CRV is Curve Finance's governance and incentive token, using vote-escrowed locking, gauge weight voting, and expanding into crvUSD stablecoin and LlamaLend to anchor one of DeFi's largest AMM ecosystems.

+3 sources across the wider coverage universe

Curve DAO opens vote for 5M CRV veFunder gauge to remediate borrowers hit by sDOLA inflation attack2026-06

Curve DAO opens vote for 5M CRV veFunder gauge to remediate borrowers hit by sDOLA inflation attack2026-06 $iREET launches, enabling up to 25%+ $CRV APR on tokenized real estate via RAAC protocol2026-04

$iREET launches, enabling up to 25%+ $CRV APR on tokenized real estate via RAAC protocol2026-04 Weekly yield and Curve ecosystem metric updates as of the 8th January, 20262026-01

Weekly yield and Curve ecosystem metric updates as of the 8th January, 20262026-01 Curve Finance founder Michael Egorov has proposed a $6.6M CRV grant (17.45M CRV) to fund long-term ecosystem development. The funds would go to Swiss Stake AG to support its 2026 roadmap, including Llamalend upgrades, infrastructure, security, and continued R&D, with biannual transparency reports and open-source commitments.2025-12

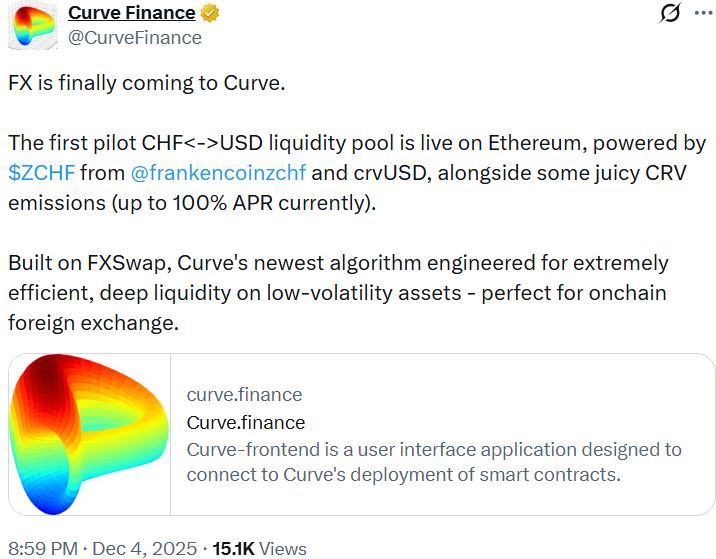

Curve Finance founder Michael Egorov has proposed a $6.6M CRV grant (17.45M CRV) to fund long-term ecosystem development. The funds would go to Swiss Stake AG to support its 2026 roadmap, including Llamalend upgrades, infrastructure, security, and continued R&D, with biannual transparency reports and open-source commitments.2025-12 Curve debuts FXSwap via pilot CHF-USD liquidity pool on mainnet, powered by $ZCHF from Frankencoin and crvUSD, alongside some juicy CRV emissions.2025-12

Curve debuts FXSwap via pilot CHF-USD liquidity pool on mainnet, powered by $ZCHF from Frankencoin and crvUSD, alongside some juicy CRV emissions.2025-12 Aave unanimously rejects proposal to ice Mich's $CRV loan 2023-06

Aave unanimously rejects proposal to ice Mich's $CRV loan 2023-06

CRV is the native governance and incentive token of Curve Finance, the Ethereum-based automated market maker purpose-built for low-slippage swaps between assets of similar value—primarily stablecoins and liquid staking derivatives.

What Curve Finance Is, and Why CRV Exists

Launched in January 2020, Curve Finance solved a specific problem in the early DeFi stack: constant-product AMMs like Uniswap imposed high slippage on trades between pegged assets. Curve's StableSwap invariant concentrates liquidity near parity, making it the dominant venue for USDC/USDT swaps, ETH/stETH trades, and similar pairs.

CRV was introduced in August 2020 primarily as a liquidity mining reward. Liquidity providers (LPs) who deposit into Curve pools earn trading fees plus CRV emissions, which flow through a gauge system that lets the DAO direct inflation to whichever pools it prioritizes. Over time, CRV evolved from a simple farming token into the load-bearing governance primitive for one of DeFi's largest protocols. As of early 2026, Curve's total value locked (TVL) has crossed $2.88 billion—an 11.7% increase year-over-year—while CRV inflation has been cut to roughly 5% annually, down from its earlier trajectory (Curve DAO, 2025).

