Deep dive on Resupply, a Curve- and Convex-aligned CDP protocol that issues yield-backed reUSD, covers its design, exploit and recovery, integrations like sreUSD and Llamalend, and what it signals for the future of DeFi stablecoins.

- x.com23

- etherscan.io2

- news.curve.finance2

- youtube.com2

- discord.com1

- snapshot.prismafinance.com1

- wavey.info1

+1 sources across the wider coverage universe

Convex recaps the history of Resupply ($RSUP) and its $reUSD stablecoin backed by yield-bearing positions in Curve Lend and Fraxlend2026-05

Convex recaps the history of Resupply ($RSUP) and its $reUSD stablecoin backed by yield-bearing positions in Curve Lend and Fraxlend2026-05 Feel good using Resupply? That’s by design2025-12

Feel good using Resupply? That’s by design2025-12 Resupply outlines a next-generation CDP model built around stable, yield-generating collateral, reducing liquidation risk while improving capital efficiency versus traditional ETH/BTC-based CDPs. By integrating real revenue, looping strategies, and stable LTVs, Resupply reframes CDPs into productive capital primitives.2026-01

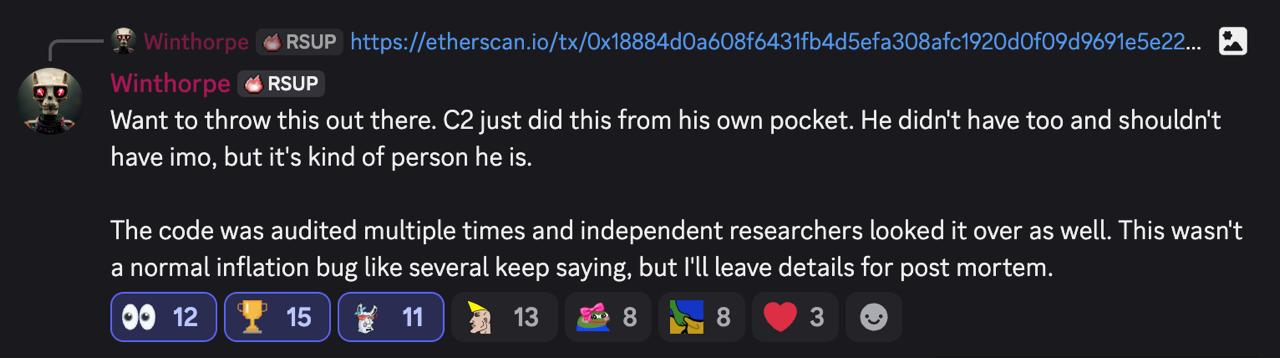

Resupply outlines a next-generation CDP model built around stable, yield-generating collateral, reducing liquidation risk while improving capital efficiency versus traditional ETH/BTC-based CDPs. By integrating real revenue, looping strategies, and stable LTVs, Resupply reframes CDPs into productive capital primitives.2026-01 Convex/Resupply dev C2tP conributes 1,407,736.68 reUSD ($1,395,431.66) out of his own pocket towards paying off Resupply exploit bad debt... "It's the kind of person he is," posts protocol co-founder Winthorpe2025-06

Convex/Resupply dev C2tP conributes 1,407,736.68 reUSD ($1,395,431.66) out of his own pocket towards paying off Resupply exploit bad debt... "It's the kind of person he is," posts protocol co-founder Winthorpe2025-06 Resupply Finance passes $10MM $reUSD borrowed2025-03

Resupply Finance passes $10MM $reUSD borrowed2025-03 Curve proposal from Resupply introduces crvUSD minting directly into the sreUSD lending market on Curve Lend2025-10

Curve proposal from Resupply introduces crvUSD minting directly into the sreUSD lending market on Curve Lend2025-10

Resupply: A Yield-Backed Stablecoin Protocol Built on Curve and Convex

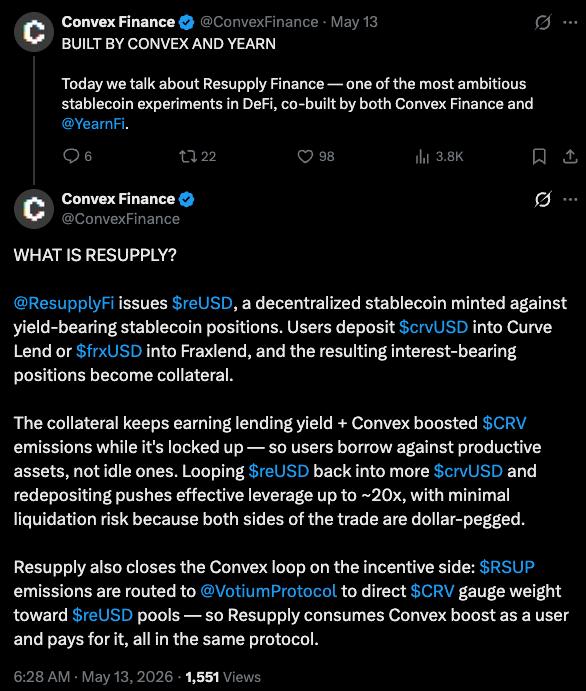

Resupply is a decentralized stablecoin and lending protocol that lets users borrow the reUSD stablecoin against yield-bearing stablecoins such as crvUSD, turning collateral into a productive asset while attempting to maintain a tight dollar peg. Built by contributors from the Curve, Convex, and Yearn ecosystems, it reframes collateralized debt positions (CDPs) around stable, income-generating assets rather than volatile tokens like ETH or BTC, with the goal of improving capital efficiency and reducing liquidation risk.

