Explainer on Resolv’s USR stablecoin, covering its three‑token architecture, the March 2026 key‑compromise exploit, depeg contagion across Fluid and Venus, Resolv’s phased recovery and Vault Street pivot, and lessons for stablecoin and DeFi security.

+5 sources across the wider coverage universe

Chainalysis traces Resolv's $25M exploit to compromised AWS key that minted 80M unbacked USR2026-03

Chainalysis traces Resolv's $25M exploit to compromised AWS key that minted 80M unbacked USR2026-03 Resolv unveils a three‑month exploit recovery program for USR, RLP and LP users and launches Vault Street with its first leveraged institutional RWA product, primeUSD, while keeping RESOLV token utility and staking unchanged.2026-05

Resolv unveils a three‑month exploit recovery program for USR, RLP and LP users and launches Vault Street with its first leveraged institutional RWA product, primeUSD, while keeping RESOLV token utility and staking unchanged.2026-05 Resolv has been exploited, exploiter minted 50M $USR with 100K $USDC2026-03

Resolv has been exploited, exploiter minted 50M $USR with 100K $USDC2026-03 Fluid core team personally secures loans to cover 100% of bad debt from Resolv USR exploit2026-03

Fluid core team personally secures loans to cover 100% of bad debt from Resolv USR exploit2026-03 Aave sails clear of Resolv USR storm. Resolv's supplied assets hold steady in the protocol's hold; backing intact, graceful exit underway with debt repayments begun. No turbulence for Aave liquidity providers or protocol.2026-03

Aave sails clear of Resolv USR storm. Resolv's supplied assets hold steady in the protocol's hold; backing intact, graceful exit underway with debt repayments begun. No turbulence for Aave liquidity providers or protocol.2026-03 Resolv reveals $25M exploit stemming from compromised contractor GitHub credential, 80M USR illicitly minted2026-04

Resolv reveals $25M exploit stemming from compromised contractor GitHub credential, 80M USR illicitly minted2026-04

USR (Resolv USD): Design, Collapse, and Reconstruction of a DeFi-Native Stablecoin

USR, or Resolv USD, is a crypto-native, yield-bearing stablecoin issued by the Resolv protocol and designed to provide dollar-denominated returns without directional market exposure. It sits at the center of a three-layer architecture that pairs a “premium” stable asset with an insurance token (RLP) and a governance token (RESOLV), and in 2026 it became a high-profile case study in how off-chain key compromises can destabilize an entire DeFi ecosystem even when on-chain collateral remains intact.

At its peak, USR was positioned as the flagship product of Resolv’s “financial layer for stable returns,” offering users a way to convert deposits such as USDC into a stable-yielding on-chain dollar instrument that could circulate across decentralized exchanges (DEXs), lending protocols, and structured products. The design sought to combine a conservative collateral pool and delta-neutral hedging strategies with capital-efficient liquidity deployment, targeting predictable returns without exposing users to unhedged crypto price swings. On 22 March 2026, however, an attacker compromised a privileged signing key in Resolv’s cloud infrastructure, used it to mint roughly 80 million unbacked USR against a deposit of only about 100,000–200,000 USDC, and extracted approximately 23–25 million dollars of value before the protocol was paused. USR’s price collapsed, integrated protocols such as Fluid and Venus rushed to contain exposure, and Resolv pivoted into a multi-stage recovery that now blends snapshot-based redemptions with a new institutional “Vault Street” product line focused on real-world assets (RWAs). The USR episode has since become a touchstone in debates about stablecoin design, off-chain key management, oracle behavior during depegs, and the responsibilities of integrated DeFi protocols when a collateral asset fails.

Origins and Architecture of USR and the Resolv Protocol

USR as the core “prime” asset in Resolv’s three-layer system

Resolv presents itself as a “financial layer for stable returns,” built around a three-tiered architecture that separates users by risk and yield preference. At the top sits USR, also described as Resolv USD, which the team frames as a “crypto-native prime asset” intended to offer a stable dollar peg and yield-bearing exposure while avoiding directional bets on crypto prices. Below USR sits RLP, a more volatile “insurance layer” that absorbs losses and gains from the protocol’s strategies, effectively underwriting USR’s stability in exchange for higher expected returns. The RESOLV governance token completes the stack, conferring protocol governance rights and, in practice, being used in incentive schemes such as staking rewards that align governance with the long-term health of the system.

The conceptual appeal of this architecture is to give different categories of users distinct risk-return profiles within a single coordinated system. A conservative depositor might choose USR for a relatively low-volatility, yield-bearing dollar asset, while a risk-seeking participant might hold RLP to gain leveraged exposure to the protocol’s performance and to the tail risk associated with insuring USR. Meanwhile, RESOLV serves as a meta-layer, enabling tokenholders to shape parameters such as collateral management, strategy selection, and fee distribution that ultimately affect both USR and RLP. This separation of roles is a recurring theme across DeFi, but Resolv’s explicit framing of USR as “premium” and RLP as “insurance” made the risk hierarchy unusually clear compared with many yield-bearing stablecoin designs.

From a systems perspective, USR is not merely a token but the accounting unit of an on-chain balance sheet whose assets include stablecoins, liquidity positions, and hedged derivatives portfolios. The protocol’s marketing emphasized that USR’s returns would be generated by market-neutral strategies and diversified liquidity provision rather than speculative directional exposure to volatile crypto assets. By maintaining USR-backed liquidity pools, for example as collateral for other stablecoins such as DOLA, Resolv aimed to become a base layer that other protocols could safely build upon, treating USR as a relatively dependable yield-bearing dollar primitive. This positioning, and the rapid growth that followed, set the stage for the systemic impact once the minting system was compromised.

Growth trajectory and positioning in the stablecoin landscape

Prior to the exploit, USR grew rapidly into a mid-sized stablecoin with broad DeFi integrations. On-chain data analyzed by third-party research indicated that USR’s market capitalization approached 400 million dollars in early 2026 before retracing toward roughly 100 million in the weeks preceding the March 22 incident. This placed USR well below systemically dominant assets such as USDC or USDT, but comfortably within the tier of specialized stablecoins that had become meaningful components of liquidity pools and lending markets. The protocol’s total value locked (TVL), when including underlying collateral and associated strategies, was cited in tens or hundreds of millions of dollars, underscoring the scale at which its mechanisms were operating when the exploit occurred.

In narrative terms, USR occupied a hybrid space between fully fiat-backed stablecoins like USDC and more experimental algorithmic designs. On one hand, it was backed by actual collateral—primarily other stablecoins—deployed into strategies intended to generate relatively predictable yields. On the other hand, the minting process, hedging, and liquidity management relied on sophisticated off-chain infrastructure and privileged roles, making the system partly discretionary and, as it turned out, exposed to operational security failures. This combination of real collateral and complex off-chain control gave USR a different risk profile from purely algorithmic stablecoins such as the now-defunct TerraUSD, yet it also meant that users had to trust not only on-chain code but also the integrity of cloud-based systems and key management practices.

