In-depth explainer on YB and Yield Basis, covering its impermanent-loss-free design for BTC/ETH LPs, YB tokenomics, veYB governance, Curve/crvUSD integration, liquid lockers like yYB/sdYB, and key risks and opportunities in the broader DeFi ecosystem.

+43 sources across the wider coverage universe

Yield Basis completes first full market cycle, distributes $3.84M in fees to YB lockers2026-04

Yield Basis completes first full market cycle, distributes $3.84M in fees to YB lockers2026-04 YB Fee Switch: the next YieldBasis milestone2025-12

YB Fee Switch: the next YieldBasis milestone2025-12 Stake DAO's sdYB Liquid Locker for Yield Basis's YB token has passed 3M veYB2025-12

Stake DAO's sdYB Liquid Locker for Yield Basis's YB token has passed 3M veYB2025-12 Yearn announces yYB, a liquid locker for Yield Basis's YB token2025-12

Yearn announces yYB, a liquid locker for Yield Basis's YB token2025-12 Yearn’s yYB crosses 1 million YB locked2026-01

Yearn’s yYB crosses 1 million YB locked2026-01 New Proposals Aim to Scale crvUSD and Expand Yield Basis Capacity — Plans include boosting Curve DAO’s YB incentives up to 360K YB/week, raising PegKeeper limits from $108M to $300M, and allocating $1B crvUSD to Yield Basis to unlock $500M capacity, strengthening peg stability and system value ahead of broader scaling.2025-10

New Proposals Aim to Scale crvUSD and Expand Yield Basis Capacity — Plans include boosting Curve DAO’s YB incentives up to 360K YB/week, raising PegKeeper limits from $108M to $300M, and allocating $1B crvUSD to Yield Basis to unlock $500M capacity, strengthening peg stability and system value ahead of broader scaling.2025-10

YB and Yield Basis: An Evergreen Guide to Impermanent-Loss-Free Liquidity

YB is the governance and value-accrual token of Yield Basis, a DeFi protocol created by Curve founder Michael Egorov that aims to turn BTC and ETH price volatility into yield while neutralizing impermanent loss for liquidity providers. In practice, Yield Basis routes user deposits into leveraged positions on Curve’s cryptopools and actively rebalances them so that LPs retain a linear exposure to their underlying assets while earning trading fees, borrow incentives, and YB emissions. This design has positioned YB as a focal token at the intersection of Curve, crvUSD, Bitcoin yield strategies, and emerging “liquid locker” markets led by protocols like Yearn and Stake DAO, while also raising new questions about leverage, governance power concentration, and systemic risk in DeFi’s yield stack.

What Problem Is Yield Basis Trying To Solve?

The starting point for understanding YB is the long-standing tension between automated market maker design and capital preservation for liquidity providers. In a typical constant-product AMM such as Uniswap v2, a liquidity provider who deposits an asset pair like BTC and a stablecoin takes on a nonlinear exposure to the underlying prices, which leads to the phenomenon known as impermanent loss when prices move away from the entry ratio. Impermanent loss arises because the AMM continually rebalances the pool to maintain the invariant \(x \cdot y = k\), so an LP ends up holding more of the underperforming asset and less of the outperforming one compared with simply holding both in a wallet. Over time, trading fees can offset or exceed this loss, but in volatile markets, especially for assets like BTC and ETH, the magnitude of impermanent loss can dominate fee income and turn liquidity provision into a structurally risky bet. This dynamic has constrained how much “real” Bitcoin and Ethereum liquidity DeFi can attract, especially from long-term holders who are unwilling to bleed exposure in exchange for uncertain yield.

Curve Finance took a different approach by specializing in stable and like-pegged assets, where volatility between the pair is low and thus impermanent loss is naturally reduced. Its cryptopools extended this model to volatile pairs, combining Curve’s bonding curve design with risk parameters tuned for assets like BTC and ETH, but volatility and correlation risk still impose meaningful trade-offs for LPs. As DeFi matured, more capital demanded not only high yield but also better control of directional exposure and downside risk; meanwhile, on the protocol side, teams sought ways to generate sustainable, fee-driven revenue that was less dependent on inflationary token emissions. Yield Basis is explicitly framed as an answer to this set of constraints: it uses leverage and automated rebalancing to construct a synthetic position whose payoff closely tracks the underlying asset price plus accumulated fees, while avoiding the classical impermanent loss profile of AMMs.

The ambition is broader than a single vault design. Yield Basis’s public messaging describes the project as “turning crypto into productive assets using original Automatic Market Making without IL,” with a particular emphasis on Bitcoin as the first target market. The protocol’s own site highlights the slogan “Market volatility is your yield,” underscoring that it tries to flip volatility from a source of LP risk into a core driver of returns by capturing trading fees and basis movements in leveraged pools. Against this backdrop, the YB token becomes the coordination and value-sharing mechanism: it governs how much capacity Yield Basis offers, how emissions are allocated, how fees are shared with lockers, and how deeply the protocol integrates with Curve’s crvUSD ecosystem and with external DAOs such as Yearn and Stake DAO. Understanding YB therefore requires understanding both the economic mechanics of impermanent-loss-free liquidity and the governance architecture that decides who benefits from those mechanics over time.

