Deep dive on Galaxy Digital’s role in institutional crypto, covering trading, OTC, Solana and Bitcoin products, mining, tokenization, AI payments, regulation and risk to explain how the firm bridges Wall Street and digital assets.

+4 sources across the wider coverage universe

Galaxy Digital says seven Senate Democrats could decide the fate of the CLARITY Act, a key crypto market structure bill facing markup this Thursday2026-05

Galaxy Digital says seven Senate Democrats could decide the fate of the CLARITY Act, a key crypto market structure bill facing markup this Thursday2026-05 Galaxy Digital expands U.S. retail platform with Solana staking, offering up to 6.5% variable APY for passive income2026-04

Galaxy Digital expands U.S. retail platform with Solana staking, offering up to 6.5% variable APY for passive income2026-04 Galaxy Digital confirms testnet breach, no client funds or data compromised2026-04

Galaxy Digital confirms testnet breach, no client funds or data compromised2026-04 Galaxy Digital and DeFiance Capital settle large OTC trade using yield-bearing stablecoin USDO2026-04

Galaxy Digital and DeFiance Capital settle large OTC trade using yield-bearing stablecoin USDO2026-04 Galaxy's latest research finds the x402 standard is turning AI agents into autonomous economic actors that transact in stablecoins over HTTP, positioning blockchains as invisible payment infrastructure for the machine-to-machine economy rather than consumer-facing crypto applications.2026-01

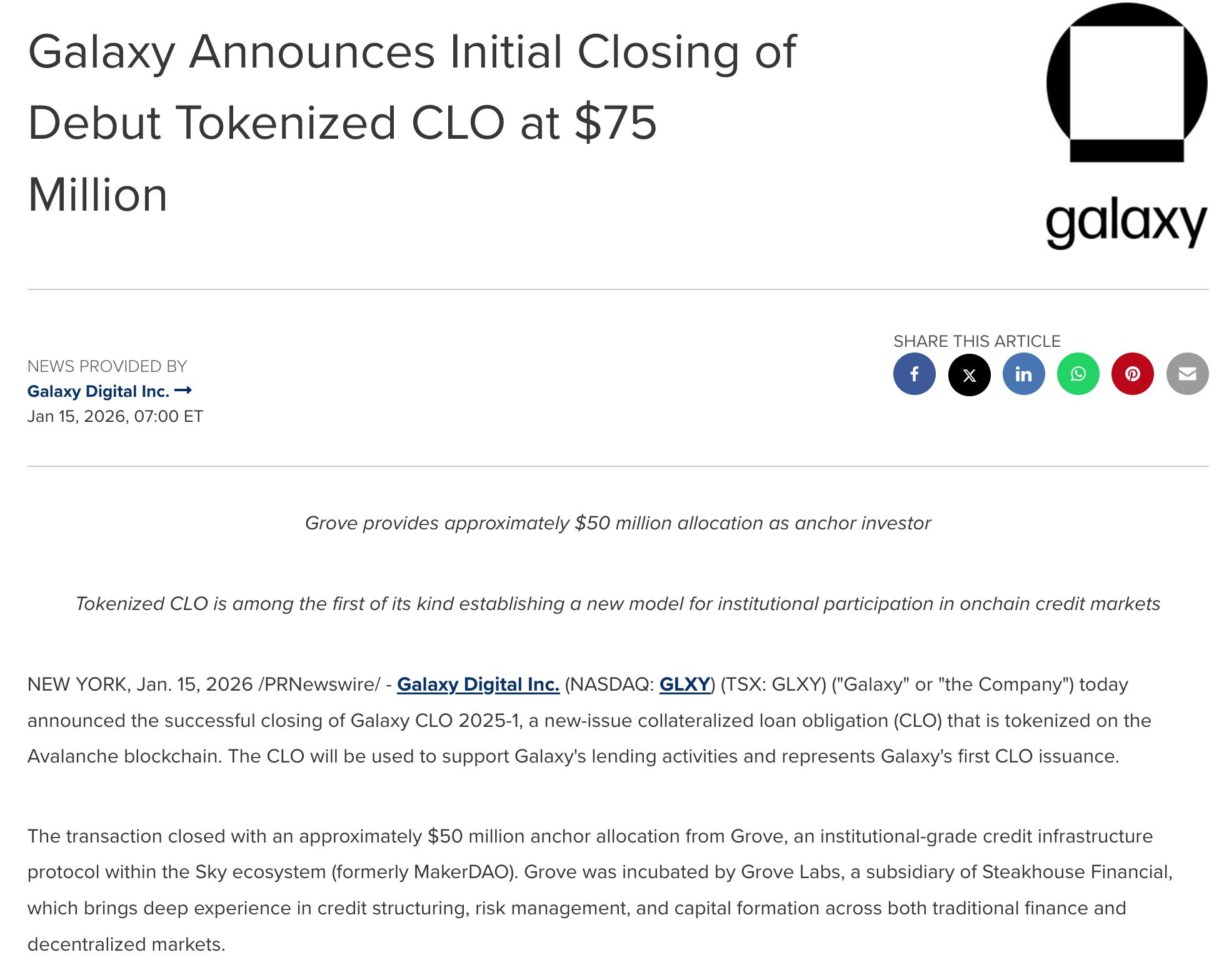

Galaxy's latest research finds the x402 standard is turning AI agents into autonomous economic actors that transact in stablecoins over HTTP, positioning blockchains as invisible payment infrastructure for the machine-to-machine economy rather than consumer-facing crypto applications.2026-01 Galaxy debuts $75M CLO Tokenized fund on Avalanche with Accountable capital data verification network tech2026-01

Galaxy debuts $75M CLO Tokenized fund on Avalanche with Accountable capital data verification network tech2026-01

Galaxy Digital: Institutional Crypto, Infrastructure, and Research Explained

Galaxy Digital is a diversified digital asset financial services and infrastructure firm that focuses on institutional trading, asset management, venture investing, and mining while increasingly positioning itself as a bridge between crypto markets, tokenized traditional finance, and AI infrastructure. Built around Wall Street-style risk management and research but native to Bitcoin, Ethereum, Solana, and broader crypto markets, Galaxy has become one of the key firms shaping how large pools of capital access and structure exposure to digital assets.

Origins and Leadership

Understanding Galaxy Digital begins with its founder and chief executive, Michael Novogratz, whose personal trajectory mirrors the broader migration of talent and capital from traditional finance into crypto. Novogratz is an American investor best known before Galaxy as a co‑founder and former president of Fortress Investment Group, where he also served as chief investment officer of the Fortress Macro Fund, running large global macro strategies. After Fortress, he became an early and vocal investor in Bitcoin and other digital assets, building a reputation as one of the first high‑profile Wall Street figures to publicly commit personal capital and credibility to crypto markets. This combination of macro trading experience and early crypto conviction set the stage for Galaxy’s creation as a firm designed to import institutional standards into a still‑nascent market infrastructure.

Galaxy Digital was founded around 2018, at a time when crypto markets were emerging from the froth of the 2017 ICO boom and beginning to institutionalize. Novogratz’s thesis was that the next phase of growth would require professional trading desks, regulated structures, and research‑driven capital allocation, rather than the retail‑dominated speculative cycles that had characterized earlier eras. The company was structured as a kind of merchant bank for digital assets, combining proprietary trading, principal investments, advisory, and asset management in a single platform that could allocate firm capital alongside client capital. Over time, that initial vision expanded into a multi‑segment operating business, but the core idea—bringing Wall Street disciplines to crypto markets—remains central to the company’s identity.

Novogratz’s public presence has also played a significant role in Galaxy’s brand positioning. He has remained active on social media platforms such as X, where he describes himself succinctly as “CEO, $GLXY. Early investor: #Bitcoin,” signaling both his leadership role at Galaxy and his personal alignment with the asset class. Galaxy itself emphasizes that it was built in New York and is licensed by the New York State Department of Financial Services (NYDFS), underscoring its focus on regulatory compliance and institutional credibility in one of the world’s most demanding financial jurisdictions. In a market often associated with opaque offshore entities and regulatory arbitrage, this emphasis on licensure and transparency is a deliberate differentiator.

The firm’s corporate evolution reflects both strategic opportunism and responsiveness to changing market structure. Initially framed as a diversified financial services and investment management company in the digital asset sector, Galaxy has since broadened into what it now describes as a global leader in digital assets and AI infrastructure. That shift reflects its acquisition of large‑scale data center assets, expansion into Bitcoin mining, and growing focus on providing compute and infrastructure to AI workloads, which increasingly intersect with blockchains and stablecoins as payment rails. Novogratz’s leadership continues to center on navigating these overlapping domains—crypto markets, tokenized finance, and AI infrastructure—while managing the volatility and regulatory uncertainty inherent in all three.

