Deep-dive explainer on what “discount” really means in crypto, covering BTC price dips, Binance fee and yield promos, DeFi referrals, AI token discounts, tax breaks, and buybacks, with a focus on risks, trade-offs and how to evaluate “bargains.”

+11 sources across the wider coverage universe

Aave founder Stani Kulechov dismisses reports of a Payward stake sale at a 70% discount, saying AAVE isn't for sale as DAO revenue tops $134M annually2026-06

Aave founder Stani Kulechov dismisses reports of a Payward stake sale at a 70% discount, saying AAVE isn't for sale as DAO revenue tops $134M annually2026-06 Australia plans to scrap its 50% capital gains tax discount for crypto, replacing it with an inflation-indexed model that could raise investor tax burdens2026-05

Australia plans to scrap its 50% capital gains tax discount for crypto, replacing it with an inflation-indexed model that could raise investor tax burdens2026-05 MARA Holdings sells 15,133 BTC for $1.1B, slashes convertible debt by 30% with discounted buyback2026-03

MARA Holdings sells 15,133 BTC for $1.1B, slashes convertible debt by 30% with discounted buyback2026-03 You Don't Have a Bitcoin Problem. You Have a Psychology Problem.2026-02

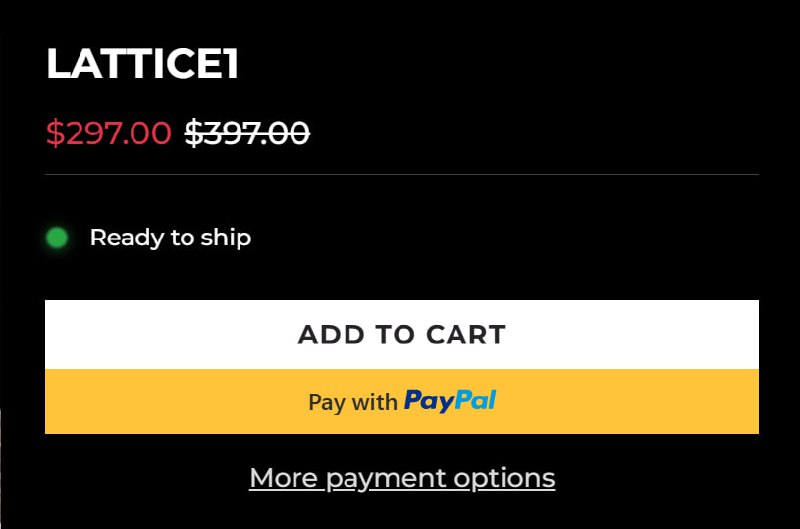

You Don't Have a Bitcoin Problem. You Have a Psychology Problem.2026-02 GridPlus celebrates the Lunar New Year with a sale - a $100 dollar discount on the flagship Lattice1 wallet, with 3 SafeCards, for $297 instead of $397!

Available until February 24th!2026-02

GridPlus celebrates the Lunar New Year with a sale - a $100 dollar discount on the flagship Lattice1 wallet, with 3 SafeCards, for $297 instead of $397!

Available until February 24th!2026-02

Discount in Crypto: An Evergreen Explainer

In digital asset markets, a discount generally means that something is priced below an anchor value, whether that anchor is today’s spot price, a calculated “fair value,” a future payoff, or a posted fee schedule. In crypto, the same word also describes a family of tools and strategies that swap risk, time and liquidity for cheaper prices, higher yields or lower costs, from Bitcoin “buy the dip” narratives to Binance fee reductions and AI-payment promotions.

What “discount” means in crypto

Although traders use the word casually to describe a bargain, the idea of a discount in finance is precise: it is the difference between a value today and a value at some reference point in time or space, often captured through discounting, the process of translating future cash flows into their present value. In traditional finance, this process relies on a discount rate that encodes both the time value of money and the riskiness of the cash flows, with higher risk and longer horizons leading to deeper discounts to today’s value. When the crypto industry borrows this vocabulary, it brings across the same underlying logic: any time you see “discount” in a Bitcoin or DeFi headline, it usually signals some trade-off between price, time, risk and liquidity.

The crypto ecosystem, however, multiplies the contexts in which the term appears. In spot markets, a token or fund might be said to trade at a discount if its price is below its net asset value or below some estimate of intrinsic worth, echoing the way exchange-traded products in traditional markets can trade at a premium or discount to their underlying holdings. In derivatives and yield products, platforms such as Binance now offer Discount Buy structures that promise the chance to purchase crypto below the prevailing market price or earn high annualized yields, explicitly wrapping the concept into product branding. On centralized and decentralized exchanges alike, discounts also appear as fee reductions, often tied to holding a native token, entering a referral code, or hitting volume tiers, as seen with BNB trading-fee discounts on Binance, permanent fee cuts on protocols like Avantis, and promotional offers around PROS- or AVA-based campaigns.

Beyond trading infrastructure, “discount” has become part of how investors talk about cycles in Bitcoin and other major tokens. When commentators describe a selloff as an opportunity for long-term BTC holders to “pick some stuff up on discount,” they are implicitly comparing the current spot price to a higher reference level such as recent highs or their own estimate of Bitcoin’s long-run value. Crypto companies and protocols extend the theme into corporate finance, repurchasing debt or tokens at a discount to face value, as seen in Strategy’s decision to retire a large block of convertible notes below par, or structuring governance and buyback programs to take advantage of depressed valuations. Governments, too, import the language: Australia’s longstanding capital gains tax (CGT) discount for long-held assets has become a flashpoint as policymakers discuss scrapping the 50% reduction for crypto, replacing it with inflation indexation that could shift effective tax burdens for digital-asset investors.

