Explainer on crypto VC: how venture funds back blockchain and Web3 startups, key funding trends, AI’s impact, evolving deal structures, and the shift from speculative token launches to fundamentals-driven, compliance-first investing.

+7 sources across the wider coverage universe

Former Hyperliquid skeptic Pavel Paramonov argues HYPE is among crypto's few truly investable assets, citing its no-VC structure, token buybacks and growing challenge to Binance's dominance2026-06

Former Hyperliquid skeptic Pavel Paramonov argues HYPE is among crypto's few truly investable assets, citing its no-VC structure, token buybacks and growing challenge to Binance's dominance2026-06 Dragonfly Fund IV sparks a candid playbook on building a crypto VC, covering fundraising, differentiation, winning deals, and surviving cycles.2026-02

Dragonfly Fund IV sparks a candid playbook on building a crypto VC, covering fundraising, differentiation, winning deals, and surviving cycles.2026-02 Crypto VCs are shifting toward FinTech-style investing as token-first exits fade, prioritizing real revenue, payments, trading, and compliance-driven models. Stablecoins and markets now anchor sustainable crypto businesses as fundamentals replace narrative-driven growth.2025-12

Crypto VCs are shifting toward FinTech-style investing as token-first exits fade, prioritizing real revenue, payments, trading, and compliance-driven models. Stablecoins and markets now anchor sustainable crypto businesses as fundamentals replace narrative-driven growth.2025-12 AlphaGrowth launches largest crypto VC and DAO treasury dataset on SerenAI x402 payment gateway with over 70,000 deals tracked2025-12

AlphaGrowth launches largest crypto VC and DAO treasury dataset on SerenAI x402 payment gateway with over 70,000 deals tracked2025-12 VC money is flooding back into crypto, with nearly $25B deployed in 2025—a 150% jump led by Binance, Polymarket, and Circle. Investors are now backing compliance-first, revenue-real businesses as the market matures.2025-11

VC money is flooding back into crypto, with nearly $25B deployed in 2025—a 150% jump led by Binance, Polymarket, and Circle. Investors are now backing compliance-first, revenue-real businesses as the market matures.2025-11 VC-backed crypto token launches are failing in 2025, with 85% underwater and the old “Top VC = pump” playbook breaking down as capital dries up and fundamentals start to matter.2026-02

VC-backed crypto token launches are failing in 2025, with 85% underwater and the old “Top VC = pump” playbook breaking down as capital dries up and fundamentals start to matter.2026-02

Crypto VC: How Venture Capital Shapes the Digital Asset Industry

Crypto venture capital, often shortened to crypto VC, refers to professional investment funds that back cryptocurrency, blockchain, and Web3 startups—typically in exchange for equity, tokens, or both—while aiming to generate outsized returns from the growth of digital asset markets. In the past decade, crypto VC has evolved from small, experimental Bitcoin bets into an institutional-scale asset class that now sits at the crossroads of global venture capital, public token markets, and the rapidly expanding field of artificial intelligence.

What Is Crypto VC?

At its core, crypto VC is a specialization of traditional venture capital focused on companies and protocols building on or around blockchains and digital assets. These investors fund centralized exchanges, decentralized finance (DeFi) protocols, wallet and custody providers, stablecoin issuers, developer tooling, infrastructure layers, and newer verticals such as AI–crypto hybrids and on-chain gaming. In return, they receive ownership that can take the form of private company equity, allocations of project tokens, or complex structures that combine both. Unlike classic tech VC, however, crypto VC operates in an environment where early-stage assets can become liquid via token listings long before a company reaches maturity, blurring the lines between private and public markets.

The scope of crypto VC has broadened dramatically as the industry has matured. What began as a niche for early believers in Bitcoin and Ethereum has evolved into a global capital market where multibillion-dollar specialized funds compete with diversified firms and corporate investors. Dedicated firms like Dragonfly describe themselves as backing the "best researchers and builders" across the crypto ecosystem, signaling a shift from pure speculation to research-driven, thesis-led investing. Large generalist firms such as Andreessen Horowitz (a16z) have carved out dedicated crypto arms, while organizations like Coinbase have evolved from VC-backed startups into major public companies with their own corporate venture arms, reinvesting into the ecosystem they helped create.

Crypto VC also interacts more directly with retail investors than most other forms of private capital. Tokens issued by VC-backed projects can trade on global exchanges, allowing retail traders to participate far earlier than they would in traditional equity-only startups. This early liquidity can create powerful feedback loops: VC investors seed a project, early users and speculators join once tokens list, and market sentiment—often amplified by social media—can influence subsequent funding rounds and strategic decisions. The increasingly common critique that "VCs dump on retail" emerges directly from this dynamic, and it has pushed both founders and funds to experiment with new models of token distribution and governance.

