In‑depth explainer on Curve’s LlamaLend lending layer, covering LLAMMA soft liquidations, crvUSD integration, market design, risks, cross‑chain v2 expansion, governance, and how borrowers, lenders and builders actually use it.

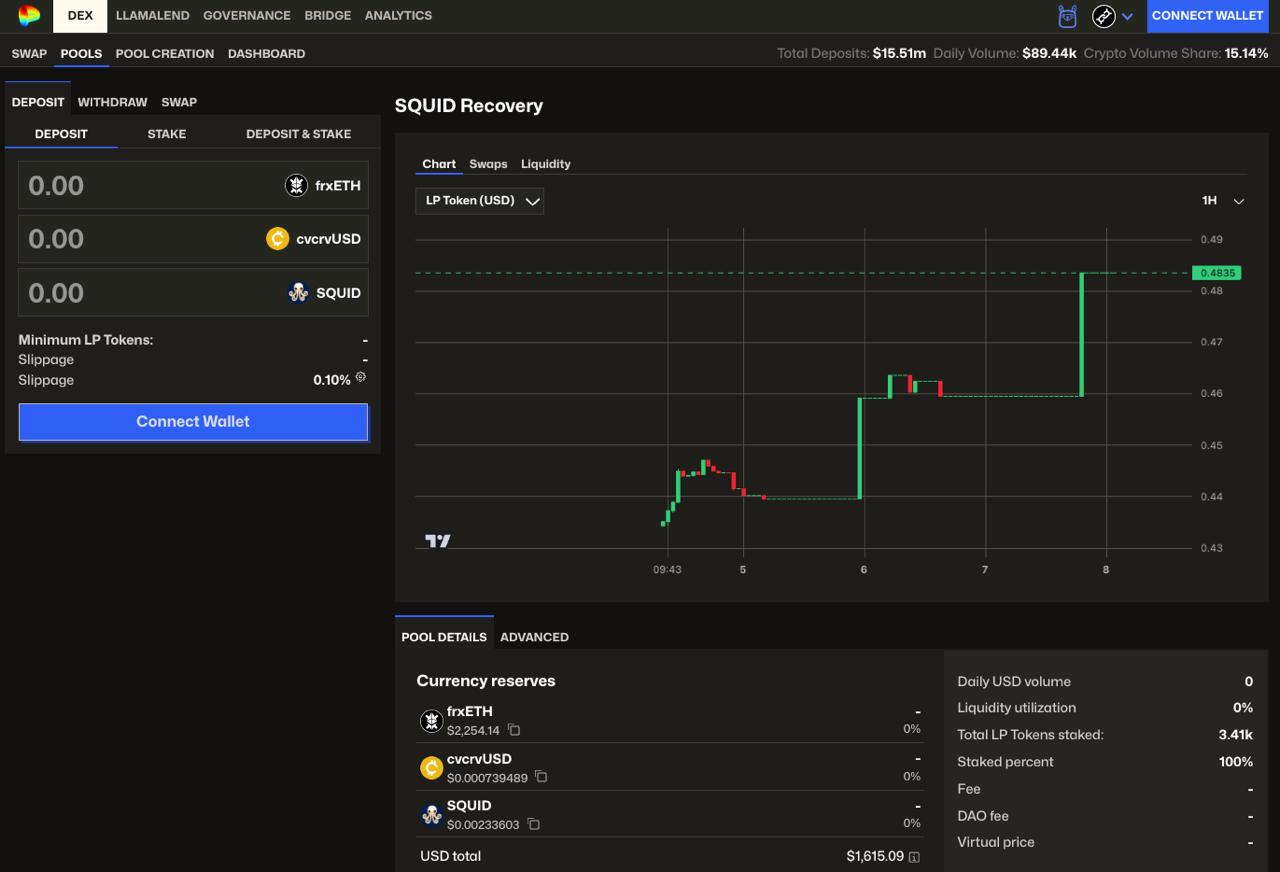

Leviathan SQUID DAO launches recovery pool for lenders affected by Llama Lend bad debt on Fraxtal2026-04

Leviathan SQUID DAO launches recovery pool for lenders affected by Llama Lend bad debt on Fraxtal2026-04 Curve DAO debates Llama Lend SQUID-recovery pool gauge2026-05

Curve DAO debates Llama Lend SQUID-recovery pool gauge2026-05 Curve deploys Llamalend v2 on Optimism with a 250K OP grant, expanding lending beyond crvUSD pairs and enabling LP tokens as collateral2026-06

Curve deploys Llamalend v2 on Optimism with a 250K OP grant, expanding lending beyond crvUSD pairs and enabling LP tokens as collateral2026-06 Donation attack manipulates sDOLA price on Curve LlamaLend, triggering mass liquidation of crvUSD borrowers for ~$240K2026-03

Donation attack manipulates sDOLA price on Curve LlamaLend, triggering mass liquidation of crvUSD borrowers for ~$240K2026-03 LlamaRisk post-mortem pins LlamaLend sDOLA exploit on unsmoothed vault oracle reads; $190K donation inflated PPS 13.79%, hard-liquidating 27 borrowers2026-03

LlamaRisk post-mortem pins LlamaLend sDOLA exploit on unsmoothed vault oracle reads; $190K donation inflated PPS 13.79%, hard-liquidating 27 borrowers2026-03 Curve’s 2025 marked a quiet but pivotal build year, scaling liquidity and crvUSD usage while launching FXSwap and preparing Llamalend V2 to position Curve as a full-stack DeFi FX and lending platform for 2026.2026-01

Curve’s 2025 marked a quiet but pivotal build year, scaling liquidity and crvUSD usage while launching FXSwap and preparing Llamalend V2 to position Curve as a full-stack DeFi FX and lending platform for 2026.2026-01

LlamaLend: Curve’s Soft-Liquidation Lending Layer Explained

A permissionless lending system built around Curve’s crvUSD stablecoin, LlamaLend combines an automated market maker with a lending engine to offer high‑LTV borrowing and “soft” liquidations instead of the hard liquidations common in most DeFi money markets. By tying loan health to on‑chain pricing curves rather than fixed thresholds, it aims to make leverage on assets like CRV, LP tokens, and blue‑chip collateral more capital‑efficient and less prone to liquidation cascades.