Because of this diversity, understanding discounts in crypto requires a map. There are time-based discounts, where future payouts are worth less today; market-structure discounts, where instruments trade below underlying value; fee and product discounts, where platforms deliberately lower visible costs or prices; and regulatory or tax discounts, where law reduces liabilities for certain behaviors. The common thread is that a discount is never free. It is always paid for—explicitly or implicitly—by taking on risk, enduring constraints, or providing some service to the system, whether that is liquidity, volume, or patience.

To orient that map, it helps to start from the core financial meaning of discounting, then move outward toward its crypto-specific incarnations. Once the time-value-of-money foundation is clear, the various ways Bitcoin, DeFi protocols, exchanges and AI platforms talk about discounts become different applications of the same basic idea: trading something you have now for something you want later, at a price that reflects risk and opportunity cost.

Aave founder Stani Kulechov dismisses reports of a Payward stake sale at a 70% discount, saying AAVE isn't for sale as DAO revenue tops $134M annually

$50M buyback framework against a ~$1.3B AAVE mcap is why the discount rumor had teeth: this isn't a passive governance token waiting for someday value accrual. Aave has already pushed toward surplus distribution via Umbrella, treasury-funded buybacks, GHO revenue, and Chainlink SVR liquidation MEV, so any strategic stake sale would reprice DeFi cash-flow tokens way beyond AAVE. A forced-looking 70% print would have handed bears a comp; Stani killing it fast keeps the valuation debate on protocol economics instead of cap-table distress.

Readers engage 'discount' not as a bargain-hunting signal but as a stress indicator — whether it's a treasury company buying back debt below par, a government repricing crypto tax relief, or a token trading at 70% below fair value, the click is about who is under pressure and who is exploiting it.↗

Discounting and the time value of money

At the heart of modern finance lies the recognition that a dollar today is worth more than a dollar tomorrow, because today’s dollar can be invested, spent, or used as collateral in ways that generate value over time. Discounting formalizes this intuition by converting future cash flows into their present value (PV) using a discount rate, typically expressed through the formula \(PV = \frac{FV}{(1+r)^n}\), where \(FV\) is the future value, \(r\) is the annual discount rate, and \(n\) is the number of years until payment. A higher discount rate or longer time horizon yields a lower present value, meaning the future payoff is more heavily “discounted” when viewed from today.

In traditional settings, the discount rate often reflects both a base risk-free interest rate and compensation for various forms of risk, including credit risk, inflation risk and liquidity risk. When market interest rates rise, discount rates increase, and the present value of long-dated cash flows falls, which is why bond prices drop when central banks tighten policy. Crypto assets, for all their novelty, are not exempt from this logic. Valuations of yield-bearing DeFi tokens, tokenized bonds, and even revenue-sharing governance tokens are, in principle, the discounted present value of expected future cash flows or utility, even if the market narrative tends to focus more on momentum and narratives than on explicit discounted cash flow models.

This discounting framework becomes especially visible in locked or vesting tokens and yield-bearing derivatives. If you hold a claim that will mature into 1 BTC in two years, and your required annual return for bearing Bitcoin volatility and smart-contract risk is 15%, then the maximum you should be willing to pay today is the discounted present value, which would be markedly less than a full bitcoin at spot. In practice, this is what happens when liquid staking tokens or locked-claim derivatives trade at a discount to the underlying asset they eventually convert into, reflecting both time and risk. The same is true for zero-coupon bond-like instruments in DeFi, where a token might promise 1 USDC at a future date but trade below that amount today, the difference being the implied yield you earn by holding.

The time value of money also intersects with the broader macro environment, including the central bank discount rate, which is the interest rate charged to commercial banks on short-term loans from facilities like the Federal Reserve’s discount window. When the Fed raises discount rates or signals caution about reserve availability, as highlighted in its published minutes and surveys of bank treasurers, the overall cost of dollar funding climbs, making speculative assets like Bitcoin relatively less attractive compared with interest-bearing cash and Treasuries. Even though most crypto assets do not have cash flows in the traditional sense, traders implicitly apply higher discount rates to expected future adoption and revenue when risk-free yields are high, which tends to compress valuations.

In crypto corporate finance, discounting shows up in the valuation of convertible notes, treasury reserves and buyback decisions. A firm might issue zero-coupon convertible debt that promises a fixed face value at maturity plus an option to convert into equity if the stock trades above a certain price. If the company’s shares fall well below that conversion threshold, the embedded equity option becomes nearly worthless, and the notes trade at a discount to their par value. When Strategy repurchased a large block of such convertible notes for roughly 1.38 billion dollars against a face value of 1.5 billion dollars, it was effectively exploiting a market discount of about 8% to reduce its liabilities at less than full face value, even as critics debated the trade-off between debt reduction and preserving cash for Bitcoin accumulation. The transaction’s economics are understood by discounting the remaining expected payments under the notes and comparing them with the buyback price.

The same mathematics underlies many yield products marketed to crypto users as high-APR opportunities. When you see an advertised return of 50% annualized on a structured product, as in Binance’s Discount Buy campaigns, the platform is not creating free money but rather compensating the buyer for taking on price risk, path dependency and sometimes illiquidity over a fixed term. That compensation is calculated using a discount rate that embeds expected volatility and the probability distribution of future prices. In other words, the “bonus yield” is the flip side of the discount at which you are willing to commit capital relative to future market uncertainty.

Understanding this time-value foundation does not turn crypto trading into an exercise in textbook finance, but it does provide a common language. Whether you are evaluating a staking derivative trading below par, a token-locked vesting schedule, or a high-yield “discount buy” offer, you are ultimately asking the same question: does the discount offered today adequately compensate me for the time and risk I am taking on?

Market-structure discounts: premiums, NAV gaps and cross-exchange pricing

Beyond time-value considerations, one of the most visible uses of “discount” in both traditional and crypto markets is the gap between an instrument’s market price and its underlying net asset value (NAV). For exchange-traded funds and similar vehicles, the NAV represents the fair value of the fund’s underlying holdings, while the traded price can deviate from this value due to supply-demand imbalances, liquidity conditions and market sentiment. When the ETF’s price is below its NAV, it trades at a discount; when it is above, it trades at a premium. In calm markets, arbitrage via the creation and redemption mechanism usually keeps these deviations small and short-lived, but during stress, prices can drift away from NAV as the ETF adjusts more quickly than underlying markets, or vice versa.