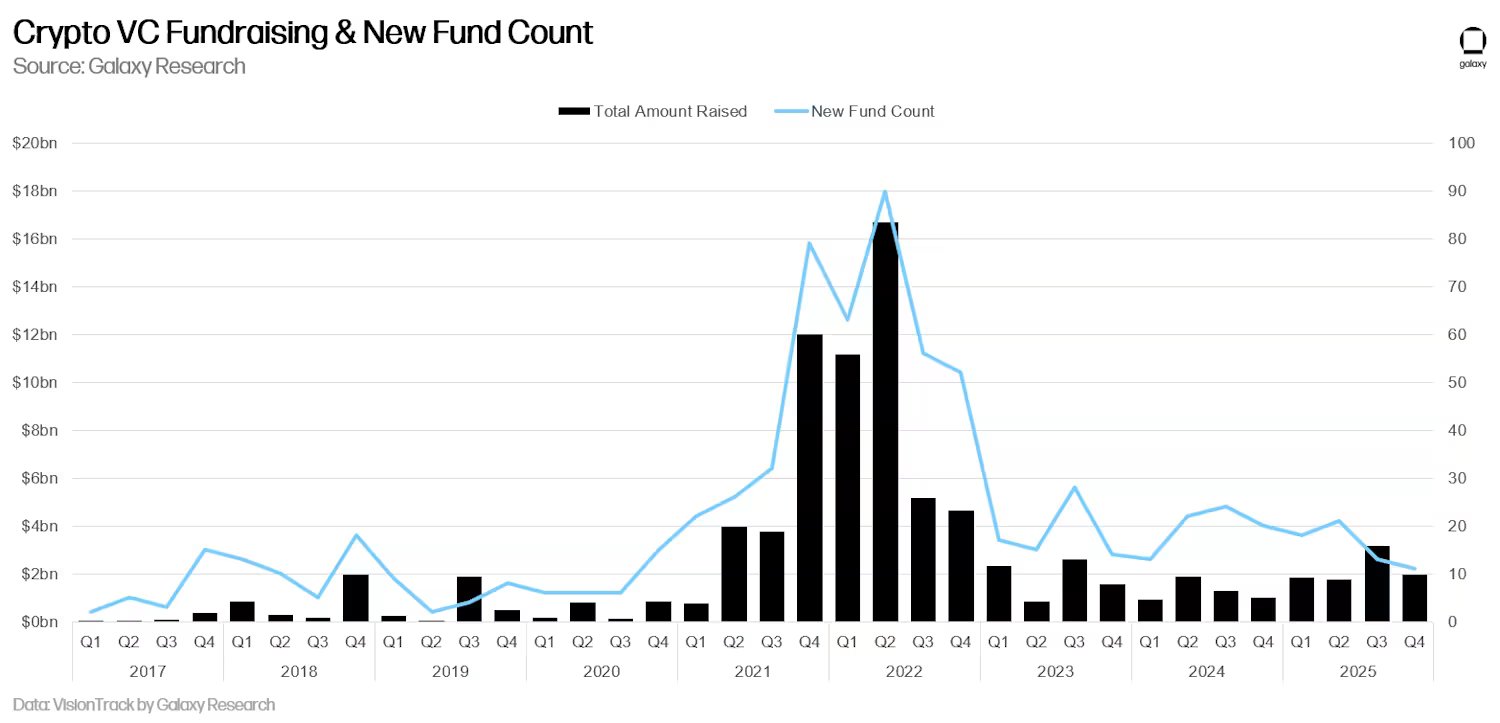

Another distinctive characteristic of crypto VC is its tight coupling to macro cycles in digital asset prices. Bull markets in Bitcoin and Ethereum tend to attract both founders and financiers, leading to rapid growth in deal volume and fund formation, while bear markets impose harsh discipline. Data from Galaxy Research, for instance, shows that crypto VC fundraising peaked in 2022 and has since cooled sharply, with the number of new crypto funds falling to a five-year low and recent quarterly fundraising totaling only about 12% of the levels seen in the second quarter of 2022. This cyclicality is not unique to crypto, but the amplitude is unusually high because token prices provide a real-time, highly volatile mark-to-market for sentiment and perceived opportunity.

Over time, crypto VC has come to sit at the intersection of several broader forces: the rise of AI, the institutionalization of digital assets, the growth of stablecoins as a de facto dollar-based payment rail, and evolving regulatory debates about investor protection and market access. Venture capital investments in AI firms accounted for an estimated 61% of global VC spending in 2025—about USD 258.7 billion out of USD 427.1 billion in total—which means that crypto VC now competes for capital not only with other technology verticals but with an AI sector that dominates investor attention. This competition, in turn, is nudging crypto VCs toward thematic convergence, where a growing share of crypto investments are explicitly tied to AI infrastructure, agents, or data markets.

From Early Bitcoin Bets to Specialized Crypto Funds

The history of crypto VC can be traced back to the early 2010s, when a handful of investors began backing Bitcoin payment companies, mining operations, and early exchange platforms. These early bets on companies like Coinbase, which launched as a simple consumer-friendly on-ramp and grew into one of the largest regulated crypto exchanges globally, established the template for VC-backed crypto success. Coinbase’s trajectory—from seed-stage startup to publicly listed company—demonstrated that crypto ventures could follow a path broadly familiar to Silicon Valley investors, even as they operated in a novel asset class.

As Ethereum and smart contracts gained traction, a new wave of crypto-native funds emerged to specialize in protocol-layer investments and token-based projects. Over time, sophisticated firms such as Paradigm and a16z Crypto raised dedicated vehicles often measured in the billions of dollars, while multi-strategy groups like Galaxy Digital blended venture-style equity investments with trading, lending, and asset management businesses. This institutionalization brought more rigorous research, better legal structuring, and deeper technical expertise into the space, but it also raised concerns among some community members that crypto was becoming dominated by the same elite capital networks it set out to disrupt.

The explosive 2020–2021 bull market accelerated this trajectory. According to data cited by Binance Research, crypto VCs raised nearly USD 17 billion across more than 80 new funds in the second quarter of 2022 alone, representing a historical peak in new crypto-focused capital formation. These funds were raised into an environment of soaring token prices, booming DeFi and NFT adoption, and a broad narrative that Web3 would rewire the internet and financial system. The subsequent bear market, marked by exchange failures, protocol hacks, and sharp price declines, severely tested that thesis and forced both LPs and GPs to reevaluate how much capital the sector could absorb responsibly.

Why Crypto Needs (and Challenges) Venture Capital

Proponents argue that venture capital is essential to the crypto ecosystem because many of the most ambitious projects—new L1 blockchains, scaling solutions, enterprise infrastructure, advanced cryptography—require years of research and development before generating meaningful revenue. In this view, long-horizon capital from specialized VCs enables innovation that would not be funded by short-term token speculators alone. The focus among many investors on foundational blockchain technologies rather than purely speculative assets, as described by CV VC in its analysis of 2025 investment trends, reflects this perceived need to fund core infrastructure.

At the same time, crypto challenges many of the assumptions behind traditional VC. The existence of liquid tokens allows projects to raise substantial capital from public markets relatively early in their lifecycle, often via token generation events (TGEs) or initial DEX offerings (IDOs). This can reduce dependence on private funding, but it can also create perverse incentives, as projects may prioritize launching a token quickly over building a sustainable product. The "raise a round, launch a token, and sell into retail demand" playbook that dominated earlier cycles is now widely viewed as brittle, particularly given how many such tokens have underperformed.

Critics also point out that the combination of private pre-sales, large VC allocations, and aggressive vesting schedules has often left retail participants holding the bag. Binance Research has noted that around 85% of tokens launched in 2025 were trading below their initial listing prices, with many VC-backed projects barely breaking even or posting significant losses. In such an environment, the mere presence of a "top VC" on a cap table has ceased to be a reliable bullish signal, and the market has started to reward projects that demonstrate real user adoption, revenue, and fairer launch mechanisms over those that rely primarily on narrative or branding.

