Deep explainer on Aave’s GHO stablecoin: how it works, its Aave-native design, governance and risk, cross-chain growth, CeFi ramps, Curve and Horizon integrations, and how it compares to USDC and other CDP stablecoins.

+7 sources across the wider coverage universe

Standard Chartered sees Aave outperforming Bitcoin and Ethereum through 2030, citing V4 upgrades, GHO growth, token buybacks and a 37x expansion in DeFi assets2026-06

Standard Chartered sees Aave outperforming Bitcoin and Ethereum through 2030, citing V4 upgrades, GHO growth, token buybacks and a 37x expansion in DeFi assets2026-06 Stani Kulechov outlines Aave’s 12-month strategy focused on diversifying revenue streams, scaling GHO adoption and growing the Aave app ecosystem2026-05

Stani Kulechov outlines Aave’s 12-month strategy focused on diversifying revenue streams, scaling GHO adoption and growing the Aave app ecosystem2026-05 ⚠️ Fluid rewards exploit: attacker abused “empty-proof” Merkle claims after a key compromise to drain 125k FLUID and 51.9k GHO, swap and launder via Tornado Cash, while Fluid quietly paused claims without disclosing the loss.2026-05

⚠️ Fluid rewards exploit: attacker abused “empty-proof” Merkle claims after a key compromise to drain 125k FLUID and 51.9k GHO, swap and launder via Tornado Cash, while Fluid quietly paused claims without disclosing the loss.2026-05 Yield has suffered a major financial hit totaling $3.73 million. The loss occurred during a Vault operation which involves a token swap from stkGHO to USDC. Due to extreme slippage, 3.84M GHO was exchanged for a mere 112K USDC.2026-01

Yield has suffered a major financial hit totaling $3.73 million. The loss occurred during a Vault operation which involves a token swap from stkGHO to USDC. Due to extreme slippage, 3.84M GHO was exchanged for a mere 112K USDC.2026-01 Deep dive by intern_cc auditing the financial health of Aave2025-12

Deep dive by intern_cc auditing the financial health of Aave2025-12 LlamaRisk Insights: GHO’s backing and RWA integration, a portfolio analysis.2025-12

LlamaRisk Insights: GHO’s backing and RWA integration, a portfolio analysis.2025-12

GHO Stablecoin: An Evergreen Guide to Aave’s Native Dollar-Pegged Asset

GHO is Aave’s native, decentralized, overcollateralized stablecoin: an ERC‑20 token designed to track the U.S. dollar while being minted directly against crypto collateral deposited in Aave’s lending markets, with interest flowing back to the Aave DAO rather than to a centralized issuer.

Background: Aave, Stablecoins and the Emergence of GHO

To understand why GHO exists, it helps to place it in the wider evolution of stablecoins and of Aave itself. Aave began as one of Ethereum’s earliest money markets, allowing users to supply assets to earn yield and borrow against them in a non-custodial way. Over time, Aave grew into a systemically important DeFi protocol, with its own governance token AAVE and an on-chain Safety Module that lets token holders backstop the system in exchange for yield. This scale created a natural demand for a stable, protocol-native unit of account and collateral, leading to the concept of GHO as a stablecoin tightly integrated with Aave’s risk, governance and revenue architecture.

Stablecoins themselves emerged as a response to volatility in crypto markets, giving traders and protocols a dollar-like asset without repeatedly moving funds through the banking system. Fiat-backed stablecoins such as USDC and USDT rely on off-chain reserves held by centralized entities, who manage bank accounts and short-term securities portfolios to maintain a one-to-one backing for their tokens. Crypto-collateralized stablecoins like MakerDAO’s DAI instead use on-chain vaults, where users deposit volatile crypto collateral to mint stablecoins under overcollateralization constraints. GHO belongs to this latter “CDP-style” category, alongside DAI and Sky’s USDS, but is architected specifically around Aave’s lending markets and governance process.

Aave governance first floated the idea of GHO as a way to capture more of the value created inside the protocol. In traditional Aave markets, interest paid by borrowers is largely passed through to depositors of the borrowed asset. With GHO, the system can mint a new stablecoin against existing collateral and charge an interest rate that accrues to the Aave DAO treasury, allowing the DAO to fund development, risk management and incentives without depending solely on AAVE emissions or protocol fee skim. At the same time, Aave users get a dollar-pegged asset that is deeply integrated into the protocol’s risk engine, collateral framework and Safety Module.

When GHO launched on Ethereum mainnet in 2023, it was positioned not as yet another generic dollar token but as a strategic pillar of Aave’s long-term roadmap. The initial design featured a fixed borrow rate of 1.5% for GHO, with a discounted rate for AAVE stakers, and a debt ceiling of 100 million GHO to limit early-stage risk. Over the subsequent years, Aave’s founder Stani Kulechov and the broader DAO have repeatedly emphasized GHO as a core focus of their forward-looking strategy, with a 12‑month roadmap centered on scaling GHO adoption, diversifying protocol revenue streams and expanding the Aave app ecosystem around the stablecoin. That strategic emphasis has coincided with steady growth in supply, cross-chain expansion and integrations across major DeFi primitives.

As of early 2025, GHO’s circulating supply had already climbed past 500 million, according to market data cited by The Defiant, representing more than 245% growth since the start of that year. By mid‑2026, analytics from DeFiLlama and ecosystem documentation place GHO’s supply in the mid hundreds of millions, making it one of the larger crypto-collateralized stablecoins by market share. This growth has not been purely organic; it has been deliberately cultivated by the Aave DAO through governance decisions on interest rates, collateral listings, staking yields, and targeted incentives in both Aave’s own markets and external liquidity pools. The result is a stablecoin that is now increasingly central to Aave’s identity and balance sheet.

Standard Chartered sees Aave outperforming Bitcoin and Ethereum through 2030, citing V4 upgrades, GHO growth, token buybacks and a 37x expansion in DeFi assets

DefiLlama has Aave around $12.5B TVL, $10.1B borrowed and ~$597M GHO outstanding, so the 2030 case is mostly a bet that lending revenue starts compounding through a native stablecoin plus buybacks instead of leaking to LPs. V4’s hub-and-spoke model matters because post-rsETH/Kelp, growth into LRTs, Ethena-style collateral, XAUt and RWAs only works if credit lines and silos keep bad collateral from becoming protocol-wide bad debt. If GHO becomes the balance-sheet asset while AAVE becomes the claim on treasury-driven buybacks, the comp is closer to onchain bank equity with liquidation/oracle risk priced in.

Readers clicked GHO not as a stablecoin product story but as a governance-accountability story: the clicks cluster around who was appointed to fix the peg, whether that appointment was legitimate, and whether DAO committees can actually rescue a broken mechanism — revealing that DeFi stablecoin credibility is now a political problem as much as a technical one.↗

Design and Mechanics: How GHO Works Under the Hood

Borrow–mint model and overcollateralization

GHO’s core issuance mechanism is often described as “borrow–mint” rather than the more traditional “borrow against deposits” model that underpins Aave’s other markets. In practice, Aave v3 and v4 users deposit collateral such as ETH, wrapped staked ETH (wstETH), WBTC, USDC or other approved assets into Aave’s lending pools, just as they would to borrow any other token. Instead of borrowing a pre-existing pool of stablecoins supplied by other users, however, GHO borrowers trigger the protocol itself to mint new GHO tokens directly to their address, up to limits set by governance. The resulting GHO debt is accounted for within the Aave market, secured by the user’s collateral, and subject to interest and liquidation rules similar to other borrow positions.

This model makes GHO an overcollateralized stablecoin by design. Users cannot mint more GHO than allowed by their risk-adjusted collateral value; the system enforces collateralization ratios such that the value of assets posted always exceeds the value of GHO borrowed, with a buffer to cover price volatility. If the value of a borrower’s collateral falls below liquidation thresholds, Aave’s usual liquidation mechanisms kick in: liquidators can repay the debtor’s GHO and seize collateral at a discount. This process both protects the protocol from bad debt and provides a market-driven lever that helps keep GHO backed by high-quality assets on-chain.

