In-depth explainer on crypto and DeFi risk management, covering 24/7 markets, hacks, stablecoins, DeFi frameworks, Aave and Curve cases, institutional convergence, and how AI and data tools are reshaping onchain risk practices.

- x.com10

- theblock.co2

- forbes.com1

- leviathannews.substack.com1

- tradingview.com1

- archive.md1

- cryptoslate.com1

+10 sources across the wider coverage universe

Ethena launches a dedicated lending market on Jupiter Lend, with Bitwise overseeing risk management and institutional participation on Solana2026-05

Ethena launches a dedicated lending market on Jupiter Lend, with Bitwise overseeing risk management and institutional participation on Solana2026-05 Chainlink CEO, Sergey Nazarov on why Chainlink CCIP leads cross-chain security, citing multi-network decentralization, risk management layer, and separate codebases preventing single points of failure2026-04

Chainlink CEO, Sergey Nazarov on why Chainlink CCIP leads cross-chain security, citing multi-network decentralization, risk management layer, and separate codebases preventing single points of failure2026-04 Piraeus Bank launches AI hub with Accenture and Anthropic, shifting from isolated use cases to unified enterprise AI across operations, risk management, and customer services2026-04

Piraeus Bank launches AI hub with Accenture and Anthropic, shifting from isolated use cases to unified enterprise AI across operations, risk management, and customer services2026-04 YO has opened its Risk Graph to external developers and AI agents. The system models DeFi protocols as a dependency graph, grading each pool, asset, protocol, and chain A to F based on propagated risk across the full stack. Access is pay-per-query via x402 in USDC on Base, no API key required.2026-06

YO has opened its Risk Graph to external developers and AI agents. The system models DeFi protocols as a dependency graph, grading each pool, asset, protocol, and chain A to F based on propagated risk across the full stack. Access is pay-per-query via x402 in USDC on Base, no API key required.2026-06 Curve DAO extends LlamaRisk partnership through April 2027 for risk management and crvUSD growth2026-03

Curve DAO extends LlamaRisk partnership through April 2027 for risk management and crvUSD growth2026-03 The Cyfrin Solodit API is now live, with access to 50,000 smart contract vulnerabilities2026-01

The Cyfrin Solodit API is now live, with access to 50,000 smart contract vulnerabilities2026-01

Risk Management in Crypto and DeFi

Risk management in crypto is the discipline of identifying, measuring, and controlling the financial, technical, and governance risks that come with holding, trading, or building on digital assets. It translates hard‑earned lessons from traditional finance into a world of 24/7 markets, open-source code, composable DeFi protocols, and ever-present hack and governance risks.

At its core, risk management in digital assets is a structured process: participants identify the key threats to their capital, analyze how likely those threats are and how severe their impact could be, assess which ones matter most, and then implement mitigation strategies such as diversification, hedging, limits, automation, or insurance. This same four-step loop now underpins the way banks, funds, and major protocols approach crypto, from Bitcoin markets on regulated venues to complex collateral systems in DeFi lending. As stablecoins, perpetual futures, cross‑chain bridges, and real‑world asset (RWA) tokens have proliferated, the risk surface has expanded from simple price volatility to include smart contract flaws, oracle failures, governance capture, and regulatory and compliance concerns. At the same time, new tools—onchain data feeds, protocol‑level risk engines, dependency graphs like YO’s Risk Graph, and verifiable analytics—have made it possible to model, monitor, and automate risk management in ways that are difficult in legacy finance. For a crypto news audience, understanding how these risk practices work, and how they are rapidly converging with institutional standards, is essential context for evaluating every new market, hack, or “risk-managed” product that comes along.

Foundations of Risk Management in Crypto

Defining Risk and Risk Management in Digital Assets

In finance, risk is generally defined as the combination of the probability that something adverse happens and the magnitude of the loss if it does. In crypto, that basic definition holds, but the list of adverse events is wider and often more severe: extreme price swings, protocol exploits, stablecoin depegs, chain reorganizations, and sudden regulatory shocks can all threaten capital. For investors and builders, risk management is therefore the discipline of systematically identifying, analyzing, assessing, and treating these threats, rather than simply hoping that markets go up. Properly understood, it is not about eliminating risk—impossible in an open, experimental ecosystem—but about making sure each unit of risk taken is intentional, sized, and compensated.

Formal risk management frameworks in crypto now mirror those used by banks and asset managers. The Financial Crime Academy, for example, describes a four-step process of risk identification, risk analysis, risk assessment, and treatment planning as the cornerstone for financial institutions that are adding cryptocurrencies to their portfolios. In this view, a trading firm or DeFi protocol starts by mapping out all relevant risk categories, from market volatility and liquidity risk to cybersecurity, operational, and regulatory exposure. It then conducts quantitative and qualitative analyses—scenario analysis, stress testing, and sensitivity analysis—to understand how different shocks would propagate through its positions or protocol. Next, it assigns relative scores or ratings to prioritize which risks are acceptable and which demand immediate mitigation. Finally, it designs and implements treatment plans that might involve portfolio diversification, hedging with derivatives, stricter collateral rules, or investment in better operational security.

For traders, especially those active in volatile instruments such as Bitcoin perpetual futures or altcoin liquidity pools, risk management often first shows up as “basic trading hygiene”: deciding how much of a portfolio to allocate to a single position, where to place stop-loss orders, how much leverage to use, and when to avoid trading entirely. Educational resources aimed at retail traders now consistently emphasize developing a risk plan before entering positions, using tools such as position sizing rules, maximum drawdown limits, and restricting leverage to levels appropriate for individual risk tolerance. These practices, while simple, are entry points into a much broader risk management mindset that also encompasses counterparty risk on centralized exchanges, custody risk in self‑hosted wallets, and smart contract risk in DeFi.

The distinction between risk and uncertainty is particularly important in crypto. Many traditional models assume that future returns will behave somewhat like past returns and that extreme events will be rare; in practice, digital asset markets routinely produce “fat‑tail” events that violate those assumptions. As a result, crypto risk management leans more heavily on scenario analysis (“What happens if this stablecoin depegs to 80 cents?”) and forward‑looking stress tests than on narrow statistical models that assume normality. This does not mean quantitative methods are useless; rather, they must be supplemented with qualitative judgment about technology, governance, and regulatory trajectories that are hard to capture in a single volatility number.

Traditional Finance Roots and Crypto Adaptation

Modern risk management frameworks did not originate in crypto; they evolved over decades in foreign exchange, fixed income, and derivatives markets, as banks, corporates, and regulators grappled with currency volatility, interest‑rate shocks, and credit crises. Workshops and training programs in the 1990s were already teaching treasury professionals to understand exposures, use hedging instruments, and apply techniques such as value‑at‑risk and stress testing to currency and interest‑rate positions. These foundations—classifying risk into market, credit, liquidity, and operational buckets, and then assigning capital and limits against each—remain the baseline for institutional thinking about risk today.

As banks and asset managers step into crypto, they are importing these frameworks and asking what needs to change. Research on institutional trading in digital assets notes that, while the asset class is novel, institutions expect the same kind of infrastructure and controls they rely on in other markets: robust custody arrangements, pre‑ and post‑trade risk checks, real‑time monitoring, and clear escalation paths for incidents. Chainalysis, for instance, has highlighted the importance of better infrastructure and risk management tools to make digital asset markets safer and more attractive for institutional traders. This includes both traditional elements, such as counterparty due diligence and anti‑money‑laundering controls, and crypto‑specific tools, such as onchain transaction screening and smart contract security assessments.

Within the crypto-native world, there has been a decade‑long trend toward converging on these traditional risk standards. Industry participants such as Centrifuge have observed that crypto risk management has spent years “closing the distance” to how banks actually run risk, and that this convergence is a precondition for institutional capital coming onchain at scale. That convergence can be seen in the emergence of DeFi risk guidelines, protocol‑specific risk frameworks, and the growing use of external risk providers that resemble rating agencies or risk consultancies. It is also evident in the adoption of concepts like underwriting, risk committees, and independent validation functions within DAOs and DeFi ecosystems, all of which are standard in banking.

