Liquidity incentives are the token rewards, fee shares, and bribes DeFi protocols pay to attract capital. Learn how emissions, veCRV gauges, vote markets, and liquidation bonuses work—and why sustainability matters.

Morpho Midnight's fixed-rate credit markets shift risk to lenders through socialized bad debt, making LLTV, maturity and liquidation incentives critical parameters2026-06

Morpho Midnight's fixed-rate credit markets shift risk to lenders through socialized bad debt, making LLTV, maturity and liquidation incentives critical parameters2026-06 Aerodrome unveils Predictive Allocation, a liquidity incentive model that rewards users for forecasting future liquidity demand rather than chasing historical fees2026-06

Aerodrome unveils Predictive Allocation, a liquidity incentive model that rewards users for forecasting future liquidity demand rather than chasing historical fees2026-06 Aave Chan Initiative Accuses Aave Labs of Diverting DAO Revenues and Privatizing Protocol Economics, Demands Clarity on CowSwap Integration, Vault Fees, Horizon Deals, and V4 Liquidation Engine Incentives.2025-12

Aave Chan Initiative Accuses Aave Labs of Diverting DAO Revenues and Privatizing Protocol Economics, Demands Clarity on CowSwap Integration, Vault Fees, Horizon Deals, and V4 Liquidation Engine Incentives.2025-12 Linea launches Yield Boost, converting bridged ETH into staking-powered liquidity via Lido to deliver sustainable DeFi yields without incentives, rebasing, or new tokens2026-03

Linea launches Yield Boost, converting bridged ETH into staking-powered liquidity via Lido to deliver sustainable DeFi yields without incentives, rebasing, or new tokens2026-03 Crypto is increasingly rigged against founders as exchange listing fees, market maker deals, and liquidity incentives create heavy sell pressure2026-03

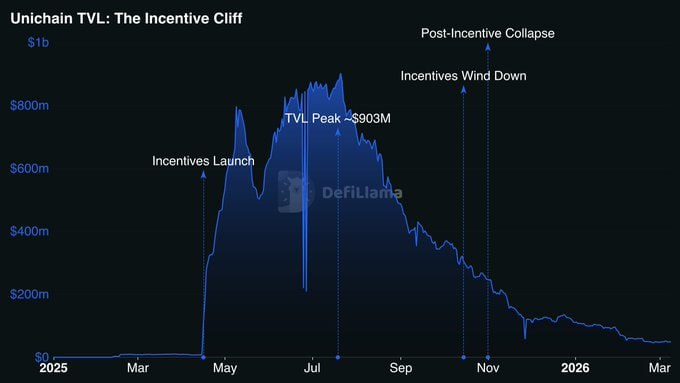

Crypto is increasingly rigged against founders as exchange listing fees, market maker deals, and liquidity incentives create heavy sell pressure2026-03 Unichain collapsed from a peak TVL of 900M to 49M, burning 21M in incentives, because it lacked any real purpose or differentiation and paid users to further fragment liquidity.2026-03

Unichain collapsed from a peak TVL of 900M to 49M, burning 21M in incentives, because it lacked any real purpose or differentiation and paid users to further fragment liquidity.2026-03

I have enough grounding. Writing the explainer now.

Liquidity incentives are the rewards—usually a protocol's native token, fee shares, or third-party "bribes"—that decentralized finance (DeFi) applications pay to attract capital into their pools and markets. They are one of DeFi's central coordination tools and one of its most contested, because the same mechanism that bootstraps a new market can also rent capital that flees the moment payments stop.

What "liquidity" means here, and why protocols pay for it

In DeFi, liquidity refers to assets deposited into a smart contract so others can trade against them, borrow them, or settle positions. On an automated market maker (AMM) such as Curve, liquidity providers (LPs) deposit pairs or baskets of tokens; on a lending market such as Aave, suppliers deposit assets that borrowers draw against. Deeper liquidity means lower slippage for traders and more available credit for borrowers, which in turn attracts more users—a flywheel every protocol wants to start.