Galaxy Digital says seven Senate Democrats could decide the fate of the CLARITY Act, a key crypto market structure bill facing markup this Thursday

Readers engage Galaxy simultaneously as a credible macro oracle — clicking its VC reports, Bitcoin L2 warnings, and debt alerts — and as a cautionary protagonist, clicking its LUNA settlement and embezzlement scandal with equal intensity, revealing an audience that trusts Galaxy's market calls precisely while suspecting its self-interest.↗

Business Model and Corporate Structure

At its core, Galaxy is best understood as a multi‑line institutional platform operating across trading, asset management, investment banking, principal investments, and digital infrastructure, with a balance sheet that takes both liquid and illiquid risk in the crypto ecosystem. The firm describes itself as a digital asset and blockchain leader that helps institutions, startups, and individuals “shape a changing economy,” language that reflects its dual role as both market intermediary and ecosystem builder. Unlike pure exchanges or single‑product asset managers, Galaxy’s business architecture is deliberately diversified so that it can monetize trading flow, manage third‑party assets, advise on capital markets transactions, and own infrastructure and venture positions that may benefit from long‑term adoption.

Public analyses of the company typically describe three headline segments: trading and brokerage, asset management, and investment banking, with additional contributions from principal investments and mining or digital infrastructure. The trading and brokerage division operates Galaxy’s global markets business, which provides 24/7 electronic and over‑the‑counter (OTC) trading in more than 100 cryptocurrencies, offering deep liquidity and customized execution for institutions that cannot simply trade on retail exchanges. The asset management segment structures and manages funds and exchange‑traded products (ETPs), often in partnership with large traditional asset managers, giving investors regulated vehicles for exposure to Bitcoin, Ethereum, Solana, and other digital assets. Investment banking and advisory services, meanwhile, focus on capital raising, mergers and acquisitions, and strategic advisory for companies and protocols operating in or adjacent to digital assets.

Complementing these client‑facing businesses, Galaxy also runs a principal investment portfolio—including venture capital and strategic stakes—and a mining and digital infrastructure segment that owns and operates data center assets such as its West Texas campus, often referred to as Helios. The Helios facility provides the physical foundation for both Bitcoin mining and AI compute infrastructure, further blurring the line between crypto and broader digital infrastructure. By owning and operating infrastructure while also financing and advising miners and infrastructure startups, Galaxy seeks to capture value along multiple points in the digital asset supply chain. This vertically and horizontally integrated model is unusual compared with traditional financial firms, which often separate trading, asset management, and infrastructure.

The interlocking nature of Galaxy’s business lines can be summarized as follows:

| Segment | Primary Focus | Example Activities |

|---|---|---|

| Trading & Brokerage | Institutional execution and liquidity | 24/7 electronic and OTC trading across 100+ cryptocurrencies; derivatives; hedging |

| Asset Management | Structuring and managing pooled investment products | Bitcoin and Solana‑linked ETPs; multi‑asset funds; passive and active strategies |

| Investment Banking & Advisory | Corporate finance for crypto and infrastructure firms | Capital raising, M&A advisory, strategic consulting for miners and protocols |

| Principal Investments & Ventures | Long‑term strategic and venture capital investments | Stakes in tokenization platforms, DeFi protocols, and infrastructure startups |

| Mining & Digital Infrastructure | Physical and digital infrastructure operations | Bitcoin mining, data center campus in West Texas, AI workloads hosting |

This structure allows Galaxy to deploy its balance sheet and expertise in multiple ways. For instance, when it launched Galaxy Digital Mining as a dedicated business unit in 2021, the firm emphasized that the mining unit would integrate with existing trading, lending, and advisory operations to offer a comprehensive suite of financial services to Bitcoin miners. Those services include trade and risk management solutions, principal lending, equity investments, and M&A advisory, demonstrating how a single vertical—mining—can touch almost every part of the firm’s platform. A miner might borrow capital from Galaxy, hedge price risk through its trading desk, engage in strategic transactions with advisory support, and colocate hardware in a Galaxy‑controlled data center, all under one corporate umbrella.

Running its own book of digital assets on balance sheet further differentiates Galaxy’s model. The firm is not just a neutral agent executing client flows; it is also a risk‑taking entity that holds Bitcoin, Ethereum, Solana, and other assets, as well as equity stakes in startups and infrastructure assets. This merchant‑bank style approach can amplify returns in bullish environments but also exposes the firm to market drawdowns and illiquidity in downturns. Managing this balance between client services and proprietary risk is a central strategic and governance challenge, particularly in a regulatory environment that is still adapting to such hybrid models.

Trading, OTC Markets, and Liquidity Provision

Galaxy’s trading and brokerage operations are often the most visible part of its business, especially to market participants tracking large on‑chain flows and OTC activity. Through its Global Markets division, Galaxy offers institutions 24/7 electronic and over‑the‑counter trading in more than 100 cryptocurrencies, combining algorithmic execution, voice trading, derivatives, and bespoke structured products. For large hedge funds, family offices, miners, and corporates, executing a multi‑million‑dollar Bitcoin or Solana trade on a retail exchange is often impractical due to slippage, market impact, and counterparty risk. Galaxy’s desk exists to intermediate those trades, quoting two‑sided markets and absorbing or laying off risk across its balance sheet and broader liquidity network.

Over‑the‑counter trading is particularly important in this context. OTC trades are typically negotiated bilaterally between a client and a liquidity provider like Galaxy, with bespoke terms on size, price, settlement currency, and timing. This channel is well‑suited to large allocations or exits in less liquid tokens, where public order books would reveal intent or struggle to absorb volume without extreme price moves. Recent on‑chain data and reporting from the news ecosystem, for example, have highlighted Galaxy’s OTC flows in niche tokens such as HYPE, where the firm has been associated at times with both large accumulations and subsequent selling as part of its risk management and client facilitation activities. Such flows illustrate how OTC desks can effectively become the “whales behind the whales,” enabling or accommodating the positioning of large speculators and funds without broadcasting those trades in real time to public markets.

Galaxy’s trading business is not limited to spot crypto assets. It encompasses derivatives and increasingly exotic exposures, including event‑linked contracts that blur the line between traditional financial derivatives and prediction markets. In a notable strategic expansion, Galaxy launched institutional OTC prediction markets trading through its Global Markets desk, initially offering instruments referencing non‑sports event contracts traded on platforms such as Kalshi and Polymarket. These instruments span economic releases, political outcomes, geopolitical events, and other event‑driven scenarios, allowing institutional clients to express views on macro and political risk via contracts that ultimately settle on regulated or semi‑regulated prediction markets. By offering OTC access, Galaxy can provide larger ticket sizes and greater discretion than retail interfaces typically allow, which is essential for funds that need to move tens of millions of dollars without moving the underlying markets or revealing positions.

Early coverage of this initiative noted that Galaxy’s OTC prediction market desk kicked off with a sizable trade—on the order of $10 million—linked to Kalshi markets, signaling that there is institutional appetite for event‑driven exposures when they can be packaged with professional execution, credit, and settlement processes. In practice, these trades may be structured as swaps or forwards where Galaxy intermediates between a client and the underlying venue, handling collateral, margin, and netting. This kind of structuring allows funds that are comfortable with OTC derivatives but unfamiliar with prediction market interfaces to access new sources of uncorrelated risk in a familiar format.

Settlement innovation is another defining feature of Galaxy’s trading operations, particularly as stablecoins and tokenized cash instruments proliferate. In one high‑profile example, Galaxy executed an OTC trade with DeFiance Capital where settlement was conducted using USDO, a yield‑bearing stablecoin issued by OpenEden. In that transaction, Galaxy and DeFiance used USDO not simply as a neutral unit of account but as a settlement currency that accrues yield from underlying tokenized Treasury‑like assets, demonstrating how stablecoins can function as both payment rails and yield‑bearing collateral for institutional trading. For market structure, this is significant: it points toward a future where OTC desks operate on top of programmable money that blurs the line between cash, repo, and short‑term debt, and where settlement currencies themselves carry risk and return characteristics that must be risk‑managed alongside the underlying crypto positions.

