In-depth explainer on Pendle, DeFi’s leading yield tokenization platform. Covers SY–PT–YT mechanics, fixed vs variable yield strategies, Aave/Morpho composability, RWA and stablecoin integrations, AI agents, risks, and long-term outlook.

+4 sources across the wider coverage universe

Apyx brings Strategy’s DAT preferred stock dividends onchain via Pendle, letting DeFi users lock fixed or floating yield strategies targeting 13-15% APY2026-05

Apyx brings Strategy’s DAT preferred stock dividends onchain via Pendle, letting DeFi users lock fixed or floating yield strategies targeting 13-15% APY2026-05 Dune data confirms “Pendle Effect” as PT/YT markets drive token demand surges, boosting holders, supply, and capital inflows via yield tokenization and DeFi composability2026-05

Dune data confirms “Pendle Effect” as PT/YT markets drive token demand surges, boosting holders, supply, and capital inflows via yield tokenization and DeFi composability2026-05 Pendle emerges as DeFi’s yield standard, turning fixed-rate PT tokens into liquid collateral and attracting institutional flows into tokenized yield markets2026-03

Pendle emerges as DeFi’s yield standard, turning fixed-rate PT tokens into liquid collateral and attracting institutional flows into tokenized yield markets2026-03 Bungee enables Pendle PTs to be access from any chain and from one deep pool on Ethereum.2026-04

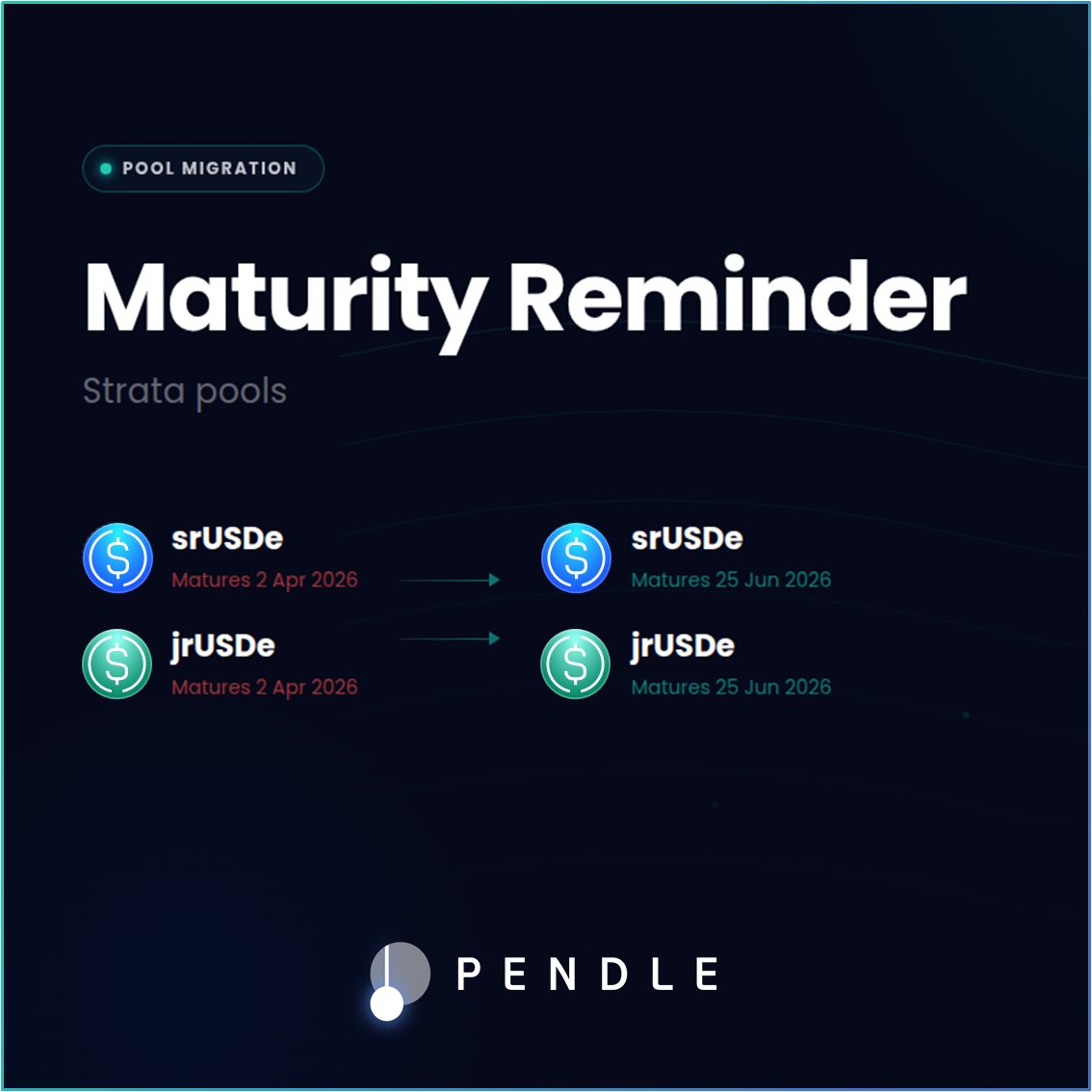

Bungee enables Pendle PTs to be access from any chain and from one deep pool on Ethereum.2026-04 Pendle to sunset April Strata pools at maturity, urging users to migrate positions as new June srUSDe and jrUSDe markets go live2026-04

Pendle to sunset April Strata pools at maturity, urging users to migrate positions as new June srUSDe and jrUSDe markets go live2026-04 Tangent unveils $USG, a CDP stablecoin backed by Curve LP tokens and Pendle PTs, unlocking borrowing against yield positions2026-03

Tangent unveils $USG, a CDP stablecoin backed by Curve LP tokens and Pendle PTs, unlocking borrowing against yield positions2026-03

Pendle: On‑Chain Markets For Fixed And Variable Yield

Pendle is a decentralized protocol that turns yield-bearing crypto assets into tradable fixed and variable income instruments, allowing users to lock in predictable returns or speculate on future yields through tokenized markets for principal and yield. By standardizing yield tokenization and building automated markets around these instruments, Pendle has grown into one of the largest crypto yield trading platforms and a leading piece of on-chain fixed income infrastructure.

The Rise Of Yield And Fixed Income In DeFi

Yield has been one of the defining narratives in decentralized finance because it translates the volatility of crypto assets into streams of income that resemble interest, dividends, or coupons in traditional markets. In early DeFi, most yield came from lending protocols, liquidity provision on automated market makers, and incentive programs that distributed governance tokens, all of which exposed users to fluctuating variable rates. Variable yield can be attractive when rates rise, but it complicates planning and risk management for both individuals and institutions that need some degree of certainty about future cash flows. The absence of robust fixed-rate and term-structured products meant that DeFi often lacked a direct analogue to bonds or interest rate derivatives, even as total value locked grew into the hundreds of billions of dollars during peak cycles. This structural gap created demand for protocols that could transform volatile, path-dependent yield into predictable, tradable instruments.

Traditional finance offers a useful lens for understanding why this matters. In conventional markets, government and corporate bonds, interest rate swaps, and structured credit products allow savers, borrowers, and traders to exchange fixed and floating rates across different maturities. Those instruments underpin everything from mortgage markets to corporate treasury management, and they are deeply interconnected with banking and derivatives markets. DeFi replicated some pieces of this stack with overcollateralized lending and perpetual futures, but the ability to separate and trade the yield on assets remained relatively underdeveloped. Without a liquid, transparent term structure for on-chain yields, it was difficult to price risk, hedge interest rate exposure, or build more advanced credit products on top of existing protocols.