At the same time, crypto has forced traditional risk frameworks to adapt. Unlike most traditional assets, crypto markets settle on public blockchains, operate without central clearinghouses, and rely heavily on open-source software and anonymous counterparties. This creates new risk categories that do not map neatly onto legacy buckets, such as smart contract vulnerabilities, oracle manipulation, bridge exploits, and governance capture via token voting. For institutions operating in this environment, risk management becomes a hybrid discipline, requiring both financial expertise and deep technical understanding of blockchain systems.

Core Risk Categories in Digital Assets

Although labels vary, most comprehensive crypto risk frameworks now converge on a similar set of core risk categories. For financial institutions, the Financial Crime Academy highlights market volatility, liquidity, cybersecurity, regulatory, and operational risks as key dimensions to consider when investing in cryptocurrencies. For DeFi protocols, the Enterprise Ethereum Alliance (EEA) DeFi Risk Assessment Guidelines expand this checklist to cover software and protocol design risks, governance structures, liquidity and tokenomics, external market linkages, and compliance with applicable regulatory and technical standards. Ratings agencies, risk DAOs, and tools like YO’s Risk Graph build on these categories when scoring protocols and pools.

Market risk remains the most visible category, driven by the high volatility and cyclicality of digital asset prices. Even large-cap assets like Bitcoin and Ether routinely experience double‑digit percentage moves over short timeframes, while smaller tokens can exhibit extreme “pump‑and‑dump” dynamics. For leveraged traders and collateralized lending protocols, these price moves translate directly into liquidation risk, forcing risk managers to pay close attention to volatility, correlations, and liquidity depth across trading venues. Liquidity risk, in turn, is critical because many tokens trade primarily on a handful of centralized exchanges or DeFi pools, where order‑book depth or pool size can collapse during stress, amplifying price impact for large trades.

Credit and counterparty risk also manifest in crypto, albeit in new forms. In centralized finance (CeFi), counterparty risk arises from holding assets on exchanges, lending to brokers, or engaging in over-the-counter (OTC) trades without central clearing. In DeFi, the analogous risks include smart contract risk for lending protocols, as well as exposure to liquidators, oracles, and stablecoin issuers whose failure or misbehavior could cascade through a protocol’s balance sheet. Operational risk covers failures in internal processes, key management, and human oversight, such as the misuse or compromise of private keys that control protocol admin functions or treasury assets.

Software and protocol risks are especially salient in DeFi. The EEA guidelines explicitly identify software errors, vulnerabilities in smart contracts, governance design flaws, and misaligned tokenomics as major sources of risk. These risks are compounded by the composable nature of DeFi: a lending protocol may rely on a price oracle, which in turn depends on multiple exchanges, while its collateral could be liquidity provider tokens from another protocol, themselves backed by a mix of volatile and stable assets. Governance risk encompasses the possibility that tokenholders or delegated DAOs make decisions that compromise protocol safety, such as approving risky collateral, raising leverage limits too aggressively, or cutting funding for security and risk teams.

To anchor these categories, it can be useful to summarize them in a simple comparative table:

| Risk Type | Description | Example in Crypto Markets |

|---|---|---|

| Market risk | Losses from adverse price moves and volatility | BTC price crash triggering mass liquidations on perps exchanges |

| Liquidity risk | Inability to trade without large price impact | Thin weekend liquidity amplifying a sell‑off in a DeFi pool |

| Smart contract risk | Bugs, exploits, or flawed logic in code | Vulnerability in a lending protocol enabling bad‑debt creation |

| Governance and tokenomics | Misaligned incentives or hostile governance actions | Tokenholders voting to dilute safety modules for short-term gains |

| Operational and key risk | Failures in processes, key management, or security | Compromised admin key minting unbacked tokens |

| Regulatory and compliance | Legal crackdowns or sanctions affecting operations | Exchange forced to delist a major asset following enforcement |

This table is not exhaustive, but it illustrates the breadth of the risk surface that must be considered in modern crypto risk management frameworks.

Ethena launches a dedicated lending market on Jupiter Lend, with Bitwise overseeing risk management and institutional participation on Solana

30m/hour Stargate bridge capacity gives this launch a hard throttle, so the first thing to watch is whether USDe loops actually fill or just farm promo APY. Bitwise curating an isolated market gives funds a named risk desk to underwrite, but USDe basis/funding risk still lives underneath the collateral. If Solana can absorb synthetic-dollar leverage without ugly depeg/liquidation wicks, Jup Lend starts looking less like another yield UI and more like a credit venue.

Readers click risk management stories not for frameworks or theory, but for moments when a named protocol's risk controls visibly failed or were stress-tested under live market conditions — with real money, named actors, and immediate consequences.↗

What Makes Crypto Risk Different?

24/7 Markets and Thin Liquidity Windows

One of the most distinctive features of crypto markets is that they trade continuously, without weekends, holidays, or fixed sessions. This always‑on structure fundamentally changes how risk must be managed, especially compared with equities or even many FX markets where liquidity is concentrated in business hours. Coverage of 24/7 crypto trading has highlighted how traditional risk safeguards, calibrated for daytime trading, can fail when liquidity thins out during nights and weekends. For example, risk systems that assume stable liquidity may underestimate how quickly prices can gap when fewer market makers are active, leaving leveraged traders and protocols exposed to outsized slippage and cascading liquidations.

Weekend and overnight risk is especially pronounced for retail traders who keep positions open around the clock but may not be watching markets continuously. Reports note that 24/7 crypto trading has shifted risk toward periods of thin liquidity, with experts warning that old safeguards—like margin calls timed to business hours—no longer capture the true exposure of always‑on positions. In this environment, traders and protocols alike have to adjust: margining systems must account for intraday and overnight volatility, liquidation mechanisms must be robust under stress, and monitoring systems must be automated rather than dependent on human oversight during office hours.

Decentralized perpetuals exchanges and onchain lending protocols are particularly exposed to these dynamics. A platform like Hyperliquid, which offers high‑leverage perpetual futures on a wide range of crypto assets, must handle real‑time funding rate adjustments, continuous mark‑to‑market, and automated margin calls 24/7. While such platforms can design liquidation bots and insurance funds to absorb some shocks, extreme moves during illiquid windows can still strain their models. For DeFi lending markets, thin liquidity on underlying spot markets can make price oracles less reliable, increasing the risk of manipulation or inaccurate pricing, especially for long‑tail assets with limited trading venues.

From a risk management perspective, 24/7 markets demand both better data and more conservative assumptions. Historical volatility and liquidity patterns need to be analyzed on an intraday basis, with particular attention to the tails of the distribution during weekends or regional holidays. Stress tests should explicitly model scenarios where key market makers withdraw, order‑book depth evaporates, or DeFi pools see large single‑sided withdrawals, and then assess whether leverage limits, liquidation discounts, and insurance mechanisms remain adequate. Human risk committees, whether in centralized exchanges or DAOs, must recognize that manual interventions will often be too slow; the bulk of risk response must be encoded in automated, transparent rules.

Onchain Transparency, Composability, and Dependency Graphs

Another hallmark of crypto is the availability of granular, real‑time onchain data. Every token transfer, swap, loan, and liquidation on public chains is recorded on a shared ledger that anyone can inspect. This transparency is a double‑edged sword for risk management. On the one hand, it allows sophisticated participants to monitor protocol health, collateral composition, and even individual whale positions far more closely than is possible in opaque traditional markets. On the other hand, it enables highly complex composability, where protocols and products are built on top of each other in intricate dependency chains that can transmit shocks rapidly across the ecosystem.