The problem is the cold-start. A brand-new pool with little capital offers poor execution, so traders avoid it, so LPs earn little fee revenue, so capital stays away. Liquidity incentives break the deadlock by paying LPs an additional return on top of organic trading or lending fees. That subsidy is most often denominated in the protocol's own governance token, which lets a project bootstrap markets using an asset it can issue rather than spending scarce stablecoins or ETH.

The headline metric these programs target is total value locked (TVL): the dollar value of assets deposited in a protocol. TVL is an imperfect proxy—it can be inflated by incentives and by double-counting across composable protocols—but it remains the industry's default scoreboard for how much capital a market has attracted.

Bankr launches on Base with 85% of tokens seeded to Uniswap, aligning creator incentives through vested positions and on-chain liquidity

85/15 with a 90-day cliff puts Bankr closer to a Clanker-style launchpad than a pure fee router: creators get inventory, but the pool still owns most of the float at genesis. The constraint that the vested 15% stays with the original reward recipient matters because fee-right transfers no longer carry token upside unless people wrap the deal offchain. On Base, the 0.7% Uniswap v4 fee and 95/5 creator/Doppler split now give agents two monetization rails: trading flow for runway, vested inventory for reflexivity.

Readers click liquidity incentive stories not for APY numbers but to track whether a specific protocol's incentive spend is building durable network effects or subsidizing mercenary capital flight — the Unichain $21M burnout and Instadapp's ARB grant governance proposal both outperform generic yield announcements because they answer the same question: did it work?

How incentive programs are structured

Most incentive designs fall into a few families.

Direct emissions ("liquidity mining"). The protocol mints new governance tokens and distributes them to LPs in proportion to their share of a pool. This was the dominant model of the 2020 "DeFi summer" and remains common. It is simple but inflationary: continuous emissions dilute holders and create persistent sell pressure as farmers harvest and sell rewards.

Vote-escrow ("ve") models and gauge voting. Curve pioneered the most influential refinement. Users lock CRV for up to four years to receive vote-escrowed CRV (veCRV), whose voting power decays linearly with time remaining. veCRV holders vote weekly on gauge weights that decide how much of Curve's CRV emission each pool receives; updated weights take effect every Thursday (Curve Docs). Locking also boosts an LP's own CRV rewards by up to 2.5x (Curve Resources). This ties incentive direction to long-term, locked stakeholders rather than transient farmers.

Bribe or "vote" markets. Because controlling gauge votes means controlling where emissions flow, projects that want liquidity for their own token will pay veCRV holders to vote for their pool. These payments—originally called "bribes," now often "incentives" or "vote markets"—turned governance into a market. The dynamic became known as the Curve War, with Convex Finance accumulating enough veCRV to dominate emissions routing and build a durable revenue engine around it; platforms like Votemarket and Stake DAO now intermediate tens of millions in such payments. Recent newsroom coverage of Stake DAO's $70M+ in votemarket incentives and Convex's continued centrality illustrates how entrenched this layer has become.

ve(3,3) and predictive models. Base's Aerodrome and similar DEXes adapted the ve model so that trading fees and incentives flow to the voters who direct emissions, aligning fee revenue with vote weight. Aerodrome has gone further with Predictive Allocation, launching to reward participants who forecast future liquidity demand rather than allocating purely on historical fees—an attempt to make emissions forward-looking instead of backward-looking.

Points and off-chain promises. Many newer protocols issue "points" with no fixed token value, deferring the actual reward to a future airdrop. This preserves treasury tokens during a launch but trades on user trust; the xSPCX-USDT and CAKE/"Paimon Points" programs in recent coverage show how points are now bundled with conventional incentives.

- 01Cross-chain expansion incentive grants

Readers are tracking where named token grants (ARB, LINEA, OP, FLOX) are being deployed and whether multichain expansion is backed by credible on-chain governance proposals, not just announcements.

- 02Incentive failure and TVL mercenaries

The Unichain collapse story — $21M burned, TVL from $900M to $49M — crystallized a widespread fear that undifferentiated protocols are paying users to fragment liquidity, not build it.

