Fluid is a unified DeFi liquidity layer combining lending, high‑LTV vaults, and a capital‑efficient DEX, now central to stablecoin and institutional markets but tested by exploits, bad debt, and systemic risk across onchain finance.

+4 sources across the wider coverage universe

Hashi adds Cumberland, Fluid, and SwissBorg before July global testnet to unlock over $1T in dormant BTC2026-06

Hashi adds Cumberland, Fluid, and SwissBorg before July global testnet to unlock over $1T in dormant BTC2026-06 Fluid rolls out $1B-cap aWETH Redemption Protocol with Lido Finance, EtherFi, and 1inch to reduce systemic DeFi risk and unlock trapped ETH liquidity on Aave2026-04

Fluid rolls out $1B-cap aWETH Redemption Protocol with Lido Finance, EtherFi, and 1inch to reduce systemic DeFi risk and unlock trapped ETH liquidity on Aave2026-04 Avici launches “Grow” yield vaults and “Smart Credit” lending, letting users earn instantly and get paid to borrow USDC/EURC against SOL via Jupiter Lend and Fluid2026-04

Avici launches “Grow” yield vaults and “Smart Credit” lending, letting users earn instantly and get paid to borrow USDC/EURC against SOL via Jupiter Lend and Fluid2026-04 Fluid uses $8M DEX Lite credit line before DAO vote, shifting Resolv cleanup risk to USDC and USDT suppliers2026-05

Fluid uses $8M DEX Lite credit line before DAO vote, shifting Resolv cleanup risk to USDC and USDT suppliers2026-05 ⚠️ Fluid rewards exploit: attacker abused “empty-proof” Merkle claims after a key compromise to drain 125k FLUID and 51.9k GHO, swap and launder via Tornado Cash, while Fluid quietly paused claims without disclosing the loss.2026-05

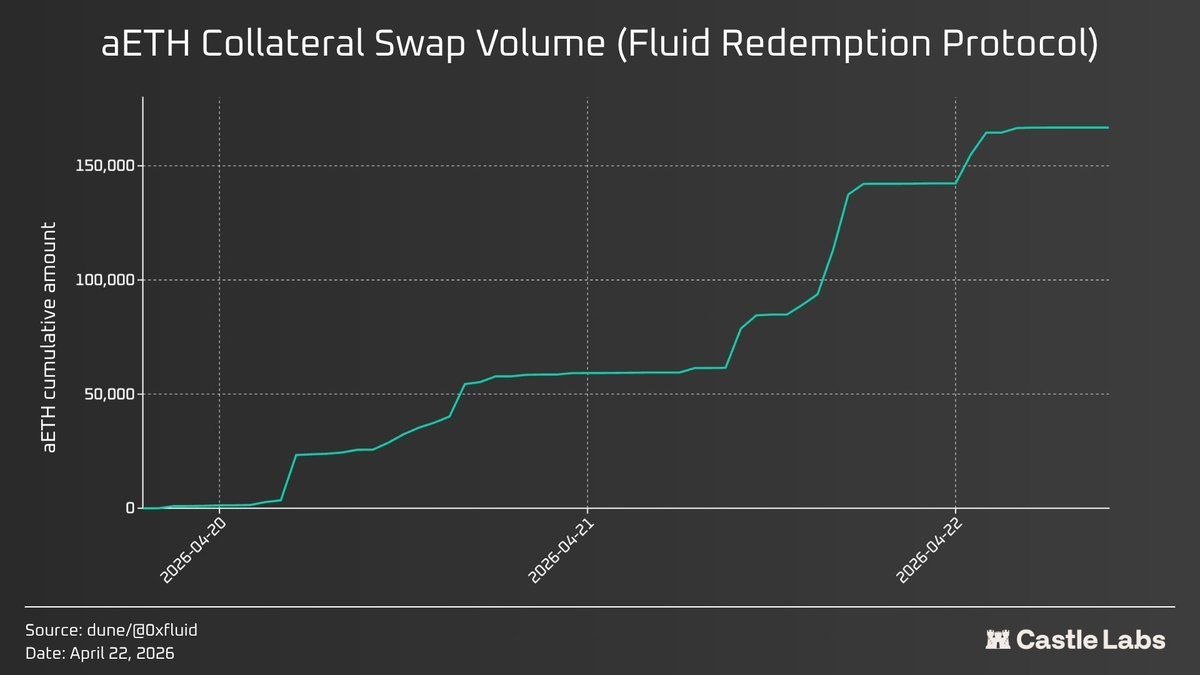

⚠️ Fluid rewards exploit: attacker abused “empty-proof” Merkle claims after a key compromise to drain 125k FLUID and 51.9k GHO, swap and launder via Tornado Cash, while Fluid quietly paused claims without disclosing the loss.2026-05 Fluid's aWETH redemption protocol clears 166,772 aETH ($400M) from Aave in two days2026-04

Fluid's aWETH redemption protocol clears 166,772 aETH ($400M) from Aave in two days2026-04

Fluid: A Unified Liquidity Layer Reshaping DeFi Lending and DEX Markets

Fluid is a decentralized finance protocol that combines a lending market, high‑LTV borrowing vaults, and a capital‑efficient DEX on top of a single shared liquidity layer. Built by the team behind Instadapp, it is designed to let users and other protocols lend, borrow, and trade against the same pool of assets while keeping risk controls, liquidations, and incentives tightly integrated.

Origins and Evolution: From Instadapp Middleware to Fluid Liquidity Layer

Fluid did not emerge as a standalone project in a vacuum; it is the culmination of several years of infrastructure work that began under the Instadapp brand. Instadapp initially positioned itself as a middleware and smart‑wallet layer that allowed users and protocols to route liquidity across major DeFi platforms such as MakerDAO, Aave, and Compound. Over time, as DeFi markets matured and gas costs, fragmentation, and cross‑protocol risk became more visible, the team’s focus shifted from aggregation to building a foundational liquidity layer that other applications could build on directly. This strategic evolution set the stage for Fluid as a native protocol rather than merely a routing interface.

The rebranding from Instadapp to Fluid was framed in governance discussions as a way to align the protocol’s identity, tokenomics, and roadmap with its new role as a “liquidity layer” rather than a toolkit or dashboard. In the rebrand proposal, the team emphasized capital efficiency, advanced liquidation mechanisms, and a design where lending and DEX functions are structurally fused rather than glued together via external integrations. The same document highlighted that Fluid had already surpassed roughly one billion dollars in market size, with the vast majority of activity concentrated on Ethereum and growing largely via organic usage rather than short‑term incentives. That context matters because it shows that Fluid’s trajectory was driven by usage patterns that validated the unified liquidity thesis before token branding caught up.

An important aspect of the transition was that existing Instadapp governance and token holders were not left behind. The governance proposal specified that the INST token would seamlessly convert to FLUID at a one‑to‑one ratio, preserving the same token contract address and total supply of one hundred million tokens on Ethereum. Holders did not need to perform manual swaps or migrations; instead, the protocol simply updated the token’s branding and economic logic while keeping the underlying address and supply intact. This approach aimed to avoid the confusion and fragmentation that often accompany token migrations while allowing a fresh start for narrative and incentive design.

Fluid’s ambition goes beyond incremental improvements in lending UX or yield optimization. Governance materials explicitly outline a vision to become a “liquidity layer” serving the broader DeFi ecosystem, with milestones such as reaching ten billion dollars in market size and becoming the largest DEX on Ethereum by volume within a relatively short time horizon. That vision is not purely aspirational: according to governance and external research, Fluid’s DEX rapidly climbed to the upper ranks of Ethereum spot trading, at one point becoming the third largest DEX by volume with just a handful of pools live and projecting a path to second place as more markets launched. This trajectory is central to understanding why other protocols, stablecoin issuers, and even real‑world asset platforms have started to treat “Fluid‑powered” markets as infrastructure rather than a niche venue.