The EEA DeFi Risk Assessment Guidelines explicitly emphasize that DeFi protocols must understand not only their own code and parameters but also their dependencies on other protocols, tokens, and external services. For example, a lending protocol that accepts liquidity provider (LP) tokens as collateral is implicitly exposed to the underlying assets in the LP pool, the router contracts that manage swaps, and the oracles that price those assets. If any component fails or is exploited, the lending protocol may incur bad debt or systemic losses. Without a clear map of these dependencies, risk managers can easily overlook critical pathways of contagion.

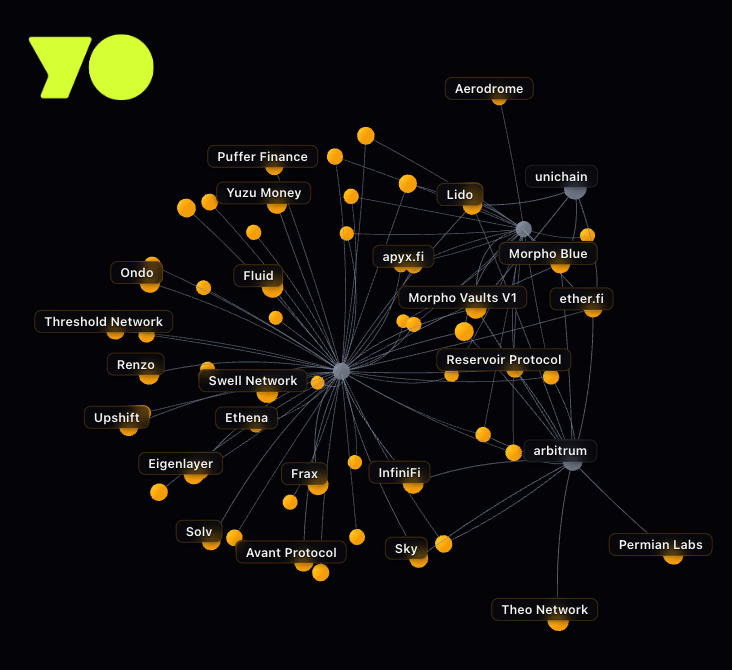

To tackle this complexity, some projects are modeling DeFi as a graph of dependencies. A general description of dependency graphs in financial services characterizes them as tools for managing complicated chains of calculations, clarifying how changes in one data point propagate through models, and enabling efficient recalculation and drill‑downs. This concept has been applied to DeFi by systems like YO’s Risk Graph, which maps pools, assets, protocols, and chains as nodes in a dependency graph and grades each from A to F based on how risk propagates through the stack. By answering questions such as “Which pools have direct exposure to this asset?” or “Which protocols are systemically important for this stablecoin?”, these graphs provide a high‑level view of interconnected risk that is difficult to obtain from individual dashboards.

Onchain transparency also makes it possible to monitor behavioral patterns that may signal elevated risk, such as repeated interactions with known exploit addresses or unusually concentrated holdings of governance tokens. The EEA guidelines encourage projects to provide the documentation and data necessary for investors and third‑party analysts to perform their own risk assessments, including detailed descriptions of external dependencies and monitoring practices. Over time, the combination of open data, dependency graphs, and standardized reporting may bring DeFi risk management closer to the kind of ecosystem‑wide stress testing and systemic risk analysis that regulators perform in traditional banking systems.

Code Risk, Smart Contracts, and DeFi Hacks

Unlike traditional financial instruments, many crypto products are implemented directly in software that both executes economic logic and holds user funds. This introduces a category of risk that is uniquely central in DeFi: smart contract risk. When the code that governs asset custody, collateralization, or trading contains a bug or design flaw, attackers can exploit it to drain funds or create unauthorized assets. Recent analyses by S&P Global have underscored how a series of DeFi hacks highlight the importance of robust operational security and risk management to defend against bad actors. These incidents demonstrate that even well‑known protocols can suffer devastating losses if they underestimate software risk or fail to implement rigorous controls.

The EEA DeFi Risk Assessment Guidelines catalog a broad set of software and operational risks. These include vulnerabilities in contract logic, inadequate input validation, reentrancy issues, faulty upgrade mechanisms, insecure admin key management, and failures in deployment or configuration. Governance-related code, such as voting modules and timelocks, also presents risk if it can be bypassed or manipulated. Because DeFi contracts are typically immutable once deployed, or only upgradable through tightly controlled processes, risk managers must pay close attention to pre‑deployment audits, formal verification, and battle‑testing on testnets or with limited funds. Post‑deployment, continuous monitoring and prompt response plans for potential vulnerabilities become essential.

DeFi hacks often blend smart contract risk with other risk categories. For example, an exploit might involve manipulating a low‑liquidity asset’s price on a DEX to trick an oracle, then triggering a lending protocol’s liquidation logic under false assumptions. This combines oracle risk, liquidity risk, and software risk into a single incident. S&P’s commentary notes that such multi‑vector attacks underscore the need for robust risk management frameworks that go beyond code audits to include operational controls, multisignature key management, and clear incident response procedures. In practice, many protocols now complement external audits with bug bounty programs, internal security teams, and third‑party continuous monitoring services.

Despite these efforts, the frequency and scale of DeFi exploits remain high enough to shape institutional perceptions of the sector’s riskiness. This has, in turn, accelerated the development of standardized frameworks and guidelines aimed at reducing the attack surface and improving resilience. Initiatives like the EEA’s guidelines, as well as protocol‑specific risk frameworks and specialist risk providers, can be understood as ecosystem responses to the hard lessons of past hacks. For investors and users, scrutinizing how a given project addresses code and operational risk—through design choices, audits, and governance—is a critical part of any risk assessment.

Stablecoins and Systemic Liquidity Risk

Stablecoins occupy a special place in the crypto risk landscape because they function as the primary medium of exchange, unit of account, and base collateral in much of the ecosystem. The Depository Trust & Clearing Corporation (DTCC) has described stablecoins as a “cornerstone” of the digital asset ecosystem, noting that they bridge traditional finance and blockchain‑based transactions and are increasingly intertwined with institutional products like tokenized money market funds and government securities. When stablecoins function well, they provide predictable liquidity and pricing; when they fail, the consequences can be systemic, affecting exchanges, DeFi protocols, and users simultaneously.

Risk management for stablecoins must address both asset‑side and liability‑side vulnerabilities. On the asset side, reserve management and transparency are paramount: fiat‑backed stablecoins must hold high‑quality, liquid assets to honor redemptions, while algorithmic or crypto‑collateralized designs must maintain sufficient overcollateralization and robust liquidation mechanisms. DTCC’s analysis emphasizes how institutional stablecoins and tokenized funds are reshaping liquidity dynamics in capital markets, implying that the quality and governance of backing assets are critical to broader financial stability as tokenization grows. On the liability side, stablecoin issuers face regulatory, operational, and reputational risks that can trigger runs if users lose confidence.

In DeFi, stablecoin risk is magnified by the extent to which stablecoins serve as collateral and settlement assets. Lending protocols, derivatives platforms, and automated market makers often use one or two dominant stablecoins as base assets for pools, collateral for credit lines, and units for accounting and yield calculations. If a major stablecoin depegs or faces regulatory enforcement, the resulting losses and liquidity crunch can propagate through multiple layers of the stack. This is why many risk frameworks treat stablecoin issuer risk and peg stability as core inputs when determining collateral factors or concentration limits for lending and leveraged products. Observers note that, despite numerous algorithmic and yield‑bearing stablecoin experiments, the largest fiat‑backed stablecoins continue to command the lion’s share of liquidity, reflecting a collective preference for perceived safety.

As institutional players and market infrastructures such as DTCC explore tokenized cash and securities, stablecoin risk management is becoming a mainstream topic for regulators and traditional risk committees. For crypto‑native users and builders, understanding the design, governance, and regulatory posture of each stablecoin they rely on is a non‑negotiable part of risk management. Diversifying stablecoin exposure, imposing conservative collateral factors, and stress‑testing protocols for stablecoin shocks are all being incorporated into contemporary DeFi risk practices.

