In‑depth explainer on Yield Basis, Curve’s BTC‑ and ETH‑focused IL‑free liquidity protocol. Covers FXSwap design, crvUSD credit lines, YB tokenomics, Hybrid Vaults, risks, and how it compares to Uniswap v3 and other DeFi yield strategies.

+1 sources across the wider coverage universe

Yield Basis selected Firepan to perform an AI-powered security review of its live mainnet FeeDistributor contract, identifying 18 findings across 22 attack surfaces, including a previously undocumented MEV vector.2026-05

Yield Basis selected Firepan to perform an AI-powered security review of its live mainnet FeeDistributor contract, identifying 18 findings across 22 attack surfaces, including a previously undocumented MEV vector.2026-05 FXSwap might have just fixed the biggest problem in LP design2026-06

FXSwap might have just fixed the biggest problem in LP design2026-06 YieldBasis launches new pools with most capacity reserved for LP migrations as Curve flags crvUSD upside2026-05

YieldBasis launches new pools with most capacity reserved for LP migrations as Curve flags crvUSD upside2026-05 Yield Basis confirms hybrid ETH vault is now live after governance approval, opening early access to new yield strategies and marking next phase of protocol growth2026-04

Yield Basis confirms hybrid ETH vault is now live after governance approval, opening early access to new yield strategies and marking next phase of protocol growth2026-04 Yield Basis completes first full market cycle, distributes $3.84M in fees to YB lockers2026-04

Yield Basis completes first full market cycle, distributes $3.84M in fees to YB lockers2026-04 Yield Basis: Solving Impermanent Loss to Scale DeFi for the Bitcoin Macro Cycle2026-02

Yield Basis: Solving Impermanent Loss to Scale DeFi for the Bitcoin Macro Cycle2026-02

Yield Basis: Leveraged, Impermanent‑Loss‑Free Liquidity on Curve

Yield Basis is a Bitcoin‑native yield and liquidity protocol built around Curve’s FXSwap AMM and the crvUSD ecosystem, aiming to give LPs leveraged BTC and ETH exposure while neutralizing classic impermanent loss through a fixed‑leverage design. At its core, Yield Basis routes BTC and WETH deposits into specialized Curve pools, pairs them with borrowed crvUSD, and continuously rebalances positions so that LPs earn fees on an effective 2× liquidity position while retaining a nearly linear exposure to the underlying crypto asset rather than the usual convex AMM payoff.

From Impermanent Loss to Linear Exposure: The Problem Yield Basis Tries to Solve

Any attempt to understand Yield Basis begins with impermanent loss, the pervasive, often misunderstood risk that arises when providing liquidity to automated market makers. Classic constant‑product AMMs such as Uniswap v2 embed a simple pricing rule, typically written as \(x \cdot y = k\), where \(x\) and \(y\) are the reserves of two assets and \(k\) is a constant. As prices move, the pool automatically rebalances, meaning LPs end up with more of the underperforming asset and less of the outperforming one, which creates a gap between the value of their LP position and the value they would have had if they simply held the assets in their original proportions. This gap is what DeFi calls impermanent loss, and it can outweigh trading fees in volatile markets, particularly for retail LPs who are not actively managing their positions.

The introduction of concentrated liquidity with Uniswap v3 allowed LPs to choose specific price ranges within which they provide liquidity, theoretically improving capital efficiency and allowing sophisticated operators to offset impermanent loss with more targeted fee capture. However, this came at the cost of significantly increasing complexity and maintenance demands: if the market moves outside an LP’s chosen range, their position becomes effectively idle, no longer earning fees until it is manually rebalanced. Empirical work and on‑chain experience have shown that many LPs underperform simple buy‑and‑hold strategies because they cannot or do not actively manage positions, particularly through sharp market moves. This context—high IL risk for passive LPs and operational overhead for active ones—is the backdrop against which Yield Basis presents itself as a new paradigm.

Curve Finance historically approached this problem from a different angle, focusing on stableswap designs optimized for assets that should track each other closely, such as stablecoins or tokenized versions of the same underlying asset. By targeting low slippage within a narrow band around a shared peg, Curve’s original stableswap algorithm greatly reduced impermanent loss risk for LPs relative to volatile‑asset pools. As the protocol expanded into CryptoSwap for correlated but volatile assets, and later into FXSwap for pairs that drift over time, it progressively generalized this approach while maintaining an emphasis on passive liquidity and reduced IL. FXSwap, in particular, was designed for volatile and FX‑style pairs that do not share a fixed peg, combining pricing elements from Stableswap and Cryptoswap with a new mechanism called “Refueling” to keep liquidity deep without requiring continuous LP micromanagement.

Even with these advances, volatile‑asset pools still expose LPs to price‑path‑dependent payoffs, and therefore to impermanent loss in the conventional sense. Yield Basis explicitly targets this residual risk by combining Curve’s AMM architecture with a fixed‑leverage strategy that aims to linearize LP exposure to BTC and ETH. The central idea is to use leverage not to amplify speculative bets, but to reshape the payoff profile of LPs so that they look more like straightforward long positions on the underlying assets, while still capturing trading fees and, potentially, additional yield from borrowing and lending flows. For long‑term Bitcoin holders and DeFi treasuries that want protocol‑native yield without sacrificing directional exposure, this promise is powerful, and it explains both the enthusiasm and the scrutiny surrounding Yield Basis.

FXSwap might have just fixed the biggest problem in LP design

$10M BTC clips being ~2% better in ~80% of sampled blocks is enough for aggregators; the static 1% YieldBasis fee just means small flow can stay on Uni while whale flow routes where depth survives volatility. YieldBasis already showed the bottleneck: caps filled in minutes at $300M, so scaling comes down to crvUSD/PegKeeper capacity plus refuel funding, not LP appetite. If Curve keeps that credit/subsidy loop disciplined, FXSwap starts looking like sponsored onchain market making for BTC, ETH, and FX stables without handing the PnL to offchain desks.

Readers are not clicking Yield Basis for yield numbers alone — they are working through a credibility audit: does Michael Egorov's IL-elimination claim hold up under real market stress, adversarial scrutiny, and crvUSD's sovereign risk exposure?↗