Resolv’s collateral strategy further distinguished USR from simple “cash-in, cash-out” models. Rather than passively holding USDC in wallets, the protocol deployed capital into yield-generating opportunities, including delta-neutral strategies and liquidity provision, with losses and gains ultimately flowing through the USR–RLP capital structure. The intention was to capture a “real yield” above what users could access by holding base stablecoins directly, while using conservative hedging and insurance layering to keep the peg robust. For a time, this vision appeared to resonate with market participants, as evidenced by integrations across DeFi protocols and the willingness of other platforms to accept USR as collateral.

The role of RLP and RESOLV around USR

RLP’s function as an insurance or junior capital layer is critical to understanding USR’s economic design and, later, the allocation of losses and compensation after the exploit. In Resolv’s own framing, USR is the “premium” or senior asset, while RLP explicitly exists to absorb protocol-level losses in order to protect USR holders. When strategies underperform or if adverse events strike, the first line of defense against shortfalls is the RLP capital base, which is meant to take mark-to-market hits in exchange for upside during normal or favorable conditions. This structure resembles the tranching of risk in traditional finance, where junior tranches absorb defaults before senior tranches are impaired.

The RESOLV governance token, by contrast, is not directly part of the solvency stack but influences how risks and rewards are structured. The token is used in staking programs and governance, including decisions about strategy allocation, fee structures, and, eventually, the design of the post-exploit recovery plan. After the March 22 incident, the Resolv Foundation earmarked 10% of the total RESOLV token supply for compensation, with approximately 70% of that allocation directed toward RLP holders to bring their recovery level above 60% of pre-exploit value. This decision reinforced the view of RLP as the designated risk-absorbing layer while also recognizing that governance tokenholders bear some responsibility for the protocol’s failures and recovery.

In practice, this three-token system created interdependencies that became highly visible during the recovery process. USR holders, especially those who held the token before the exploit, were prioritized for full or near-full redemption at par, reflecting their seniority. RLP holders, as the insurance cohort, accepted deeper haircuts but received a mix of stablecoin and governance token compensation. RESOLV stakers saw their token’s role broadened as part of the recovery and future protocol roadmap, including via resumed staking rewards and the launch of new products under the Vault Street brand. The way losses were socialized across these tiers has since been examined as a template—both positive and negative—for how complex DeFi systems might allocate responsibility when design or operational failures emerge.

Chainalysis traces Resolv's $25M exploit to compromised AWS key that minted 80M unbacked USR

Wtf, this is actually crazy.. Revolut just has a crappy security system and that's all

Readers treated the USR exploit as a real-time audit of their own positions elsewhere — clicks on 'Aave sails clear' and 'Venus paused' matched the forensic Chainalysis story, revealing that DeFi users cared more about cross-protocol contagion checks than about Resolv's own recovery.↗

Mechanics of USR: Issuance, Redemption, and Market Integrations

Two-step minting: requestSwap and completeSwap

USR’s minting mechanism was built around a two-step flow that combined on-chain transactions with off-chain authorization. In normal operation, a user who wished to mint USR would first deposit USDC or another approved collateral by calling a function on the USR Counter contract, commonly referred to as requestSwap. This transaction recorded the deposit and created a pending request but did not itself mint USR, instead waiting for an off-chain service to validate and finalize the operation. The off-chain component was controlled by a privileged role dubbed SERVICE_ROLE, which held a private key authorized to sign messages that specify how much USR should be issued against each deposit.

The second step, completeSwap, was triggered when the off-chain service used the SERVICE_ROLE key to call back into the contract with a signed authorization that included the mint amount. Upon verifying the signature, the smart contract would mint the requested quantity of USR to the user, as long as certain minimum output conditions were met. Crucially, however, there was no on-chain enforcement of a maximum mint amount tied to the size of the deposit, no ratio check between collateral and newly minted USR, and no direct integration with a price oracle for that purpose. The contract effectively trusted that the off-chain signer would always behave correctly and would not authorize minting beyond what the underlying collateral justified.

This architecture was not unusual among complex DeFi systems that require off-chain validation or that want flexibility to factor in risk limits, compliance checks, or dynamic strategy conditions before issuing new tokens. It did, however, concentrate enormous power in a single key and assume that operational security in the off-chain environment would be at least as robust as the on-chain code. In Resolv’s case, the SERVICE_ROLE was reportedly a plain externally owned address (EOA) rather than a multisignature or threshold scheme, even though the admin role for the contracts was controlled by a multisig. This meant that day-to-day minting authority depended on a single key whose compromise would grant an attacker essentially unrestricted minting capability, subject only to the protocol’s internal monitoring and reactive controls.

Redemption flows and the role of the collateral pool

Redemption flows for USR mirrored the minting process conceptually, although their exact implementation details differ across versions and chains. In broad terms, a USR holder could return tokens to the protocol to redeem underlying collateral, typically in USDC or a closely related asset, reflecting a target 1:1 peg. The protocol maintained a collateral pool composed of stablecoins and other positions, which served as backing for USR in circulation and as a source of capital for its hedged yield strategies. As long as the pool remained solvent and liquid, redemptions could generally be honored at or near par, with minor slippage depending on system state.

Resolv’s public communications during and after the exploit repeatedly stressed that this collateral pool had remained “fully intact” throughout the incident and that no underlying assets were directly stolen from the pool. Instead, the attack inflated the supply of USR without adding matching collateral, effectively diluting legitimate holders and triggering a market-driven depeg when the attacker dumped large quantities of newly minted tokens into DEX liquidity pools. From the perspective of pre-exploit USR holders, the backing per token collapsed because the same collateral now had to support a much larger supply, even though the absolute value of the collateral pool had not fallen. This distinction—between loss of collateral and dilution of claims—proved crucial in enabling a recovery based on snapshots and controlled redemptions rather than a full-scale insolvency.

Redemption mechanics became more complex after the exploit as Resolv moved into recovery mode. The team introduced phases in which pre-exploit USR holders, starting with allowlisted wallets, were granted access to redeem their holdings for USDC at a 1:1 rate, while post-exploit holders faced different terms. These redemptions relied on the underlying collateral pool and on additional resources mobilized by the Resolv Foundation, but they were constrained by the need to neutralize illicitly minted tokens and to balance fairness across user categories. The fact that the collateral backing pre-exploit USR remained intact meant that, in principle, there was enough value to make legitimate holders whole, but executing that in practice required careful coordination across contracts, chains, and counterparties.