What Is Resupply?

Resupply is best understood as a specialized CDP protocol that lives on top of Curve Finance’s lending stack and adjacent money markets such as Fraxlend, using those venues as its primary source of collateral and liquidity. At its core, the protocol issues reUSD, a decentralized, dollar-pegged stablecoin minted when users deposit other stablecoins that already earn yield in external lending markets, notably Curve Lend (also known as Llamalend) and Fraxlend. Instead of locking volatile assets and hoping their price stays above a liquidation threshold, users lock stablecoins that accrue interest, and they pay a borrow rate that is explicitly designed to be lower than the yield generated by the underlying collateral.

From a design perspective, Resupply sits as a sub-DAO within the Yearn and Convex orbit, with development and incentives aligned around deepening liquidity and utility for crvUSD and other Curve-centric assets. The protocol’s governance and economic flywheel are closely tied to RSUP, its native token, and to staked CRV and CVX positions which help the system direct emissions and boost yields in Curve and Convex pools. In effect, Resupply is not just another standalone stablecoin project; it is a capital-efficiency layer on top of Curve’s existing infrastructure, attempting to make the stablecoin side of DeFi more productive while driving demand for crvUSD and Curve Lend markets.

The protocol quickly attracted attention after launch, with total value locked (TVL) growing into the tens of millions of dollars and reUSD borrowing volumes scaling into eight figures as users discovered looping strategies built on Curve Lend and Fraxlend. Media coverage from ecosystem outlets like Leviathan News emphasized both the technical innovation and the user experience, noting how Resupply’s interface and product design were deliberately crafted to make leveraging complex yield strategies feel intuitive and reassuring rather than intimidating. At the same time, Resupply’s trajectory has been shaped by a major exploit and subsequent recovery that tested both its risk framework and its social capital across Curve, Convex, and Yearn communities, making it a useful case study in how next-generation DeFi protocols navigate growth, security, and governance.

Convex recaps the history of Resupply ($RSUP) and its $reUSD stablecoin backed by yield-bearing positions in Curve Lend and Fraxlend

33.1m reUSD outstanding against ~$36.5m Resupply TVL is a pretty tight credit loop, especially with collateral skewed almost entirely to crvUSD (~$35.5m vs <$1m frxUSD). That makes RSUP less of a standalone stablecoin bet and more a levered bid on Curve Lend utilization, Votium incentives, and PegKeeper depth. June 2025 already showed the weak spot: a ~$9.8m wstUSR/empty-vault exploit pushed bad debt into the insurance pool, so this thing lives or dies by oracle hygiene and redemption friction more than by classic liquidation risk.

Readers clicked Resupply not for protocol mechanics but for moral theatre: a dev voluntarily paying $1.4M of his own money after an exploit revealed that the strongest trust signal in DeFi is still individual accountability, not audits or DAO votes.↗

The Design of reUSD: A Yield-Backed Stablecoin

At the center of the protocol is reUSD, often stylized as REUSD on price trackers, a dollar-pegged stablecoin issued when users open CDPs against yield-bearing stablecoins. According to market data, reUSD (REUSD) trades around the one-dollar mark, with relatively tight trading ranges and modest 24‑hour price volatility, reflecting its design as a low-volatility debt asset rather than a speculative token. The supply of reUSD is determined entirely by user demand for leverage and liquidity: borrowers decide how much reUSD to mint against their stablecoin collateral, subject to collateralization ratios and borrowing limits defined by the protocol’s risk parameters.

Resupply’s defining feature is that the collateral backing reUSD is itself earning yield in external lending markets like Curve Lend and Fraxlend, rather than sitting idle. When a user deposits crvUSD or another supported yield-bearing stablecoin, that collateral is typically supplied into a lending market where it earns an interest rate; the protocol then charges a borrow rate on reUSD that is designed to be lower than the collateral’s yield under normal conditions. Public documentation and market descriptions emphasize that the borrow rate is targeted to be approximately half the lending rate being earned by the collateral, half the prevailing risk‑free rate, or two percent annually, whichever is higher. By construction, this aims to ensure that the collateral’s income exceeds the debt cost, turning the CDP into a positive carry position as long as rates behave as expected.

This structure stands in contrast to more traditional CDP stablecoins like DAI, where users often borrow against volatile assets such as ETH and rely on price appreciation or external yield opportunities to justify the cost of leverage. In Resupply’s model, the core trade is not necessarily directional price exposure but the spread between collateral yield and borrow cost, combined with the ability to redeploy reUSD into additional yield strategies, liquidity pools, or savings products like sreUSD. The yield-on-yield dynamic is further enhanced by Convex incentives, as users can earn RSUP, CRV, and CVX rewards alongside base interest by participating in Resupply-related pools and vaults.

The peg stability of reUSD is supported by several mechanisms that are conceptually similar to other overcollateralized stablecoins. First, every reUSD in circulation is backed by a portfolio of on-chain assets whose market value, under stress-tested conditions, should exceed the value of outstanding debts. Second, borrowers face liquidation if the value of their collateral, net of haircuts and risk parameters, falls below required thresholds, which incentivizes them to repay or adjust their positions when markets move. Finally, liquid secondary markets on Curve and other decentralized exchanges allow traders and arbitrageurs to buy or sell reUSD around one dollar, tightening the peg whenever material deviations appear. The fact that reUSD’s main collateral types are themselves stablecoins means that price volatility in the backing assets is typically much lower than in volatile-token CDPs, which can contribute to more stable LTV ratios and fewer cascades of forced liquidations during market drawdowns.