Curve, crvUSD, and the Infrastructure Behind Yield Basis

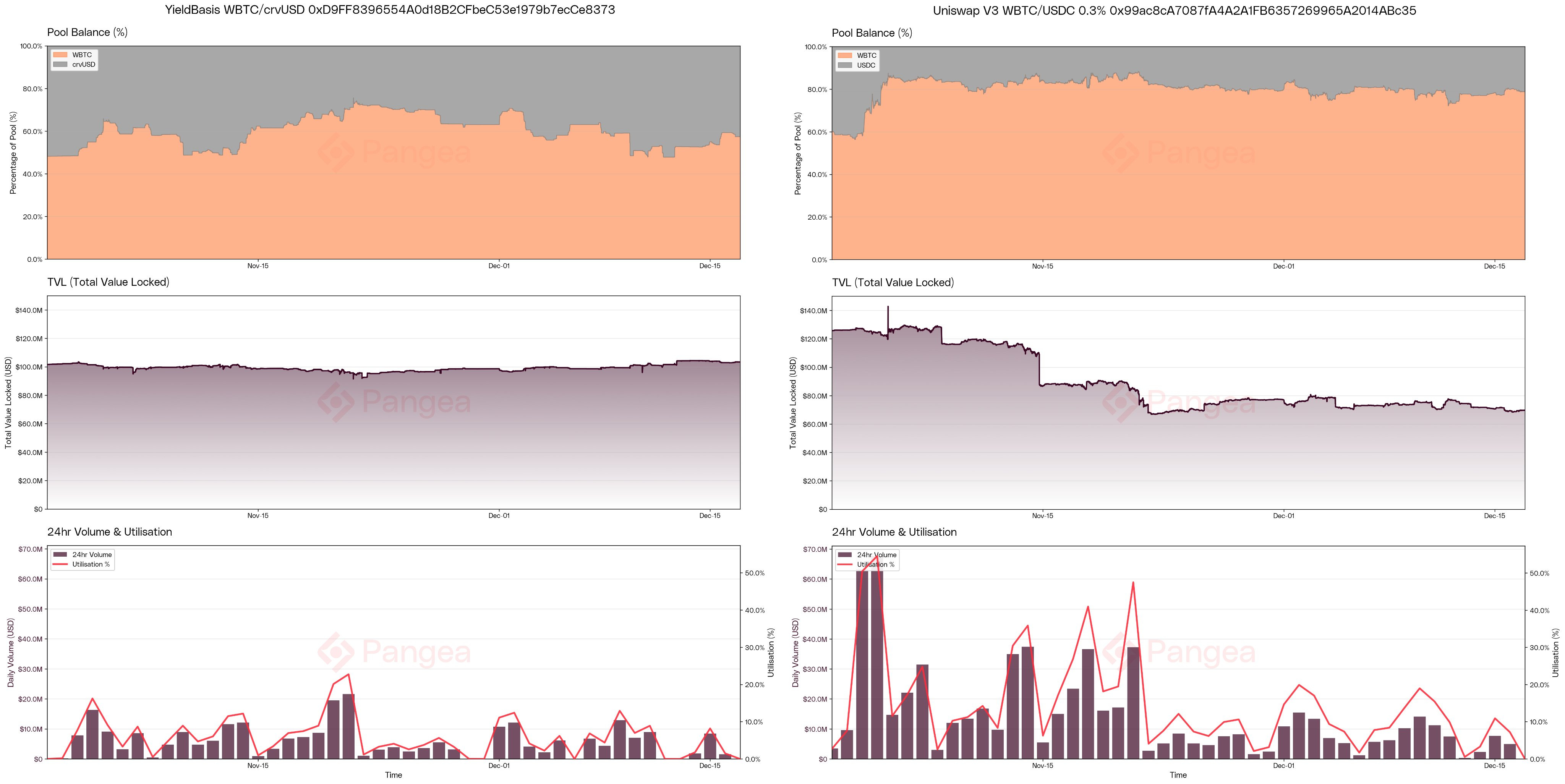

Yield Basis does not operate in isolation; it is deeply intertwined with Curve Finance and its native stablecoin, crvUSD. Curve’s evolution from a stablecoin DEX to a broader AMM infrastructure provider is crucial context for understanding YB’s design choices, since it uses Curve’s FXSwap AMM as the primary liquidity engine for its pools. FXSwap was introduced as a new algorithm specifically for trading volatile and FX‑style asset pairs that are expected to drift over time rather than maintain a tight peg. In practice, it has been used both for classic crypto‑volatile pairs, such as BTC‑crvUSD and ETH‑crvUSD, and for lower‑volatility foreign‑exchange and real‑world‑asset pairs such as CHF, GBP, BRZ, and IDR.

The FXSwap algorithm attempts to combine the pricing efficiency of Stableswap with the passive rebalancing framework of Cryptoswap, layered with a mechanism called Refueling that helps maintain deep liquidity even as prices drift over longer horizons. Independent analysis from Pangea suggests that FXSwap offers significantly improved performance for large trades relative to comparable Uniswap v3 pools, especially in terms of slippage and depth, making it a compelling base for protocols that want to deploy large, passive liquidity positions. This is directly relevant for Yield Basis, which needs to move sizable amounts of BTC and crvUSD while maintaining a consistent leverage ratio and not relying on active per‑position management.

The other pillar of Yield Basis’s design is crvUSD, Curve’s native dollar‑pegged stablecoin. crvUSD is minted via overcollateralized borrowing against volatile assets, using a mechanism known as LLAMMA (Lending‑Liquidating AMM Algorithm), which gradually liquidates collateral as its price falls rather than relying on abrupt liquidations at fixed thresholds. This soft‑liquidation framework attempts to make leverage more forgiving, smoothing the impact of volatility and distributing liquidation risk over a broader price band. While the details of LLAMMA are beyond the scope of this explainer, the key point is that crvUSD issuance is naturally tied to the volatility and liquidity of the underlying collateral markets, which in Yield Basis’s case are deeply connected to BTC and ETH pools.

Yield Basis uses crvUSD as the stablecoin leg of its primary liquidity pools and also relies on a credit line of crvUSD from Curve’s Llamalend lending markets to achieve its targeted 2× effective leverage. According to project disclosures and independent analysis, Yield Basis initially secured a roughly 60 million crvUSD credit line sourced from Curve DAO governance, with subsequent proposals—championed by Curve founder Michael Egorov—seeking to increase this allocation up to 1 billion crvUSD as the protocol scales. This credit line is a core piece of the design: it allows Yield Basis to borrow crvUSD against BTC collateral in a way that is tightly integrated with Curve’s risk management framework, then pair that borrowed crvUSD with user‑supplied BTC or WETH in FXSwap pools to create leveraged, yet supposedly IL‑free, LP positions.

Because of this tight integration, structural flows between Yield Basis and crvUSD have become a major topic of research and debate. Pangea’s analysis finds that Yield Basis flows now account for more than 36% of Curve’s crvUSD trading volume, climbing above 60% on days of high BTC volatility. Their research concludes that these structural flows tightly couple the crvUSD system as a whole to Bitcoin price movements, meaning that BTC market cycles can have outsized effects on crvUSD issuance and trading dynamics. A companion study from Pangea observes a notable increase in the volatility and peg deviation of crvUSD since the launch of Yield Basis, while explicitly stopping short of asserting a direct causal relationship. Together, these findings highlight both the strategic importance of Yield Basis for Curve’s growth and the systemic risks that can arise when a stablecoin’s activity becomes highly concentrated in a single yield mechanism.

Against this backdrop, Yield Basis positions itself as “built for the Bitcoin macro cycle,” offering BTC‑native yield strategies that leverage Curve’s AMM infrastructure and crvUSD’s design to align liquidity provision with long‑term BTC exposure. This macro framing is not merely marketing; it encapsulates the idea that, if Bitcoin undergoes another major multi‑year bull cycle, a protocol that can safely recycle BTC collateral into deep stablecoin liquidity while shielding LPs from IL could become a critical piece of DeFi infrastructure. It is within this narrative—Bitcoin as reserve asset, Curve as liquidity hub, crvUSD as native dollar, YB as yield layer—that the protocol’s ambition and risk profile must be evaluated.

What Yield Basis Is and How It Is Structured

Yield Basis can be described as a specialized liquidity and leverage protocol that builds on Curve’s AMM architecture to deliver BTC‑ and ETH‑denominated yield with a targeted elimination of classical impermanent loss. Conceived by Michael Egorov, the founder of Curve Finance, Yield Basis launched in early 2025 with an initial focus on Bitcoin, using BTC‑crvUSD FXSwap pools to implement its core design. Over time, it has expanded to support WETH‑crvUSD pools and more advanced structured products such as Hybrid Vaults, while maintaining its central promise: LPs earn fees and borrow‑lending spread on an effectively 2× leveraged liquidity position, but their net price exposure behaves like a simple long on BTC or ETH rather than the usual AMM curve.

