In-depth explainer on Aave and the AAVE token, covering protocol mechanics, GHO stablecoin, Horizon RWAs, governance, risk events like the rsETH exploit, and evolving tokenomics that tie DeFi lending cash flows to AAVE’s long-term value.

- x.com134

- governance.aave.com31

- aavechan.notion.site15

- theblock.co13

- dlnews.com10

- youtube.com5

- snapshot.org4

+19 sources across the wider coverage universe

Aave founder Stani Kulechov dismisses reports of a Payward stake sale at a 70% discount, saying AAVE isn't for sale as DAO revenue tops $134M annually2026-06

Aave founder Stani Kulechov dismisses reports of a Payward stake sale at a 70% discount, saying AAVE isn't for sale as DAO revenue tops $134M annually2026-06 Someone lost $50M swapping USDT for AAVE2026-03

Someone lost $50M swapping USDT for AAVE2026-03 Following BGDLabs example, the Aave-chan Initiative share it's plans to leave the AAVE DAO in 4 months citing governance capture2026-03

Following BGDLabs example, the Aave-chan Initiative share it's plans to leave the AAVE DAO in 4 months citing governance capture2026-03 Aave expands to Solana as $AAVE goes live via Sunrise, marking a major cross-chain move to bring DeFi lending into Solana’s high-speed ecosystem2026-04

Aave expands to Solana as $AAVE goes live via Sunrise, marking a major cross-chain move to bring DeFi lending into Solana’s high-speed ecosystem2026-04 Researcher argues crypto's next cycle will favor revenue-generating assets over speculative tokens, with protocols like AAVE and Jupiter outperforming through buybacks and value accrual2026-06

Researcher argues crypto's next cycle will favor revenue-generating assets over speculative tokens, with protocols like AAVE and Jupiter outperforming through buybacks and value accrual2026-06 Update: User loses almost entire $50M USDT trying to buy AAVE via Aave after accepting an extreme slippage warning Stani says which was clearly flagged in the interface, prompting debate and a 600k fee refund pledge2026-03

Update: User loses almost entire $50M USDT trying to buy AAVE via Aave after accepting an extreme slippage warning Stani says which was clearly flagged in the interface, prompting debate and a 600k fee refund pledge2026-03

AAVE and the Aave Protocol: An Evergreen DeFi Explainer

One of the longest-running and most systemically important DeFi lending platforms, Aave is a non‑custodial money market protocol where users supply assets like ETH and USDC to earn interest and borrow against overcollateralized positions. The AAVE token sits at the center of this ecosystem as a governance and risk‑backing asset that is gradually evolving into a pure cash‑flow token, as protocol revenue, the GHO stablecoin, and new RWA initiatives like Aave Horizon deepen the link between protocol usage and token value.

Origins and Evolution of the Aave Protocol

From ETHLend to a Leading DeFi Money Market

Aave traces its roots to ETHLend, one of the earliest experiments in decentralized, peer‑to‑peer crypto lending on Ethereum. ETHLend originally matched individual lenders and borrowers directly, but the approach proved difficult to scale because each loan required its own order book and negotiation. The team pivoted to a pooled liquidity model and rebranded as Aave, launching what would become a generalized, non‑custodial liquidity protocol that allows users to supply and borrow from shared asset pools. This design choice—shifting from bilateral loans to algorithmic money markets—has been central to Aave’s subsequent growth and resilience.

At its core, the protocol enables two primary behaviors. Suppliers deposit assets such as ETH, USDC, or other tokens into on‑chain pools and receive interest‑bearing aTokens in return, while borrowers tap these pools by posting collateral whose value exceeds the amount they wish to borrow. Interest rates are determined algorithmically based on the utilization of each pool, meaning markets continuously balance supply and demand without centralized intermediaries. The combination of overcollateralization and transparent on‑chain liquidation rules allowed Aave to function as a kind of “bank without bankers,” an analogy later picked up by research from traditional‑style asset managers evaluating AAVE as a cash‑flow generating token.

Over time, Aave grew from a niche Ethereum dApp into a multi‑chain protocol spanning major L1 and L2 environments. Each deployment retains the same core architecture but can be configured with different asset listings and risk parameters, allowing the protocol to adapt to the idiosyncrasies of each network’s liquidity and security profile. This modular expansion strategy positioned Aave as a base layer of DeFi credit infrastructure, with other protocols integrating Aave markets as a source of leverage, yield, or liquidity, while leaving governance and risk management to the Aave DAO.

Growth, TVL, and Market Share

By 2025, Aave had become the dominant decentralized lending platform by total value locked (TVL) and market share. Aave’s own year‑end recap reported that deposits peaked at approximately 75 billion dollars in 2025, the highest ever recorded by a DeFi protocol at that time, ending the year around 55 billion dollars, a 57 percent increase from the start of the year. Independent market analyses similarly found that Aave commanded roughly 62 percent of the on‑chain lending market in 2025 when compared to peers such as Compound and Maker, a level of concentration that underscores both the protocol’s success and its systemic importance within DeFi.

This scale is not solely the result of early‑mover advantage. Aave’s product roadmap included features such as multiple interest rate modes, flexible collateral types, and later innovations like the GHO native stablecoin and the Aave Horizon RWA market, all of which expanded the protocol’s addressable user base. Governance decisions by the Aave DAO to list new assets, launch on additional chains, and experiment with novel collateral like liquid restaking tokens also contributed to TVL growth, albeit at the cost of increased complexity and risk, as later exploits involving third‑party tokens would show.

From a macro perspective, Aave’s growth occurred against a backdrop of volatile crypto cycles, regulatory uncertainty, and alternating periods of speculative mania and risk‑off deleveraging. Yet, despite these headwinds, the protocol’s cumulative revenue and liquidity metrics have trended upward over multi‑year horizons, supporting the thesis that decentralized credit markets can function as enduring financial primitives rather than short‑lived speculative fads. This resilience is central to the emerging narrative that protocols like Aave, which generate measurable cash flows, may be better candidates for long‑term valuation frameworks than purely narrative‑driven tokens.

Major Milestones and Multi‑Chain Expansion

Several milestones mark Aave’s transition from experimental project to DeFi mainstay. The introduction of the AAVE governance token on Ethereum formalized the protocol’s decentralized governance structure, giving token holders the ability to propose and vote on changes to risk parameters, asset listings, and new product launches. Subsequent versions of the protocol—v2, v3, and beyond—refined interest rate models, added isolation and efficiency modes for different collateral types, and improved capital efficiency across markets.

Aave also steadily embraced a multi‑chain strategy by deploying on rollups and alternative L1s. A notable step in this direction was the launch of the AAVE governance token natively on Solana via Sunrise DeFi, supported by a loan of USDT from the Solana Foundation and immediate ecosystem integrations to bootstrap liquidity. This move signaled that Aave’s ambitions extend beyond the Ethereum ecosystem, aiming to bring its lending model into high‑throughput environments where user demand for low‑fee, low‑latency transactions is high. At the same time, such cross‑chain expansion introduces new governance, bridging, and risk‑management challenges, forcing the DAO to weigh growth opportunities against the potential for fragmented liquidity and security assumptions.

In parallel, Aave launched the GHO stablecoin and Aave Horizon, representing two strategic bets: one on capturing stablecoin demand within the protocol’s own credit system, and another on onboarding real‑world assets (RWAs) and institutional capital into permissioned DeFi markets. These milestones collectively illustrate Aave’s evolution from a single‑product lending dApp to a broader financial platform with interconnected components spanning retail users, DeFi power users, and regulated institutions.

Aave founder Stani Kulechov dismisses reports of a Payward stake sale at a 70% discount, saying AAVE isn't for sale as DAO revenue tops $134M annually

$50M buyback framework against a ~$1.3B AAVE mcap is why the discount rumor had teeth: this isn't a passive governance token waiting for someday value accrual. Aave has already pushed toward surplus distribution via Umbrella, treasury-funded buybacks, GHO revenue, and Chainlink SVR liquidation MEV, so any strategic stake sale would reprice DeFi cash-flow tokens way beyond AAVE. A forced-looking 70% print would have handed bears a comp; Stani killing it fast keeps the valuation debate on protocol economics instead of cap-table distress.