This dynamic has clear parallels in crypto-linked products. Although crypto-specific ETF structures may differ by jurisdiction and asset, the same principle applies: if a fund or trust holds a basket of Bitcoin or other tokens and its shares trade below the market value of those holdings, it is said to be trading at a discount. Investors sometimes interpret such discounts as bargains, but as Fidelity’s discussion of ETF premiums and discounts cautions, persistent discounts can signal structural frictions, low liquidity or market skepticism, and they can widen further, meaning a seemingly cheap entry point may still deliver losses if discounts deepen. For crypto traders, this means that a “Bitcoin fund at a 10% discount” headline is only the starting point; the key question is whether the mechanisms exist for that gap to close and over what horizon.

Discounts also arise across spot markets for the same asset. In a study of cryptomarket pricing, researchers define “Bitcoin discounts” as the ratio between the BTC price on a given market and the volume-weighted average price across all markets, allowing them to systematically measure how much any exchange’s quote diverges from the global norm. They find that these discounts can reflect exchange-specific factors such as local demand, fiat on-ramp constraints, capital controls, or even perceived solvency risk, rather than pure arbitrage opportunities. In extreme episodes, Bitcoin has historically traded at significant discounts or premiums in certain countries relative to global averages, as local traders faced either scarcity of fiat liquidity or difficulty moving capital across borders, creating quasi-segmented markets.

Even within a single currency and jurisdiction, order-book microstructure can create momentary discounts that high-frequency traders arbitrage away. When liquidity thins on one venue, a large market order can temporarily push the price below concurrent quotes elsewhere, creating a fleeting discount that algorithmic traders can capture by buying on the cheap venue and selling on the richer one. Over longer horizons, however, sustained cross-venue discounts may indicate deeper problems, such as withdrawal issues, regulatory uncertainty, or lack of institutional participation on the discounted platform, all of which add risk to attempting arbitrage.

Market-structure discounts also appear in derivatives basis. Futures contracts on Bitcoin and other crypto assets can trade at a premium or discount to the spot price depending on the balance of hedging flows, funding costs and expectations of future price movements. A positive basis, where futures trade above spot, is often interpreted as the market pricing in bullish expectations or reflecting the cost of carrying long exposure, while a negative basis suggests the opposite. Although we do not have a specific source in the search results detailing crypto basis, the logic matches the premium/discount framework of ETFs: the future price is an implied fair value for delivery, and deviations from spot can be thought of as time- and risk-adjusted discounts.

This context is essential when analyzing headlines describing a “Bitcoin discount” in the spot market. When Bitcoin sells off sharply but fundamental narratives remain intact for long-term believers, commentators such as 0xMert have framed the move as capital rotation rather than structural damage, arguing that for investors with a two- to three-year horizon, the lower price represents “a great time to pick some stuff up on discount.” What counts as a discount here is not a gap to NAV or to some mechanical benchmark, but a subjective view of fair value anchored in longer-term adoption and macro theses. For arbitrageurs and quant funds, by contrast, discounts are often defined precisely relative to cross-venue averages, NAV calculations or index levels, as in the cryptomarket discount methodology.

The practical takeaway is that not all discounts are comparable. A 5% discount on one exchange relative to another may be a fleeting microstructure glitch, a 20% discount of a closed-end Bitcoin fund to NAV may be a structural feature that persists for years, and a 30% drawdown in BTC spot may be a discount only if your long-term thesis remains intact. The word is the same, but the economics depend heavily on what the reference value is and how likely it is that the gap will close.

- 01BTC treasury debt buybacks↗

MARA's move to sell BTC and retire convertible notes at a 9-30% discount revealed how leveraged corporate crypto treasuries are actively using market dislocations to restructure balance sheets, not just accumulate.

- 02mNAV discount on crypto companies

GD Culture liquidating BTC to close a widening mNAV discount shows readers are watching the gap between a company's net asset value and share price as a live stress signal for crypto-equity vehicles.

- 03Australia CGT discount removal↗

Scrapping a long-standing 50% capital gains tax discount in favour of an inflation-indexed model is a concrete policy shift that directly reprices the after-tax return on crypto for Australian holders.

- 04Crypto equity buying the dip

Bernstein framing a 60% crash in crypto stocks as a 'big discount' buying opportunity signals institutional analysts treating depressed crypto equities like distressed debt, not speculative growth.

- 05Protocol token stake discounts

Aave's founder publicly dismissing a reported 70% discount stake sale — while citing $134M in DAO revenue — shows that discount rumors around governance tokens are a live threat to protocol credibility.

- 06Exchange fee discount mechanics↗

Binance's time-limited TradFi Perps fee discount and GMX referral rebates reveal how platforms use fee structures as retention levers, making discount terms a competitive battleground for liquidity.

Fee and product discounts: exchanges, referrals and token utility

Where market-structure discounts are emergent properties of trading activity, fee and product discounts are deliberate design choices by platforms competing for users and liquidity. Centralized exchanges, decentralized protocols, and crypto-powered services increasingly use reduced fees, promotional APRs and partnered discounts to attract and retain customers, often tying these benefits to holding or using a specific token.