At a high level, Yield Basis works by splitting the economic roles between different participants and smart contracts. Users deposit BTC (or wrapped BTC) or WETH into Yield Basis vaults, which then use that collateral to open leveraged positions in Curve’s FXSwap pools by borrowing crvUSD through Llamalend or a similar mechanism. The protocol algorithmically targets a fixed leverage ratio—commonly described as 2×—meaning that for every dollar of user BTC collateral, it aims to deploy roughly two dollars’ worth of liquidity in the BTC‑crvUSD pool. This is achieved by pairing the BTC with an equal notional amount of crvUSD, half of which is effectively funded by borrowing. The result is a synthetic 50/50 BTC‑crvUSD LP position with total notional value of about twice the user’s initial BTC contribution.

What makes this design distinct from simply levering up in any other AMM pool is that Yield Basis continuously rebalances the position to maintain both the target leverage and a specific exposure profile. Independent commentary from Pangea and Mirador explains that by fixing the compounding leverage at roughly 2× and actively managing the BTC‑to‑crvUSD split around a 50/50 target between debt and equity, Yield Basis “removes classic AMM impermanent loss” and neutralizes the curvature of the LP payoff. In other words, the protocol uses leverage and rebalancing to cancel out the convexity introduced by the constant‑product or hybrid AMM curve, so that LPs end up with a payoff that is approximately linear in BTC price, similar to holding BTC directly, plus the additional yield from trading fees and interest flows.

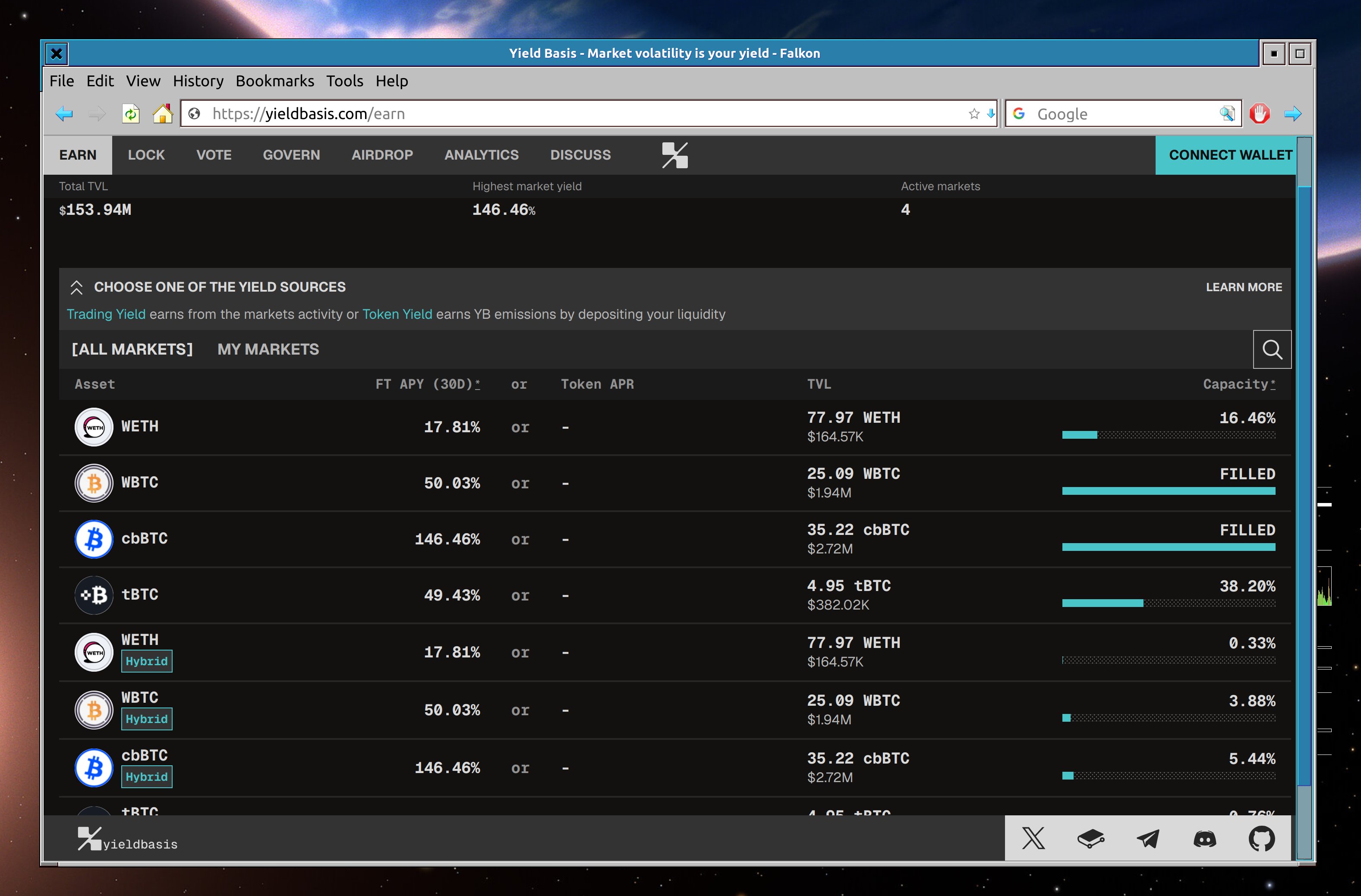

From a user’s perspective, the primary interface with Yield Basis is through its vaults and pools. The protocol has iterated through multiple pool implementations, culminating in what it refers to as “v3 pools,” with plans and governance proposals for migrating all existing LP positions into this new architecture. According to governance and community updates, new pools implementations and dedicated migration contracts are deployed through YieldBasisDAO, with early capacity often reserved for migrating LPs to ensure continuity and minimize slippage during transition periods. Over time, the protocol has also introduced Hybrid Vaults that sit atop these pools, offering more complex yield strategies with per‑LP caps to manage risk and maintain crvUSD peg stability as the system scales.

Yield Basis is governed and incentivized via the YB token, a capped‑supply governance and fee‑sharing asset with a maximum supply of 1 billion tokens, of which roughly 300 million entered circulation at launch. The token is distributed across community incentives, team allocations, development reserves, investor sales, Curve ecosystem permissions, and partner allocations, with one analysis indicating that the team and investors collectively control about 35% of the supply, and the Curve ecosystem allocation brings insider‑associated holdings to approximately 45%. Holders can lock YB into a vote‑escrowed form known as veYB, similar to Curve’s veCRV model, to gain governance power and a share of protocol fees. Over time, third‑party protocols such as Stake DAO and Yearn have launched liquid lockers for YB, known respectively as sdYB and yYB, further integrating Yield Basis into the broader DeFi governance and yield ecosystem.

Thus, structurally, Yield Basis is best understood as a layered protocol: at the base, Curve’s FXSwap pools for BTC‑crvUSD and WETH‑crvUSD; in the middle, leverage management and rebalancing logic that maintains 2× effective exposure and neutralizes IL; and at the top, governance, tokenomics, and structured vault strategies that distribute fees and risks among YB holders, veCRV holders, and LPs.

The Mechanics: How Yield Basis Makes Impermanent Loss “Zero”

The central technical claim of Yield Basis is that it can make impermanent loss effectively “zero” for LPs, at least in the sense of classic AMM IL measured against a simple buy‑and‑hold benchmark. To unpack this, it is useful to revisit how IL arises in a constant‑product AMM and then show how a fixed‑leverage, actively rebalanced strategy can cancel out the curvature that causes this loss.