Readers don't click Aave for yield rates or TVL milestones — they click for governance as power struggle: who controls risk decisions, whose whale position threatens the whole protocol, and whether influential outsiders (Vitalik, Mich, Gauntlet) validate or destabilize the system with a single on-chain move.↗

How the Aave Protocol Works

Non‑Custodial Liquidity Pools and Overcollateralized Lending

Aave operates as a set of non‑custodial liquidity pools where users retain control of their funds through smart contracts rather than entrusting them to a centralized entity. When a user supplies an asset—such as ETH, USDC, or another supported token—they receive a corresponding aToken that represents their share of the pool plus accrued interest. These aTokens are themselves ERC‑20 compatible, meaning they can be transferred, used as collateral in other protocols, or integrated into more complex DeFi strategies without withdrawing the underlying funds from Aave.

Borrowers interact with the same pools by locking collateral that exceeds the value of the assets they wish to borrow, enforcing an overcollateralization ratio designed to protect lenders in the event of price volatility. The protocol calculates a “health factor” for each account based on the value and risk parameters of its collateral and borrowed assets; if this health factor falls below a threshold due to adverse price movements or additional borrowing, the position becomes eligible for liquidation. This mechanism, while harsh for under‑collateralized users, is central to maintaining the solvency of the lending pools and ensuring that lenders can always withdraw their funds, barring extreme market dislocations.

Because Aave is permissionless at the protocol level, anyone with a compatible wallet can supply or borrow, without undergoing traditional credit checks or Know‑Your‑Customer (KYC) procedures on the core markets. This open access is part of what makes Aave a powerful composable primitive in DeFi but also raises policy questions as regulators increasingly scrutinize non‑custodial credit platforms. Aave’s answer to this tension has been to keep the core markets permissionless while building separate, permissioned environments like Aave Horizon for regulated entities, rather than retrofitting the original protocol with access controls.

Interest Rate Models and Utilization Dynamics

Interest rates on Aave are not set by human discretion but emerge from algorithmic curves that adjust based on the utilization of each asset pool. When a pool is lightly utilized—meaning a large fraction of supplied assets remain unborrowed—borrow rates are relatively low and supply rates are modest, reflecting ample liquidity and limited demand. As more users borrow a particular asset and utilization rises, the protocol gradually increases the borrow rate, which in turn raises the yield for suppliers. At high utilization levels approaching a “kink” point, the rate curve becomes steeper, sharply increasing the cost of borrowing to incentivize repayments or additional supply.

This utilization‑based model is especially important for stablecoins like USDC, which often serve as the primary borrowed asset for traders seeking leverage or hedging, and for ETH or liquid staking derivatives like wstETH, which are popular as collateral. During periods of market stress, utilization can spike rapidly as users rush to borrow stablecoins, sometimes pushing markets toward 100 percent utilization. When this occurs, new withdrawals are effectively blocked until some borrowers repay or liquidations free up liquidity, a dynamic that became highly visible during the KelpDAO rsETH exploit when Aave’s primary stablecoin markets reached full utilization following emergency freezes on affected assets.

Aave offers both variable and, in earlier iterations, more stable interest rate options, though the specifics vary across protocol versions and markets. Variable rates adjust continuously according to utilization, while “stable” rates aim to offer more predictable costs but can still be rebalanced if market conditions shift dramatically. For sophisticated users, these rate modes provide additional levers for managing interest rate risk, though the complexity also increases the learning curve for newcomers.

Liquidations, Collateral Parameters, and Risk Management

Liquidations are a central, if contentious, component of Aave’s risk engine. Each supported asset is assigned specific parameters, including loan‑to‑value (LTV) ratios, liquidation thresholds, and liquidation bonuses, which together define how much can be borrowed against a given collateral and how aggressively positions are liquidated under stress. These parameters are tuned by governance and risk service providers based on factors such as volatility, liquidity, and smart‑contract risk of the underlying assets.

When a position’s health factor falls below one due to collateral price declines or increased borrowing, liquidators can repay part of the debt on behalf of the user and, in return, receive a discounted portion of the collateral. This discount, or liquidation bonus, compensates liquidators for the risk of executing the transaction during moments of price dislocation and for potential slippage when selling the seized collateral. In practice, this creates an incentive layer of bots and market‑makers that continually monitor on‑chain positions and step in to restore solvency when positions become undercollateralized.

Risk management in Aave is not static. Third‑party risk teams such as Chaos Labs have historically provided parameter recommendations and stress‑testing, working alongside other contributors like BGD Labs to enhance protocol safety tools. However, disagreements about appropriate risk levels—especially around newer asset classes like liquid restaking tokens—can become governance flashpoints. Chaos Labs’ decision to depart from Aave governance in 2026, citing a misalignment between its preferred risk approach and the DAO’s direction, illustrates the inherent tension between growth and prudence in an open governance system. These dynamics directly affect end users, because aggressive listings or loose parameters can enhance yields in the short term while raising the probability of bad debt in extreme scenarios.

Multi‑Chain Architecture and Cross‑Chain Design Choices

While Aave originated on Ethereum, its architecture has been adapted to multiple networks, including major L2 rollups and alternative L1s. Each deployment is governed by the same DAO, but risk settings, asset listings, and in some cases even feature sets can diverge to reflect differences in underlying chain security, liquidity depth, and user demand. This approach allows Aave to capture users where gas costs are lower or where specific ecosystems—such as gaming‑heavy networks—require localized credit infrastructure, all while maintaining a unified governance and token system centered on AAVE.

The native issuance of AAVE on Solana through Sunrise DeFi adds another dimension to this cross‑chain strategy. Instead of merely bridging wrapped AAVE from Ethereum, a native Solana deployment allows for deeper integrations with Solana‑specific DeFi protocols and avoids some of the security assumptions associated with third‑party token bridges. The Solana Foundation’s support via a USDT loan underscores the perceived strategic value of aligning a leading Ethereum‑origin protocol with Solana’s high‑throughput environment. Nevertheless, this move raises important questions about token supply consistency, cross‑chain governance coordination, and how to prevent divergent communities from fragmenting the governance base of the protocol.

Cross‑chain design decisions also intersect with risk, as the KelpDAO/LayerZero exploit demonstrated. That incident did not involve Aave’s core contracts being hacked but instead stemmed from an exploit of a cross‑chain bridge used by a collateral token (rsETH), which then propagated risk into Aave markets. As more assets become “omnichain” via bridge standards, Aave’s multi‑chain architecture must increasingly account for security assumptions outside its own codebase, complicating risk evaluation and governance deliberations around asset listings.

The AAVE Token: Governance, Risk, and Value Accrual

Core Properties and Governance Role

AAVE is the native governance token of the Aave protocol, deployed as an ERC‑20 asset on Ethereum and widely traded across centralized and decentralized exchanges. Holding AAVE confers the right to participate in Aave DAO governance, where token holders and their delegates can submit and vote on Aave Improvement Proposals (AIPs) that determine protocol parameters, treasury allocations, and strategic initiatives. This gives the token a dual character: it is both a speculative asset whose price fluctuates with market sentiment and a functional governance instrument that underpins protocol decision‑making.

The governance process is anchored by the Aave governance forum, where proposals are discussed and refined before on‑chain voting. Proposals typically move through stages such as temperature checks, signaling, and formal AIPs, with off‑chain deliberation helping to surface trade‑offs and stakeholder concerns. Token holders can vote directly or delegate their voting power to representatives, including professional governance firms, DAOs, or individual experts. Over time, large token holders—such as venture firms, protocols, or dedicated governance entities—have accumulated significant voting power, shaping the protocol’s long‑term direction.

Beyond pure voting, AAVE also serves as a coordination tool for contributors and partners. Grants, service provider agreements, and ecosystem incentives are often denominated in AAVE or include AAVE components, allowing the DAO to align key stakeholders with the protocol’s long‑term success. This has important implications for token distribution: as the DAO acquires more AAVE via revenue or strategic deals and distributes some back to contributors, the token’s ownership gradually migrates toward entities most involved in governance and operations. Governance debates increasingly revolve around how concentrated this ownership should be and what mechanisms—such as buybacks, fee distribution, or further incentives—are appropriate for balancing decentralization with effective decision‑making.