Early attempts at on-chain fixed income experimented with tokenizing claims on future yield, but they often faced problems of fragmentation, illiquidity, or narrow asset coverage. Many designs targeted specific collateral types or relied on bespoke contract interfaces that made composability difficult. Protocols had to build their own markets, integrations, and risk frameworks from scratch for each new yield source, limiting network effects. In addition, yield in DeFi is not a single phenomenon but a mosaic of sources including staking rewards, lending interest, real-world asset cash flows, and protocol incentives, each with distinct risk profiles. A generalized, permissionless way to tokenize and trade yield across this spectrum therefore required a flexible architecture that could map diverse underlying assets into a common interface without sacrificing risk transparency.

This is the environment into which Pendle emerged. By focusing squarely on yield tokenization and designing a common standard for wrapped yield-bearing assets, the protocol aimed to provide an underlying infrastructure layer rather than a single-purpose product. Rather than re-creating a bespoke market for each new asset, Pendle introduced a framework capable of handling staking derivatives, money market tokens, stablecoins, and, increasingly, real-world asset yields. Over time, that design has allowed Pendle to develop a complex ecosystem of markets, integrations, and strategies centered around one core idea: separating the ownership of principal from the right to its future yield.

Apyx brings Strategy’s DAT preferred stock dividends onchain via Pendle, letting DeFi users lock fixed or floating yield strategies targeting 13-15% APY

$237M of Apyx TVL on Pendle is already enough for a mini forward curve on Saylor/Strive preferred dividends, but the clean trade is knowing which leg you own. PT-apyUSD is underwriting STRC/SATA monthly rate policy; PT-apxUSD’s 15% handle is paid by APYX points speculators because the underlying has 0% yield. That makes this stack a hybrid credit/airdrop basis trade, with nasty convexity if DAT dividends and Pips pricing re-rate at the same time.

Readers engage with Pendle not as a yield-splitting tool but as DeFi's premier leverage amplifier — the top clicks cluster around Boros margin trading, EigenLayer speculation, and Ethena looping risk, revealing that Pendle's real audience is tracking it as the fulcrum where speculative capital gets institutionalized and systemic risk cascades.↗

What Is Pendle Finance?

Origins, Scale, And Recognition

Pendle Finance is a specialized DeFi protocol that enables users to tokenize and trade the yield of interest-bearing crypto assets through a standardized system of principal and yield tokens. It was founded in 2020 by Vu Nguyen and TN Lee, both of whom previously worked at projects such as Digix and Kyber Network, bringing experience in tokenization and on-chain liquidity to the design of the protocol. Over several market cycles, Pendle has grown into one of crypto’s largest fixed-income platforms, with more than 1.1 billion dollars in total value locked reported in 2026 and an expanding footprint across Ethereum and other chains. The protocol describes itself as the world’s largest crypto yield trading platform, emphasizing its focus on trading and structuring around yield rather than spot price direction alone.

This positioning has been recognized beyond the DeFi-native community. Fortune named Pendle to its 2026 Crypto Innovators list, highlighting it as one of thirty companies and projects pushing the digital asset ecosystem forward from a pool of more than 150 nominations that included global financial institutions such as State Street, DBS Bank, and SBI Holdings. Within that list, Pendle appears under the decentralized finance category, underscoring its role in building out fixed-income primitives on-chain rather than simply offering another trading venue for volatile tokens. Coverage around this recognition has emphasized that, for much of crypto’s history, there was no close analogue to fixed income on-chain, and Pendle has helped change that by making yield itself a first-class, tradable object.

Alongside this external recognition, Pendle has seen increasing engagement from institutional players. Reports have highlighted the protocol’s participation in a Vietnam International Finance Corporation delegation alongside firms such as BlackRock, Morgan Stanley, and Deutsche Bank, where it presented tokenized yield markets as part of a broader vision for on-chain fixed income. This type of engagement suggests that Pendle is not just an isolated DeFi experiment but is increasingly viewed as infrastructure that could interface with regulated asset managers, credit providers, and banks seeking to experiment with tokenization. In parallel, sophisticated crypto-native firms such as Wintermute have begun integrating Pendle’s principal tokens into strategies run on lending protocols like Morpho, demonstrating how institutional market makers and funds can use tokenized yield as collateral and building blocks for more complex structures.

Pendle’s Role In The DeFi Stack

Pendle sits at an interesting junction within the DeFi stack because it does not compete directly with lending protocols, staking services, or real-world asset originators. Instead, it builds a secondary set of markets on top of yield-bearing tokens issued by those platforms. When a protocol such as Lido issues staked Ether, or when Aave and other money markets issue interest-bearing stablecoins, Pendle can wrap those tokens and split them into principal and yield components, creating a parallel layer of trading that focuses on interest rate expectations rather than spot token prices. In this sense, Pendle resembles an on-chain interest rate derivatives platform whose underlying assets are the yield-bearing tokens of other protocols.

This approach has two important consequences. First, Pendle’s growth is closely tied to the expansion of yield-bearing assets in the broader ecosystem. As more real-world credit vaults, staking derivatives, and structured stablecoins emerge, each of them becomes a potential input into Pendle’s tokenization pipeline. This dynamic is visible in the proliferation of markets around assets such as tokenized US Treasury proxies, real-world credit vaults, and stablecoin strategies where Pendle users can either lock in fixed portions of the underlying yield or take leveraged views on its variability. Second, because principal tokens often behave like discounted claims on future redemption, they can be used as collateral in other protocols without sacrificing the right to future yield when combined with yield tokens or other hedging strategies. This composability has underpinned integrations with lending markets, collateralized debt position (CDP) systems, and cross-chain routing services.

Pendle’s footprint therefore extends beyond its own automated market maker pools. The protocol’s principal tokens are increasingly visible as collateral on money markets, as reserve assets in CDP stablecoins, and as components in more elaborate “meta-strategies” that combine fixed and floating exposure across multiple underlying yield sources. A notable example is the use of Pendle PTs in Tangent’s USG stablecoin, where CDP positions are backed in part by Curve liquidity tokens and Pendle principal tokens, effectively allowing users to borrow against capital that simultaneously earns yield in other protocols. This type of nested composability is one of the mechanisms by which Pendle has started to function as what some commentators describe as a “yield standard” for DeFi: a set of common instruments around which other protocols can build.

Core Mechanics: SY, Principal Tokens, And Yield Tokens

The SY Standard: A Common Wrapper For Yield

At the heart of Pendle’s design is a token standard called SY, which provides a standardized interface for wrapped yield-bearing tokens within smart contracts. The idea is that yield-bearing assets in DeFi come in many forms and contract interfaces, from staking derivatives like stETH to lending receipts such as aUSDC or cDAI, and they are not homogeneous from the perspective of protocols that want to build on top of them. SY allows any such asset to be wrapped into a token that exposes a common set of functions related to deposit, redemption, and yield accounting, so that Pendle’s core contracts can treat all underlying yield-bearing assets in a uniform way.

Typically, one SY token represents one unit of the underlying yield-bearing asset, such that one SY-rsETH corresponds to one rsETH, and so on. This design preserves intuitive accounting while letting the Pendle protocol interact solely with SY tokens as its main interface to yield-bearing assets. Users can wrap and unwrap through a converter integrated into Pendle’s interface, which handles the routing between the original yield-bearing token and its SY representation. This is an important abstraction layer because it decouples the Pendle system from the idiosyncrasies of specific underlying protocols, making it easier to integrate new assets without rewriting core logic.