The broader market environment also shaped Fluid’s evolution. Since late 2025, deposits in major crypto lending protocols have contracted sharply, with outflows concentrated at large incumbents such as Aave, Spark, and Euler. In that environment, protocols that offered materially higher capital efficiency, integrated trading, or novel forms of risk management began to see inflows as users rotated away from platforms perceived as more exposed to exploit‑driven bad debt or inefficient collateral parameters. Fluid’s growth in total value locked, including notable weekly surges during periods of broader market stress, needs to be understood against that backdrop of rotation and consolidation in the lending sector. The protocol is trying to prove that a tightly coupled liquidity layer can preserve user safety while still delivering higher utilization and yield than siloed venues.

Hashi adds Cumberland, Fluid, and SwissBorg before July global testnet to unlock over $1T in dormant BTC

Sui says Cumberland, Fluid, and SwissBorg have joined Hashi, its native Bitcoin finance primitive, weeks before a July global testnet. The bet is to turn over $1T of idle BTC into verifiable collateral without moving Bitcoin off its native chain: Sui smart contracts handle the programmatic rights, while the partner stack covers custody, liquidity, lending, oracles, insurance, and audits. It is an institutional BTCfi push, but still testnet-first; the real signal comes when liquidity and borrowers show up on mainnet.

Readers track Fluid almost entirely through its governance and token-economic moves — multichain incentive packages, the $INST→$FLUID rebrand, and DAO debt-coverage votes — revealing that the protocol's credibility is being stress-tested at the governance layer, not the smart-contract layer.↗

Core Architecture: Liquidity Layer, Lending, Vaults, and DEX

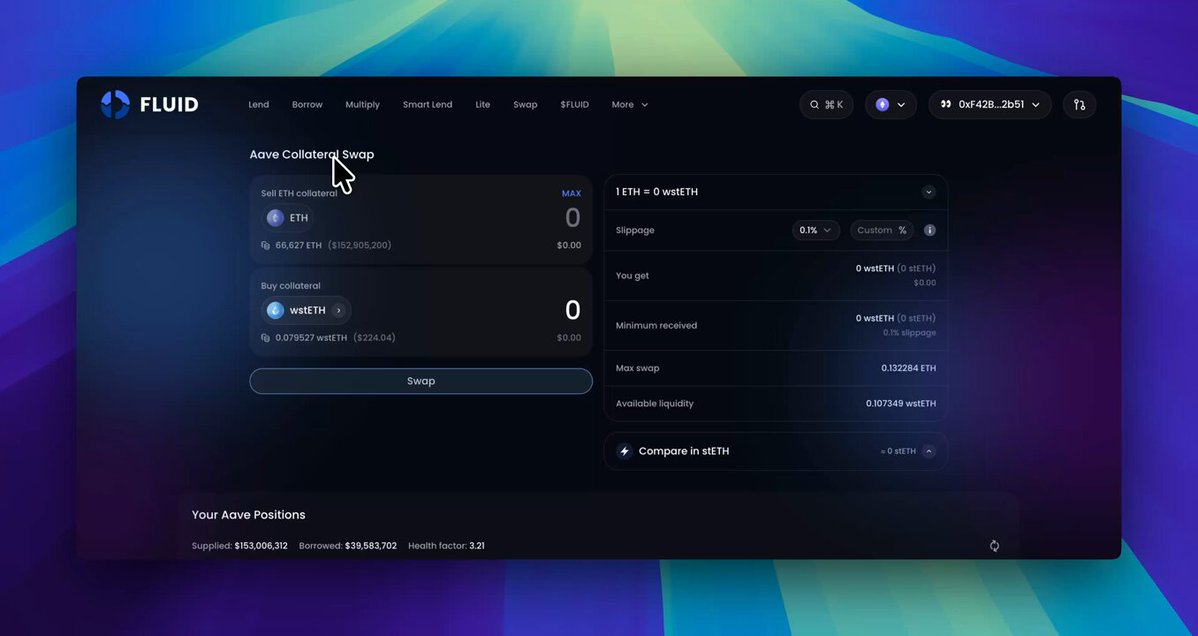

At the heart of Fluid lies a single on‑chain “Liquidity” contract that holds user funds and interfaces with the various protocol modules built on top of it. Unlike legacy DeFi designs where each market or product maintains its own pool of liquidity, Fluid’s architecture consolidates deposits into this core contract and then exposes them through different abstractions: a straightforward lending market, a vault‑based borrowing system, and a DEX that is aware of collateral and debt positions. Ordinary users do not interact with the Liquidity contract directly; instead, they deposit via ERC‑4626‑style vault tokens or open vaults and trades through higher‑level interfaces. This separation between the core pool and the user‑facing protocols is central to the project’s claim of unified liquidity.

One of the practical advantages of this design is that the same underlying capital can simultaneously support lending, borrowing, and trading, subject to risk parameters, without being idle in isolated pools. In traditional DeFi deployments, a user who provides liquidity to a DEX pool cannot at the same time have that capital deployed as collateral for a loan unless they first deposit the LP token into a separate lending protocol, adding complexity and smart‑contract risk. Fluid’s approach, in contrast, allows collateral to earn LP fees directly within the system while also backing loans or leveraged positions, because all those activities plug into the same balance sheet. This concept of “shared liquidity with multiple roles” is key to understanding why Fluid claims to improve capital efficiency relative to both standalone DEXes and standalone money markets.

However, unifying liquidity also increases the importance of internal accounting and risk boundaries. If a flaw in the DEX logic could drain assets from the Liquidity contract, the effect would propagate immediately to lenders and borrowers. Fluid’s technical documentation repeatedly emphasizes that view functions and periphery logic are kept outside the core contracts to minimize attack surface and that strict interaction patterns govern how modules call into the liquidity layer. Even so, the project’s own materials and risk disclosures acknowledge that users face smart contract risk, market risk, and the potential for complete loss of funds, as is the case for virtually all DeFi protocols operating without deposit insurance or off‑chain guarantees. The architecture’s strengths and weaknesses therefore hinge on whether its segregation of functionality within a single liquidity pool is robust enough to withstand both direct exploits and emergent behavior during stress events.

The unified structure also underpins Fluid’s approach to pricing, interest rates, and liquidations. Because lending and trading all tap into the same liquidity, interest rate curves and pool utilization metrics can be tuned to reflect not only borrowing demand but also trading volumes and LP fee flows. Documentation describes a framework in which the lending protocol and vault protocol are effectively two lenses on the same underlying funds, with fTokens representing claims on the liquidity pool and vaults representing collateralized borrowing positions against that pool. This means that when a large trade or liquidation event occurs on the DEX, it can immediately impact utilization, rates, and collateral health in a way that is visible to the entire system. The hope is that this tight coupling allows for faster, more transparent rebalancing compared to architectures where exchanges and money markets are siloed.

The Liquidity Layer and fToken Lending

Fluid’s lending layer is positioned as the most straightforward entry point for users, described in the project’s documentation as a simple “Lend and Earn” protocol intended to generate long‑term, sustainable yields. Users deposit assets into lending markets and receive ERC‑4626‑compliant fTokens in return, representing pro‑rata claims on the liquidity pool plus accrued interest. These fTokens function similarly to cTokens or aTokens in other money markets, but they are explicitly designed as the canonical interface to the Liquidity contract. They can, at least in principle, be used by external protocols as collateral or building blocks for other strategies, just as DeFi has done with interest‑bearing tokens from earlier platforms.