A key structural distinction from many legacy Aave markets is that there is no “supplier side” for GHO in the underlying borrow–mint mechanism. No one deposits GHO to fund the loans that mint GHO; instead, every unit of GHO originates as a liability of someone’s overcollateralized borrow position, or via other governed facilitators discussed below. That makes the economics relatively clean: the interest rate on GHO borrowing is not shared with GHO depositors but is a pure revenue stream flowing to the Aave DAO treasury. This contrasts with assets like USDC, where depositors on Aave expect a share of the interest paid by USDC borrowers, and the protocol captures only a portion in fees.

Once a borrower repays their GHO debt plus accrued interest, the protocol burns the returned GHO, shrinking the total supply. This mint-and-burn dynamic means that GHO’s circulating supply is elastic, expanding when users demand leveraged liquidity or stablecoin exposure and contracting as they deleverage. In this respect, GHO behaves similarly to other CDP stablecoins such as DAI and USDS, where user behavior and interest rate policy jointly determine the size of the supply, rather than a centralized issuer’s treasury operations.

Facilitators, mint caps and governance controls

The issuance of GHO is mediated through a “facilitator” framework that gives Aave governance fine-grained control over who can mint and burn GHO and under what conditions. A facilitator is any smart contract that has been approved by the Aave DAO to create and destroy GHO, subject to a governance-defined minting capacity known as a mint cap. The Aave v3 Ethereum GHO borrow–mint market is one such facilitator. In principle, additional facilitators can include isolated vaults, cross-chain bridges, stability modules, or external protocols that integrate GHO as a native asset.

Each facilitator’s mint cap acts as a circuit breaker on systemic risk. If, for example, the Aave v3 facilitator is given a 500 million GHO cap, no more than that amount can be minted through that route, regardless of user demand. Governance can choose to raise or lower caps over time in response to risk assessments, market conditions and strategic goals. This modularity allows the DAO to diversify GHO’s issuance sources while maintaining an overall risk framework that is comparable to a bank’s credit limits across product lines and regions.

In practice, the Aave DAO, composed of AAVE token holders and delegates, sets critical parameters for GHO’s operation. These include the borrow rate for GHO in core markets, facilitator mint caps, collateral eligibility and risk parameters, as well as decisions about cross-chain deployments and stability mechanisms. The initial mainnet deployment, for example, offered a fixed 1.5% borrow rate on GHO with a 30% discount for staked AAVE holders, alongside a 100 million cap to limit early expansion. Subsequent governance proposals have iteratively tuned rates, caps and discount structures as GHO supply and demand evolved.

The facilitator model is evident in newer initiatives as well. Governance discussions and proposals have explored additional facilitators such as Horizon markets, specialized GHO stability modules, and cross-chain bridges using Chainlink’s CCIP on Base and planned deployments on Arbitrum. In each case, the DAO evaluates risk reports from independent risk managers like LlamaRisk and Chaos Labs before allocating a mint cap to the new facilitator, creating a layered defense against uncontrolled expansion.

Peg dynamics and stability mechanisms

Like any stablecoin, GHO aims to trade close to one U.S. dollar on secondary markets, but it does not guarantee a hard redemption right for $1 of off-chain assets. Instead, its peg is maintained through a combination of overcollateralization, interest rate policy, arbitrage incentives and, increasingly, specialized stability mechanisms. Because GHO is minted and burned via borrow positions on Aave, its effective “real-world” redemption route is to buy GHO on the open market, repay a loan, and unlock the underlying collateral. If GHO trades below $1, underleveraged borrowers can profitably buy it at a discount, repay debt, and withdraw more valuable collateral, which creates buying pressure that pushes the price back up. If it trades above $1, users can mint new GHO at par by borrowing against collateral and sell it on the market, increasing supply and pushing the price down.

Governance can influence these dynamics by adjusting the borrow rate. A lower rate makes it cheaper to mint GHO, encouraging supply growth that can compress a persistent premium; a higher rate reduces the incentive to mint and creates demand to repay leverage, which can help lift a persistent discount. This interest-rate “monetary policy” is conceptually similar to MakerDAO’s stability fees for DAI, or to the policy levers used by Sky to manage USDS. Because GHO’s interest revenue accrues to the Aave DAO, changes in the borrow rate affect both peg stability and protocol income, forcing governance to weigh risk, growth and revenue in tandem.

Beyond these core mechanics, Aave governance has been building and iterating on more explicit stability modules and liquidity backstops. One major line of development is the GHO Stability Module (GSM), which is intended to function somewhat analogously to MakerDAO’s Peg Stability Module for DAI. A recent temperature-check proposal outlined upgrades to the GSM to manage the stablecoin system more efficiently by integrating BUIDL, BlackRock’s tokenized fund representing traditional assets like cash and U.S. Treasury bills, into GHO’s liquidity and backing structure. This would give GHO indirect exposure to real-world assets (RWAs) and diversify its balance sheet beyond on-chain crypto collateral, at the cost of introducing external custodial and regulatory dependencies.

GHO has also become part of Curve Finance’s broader peg-keeping ecosystem. Curve’s Peg Stability Reserves (PSRs) are autonomous smart contracts designed to buy or sell stablecoins in targeted liquidity pools to keep their price close to $1. Each PSR monitors the price in a specific Curve pool and can deploy capital to counter deviations. Recent integrations have seen GHO included in baskets such as crvUSD’s PegKeeper system after a LlamaRisk review cleared peg stability risks, effectively enlisting Curve’s algorithmic liquidity tools as an additional line of defense for GHO’s dollar peg. While these mechanisms reside outside the Aave protocol, they interact with GHO’s core economics by influencing secondary market liquidity and arbitrage efficiency.

Yield, stkGHO and the Aave Safety Module

Unlike fiat-backed stablecoins whose issuers earn yield on off-chain reserves, GHO itself does not pay a passive yield to holders at the protocol level. The core borrow–mint mechanism has no supplier side, so simply holding GHO in a wallet does not entitle the holder to any share of interest paid by borrowers. Instead, GHO holders seeking yield can opt into additional risk-bearing roles, primarily by staking GHO into the Aave Safety Module or deploying it in external liquidity and structured-yield protocols.

The Aave Safety Module is the protocol’s backstop reserve, funded by users who stake assets such as AAVE, ABPT (Aave–Balancer Pool Tokens) and, more recently, GHO itself via the stkGHO token. When a user stakes GHO, they receive stkGHO at the current exchange rate, representing a claim on their staked position plus any accrued rewards. In exchange, they take on the role of last-resort liquidity in the event of a shortfall event in the Aave protocol, such as a major insolvency or exploit. In such cases, staked assets in the Safety Module can be partially “slashed” to cover losses, making this yield path explicitly risk-bearing.

Rewards for stkGHO are funded through the Aave DAO’s ecosystem reserve and potentially through direct distributions of GHO and AAVE, with the rate set by governance. As of mid‑2026, published stkGHO yields are described as competitive relative to supply rates for USDC and USDT on comparable chains, though exact figures vary over time. A Defiant report from early 2025 highlighted that Aave incentivizes GHO use by offering a higher yield on interest-bearing sGHO than for most other stablecoins on its platform, citing an APY of around 5.52% for GHO deposits versus 3.7% for USDC and 2.65% for USDT at that time, though these numbers are historically contingent. Together, these incentives have contributed to rapid growth in staked GHO; internal analytics and community reporting have noted that stkGHO supply has increased by well over 200% year-on-year, a trend framed as a vote of confidence in Aave’s stablecoin strategy.

Outside the Safety Module, GHO can be deployed in various DeFi strategies. Liquidity providers can supply GHO to stablecoin pools on platforms like Curve and Balancer, often paired with USDC or USDT, earning swap fees and incentives while bearing impermanent loss and smart contract risk. On yield tokenization protocols such as Pendle, users can trade or speculate on tokenized future GHO yields. However, it remains important to emphasize that none of these returns are “risk free”: they depend on counterparty contracts, oracle integrity, and the health of both Aave and the broader DeFi ecosystem.