In a standard constant‑product AMM, an LP providing equal values of BTC and a stablecoin such as crvUSD initially holds a 50/50 portfolio by value. As the BTC price rises relative to crvUSD, the pool algorithm automatically sells BTC for crvUSD to keep \(x \cdot y = k\) balanced, which means the LP ends up holding relatively less BTC and more crvUSD than they would if they simply held their initial BTC plus stablecoin. When they withdraw liquidity, they receive fewer BTC than if they had never LP’d but instead merely held both assets in a fixed ratio in a wallet. The foregone upside—often expressed as a percentage of the hold strategy’s final value—is what we call impermanent loss. Mathematically, the LP’s payoff resembles a concave function of BTC price, since they are systematically selling into rallies and buying into dips.

Yield Basis attacks this concavity by superimposing a leverage layer on top of the AMM exposure. According to Pangea’s explanation, Yield Basis targets a fixed compounding leverage of 2× by borrowing crvUSD against BTC collateral, then using both the borrowed crvUSD and the original BTC to provide liquidity in a Curve FXSwap pool. In practice, this means that the system tries to maintain a roughly 50/50 split between a user’s “equity” exposure and “debt” exposure, so that half of the pool position is effectively funded by borrowed crvUSD, while the other half corresponds to the user’s own BTC. Because the borrowed crvUSD liability is fixed in nominal terms, while the BTC portion fluctuates with price, the combined position can be constructed such that its net delta (price sensitivity) approximates one BTC per unit of user collateral.

Mirador’s analysis further clarifies that Yield Basis continuously adjusts positions—essentially rebalancing the mix of BTC and crvUSD in the pool and the debt balance—to maintain this target exposure. Because the system is constantly adjusting, the curvature of the LP payoff that would normally arise from the AMM’s pricing function is effectively neutralized at the portfolio level. The resulting structure behaves like a linear position: as BTC price rises or falls, the LP’s net value moves almost one‑for‑one with BTC, plus or minus the contribution from trading fees and borrowing costs. Leveraging by a factor of roughly two in the pool amplifies fee earnings relative to the user’s initial BTC deposit, which is why Yield Basis can advertise an effective “market‑making effect” of 1,000 dollars of liquidity for every 500 dollars of BTC supplied.

One way to visualize this is to think in terms of two conceptual sub‑positions. The first is a leveraged LP position in the BTC‑crvUSD pool, which on its own would be highly nonlinear and subject to substantial impermanent loss. The second is a synthetic position created by borrowing and lending that offsets the curvature of the first position, leaving a residual payoff curve that is much closer to a straight line. By fixing the leverage and maintaining the 50/50 debt‑to‑equity split, Yield Basis effectively transforms the LP role into something akin to a structured product: a leveraged, fee‑earning long BTC position with termless duration, collateralized by BTC and denominated in a mix of BTC and crvUSD.

This does not mean that all forms of risk are eliminated—far from it. The structure still exposes users to BTC price volatility, potential liquidation risk if BTC prices fall far enough, and counterparty risk related to the crvUSD credit line and Curve smart contracts. What Yield Basis specifically targets is the subset of risk known as classical impermanent loss relative to buy‑and‑hold, which it seeks to neutralize using leverage and continuous rebalancing. Independent commentary from Leviathan‑adjacent educational content and Mirador’s “Impermanent Loss and how Yield Basis makes it ‘zero’” series emphasizes that, under the model assumptions, IL is effectively removed, but stresses that users must still understand leverage, liquidation, and stablecoin risks.

In practice, the effectiveness of this IL neutralization depends on how well the protocol maintains its leverage target and rebalancing cadence, as well as how accurately external factors such as oracle prices and AMM pricing reflect true market conditions. Slippage, MEV, and extreme volatility events can all introduce deviations between the idealized model and real‑world performance, which is why empirical performance analysis, such as that undertaken by Pangea and other researchers, is essential to assessing whether Yield Basis’s IL‑free claim holds at scale.

YieldBasis launches new pools with most capacity reserved for LP migrations as Curve flags crvUSD upside

Michael Egorov says the new YieldBasis pools are live, with limited direct-deposit capacity available when a pool shows under 100% and most room reserved for migrations from the old vaults. YieldBasis later said migration has started for LPs, while Curve called the move good for crvUSD. The new markets are already making fees, but Egorov says distribution depends on a new vote passing.

- 01IL elimination mechanism credibility↗

The core claim — leveraged Curve v2 pools eliminate impermanent loss on BTC and ETH — drove the highest-clicked headline and spawned a separate whitepaper thread, signaling readers wanted the math, not just the marketing.

- 02crvUSD scaling governance↗

Multiple high-click proposals to raise the crvUSD credit line from $108M to $300M to $1B revealed an ongoing governance negotiation readers tracked as a proxy for whether Curve DAO trusted Yield Basis with real capital.

- 03Isolated vault systemic risk↗

Community concern that Yield Basis drew from a private crvUSD mint market unavailable to public borrowers made readers want to evaluate whether this created hidden backstop risk for the broader Curve ecosystem.

- 04Security audit findings↗

Firepan's AI-powered audit of the live mainnet FeeDistributor contract finding 18 issues including an undocumented MEV vector signaled that readers were tracking real attack surface exposure, not theoretical risk.

- 05YB token and veYB launch↗

The $YB airdrop for Curve DAO supporters and liquid locker pre-secondary-market risk drove clicks from readers evaluating entry timing and governance token distribution fairness.

- 06Flash crash stress test↗

Pangaea's detailed post-mortem of LP gains and losses during the October 10 flash crash gave readers the first real-world performance data against the IL-free claim under adverse conditions.

FXSwap, Llamalend, and the Role of crvUSD Credit Lines

Yield Basis’s mechanics rely heavily on two key pieces of infrastructure: Curve’s FXSwap AMM and crvUSD credit lines sourced from Llamalend or equivalent lending modules. FXSwap, as described in Curve’s own documentation, is an AMM algorithm engineered for asset pairs that are expected to drift rather than maintain a strict peg, including both volatile crypto pairs and foreign‑exchange style pairs. It incorporates pricing efficiency from Stableswap, which excels at tight‑spread trading near a peg, and the passive rebalancing approach of Cryptoswap, which handles correlated volatility better, plus a new “Refueling” mechanism that helps ensure liquidity persists even as prices move over wider ranges. Back‑testing and on‑chain data analyzed by Pangea indicate that FXSwap can offer materially better execution for large trades than comparable Uniswap v3 pools, particularly due to its sustained depth and lower slippage profile across a broader price band.

This makes FXSwap an attractive base for Yield Basis, which needs to maintain deep two‑sided liquidity in BTC‑crvUSD and WETH‑crvUSD pairs while rebalancing positions to preserve a fixed leverage ratio. Unlike Uniswap v3, where LPs must actively select and adjust price ranges, FXSwap facilitates more passive liquidity deployment, aligning with Yield Basis’s goal of offering set‑and‑forget yield strategies to BTC and ETH holders. Moreover, because FXSwap is native to Curve, it can be tightly integrated with crvUSD issuance and Llamalend borrowing, enabling a more seamless management of collateral, debt, and LP positions across shared smart‑contract infrastructure.

The crvUSD credit line is the other crucial link. Gate.io’s analysis and protocol documentation indicate that Yield Basis originally received a 60 million crvUSD credit line from Curve DAO, which is used to borrow the stablecoins that pair with BTC and WETH in its pools. Additional proposals—championed by Michael Egorov and discussed in Curve governance channels—have sought to raise this cap significantly, with some discussions targeting up to 1 billion crvUSD to support larger‑scale deployments as the protocol matures. Pangea’s “Scaling YieldBasis to $1bn” research explores the implications of such an expansion, emphasizing that structural flows between Yield Basis and crvUSD grow proportionally with the credit line, further entangling the stablecoin’s dynamics with BTC’s price cycle.