Yield Basis completes first full market cycle, distributes $3.84M in fees to YB lockers

Readers engage with YB not for APY numbers but for the tokenomics chokepoints that determine whether its BTC yield promise survives at scale — specifically emissions control, veYB lock-up capture, and whether liquid lockers have any viable exit before a secondary market materializes.↗

The Yield Basis Protocol: Architecture and Core Mechanics

Yield Basis is built around the idea that it is possible to engineer a hedged liquidity position whose value is approximately linear in the price of an underlying volatile asset while still earning AMM fees. In interviews, Michael Egorov has explained that a standard AMM LP position in a volatile-asset-versus-stablecoin pool tends to have a payoff proportional to the square root of the asset price, reflecting the way constant-product curves redistribute exposure as prices move. If an LP could combine this position with another that has the opposite square-root dependence, they could in principle cancel the curvature and restore a payoff that is closer to a simple long exposure on the asset plus accumulated fees. Yield Basis attempts to construct such a combined exposure using leverage and constant loan-to-value management rather than traditional derivatives.

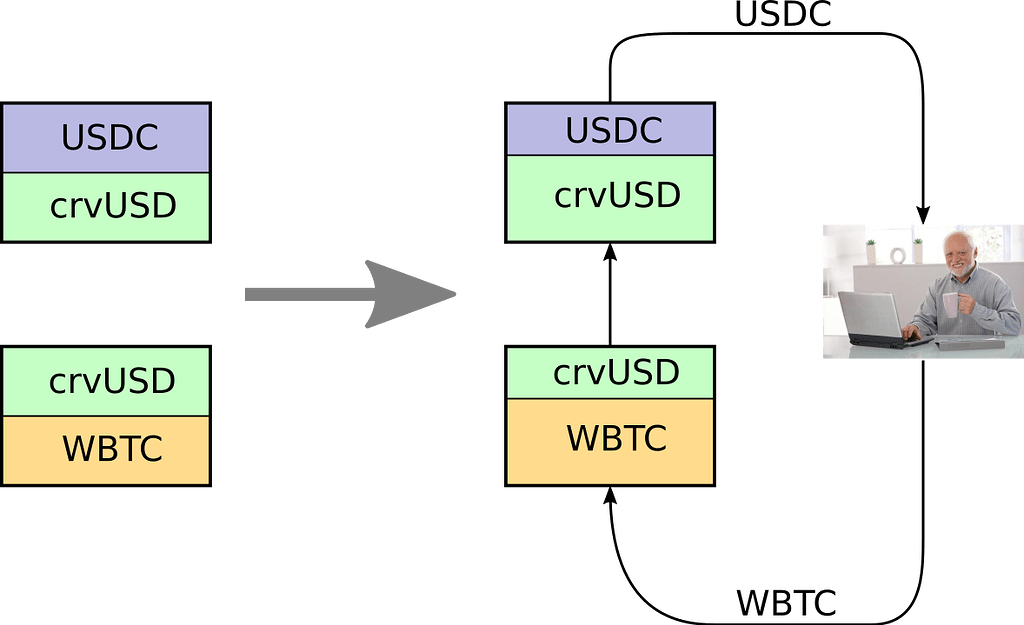

Operationally, a typical Yield Basis vault for Bitcoin works roughly as follows, in simplified form. A user deposits BTC (or tokenized BTC variants such as WBTC or tBTC in some markets) into the protocol and receives a receipt token such as ybBTC that represents their share of the strategy. The protocol then borrows an amount of crvUSD roughly equal to the USD value of the deposited BTC and pairs this borrowed crvUSD with the BTC in a Curve cryptopool, thereby deploying a 2x leveraged liquidity position consisting of 50 percent debt and 50 percent equity. The LP tokens from this Curve pool are posted as collateral against the crvUSD debt, and the system continuously rebalances the position to keep the loan-to-value ratio near a target, typically around 50 percent, using a secondary automated market maker that Egorov has referred to as “relev”. Because the leverage is maintained automatically and symmetrically, the net effect is to square the already nonlinear exposure of the AMM position, which can be designed to cancel out the square-root behavior and produce a payoff closer to linear price exposure plus fee income.

Two critical flows fund this architecture. First, all borrow rates paid by liquidity providers on their crvUSD loans are directed back into a budget that the protocol uses to perform rebalances in the underlying Curve cryptopools. This effectively recycles interest payments into market operations that stabilize the leveraged positions and help them track the intended exposure profile. Second, trading fees from the Curve pools accrue to the LP position as usual, but because the LP tokens are held by the vault and leveraged, these fees are magnified relative to unleveraged provisioning. Over time, Yield Basis aims for protocol fees and trading revenue to dominate any residual slippage or rebalancing costs, making volatility a net positive for yield generation rather than a source of impermanent loss.

The protocol is tightly coupled to Curve’s infrastructure, not only at the pool level but also through crvUSD, Curve’s overcollateralized stablecoin. In a governance proposal to create a dedicated crvUSD credit line for Yield Basis, the team described a structure in which crvUSD lending capacity is earmarked for the protocol’s vaults, and in return a portion of YB token emissions and fee flows are directed back to the Curve ecosystem. Yield Basis commits to allocating 25 percent of the YB rewards that its own liquidity providers earn to Curve, which, under plausible assumptions, amounts to roughly 20 percent of total YB inflation accruing to Curve-aligned stakeholders. When combined with fees captured through veYB-style mechanisms, the Curve ecosystem may end up receiving between 35 and 65 percent of the total economic value distributed to veYB holders from Yield Basis fees, depending on market conditions and governance decisions. This arrangement makes explicit that Yield Basis is designed as an extension of Curve’s liquidity and governance universe rather than a standalone competitor.