From the perspective of on-chain fixed income, SY tokens can be thought of as standardized “deposit receipts” for a wide range of yield-generating positions. Once wrapped, they become eligible to be split into principal and yield claims. This is what allows the protocol to turn a heterogeneous universe of staking tokens, lending receipts, and structured stablecoins into a homogeneous set of principal tokens and yield tokens that can be traded against each other in shared markets. Without such a standard, each asset would require bespoke integration, and the liquidity for interest rate trading would likely fragment across many incompatible pools.

Splitting Yield: From SY To PT And YT

When a user deposits a yield-bearing asset like stETH or an interest-bearing stablecoin into Pendle, it is first wrapped into the appropriate SY token and then split into two new instruments: Principal Tokens (PT) and Yield Tokens (YT). PT represent ownership of the underlying principal and carry a right to redeem that principal at a specified maturity date, while YT represent the right to receive the future yield generated by the underlying asset over that same period. In economic terms, this process decomposes a single yield-bearing position into a zero-coupon-like claim on principal plus a separate claim on the cash flows produced between now and maturity.

The behavior of PT and YT is anchored in the characteristics of the underlying yield-bearing asset. For instance, if the underlying SY token corresponds to a stablecoin strategy that reliably accrues interest over time, the YT linked to that asset will receive those interest payments as they are generated, while the PT will simply track the discounted value of the principal amount that will be redeemable at maturity. If, instead, the underlying is a staking derivative with variable rewards linked to network conditions, YT will embody that variability and PT will again represent a more stable, discounted claim on the staked principal. In both cases, the aggregate value of PT and YT should, in principle, converge to the value of the underlying SY token, subject to market expectations and discounting for time and risk.

In practice, tokenization works as follows. A user supplies a yield-bearing token such as stETH or aUSDC into Pendle and receives an equivalent amount of SY, which is then converted into PT and YT in equal nominal quantities. The user can choose to hold both tokens, effectively replicating their original position but now with greater flexibility to trade one side or the other. Alternatively, they may sell the YT to another market participant who wants exposure to future yield while keeping the PT. In that case, the original user has effectively converted a variable yield position into something closer to a discounted bond: if they hold the PT to maturity, they will redeem the full notional of the underlying asset, and the discount at which they bought or retained the PT relative to face value determines their realized fixed return.

From Discounts To Implied Fixed Rates

The pricing of principal tokens is where fixed income intuition enters the picture. Because PT entitle the holder to a fixed amount of the underlying at maturity, they are analogous to zero-coupon bonds whose yield is determined by the discount to face value and the time remaining until redemption. If a PT that will redeem for one unit of a stablecoin in one year is trading at 0.95 units today, its implied annual yield is a function of the 0.05 difference over the remaining time. Formally, if a PT pays \( F \) units at maturity \( T \) and is priced at \( P \) today, the implied simple annual yield \( y \) over \( n \) years can be approximated as \( y \approx \frac{F - P}{P \cdot n} \), while more precise compounding would use \( y = \left(\frac{F}{P}\right)^{1/n} - 1 \). These formulas apply directly to PT pricing given their redemption structure.

This relationship allows users to “lock in” fixed yields by purchasing PT at a discount to their redemption value and holding them to maturity. For example, if a Pendle market offers PT tied to an Origin Dollar (OUSD) yield vault that redeems at par in the future, a user can buy those PT below par, effectively securing a known return as long as the underlying vault remains solvent and the PT is held until maturity. Origin has highlighted that Pendle enables OUSD holders to lock in a specific annual percentage yield by buying PT, while other participants in the same market may choose to hold or buy YT to gain leveraged exposure to any upside in the variable OUSD yield. This separation converts what was previously a single floating-rate position into two tradable instruments with different risk–return profiles.

Yield tokens, for their part, tend to embody greater convexity and risk. Because they represent only the stream of future yield, their value can be sensitive to expectations about rate paths, reward schedules, or protocol incentives. Traders who believe that the yield on a particular asset will remain high or increase can purchase YT, effectively going long on future yield and often achieving leveraged exposure relative to simply holding the underlying asset. Conversely, if traders expect yield to fall or are looking to hedge yield exposure, they can sell YT or take offsetting positions. In some Pendle markets, the structure of incentives has led to very high prospective returns on YT, such as reports of YT-sUSDD positions tracking nominal returns on the order of several dozen percent annualized when combining base yield and reward streams, although such figures are highly path-dependent and subject to change over time.

Economic Intuition And Use Cases

The economic intuition behind Pendle’s design is that separating principal and yield allows different market participants to specialize in the risks they are best equipped to bear. Conservative capital can accumulate PT to earn relatively predictable yields, much like bond investors in traditional markets, while more risk-tolerant traders can take the other side by accumulating YT, effectively speculating on how yield will evolve. Protocols that generate yield, such as staking services or real-world credit vaults, can reach a wider range of investors by offering both fixed and floating versions of their cash flows via Pendle markets. This segmentation can increase capital efficiency because it allows some investors to underwrite interest rate and incentive risk while others simply seek principal stability and known returns.

Over time, this mechanism has given rise to a variety of strategies. Some users deposit a yield-bearing asset, sell the YT immediately, and hold PT to maturity, thereby synthetically creating a fixed-rate position. Others may buy both PT and YT separately if they see mispricing between the combined package and the underlying asset, engaging in arbitrage that helps keep the system in balance. Advanced users can combine PT and YT positions from different markets to construct custom duration profiles, hedges, or yield curves across various stablecoins, staking tokens, and real-world asset vaults. The flexibility of the PT–YT decomposition, together with Pendle’s standardized SY wrapper, is what turns an otherwise simple yield-bearing token into a building block for more sophisticated on-chain fixed-income strategies.

To summarize this relationship, it is useful to view SY, PT, and YT as three closely linked representations of the same underlying position. The table below provides a conceptual comparison based on Pendle’s design.

| Token type | Underlying claim | Key risk profile | Typical user goal |

|---|---|---|---|

| SY | Full principal plus yield in a single token | Combined exposure to price and yield volatility | Maintain original yield-bearing position with added composability |

| PT | Fixed redemption of principal at maturity | Discount and interest rate risk; lower yield variability | Lock in fixed yield, use as collateral or bond-like asset |

| YT | Stream of future yield until maturity | High sensitivity to yield changes and incentives | Speculate on or hedge future yield, often with leverage |

This structure is the foundation upon which Pendle builds its automated markets, external integrations, and strategy ecosystem.

- 01Boros margin yield trading↗

Pendle extending into leveraged yield speculation via Boros was the single highest-engagement story, signaling readers see it as a new DeFi primitive, not an incremental feature.

- 02EigenLayer airdrop speculation cycle

A 74% PENDLE price surge tied to EigenLayer hype — and subsequent $1.3bn LRT outflows — showed readers treating Pendle as the liquid expression of restaking narratives.

- 03Ethena USDe Aave looping risk↗

Chaos Labs flagging $6.6B USDe exposure built through Pendle-enabled looping on Aave pulled readers focused on cascading deleveraging and systemic contagion, not just yield mechanics.

- 04Penpie hack accountability trail

Multiple overlapping headlines — PSA, post-mortem, contract pause, whale flashloan — show readers followed the full arc of incident response and blame attribution, not just the initial exploit.

- 05Multi-chain TradFi KYC expansion↗

Solana, Hyperliquid, TON targets plus KYC-compliant yield and a Vietnam IFC delegation alongside Blackrock and Deutsche Bank positioned Pendle as a bridge between on-chain yield and institutional finance.