One point of contention has been the nature of the lending model underpinning this credit line. Gate.io’s critical review argues that Yield Basis relies on what it calls “equivalent lending,” in contrast to more traditional overcollateralized lending models in DeFi. While the specific terminology can be debated, the critique centers on the idea that the crvUSD reserves backing the credit line may be insufficient if BTC prices fall sharply and YB positions are forced to unwind quickly, given that the BTC collateral is simultaneously a source of liquidity and the asset backing the loans. In this view, the intricate interplay between BTC‑denominated collateral, crvUSD debt, and FXSwap liquidity resembles, in some respects, the circular structures observed in failed systems such as Luna‑UST, albeit with important differences in collateralization and risk control.

Supporters counter that crvUSD remains an overcollateralized stablecoin with LLAMMA‑based soft liquidations, and that the credit line is subject to risk parameters and governance oversight designed to prevent reckless expansion. Pangea’s research, for example, does not label the system as unsound but instead highlights how structural flows from Yield Basis couple crvUSD’s behavior to BTC price movements and recommends careful calibration and monitoring as the credit line grows. The key takeaway for observers is that Yield Basis’s reliance on an expanding crvUSD credit line introduces systemic linkages between a major stablecoin and a single yield protocol, which must be managed prudently through stress testing, governance, and coordinated risk oversight across Curve, YieldBasisDAO, and external risk managers such as LlamaRisk.

The existence of this credit line also shapes YB’s yield profile. The protocol’s original profit formula has been described as something like: profit equals twice the transaction fees minus the borrowing rate minus rebalancing costs. The “2× transaction fee” term comes from the fact that a user supplying 500 dollars’ worth of BTC can support a 1,000‑dollar liquidity position thanks to leverage, effectively doubling their fee‑earning capacity. The borrowing rate represents the interest paid on crvUSD loans from Llamalend, while rebalancing costs include the expenses incurred by arbitrageurs and active traders who help maintain the system’s target leverage and peg relationships. After covering these costs, residual profits are shared among LPs, YB token stakers, and, in some structures, veCRV holders, as discussed in the next section.

YB Tokenomics, Governance, and Fee Flows

The YB token sits at the center of Yield Basis’s governance and incentive structure, functioning analogously to how CRV and veCRV operate in the broader Curve ecosystem. OKX’s overview and Gate.io’s deep dive both describe YB as a capped‑supply token with a total maximum supply of 1 billion units, of which 300 million were initially in circulation. The supply is allocated across several categories: community incentives, team allocations, development reserves, investor sales, Curve ecosystem permissions, and partner allocations. One breakdown suggests that the team receives about 25% of the supply and investors around 10%, while community incentives constitute roughly 30%, with additional slices for development, partners, and the Curve ecosystem, bringing insider‑associated allocations to around 45%.

YB holders can lock their tokens into a vote‑escrowed format known as veYB, similar in design to veCRV, to gain governance rights and a share of protocol fees. Revenue sharing is a key part of the value proposition: both OKX and Gate.io note that Yield Basis distributes a meaningful portion of its fee revenue to token holders and related stakeholders, albeit with somewhat different emphases. The OKX analysis emphasizes that Yield Basis allocates between 35% and 65% of its revenue to veCRV holders, thereby strengthening Curve governance and tokenomics by giving Curve stakers a direct stake in YB’s success. Gate.io, by contrast, focuses on the internal flow of fees between LPs, YB token stakers, and veYB, highlighting how a fixed share of transaction fees is reserved for the pool itself, with the remaining portion split between LPs and YB, and a minimum guarantee for veYB holders.

According to Gate.io’s breakdown, Curve pools charge trading fees that are split between liquidity providers and the YB protocol, with the pool retaining 50% of the fees and the remaining 50% shared between LPs and YB via a dynamic mechanism. Within the YB share, veYB holders are guaranteed a minimum of 10% of total fees, while the rest is allocated dynamically among ybBTC (or analogous LP‑linked tokens) and veYB. This structure means that even if no one stakes ybBTC, LP‑linked holders can only capture roughly 45% of total trading fees, while veYB—and by extension, YB token holders—are guaranteed at least about 5%. In practice, the actual distribution depends on the staking behavior of participants and the activation of various “fee switches” governed by YieldBasisDAO.

This fee architecture has been a source of both interest and criticism. On the one hand, it creates strong incentives for long‑term alignment, as YB holders who lock into veYB receive a stream of revenue that grows with protocol volume, and veCRV holders also benefit from a share of YB‑generated fees. On the other hand, critics argue that the fact that insiders—comprising the team, investors, and potentially allied Curve interests—control a large portion of the YB supply, combined with guaranteed fee streams, raises centralization and fairness concerns. Gate.io’s article, for example, questions where the fundamental value of the YB token comes from, concluding that it is ultimately derived from fee‑sharing on the crvUSD/BTC trading pair and cautioning that concentration of token ownership could distort governance outcomes.

Governance itself is carried out through YieldBasisDAO, in which veYB holders can propose and vote on protocol changes, including new pool deployments, migration plans, fee‑switch activations, and the launch of structured products like Hybrid Vaults. Community communications and X posts from the official Yield Basis account indicate that significant decisions—such as the rollout of new pool implementations, v3 migrations, and the introduction of Hybrid Vaults—are subject to governance approval, often preceded by research from external groups such as Pangea and risk reviews from LlamaRisk. The protocol has also engaged external security firms; for example, Firepan was selected to perform an AI‑assisted security review of the FeeDistributor contract, identifying multiple findings across various attack surfaces, while a separate security review by Block 7 fellows, Panda, and HHK uncovered a critical vulnerability in the VotingEscrow transfer functions used for veYB.

The latter security review highlights the importance of ongoing governance and auditing. The report describes a critical issue in the VotingEscrow contract, where insufficient input validation in transfer functions could allow an attacker to steal veYB positions by manipulating slope changes and lock parameters. It also points to incorrect slope change accounting that could permanently corrupt voting power distribution if exploited. While the report is framed as an update security review and likely accompanied by remediation recommendations, it underscores that governance tokens and fee‑distribution mechanisms are themselves complex smart‑contract systems that must be rigorously tested and monitored. For prospective YB holders and veYB lockers, understanding the security posture of these contracts is as important as understanding the economics of fee flows.

Over time, the ecosystem around YB has grown to include liquid lockers such as Stake DAO’s sdYB and Yearn’s yYB, which allow users to gain exposure to veYB’s fee streams and governance rights without locking their tokens directly for long durations. These integrations both deepen YB’s liquidity—since liquid‑locking protocols accumulate and lock tokens on behalf of users—and introduce additional layers of complexity and risk, as users must now consider smart‑contract and governance risks in multiple protocols rather than just Yield Basis itself.

Hybrid Vaults, ETH Expansion, and Advanced Yield Strategies

While Yield Basis began as a Bitcoin‑centric protocol, designed to resolve impermanent loss for BTC LPs and align with the Bitcoin macro cycle, it has progressively expanded into ETH and more complex multi‑strategy vaults. A major recent development has been the introduction of Hybrid Vaults, a structured product that layers additional strategies on top of the core IL‑free LP design. According to project communications and coverage, Hybrid Vaults introduce per‑LP caps to enable scalable growth while maintaining crvUSD peg stability, and they offer a concentrated volatility bet for LPs, providing dual yields in BTC and stablecoins driven by market volatility. In practice, this means that Hybrid Vaults combine fee income from FXSwap pools with carefully controlled exposure to BTC price swings and borrowing‑lending spreads, aiming to enhance returns without magnifying systemic risks.