Background: Curve, crvUSD and the Evolution Toward LlamaLend

Curve Finance began in 2020 as a specialized automated market maker for like‑kind assets, especially stablecoins, optimizing for deep liquidity and minimal slippage within narrow price bands. Over time, Curve’s pools expanded beyond dollar‑pegged stablecoin pairs to include wrapped bitcoin and ether, liquid staking tokens, and yield‑bearing derivatives, but the core design philosophy remained the same: concentrate liquidity where trades actually happen, reduce impermanent loss, and use incentives from the CRV token to bootstrap depth. This combination turned Curve from a niche venue into a critical piece of DeFi’s base liquidity, with many protocols routing stablecoin and LSD trades through Curve to minimize execution cost. The launch of veCRV governance, which locks CRV for extended periods in exchange for boosted rewards and voting power, further entrenched Curve as a coordination layer for directing emissions and liquidity across the ecosystem.

As the protocol matured, Curve’s community and founder Michael Egorov pushed to evolve from a single‑purpose AMM into a broader “full‑stack” DeFi platform spanning swaps, stablecoin issuance, and lending. A key motivation was that Curve’s deep liquidity and governance flywheel could be used not only to facilitate trades but also to back a native over‑collateralized stablecoin, enabling new feedback loops between liquidity provision, borrowing, and protocol revenue. This vision crystalized in crvUSD, a stablecoin backed by crypto collateral and managed by a novel liquidation AMM known as LLAMMA, which replaces sharp liquidation thresholds with gradual, price‑band based collateral rebalancing. The crvUSD design effectively treats a borrower’s collateral as being partially pre‑swapped along a curve as prices move, enabling more graceful unwinding of risk during market stress.

LlamaLend sits on top of this foundation as Curve’s lending layer, enabling users to borrow crvUSD or other assets against various forms of collateral, or to lend crvUSD into markets to earn interest. Early iterations of LlamaLend were tightly coupled to crvUSD: by design, each market had to include crvUSD on at least one side, either as the borrowed asset or the posted collateral. This constraint aligned incentives around the stablecoin and simplified risk management, since the liquidation engine and monetary policy could be tuned around a common denominator. Over time, however, demand grew to support more flexible pairings, non‑stable collateral such as LP tokens, and deployment across multiple chains. That expansion has culminated in LlamaLend’s multi‑market, multi‑chain roadmap, with LlamaLend v2 on Optimism and further deployments on ecosystems like Arbitrum and Fraxtal.

The backdrop for this evolution has been a broader DeFi environment grappling with the trade‑offs between capital efficiency and safety in lending protocols. Incidents on under‑collateralized money markets and over‑leveraged positions in volatile tokens have repeatedly shown how brittle conventional hard‑liquidation models can be under stress. Curve’s approach, by contrast, attempts to embed risk management into the AMM itself through LLAMMA, while relying on independent risk specialists such as LlamaRisk to study interest‑rate models, oracle design, and market configuration. The combination of economic research, protocol‑native stablecoin tooling, and governance‑driven experimentation has made LlamaLend both an innovative and sometimes controversial testbed for new ideas in DeFi lending.

Against this backdrop, the Curve community has also been debating long‑term resource allocation to sustain development. A notable proposal from Egorov seeks a large CRV grant flowing to Swiss Stake AG to fund Curve’s 2026 roadmap, which explicitly includes LlamaLend upgrades, infrastructure, security work, and continued research and development. That kind of dedicated funding is meant to ensure that lending infrastructure, including LlamaLend’s risk controls and cross‑chain deployments, can keep pace with the protocol’s ambitions to become a full‑stack FX and lending platform alongside its core AMM business.

Leviathan SQUID DAO launches recovery pool for lenders affected by Llama Lend bad debt on Fraxtal

Great. As a squid holder, news contributor & voter, I'm happy that Leviathan is restoring faith in its community. It's very unfortunate that the bad debt incident occur.

Readers treat each new LlamaLend isolated-market launch as its own speculative event rather than a protocol-wide exposure, with the Arbitrum FXN market alone pulling 3× more clicks than any single exploit — revealing that the per-market isolation architecture that was designed as a risk firewall has instead become the primary engagement engine.↗

What LlamaLend Is and How It Fits into Curve

LlamaLend is Curve’s non‑custodial lending infrastructure that allows users to borrow crvUSD against their crypto assets or lend crvUSD into markets to earn yield. In practice, this means that each LlamaLend market is a specialized vault or pool where one set of users deposits collateral and borrows, while another set supplies the borrowable asset and collects interest. The system is fully built around crvUSD at the base layer, such that every market must contain crvUSD as either the borrow token or the collateral token in the original design. That architecture allows the protocol to rely on a common stable unit for accounting and to leverage LLAMMA’s liquidation engine whenever crvUSD is involved. It also reinforces crvUSD’s role as the central liquidity and risk hub for the Curve ecosystem.

From a user’s perspective, there are two primary ways to interact with LlamaLend. Borrowers can deposit supported collateral and take out a loan in crvUSD or in another asset depending on the market configuration. This process can happen in what the documentation calls “mint markets” or “lending markets.” In mint markets, crvUSD is minted directly by the protocol when a user borrows rather than being drawn from a pool of previously supplied liquidity. That design resembles MakerDAO’s vaults but with LLAMMA‑based liquidations. In lending markets, by contrast, crvUSD or another borrowable asset is lent by other users, and borrowers draw from this shared pool, paying a variable interest rate determined by the market’s utilization and chosen monetary policy. This bifurcation gives Curve flexibility to structure different types of leverage products while keeping a consistent user experience under the LlamaLend umbrella.

Lenders, or “suppliers,” interact only with the lending markets, not the mint markets. They deposit crvUSD (or another designated deposit token) into a market’s vault contract and receive a claim on the pool plus accrued interest over time. Platforms like Yield.xyz surface these opportunities by listing yields on Curve lending markets, all of which use crvUSD as the deposit token even when the underlying collateral differs. This approach turns LlamaLend into an income layer for crvUSD holders who want to earn additional return by taking on counterparty risk to borrowers seeking leverage on assets such as CRV, liquid staking tokens, or LP shares in Curve pools.