CDPs with Yield-Bearing Stablecoin Collateral

Resupply’s CDP architecture is explicitly optimized around one idea: that the safest and most capital-efficient debt positions in DeFi are those backed by income-generating stable collateral rather than speculative tokens. Public descriptions of the protocol consistently emphasize that Resupply “leverages the liquidity and stability of lending markets” and that its stablecoin is “backed by other stablecoins that are earning interest on other lending markets.” In practice, this means that the protocol integrates deeply with Curve Lend (Llamalend) and Fraxlend, two lending systems where stablecoins like crvUSD and FRAX-based assets can be deposited to earn floating yields.

In a typical Resupply flow, a user starts with a stablecoin such as crvUSD, the native stablecoin of the Curve ecosystem. They deposit that crvUSD as collateral in a Resupply market, and under the hood, the protocol routes or links that collateral into a lending venue where it begins to earn yield. As soon as the position is opened, the user can borrow reUSD against their collateral, paying an interest rate that is meant to be lower than the yield paid on their supplied stablecoins. Because both the asset side (collateral) and liability side (reUSD debt) are denominated in nominal dollars, the primary risk to the position is not price volatility but interest-rate differentials and any depegging events in the underlying stablecoins, rather than the kind of sharp price crashes associated with ETH or BTC.

This design choice has several implications for capital efficiency. First, collateral ratios can be set more aggressively than in volatile-asset CDPs because the underlying price risk is lower; so long as the stablecoins maintain their pegs, the protocol does not need to buffer against thirty to fifty percent price swings. Second, the presence of real yield on the collateral means that the effective cost of leverage can be negative for responsible users, since their interest income can exceed borrowing costs. Third, the system allows for looping strategies, where a user borrows reUSD, swaps it back into a supported stablecoin, re-deposits it as collateral, and repeats the process multiple times to amplify the size of their income-earning position relative to their initial capital.

Resupply’s own documentation describes a “leverage” interface where users can toggle an option that automatically loops the borrow-and-deposit cycle, with a slider allowing leverage from around 2x up to more than 19x notional exposure under certain configurations. When leverage is activated, the system borrows reUSD against the existing collateral, swaps that reUSD into crvUSD or other accepted stablecoins, and then deposits the proceeds back into the collateral pool, increasing both the total collateral and total borrowed amount. The interface displays key metrics such as initial deposit, total borrowed, total collateral, collateral ratio, and estimated slippage from the stablecoin swaps, helping users understand how aggressive their position is and how sensitive it might be to market conditions.

Because these looping strategies amplify both yield and risk, they underscore the dependence of Resupply on the stability and liquidity of its underlying markets. If Curve Lend or Fraxlend experience disruptions, sharp changes in interest rates, or liquidity shortfalls, highly leveraged positions on Resupply could become fragile even though the assets involved are nominally “stablecoins.” Similarly, substantial depegs in backing assets like crvUSD or FRAX-based tokens would translate into immediate stress for reUSD collateral pools, potentially triggering liquidations or forcing protocol-level interventions. For this reason, the Resupply design highlights the importance of robust oracle mechanisms, conservative risk parameters, and careful monitoring of collateral markets, a theme that became painfully concrete in the wake of the wstUSR market exploit.

Resupply in the Curve and Convex Ecosystem

Resupply’s strategic positioning is inseparable from Curve Finance and Convex Finance. Curve provides the stablecoin and LST-focused AMM and lending infrastructure on which Resupply builds, and Convex acts as an amplifier for Curve incentives, allowing protocols like Resupply to direct CRV emissions and boost yields through aggregated veCRV and vlCVX positions. The interplay among these three protocols creates a kind of “Curve stack” for stablecoins: crvUSD serves as the base stablecoin, Curve Lend (Llamalend) enables leveraged borrowing and lending, Convex helps route incentives, and Resupply adds a yield-backed CDP layer on top.

From Curve’s perspective, Resupply is an important demand driver for crvUSD and Curve Lend markets. Curve’s own documentation and monthly recaps describe how the launch of Resupply, and especially its integration with Llamalend, significantly increased crvUSD supply and TVL in associated markets. By encouraging users to deposit crvUSD as collateral and by proposing initiatives such as minting and supplying 5 million crvUSD directly into the sreUSD Llamalend market, Resupply effectively deepens liquidity and usage for Curve’s native stablecoin. This, in turn, makes Curve’s lending markets more robust and attractive, creating a flywheel in which more crvUSD adoption fuels more Resupply activity and vice versa.

Convex Finance plays a complementary role by helping Resupply optimize incentives and yield routing. A well-known Convex recap highlighted how users who borrow against their collateral in Resupply can earn not only protocol-native rewards like RSUP but also CRV and CVX incentives tied to Curve and Convex liquidity pools. By aggregating voting power and reward streams, Convex enables Resupply to direct emissions toward the pools that matter most for reUSD liquidity and collateral efficiency, reinforcing the protocol’s peg stability and its attractiveness as a leverage venue.