A further design choice is capacity capping. Egorov has noted that simulations of Yield Basis strategies suggest the potential for annualized yields of 20 percent or higher in high-volatility regimes, but also emphasized that these models assume a controlled total value locked and sufficient market depth in the underlying Curve pools. To avoid overstressing liquidity and creating reflexive feedback loops in crvUSD or BTC markets, the protocol has signaled that it will impose TVL caps, at least in early phases, with figures on the order of tens of billions of dollars discussed as upper bounds in long-run scenarios. By tying capacity expansion to both risk modeling and governance approval, Yield Basis aims to scale without undermining the very markets it relies on for hedging and fee generation.

YB Token Basics: Market Presence and Initial Distribution

YB itself is an ERC‑20 token deployed on Ethereum, serving both as a governance asset and as the recipient of protocol value flows over time. On-chain metadata compiled by analytics platforms such as Etherscan indicates that YB has thousands of holders and a circulating value in the tens of millions of dollars, reflecting its emergence as a mid-cap governance token tied to a specialized DeFi protocol. Centralized exchanges have listed YB in spot markets, with pairs such as YB/USDT on major venues like Binance, whose market pages describe Yield Basis as a DeFi protocol that provides yield to liquidity providers while mitigating impermanent loss using leverage. These listings supplement on-chain liquidity and make YB accessible to a broader base of traders who may not yet interact directly with Curve or Yield Basis vaults.

The token’s launch and early distribution followed a now-familiar pattern in DeFi, but with a notable emphasis on rewarding Curve ecosystem participants. Prior to full emissions, Yield Basis announced an airdrop of YB to early liquidity providers and to veCRV voters who had supported the protocol’s Curve pool gauges, explicitly recognizing the role of Curve DAO in bootstrapping its liquidity. Additional allocations were distributed through “Genesis of Bitcoin Yield” campaigns highlighted in the project’s social channels, which combined promotional narratives about Bitcoin yield with structured reward schedules for early adopters. Outside the DeFi-native sphere, partnerships with centralized platforms such as Binance and Kraken helped broaden distribution further, for example through exchange-based airdrop programs that awarded YB to users who held or staked other assets on those venues ahead of its listing.

From a capital-raising perspective, YB’s early funding rounds attracted a mix of institutional and community investors, with public trackers reporting that Yield Basis had raised on the order of tens of millions of dollars across several rounds prior to and around token generation. These rounds provided runway for both protocol development and liquidity seeding, but they also introduced vesting schedules and allocation overhangs that YB holders must consider when assessing potential supply dynamics. While precise vesting terms can change through governance and are subject to contractual arrangements, the broad pattern aligns with other DeFi governance tokens: a mixture of team, investor, ecosystem, and community allocations gradually unlocked over several years, overlaid with ongoing emissions directed to protocol users and partners.

An important part of YB’s economic design is its explicit linkage to Curve and the broader crvUSD ecosystem. As noted in the crvUSD credit line proposal, Yield Basis commits a fixed portion of its inflationary emissions to the Curve DAO, with the aim of both compensating Curve for the use of its cryptopool technology and creating long-run alignment between veYB and veCRV holders. This arrangement effectively means that Curve’s governance and liquidity providers hold a structural claim on the success of Yield Basis, while YB holders in turn depend on Curve’s health and willingness to allocate crvUSD liquidity and gauge incentives to YB-related pools. In practice, this interdependence manifests in shared governance debates over gauge weights, PegKeeper parameters, and crvUSD capacity limits, all of which can materially affect the profitability and resilience of Yield Basis strategies.

- 01crvUSD/YB scaling governance↗

Proposals to raise PegKeeper limits from $108M to $300M and direct $1B crvUSD at Yield Basis showed readers whether the protocol can grow to institutional TVL under Curve DAO control.

- 02liquid locker secondary market risk↗

DeFiShaka's warning that sdYB buyers face stranded capital before a secondary swap market exists turned an abstract tokenomics risk into a concrete, named trap that readers recognized.

- 03BTC gauge implementation milestones↗

Adding WBTC, cbBTC, and tBTC gauges was the production-readiness gate that would route real YB emissions to BTC liquidity, so readers tracked it as the protocol's prove-it moment.

- 04veYB airdrop and token launch structure↗

A structured launch via Kraken and Legion with a defined veCRV holder airdrop gave readers clear participation eligibility, which drove engagement beyond pure speculation.

- 05impermanent loss elimination mechanics↗

Yield Basis's core claim — sustainable BTC yield without impermanent loss — is novel enough that readers clicked to understand the mechanism rather than just accept the headline APY.

- 06fee revenue and first market cycle proof↗

The $3.84M first-cycle fee distribution to YB lockers validated that yield was real and non-subsidized, converting skeptics tracking the 'genesis' recap into believers.

How YB Accrues Value: Fees, Emissions, and the “Fee Switch”

In its initial phases, YB, like many DeFi tokens, derived much of its perceived value from the prospect of future governance power and protocol growth rather than from direct cash flows. However, Yield Basis has progressively introduced mechanisms by which holders who lock YB into veYB receive a share of protocol revenues, often described in community discourse as the “fee switch.” Under this model, a portion of the fees and interest spreads generated by Yield Basis vaults is directed to veYB lockers, either directly in base assets or indirectly via market operations and buybacks, while another portion is committed to external partners such as Curve’s veCRV holders according to predefined formulas. This structure aligns YB more closely with a cash-flow-bearing asset, though the exact magnitude of these flows will depend on trading volumes, borrow demand for crvUSD, and the success of Yield Basis in scaling its TVL.