At the smart contract level, LlamaLend integrates with Curve’s broader infrastructure and governance. Markets can be created through permissionless or semi‑permissionless factories subject to parameters configured or approved by Curve DAO votes, and CRV emissions can be directed via gauges to incentivize liquidity and usage in specific lending markets. Treasury‑level strategies, such as the “Resupply” initiative, can mint crvUSD directly into LlamaLend markets to bootstrap liquidity while routing the resulting interest income back to the DAO. This tight integration with the veCRV and gauge system positions LlamaLend not just as a separate product line but as a capital allocator within Curve’s overall economic engine.

An important nuance is that LlamaLend is not a single monolithic protocol in the way that compound money markets historically were. Rather, it is a collection of markets, each with its own collateral type, interest‑rate model, oracle configuration, and risk profile. A CRV‑long market where users post CRV as collateral to borrow crvUSD behaves differently from, say, a stablecoin‑denominated market using yield‑bearing tokens as collateral, or a market on Fraxtal or Optimism with chain‑specific parameters. This modularity allows markets to be tuned individually but also means that risk is not automatically shared across the entire system; isolated markets can incur bad debt or experience volatility without necessarily spreading contagion to others.

The design goal, therefore, is to combine this modularity with robust risk management and clear tooling for users and governance participants. The Curve team has invested in interfaces, like the updated LlamaLend UI and the @LlamalendMonitorBot on Telegram, that surface real‑time loan health and market metrics, while external research groups such as LlamaRisk provide ongoing assessments of parameter choices and incidents. As LlamaLend expands across chains and supports more exotic collateral types, this interplay between protocol design, third‑party research, and community governance becomes increasingly central to its long‑term viability.

LLAMMA and Soft Liquidations: The Core Innovation

The defining technical feature behind LlamaLend is the LLAMMA, or “lending‑liquidating AMM algorithm,” originally introduced in the crvUSD whitepaper. Rather than treating collateral and debt as separate entries in a simple account, LLAMMA conceptually embeds a borrower’s collateral into an AMM curve that gradually trades between the collateral asset and the borrowed asset as the price of the collateral moves. When collateral prices fall, the LLAMMA progressively converts collateral into crvUSD (or another reference asset) within predefined “bands” instead of triggering a single liquidation when a threshold is breached. When prices recover, the process can reverse, re‑exposing the borrower to the upside. This mechanism is designed to minimize the slippage and market impact associated with liquidations and to keep borrowers in the system longer by smoothing out their risk profile.

In traditional DeFi lending protocols, such as many Aave or Compound‑style markets, positions are liquidated abruptly. When the value of a borrower’s collateral falls below a loan‑to‑value threshold, liquidators are incentivized to repay part of the debt and seize collateral at a discount, often selling it on the open market. This can exacerbate price declines, especially in thin markets, and can lead to cascading liquidations where the act of liquidating itself pushes prices down further. LLAMMA aims to mitigate this by turning the liquidation process into a sliding mechanism controlled by an AMM, where liquidation is effectively a sequence of small rebalancing trades spread across a range of prices rather than a single event.

LlamaLend uses this concept to offer what it calls “soft liquidations.” When a user’s position enters a collateral “erosion zone,” the LLAMMA engine gradually converts their collateral into the borrowed asset (often crvUSD) to protect the position before it becomes under‑collateralized. The process is automatic and continuous within the configured price bands, meaning borrowers are less likely to wake up to a fully liquidated position after a sharp move. A video tutorial produced for LlamaLend emphasizes that this soft liquidation is a key advantage for borrowers, providing a buffer against sudden market moves and reducing the punitive nature of traditional DeFi liquidations.

From a risk perspective, soft liquidations do not eliminate the possibility of loss; borrowers can still see their collateral converted into a more stable asset at depressed prices, and if markets gap beyond the coverage of the price bands or if oracles fail, bad debt can still arise. However, the structure tends to spread liquidations across more prices and time, which can be particularly valuable for volatile or less liquid tokens where order‑book depth in external venues is limited. It also aligns more closely with many users’ intuitive preferences: gradually de‑risk as conditions deteriorate, rather than facing an all‑or‑nothing cliff.

Another advantage of the LLAMMA approach is that it integrates naturally with Curve’s existing AMM technology. Since the protocol is already optimized for low‑slippage stable and near‑stable swaps, routing liquidation trades through similar curves can reduce losses compared to dumping collateral into a thin order book. The design also opens the door to more complex products where LP tokens or yield‑bearing assets serve as collateral: if liquidations can be managed smoothly via AMM curves, then the system can, in principle, support collateral types that would be dangerous to liquidate via naive market sales.

LlamaLend builds on LLAMMA but also extends it. In some markets, particularly those that involve cross‑asset borrowing or LP tokens, the details of how liquidation bands are configured and how oracles feed prices into the engine become crucial design choices. Research from LlamaRisk has explored how the shape of the interest‑rate curve and the dynamics of utilization interact with LLAMMA‑based liquidation to determine overall system stability. Their work recommends specific monetary policies and highlights how unsmoothed or stale oracle readings can undermine the benefits of soft liquidation, as seen in some real‑world incidents discussed later. These findings underscore that LLAMMA is a powerful tool but not a silver bullet; it must be paired with careful parameter selection and robust oracle design.

Ultimately, LLAMMA and LlamaLend’s soft liquidations reflect a broader trend in DeFi toward embedding more of the risk management logic into continuous mechanisms rather than discrete events. By turning liquidation into a spectrum rather than a binary trigger, LlamaLend attempts to create a more resilient lending environment that can handle volatile non‑stablecoin collateral without constant fears of instant liquidation, while still protecting lenders from uncompensated risk.

Curve DAO debates Llama Lend SQUID-recovery pool gauge

$130.8K of SQUID-long bad debt on Fraxtal is small next to the CRV-long hole, but a gauge changes the recovery pool from a distressed-claim venue into a CRV-subsidized liquidity sink. Once veCRV starts paying depth for impaired LlamaLend vault shares, governance is pricing more than SQUID recovery; it is setting the boundary between permissionless market risk and DAO-endorsed market cleanup. The earlier SQUID market flashing 100%+ APY at tiny TVL is the ugly part: emissions can make thin collateral look like yield until exit liquidity becomes the product.