The broader Curve ecosystem also includes other protocols that sit adjacent to Resupply, such as Prisma, which focuses on CDP-style stablecoin issuance against liquid staking derivatives, and Sky Protocol, which evolved from Maker’s ecosystem and issues stablecoins like DAI and USDS. Resupply’s growth has been significant enough that it has featured in stablecoin indices like the OPEN Stablecoin Index, where it reportedly displaced Sky’s stablecoins in one recent rebalance, signaling that market participants view reUSD as a meaningful component of the decentralized stablecoin landscape. While Resupply and Prisma target different collateral types—yield-bearing stablecoins versus LSDs—they share a broader design goal of making on-chain collateral productive and moving beyond the first-generation model of idle, overcollateralized deposits.

Community media such as Leviathan News and ecosystem livestreams have further embedded Resupply into the Curve narrative. Features like “Llama Party” livestreams and interviews with Resupply’s designers emphasize how the protocol’s user interface and brand were consciously designed to make complex leverage and yield strategies feel approachable, underpinned by clear risk disclosures and a playful yet polished aesthetic. In this way, Resupply does not just function as back-end financial plumbing; it also serves as a public-facing entry point into the Curve-Convex stack, giving new users a curated experience that abstracts some of the complexity of Llamalend, Fraxlend, and Convex gauge voting while still routing activity back into those systems.

Feel good using Resupply? That’s by design

TL;DR: Ionut Nechifor, Resupply’s UI/UX designer, crafted the protocol’s visual identity and the iconic hippo mascot. His philosophy blends clarity, usability, and emotional connection, turning complex DeFi mechanics into approachable, intuitive interfaces. Drawing on traditional sketching, vector graphics, and game-inspired aesthetics, he emphasizes simplicity, trust, and storytelling in design. Currently, he’s developing Forma, a modular UI kit for Web3 designers, aiming to streamline professional UI creation with optional AI-powered features.

- 01C2tP personal exploit bailout↗

The image of a core dev spending over $1.4M of personal funds to cover bad debt turned a crisis story into a character study that dominated clicks by a factor of 2.5x over the next headline.

- 02Exploit mechanics and recovery arc↗

The wstUSR market exploit, Peckshield alert, post-mortem, and Yearn loan formed a multi-chapter narrative that readers followed across at least six distinct headlines.

- 03Curve and crvUSD integration↗

Proposals to mint crvUSD directly into sreUSD and supply $5M into Llamalend positioned Resupply as the demand engine for the Curve ecosystem, attracting readers who track crvUSD adoption.

- 04Prisma Finance to Resupply transition↗

The governance vote to shut down Prisma and launch Resupply — complicated by the discovery of multiple high-severity bugs in Prisma's contracts — gave the origin story real dramatic weight.

- 05sreUSD savings product launch↗

The introduction of Savings reUSD as a fee-driven, emission-free yield product signalled a maturing protocol trying to grow demand without diluting token holders.

- 06Protocol growth milestones↗

$10M borrowed and $100M TVL in under a month gave readers concrete proof-of-traction benchmarks to track against the protocol's ambitious positioning.

Savings reUSD (sreUSD) and the Savings Layer

Alongside its core CDP engine, Resupply has introduced a savings-oriented product called Savings reUSD, or sreUSD, designed to give reUSD holders a simple way to earn a share of protocol revenue and integrated yields. Coverage around the protocol describes sreUSD as a mechanism that allows users to stake reUSD and receive a higher-yielding representation, with the protocol using dynamic fees and integration incentives rather than heavy token emissions to drive adoption. In this model, holding sreUSD becomes equivalent to holding a claim on a basket of income streams: interest paid by borrowers, yield from underlying collateral in Curve Lend and Fraxlend, and external incentives gathered via Convex and Yearn positions.

Curve governance materials document a proposal in which Resupply requested that the Curve DAO mint and supply 5 million crvUSD directly into the sreUSD Llamalend market. The idea was to bootstrap deep liquidity and borrowing capacity around the savings product, allowing users to borrow against sreUSD and further integrate it into the Curve lending ecosystem. Because Llamalend markets must include crvUSD as either the borrow or collateral token, this kind of direct mint-and-supply arrangement embeds Resupply’s savings layer even more tightly into Curve’s infrastructure, blurring the distinction between “Curve-native” and “Resupply-native” products.

Resupply has also pursued integrations with other Llamalend markets, such as fxSAVE-linked markets that connect to Frax’s savings products and other yield-bearing stablecoins. Governance updates from the LlamaRisk team, which advises on risk parameters for Curve Lend markets, highlight the creation and tuning of new markets like fxSAVE Llamalend on mainnet, demonstrating that the ecosystem is actively managing the risk of these novel, yield-bearing collateral types. As these markets go live and accumulate TVL, Resupply can plug them into its CDP engine, offering new collateral options and additional avenues for reUSD and sreUSD to circulate.

The introduction of sreUSD reflects a broader trend in DeFi stablecoin design: protocols are increasingly trying to offer “savings-layer” tokens that allow users to hold a stable asset while automatically accruing yield from diversified sources. In this sense, sreUSD competes conceptually with products like sUSDS in the Sky ecosystem or yield-bearing stablecoins created by other protocols that wrap a base stablecoin with an interest-bearing wrapper. For Resupply, the savings layer also has a governance and growth dimension, since having a sticky base of sreUSD holders can support deeper liquidity, more predictable protocol revenues, and additional integrations across the Curve and Convex stacks.