- 06USD0++ depeg DeFi contagion

Usual Money's abrupt redemption changes rippling through Pendle and Morpho resonated because it exposed how a single stablecoin policy shift can trap leveraged farmers across interconnected protocols.

Pendle Markets, Liquidity, And Tooling

AMMs For Yield Trading

Pendle’s markets center around automated market maker pools that trade principal tokens against SY, with yield tokens priced implicitly through the relative values of PT, SY, and the underlying asset. By pairing PT with SY rather than with the underlying token directly, Pendle ensures that liquidity focuses on the standardized wrapped representation, simplifying math and integration. The AMM design is optimized for fixed-income style instruments whose value converges to par at maturity, meaning that pricing behavior differs from constant-product pools used for spot token swaps. This specialized design aims to provide deeper liquidity and more predictable slippage for PT trading across different maturities.

Because YT represent only yield, their price can be derived from the relationship between the PT price and the combined value of PT and YT relative to SY. In practice, many Pendle interfaces abstract away this complexity by focusing on implied fixed APYs for PT and projected variable APYs for YT. However, the AMM mechanics ensure that when traders act on these implied yields by buying or selling PT and indirectly YT, the pool prices adjust accordingly, embedding market expectations about future interest rates and incentive flows into PT discounts. Over time, this leads to an emergent term structure of on-chain yields across different assets and maturities, visible directly in Pendle’s markets.

Liquidity in Pendle pools is critical because it determines how easily users can enter or exit fixed-rate or yield positions without incurring large price impact. To support this, Pendle relies on a mix of organic volume, liquidity mining incentives, and integrations with other DeFi protocols that supply or route liquidity into PT–SY pools. Origin’s wOUSD market on Pendle illustrates how this can work in practice: Origin has highlighted that liquidity providers in the wOUSD Pendle market can earn triple-digit annual percentage yields when combining trading fees, Pendle incentives, and Origin’s own rewards, while OUSD holders can use PT to lock in a lower but more predictable APY on their stablecoin yield. Such arrangements incentivize LPs to deepen liquidity while offering end users a choice between fixed and variable exposure.

Limit Orders, Liquidity Programs, And The Trading Alert Bot

Pendle has experimented with more advanced liquidity tools beyond standard AMM provision. One notable area has been the introduction of incentive programs targeted at limit order flow, which aim to attract resting orders that improve market depth around key price levels. Reports have described how a pilot program for limit order incentives boosted liquidity multiple times over in a short period, although this came at the cost of reducing direct PENDLE token rewards for some liquidity providers, potentially introducing new volatility in the governance token’s incentive dynamics. These experiments illustrate the protocol’s willingness to adjust its market microstructure to better balance active and passive liquidity provision, even as it navigates the trade-offs inherent in any incentive redesign.

To help users interact more effectively with its markets, Pendle has also rolled out ancillary tooling such as the Pendle Trading Alert Bot. This Telegram-integrated tool allows users to configure alerts for a variety of events, including limit order fills, new market launches, newsfeed updates, and custom watchlist triggers, delivering notifications without requiring constant manual monitoring of the interface. The team has emphasized that the bot now stores only a user’s Telegram ID rather than broader data, reflecting a privacy-conscious design even as the tool becomes more feature rich. For traders constructing complex fixed-income strategies or monitoring multiple PT and YT positions across different maturities, such alerting infrastructure reduces friction and can improve risk management.

TVL Growth And Market Breadth

Pendle’s total value locked and the breadth of its markets have expanded significantly as yield-bearing assets have proliferated. Recent data and commentary refer to a phenomenon sometimes labeled the “Pendle Effect,” where the listing of a yield-bearing asset on Pendle is followed by rapid growth in that asset’s on-chain presence and associated TVL, as users are attracted by new opportunities to trade and lock in its yield. Analytics from Dune have highlighted that SY tokens, which sit at the base of Pendle’s tokenization mechanism, accounted at one point for over a quarter of the protocol’s total value locked on Ethereum, underlining the scale of wrapped yield-bearing assets flowing through the system. As TVL accumulates in PT–SY markets, those markets increasingly influence pricing and capital flows in the underlying protocols.

Specific pools illustrate this feedback loop. The USDG pool on Pendle, associated with a regulated, yield-bearing stablecoin product, crossed the 200 million dollar TVL mark and continued to grow, with recent snapshots showing roughly 230 million dollars in liquidity and close ties to supply caps on lending protocols such as Aave. Pendle has framed that growth as evidence of sustained demand for fixed-rate exposure to yield generated by regulated stablecoin reserves, with PT-USDG positions allowing users to lock in that yield over a given maturity while others trade YT to express views on its variability. In parallel, other stablecoin and RWA-linked markets such as those for OUSD, ACRED real-world credit vaults, and various structured dollar products have joined the platform, further widening Pendle’s coverage of the on-chain fixed income landscape.

At the same time, Pendle has pushed into more exotic and diversified markets. Reports have described new pools for assets such as sENA (linked to the Ethena ecosystem), jrUSDe and srUSDe tranches of synthetic dollar vaults, and even S&P 500-linked tokenized indices, where traders can tap into off-chain equity yield streams through on-chain PT and YT. The protocol has also added so-called Boros markets referencing commodities and non-crypto exposures such as Brent oil and foreign exchange proxies, expanding the universe of yield sources beyond traditional crypto-native tokens. These developments demonstrate how Pendle aims to position itself as a generalized marketplace for tokenized yield, regardless of whether the underlying risk relates to staking, stablecoins, credit, or traditional assets brought on-chain.

Dune data confirms “Pendle Effect” as PT/YT markets drive token demand surges, boosting holders, supply, and capital inflows via yield tokenization and DeFi composability

Composability With Aave, Morpho, And Other Protocols

Principal Tokens As Collateral And Building Blocks

One of Pendle’s most significant strengths is the composability of its principal tokens with other DeFi protocols, especially lending markets like Aave and Morpho. Because PT represent discounted claims on future redemption of an underlying asset, they can often serve as collateral in money markets while still preserving exposure to the underlying principal. Galaxy research into Aave’s leverage markets has shown that unexpired Pendle PTs appear among the more levered collateral types on Aave V3, though they still account for a modest single-digit percentage of total collateral supplied compared to dominant assets like liquid staking tokens. This presence nevertheless underscores that users are already borrowing against PT positions, creating leveraged fixed-income strategies where they might, for example, lock in a fixed yield via PT while rehypothecating those tokens as collateral to pursue additional returns.

On Morpho, which sits atop lending protocols to optimize yields and execution, Pendle PTs have become even more prominent. Data shared by Pendle and community analysts show that APYX principal tokens, which represent tokenized dividends from Strategy’s DAT preferred stock brought on-chain, have grown into the largest PT markets on Morpho with around 50.5 million dollars in TVL and yields in the range of 60 to 110 percent annualized in certain periods. In this configuration, users can deposit PT-APYX into Morpho markets, borrow against them, and construct leveraged or hedged positions that intertwine fixed and floating exposures. The fact that PTs from Pendle have grown into top collateral types on a major lending optimizer highlights Pendle’s role as a source of yield-bearing collateral rather than merely a trading venue.