Curve DAO opens vote for 5M CRV veFunder gauge to remediate borrowers hit by sDOLA inflation attack

Promoting from Tsunami auto-feed. Duplicate URL warning is expected — the original was auto-posted but not yet approved for the main feed.

Readers aren't clicking CRV for protocol mechanics — they're tracking a single founder's leveraged position as a live systemic stress test, treating Michael Egorov's collateral decisions as a real-time barometer for DeFi contagion risk across Aave, Abracadabra, Llama Lend, and UwU Lend simultaneously.

The veCRV Locking Mechanism

CRV's design centers on vote-escrowed CRV, or veCRV. To participate in governance and earn protocol fee revenue, holders must lock CRV for a period of their choosing—anywhere from one week up to four years. The longer the lock, the more veCRV received, and veCRV balance decays linearly toward zero as the lock expires. This mechanism deliberately penalizes short-term extractive behavior and aligns token holders with the protocol's multi-year trajectory.

Holding veCRV confers three concrete benefits:

1. Gauge weight voting. Every two weeks, veCRV holders vote on how CRV emissions are allocated across Curve's many liquidity pools. Pools with higher gauge weight attract more CRV rewards, which in turn draw more liquidity—creating a flywheel that makes gauge votes commercially valuable.

2. LP boost. veCRV holders who also provide liquidity can earn up to 2.5× the base CRV reward rate on their deposits.

3. Protocol fee share. A portion of Curve's trading fees (historically 50%) is distributed to veCRV holders as 3CRV (a Curve LP token redeemable for stablecoins).

A governance proposal currently under consideration would remove the veCRV whitelist entirely, making CRV locking fully permissionless—a move that would lower the barrier for new protocols to participate in gauge weight markets.

Governance and the Curve DAO

The Curve DAO governs the protocol's fee parameters, gauge approvals, treasury allocations, and protocol upgrades via on-chain proposals that require veCRV votes to pass. Governance has grown increasingly active and consequential.

Recent examples illustrate the range of decisions the DAO handles. In late 2025, a vote opened to create a 5 million CRV veFunder gauge specifically to remediate borrowers harmed by an sDOLA inflation attack—a targeted use of the emissions system as a recovery mechanism for a third-party protocol failure. Founder Michael Egorov separately proposed a $6.6 million CRV grant (17.45 million CRV tokens) to Swiss Stake AG to fund Curve's 2026 development roadmap, covering LlamaLend upgrades, infrastructure hardening, security audits, and R&D, with biannual transparency reports and open-source commitments required as conditions.

The DAO also maintains tooling to keep governance sound. A tool called the Curve DAO Gauge Validator, developed by community contributor wavey, parses call data within active governance proposals, detects all add_gauge actions, and flags gauges deployed from untrusted sources—a lightweight but meaningful defense against malicious or low-quality gauge submissions slipping through.

Egorov himself has remained an active participant at the protocol layer. He received a 48.5 million veCRV boost delegation through SDGP-57, which pushed Stake DAO's total veCRV influence above 200 million—over 25% of total supply. He also purchased 1.08 million CRV at an average price of $1.114 in a single three-hour window following the June 2023 liquidation cascade that had put heavy selling pressure on the token, signaling personal confidence in the protocol's recovery.

$iREET launches, enabling up to 25%+ $CRV APR on tokenized real estate via RAAC protocol

RAAC controls 4.1% of all Curve voting power through accumulated $CVX — that's the entire engine behind the 25%+ APR. Strip away the CRV emissions subsidy and you're looking at maybe 5-7% from actual rental yield on the underlying properties, which is standard cap rate territory for tokenized RE. The Convex flywheel bootstrapping RWA liquidity is a clever play, but every protocol that's leaned on directed gauge emissions eventually faces the same cliff when TVL outpaces incentive budgets — ask Frax how that math works at scale. Borrowing crvUSD against iREET collateral adds composability, but the liquidation mechanics on illiquid tokenized property NFTs during a drawdown are an unsolved problem that no amount of Chainlink price feeds will fully derisk.

- 01Egorov collateral position saga

The founder controlling ~32% of circulating CRV while borrowing against it across multiple protocols created a months-long liquidation cliff that readers followed obsessively as a real-time contagion thriller.

- 02Aave governance CRV standoff

Whether Aave DAO would freeze or accommodate the largest single borrower position pitted risk management against political reality, drawing readers who wanted to know if DeFi governance could act against a founding-class member.

- 03July 2023 hack fallout and compensation

The $61M Vyper exploit and subsequent DAO vote to compensate victims with $44M in CRV raised concrete questions about who bears protocol losses and whether token-funded restitution is credible.