The risks inherent in OTC markets are underscored by episodes where counterparties have incurred large mark‑to‑market losses on positions sourced through Galaxy’s trading channels. One widely discussed case involved Multicoin Capital, a prominent crypto hedge fund, which reportedly received more than 338,000 AAVE tokens from a Galaxy OTC wallet over a multi‑week period at an average price around $218 per token, only to be sitting on tens of millions of dollars in unrealized losses as market conditions turned against the trade. While Galaxy’s economic exposure in such transactions may be limited depending on how it hedged or structured the deals, episodes like this highlight how OTC desks sit at the center of concentrated risk‑taking by leveraged institutions. They must therefore manage credit risk, collateral arrangements, and liquidity stress precisely, especially in drawdowns when clients may need to unwind positions into thin markets.

Overall, Galaxy’s trading and OTC business functions as a key plumbing layer in the crypto economy, linking Bitcoin, ETH, Solana, and a long tail of tokens with large pools of institutional capital. Its expansion into prediction markets, use of yield‑bearing stablecoins like USDO for settlement, and facilitation of large directional trades in both blue‑chip and niche assets together illustrate how institutional crypto trading has grown more complex and interconnected. Galaxy’s ability to navigate these markets safely and profitably is central to its franchise value—and a major source of both opportunity and risk.

Asset Management and Investment Products

Beyond trading, Galaxy has built a significant asset management franchise that packages crypto exposures into regulated, scalable products for both institutional and, increasingly, retail investors. Asset management is structurally different from trading: rather than focusing on spreads and flow, it involves designing funds, ETPs, and other vehicles, raising assets, and earning fees based on assets under management (AUM). For a firm like Galaxy, which already has deep markets expertise and corporate relationships, asset management is a natural extension that allows it to monetize research and structuring capabilities at scale.

One of the most visible manifestations of this strategy is Galaxy’s partnership with Invesco, a large global asset manager, on a suite of exchange‑traded products linked to digital assets. A recent example is the Invesco Galaxy Solana ETP (ticker QSOL), which provides regulated exposure to Solana (SOL) while staking its SOL holdings through Galaxy Digital Infrastructure to potentially generate staking rewards for the trust. By staking the underlying SOL, the ETP can capture on‑chain staking yields and treat them as income to the vehicle, thereby enhancing the total return profile relative to a purely passive, non‑staked exposure. Structuring such a product requires not only deep technical integration with Solana’s staking mechanisms but also legal and regulatory work to ensure that staking rewards are handled correctly from a tax and securities law perspective, reflecting the value of Galaxy’s dual expertise in crypto protocols and traditional fund structures.

Staking‑linked ETPs like QSOL illustrate how asset managers are beginning to embed native blockchain features into regulated wrappers. In the Solana ecosystem, staking involves delegating tokens to validators to help secure the network, receiving rewards denominated in SOL in exchange for assuming certain risks such as slashing or downtime. Galaxy’s infrastructure arm works as the staking provider behind QSOL, abstracting away these technical and operational complexities for Invesco and end investors. For institutions that cannot or do not want to hold SOL directly or manage validator relationships, ETPs of this kind provide a familiar instrument that is traded on conventional exchanges but still taps into the economics of proof‑of‑stake networks.

Galaxy has also expanded its reach to individual investors through GalaxyOne, a platform that combines custody, trading, and yield‑generation features. In an important step for its retail‑adjacent strategy, GalaxyOne began allowing eligible users to stake Solana directly in the app, with marketing materials citing variable yields up to around 6.5% annualized based on network conditions. This brings Solana staking into a more consumer‑friendly interface, leveraging Galaxy’s infrastructure and risk controls while demystifying staking as a source of passive income. At the same time, it raises questions about how to communicate staking risks—such as volatility of rewards, smart contract risks in liquid staking derivatives, and the possibility of protocol‑level slashing—in a way that is both compliant and comprehensible to less sophisticated users.

Beyond Solana, Galaxy’s asset management lineup and ambitions extend across Bitcoin, Ethereum, and multi‑asset strategies, often in the form of institutional funds or co‑branded ETPs. In the Bitcoin realm, Galaxy has been involved in various capacities in the broader ecosystem of exchange‑traded products and funds, from research and commentary on spot Bitcoin ETFs to potential future vehicles combining Bitcoin with other assets such as Treasuries or gold. Ethereum‑linked products and strategies similarly build on Galaxy’s trading expertise in ETH and exposure to DeFi yields and staking, though these offerings must navigate the evolving regulatory and tax treatment of Ethereum’s proof‑of‑stake and associated derivative instruments.

A major emerging area of focus for Galaxy is tokenized traditional finance, where instruments like collateralized loan obligations (CLOs), commercial paper, or equities are issued and traded on public blockchains. Galaxy has debuted a tokenized CLO fund on Avalanche, using an on‑chain data verification network to ensure “accountable capital,” meaning that investors and regulators can transparently see positions and cash flows encoded in smart contracts. While details continue to evolve, the broad idea is that tokenizing slices of a roughly \(6 \text{ trillion}\) dollar credit market and placing them on programmable ledgers can enable more efficient distribution, composability with DeFi protocols, and real‑time risk management. Galaxy’s role as structurer and manager in such products reflects its attempt to be at the foreground of real‑world asset tokenization rather than limit itself to native crypto tokens.

Relatedly, the firm has been involved in initiatives to bring tokenized stocks and traditional ETFs onchain, enabling global investors to access vehicles such as the Fidelity Solana fund, BlackRock’s Bitcoin ETF, and various commodity and equity funds via blockchain rails rather than legacy broker‑dealer infrastructure. In this context, Galaxy may act as a liquidity provider, structurer, or partner to tokenization platforms, helping to create secondary markets and manage risks associated with on‑chain representation of off‑chain assets. This direction aligns with the broader industry view—reinforced by Galaxy’s own research—that stablecoins and tokenization will be major drivers of real‑world adoption in the coming cycle.

In sum, Galaxy’s asset management activities span a rich continuum: from straightforward Bitcoin and SOL exposure to staking‑enhanced ETPs, retail staking in GalaxyOne, tokenized credit funds on Avalanche, and potentially tokenized stock portfolios. These initiatives make Galaxy not simply a taker of market structure but a designer of new product categories that integrate crypto, Solana, Bitcoin, ETH, and traditional assets in ways that can be consumed by regulated institutions and, in some cases, retail investors.

Mining, Data Centers, and AI Infrastructure

Galaxy’s mining and digital infrastructure business illustrates how the firm has moved beyond purely financial intermediation into the physical layer of blockchain networks and compute infrastructure. In January 2021, Galaxy announced the launch of Galaxy Digital Mining, a new business unit committed to providing Bitcoin miners with a comprehensive suite of financial services and products. This mining unit was explicitly designed to integrate with the firm’s existing trading, lending, and advisory businesses, enabling Galaxy to offer miners not only access to capital but also trade and risk management solutions, principal lending, equity investments, and M&A advisory services. The underlying logic is that miners are both clients and strategic partners, requiring financing, hedging, and strategic support across their lifecycle.

The mining business also sits atop Galaxy’s ownership of data center assets, most notably the large Helios campus in West Texas that Galaxy acquired and integrated into its operations. West Texas is attractive for energy‑intensive workloads like Bitcoin mining and AI training because of its access to relatively inexpensive electricity, including renewables and curtailed energy that might otherwise go unused. By operating its own facility, Galaxy can control critical variables such as energy contracts, cooling, physical security, and hardware management, and can flex capacity between mining and other high‑performance computing workloads as economics and market conditions evolve. This level of vertical integration—financial services layered on top of owned infrastructure—is relatively rare among institutional crypto firms, which more commonly rely on third‑party miners and hosting providers.

The 2021 launch of Galaxy Digital Mining underscored the firm’s ambition to be more than a passive investor in mining companies. The unit’s mandate includes principal lending to miners, providing them with capital secured by mining rigs or future Bitcoin production, equity investments in mining companies, and advisory roles in mergers and acquisitions as the mining industry consolidates. For example, Galaxy can structure loans where miners post their ASIC hardware or Bitcoin reserves as collateral, while also using Galaxy’s trading desk to hedge coin price risk through futures or options, thereby stabilizing cash flows in volatile markets. Similarly, equity investments and M&A advisory allow Galaxy to help miners scale, merge, or pivot in response to changes in network difficulty, halving events, and regulatory regimes.