Other integrations reinforce this trend. Tangent’s USG stablecoin uses Pendle PTs, alongside Curve liquidity pool tokens, as backing for overcollateralized borrowing positions, letting users mint new stablecoins against tokenized claims on future yield. This design effectively allows capital to serve multiple roles simultaneously: earning fixed yield via PT in Pendle markets while supporting a stablecoin through a CDP mechanism. In addition, cross-chain routing protocols such as Bungee have integrated Pendle principal tokens, enabling users on other chains to access Pendle PTs via deep liquidity pools on Ethereum without manually bridging and trading across multiple interfaces. This omnichain access further cements PTs as modular, portable building blocks in the broader DeFi ecosystem.

Ties To Aave And Capital Flows Around Stablecoins

The relationship between Pendle and Aave is bidirectional, particularly in the context of stablecoin and RWA-linked markets. The USDG pool on Pendle has not only amassed substantial TVL but has also interacted with Aave’s risk parameters, as supply caps for USDG on Aave filled up alongside growth in PT-USDG positions on Pendle. This dynamic suggests that as users seek to earn yield on USDG through Aave or to borrow against it, some of that activity feeds into Pendle, where they can further transform Aave’s variable yield into fixed-rate PT and speculative YT positions. The interplay between Aave’s caps, Pendle’s PT pricing, and external demand for regulated stablecoin exposure illustrates how tokenized fixed income can influence liquidity and risk distribution in core lending markets.

Galaxy’s stress tests of Aave’s leverage market exposures have shown that concentration risk in certain collateral types, such as weETH and other liquid staking tokens, dominates under depeg scenarios, while PTs contribute a smaller share of overall risk. However, the presence of PTs among the set of levered collateral types raises important questions for risk managers. If PTs are used extensively as collateral across Aave, Morpho, and CDP stablecoins, a shock to the underlying yield, a governance failure in a real-world asset vault, or a smart contract bug in Pendle could propagate through multiple layers of leverage. On the other hand, PTs can also be used to de-risk positions by locking in fixed yield and insulating borrowers from rate volatility, potentially acting as stabilizing instruments in some scenarios. Managing these trade-offs is becoming an increasingly visible topic among protocol risk teams and external analysts.

Institutional Strategies: Wintermute, Armitage, And Beyond

Institutional actors have begun using Pendle’s instruments as components in structured products and strategies. One example is Wintermute’s Armitage USDC vault on Morpho, which allocates part of its assets to Pendle PT-reUSD and PT-USDat, thereby embedding fixed-yield exposures into a broader yield maximization strategy run by a professional market maker. In this configuration, the vault’s depositors effectively rely on Wintermute to balance PT-based fixed yields against other opportunities and borrowing costs, while Pendle provides the underlying infrastructure that turns variable yields from reUSD and USDat strategies into tradeable PT and YT. Such structures signal that Pendle’s markets are sufficiently deep and reliable to attract allocations from sophisticated funds managing capital at institutional scale.

A similar dynamic is visible in the integration of Strategy’s STRC dividends through the Saturn ecosystem and Pendle. Saturn Credit tokenizes STRC dividends into a synthetic stable asset called sUSDat, which can then be brought into Pendle markets where PT and YT allow users to trade, hedge, or lock in that dividend stream. CoinGecko’s coverage has noted that the pipeline from STRC to sUSDat to Pendle opens up yield strategies targeting mid-teens annual percentage yields, demonstrating how real-world or off-chain cash flows, such as preferred stock dividends, can be transformed into on-chain fixed and floating rate instruments. For institutions that understand the underlying credit or equity risk but want on-chain flexibility and composability, Pendle’s role in this pipeline is that of a financial engineering layer.

Beyond credit-linked assets, Pendle has hosted markets for synthetic dollar strategies tied to products like sUSDD, where fixed yield, YT trading, and liquidity provider incentives create a rich set of opportunities around stable-yield strategies. Coverage has described how sUSDD markets on Pendle have enabled users to combine fixed-rate PT positions, leveraged YT trades, and LP roles to capture different slices of the protocol’s underlying yield, with some YT-sUSDD positions at times projecting very high nominal returns based on combined yield and incentive streams. These examples highlight a broader pattern: Pendle acts as a crucible where yield from diverse sources—lending, staking, credit, synthetic dollars—is reshaped into modular instruments that both retail and institutional players can deploy inside more complex strategies.

- 2023-04launch

Pendle V2 launches on Ethereum mainnet

- 2023-08milestone

Binance Labs announces strategic investment

- 2024-04milestone

EigenLayer airdrop speculation drives 74% PENDLE surge

- 2024-09exploit

Penpie protocol hacked; Pendle pauses all contracts

- 2025-01exploit

USD0++ depeg causes contagion across Pendle and Morpho

Pendle goes live on Sonic mainnet

Boros margin yield trading platform launched by Pendle

sPENDLE tokenomics overhaul replaces locked vePENDLE with liquid staking

Stablecoins, Real-World Assets, And The “Pendle Effect”

Tokenized Yield From Stablecoins And RWAs

The stablecoin and real-world asset segments have become central to Pendle’s growth narrative. Stablecoins, especially those backed by short-term government securities or similar instruments, generate relatively predictable off-chain yield that can be shared with token holders through on-chain mechanisms. Pendle’s USDG market is a prominent example: USDG is a regulated stablecoin product that pays yield derived from underlying reserves, and Pendle’s PT-USDG and YT-USDG markets allow users to choose between locking in that yield at a fixed rate or speculating on its future path. The rapid rise of the USDG pool to over 200 million dollars in TVL, and further toward 230 million dollars, has been framed as evidence that users are eager to access fixed-rate exposure to regulated stablecoin yield, rather than relying solely on variable lending or liquidity mining returns.

Real-world asset (RWA) vaults take this a step further by tokenizing specific credit exposures, such as corporate lending or trade finance, and turning their cash flows into on-chain yield claims. Pendle has begun to support PT and YT markets tied to RWA credit strategies, including ACRED’s vaults, which package underlying credit risk and distribute it through tokenized tranches. In this framework, PT-ACRED positions can function like tokenized fixed-income securities backed by diversified credit portfolios, while YT-ACRED instruments allow traders to express views on default rates, recovery, and credit spreads. Combined with stablecoin markets, this expansion into RWA-linked yield positions Pendle as a hub for tokenized fixed income that spans everything from digital dollars to off-chain corporate credit.

Stablecoin strategies also interact with Pendle through products like Origin Dollar (OUSD), whose yield-bearing version can be wrapped into wOUSD and traded on Pendle. Origin has emphasized that OUSD holders can lock in a relatively modest but stable APY of around 3.5 percent by purchasing PT-wOUSD, while liquidity providers in its Pendle market have, at times, earned significantly higher returns due to protocol incentives layered on top of the base yield. Other stablecoin-related integrations include new synthetic dollar products such as USD3 from the 3Jane ecosystem, which tap Pendle to create fixed and variable yield exposures for their underlying strategies. Together, these integrations illustrate how stablecoin issuers and structured dollar protocols can use Pendle to offer their users a menu of rate options analogous to fixed and floating bank deposits or bond funds.

The Pendle Effect: How Yield Markets Drive Token Demand

The “Pendle Effect” is shorthand used by analysts to describe the feedback loop between yield tokenization on Pendle and demand for the underlying assets. As documented in community analyses and Dune dashboards, when a yield-bearing asset is listed on Pendle and gains active PT and YT markets, several things tend to happen. First, the asset often sees increased primary demand as users are attracted by the ability to trade, hedge, or lock in its yield via Pendle’s markets. Second, liquidity and TVL in both the Pendle pools and related lending or staking protocols rise, as traders and liquidity providers allocate capital to exploit new strategies and arbitrage opportunities. Third, the asset may start to appear as collateral or reserve in other protocols, as PT and SY tokens become integrated into money markets, CDPs, and yield optimizers.