USR in DeFi markets: DEX liquidity, lending, and cross-protocol usage

Prior to March 2026, USR was actively traded and used in multiple DeFi contexts. Liquidity pools on decentralized exchanges such as Curve, KyberSwap, and Velodrome facilitated swaps between USR and other stablecoins like USDC and USDT, providing price discovery and exit liquidity for users. These pools were often deep enough to support significant volume, reflecting both organic usage and liquidity mining incentives. Some implementations wrapped USR into staked or derivative forms, such as wstUSR, which represented a staked share in the USR pool and circulated as a separate token, adding another layer to the ecosystem.

Beyond spot trading, USR found its way into lending protocols and structured products. On Venus Protocol, for example, Flux markets for USR were created, allowing users to supply USR as collateral or to borrow it, integrating the stablecoin into BNB Chain money markets. This made USR part of leverage loops and yield strategies that depended on its stability and on oracle prices treating it as a one-dollar asset. Fluid, a separate DeFi lender, likewise integrated USR into its collateral and liquidity framework, creating exposure to USR’s peg for both the protocol treasury and its users. Each of these integrations amplified USR’s systemic footprint, as instability in the token could translate into liquidations, bad debt, or impaired collateral across multiple platforms.

USL-backed liquidity was also used as direct collateral for other stablecoins. Resolv maintained USR-backed liquidity pools that served as collateral for DOLA, the stablecoin issued by Inverse Finance, demonstrating how one stable asset could become the foundation for another in a layered DeFi stack. In these structures, assumptions about the quality of USR as collateral were critical; if USR deviated materially from its peg or if its backing became suspect, protocols relying on it could suffer cascading consequences. This is precisely what transpired once the exploit-induced depeg began, forcing protocols to rapidly reassess risk and, in several cases, to pause markets or inject external capital to protect users.

The integration of USR into such a wide range of markets underscores its dual role as both a standalone product and a building block that other protocols treated as infrastructure. That duality magnified both its utility during normal operation and its potential to propagate stress during the crisis. It also brought into focus the systemic importance of decisions around minting, redemption, oracles, and emergency governance for any stablecoin aspiring to be a “financial layer” rather than just a niche asset.

- 0150M USR minted for 100K USDC↗

The extreme capital efficiency of the attack — 500:1 leverage against collateral — made the exploit viscerally alarming and immediately viral.

- 02Cross-protocol contagion containment↗

Readers with liquidity in Aave, Venus Flux, and Fluid urgently needed to know whether their positions were safe before the dust settled on Resolv.

- 03Compromised key attribution↗

Chainalysis tracing the exploit to a contractor's AWS KMS / GitHub credential shifted the narrative from smart-contract risk to centralized infrastructure failure, which readers found more damning.

- 04Fluid bad debt socialisation

The Fluid core team personally securing loans to cover 100% of bad debt was an unusual accountability move that readers clicked to verify — and assess whether it held.

- 05Recovery program credibility↗

Resolv's structured three-month recovery plan and the simultaneous Vault Street / primeUSD launch raised scepticism about whether the rebranding outpaced actual restitution.

- 06Hardcoded oracle blind spot↗

The revelation that USR's price feed kept reporting $1.00 while 80M unbacked tokens were being minted exposed a fundamental oracle design flaw that concerned readers holding other collateralised stablecoins.

The March 22, 2026 Exploit: From Compromised Key to Depeg

Timeline and attack path

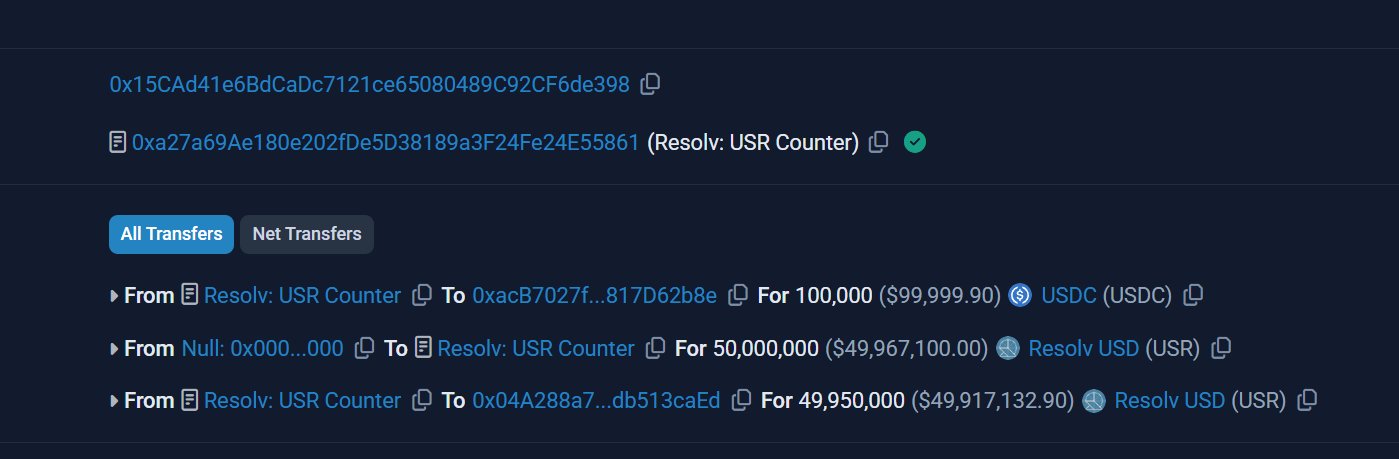

On 22 March 2026, Resolv’s seemingly routine minting flow became the avenue for one of the year’s most consequential DeFi exploits. According to Resolv’s own notice and subsequent analyses by independent firms, a malicious actor gained unauthorized access to Resolv’s infrastructure by compromising a private key associated with the protocol’s off-chain signing environment. This key controlled the SERVICE_ROLE, the privileged signer responsible for authorizing USR mints in the completeSwap function. Once in possession of this key, the attacker was able to instruct the protocol’s contracts to mint vastly more USR than the deposited collateral warranted.

The attacker began by depositing a relatively modest amount of USDC—variously estimated between roughly 100,000 and 200,000 dollars—into the USR Counter contract via requestSwap transactions. Under normal conditions, such deposits would have resulted in an equal amount of USR being minted after off-chain approval. This time, however, the compromised SERVICE_ROLE key was used to call completeSwap with output parameters instructing the contract to mint tens of millions of USR in exchange for those deposits. Because the smart contract only checked that the signature was valid and that a minimum output threshold was satisfied, it complied with the request, minting approximately 50 million USR in one transaction and around 30 million in another, for a total of roughly 80 million new tokens.

Resolv’s official communication framed the incident as involving approximately 80 million dollars’ worth of uncollateralized USR, while blockchain analytics companies estimated that the attacker ultimately extracted about 23–25 million dollars in realizable value before the protocol was paused. This discrepancy reflects the difference between the notional value of the unbacked tokens at the pre-exploit peg and the actual proceeds the attacker managed to obtain by selling into finite on-chain liquidity as prices collapsed. Within about seventeen minutes of the initial illicit mint, USR’s price on certain Curve pools had plunged from near parity to a few cents, and the attacker’s wallet had accumulated thousands of ETH.