- 03DAO governance capture of incentive tap

The ACI vs. Aave Labs conflict over diverted DAO revenues and the Ethereum Foundation researcher EigenLayer payments exposed how the same actors who set incentive policy can quietly benefit from it.

- 04New chain bootstrap dollar amounts

Readers responded to precise dollar figures tied to specific new deployments — $750K on Monad, $100M on BNB Chain, $3M COMP+POL on Polygon — treating them as signals of ecosystem conviction rather than marketing.

- 05Yield stacking via staking design

Yearn's yLockers and Gearbox's Stimmies program attracted clicks by offering compounding incentive layers (longer lock = higher incentive, borrowed leverage + emissions) that reward protocol-native behavior rather than pure mercenary farming.

- 06Emissions elimination and protocol sustainability

Balancer's failed attempt to eliminate emissions — with falling TVL and brand damage following — sharpened reader focus on whether any protocol can actually wean LPs off token subsidies without capital exit.

"Mercenary capital" and the sustainability problem

The core criticism of liquidity incentives is that they often rent capital rather than build loyalty. Mercenary liquidity describes funds that chase the highest current yield and exit the instant a better farm appears or emissions taper. When incentives are the only reason capital is present, withdrawing them can trigger a rapid unwind.

Recent events make the stakes concrete. Newsroom coverage describes Unichain collapsing from a peak TVL near $900M to roughly $49M after burning some $21M in incentives, the argument being that paid liquidity without an underlying reason to stay simply fragmented capital. Conversely, Balancer's attempt to eliminate emissions reportedly failed to hold liquidity: superior technology alone did not compensate LPs for smart-contract and brand risk, and capital exited without a risk premium. The lesson cuts both ways—incentives that are pure subsidy are fragile, but in a competitive market, removing them unilaterally can be just as destabilizing.

This has pushed designers toward incentives that aim to be self-funding or to convert mercenary deposits into something stickier. Linea's Yield Boost, for example, routes bridged ETH into Lido staking so that yield derives from staking rewards rather than token emissions, marketing it as sustainable yield "without incentives, rebasing, or new tokens." The broader trend is to back rewards with real revenue—trading fees, lending spreads, or staking yield—rather than perpetual inflation.

- 2024-09launch

EigenLayer mainnet AVS launch with incentive framework announced

- 2025-01regulatory

Trump crypto executive orders signed; Ethena integrates into Spark Liquidity Layer unlocking $1.1B

- 2025-02milestone

Unichain TVL collapses from $900M to $49M after $21M incentive burn

- 2025-03governance

ACI formally accuses Aave Labs of diverting DAO revenues and privatizing protocol economics

- 2025-04launch

Monad mainnet launches; Curvance deploys with $750K month-one liquid incentives

- 2025-04launch

Monad Foundation launches Momentum incentive-matching program for ecosystem growth

- 2025-05governance

Instadapp Fluid Arbitrum deployment proposed with 400K ARB incentives on governance forum

- 2025-06launch

Boyco opens reward claims; BeraChain vault and protocol incentives go live for users

Incentives in lending and credit markets

Liquidity incentives are not only an AMM phenomenon. In money markets such as Aave, protocols subsidize both supply and borrow sides to seed new assets, and—critically—use incentives to keep the system solvent. Liquidation incentives are the bonus paid to third parties who repay the debt of an unhealthy position in exchange for discounted collateral.

Aave's V4 redesign illustrates how sophisticated this has become. Instead of a fixed liquidation bonus and close factor, V4 uses a solver targeting a Target Health Factor and a variable, Dutch-auction-style bonus that grows as a position's health factor falls, so the riskiest positions attract liquidators fastest while healthier ones are restored with minimal overshoot (Aave). The same coverage notes this reshapes maximal-extractable-value (MEV) dynamics, with solver infrastructure already recapturing meaningful revenue from liquidations. Newer fixed-rate credit designs such as Morpho's make liquidation incentives, loan-to-value thresholds, and maturity parameters even more load-bearing, because socialized bad debt shifts risk directly onto lenders.