On centralized exchanges, trading fee discounts are standard. Binance, for example, offers baseline maker and taker fees that can be materially reduced by either holding BNB, the exchange’s native token, or by achieving higher VIP tiers through trading volume. As documented in a comparative analysis of exchange fees, Binance users who pay fees in BNB can receive a 25% reduction compared with standard spot trading costs, while derivatives promotions further adjust maker and taker rates. In a more targeted campaign for USD-margined perpetual futures, Binance announced a limited-time fee structure where all users from regular through VIP 9 enjoy zero maker fees on USD1-margined contracts and reduced taker fees scaled by VIP level, with an additional 10% discount if taker fees are paid in BNB. The resulting fee grid shows regular users paying 0.04% taker fees, while top-tier VIP 9 users pay as little as 0.0094%, or even less when combining BNB payments.

DeFi protocols mirror and extend this logic. Avantis, a derivatives venue built on the Base network, offers perpetual contracts across cryptocurrencies, foreign exchange pairs and commodities, and uses a referral-based fee discount to bootstrap liquidity. Traders who apply the referral code “rebate” before creating their account lock in a permanent 15% discount on all trading fees, with the discount applied automatically at the protocol level each time a position settles. Unlike many centralized promotions, this discount has no volume thresholds, expiry dates or token-holding requirements: from the first trade onward, the user pays only 85% of the standard 0.08% round-trip fee on crypto perps, effectively reducing it to 0.068%. Collateral and settlement are denominated in USDC, tying the promotion directly to stablecoin-based activity and reinforcing the role of USDC as a base currency in DeFi fee structures.

The same mechanism appears in token-utility programs where holding or using a token unlocks discounts beyond trading fees. Travala’s AVA ecosystem, for instance, provides Smart Membership tiers that confer both upfront Smart Discounts at checkout and post-transaction givebacks in AVA, Bitcoin or travel credits when booking services such as car rentals. Even users at the free Basic tier are eligible for car rental givebacks, while higher membership levels scale the percentage of discounts and givebacks, effectively rewarding deeper engagement with the token and platform. Complementing this, a Kraken trading campaign tied to AVA offers a 100,000 AVA prize pool and discount vouchers worth 100 dollars for travel bookings on Travala for the top thousand traders, blending trading activity with real-world travel discounts.

Other projects target vertical-specific discounts in sectors like AI. The PROS token, for example, has been integrated into an AI model-as-a-service platform where users can pay in PROS and USDC to access models such as Gemini, Claude, ChatGPT, Qwen and DeepSeek, receiving an exclusive 20% discount on payments made with PROS during a launch month promotion. This turns PROS into a kind of discount token within an AI economy, aligning incentives for token adoption with demand for compute-intensive services. In practice, such arrangements make PROS a lever for reducing the cost of AI inference, while embedding the token into a broader RealFi narrative that links DeFi capital to real-world economic activity.

Even hardware and community projects leverage discounts to reward early supporters. The DogeBox1 device launch, for instance, limited to a hundred units worldwide, invited users to complete early supporter quests to earn perks such as a private early access window, priority purchasing rights, and an instant twenty-dollar discount on the device’s eventual public sale price. Similarly, conferences like BTC Prague have partnered with travel and service providers to offer attendees fixed-dollar discounts on flights, hotels and activities when booked through official channels, effectively turning brand partnerships into concrete price reductions for Bitcoin enthusiasts.

These fee and product discounts serve multiple strategic purposes for platforms. First, they act as customer acquisition tools, making it cheaper to test a new venue or service, particularly in saturated markets where many exchanges offer similar core functionality. Second, they weaponize token utility, using discounts to create demand for holding and spending native tokens like BNB, AVA or PROS. Third, they can be tuned dynamically: promotions like Binance’s USD1 maker-fee waiver or PROS’s launch-month AI discount are explicitly time-limited, enabling platforms to boost volume around product launches or market campaigns. From a user perspective, however, the proliferation of discounts can be confusing. A 15% lifetime trading fee reduction, a 25% BNB fee discount, and a 50% APR on a structured product are not directly comparable; each embeds different forms of risk, lock-up, and behavioral expectations.

For traders and long-term investors, the key is to recognize that fee discounts, while attractive, seldom change the fundamental economics of trading strategies by themselves. A 15% cut on a 0.08% fee is meaningful for high-frequency activity but marginal for infrequent swing trades. Conversely, extremely high promotional APRs, such as “up to 50%” on some structured products, usually compensate for taking on non-trivial tail risks. Evaluating these offers requires the same rigor as evaluating any other discount: understanding what you give up in exchange for what you save.

Structured “Discount Buy” products and yield trade-offs

Among the most explicit uses of the term in product branding is Binance Earn’s Discount Buy, a family of structured products that give users the possibility either to accumulate crypto at a lower-than-market price or to earn elevated yields if the market moves in their favor. During promotional periods, Binance advertises annualized percentage rates (APRs) of up to 50% for participants who subscribe to Discount Buy products, subject to market performance and specific settlement conditions. In parallel, the exchange has layered on gamified campaigns such as a leaderboard that ranks participants by their average Discount Buy subscription amount, offering top users rewards worth up to 888 USDC in the form of additional Discount Buy subscriptions.

Mechanically, each Discount Buy position is defined by a target buy price, a knockout price, a settlement date and a notional amount, typically denominated in stablecoins like USDT or USDC. At settlement, three main outcomes are possible. If the underlying asset’s price at settlement is at or above the knockout level, the user’s principal is returned in stablecoins along with interest computed from the specified APR, effectively mimicking a high-yield savings product over the term. If the settlement price falls between the target buy and knockout levels, half of the user’s principal is used to purchase the crypto asset at the agreed target price, while the remaining half, kept in stablecoins, accrues interest at a high average APR, reflecting the partial risk taken. Finally, if the settlement price is at or below the target buy level, the user’s full principal is used to purchase the crypto asset at the target price, with no additional yield.

Binance provides a formula for calculating the effective APR in the intermediate scenario, where only part of the capital is converted to crypto. The APR is effectively proportional to the difference between the knockout and target prices divided by the target price and scaled by the duration of the product, leading to average APRs that can exceed 100% on an annualized basis in some configurations, albeit over very short holding periods. These eye-catching yields stem from the fact that the user is implicitly selling optionality to the platform: they give Binance the right to decide, at settlement, whether to return principal plus yield or to deliver discounted crypto instead, depending on where the market settles relative to the preset levels.