Exploit mechanics: missing on-chain guardrails and overtrusted off-chain roles

The exploit’s technical core lay in the interaction between the two-step minting process and the absence of on-chain constraints on maximum mint amounts. The requestSwap function correctly recorded deposits of USDC and created pending swap requests, but it did not enforce any ratio between deposited collateral and the USR that would later be minted. Instead, it passed along data that the off-chain SERVICE_ROLE was expected to interpret and validate. When the compromised SERVICE_ROLE key later invoked completeSwap, it supplied output parameters that instructed the contract to mint USR far in excess of what the deposit justified. The contract checked the signature, confirmed a minimum output condition, and proceeded to mint the tokens, as designed.

Analysts highlighted that basic protective patterns—such as bounding the mint amount relative to the recorded deposit, limiting any single mint to a percentage of total supply, or checking against oracle-supplied price data—were absent in this flow. The design effectively treated the SERVICE_ROLE signer as infallible, granting it the ability to mint arbitrary quantities of USR in a single transaction. Combined with the fact that the SERVICE_ROLE was implemented as a single EOA rather than a multisignature or threshold scheme, this created a single point of catastrophic failure in the protocol’s monetary system.

Importantly, the exploit was not a traditional smart contract bug in the sense of a reentrancy flaw, integer overflow, or mispriced swap function; independent security firms noted that Resolv’s Solidity contracts had been audited and that the attack path followed the intended logic. The vulnerability instead resided one layer above, in the operational security of the cloud infrastructure and key management controlling the privileged off-chain signer. The attacker did not need to trick the contract into unexpected behavior; they simply used the protocol’s own configured minting authority, after compromising it, to create unbacked tokens on demand.

Subsequent postmortem analysis by Chainalysis and others traced the compromise to Resolv’s AWS Key Management Service (KMS) environment, where the signing key for the SERVICE_ROLE was stored. Once the attacker gained control in that environment, they could use the key to authorize minting operations just as the legitimate service would have. This chain of events illustrated how, in modern DeFi systems, the most critical attack surfaces may reside not in Solidity code but in cloud consoles, IAM policies, CI/CD pipelines, and key management setups that traditional smart contract audits rarely cover.

Market impact: USR depeg, liquidity shocks, and cross-protocol contagion

The immediate market consequence of the illicit mint was a flood of unbacked USR entering DEX liquidity pools. The attacker converted a substantial portion of the newly minted USR into wstUSR, the staked derivative, and then began unwinding positions across markets including Curve, Uniswap, KyberSwap, and others, swapping into stablecoins and ultimately into ETH. On-chain tracking by firms such as PeckShield and security researchers documented that the attacker’s wallets ended with around 11,400 ETH, worth about 23–25 million dollars at the time, along with residual wstUSR still exposed to the collapsing price.

As the attacker sold, USR’s price began to decouple sharply from its intended one-dollar peg. On Curve’s USR/USDC pool, reports indicate that the price fell to as low as approximately 2.5 cents at one point, reflecting an almost total loss of market confidence in the token within minutes. Aggregated price trackers such as CoinGecko showed USR printing lows in the range of 0.20–0.25 dollars during the early phases of the depeg, depending on the venue and liquidity conditions. Although the price later stabilized at a higher but still depressed level on some pairs, the peg failure remained severe and persistent, with some markets reporting values as low as 5–7 cents during subsequent trading.

Compounding the immediate sell pressure was the behavior of oracles and automated allocators. Analyses of the incident noted that certain oracle configurations effectively hard-coded USR at one dollar, or otherwise failed to respond quickly to the depeg, leading strategies and protocols that relied on those feeds to continue treating USR as a stable asset. In some cases, this meant that automated systems kept allocating capital into USR or USR-linked strategies according to pre-set rules, despite the fact that the token’s on-chain float had been massively inflated without corresponding growth in reserves. The mismatch between price feeds and reserve reality highlighted the danger of oracles that do not integrate information about supply, collateralization, or protocol-level events beyond spot market price.

The impact on integrated DeFi protocols was significant. Fluid, which had incorporated USR into its lending and liquidity framework, found itself facing a large amount of USR-denominated bad debt as the token’s value collapsed. Rather than pass these losses onto its users, the Fluid team announced that they had secured short-term loans and funding commitments—some reportedly from the core team itself—to repay approximately 70 million dollars in USR-related debt as of March 25, 2026, with a stated intention to continue until all obligations were cleared. This decision turned the Resolv exploit into one of the larger post-exploit repayment campaigns in DeFi and underscored the degree of inter-protocol entanglement created by USR’s adoption.

Venus Protocol, for its part, paused its Venus Flux markets for USR in response to the ongoing depeg, stating publicly that the suspension was a risk management measure while the situation unfolded. By halting borrowing and lending activities involving USR, Venus sought to prevent further contagion within its markets and to protect users from interacting with a rapidly destabilizing asset. Other platforms monitoring the situation similarly moved to freeze or limit USR-related activity, and some DEXs and security partners took steps to track, and in certain cases block, wallets associated with the exploit from further interaction.

Comparison to earlier DeFi exploits and the KyberSwap Elastic incident

The Resolv–USR exploit stands in contrast to other notable DeFi incidents, such as the November 2023 KyberSwap Elastic exploit, which stemmed from a vulnerability in the swap mechanism of a tick-based concentrated liquidity AMM. In the KyberSwap case, attackers exploited a discrepancy between cross-tick estimation and final price calculation, exacerbated by a rounding error, to manipulate pool states and drain liquidity from affected pools. The vulnerability was internal to the AMM’s on-chain code and persisted despite prior audits, showing that even deeply scrutinized smart contract logic can contain latent bugs.

By comparison, USR’s failure mode involved no such unexpected behavior on-chain; the Resolv contracts followed the designed minting flow, and the bug lay in the implicit assumption that a single off-chain signer could be fully trusted indefinitely. In both cases, however, a combination of powerful privileged roles, incomplete guardrails, and insufficiently scoped audits contributed to catastrophic loss of value. KyberSwap’s postmortem emphasized the need for more comprehensive testing around edge cases and for strengthened monitoring and incident response, while the Resolv case has been cited as evidence that DeFi security practices must extend beyond Solidity to include infrastructure, key management, and organizational controls.

Taken together, these incidents illustrate the broadening attack surface of modern DeFi. Protocols increasingly rely on off-chain services, oracles, governance multisigs, cloud-hosted keepers, and bridges, any of which can become the weakest link even when core contracts are sound. USR’s collapse underscores that stablecoin systems, in particular, must be engineered and audited as full-stack architectures whose monetary integrity depends on both on-chain and off-chain components.

Resolv unveils a three‑month exploit recovery program for USR, RLP and LP users and launches Vault Street with its first leveraged institutional RWA product, primeUSD, while keeping RESOLV token utility and staking unchanged.