Over time, the company has broadened the narrative around its infrastructure business from “mining” to “AI infrastructure,” reflecting the convergence of compute‑intensive workloads across blockchains and machine learning. Galaxy now describes itself as a global leader in digital assets and AI infrastructure, emphasizing that the same data centers used to mine Bitcoin or validate Solana can also be used to host GPUs and AI clusters. This opens a dual‑revenue model: in periods when Bitcoin mining margins are thin, Galaxy can allocate capacity to AI clients; when mining economics improve, it can scale hash rate. The combination also positions Galaxy to benefit from research such as its x402 work, which envisions AI agents transacting autonomously over blockchain rails, creating a natural bridge between the firm’s infrastructure and financial services segments.

The mining and infrastructure segment is not without challenges. Bitcoin mining in particular is highly cyclical, subject to halving‑induced revenue shocks, fluctuating energy prices, and periodic regulatory crackdowns on energy usage or perceived environmental impact. Owning physical infrastructure adds capital intensity and operational risk: hardware obsolescence, cooling failures, and cybersecurity at the facility level can all erode returns if not managed carefully. However, by embedding mining within a broader platform that includes trading, lending, and advisory, Galaxy can partially offset these risks through financial engineering and diversified revenue streams, while also using its infrastructure footprint as a laboratory for the design of new on‑chain and AI‑powered services.

- 01Galaxy research as market signal↗

Readers treat Galaxy's VC funding reports, Bitcoin L2 sustainability warnings, and crypto debt alerts as forward-looking intelligence worth acting on.

- 02NY AG LUNA settlement accountability

The $200M settlement over undisclosed LUNA promotions and profits made Galaxy the subject of the scrutiny it usually directs at others.

- 03Institutional tokenization launches↗

Galaxy's co-ventures — AllUnity euro stablecoin, SWEEP tokenized liquidity fund with State Street, and CLO on Avalanche — signal where institutional crypto product development is heading.

- 04Galaxy ETH-to-SOL portfolio pivot

Swapping $105M ETH for $98M SOL functioned as a public directional bet, making Galaxy's own balance sheet a proxy trade signal for the L1 competition.

- 05Senate bill financial surveillance risk↗

Galaxy's own analysis warning that a crypto Senate bill would trigger the largest expansion of Treasury surveillance since the Patriot Act alarmed readers invested in regulatory outcomes.

- 06Galaxy venture capital deal flow↗

Galaxy's co-investments in Renzo, Parsec, MoonPay, and Sonic Labs position it as a key signal for which infrastructure sectors attract institutional conviction.

Venture Investing, Tokenization, and DeFi Exposure

Galaxy’s principal investment and venture activities extend its reach into the frontier of crypto and tokenization innovation, often in ways that are not immediately visible to public markets but can shape the firm’s long‑term optionality. The company uses its balance sheet to invest in startups, protocols, and infrastructure projects that align with its theses around stablecoins, tokenization, DeFi, and AI, effectively operating as a specialized venture capital investor alongside its other businesses. These investments can take the form of equity, SAFEs, token warrants, or direct token purchases, and often come with advisory or strategic relationships that deepen Galaxy’s influence in specific sub‑ecosystems.

One example from the tokenization space is Tenbin Labs, a project focused on representing financial assets as tokens on public blockchains. Tenbin’s mission centers on building the tooling and standards needed to tokenize instruments such as funds, equities, or credit exposures, making them composable within DeFi protocols and accessible across borders via blockchain settlement. The project has raised around \(7.1 \text{ million}\) dollars, and Galaxy’s participation signals its conviction that tokenization infrastructure will be a critical layer in the next phase of digital asset adoption, especially as more of the \(6 \text{ trillion}\) dollar credit market and other real‑world assets migrate onchain. For Galaxy, backing such platforms is strategic: it creates upstream optionality for future asset management products, trading flows, and advisory mandates.

Galaxy has also led or participated in larger tokenization‑adjacent rounds, such as a \(20 \text{ million}\) dollar investment in Fence, a company aiming to overhaul backend infrastructure for the credit markets. Fence’s focus on modernizing the plumbing of a \(6 \text{ trillion}\) dollar credit market aligns with Galaxy’s tokenized CLO initiative on Avalanche and broader thesis that on‑chain representation of credit instruments will unlock efficiencies in issuance, distribution, and risk management. By anchoring these rounds, Galaxy positions itself as a central node in the emerging real‑world asset (RWA) supply chain, able to connect tokenization platforms with liquidity, institutional investors, and secondary market infrastructure.

DeFi, in the narrower sense of decentralized protocols for lending, trading, and derivatives, is another domain where Galaxy’s venture and trading arms interact. The firm has provided liquidity, structured deals, or held positions in major protocols like AAVE, often via OTC transactions with funds that seek to accumulate or distribute governance tokens without triggering slippage on public markets. The episode in which Multicoin Capital accumulated a substantial AAVE position via Galaxy OTC, only to face steep paper losses as the price fell, illustrates both the depth of Galaxy’s DeFi connectivity and the risks associated with concentrated bets on protocol tokens. In such situations, Galaxy sits at the intersection: it may earn spreads and fees facilitating the trade, while its venture arm may hold equity or token stakes in related projects, amplifying its exposure to DeFi’s boom‑bust cycles.

More speculative or momentum‑driven tokens such as HYPE further highlight this dynamic. Reports of Galaxy accumulating nearly 400,000 HYPE tokens across wallets over short periods, then later unstaking and selling large tranches, suggest that the firm’s trading operations can become deeply entwined with the liquidity and price action of relatively illiquid tokens. Whether Galaxy is acting purely as a market maker fulfilling client demand or also taking directional views, such activity underscores the complexities of managing reputational and market risk in tokens that lack the depth and fundamental grounding of assets like Bitcoin or ETH. For venture and principal investment teams, the question is how to differentiate between durable protocols and ephemeral narratives while still monetizing short‑term flows.

Taken together, Galaxy’s venture, tokenization, and DeFi exposures reveal a firm trying to position itself at the cutting edge of both on‑chain finance and traditional markets modernization. Investments in platforms like Tenbin and Fence, combined with involvement in tokenized CLOs, Solana‑based treasuries, and DeFi protocols, reinforce the themes that appear in its research: that stablecoins, tokenization, DeFi, and AI are likely to drive the next real adoption wave in crypto. The challenge is that being early in these areas often means bearing higher technology, regulatory, and market risks—risks that must be balanced against the advantages of being a first mover.

Galaxy Digital expands U.S. retail platform with Solana staking, offering up to 6.5% variable APY for passive income

Galaxy Digital bringing Solana staking to retail with 6.5% yield is smart timing. People want passive income and SOL staking is a good way

Research, Policy Analysis, and Thought Leadership

A distinctive feature of Galaxy relative to many trading‑centric crypto firms is the depth and visibility of its research operation. Galaxy’s research team produces in‑depth reports across topics such as crypto mining, hedge fund activity, venture capital trends, regulatory developments, and new protocol standards, with the aim of informing both internal decision‑making and external clients. These reports often combine on‑chain data, market intelligence from the firm’s trading and venture arms, and legal analysis, thereby providing a more holistic view than many external research outlets can achieve. For institutions still learning the contours of crypto markets, Galaxy’s research functions as both educational material and marketing for the firm’s broader services.

One strand of Galaxy research focuses on capital formation and venture funding in the crypto and blockchain ecosystem. For example, a Q1 2026 report on crypto and blockchain venture capital found that VC activity cooled in that quarter after a very strong Q4 2025, with roughly \(4 \text{ billion}\) dollars invested across 355 deals, indicating a moderation from peak exuberance while still reflecting substantial ongoing investment. Such data points help institutions calibrate their expectations around growth, valuations, and the maturity of specific sub‑sectors. For Galaxy itself, tracking these flows informs its own venture allocation strategy and advisory pitches to startups and corporates considering token launches or equity raises.

Regulatory and policy analysis is another major area of emphasis. Galaxy’s research team has produced detailed commentary on the CLARITY Act and related U.S. crypto market structure bills, including breakdowns of voting patterns in the House of Representatives and assessments of how proposed rules would allocate jurisdiction between agencies such as the SEC and CFTC. One analysis highlighted that all 216 Republicans who voted supported a key bill, with 78 Democrats crossing the aisle to vote in favor while 134 opposed, underscoring the partisan and intra‑party dynamics at play in shaping the future of crypto regulation in the United States. More recent commentary from the firm has noted that a small group of Senate Democrats—on the order of seven legislators—could effectively decide the fate of the CLARITY Act in committee markup, emphasizing the narrowness of the political margin for major changes to U.S. crypto market structure.