Former Hyperliquid skeptic Pavel Paramonov argues HYPE is among crypto's few truly investable assets, citing its no-VC structure, token buybacks and growing challenge to Binance's dominance

DefiLlama has Hyperliquid at ~$79M of fees over the last 30 days, with 99% of core perp/spot fees routed to the Assistance Fund for HYPE buys, so the token is closer to an exchange cash-flow sink than another emissions farm. SpaceX perps doing ~$1.3B in 24h volume matters because it turns Hyperliquid from a crypto perp venue into 24/7 macro/RWA rails in the same account as BTC and ETH. HYPE still carries validator/governance centralization risk, but if non-crypto markets keep finding liquidity there, the buyback loop gets fed by categories CEXs used to own alone.

Readers click Crypto VC stories not to track money flows but to audit the power asymmetry — who gets refunds, who hoards insider allocations, and whether VC-friendly tokenomics leave public buyers holding the bag.↗

How Crypto VC Funds Operate

Crypto VC funds are typically structured similarly to traditional venture funds: limited partners (LPs) such as family offices, endowments, and high-net-worth individuals commit capital to a closed-end vehicle managed by a general partner (GP), who deploys that capital into a portfolio of startups and protocols over several years. What differs are the instruments used, the speed of liquidity, and the interplay with public token markets.

Fund Structures, LPs, and Capital Raising

Most crypto VC funds are organized as multi-year vehicles, often with a 10-year life and a defined investment period during which new deals can be made. In 2022, even as public crypto markets softened, flagship managers continued to raise large dedicated vehicles: Haun Ventures and a16z Crypto collectively raised about USD 3.2 billion for new funds, underscoring that top-tier GPs could still attract significant capital despite market volatility. Later, in a more challenging fundraising environment, the crypto-focused firm Dragonfly closed a USD 650 million fourth fund, even as many smaller blockchain VCs faced what one report described as a "mass extinction." Dragonfly positions itself as a leading crypto investment fund backing research-driven builders across the ecosystem, reflecting the increasing emphasis on intellectual and technical edge.

The LP base for these funds is evolving as well. Early crypto VCs often relied on wealthy individuals and a handful of forward-looking family offices; over time, institutional allocators have shown greater interest, though many remain cautious due to regulatory uncertainty and past boom-bust cycles. Pension funds, sovereign wealth funds, and insurance companies are selectively exploring digital asset exposure, sometimes via venture funds and sometimes via public-market vehicles like Bitcoin ETFs, but their participation remains much lower than in traditional tech VC. The intense competition from AI—now absorbing roughly three-fifths of global VC capital—also makes it harder for crypto-focused managers to secure large commitments.

Fundraising dynamics have shifted since the 2022 peak. Data compiled by Galaxy Research and highlighted in industry analysis shows that while crypto VCs raised enormous sums in 2022, deployment from 2023 to 2025 has been relatively gradual, with total capital deployed during that period roughly equal to what was raised in 2022 alone. At the same time, new fund formation has slowed sharply, and some LPs have reallocated risk budgets toward AI and other sectors. Crunchbase data on Q1 2026 venture funding reveals a broader pattern in tech: more capital is flowing overall, but it is being concentrated into fewer companies, suggesting that GPs and LPs are both becoming more selective about where they place large bets.

Stages, Rounds, and Deal Structures

Crypto VC operates across the full lifecycle of company building, from pre-seed experiments to late-stage growth rounds, but the instruments used can differ from mainstream tech. In a typical seed round, founders might sell equity in their operating company via SAFEs or convertible notes, optionally combined with token warrants that entitle investors to a certain percentage of future token supply. At later stages—Series A, B, and beyond—structures can become more complex, incorporating preferred equity rights, board seats, pro rata rights for future token allocations, and detailed vesting schedules.

Token-specific agreements such as SAFTs (Simple Agreements for Future Tokens) are common in projects where the primary value will accrue to tokens rather than equity. These instruments promise investors a share of tokens once they are created and legally able to be distributed, often at a discount to future public listing prices in exchange for early risk capital. In many deals, equity and token rights are bundled so that investors participate in both corporate upside and on-chain asset appreciation. This dual-asset structure can increase alignment but also creates challenging questions about valuation, governance, and regulatory classification.

The following table summarizes, in simplified form, how stages and instruments often map in crypto VC:

| Stage | Typical Instruments | Main Focus |

|---|---|---|

| Pre-seed/Seed | Equity (SAFE/convertible), token warrants, SAFTs | Team, vision, technical feasibility |

| Series A | Preferred equity, SAFTs, token options | Product-market fit, early revenue or usage |

| Series B+ | Preferred equity, structured token deals | Scaling, regulation, international expansion |

This mapping is not exhaustive, but it illustrates how token-related instruments become relevant very early in a crypto startup’s life while remaining central all the way through growth stages. In DeFi and protocol projects that lack a traditional company structure, token allocations to early backers may effectively serve as the primary investment vehicle. In such cases, the economics resemble those of a high-beta public equity, but with governance rights, code upgrade influence, and sometimes revenue-sharing embedded in smart contracts.

Exits, Liquidity, and the Fading Token-Launch Playbook

In classic venture capital, liquidity is typically achieved via trade sales (M&A) or IPOs after many years. Crypto VC adds three additional, earlier potential exit paths: token listings on centralized exchanges, liquidity mining distributions that increase token float, and secondary sales of token or equity positions to other investors. These mechanisms can, in theory, allow VCs to realize returns sooner and recycle capital into new projects.

However, the industry’s experience with the 2020–2022 cycle has highlighted the pitfalls of relying too heavily on fast token liquidity. Binance Research data indicates that approximately 85% of tokens launched in 2025 are trading below their listing prices, and the return on investment for VC portfolios has been trending downward since 2022. The strategy of raising a round, launching a token quickly, and selling into a wave of retail enthusiasm is no longer reliable; in fact, market participants increasingly view such patterns with suspicion, especially when token unlock schedules and insider allocations are opaque.

As a result, both founders and investors are experimenting with longer token lockups, more gradual emission schedules, and launch strategies that prioritize actual usage over speculative hype. In parallel, interest has grown in equity-first models where tokenization, if it happens at all, occurs after a product has demonstrated traction and a sustainable business model. This shift aligns with a broader trend noted in industry analysis, where crypto VCs are moving toward a more FinTech-style approach that emphasizes real revenue, payments, trading, and compliance-driven models over purely narrative-driven token launches.

At the same time, traditional exit routes remain relevant. Exchanges, infrastructure providers, and data companies in crypto can be acquired by larger financial or technology firms, offering equity exits to their investors. As regulatory clarity improves in some jurisdictions, more companies may follow the Coinbase path of pursuing public listings, providing long-duration, equity-based liquidity alongside any token-related value accrual.