- 01Arbitrum market expansion↗

The FXN launch and broader Arbitrum rollout dominated clicks because each isolated new market represents a bounded, independently evaluable yield opportunity that readers can act on immediately.

- 02Llama Risk governance tuning↗

Repeated Llama Risk parameter adjustment posts drew 987 clicks because readers track rate model and collateral factor changes as live signals that directly alter their borrow cost and liquidation exposure.

- 03Egorov founder leverage positions

The Curve founder repeatedly using his own protocol for large leveraged CRV positions — and publicly taunting liquidators — turned his on-chain activity into a must-watch market event with real liquidation consequences.

- 04Oracle manipulation exploits↗

The sDOLA donation attack and UwU hacker loan demonstrated that vault-oracle unsmoothed reads can bypass LLAMMA's soft-liquidation design and trigger mass hard liquidations, undermining the protocol's core safety claim.

- 05Fraxtal bad debt and recovery

A bad debt incident on Fraxtal forced a SQUID DAO recovery pool and a contentious Curve DAO gauge debate, revealing that isolated markets can still produce community-wide bailout obligations.

- 06Interest rate model optimization↗

LlamaRisk's comparative IRM and Semilog monetary policy research attracted readers who understand that rate parameter choices directly govern borrowing cost volatility and liquidation frequency.

Market Types, Interest Rates and Monetary Policy

At the heart of each LlamaLend market lies a set of parameters that determine who can borrow what, under which conditions, and at what price. The Curve documentation distinguishes between “mint markets” and “lending markets,” a conceptual split that has implications for both risk and yield. In mint markets, borrowers deposit collateral and mint new crvUSD directly against it, similar to a Maker‑style CDP system but governed by LLAMMA‑based liquidations; there is no pool of external depositors lending out existing crvUSD in this case. In lending markets, by contrast, there is a designated deposit token, typically crvUSD, that suppliers lend into a shared pool from which borrowers draw their loans. The presence of outside lenders introduces utilization dynamics and a variable interest rate that responds to supply and demand.

Interest‑rate modeling for these markets has been a focus of ongoing research. LlamaRisk’s “Monetary Policy Optimization” study examined several interest rate models (IRMs) available for LlamaLend, including a Semilog model and various alternatives, with the aim of finding a policy that balances market efficiency with user protection. Their follow‑up comparative analysis of IRMs concluded that LlamaLend would benefit from adopting a single continuous interest rate model, recommending a quadratic variant of the Semilog policy as the default for LlamaLend v2. The quadratic Semilog model is designed to keep rates relatively low and stable at moderate utilization levels while ramping up costs more aggressively as utilization approaches the pool’s capacity, thereby discouraging situations where markets are fully borrowed out and lenders lack liquidity.

The implications of these design choices can be summarized conceptually, and a simplified comparison of model characteristics is helpful.

| Interest Rate Model | Shape at Low Utilization | Behavior Near High Utilization | LlamaRisk Assessment for LlamaLend |

|---|---|---|---|

| Linear | Proportional increase | Predictable but slow to react | Too blunt; can under‑price tail risk |

| Piecewise Linear | Stepwise rate jumps | Sudden hikes at thresholds | More control but can create cliffs |

| Semilog | Slow rise then exponential | Better stress protection | Good trade‑off, but can be refined |

| Quadratic Semilog (recommended) | Gentle early slope | Smooth but sharp increase | Best balance of performance and protection |

Lenders care about these curves because they determine yield, while borrowers care because rates affect the cost of leverage and the feasibility of long‑term positions. A gently sloping curve at moderate utilization encourages borrowing and can grow total value locked (TVL), but if the curve does not steepen sufficiently near high utilization, markets may become illiquid and vulnerable to shocks. A more convex curve, such as the quadratic Semilog, aims to keep the system in a healthy zone where there is enough borrowing to generate yield but enough spare liquidity to absorb redemptions and unwind positions without large rate spikes under normal conditions.

Beyond interest rates, each LlamaLend market configures collateral factors, liquidation bands, oracle sources, and borrowing caps. Collateral factors determine how much a user can borrow relative to their posted collateral, while LLAMMA bands define how quickly collateral is converted as prices move. Oracle configuration is particularly sensitive in LlamaLend because the system often relies on vault share prices or LP prices rather than simple spot feeds, especially in markets where collateral is a yield‑bearing token or Curve LP share. If the oracle reading is noisy, delayed, or easily manipulated, then LLAMMA’s smooth liquidation behavior can break down, as illustrated by the sDOLA‑long2 incident in which unsmoothed vault oracle reads were exploited.

Borrowing caps and other governance‑set limits provide a final layer of control. Curve DAO can vote to raise or lower caps on specific markets, adjust interest‑rate parameters, or even pause markets if risks are identified. In practice, these levers have been used in response to incidents and changing market conditions, often following recommendations by LlamaRisk posted to governance forums. Over the past cycles, LlamaRisk has repeatedly suggested parameter tweaks to LlamaLend and crvUSD markets, demonstrating an iterative approach where real‑world data informs gradual refinements rather than sweeping redesigns.

For end users, much of this complexity is abstracted away by the LlamaLend interface, which displays current borrow and supply rates, utilization, and loan health metrics. However, for sophisticated participants such as strategy builders and DAO treasuries, understanding the monetary policy and market configuration is crucial. Initiatives like Resupply, which proposed minting and supplying 5 million crvUSD into the sreUSD LlamaLend market with the expectation of generating roughly 8.1% annual yield for the Curve DAO, rely on these parameters to model expected returns and risk. The growing role of these structured strategies in Curve’s treasury management underscores that LlamaLend is not merely a retail borrowing tool but also a venue for protocol‑level capital deployment.

Risk Management, Incidents and Lessons Learned

Any lending protocol that offers leverage on volatile assets must contend with the possibility of liquidation failures, oracle manipulation, and smart‑contract vulnerabilities. Curve’s own risk documentation emphasizes that users depositing assets into LlamaLend vaults may face partial or total losses due to smart contract bugs, exploits, economic attacks, or failures of underlying assets, including stablecoins losing their peg. The protocol is non‑custodial and permissionless, which enhances openness but also means there is no centralized backstop if markets go awry. Instead, risk mitigation relies on careful protocol design, robust auditing, conservative parameterization, and, in some cases, ex‑post community efforts to socialize or repair losses.