Dune’s analysis of Pendle metrics underscores this phenomenon. At one point, SY tokens associated with Pendle’s yield-tokenization mechanism represented nearly 28 percent of the protocol’s total value locked on Ethereum, with PT-USDG deposits on lending markets and other PT types making up a significant share of collateral in composable strategies. At the same time, Pendle’s own reporting on Apyx’s DAT preferred stock dividends shows how APYX PT markets grew more than fourteen-fold in TVL, reaching roughly 371 million dollars and becoming the largest PT markets on Morpho with yields in the range of 60 to 110 percent annualized for certain periods. These figures illustrate how the presence of a Pendle market can catalyze capital inflows into the underlying yield source, often far beyond what would have been attracted by the original protocol alone.

The STRC–Saturn–Pendle pipeline provides another concrete instance of the Pendle Effect. Strategy’s STRC token generates dividends that Saturn tokenizes into sUSDat, which then feeds into Pendle markets where users can trade PT-sUSDat and YT-sUSDat. CoinGecko has described how this arrangement brings preferred stock-like dividends on-chain as tradeable DeFi yield, targeting mid-teen annual returns. As Pendle users discover and trade these instruments, demand for STRC and sUSDat can increase, driving up their usage and on-chain presence. Community commentary working with on-chain data has suggested that Pendle’s tokenization and yield-trading functionality can significantly boost the holder base, circulating supply utilization, and overall capital inflows into such assets, effectively acting as a demand amplifier.

Stablecoin Design And Second-Order Effects

Pendle’s role in stablecoin and RWA ecosystems also has second-order effects on how these instruments are designed. Stablecoins such as USDG, USDat, and USG have begun to explicitly consider how their yield-bearing mechanics will interact with Pendle-style tokenization. For instance, Tangent’s USG stablecoin, backed by a mix of Curve LP tokens and Pendle PTs, is constructed with the expectation that PTs can both serve as collateral and generate fixed yield that supports the stability of the peg and the economics of the CDP system. Similarly, some RWA vaults design their tokenization parameters, tranching structures, and redemption schedules with an eye toward enabling clean mapping into Pendle’s SY–PT–YT framework.

This co-design can influence capital allocation. If an issuer knows that listing on Pendle will likely trigger the Pendle Effect, with increased demand and TVL flowing into its assets, it has an incentive to structure products in a way that is Pendle-compatible from the outset. Over time, this could create a form of soft standardization, where yield-bearing tokens are architected with tokenized principal and yield markets in mind, reinforcing Pendle’s role as a reference infrastructure layer for on-chain fixed income. Conversely, protocols that are not easily integrable into Pendle may find themselves at a relative disadvantage in attracting yield-focused capital, highlighting the competitive implications of yield tokenization becoming a norm in DeFi.

User Strategies: Fixed Yield, Directional Yield Trading, And Liquidity Provision

Locking In Fixed Yield With Principal Tokens

For many users, the most straightforward use case for Pendle is to obtain fixed yield from inherently variable yield-bearing assets. The mechanics are conceptually simple: a user who currently holds a yield-bearing token such as stETH, aUSDC, OUSD, or a real-world asset vault token can deposit it into Pendle, receive PT and YT in return, and then sell the YT while retaining the PT. By doing so, they forgo future variable yield in exchange for a known upfront payment, and the discount at which PT trade relative to their redemption value determines the fixed rate they earn if they hold the PT to maturity. In effect, the buyer of the YT compensates them today for the right to receive all future yield, turning the seller’s position into a fixed-rate bond-like instrument.

For example, an OUSD holder who wants predictability rather than variable yield could sell their YT in the wOUSD Pendle market and keep the PT, thereby locking in a fixed APY close to the yield that OUSD is expected to generate over the period. Similarly, a user exposed to a synthetic dollar strategy such as sUSDD or jrUSDe that offers high but uncertain yield may prefer to convert into PT to remove rate volatility from their portfolio. This kind of de-risking is particularly attractive in environments where nominal yields are high enough that users are willing to sacrifice some upside in exchange for certainty, or when they expect yields to trend downward due to competition, emission reductions, or macroeconomic shifts.

From a portfolio perspective, PT-based strategies can be used to build bond ladders and duration profiles. Users can buy PT across multiple maturities and assets, constructing a staggered schedule of fixed income streams that approximate traditional bond ladders. Institutions such as treasuries, DAOs, or market makers might allocate a portion of their holdings to short-dated PT in highly liquid markets, using them as a yield-generating cash management tool while maintaining flexibility to redeploy capital at maturity. As Pendle’s range of supported assets and maturities grows, this kind of fixed-income portfolio construction becomes more viable, particularly when combined with external tools for analytics, risk management, and execution.

Speculating On And Hedging Yield With YT

Yield tokens are naturally suited for more aggressive or tactical strategies because they concentrate exposure to the future path of yield. Traders who believe that yield on a given asset will remain elevated or increase can buy YT, often gaining leveraged exposure compared with simply holding the underlying asset, because the YT represent only the variable component. For instance, if a synthetic dollar product like sUSDD is expected to maintain very high yields due to protocol incentives and favorable market conditions, traders may accumulate YT-sUSDD positions to capture that stream, accepting the risk that yields could fall or incentive programs may change. Coverage in Pendle-focused reports has pointed to YT-sUSDD positions with projected annualized returns approaching eighty percent at certain times, reflecting periods when the underlying yield plus incentives are unusually rich, although such figures should be treated as time-specific snapshots rather than guarantees.

YT can also function as a hedging instrument. Lenders who earn variable interest on stablecoins via Aave or Morpho might buy YT linked to similar assets on Pendle to offset the risk of yield decline; conversely, borrowers who pay variable interest could sell YT to synthetically receive a fixed rate. Real-world credit protocols might hold YT to retain upside exposure to spreads while selling PT to investors who seek fixed coupons. In this way, YT markets enable a variety of interest-rate-style trades analogous to those facilitated by swaps and options in traditional finance, with the important difference that they are tokenized and integrated directly into DeFi’s composable architecture.

Because YT prices reflect discounted expectations of cumulative future yield, they can also be used as signals. For example, if market participants anticipate that stablecoin yields derived from US Treasuries will compress as rates fall, they may bid PT higher (reducing implied fixed yield) while marking down YT, leading to term structures that encode the expected path of monetary policy and credit conditions. Analysts and protocols can monitor these curves to infer market expectations about future yield environments, informing treasury decisions or governance proposals. Over time, as liquidity and maturity coverage deepen, Pendle’s YT and PT markets could evolve into a de facto interest rate curve for on-chain assets.

Liquidity Provision And Meta-Yield Strategies

Liquidity providers occupy a third role in Pendle’s ecosystem, sitting between PT and YT traders. By adding capital to PT–SY pools, LPs earn trading fees from users who swap between principal tokens and SY, along with any protocol incentives offered by Pendle or external partners. In markets like the wOUSD pool, Origin has combined emissions with Pendle’s incentives to offer LPs annualized yields well above what they would earn from simply holding OUSD, albeit with the added risk of impermanent loss and exposure to PT pricing volatility. In other pools, such as those linked to sUSDD, jrUSDe, or srUSDe, LPs may capture a share of high-yield activity around novel structured dollars, with returns amplified by token incentives and the underlying yield-bearing nature of SY.