10% of RESOLV supply earmarked for recoveries, with 70% of that going to RLP, turns part of the junior-tranche recovery into a two-year token carry trade rather than clean restitution. The sharper test is whether primeUSD can borrow credibility from the Aave Horizon/Centrifuge rails Resolv used for the $100M JAAA loop while proving the KMS/completeSwap failure was actually fenced off. Levered T-bill vaults are boring until borrow caps move or liquidity vanishes, and March showed how fast “senior” exposure leaks into Morpho/Gauntlet-style vault plumbing.

Compromised contractor credential grants signing key access; 80M unbacked USR minted against ~$200K collateral

USR depegs 74% to $0.257; Resolv pauses protocol and warns against trading illicit tokens

Venus Flux USR markets temporarily anchored; Fluid automated ceilings limit borrowing and USR markets paused

Resolv burns 57% of illicit USR supply; Fluid core team secures personal loans to cover 100% of protocol bad debt

Chainalysis publicly traces exploit to compromised AWS KMS key, confirming $25M net loss

Resolv publishes full postmortem attributing attack to compromised signing key on March 22, 2026

$77M+ redeemed for allowlisted pre-exploit USR holders, representing 90%+ of that cohort; Phase 1 recovery complete

Resolv unveils three-month recovery program, launches Vault Street with primeUSD institutional RWA product, and proposes fee switch for RESOLV token

Recovery Efforts and Resolv’s Strategic Pivot

Immediate response: protocol pause, burn, and investigation

Following the detection of the exploit, Resolv Labs moved quickly to halt further damage by suspending protocol functions. In a public statement issued on behalf of Resolv Digital Assets Ltd., the team confirmed that a malicious actor had gained unauthorized access to their infrastructure through a compromised private key and had minted approximately 80 million dollars of uncollateralized USR. They emphasized that the incident had been identified quickly, that the relevant smart contracts were promptly paused, and that initial analysis indicated that the protocol’s underlying collateral remained intact.

As part of the immediate remediation, Resolv reported that roughly 9 million USR held by the attacker had been burned, reducing the potential impact of the illicitly minted supply. This burn reflected USR that had either not yet been sold into the market or had been recovered in some fashion, and its removal from circulation helped narrow the gap between USR supply and the collateral pool, albeit modestly relative to the total illicit mint of around 80 million tokens. The team also warned users against trading USR or related Resolv tokens during the recovery process, cautioning that post-exploit trading behavior could affect compensation outcomes and that the system was in a state of flux.

Resolv engaged external security and forensics firms to investigate the breach and to assess whether any insider involvement was present. In a later update shared by co-founder Ivan, the team noted that they were working with investigators including Mandiant and Zeroshadow and that, as of that stage in the investigation, no evidence of insider participation had been found. They reiterated that the incident stemmed from an unauthorized third-party compromise of infrastructure and key material, and that efforts were under way to trace illicitly minted USR, coordinate with partners, and pursue legal avenues to recover assets where possible. The postmortem published on Resolv’s own site noted that the attack vector had been eliminated and that compromised credentials and infrastructure components had been rotated or replaced.

Phased redemptions for pre- and post-exploit USR holders

Because the collateral pool backing USR remained intact, Resolv was in a position—unlike in many stablecoin failures—to use snapshots and controlled redemptions to restore value to legitimate holders. The central challenge was to distinguish between users who held USR before the exploit and those who purchased or received tokens after the depeg, as well as to balance the interests of RLP holders, liquidity providers, and other ecosystem participants. Resolv elected to pursue a phased recovery framework, with initial priority given to pre-exploit USR holders whose balances could be verified via on-chain snapshots.

In the earliest phase, the team enabled redemptions for allowlisted wallets that held USR prior to the incident, initially processing these through a partially manual process to minimize further market disruption. According to Ivan’s update, verified allowlisted wallets allowed the team to act within twenty-four hours of the exploit, and by the time of that communication, approximately 98% of redemptions for this group had been completed. These users were able to redeem their pre-exploit USR at a 1:1 rate for USDC, effectively restoring the peg for this cohort and providing a proof-of-concept for broader redemption mechanics. The team indicated that non-whitelisted pre-exploit USR holders could expect the same 1:1 treatment once the technical solution for scaling redemptions beyond the initial allowlist was finalized.

Subsequently, the Resolv Foundation announced a comprehensive recovery plan with a three-month claims window running from May 26 to August 26, 2026. Under this framework, USR and wstUSR held before the attack would be redeemable at a one-to-one ratio for USDC, reaffirming the protocol’s commitment to fully compensating pre-exploit holders. USR acquired after the incident, by contrast, would be compensated at a rate of one USR to 0.5 USDC, reflecting the view that post-exploit buyers were effectively speculating on the distressed asset and should share more of the downside. This differentiation sought to balance fairness and deterrence, acknowledging that some users provided liquidity or bought during the chaos without full information, while still preserving incentives against opportunistic speculation during crisis periods.

Compensation for RLP holders and LPs, and RESOLV token allocation

RLP holders and liquidity providers occupied a distinct position in the recovery hierarchy. By design, RLP functioned as the insurance layer meant to absorb protocol losses before USR was impaired. In the wake of the exploit, Resolv’s recovery plan allocated a significant portion of the burden to this class, consistent with that role, but also provided compensation intended to restore a majority of their pre-incident value. According to the announced framework, RLP holders would receive a compensation package targeting a recovery ratio above 60% of the last reference price before the incident, translated into an effective reference of about 0.71 USDC per RLP unit. This compensation would be delivered through a combination of stablecoin redemptions and new RESOLV token allocations, aligning RLP holders with the protocol’s future upside.

To finance this and other compensation, the Resolv Foundation committed 10% of the total RESOLV token supply to recovery efforts, earmarking around 70% of that allocation specifically for RLP holders. The remaining portion was directed to other affected users, including liquidity providers and post-exploit USR holders, further blurring the boundaries between governance stakeholders and economic claimants. This choice to mobilize governance tokens for compensation underscored the view that protocol tokenholders share collective responsibility for design and operational failures, even when those failures do not stem from explicit governance decisions.

Liquidity providers in USR-related pools also faced losses as pool composition shifted heavily toward USR during the depeg. While the specifics varied by venue and pool structure, many LPs experienced a situation where their positions ended up overwhelmingly denominated in USR, whose market price had collapsed, rather than in the more stable paired asset. Resolv’s framework included recovery terms for these LPs, though the precise ratios and mechanisms differed depending on pool type and timing of participation. The overarching objective was to avoid leaving LPs bearing disproportionate losses—especially where they had provided liquidity under the assumption that USR was a reliable stablecoin—and to preserve the willingness of market makers to support future Resolv or Vault Street products.