The lending protocol is marketed as a way to access the liquidity layer directly, without needing to understand more complex vault mechanics or DEX interactions. From a user’s perspective, the flow is familiar: deposit assets such as ETH, stablecoins, or liquid staking tokens, and then earn yield driven by borrowing demand, protocol fees, and possibly additional incentives from governance. Under the hood, however, those deposits can be allocated to support vault borrowing and trading liquidity at the same time, which potentially enhances yields compared with a pure lending setup where returns come almost entirely from interest paid by overcollateralized borrowers. That said, it also means lenders are indirectly exposed to the risks of the DEX and vaults, because all three modules draw from the same capital base.

The protocol’s risk disclosures explicitly remind users that even seemingly “safe” deposit‑and‑earn strategies carry smart contract risk, oracle risk, and market risk, including the possibility of total loss. These cautions have proved prescient across DeFi: the collapse of ostensibly conservative pools in other protocols has shown that yield from lending markets is only as solid as the assumptions baked into interest rates, collateral parameters, and liquidation incentives. Fluid’s approach adds another layer, because its lending yields are intertwined with the DEX’s fee dynamics and any ongoing incentive programs on top of base rates. The architecture can therefore deliver relatively attractive returns in benign markets, but the same linkages can feed volatility back into lending yields when trading or vault activity becomes stressed.

Vault Protocol: High‑LTV Borrowing and Liquidation Design

On top of basic lending, Fluid offers a vault‑based borrowing system modeled conceptually on MakerDAO‑style collateralized debt positions, but with several significant upgrades. The vault protocol allows users to lock a single collateral asset and borrow a single type of debt asset against it, with the maximum loan‑to‑value ratio determined by oracle‑driven collateral pricing and protocol risk parameters. Governance and documentation highlight that Fluid aims to offer unusually high loan‑to‑value ratios—up to around 95 percent on some collateral types—while keeping liquidation penalties relatively low compared with legacy systems. That combination makes the vaults attractive to sophisticated users seeking leverage but also increases reliance on accurate pricing, reliable oracles, and responsive liquidator participation.

The vault design builds on lessons from earlier generations of DeFi lending. Rather than requiring users to manage multiple collateral types in a single position, the protocol uses the familiar pattern of “one collateral, one debt” per vault, simplifying accounting and enabling more targeted risk controls per market. At the same time, Fluid adds what it describes as “smart collateral” and “smart debt” features when vaults are combined with the DEX, meaning that a position’s collateral can be dynamically placed into LP strategies or otherwise optimized without exiting the borrowing arrangement. This allows a user, for example, to deposit a yield‑bearing token or LP token as collateral, borrow against it, and still earn fees or staking rewards on the underlying, effectively stacking multiple yield streams on a single base asset.

Liquidation is a critical piece of this system. Fluid emphasizes an “advanced liquidation mechanism” that aims to reduce the cost and slippage associated with closing under‑collateralized positions, particularly in volatile markets or for large positions. While different markets may have different parameters, research and exchange reporting on Fluid V2 underline that the protocol targets liquidation penalties as low as approximately 0.1 percent in some configurations, far below the double‑digit penalties historically common in protocols like MakerDAO. In theory, such low penalties should make forced deleveraging less painful for users while still compensating liquidators for executing timely trades. In practice, however, maintaining such thin margins depends on a deep, liquid DEX and robust arbitrage participation, which is why the DEX module is tightly intertwined with vault operations.

Fluid DEX and Flash Accounting: Trading on a Unified Pool

Fluid’s DEX is arguably the most distinctive element of the protocol, because it effectively embeds a spot exchange into the same architecture that powers lending and vault borrowing. Rather than treating liquidity provision as a separate activity with its own tokenized LP shares detached from the lending markets, Fluid allows users’ collateral or borrowed assets to serve as liquidity in trading pools, generating fees while they simultaneously back loans or leveraged positions. This arrangement is meant to reduce idle capital, increase capital efficiency, and blur the distinction between “LPs” and “borrowers” by having both roles draw from the same liquidity.

From a market‑structure perspective, Fluid’s DEX has quickly become a meaningful venue on Ethereum. Governance materials from 2024–2025 describe how, within just three weeks of launch, Fluid’s DEX had processed over one billion dollars in trading volume and climbed to the third‑largest spot DEX on Ethereum by volume, with only three pools live at the time. Later communication from the protocol and external research notes that by Q4 of a subsequent year, Fluid’s DEX had facilitated roughly 54.2 billion dollars in quarterly volume and was vying for second place among Ethereum DEXes. More recent exchange analysis reports that by the time Fluid V2 was preparing to launch, the protocol had processed more than two hundred billion dollars in cumulative trading volume, solidifying its status as the second‑largest DEX on Ethereum. Those numbers indicate that the DEX is not merely a side feature of a lending protocol but a core venue in its own right.

The key technical innovation in Fluid DEX V2 is what the project calls “Flash Accounting.” According to exchange research and protocol materials, Flash Accounting consolidates all trading pools into a single contract and defers token transfers until the end of a transaction, settling only the net amounts owed after internal offsets. In practice, that means that if a user performs several swaps, opens or closes vault positions, and rebalances collateral in one transaction bundle, the protocol need not move tokens back and forth between multiple pool contracts for each step. Instead, it tracks the state transformations virtually during execution and applies the minimal set of actual transfers at the end. This reduces gas overhead, simplifies capital accounting, and makes it easier for the protocol to treat all liquidity as part of a single shared balance sheet.

The connection between Flash Accounting and risk management is subtle but important. By tracking positions across lending, vaults, and trading inside one unified accounting engine, Fluid can theoretically liquidate or rebalance accounts more efficiently and with less slippage, because it can offset trades internally before touching external markets. At the same time, the more operations that are wrapped into one contract, the higher the stakes if that contract is compromised or mis‑parameterized. That is why Fluid’s documentation and independent reviews stress the importance of modularizing view logic and of careful governance over system parameters, as any bug or misconfiguration in the unified DEX could reverberate through the lending and vault layers. The architecture offers powerful composability, but it also concentrates technical risk.

Products and Integrations: Stablecoins, Yield Vaults, and “Fluid‑Powered” Markets

Beyond its core lending and DEX primitives, Fluid has increasingly emphasized a product strategy that makes it easy for both end users and other protocols to access stablecoin yields, fixed‑rate vaults, and white‑label lending markets. Stablecoins such as USDC, USDT, and GHO play a central role in this ecosystem, serving as the primary borrowing currency in many vaults and as base assets in high‑liquidity DEX pools. Fluid’s architecture allows these stablecoins to circulate between lending, collateral, and trading roles within the same liquidity layer, which opens up opportunities for structured products and integrations that abstract away the underlying complexity.

One of the flagship offerings in this vein is the Fluid Lite USD Vault, which the team introduced as a fixed‑rate, cross‑chain vault designed to deliver what it describes as “the best risk‑adjusted yield on stablecoins.” Promotional materials characterize Lite USD Vault as fully automated: users simply deposit stablecoins, and the protocol routes those funds into yield strategies while handling cross‑chain bridging, rate management, and rebalancing under the hood. Although detailed documentation on the vault’s strategy mix is limited in public posts, the messaging suggests that Lite USD Vault is meant as a simplified front door for users who want stablecoin yield without actively managing positions in lending markets or leveraged basis trades. Because it is built directly on Fluid’s liquidity layer, the vault’s performance depends heavily on the protocol’s risk management and the health of its underlying markets.

Synthetic dollar products and restaking‑based dollars have also found a home on Fluid’s infrastructure. For example, the USDAI project, which issues a yield‑bearing synthetic dollar, has publicly highlighted that Fluid has become the dominant venue for its staked USDAI (sUSDAI) token. Since around mid‑February of a recent year, USDAI’s team reported that Fluid captured approximately 60 percent of the entire sUSDAI supply, a shift they described as rapid and notable in their upcoming quarterly report. That concentration signals both a vote of confidence in Fluid’s liquidity layer and a risk factor: if the majority of a synthetic dollar’s staked supply is parked in one protocol, shocks to that protocol can propagate directly to the stablecoin’s holders and peg dynamics.