GHO in the Stablecoin Landscape

Comparing GHO with USDC and centralized stablecoins

GHO’s design places it in clear contrast with centralized, fiat-backed stablecoins such as USDC. USDC is issued by Circle and backed by reserves of cash and short-term U.S. Treasuries held in regulated financial institutions, with monthly attestations and, more recently, increasing regulatory scrutiny. By contrast, GHO is fully backed by on-chain collateral and supported by the overcollateralization model of the Aave Protocol, rather than a centralized reserve account. This difference affects everything from risk profile and transparency to revenue flows and regulatory classification.

On the transparency front, GHO’s backing is visible on-chain: observers can inspect Aave markets, collateral compositions, and GHO debt positions in real time, supplemented by external dashboards like Chaos Labs’ GHO Risk Monitoring Dashboard and LlamaRisk’s portfolio analyses. USDC’s backing is off-chain, making it reliant on third-party attestations and audits. At the same time, fiat-backed stablecoins typically maintain a tighter soft peg to $1 through direct redemption for dollars, whereas GHO’s peg relies on market incentives, interest rate policy and secondary liquidity structures.

The revenue model is also markedly different. For USDC, yield from reserves accrues primarily to the issuer and its shareholders. For GHO, interest paid by GHO minters goes directly to the Aave DAO treasury, supporting protocol sustainability and governance. This aligns stablecoin growth with the economic health of the protocol and potentially with AAVE tokenholders, especially as the DAO explores tokenomics revamps that could redistribute a portion of GHO revenue to stakers and other stakeholders. However, it also means that GHO users implicitly subsidize protocol operations through the borrow rate, rather than paying an explicit spread embedded in off-chain reserve yields.

From a user’s perspective, the practical experience of holding GHO versus USDC may be similar: both behave as ERC‑20 tokens transferable across wallets and DeFi protocols on Ethereum and, increasingly, on layer‑2 networks. Yet the underlying risk exposures differ. GHO holders bear exposure to Aave’s smart contracts, oracle integrity, collateral markets (including large positions in assets like ETH, LSTs and potentially RWAs) and governance decisions. USDC holders bear exposure to Circle’s solvency, banking partners, regulatory environment and the quality of off-chain reserve management. These trade-offs matter for institutions and sophisticated DeFi users who consciously diversify their stablecoin holdings based on risk appetite and use case.

A simplified comparison can be summarized as follows:

| Feature | GHO | USDC |

|---|---|---|

| Issuer / Controller | Aave DAO via on-chain governance | Circle and partners (centralized company) |

| Backing | Overcollateralized crypto and RWA exposure on-chain, via Aave positions and facilitators | Off-chain cash and U.S. Treasuries managed by issuer |

| Mint / Burn Mechanism | Minted against Aave collateral by facilitators; burned on loan repayment | Minted and redeemed by authorized partners for fiat |

| Interest / Revenue | Borrow interest flows to Aave DAO treasury | Reserve yield accrues to issuer |

| Transparency | On-chain positions plus third-party dashboards | Off-chain attestations and regulatory filings |

| Redemption for USD | Indirect via repaying loans and unlocking collateral | Direct via issuer and partners |

| Regulatory Classification | Decentralized CDP stablecoin; not a “payment stablecoin” under GENIUS Act analysis | Regulated fiat-backed e‑money–like asset, MiCAR and U.S. regimes evolving |

This table simplifies a complex reality, but it highlights that GHO is not a fiat-substitute in the same way as USDC; it is a DeFi-native building block whose stability is anchored in the robustness of Aave and its governance, not in direct bank account claims.

GHO among CDP stablecoins: DAI, USDS and crvUSD

Within the cohort of crypto-collateralized stablecoins, GHO is often mentioned alongside MakerDAO’s DAI and Sky’s USDS. Like DAI, GHO is typically minted against overcollateralized positions secured by a mix of assets, and its supply expands and contracts based on user borrowing behavior and protocol-set interest rates. However, GHO’s architecture is more tightly coupled to a single lending protocol—Aave—whereas DAI is minted in dedicated Maker vaults that sit somewhat more independently from other money markets. Sky’s USDS similarly uses an overcollateralized CDP design with its own peg stability tools, including a dedicated stability module, making it conceptually close to GHO’s evolving GSM.

Curve’s crvUSD adds another reference point. crvUSD is backed by crypto collateral but uses a unique “LLAMMA” liquidation mechanism and a suite of Peg Stability Reserves (PSRs) that automatically trade stablecoins in Curve pools to keep them near $1. GHO’s integration into crvUSD’s PegKeeper basket effectively makes it part of this ecosystem of peg stabilization tools. Although GHO does not itself use LLAMMA-style liquidations, the combination of Aave’s robust risk engine and external peg-keeping via Curve’s PSRs moves it closer to a hybrid model where both lending-market dynamics and specialized liquidity contracts contribute to stability.

What differentiates GHO within this group is its explicit alignment with a single protocol’s long-term economics and strategy. MakerDAO and Sky focus on building resilient balance sheets that can weather market stress and regulatory changes, increasingly leaning into RWAs like U.S. Treasuries. Aave, by contrast, is leveraging GHO to turn its lending protocol into a quasi–on-chain bank whose core liabilities are its own stablecoins, whose revenues are GHO interest, and whose capital structure is mediated by AAVE and the Safety Module. This tight integration explains why Aave’s internal risk teams and external partners like LlamaRisk invest so heavily in analyzing GHO’s backing, RWA integration and regulatory positioning.

LlamaRisk, Chaos Labs and risk governance

Risk management has become a distinguishing feature of GHO’s evolution, with Aave leaning on specialized firms to provide independent analysis and monitoring. LlamaRisk brands itself as a “guardian of DeFi,” offering analytics, risk research and security tooling for protocols. In the context of GHO, LlamaRisk has produced deep dives on the stablecoin’s backing and RWA integration, including a portfolio analysis assessing the impact of integrating USCC, a crypto carry fund utilizing CME futures and U.S. Treasuries, into GHO’s effective balance sheet. This work helps the Aave DAO understand how exposure to basis trades and Treasury yields can affect GHO’s risk-return profile under different market regimes.

LlamaRisk has also examined GHO’s status under the U.S. GENIUS Act, concluding in a preliminary memorandum that GHO does not qualify as a “payment stablecoin” under the act’s statutory definition, provided it maintains its current architecture. This finding has implications for the regulatory obligations GHO might face in the United States and underscores the importance of design choices such as overcollateralization and decentralized governance in shaping legal outcomes. Beyond formal reports, LlamaRisk has engaged the community through media appearances, interactive broadcasts and monthly recaps, sharing findings about GHO user profiles, cross-chain integration prospects and concentration risks in Aave’s collateral base.

Chaos Labs, meanwhile, has focused on quantitative modeling and real-time monitoring. Ahead of GHO’s launch, Chaos Labs introduced a GHO Risk Monitoring Dashboard designed to track key metrics such as collateral composition, concentration, liquidation risk and peg deviations. This tooling gives Aave governance and the broader community visibility into how GHO behaves in the wild and provides early warning indicators that can inform parameter changes or emergency responses. The combination of these external perspectives with Aave’s internal risk teams creates a layered governance process that is relatively sophisticated by DeFi standards.

- 01GHO peg failure and repeg campaign↗

A blue-chip protocol's stablecoin depegging immediately after launch and staying below $1 for six months created sustained reader urgency around whether the fixed-rate minting model was structurally broken.

- 02Tokenomics revamp and Anti-GHO token↗

The top-clicked headline — Aave's proposal for revenue redistribution, an 'Umbrella' safety module, and a non-transferable Anti-GHO debt-offset token — signaled a root-level rethinking of how GHO risk and protocol revenue are shared with AAVE stakers.

- 03GHO Liquidity Committee and TokenBrice mandate

Appointing a named individual as 'benevolent temporary dictator' to lead repeg efforts — followed by his public farewell post critiquing 'DeFi newspeak' — turned a routine governance mechanism into a pointed debate about whether committee-style DAO governance is compatible with stablecoin credibility.