Fluid, Venus, and ecosystem responses

The USR exploit tested not only Resolv’s resilience but also the risk management practices of protocols integrated with USR. Fluid’s response has been particularly noted because of the scale of its USR exposure and the decision to socialize losses at the protocol and team level rather than at the user level. As USR’s depeg generated bad debt in Fluid’s markets, the team announced that they had secured short-term loans and contributed funds from core members and external partners to cover 100% of the bad debt associated with the Resolv incident. By March 25, 2026, Fluid reported having repaid approximately 70 million dollars in USR-related obligations, with the caveat that the final total liability remained uncertain and that repayment work would continue until all affected users were made whole.

Fluid framed this effort as a commitment to user protection and as a recognition that integrating an external stablecoin entails shared responsibility for due diligence and ongoing monitoring. The campaign also highlighted the financial and reputational risks that DeFi protocols incur when accepting non-blue-chip collateral and underscored the importance of having contingency plans and capital buffers for such tail events. In a broader sense, Fluid’s actions contributed materially to containing contagion from the USR depeg, preventing forced liquidations and cascading losses that might have propagated through its user base and into interconnected protocols.

Venus Protocol took a different but complementary approach, focused on rapid containment rather than ex post compensation. In response to the USR depeg event, Venus announced that it was pausing its Venus Flux markets for USR, effectively freezing borrowing and lending activity involving the asset. This pause reduced the risk of further bad debt accumulation and gave the Venus team time to assess the impact of the depeg on its balances and users. Venus also communicated that funds in other markets remained protected and that the suspension was a targeted risk management measure rather than a sign of systemic failure. The quick decision to isolate USR exposure demonstrated the value of modular market design, where riskier assets can be ring-fenced from the core protocol.

Other protocols and platforms, including DEXs that had hosted USR or wstUSR liquidity, responded by monitoring exploit-linked wallets, implementing address blacklisting where appropriate, and collaborating with analytics and security firms to trace flows. These coordinated responses limited the attacker’s options for further laundering or exploiting the stolen funds and signaled a maturing ecosystem in which cross-protocol communication can mitigate, though not fully prevent, damage from major incidents.

Vault Street, primeUSD, and the institutional RWA pivot

In parallel with the recovery program for USR, Resolv announced a strategic expansion into tokenized real-world assets under a new product line called Vault Street. Managed by the Resolv Foundation, Vault Street is positioned as an institutional-grade platform for distributing tokenized RWAs and structured yield products, representing a partial pivot from the exclusively crypto-native focus that characterized USR’s original design. The initiative aims to bring more traditional, legally structured fixed-income exposures on-chain, leveraging the protocol’s experience in building stable-yield instruments while addressing some of the trust and risk concerns exposed by the exploit.

The first product in this new line, primeUSD, is described as a leveraged institutional RWA instrument that accepts stablecoin deposits and provides exposure to tokenized U.S. Treasury bonds and DeFi money markets. PrimeUSD is initially being rolled out to professional institutional investors through a private testing phase, with plans for a broader launch in June 2026. The product’s design reportedly uses leverage on tokenized Treasury exposure, combined with on-chain lending markets, to enhance yield, while targeting a risk profile and legal structure suitable for institutional participation.

By launching Vault Street and primeUSD while simultaneously conducting USR redemptions and compensation, Resolv is signaling that it views the exploit not as the end of its ambitions but as a forcing function to upgrade its security architecture and to reposition around institutional-grade products. The Foundation has emphasized ongoing security architecture upgrades and the development of an “institutional-grade asset on-chain infrastructure,” suggesting a renewed focus on governance, key management, and regulatory alignment. The continued utility and staking functionality of the RESOLV token, including the resumption of staking rewards with a 300,000 RESOLV pool for the initial two-week cycle after the recovery plan’s launch, further indicates an intention to maintain and grow the governance ecosystem around these new products.

A single compromised contractor GitHub credential and AWS KMS signing key was sufficient to mint 80M unbacked USR with no on-chain circuit breaker, making the system's trust surface the primary exploit vector.

The exploit succeeded through a failure in centralized parameter validation rather than a conventional code bug, allowing ~$200K in collateral to back $80M in minted tokens.

A hardcoded $1.00 price feed had no mechanism to detect reserve expansion without corresponding collateral growth, leaving automated allocators supplying USDC for hours during the active exploit.

USR crashed 74% to $0.257 at peak depeg; illicit token mixing and Venus market pauses created multi-protocol liquidity disruption before redemption phases began.

Aave's supplied Resolv assets remained backed and exits were orderly, while Fluid's core-team loan backstop and Venus's temporary anchor prevented systemic cascade — but only through discretionary human intervention.

The uncollateralised minting of $80M in a regulated-adjacent stablecoin and the subsequent formal Chainalysis forensic engagement increases the likelihood of scrutiny over algorithmic or hybrid stablecoin reserve attestation requirements.

Security Lessons from the USR Incident for Stablecoins and DeFi

Off-chain infrastructure as a primary attack surface

Perhaps the most striking lesson of the USR exploit is that DeFi protocols are no longer purely on-chain systems; the integrity of their monetary policies and positions often depends on off-chain infrastructure at least as much as on smart contracts. In the Resolv case, the Solidity code governing USR minting executed exactly as designed, with no reentrancy, arithmetic, or logic errors exploited. The vulnerability lay instead in the off-chain environment: a compromised AWS KMS key controlling the SERVICE_ROLE signer allowed an attacker to mint unbacked tokens at will. This shows that key management and cloud security can be as critical to protocol safety as formal verification and contract audits.

Traditional smart contract audits typically focus on contract logic, invariants, and interactions among on-chain components, but they do not routinely extend to AWS IAM policies, provider access logs, CI/CD pipelines, or hardware security module configurations. The Resolv exploit demonstrates that this division of responsibility is no longer adequate for complex protocols that rely on off-chain signers, oracles, and automation. A holistic security posture for such systems must include rigorous auditing of cloud infrastructure, key storage practices, access controls around signing services, and monitoring for anomalous key usage that could indicate compromise.

The attack also raises questions about the centralization of control in single keys, even when those keys are used by trusted internal services. A single SERVICE_ROLE key was able to authorize arbitrary mints, meaning that the entire USR supply and, by extension, the protocol’s perceived solvency, sat behind one digital secret stored in a cloud environment. From a risk management perspective, this is analogous to a bank placing its entire ledger under the control of a single password-protected machine. In the wake of the exploit, security commentators have argued for greater use of threshold signature schemes, hardware-backed multi-party computation (MPC), and stricter compartmentalization of privileges to ensure that no single credential can unilaterally compromise a system’s monetary integrity.