From a risk perspective, Discount Buy products can be interpreted as variants of cash-secured put writing, a classic options strategy where an investor agrees to buy an asset at a strike price below the current spot in exchange for receiving option premium upfront. If the asset remains above the strike, the investor keeps the premium and never buys the asset; if it falls below, they are obligated to buy at the strike, effectively “catching a falling knife” at a predetermined level. The “discount” in Discount Buy is that strike price below current spot, which is attractive only if the investor truly wants to own the asset at that level and is comfortable with further downside risk beyond it. The advertised APRs correspond to the option premium earned for taking this conditional obligation.

The USDC-denominated leaderboard rewards add another layer of incentive. By ranking users based on their average Discount Buy subscription amount, recalculated using a duration-adjusted formula that normalizes different product tenors to a 30-day equivalent, Binance encourages larger and longer commitments of capital. Rewards are paid out as additional Discount Buy subscriptions with fixed durations, rather than unrestricted cash, further reinforcing engagement with the product line. For participants, the potential to earn up to 888 USDC worth of Discount Buy subscriptions is meaningful, but it should be weighed against concentration risk: pursuing leaderboard status may lead users to allocate outsized portions of their stablecoin holdings to path-dependent structures instead of more flexible instruments.

Crucially, the word “discount” in this context does not guarantee a bargain in the colloquial sense. If Bitcoin’s price falls sharply below the target buy level by settlement, the user ends up owning BTC at a price that is higher than the market, despite technically acquiring it at a discount relative to its level when the product was initiated. The discount is defined relative to the initial spot price, not the eventual market trajectory. Additionally, because the payoff profile is asymmetric—limited upside via fixed APRs, but potentially large downside if the asset collapses—Discount Buy products are best suited to investors who both desire downside exposure at the target price and understand how sold optionality can amplify losses in tail scenarios.

For experienced traders, such structures can be useful for expressing limit-bid strategies in a yield-enhanced way: instead of posting a spot limit order at a desired purchase price that may or may not be filled, the investor enters a Discount Buy that either yields interest or fills the purchase at that level, depending on realized prices. For less sophisticated users, however, the marketing focus on high APRs and the notion of buying coins at a discount can obscure the risks. As with any discount in crypto, the critical question is what is being exchanged for that favorable price: in this case, it is the user’s willingness to bear downside volatility over a fixed time window and to have their capital locked in a pre-committed payoff structure.

- 2026-01regulatory

US Federal Reserve publishes minutes of discount rate meetings (Jan 20 & 28)

- 2026-02milestone

GridPlus Lattice1 hardware wallet offered at $100 discount until Feb 24

MARA Holdings sells 15,133 BTC for $1.1B, retires convertible debt at up to 30% discount

Binance Futures TradFi Perps fee discount programme extended through March 31

- 2026-03milestone

Bernstein publishes note calling 60% crypto equity crash a rare discounted entry point

- 2026-04governance

Aave founder publicly denies Payward stake sale at 70% discount; cites $134M DAO revenue

Australia announces proposal to scrap 50% CGT discount for crypto, replacing with inflation-indexed model

- 2026-06milestone

GD Culture announces BTC liquidation to fund share repurchase as mNAV discount widens

Asset-price discounts and “buying crypto on sale”

Outside structured products, the most intuitive use of “discount” for many retail participants is straightforward: when Bitcoin or another major crypto asset drops significantly from recent highs, enthusiasts describe it as “trading at a discount” or being “on sale.” This framing hinges on the idea that there is some reference value—perhaps the last bull-market peak, a moving average, or a fundamental valuation model—against which the current price looks cheap. When prominent commentators such as Mert argue that a sharp Bitcoin selloff is “just capital rotation” and that investors with a two- to three-year horizon may find it “a great time to pick some stuff up on discount,” they are appealing to this narrative of temporary mispricing relative to long-term fair value.

In practice, whether a drawdown constitutes a genuine discount depends on both one’s time horizon and the validity of the underlying thesis. A 30% decline from a local high might be a bargain if Bitcoin adoption, regulatory clarity and macro tailwinds continue to improve, but it could equally be a prelude to deeper losses if structural headwinds intensify. Crypto markets are notorious for long bear phases where assets that look “cheap” relative to previous cycles keep falling as liquidity dries up and narratives shift. Historical examples include altcoins that never revisit their prior peaks despite appearing deeply discounted for years, underscoring that discounts relative to past prices are not guarantees of mean reversion.

Whale behavior often reinforces the discount narrative. Stories of large investors who manage to rotate hundreds of millions of dollars’ worth of assets into stablecoins or other hedges ahead of crashes, only to buy back more Bitcoin or Ether at steep discounts, are staples of on-chain analysis coverage. Such trades hinge on timing market cycles and exploiting liquidity pockets; the “discount” captured is the difference between the price at which risk was shed and the lower re-entry price. For smaller investors watching these moves, the temptation is to mimic the behavior, but without access to the same tools, information and execution quality, attempts to “trade the discount” can easily backfire.

Cryptomarket discounts across exchanges add another dimension to asset-price discounts. If BTC trades at a lower price on one venue than another because of temporary imbalances or structural frictions, a sophisticated arbitrageur can buy at the cheaper exchange and sell at the richer one, crystallizing a risk-limited discount capture. Yet this is rarely feasible for typical users, particularly when the discounted venue has withdrawal constraints, higher counterparty risk, or capital controls. In such cases, the discount reflects embedded risk and friction, not a free lunch. An exchange that offers persistently lower BTC prices may simply be pricing in a higher probability of default or regulatory crackdown, making the apparent bargain a poor trade-off once those risks materialize.