GN Crypto’s reporting notes that early deployments of Yield Basis Hybrid Vaults saw deposits jump by around 120%, signaling strong demand for these more sophisticated strategies and a willingness among LPs to embrace products that offer leveraged volatility exposure within a managed framework. To prevent this growth from destabilizing crvUSD or over‑concentrating risk, Hybrid Vaults impose per‑LP caps, limiting the size of any single participant’s exposure and thereby reducing the risk of sudden, large unwinds in stress scenarios. This design choice reflects lessons learned from other DeFi leverage products, where unconstrained growth by a handful of large positions has occasionally led to cascading liquidations and protocol stress.

Parallel to the development of Hybrid Vaults, Yield Basis has pursued expansion into ETH markets. In late 2025 and early 2026, the protocol announced plans for IL‑free Ethereum pools, positioning WETH‑crvUSD pools on Curve as a “liquidity backbone” for ETH LPs seeking leveraged yield without impermanent loss. According to Yield Basis’s own communications, IL‑free AMM pools for BTC had already generated organic, non‑subsidized yields in the 12%–22% range for BTC LPs during 2025, which the team cited as justification for expanding beyond Bitcoin into ETH. The proposed ETH pools mirror the BTC design: LPs deposit WETH, the protocol borrows crvUSD against it via Llamalend or a similar mechanism, and the combination is deployed into FXSwap pools with a target 2× leverage and linearized exposure.

The ETH expansion also ties into broader debates about the resilience of concentrated liquidity strategies during major market moves. Reports and commentary from the Yield Basis community have highlighted episodes where ETH price drops of around 30% pushed many Uniswap v3 LP positions out of range, rendering them inactive until positions were manually adjusted, while Yield Basis pools, using FXSwap and dynamic rebalancing, retained exposure and provided faster recovery paths for TRD (Target Rate Distribution) and liquidity metrics. Although such comparisons are inherently context‑dependent and may rely on specific market conditions, they illustrate the protocol’s argument that passive, IL‑free LP strategies can be more robust for certain user profiles than actively managed concentrated liquidity positions, especially through sharp market corrections.

Beyond BTC and ETH, the conceptual framework of Yield Basis could, in principle, be extended to other assets that have sufficiently liquid crvUSD or equivalent stablecoin pairs on Curve. However, this would require careful consideration of each asset’s volatility profile, collateral usefulness, and systemic implications. For now, the protocol’s roadmap, as reflected in governance discussions and research collaborations, appears focused on scaling BTC and ETH vaults, refining Hybrid Vaults, and securing larger crvUSD credit lines while maintaining crvUSD peg stability and managing risk.

Yield Basis confirms hybrid ETH vault is now live after governance approval, opening early access to new yield strategies and marking next phase of protocol growth

"On-chain data shows 12k ETH deposited into the vault in first 6 hours. Whale wallets (>10k ETH) account for 45% of inflows. Protocol TVL up 18% since announcement, but watch the 7-day moving average - similar spikes preceded 30% drawdowns in Q2." (280 chars)

$5M seed raise announced; IL-free BTC/ETH LP framing introduced

YAudit update security report published on core contracts

Whitepaper released detailing leveraged Curve v2 IL-elimination method

Mainnet launch; $30M cap filled within minutes of going live

October 10 flash crash; Pangaea publishes LP gains/losses post-mortem

Firepan AI security review finds 18 findings including novel MEV vector on live FeeDistributor

Egorov proposes scaling crvUSD credit line to $1B; LlamaRisk proposes phased rollout model

Hybrid ETH vault goes live after governance approval; multiple audits completed

Risks, Criticisms, and Systemic Considerations

No assessment of Yield Basis would be complete without a detailed discussion of its risks and the criticisms leveled against it. Some of these critiques focus on technical aspects of the protocol, while others address broader systemic and governance issues that arise from its deep integration with crvUSD and Curve.

One major area of concern is the impact of Yield Basis on crvUSD’s peg stability and volatility. As noted earlier, Pangea’s research shows that structural flows from Yield Basis account for more than 36% of Curve’s crvUSD volume, occasionally exceeding 60% on days of high BTC volatility. This concentration means that YB’s behavior—particularly during periods of leveraged expansion or contraction—can significantly influence crvUSD liquidity and trading dynamics. In a separate study, Pangea reports an increase in crvUSD’s volatility and peg deviations following the launch of Yield Basis, while explicitly emphasizing that this does not prove causation but does indicate that the protocol’s growth coincided with a more turbulent environment for the stablecoin. From a risk perspective, this suggests that any fast withdrawal or deleveraging of YB positions during a BTC drawdown could amplify stress on crvUSD if not carefully managed.

Another set of concerns relates to the lending model and comparisons to historically fragile designs like Luna‑UST. Gate.io’s critical review argues that Yield Basis’s reliance on “equivalent lending” and a complex three‑layer token structure involving ybBTC, YB, and veYB bears resemblance to the interlocked dynamics of Luna and UST, where value feedback loops between the governance token and the stablecoin ultimately led to collapse. The article notes that the project relies on crvUSD reserves that might be insufficient in extreme scenarios, and that the fee‑sharing and token incentive structures are designed primarily to support crvUSD issuance rather than to fundamentally eliminate impermanent loss. It goes so far as to suggest that the true purpose of Yield Basis may be to drive a surge in crvUSD issuance, casting the IL‑free narrative as secondary.

Supporters respond that the analogy to Luna‑UST is imperfect at best, given that crvUSD is designed as an overcollateralized stablecoin with LLAMMA‑based soft liquidations rather than as an algorithmic stablecoin dependent on reflexive mint‑burn dynamics between the stablecoin and a volatile governance token. They also point out that Yield Basis’s credit line and risk parameters are subject to Curve DAO governance, with independent risk managers like LlamaRisk and research organizations like Pangea involved in stress testing and policy recommendations. Nonetheless, the criticisms underscore that any system in which a major stablecoin’s growth and fee flows are heavily tied to a single leveraged yield protocol must contend with reflexivity and the possibility of rapid, self‑reinforcing unwinds in times of stress.

Smart‑contract and MEV risk constitute another important dimension. The previously mentioned security review of YieldBasisDAO’s contracts, conducted by Block 7 fellows, Panda, and HHK, identified a critical vulnerability in the VotingEscrow system, where flawed transfer functions and slope change accounting could allow position theft and permanent corruption of voting power distributions. This finding highlights that even ostensibly peripheral contracts, such as those controlling vote‑escrowed governance tokens and fee distribution, can be critical to protocol safety and fairness. Separately, an AI‑powered security review by Firepan of the FeeDistributor contract uncovered multiple findings across numerous attack surfaces, including a previously undocumented MEV vector. While such audits are a sign of diligence and have likely led to mitigations, they also reveal that the protocol’s complexity creates a broad attack surface that must be continuously monitored and patched.

Market risk and liquidation dynamics remain core concerns for participants. Although Yield Basis is designed to neutralize impermanent loss relative to buy‑and‑hold, it does not insulate users from BTC or ETH price risk, nor from the risk of forced deleveraging if collateral prices fall below acceptable thresholds. In extreme BTC drawdowns, the LLAMMA‑based liquidation of crvUSD loans, combined with Yield Basis’s own position‑management logic, could lead to substantial BTC sales into thin markets, potentially exacerbating price moves. At the same time, the linearized exposure means that LPs will participate fully in BTC downside, just as they would if they simply held BTC, but with the added complexity of crvUSD debt and fee structures layered on top.