Governance, auditors, and the design of privileged roles

USR’s story also highlights the interplay between governance design, auditing practices, and privileged roles. The fact that the SERVICE_ROLE was a single EOA while the admin role was a multisig suggests that operational convenience and perceived risk influenced how different privileges were architected. Administrators, who might change contract parameters or upgrade components infrequently, were placed behind a higher-assurance multisignature, whereas the day-to-day service actor, which needed to sign frequent mint transactions, was left as a single key for ease of use. In hindsight, the latter role was far more critical because it controlled the issuance of the stablecoin itself.

Auditors reportedly reviewed Resolv’s contracts and found no critical issues with the minting logic, which, strictly speaking, behaved as intended. However, this reveals a gap between what is technically correct in code and what is robust at the systemic level. A design that allows a privileged signer to mint unlimited tokens without on-chain ratio checks or caps is logically consistent but arguably unsafe by construction. This raises broader questions about the scope of audits and the responsibility of both auditors and protocol teams to challenge not only implementation bugs but also architectural assumptions about trust and privilege. There is a growing argument that audits should explicitly evaluate the blast radius of compromised keys and privileged actors, as well as recommend concrete mitigations such as on-chain mint caps, rate limiting, and segregation of duties.

Resolv’s post-exploit responses, including the use of RESOLV governance tokens to fund compensation and the introduction of a more institutionally oriented product line, implicitly acknowledge that governance must be accountable when such architectural choices lead to loss. Governance processes can play a preventive role by setting standards for how privileged roles are created, rotated, and monitored, and by mandating periodic reviews of whether existing roles remain justified. The USR incident illustrates that governance tokens are not merely speculative instruments but claims on the protocol’s ability to manage risk, respond to crises, and realign incentives after failures.

Oracles, depegs, and reserve awareness

Another key lesson from the USR exploit concerns the behavior of oracles and automated systems during depeg events. In this case, some oracles continued to report a one-dollar price for USR even as the token’s market value collapsed, in part because their configurations relied on assumptions or feeds that did not immediately reflect on-chain DEX prices. As a result, protocols and strategies that referenced these feeds treated USR as though it remained fully backed and stable, continuing to accept it as collateral or allocating capital into USR-linked strategies according to pre-exploit parameters. This created a situation where the supply of USR expanded dramatically without corresponding growth in reserves, yet the systems meant to guard against such imbalances did not respond until after significant damage had been done.

This phenomenon underscores the limitations of price-only oracles, particularly for stablecoins. A feed that targets a dollar parity may remain at or near one dollar until extreme market pressures or liquidity shortages force a re-quotation, even if underlying reserves are compromised or diluted. For assets whose stability depends on a specific reserve ratio, oracles that are blind to supply and collateral changes cannot fully capture solvency risk. A more robust approach would combine price data with reserve-aware metrics, such as on-chain information about collateral holdings, supply issuance, and mint/redeem activity, to detect anomalies like sudden supply spikes unaccompanied by collateral inflows.

The USR case also illustrates the systemic risks of assuming that oracles will always reflect market reality faster than adversaries can act. In the seventeen minutes during which the attacker minted and dumped unbacked USR, the combination of oracle lag, deep liquidity, and automated strategies created a window in which the exploit could be monetized before protective mechanisms kicked in. Protocol designers and oracle providers may need to consider explicit depeg detection logic, circuit breakers, and governance-controlled emergency switches that can respond to unusual patterns in supply, price, and on-chain activity, even when price feeds alone appear benign.

Stablecoin design trade-offs and the importance of collateral separation

The USR episode occupies an important place in the broader discourse about stablecoin design. Unlike purely algorithmic stablecoins that rely on endogenous tokens and reflexive market incentives for backing—such as the ill-fated TerraUSD—USR was designed to be backed by real collateral in the form of stablecoins and hedged positions, with a separate insurance token (RLP) absorbing losses. When the exploit occurred, this architecture meant that the collateral pool itself was not directly drained, and that, in principle, enough value remained to restore pre-exploit USR holders through snapshots and redemptions. This stands in contrast to cases where both the stablecoin and its backing asset collapse simultaneously, leaving no residual pool from which to compensate users.

At the same time, USR’s design collapsed two critical concerns—collateral custody and minting authority—into a single architecture where a compromised key could create claims far exceeding even a robust collateral base. Well-designed systems aim to ensure that, even if a minting key is compromised, the attacker cannot create tokens that are redeemable against reserves beyond a certain cap or without passing on-chain checks linked to collateral. In Resolv’s case, the lack of such checks allowed unbacked claims to proliferate, forcing the team to rely on post hoc governance and off-chain processes to determine which tokens would be honored at par. Future designs are likely to place greater emphasis on separating the control over collateral from the authority to issue claims against it.

The allocation of losses and compensation in the USR recovery plan also illustrates how capital structure design shapes crisis outcomes. Because RLP was explicitly marketed as the insurance layer, RLP holders were prepared—at least in theory—to bear losses before USR was impaired, which likely reduced the political and ethical friction around assigning them deeper haircuts. Governance tokenholders, meanwhile, accepted dilution through the allocation of 10% of RESOLV’s total supply to compensation, reflecting their ultimate responsibility for the protocol’s risk architecture. These mechanics may inform how future stablecoins structure their seniority tiers, ensuring that recovery paths exist and are understood by participants long before a crisis hits.

Resolv has been exploited, exploiter minted 50M $USR with 100K $USDC

Lol, this is no longer an exploit. This is a protocol's failure. Tf you mean minted 50m with 100k

USR in Practice: Use Cases, User Profiles, and Market Behavior

Pre-exploit use cases for traders and yield seekers

Before the exploit, USR appealed to a broad spectrum of DeFi participants seeking yield on dollar-denominated holdings. Retail users could swap USDC or other stablecoins into USR to access a higher yield than they might receive from passive holding, relying on Resolv’s collateral management and delta-neutral strategies to generate the additional return. For these users, USR functioned as a kind of “DeFi savings account,” offering a combination of stability and yield without requiring them to manage complex strategies themselves. The promise of “stable returns without directional market risk” was core to this value proposition.

More sophisticated participants integrated USR into multi-leg strategies, combining it with lending, leverage, and structured products. For instance, users could supply USR as collateral on a protocol like Fluid or Venus, borrow another asset, and loop the position to amplify yield or directional exposure. Others participated in liquidity provision by pairing USR with USDC or other stablecoins in DEX pools, earning fees and incentives while effectively betting that USR would remain pegged within a narrow range. Some strategies involved staking wstUSR, the staked derivative, to capture additional protocol rewards, reflecting a stacking of yield layers on top of the core USR instrument.

These use cases highlight how quickly a stablecoin can become entangled in complex strategies and risk profiles. For many users, USR was not just a passive stable asset but an input into recursive loops of leverage and yield, making their eventual losses and the need for recovery mechanisms more multifaceted than in simple spot holding scenarios. The diversity of user types—ranging from conservative savers to aggressive yield farmers—also complicated the design of fair compensation, as the same token played very different roles in their portfolios.