Fluid’s role as an infrastructure provider is further underscored by partnerships with emerging “crypto neobank” and yield platforms. Avici, for instance, launched its Grow and Smart Credit products in collaboration with Jupiter Lend and Fluid. According to exchange news, Avici Grow allows users to deposit assets and earn yield with no lock‑up period, while Smart Credit enables instant borrowing of USDC or EURC against SOL collateral, with the twist that the SOL continues to earn yield while serving as collateral. Fluid appears in this stack as the underlying lending and liquidity engine that makes the “borrow and earn” model possible, demonstrating how protocols can layer branded user experiences atop Fluid’s core primitives without having to build an entire lending and DEX system themselves.

Similarly, other protocols have launched “Fluid‑powered” markets that embed Fluid’s vault and lending logic into their own ecosystems. Research by independent auditors notes that Fluid’s vault contracts are designed to utilize liquidity from multiple sources and to protect users from abrupt fund movements by controlling how and when liquidity can be shifted between vaults and borrowing markets. This design is attractive for platforms like Venus‑style vaults or RWA issuance protocols that want to tap deep on‑chain liquidity without taking on the full complexity of designing liquidation and rate curves from scratch. In practice, these integrations mean that when users interact with branded frontends such as new “Flux” vaults or institutional lending desks, their positions may ultimately be backed by Fluid’s liquidity layer.

Stablecoins remain central to the story. USDC and USDT are the primary sources of dollar liquidity in many DeFi systems, and Fluid is no exception. In normal times, these assets serve as base currencies in DEX pools and as the primary debt tokens in borrowing markets, providing the reference unit for yield calculations and leverage. In times of stress, however, they can also become the shock absorbers for protocol‑level bad debt. During the cleanup following the Resolv USR exploit, for example, internal reporting and governance debates highlighted tensions over how much of the burden for repaying USR‑related bad debt should fall on USDC and USDT suppliers via mechanisms such as DEX Lite credit lines. Those debates illustrate that while stablecoins can provide stability at the user level, their role inside the protocol balance sheet is far from risk‑free.

- 01Arbitrum multichain expansion↗

The combination of a live governance proposal and 400k $ARB incentives made this the most concrete near-term alpha on the page, drawing nearly 4× more clicks than any other story.

- 02$INST to $FLUID rebrand↗

Token rename proposals directly threaten existing holder value and unlock airdrop speculation, reliably pulling readers who need to decide whether to hold, sell, or accumulate.

- 03Bad debt and exploit accountability↗

Three separate incidents — rewards-contract key compromise, Resolv USR bad debt covered personally by the core team, and unilateral use of an $8M credit line before a DAO vote — gave readers a running accountability scoreboard for who absorbs losses.

- 04Capital-efficiency DEX design↗

The 'most capital-efficient exchange' framing and v2 Smart Collateral/Smart Debt range features positioned Fluid as a direct challenger to incumbent AMMs, attracting readers benchmarking against Uniswap and Curve.

- 05Cross-protocol partnerships and integrations↗

Venus Flux on BNB, Jupiter Lend on Solana, and the Lido/EtherFi/1inch aWETH redemption protocol each represented new TVL surfaces, and readers clicked to gauge whether Fluid's liquidity was genuinely expanding or just being recycled.

- 06Curve community rivalry and dev drama↗

The 'Low IQ' jab at the Curve community condensed an ongoing narrative about Fluid's aggressive positioning into a single quotable moment that functioned as social proof of competitive tension.

Risk Management, Liquidations, and Systemic DeFi Events

Given its ambition to be a core liquidity layer rather than a single‑purpose application, Fluid sits at the center of several recent stress events in DeFi. The protocol’s handling of liquidations, its collaboration on escape‑hatch mechanisms, and its exposure to external stablecoin exploits all provide insight into how its risk management philosophy works in practice. At a high level, Fluid combines parameter‑based safeguards such as borrowing ceilings and collateral haircuts with more structural tools like stETH redemption and aWETH unwinding to try to minimize systemic risk while still offering aggressive capital efficiency.

Liquidation Mechanics and Capital Efficiency under Stress

Fluid’s promise of high loan‑to‑value ratios and low liquidation penalties requires a liquidation system that can function reliably even during sharp market dislocations. The protocol’s vaults, as described earlier, are structured to give users the ability to borrow up to roughly 95 percent of the value of their collateral in some markets, a level far above the more conservative thresholds common in older lending platforms. To make that feasible, Fluid relies on accurate price oracles, a DEX with deep liquidity for relevant pairs, and incentives that ensure liquidators can close positions quickly without incurring excessive slippage.

Reports on Fluid V2 stress that its Flash Accounting design is meant to make liquidations more capital efficient by allowing internal netting of trades across the liquidity layer before hitting external markets. If a user’s collateral and debt can be offset within the system at near oracle prices, then the protocol can keep liquidation penalties extremely low—on the order of 0.1 percent in some envisioned configurations—because the risk of poor execution is reduced. However, if oracles are manipulated, internal liquidity dries up, or external markets become disorderly, the system may have less room to maneuver than protocols that impose heavier cushions and penalties. High LTV designs inherently push risk closer to the edge; the question is whether the protocol’s dynamic ceilings and real‑time monitoring are sufficient to pull back before losses crystallize.

Fluid’s behavior during the Resolv USR incident provides a concrete example of its parameter‑based defenses. When Resolv’s USR stablecoin was exploited and began to depeg sharply, Fluid’s automated borrowing ceilings on USR markets kicked in to limit further exposure, and the protocol paused USR markets to prevent additional borrowing against the compromised asset. In post‑incident communication, the team emphasized that these safeguards “worked as intended” to contain the situation and committed that any remaining bad debt would be covered such that user losses would be fully compensated. While ceilings and pauses cannot retroactively prevent losses that have already occurred, they can prevent a cascade of new positions from compounding the damage once an exploit is detected.

Aave Escape Hatch: aWETH and stETH Redemption Protocols

One of Fluid’s most visible contributions to DeFi risk management has been its work on unwinding large, illiquid leveraged positions in other protocols. The project’s stETH Redemption Protocol, for example, is designed as a specialized mechanism for deleveraging stETH/ETH positions at a one‑to‑one rate with Lido, using short‑term loans to avoid dumping large amounts of stETH into open markets. According to Fluid’s technical documentation, this approach can reduce the transaction cost of unwinding such positions by up to an order of magnitude compared with traditional market selling, because it sidesteps slippage and MEV extraction by routing redemptions directly through Lido.

Building on that experience, Fluid launched an aWETH Redemption Protocol in collaboration with Lido, Ether.fi, 1inch, and multiple other DeFi players to help clear frozen WETH positions on Aave. After an event in which a large number of aWETH positions on Aave became effectively stuck due to parameter freezes and risk concerns, the escape‑hatch protocol allowed users to redeem their aWETH for underlying ETH or liquid staking derivatives in a controlled manner. According to coverage by The Defiant, Fluid’s aWETH Redemption Protocol processed roughly 136 million dollars’ worth of Aave’s frozen WETH in the first forty‑eight hours alone, working alongside routing partners such as 0x and Kyber to keep markets functioning. Subsequent reporting indicates that the protocol later expanded its capacity to handle hundreds of millions of dollars in trapped positions, demonstrating the scale at which Fluid aims to operate as systemic infrastructure rather than just a self‑contained app.