The sources of protocol income that feed the fee switch can be grouped conceptually into trading fees, borrow rate spreads, and emissions-derived external incentives. Trading fees arise from the Curve cryptopools where Yield Basis deploys its leveraged liquidity, and because the vaults often operate at two times leverage, these fees are amplified relative to unleveraged positions for the same notional exposure. Borrow rate spreads emerge when the interest paid on crvUSD loans by LPs exceeds the funding cost that Yield Basis itself faces from its credit lines, enabling the protocol to retain a margin that can be shared with governance token holders. Emission-derived incentives include any secondary tokens that the vault earns from protocols whose pools it utilizes, such as CRV or other reward assets, some of which may be recycled to veYB lockers via swaps or redistributed directly, depending on governance decisions.

In parallel, YB emissions continue to play a significant role in incentivizing behavior across the ecosystem. Liquidity providers in Yield Basis vaults receive YB tokens in proportion to their deposit size, lock duration, and sometimes their governance preferences, creating a feedback loop in which YB emissions steer both where liquidity flows and how veYB voting power is deployed. A fixed share of these emissions is allocated to Curve as compensation for infrastructure and gauge support, making YB one of the more tightly integrated “satellite” tokens around the CRV and veCRV universe. Over time, as more of the circulating YB supply becomes locked into veYB or into liquid locker derivatives such as yYB and sdYB, the effective float available for trading may decline, potentially amplifying price sensitivity to demand shocks while concentrating governance and fee rights among long-term stakeholders.

At the narrative level, the introduction of a YB fee switch has been treated within the community as a milestone in the protocol’s evolution from experimental mechanism to revenue-generating financial primitive. Once fees began flowing meaningfully to lockers, YB shifted closer to a quasi-equity role within the protocol, with its valuation increasingly anchored not only in speculation about future adoption but also in observed fee performance and expectations about long-run sustainable yields to veYB. This transition also raised the stakes of governance choices, since changes in vault configurations, capacity allocation, or crvUSD integration can now affect not only depositor returns but also explicit cash flows to token holders and partner DAOs.

YB Fee Switch: the next YieldBasis milestone

"TL;DR Upcoming governance proposal introduces the Fee Switch - the distribution of captured fees to veYB holders The 17.13 BTC (approximately ~$1.578m) of collected fees awaits distribution to veYB holders The Fee Switch enables the full scope of YB utility and has a synergistic impact on YieldBasis DAO, Curve DAO, and crvUSD"

veYB Governance: Locking, Voting, and Protocol Control

Like many projects inspired by Curve’s governance design, Yield Basis employs a voting-escrow model in which YB can be locked to obtain veYB, a non-transferable token that confers governance power and a share of protocol revenues. Users commit YB for a chosen duration, often up to multiple years, and receive veYB in an amount that reflects both the quantity locked and the remaining lock time, typically following a decaying linear or similar schedule. Longer locks yield more veYB per unit YB, incentivizing long-term alignment and penalizing short-term exits. During the lock period, holders can vote on proposals that range from technical parameter updates to economic policy decisions, and they can receive boosted yields, fee shares, or other privileges compared with liquid YB holders.

In the case of Yield Basis, governance topics have centered on three broad areas: pool configuration and capacity, emissions allocation, and integration parameters with Curve’s crvUSD framework. On the pool side, veYB holders help decide which asset markets Yield Basis supports, such as BTC or WETH, and under what leverage and risk parameters, including TVL caps, LTV targets, and rebalancing thresholds. They also oversee upgrades, for example the migration to “v3 pools” that the project has prepared for existing markets, requiring LPs to move their positions to new vault contracts once governance approves the deployment. Such upgrades can incorporate improvements in capital efficiency, risk controls, or compatibility with external platforms, but they also impose coordination costs on users, making the timing and communication of governance decisions critical for user trust.

Emissions allocation is another contentious domain. veYB can be used to direct YB incentives across different vaults and partner pools, mirroring Curve’s gauge voting model in which veCRV holders allocate CRV emissions. This mechanism allows veYB holders, including aggregators like Yearn and Stake DAO, to steer where subsidies go and thereby influence which assets and strategies attract the most liquidity. The interplay between governance token holders and liquidity mercenaries thus becomes a core dynamic: protocols may bribe veYB holders for votes, users may stake YB with liquid lockers that can coordinate large voting blocs, and the resulting emissions patterns may favor strategies that are politically powerful rather than strictly risk-optimal.

The third pillar of veYB governance concerns Yield Basis’s deep integration with Curve’s crvUSD and with broader DAO-to-DAO arrangements. The proposal to create a crvUSD credit line for Yield Basis demonstrated how YB governance and Curve DAO deliberations intertwine, since parameters such as credit limits, PegKeeper thresholds, and incentive allocations directly affect Yield Basis’s ability to operate its leveraged vaults. Future proposals discussed in public forums include scaling crvUSD allocations to Yield Basis up to hundreds of millions or even a billion dollars and increasing YB incentives directed to Curve gauges, reflecting a deliberate strategy to make YB a significant driver of crvUSD adoption and stability. In this context, veYB is not only a governance right over a single protocol but also a lever through which holders can shape liquidity flows and risk distribution across the broader Curve-centred DeFi ecosystem.

