Explainer on how “genesis” is used across crypto: from Bitcoin’s genesis block to NFTs, points programs, and Genesis‑branded firms entangled with FTX claims. Unpacks launches, mainnets, risks, rewards, and what “being early” really means.

+3 sources across the wider coverage universe

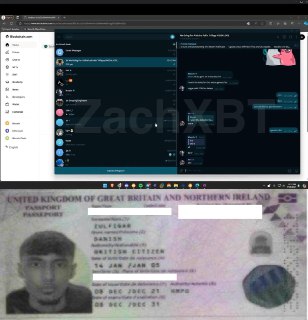

ZachXBT says law enforcement seized $18.9M from actors tied to Genesis creditor theft2026-06

ZachXBT says law enforcement seized $18.9M from actors tied to Genesis creditor theft2026-06 Draper Dragon opens $80M OrionFund for Cardano builders across Genesis and Apex tracks2026-06

Draper Dragon opens $80M OrionFund for Cardano builders across Genesis and Apex tracks2026-06 Cancore launches Genesis program to reward early adopters and contributors as Mainnet rolls out.2026-04

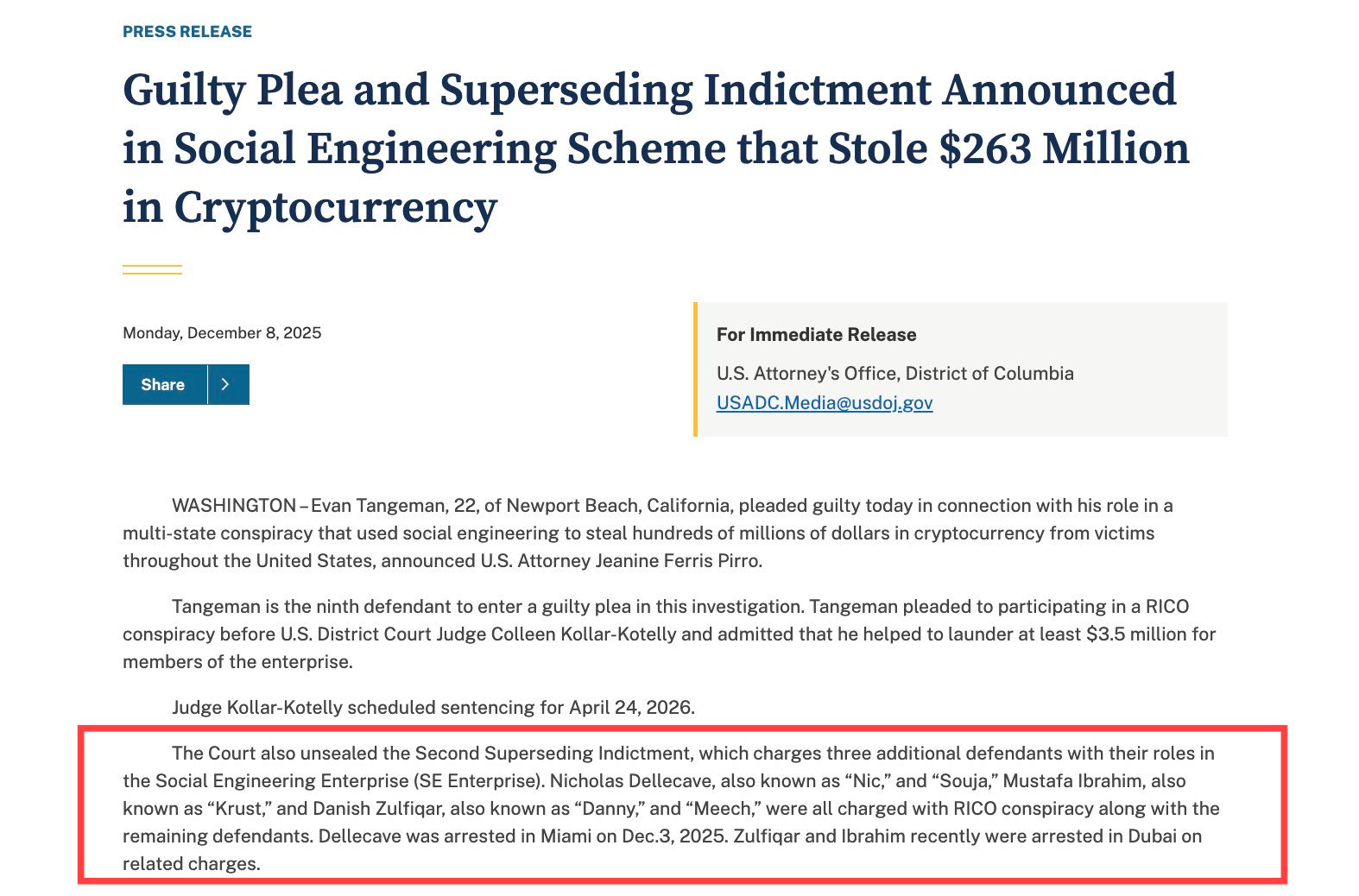

Cancore launches Genesis program to reward early adopters and contributors as Mainnet rolls out.2026-04 British Hacker Behind Genesis Creditor Heist Likely Arrested as $18.6M in Crypto Seized After Dubai Raid2025-12

British Hacker Behind Genesis Creditor Heist Likely Arrested as $18.6M in Crypto Seized After Dubai Raid2025-12 Genesis completes bankruptcy restructuring and plans to begin distributing $4 billion in crypto and cash with creditors receiving an average of 64% restitution2024-08

Genesis completes bankruptcy restructuring and plans to begin distributing $4 billion in crypto and cash with creditors receiving an average of 64% restitution2024-08 Genesis reaches settlement with New York regulator, will forfeit BitLicense and pay $8 million fine.2024-01

Genesis reaches settlement with New York regulator, will forfeit BitLicense and pay $8 million fine.2024-01

In crypto, the word “genesis” signals an origin moment: the first block in a blockchain, the first NFT in a collection, or the earliest phase of a protocol’s launch and incentive design. It has also become a powerful branding term for companies, capital programs, and points schemes that try to capture the premium associated with being early.

What “Genesis” Means In Crypto