For listed companies heavily exposed to Bitcoin, such as Strategy, asset-price discounts also intersect with corporate balance sheets. When the BTC price falls below a firm’s average acquisition cost, its Bitcoin treasury trades at an accounting loss relative to cost basis, even if the company does not mark holdings to market in certain jurisdictions. For managers committed to long-term accumulation, such as Michael Saylor’s team, these drawdowns can be framed as opportunities to acquire additional BTC at a discount relative to their historical average, assuming the long-run thesis remains intact. However, if the company simultaneously uses cash to repurchase its own debt at a discount, as Strategy did when buying back zero-coupon convertible notes below face value, it faces a capital allocation choice: deploy liquidity to capture discounts in its liabilities, in its Bitcoin purchases, or both.

In crypto corporate finance more broadly, buybacks at a discount have become a recurring theme. DeFi-focused public companies that repurchase convertible bonds or equity when trading significantly below their assessed intrinsic value are effectively telling the market they believe their own securities are underpriced. When these buybacks are funded without impairing operational liquidity, they can be accretive to remaining shareholders. Conversely, if repurchases at a discount are financed by selling core assets such as Bitcoin or by overleveraging, they may weaken the firm’s long-term position even if they capture a short-term valuation gap. The discount, in other words, is real only if it does not compromise the issuer’s resilience.

For individual investors deciding whether to “buy the dip,” the lesson is to distinguish between headline discounts and structural value. A discount relative to last month’s price is not the same as a discount relative to sustainably growing cash flows, improving network effects, or robust governance. In many cases, what appears to be a bargain may instead be a justified repricing of risk. Anchoring on previous highs or promotional narratives can make normal volatility look like opportunity, when in fact it might be a warning. Treating discounts as hypotheses rather than facts—questions about value rather than assertions about cheapness—is a more robust approach in crypto’s notoriously noisy markets.

Corporate, tax and regulatory discounts

Beyond markets and products, the notion of discount shapes how legal systems and corporate strategies interface with crypto. One prominent example is the capital gains tax (CGT) discount for long-held assets in Australia, which has long offered individuals a 50% reduction in taxable capital gains on investments held for more than twelve months. In the crypto context, this meant that long-term holders of Bitcoin and other digital assets could effectively halve their taxable gains compared with short-term traders, provided they met holding-period requirements and other criteria. This tax discount rewarded patience and encouraged investors to treat crypto as an investment asset rather than a speculative trading chip.

Recent policy discussions, however, have targeted this discount. Proposals highlighted by tax tools and social-media commentary suggest that Australia may scrap the 50% CGT discount for crypto and other investments, replacing it with a system of inflation indexation starting in July 2027. Under inflation indexation, the cost base of an asset is adjusted upward over time by official inflation measures, so that only real gains above inflation are taxed. While this change would protect investors from paying tax on purely inflationary nominal gains, it could also increase the effective tax burden on high-return assets like crypto if real gains remain large relative to inflation, especially compared with the prior regime’s blunt 50% discount. For Bitcoin holders, the shift would alter the calculus of long-term holding versus more active management, making careful record-keeping of transaction dates and inflation indices essential.

The broader concept of discount also appears in takeover bids and valuation disputes involving crypto-adjacent firms. When Rezolve AI made a stock-for-stock acquisition proposal to buy Commerce.com at an exchange ratio that implied a value below Commerce’s prevailing market price, the target’s board characterized the offer as being at a discount to current trading levels and described it as “deeply discounted” relative to what they saw as the company’s prospects. Such language reflects the practice in mergers and acquisitions of comparing bid prices not only to last traded prices but also to longer-term averages, analyst valuations and strategic value assessments. For shareholders, accepting a discounted bid can be rational if they believe the stand-alone value of the company is lower than the market implies, while boards often resist such offers when they see them as opportunistic attempts to capture temporary weakness.

In the regulatory sphere, the central bank discount rate and discount window may appear distant from crypto, but they indirectly shape digital-asset valuations. The discount rate is the interest rate at which commercial banks can borrow reserves from a central bank facility like the Federal Reserve’s discount window, and its level and usage patterns offer insights into broader liquidity conditions. Surveys and minutes released by the Fed on banks’ use of the discount window and their reserve management strategies shed light on how much stress or caution exists in the banking system. During periods when discount rates are high or banks are reluctant to tap the window, dollar funding becomes more expensive, contributing to risk-off behavior that can spill into crypto as investors rotate into safer assets.

Conversely, when discount rates are low and liquidity is abundant, speculative assets such as Bitcoin often benefit as investors search for yield and capital gains in riskier markets. Although crypto markets can and do move independently of traditional indicators, the opportunity cost of capital—the return forgone by holding non-yielding assets like BTC instead of interest-bearing cash or bonds—is heavily influenced by central bank policy. In effect, the discount rate informs the discount factor that investors implicitly apply to the uncertain future payoffs of crypto adoption and innovation. A higher risk-free rate increases that discount, all else equal, compressing valuations.

At the intersection of corporate finance and regulation, buybacks at a discount illustrate how firms navigating public markets and crypto exposure use discounts strategically. Strategy’s repurchase of its 0% Convertible Senior Notes due 2029 at roughly 92 cents on the dollar represented a classic liability management exercise: the company reduced its outstanding debt by 1.5 billion dollars of face value while paying only about 1.38 billion in cash, capturing an 8% discount that accrues to equity holders and creditors by lowering leverage without resorting to Bitcoin sales. Observers noted that the notes were trading at a discount primarily because the company’s stock price had fallen well below the notes’ conversion price of roughly 672 dollars, rendering the embedded equity option nearly worthless and leaving the notes behaving like discounted straight debt.