- 04Cross-chain expansion via Chainlink CCIP↗

Aave's choice of Chainlink CCIP for GHO's Arbitrum launch — rather than a native bridge — drew readers tracking how canonical cross-chain stablecoin infrastructure is being decided at the protocol layer.

- 05LLAMMA soft-liquidation IP dispute with Curve

Curve publicly accusing Aave of appropriating its soft-liquidation mechanism for Aave v4's GHO integration elevated a technical design choice into a high-profile inter-protocol IP confrontation.

- 06RWA collateral and BlackRock BUIDL integration↗

The proposal to back GHO's Stability Module with BlackRock's tokenized BUIDL fund attracted readers tracking TradFi-DeFi convergence in stablecoin collateral design.

Adoption, Integrations and Market Structure

Market cap growth and DeFi usage

Since its launch, GHO has progressed from a cautious pilot to a significant player in the on-chain stablecoin market. The Defiant reported that GHO’s market capitalization broke the $500 million mark, with supply staying above half a billion and growing over 245% since the start of 2025. More recent ecosystem analyses from Aave-aligned documentation point to total supply in the mid hundreds of millions by Q2 2026, positioning GHO among the leading CDP-style stablecoins by size. This growth trajectory reflects both organic adoption by sophisticated DeFi users and targeted incentives deployed by Aave governance.

Within Aave markets, GHO serves as a borrowable stablecoin that allows users to access dollar-pegged liquidity while retaining exposure to yield-bearing collateral such as wstETH or tokenized T-bills. Because users continue to earn interest or staking rewards on their posted collateral, GHO borrowing can be used to build leveraged strategies, either by looping into more collateral, providing liquidity elsewhere, or diversifying portfolios. At launch, Aave v3 users on Ethereum could mint GHO against all collateral assets supplied to the protocol, subject to risk parameters, creating a broad base of potential borrowers. Over time, additional Aave markets and facilitators have been configured to support GHO issuance on other networks and within specialized products.

The Aave DAO has also engineered demand for GHO by making it attractive to hold and deploy inside the protocol. As noted earlier, a Defiant analysis highlighted that GHO depositors could earn a higher APY than USDC or USDT depositors on Aave at certain points in time, a deliberate choice by governance to bootstrap usage. Incentive programs have steered liquidity into GHO-containing pools on external platforms, and facilitator deposits, such as an additional 1 million GHO moved into Horizon-associated markets, have been used to seed new venues. These efforts, alongside the rise of stkGHO and integration into protocols like Curve, Balancer and Pendle, have made GHO an increasingly familiar component of DeFi portfolios and strategies.

Interestingly, risk analyses by LlamaRisk suggest that GHO’s user base skews toward wealthier, sophisticated DeFi participants. While exact user-level data is not public, this qualitative assessment aligns with the idea that GHO’s early adopters are power users comfortable with Aave’s risk model, willing to manage collateralized debt positions, and interested in yield-bearing stablecoin strategies. As GHO becomes more accessible through centralized exchanges and regulated on/off ramps, this demographic may diversify, but understanding who holds and uses GHO remains a key input to systemic risk assessments.

Centralized exchange listings and compliant on/off ramps

For a stablecoin to achieve broad adoption, it typically needs both deep on-chain liquidity and easy access points from traditional finance. GHO has taken steps on both fronts. One milestone was its first centralized exchange listing on Bitget, which announced support for GHO in its Innovation Zone. Bitget’s listing materials emphasized GHO’s decentralized, overcollateralized design and native integration with Aave, giving traders an opportunity to buy, sell and hold GHO alongside more established stablecoins. Centralized listings can help tighten the peg by facilitating arbitrage between exchange prices and on-chain markets, as well as introducing new user cohorts to the token.

A more structurally significant development has been Aave’s push into regulated fiat on-ramps and off-ramps, particularly in Europe. Aave Labs announced the launch of zero-fee on-ramping and off-ramping for GHO and other stablecoins across its products in Europe, leveraging regulatory approvals under the EU’s Markets in Crypto-Assets Regulation (MiCAR) framework. This initiative allows users to convert euros into GHO and back without explicit fees at the protocol’s front-end layer, effectively offering a compliant, low-friction gateway between bank accounts and DeFi positions. While the underlying payment infrastructure and partner relationships are complex, the net effect is to position GHO not just as a DeFi-native asset but as a bridge between traditional and decentralized finance.

These on/off-ramp initiatives also play into Aave’s broader strategic narrative. With global stablecoin demand surpassing hundreds of billions of dollars, protocols that can offer regulated, user-friendly access to stablecoins stand to capture significant order flow. By bundling Aave’s lending products, GHO’s borrow–mint mechanics, and fiat rails under a MiCAR-compliant umbrella, Aave Labs aims to make GHO a default choice for users entering DeFi via the Aave app, especially in jurisdictions where regulatory clarity is greatest. At the same time, this path introduces its own regulatory and operational challenges, from AML/KYC obligations to fraud prevention and custody risk.

Cross-chain expansion: Base, Arbitrum and L2 ecosystems

GHO started life on Ethereum mainnet, but Aave’s roadmap has always envisioned a multi-chain existence for the stablecoin. A major step in this direction was GHO’s launch on Base, Coinbase’s Ethereum layer‑2 network, with Chainlink’s Cross-Chain Interoperability Protocol (CCIP) serving as the underlying bridge infrastructure. According to Chainlink’s coverage, Aave launched its GHO stablecoin on Base following a successful community vote, leveraging CCIP to manage secure cross-chain messaging and token transfers. GHO quickly reached a market cap of $2.5 million within two days of launch on Base and grew to over 191 million in circulation overall at the time of that report, indicating substantial existing demand for the asset.

The use of CCIP reflects a broader shift toward more secure, programmable cross-chain bridges, as the industry seeks to mitigate the risk of bridge exploits that have plagued earlier designs. Under such frameworks, GHO minted on Ethereum can be locked or burned while corresponding representations are minted on Base, with CCIP ensuring consistent accounting and enabling cross-chain liquidity strategies. For users, this means that GHO can serve as a native-feeling stablecoin on Base, supporting lending, trading and yield strategies in that L2 ecosystem while ultimately being rooted in Aave’s Ethereum-based governance and collateral.

Aave governance has also prepared for cross-chain expansion to other L2s such as Arbitrum. An Aave governance forum post describes a cross-chain launch of GHO on Arbitrum, supported by an allocation of 750,000 ARB tokens from the Arbitrum DAO’s Long-Term Incentives Pilot program. These ARB incentives are intended to bootstrap GHO liquidity and usage on Arbitrum, where Aave’s lending markets already operate. The combination of GHO, Aave, and ecosystem-native incentives creates a feedback loop whereby GHO becomes a common unit of account and collateral across multiple rollups, deepening its strategic importance for Aave and DeFi more broadly.

Meanwhile, governance discussions including a “GHO Gas Token Framework” temp check by the Michigan Blockchain group have argued in favor of allowing users to pay gas fees on certain L2 networks using GHO instead of the native network token. Such proposals would turn GHO into not just a store of value and medium of exchange within DeFi, but also a direct utility token for transaction fees in rollup ecosystems. While these ideas remain at the proposal and experimentation stage, they underscore how cross-chain expansion is not just about extending GHO’s footprint but about embedding it deeply into the operational fabric of L2s.

Curve, Horizon and other DeFi integrations

Beyond Aave’s core markets, GHO has been integrated into several cornerstone DeFi protocols, shaping its liquidity profile and risk surface. On Curve, GHO participates in stablecoin pools that pair it with assets like USDC or USDT, enabling low-slippage swaps and forming the basis for peg protection via Curve’s Peg Stability Reserves and crvUSD PegKeeper system. Following a review by LlamaRisk that cleared peg stability risks, GHO was added to a PegKeeper basket with a $3 million debt ceiling, providing automated support for its dollar peg via smart-contract-driven rebalancing. This arrangement complements Aave’s own stability tools and broadens the set of arbitrageurs and liquidity providers who have a direct financial interest in maintaining GHO’s stability.