Governance and centralization risks also deserve attention. With insiders reportedly controlling around 45% of the YB supply, including allocations to the team, investors, and the Curve ecosystem, questions arise about the decentralization and resilience of YieldBasisDAO decision‑making. While real‑world usage, liquid lockers, and secondary markets can dilute this influence over time, the initial distribution and the interplay with veCRV and other governance systems create a complex political economy around the protocol. If YB and crvUSD become deeply intertwined with major DeFi platforms, governance capture or misaligned incentives in one domain could have cascading effects elsewhere.

Finally, user‑level risk must be considered. The promise of IL‑free, leveraged yield is seductive, especially in an environment where passive LP strategies on other platforms have often underperformed expectations. However, as Mirador and Leviathan‑adjacent educational content emphasize, users must carefully distinguish between the elimination of a particular risk (impermanent loss in its classical sense) and the persistence—or even amplification—of other risks such as leverage, liquidation, and stablecoin depegging. Evaluating Yield Basis therefore requires a holistic understanding of both its mechanical innovations and its systemic embedding in the broader DeFi landscape.

Comparative Positioning: Yield Basis vs. Uniswap v3 and Other BTC/ETH Yield Strategies

To situate Yield Basis within the broader DeFi ecosystem, it is useful to compare its design and value proposition to alternatives such as Uniswap v3 LPing, lending protocols, and centralized yield products. Uniswap v3, as formalized in the “Strategic Liquidity Provision in Uniswap v3” paper, allows LPs to concentrate liquidity within custom price ranges, achieving high capital efficiency when prices remain within that range but exposing them to range‑exit risk and frequent maintenance needs when markets move. Empirical evidence suggests that many LPs, especially smaller ones, either fail to rebalance in time or take on ranges that are too narrow, resulting in periods of zero fee income and, in some cases, underperformance relative to buy‑and‑hold strategies due to adverse selection and MEV.

By contrast, Yield Basis aims to offer a more passive experience: once users deposit BTC or WETH into YB vaults, the protocol’s algorithms handle rebalancing, maintaining leverage, and optimizing fee capture within Curve’s FXSwap pools. The IL‑free design means that, in the absence of extreme events, LPs should not underperform a simple long BTC or long ETH position purely due to AMM curvature, although they will still face the full effects of price volatility and potential costs from borrowing and rebalancing. For users who are primarily long BTC or ETH and do not want to micromanage LP positions, this can be an attractive proposition, particularly if effective yields in the 12%–22% range—as reported by the project for BTC pools in 2025—prove sustainable without heavy incentive subsidies.

Compared to simple lending or staking products, Yield Basis offers a different risk‑return profile. Traditional BTC lending, whether on centralized platforms or on‑chain, typically provides modest yields by letting users lend BTC or wrapped BTC to borrowers, with risks primarily associated with counterparty solvency and, in on‑chain contexts, smart‑contract vulnerabilities. Yield Basis, by contrast, transforms users into leveraged LPs in an AMM pool while attempting to neutralize one particular risk (IL) and monetize another (trading‑driven volatility) through fee capture and structured vault strategies. The trade‑off is that users must accept both BTC price risk and the complexities of crvUSD lending, FXSwap dynamics, and protocol‑governance risk.

The table below provides a high‑level comparison of key features between a generic Uniswap v3 LP position and a Yield Basis vault position for BTC or WETH.

| Feature | Uniswap v3 LP (BTC/Stable) | Yield Basis LP (BTC/WETH‑crvUSD) |

|---|---|---|

| Impermanent Loss relative to HODL | High, depends on volatility and range; typically non‑zero even with careful management. | Targeted to be near zero via fixed 2× leverage and continuous rebalancing, under model assumptions. |

| Capital Efficiency | High when price stays in range; zero when out of range. | High, with effective 2× notional exposure per unit BTC/WETH deposit; always active in FXSwap pools. |

| Management Overhead | Significant; LP must monitor prices, adjust ranges, and rebalance positions. | Low for end users; rebalancing and leverage management handled by protocol vaults. |

| Price Exposure | Non‑linear (concave payoff); systematically sells winners and buys losers. | Approximately linear long BTC or long ETH exposure, plus fee and yield components. |

| Dependencies | Uniswap protocol, oracles, and underlying chain. | Curve FXSwap, crvUSD, Llamalend credit lines, YB tokenomics, and associated governance and risk systems. |

This comparison indicates that Yield Basis does not simply replicate existing LP strategies but rather introduces a distinct risk bundle. Users sidestep classical impermanent loss and the need for active management, but at the cost of taking on leveraged exposure to a complex, multi‑layered ecosystem built around Curve, crvUSD, and YB tokenomics. For sophisticated users who understand these links and are comfortable with them, the trade‑off may be attractive, especially in a BTC or ETH bull cycle where fees and volatility are elevated. For others, the additional complexity and systemic risk may outweigh the benefits of IL neutralization.

Governance, Research, and the Role of Public Discourse

Yield Basis has not grown in a vacuum; its trajectory has been shaped by a lively public discourse involving researchers, risk managers, governance forums, and media outlets. Pangea has played a particularly visible role, publishing analyses on FXSwap’s performance, YB’s impact on crvUSD volumes, and scenarios for scaling the protocol to a 1 billion crvUSD credit line. Their findings that FXSwap offers superior depth and slippage profiles for large trades relative to Uniswap v3 have bolstered the case for using Curve as the base AMM for sophisticated yield protocols. At the same time, their warnings about the tight coupling between Yield Basis flows and crvUSD behavior have informed Curve and YieldBasisDAO governance debates about how fast to expand credit lines and how to design safeguards.

LlamaRisk and other risk‑focused entities have worked alongside Pangea to model potential stress scenarios, looking at how BTC price shocks, liquidity crunches, or shifts in veCRV voting patterns might affect Yield Basis and crvUSD. This research has fed into proposals for per‑LP caps in Hybrid Vaults, dynamic fee switches, and updated risk parameters for Llamalend markets that back YB’s leverage. Governance discussions have also surfaced concerns from community members who worry about centralization, token distribution, and the possibility that YB’s growth could crowd out other crvUSD use cases or distort veCRV incentives.

Media coverage from crypto‑native outlets, including Leviathan’s livestreams and various news sites, has further amplified the conversation. Educational series such as Mirador’s “Impermanent Loss and how Yield Basis makes it ‘zero’” have attempted to demystify the math behind YB’s design, while investigative pieces like Gate.io’s critical review have raised red flags about potential systemic risks and conflicts of interest. Meanwhile, protocol‑aligned communications—such as Yield Basis’s own X posts, Michael Egorov’s essays on scaling YB and crvUSD, and project updates about v3 pools, migrations, and fee switch activations—provide insight into the team’s priorities and strategic direction.

This interplay between research, risk analysis, governance, and media is central to how complex DeFi protocols evolve. In Yield Basis’s case, it has led to concrete changes, such as the introduction of per‑LP caps in Hybrid Vaults to mitigate concentration risk, multiple rounds of independent security reviews of core contracts, and staged scaling of the crvUSD credit line rather than an immediate jump to 1 billion. It has also fostered a culture in which protocol decisions—such as launching IL‑free WETH‑crvUSD “liquidity backbone” pools or activating the YB Fee Switch to reroute more revenue to token holders—are debated publicly before being ratified via on‑chain governance.

For users and observers, this discourse serves as a critical resource. Understanding Yield Basis means not only grasping its mechanical design, but also tracking how its risk profile co‑evolves with market conditions, governance choices, and external critiques. The presence of independent research outfits, risk managers, and critical media is an important check on potential blind spots, especially in a system as interconnected as Yield Basis and crvUSD.