These redemption mechanisms exemplify Fluid’s strategic positioning. By offering tooling that helps other major protocols unwind risk without blowing out on‑chain markets, Fluid deepens its relationships with both end users and institutional actors who depend on orderly liquidations. At the same time, it exposes the protocol to complex counterparty and operational risk: if a redemption mechanism misprices assets, misroutes flows, or encounters a bug while handling hundreds of millions of dollars, the impact could be severe. The success of the aWETH and stETH redemption efforts to date helps build Fluid’s reputation as a risk‑aware architect, but each such mechanism also increases the protocol’s systemic importance and therefore the stakes of any future failure.

The Resolv USR Exploit and Fluid’s Bad Debt Response

The Resolv USR exploit in early 2026 provides a detailed case study of how Fluid deals with external stablecoin failures and the resulting bad debt. According to an incident report by Nexus Mutual, the trouble began when an attacker deposited roughly two hundred thousand dollars in USDC into the Resolv protocol and, due to a critical flaw, was able to mint around eighty million USR stablecoins in return. Within minutes, USR’s price collapsed from its one‑dollar target to a few cents on Curve, as the attacker dumped freshly minted USR into various markets including Curve, KyberSwap, Uniswap, and Velodrome, extracting an estimated twenty‑three to twenty‑five million dollars in value. The exploit left a large portion of USR unbacked and triggered a cascade of effects in protocols that had integrated the asset as collateral.

On Morpho, Nexus Mutual reports, several USR and wrapped‑USR collateral markets ended up at one hundred percent utilization with zero available liquidity, locking in roughly 7.8 million dollars’ worth of lending exposure. Fluid faced a related but distinct problem: because USR had been integrated into its own markets, the depeg left some users with loans or positions that could not be fully covered by the now‑impaired collateral. Fluid confirmed that it had incurred bad debt as a result and publicly committed to covering its users’ losses in full. Shortly after the incident, the team activated its automated ceilings and paused USR markets, which limited further accumulation of exposure and effectively quarantined the problem.

The question then became how, and over what time frame, the protocol would make affected users whole. Coverage from centralized exchanges and DeFi media describes a multi‑step repayment campaign, in which the Fluid core team and external partners secured short‑term loans to cover one hundred percent of the bad debt currently in the protocol, ensuring that no user funds were at risk despite the hole left by the USR collapse. Subsequent announcements from Fluid confirmed that the protocol had repaid approximately seventy million dollars’ worth of USR‑related debt as of March 25, 2026, emphasizing that repayments would continue until all outstanding obligations were cleared. However, Fluid did not disclose the total size of its USR‑related liability, which means users and observers cannot yet calculate what percentage of the eventual hole has been filled and how much remains.

This opacity illustrates a tension in DeFi between rapid crisis response and transparency. On the one hand, Fluid’s ability to mobilize capital and repay tens of millions of dollars in bad debt, including around twenty‑one million dollars of fully recognized bad debt in a relatively short period, demonstrates an operational capacity and willingness to socialize losses that many protocols lack. On the other hand, the absence of a clear, public liability figure complicates independent risk assessment and makes it difficult for depositors to gauge the protocol’s residual exposure to USR. The Resolv episode thus serves both as a proof point for Fluid’s crisis management and as a reminder that even sophisticated risk architectures remain vulnerable when integrating external assets whose own security assumptions fail.

Bridge Exploits, rsETH, and System‑Level Contagion

Fluid’s risk environment is also shaped by exploits that do not directly target its contracts but nonetheless reshape DeFi markets in which it participates. The 2026 KelpDAO/LayerZero exploit involving the restaking token rsETH offers a vivid example. According to research from Galaxy Digital, the attacker exploited a critical weakness in KelpDAO’s use of LayerZero’s omnichain fungible token bridge, delivering a forged packet that caused the bridge adapter to release about 116,500 rsETH from Ethereum mainnet escrow in a single transaction. The stolen rsETH, worth roughly 290 million dollars at the time, was then deposited as collateral on protocols including Aave, Compound, and Euler, against which the attacker borrowed an estimated 236 million dollars in WETH and wstETH.

The fallout was severe across the DeFi landscape. Aave’s emergency guardians froze rsETH and wrapped‑rsETH markets across all deployments and, for a time, froze WETH markets on multiple networks, while primary stablecoin markets hit one hundred percent utilization, leaving no liquidity for withdrawals. Galaxy’s analysis estimates that Aave alone faced potential bad debt on the order of 120 to 230 million dollars depending on how losses were socialized between mainnet and L2 markets. DeFi’s total value locked dropped by around thirteen to fifteen billion dollars in the days following the exploit, with lending protocols bearing the brunt of outflows even when they had no direct rsETH exposure.

Fluid’s position in this environment is twofold. First, as a lending and DEX protocol integrated into the broader restaking and liquid staking ecosystem, it must constantly assess the risk of accepting assets like rsETH as collateral or trading pairs. Second, as a provider of infrastructure for other protocols and institutional products, it must consider how upstream bridge designs and multisig security can create systemic vulnerabilities that eventually flow into its own balance sheet. The rsETH exploit underlines that even if a protocol like Fluid maintains robust contracts and governance, it can still be impacted by failures in assets it adopts, particularly when those assets are wrapped or bridged across chains. The lesson for Fluid and its users is that asset listing and collateral frameworks must take into account not only on‑chain price volatility but also off‑chain governance and bridge security assumptions.

Governance, Tokenomics, and FLUID Incentives

Fluid’s economic design and governance structure are central to how it attracts liquidity, funds growth, and aligns incentives between users, the core team, and external partners. The rebrand from Instadapp to Fluid was not only a cosmetic shift but also an opportunity to introduce new tokenomics, a revamped growth plan, and an explicit buyback‑driven value accrual model tied to protocol revenue. Understanding these mechanics is important for anyone evaluating FLUID as a governance and incentive token.

FLUID Token Basics and Instadapp Conversion

At the technical level, FLUID is simply a rebranded INST token with the same contract address and total supply. Governance documentation makes clear that INST holders were to be converted one‑to‑one into FLUID, with no change to the underlying token contract on Ethereum and no need for user‑initiated migration. The total supply remains fixed at one hundred million tokens, and the choice to reuse the existing contract address is meant to preserve the continuity and track record of the original governance token while aligning the name with the new protocol identity.

This approach has several implications. It avoids creating a new token that might fragment liquidity or confuse users, and it allows exchanges, index providers, and custodians to maintain continuity by simply updating labels and tickers. At the same time, it means that any historical distribution issues or concentration of holdings in the INST era carry over into the FLUID era; the rebrand does not reset governance or ownership patterns. Instead, the new tokenomics are implemented via governance decisions on treasury allocations, incentives, and buybacks rather than via a new supply schedule or token contract.

Treasury Strategy, Growth Plan, and Buybacks

Fluid’s governance proposal articulated a concrete plan for deploying treasury resources to accelerate growth. Specifically, it called for allocating around twelve percent of the governance treasury to key initiatives such as exchange listings, market‑making support, fundraising‑related activities, and team expansion. Rather than distributing these tokens directly to users as generalized liquidity mining rewards, the plan emphasizes using treasury resources to improve market access, deepen liquidity for FLUID itself, and fund development and operational capacity. This reflects a shift from the indiscriminate yield farming era toward more targeted, strategic spending to build durable infrastructure and partnerships.

The protocol also committed to establishing and maintaining FLUID liquidity on DEXes by dedicating around five percent of the total token supply to seeding liquidity pools. According to governance discussions, approximately half of that allocation—about 2.5 percent of the supply—was already being used to support trading liquidity, with the remainder available for future deployment or to be returned to the DAO if not needed. By placing treasury‑owned liquidity in wide ranges and capturing LP fees, Fluid aims to generate revenue for the DAO while stabilizing the token’s on‑chain markets and lowering slippage for large trades.