Market Cycles and the State of Crypto VC Funding

Crypto VC does not operate in a vacuum; it is deeply intertwined with macroeconomic conditions, interest rates, global risk appetite, and the boom-bust rhythms of digital asset markets. Understanding recent funding trends helps explain how investors are recalibrating their strategies.

From 2022’s Peak to a Sharp Cooldown

Frameworks from Galaxy Research and other data providers depict 2022 as the high-water mark of the last cycle, particularly in terms of fund formation and headline-grabbing deal sizes. In the second quarter of 2022 alone, crypto venture firms raised nearly USD 17 billion across more than 80 new funds, reflecting strong institutional interest and widespread belief that Web3 would define the next generation of internet platforms. This capital was largely committed when token prices were high, central bank policies were relatively accommodative, and venture LPs were flush from a decade of strong tech returns.

The subsequent tightening of monetary policy, coupled with high-profile failures in the crypto industry, triggered a painful unwind. As digital asset prices fell, several large centralized players collapsed, and regulatory scrutiny intensified, many VCs slowed their pace of deployment. New fund launches declined sharply, with the number of new crypto funds dropping to a five-year low, and overall VC ROI in the sector trended downward. For LPs, the combination of weaker mark-to-market performance and uncertainty about regulatory outcomes made it difficult to justify large fresh commitments, especially when AI and other sectors were offering compelling narratives.

Despite this, the sheer amount of capital raised in 2022 created a latent reservoir of "dry powder." Binance Research notes that total capital deployed from 2023 to 2025 is roughly equal to what was raised in 2022 alone, suggesting that managers have been deploying cautiously rather than shutting off the spigot entirely. This slow drip reflects both prudence and the structural reality that venture funds are obligated to invest committed capital over a defined timeframe, albeit with flexibility in pacing and sector allocation.

Signs of Rebound: 2025–2026 Data

By 2025, evidence emerged that crypto VC was reawakening, albeit in a more disciplined form. According to CV VC, blockchain and crypto startups raised USD 4.8 billion in the first quarter of 2025, marking the strongest quarter since late 2022. Strikingly, the capital deployed in Q1 2025 alone equaled about 60% of all crypto VC capital deployed in 2024, highlighting how quickly activity can rebound once macro conditions stabilize and token markets recover. This resurgence was not merely a reversion to prior behavior; much of the funding was directed toward core infrastructure and foundational technologies, rather than purely speculative plays.

Other datasets corroborate this shift. Binance Research reports that VC investment in the sector reached USD 8.5 billion in a recent quarter, up 84% quarter-over-quarter, though much of that capital is believed to be drawn from funds raised in 2022 rather than new inflows from LPs. This indicates that while LPs remain cautious about committing fresh capital, existing funds are again finding deals they consider sufficiently attractive to justify deployment. Meanwhile, monthly snapshots such as DefiLlama’s figures for February 2026—showing USD 883 million funnelled into crypto startups that month—suggest that investors are still willing to write sizable checks, even amid lingering uncertainty.

Importantly, the composition of funding has shifted. A VC interviewed about 2026 investment trends highlighted three key themes driving capital flows: stablecoins and payments infrastructure, AI agents that interact with crypto systems, and institutional tools such as compliance and treasury management. This thematic focus underscores the move toward more utilitarian, revenue-generating businesses that can anchor the ecosystem regardless of speculative cycles.

Concentration and “Fewer but Bigger” Bets

Zooming out to the broader venture environment, Crunchbase notes that overall venture funding recently hit record levels, but the underlying story is more nuanced: more capital is flowing, but to fewer companies. That pattern is clearly visible in crypto. Mega-rounds like Morpho’s USD 175 million strategic raise, led by top-tier firms such as Paradigm, a16z Crypto, and Ribbit Capital, exemplify a world where investors are willing to concentrate large amounts of capital into a small number of perceived category leaders rather than spreading bets thinly across many projects.

This concentration reflects both risk management and conviction. After a cycle in which the "spray-and-pray" approach led to a long tail of underperforming tokens and struggling projects, many VCs are narrowing their focus to teams with demonstrated execution, clear product-market fit, regulatory awareness, and defensible moats. The result is an ecosystem where early-stage founders may find it harder to raise capital without strong traction, while winners that can show real data on usage and revenue may enjoy more robust support than ever.

Dragonfly Fund IV sparks a candid playbook on building a crypto VC, covering fundraising, differentiation, winning deals, and surviving cycles.

Definitely advise anyone will to become a VC to read this

- 01Post-FTX funding cycle recovery↗

The collapse of SBF's capital recycling machine gutted early-stage deal flow, and readers tracked every data point — Galaxy's $11.5B figure, Q1 2025's $4.8B rebound — as evidence the drought was ending.

- 02Insider tokenomics and refund deals

Berachain's secret $25M refund to Brevan Howard and BERA's VC-heavy allocation structure crystallized the suspicion that token launches are structured to eliminate downside for insiders while retail absorbs it.

- 03Points replacing airdrops, VCs win

The 40 billion points issuance story exposed a structural shift where projects defer token distribution indefinitely, benefiting VC lock-up timelines while leaving community participants uncertain.

- 04Mega fund raises and strategy pivots↗

Announcements from Polychain, Dragonfly, and Pantera — each raising $200M–$1B — signaled which firms survived the bear cycle and were positioning for the next deployment wave.

- 05Stablecoin infrastructure as next VC thesis↗

The framing of a 'stablecoin era' backed by $100M in a single week and a new VC-backed stablecoin chain gave readers a clear narrative about where smart money was concentrating post-2024.

- 06Regulatory opening for crypto VC

Japan's cabinet approval for VCs to invest directly in crypto startups represented a concrete, jurisdiction-level unlock that readers recognized as a structural change rather than mere sentiment.

Strategy Shifts: From Token Pumps to Real Businesses

The most significant evolution in crypto VC over the last few years has been strategic rather than purely financial. Investors are moving away from approaches that implicitly depended on speculative excess and toward models that resemble those used in more mature sectors like FinTech and enterprise software.

The End of the “Spray-and-Pray” Era

Several data points reinforce the sense that the indiscriminate phase of crypto VC is over. Binance Research’s analysis showing that approximately 85% of tokens launched in 2025 trade below their initial listing prices underscores how damaging the prior cycle’s approach has been for both retail participants and LPs. The downward trend in VC ROI since 2022, coupled with a collapse in new fund launches, reflects a collective realization that simply backing a large number of token projects and expecting a few to "moon" is not a repeatable institutional strategy.