The Risk Management Lifecycle for Crypto Participants

Step 1: Identifying Risks

Every robust risk program begins with a thorough inventory of the risks faced by an institution, protocol, or individual trader. In the context of cryptocurrencies, the Financial Crime Academy emphasizes that risk identification should encompass market volatility, liquidity risk, cybersecurity risk, regulatory risk, and operational risk, among others. This stage is not about quantifying probabilities or severities yet; it is about “leaving no stone unturned” in mapping all potential threats, regardless of how likely they may initially seem. For a centralized exchange, this might include custody arrangements, internal control failures, and legal jurisdiction risk. For a DeFi protocol, it extends to smart contract vulnerabilities, governance mechanisms, oracle dependencies, and counterparty risk via integrated protocols.

In practice, institutions use tools such as risk checklists, risk registers, and structured workshops to facilitate this identification process. A risk checklist for a DeFi lending protocol, for example, may include items related to collateral types, liquidation mechanisms, oracle sources, admin key governance, external integrations, and third‑party service providers. Each identified risk is then captured in a risk register that documents its nature, potential impact, existing controls, and owners responsible for monitoring it. This documentation not only creates a shared understanding within the team but also supports transparency for investors and regulators, aligning with EEA guidance that projects should provide ample data and documentation to support external risk assessments.

For individual traders, risk identification is often less formal but no less important. Educational resources emphasize that traders should identify their primary exposures before trading: asset‑specific risk, leverage risk, counterparty risk at the exchange or protocol, and even personal operational risk such as insecure key storage or poor password practices. A Bitcoin spot holder on a regulated exchange has a different risk profile from a DeFi user who is providing liquidity to volatile token pairs or looping collateral to leverage fixed‑yield positions. Recognizing these differences is the first step toward tailoring appropriate risk controls.

Risk identification is not a one‑time exercise, especially in an ecosystem as dynamic as crypto. New protocols launch, governance decisions change parameters, regulatory landscapes shift, and previously unknown vulnerabilities come to light. Mature risk programs incorporate periodic reviews and triggers—such as onboarding a new asset, integrating a new protocol, or entering a new jurisdiction—that automatically prompt fresh risk identification exercises. This ongoing vigilance is particularly important in DeFi, where composability means that adding one new dependency can introduce multiple hidden risks downstream.

Step 2: Analyzing and Quantifying Risk

Once risks are identified, the next step is to analyze them in greater depth, estimating both their likelihood and potential impact. The Financial Crime Academy notes that institutions can apply both quantitative and qualitative techniques at this stage, including scenario analysis, stress testing, and sensitivity analysis. For market risk, this may involve calculating historical volatility, correlations, and drawdowns for relevant assets, then modelling how a given portfolio would have behaved in past crises or hypothetical shock scenarios. For operational and cybersecurity risk, qualitative assessments of control strength, process maturity, and exposure to specific threat vectors may be more appropriate.

Scenario analysis is particularly important in crypto because historical data may not capture future tail events adequately. Risk managers might simulate a 50% intraday crash in Bitcoin, a sudden 30% drawdown in a major collateral token, or a temporary depeg of a key stablecoin, then assess the impact on collateralized positions, liquidity pools, and protocol solvency. Stress tests can also consider multi‑factor events, such as simultaneous price shocks and liquidity withdrawals or oracle outages. Sensitivity analysis, meanwhile, examines how changes in parameters like haircuts, collateral factors, liquidation penalties, or funding rates affect overall risk, helping protocol designers choose more conservative settings where appropriate.

For traders, Changelly’s educational material suggests practical risk analysis techniques such as backtesting strategies on historical data, calculating maximum drawdowns, and using realized volatility to calibrate position sizes and stop‑loss levels. While these methods may lack the sophistication of institutional models, they are valuable for aligning trading behavior with individual risk tolerance and preventing catastrophic losses. Retail traders can also analyze exchange‑specific risk factors—such as custody arrangements, insurance policies, and jurisdictional protections—to decide where to hold funds and how much to leave on centralized platforms versus self‑custody.

Onchain analytics and dependency graphs add another dimension to risk analysis. By mapping protocols as nodes in a graph and tracing asset flows, analysts can estimate how an adverse event—such as a hack, depeg, or chain halt—would propagate through DeFi. YO’s Risk Graph, for example, grades pools, assets, protocols, and chains based on their exposure and systemic importance, allowing users to see not just the direct risk of a given position but also its indirect risk via upstream dependencies. This kind of network‑level analysis complements traditional portfolio risk measures by incorporating composability and interdependence, which are defining features of DeFi.

Step 3: Assessing and Prioritizing Risks

Risk assessment and prioritization translate analysis into action by ranking risks according to their significance. The Financial Crime Academy describes this phase as assigning a risk score to each identified risk based on its likelihood and potential impact, often using tools such as likelihood–impact matrices or risk heat maps. In a heat map, risks with both high probability and high impact are flagged as critical, demanding immediate mitigation or avoidance, while those with low probability and low impact may be accepted or monitored with minimal intervention. This structured approach helps ensure that limited risk management resources are allocated efficiently.

In DeFi, assessment often takes the form of ratings and categorizations that are understandable to governance participants and users. EEA’s guidelines encourage the development of clear, documented criteria for judging risks in areas like software quality, governance robustness, liquidity depth, token distribution, and compliance posture. These criteria can then be used to assign scores or labels—for example, rating a protocol’s governance as “centralized” if a small multisig can change core parameters without delay, or labeling liquidity as “thin” if volume and depth fall below established thresholds. Such standardized assessments make it easier to compare protocols and to set consistent collateral or exposure limits.

External risk scorers and tools bring additional perspectives. YO’s Risk Graph assigns grades from A to F to pools, assets, protocols, and chains based on propagated risk across the full stack. A DeFi protocol heavily dependent on a lightly traded collateral asset or a single cross‑chain bridge might receive a lower grade, signaling higher systemic risk. Similarly, services like LlamaRisk and other risk DAOs produce detailed risk reports, often culminating in parameter recommendations or warnings that governance forums can act upon. These assessments function much like credit ratings or analyst reports in traditional finance, shaping community and institutional perceptions of risk.

Prioritization is especially important because not all risks can be mitigated at once, and some risks are inherent to the business model. For example, a perps exchange must take on certain market and liquidity risks to offer leveraged products, but it can choose to prioritize mitigating oracle and smart contract risks by using battle-tested components and rigorous audits. A lending protocol may accept the risk of volatile collateral but prioritize strict limits on concentration and leverage. Clear articulation of risk appetite—the level and types of risk an entity is willing to bear—helps align these prioritization decisions with strategy and governance.

Step 4: Treatment, Hedging, and Continuous Monitoring

The final step in the risk management cycle is to decide what to do about prioritized risks. The Financial Crime Academy outlines four primary treatment strategies: risk avoidance, risk reduction, risk transfer, and risk acceptance. Risk avoidance involves discontinuing activities that are too risky relative to potential reward, such as delisting a thinly traded token or declining to integrate an unaudited protocol. Risk reduction seeks to lower the probability or impact of adverse events through controls, such as imposing stricter margin requirements, implementing multi‑sig governance, or diversifying collateral. Risk transfer typically involves shifting risk to another party, for example by purchasing insurance or hedging with derivatives. Risk acceptance acknowledges that some risks are inherent and must be borne, albeit consciously and within defined limits.

In crypto markets, hedging and transfer mechanisms are rapidly evolving. Centralized venues and traditional derivatives exchanges increasingly offer instruments designed specifically for digital assets, such as futures, options, and soon even bitcoin volatility futures. These products enable miners, funds, and other large holders to hedge price and volatility exposure more precisely, aligning crypto risk management with established practices in commodities and FX. On the DeFi side, protocols provide onchain options, structured products, and volatility vaults that can be used to offset specific risks, though these instruments themselves introduce smart contract and counterparty risks that must be managed.