One of the most instructive incidents in LlamaLend’s history has been the sDOLA‑long2 market exploit, which LlamaRisk analyzed in a detailed post‑mortem. In that case, an attacker exploited the fact that the market used unsmoothed vault oracle reads. A donation of approximately 190,000 units to the underlying vault artificially inflated its price‑per‑share by about 13.79%, making it appear as though the collateral was worth significantly more than it actually was. This mispricing allowed the attacker to open over‑leveraged positions and then withdraw value before the oracle normalized, leaving the system with bad debt. The abrupt upward move in the oracle also pushed 27 ordinary borrowers into hard liquidation as their positions were suddenly mis‑measured relative to the inflated price, undermining the promise of soft liquidations.

LlamaRisk’s analysis concluded that smoothing oracle inputs over time and using more robust data sources could have mitigated or prevented this attack. The episode highlighted that even sophisticated mechanisms like LLAMMA are only as reliable as the data they ingest; if the oracle can be manipulated, the AMM‑based liquidation engine can be tricked into making poor trades. In response, Curve’s development and risk teams have increasingly emphasized the importance of oracle design, including proposals for block‑based oracles and multi‑source feeds to reduce susceptibility to single‑block manipulation. The sDOLA incident also accelerated governance discussions about parameter tightening in markets with complex collateral, and informed LlamaRisk’s recommendations for aligning IRMs and oracle policies with the specific risk profile of each market.

A separate but related episode involved concerns that a series of suspicious liquidations at Inverse Finance were linked to LlamaLend. YAM Finance publicly clarified that a reported exploit involving Inverse was not caused by LlamaLend, pushing back against early speculation that Curve’s lending layer was the vector. While LlamaLend itself was not at fault, the incident underscored how intertwined DeFi protocols have become: positions in one system are often financed via another, and on‑chain forensic traces can be difficult to interpret quickly. For media and users alike, this complexity demands care in attributing causality when a hack or exploit surfaces, and for protocols it reinforces the value of transparent post‑mortems like those provided by LlamaRisk.

Another category of risk emerges when large concentrated positions interact with system constraints. Curve and its ecosystem have had to navigate high‑profile events around CRV‑backed loans, including fears of cascading liquidation if a large position secured by CRV were to unwind. Community‑driven analyses, such as those by CurveCap, have examined how LlamaLend and crvUSD markets handled stress around CRV price moves, finding that while volatility did test the system, it did not produce the catastrophic liquidation spiral some feared. These episodes have been instructive both in validating aspects of LLAMMA’s design and in highlighting areas where parameters and incentives could be better tuned to handle large whales without unduly exposing lenders.

Short‑lived but notable episodes, such as the “brief wondrous life” of the UwU hacker’s LlamaLend loan, also illustrate how opportunistic attackers attempt to use lending protocols as temporary liquidity sources. In that case, a hacker who compromised UwU Lend attempted to interact with LlamaLend, only to have the loan quickly closed out or rendered uneconomical due to risk controls and market realities. While anecdotal, such stories highlight the evolving cat‑and‑mouse dynamic between exploiters seeking to route stolen funds through lending markets and protocol defenses designed to prevent system‑level contagion.

In some instances, LlamaLend markets on newer chains have accumulated bad debt, prompting recovery efforts by third‑party communities. On Fraxtal, for example, an incident left lenders in a LlamaLend market with losses that led Leviathan’s SQUID DAO to launch a recovery pool aimed at gradually recapitalizing affected users. That same DAO later proposed a gauge for its LlamaLend‑related pool on Curve, seeking CRV incentives in recognition of its role in absorbing part of the loss and rebuilding confidence. These community‑led recovery efforts underscore both the limits of protocol‑level protections and the social layer that often emerges in DeFi, where DAOs and media outlets like Leviathan News coordinate narratives and capital to heal wounds from exploits.

LlamaRisk’s ongoing work, including the introduction of tools like LlamaGuard for proof‑of‑security and continuous risk assessments of LlamaLend markets, represents a structural response to these incidents. By publishing research on optimal interest rate models, monitoring ownership shifts in key assets, and conducting post‑mortems when things go wrong, LlamaRisk provides a feedback loop that informs Curve governance and development. Combined with Curve’s own security resources and documentation warning users about lending risks, this ecosystem of risk evaluation is meant to make LlamaLend safer over time, even as it experiments with new forms of collateral and cross‑chain deployments.

Finally, it is worth noting that while soft liquidations and LLAMMA reduce some forms of risk, they introduce new ones. The gradual conversion of collateral can leave borrowers with portfolio compositions different from what they expect, especially after volatile periods, and can be confusing without clear UX. Efforts like the LlamaLendMonitorBot, which notifies users about changes in loan health via Telegram, are attempts to bridge this gap by making LLAMMA’s behavior more transparent and predictable. The evolution of user tooling will likely be as important as the underlying math in determining how safely the broader user base can navigate LlamaLend’s unique liquidation model.

Curve deploys Llamalend v2 on Optimism with a 250K OP grant, expanding lending beyond crvUSD pairs and enabling LP tokens as collateral

DefiLlama still has Curve LlamaLend on Optimism at ~$7k TVL and ~$9k borrowed, so 250K OP is a cold-start subsidy, not just another emissions wrapper. The useful unlock is turning Curve LP inventory into borrowable collateral, but LP tokens are messy collateral: liquidations depend on pool depth, oracle composition, and whether one side of the pair is already breaking. LlamaRisk curating markets is the guardrail; without tight caps, this becomes leverage on top of liquidity that may disappear exactly when LLAMMA needs to unwind it.

LlamaLend isolated lending markets launch on Ethereum mainnet

- 2024-06exploit

UwU hacker opens LlamaLend loan using proceeds from the UwU Lend exploit

Curve LlamaLend contracts deployed to Arbitrum

sDOLA donation attack hard-liquidates 27 borrowers via unsmoothed vault oracle; ~$240K impact

- 2024-11milestone

Michael Egorov opens large CRV lending position on LlamaLend, publicly challenges liquidators

Arbitrum FXN isolated market launches; Curve 2024 highlights LlamaLend as flagship product

Resupply proposes minting $5MM crvUSD into the sreUSD LlamaLend market

LlamaLend V2 wishlist published; Curve positions V2 as full-stack DeFi FX and lending platform

Cross‑Chain Expansion and LlamaLend v2

Originally, every LlamaLend market required crvUSD on at least one side, reflecting the protocol’s design as a crvUSD‑centric lending layer. As usage grew and the Curve roadmap expanded toward on‑chain foreign exchange (FX) and multi‑asset leverage, this constraint began to look limiting. In particular, there was rising interest in using LP tokens, including pool shares from Curve’s own AMMs, as collateral and in creating markets that did not revolve exclusively around crvUSD pairs. These demands set the stage for LlamaLend v2, an upgrade designed to support a broader variety of asset combinations and more flexible collateral options.