For creditors, such repurchases at a discount can be positive, as they reduce default risk and clarify capital structure, while for shareholders, they raise questions about optimal capital allocation—whether the cash used would have generated more value if deployed into additional BTC buys at what some see as a price discount. Similar patterns appear in DeFi companies that repurchase convertible instruments or tokens at heavy discounts, such as the reported 41% discount in a DeFi Development Corp convertible buyback. The fundamental trade-off is consistent: capturing a discount on liabilities or equity can be accretive, but only if it does not undermine operational flexibility or long-term strategic positioning.

These corporate and tax examples underline a recurring theme: discounts are policy tools and strategic levers, not just market accidents. Governments use tax discounts and central-bank rates to shape behavior and allocate risk; companies exploit discounts in their securities to manage capital structure; boards invoke discount language to defend or contest takeover bids. For crypto participants who often focus mostly on token prices and protocol yields, paying attention to these higher-level discount mechanisms can provide important context for how the broader financial system and corporate actors respond to and influence digital-asset markets.

Australia's proposal to replace the 50% CGT discount with an inflation-indexed model could materially increase tax burdens on crypto holders and set a precedent for other jurisdictions to revisit legacy crypto tax concessions.

Tokens trading at 90% discounts to implied fair value signal acute liquidity crises where forced sellers overwhelm buyers, creating cascading repricing across correlated assets.

Corporate treasuries that fund debt buybacks by selling BTC concentrate liquidation pressure in spot markets; a simultaneous sell from multiple leveraged treasury vehicles could amplify discounts self-reinforcingly.

- CentralizationMedium

A single company securing 7,000+ BTC as the world's largest public treasury while 'mining and buying at discount' concentrates supply-side leverage in a way that can move market prices on exit.

- Smart-contractLow

Fee discount mechanisms in DeFi protocols such as GMX referral rebates and Avantis staking tiers are straightforward on-chain logic with limited attack surface compared to lending or bridge contracts.

- GovernanceMedium

Rumoured stake sales at steep discounts — as seen with the reported Payward-AAVE deal — can fracture DAO confidence and trigger governance votes that alter tokenomics under duress, even when the sale is denied.

How to evaluate discounts in a crypto context

Given the myriad ways “discount” is used around Bitcoin, DeFi and AI-linked tokens, a structured approach to evaluation is essential. A helpful starting point is to classify any given discount along two axes: what is being discounted (price, fees, taxes, or time) and what risk or constraint you are accepting in exchange. The table below provides a high-level comparison of common discount types in crypto.

| Discount type | Reference value | Typical vehicle or setting | Main risk or trade-off |

|---|---|---|---|

| Time-value discount | Future cash flows | Locked tokens, zero-coupon claims, bonds | Market, credit, smart-contract and duration risk |

| Market-structure discount | NAV, index or cross-venue average | ETFs, trusts, exchange spreads | Liquidity, structural, counterparty and basis risk |

| Fee / product discount | Standard fee or posted price | Exchange trading, AI services, travel, hardware | Usage commitment, token exposure, promotion expiry |

| Tax / regulatory discount | Statutory rate or rule | CGT discounts, incentives | Policy change risk, compliance complexity |

| Corporate finance discount | Face value or assessed intrinsic value | Convertibles, equity and token buybacks | Liquidity, leverage and execution risk |

A time-value discount is present whenever you buy a claim on future tokens or cash at a price below the eventual payout. Evaluating such discounts involves comparing the implied yield to alternative uses of capital, factoring in both the duration and the full spectrum of risks, from smart-contract vulnerabilities to market volatility. If the implied annualized return on a locked 1 BTC claim is only slightly above the risk-free rate while requiring you to bear large crypto price swings, the discount may be inadequate; conversely, if it offers a generous yield but relies on a fragile protocol, the risk may outweigh the reward.

Market-structure discounts demand scrutiny of liquidity and mechanisms for convergence. An ETF-style product trading at a discount to NAV may never fully close the gap if the structure lacks efficient creation and redemption mechanisms or if demand remains weak. Cross-exchange discounts can evaporate before you can arbitrage them, or they may reflect genuine concerns about the discounted platform’s solvency or regulatory status. In both cases, the central question is whether the discount is compensation for illiquidity and risk or simply an artifact of mispricing that can be reliably captured. In crypto, the former often dominates, especially during stress.

Fee and product discounts should be evaluated in terms of net impact on your strategy rather than headline percentages. A permanent 15% fee discount on Avantis is valuable if you trade frequently in size, but it may be marginal if your activity is sporadic. A 20% discount on AI model access when paying in PROS is attractive for heavy users of the platform, but only if the opportunity cost of holding or acquiring PROS is reasonable relative to the savings. For travel and service discounts, like AVA’s Smart Discounts or Kraken-linked Travala vouchers, the benefit is tangible, yet it depends on actually using the services before promotions expire. The key is to translate all these discounts into expected dollar savings over your actual usage patterns, not your aspirational ones.

Tax and regulatory discounts require a long-term and jurisdiction-specific lens. The Australian CGT discount has historically made long-term holding of crypto more tax-efficient, but the potential shift to inflation indexation illustrates how such policies can change, sometimes retroactively altering optimal strategies. Investors should avoid basing their entire thesis on tax discounts that may be politically untenable, while still incorporating current rules into their after-tax return calculations. Similarly, central-bank discount rates and discount-window usage should be seen as macro inputs into the opportunity cost of capital rather than direct trading signals.

Finally, corporate finance discounts—whether in the form of convertible note buybacks, equity repurchases, or deeply discounted takeover bids—should be assessed in terms of governance and balance-sheet health. A firm that repurchases debt at a 40% discount while maintaining robust liquidity and transparent Bitcoin treasury management may be enhancing shareholder value. One that does so by selling core BTC holdings at a moment when those holdings themselves are trading at a perceived discount to long-term value may simply be shuffling risk. For token holders, similar logic applies when protocols use treasury funds to buy back tokens: the question is whether the buyback at a discount is consistent with sustainable development and security, or whether it is a cosmetic attempt to boost price.