Yield Basis mainnet launch on Ethereum

YB token launched via Kraken and Legion; veCRV holder airdrop distributed

WBTC, cbBTC, and tBTC pool gauges added to YB emissions

- 2025-04milestone

YB Fee Switch activated as next protocol milestone

Yearn Finance launches yYB liquid locker for veYB exposure

- 2025-05launch

Stake DAO launches sdYB liquid locker; passes 3M veYB locked

First full market cycle complete; $3.84M in fees distributed to YB lockers

Governance proposals to allocate $1B crvUSD and raise YB emissions to 360K/week

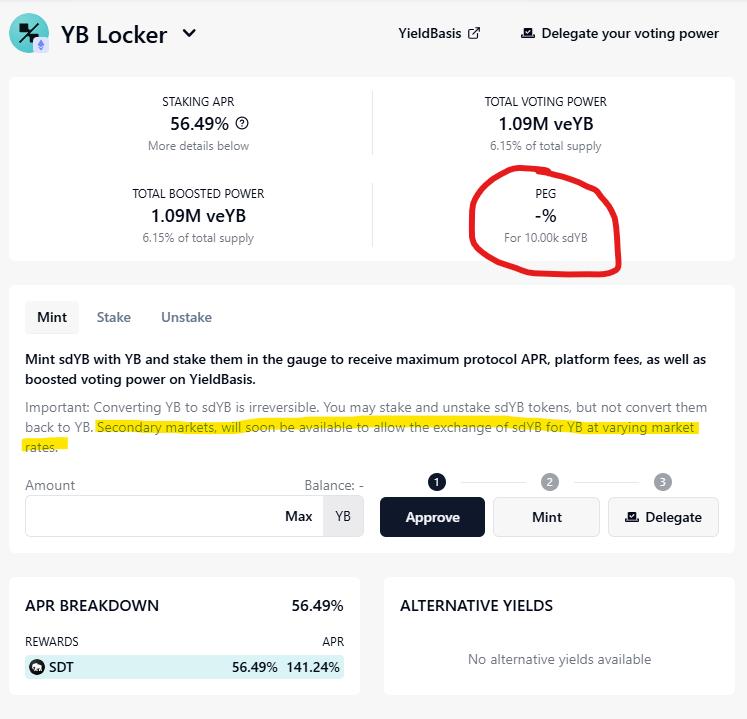

Liquid Lockers: yYB, sdYB, and the Governance Power Market

As veYB governance became economically meaningful, external protocols began building “liquid lockers” for YB, mirroring earlier designs around veCRV, veBAL, and similar models. These liquid lockers aim to solve a core trade-off in the voting-escrow system: locking provides powerful rights and yield boosts, but also immobilizes tokens for long periods, reducing flexibility and opportunity for exit. By pooling user deposits, locking them collectively for maximal duration, and issuing a liquid derivative token in return, liquid lockers like Yearn’s yYB and Stake DAO’s sdYB attempt to preserve most of the economic and governance benefits of veYB while restoring some degree of tradable liquidity.

Yearn’s yYB product provides a representative example of this approach. According to Yearn’s documentation, users can deposit YB into the yYB vault, where Yearn locks the underlying YB as veYB and actively participates in Yield Basis governance on behalf of depositors. In exchange, depositors receive yYB, a liquid token that can be held, traded, or used as collateral in other DeFi protocols once integrations develop. The yield to yYB holders comes from multiple sources: fee and reward streams tied to veYB, plus any additional incentives that Yearn may negotiate, and potentially the appreciation of governance power if YB grows more scarce through long-term locking. In parallel, Yearn aggregates voting power, allowing it to influence emissions allocation, vault parameters, and DAO-to-DAO deals in ways that individual YB holders might not be able to achieve alone.

Stake DAO’s sdYB follows a similar conceptual pattern, representing deposits of YB that Stake DAO locks to accumulate veYB voting power and fee rights. While detailed documentation may vary by version, Stake DAO’s design for other governance tokens typically includes distributing a combination of veYB-derived fees, native STAKE or SDT rewards, and sometimes boosted yield opportunities in partner protocols to sdYB holders. By surpassing multiple millions of veYB equivalent, sdYB-type lockers can become major governance actors in the Yield Basis ecosystem, able to sway decisions on key matters like the YB fee switch configuration, crvUSD credit lines, and v3 migration timing. This concentration of voting power in a few aggregators raises familiar debates about decentralization and the risk that governance outcomes may favor locker strategies over the interests of smaller, direct veYB lockers.

The presence of multiple liquid lockers also introduces a new dimension of market risk: the relationship between YB and its derivative tokens such as yYB and sdYB. In an ideal equilibrium, these derivative tokens trade near parity with YB, reflecting a bundle of veYB rights and discounted lock-up risk. In practice, however, imbalances in liquidity, market sentiment, or protocol-specific risks can lead to deviations from parity. Community researchers have highlighted scenarios in which liquid locker tokens may trade at a discount if secondary liquidity is shallow or if investors fear that the locker’s governance strategy could underperform expectations. Conversely, arbitrageurs may see opportunities to “repeg” these derivatives when market conditions normalize, particularly once deep liquidity pools between YB and its derivatives exist. For YB holders and protocol users, these dynamics mean that liquid lockers add both optionality and complexity: they can amplify governance efficiency and yield, but they also introduce new failure modes linked to liquidity fragmentation and derivative mispricing.

