this landscape, Convex offers both opportunities and trade-offs. Its products can significantly enhance yields and simplify exposure to complex governance systems, but they also embed users within a layered, financialized governance economy whose long-term equilibrium remains uncertain. As DeFi continues to experiment with new forms of coordination and incentive design, Convex’s experience demonstrates both the power and the perils of turning governance into a market-driven primitive. Whether it ultimately stands as a model to emulate or a cautionary tale will depend on how well it balances yield optimization with sustainable, resilient governance in the years to come.

Latest Convex news

Convex recaps the history of Resupply ($RSUP) and its $reUSD stablecoin backed by yield-bearing positions in Curve Lend and FraxlendConvex Finance rose from Curve’s vote-escrow model to dominate the Curve Wars, centralizing veCRV power and reshaping DeFi governance.Convex Finance turned DeFi governance’s biggest weaknesses—low participation and concentrated power—into a system advantage by optimizing around liquidity coordination and incentive routing rather than idealized voting. By monetizing governance through bribes and veCRV control, Convex built a durable revenue engine that has survived multiple market cycles.Perry breaks down the Curve War, explaining how veCRV became DeFi’s “Liquidity Stone,” directing emissions, incentives, and power. From StakeDAO and Yearn to Convex’s dominance, control of veCRV ultimately meant control of liquidity flows across Curve.Convex Finance co-founder Winthorpe suggests an intermediate "stopgap" funding proposal is in the works, following a chilly reception to the 2026 Swiss Stake funding request Liquid lockers like Convex, Yearn, and StakeDAO pool CRV into veCRV, giving users access to boosted yields and governance influence without a four-year lock. These communal boosts have become the norm, reshaping Curve governance and rewards, while direct veCRV still benefits large holders seeking maximum control.

Liquid lockers like Convex, Yearn, and StakeDAO pool CRV into veCRV, giving users access to boosted yields and governance influence without a four-year lock. These communal boosts have become the norm, reshaping Curve governance and rewards, while direct veCRV still benefits large holders seeking maximum control.Sources

- https://www.convexfinance.com

- https://x.com/dcfgod/status/2031813215857099152

- https://x.com/CurveFinance/status/2014721197611667813

- https://docs.convexfinance.com/convexfinance/general-information/tokenomics

- https://blog.pessimistic.io/convex-finance-defi-integration-tips-1bacfe73d3ce

- https://x.com/ConvexFinance/status/2054554463415795972

- https://x.com/ConvexFinance/status/1876252412383822194

- https://github.com/stake-dao/only-boost/blob/main/audit/StakeDAOPreliminaryAuditReport.md

- https://www.curve.finance/dex/fraxtal/pools/

- https://x.com/ConvexFinance?lang=en

- https://www.binance.com/en-NG/square/post/10362564649769

- https://mixbytes.io/blog/modern-defi-lending-protocols-how-its-made-curve-llamalend

- http://gov.curve.finance/t/funding-proposal-for-swiss-stake-ag-grant-proposal-2026/10953

- https://blog.portals.fi/convex-finance-the-protocol-that-super-charges-your-curve-rewards/

- https://www.convexfinance.com/vote

- https://www.youtube.com/watch?v=O41paZC5sYw

- https://news.convex.dev/enterprise-launch/

- https://x.com/llamalend?lang=en

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…