Aave’s Horizon product, which packages lending markets and incentives into a more curated experience, has also become a venue where GHO plays a role. Governance highlights describe Horizon TVL surging past $300 million, dominated by RLUSD markets while GHO expands rapidly and incentive programs for USDC borrow and RLUSD supply are renewed. Among these updates, the GHO facilitator deposited an additional 1 million GHO, which both seeds liquidity and signals confidence from Aave’s governance in the stablecoin’s use within Horizon. Although RLUSD—another RWA-backed stablecoin—currently leads in Horizon’s supply markets, GHO’s integration there exemplifies how Aave is weaving its native stablecoin into product lines aimed at a broader audience than DeFi power users.

Elsewhere, GHO has been woven into structured products, vaults and strategies across DeFi. Yield strategies on platforms like Pendle tokenize and trade the future yield from GHO-related positions, while other protocols accept GHO as collateral for derivatives or vault products. Not all integrations have been smooth, however. One particularly costly incident occurred on a protocol named Yield, which suffered a loss of roughly $3.73 million when a vault swapped 3.84 million GHO (in the form of stkGHO unwound to GHO) for only about 112,000 USDC due to extreme slippage in a poorly executed trade, as flagged by security firm PeckShield. This event did not reflect a flaw in GHO itself, but it illustrates the risks that arise when large GHO positions interact with thin liquidity and complex routing logic in DeFi.

Governance, Proposals and Regulatory Positioning

Aave DAO, AAVE and the political economy of GHO

GHO is governed by the Aave DAO, where AAVE token holders and delegates propose, debate and vote on changes. The DAO’s authority spans core parameters like GHO’s borrow rate, facilitator mint caps, collateral eligibility and risk configurations, as well as strategic decisions about cross-chain deployments, stability modules and tokenomics. Because interest paid by GHO borrowers flows to the DAO treasury, each governance decision about rates and incentives has direct fiscal implications. In effect, the DAO is playing the role of a central bank and fiscal authority for GHO, balancing growth, stability and revenue.

AAVE tokenomics and the Safety Module are deeply intertwined with GHO. Historically, AAVE holders could stake their tokens in the Safety Module to earn yield and backstop protocol risk. With the introduction of stkGHO, GHO joins AAVE and ABPT as a core asset in this backstop system, giving the DAO more flexibility in how it sources “capital” to absorb potential losses. Recent governance discussions and proposals have explored a substantial tokenomics revamp, including an “Umbrella” safety system, revised revenue distribution mechanisms, and an “Anti-GHO” non-transferable token concept designed to offset GHO debt under certain circumstances. While many of these ideas remain under active debate, they all center GHO in the long-term vision for Aave’s economic architecture.

Governance has also used GHO as a lever to deepen Aave’s integration with other DeFi protocols. Aave Labs has submitted proposals to the Uniswap DAO, for instance, to create a v4 Position Manager that would allow Uniswap LPs to use their Uniswap v4 LP positions as collateral on Aave to borrow GHO. If implemented, this would effectively turn Uni v4 LP shares into “productive collateral” that can be leveraged to mint GHO, tying together two of DeFi’s most important protocols and potentially driving additional demand for both Uniswap liquidity and GHO borrowing. Another proposal seeks funding from the Uniswap DAO to help support development of this integration, illustrating how governance processes across multiple DAOs are converging around GHO as a shared primitive.

Key proposals: gas token, RWA integration and stability module

Several notable governance initiatives have shaped or are poised to shape GHO’s trajectory. The Michigan Blockchain “GHO Gas Token Framework” temp-check proposal argued that allowing users to pay gas fees on L2 networks in GHO would improve user experience and drive adoption by reducing the need to manage native gas tokens. The proposal outlined architectural considerations for integrating GHO into transaction fee mechanisms and explored how Aave could coordinate with rollup operators to support such a feature. While the idea raises complex questions about network economics and security, it reflects an ambition to make GHO a primary transactional currency within certain DeFi ecosystems.

On the asset side, the integration of USCC into GHO’s broader balance sheet has been a focus of risk and governance debates. LlamaRisk’s portfolio analysis described USCC as a crypto carry fund that exploits basis trades between CME futures and spot markets while holding U.S. Treasuries, thus providing diversified exposure to both derivatives and short-term government debt. By including USCC among the assets backing GHO, Aave aims to capture some of the yield from these strategies while diversifying away from pure crypto collateral. However, this also increases exposure to futures basis risk, RWA custodial arrangements and regulatory developments affecting derivatives and securities markets.

The evolving GHO Stability Module represents another crucial governance frontier. As mentioned earlier, a temp-check proposal has suggested upgrading the GSM to integrate BlackRock’s tokenized BUIDL fund, which holds cash and U.S. Treasury bills, as a core building block of GHO’s liquidity management. This would further entrench RWAs in GHO’s backing, bridging DeFi with some of the deepest and most regulated capital markets in the world. In parallel, GHO’s inclusion in Curve’s PegKeeper system after a LlamaRisk review adds an external stability layer that operates under Curve governance but materially affects GHO’s peg dynamics. The interplay between these internal and external modules underscores how GHO’s stability is increasingly a multi-DAO, multi-asset governance problem.

Regulatory analysis: GENIUS Act, MiCAR and beyond

As stablecoins climb the regulatory agenda globally, GHO’s design choices have direct implications for how it may be treated under emerging laws. LlamaRisk’s memorandum on the U.S. GENIUS Act (Public Law 119‑27) provides one of the clearest public analyses of GHO’s position. The memo concludes that GHO does not qualify as a “payment stablecoin” under the act’s statutory definition, primarily because it is not a fiat-redeemable, centrally issued token designed for retail payments in the same way as USDC or PayPal’s PYUSD. Instead, GHO is categorized more as a decentralized, crypto-collateralized asset governed by a DAO, which currently falls outside the scope of the GENIUS Act’s core requirements.

This classification has both advantages and challenges. On the plus side, it may relieve Aave and GHO facilitators from certain licensing obligations and reserve requirements that would otherwise apply to payment stablecoin issuers. On the other hand, it leaves GHO in a more ambiguous space where general securities, commodities and banking laws could still be invoked depending on specific use cases or perceived risks. LlamaRisk’s recommendation that GHO maintain its current architecture to avoid tripping the GENIUS Act’s thresholds underscores how technical design—including decentralized governance, overcollateralization and the absence of fiat redemption rights—can become a regulatory shield.

In Europe, MiCAR has emerged as a key regulatory framework for crypto assets, including stablecoins. Aave’s securing of MiCAR authorization for its EU-facing services, enabling zero-fee euro-to-stablecoin ramps that include GHO, signals a willingness to operate within regulated boundaries and to subject front-end services to compliance obligations. While GHO itself, as a decentralized ERC‑20 token, may not be directly licensed under MiCAR, the interfaces that allow users to acquire and redeem it in fiat terms are increasingly subject to oversight. This duality—permissionless on-chain token, regulated off-chain rails—is likely to define GHO’s path as it aims for broader mainstream usage.

GHO launches on Ethereum mainnet

GHO depegs; farmers sell fixed-rate stablecoin to capture yield elsewhere

GHO achieves $1.00 peg, six months after mainnet launch

Aave DAO votes to launch GHO on Arbitrum via Chainlink CCIP

- 2024-09governance

Curve publicly warns Aave over alleged LLAMMA soft-liquidation mechanism appropriation for GHO v4

GHO market cap breaks $500 million

Aave proposes integrating BlackRock BUIDL into GHO Stability Module

Aave announces Umbrella safety system, Anti-GHO token, and revenue redistribution in tokenomics revamp

Risks, Incidents and Risk Management

Core risks: smart contracts, markets and governance

As with any DeFi protocol and CDP-style stablecoin, GHO carries a spectrum of risks that users must consider. Smart contract risk is ever-present: vulnerabilities in Aave’s core contracts, facilitators, or integrated protocols like Curve could, in the worst case, lead to loss of funds or destabilization of GHO’s peg. While Aave has a strong track record of audits, bug bounties and formal verification efforts, no complex system is immune to unknown exploits. Similarly, oracle risk—if price feeds used to value collateral are manipulated or fail—could lead to incorrect liquidations or undercollateralized GHO issuance.