Risk treatment in DeFi also encompasses parameter setting and governance. Lending platforms like Aave use risk frameworks to determine collateral factors, liquidation thresholds, borrow caps, and reserve factors for each listed asset, explicitly balancing growth opportunities against the potential for bad debt and cascading liquidations. Proposed frameworks for Aave V3, V4, and Horizon create standards for how each asset is evaluated and re‑assessed quarterly, with asset‑specific settings that reflect characteristics such as volatility, liquidity, and technical risk. Recent efforts to expand Aave’s framework to include asset, bridge, and chain risk, along with automated monitoring, illustrate how protocol risk treatment is becoming multi‑dimensional and increasingly automated.

Continuous monitoring closes the loop and feeds back into new rounds of identification and analysis. In 24/7 markets, monitoring cannot be a manual process limited to business hours; automated systems must track key risk indicators such as collateral ratios, liquidity utilization, oracle deviations, and unusual onchain flows in real time. When thresholds are breached, protocols may trigger automatic responses (such as pausing markets or adjusting parameters) or alert human operators to intervene. As risk engines and AI‑driven analytics improve, the boundary between monitoring and treatment will blur further, with systems that dynamically adjust risk parameters based on evolving market and onchain conditions.

- 01Hyperliquid liquidation crisis↗

A single trader exploiting thin liquidity forced Hyperliquid's insurance fund (HLP) to absorb losses and publicly revise risk parameters, making the exchange's backstop mechanisms a live test rather than a theoretical safeguard.

- 02Institutional forensics partnerships↗

Fidelity and EY collaborating on blockchain analytics signaled that traditional finance is treating on-chain risk management as an infrastructure problem, not a compliance checkbox.

- 03Protocol-level risk advisory market↗

Gauntlet, Chaos Labs, and LlamaRisk competing for and losing DeFi risk mandates revealed that risk management is now a contested, high-stakes service layer with governance politics attached.

- 04Resolv hack and DeFi hull breaches↗

A $23m exploit on a delta-neutral protocol that explicitly marketed institutional-grade risk management exposed the gap between audited frameworks and runtime resilience.

- 05Leverage and margin parameter changes↗

Hyperliquid's post-incident 20% margin ratio requirement and ETH/BTC parameter adjustments showed readers how retail-accessible leverage directly shapes systemic risk at the exchange level.

- 06On-chain dependency graph scoring↗

Tools like YO's Risk Graph modeling DeFi pools A-to-F by propagated risk attracted readers seeking programmatic, composability-aware risk signals rather than static audits.

DeFi, Protocol-Level Risk, and Emerging Frameworks

The EEA DeFi Risk Assessment Guidelines

To bring order to the expanding universe of DeFi risk, industry bodies have started to codify best practices. The Enterprise Ethereum Alliance (EEA) has released DeFi Risk Assessment Guidelines that offer a broad‑based, industry‑backed guide to the risks involved in working with DeFi and how to assess, manage, account for, and mitigate them. This pioneering document compiles a wide range of risk types relevant to DeFi protocols, including software and smart contract risk, governance and organizational risk, liquidity and tokenomics, external market and ecosystem risk, and regulatory and standards compliance. Its aim is to help both projects and investors speak a common language about risk and to set expectations for documentation and transparency.

The guidelines go beyond simply listing risks; they also specify the documentation and data that projects should make available to support rigorous risk assessment. This includes detailed technical documentation, architecture diagrams, descriptions of governance models and decision‑making processes, audit reports, bug bounty programs, and quantitative data on liquidity, usage, and historical performance. By providing this information, projects enable investors, regulators, and third‑party analysts to evaluate both the design of the protocol and the effectiveness of its risk mitigations. This aligns with the broader trend toward institutionalizing DeFi risk management and making it more compatible with traditional risk frameworks.

A key contribution of the EEA guidelines is their emphasis on governance and tokenomics as integral components of risk. While smart contract audits focus on code correctness, governance structures determine how quickly and safely parameters can be adjusted, how upgrades are deployed, and how conflicts of interest are managed. Token distribution, voting mechanisms, and the presence or absence of safeguards like timelocks and emergency pause functions all influence the resilience of a protocol. The guidelines encourage projects to be explicit about these design choices and to justify them in terms of risk and incentive alignment.

Finally, the EEA guidelines serve as a bridge between DeFi and regulatory concerns. By explicitly addressing regulatory and standards compliance, they acknowledge that DeFi protocols operate within broader legal and policy environments that can introduce their own risks. For example, protocols that facilitate lending or derivatives may be subject to securities or commodities regulation in some jurisdictions, while those that fail to prevent sanctioned entities from using their services may face enforcement or deplatforming risk. Incorporating these considerations into risk assessment frameworks helps protocols anticipate and mitigate legal and regulatory shocks.

Aave’s Multi-Dimensional Risk Framework

Aave, one of the largest DeFi lending protocols, offers a concrete example of how sophisticated risk frameworks are being embedded at the protocol level. Over the past several months, the Aave community has been developing a new risk framework that explicitly covers asset risk, bridge risk, and chain risk, along with monitoring and automation components designed to manage these dimensions in a unified way. This framework aims to set a standardized benchmark for how every asset is evaluated across Aave V3, the forthcoming V4, and Aave Horizon, covering both initial onboarding and ongoing risk management.

According to governance proposals, the Aave Risk Framework is intended to be binding at key decision points. When a new asset is proposed for listing, it must be evaluated under this framework, which integrates measures of volatility, liquidity, technical and smart contract risk, oracle reliability, and composability with other DeFi protocols. Once listed, assets are subject to periodic re‑assessment, typically on a quarterly cadence, allowing risk parameters such as loan‑to‑value ratios, liquidation thresholds, and caps to be adjusted in response to changing market conditions or new information. By formalizing these processes, Aave moves away from ad hoc risk decisions and toward a more predictable, transparent risk governance structure.

The inclusion of bridge and chain risk reflects the growing complexity of multi‑chain DeFi. As Aave deploys on multiple networks and accepts assets bridged from other chains, it must consider not only the risk of the asset itself but also the reliability and security of the bridging mechanisms and the underlying chains. A failure in a cross‑chain bridge could render bridged collateral worthless on the destination chain, while a consensus failure or censorship event on a smaller chain could undermine the integrity of transactions and positions there. The new framework seeks to encapsulate these systemic risks and assign them appropriate weight in asset listings and parameter choices.

Aave’s risk management story also illustrates the human and organizational side of DeFi risk. The protocol has relied on external risk providers such as Chaos Labs, which recently announced its exit from Aave’s risk management engagement, citing differences in risk management philosophy and noting contributor departures and governance turbulence within the DAO. These developments, along with debates around Aave V4’s design and risk implications, highlight that risk management is not just about models and parameters but also about aligning community incentives, ensuring adequate funding for risk work, and managing governance disputes. The evolving risk framework can be seen as part of a broader effort to institutionalize risk within a decentralized ecosystem.

Protocol Underwriting: Lending Markets from Aave to Jupiter Lend

The concept of underwriting—systematically evaluating and pricing risk before taking exposure—is increasingly visible in DeFi lending. While early protocols adopted relatively simple, overcollateralized models, modern designs often feature asset‑specific and market‑specific underwriting that resembles traditional credit analysis. The Ethena lending market on Jupiter Lend, with Bitwise overseeing risk management and institutional participation, provides an example of this trend. In this setup, Ethena’s USDe product has a dedicated lending market on Jupiter Lend that is isolated from the broader liquidity layer, with parameters and risk controls specifically tailored for institutional capital.

This isolated market design serves several risk management goals. First, by segregating USDe lending from other Jupiter markets, it reduces contagion risk: issues with USDe or its backing do not automatically spill over into unrelated pools. Second, by partnering with a specialist manager like Bitwise, the platform leverages external expertise in assessing asset quality, liquidity, and counterparty risk, aligning with how traditional financial institutions delegate certain risk functions to specialist units or partners. Third, the institutional orientation of the market influences everything from collateral factors to monitoring routines, aiming to meet the expectations of professional investors and risk committees.