Protocol-level dependence and systemic importance

From a protocol perspective, USR’s stability and liquidity made it an attractive building block. Fluid integrated USR into its markets, allowing users to borrow and lend the asset and to use it as collateral, effectively giving USR a role akin to a core stablecoin within its system. Venus incorporated USR into its Flux markets, granting it similar status within BNB Chain lending markets. Inverse Finance used USR-backed liquidity as collateral for its DOLA stablecoin, layering one stable asset on top of another. These integrations not only boosted USR’s adoption but also made the health of USR a matter of systemic importance to those protocols.

The exploit revealed how such dependence can create difficult trade-offs during crises. Protocols had to decide whether to move quickly to protect their own users, potentially realizing losses and forgoing future upside from any recovery, or to wait and coordinate with Resolv’s remediation efforts. Fluid chose a proactive path, assuming responsibility for USR-related bad debt and raising external capital to cover users. Venus opted to isolate the risk by pausing USR markets, balancing user protection with a wait-and-see approach regarding Resolv’s recovery. Other protocols monitored from the sidelines, adjusting risk parameters and collateral factors where necessary.

These divergent responses will likely influence how future protocols assess the integration of newer or more complex stablecoins. The USR incident may push platforms to demand stronger guarantees about minting mechanisms, audit scope, and recovery plans before listing such assets as core collateral. It may also encourage the use of isolated markets, conservative collateral factors, and dynamic risk monitoring for non-blue-chip stablecoins, reducing the chances that a single exploit can propagate widely across DeFi.

Legal, regulatory, and reputational dimensions

Resolv’s structured response to the exploit, including formal notices issued under the name of Resolv Digital Assets Ltd. and cooperation with law enforcement and on-chain analytics firms, reflects an increasing convergence between DeFi operations and traditional legal frameworks. The team’s communications emphasized that the incident resulted from unauthorized third-party actions, that no underlying collateral was directly compromised, and that they were actively pursuing avenues to recover assets and hold responsible parties accountable. This framing is important not only for user reassurance but also for potential regulatory scrutiny, as authorities increasingly examine whether stablecoin issuers operate with adequate controls and incident response capabilities.

The reputational impact of the exploit on USR is significant and likely persistent. Even if pre-exploit holders are made whole and RLP and LP participants achieve partial recovery through the compensation program, the incident has fundamentally altered perceptions of USR’s risk profile and of Resolv’s design choices. The launch of Vault Street and primeUSD indicates an attempt to reposition the brand and product suite toward institutional markets, but any future stablecoin-like product emerging from the Resolv ecosystem will be evaluated through the lens of the March 22 event. Trust, once compromised, requires stronger evidence and stricter controls to be rebuilt.

At the same time, the transparency of the postmortem process, including detailed analyses by third parties like Chainalysis and independent researchers, may contribute positively to the broader ecosystem by surfacing lessons that other protocols can incorporate. The key question is whether those lessons will be internalized in concrete design changes—such as mandatory on-chain mint caps, multi-party key management, and reserve-aware oracles—or whether the industry will move on without substantive reform, leaving similar vulnerabilities in place elsewhere.

Outlook

USR’s trajectory from promising yield-bearing stablecoin to high-profile exploit victim to case study in recovery and redesign encapsulates many of the central questions facing DeFi today. Architecturally, USR showed that it is possible to build a layered system in which a senior stable asset is backed by real collateral and protected by an explicit insurance layer, offering a clearer capital structure than many contemporaries. Operationally, the exploit demonstrated that even well-audited on-chain code cannot compensate for weaknesses in off-chain key management and cloud infrastructure, especially when a single signer holds the power to mint unlimited tokens. Systemically, the integration of USR into lending markets, liquidity pools, and derivative structures amplified both its benefits and its risks, turning a key compromise into a sector-wide event.

Resolv’s response—combining fast protocol pauses, targeted burns, cooperative investigations, a structured three-month recovery program, and a strategic pivot toward institutional RWA products under Vault Street—offers a blueprint for how a protocol can attempt to navigate such a crisis. Pre-exploit USR holders have been prioritized for full redemption at par, while post-exploit holders, RLP participants, and LPs receive partial compensation calibrated to their position in the risk stack and funded in part by governance token dilution. Whether this approach will be viewed as successful in the long run will depend on how fully users are ultimately made whole, how robust future products prove to be, and how the broader market judges Resolv’s governance and security reforms.

For the wider stablecoin and DeFi ecosystem, the USR incident underscores the necessity of treating off-chain infrastructure as a first-class component of protocol security, the importance of designing minting flows that are resilient even under key compromise, and the need for oracles and integrated protocols to be reserve-aware rather than solely price-aware. It also highlights the value of clearly articulated capital structures that specify which tokens absorb losses and how recovery will proceed in adverse scenarios. As new products like primeUSD come online and as other protocols weigh the trade-offs of integrating complex yield-bearing stablecoins, USR’s rise, fall, and reconstruction will remain a reference point—both as a cautionary tale and as a source of hard-earned design insights.

Latest USR news

Chainalysis traces Resolv's $25M exploit to compromised AWS key that minted 80M unbacked USRResolv unveils a three‑month exploit recovery program for USR, RLP and LP users and launches Vault Street with its first leveraged institutional RWA product, primeUSD, while keeping RESOLV token utility and staking unchanged.Resolv has been exploited, exploiter minted 50M $USR with 100K $USDCFluid core team personally secures loans to cover 100% of bad debt from Resolv USR exploitAave sails clear of Resolv USR storm. Resolv's supplied assets hold steady in the protocol's hold; backing intact, graceful exit underway with debt repayments begun. No turbulence for Aave liquidity providers or protocol.Resolv reveals $25M exploit stemming from compromised contractor GitHub credential, 80M USR illicitly mintedSources

- https://resolv.xyz

- https://docs.resolv.xyz

- https://defiprime.com/resolv-usr-exploit

- https://x.com/ResolvLabs/status/2035830314799599616

- https://blockeden.xyz/blog/2026/04/21/resolv-labs-usr-stablecoin-exploit-aws-kms-key-compromise/

- https://www.binance.com/en/square/post/327493149117425

- https://www.binance.com/en/square/post/327360361575538

- https://www.mexc.com/news/980026

- https://x.com/VenusProtocol/status/2035579052317438340

- https://x.com/ResolvLabs/status/2038963136443600944

- https://www.chainalysis.com/blog/lessons-from-the-resolv-hack/

- https://resolv.xyz/blog/resolv-postmortem-march-22-2026-incident

- https://blog.kyberswap.com/post-mortem-kyberswap-elastic-exploit/

- https://coinmarketcap.com/top-stories/69c3a5d90bedf11830621fd4/

- https://www.facebook.com/cointelegraph/posts/-alert-resolv-labs-usr-stablecoin-loses-its-peg-after-an-attacker-exploits-its-c/1250243550615804/

- https://rekt.news/resolv-labs-rekt

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…