- 04veCRV tokenomics and supply control

Convex holding 51% of veCRV, automatic inflation cuts, and permissionless locking proposals all touch who actually controls gauge emissions and therefore DeFi liquidity incentives broadly.

- 05CRV cross-protocol collateral spread

CRV being used simultaneously as collateral on Aave, Llama Lend, Abracadabra, Silo, UwU Lend, and even Frankencoin (for Swiss Francs) illustrated how a single illiquid token's price determines credit conditions across a swath of DeFi.

- 06Llama Lend and Curve product expansion

Curve's own lending market launching while its founder was simultaneously borrowing against CRV elsewhere created a pointed narrative about whether new products could absorb or worsen the systemic risk.

crvUSD and LlamaLend

Curve's most significant product expansion beyond AMM pools is crvUSD, a native overcollateralized stablecoin launched in 2023. Unlike traditional CDP stablecoins, crvUSD uses a novel liquidation mechanism called LLAMMA (Lending-Liquidating AMM Algorithm), which converts a borrower's collateral into crvUSD gradually as prices decline rather than triggering discrete liquidations. This softens the penalty for borrowers caught in volatile markets and reduces systemic liquidation cascades.

LlamaLend (also called Llamalend) extends this architecture into a permissionless isolated lending market system. Each LlamaLend market pairs a collateral token with crvUSD borrowing, with its own risk parameters and interest rate curves. The system allows new assets to be supported without exposing the entire protocol to shared collateral risk.

CRV itself has been used as collateral in LlamaLend markets. Following a turbulent period in mid-2023—when Egorov's large CRV-backed positions across multiple protocols, including Aave, faced liquidation pressure—the CRV-long LlamaLend market saw recovery as prices stabilized. The Aave connection is important context: CRV's price volatility briefly threatened bad debt accumulation on Aave, catalyzing an industry-wide discussion about the risks of using governance tokens as collateral in shared lending pools.

A LlamaLend V2 wishlist process solicited community feedback in 2025, suggesting active iteration on the lending architecture. The broader crvUSD ecosystem has attracted integrations: USDaf from Asymmetry Finance was approaching $5 million in borrows, offering yields denominated in CRV and DAI, illustrating how third-party protocols build structured yield products on top of Curve's primitives.

Liquid Lockers: Convex, Yearn, and StakeDAO

One of the most consequential developments in the CRV ecosystem is the emergence of liquid lockers—protocols that pool CRV from many holders, lock it as veCRV collectively, and issue a liquid receipt token in return.

The dominant example is Convex Finance, which controls the largest single block of veCRV. When users deposit CRV into Convex, they receive cvxCRV—a token that can be traded or staked for boosted CRV rewards and a share of Convex's own CVX emissions, without surrendering liquidity for four years. Yearn Finance and StakeDAO operate analogous systems (yveCRV and sdCRV, respectively).

The effect on Curve's governance has been significant. Rather than individual token holders amassing veCRV, the gauge weight market is increasingly dominated by a small number of liquid locker DAOs, which aggregate votes and sometimes sell or delegate them via bribe markets—platforms like Votium and Hidden Hand where protocols pay veCRV holders to vote for their gauge. This turns CRV emissions into a competitively priced resource, with DeFi protocols bidding for liquidity incentives the way firms bid for advertising inventory.

Stake DAO's Onlyboost strategies, for instance, now command over 200 million veCRV in boost power following Egorov's delegation, enabling boosted LP yields for Stake DAO depositors without requiring each user to lock CRV individually. For ordinary holders, liquid lockers offer a practical path to veCRV economics without the capital lockup—but at the cost of reduced direct governance participation.