The Safety Module and Staking‑Backed Risk

One of AAVE’s distinguishing features is its role in the Safety Module, a mechanism designed to act as a backstop against protocol shortfalls. AAVE holders can stake their tokens into the Safety Module in exchange for rewards, with the understanding that these staked tokens may be partially slashed if the protocol incurs bad debt due to unforeseen events such as oracle failures, extreme market crashes, or exploits that affect collateral valuations. The Safety Module thus converts the governance token into a risk‑bearing asset that underwrites the solvency of the wider protocol.

The design of the Safety Module has evolved through multiple iterations, with proposals like the Aave Safety Module v1.5 refining parameters around slashing, reward distribution, and the role of specialized “slashing admins.” For example, one configuration allows a slashing admin to trigger a slash of 2,000 AAVE to cover potential price depreciation during a liquidation event, illustrating how specific risk scenarios are mapped to quantified token losses. While such amounts may be small relative to the total token supply, their existence provides a credible commitment that token holders have “skin in the game” and that governance decisions around risk are not costless.

In practice, the Safety Module has dual implications for AAVE’s valuation. On one hand, staking rewards and the prospect of future protocol revenue streams can make AAVE resemble a yield‑bearing asset, nudging it closer to equity‑like valuation frameworks. On the other hand, the possibility of slashing introduces downside tail risk that must be priced in by holders. The net effect depends on the market’s view of Aave’s risk management effectiveness: the more confident participants are that the protocol can avoid catastrophic shortfalls, the more they may be willing to stake AAVE in exchange for yield and governance influence.

“Aave Will Win” and the Shift to Token‑Centric Value Accrual

A pivotal governance moment for the token was the passage of the so‑called “Aave Will Win” proposal, which founder Stani Kulechov described as the most important vote in Aave’s history. The proposal’s core vision is to make Aave “fully token‑centric,” consolidating the protocol’s economic and governance model around a single asset, AAVE, under a “one asset, one model” design. Among other elements, the plan redirects protocol revenue more explicitly toward AAVE holders, targeting 100 percent of revenue to benefit the token, and retools the system to further entwine AAVE with protocol growth and risk.

Prior to this shift, protocol revenue as defined under AIP‑1 accrued largely to the Aave DAO treasury. In 2025, this revenue reportedly totaled around 140 million dollars, reflecting fees and interest spreads captured across Aave markets. By moving toward a structure where this revenue, or its economic equivalent, increasingly accrues to AAVE holders—whether via buybacks, fee sharing, or staking enhancements—the DAO effectively begins to treat AAVE as a claim on protocol cash flows rather than a purely governance‑oriented asset. This change bolsters the case for valuing AAVE with methodologies akin to those used for financial businesses, such as price‑to‑earnings multiples or discounted cash flow analyses.

The approval of “Aave Will Win” also catalyzed renewed market interest in the token. Coverage at the time noted that AAVE’s price responded positively to the proposal’s passage, reflecting investor enthusiasm for a clearer link between usage and token value. However, such token‑centric designs also raise governance risks: as financial stakes tied directly to protocol revenue grow, so too does the incentive for large holders to influence decisions in ways that maximize short‑term profit at the expense of conservative risk management or user protection. The long‑term success of the shift will depend on whether Aave’s governance can balance these competing pressures.

Valuation Frameworks and the Grayscale Thesis

Research from traditional‑style crypto asset managers, including Grayscale, has highlighted AAVE as an example of a cash‑flow driven DeFi token that can be valued like a financial business. Analysis cited by CoinDesk summarized Grayscale’s view that at a market price of around 75 dollars, AAVE appeared undervalued, with an estimated fair value in the 80‑to‑100‑dollar range and a base‑case price target of roughly 175 dollars over a one‑year horizon. The report reportedly projected Aave’s 2026 revenue at around 60 million dollars and applied a fintech‑style earnings multiple in the 20x to 25x range, situating AAVE conceptually alongside high‑growth financial technology firms rather than purely speculative crypto assets.

Grayscale’s research also characterized Aave as “essentially a bank without bankers,” noting that its net interest margins—the spread between borrowing and lending rates captured as protocol revenue—are lower than those of many traditional banks, but that it benefits from continuous operation, global reach, and minimal overhead costs. This framing underscores the hybrid nature of DeFi protocols: they perform economically similar functions to banks or money market funds but do so through transparent smart contracts, with risks tied to code, governance, and collateral volatility rather than to human operators and regulated capital ratios.

Importantly, valuation theses like Grayscale’s are both time‑bound and assumption‑heavy. Revenue forecasts depend on variables such as crypto market cycles, competition from other lending venues, regulatory developments, and the success of new products like GHO and Aave Horizon. Nonetheless, the very fact that such research can model AAVE in cash‑flow terms reflects a broader shift in crypto investing, where some analysts argue that future cycles may increasingly reward protocols with measurable, on‑chain revenue and robust tokenomics over meme‑driven or purely narrative assets. In that context, AAVE stands as a canonical case study for how DeFi tokens might evolve into quasi‑equity instruments while still retaining open governance characteristics.

- 01Mich CRV loan saga↗

A single whale's undercollateralized CRV position forced Aave governance into a months-long public fight over whether to freeze the asset, buy the debt, or let the protocol absorb bad risk — readers tracked it like a slow-motion systemic crisis.

- 02Vitalik deposit as protocol verdict

Vitalik publicly depositing 1,900 ETH into Aave after DeFi community pressure reframed the act as a credibility signal, drawing the highest click volume of any Aave headline and turning a routine deposit into a cultural event.

- 03Risk provider power struggle↗

Gauntlet's abrupt exit and Llama Risk's contested onboarding exposed that Aave's safety depends on a small number of external firms whose departure can leave a multi-billion-dollar protocol without a functioning risk layer.

- 04Fee switch and AAVE tokenomics↗

Mark Zeller's revenue redistribution and buyback proposal triggered a 45% AAVE token rally and $188M market cap gain overnight, proving readers treat governance temp checks as price catalysts worth front-running.

- 05Multichain expansion and ecosystem exits↗

Aave's simultaneous deployment push onto Base, ZKsync, and Solana — while threatening to abandon Polygon over a bridge liquidity dispute — showed readers a protocol actively redrawing its geographic map through governance votes.

- 06Umbrella safety module redesign↗

The replacement of the original Safety Module with Umbrella, bundled with the fee switch proposal, signaled a structural rethink of how Aave backstops bad debt — readers engaged with it as both a risk story and a token-value story simultaneously.

Aave’s Product Suite: Core Markets, GHO Stablecoin, and Horizon RWAs

Core Lending Markets: ETH, USDC, and Beyond

The heart of Aave remains its generalized lending markets, where users supply and borrow a wide range of crypto assets. ETH frequently serves as a primary collateral asset, reflecting its status as the base asset of the Ethereum ecosystem and a relatively liquid, institutionally tracked cryptocurrency. Stablecoins such as USDC, USDT, and others are heavily utilized on the borrowing side, as traders and DeFi participants often seek dollar‑denominated leverage while posting volatile assets as collateral. This combination allows users to maintain long exposure to ETH or other tokens while accessing liquidity in stablecoins for trading, hedging, or real‑world spending via off‑ramps.

Each asset in Aave’s core markets has its own set of risk parameters, including maximum LTV, liquidation thresholds, reserve factors, and interest rate curves. For instance, highly liquid, relatively stable assets like USDC may be assigned higher collateralization caps and more forgiving thresholds than niche or volatile tokens, which are often listed in isolation or with lower borrowing capacities. Across chains, these configurations may differ: an asset that is safe to list with high limits on Ethereum may warrant stricter constraints on a smaller L2 or alternative L1 with thinner liquidity. Governance is continually asked to evaluate new asset listing proposals and adjust parameters in response to market data, making the composition of Aave’s core markets a living reflection of both market demand and the DAO’s risk appetite.

From a user standpoint, the core markets provide a familiar entry point into DeFi lending. Wallet integration is typically straightforward, and many interfaces abstract away complexity by showing users simple metrics such as APY for supplying or borrowing, along with their health factor and liquidation price estimates. Behind this user experience, however, lies a sophisticated risk and rate engine that constantly recalibrates the incentives for suppliers and borrowers, as well as an increasingly intricate interplay with downstream protocols that build on top of Aave’s liquidity.