Galaxy has also warned that some proposed Senate crypto legislation, while delivering significant industry wins in terms of legal clarity and broader institutional access, could simultaneously trigger the largest expansion of U.S. financial surveillance since the Patriot Act by dramatically broadening the Treasury Department’s powers over digital assets. In these analyses, the firm walks a careful line, acknowledging that many industry participants are eager for clearer rules while also voicing civil liberties concerns about expansive surveillance and reporting mandates that could capture not just centralized intermediaries but also developers, wallet providers, and potentially smart contract frontends. This stance positions Galaxy not only as a beneficiary of institutionalization but also as a participant in debates about how to balance innovation, consumer protection, and privacy.

On the technology frontier, Galaxy Research has invested heavily in understanding and shaping standards that tie AI and blockchains together. A prominent example is its work on the x402 standard, which defines a way for AI agents to make “agentic payments”—that is, to act as economic agents capable of initiating and receiving payments autonomously—using stablecoins over HTTP. In Galaxy’s framing, standards like x402 allow blockchains to power the payment layer of a machine‑to‑machine economy in which AI agents transact with one another, with humans, and with services, all without crypto necessarily being visible at the user interface layer. Blockchains, in this vision, become invisible backend infrastructure for programmable money and data integrity, while frontend applications look like ordinary web or AI agents.

Galaxy’s research has also synthesized its macro view of the crypto cycle, arguing that even if 2025 was a year of price stagnation or consolidation in some segments, it laid the groundwork for 2026 and beyond by accelerating the development of stablecoins, tokenization platforms, DeFi protocols, and AI integrations. According to this thesis, these four pillars—stablecoins, tokenization, DeFi, and AI—will drive the next real adoption wave, with institutions and large platforms building products that abstract away much of the crypto complexity while relying heavily on blockchains behind the scenes. This narrative is reflected throughout Galaxy’s businesses: USDO‑settled OTC trades, tokenized CLOs on Avalanche, Solana‑based ETPs and treasuries, and AI‑ready data centers in Texas can all be read as concrete cross‑checks of the research team’s thematic calls.

Combined, Galaxy’s research and policy engagement efforts serve multiple purposes. They educate market participants, build Galaxy’s brand as an expert and responsible actor, inform the firm’s own capital allocation, and position it as a stakeholder in legislative and regulatory negotiations. For a crypto news audience, they also provide a rich source of analysis that often shapes how journalists, policymakers, and other firms frame key debates about Bitcoin, ETH, Solana, market structure, and AI‑driven payments.

Regulatory Footprint and Market Structure

Galaxy’s operations are deeply interwoven with the evolving regulatory landscape for digital assets, particularly in the United States and other major financial centers. The firm is publicly listed under the ticker GLXY on the Toronto Stock Exchange, a status that imposes rigorous disclosure and governance requirements akin to those for traditional financial companies. Being publicly traded provides investors a way to gain equity exposure to the digital asset ecosystem through a diversified operating company rather than directly holding volatile cryptocurrencies, while also forcing Galaxy to report its financials, risk management practices, and material events to regulators and shareholders.

In addition to its public listing, Galaxy emphasizes its regulatory licensing in key jurisdictions, notably New York. The firm highlights that it was built in New York and is licensed by the New York State Department of Financial Services, which oversees the state’s BitLicense regime for virtual asset businesses. Securing and maintaining a NYDFS license is non‑trivial, involving stringent requirements for capital, compliance, cybersecurity, anti‑money‑laundering controls, and consumer protection. For institutional clients, particularly those with fiduciary obligations, this licensing provides comfort that Galaxy operates under familiar regulatory oversight rather than exploiting regulatory arbitrage in offshore hubs.

The firm’s regulatory engagement extends beyond compliance into active participation in market structure debates. Galaxy’s analyses of the CLARITY Act and related legislation reflect its interest in how U.S. law will eventually classify and regulate different types of digital assets, intermediaries, and protocols. The CLARITY framework, broadly understood, aims to define which digital assets fall under securities law, which under commodities law, and how centralized intermediaries and decentralized protocols should be treated for purposes of disclosure, registration, and enforcement. As a firm that combines trading, asset management, venture investing, and infrastructure, Galaxy has a strong interest in rules that are predictable, technology‑neutral, and do not unduly burden innovation.

At the same time, Galaxy has been unusually candid in warning that certain legislative proposals could significantly expand U.S. financial surveillance powers. By pointing out that some bills would give the Treasury Department broad discretion to define new categories of “covered” digital asset activities, impose expansive reporting and monitoring obligations, and potentially capture non‑custodial wallets or DeFi interfaces, Galaxy positions itself as an advocate not only for industry growth but also for civil liberties and privacy considerations. This dual stance—seeking legal clarity but wary of overreach—resonates with many in the crypto community but also places the firm in complex dialogues with policymakers who are balancing national security, consumer protection, and competitiveness concerns.

Galaxy’s regulatory posture has concrete implications for its product design. Its OTC prediction markets trading, for example, is restricted to institutional clients and is structured around underlying venues like Kalshi that operate under regulatory frameworks in the United States. This is in contrast to retail‑facing prediction markets that may operate in regulatory gray zones or be accessible only from certain jurisdictions. Similarly, Galaxy’s use of stablecoins like USDO in institutional settlements must account for stablecoin issuer regulation, sanctions compliance, and custody considerations, embedding regulatory risk into product engineering. Asset management products such as the Invesco Galaxy Solana ETP must navigate securities regulations, listing rules, and tax treatment of staking rewards across multiple jurisdictions.

Globally, Galaxy operates in a patchwork of regulatory regimes, from Europe’s Markets in Crypto‑Assets (MiCA) framework to varying regimes across Asia and the Middle East. While details differ, the themes are broadly similar: stablecoins are coming under payments and banking regulation; crypto asset service providers must meet more stringent licensing requirements; and tokenization of traditional securities often falls squarely under existing securities and fund rules, albeit in a new technical form. For Galaxy, the ability to design compliant products and services in this environment is a source of competitive advantage—but also a persistent operational challenge, as it must maintain a large compliance and legal apparatus to keep up with fast‑moving changes.

Galaxy, Solana, and the Multi‑Chain Thesis

Galaxy’s activities illustrate a clear multi‑chain thesis in which Bitcoin, Ethereum, Solana, and other networks each play distinct roles within a broader digital asset system. Bitcoin functions primarily as a macro asset and collateral, Ethereum as a programmable settlement and DeFi layer, and Solana as a high‑throughput, low‑latency platform for trading, tokenization, and consumer‑adjacent applications. Galaxy’s strategic partnerships and product launches around Solana are particularly instructive for understanding how it views the balance of these networks.

The firm’s work with Invesco on the Galaxy Solana ETP, QSOL, is one pillar of this strategy. By offering a regulated exchange‑traded vehicle that holds and stakes SOL via Galaxy’s infrastructure arm, the firm is effectively betting that institutional investors will seek performance and exposure beyond Bitcoin and Ethereum, particularly in assets that power high‑performance smart contract platforms. This is reinforced by Galaxy’s retail‑adjacent offering of Solana staking via GalaxyOne, where users can directly stake SOL and earn variable yields around 6.5%, again leveraging the firm’s validator and infrastructure capabilities. Together, these products create a continuum from retail to institutional access to Solana, anchored in Galaxy’s infrastructure footprint.

Galaxy’s involvement in large Solana‑based treasury and capital market transactions further underscores its conviction. Forward Industries, a Nasdaq‑listed company that reoriented itself into a Solana‑focused treasury strategy, raised a staggering \(1.65 \text{ billion}\) dollar private investment in public equity (PIPE), led by Galaxy Digital, Jump Crypto, and Multicoin Capital, to purchase SOL and establish a corporate cryptocurrency treasury operation. According to SEC filings, Forward intended to use net proceeds primarily to buy SOL for working capital and future transactions, as well as to build its treasury operations. Galaxy’s role as lead investor and adviser in this PIPE demonstrates its willingness to underwrite large, concentrated bets on Solana’s long‑term viability as a core layer in corporate treasury and transactional systems.

However, the subsequent market performance of SOL—at one point leaving Forward sitting on nearly a billion dollars of paper losses—also highlights the risks embedded in such concentrated, novel strategies. For Galaxy, these episodes are double‑edged. On one hand, they showcase its ability to structure and syndicate multi‑billion‑dollar crypto capital raises, putting it at the heart of a new corporate treasury paradigm. On the other, they tie the firm’s reputation to volatile outcomes and raise questions about how to manage concentration and timing risk when orchestrating large treasury shifts into single‑asset exposures.