RSUP Tokenomics, TVL, and Governance

The RSUP token underpins Resupply’s incentive structure and long-term governance. While exact tokenomics can evolve over time, public market trackers describe RSUP as the governance and reward token associated with the Resupply protocol, with a market capitalization in the low millions of dollars and an all-time high that was significantly above current levels. Resupply’s TVL, measured across its various markets on Ethereum, has reached into the tens of millions of dollars, with DeFiLlama reporting around 35 million dollars in total value locked at one snapshot, and an average APY on supplied assets of roughly one to two percent before external rewards. These numbers are dynamic but illustrate that Resupply has become a non-trivial player within the Curve-focused DeFi cluster.

RSUP serves several functions. First, it is distributed as part of the reward stack to users who supply collateral, borrow reUSD, or provide liquidity in key pools, often alongside CRV and CVX incentives. Second, RSUP can be staked or locked by aligned actors such as Convex and Yearn, who use their positions to influence protocol parameters, direct incentives, and potentially participate in governance decisions around risk, collateral onboarding, and integrations. Third, the protocol’s bad-debt recovery and recapitalization efforts following the 2025 exploit have hinged, in part, on the revenue streams derived from staked RSUP and its associated yield-bearing strategies.

The Yearn governance proposal YIP‑86, for instance, outlines a loan agreement in which Yearn extends 1.13 million crvUSD to Resupply to cover outstanding reUSD bad debt that remained after an exploit. The terms specify a six percent annual interest rate and repayment in full, with the loan being repaid over up to one year. Crucially, the proposal notes that Yearn agrees to forgo its usual staking revenue during the life of the loan, and that the repayment will be funded by protocol revenue, including the yield generated from Convex and Yearn’s staked RSUP positions. This illustrates how RSUP is not merely a speculative governance token but also a productive asset within the ecosystem’s treasury strategies, with its yield streams explicitly earmarked for protocol recapitalization and stability.

Governance discussions around Resupply have also highlighted the protocol’s collaborative relationship with Curve, Convex, and Yearn communities. Curve founder Michael Egorov publicly commented on the Resupply exploit and proposed the creation of a dedicated Curve-focused security review team, arguing that relying solely on third-party audits—even from top-tier firms—was insufficient to catch all protocol-specific edge cases. Yearn’s willingness to extend a loan on favorable terms, combined with personal contributions from Resupply and Convex developers, underscored the social layer of trust and mutual support that underpins the economic relationships among these protocols. In this sense, RSUP’s value is tied not only to future cash flows but also to the credibility and alignment of the teams and communities that stand behind the Resupply protocol.

The June 2025 Exploit: Anatomy of the wstUSR Attack

On June 26, 2025, Resupply suffered a serious exploit in a newly added market that used wstUSR, an ERC‑4626 vault-based token, as collateral. The issue centered on a design flaw in the way the vault handled initial deposits and the exchange rate between shares and underlying assets when the vault contained effectively zero liquidity. According to post-mortems and technical analyses, the attacker took advantage of the empty vault state and the absence of appropriate safeguards to manipulate the share price, allowing them to borrow the entire reUSD borrow limit of the market—10 million reUSD—against virtually worthless collateral.

In detail, Resupply had deployed a new wstUSR market using ERC‑4626 vault contracts, a standardized interface for tokenized vaults representing shares in an underlying asset pool. The vault was launched with almost no assets, and the protocol did not implement virtual shares, minimum exchange-rate bounds, or sufficient initial seeding to prevent manipulation of the share-to-asset ratio. The attacker used a flash loan to deposit a minuscule amount of collateral—on the order of one wei, an infinitesimal fraction of a token—into the empty vault, thereby influencing the accounting in such a way that they could bypass loan-to-value checks and treat this near-worthless collateral as if it were sufficient to back a very large borrow.

Once the conditions were in place, the attacker executed a single transaction that borrowed the full 10 million reUSD borrow limit of the market, draining the protocol’s capacity and leaving behind bad debt when the reUSD was moved out of the system. A Guardrail AI write-up describes how the exploit involved a sequence of steps typical of advanced DeFi attacks—flash loans, manipulation of low-liquidity vaults, and the exploitation of inadequate initialization logic—culminating in the drainage of funds and the creation of protocol-level insolvency in the affected market. Importantly, only the wstUSR market was impacted; other Resupply markets continued to function as intended, and the team was able to identify and pause the compromised contract quickly after receiving alerts, including from security monitoring services such as PeckShield.

Resupply publicly acknowledged the exploit shortly after it occurred, announcing that the wstUSR market had been paused and stressing that the rest of the protocol remained operational. Subsequent coverage from Curve and ecosystem outlets framed the incident as a serious but contained event: while the exploit created roughly 10 million dollars in bad debt for Resupply, a large portion of that debt was rapidly covered by the Resupply and Convex treasuries, as well as personal funds contributed by one of the core developers, known as C2tP. This immediate response reduced the outstanding deficit to approximately 1.13 million dollars, which then became the focus of the Yearn loan proposal aimed at fully restoring solvency.

Resupply outlines a next-generation CDP model built around stable, yield-generating collateral, reducing liquidation risk while improving capital efficiency versus traditional ETH/BTC-based CDPs. By integrating real revenue, looping strategies, and stable LTVs, Resupply reframes CDPs into productive capital primitives.

"Traditional CDPs built on $ETH and $BTC expose users to sudden liquidations, even when aggregate metrics appear healthy. Resupply addresses this structural weakness by centering CDPs around stable, yield-generating collateral, while borrowing proven ideas from MakerDAO and Liquity. By combining stability, composability, and layered yield, Resupply reframes the CDP model from a leverage tool into a productive capital primitive. No FOMO. No forced liquidations. Just capital that keeps working."