Yield, Performance, and Risk Across a Full Market Cycle

Yield Basis explicitly markets itself around the idea that “market volatility is your yield,” framing its strategies as ways to harvest volatility rather than suffer from it. The core yield components for a depositor in a Yield Basis vault include trading fees from Curve cryptopools, protocol-level incentives (including YB emissions and possibly CRV or other reward tokens), and the implicit benefit of impermanent-loss mitigation, which protects directional exposure compared with a traditional AMM LP. For BTC-based strategies in particular, where many participants are long-term holders, the ability to earn yield while retaining something close to a pure Bitcoin price exposure is a key part of the protocol’s appeal. However, these yield sources are inherently path-dependent: they depend on realized volatility, market depth, fee structures, and the health of crvUSD credit markets, among other variables.

Simulations presented by Egorov and referenced in audits suggest that under certain conditions of Bitcoin volatility and crvUSD market stability, Yield Basis vaults could generate annualized returns in excess of 20 percent, driven primarily by amplified trading fees and the structural demand for balanced liquidity in BTC/crvUSD pools. Yet these forward-looking estimates come with caveats. They assume that the leveraged positions can be maintained without frequent liquidations, that trading volumes remain robust, and that the cost of borrowing crvUSD does not erode the fee margin. They also generally do not account for extreme tail events, such as sudden de-pegs, protocol exploits, or cross-market contagion, which can have outsized impact on leveraged strategies. As the protocol matures and accumulates live performance data, observers have begun to analyze how Yield Basis behaves across full market cycles, defined in traditional finance as peak-to-peak periods including drawdowns of at least 20 percent over several months.

Recent reporting has highlighted that Yield Basis has now navigated at least one such full market cycle, including significant swings in BTC and ETH prices, while distributing several million dollars in fees to YB lockers. The completion of a full cycle without catastrophic loss events is an important proof point for any leveraged DeFi strategy, but it does not eliminate structural risks. For liquidity providers, key risk vectors include the possibility that rebalancing mechanisms fail to keep pace with rapid price moves, leading to liquidations or residual impermanent loss; that crvUSD liquidity dries up or its peg weakens, impairing the value of collateral; and that governance decisions misprice capacity or leverage, exposing the protocol to correlated stress precisely when volatility spikes. For YB holders, the main risks revolve around revenue variability, dilution from emissions, governance capture by large lockers, and downstream consequences of any smart contract failures in either Yield Basis or its Curve dependencies.

The role of derivatives markets adds another layer. YB has been listed not only in spot markets but also in perpetual futures on some centralized exchanges, and changes in derivative support—such as the suspension of YB-perpetual trading on certain venues—signal how centralized risk managers perceive the token’s volatility and liquidity profile. Derivative delistings can dampen speculative interest and reduce hedging avenues for large holders, but they can also redirect attention back to the protocol’s fundamental cash flows and governance role rather than short-term trading. For an investor approaching YB from a fundamental perspective, the key question is whether the combination of protocol revenues, governance influence over an increasingly important BTC and ETH liquidity primitive, and its embedded linkages to Curve and crvUSD justify the associated leverage and concentration risks.

Stake DAO's sdYB Liquid Locker for Yield Basis's YB token has passed 3M veYB

Impressive, this is looking good so far

Yield Basis builds on Curve's audited AMM primitives but the BTC rebalancing and veYB locking logic are novel; a v3 pool migration requiring all LPs to move positions adds execution risk.

Both sdYB and yYB liquid lockers convert YB into effectively illiquid veYB exposure before any secondary market exists for swapping back, creating a capital-trap risk explicitly flagged by DeFiShaka.

YB emissions schedules, gauge weights, PegKeeper limits, and crvUSD credit lines are all governed by Curve DAO, making a single governance body the critical dependency for the protocol's scaling path.

The impermanent-loss mitigation model relies on rebalancing mechanics calibrated to liquid BTC markets; it has completed only one full market cycle and has not been stress-tested through a prolonged BTC drawdown.

- RegulatoryLow

Yield Basis is a non-custodial DeFi yield protocol with no identified specific regulatory exposure beyond the sector-wide uncertainty around DeFi tokens and yield products.

Technical Innovation: Two AMMs, Constant Leverage, and v3 Pools

What sets Yield Basis apart technically is its use of two intertwined automated market makers and continuous leverage management to engineer a desired payoff profile. The first AMM is the familiar Curve cryptopool, where BTC or ETH is paired with crvUSD or another stable asset under a bonding curve optimized for low-slippage swaps. The second, sometimes referred to in community materials as “relev,” is an internal mechanism that adjusts the leverage of the position by trading against the vault’s own collateral and debt balances to maintain a near-constant loan-to-value ratio. When asset prices move, the AMM position’s effective LTV drifts; the rebalancing AMM intervenes to either repay some debt or increase it, restoring the target leverage. This continual rebalancing transforms the LP’s exposure: instead of passively riding the AMM’s square-root payoff, the position becomes more akin to a dynamically hedged portfolio, constructed entirely on-chain.

From a mathematical standpoint, Egorov has described the effect of constant leverage on AMM exposure by noting that an AMM position’s value often scales roughly with the square root of the underlying asset price over reasonable ranges. Applying leverage that itself responds quadratically to price changes can yield a combined exposure that approximately cancels the curvature, leaving a net payoff proportional to the asset price plus accumulated fees. In simple terms, if the AMM alone gives you a function like \(V_{\text{AMM}}(P) \propto \sqrt{P}\), and the leverage control creates another factor that scales as \(\sqrt{P}\), then the product approximates \(P\), a linear function of price.\ While this description abstracts from many real-world complexities, it highlights the conceptual creativity of using leverage as a hedging tool rather than merely as a way to amplify directionality.