Market risk is inherent in the collateral backing GHO. Sharp price drops in major collateral assets like ETH, wstETH or WBTC could stress Aave’s liquidation mechanisms, especially if liquidity in those assets is thin or if multiple protocols are forced to unwind positions simultaneously. While overcollateralization and conservative risk parameters mitigate this to some extent, extreme scenarios remain a concern. The integration of RWAs and derivatives exposure through assets like USCC and potentially BUIDL introduces additional layers of risk tied to interest rates, futures basis, and off-chain custodians. These risks are partially offset by diversification benefits but require careful monitoring and governance.

Governance risk, finally, is a defining feature of GHO. Because Aave DAO can change key parameters such as borrow rates, mint caps, collateral policies and even the design of the Safety Module, users are exposed to the collective decision-making of AAVE token holders and delegates. Poor governance decisions—whether due to coordination failures, misaligned incentives, or governance capture—could degrade GHO’s stability or risk profile over time. The presence of external risk managers like LlamaRisk and Chaos Labs, and the increasing professionalization of DeFi governance, are positive developments, but they do not eliminate the underlying political economy challenges.

Incidents involving GHO: Fluid exploit and Yield slippage loss

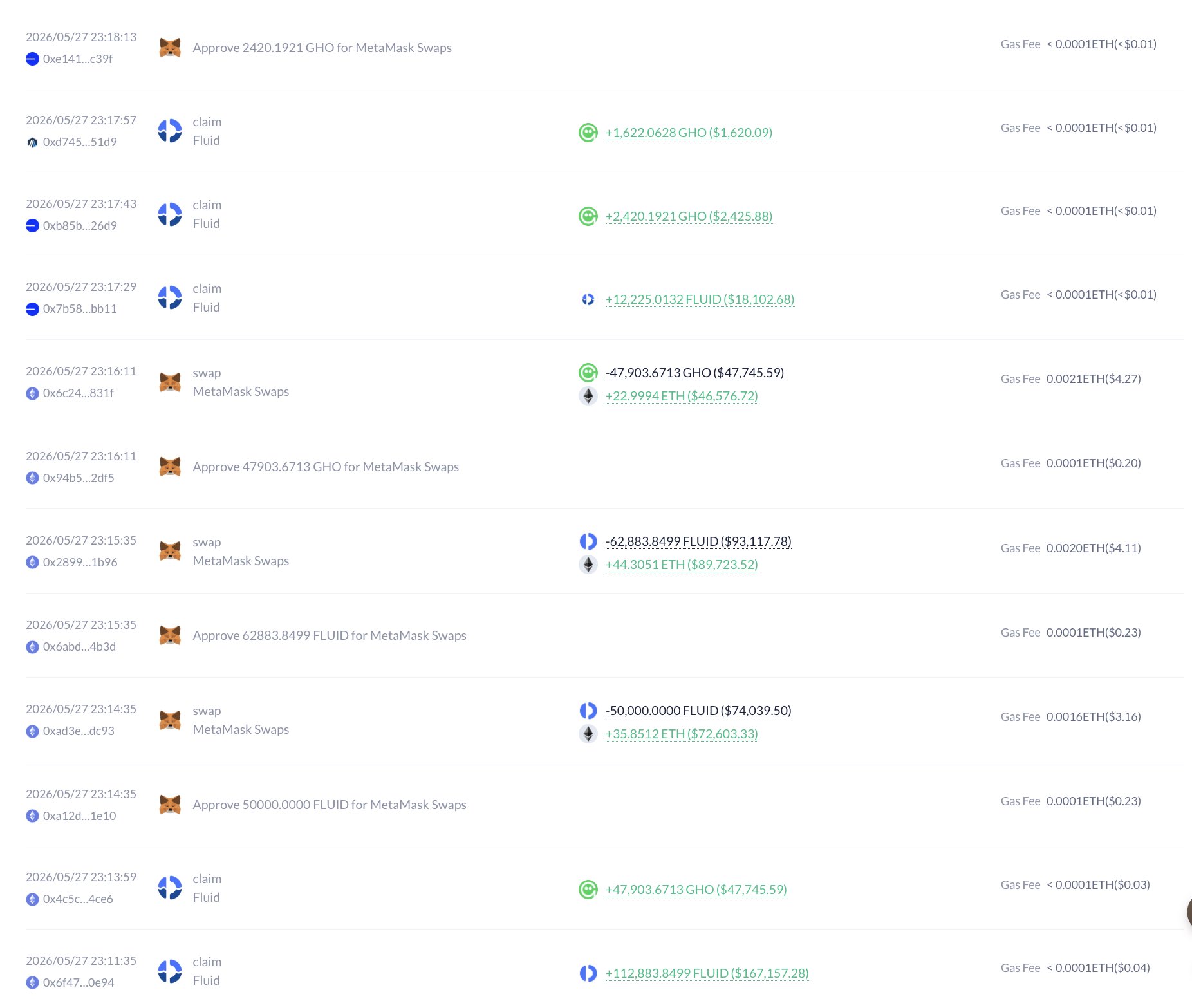

GHO itself has not suffered a direct protocol-level exploit, but it has been involved in significant incidents affecting protocols that held or interacted with GHO. One such event occurred on Fluid, a DeFi protocol whose reward distribution system on Ethereum was compromised. According to reporting by DeFi risk intelligence platform BlackHart and summarized by CryptoRank, attackers compromised two operational keys, exploiting “empty-proof” Merkle claims to drain approximately $215,000 worth of assets, including 112,883 FLUID, 47,903 GHO and some cbBTC, which were then swapped to ETH and laundered through Tornado Cash. Fluid stated that its lending markets, vaults, DEX and user deposits were unaffected and that it had replaced the compromised keys and moved remaining funds to a secure address, emphasizing that the incident stemmed from operational key management rather than flaws in core smart contracts.

This Fluid exploit illustrates a recurring theme in DeFi risk: even if a stablecoin’s own protocol is secure, integrations and ancillary systems—such as reward distributors, front-ends, or cross-chain bridges—can create attack surfaces where that stablecoin is lost. In this case, GHO functioned as a valuable, liquid token that attackers targeted once they had control, underscoring the importance of robust key management, multisig setups, time-locks and transparent incident disclosure in any protocol that holds significant GHO balances.