Convex publishes Resupply history and launch preview

Resupply goes live on mainnet

Resupply surpasses $100M TVL within first month

wstUSR market exploit identified and affected contract paused

Official post-mortem published; ~$10M bad debt confirmed

YIP-86: Yearn loans $1.13M to Resupply sub-DAO for bad debt at 6% interest

C2tP personally contributes ~$1.4M reUSD; full $10M bad debt repaid

Resupply proposes $5M crvUSD mint into sreUSD Llamalend market

Post-Mortem, Recovery, and Risk Lessons

In the wake of the exploit, Resupply and external security researchers published detailed post-mortems outlining both the technical root cause and the broader risk-management lessons. The consensus was that the fundamental issue lay in deploying an ERC‑4626 vault-based market without proper initialization: the vault was launched effectively empty, with no initial liquidity, virtual shares, or exchange-rate guards, making it possible for a tiny donation of collateral to distort the internal accounting and bypass safety checks. This was not a failure of the ERC‑4626 standard itself but of how it was implemented and parameterized in the specific context of Resupply’s lending markets.

Security experts and the Guardrail AI analysis highlighted several best practices that could have prevented the exploit or at least made it economically infeasible. First, implementing virtual shares—synthetic initial shares that make the vault behave as if it already contains a baseline amount of assets—would have prevented manipulation of the exchange rate when the vault was empty. Second, properly seeding the vault with a meaningful amount of initial liquidity, even on the order of thousands of tokens, would have raised the cost of any donation-based attack, making it unprofitable relative to the potential gains. Third, enforcing minimum exchange-rate thresholds and using time-weighted averages for critical price calculations would have further insulated the system from sudden, single-transaction distortions.

The incident also underscored the importance of real-time monitoring and preemptive security tooling in DeFi. Guardrail’s post-mortem argued that continuous monitoring of vault initialization practices and anomalous transactions could have flagged the dangerous state earlier, allowing the protocol to correct course before the exploit occurred. In parallel, other security platforms such as Bugcrowd have promoted AI-assisted approaches like Savant, which focus on discovering exploitable attack surfaces before they are used in the wild, emphasizing risk reduction rather than purely reactive defenses. Within the Resupply community, there has been growing interest in tools like Savant Chat—AI-driven auditors that can reason about smart contract interactions and potential edge cases—complementing, rather than replacing, traditional firms and manual reviews.

Perhaps the most sobering lesson was that even protocols audited by top-tier firms are not immune from sophisticated, context-specific exploits. Curve founder Michael Egorov noted publicly that Resupply had undergone audits by highly reputable organizations, yet the wstUSR bug still slipped through. He argued that this reality justified creating a dedicated Curve-specific security team, one intimately familiar with Curve’s own codebase, Llamalend mechanics, and the kinds of integrations that protocols like Resupply pursue. Such a team could act as a second line of defense, providing ecosystem-aware reviews that complement generic audits and bringing a deeper understanding of how new markets, vaults, and cross-protocol interactions might fail.

From a recovery standpoint, the Resupply exploit also serves as a case study in social and economic resilience. Within days, the majority of the bad debt had been covered by protocol treasuries and a significant personal contribution from core developer C2tP, demonstrating a strong commitment from both the team and its backers to make users whole. The remaining deficit was addressed through the Yearn loan, which not only provided capital but also symbolized confidence from a major DeFi institution in Resupply’s long-term viability. As the loan is repaid via protocol revenue, including yield from staked RSUP, the process effectively channels future growth and cash flows into repairing past damage, aligning incentives for all stakeholders to support a secure and sustainable version of the protocol going forward.

User Flows, Strategies, and Risks

For end users, Resupply presents itself as a way to turn stablecoin holdings into levered, yield-bearing positions with a familiar CDP interface. The most common entry path is via Curve’s crvUSD: a user who holds crvUSD deposits it into a Resupply market, where it becomes collateral that is simultaneously earning yield in a lending venue like Llamalend. The user then borrows reUSD against this collateral, paying a borrow rate that is typically designed to be lower than the yield generated by their deposit, resulting in a positive spread as long as conditions remain favorable. The borrowed reUSD can be deployed in several ways, including swapping into other stablecoins, providing liquidity on Curve, depositing into savings products like sreUSD, or looping back into Resupply as additional collateral.

The protocol’s leverage interface automates the looping strategy, allowing users to choose a target leverage factor and have the system handle the repeated borrowing, swapping, and re-depositing operations. For example, a user might start with a 1,000‑dollar crvUSD deposit and use the leverage slider to reach a notional exposure several times larger, transforming their initial capital into a more substantial yield-generating position at the cost of higher liquidation risk. The interface highlights collateral ratios, total borrowed amounts, and estimated slippage from the reUSD-to-crvUSD or reUSD-to-frxUSD swaps, giving users visibility into how their risk changes as they increase leverage. Once the position is established, the user’s net return depends on the spread between collateral yields, borrowing costs, and any additional rewards in the form of RSUP, CRV, or CVX received for participating in Resupply-related pools.