Against this backdrop, the symbolic power of having a "top VC" on a cap table has diminished. Where once the presence of a brand-name fund might have been enough to spark short-term price appreciation, market participants now scrutinize token allocations, vesting schedules, and governance structures more carefully. Analysts increasingly emphasize fundamentals such as protocol revenue, user retention, and real-world integration, and they question projects whose valuations rest primarily on narrative. Binance Research has observed that the old playbook of raising a round, launching a token, and selling into retail demand is fading, replaced by a focus on building real user bases and sustainable products.

This shift is not purely defensive. Many VCs genuinely believe that the next generation of crypto value creation will come from systems that solve tangible problems—such as cross-border payments, risk management, and programmable money—rather than from speculative instruments alone. The recalibration of strategy can therefore be seen as a maturation of the asset class, even if it has been catalyzed by painful lessons.

What VCs Want Now: Stablecoins, Revenue, and Infrastructure

Recent deal flow illustrates a changing hierarchy of priorities. As one 2026 analysis summarized, stablecoins and payments infrastructure, AI agents, and institutional tools like compliance and treasury management have become key themes for crypto VCs. Stablecoins in particular are emerging as a central pillar of the ecosystem, functioning as a bridge between traditional finance and on-chain applications. For VCs, investments in stablecoin issuers, on/off-ramp providers, and payment processors resemble FinTech bets, with clearer revenue models and regulatory frameworks than many purely speculative tokens.

The emphasis on institutional tools reflects a recognition that long-term adoption requires robust compliance, monitoring, and treasury solutions. Projects that help asset managers, corporates, and DAOs safely interact with on-chain assets—by providing KYC/AML capabilities, reporting tools, and risk dashboards—are increasingly seen as attractive VC targets. This aligns with a broader trend toward "compliance-first, revenue-real" businesses that can withstand regulatory scrutiny and operate profitably even in sideways markets, rather than relying solely on bull market trading volumes.

Infrastructure investments remain critical as well. CV VC’s analysis of 2025 funding trends highlights that venture capital is increasingly concentrating on foundational blockchain technologies rather than speculative assets. This includes L1 and L2 networks, interoperability solutions, data availability layers, security and auditing platforms, and developer tooling. These investments may not produce explosive short-term token gains, but they provide the scaffolding on which higher-level applications—and future revenue streams—depend.

Case Study: Morpho’s USD 175 Million Strategic Round

Morpho, a Paris-based decentralized lending protocol, provides a concrete example of how these strategic shifts manifest in practice. In 2025, Morpho raised a USD 175 million strategic funding round led by marquee firms Paradigm, a16z Crypto, and Ribbit Capital, signaling a high degree of conviction in its long-term potential. Unlike many projects that raised during the previous cycle on the back of loosely defined roadmaps, Morpho secured this capital after demonstrating real traction in DeFi lending, offering users optimized yields by routing liquidity between lending pools and peer-to-peer matches.

The description of Morpho’s raise as a "strategic" round is telling. It implies that investors see more than just financial upside; they view Morpho as a key piece of the future DeFi infrastructure stack. For Paradigm and a16z Crypto, whose brands are closely associated with deep technical research, backing a protocol like Morpho fits a thesis that sophisticated, composable financial primitives will underpin the next wave of on-chain finance. For Ribbit Capital, which has a strong track record in FinTech, the investment reinforces the convergence between traditional financial innovation and decentralized architectures.

Morpho’s round also illustrates the trend toward larger, more concentrated bets on category leaders. Raising USD 175 million in a single round would have been unthinkable for most DeFi projects in earlier cycles; today, it reflects both the scale of ambition and the expectation that regulatory compliance, security, and institutional integration will require significant capital. The presence of multiple top-tier funds at once highlights how cooperative co-investment, rather than purely competitive deal-making, can help de-risk complex, long-horizon projects.

The AI–Crypto Convergence

As AI has captured the imagination of the global venture ecosystem, its gravitational pull has profoundly affected crypto VC. Rather than being eclipsed outright, crypto is increasingly entangled with AI in hybrid business models and shared infrastructure plays.

AI’s Dominance in Global VC

According to an OECD analysis of venture capital investments through 2025, AI firms accounted for about 61% of global VC investment in 2025, absorbing roughly USD 258.7 billion out of a total of USD 427.1 billion. Binance Research has echoed these figures, emphasizing that the scale of AI funding dwarfs most other sectors and has reshaped LP allocation decisions. This dominance reflects not only AI’s broad applicability across industries but also the perception that foundational AI models and infrastructure platforms could generate near-monopolistic returns.

For crypto VCs, AI’s ascent has two direct consequences. First, it makes fundraising more challenging, as LPs with finite risk budgets may prefer to allocate marginal dollars to AI-focused funds. Second, it changes the opportunity set, as many of the most compelling crypto-native opportunities now involve AI components, from autonomous agents transacting on-chain to decentralized compute marketplaces that rent GPU resources.

Competition and Overlap in Crypto VC Dollars

The convergence between AI and crypto is visible not only at the global VC level but within crypto-specific allocations. Silicon Valley Bank’s analysis of the future of crypto notes that VC-backed companies are increasingly merging AI and crypto technologies, and that for every VC dollar invested into crypto companies in 2025, roughly 40 cents goes to firms integrating AI and crypto. Binance Research similarly warns that AI now claims around 40% of "crypto VC treasure," meaning that a significant share of capital nominally allocated to crypto is effectively being channeled into AI–crypto hybrids.

This partial reallocation has both benefits and drawbacks. On the positive side, it pushes crypto founders to think more creatively about how blockchains and tokens can complement AI—providing verifiable data provenance, censorship-resistant compute coordination, or incentive mechanisms for collective model training. On the negative side, it risks crowding out important but less obviously AI-related infrastructure work, as investors chase the latest cross-over narrative. The danger of superficial "AI-washing"—projects adding AI buzzwords without meaningful technical integration—is as real in crypto as in other sectors.

Despite the hype, AI-related assets currently represent a modest share of the overall crypto market by capitalization. Market observers have estimated that "crypto AI tokens" account for only about 2.9% of the altcoin market cap, a small fraction compared with their share of narrative attention. This disconnect suggests that while VCs are proactively positioning for future AI–crypto synergies, the market has yet to fully price in which models will actually capture durable value.

AI–Crypto Hybrid Startups and Protocols

Within this convergence zone, several archetypes are emerging. Some startups are building AI agents that can interact with DeFi protocols, execute trades, or manage on-chain portfolios on behalf of users, using smart contracts as both execution layer and accountability mechanism. Others focus on decentralized compute and storage networks designed to host AI workloads, using tokens as coordination tools to allocate scarce GPU resources. Still others apply machine learning to improve on-chain security—detecting anomalies, preventing fraud, and optimizing gas costs.