More experimental DeFi credit systems push underwriting further. Protocols that offer undercollateralized or partially collateralized loans, structured credit tranches, or fixed‑yield products must gather detailed information about borrowers, assets, and market conditions, and then encode underwriting criteria into smart contracts and governance processes. Looping strategies—such as those involved in Solstice PT looping, where users deposit PT‑USX as collateral inside a protocol like Loopscale, borrow against it, and re‑enter positions to amplify fixed yield—highlight the need for strict risk management, including conservative collateral factors, real‑time monitoring, and clear liquidation rules. Without disciplined underwriting, such strategies can quickly become unstable under stress.

These developments illustrate how DeFi is beginning to replicate, and in some cases improve upon, traditional underwriting practices. By combining onchain transparency, programmable collateral rules, and external risk expertise, protocols can create credit markets that are more modular and auditable than opaque, off‑balance‑sheet arrangements in legacy finance. At the same time, they inherit and expand the range of risks that must be managed, making robust risk frameworks and governance all the more essential.

Risk Oracles, Risk Graphs, and Data Infrastructure

Effective risk management depends on high‑quality data and robust analytics. In DeFi, this has given rise to a growing ecosystem of risk oracles, analytics platforms, and dependency graph tools. As noted earlier, YO’s Risk Graph models DeFi protocols as a dependency graph, answering questions such as which pools have direct exposure to a given asset and which protocols are systemically important. This approach leverages the concept of dependency graphs from financial services more broadly, where they are used to clarify calculation flows, analyze dependencies, and efficiently recalculate values when inputs change. In DeFi, such graphs support tasks like tracing exposure to a risky collateral token, modeling the impact of a potential hack, or identifying chokepoints where failure could propagate widely.

Beyond dependency graphs, price and risk oracles play a central role in quantifying and transmitting risk signals. Modern investors increasingly demand high‑fidelity, multi‑asset pricing layers built specifically for 24/7 risk management, product expansion, and institutional scale. New oracle products such as Pyth Pro X aim to provide this kind of granular, low‑latency data across chains, enabling more accurate mark‑to‑market, funding calculations, and collateral assessments. Similarly, Chainlink’s Cross‑Chain Interoperability Protocol (CCIP) has been positioned as a cross‑chain security solution that incorporates a dedicated risk management layer, multi‑network decentralization, and separate codebases to avoid single points of failure in cross‑chain messaging. These developments illustrate how data providers themselves are embedding risk management into their architectures.

Data infrastructure for risk is also evolving along the dimension of verifiability. Space and Time, for example, has introduced zero‑knowledge (ZK) proven historical data queries that allow smart contracts to verify time‑based and behavioral computations onchain without adding trust or centralization assumptions. This means a protocol could, in principle, base its risk decisions on complex offchain analytics—such as a borrower’s long‑term DeFi behavior or a market’s historical volatility profile—while still being able to verify the correctness of those computations through cryptographic proofs. Such capabilities could unlock more sophisticated lending, derivatives, and risk management designs that go beyond simple, static parameters.

As these tools mature, risk management in DeFi is becoming increasingly data‑driven and automated. However, data quality, model risk, and reliance on external providers introduce their own risks, which must be incorporated into overall risk frameworks. Projects and investors must assess not only the technical reliability and decentralization of oracles and analytics providers but also their economic incentives, governance, and resilience to regulatory pressure or operational failure.

Chainlink CEO, Sergey Nazarov on why Chainlink CCIP leads cross-chain security, citing multi-network decentralization, risk management layer, and separate codebases preventing single points of failure

Chainlink's separate-codebase pitch matches the actual bridge post-mortems: Wormhole's $325M hack was a single signature bug, Nomad's $190M drain was an empty merkle root, Ronin's $600M was 5-of-9 multisig keys. CCIP's Active Risk Management Network works as a kill switch, trading decentralization for safety — LayerZero's ULN model takes the opposite bet. Yet CCIP handles a fraction of LayerZero's volume. Shippers pick latency and UX over extra security layers.

Learning from Hacks and Incidents

The Resolv $23 Million Hack and Key Management Failures

High‑profile hacks and exploits are among the most visible manifestations of risk in crypto, and each incident offers lessons for improving risk management. The Resolv hack, analyzed in detail by Chainalysis, is a case in point. In that incident, a single compromised private key allowed an attacker to mint approximately $23 million worth of tokens, effectively “printing” assets that were not backed by underlying reserves. The attacker then laundered funds through DeFi protocols, turning what was essentially an internal control failure into a broader market event.

Chainalysis’s review of the incident emphasizes that the root cause was not an obscure smart contract bug but poor key management and governance. A single key had the authority to mint large quantities of tokens, creating a classic single point of failure. From a risk management perspective, this is a textbook violation of operational security principles, which call for segregation of duties, multi‑signature controls, and robust access management for critical functions. If minting authority had been distributed across multiple keys controlled by independent parties, and if mints were subject to timelocks or onchain governance votes, the attack vector would have been much harder to exploit.

S&P Global’s broader commentary on DeFi hacks highlights how incidents like the Resolv exploit underscore the importance of operational security and risk management to defend against bad actors. It notes that, regardless of how innovative a protocol’s economic design may be, weak operational controls can bring it down. This includes not only key management but also processes for deploying and upgrading contracts, handling emergencies, and communicating transparently with users during incidents. In Resolv’s case, the hack also exposed the limitations of post‑facto responses: once funds were minted and moved through liquidity pools, recovery options became limited.

The key lessons from Resolv for risk management are therefore multi‑layered. Projects must design their admin and minting functions with the assumption that any single key can be compromised, employing multi‑sig wallets, hardware security modules, and strict operational procedures. They must also consider limiting the scope of what any one contract or key can do, using modular architectures and caps. Finally, they should plan for incident response in advance, including monitoring for unusual activity patterns, engaging forensic partners quickly, and having clear communication templates for users and partners. These measures do not eliminate the possibility of hacks but can greatly reduce both their likelihood and their impact.

Operationalizing Risk at Curve with LlamaRisk

Curve Finance, a major DeFi protocol focused on stablecoin and pegged-asset liquidity, offers a different lens on risk: the role of specialized risk providers embedded in protocol governance. LlamaRisk, a risk and research group, has been working with Curve to assess and manage risks related to liquidity pools, collateral choices, and the growth of its native stablecoin, crvUSD. In a recent governance proposal, LlamaRisk sought to renew its partnership with Curve for an annual engagement spanning April 2026–2027, highlighting the significant risk management work undertaken in the preceding year.

According to the proposal, LlamaRisk’s services include a range of activities central to protocol‑level risk management. These involve analyzing the risk profiles of new and existing pools, evaluating collateral options for crvUSD, conducting stress tests and scenario analyses, monitoring onchain metrics such as utilization and liquidation events, and providing parameter recommendations to mitigate identified risks. The group also contributes research and educational materials to help the Curve community understand complex risk topics, aligning governance debates with informed, data‑driven analysis.

The Curve–LlamaRisk relationship illustrates how DeFi protocols are increasingly institutionalizing risk functions. Instead of relying solely on ad hoc community discussions, protocols are commissioning dedicated teams with expertise in both financial modeling and smart contract systems to perform systematic risk analysis. These teams often operate semi‑independently, providing their findings to DAOs, which then deliberate and vote on parameter changes or new listings. This structure resembles the relationship between traditional banks and their internal risk departments or external consultants, adapted to an onchain, transparent governance model.

From a broader perspective, LlamaRisk’s work underscores the EEA guidelines’ emphasis on documentation, data, and independent risk assessment. By producing written reports, parameter proposals, and public dashboards, risk providers contribute to the transparency and accountability of DeFi protocols. For users and investors, the presence of a credible risk partner is increasingly seen as a positive signal, much like multiple independent audits or robust bug bounty programs. However, as Aave’s experience with risk provider turnover shows, aligning incentives, scope, and risk philosophy between DAOs and their risk partners remains a complex governance challenge.