Advanced strategies often layer these roles. A user might simultaneously act as an LP, hold PT, and trade YT across several markets to construct complex income and risk profiles. For instance, they might provide liquidity in a PT–SY pool to earn fees and incentives, hold some PT to earn fixed yield, and hold or short YT to hedge or enhance their exposure to yield volatility. Others may use external lending protocols to lever up their Pendle positions, depositing PT into Morpho or Aave as collateral, borrowing stablecoins, and then re-entering Pendle to buy more PT or YT, thereby compounding returns at the cost of additional liquidation risk. These “meta-yield” strategies are constrained primarily by risk appetite, collateral parameters on integrated lending markets, and the depth of Pendle’s own liquidity.

Automation is increasingly important in managing such strategies, and this is where Pendle’s AI-focused tooling, discussed below, enters. Automated agents can monitor implied yields, price dislocations, and collateral ratios across multiple protocols, executing adjustments that would be cumbersome for human traders to perform manually. Combined with alerting tools like the Pendle Trading Alert Bot, this automation can make complex fixed-income strategies more accessible to a broader range of users, although it also introduces new operational and security risks that must be managed carefully.

Pendle emerges as DeFi’s yield standard, turning fixed-rate PT tokens into liquid collateral and attracting institutional flows into tokenized yield markets

Pendle becoming DeFi yield standard is huge for fixed-rate adoption

- Smart-contractHigh

The Penpie exploit (which triggered a full Pendle contract pause) and a separate whale wallet compromise via an unprotected flashloan callback in approveDelegation demonstrate that Pendle's composable architecture creates non-obvious attack surfaces in dependent protocols.

A single EigenLayer narrative shift drained over 396k ETH ($1.3bn+) from Pendle pools, and Chaos Labs warned that a funding-rate reversal on Ethena's $6.6B Aave position could trigger rapid mass deleveraging through Pendle PT positions.

- MarketHigh

PENDLE's 74% surge on EigenLayer airdrop speculation followed by large LRT outflows illustrates extreme reflexivity — token price and TVL are tightly coupled to external narrative cycles rather than intrinsic protocol revenue.

Pendle PT tokens now serve as collateral on Aave, Morpho, Gearbox, and Dolomite simultaneously; the USD0++ depeg demonstrated how a single upstream stablecoin policy change propagates losses and trapped positions across all integrated venues at once.

Pendle's deliberate pursuit of KYC-compliant yields for TradFi and participation in Vietnam's IFC delegation alongside Blackrock and Deutsche Bank invites regulatory scrutiny of whether tokenized fixed-rate instruments constitute unregistered securities.

- CentralizationLow

The Pendle Twitter account compromise was a social-layer incident with no on-chain impact, but it temporarily spread panic about a protocol hack — indicating the team's single official communication channel is a reputational single point of failure.

Governance, Token Dynamics, And Institutional Adoption

Pendle’s native token, PENDLE, underpins governance and incentive mechanisms in the protocol’s ecosystem. While the precise tokenomics are beyond the scope of the available sources, recent coverage has highlighted that the protocol has undertaken substantial buyback programs, including a charted plan to repurchase around 1.7 million PENDLE on the open market, and that holders of a staked version of the token, sPENDLE, have received sizable airdrop rewards in connection with these activities. Such programs suggest a model in which protocol revenue and ecosystem growth translate into value capture for token holders, whether through direct buybacks, fee distributions, or control over the allocation of liquidity incentives.

Governance decisions in Pendle include choices about which assets to list, how to configure market parameters, and how to direct incentive emissions across pools. As institutional usage of PT and YT grows, these decisions become more consequential because they affect not only retail traders but also strategies run by funds, treasuries, and structured product issuers. For example, the introduction or sunsetting of specific Strata pools—Pendle’s fixed maturity structures for certain assets—can shape capital flows and rollover behavior for large users. Recent communications from the team have discussed sunsetting April Strata pools at maturity and guiding users to migrate into new June srUSDe and jrUSDe markets, reflecting an active management approach to maintaining coherent term structures and ensuring that liquidity remains concentrated in current maturities rather than fragmenting across stale pools.

Institutional adoption has been bolstered by both technical and reputational factors. On the technical side, Pendle’s emergence as a “yield standard” has been underscored by the growing use of PT as liquid collateral across lending markets and CDP stablecoins, with institutional players like Wintermute and other financial firms making PT-based strategies part of their product offerings. On the reputational side, inclusion in Fortune’s Crypto Innovators list and participation in high-profile delegations alongside large traditional finance institutions, such as the Vietnam IFC mission featuring BlackRock, Morgan Stanley, and Deutsche Bank, have signaled to the broader market that Pendle is viewed as a credible and innovative project by mainstream actors.

At the same time, this rising profile comes with heightened expectations around risk management, security, and regulatory awareness. As Pendle’s markets increasingly touch real-world asset flows and regulated stablecoin reserves, and as institutional capital allocates to PT and YT, the protocol’s governance must remain attentive to potential legal, compliance, and systemic risk issues. Decisions about which RWA issuers to integrate, how to handle KYC-encumbered assets, and how to respond to regulatory developments in key jurisdictions will all shape Pendle’s medium-term trajectory. The protocol’s stated product roadmap aims to balance simplicity and power by refining user experience while maintaining sophisticated under-the-hood mechanics, an approach likely designed to make the platform accessible to both retail and institutional participants without sacrificing flexibility.

AI Agents, Automation, And Security Considerations

Pendle has explicitly positioned itself as “AI-ready” by launching Pendle Skills and a Multi-Chain Protocol (MCP) interface that allow autonomous agents to interact with its markets programmatically. The team has highlighted integrations with leading AI platforms such as Anthropic’s Claude and OpenAI’s ChatGPT, enabling AI agents to query market data, assess yield opportunities, and execute transactions within Pendle’s ecosystem. In principle, this opens the door for highly automated strategies where agents can monitor implied yields across PT markets, evaluate the risk of different YT positions, and rebalance portfolios based on predefined objectives or learned patterns, all without continuous human oversight.

This trend reflects a broader movement in financial services, where AI agents are increasingly deployed not only for customer support but also for cybersecurity, fraud detection, and, in the future, direct facilitation of payments and financial transactions. A survey by the Cloud Security Alliance found that roughly 62 percent of financial firms had deployed AI agents, with 93 percent granting them some degree of autonomy, yet many had not fully secured these tools or even verified whether they had been abused by attackers. The same report noted that around one-fifth of respondents had experienced security incidents linked to misconfigured AI tools, and another fifth were unsure whether such incidents had occurred, underscoring the opacity and risk associated with agentic AI in sensitive environments.

For a protocol like Pendle, this context raises important questions. On the one hand, AI agents could significantly enhance the efficiency of yield strategies by dynamically shifting between PT, YT, and LP positions, monitoring on-chain risk indicators, and reacting to governance or market changes faster than human traders. Agents could also be used by treasuries and DAOs to implement policy mandates, such as maintaining target fixed-income allocations or automatically rolling PT positions at maturity into new instruments. On the other hand, if agents are misconfigured, compromised, or over-privileged, they could execute harmful trades, leak sensitive strategy parameters, or interact with malicious contracts, especially in a permissionless environment where exploits can be orchestrated at machine speed.

Pendle’s AI tooling and integrations therefore need to be considered alongside robust security practices. Users and institutions deploying agents to trade on Pendle should implement strict access controls, limit spending and approval allowances, and monitor agent behavior for anomalies. The protocol itself can contribute by providing well-documented, least-privilege interfaces, transparent audit trails, and tools for simulating and testing agent strategies in sandbox environments. As agentic AI becomes more prevalent in DeFi, the interplay between automated yield optimization and protocol-level safeguards will become a central theme, and Pendle’s early move into AI integrations places it at the forefront of that discussion.