These models appeal to VCs because they blend the high-upside potential of both AI and crypto. They also align with the thematic focus on institutional tools and real-world utility, as AI agents and risk models can make crypto systems more accessible and safer for mainstream users. At the same time, they pose new challenges around governance, liability, and regulation, especially when autonomous agents can control significant on-chain value.

For founders and investors, the key question is whether AI–crypto hybrids can transcend buzzwords and deliver measurable advantages over purely centralized or purely on-chain alternatives. The answer will likely vary by use case; in some domains, decentralized verification and token incentives add significant value, while in others, centralized AI services may remain more efficient. Crypto VC’s role is to identify where the combination is genuinely synergistic and to avoid chasing narratives that lack substantive technical or economic foundations.

Crypto VCs are shifting toward FinTech-style investing as token-first exits fade, prioritizing real revenue, payments, trading, and compliance-driven models. Stablecoins and markets now anchor sustainable crypto businesses as fundamentals replace narrative-driven growth.

- 2023-06milestone

Global VC funding falls 48% in H1 2023 despite AI frenzy

- 2023-11governance

DevConnect Istanbul: MakerDAO's Rune Christensen addresses crypto's structural challenges

- 2024-12milestone

Galaxy Digital reports $11.5B crypto VC deployed in 2024, large funds shift to Bitcoin ETFs

- 2025-02governance

Berachain TGE; leaked docs later reveal $25M full refund given to Brevan Howard's Nova Digital pre-launch

- 2025-03milestone

Galaxy reports $4.8B–$4.9B raised in Q1 2025, but MGX's $2B Binance deal accounts for 40% of total

Industry consensus: $13.7B raised in 2024; top crypto VCs publish 2025 outlooks emphasizing user adoption over infrastructure

Dragonfly closes fourth crypto VC fund; Polychain's fourth fund raises $200M with staff restructuring

Power, Incentives, and Critiques of Crypto VC

As crypto VC has matured, debates about its legitimacy, power, and incentive structures have intensified. The sector sits at the center of controversies about token distribution, founder behavior, and the role of large funds in supposedly decentralized ecosystems.

Ownership, Lockups, and the “Top VC = Pump” Myth

In earlier cycles, many token projects allocated large percentages of their supply to private investors and insiders, with relatively small floats available to the public at listing. When coupled with aggressive marketing and short vesting schedules, this setup often created conditions where prices could be driven up quickly, allowing early investors to lock in gains before retail buyers fully appreciated the risks. The subsequent underperformance of most 2025 token launches—roughly 85% of which now trade below their listing prices—has discredited this approach in the eyes of many market participants.

The erosion of the "Top VC = pump" myth is evident in the way traders and analysts discuss new launches. Binance Research notes that the presence of a well-known VC on a cap table is no longer a strong market catalyst and that investors are increasingly demanding evidence of real users, real revenue, and product maturity. Projects that rely predominantly on brand-name backers without articulating a clear path to sustainable economics face growing skepticism. In response, some VCs are voluntarily adopting longer lockups, more transparent disclosures, and governance commitments designed to reassure communities that they are long-term partners rather than short-term speculators.

This recalibration is also informed by better data. Platforms such as AlphaGrowth, which recently launched what it described as the largest combined crypto VC and DAO treasury dataset—tracking over 70,000 deals on the SerenAI payment gateway—are making it easier for analysts and communities to see who owns what, under what terms, and with what vesting schedules. Greater transparency around cap tables and treasury management can help align expectations and discourage practices that rely on opacity.

Founder Secondaries and Downside Protection

Another contentious area involves secondary sales, where founders or early employees sell a portion of their holdings to new or existing investors prior to a traditional exit. In mainstream tech, secondary sales are increasingly common in late-stage companies; in crypto, they have appeared earlier in the lifecycle. Journalistic reporting has highlighted cases where founders of high-profile crypto startups such as Farcaster and Mesh sold USD 15–20 million worth of their shares in Series A or B rounds, demonstrating that early stakeholders can "take some off the table" while the company is still in its formative stages.

Defenders argue that such sales can be healthy, reducing pressure on founders to push for premature exits and allowing them to focus on long-term value creation. Critics worry that large early cash-outs may weaken alignment between founders and later-stage investors or community members, especially if accompanied by generous token allocations and limited vesting. The perception that insiders are de-risking while inviting others to shoulder the remaining risk has fueled broader distrust toward both founders and the VCs who enable such deals.

Structured downside protection for investors has also drawn scrutiny. Some deal terms reportedly give certain VCs the right to reclaim their entire investment if a project’s token underperforms after launch, effectively shielding them from losses while leaving other stakeholders fully exposed. While such terms can be framed as a way to compensate for regulatory or technical uncertainty, they raise questions about fairness and the distribution of risk. For crypto VC to maintain legitimacy, many observers argue, it must avoid arrangements that create asymmetric downside protection for a select few.

The No-VC Counter-Narrative: Hyperliquid and Beyond

In reaction to these dynamics, a powerful counter-narrative has emerged: that the most investable crypto assets may be those that do not have traditional VC backing at all. Hyperliquid, a derivatives exchange and associated crypto asset, has become a prominent example. Grayscale Research has described Hyperliquid as a breakout success in modern digital assets, citing approximately USD 800 million in revenue in 2025 and noting that its token ranks as the eighth-largest crypto asset by market capitalization despite having no venture capital backing. The project remains geoblocked in the United States, underscoring how regulatory constraints can limit access even to some of the ecosystem’s strongest performers.

Former Hyperliquid skeptic Pavel Paramonov has articulated why some investors see its token, HYPE, as uniquely attractive: it is not a stock, offers no formal equity claim or corporate structure, and yet is more than a purely speculative asset because it is tightly linked to the economics of the exchange. HYPE thus occupies a grey zone between equity and utility, with no VC overhang and a token design that emphasizes buybacks and value accrual to long-term holders. For critics of traditional crypto VC, Hyperliquid stands as evidence that community-driven, non-VC-funded projects can achieve both scale and profitability.

The no-VC narrative resonates with a segment of the crypto community that sees venture capital as antithetical to decentralization. However, it also has limitations. Building a complex exchange or infrastructure protocol without VC funding requires either extraordinary early revenue, significant founder capital, or alternative fundraising mechanisms such as fair launches and community pools. These models may not be feasible for more research-intensive projects, especially those requiring years of development before generating cash flow. As with many debates in crypto, the reality is likely to be pluralistic: some of the most important networks may be VC-backed, while others emerge from grassroots efforts.