Address- and Identity-Based Controls in DeFi

While DeFi aims for permissionless access, risk management and regulatory realities are pushing some protocols to implement address‑based controls and other security measures. Aggregators such as 1inch, for instance, have introduced features to block interactions with high‑risk addresses, including those associated with known hacks, sanctions lists, or suspicious activity patterns, as part of a broader set of “risk management sails” guiding users toward safer DeFi routes. These controls aim to protect users from inadvertently transacting with exploiters or sanctioned entities, while also reducing legal and reputational risk for the protocols themselves.

The EEA DeFi Risk Assessment Guidelines highlight regulatory and standards compliance as key risk categories for protocols, making it clear that ignoring sanctions, anti‑money‑laundering requirements, or consumer protection laws can create material risks. Implementing address‑based controls is one way protocols can mitigate these risks, though it raises debates about censorship, decentralization, and the boundaries of permissionlessness. S&P Global’s commentary on DeFi hacks notes that many exploits are carried out by repeat offenders whose addresses are well‑known to the community, suggesting that some degree of transaction filtering can reduce the incidence or impact of attacks without fully compromising openness.

For risk managers, the challenge is to design controls that are effective, transparent, and as minimally invasive as possible. This may involve using community‑maintained lists of high‑risk addresses, integrating with chain‑analysis providers, and offering users clear warnings and opt‑outs. Protocols must also consider how these controls are governed: who decides which addresses are blocked, how appeals are handled, and how errors are corrected. By treating address‑based controls not as arbitrary blacklists but as structured risk mitigations governed by clear policies, DeFi can balance risk reduction with its foundational values.

Blockchain forensics and risk firm enter Fintech 50 top 3

Hyperliquid $JELLY forced liquidation; HLP absorbs loss

Hyperliquid raises ETH/BTC margin ratio to 20% post-incident

Curve DAO extends LlamaRisk partnership through April 2027

Jupiter Lend onboards Bitwise for Ethena market risk curation on Solana

Resolv $23m hack highlights delta-neutral protocol risk gaps

Fidelity Digital Assets partners with EY for blockchain analytics

Chaos Labs exits Aave risk management mandate citing governance misalignment

Institutional Adoption and the Convergence of Standards

How Banks, Brokers, and Asset Managers Think About Crypto Risk

Institutional interest in digital assets has grown alongside improvements in risk management standards and infrastructure. The Financial Crime Academy explicitly notes that investing in cryptocurrencies involves inherent risks that necessitate careful identification and management by financial institutions, stressing the need for a structured risk management process when adding crypto exposures to portfolios. For banks, brokers, and asset managers, this process extends existing risk governance frameworks to a new asset class, incorporating crypto into firm‑wide market, credit, liquidity, and operational risk dashboards.

Chainalysis has documented the convergence of crypto and institutional trading, emphasizing that institutional adoption depends on better infrastructure and risk management tools tailored to digital assets. This includes regulated custody solutions, transparent market data, robust compliance and anti‑money‑laundering controls, and integration of onchain analytics into traditional risk systems. Institutions are seeking to apply familiar tools—such as portfolio risk reports, stress tests, risk limits, and independent model validation—to crypto positions, even as they adapt to the unique features of blockchain‑based instruments.

Industry participants like Centrifuge have observed that crypto risk management has spent a decade closing the distance to how banks actually run risk, and that this convergence is a precondition for institutional capital to move onchain at scale. This convergence can be seen in the adoption of formal risk committees within DAOs, the commissioning of independent risk providers, the development of standardized guidelines like the EEA’s, and the integration of DeFi exposures into institutional risk dashboards. As traditional financial market infrastructures, such as DTCC, explore tokenized assets and stablecoins, the overlap between traditional and crypto risk considerations will only increase.

Banks are also experimenting with new technologies to enhance risk management capabilities. Piraeus Bank, for example, has launched an AI hub in partnership with Accenture and Anthropic, aiming to shift from isolated AI use cases to a unified enterprise AI strategy across operations, risk management, and customer services. Such initiatives indicate that institutions see AI‑driven analytics and automation as key tools for managing complex, fast‑moving risks, including those associated with digital assets. As these capabilities mature, we can expect tighter integration of onchain data and DeFi positions into institutional risk engines.

Instruments and Markets for Hedging Digital Asset Exposures

The maturation of crypto derivatives markets is another driver of institutional adoption, as it provides tools for hedging and risk transfer. Futures and options on major cryptocurrencies are now available on both crypto‑native venues and traditional exchanges, enabling miners, corporates, and funds to manage price and volatility risk more systematically. Planned products such as bitcoin volatility futures on CME Group would push this evolution further, allowing market participants to hedge or take positions on volatility itself, similar to VIX futures in equities. These instruments can play a central role in risk management strategies that seek to stabilize portfolio volatility or protect against sharp moves.

Onchain, DeFi protocols are building analogous hedging capabilities. Perpetual futures platforms offer leveraged long and short exposure with continuous funding, while options protocols provide call and put options on various assets. Structured products, such as covered‑call vaults and volatility harvesting strategies, package these instruments into automated yield products that can be used to hedge or express specific risk views. At the same time, innovations like atomic SolvBTC redemptions—enabling seamless conversion between tokenized Bitcoin and underlying BTC—create new opportunities for risk management in Bitcoin‑backed lending and yield strategies by reducing basis and liquidity risk between wrapped and native forms.

Stablecoins and tokenized cash instruments add another dimension to hedging and liquidity management. DTCC’s analysis of stablecoins notes that institutional stablecoins, tokenized money market funds, and tokenized government securities are reshaping liquidity dynamics, suggesting that future risk management strategies may involve shifting between onchain and offchain liquidity pools depending on conditions. In this context, risk managers must understand not only price and volatility risk but also legal, operational, and settlement risks associated with different tokenization models. For instance, hedging a DeFi position with a tokenized T‑bill fund introduces exposure to the issuer, the underlying custody arrangement, and the regulatory regime governing the token.

Lastly, risk transfer through insurance and reinsurance mechanisms is slowly gaining traction in crypto. Both onchain and offchain insurance products aim to cover exchange hacks, smart contract exploits, and custodial failures, although capacity and coverage terms remain limited. These products allow some participants to transfer specific risks to specialized providers who diversify across many protocols and incidents. As with other hedging tools, however, using insurance introduces counterparty and model risk, which must be incorporated into overall risk frameworks.

Service Providers, Risk Committees, and DAO Governance

As risk management becomes more central to digital asset markets, a growing cast of specialized service providers and governance structures has emerged. In DeFi, protocols like Aave and Curve have engaged external risk teams—Chaos Labs, Gauntlet, LlamaRisk, and others—to perform detailed risk analysis, parameter optimization, and ongoing monitoring. These providers function similarly to internal risk departments in banks, but operate under DAO mandates and public governance processes. Their recommendations on collateral factors, borrow caps, liquidation incentives, and asset listings carry significant weight in governance debates and risk outcomes.

The Aave ARFC (Aave Request for Comment) on the risk framework illustrates how DAO governance can formalize the role of risk standards. The proposal describes a framework that sets a binding risk standard for every asset on Aave V3, V4, and Horizon, covering onboarding decisions and quarterly reviews. Governance forums debate the framework’s parameters and implementation, while external risk providers contribute analysis and models. This structure creates a feedback loop between quantitative risk assessments and community values, with tokenholders ultimately deciding how much risk to take in pursuit of growth.

Curve’s extension of its partnership with LlamaRisk, meanwhile, highlights the importance of continuity and long‑term collaboration in risk management. The proposal details LlamaRisk’s contributions to crvUSD growth and Curve ecosystem risk mitigation over the prior year, and seeks to lock in another year of work, emphasizing that effective risk management is not a one‑off engagement but an ongoing process. For DAOs, securing consistent risk expertise and aligning its incentives with long‑term protocol health is an essential governance task.