The protocol’s reliance on Curve cryptopools and crvUSD PegKeepers means that low-level changes in those systems can materially affect Yield Basis. Upgrades such as “TwoCrypto” implementation updates in Curve’s pool factory, which improve how donations and specialized hooks like Yield Basis integrations are handled, lay the groundwork for more robust and flexible pool behavior. Yield Basis’s own “v3 pools” initiative builds on this foundation, with the project preparing to deploy upgraded vault contracts and strategy logic for existing markets. These v3 pools are expected to refine leverage management, address lessons learned from early versions, and potentially introduce more granular control over risk parameters, although their exact design is subject to governance approval and continued iteration. For users, migration to v3 pools typically involves withdrawing or migrating LP positions from legacy vaults to new ones, which carries both operational friction and an opportunity to reassess risk exposure.

The coupling of protocol upgrades to governance also underscores the importance of secure and resilient smart contract architecture. Independent audits, like the one provided by Envelop, have praised Yield Basis for its genuine technological innovation in tackling impermanent loss but also flagged the complexity inherent in its multi-contract, multi-AMM setup. Complexity can be a double-edged sword: it enables sophisticated payoff engineering, but it also increases the surface area for bugs and unintended interactions, particularly when upgrades are frequent and involve coordination among multiple DAOs. The move toward v3 pools, therefore, is not only a performance optimization but also an exercise in hardening the protocol’s architecture and its upgrade processes for long-term sustainability.

Positioning Within the DeFi and Bitcoin Yield Landscape

Yield Basis sits at the crossroads of several important trends in DeFi: the search for sustainable Bitcoin and Ethereum yield, the evolution of AMM design beyond simple constant-product models, and the rise of DAO-to-DAO coordination around governance tokens and voting power. Its core value proposition—to offer impermanent-loss-free liquidity provision for BTC and ETH while leveraging Curve’s infrastructure—addresses a clear gap in the market. Many Bitcoin holders have historically faced a dilemma between leaving BTC idle in cold storage, lending it through centralized platforms with opaque risk, or providing liquidity in AMMs that expose them to significant impermanent loss. By engineering a position that approximates a long BTC exposure plus fee income, Yield Basis offers a middle path that remains fully on-chain and composable.

The project’s close alignment with Curve and crvUSD also shapes its strategic positioning. Rather than building its own AMM stack and stablecoin, Yield Basis leans on Curve’s battle-tested cryptopools and on crvUSD’s PegKeeper system for stability, while paying back a meaningful share of its emissions and fees to the Curve ecosystem. Governance proposals have outlined ambitious plans to deepen this integration, including scaling crvUSD allocations to Yield Basis vaults, increasing YB incentives on relevant Curve gauges, and using Yield Basis as a major sink for crvUSD demand and a stabilizing force for its peg. In this vision, YB becomes both a beneficiary and a driver of Curve’s growth: as Yield Basis attracts more BTC and ETH liquidity, Curve’s volumes and fees grow, crvUSD’s utility expands, and the entire cluster of interconnected DAOs—Curve DAO, Yield Basis governance, Yearn, Stake DAO, and others—benefits.

At the same time, YB faces competition and comparison from other BTC and ETH yield strategies. Alternatives include centralized exchange staking programs, on-chain lending protocols, restaking and rehypothecation schemes, and more traditional yield farms that rely heavily on inflationary token rewards rather than fee-based revenue. Yield Basis differentiates itself by focusing specifically on impermanent loss elimination, by grounding its strategy in spot liquidity and stablecoin borrowing rather than in more exotic derivatives, and by foregrounding its DAO-governed status as a core part of its identity. For risk-aware users, especially those with a background in Curve and crvUSD, these features may make YB more attractive than opaque or highly synthetic yield offerings, although the leverage and structural dependencies involved remain significant and require careful due diligence.

The emergence of liquid lockers and governance power markets around YB underscores that large parts of DeFi view governance tokens not only as speculative assets but also as tools for active meta-governance across protocols. Yearn’s yYB and Stake DAO’s sdYB are emblematic of this trend, aggregating YB deposits to build sizable veYB positions that can then be deployed to influence emissions, integrations, and broader strategic directions for Yield Basis. For users who are uninterested in micro-managing their governance participation, delegating to such aggregators can be appealing, especially when combined with additional yield opportunities. However, as with Curve’s own governance markets, the concentration of voting power in a few liquid lockers can raise questions about whose interests are ultimately represented and how conflicts between short-term yield maximization and long-term protocol health will be resolved.

Conclusion

YB and the Yield Basis protocol represent one of the more ambitious attempts in DeFi to reconcile the benefits of automated liquidity provision with the risk preferences of long-term BTC and ETH holders. By combining Curve’s cryptopools, crvUSD credit lines, and a second layer of leverage management, Yield Basis seeks to construct on-chain portfolios whose payoff profiles approximate a simple long exposure to BTC or ETH plus amplified fee income, thereby neutralizing the impermanent loss that has historically deterred many would-be LPs. The YB token wraps this innovation in a governance and value-sharing structure that ties together veYB lockers, liquid locker protocols, and the Curve DAO, with explicit revenue-sharing commitments and a gradually activated fee switch that channels protocol income back to token holders and partner ecosystems.