A key milestone in this expansion has been the deployment of LlamaLend v2 on Optimism. Community coverage of the launch highlighted that v2 on Optimism removes the earlier restriction limiting markets to crvUSD pairs, allowing any combination of assets to form a lending market. This change opens the door to markets where, for example, one can borrow ETH against OP, or use LP tokens from Curve’s Optimism pools as collateral to borrow a stablecoin, all within the LLAMMA‑powered liquidation framework. At the same time, Curve DAO approved the use of OP incentives to bootstrap these Optimism markets, voting to allocate 60,000 OP over a seven‑week period to both LlamaLend markets and on‑chain liquidity for crvUSD. These incentives are intended to attract initial suppliers and borrowers, ensuring there is enough depth to support healthy utilization and to test v2’s expanded capabilities in a real‑world setting.

The Optimism deployment sits within a broader cross‑chain push. On Arbitrum, for example, Curve founder Michael Egorov proposed that the Arbitrum DAO match his personal donation of 237,500 ARB to bootstrap Curve lending and LlamaLend markets on that chain. The proposal envisions creating ARB/crvUSD lending markets and potentially deploying new pools where ARB can be used as collateral or borrowed against crvUSD, with the initiative coordinated via a multisig controlled by LlamaRisk. This collaboration illustrates how off‑chain actors like LlamaRisk can help steward cross‑chain expansions, while also ensuring that risk oversight keeps pace with new deployments.

On top of native deployments, LlamaLend has become a foundation for meta‑protocols like Resupply, which build higher‑level lending products by plugging into LlamaLend markets. Resupply’s “success story” post notes that its launch quickly tripled LlamaLend’s TVL, from about 37 million dollars to over 181 million dollars, by minting and supplying crvUSD into lending markets and packaging the resulting yields for end users. A subsequent proposal from Resupply asked Curve DAO to mint and supply 5 million crvUSD directly into the sreUSD LlamaLend market via a factory contract, with all revenue from this strategy flowing back to the DAO treasury. Based on an average supply rate of roughly 8.1% in that market, the proposal estimated around 405,000 dollars in annual return for the DAO, with full governance control over any changes in allocation. These measures show how LlamaLend can act as a yield source for protocol‑level capital, not just individual users.

The interplay between LlamaLend and emerging FX products is another important dimension of v2 and beyond. Curve’s 2025 Year in Review highlighted that the roadmap ahead includes on‑chain FX markets, crvUSD expansion through initiatives like YieldBasis, and LlamaLend v2 as part of a broader effort to position Curve as a full‑stack DeFi FX and lending platform. In concrete terms, this means users could eventually post foreign‑currency stablecoins or FX LP tokens as collateral to borrow crvUSD or other assets, while LLAMMA handles liquidation across currency pairs. The fxSAVE market that went live on Resupply, quickly passing 1 million in TVL, is one example of how FX‑related strategies can be layered on top of LlamaLend to create structured products that appeal to users seeking diversified yield.

The expansion has not been without challenges. On newer chains like Fraxtal, LlamaLend markets have experienced bad‑debt events that required community coordination to address, including the Leviathan SQUID DAO’s recovery pool for impacted lenders. At the same time, such incidents have spurred governance debates around LlamaLend‑related gauges, such as proposals to direct CRV emissions to SQUID recovery pools or to specific LlamaLend markets where additional incentives could accelerate healing and growth. These debates underscore that cross‑chain expansion for a lending protocol is not merely a technical porting exercise; it is an ongoing process of social negotiation, incentive design, and risk calibration that must be revisited as usage evolves.

Looking ahead, the combination of LlamaLend v2’s expanded asset flexibility, cross‑chain deployments, and integration with FX‑oriented products suggests that LlamaLend is likely to become more heterogeneous over time. Rather than a single profile of “crvUSD‑against‑blue‑chip collateral,” the system is evolving into a platform where each chain and market may have distinct collateral types, oracles, monetary policies, and incentive schemes. For users and analysts, this makes it even more important to examine each LlamaLend market on its own terms, rather than assuming uniform risk and behavior across the suite.

Governance, Ecosystem Integration and Tooling

LlamaLend is deeply woven into Curve’s governance and incentive machinery, particularly the veCRV and gauge system. CRV holders who lock their tokens as veCRV can vote on gauge weights that direct CRV emissions to specific pools and markets, including LlamaLend markets in some configurations. This mechanism allows the community to prioritize certain types of borrowing and lending activity, such as CRV‑long markets, LP‑collateral markets, or cross‑chain deployments on Optimism and Arbitrum. It also creates a feedback loop where external protocols, like Resupply or Leviathan’s SQUID DAO, lobby for gauge support for their associated LlamaLend pools, often highlighting their contributions to liquidity, recovery efforts, or ecosystem growth.

Treasury‑level governance plays a parallel role. The Resupply proposals to mint crvUSD into LlamaLend markets are subject to Curve DAO votes, which decide whether to allocate newly created crvUSD to lending markets like sreUSD, set caps on those allocations, and determine how yield is handled. In Resupply’s design, all revenue earned from such deployments flows back to the Curve DAO treasury, aligning protocol‑level financial interests with the performance of LlamaLend markets. The DAO thus acts both as an owner and a sophisticated user of LlamaLend, using it to generate yield on newly minted stablecoin supply while bearing the associated risks.