Regulators and rating agencies are also becoming part of the risk governance landscape. S&P Global’s analyses of DeFi hacks and operational security issues signal that traditional credit rating frameworks may eventually be extended to DeFi protocols or tokenized instruments, further integrating crypto into established risk taxonomies. Meanwhile, guidelines like those from the EEA provide a common reference point for both builders and regulators to assess risk in a structured way. Over time, we can expect formal risk committees within DAOs, standardized disclosure templates, and perhaps even regulatory recognition of specific DeFi risk management frameworks.

Practical Risk Management Playbooks

Retail Traders on Centralized and Decentralized Venues

For retail participants, risk management often begins with personal rules and habits rather than formal frameworks, but the underlying principles are similar. Educational content on crypto trading stresses the importance of defining risk tolerance, setting clear objectives, and using tools like position sizing and stop‑loss orders to keep losses within acceptable bounds. A common guideline is to risk only a small percentage of total capital on any single trade, adjusting position size based on asset volatility and leverage. Traders are also advised to avoid over‑leveraging, particularly in volatile markets where liquidation thresholds can be hit quickly.

The 24/7 nature of crypto markets further complicates retail risk management. As coverage of always‑on markets points out, traditional trading safeguards assume that major moves happen during business hours when traders and risk systems are alert, but crypto markets can experience sharp moves at any time. Retail traders who cannot monitor positions continuously must be especially cautious with leveraged products, such as perpetual futures on centralized exchanges or DEXs like Hyperliquid, where price gaps and thin liquidity can lead to unexpected liquidations. Using conservative leverage, wider stop‑losses, or avoiding overnight and weekend exposure altogether are practical ways to mitigate this risk.

Exchange and custodial risk are also central considerations. Users must assess the security track records of centralized exchanges, their regulatory jurisdictions, and their policies on segregation of client assets and insurance. Self‑custody eliminates exchange counterparty risk but introduces operational risk around key management, wallet security, and phishing. For DeFi, additional layers of risk include smart contract vulnerabilities, protocol governance risk, and exposure to stablecoin or oracle failures. Retail users can mitigate these risks by favoring audited, battle‑tested protocols, diversifying across platforms, limiting exposure to experimental projects, and staying informed about governance and security developments.

Ultimately, the most effective retail risk management strategies combine sensible trading rules with an awareness of platform‑level and ecosystem risks. This might include maintaining a long‑term core position in more established assets such as Bitcoin and Ether while limiting speculative exposures, keeping a cash reserve in stablecoins diversified across issuers, and using onchain analytics or dashboards to monitor positions. As tooling improves, more retail users may also leverage risk scores, dependency graphs, and protocol‑level risk dashboards to inform their decisions.

DeFi Farmers, LPs, and Leveraged Strategies

Yield‑seeking DeFi users face a complex mix of risks that go beyond simple price volatility. Liquidity providers in automated market makers must contend with impermanent loss, where price movements between paired assets erode the value of their position relative to holding the assets outright. Lenders and borrowers on DeFi money markets face liquidation risk if collateral prices fall or borrowed asset prices rise. Leveraged strategies such as looping—depositing assets as collateral, borrowing against them, and redepositing to increase yield—amplify both returns and risks, making disciplined risk management essential.

Solstice PT looping, for example, allows users to deposit PT‑USX as collateral in a protocol like Loopscale, borrow against it, then use the borrowed funds to purchase more PT‑USX and repeat the cycle. This can significantly increase effective yield on the underlying fixed income position but also raises liquidation risk if PT‑USX prices move unfavorably, USX experiences issues, or protocol parameters change. Strict risk management in such setups involves carefully modeling worst‑case scenarios for price, liquidity, and interest rate changes; setting conservative leverage limits; and monitoring collateral ratios and liquidation thresholds closely. Protocols may assist by providing health factor dashboards, alerts, and automated deleveraging options, but the ultimate responsibility rests with users.

DeFi farmers must also consider composability risk. A seemingly simple yield farm may depend on multiple protocols under the hood—a lending market, a DEX, a yield aggregator, and an oracle—each with its own risk profile. The EEA guidelines encourage users and analysts to map these dependencies and assess the cumulative risk, rather than evaluating each component in isolation. Tools like YO’s Risk Graph can help by visualizing how various protocols and pools connect, and by providing risk grades that incorporate upstream exposures. Using such tools, farmers can prioritize strategies that rely on more robust, highly rated protocols and avoid those that hinge on fragile or unaudited components.

Diversification, position sizing, and disciplined exit strategies are key risk management techniques for DeFi yield strategies. Rather than concentrating capital in a single high‑yield pool, users can spread exposures across different chains, protocols, and asset types, while limiting total allocation to any one experimental or illiquid strategy. Planning exit criteria—such as withdrawing if yield falls below a threshold, if TVL drops sharply, or if governance or security concerns arise—is also critical. DeFi’s fluidity makes it easy to chase yield, but without a risk framework, this can lead to serial exposure to the riskiest corners of the ecosystem.

Builders, DAOs, and Protocol Risk Officers

For builders and DAOs, risk management is a governance and design responsibility as much as a technical one. The EEA DeFi Risk Assessment Guidelines provide a roadmap for what a well‑run protocol should document and disclose, including technical architecture, governance mechanisms, admin key policies, security audits, and risk mitigations. Adhering to these guidelines not only facilitates external risk assessment but also disciplines internal thinking, forcing teams to confront questions such as who can upgrade contracts, under what conditions markets can be paused, and how new asset listings are evaluated for risk.

Embedding risk officers or risk working groups within DAOs is becoming more common. Protocols like Aave and Curve have dedicated risk channels and committees that review proposals, commission analyses, and maintain risk dashboards. These structures help translate technical and market information into governance decisions, ensuring that asset listings, parameter changes, and new product launches are evaluated through a risk lens. Aave’s binding risk framework for asset onboarding and quarterly reviews is a notable example of institutionalized risk governance within a decentralized protocol. DAOs that lack such structures may find it harder to respond coherently to emerging risks or to maintain investor confidence over time.

Builders also bear responsibility for incorporating risk mitigations into protocol design. This includes using upgradeable contracts judiciously with appropriate safeguards, implementing timelocks for sensitive changes, designing safe defaults for parameters, and providing robust monitoring and alerting systems. Dependency on external services like oracles, bridges, and analytics providers must be carefully evaluated, with fallbacks or circuit breakers where possible. While external audits and bug bounties are important, they must be complemented by internal security culture and ongoing risk reviews.

Finally, DAOs and builders must grapple with the social and communication aspects of risk. Clear, timely disclosures of vulnerabilities, incidents, and risk changes are essential for maintaining trust, especially when user funds are at stake. Governance communications should explain the rationale behind risk‑related decisions, such as raising collateral factors or delisting assets, in accessible terms. Over time, protocols that consistently demonstrate strong risk governance may benefit from a reputational premium, attracting more cautious users and institutional capital.

Bitcoin-Focused vs Multi-Asset Portfolios

Risk management considerations differ significantly between Bitcoin‑focused portfolios and multi‑asset crypto portfolios. A portfolio concentrated in Bitcoin primarily faces market and liquidity risk associated with a single, relatively mature asset that trades on many venues with deep liquidity. While Bitcoin remains volatile compared with traditional assets, its market structure and historical data allow for more robust modeling of risk than is possible for newer tokens. For such portfolios, hedging strategies may focus on futures, options, and volatility products tied to BTC, as well as diversification into stablecoins or traditional assets.

Multi‑asset crypto portfolios, by contrast, introduce additional layers of idiosyncratic risk. Altcoins may have limited liquidity, concentrated holdings, opaque tokenomics, and higher smart contract or governance risk. DeFi governance tokens may be exposed to protocol‑specific hacks or governance failures. Stablecoins introduce issuer and peg risk, as discussed earlier. From a risk management standpoint, these portfolios require more granular analysis and diversification, as correlations between assets can spike during market stress, undermining the benefits of naive diversification.