Across all these domains, a common rhetorical strategy is to anchor discounts to emotionally salient baselines: “50% APR,” “20% off,” “buy Bitcoin 30% below last month’s high.” Yet the true economic meaning of a discount in crypto always comes back to the underlying trade-off: what you give up in risk, time, flexibility or opportunity cost for what you gain in lower prices or higher yields. Recognizing that trade-off, and quantifying it where possible, is the cornerstone of sober decision-making in a market where promotions and narratives often outpace analysis.

Conclusion

The concept of discount in crypto is both familiar and deceptively complex. At a surface level, it evokes sales, bargains and percent-off promotions, from Binance’s fee reductions and Discount Buy products to AVA’s travel savings and PROS’s discounted AI payments. Digging deeper, however, reveals that discount sits at the intersection of time, risk and value. Classical discounting translates future payoffs into present value through a discount rate that encodes opportunity cost and uncertainty. Market-structure discounts emerge when traded prices diverge from underlying value or from cross-venue averages. Fee and product discounts are strategic levers used by platforms to shape behavior and bootstrap ecosystems. Tax and regulatory discounts reflect policy choices that can reconfigure after-tax returns and portfolio strategies. Corporate finance discounts, through buybacks and liability management, influence how crypto-exposed companies like Strategy manage risk and capitalize on market dislocations.

For Bitcoin and broader crypto markets, discount narratives play a powerful psychological role. When prices fall sharply, calling the downturn a “discount” reinforces a long-term bullish narrative and encourages dip-buying behavior, as seen in commentary framing recent selloffs as capital rotation and opportunities for investors with multi-year horizons. Yet not every price decline is a bargain, and not every discount closes. Crypto’s history is littered with assets that looked cheap relative to past highs but never regained those levels, as well as with funds and tokens that traded at persistent discounts to NAV or intrinsic value because of structural flaws. The discipline lies in distinguishing between superficial discounts—anchored to arbitrary reference points—and economically meaningful ones, where the gap between price and value is both real and realistically bridgeable.

Ultimately, understanding discounts in crypto is about making trade-offs explicit. Every high APR on a Discount Buy product is the flip side of sold optionality and locked capital. Every trading fee discount is financed by platform economics and user behavior, not magic. Every CGT discount or inflation indexation scheme reflects a political compromise about how to tax risk-taking in volatile assets. Every buyback at a discount represents a choice about balance-sheet strength versus opportunistic value capture. For a sophisticated crypto audience—from retail strategists to institutional allocators—the challenge is not to shun discounts but to analyze them with the same rigor applied to any other source of return.

Viewed through this lens, discounts become less about marketing and more about pricing risk, time and liquidity in an environment where volatility, innovation and regulation are all in flux. By grounding discount language in financial reality and concrete mechanisms, market participants can better navigate promotions, dips and corporate maneuvers, aligning their use of discounts with coherent, risk-aware strategies rather than with mere slogans.

Outlook

As crypto matures and converges further with traditional finance and AI-driven services, the role of discounts is likely to expand rather than shrink. Platforms will continue to experiment with fee structures, referral programs and token-utility schemes, using discounts to differentiate in increasingly crowded markets. Structured products like Discount Buy will evolve alongside options and futures markets, offering more granular ways to express views on Bitcoin and other assets, but also requiring greater sophistication from users to understand their discounted payoffs. Tax authorities will keep revisiting preferential treatments such as CGT discounts in light of fiscal pressures and evolving views on crypto’s place in the financial system, with Australia’s proposed shift toward inflation indexation a bellwether of more nuanced, if complex, regimes.

At the same time, the macro backdrop—shaped by central-bank discount rates, liquidity conditions and regulatory attitudes—will continue to influence how aggressively investors discount crypto’s future cash flows and adoption. In periods of easy money and bullish sentiment, discounts may appear scarce and fleeting; in tightening cycles and risk-off phases, genuine long-term discounts may emerge amid forced selling and structural dislocations. AI’s integration with crypto, from PROS-powered payments for model access to AI-assisted trading and risk analysis, will add further layers, enabling more precise pricing of discounts but also creating new avenues for promotional campaigns and complex products.

For a crypto news audience, the enduring task is to look past the label and into the mechanics every time “discount” appears in a headline, whether it concerns Bitcoin’s spot price, a Binance promotion, an AVA travel perk, or a Strategy buyback. Understanding who is offering the discount, what they gain from it, and what risks you assume in accepting it will remain a critical skill as digital assets continue to intertwine with global finance, regulation and technology.

Latest Discount news

Sources

- https://www.investopedia.com/terms/d/discounting.asp

- https://www.sciencedirect.com/science/article/pii/S026156062300164X

- https://www.binance.com/en/support/announcement/detail/2b410dc9ef094cbb9c39e96b25720d1e

- https://www.fidelity.com/learning-center/investment-products/etf/premiums-discounts-etfs

- https://www.stockspot.com.au/cgt-calculator

- https://koinly.io/blog/crypto-exchange-with-lowest-fees/

- https://www.facebook.com/groups/savvyinvestors/posts/2744515372579825/

- https://www.strategy.com/purchases

- https://www.binance.com/en/support/announcement/detail/2526d2ed10c14a34a4fa467b34c47ba2

- https://www.binance.com/en/square/post/329999428935489

- https://www.binance.com/en/square/post/312732106001473

- https://www.travala.com/blog/ava-givebacks-discounts-now-available-for-car-rentals/

- https://avantis-referral-code-rebate.vercel.app

- https://x.com/cysic_xyz/status/2055413716137771251

- https://x.com/CryptosR_Us/status/2063638863919075401

- https://x.com/leviathan_news/status/2053730381296218201

- https://x.com/niklaus651/status/2066524292267844060

- https://x.com/AVAFoundation/status/2065328249186758715

- https://www.instagram.com/reel/DYXbm7_IOCl/?hl=en

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…