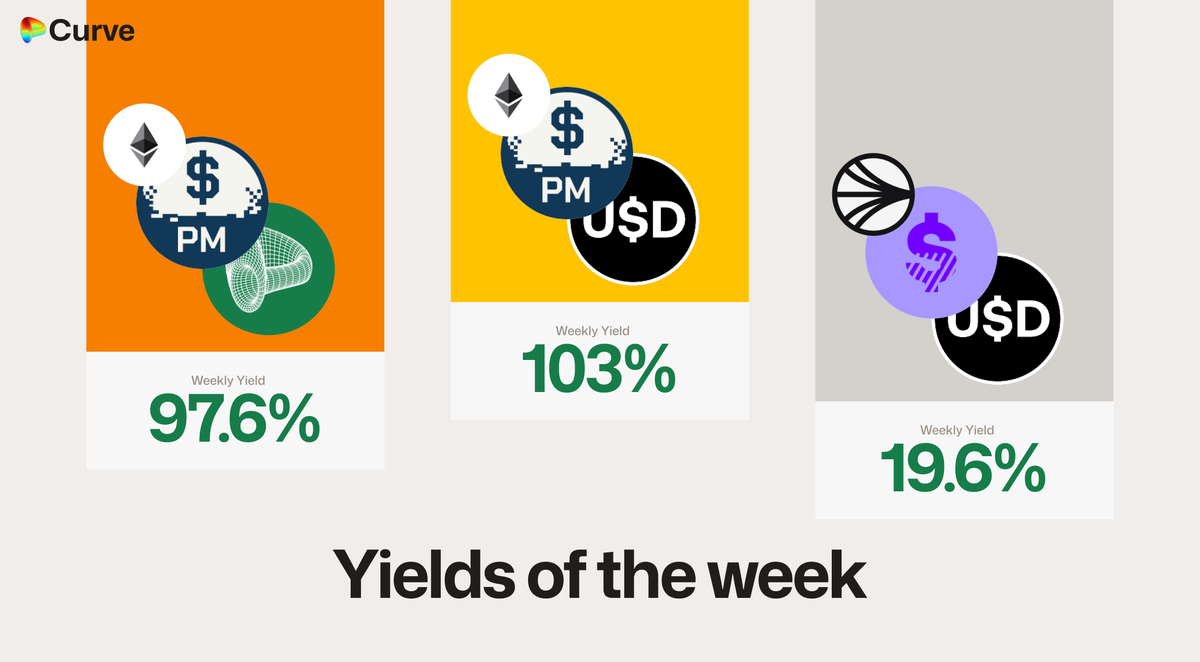

Weekly yield and Curve ecosystem metric updates as of the 8th January, 2026

TL;DR: Curve had a strong Week 2 (2026) with TVL up to $2.57B (+4.3%), surging activity across DEX, Llamalend, and crvUSD markets. pmUSD pools dominated yields (up to 103.6% on Ethereum), while crvUSD borrowing jumped 19% to $91M, signaling rising demand for Curve’s stablecoin and lending stack. DEX volumes and fees rebounded sharply (volume +45% WoW), CVX volatility drove standout LP fees, and DAO metrics improved with higher veCRV distributions. Overall: higher yields, rising leverage, strong volumes, and improving protocol health across the Curve ecosystem.

- 2023-07exploit

Vyper exploit drains CRV/ETH pool; $61M hack

- 2023-08milestone

Egorov sells $11.7M CRV via OTC deals with 6-month lockups to avoid liquidation

- 2023-10governance

Gauntlet recommends freezing CRV on Aave v2; Aave DAO unanimously rejects

- 2023-11governance

Curve DAO votes to allocate $44M in CRV to compensate July hack victims

- 2024-08milestone

CRV inflation automatically cut from 20.17% to 6.34% on fourth anniversary as team vesting completes

- 2024-09milestone

Egorov repays entire CRV debt position on Aave

- 2024-12milestone

Curve 2024 recap: Llama Lend launch, scrvUSD, CRV-Lite rollout, TradFi integrations

- 2025-09milestone

Convex reaches 400M CRV locked, representing 51.04% of total veCRV supply

CRV Tokenomics and Emission Schedule

CRV launched with an initial supply and a long emission schedule designed to distribute tokens to liquidity providers over many years. Emission rates are not fixed but decay over time—every four years the annual inflation rate is approximately halved, mirroring Bitcoin's halving logic. CRV's fifth anniversary in 2025 coincided with an emissions cut that reduced the annualized inflation rate to around 5% (Curve DAO, 2025).

The total supply is capped at approximately 3.03 billion CRV, with the majority allocated to liquidity providers (roughly 62%), with smaller tranches going to shareholders, the team, and the community reserve. Importantly, the gauge system means emission recipients are not passively determined—veCRV voters actively choose which pools attract inflation each epoch.

CRV's listing on Robinhood in 2025, and its inclusion in Grayscale's DeFi Fund alongside UNI, MKR, and LDO, represent incremental steps toward mainstream accessibility. The $iREET launch enabled CRV-denominated yields of 25%+ on tokenized real estate via the RAAC protocol, illustrating appetite for CRV as a yield-bearing asset class beyond native DeFi.

Ecosystem Expansion

Curve has deliberately expanded its surface area in several directions.

FXSwap, debuted in late 2025 via a pilot CHF/USD pool powered by ZCHF (from Frankencoin) and crvUSD, marks Curve's entry into foreign exchange pairs between fiat-pegged stablecoins—a natural extension of its StableSwap expertise into TradFi-adjacent territory. CRV emissions are attached to the pilot pools as liquidity incentives.