A notable feature of Fluid’s tokenomics is its revenue‑linked buyback program. The governance proposal outlines a mechanism under which, once the protocol achieves ten million dollars in annualized revenue, a dynamic fraction of earnings of up to one hundred percent can be used to buy back FLUID on the open market. The buyback function is described as following an “x * y = k” model, implying a curve that adjusts buyback intensity based on the token’s fully diluted valuation to optimize value accrual without pushing prices excessively. Any funds not used for buybacks in a given period are to be returned to the governance treasury, maintaining flexibility. Public reporting from Fluid’s Chinese‑language community account indicates that by early 2026, approximately 4.18 million dollars had already been deployed to FLUID buybacks, corresponding to about 1.08 percent of total supply and 1.39 percent of circulating supply at that time. Those figures suggest that the buyback policy is not merely theoretical but an active component of the protocol’s economic strategy.

Reward Programs, Merkle Trees, and the 2026 Rewards Exploit

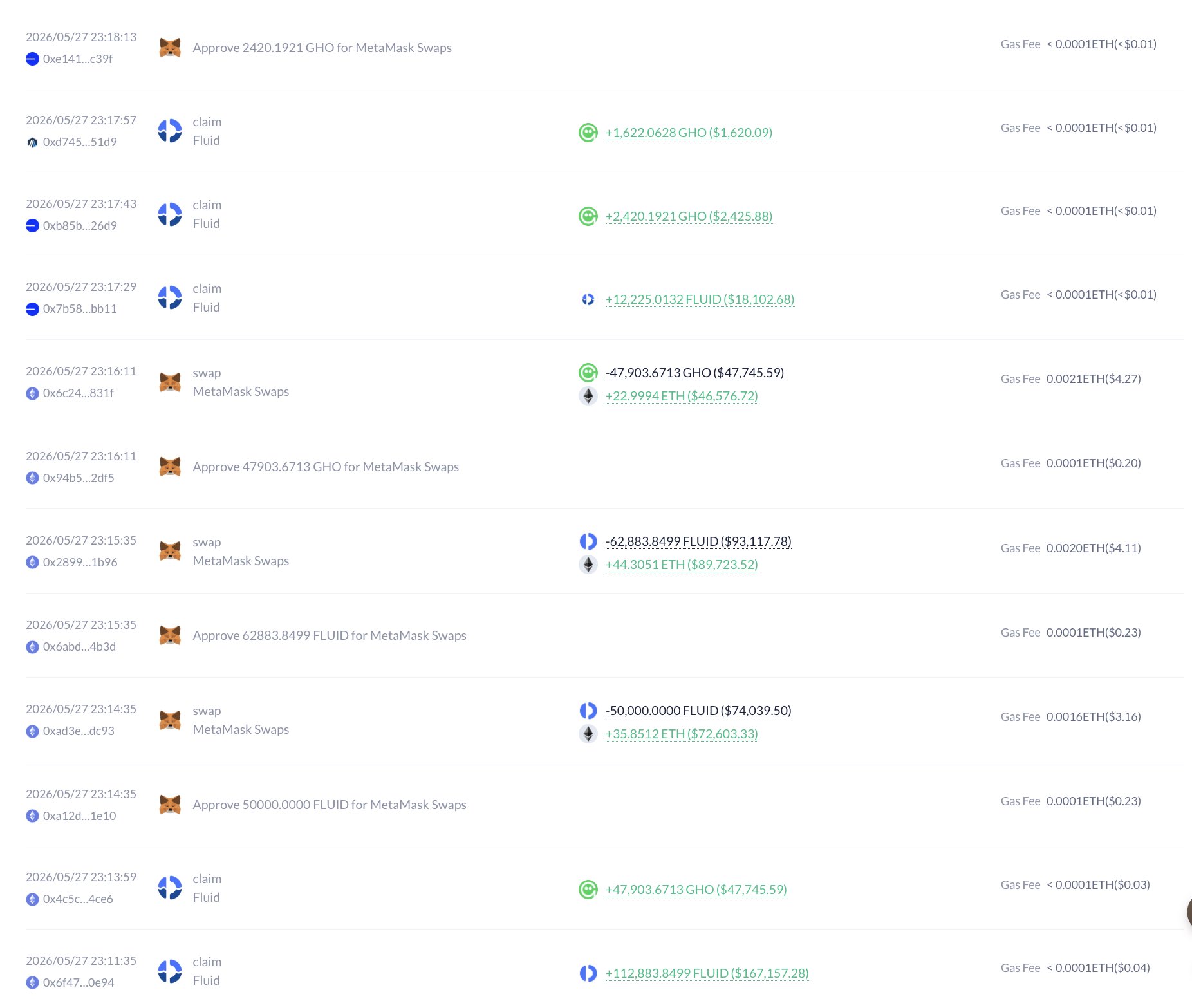

While Fluid’s core protocol contracts have so far avoided major exploit‑driven losses, the project did experience a significant security incident related to its off‑chain rewards distribution infrastructure. In early 2026, a compromise of the Merkle rewards process used for distributing FLUID and other tokens exposed what observers described as a critical control‑path failure. According to forensic analysis summarized by CoinStats, the rewards system relied on a two‑step model in which one key proposed a Merkle root defining eligible reward recipients and amounts, and a second key approved that root before users could claim. The idea was that no single compromised key could unilaterally push a malicious reward distribution.

In practice, the attacker managed to obtain control of both roles. They submitted a reward list that effectively routed rewards only to their own wallet, used the second key to approve that list, and then executed claims using an “empty‑proof” Merkle claim method that bypassed the intended restrictions. The drain affected three reward distributors and resulted in the theft of approximately 112,883 FLUID, 47,903 GHO, and a small amount of cbBTC, with later public tallies estimating the broader movement at around 125,000 FLUID and 51,900 GHO. The stolen assets were subsequently swapped into ETH, with proceeds laundered through Tornado Cash, making recovery unlikely.

Crucially, the exploit did not touch Fluid’s lending markets, vaults, DEX, or liquidity layer; the attack path was confined to rewards distribution rather than the core protocols that hold user deposits. Once the compromise was identified, Fluid removed the affected roles and moved remaining reward funds out of harm’s way, pausing Merkle‑based claims while preparing an updated distribution system. Rewards were expected to continue accruing retroactively during the pause, so that users would not lose earned incentives once claiming resumed. Nonetheless, the incident underscored that “non‑core” infrastructure can still become a direct loss vector when operational keys are not properly segregated and monitored.

The communication around the exploit drew particular scrutiny. Initial public messaging reportedly focused on the fact that rewards claiming was paused for infrastructure updates, without immediately disclosing the key‑compromise angle or the loss magnitude. Independent on‑chain sleuths were the first to piece together the full picture, leading to concerns that users had not been promptly informed of a material security incident affecting protocol‑associated funds. For Fluid, the direct financial hit of approximately 215,000 dollars was modest by DeFi exploit standards, especially in light of the much larger sums the protocol has managed in other contexts. The reputational impact, however, lay in the revelation that a two‑key approval model can fail if those keys are not operationally separated, and that off‑chain governance and reward systems must be treated with the same rigor as core contracts.

Fluid lending protocol launches out of Instadapp test phase

Fluid DEX goes live, marketed as most capital-efficient AMM

Venus Flux unified liquidity layer launches on BNB Chain via Fluid

Rebranding proposal: $INST token renamed to $FLUID with growth plan

Arbitrum Foundation proposes Fluid DEX deployment with 400k $ARB incentives

Resolv USR bad debt incident; Fluid core team personally covers losses

Rewards contract key compromise drains 125k FLUID and 51.9k GHO via Tornado Cash

Jupiter Lend powered by Fluid launches on Solana

Evaluating Fluid’s Role in a Changing DeFi Market

With its unified liquidity architecture, aggressive capital efficiency, and growing network of integrations, Fluid occupies a distinctive niche in today’s DeFi landscape. To evaluate its significance, it is helpful to situate the protocol against broader market trends, including the contraction in traditional lending TVL, the rise of restaking and synthetic dollars, and the increasing importance of protocol‑to‑protocol infrastructure relationships. Fluid’s trajectory reflects both the opportunities and the risks of attempting to be a “liquidity layer” rather than a single venue.