Risks, Challenges, And Competitive Landscape

Like all DeFi protocols, Pendle exposes users to a range of risks that must be understood in context. At the base layer, smart contract risk is ever-present: bugs or design flaws in the SY wrapper, PT and YT minting logic, AMMs, or governance processes could lead to loss of funds or mispricing. Because Pendle sits atop other protocols—staking services, lending markets, stablecoin issuers, RWA vaults—it also inherits their risks. If an underlying yield-bearing asset suffers a depeg, default, governance failure, or hack, PT and YT markets linked to that asset will reflect the shock, potentially transmitting it to other protocols where PT are used as collateral. This layered risk structure makes Pendle both powerful and complex, as it can amplify yield but also propagate stress.

Interest rate and basis risk are core to Pendle’s design. Users locking in fixed yield via PT face the risk that market yields may rise after they enter their position, leading to opportunity cost, or that they misjudge the credit or protocol risk of the underlying asset. YT holders are exposed to the risk that future yield falls short of expectations, whether due to reduced emissions, competition, or macroeconomic changes that compress returns on underlying assets such as Treasuries and corporate credit. Liquidity risk is also significant: while some Pendle markets are deep and active, others are more niche, and exiting a PT or YT position in a stressed environment may involve substantial price impact, particularly for long-dated or RWA-linked instruments.

The increasing use of PT as collateral introduces systemic considerations. If a large share of PT is rehypothecated across Aave, Morpho, CDP stablecoins like USG, and other protocols, sudden changes in PT pricing could trigger liquidations and deleveraging cascades. Galaxy’s analysis of Aave’s leverage markets already points to concentrated risk in liquid staking derivatives, with PT contributing a smaller but non-trivial share of levered collateral. As the Pendle ecosystem expands and more PT types become accepted collateral, risk managers will need to track correlations between PT markets, underlying assets, and other collateral types to avoid unexpected feedback loops under stress.

Competition is another dimension. Pendle is not the only protocol exploring tokenized fixed income and yield derivatives, and it must continue to innovate in order to maintain its position as a leading yield trading platform. Competitors may emerge with alternative designs, improved UX, or more targeted regulatory positioning, especially as real-world asset issuers and large financial institutions build their own tokenization stacks. In addition, macroeconomic changes that substantially lower global interest rates or reduce spreads on RWA strategies could compress the yield available to distribute via PT and YT, making the economics less compelling for users. Conversely, if on-chain yields become artificially high due to aggressive incentives, the system might attract speculative capital that is quick to exit when incentives are reduced, leading to TVL volatility.

Finally, regulatory and compliance developments will shape the environment in which Pendle operates. As tokenized Treasury products, credit funds, and stablecoins interact with protocols like Pendle, questions about the status of PT and YT under securities laws, tax treatment of tokenized yield, and the responsibilities of protocol governance may come to the fore. Pendle’s participation in initiatives such as the Vietnam IFC delegation alongside global banks indicates awareness of these issues and a desire to engage with policymakers and institutions. However, navigating this landscape will require careful design choices and ongoing dialogue to ensure that the benefits of on-chain fixed income are realized without running afoul of evolving regulatory frameworks.

Outlook

Pendle’s trajectory so far suggests that tokenized yield markets are likely to remain a central pillar of DeFi’s evolution. By standardizing the separation of principal and yield through the SY–PT–YT framework, and by building deep, composable markets around these instruments, Pendle has translated a wide range of on-chain and off-chain cash flows into tradable fixed and floating rate exposures. Its integration into lending protocols like Aave and Morpho, its role in stablecoin and RWA ecosystems such as USDG, OUSD, and ACRED vaults, and its involvement in pipelines like STRC–Saturn–sUSDat all point toward a future where PT and YT function as common building blocks in on-chain financial engineering.

At the same time, the protocol’s embrace of AI agents and automation, its experimentation with new market designs and liquidity incentives, and its growing recognition among both crypto-native and traditional finance institutions indicate that Pendle is not static but actively adapting to a rapidly changing ecosystem. If it can continue to deepen liquidity, broaden asset coverage, and maintain robust risk management while simplifying user experience, Pendle is well-positioned to serve as a foundational layer for on-chain fixed income and yield derivatives. The key challenges will be managing compositional risk across stacked protocols, addressing the security and governance implications of automated agent participation, and navigating the regulatory terrain around tokenized interest-bearing instruments.

For market participants, Pendle offers both opportunity and responsibility. Fixed-yield seekers, yield speculators, liquidity providers, and institutional structurers can all find tools within its ecosystem to implement sophisticated strategies that would have been difficult or impossible in earlier phases of DeFi. But they must also understand the underlying mechanics, recognize that PT and YT are not risk-free, and appreciate how Pendle’s markets interact with broader crypto and macroeconomic conditions. As DeFi matures and converges with traditional financial infrastructure, Pendle’s experiment in making yield itself a liquid, programmable primitive will be an important case study in what it means to build fixed income for a decentralized, tokenized world.

Latest Pendle news

Apyx brings Strategy’s DAT preferred stock dividends onchain via Pendle, letting DeFi users lock fixed or floating yield strategies targeting 13-15% APYDune data confirms “Pendle Effect” as PT/YT markets drive token demand surges, boosting holders, supply, and capital inflows via yield tokenization and DeFi composabilityPendle emerges as DeFi’s yield standard, turning fixed-rate PT tokens into liquid collateral and attracting institutional flows into tokenized yield marketsBungee enables Pendle PTs to be access from any chain and from one deep pool on Ethereum.Pendle to sunset April Strata pools at maturity, urging users to migrate positions as new June srUSDe and jrUSDe markets go liveTangent unveils $USG, a CDP stablecoin backed by Curve LP tokens and Pendle PTs, unlocking borrowing against yield positionsSources

- https://www.pendle.finance

- https://nansen.ai/post/what-is-pendle-finance-yield-tokenization-explained-how-to-earn

- https://pluang.com/en/news-feed/pendle-dan-tokenized-yield-narasi-baru-defi-dengan-suku-bunga-tetap

- https://docs.pendle.finance/pendle-v2/ProtocolMechanics/YieldTokenization/SY

- https://x.com/tn_pendle/article/2054722120626885072

- https://x.com/pendle_fi/status/2056241500691079487

- https://x.com/pendle_fi/status/2037364071927034001

- https://fortune.com/2026/06/11/crypto-innovators-2026-asia-europe-usa/

- https://x.com/pendle_fi/status/2066460767407456302

- https://x.com/coingecko/status/2055272773862212071

- https://x.com/Dune/article/2051286497974980686

- https://x.com/pendle_fi/status/2055181434340680125?lang=en

- https://www.originprotocol.com/blog/pendle-wousd-market

- https://www.investing.com/news/cryptocurrency-news/pendle-joins-vietnam-ifc-delegation-alongside-blackrock-morgan-stanley-and-deutsche-bank-4589148

- https://www.cybersecuritydive.com/news/ai-agents-financial-services-payments-security-risks/822800/

- https://www.coingecko.com/learn/strategy-strc-defi-strc-yield-saturn-pendle

- https://www.galaxy.com/insights/research/aave-how-much-leverage-defi-looping-eth-weth-weeth-rseth-wsteth

- https://x.com/pendle_fi/status/2054724105694478723

- https://x.com/pendle_fi/status/2066830653522636944

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…