Galaxy’s involvement in tokenized credit and commercial paper on Solana also fits this multi‑chain thesis. In a landmark transaction, J.P. Morgan arranged a U.S. commercial paper issuance on the Solana blockchain for Galaxy Digital Holdings, with Galaxy itself acting as structurer and Coinbase and Franklin Templeton participating as investors. This transaction, one of the first debt issuances executed on a public blockchain, illustrates why Solana’s throughput and settlement characteristics are attractive for primary issuance and secondary trading of tokenized fixed‑income instruments. For Galaxy, it is both a proof‑of‑concept and a template: the firm can issue or structure debt onchain, distribute it to a mix of crypto‑native and traditional investors, and potentially integrate it into DeFi‑like secondary markets.

Ethereum, by contrast, remains the locus of much of Galaxy’s DeFi and tokenization exposure, particularly on the smart contract side. Lending protocols like AAVE and stablecoin‑centric systems often live on Ethereum or EVM‑compatible chains, and Galaxy’s OTC dealings in governance tokens reflect its continuing engagement with the Ethereum ecosystem. Bitcoin, meanwhile, anchors the firm’s macro and mining businesses, as discussed below. The resulting picture is not one of maximalist allegiance to a single chain but of pragmatic positioning across networks whose technical and economic profiles align with distinct product lines.

For a crypto news audience, the key point is that Galaxy’s actions—Solana ETPs, Solana‑based treasuries and commercial paper, Ethereum DeFi exposure, Bitcoin mining and treasury—are real‑world expression of an institutional multi‑chain thesis. They suggest that large financial intermediaries expect different chains to specialize and that their own businesses will be built to take advantage of those differentiations, rather than expecting a single “winner” chain.

- 2022-05regulatory

LUNA ecosystem collapse; Galaxy held undisclosed exposure and promotion ties

SEC delays Invesco Galaxy Spot Ethereum ETF decision

- 2024-07regulatory

Galaxy settles with New York AG for $200M over LUNA promotions

Galaxy reports $11.5B crypto VC allocated in 2024, down from prior cycle

- 2025-01milestone

Galaxy and Ripple extend $160M lifeline to MoonPay amid Trump memecoin surge

Galaxy reports $4.8B in Q1 2025 crypto VC across 446 deals

- 2025-06exploit

Galaxy confirms testnet breach; no client funds or data compromised

- 2026-01launch

State Street and Galaxy announce SWEEP tokenized liquidity fund on Solana

Galaxy and Bitcoin: Trading, Treasury, and Macro

Bitcoin has played a foundational role in Galaxy’s story from its earliest days, both as an asset on the firm’s balance sheet and as a core trading and mining focus. Mike Novogratz has long been associated with early Bitcoin investing, and Galaxy’s brand has often been aligned with Bitcoin’s institutional adoption narrative. The firm provides deep liquidity in BTC through its Global Markets desk, intermediating flows between miners, exchanges, hedge funds, corporates, and other institutions that view Bitcoin as a macro asset akin to digital gold. Its mining operations further tie Galaxy to Bitcoin’s network security and supply issuance, giving it exposure to block rewards and transaction fees as part of its infrastructure business.

As Bitcoin matures into a macro asset held by corporates, funds, and even nation‑states, Galaxy’s role extends into treasury advisory and product structuring. The firm has been involved in the broader ecosystem of Bitcoin ETFs and ETPs, providing research, market commentary, and in some cases trading support or index services. It also holds Bitcoin on its own balance sheet as part of its treasury strategy, although in recent cycles other entities have at times overtaken Galaxy in aggregate BTC holdings. Coverage of corporate Bitcoin treasuries has noted, for instance, that an entity linked to former president Donald Trump—American Bitcoin—has amassed a larger publicly reported BTC holding than Galaxy, underlining the competitive and symbolic nature of Bitcoin accumulation among public entities.

Galaxy’s trading desk plays a particularly important role during periods of geopolitical stress or macro dislocation. In one episode, Bitcoin whales shifted more than \(223 \text{ million}\) dollars worth of BTC into Galaxy’s channels amid rising tensions in the Middle East and an oil price surge linked to conflict involving Iran, highlighting how large holders may view institutional desks as a safe harbor or execution venue when repositioning in volatile environments. Such flows can reflect a desire for professional risk management, better spreads, or simply a preference to deal with a familiar institutional counterparty rather than retail exchanges that may face outages or liquidity gaps during crises.

The firm’s research and market commentary often frame Bitcoin within a macroeconomic context: as an asset sensitive to real yields, monetary policy, inflation expectations, and currency debasement fears. For institutional allocators, Galaxy can model Bitcoin’s correlation patterns with equities, bonds, and commodities over time, helping to position BTC within multi‑asset portfolios as either a diversifier, an inflation hedge, or a source of idiosyncratic risk. Over shorter time horizons, the trading desk may focus on basis trades, options volatility, and funding rates, while the asset management arm considers how to incorporate Bitcoin into products that meet regulatory and risk constraints.

In parallel, Galaxy’s mining business provides an operational lever on Bitcoin’s economics. By owning and financing miners, the firm can benefit from hash price increases and block subsidy revenues, albeit with exposure to halving events that periodically cut block rewards in half. The interplay between mining and trading can be symbiotic: miners may sell BTC via Galaxy, hedge future production, or borrow against reserves; Galaxy can, in turn, manage its inventory and provide two‑sided markets to other participants. This integrated approach positions Bitcoin not just as a speculative asset for Galaxy, but as a multi‑faceted business domain spanning infrastructure, trading, and advisory.

Risk Management, Cybersecurity, and Operational Resilience

Running an institutionally focused crypto and infrastructure platform at Galaxy’s scale requires sophisticated risk management across multiple dimensions: market, credit, liquidity, operational, legal, and cybersecurity. The cyclical nature of crypto prices, the leverage embedded in DeFi and derivatives markets, and the technical complexity of novel protocols create a risk environment more dynamic than that of many traditional asset classes. Galaxy’s challenge is to harness these dynamics for profit while avoiding catastrophic losses or reputational damage.

In its mining and financing business for Bitcoin miners, Galaxy has articulated a risk management strategy that combines trade and risk management solutions with principal lending and equity investments. For example, when providing loans to miners, the firm may require overcollateralization in the form of mining rigs or Bitcoin reserves, and it may hedge coin price exposure through derivatives. Risk management teams monitor hash rate, network difficulty, and energy prices to assess miners’ ability to service debt, while treasury teams manage the liquidity of underlying collateral. These practices mirror structured credit and commodity finance in traditional markets, adapted to the specifics of proof‑of‑work mining.

Cybersecurity is another critical pillar. Galaxy has acknowledged incidents such as a breach in a segregated research and development testnet environment, which it has stated did not compromise client funds or user information and did not affect core production systems. While such an episode might have been less alarming than a direct hot wallet hack, it underscores the importance of network segmentation, least‑privilege access, and robust monitoring. For a firm that runs trading, custody, and staking infrastructure, segregating testnet and R&D systems from live environments is essential to preventing attack paths from experimental code or unvetted dependencies into production. Publicly disclosing such incidents and the lack of impact on client assets also reflects an understanding that transparency is crucial for maintaining institutional trust.

Galaxy’s involvement in complex OTC structures, yield‑bearing stablecoins, and DeFi interfaces adds layers of operational and legal risk. Using USDO, a yield‑bearing stablecoin, as a settlement currency in OTC trades requires careful management of how yield is accounted for, who bears smart contract and issuer risk, and how these instruments are treated under securities, commodities, and banking rules. When structuring prediction markets‑linked OTC trades around venues like Kalshi and Polymarket, the firm must ensure that contracts are legally robust, that they comply with restrictions on retail access, and that event risk is properly understood and hedged. Similarly, venture or principal investments in DeFi projects can create conflicts of interest if Galaxy is simultaneously a liquidity provider, OTC counterparty, or governance participant.

Episodes like Multicoin’s AAVE losses also highlight the reputational risks associated with being a central counterparty in volatile markets. While Galaxy may not bear the economic loss when clients make directional bets that turn sour, public awareness that such positions were sourced through Galaxy’s OTC desks can create perceptions—fairly or not—about the firm’s role in facilitating risky leverage. This dynamic is not unique to Galaxy; it echoes debates in traditional finance about the responsibilities of prime brokers and structured product desks that serve hedge funds. For Galaxy, maintaining strong risk limits, collateral policies, and suitability assessments is not only a prudential necessity but also a reputational safeguard.