The protocol’s trajectory to date underscores both the promise and the fragility of highly engineered DeFi mechanisms. On the positive side, Yield Basis has successfully launched on mainnet, navigated substantial market volatility, integrated deeply with Curve and crvUSD, and attracted enough capital and governance interest to support a burgeoning ecosystem of liquid lockers and secondary markets. It has done so while foregrounding risk management concepts such as capacity caps, full-market-cycle performance evaluation, and careful coordination with the infrastructure on which it depends. On the challenging side, its design remains complex, with multiple interacting smart contracts, dependencies on external peg stability and governance, and nontrivial liquidation and rebalancing dynamics under stress. For YB holders and vault users alike, these features demand an ongoing commitment to monitoring governance proposals, protocol upgrades like the v3 pool migration, and evolving relationships with key partners such as Curve, Yearn, and Stake DAO.

For a crypto news audience evaluating whether YB belongs in the mental map of important DeFi tokens, three aspects are particularly salient. First, YB is one of the clearest examples of how governance tokens can sit at the nexus of several DAOs, mediating complex value flows between liquidity providers, stablecoin issuers, and meta-governance aggregators. Second, Yield Basis’s approach to impermanent loss offers a template for future AMM designs that use leverage and dynamic rebalancing to reshape payoff profiles, pointing toward a more mature era of on-chain market making where LPs are no longer passive counterparties to arbitrageurs. Third, the emergence of YB-focused liquid lockers and governance markets illustrates both the power and the risk of treating governance as a tradable commodity, with concentrated veYB blocs capable of steering protocol strategy far beyond the direct control of individual token holders. How these forces balance over the coming years will determine whether YB becomes a durable pillar of the DeFi liquidity stack or remains an influential but ultimately niche experiment.

Outlook

Yield Basis and YB sit at an inflection point where several structural trends in DeFi converge: the institutionalization of Bitcoin and Ethereum on-chain, the professionalization of AMM design, and the increasing interdependence of major DAOs such as Curve, Yearn, and Stake DAO. In the near to medium term, the protocol’s priorities are likely to include the successful deployment and migration to v3 pools, continued refinement of leverage and risk parameters in light of observed market behavior, and deeper expansion into Ethereum-native strategies that apply its impermanent-loss-mitigation framework beyond BTC. Governance debates will probably focus on how aggressively to scale crvUSD credit lines and capacity limits, how to balance emissions between incentivizing new liquidity and rewarding long-term veYB and liquid-locker participants, and how to manage the concentration of voting power among a small number of aggregators without undermining decentralization.

Over a longer horizon, the success of YB will depend on whether Yield Basis can remain robust across multiple full market cycles, including periods of low volatility and adverse credit conditions, while continuing to deliver yields that justify the added complexity and leverage. If the protocol can do so, it may help define a new standard for “productive” BTC and ETH in DeFi, one in which LPs can earn fee-driven returns without sacrificing the core directional exposures they care about most. If not, YB will still stand as an important case study in how far on-chain mechanism design can be pushed in pursuit of impermanent-loss-free liquidity, and its governance experiments will inform how future projects structure the relationship between protocol tokens, liquid lockers, and DAO-to-DAO alliances in an increasingly interconnected DeFi landscape.

Latest YB news

Yield Basis completes first full market cycle, distributes $3.84M in fees to YB lockersYB Fee Switch: the next YieldBasis milestoneStake DAO's sdYB Liquid Locker for Yield Basis's YB token has passed 3M veYBYearn announces yYB, a liquid locker for Yield Basis's YB tokenYearn’s yYB crosses 1 million YB locked Researcher DeFiShaka highlights risk of YB liquid locker investment before secondary market exists for swapping $YB and $sdYB. Stake Dao's Hubirb reminds not to overlook the 'arbitrage opportunity to repeg'

Researcher DeFiShaka highlights risk of YB liquid locker investment before secondary market exists for swapping $YB and $sdYB. Stake Dao's Hubirb reminds not to overlook the 'arbitrage opportunity to repeg'Sources

- https://yieldbasis.com

- https://www.binance.com/en/trade/YB_USDT

- https://etherscan.io/token/0x01791f726b4103694969820be083196cc7c045ff

- https://www.gate.com/learn/articles/introduction-to-yield-basis-a-new-project-by-curve-founder/8478

- https://x.com/yieldbasis/status/1975158712466612424

- http://gov.curve.finance/t/create-a-crvusd-credit-line-to-yield-basis/10774

- https://www.youtube.com/watch?v=VhiHD_w-YdA

- https://www.binance.com/en/support/announcement/detail/8b48c0db0eeb472ab0314377938af2dc

- https://x.com/yieldbasis/article/2057252321198059624

- https://icodrops.com/yield-basis/

- https://docs.yearn.fi/getting-started/products/ylockers/yyb/overview

- https://www.youtube.com/watch?v=EdA7CNt-DsY

- https://x.com/torukmakt0x

- https://fpa.com/the-importance-of-full-market-cycle-returns/

- https://www.youtube.com/watch?v=jO4yIx4qoE4

- https://index.envelop.is/reports/yb_audit.html

- https://x.com/yieldbasis/status/1962636033641849063

- https://x.com/yieldbasis/status/2008859121806881270

- https://x.com/yieldbasis?lang=en

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…