Navigating Today’s Crypto VC Landscape

For both founders and investors, the current crypto VC environment is more demanding than in prior cycles. Capital is available, but the bar has risen, and strategies must adapt to new realities.

Founders: When and How to Raise

Founders building in crypto today face a series of intertwined decisions: whether to raise VC at all, when to do so, in what structure, and from whom. The appetite for early-stage experimentation has not disappeared, but investors now scrutinize technical clarity, regulatory awareness, and economic design more closely. Seed rounds that once could be raised on the basis of a compelling vision and a short whitepaper now often require prototypes, testnet deployments, or meaningful community engagement.

At the same time, the relative attractiveness of equity versus token funding has shifted. With many 2025 token launches trading below listing prices and public sentiment wary of heavily VC-owned tokens, founders may prefer to delay tokenization until they have a working product and clearer value proposition. Equity-based seed and Series A rounds can provide the runway to reach this point while minimizing the risk of misaligned token incentives. Token warrants or SAFTs can still be part of the package, but their terms and vesting schedules must be designed with community perception in mind.

Choosing the right investors is increasingly about more than brand. Specialized firms like Dragonfly, Paradigm, and a16z Crypto bring deep research capabilities and technical expertise, while corporate investors such as exchanges and stablecoin issuers may offer distribution and regulatory guidance. Founders must balance the benefits of such partnerships against potential conflicts of interest, especially when investors also operate platforms on which the project’s tokens will trade.

VCs: Building a Durable Crypto Franchise

For venture firms, the challenge is to demonstrate that they add value beyond capital in a sector where community trust is fragile. The "mass extinction" of weaker crypto VCs described in reporting around Dragonfly’s Fund IV illustrates how difficult it has become to raise and sustain a dedicated franchise. To survive and thrive, funds must articulate clear theses, develop technical and regulatory expertise, and build reputations for fair dealing with both founders and communities.

Part of this involves adjusting time horizons and expectations. With AI absorbing a large share of global VC attention and crypto regulatory regimes still in flux, some LPs may demand more conservative pacing of deployment and clearer risk management frameworks. Funds that raised large vehicles in 2022 must prove that they can deploy this capital into high-quality opportunities rather than merely chasing the next narrative. Data-driven research from organizations like Galaxy Research and datasets like AlphaGrowth’s 70,000-deal repository can help inform such decisions, enabling more nuanced assessments of market saturation, tokenomics, and competitive dynamics.

Another part involves embracing more transparent and inclusive practices. This can mean publishing token lockup schedules, engaging meaningfully in on-chain governance, and supporting mechanisms that give users and communities a voice in major decisions. It can also mean resisting overly aggressive terms that shift risk disproportionately onto founders or retail participants, in recognition that reputational capital is as important as financial performance in a social, open-source ecosystem.

The Role of Exchanges, Banks, and Data Platforms

Crypto VC does not exist in isolation from other financial actors. Exchanges like Coinbase and Binance, stablecoin issuers, and multi-strategy firms like Galaxy Digital all play multiple roles: they are portfolio companies of earlier VC rounds, direct investors in new ventures, and key infrastructure providers for token liquidity and custody. Corporate venture arms and strategic investment programs run by these entities can complement or compete with independent VCs, offering founders alternatives that may include integration, listings, or co-marketing.

Banks and traditional financial institutions are gradually entering the space as well, often focusing on custody, tokenization of real-world assets, and regulated access products. Their involvement can create exit opportunities for venture-backed startups via acquisitions or partnerships, further intertwining crypto VC with mainstream finance. Meanwhile, research and data platforms—from on-chain analytics to specialized venture datasets—are improving transparency and enabling more sophisticated risk assessment.

In this interconnected environment, founders and investors must navigate not only financial considerations but also ecosystem politics. Aligning with a particular exchange, stablecoin issuer, or financial institution can bring significant benefits but may also foreclose other options. The strategic decisions made at the fundraising stage can therefore shape not just a project’s cap table but its long-term place in the broader crypto economy.

Crypto VC funding swung from a 72% post-FTX plunge to a $13.7B 2024 rebound, with Q1 2025 skewed by a single $2B Binance deal — the underlying deal count recovery is shallower than headline figures suggest.

- Centralization / Insider AllocationHigh

Secret refund arrangements like Berachain's $25M Brevan Howard deal and VC-heavy token unlocks structurally transfer downside risk to public markets while insiders secure preferred exit terms.

Zombie VC funds holding illiquid positions from 2021–2022 vintages remain unresolved, while the rise of founder secondary sales signals that even pre-exit liquidity is being front-run.

Directional tailwinds exist — Japan's legislative change and U.S. ETF approvals drew large capital away from early-stage VC into Bitcoin ETFs — but jurisdiction-level rules for token-based VC returns remain unsettled.

Paradigm's $1B token valuation for Nous Research and Dragonfly's $500M raise during a selective deal environment suggest top-tier funds are still writing large checks into AI-crypto crossover at stretched multiples.

The industry's own 2025 outlook consensus — 'focus shifts to product-market fit and user adoption' — is an implicit acknowledgment that the 2024 cohort was funded before demonstrating sustainable demand.

Retail, Regulation, and Access to VC-Style Returns

Crypto’s promise to "democratize finance" sits uneasily alongside the reality that many of the biggest early gains still accrue to private investors. The interplay between tokens, securities law, and retirement savings is at the heart of ongoing policy debates.

Tokens, Accredited Investors, and Blurred Boundaries

In traditional venture capital, access to early-stage deals is largely limited to accredited investors and institutions, reflecting regulatory judgments about who can bear high risk. Crypto complicates this picture because tokens can, in principle, be traded by anyone with an internet connection and a compatible wallet. When VC-backed projects issue tokens that quickly become liquid on exchanges, retail participants effectively gain access to early-stage, high-volatility assets without the usual protections or disclosures associated with public markets.

The poor performance of many 2025 token launches has highlighted the downsides of this model. Retail buyers who enter shortly after listing may be purchasing from early insiders or VCs at prices that do not reflect long-term fundamentals, particularly when information asymmetries are large. At the same time, some of the most successful assets, such as Hyperliquid’s HYPE token, are not even available to certain jurisdictions: the exchange remains geoblocked in the United States, limiting access for U.S. investors despite its substantial revenue and market capitalization. This creates a paradox where retail investors may have easy access to riskier, lower-quality tokens while being fenced out of some of the strongest performers.

Opening VC to the Masses?