Beyond leverage, more conservative users may choose to simply hold reUSD or convert it into sreUSD to earn protocol-level yield without taking on significant additional leverage. sreUSD, as a savings-layer token, offers a simplified path for users who want exposure to the income streams generated by Resupply’s CDPs without actively managing collateral ratios or leverage levels. Meanwhile, liquidity providers can supply reUSD and other stablecoins to Curve pools, contributing to peg stability while earning trading fees and convexified rewards. Active DeFi participants may also combine Resupply with other protocols in the Curve stack, such as using Prisma or other CDP systems to borrow against different collateral types and diversify their leverage portfolios across multiple stablecoins and strategies.

All of these strategies come with risks that go beyond the simple volatility of a stablecoin’s peg. Smart contract risk is primary: as the 2025 exploit demonstrated, even audited contracts can contain subtle bugs, especially when integrating complex standards like ERC‑4626 and when launching new markets with novel collateral types. Market and liquidity risk also matter: if Curve Lend or Fraxlend experience abnormal behavior, sharp changes in interest rates, or liquidity crunches, the yield assumptions underpinning Resupply’s positive carry can break down, and liquidations may become more frequent or severe. There is also stablecoin-specific risk, including depegs or design failures in backing assets like crvUSD, FRAX-based tokens, or other integrated stablecoins; such events could directly impair collateral values and undermine reUSD’s backing.

Additionally, leverage and looping strategies magnify these underlying risks. A small shock to interest rates, oracle feeds, or collateral pegs that might be manageable in an unlevered position can become catastrophic when applied to a heavily leveraged CDP. Users must therefore calibrate their leverage levels, monitor collateral ratios closely, and be prepared to top up or unwind positions during periods of market stress. Finally, governance and counterparty risk at the protocol level cannot be ignored: Resupply’s dependence on the goodwill and coordination of Curve, Convex, Yearn, and its own core contributors means that political or organizational disruptions could affect everything from incentive flows to recapitalization capacity in the event of future incidents.

Competitive Landscape: Resupply Among Stablecoin CDPs

Resupply operates in a crowded field of decentralized stablecoins and CDP protocols, but its focus on yield-bearing stablecoin collateral gives it a distinctive niche. MakerDAO’s DAI remains the archetypal overcollateralized stablecoin, backed by a mix of crypto assets, tokenized real-world assets, and other stablecoins, with the protocol increasingly focused on real-world yield strategies and institutional-grade collateral. Sky Protocol’s ecosystem, which emerged from Maker’s evolution, has expanded the set of stablecoins it issues—including DAI, USDS, and sUSDS—and as of late 2025 was generating hundreds of millions of dollars in annualized gross revenue and significant net protocol profits. Protocols like Sky demonstrate the scale and profitability that mature stablecoin systems can achieve when they successfully integrate yield-bearing collateral at size.

Prisma offers another point of comparison, focusing on allowing users to mint stablecoins against liquid staking derivatives such as stETH, rETH, or other LSTs, and then route those assets into Curve and Convex to optimize yields and liquidity. In contrast, Resupply concentrates on stablecoin collateral rather than LSTs, which changes its risk profile and integration surface. Whereas Prisma users seek to unlock value from yield-bearing versions of ETH and other volatile assets, Resupply users focus on turning stablecoins like crvUSD into even more productive capital, relying on interest-rate spreads and composability within the Curve stack. Both models are built around the idea that CDPs should be backed by inherently income-generating assets, but they target different segments of the DeFi collateral landscape.

Algorithmic and undercollateralized stablecoins provide a cautionary backdrop for Resupply’s design philosophy. Past experiments that relied on reflexive demand, purely algorithmic pegs, or insufficient collateral have often experienced catastrophic failures during periods of stress. By insisting on overcollateralization, integrating with battle-tested lending markets, and tying minting capacity to stable, yield-bearing assets, Resupply situates itself firmly within the “conservative” camp of stablecoin engineering, even as it pushes the envelope on capital efficiency and yield stacking. Its exploit history, however, shows that conservatism in collateral type does not automatically eliminate protocol risk; smart contract design and risk management remain crucial.

Index products such as the OPEN Stablecoin Index have started to include or rebalance toward reUSD, reflecting a market perception that Resupply has become a meaningful part of the decentralized stablecoin universe. This positioning matters because it can influence how DeFi users and DAOs allocate treasury assets, collateral choices, and liquidity mining programs. If Resupply continues to grow its integrations—especially via products like sreUSD, fxSAVE-linked markets, and cross-protocol strategies involving Curve, Convex, and Yearn—it could solidify its role as a core building block in the stablecoin leg of the DeFi stack, alongside incumbents like DAI, FRAX, and newer entrants from ecosystems like Sky and Prisma.

An exploit in the wstUSR market generated ~$10M in bad debt; separately, multiple high-severity bugs were discovered in inherited Prisma Finance contracts during the shutdown process.

Protocol recovery relied heavily on voluntary action by a single named developer (C2tP) and bilateral negotiation with Yearn Finance rather than a fully autonomous DAO treasury mechanism.

A $10M bad-debt hole required a two-part patchwork — direct developer contribution plus a one-year Yearn loan at 6% interest — exposing the protocol's limited on-chain emergency liquidity.

Stable-on-stable redemption mechanics and the reUSD peg to USD reduce directional market risk relative to protocols collateralised by volatile assets.

The Prisma-to-Resupply migration required a Snapshot vote and an airdrop to vePRISMA holders, creating a window where governance legitimacy and token distribution were contested simultaneously.

Despite completing a second audit before launch, an AI auditing tool (Savant Chat) was subsequently credited with surfacing the bug that caused the exploit, raising questions about audit scope coverage.