DeFi Lending Contraction and Flight to Quality

Since late 2025, data aggregators and DeFi analytics platforms have documented a substantial decline in deposits across major crypto lending protocols, with aggregate balances falling by tens of billions of dollars. Much of this decline has been concentrated in a handful of large incumbents, particularly Aave, Spark, and Euler, which faced both direct exploit‑related losses and broader crises of confidence around collateral frameworks and governance. In parallel, new protocol categories such as restaking services, EigenLayer‑based strategies, and RWA‑backed credit pools have emerged as alternative destinations for yield‑seeking capital, drawing liquidity away from classic overcollateralized lending.

Fluid’s growth during this period suggests that some capital is rotating not out of DeFi entirely but toward platforms perceived as offering more efficient or resilient structures. Weekly and monthly recaps published by the project have highlighted periods in which Fluid’s total value locked surged by more than sixty percent, even as aggregate lending TVL declined. These inflows were often associated with the launch of new products such as the Fluid Lite USD Vault, the onboarding of new institutional partners, or the absorption of liquidity from protocols facing stress events. For example, when cross‑protocol exploits froze markets elsewhere, some users moved collateral and trading activity to Fluid, particularly where escape‑hatch tools like the aWETH redemption protocol offered clear paths to liquidity.

This pattern aligns with a broader “flight to quality” dynamic within DeFi, where users increasingly differentiate between protocols based on risk management, operational responses to incidents, and the ability to coordinate with other major players. Fluid’s involvement in joint initiatives with Lido, Ether.fi, and large aggregators as part of the aWETH unwinding, as well as its cooperative response to the Resolv incident, have helped position it as an active participant in systemic risk mitigation rather than an isolated venue. At the same time, the protocol’s own rewards exploit and unresolved questions about total USR‑related liabilities remind users that there is no risk‑free harbor and that due diligence remains essential even for apparently well‑run platforms.

Capital Efficiency versus Risk: Trade‑offs in Unified Liquidity

A core selling point of Fluid is its claim to “redefine capital efficiency” by letting the same assets serve multiple roles across lending, borrowing, and trading. From a purely financial engineering standpoint, the merits are clear: if collateral can simultaneously earn LP fees in a DEX pool, serve as backing for a levered position, and support stablecoin liquidity, then the protocol can generate more yield per unit of capital than a siloed system where each function requires separate deposits. High loan‑to‑value ratios and low liquidation penalties further enhance perceived user friendliness, especially for sophisticated participants comfortable managing their own risk.

However, these same features also compress buffers that traditionally protect lenders and depositors. With LTVs approaching ninety‑plus percent, even modest price declines or oracle disruptions can push vaults into liquidation territory, and low penalties leave relatively little room to compensate liquidators for adverse execution. The reliance on internal DEX liquidity and Flash Accounting means that the liquidity layer must remain robust under stress; if trading volumes fall or LPs withdraw during a market shock, the protocol’s ability to execute smooth liquidations may be impaired. Fluid’s parameterized ceilings, pauses, and dynamic interest rate curves are designed to mitigate this risk, but they cannot eliminate it entirely.

The Resolv incident underscores how external asset failures can stress this trade‑off. USR’s collapse was not caused by Fluid, but once the asset depegged, the protocol’s shared liquidity architecture meant that USR‑related bad debt effectively became a problem for the entire system and its governance token holders. Fluid’s decision to cover user losses and repay tens of millions of dollars in debt helped preserve depositor confidence, but it also highlighted the systemic consequences of listing high‑yield, experimental stablecoins in a platform where all activities draw from the same liquidity pool. Future governance decisions about asset listings and collateral parameters will likely weigh the incremental yield benefits of such assets against the potential cost of similar rescue operations.

Comparing Fluid to Legacy Lending and DEX Designs

To understand what is truly novel about Fluid, it is helpful to compare it conceptually with legacy DeFi models. Traditional lending protocols such as Compound and early Aave maintain distinct pools of liquidity for each asset; lenders deposit, borrowers draw against those pools, and liquidations occur by selling collateral into external markets. DEXes like Uniswap operate separate automated market maker pools, where LPs provide capital and traders pay fees; lending and trading intersect only when LP tokens themselves are used as collateral in external lending protocols. This modular design has the virtue of isolation—problems in one system do not automatically infect another—but it also leads to fragmented liquidity and reduced capital efficiency.

Fluid’s architecture instead resembles a unified on‑chain balance sheet. Its Liquidity contract holds assets that simultaneously back loans, collateral, and DEX pools, and its Flash Accounting system tracks these roles internally before net‑settling transfers. In a sense, this moves DeFi a step closer to how prime brokers and internalizers operate in traditional finance, where client positions across markets are netted and risk‑managed at the firm level rather than on a venue‑by‑venue basis. The advantage is that capital can be redeployed rapidly across use cases, and liquidations can, in theory, be executed more efficiently by matching exposures internally before tapping external markets. The drawback is that the protocol becomes a single point where multiple risk vectors converge.

In the context of DEX competition, Fluid’s approach also differs from Uniswap‑style designs. Rather than requiring each pair to have its own pool contract with its own LP token, Fluid’s DEX treats pools as logical constructs within a unified contract, which may simplify routing and reduce gas usage. Moreover, the tight integration with vaults allows for features like “smart debt,” where a borrowed asset can be automatically swapped and deployed according to predefined strategies, something that has historically required multiple steps across separate protocols. Whether this model will ultimately displace or coexist alongside more modular designs remains an open question, but early volume metrics indicate that traders and aggregators are willing to route significant flow through the unified liquidity model when it offers competitive pricing and depth.

Practical Considerations for Users and Builders

For everyday users, sophisticated traders, and protocol teams considering building on top of Fluid, the architecture and history outlined above translate into concrete questions about risk, yield, and integration choices. Evaluating Fluid requires understanding not only its advertised features but also the implications of its unified design for stablecoin holders, borrowers, and white‑label partners.

Depositors, Stablecoin Holders, and Yield Seekers

Users who deposit assets such as USDC, USDT, GHO, or synthetic dollars into Fluid’s lending markets or yield vaults are primarily seeking steady returns with manageable risk. In Fluid’s ecosystem, those yields are generated not only from borrower interest but also from DEX fees, liquidation income, and possibly governance incentives. Products like the Lite USD Vault further abstract this complexity by offering fixed‑rate, cross‑chain stablecoin yields with automated strategy management. For depositors, this can be appealing, especially in an environment where yields on centralized platforms or traditional bonds are volatile and where DeFi competitors might offer either lower rates or higher perceived risk.

However, depositors must recognize that the protocol’s capital efficiency and unified liquidity model make them indirect participants in the entire system’s risk profile. When Fluid lists new stablecoins such as GHO or USR, accepts synthetic dollars like sUSDAI as collateral, or partners with external platforms for leveraged yield strategies, depositors’ funds are ultimately part of the liquidity that underwrites these activities. The Resolv episode showed that when a listed stablecoin fails, Fluid may shoulder the resulting bad debt rather than passing losses directly to depositors, but such decisions are ultimately governance and business choices, not hard guarantees. Users looking to minimize risk may prefer to stick to markets backed by long‑established stablecoins like USDC and USDT, while those seeking higher yields may explore more experimental pools with the understanding that both asset risk and protocol risk are elevated.