GHO: A Native, Overcollateralized Stablecoin

GHO is Aave’s native, decentralized, overcollateralized stablecoin, designed to be minted directly against users’ Aave collateral positions rather than relying on external issuers. Users who deposit approved collateral into Aave can mint GHO as a debt position, much like borrowing USDC or another stablecoin from the protocol, but in this case they are creating new GHO that is secured by their collateral and governed by the Aave DAO. This design allows Aave to internalize stablecoin demand, capturing additional revenue from interest on GHO debt and integrating the stablecoin more deeply into its broader ecosystem.

By early 2026, GHO’s supply had grown to around 500 million dollars, with its market capitalization nearly tripling in 2025 alone. Aave’s 2025 recap emphasized that GHO had become a meaningful revenue driver, generating more than 14 million dollars in annualized revenue by the end of that year. These figures highlight the strategic importance of GHO: rather than relying solely on spreads between deposited and borrowed third‑party stablecoins, Aave can capture stablecoin activity under its own brand, with governance control over parameters such as interest rates, minting caps, and facilitator roles.

GHO also plays into the protocol’s tokenomics. Interest paid on GHO borrowing contributes to overall protocol revenue, which under the evolving “Aave Will Win” framework is increasingly directed toward supporting AAVE holders and the DAO. At the same time, maintaining GHO’s peg and liquidity requires careful coordination with market‑makers, DEXs, and other DeFi protocols that integrate GHO into trading pairs, yield strategies, and cross‑chain stablecoin flows. In this sense, GHO is both a product and a coordination challenge, whose success depends on robust on‑chain liquidity, conservative collateral policies, and credible governance.

Aave Horizon: Real‑World Assets and Institutional DeFi

Aave Horizon represents the protocol’s foray into real‑world assets and institutional‑grade DeFi. Launched by Aave Labs as a new lending market on Ethereum, Horizon allows institutions and other qualified users to borrow stablecoins against tokenized RWAs, such as funds, credit products, or other compliant instruments. Unlike Aave’s permissionless core markets, Horizon is built to meet regulatory and compliance requirements, including permissioned access and enhanced due diligence for participants.

The design goal of Horizon is to transform RWAs into productive on‑chain assets that can be used as collateral in DeFi, while still satisfying the regulatory needs of the entities that issue or hold them. This involves not only technical integration with tokenization platforms but also governance decisions about which issuers and asset types are acceptable, how risk is assessed, and how to handle events like defaults or regulatory actions in the off‑chain world. Because RWAs inherently link on‑chain credit to off‑chain legal claims, Horizon sits at the intersection of DeFi innovation and traditional financial law.

One of the early flagship integrations on Horizon is Bitwise’s tokenized carry fund, USCC (now the Bitwise Crypto Carry Fund), which seeks to capture yield via a market‑neutral basis trade strategy. Bitwise, a large crypto asset manager with around 11 billion dollars in client assets as of April 2025, has been approved as an asset issuer on Aave Horizon. This means that institutions can pledge tokens representing shares in the carry fund as collateral to borrow stablecoins within Horizon, effectively bringing a sophisticated trading strategy into the DeFi collateral universe. The collaboration underscores Aave’s ambition to set a high standard for institutional RWA adoption, positioning Horizon as a hub where traditional financial players can safely interact with on‑chain credit.

Cross‑Chain Expansion and AAVE on Solana

The native launch of AAVE on Solana marks a distinct, cross‑ecosystem step beyond EVM‑centric deployments. Through a collaboration with Sunrise DeFi and support from the Solana Foundation, AAVE became available as a native Solana token, not merely a wrapped representation of the Ethereum asset. This move was accompanied by initiatives to seed liquidity and encourage DeFi protocols on Solana to integrate AAVE, thereby extending the token’s reach and governance community into a high‑throughput, low‑fee environment.

From a strategic perspective, this expansion serves multiple purposes. First, it hedges against ecosystem concentration risk by ensuring that Aave’s brand and governance token are not tied exclusively to Ethereum’s fate. Second, it opens the door for future Aave‑style lending markets or integrated credit products tailored to Solana’s technical architecture and user base. Third, it tests cross‑chain governance models, as AAVE holders on Solana must remain aligned with Ethereum‑based governance decisions despite operating on a different execution layer.

At the same time, cross‑chain token issuance raises operational and economic complexities. Maintaining fungibility between AAVE on Ethereum and AAVE on Solana requires clear communication about total supply, bridging mechanisms, and governance voting rights. If not carefully managed, discrepancies or confusion could create arbitrage opportunities or fragmentation of the community. How Aave navigates these issues will be an important case study for other protocols considering native token deployments across fundamentally different chains.

Institutionalization and the Blending of On‑ and Off‑Chain Credit

The combination of GHO, Horizon RWAs, and institutional partnerships like Bitwise’s USCC positions Aave as a bridge between purely crypto‑native lending and more traditional financial use cases. On one side, individual users and DeFi protocols continue to use Aave for leverage, liquidity, and yield strategies involving assets like ETH, USDC, and GHO. On the other side, regulated entities can enter Horizon markets with tokenized funds and other RWAs, bringing new forms of collateral and borrowing demand onto the same broad platform.

This blending of on‑ and off‑chain credit creates opportunities but also new systemic concerns. As more real‑world economic activity becomes entangled with Aave’s smart contracts, failures in either domain—whether a DeFi exploit or a default in a tokenized bond—can propagate across boundaries. Governance must therefore develop expertise not only in crypto risk but also in legal, regulatory, and macroeconomic factors that affect RWA issuers and structures. The pace at which Aave can scale Horizon and similar initiatives will likely depend on its ability to cultivate such interdisciplinary governance competence, as well as the willingness of institutions to accept decentralized governance as a counterpart.

Governance, the Aave DAO, and Ecosystem Politics

Treasury, Revenue, and Capital Allocation

The Aave DAO controls a substantial treasury of crypto assets accumulated through protocol revenue, token allocations, and strategic deals. A governance report in early 2026 noted that the DAO held approximately 37.9 million dollars in ETH‑correlated assets, and that in February 2026 alone, Single Variable Rate (SVR) liquidation fee revenue totaled about 2,253.4 ETH, worth roughly 4.5 million dollars at an assumed price of 2,000 dollars per ETH. The same report highlighted that the DAO was acquiring more AAVE than it was distributing, implying a net consolidation of governance power inside the treasury.

This accumulation intersects directly with the “Aave Will Win” token‑centric shift. As protocol revenue increasingly flows toward buybacks or other mechanisms benefitting AAVE holders, the DAO must decide how much of that value accrual should be retained in the treasury versus passed through to stakeholders. Treasury management proposals frequently debate issues such as diversification between ETH, stablecoins, and AAVE, investment in growth initiatives or partnerships, and the level of reserves appropriate for covering tail‑risk events.

In parallel, the DAO periodically approves funding packages for core development teams, such as Aave Labs, and for service providers responsible for risk, security, and ecosystem growth. A recently approved package reportedly committed tens of millions of dollars and significant AAVE allocations to Aave Labs to sustain protocol development over a multi‑year horizon, reflecting token holder willingness to invest in the protocol’s long‑term roadmap. Such allocations must be weighed against competing uses of funds, including buybacks, liquidity incentives, or expanding the Safety Module.

Governance Processes and Proposal Dynamics

Governance activity is coordinated through the Aave governance forum and on‑chain voting systems. Proposals are typically authored by core contributors, ecosystem partners, or independent community members and then undergo open discussion where parameters, risks, and potential benefits are debated. Once a proposal gains sufficient support and clarity, it can advance to on‑chain voting, where AAVE holders or their delegates cast votes weighted by token holdings.

Some proposals, like routine parameter adjustments, may attract limited attention beyond specialized risk teams and power users. Others, such as the “Aave Will Win” proposal, become highly publicized events that rally community engagement and political campaigning. The passage of that proposal by a wide margin underscored the community’s appetite for a more explicitly token‑centric economic model, even as it sparked concerns about how revenue concentration might affect long‑term protocol resilience and user outcomes.

Governance processes also interact with external stakeholders. For instance, when MantleCore submitted a draft MIP‑34 proposal to lend up to 30,000 ETH from the Mantle Treasury to the Aave DAO at a rate of Lido staking yield plus 1 percent, the move was tied to Aave’s need to address bad debt stemming from the rsETH exploit and was accompanied by Mantle’s accumulation of approximately 130,000 AAVE in voting power. This episode demonstrates how external treasuries can use both financial arrangements and governance participation to influence DeFi protocol trajectories, blurring the line between protocol‑to‑protocol credit relationships and governance coalitions.