The "Unified Liquidity Layer" pattern—seen in Venus Flux's $1M launch incentives on BNB Chain—pushes the other direction, pooling a single deposit across lending, borrowing, and trading so that incentivized capital is reused rather than siloed.

- Liquidity (mercenary capital)High

Unichain's collapse from $900M to $49M TVL after burning $21M in incentives demonstrates that undifferentiated protocols face near-total LP withdrawal once emissions slow, with no sticky liquidity base remaining.

- Centralization (incentive governance)High

The ACI vs. Aave Labs dispute over CowSwap integration fees and V4 liquidation engine incentives, and EF researcher EigenLayer token disclosures, reveal that incentive allocation is routinely captured by insiders before DAO ratification.

- Market (emissions inflation)High

Programs distributing hundreds of millions of native tokens as LP rewards — 1B LINEA, 400K ARB, 600K OP in a single summer — create persistent sell pressure that erodes the token value underpinning those same incentives.

- Smart contractMedium

Simultaneous multi-chain deployments across Arbitrum, Fraxtal, Monad, BNB Chain, and Etherlink multiply audited-but-unproven code surface area precisely when TVL is highest and incentive-chasing capital is most concentrated.

- Slashing / penaltyMedium

EigenLayer's introduction of its slashing protocol with economically aligned AVS incentives means restakers earning EigenLayer-sourced yield now carry explicit on-chain penalty exposure that previously existed only in documentation.

- RegulatoryLow

Reports of Trump administration crypto-friendly executive orders — including reversal of restrictive accounting policies and a potential Bitcoin national reserve designation — suggest near-term US regulatory risk for DeFi incentive programs is reduced, though implementation details remain unconfirmed.

Stablecoin liquidity and the USDC/Curve nexus

Some of the most durable incentive demand comes from stablecoin issuers, who need deep, low-slippage pools so their token holds its peg. Curve's stable-optimized pools are the canonical venue, which is why issuers spend heavily to direct emissions and bribes toward pools pairing their asset with USDC, USDT, or DAI. The recent return of MIM is a textbook case: its team funded a new Curve pool with an initial $100,000 of MIM, USDT, and USDC and deployed 70M SPELL to incentivize the MIM-2Pool on Curve, explicitly to "rebuild liquidity" and restore peg stability after earlier withdrawals. Here incentives are not a growth tactic but a monetary one—payment for the peg defense that deep liquidity provides.

Governance, capture, and contested economics

Because incentives decide who gets paid, they make governance valuable—and therefore a target for capture. The veCRV system intentionally concentrates power in long-term lockers; Convex then concentrated it further. That can be efficient (locked holders coordinate liquidity well) or extractive (a few actors monetize emissions everyone else funds).

The tension is now spilling into open governance disputes. The Aave Chan Initiative has publicly accused Aave Labs of diverting DAO revenue and "privatizing" protocol economics, demanding clarity on vault fees and the V4 liquidation engine's incentives—an early sign that as incentive systems mature, the fight moves from how much to emit to who controls and profits from the emission. Cosmos's push to redesign ATOM tokenomics around revenue-driven sustainability and lower inflation reflects the same maturation across the industry.

Critics also note the cost falls unevenly. Reporting in our coverage argues that listing fees, market-maker deals, and liquidity incentives can stack into heavy sell pressure that disadvantages founders and long-term holders, since incentive tokens are frequently sold the moment they vest.

Outlook

Liquidity incentives are unlikely to disappear—cold-start coordination is a permanent feature of permissionless markets—but the design center is shifting from raw emissions toward incentives backed by real yield, forward-looking allocation, and tighter governance accountability. Expect continued experimentation: predictive and prediction-market-style allocation (Aerodrome), staking-funded yield (Linea), unified liquidity layers (Venus), and risk-sensitive liquidation incentives (Aave V4, Morpho). The protocols that endure will likely be those that convert rented, mercenary capital into liquidity with a reason to stay—whether through fee revenue, peg utility, or genuine product demand—rather than those that simply outspend rivals on emissions.

Latest Liquidity Incentives news

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…