Borrowers, Leverage Users, and Liquid Staking Strategies

Borrowers on Fluid, particularly those using high‑LTV vaults backed by liquid staking tokens or synthetic assets, are drawn by the ability to maximize capital efficiency while still earning yields on collateral. A user might, for instance, deposit stETH, rsETH, or other yield‑bearing tokens as collateral in a vault, borrow USDC or GHO against them at a high LTV, and then deploy the borrowed funds into further strategies or real‑world spending. Because Fluid’s DEX can deploy collateral into LP positions, borrowers can also earn additional fees on top of staking rewards, layering multiple income streams onto their base assets. This can be particularly attractive for sophisticated traders and funds familiar with cross‑margining and portfolio leverage.

The downside is that the margin for error becomes thin. With LTVs approaching ninety‑plus percent and liquidation penalties designed to be minimal, borrowers must monitor their positions closely and understand how price shocks, restaking exploits, or unexpected governance actions (such as market freezes) can impact their solvency. Events like the rsETH bridge exploit and subsequent freezing of markets across multiple protocols illustrate that even if a borrower’s collateral is fundamentally sound, liquidity constraints or collateral parameter changes can suddenly alter the risk environment. Fluid’s architecture may soften the blow by providing internal redemption mechanisms, as in the stETH and aWETH cases, but no mechanism can fully insulate over‑leveraged positions from extreme scenarios. For borrowers, disciplined leverage and diversification across collateral types and platforms remain essential.

Protocols, Institutions, and “Fluid‑Powered” Integrations

For other protocols and institutional players, Fluid presents itself as a ready‑made infrastructure layer for launching lending markets, DEXes, and stablecoin liquidity strategies. Partnerships like Avici’s Grow and Smart Credit products, which rely on Fluid and Jupiter Lend to enable “borrow and earn” experiences around SOL, showcase how teams can embed Fluid’s capabilities into branded offerings without building core lending logic themselves. Similarly, USDAI’s heavy reliance on Fluid for sUSDAI liquidity indicates that stablecoin issuers may treat Fluid as a primary venue for their tokens, shaping both liquidity and yield characteristics.

These integrations offer clear benefits. Protocols can access deep, unified liquidity and advanced liquidation mechanics without incurring the full cost and risk of operating their own lending engines. Fluid’s track record of collaborating on systemic risk solutions, such as the aWETH escape hatch and Resolv repayment framework, also enhances its appeal as a strategic partner. However, integration also means inheriting Fluid’s risk profile: if the protocol faces a serious exploit, governance crisis, or sustained loss of confidence, platforms built on top of it will likely experience correlated stress. For this reason, institutional users and teams building “Fluid‑powered” products need to conduct their own assessments of Fluid’s security audits, governance processes, and financial resilience, rather than assuming that scale and popularity guarantee safety.

From a regulatory and compliance standpoint, institutions must also consider how Fluid’s unified liquidity and cross‑chain products fit into emerging frameworks for custody, segregation of client assets, and disclosure. Fixed‑rate vaults, leveraged yield products, and synthetic dollar integrations may be scrutinized differently depending on jurisdiction, particularly when they involve exposure to off‑chain assets or restaking‑based primitives. Fluid’s role as a back‑end infrastructure provider complicates this picture, because end users may interact with branded interfaces that obscure the underlying protocol. As DeFi regulation evolves, clear documentation of how “Fluid‑powered” products work under the hood will likely become an important factor in institutional adoption.

A compromised off-chain key allowed an attacker to submit empty-proof Merkle claims and drain 125k FLUID plus 51.9k GHO; funds were laundered via Tornado Cash before the team quietly paused claims with no public disclosure.

The core team drew an $8M DEX Lite credit line and had members personally guarantee bad debt before DAO votes concluded, demonstrating that consequential financial decisions can bypass on-chain governance when the team judges speed necessary.

The v1 USDC-ETH pool incurred rebalancing losses significant enough to prompt a 500k $FLUID vesting proposal to cover LPs, signaling that the smart-collateral AMM design carries non-trivial impermanent-loss-equivalent risk.

Fluid's rapid multichain and cross-protocol expansion — Aave, Lido, EtherFi, Resolv, Venus, Jupiter — means a failure in any integrated protocol can propagate losses directly into Fluid vaults, as the Resolv USR incident demonstrated.

The $INST→$FLUID rebrand, combined with 400k $ARB incentive outlays and a proposed 500k $FLUID LP compensation package, creates meaningful near-term token supply pressure without a clear buyback or burn offset mechanism.

- RegulatoryLow

Fluid operates as a non-custodial on-chain protocol with no fiat on-ramps; current regulatory pressure in the sector is concentrated on custodial and yield-bearing products rather than permissionless lending AMMs of this type.

Outlook

Fluid sits at a crossroads in DeFi’s evolution, combining the ambition of being a universal liquidity layer with the practical realities of operating in a landscape shaped by exploits, bridge risk, and shifting regulatory expectations. Its architecture—built around a single liquidity contract, ERC‑4626 lending, high‑LTV vaults, and a DEX powered by Flash Accounting—offers a coherent vision for capital efficiency and composability that has already attracted substantial trading volume and institutional interest. At the same time, incidents like the Resolv bad debt, the Merkle rewards exploit, and the wider rsETH and USR crises highlight that even well‑engineered systems remain deeply intertwined with the broader risk fabric of DeFi.

In the near to medium term, Fluid’s trajectory will likely hinge on a few key factors. First is the protocol’s ability to continue scaling volume and TVL without compromising risk discipline, particularly as it onboards additional stablecoins, synthetic assets, and cross‑chain integrations. Second is governance: whether the FLUID token and DAO can maintain transparent, timely decision‑making around crises, asset listings, and buyback policies will shape user confidence as much as raw yield or capital efficiency. Third is its role in systemic risk management; if Fluid continues to play a constructive part in designing escape hatches and unwinding tools for other protocols, it may cement its position as critical infrastructure, but it will also shoulder more responsibility when things go wrong elsewhere.

For a crypto news audience and market participants alike, Fluid is a protocol to watch not only for its innovations but also for what its successes and failures will reveal about the feasibility of unified liquidity in decentralized finance. If the model proves resilient, it may point the way toward a new generation of DeFi platforms where lending, trading, and risk management converge in a single, composable layer. If it falters under the weight of interconnected risk, it will offer equally valuable lessons about the limits of capital efficiency and the enduring importance of modularity.

Latest Fluid news

Sources

- https://fluid.io/lending/1

- https://x.com/0xfluid/status/2024512115776655705

- https://gov.fluid.io/t/rebranding-and-growth-plan-for-fluid-protocol/985

- https://x.com/cletusEllijah/status/2034344132634882359

- https://thedefiant.io/news/defi/defi-protocols-launch-joint-escape-hatch-for-aave-eth-lenders-and-loopers

- https://x.com/0xfluid/status/2035651370607419902

- https://coinstats.app/news/6ff6ee0713dfb3201f044423d3065a3b81e30919da86084b2d39d457256ba565_Fluid-Rewards-Drain-Exposes-Key-Control-Failure-After-215K-Theft

- https://x.com/USDai_Official/status/2057482361823261180

- https://x.com/smykjain/status/1993644710867747315

- https://docs.fluid.instadapp.io

- https://imaginaryblend.com/2025/01/10/fluid-flux-documentation/

- https://www.mexc.com/news/980026

- https://phemex.com/news/article/fluid-to-launch-v2-with-flash-accounting-surpassing-200-billion-in-volume-64480

- https://nexusmutual.io/blog/resolv-protocol-incident-report-by-nexus-mutual

- https://x.com/fluid_cn/status/2028366521475768461

- https://www.galaxy.com/insights/research/kelpdao-layerzero-exploit-defi

- https://www.kucoin.com/news/flash/avici-launches-grow-and-smart-credit-products-for-yield-generation

- https://mixbytes.io/blog/modern-defi-lending-protocols-how-its-made-fluid-vault

- https://x.com/0xfluid/status/2034298868989362451

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…