Contributor Departures and Governance “Brain Drain”

While Aave’s DAO governance model has attracted a diverse set of contributors, it has also faced notable departures. Chaos Labs, a key risk service provider, announced that it was leaving Aave because its engagement no longer reflected how it believed risk should be managed, explicitly citing disagreements over the path the protocol was taking. This followed earlier exits or reduced involvement from other contributors, such as BGD Labs and the Aave Chan Initiative (ACI), raising questions about whether governance is effectively retaining specialized talent and whether decision‑making processes adequately incorporate expert recommendations.

These departures highlight structural tensions within token‑based governance. Service providers are often compensated in AAVE or stablecoins and must justify their budgets to token holders who may prioritize short‑term cost savings or token price appreciation over conservative risk management. When risk teams push for tighter controls or more conservative asset listings, they can clash with community members who favor aggressive growth and higher yields, leading to political friction. If such disagreements escalate, providers may simply choose to leave for other protocols or focus on less contentious ecosystems.

The net effect of contributor churn can be a “brain drain,” where accumulated expertise about the protocol’s risk profile, technical nuances, and historical decisions dissipates over time. To counter this, Aave’s governance may need to invest in better processes for onboarding, retaining, and incentivizing key contributors, alongside clearer mandates and performance metrics that align risk management outcomes with token holder interests.

Treasury Partnerships, Loans, and Strategic Alignments

Treasury‑level partnerships are increasingly important in Aave’s governance story. The MantleCore loan proposal is one example, where a separate DAO treasury considered lending a large amount of ETH to Aave under specific yield terms to help cover potential shortfalls created by the rsETH exploit. In exchange, Mantle also accumulated significant AAVE voting power, giving it a direct say in how Aave manages the crisis and future risk decisions. This illustrates a pattern where financial alignment—via loans, investments, or liquidity provision—goes hand in hand with governance influence.

Similar dynamics can be seen in institutional integrations like Bitwise’s participation in Aave Horizon. By becoming an approved asset issuer, Bitwise not only brings new collateral into the protocol but also becomes an important stakeholder in the success and risk profile of Horizon markets. As more institutions, DAOs, and funds establish such relationships, Aave’s governance map evolves into a complex web of overlapping economic and political interests, where decisions about risk parameters, fee structures, and product design have multi‑dimensional implications.

For token holders, understanding these alignments becomes part of the governance due diligence process. Voting for or against proposals no longer involves only abstract policy preferences but often entails taking a position on the role of specific counterparties in Aave’s ecosystem and on whether particular financial arrangements improve or impair the protocol’s long‑term health.

Community Engagement, Voter Participation, and Delegation

Despite Aave’s prominence, governance participation remains concentrated among a relatively small set of active voters and delegates, a pattern common to many token DAOs. Many AAVE holders do not vote directly, either due to the cost and complexity of participation or because they treat their holdings primarily as financial investments rather than governance instruments. Delegation systems allow these passive holders to assign their voting power to more engaged participants, but this can exacerbate centralization if a few delegates accumulate outsized influence.

The DAO has experimented with mechanisms to encourage broader engagement, including transparency reports, open community calls, and occasional governance incentives. Yet, meaningful participation still tends to require substantial technical, financial, and risk‑management expertise, which naturally limits the number of individuals able to contribute at a deep level. Over time, Aave’s governance may need to explore models that combine expert‑driven councils with broader token‑holder oversight, or adopt novel voting mechanisms that better surface informed minority positions.

In the meantime, the practical reality is that a relatively small core of engaged governance actors—comprising contributors, large token holders, DAOs, and institutional partners—plays a decisive role in steering Aave through both routine parameter updates and critical crises. How these actors coordinate and balance their interests will remain a key factor in the protocol’s trajectory.

CRV price crash triggers debate over Mich's Aave loan; Gauntlet recommends freezing CRV and zeroing LTV on v2

Aave v3 deploys on ZKsync Era mainnet with Chainlink oracle integration

Gauntlet terminates risk provider agreement with Aave DAO, citing inability to continue work

Aave DAO votes to onboard Llama Risk as second risk service provider

cbBTC onboarded to Aave; supply cap doubled from 450 to 900 BTC after hitting limit within days of launch

Fee switch and Umbrella Safety Module proposals introduced; AAVE token surges 45% in four weeks on tokenomics revamp anticipation

GHO stablecoin market cap breaks $500M

Aave deploys on Solana as part of multichain expansion strategy backed by Solana Foundation

Risk, Incidents, and Protocol Resilience

The KelpDAO/LayerZero rsETH Exploit: Anatomy of a Crisis

The KelpDAO/LayerZero exploit in 2026 provides a stark illustration of the indirect risks Aave faces from third‑party protocols and cross‑chain infrastructure. On a Saturday in early 2026, KelpDAO’s liquid restaking token, rsETH, suffered a roughly 290 million dollar exploit, the largest DeFi hack of the year to that point. The attacker exploited the single‑verifier configuration of KelpDAO’s LayerZero omnichain fungible token (OFT) bridge, tricking the bridge into releasing 116,500 rsETH from Ethereum mainnet escrow that should not have been unlocked.

Armed with the illicit rsETH, the attacker deposited the tokens as collateral on Aave, as well as on other lending protocols like Compound and Euler, across Ethereum L1 and Arbitrum deployments. Against this collateral, they borrowed an estimated 236 million dollars worth of WETH and wstETH, effectively extracting real value from the broader DeFi ecosystem in exchange for fraudulent collateral. When the exploit was discovered, the value of rsETH collapsed, leaving the borrowed positions severely undercollateralized and creating a shortfall in the lending pools.

In response, Aave’s multisig guardian and governance actors moved quickly to freeze markets related to rsETH, wrapped rsETH, and WETH across all deployments, while primary stablecoin markets reached 100 percent utilization, leaving no immediate liquidity for withdrawals. Estimates at the time suggested that Aave’s potential bad debt could reach around 123.7 million dollars under uniform socialization of losses, or as high as 230.1 million dollars if losses were isolated to L2 rsETH markets. The major parties involved—KelpDAO, LayerZero, and Aave—had not yet released a comprehensive recovery framework in the immediate aftermath, leaving users and governance to grapple with the distribution of losses and future listing policies.

Risk Controls: Freezes, Safety Module, and Emergency Governance

The rsETH incident showcased both the strengths and limits of Aave’s risk controls. On the positive side, the ability of the multisig guardian to rapidly freeze specific markets helped contain further damage, preventing additional borrowing against compromised collateral and stopping some avenues for contagion. This emergency power, while centralized relative to the ideal of pure on‑chain governance, functions as a pragmatic safeguard against slow governance cycles in crisis situations.

However, freezing markets comes with its own costs. When key assets like WETH are frozen, users who rely on Aave for leverage or liquidity can find themselves unable to adjust their positions, repay loans, or withdraw collateral. Combined with full utilization in stablecoin markets, these freezes can create a temporary liquidity crunch that feels akin to a “bank run,” even if the underlying protocol contracts remain solvent. Governance must weigh these trade‑offs: more aggressive use of freezes can limit exploit damage but also disrupt legitimate user activity and erode confidence.

The Safety Module provides an additional backstop by allowing AAVE stakers to absorb certain types of shortfalls through slashing. In theory, this mechanism can socialize losses across AAVE holders rather than concentrating them solely on affected liquidity providers or borrowers, promoting a form of mutualized insurance. In practice, whether and how to trigger slashing in events like the rsETH exploit is a contentious governance question, as it directly impacts token holders and may influence AAVE’s market price. These decisions intertwine technical risk assessment with political considerations, as different stakeholders lobby for their preferred allocation of losses.

Asset Listing Risk and the Limits of Governance Expertise

The rsETH incident underscores that Aave’s risk is not limited to its own smart contracts but extends to the broader ecosystem of assets it chooses to accept as collateral. Liquid restaking tokens (LRTs) like rsETH are complex derivatives that bundle staking rewards, restaking yield, and cross‑chain bridge assumptions into a single asset. Evaluating their risk profile requires deep understanding of validator sets, bridge designs, slashing conditions, and governance structures—far beyond the usual concerns about simple ERC‑20 tokens.