Against this backdrop, policymakers and industry participants are debating whether and how to expand retail access to venture-style opportunities in a more structured way. In public forums, regulators have suggested that retail investors might benefit from exposure to venture capital and crypto assets via vehicles such as 401(k) retirement plans, provided that appropriate safeguards and diversification limits are in place. This reflects a broader concern that restricting high-growth assets to accredited investors entrenches wealth inequality, even as it attempts to protect less sophisticated participants.

Designing such access, however, is complex. Allowing retirement plans to allocate directly to individual tokens or venture-backed startups raises significant questions about valuation, liquidity, and fiduciary duty. Collective vehicles—such as diversified venture funds, public ETFs, or tokenized index products—may offer safer avenues, but they must still contend with regulatory classifications and market volatility. For crypto VC, the key challenge is to explore ways of sharing upside more broadly without exposing retail investors to unmanageable downside.

Institutionalization and the Path Forward

The long-term trajectory of crypto VC points toward greater institutionalization, even as elements of the ecosystem retain an experimental, grassroots character. On one side, large, compliance-first, revenue-generating businesses—particularly around stablecoins, exchanges, and infrastructure—are attracting capital from both venture funds and strategic investors. On the other side, community-driven projects and no-VC protocols like Hyperliquid demonstrate that alternative paths to success remain viable.

In parallel, the integration of crypto into mainstream financial systems—through banks, asset managers, and regulated products—will likely create new exit routes and partnership models for venture-backed startups. If regulators and policymakers choose to expand controlled retail access to venture-style assets, either through tokenization of fund interests or through more flexible retirement plan rules, the boundary between "crypto VC" and "crypto public markets" may blur even further.

The outcome will depend on how well the industry addresses its most pressing challenges: aligning incentives between founders, VCs, and communities; avoiding exploitative structures; and demonstrating that blockchain-based systems can deliver tangible improvements in efficiency, transparency, and inclusion. Crypto VC has the capital and expertise to help realize that potential—but only if it evolves in step with the values and expectations of the broader ecosystem.

Outlook

Crypto venture capital stands at a transitional moment. After a euphoric 2022 peak and a harsh subsequent reset, capital is returning to the sector in significant size, but it is being deployed more cautiously, into fewer and stronger projects. Data showing USD 4.8 billion deployed into blockchain and crypto startups in the first quarter of 2025, equal to 60% of all 2024 capital, underscores the resilience of investor interest when market conditions stabilize. Yet the dominance of AI, which absorbed roughly 61% of global VC in 2025, and the fact that about 40% of crypto VC dollars now flow into AI–crypto hybrids, mean that standalone crypto narratives must compete harder for attention.

The strategic direction of crypto VC is increasingly clear. The "spray-and-pray" model of backing numerous token projects in the hope that a few will spike has given way to a focus on stablecoins, payments, infrastructure, AI agents, and institutional tools—areas where fundamentals can be measured and business models can be scrutinized. Mega-rounds like Morpho’s USD 175 million strategic financing suggest that leading DeFi and infrastructure projects will have ample access to capital, while less differentiated ventures may struggle to raise at all. Meanwhile, no-VC success stories like Hyperliquid illustrate that community-driven, non-traditionally-financed projects can challenge both incumbents and narratives about the necessity of VC.

For founders, this environment demands rigor in both product and token design, careful selection of capital partners, and a willingness to embrace longer timelines to sustainable revenue. For VCs, it requires humility, transparency, and a credible value proposition that extends beyond capital, backed by research, technical expertise, and fair engagement with communities. As regulatory debates continue about how and whether to expand retail access to venture-style returns, the legitimacy of crypto VC will hinge on whether it can align its practices with the sector’s broader aspirations toward openness and shared upside.

If the industry can strike that balance—leveraging venture capital to fund ambitious, socially useful crypto infrastructure while avoiding the excesses of past cycles—it is likely that crypto VC will remain a central force in shaping the evolution of digital assets. Its interplay with AI, stablecoins, and traditional finance ensures that the next decade of crypto investing will be more complex, more interconnected, and, for those who navigate it wisely, potentially more rewarding than any that has come before.

Latest Crypto VC news

Former Hyperliquid skeptic Pavel Paramonov argues HYPE is among crypto's few truly investable assets, citing its no-VC structure, token buybacks and growing challenge to Binance's dominanceDragonfly Fund IV sparks a candid playbook on building a crypto VC, covering fundraising, differentiation, winning deals, and surviving cycles.Crypto VCs are shifting toward FinTech-style investing as token-first exits fade, prioritizing real revenue, payments, trading, and compliance-driven models. Stablecoins and markets now anchor sustainable crypto businesses as fundamentals replace narrative-driven growth.AlphaGrowth launches largest crypto VC and DAO treasury dataset on SerenAI x402 payment gateway with over 70,000 deals trackedVC money is flooding back into crypto, with nearly $25B deployed in 2025—a 150% jump led by Binance, Polymarket, and Circle. Investors are now backing compliance-first, revenue-real businesses as the market matures.VC-backed crypto token launches are failing in 2025, with 85% underwater and the old “Top VC = pump” playbook breaking down as capital dries up and fundamentals start to matter.Sources

- https://www.cvvc.com/blogs/where-vcs-are-investing-in-2025-blockchain-vs-ai-funding-trends

- https://www.oecd.org/en/publications/venture-capital-investments-in-artificial-intelligence-through-2025_a13752f5-en/full-report.html

- https://www.svb.com/industry-insights/fintech/2026-crypto-outlook/

- https://www.dragonfly.xyz

- https://venture5.com/vc-deals/morpho-raises-175m-strategic-funding/

- https://x.com/Grayscale/status/2059641231752433983

- https://www.binance.com/en/square/post/300371481473089

- https://www.binance.com/en/square/post/292907977510146

- https://www.dlnews.com/articles/markets/crypto-startups-raise-883m-in-february/

- https://www.facebook.com/crunchbase/posts/venture-funding-just-hit-a-record-high-but-the-story-underneath-is-far-more-nuan/1417616260399529/

- https://fortune.com/2026/02/17/dragonfly-fourth-fund-crypto-venture-capital-blockchain-polymarket-ethena/

- https://x.com/leviathan_news/status/1999192688579457354

- https://www.coinbase.com/bytes/archive/why-crypto-vc-funds-just-raised-billions

- https://x.com/paramonoww/article/2066471252714528863

- https://x.com/jeffjohnroberts/status/1985381636180209682

- https://www.instagram.com/reel/DXwiV46ubnN/?hl=en

- https://x.com/matthuang

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…