Conclusion

Resupply represents a deliberate attempt to redesign the CDP-based stablecoin model around stable, yield-bearing collateral and deep integration with the Curve–Convex–Yearn stack. By allowing users to borrow reUSD against stablecoins like crvUSD that are already earning yield in lending markets, and by structuring borrow rates to be lower than collateral yields under normal conditions, the protocol aims to offer capital-efficient, positive-carry debt positions that are less exposed to the violent price swings of volatile assets. Its design extends beyond simple leverage, incorporating looping strategies, a savings-layer token in sreUSD, and a governance and incentive token, RSUP, that plugs into Convex’s yield amplification mechanisms.

At the same time, Resupply’s trajectory has been shaped by a major exploit in its wstUSR market, which revealed shortcomings in vault initialization and risk controls but also showcased the protocol’s capacity for rapid recovery through treasury support, personal contributions, and an institutional loan from Yearn. The incident catalyzed broader discussions about security in the Curve ecosystem, the limits of traditional audits, and the role of AI-driven tools such as Savant in preemptive vulnerability detection. In the months that followed, Resupply’s focus on recapitalization, transparent post-mortems, and tighter integration with Curve Lend and savings products signaled a commitment to turning a crisis into an opportunity to harden both code and governance.

For a crypto news audience tracking the evolution of DeFi stablecoins, Resupply illustrates several key themes: the shift toward yield-backed collateral, the strategic importance of ecosystem alignments with platforms like Curve and Convex, the ongoing arms race between protocol design and security threats, and the emergence of savings-layer stablecoins that blur the line between base money and yield-bearing instruments. As part of the broader Curve-centric cluster that includes crvUSD, Llamalend, Convex, Prisma, and related protocols, Resupply is likely to remain a focal point for debates about capital efficiency, risk, and the future structure of decentralized money markets.

Outlook

Looking ahead, Resupply’s prospects will depend on its ability to maintain reUSD’s peg, scale TVL and borrowing in a risk-aware manner, and translate its integrations with Curve Lend, Fraxlend, and Yearn into durable, diversified revenue streams. Continued growth of products like sreUSD and fxSAVE-linked markets, combined with active governance participation from Convex and Yearn, could solidify its status as a core yield-backed stablecoin layer within the Curve ecosystem. At the same time, the protocol will need to remain vigilant on security, embracing ecosystem-specific audits, AI-assisted monitoring, and conservative rollout practices for new markets. If Resupply can balance innovation with operational discipline, it is well positioned to remain a key reference point in the ongoing story of DeFi-native stablecoins and composable leverage.

Latest Resupply news

Convex recaps the history of Resupply ($RSUP) and its $reUSD stablecoin backed by yield-bearing positions in Curve Lend and FraxlendFeel good using Resupply? That’s by designResupply outlines a next-generation CDP model built around stable, yield-generating collateral, reducing liquidation risk while improving capital efficiency versus traditional ETH/BTC-based CDPs. By integrating real revenue, looping strategies, and stable LTVs, Resupply reframes CDPs into productive capital primitives. Resupply proposes to mint and supply $5MM crvUSD into the sreUSD Llamalend market

Resupply proposes to mint and supply $5MM crvUSD into the sreUSD Llamalend market The $SKY is falling! Resupply displaces Sky Protocol in the $OPEN Stablecoin Index Q4 Rebalance

The $SKY is falling! Resupply displaces Sky Protocol in the $OPEN Stablecoin Index Q4 Rebalance Leviathan Livestream: Join today's Llama Party with latest updates on Curve, Yield Basis, Resupply, hacks, and all the news that's fit to ink

Leviathan Livestream: Join today's Llama Party with latest updates on Curve, Yield Basis, Resupply, hacks, and all the news that's fit to inkSources

- https://www.coingecko.com/en/coins/resupply-usd

- https://x.com/ResupplyFi/status/1938092252431036491

- https://gov.yearn.fi/t/yip-86-resupply-bad-debt-repayment-loan/14516

- https://x.com/ConvexFinance/status/1876252412383822194

- https://cnginc.com/shell-cng-collaborate-circular-film-solutions/

- https://defillama.com/protocol/resupply

- https://coinsbench.com/from-1-wei-to-10m-reusd-anatomy-of-a-resupplypair-exploit-9e97748fdce1

- https://www.nasa.gov/news-release/nasa-sets-coverage-for-spacex-34th-station-resupply-launch-arrival/

- https://www.bugcrowd.com/blog/savant-bugcrowds-ai-strategy-for-preemptive-security/

- https://x.com/newmichwill/status/1939242859024228785

- https://www.guardrail.ai/blog/resupplyfi-hack

- https://docs.curve.finance/user/llamalend/overview

- https://www.coincarp.com/currencies/resupply/

- http://gov.curve.finance/t/llamarisk-progress-update-july-december-2025/10981

- http://gov.curve.finance/t/llamarisk-quarterly-update-april-june-2025/10711

- https://x.com/leviathan_news/status/2002921054792999269

- https://docs.resupply.fi/how-to-guides/using-resupply/leverage

- https://www.binance.com/az-AZ/square/post/22335071678577

- https://globalfintechseries.com/finance/sky-ecosystem-is-generating-435m-in-annualized-protocol-revenue-and-168m-in-annualized-protocol-profits/

- https://news.curve.finance/curve-monthly-recap-june-2025/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…