Chaos Labs’ departure from Aave governance, framed in part as a disagreement over risk management direction, can be read as a symptom of the difficulty in aligning community expectations with expert advice. When risk teams recommend conservative stances on emerging asset classes, they may be perceived as limiting growth and yield opportunities. Conversely, when the DAO lists such assets aggressively, it can expose the protocol to tail risks that are not fully appreciated by the broader community. The rsETH exploit, which created downstream bad debt in Aave despite no bug in Aave’s own contracts, is a tangible example of the latter scenario.

Going forward, Aave’s capacity to manage asset listing risk may hinge on its ability to integrate specialized, independent risk assessments into governance in a way that is both transparent and binding. This could involve stricter listing frameworks, tiered collateral tiers based on risk, or formalized veto powers for risk councils on particularly complex assets. Whatever form it takes, the goal would be to ensure that enthusiasm for new collateral types is balanced against a clear understanding of their composability and security assumptions.

User‑Facing Risks: Liquidations, Slippage, and Interface Errors

From an end‑user perspective, risk on Aave manifests in more familiar ways as well. Overcollateralized borrowing exposes users to liquidation risk: if the value of their collateral falls or they increase their borrowing, their health factor can slip below one, triggering liquidations that seize collateral at a discount. During volatile markets, this can happen quickly, especially for users employing high leverage or using correlated assets on both sides of the balance sheet. While liquidation bots help keep Aave solvent, they can also amplify stress for individual users who miscalculate their risk exposure.

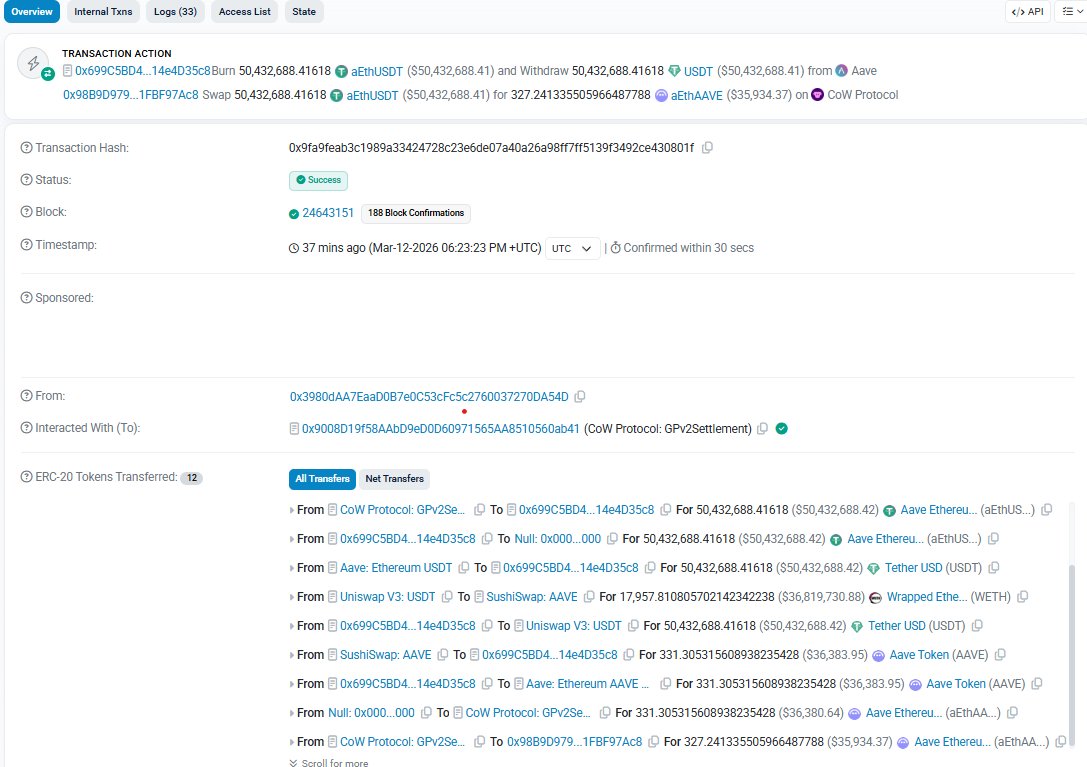

Market conditions can also impair user outcomes through slippage and liquidity shortages. The rsETH incident’s full utilization of stablecoin markets made it temporarily impossible for some users to withdraw stablecoins or adjust positions, even if their accounts were otherwise healthy. Additionally, large trades executed through DeFi interfaces can suffer severe slippage if routed through illiquid pools or misconfigured aggregators. A notable anecdote from recent coverage involved a user attempting to buy AAVE with 50 million USDT via the Aave interface but receiving only 324 AAVE due to extreme slippage, prompting Aave’s founder and engineers to investigate and commit to partial refunds and additional safeguards. Such incidents highlight the importance of robust front‑end design, user warnings, and default settings that protect against obviously adverse execution.

These user‑facing risks are not unique to Aave but are exacerbated by its scale and central role in DeFi. As more users and protocols rely on Aave as a foundational credit layer, the importance of intuitive interfaces, clear risk disclosures, and robust monitoring tools grows. Mitigating such risks may require not only technical upgrades but also educational efforts to ensure users understand concepts like utilization, liquidation thresholds, and slippage before engaging in high‑stakes transactions.

Systemic DeFi Risk and Aave’s Central Role

Because Aave commands a majority share of the DeFi lending market, its health has systemic implications for the broader ecosystem. Many protocols and traders treat Aave borrowing rates as reference benchmarks, use Aave deposits as yield‑bearing “cash,” or build structured products on top of Aave positions. When Aave experiences stress—through asset freezes, sharp rate spikes, or significant bad debt—the effects ripple outward through interconnected positions and strategies.

The rsETH exploit is one example of such systemic risk, with repercussions not only for Aave but also for protocols like Compound and Euler that accepted the compromised collateral. More generally, any major disruption to Aave’s operations—whether from a smart contract bug, an oracle failure, or extreme market dislocation—could trigger cascades of liquidations and deleveraging across DeFi. This interconnectedness is both a strength and a vulnerability: it testifies to Aave’s success as composable infrastructure but also makes it a critical point of failure.

Mitigating systemic risk involves not only internal controls but also broader ecosystem coordination. For instance, protocols that build on top of Aave may choose to implement their own circuit breakers or exposure limits, while oracle providers and monitoring tools collaborate to detect anomalies quickly. At the same time, regulators and policymakers watching DeFi may increasingly view Aave as a systemically important piece of crypto infrastructure, potentially shaping future regulatory responses to DeFi credit markets.

Market Position, Competition, and Macro Context

TVL Leadership and Competitive Landscape

Aave’s dominance in on‑chain lending is reflected in both absolute TVL and relative market share. By late 2025, the protocol reported approximately 55 billion dollars in deposits, up from lower levels at the start of the year and briefly reaching a peak of 75 billion dollars, the highest TVL ever recorded by a DeFi protocol at that time. External analyses estimated that Aave captured about 62 percent of the DeFi lending market, significantly outpacing competitors such as Compound and Maker in terms of lending volume.

While Compound remains a major lending protocol focused primarily on a subset of blue‑chip assets and emphasizes simplicity and conservative parameters, Maker occupies a somewhat different niche, acting as a credit platform centered on the DAI stablecoin and increasingly incorporating RWAs. Aave distinguishes itself by combining a broad multi‑asset lending market with a native stablecoin (GHO), multi‑chain deployments, and institutional products like Horizon. This multi‑pronged approach allows Aave to serve retail users, DeFi power users, and institutions under a single brand and governance system, albeit with varying degrees of permissioning and compliance.

In such a competitive environment, Aave’s strategic decisions around listings, chain expansion, and tokenomics are closely watched. For instance, the move to direct 100 percent of protocol revenue to AAVE holders under “Aave Will Win” not only differentiates AAVE’s value proposition from many competitors but also sets a precedent for more aggressive token‑centric models. How this affects user behavior, partner integrations, and regulatory perceptions over time will be a key determinant of Aave’s ability to sustain its leadership.

Macro Backdrop and DeFi Credit Cycles

Aave’s performance cannot be divorced from the broader macroeconomic and crypto market environment. In periods of loose monetary policy, rising crypto prices, and high risk appetite, demand for leverage increases, driving up borrowing volumes and interest spreads on protocols like Aave. Conversely, during macro uncertainty, regulatory crackdowns, or deep bear markets, users tend to deleverage, reducing protocol revenue and sometimes triggering waves of liquidations. Commentary from traditional financial media in 2026 pointed to a “mismatch” between fast‑moving speculative capital and slower‑moving institutional adoption, with macro uncertainty and a perceived lack of catalysts weighing on crypto markets.