Independent research and risk oversight bodies further shape governance outcomes. LlamaRisk, for example, publishes detailed studies on LlamaLend’s interest rate models, recommending a quadratic Semilog policy as the default IRM for LlamaLend v2 because it best balances market performance and user protection. They also issue comparative analyses of different IRMs, suggest parameter changes for specific markets, and document incidents like the sDOLA‑long2 exploit, often with concrete recommendations for improving oracle design or tightening risk parameters. These reports are referenced in governance discussions and often drive changes in market configuration, demonstrating a distributed model of “research‑driven governance” wherein external experts help steer protocol settings without holding formal veto power.

On the tooling side, LlamaLend has benefited from both protocol‑native and community‑built infrastructure. The refreshed LlamaLend UI, highlighted in Curve’s ecosystem updates, is designed to make it easier for users to understand their loan health, see how LLAMMA will behave under different price scenarios, and evaluate yields across markets. The introduction of a block oracle is another infrastructure upgrade meant to improve data quality for price feeds and reduce susceptibility to single‑block manipulation, particularly important in LP‑collateral markets where share prices can be nudged with well‑timed donations or swaps. The LlamalendMonitorBot on Telegram provides an additional real‑time monitoring layer, alerting users to changes in the health of their loans so they can adjust positions pre‑emptively rather than relying solely on periodic manual checks.

Third‑party platforms such as Yield.xyz integrate with LlamaLend by offering curated views of lending yields, all of which use crvUSD as the deposit token in Curve’s architecture. For yield‑seeking users who are less concerned with the intricacies of LLAMMA or specific collateral mechanics, these frontends provide a simpler entry point into LlamaLend’s supply side. At the same time, they contribute to overall system usage and liquidity, making markets more robust for borrowers. Strategists and vault builders may also integrate LlamaLend as a building block in leveraged strategies, basis trades, or structured products like fxSAVE, further embedding it into the DeFi composability stack.

Developer‑facing tooling is an underappreciated but important part of this picture. Tutorials such as the “Llama Lend Titanoboa Tutorial,” which walks developers through compiling a dummy Vyper price oracle contract using IPython magic commands, highlight the protocol’s use of Vyper and Titanoboa in the LlamaLend stack. By providing examples of how to build and test oracle contracts, such materials make it easier for developers to create new LlamaLend markets with custom collateral and pricing logic, while also encouraging better practices in oracle design. Given that incidents like the sDOLA exploit hinged on oracle behavior, developer‑oriented education around safe oracle patterns is as much a risk‑mitigation strategy as a convenience feature.

The Curve ecosystem’s move toward a formal DAO treasury, FXSwap deployment, and cross‑chain messaging further entwines LlamaLend with Curve’s broader ambitions. As Curve positions itself as a DeFi FX and lending platform, LlamaLend becomes the leverage engine that users and protocols tap into when expressing views on CRV, ETH, stablecoin spreads, FX pairs, or even structured points‑farming strategies on partner chains. Governance debates around long‑term funding, such as Egorov’s CRV grant proposal to Swiss Stake AG, explicitly earmark resources for LlamaLend upgrades, security work, and continued research, reflecting recognition that the lending layer is now a core pillar of the Curve stack rather than a side experiment.

A donation attack inflated sDOLA price-per-share 13.79% via an unsmoothed vault oracle read, hard-liquidating 27 borrowers for ~$190K–$240K despite LLAMMA's soft-liquidation design.

LLAMMA continuously rebalances collateral through an AMM to reduce gap risk, but oracle latency and high-volatility collateral can still cascade into hard liquidations when soft bands are exhausted.

Llama Risk holds outsized influence over market parameters via Curve governance forum recommendations, and the Curve founder's large personal leveraged positions create correlated concentration risk.

- Liquidity / bad debtMedium

Per-market isolation limits cross-market contagion but does not prevent a single market from exhausting lender liquidity entirely, as demonstrated by the Fraxtal bad debt event requiring a DAO recovery pool.

LlamaRisk research found the Quadratic Semilog variant best balances market performance and user protection; suboptimal IRM configurations expose borrowers to sudden rate spikes that compress safety margins.

- RegulatoryLow

LlamaLend operates as a permissionless isolated lending protocol with no custodial intermediaries; no specific regulatory actions have been directed at it as of the knowledge cutoff.

How Users and Builders Use LlamaLend in Practice

In practical terms, LlamaLend supports three broad constituencies: borrowers, lenders, and builders. Borrowers are typically users who want leverage on a particular asset or exposure profile. For instance, a “CRV‑long” LlamaLend market allows users to post CRV as collateral and borrow crvUSD, which they can then use to buy more CRV, deposit into LP pools, or pursue other strategies that effectively amplify their CRV exposure. When managed carefully, soft liquidations via LLAMMA can make such leveraged positions more resilient to short‑term volatility, although they remain vulnerable to large or prolonged drawdowns. Similarly, markets for wrapped bitcoin, liquid staking tokens, or LP tokens can be used to create leveraged yield‑farming positions, where the borrowed crvUSD or other asset is recycled into additional yield‑bearing collateral.

Lenders, by contrast, are primarily interested in earning interest on relatively stable holdings, often crvUSD. By depositing crvUSD into a LlamaLend lending market, they supply liquidity that borrowers draw against, earning a variable APY determined by the market’s interest‑rate model and utilization. For risk‑tolerant lenders, markets with more volatile collateral and higher average utilization can offer attractive yields, but these come with increased risk of bad debt in the event of severe price moves or oracle failures. More conservative lenders may prefer markets where collateral is a major stablecoin or a diversified LP token with deep liquidity and careful parameter settings. Platforms like Yield.xyz help surface and compare these options, but due diligence remains essential, especially when markets involve newer or less battle‑tested assets.

Builders and protocol teams constitute the third major group of LlamaLend users. For them, LlamaLend is not just a place to borrow or lend but a programmable primitive. A protocol might, for example, create a specialized LlamaLend market where its governance token is accepted as collateral to borrow crvUSD, allowing users to access liquidity without selling, and perhaps directing CRV incentives via a dedicated gauge to attract liquidity. Another builder might use LlamaLend as the leverage layer behind a structured product: a vault that borrows crvUSD against LP tokens and automatically rebalances to maintain a target leverage ratio, passing through net yield to depositors. Resupply exemplifies this approach by building on top of LlamaLend markets and amplifying their TVL through crvUSD mint‑and‑supply strategies that benefit both end users and the Curve DAO.