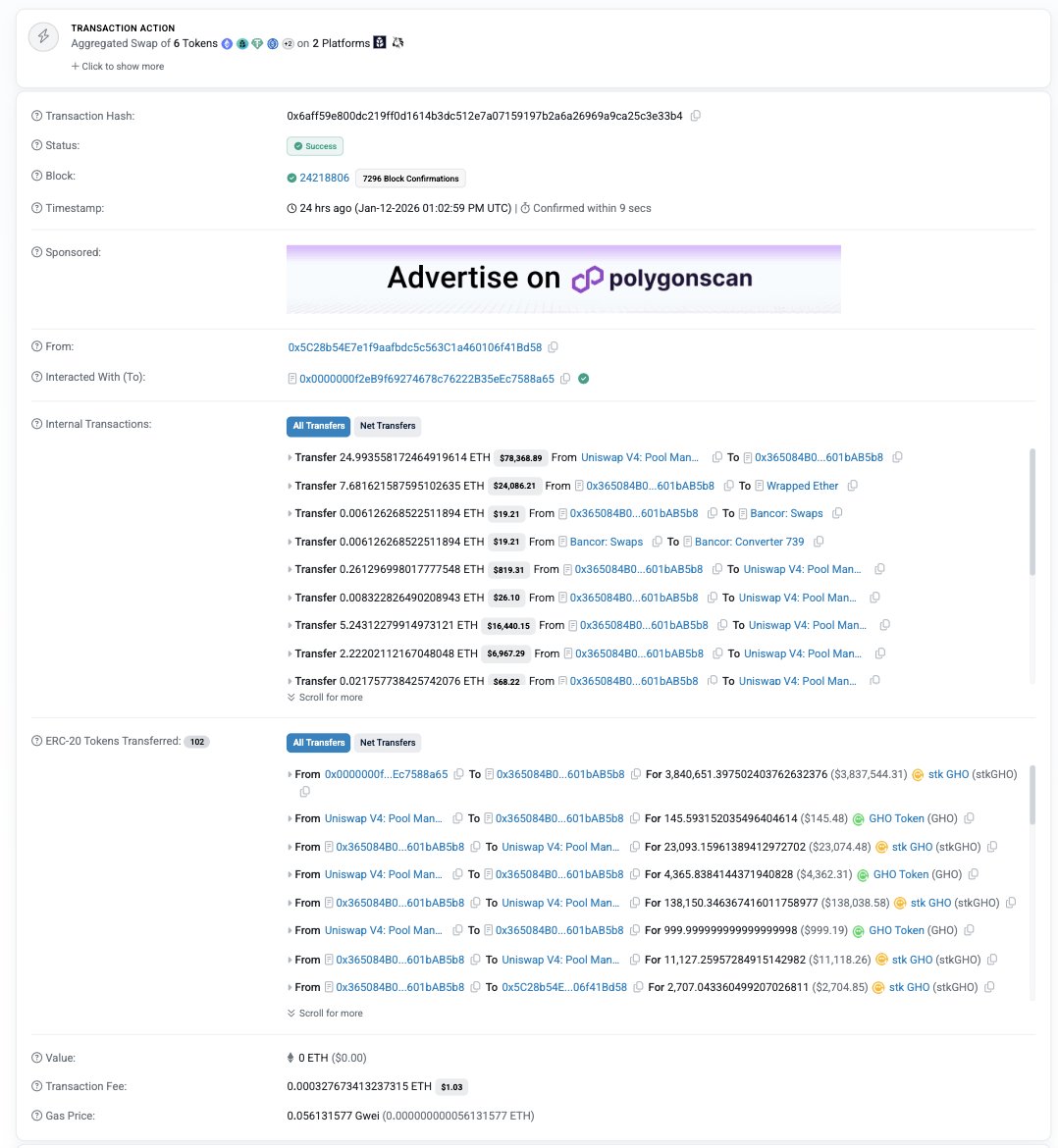

Another high-profile incident centered on a vault operation involving stkGHO and USDC. As flagged by security firm PeckShield, a vault suffered a major financial hit totaling around $3.73 million when it attempted to swap 3.84 million GHO, likely obtained by unstaking stkGHO, for USDC. Due to extreme slippage—possibly from routing through illiquid pools or misconfigured transaction parameters—the trade resulted in only about 112,000 USDC, a catastrophic execution error. This loss was not due to a bug in GHO itself or in Aave’s core contracts; rather, it reflected the dangers of moving large volumes through thin liquidity and the need for stricter slippage controls and execution safeguards in on-chain asset management.

Both incidents highlight practical lessons for protocols and users holding GHO. Large GHO positions should be unwound or rebalanced carefully, with explicit slippage limits and, where possible, through venues with deep, audited liquidity. Operational security for keys controlling GHO funds is paramount, especially when those keys manage reward systems or automated trading logic. Importantly, these episodes did not materially damage GHO’s peg or systemic functioning, but they serve as reminders that stablecoin risk must be understood at the ecosystem level, not solely at the protocol-of-origin level.

Backing, RWAs and LlamaRisk’s portfolio analysis

GHO’s backing is not static; it evolves as Aave’s collateral base, facilitator architecture and RWA integrations change. LlamaRisk’s analysis of GHO’s backing and RWA integration provides a window into this complexity. The integration of USCC, a crypto carry fund, introduces exposure to basis trades between CME futures and spot markets and to portfolios of short-term U.S. Treasuries. In favorable conditions, such a fund can generate relatively steady yield from the spread between futures and spot prices and from Treasury interest, enhancing GHO’s effective backing and the Aave DAO’s revenue. However, in stressed markets, futures basis can collapse or invert, and liquidity in derivatives markets can dry up, challenging the assumptions behind these strategies.

LlamaRisk’s portfolio analysis emphasizes diversification and risk-aware sizing of such RWA exposures, suggesting that careful limits on USCC allocations are necessary to keep GHO’s risk profile within acceptable bounds. The analysis also notes that changes in interest rates, such as declining yields on short-term T-bills, can directly affect the performance of RWA-backed assets, a dynamic also visible in other Aave-related products like RLUSD where yield expectations adjust as the underlying bond portfolio rolls into lower-yielding instruments. For GHO, the introduction of RWAs has the potential to smooth revenues and provide more stable backing, but it must be managed alongside crypto collateral risk to avoid hidden correlations.

The prospective integration of BlackRock’s BUIDL fund into the GHO Stability Module further underscores how GHO’s backing is becoming a composite of crypto assets and tokenized RWAs. While this can make GHO more resilient to crypto-specific downturns, it simultaneously makes it sensitive to regulatory, credit and interest-rate risks in traditional markets. A multi-layered risk governance structure that includes on-chain monitoring, external audits and dynamic parameter management is therefore essential for maintaining confidence in GHO over the long term.

User concentration and systemic considerations

Beyond asset-level risks, GHO’s systemic risk profile depends on who holds and uses it. LlamaRisk’s community updates and recaps suggest that GHO’s user base includes a high proportion of large, sophisticated DeFi participants with significant portfolios across protocols. This concentration cuts both ways. On one hand, such users are often more capable of managing collateral, monitoring governance and responding quickly to market stress, which can stabilize GHO in volatile conditions. On the other hand, concentrated holdings mean that deleveraging by a few large actors could have outsized effects on GHO’s supply, collateral markets and peg.

A related concern is the concentration of GHO’s collateral backing in specific asset classes or counterparties. LSTs like wstETH dominate many Ethereum DeFi collateral pools, and any idiosyncratic shock to these assets—whether from validator slashing, protocol bugs or regulatory targets—could ripple through Aave and GHO. Similarly, heavy reliance on a small number of RWA providers or tokenized funds concentrates off-chain risk. These issues are not unique to GHO, but GHO’s role as a native liability of Aave’s “balance sheet” makes them especially salient for protocol-level risk governance.

Using GHO: Practical Considerations for Participants

Borrowing, leverage and yield strategies

For individual users, the most direct way to interact with GHO is by borrowing it against collateral in Aave markets. A typical flow involves supplying an asset such as ETH, wstETH, WBTC or USDC to an Aave v3 or v4 market that supports GHO, enabling it as collateral where required, and then borrowing GHO up to a risk-adjusted limit. The borrowed GHO appears in the user’s wallet as an ERC‑20 token, while the borrow position accrues interest at a rate set by governance and subject to discounts or surcharges depending on staking status and other factors. Throughout this period, the supplied collateral continues to earn yield or staking rewards where applicable, making GHO borrowing a way to unlock liquidity against productive assets without fully unwinding positions.

Borrowers can use the GHO they mint in numerous ways. Some may simply hold GHO as a stable asset, hedging volatility in their portfolio. Others may deploy it into liquidity pools on Curve or Balancer, potentially earning additional yield through swap fees and incentives. More aggressive users might loop by swapping GHO for additional collateral and re-depositing it into Aave to increase leverage, or by entering yield strategies on protocols like Pendle that involve tokenized future yields. Each of these strategies carries its own risk profile, including liquidation risk on the underlying Aave position, smart contract risk, and market risk associated with the chosen protocol or pool.

The interest rate on GHO borrowing is a central parameter in these strategies. When rates are low, borrowing GHO to chase higher yields elsewhere may be attractive, driving supply expansion. When rates are higher, only the most compelling strategies justify the cost, and some borrowers may prefer to repay and deleverage. Historically, the Aave DAO has used GHO rates as a macro lever to influence supply growth and peg conditions, starting with a relatively low fixed rate at launch and adjusting over time as market structure matured. Users must therefore keep an eye on governance proposals and parameter changes, as they directly affect the economics of any GHO-based strategy.