For Aave, these cycles manifest in volatility in TVL, revenue, and token price. However, long‑term trends suggest that, despite cyclical drawdowns, Aave’s cumulative user base, number of integrations, and overall economic footprint continue to grow. This pattern mirrors that of many fintech platforms, which can experience significant revenue swings during economic cycles yet trend upward as they expand their user base and product suite.

Macro factors also influence Aave’s experimentation with RWAs and tokenized funds. In a high interest rate environment, tokenized money‑market strategies and basis trades like those employed by Bitwise’s USCC fund can generate attractive yields, making them compelling RWAs for Horizon markets. Conversely, shifts in yield curves, regulatory treatment of tokenized securities, or macro shocks affecting real‑world issuers can feed back into DeFi credit conditions. Aave’s success in navigating these interactions will depend on both its risk frameworks and the quality of its institutional partnerships.

Token Market Behavior: Whales, Funds, and Volatility

The AAVE token itself experiences significant volatility, influenced by both protocol fundamentals and broader market sentiment. Large holders, including crypto funds and whales, can materially move the market when they accumulate or sell significant quantities. Reports have highlighted, for example, that certain funds accumulated large AAVE positions at high prices in previous cycles and later faced substantial unrealized losses, eventually selling to cut exposure, contributing to downward pressure.[This comes from newsroom coverage rather than the provided web links.] Conversely, on‑chain data occasionally shows large wallets accumulating AAVE alongside other DeFi tokens during perceived periods of undervaluation, fueling narratives about “smart money” positioning for future cycles.

Episodes like the 50 million USDT swap mishap underscore liquidity and execution risks in token markets. While the root cause in that case appears to have been extreme slippage and routing issues rather than protocol malfunction, the result—a user receiving only a small amount of AAVE for a very large stablecoin outlay—highlighted the importance of liquidity depth and user protections in DeFi interfaces. Aave’s leadership publicly committed to engaging with the affected user and to exploring additional safeguards, illustrating how even non‑protocol‑level issues can become reputational moments for the project.

Looking ahead, token market behavior will likely continue to reflect both micro‑level protocol developments—such as progress on GHO, Horizon, and risk management—and macro‑level trends in DeFi and crypto adoption. Analytical narratives like Grayscale’s undervaluation thesis may play a growing role in shaping investor perception, particularly if Aave can sustain robust, transparent revenue streams that underpin equity‑like valuation models.

Regulatory Considerations and Policy Trajectory

As a leading DeFi lending protocol, Aave naturally sits within the sights of regulators and policymakers examining systemic risks and consumer protection in crypto markets. Its core markets are non‑custodial and permissionless, which can be both a shield and a point of concern: on the one hand, Aave does not directly custody user assets or run a traditional balance sheet; on the other, regulators may see large, globally accessible credit platforms without KYC as potential avenues for regulatory arbitrage.

Aave’s strategy appears to be one of functional separation. The core protocol remains open and non‑custodial, while products that explicitly target institutions and RWAs, such as Horizon, are built with compliance and permissioning in mind. Partnerships with regulated asset managers like Bitwise further signal a willingness to engage with existing financial frameworks rather than operate entirely outside them. How regulators respond—whether by creating DeFi‑specific categories, applying securities or banking regulations, or collaborating on standards for non‑custodial platforms—will influence Aave’s operating environment and may affect the viability of certain products or tokenomics models.

For now, Aave’s decentralized governance and open‑source nature complicate traditional regulatory approaches, as there is no single corporate entity controlling all aspects of the protocol. This decentralization, however, is not absolute; key contributors, multisig guardians, and foundation‑like entities play important roles in development and emergency response. The evolving regulatory discourse will likely probe these grey areas, testing where responsibility and accountability lie within token‑governed ecosystems.

The v3.1 upgrade introduced virtual accounting and stateful interest rate strategies specifically to harden against manipulation, but the protocol's surface area spans 15+ chains and dozens of asset markets, each with distinct adapter code.

Chaos Labs flagged that Ethena's USDe exposure on Aave reached $6.6B through Pendle looping strategies, warning that a funding rate reversal could trigger rapid correlated deleveraging across the protocol's largest market.

Aave's risk management has oscillated between a single dominant provider (Gauntlet, then Chaos Labs, then Llama Risk) — the departure of any one firm leaves the DAO temporarily without professional risk coverage on a protocol holding tens of billions in TVL.

- Regulatory riskMedium

The US Government withdrew $5.4M from Aave, signaling that state actors are active participants in DeFi liquidity pools and may increasingly scrutinize or interact with open lending protocols through legislative or enforcement channels.

Aave's near-departure from Polygon over a PoS Bridge Liquidity Program dispute demonstrated that protocol revenue sharing disagreements with L1/L2 partners can escalate to existential ecosystem splits, threatening TVL and integrations built on the assumption of permanence.

The CRV loan saga — where one founder's leveraged position in a volatile governance token nearly became a nine-figure bad debt event — illustrates that Aave's collateral risk is driven as much by individual whale behavior as by aggregate market conditions.

Using Aave and AAVE: Practical Considerations

Supplying, Borrowing, and Managing Risk

For individual users, interacting with Aave typically starts with supplying assets to earn yield. After connecting a compatible wallet, users can deposit assets like ETH or USDC into Aave markets, receiving aTokens that track their balance plus interest over time. These aTokens effectively represent claims on the underlying pool, allowing users to withdraw their funds and earned interest whenever sufficient liquidity exists. The simplicity of this mechanism makes Aave a common choice for users seeking passive yield on idle assets while retaining self‑custody.

Borrowing involves additional complexity and risk. Users must first supply collateral assets, which the protocol values using on‑chain oracles. They can then borrow other assets up to a limit determined by the collateral’s LTV and liquidation threshold. Prudent risk management requires maintaining a healthy buffer above the liquidation threshold, monitoring the health factor regularly, and understanding the volatility and correlation of both collateral and borrowed assets. Leveraged strategies—such as borrowing stablecoins against ETH to increase long exposure—can amplify returns but also magnify losses in downturns.

Users should also pay attention to interest rate dynamics. High utilization in a given market can cause borrow rates to spike, increasing the cost of maintaining positions. In extreme scenarios, such as during the rsETH crisis, 100 percent utilization can effectively lock markets, preventing new withdrawals or borrowings until conditions normalize. Understanding these mechanics, and using tools like alerts, dashboards, or conservative collateral ratios, is crucial for safe usage of Aave.

GHO vs. Third‑Party Stablecoins: Choosing a Borrowing Asset

Users deciding whether to borrow GHO or third‑party stablecoins like USDC face trade‑offs related to interest rates, liquidity, and integration. GHO, as a native Aave stablecoin, is minted directly against Aave collateral and contributes to protocol revenue, which in turn supports AAVE tokenomics. Borrowing GHO may come with governance‑tuned interest rate advantages in some configurations, reflecting the protocol’s desire to promote its native stablecoin.

Third‑party stablecoins, on the other hand, benefit from broader ecosystem integration. USDC, for example, is widely accepted across centralized exchanges, merchants, and other DeFi protocols, making it convenient for off‑ramping or cross‑protocol strategies. The relative attractiveness of GHO versus USDC borrowing will therefore depend on factors such as rate differentials, liquidity conditions, and user goals. Over time, as GHO’s supply and integrations grow, the gap in utility may narrow, but users will still need to consider the specific characteristics and risk profiles of each stablecoin.

For sophisticated users, the interplay between GHO and other stablecoins may itself present arbitrage or basis trade opportunities, such as borrowing GHO to provide liquidity in GHO‑USDC pools or to participate in governance‑sanctioned incentive programs. Such strategies, however, add layers of smart contract and market risk that must be weighed carefully.

Participating in Governance with AAVE

Holding AAVE allows users to participate in the governance of the protocol, either directly or via delegation. To vote on proposals, users typically need to hold AAVE in a wallet or stake it in governance‑enabled contracts, depending on the specific voting system. Governance participation involves monitoring the Aave forum, reading proposals, and weighing in on decisions that can affect everything from interest rate models and asset listings to treasury allocations and tokenomics changes.