Specialized markets also cater to more niche strategies. On Arbitrum, for instance, a LlamaLend market for dlcBTC wrapped bitcoin was bootstrapped with matched ARB donations from Egorov and the Arbitrum DAO, enabling up to 10x leverage on dlcBTC positions with additional points multipliers for early users. This kind of market appeals to users who are comfortable with concentrated risk in a single asset in exchange for both financial yield and non‑financial rewards such as points or future airdrops. Similarly, fxSAVE‑linked LlamaLend markets allow users to express views on FX spreads or to access yield sourced from on‑chain FX swaps, further diversifying the strategy palette.

From a workflow perspective, using LlamaLend as a borrower typically involves depositing collateral into the relevant market, selecting a borrow amount that keeps the position within safe LLAMMA bands, and monitoring health over time. Tools like the LlamaLendMonitorBot and the web UI’s health indicators assist in this, flagging when positions are entering the erosion zone where soft liquidations begin. Users can add collateral, repay part of the debt, or fully close positions at any time, subject to liquidity. Lenders, meanwhile, deposit crvUSD (or another designated asset) into a market’s vault and receive a representation of their claim. They can usually withdraw at any time, although high utilization can temporarily limit the amount available for instant withdrawal without incurring slippage or delay.

Developers creating new markets must go deeper. They need to design or select an oracle that reliably reflects collateral value, configure LLAMMA bands that match the volatility profile of the asset, choose an appropriate interest‑rate model (increasingly, the quadratic Semilog policy recommended by LlamaRisk), and set initial caps and parameters. Testing via tools like Titanoboa and dummy Vyper oracle contracts is essential to validate that the market behaves as expected under simulated conditions. Governance may then be required to approve gauges or treasury support, especially if CRV emissions or DAO‑minted crvUSD will be used to bootstrap liquidity. In this sense, each LlamaLend market is a small product in its own right, with design, launch, and maintenance phases.

The user experience is also shaped by the broader narrative ecosystem around LlamaLend. Media coverage of incidents, recoveries, and success stories influences sentiment and adoption. Weekly yield and metrics updates from Curve ecosystem observers give a sense of which markets are thriving, which are under‑utilized, and where opportunity or risk may lie. Coverage of quiet but pivotal build years for Curve, in which crvUSD and LlamaLend quietly scale in the background while headline attention focuses elsewhere, reminds users that infrastructure often matures outside of peak hype cycles. As LlamaLend becomes more ingrained in Curve’s stack and DeFi at large, the quality of this information environment will play a significant role in how safely and effectively users engage with it.

Outlook

As a lending layer built around LLAMMA and crvUSD, LlamaLend occupies a distinctive niche in DeFi’s crowded field of money markets. Its soft liquidation model and AMM‑embedded risk management offer a differentiated way to handle leveraged positions on volatile collateral, particularly for assets closely tied to Curve’s own ecosystem. At the same time, real‑world incidents such as the sDOLA‑long2 oracle exploit and chain‑specific bad debt events show that sophisticated mechanisms do not eliminate the need for conservative parameters, robust oracles, and active risk oversight.

The deployment of LlamaLend v2 on Optimism, with support for non‑crvUSD pairs and LP collateral, signals a shift toward a more general lending platform that can accommodate a wide variety of assets and strategies. Cross‑chain expansions to Arbitrum and newer ecosystems, combined with structured products like Resupply and fxSAVE building on top of LlamaLend markets, suggest that its role as a back‑end leverage engine for both users and DAOs will only grow. Governance debates around CRV funding for development, gauge allocations for recovery and growth pools, and risk‑parameter adjustments will shape how that growth unfolds.

For crypto‑native users, the key questions are whether LlamaLend’s design can sustainably deliver higher capital efficiency without commensurate increases in tail risk, and whether the ecosystem of research, tooling, and governance around it can keep pace with innovation. For Curve, success would mean that LlamaLend, alongside crvUSD and FXSwap, cements the protocol’s evolution from a stablecoin AMM into a full‑stack FX and lending platform, with LLAMMA‑based soft liquidation as a signature contribution to DeFi’s risk‑management toolkit. How well LlamaLend navigates future market shocks and cross‑chain complexity will determine whether that vision becomes a durable reality or remains an ambitious experiment.

Latest LlamaLend news

Leviathan SQUID DAO launches recovery pool for lenders affected by Llama Lend bad debt on FraxtalCurve DAO debates Llama Lend SQUID-recovery pool gaugeCurve deploys Llamalend v2 on Optimism with a 250K OP grant, expanding lending beyond crvUSD pairs and enabling LP tokens as collateralDonation attack manipulates sDOLA price on Curve LlamaLend, triggering mass liquidation of crvUSD borrowers for ~$240KLlamaRisk post-mortem pins LlamaLend sDOLA exploit on unsmoothed vault oracle reads; $190K donation inflated PPS 13.79%, hard-liquidating 27 borrowersCurve’s 2025 marked a quiet but pivotal build year, scaling liquidity and crvUSD usage while launching FXSwap and preparing Llamalend V2 to position Curve as a full-stack DeFi FX and lending platform for 2026.Sources

- https://www.curve.finance/llamalend/ethereum/markets

- https://www.youtube.com/watch?v=rfyoGfouF2o

- https://docs.curve.finance/user/llamalend/overview

- https://docs.yield.xyz/docs/curve

- https://llamarisk.com/research/llamalend-irm-optimization

- https://www.binance.com/en/square/post/297163200801042

- https://llamarisk.com/research?q=incident

- https://x.com/CryptoEconomyEN/status/2064814863918969286

- https://news.curve.finance/curve-2025-year-in-review/

- https://news.curve.finance/curve-op-incentives/

- https://news.curve.finance/resupply-success-story/

- https://news.curve.finance/curve-resupply-a-proposal-to-mint-5m-crvusd/

- https://www.youtube.com/watch?v=W47by1jPTPw

- https://forum.arbitrum.foundation/t/proposal-request-to-match-my-donation-to-boostrap-curve-lending-on-arbitrum/22975

- https://x.com/CurveCap/status/1800285500806488464

- https://resources.curve.finance/risks-security/risks/lending/

- https://thedefiant.io/news/defi/curve-crvusd-whitepaper

- https://www.llamarisk.com/research

- https://www.llamarisk.com/research/irm-comparative-analysis-llamalend

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…