Operational resilience extends to business continuity planning, disaster recovery, and talent management across geographies. Given the firm’s reliance on 24/7 trading systems, staking infrastructure, and data centers, outages can have outsized effects. Redundant systems, geographically distributed operations, and close coordination with cloud and colocation providers are therefore essential. At the same time, the firm must compete for specialized talent in fields ranging from low‑latency trading and cryptography to regulatory law and AI infrastructure, making human capital a key operational risk factor.

In summary, Galaxy’s risk management and operational resilience practices must match the complexity of its business model. Cybersecurity incidents, even when contained, are reminders of a constantly evolving threat environment, while market episodes like DeFi drawdowns test the robustness of credit, collateral, and liquidity frameworks. How effectively the firm continues to manage these risks will significantly influence its long‑term trajectory.

Galaxy Digital confirms testnet breach, no client funds or data compromised

Sub-$10k loss on an isolated testnet is a rounding error, but Galaxy closed the GK8 acquisition for $44M specifically to sell "Impenetrable Custody" to institutional clients — they just onboarded BDACS in Korea and are building out ETF infrastructure. Any breach, even on a sandboxed R&D environment, gives counterparties' compliance teams ammunition to slow-walk onboarding. Network segmentation between dev and prod better be airtight, because every institutional due diligence call Galaxy takes this quarter just got a new line item.

Case Studies: Prediction Markets, Stablecoins, and On‑Chain Credit

Concrete case studies help illustrate how Galaxy’s various lines of business intersect with evolving crypto market structure.

The launch of institutional OTC prediction markets trading is one such case. By enabling hedge funds, family offices, and other institutions to trade large, customized exposures referencing event contracts on Kalshi and Polymarket, Galaxy effectively imported prediction markets into the familiar world of OTC derivatives. An early trade reportedly around \(10 \text{ million}\) dollars in size linked to Kalshi exemplifies how macro or event‑driven funds might express views on U.S. economic data, interest rate decisions, or election outcomes using structures that ultimately settle on regulated or semi‑regulated prediction venues. For Galaxy, this business leverages its existing trading infrastructure, risk management expertise, and regulatory knowledge, while opening a potentially large category of non‑correlated revenue streams. It also raises subtle questions about market manipulation, data integrity, and the interplay between traditional financial markets, political processes, and crypto‑settled contracts.

The USDO settlement trade with DeFiance Capital provides another instructive example of innovation at the intersection of crypto and traditional trading. In that transaction, Galaxy and DeFiance used USDO, a stablecoin backed by tokenized U.S. Treasuries and designed to generate yield, as the settlement currency for an OTC trade. This arrangement differs from conventional stablecoin settlement in that the settlement asset itself accrues income over time, meaning that holding USDO as collateral or settlement could be economically more attractive than holding non‑yielding cash equivalents. From a market microstructure perspective, this could change how desks think about cash management, collateral optimization, and the opportunity cost of margin. From a legal and regulatory standpoint, it raises questions about whether such yield‑bearing stablecoins might be treated as securities or money market fund analogues, and how they should be integrated into risk management frameworks. Galaxy’s willingness to adopt USDO in a sizable institutional trade suggests that it views such instruments as important building blocks of future market infrastructure, even as their regulatory status remains in flux.

The J.P. Morgan commercial paper issuance on Solana for Galaxy Digital Holdings is a third illustrative case. By issuing U.S. commercial paper—a short‑term unsecured debt instrument commonly used by corporates to manage working capital—on a public blockchain, this transaction demonstrated that traditional money market instruments can be tokenized and distributed via crypto infrastructure. Galaxy, acting as structurer and issuer, and investors like Coinbase and Franklin Templeton participating on the buy side, showed that both crypto‑native and traditional firms are willing to experiment with on‑chain debt instruments when the legal, custody, and settlement pieces are in place. Solana’s high throughput and low latency made it a logical choice for the issuance, while Galaxy’s dual expertise in crypto and capital markets allowed it to bridge internal treasury needs with novel infrastructure. Future iterations could see tokenized commercial paper integrated with DeFi protocols, used as collateral in lending markets, or traded in 24/7 secondary markets that blur the line between traditional and crypto liquidity.

Finally, the Forward Industries Solana treasury PIPE illustrates both the potential and peril of ambitious on‑chain treasury strategies. Galaxy and its syndicate partners led a \(1.65 \text{ billion}\) dollar PIPE to fund Forward’s purchase of SOL for its corporate treasury, effectively transforming the company into a publicly traded Solana exposure vehicle. At one point, this strategy left Forward with nearly \(1 \text{ billion}\) dollars in paper losses as SOL’s price declined from peak levels, highlighting the volatility risk inherent in using a single crypto asset as a primary treasury asset. For Galaxy, the deal showcased its ability to arrange enormous capital raises and reshape a company’s balance sheet around digital assets, but it also underscored the need for careful risk disclosure and scenario analysis when structuring such transactions.

These case studies—prediction markets, yield‑bearing stablecoin settlement, tokenized commercial paper on Solana, and a mega‑PIPE into SOL—collectively highlight how Galaxy operates at the frontier of market structure innovation. Each involves blending traditional financial instruments or exposures with crypto rails, crafting new forms of risk, liquidity, and governance that regulatory frameworks are still catching up to.

Galaxy in the Institutional Crypto Landscape

In the broader institutional crypto ecosystem, Galaxy occupies a distinct niche. It is neither a pure exchange like Coinbase, a pure asset manager like some Bitcoin ETF sponsors, nor a pure infrastructure company. Instead, it is a hybrid: part trading shop, part asset manager, part merchant bank, part infrastructure operator, and part research house. This multiplicity allows Galaxy to play several roles—liquidity provider, product structurer, venture investor, policy advocate—often simultaneously, but it also complicates comparisons and valuations.

Partnerships with large traditional financial institutions are a key source of Galaxy’s influence. The Invesco Galaxy ETP lineup exemplifies how the firm can package its crypto and infrastructure expertise into products distributed by a mainstream asset manager with global reach. The J.P. Morgan commercial paper transaction on Solana showcases Galaxy’s ability to collaborate with a top‑tier global bank on tokenization and on‑chain issuance. Participation from firms like Coinbase and Franklin Templeton in that transaction further underscores Galaxy’s embeddedness in a network of both crypto‑native and traditional asset managers. These relationships enhance Galaxy’s credibility and access but also position it as a conduit through which traditional finance can cautiously experiment with blockchain technology.

Galaxy also participates in the emergent world of tokenized equities and funds, where “Wall Street onchain” is becoming a more literal description. Projects that bring tokenized versions of ETFs, individual stocks, and commodity funds onto blockchains—sometimes with the involvement of firms like Fidelity or BlackRock for underlying exposure—require intermediaries that can handle custody, market making, compliance, and sometimes even structuring for the tokenized layer. Galaxy is well‑positioned to play those roles given its combination of trading, custody, and legal expertise, and its participation in tokenized credit and commercial paper signals a willingness to extend that model across asset classes.

At the same time, Galaxy competes and collaborates with other institutional pioneers. Coinbase, for example, has its own institutional trading and custody offerings and a rapidly growing asset management arm, and it participated as an investor in Galaxy’s tokenized commercial paper issuance. Traditional banks like J.P. Morgan, Citi, and others are building their own tokenization platforms and digital asset units, some of which may compete with or bypass intermediaries like Galaxy over time. Hedge funds and proprietary trading firms are also increasingly sophisticated in crypto, sometimes sourcing liquidity from multiple OTC desks, including but not limited to Galaxy.

What distinguishes Galaxy in this landscape is its explicit embrace of a full‑stack approach that ranges from research and policy analysis through trading, asset management, venture, and physical infrastructure. This gives the firm multiple levers to pull as the market evolves: if trading volumes compress, tokenization and AI infrastructure may pick up; if DeFi yields fade, prediction markets or stablecoin settlement could grow; if crypto prices stagnate, tokenized Treasuries and on‑chain credit might provide countercyclical opportunities. The trade‑off is complexity: coordinating across these units, managing conflicts, and maintaining focus is challenging, especially in an environment as volatile and politically contested as crypto.

- RegulatoryHigh

Galaxy settled with the New York AG for $200M over undisclosed LUNA promotional activity and profits, establishing a material precedent for enforcement against institutional promotion of failed assets.

- Reputational / Internal ControlsHigh

Galaxy reported ex-partner Richard Kim for allegedly embezzling $3.67M, and a testnet breach was confirmed in 2025, signaling gaps in both personnel and technical security controls.