CRV as collateral for Swiss Francs became possible through Frankencoin's integration, allowing CRV holders to mint ZCHF against their CRV position—linking a DeFi governance token to a decentralized fiat-denominated stablecoin.

Yield Basis, a protocol introduced by Egorov at the BEL-CRV event and approaching mainnet launch, aims to eliminate impermanent loss for LPs through a novel mechanism. A successful migration to new pool implementations was in progress as of late 2025. If it functions as designed, Yield Basis could address one of AMM liquidity provision's oldest drawbacks, potentially broadening the set of assets and holders willing to deploy capital into Curve pools.

Curve Lite, a rollout for Layer 2 and smaller chains, reduces gas overhead for deploying Curve pools on networks beyond Ethereum mainnet, extending the protocol's reach without requiring each chain to maintain the full Ethereum architecture.

- Smart ContractHigh

The July 2023 Vyper compiler vulnerability drained the CRV/ETH pool and triggered a $61M exploit, demonstrating that even foundational AMM contracts carry critical infrastructure risk.

- CentralizationHigh

Convex controls over 51% of total veCRV supply and Michael Egorov at peak held ~32% of circulating CRV as personal collateral, concentrating governance power and liquidation risk in very few actors.

- LiquidityHigh

Egorov's need to exit $11.7M in CRV via private OTC deals with 6-month lockups rather than open markets revealed that CRV lacks the on-chain liquidity depth to absorb a large founder-level position without cascade risk.

- GovernanceMedium

Aave DAO's unanimous rejection of freezing Egorov's loan despite Gauntlet's risk recommendation showed that DeFi governance can be politically captured when a counterparty has sufficient community standing.

- Market / PriceHigh

CRV's price directly sets liquidation thresholds across five or more lending protocols simultaneously, meaning a sustained drawdown triggers cascading margin calls with no circuit breaker across the ecosystem.

- RegulatoryLow

Terraform Labs selling CRV holdings and Binance's $5M strategic investment both suggest regulatory scrutiny is more concentrated on Terraform and exchange relationships than on Curve's protocol itself.

Security Considerations

CRV's largest stress test to date was the July 2023 exploit of several Curve pools via a Vyper compiler bug, which drained millions of dollars of liquidity and put Egorov's large personal CRV-collateralized borrow positions at acute risk of liquidation. The incident illuminated systemic concentration risk—a single founder's debt positions large enough to threaten cascading bad debt on Aave if CRV's price fell below certain thresholds.

The protocol has since invested in security infrastructure. The 2026 Swiss Stake AG grant proposal explicitly earmarks funds for security audits as a condition. The Gauge Validator tooling reflects a broader effort to harden governance against malicious proposals. LlamaLend's isolated market design is itself partly a response to the shared-collateral risks the 2023 events exposed.

Outlook

Five years after launch, CRV occupies an unusual position in DeFi: it is simultaneously a governance token, a yield-bearing asset, an incentive mechanism for liquidity, and collateral in lending markets it helped build. The protocol's TVL recovery, emissions reduction, and product diversification into crvUSD, LlamaLend, FXSwap, and Yield Basis suggest active development rather than stagnation.

The key tensions to watch are familiar: whether liquid lockers' consolidation of veCRV power concentrates governance in ways that undermine the DAO's decentralization thesis; whether LlamaLend and crvUSD can capture meaningful market share in a competitive lending landscape; and whether CRV's emission schedule reduction, now at 5% annually and declining, will tighten supply enough to support price stability as the protocol matures. Institutional exposure via Grayscale and mainstream listing on Robinhood add a new dimension to CRV's demand side that was absent in its early years.

Latest CRV news

Curve DAO opens vote for 5M CRV veFunder gauge to remediate borrowers hit by sDOLA inflation attack$iREET launches, enabling up to 25%+ $CRV APR on tokenized real estate via RAAC protocolWeekly yield and Curve ecosystem metric updates as of the 8th January, 2026Curve Finance founder Michael Egorov has proposed a $6.6M CRV grant (17.45M CRV) to fund long-term ecosystem development. The funds would go to Swiss Stake AG to support its 2026 roadmap, including Llamalend upgrades, infrastructure, security, and continued R&D, with biannual transparency reports and open-source commitments.Curve debuts FXSwap via pilot CHF-USD liquidity pool on mainnet, powered by $ZCHF from Frankencoin and crvUSD, alongside some juicy CRV emissions. Yield Basis: upcoming migration to new pools implementation

Yield Basis: upcoming migration to new pools implementationCommunity notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…