Holding, staking and risk-aware liquidity provision

For users who prefer a more passive stance, holding GHO as a stable asset and selectively deploying it can still make sense. One relatively straightforward option is staking GHO in the Aave Safety Module to receive stkGHO and earn yields funded by the Aave DAO’s ecosystem reserve. This approach aligns the holder with the protocol’s long-term health, as they are effectively providing insurance capital in exchange for a share of protocol revenues and emissions. However, it carries explicit slashing risk: in a severe protocol shortfall event, a portion of staked GHO could be seized to cover losses, making it unsuitable for users who cannot tolerate such downside.

Alternatively, users can deposit GHO back into Aave as a supplied asset in markets that support it, earning a deposit yield that reflects demand for borrowing GHO and any additional incentives governance may layer on. As with other money market deposits, this route exposes users to protocol-level risks but not to slashing events, although it may offer lower yields than staking in the Safety Module. In periods when Aave heavily incentivizes GHO deposits, as reported in early 2025, the yield on GHO supply can exceed that on USDC or USDT, making it attractive for yield-seeking capital. Users should nevertheless bear in mind that such incentive-driven yields may not be permanent.

Providing liquidity in GHO pairs on DEXes like Curve, Balancer or Uniswap introduces a different bundle of risks and rewards. Liquidity providers earn trading fees and may receive incentive tokens, but they face impermanent loss, particularly if GHO’s peg deviates or if paired assets experience volatility. In stable-swap pools where all assets target $1, impermanent loss is often smaller, but events like the extreme slippage swap from stkGHO to USDC in the Yield incident show that execution risk and thin liquidity in specific pools remain real concerns. Careful selection of venues, position sizing and monitoring are therefore crucial.

Payments, gas and real-world usage

As Aave and its partners expand fiat on/off ramps and explore gas payment integration, GHO is likely to see more use in everyday transactional contexts. In Europe, MiCAR-compliant services that offer zero-fee euro-to-GHO conversions make it possible for users to treat GHO as a quasi–digital cash instrument for interacting with DeFi: salaries or savings held in euros can be converted into GHO, deployed in on-chain strategies, and eventually converted back, all within a single app experience built around Aave. This type of flow reduces friction and could, over time, support use cases like merchant payments, remittances, or treasury management, especially for crypto-native businesses and DAOs.

The prospect of using GHO to pay gas fees on L2 networks adds another dimension. If rollups integrate GHO as a gas token in the way proposed by the GHO Gas Token Framework, users might no longer need to juggle ETH or network-specific tokens simply to cover transaction costs. Instead, they could hold GHO as their primary balance and let the wallet or rollup infrastructure handle fee payments under the hood. This vision aligns with broader efforts in the Ethereum ecosystem to abstract gas and to make stablecoins a more central part of the user experience. However, it also raises questions about fee markets, validator incentives and the interplay between native tokens and stablecoins, all of which would need to be addressed at both technical and governance levels.

Real-world usage of GHO is still nascent compared with mature fiat-backed stablecoins like USDC, which enjoy broader merchant and institutional acceptance. Yet the combination of compliant on/off ramps, deep DeFi integrations and governance-driven utility enhancements suggests a trajectory where GHO could become a common settlement asset not only within Aave but across a constellation of Web3 applications. Achieving that vision will require continued attention to stability, liquidity, risk management and regulatory coordination.

A Yield protocol vault operation swapping stkGHO to USDC suffered a $3.73M loss from extreme slippage on 3.84M GHO, exposing real liquidity-depth risk in GHO exit paths under stress.

GHO peg defense has depended on appointed committees, a named temporary steward, and DAO-delegated Liquidity Committees rather than algorithmic or fully on-chain mechanisms, concentrating critical decisions in small groups.

GHO depegged immediately after its July 2023 launch and remained below $1 for six months as borrowers sold at a discount to capture yield elsewhere; the GHO Steward and crvUSD PegKeeper basket entry were structural responses to this persistent weakness.

LlamaRisk's analysis of GHO in the context of the GENIUS Act flags evolving U.S. stablecoin legislation as a material risk to GHO's RWA collateral strategy and its operational permissibility for U.S. users.

GHO is minted exclusively against collateral supplied on Aave, meaning a sharp Aave-wide liquidity shock or mass position closure directly threatens GHO backing with no diversified off-protocol collateral buffer.

Outlook and Conclusion

GHO has rapidly evolved from a governance idea into a core pillar of Aave’s protocol economy and a meaningful player in the crypto-collateralized stablecoin space. Its borrow–mint architecture, facilitator model and deep integration with Aave’s Safety Module and revenue flows make it a uniquely “native” stablecoin, whose fortunes are tightly interwoven with those of the lending protocol that created it. The Aave DAO’s strategic focus on scaling GHO adoption, diversifying revenue streams and expanding the Aave app ecosystem reflects an ambition to turn GHO into a central unit of account and collateral layer for DeFi, rather than a marginal side product.

At the same time, GHO’s trajectory underscores the challenges of building a decentralized stablecoin in a complex and evolving ecosystem. Its peg stability relies on a mix of overcollateralization, interest-rate policy, external liquidity modules and cross-protocol integrations, each of which introduces its own vulnerabilities and governance dependencies. Incidents like the Fluid key compromise and the Yield vault slippage loss show how GHO can be implicated in losses even when its core protocol functions as intended, highlighting the importance of ecosystem-wide risk management practices. Integrations with RWAs through vehicles like USCC and prospective BUIDL exposure promise more durable revenue and diversification but also draw GHO deeper into the domain of traditional finance risks and regulations.

Looking ahead, GHO’s success will hinge on several interlocking factors. First, continued prudence in risk governance, informed by external analyses from LlamaRisk, Chaos Labs and others, will be essential to maintain confidence in its backing and peg stability. Second, thoughtful expansion across chains and products—such as Base, Arbitrum, Horizon and potential Uniswap collateral integrations—must balance growth with containment of systemic risk. Third, regulatory navigation, from leveraging MiCAR-compliant ramps to maintaining a design that stays outside the strictest U.S. “payment stablecoin” rules, will shape how far GHO can penetrate mainstream financial use cases.

For DeFi practitioners and observers, GHO offers a case study in how a major protocol can architect its own native stablecoin as both a financial product and a governance tool. It embodies the promise and complexity of decentralized finance: transparent yet intricate, open yet governed, innovative yet exposed to new forms of risk. Whether GHO ultimately grows to “a billy” in supply and beyond will depend not only on market demand and incentive programs, but on the protocol community’s ability to sustain a stable, credible and resilient monetary asset in the face of technological, economic and regulatory change.

Latest GHO news

Sources

- https://aave.com/gho

- https://aave.com/docs/ecosystem/gho

- https://thedefiant.io/news/defi/aave-launches-gho-stablecoin-on-ethereum-mainnet

- https://eco.com/support/en/articles/15253998-aave-v4-gho-yield-2026-borrow-mint-mechanics-explained

- https://aave.com/help/gho-stablecoin/gho

- https://chainlinktoday.com/chainlink-ccip-powers-ghos-cross-chain-expansion-to-base/

- https://governance.aave.com/t/arfc-gho-cross-chain-launch/17616

- https://cryptorank.io/news/feed/0bcbc-fluid-loses-215k-reward-system-exploit-key-compromise

- https://x.com/PeckShieldAlert/status/2011069662377980147

- https://governance.aave.com/t/llamarisk-insights-gho-s-backing-and-rwa-integration-a-portfolio-analysis/23521

- https://www.curve.finance/crvusd/ethereum/pegkeepers/

- https://www.bitget.com/support/articles/12560603835078

- https://x.com/aave/status/1988970318346744258

- https://governance.aave.com/t/llamarisk-insights-gho-in-the-context-of-genius-act/23111

- https://www.youtube.com/watch?v=2q65AQ5jcmI

- https://governance.aave.com/t/horizon-weekly-highlights/23078

- https://www.llamarisk.com

- https://chaoslabs.xyz/posts/chaos-labs-aave-gho-risk-monitoring-dashboard

- https://governance.aave.com/t/temp-check-gho-gas-token-framework/21051

- https://thedefiant.io/news/defi/aave-gho-stablecoin-market-cap-breaks-usd500-million

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…