For many individual holders, actively participating in governance may be impractical due to time and expertise constraints. Delegation offers an alternative, allowing AAVE holders to assign their voting power to delegates such as DAOs, specialized governance organizations, or trusted individuals with a track record of informed participation. This can enhance governance efficiency but may also concentrate power, making it important for the community to monitor delegates’ actions and to retain the ability to reassign delegation if needed.

Staking AAVE in the Safety Module can further align holders with the protocol’s health, as stakers earn rewards but also bear the risk of slashing in the event of shortfalls. Those considering staking should understand both the reward structure and potential downside, as well as the historical frequency and severity of slashing events.

Institutional Use and Horizon Participation

Institutions interested in using Aave face a distinct set of considerations. For some, direct participation in permissionless core markets may be unacceptable due to regulatory or internal compliance constraints. Aave Horizon addresses this by offering a permissioned environment where only approved participants can interact, and where collateral and borrowing assets may include regulated RWAs and tokenized funds.

Institutional users in Horizon can, for example, pledge tokenized shares of a carry fund like Bitwise’s USCC as collateral to borrow stablecoins. This enables on‑chain leverage and liquidity strategies linked to off‑chain trading programs, blending traditional and DeFi finance. Participation, however, requires onboarding processes, legal agreements, and risk assessments aligned with institutional frameworks.

For both retail and institutional users, staying informed about governance changes, new asset listings, and product launches is essential. Aave’s rapid iteration and expanding product suite mean that the risk and opportunity landscape is constantly evolving, and strategies that were optimal at one point in time may become less suitable as parameters and market conditions shift.

Aave in the Broader Crypto Asset Thesis

Cash‑Flow Tokens vs. Narrative‑Driven Assets

A growing theme in crypto research is the distinction between revenue‑generating “cash‑flow tokens” and purely narrative‑driven or meme‑based assets. AAVE falls firmly into the former category, especially as tokenomics evolve to direct protocol revenue toward token holders via staking, buybacks, or similar mechanisms. Analysts arguing that future crypto cycles will favor such assets see Aave as a leading example, given its substantial on‑chain revenue, clear economic function as a lending platform, and increasingly formalized value accrual mechanisms.

In this view, AAVE can be analyzed using frameworks adapted from traditional finance, such as price‑to‑earnings ratios, discounted cash flows, and comparisons to high‑growth fintech firms. While the uncertainties are still greater than in mature equity markets—owing to regulatory risk, technological evolution, and crypto’s inherent volatility—the presence of measurable, on‑chain revenue streams anchors valuation more firmly than in cases where token value rests largely on speculative belief.

That said, cash‑flow tokens are not immune to narrative. Market sentiment about DeFi’s future, competition, and regulatory outlook can significantly influence multiples applied to revenue or earnings metrics. For AAVE, narratives around security (especially after exploits involving integrated assets), governance competence, and institutional adoption via Horizon and GHO will likely shape how investors weigh its cash flows relative to perceived risks.

Comparing Aave to Traditional Banks and Fintechs

Grayscale’s framing of Aave as “a bank without bankers” invites a broader comparison to traditional financial institutions. Like a bank, Aave intermediates between depositors and borrowers, capturing a spread between lending and borrowing rates as protocol revenue. Unlike a bank, it does so through transparent smart contracts operating on public blockchains, without branches, employees managing credit approvals, or traditional regulatory capital requirements.

Aave’s net interest margins may be lower than those of major banks, reflecting competitive pressures and the absence of some ancillary revenue streams, but its cost structure is radically different. Once deployed, smart contracts can operate continuously with minimal marginal operating costs, though ongoing development, security, and governance still require significant investment. Additionally, Aave’s global reach allows anyone with an internet connection and compatible wallet to interact with its markets, sidestepping geographic and regulatory segmentation that traditional banks face.

From a risk perspective, Aave replaces credit risk (borrowers failing to repay unsecured loans) with collateral and market risk (collateral value volatility, oracle issues, and smart contract bugs). The Safety Module and overcollateralization aim to mitigate these risks, but tail events like the rsETH exploit illustrate that systemic shocks can still occur. Whether these trade‑offs ultimately make Aave more or less robust than traditional banks is an open question, but the comparison helps situate AAVE within a familiar conceptual framework for investors accustomed to evaluating financial intermediaries.

Scenarios for AAVE’s Long‑Term Trajectory

AAVE’s long‑term trajectory depends on multiple interacting vectors: protocol growth, product success, governance effectiveness, and the broader regulatory and macro landscape. In optimistic scenarios, Aave continues to dominate DeFi lending, successfully scales GHO into a major decentralized stablecoin, expands Horizon into a leading RWA credit platform, and navigates cross‑chain expansion without major security incidents. In such a world, AAVE could function as a central “equity‑like” instrument for a multi‑product, multi‑chain DeFi financial platform, with cash flows and tokenomics supporting substantial valuations.

More cautious scenarios involve heightened competition from other lending protocols or from centralized and quasi‑centralized platforms that offer comparable yields with stronger regulatory comfort. Regulatory crackdowns could restrict access to core markets in certain jurisdictions or impose constraints on tokenomics and revenue sharing. Persistent governance challenges, contributor churn, or major exploits involving listed assets could erode confidence, impacting both usage and token price.

Given these uncertainties, many analysts emphasize diversification and risk‑adjusted exposure to DeFi tokens like AAVE rather than all‑or‑nothing bets. For observers and participants alike, Aave serves as a key barometer for the health and maturation of DeFi credit markets, making its evolution an important storyline not just for AAVE holders but for the broader crypto ecosystem.

Outlook

Aave occupies a central, structurally important position in decentralized finance, combining a large‑scale lending protocol with a governance and value‑accrual token that increasingly resembles a cash‑flow bearing asset. Its expansion into native stablecoins via GHO, institutional RWA markets through Horizon, and cross‑chain deployments like AAVE on Solana reflects an ambition to become a comprehensive, multi‑product financial platform spanning diverse user segments and regulatory contexts.

At the same time, the protocol faces non‑trivial challenges. The rsETH exploit highlighted both the power and peril of composability, showing how vulnerabilities in external bridges and collateral tokens can create substantial bad debt in Aave despite no direct flaw in its core contracts. Governance tensions, contributor departures, and the delicate balance between token‑centric value accrual and conservative risk management will continue to test the resilience of Aave’s DAO over the coming years.

From a market perspective, research framing AAVE as undervalued relative to its projected cash flows and likening the protocol to a “bank without bankers” encapsulates a broader shift toward viewing DeFi tokens as analyzable financial assets rather than purely speculative instruments. Whether this thesis proves accurate will depend on Aave’s ability to sustain and grow its revenue streams, manage risk prudently, and adapt to evolving regulatory and competitive landscapes. Regardless of short‑term volatility, Aave’s trajectory will remain a bellwether for the viability of decentralized, token‑governed credit markets as a durable component of the global financial system.

Latest AAVE news

Sources

- https://aave.com

- https://aave.com/docs/ecosystem/aave

- https://thedefiant.io/news/defi/aave-gho-stablecoin-market-cap-breaks-usd500-million

- https://governance.aave.com

- https://x.com/StaniKulechov/status/2043382887764930635

- https://x.com/CoinDesk/status/2067764548451320132

- https://x.com/StaniKulechov/status/2061794946219151447

- https://startupfortune.com/aave-lands-on-solana-as-the-solana-foundation-bets-on-a-defi-united-strategy/

- https://www.galaxy.com/insights/research/kelpdao-layerzero-exploit-defi

- https://governance.aave.com/t/chaos-labs-is-leaving-aave/24386

- https://aave.com/blog/aave-2025-recap

- https://bitwiseinvestments.com/newsroom/bitwise-announces-inaugural-tokenized-fund

- https://aave.com/blog/horizon-launch

- https://governance.aave.com/t/aave-dao-funding-insights/24192

- https://www.youtube.com/watch?v=5FUftOaKSwE

- https://governance.aave.com/t/bgd-aave-safety-module-v1-5/12148

- https://web3.gate.com/en/crypto-wiki/article/how-does-aave-compare-to-compound-and-maker-in-defi-lending-market-share-and-tvl-in-2025-20251227

- https://x.com/WuBlockchain/status/2047481530143182870

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…