Firepan's security review of the live mainnet FeeDistributor identified 18 findings across 22 attack surfaces including a previously undocumented MEV vector in deployed code.

Protocol design, governance proposals, crvUSD credit line requests, and public responses to criticism all flow through a single founder (Michael Egorov), concentrating upgrade and narrative authority.

Before a secondary market for $YB and $sdYB existed, liquid locker investors faced an exit illiquidity window flagged by DeFi researchers and Stake DAO's Hubirb.

The 2x compounding leverage applied to Curve LP positions amplifies both upside yield and drawdown during flash crashes, as documented in Pangaea's October 10 post-mortem.

Yield Basis depends on Curve DAO repeatedly approving larger crvUSD allocations; LlamaRisk proposed a three-phase rollout to manage Curve's escalating risk exposure responsibly.

- RegulatoryLow

No enforcement actions or regulatory flags have been publicly associated with Yield Basis; the risk profile matches generic DeFi protocol exposure rather than any jurisdiction-specific targeting.

How to Think About Participating in Yield Basis

For potential participants—whether they are BTC or ETH holders considering depositing into Yield Basis vaults, DeFi DAOs evaluating treasury allocations, or investors analyzing YB tokens—the key is to approach the protocol with a structured framework that goes beyond headline yields. The first dimension to evaluate is exposure. Depositing BTC or WETH into Yield Basis is economically similar to taking a leveraged long position on those assets, with IL neutralized but price risk fully present and potentially amplified in terms of volatility due to the layered structure of crvUSD debt and AMM liquidity. Users should be comfortable with the idea that their returns will closely track the underlying asset’s performance, plus or minus fees and costs, rather than being insulated from downturns.

The second dimension is systemic risk. Because Yield Basis is deeply integrated with Curve and crvUSD, participants are effectively taking a bet on the robustness of that ecosystem as a whole. This includes trust in Curve’s governance, confidence in crvUSD’s peg and LLAMMA liquidation mechanism, and an assessment of the likelihood that governance decisions—such as expanding the YB credit line to 1 billion crvUSD—will be made cautiously and with sufficient modeling. It also involves evaluating the concentration of crvUSD volumes in YB‑linked pools and the potential consequences of a rapid unwinding of those positions during market stress.

The third dimension is smart‑contract and governance risk. Prospective users should review the results of recent audits, such as the security assessments of VotingEscrow and FeeDistributor contracts, and monitor whether identified vulnerabilities have been patched in production deployments. The presence of MEV vectors and the complexity of fee‑distribution logic suggest that even non‑core contracts can have material effects on user outcomes. Governance risk encompasses not only the potential for insider dominance, given the token distribution, but also the risk that governance proposals are rushed through without adequate community review or independent risk assessment.

Finally, yield sustainability is a crucial factor. While Yield Basis has reported compelling yields for BTC LPs in its early years, observers should scrutinize how much of that yield is organic, coming from trading fees and genuine borrowing demand, versus how much is subsidized via token incentives or fee switches tuned to favor early participants. As with many DeFi protocols, high initial yields can compress over time as competition increases, incentives wane, or market conditions change. Evaluating the underlying sources of revenue—FXSwap trading volumes, crvUSD loan interest, and fee‑sharing arrangements with veCRV—can provide a clearer picture of long‑term prospects.

In practical terms, anyone considering participation should read the protocol documentation, review recent governance proposals and research reports, and, if possible, simulate different market scenarios to understand how Yield Basis positions would behave. While this explainer aims to provide a comprehensive overview, the evolving nature of the protocol, its governance, and its integration with Curve mean that due diligence is an ongoing process rather than a one‑time exercise.

Outlook

Yield Basis represents one of the more ambitious attempts in DeFi to fundamentally rethink how liquidity provision works for volatile assets like BTC and ETH. By combining Curve’s FXSwap AMM, crvUSD’s LLAMMA‑based lending, and a fixed‑leverage rebalancing strategy, it seeks to neutralize classical impermanent loss and offer LPs a payoff profile closer to a simple long BTC or long ETH position, augmented by trading and lending yields. Early research and data suggest that FXSwap can provide superior market depth compared to alternatives such as Uniswap v3, and that Yield Basis can deliver attractive organic yields without heavy subsidies, at least under favorable market conditions.

At the same time, the protocol’s deep integration with crvUSD and reliance on expanding credit lines introduce systemic linkages that must be managed carefully. Pangea’s findings about increased crvUSD volatility and the dominant share of crvUSD volume attributable to YB flows underscore the need for cautious scaling and robust risk management. The comparisons drawn by critics to Luna‑UST, while not exact, are a reminder that complex, circular value structures between governance tokens, stablecoins, and yield protocols can become fragile if not grounded in conservative risk parameters and transparent governance.

Looking ahead, key milestones for Yield Basis include the completion of v3 pool migrations, the maturation and scaling of Hybrid Vaults with their per‑LP caps, the secure deployment of IL‑free WETH‑crvUSD “liquidity backbone” pools, and the responsible expansion of crvUSD credit lines toward any proposed 1 billion cap. Continued security audits, integration with liquid lockers like sdYB and yYB, and active engagement with independent research and risk organizations will all play a role in determining whether Yield Basis can evolve into a stable pillar of BTC‑ and ETH‑denominated yield in DeFi, rather than a transient experiment in leveraged liquidity.

For now, Yield Basis stands as a sophisticated, high‑conviction bet on the future of BTC and ETH in DeFi, one that offers a compelling answer to the long‑standing problem of impermanent loss but demands equally sophisticated understanding of leverage, stablecoin dynamics, and protocol governance from its users.

Latest Yield Basis news

FXSwap might have just fixed the biggest problem in LP designYieldBasis launches new pools with most capacity reserved for LP migrations as Curve flags crvUSD upsideYield Basis confirms hybrid ETH vault is now live after governance approval, opening early access to new yield strategies and marking next phase of protocol growthYield Basis completes first full market cycle, distributes $3.84M in fees to YB lockersYield Basis: Solving Impermanent Loss to Scale DeFi for the Bitcoin Macro Cycle Hybrid vaults are coming as Yield Basis completes multiple audits across core and new systems, highlighting growing demand for secure, multi-strategy yield products in DeFi

Hybrid vaults are coming as Yield Basis completes multiple audits across core and new systems, highlighting growing demand for secure, multi-strategy yield products in DeFiSources

- https://x.com/yieldbasis?lang=en

- https://www.cryptoeq.io/articles/yield-basis-defi

- https://x.com/yieldbasis/status/2038610652194037966

- https://x.com/in_pangea/status/1978501066762170523

- https://x.com/MiradorNews/status/2022227636647325992

- https://news.curve.finance/fxswap/

- https://x.com/newmichwill/status/2019463665418678291

- https://x.com/leviathan_news/status/2014307346319646739?lang=bg

- https://x.com/bestagno

- https://blog.pangea.foundation/author/joe/

- https://blog.pangea.foundation/scaling-yieldbasis-to-1bn/

- https://www.okx.com/sv/learn/yield-basis-allocation-bitcoin-yields

- https://arxiv.org/html/2106.12033v5

- https://x.com/yieldbasis/status/2008859121806881270

- https://www.gncrypto.news/news/yield-basis-hybrid-vaults-deposits-jump-120-btc-exposure/

- https://reports.yaudit.dev/pdf/2025-07-YieldBasis-Update.pdf

- https://www.gate.com/news/detail/14845933

- https://x.com/yieldbasis/status/1982140801523020033

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…