- Market / DirectionalMedium

Galaxy's $105M ETH-to-SOL swap and its research dismissing Bitcoin Core governance debates expose concentrated directional bets that could underperform if consensus shifts.

Galaxy's own research flagged crypto debt exploding to $53B in Q2 with onchain loans up 42%, and warned that crypto treasury companies' $100B+ in digital assets hinge on ever-rising equity premiums.

Galaxy's analysis of the Senate crypto bill identified it as potentially the broadest expansion of U.S. financial surveillance since the Patriot Act, a risk that cuts against Galaxy's own client base.

Galaxy's OTC desk settled a large trade with DeFiance Capital using yield-bearing stablecoin USDO, and its institutional co-ventures with Deutsche Bank's DWS and State Street diversify but also concentrate exposure to TradFi partners.

Challenges and Critiques

Despite its advantages, Galaxy faces significant challenges that are important for a nuanced understanding of its role in the crypto ecosystem.

Cyclicality is a core issue. Crypto markets are notoriously boom‑and‑bust, with trading volumes, asset prices, and venture activity often rising and falling together. Galaxy’s Q1 2026 research showing a cooling in crypto VC activity, with \(4 \text{ billion}\) dollars invested across 355 deals versus a very strong Q4 2025, is one data point illustrating how quickly conditions can change. For a firm whose revenues are tied to trading spreads, performance fees, asset management fees, and valuation marks on venture and principal investments, these cycles can lead to significant earnings volatility. While diversification across business lines helps, it cannot fully insulate Galaxy from broad crypto market downturns.

Concentration risk is another concern, especially in relation to large thematic bets. The Forward Industries Solana treasury PIPE is a striking example: by leading a \(1.65 \text{ billion}\) dollar funding round aimed at building a massive SOL treasury position, Galaxy effectively tied its reputation to a high‑beta asset in a relatively concentrated way. When SOL’s price later declined, leaving Forward with enormous paper losses, skeptics questioned whether such aggressive concentration was prudent for a corporate treasury strategy and whether Galaxy and its partners had fully communicated the risks. Similar questions arise around large exposures to DeFi governance tokens or niche assets like HYPE, where Galaxy’s trading flows and potential principal positions can materially influence market dynamics.

Regulatory risk looms large. As Galaxy’s own analyses of the CLARITY Act and other bills emphasize, the U.S. regulatory regime for digital assets is still in flux, and proposed rules could significantly reshape the economics of key business lines. While some reforms could benefit Galaxy by clarifying asset classifications and enabling more mainstream adoption, others—particularly those expanding surveillance and compliance burdens—could increase costs and constrain product design. As a high‑profile, publicly listed firm with deep U.S. ties, Galaxy is more exposed to these developments than offshore or lightly regulated competitors.

Cybersecurity and operational risks remain ever‑present. Even though the firm’s reported breach was confined to a segregated R&D testnet environment, it serves as a reminder that complex organizations with multiple codebases, infrastructure layers, and integrations are continually exposed to evolving threats. Attackers may target not only wallets and exchanges but also tokenization platforms, AI infrastructure, and cross‑chain bridges in which Galaxy plays a role. Maintaining best‑in‑class security is costly and requires constant adaptation.

Finally, there are potential conflicts of interest inherent in Galaxy’s merchant‑bank model. When a firm trades on its own account, manages client assets, invests in startups, advises on capital raises, and runs infrastructure, situations can arise where the interests of one unit diverge from those of another or from those of certain clients. For example, Galaxy might hold a venture stake in a protocol whose tokens it also trades, or it might advise a company on raising capital while simultaneously taking positions in its token or equity. Managing these conflicts requires robust governance, disclosure, and internal controls. While such challenges are common in universal banks and large financial conglomerates, they are relatively new in the context of crypto, where norms and regulations are still emerging.

These challenges do not negate Galaxy’s contributions to the crypto ecosystem, but they underscore the need for critical scrutiny and informed analysis alongside acknowledgment of its innovations. For observers and participants in crypto markets, understanding both the strengths and vulnerabilities of major intermediaries like Galaxy is crucial, especially as these firms become more deeply embedded in systems that handle not only speculative capital but also tokenized real‑world assets and AI‑mediated transactions.

Conclusion

Galaxy Digital occupies a central and multifaceted position in the evolving digital asset landscape. From its origins as a crypto‑focused merchant bank founded by former Fortress macro investor Mike Novogratz, it has grown into a diversified platform that spans institutional trading and OTC markets, asset management and ETP structuring, venture investing, mining and AI‑ready data centers, and a prolific research and policy analysis arm. Each of these segments not only generates revenue but also reinforces Galaxy’s strategic role as a bridge between traditional finance and crypto‑native innovation.

Through its Global Markets desk, Galaxy provides deep liquidity and bespoke execution in Bitcoin, ETH, Solana, and a wide range of tokens, increasingly including event‑driven exposures via OTC prediction markets and settlements using yield‑bearing stablecoins such as USDO. Its asset management franchise, exemplified by partnerships like the Invesco Galaxy Solana ETP and retail‑oriented Solana staking via GalaxyOne, packages complex on‑chain features into regulated, accessible products that can be held in brokerage and fund accounts. Its mining and digital infrastructure segment, anchored by the Helios data center in Texas and the Galaxy Digital Mining unit, links financial services to physical infrastructure and positions the firm for the convergence of blockchains and AI workloads.

Venture and principal investments in tokenization platforms, DeFi protocols, and infrastructure projects align with Galaxy’s research‑driven thesis that stablecoins, tokenization, DeFi, and AI will drive the next major wave of adoption. Investments in platforms like Tenbin and Fence, tokenized CLOs on Avalanche, and Solana‑based treasuries and commercial paper show Galaxy pushing the boundaries of what can be issued, traded, and settled on public blockchains. Its research team amplifies this by providing data‑driven analysis of market cycles, venture activity, regulatory developments, and technical standards such as x402 for AI‑agent payments, while its policy work engages with legislation like the CLARITY Act and debates over financial surveillance.

At the same time, Galaxy’s ambitious, full‑stack strategy exposes it to substantial risks: the cyclicality and volatility of crypto markets, concentration in thematic bets such as Solana treasuries, regulatory uncertainty and potential surveillance overreach, cybersecurity threats, and conflicts of interest inherent in operating as both principal and agent across multiple businesses. Episodes like the Forward Industries SOL drawdown, Multicoin’s AAVE losses, and the testnet breach illustrate the practical realities of these risks and the importance of robust risk management and governance.

For a crypto news audience, Galaxy is thus best understood neither as a flawless champion of institutional crypto nor as a monolithic risk vector, but as a complex, evolving institution whose actions and strategies provide valuable insight into where digital asset markets, tokenized finance, and AI‑enabled financial infrastructure are headed. Its successes and missteps alike offer lessons about how Wall Street and crypto can—and sometimes cannot—be fused into a coherent, resilient financial architecture.

Outlook

Looking ahead, Galaxy Digital is likely to remain a bellwether for several key themes in crypto and digital finance. On the market structure side, the firm’s continued expansion into OTC prediction markets, stablecoin‑based settlements, and tokenized credit suggests that it will play a significant role in defining how institutional capital accesses non‑traditional exposures and uses programmable money. Its success or failure in scaling these businesses will provide important signals about the viability of event‑driven markets, yield‑bearing stablecoins, and on‑chain fixed income as mainstream institutional products.

On the infrastructure and tokenization fronts, Galaxy’s dual focus on data centers and on‑chain issuance positions it to benefit from the convergence of AI and blockchains. If standards like x402 gain traction and AI agents begin transacting autonomously using stablecoins over HTTP, Galaxy’s AI‑ready data centers, tokenized CLO and commercial paper experiments, and research leadership could allow it to capture new forms of fee income and trading flow at the intersection of machine‑to‑machine payments and traditional capital markets. Its continued work with partners like Invesco, J.P. Morgan, Coinbase, and Franklin Templeton will likely shape how quickly and broadly tokenization spreads across equities, credit, and alternative assets.

Regulatory outcomes will be a critical determinant of Galaxy’s trajectory. If legislation like the CLARITY Act and related bills ultimately deliver workable, innovation‑friendly frameworks without excessively expanding surveillance, Galaxy stands to benefit from increased institutional participation and a clearer operating environment. Conversely, if rules become overly restrictive or fragmented globally, the firm may face higher compliance costs and constraints on product design, potentially ceding ground to more lightly regulated competitors. Either way, Galaxy’s dual role as both subject and shaper of regulation will keep it at the center of policy debates.