The term “genesis” long predates digital assets, but in the crypto context it has taken on a very specific, technical meaning as well as a looser, marketing-driven one. At its most precise, a genesis block is the first block in a blockchain’s history, the base from which every later block is derived. Around that foundational idea, the industry has developed a broader vocabulary: “genesis” NFTs for first-edition collectibles, “genesis” phases for pre-mainnet or pre-token campaigns, and “Genesis” as the name of lending desks, mining firms, or capital programs.

This convergence of technical terminology and promotional language can be confusing, especially for newer participants who encounter “Genesis” in headlines about Bitcoin, NFT auctions, bankruptcy claims, or FTX-related litigation. For example, Ethereum’s own history includes a “genesis sale” of ETH, while newer ecosystems like Celestia’s TIA token have publicized genesis airdrops and validator sets. At the same time, newsletters and governance forums now routinely reference “Genesis Points,” “Genesis Capital,” or “Genesis Boosts” as shorthand for early access reward structures surrounding a mainnet launch or new staking product.

What unites these diverse uses of the word is the idea of initial conditions. In a blockchain, the genesis block defines the starting state that all nodes must agree on. In NFT collections, genesis tokens set the standard for scarcity, aesthetics, and community culture. In incentive programs, “genesis” designates the window during which early users establish their position in whatever distribution or claims model a project intends to run. Even corporate entities adopting the name “Genesis” tend to trade on the notion of being an early mover, whether in Bitcoin mining or centralized lending.

For a crypto news audience, understanding these distinctions matters for several reasons. Technically, the genesis block and related configuration files define who holds what and who has power in a network. Economically, genesis NFTs and genesis points programs often command a premium relative to later issues. Legally, the collapse or litigation of businesses like Genesis Global Capital or Genesis Digital Assets has shown how the aura of “genesis” does not insulate investors, counterparties, or FTX creditors from risk. Interpreting headlines about BTC, NFTs, FTX claims, TIA airdrops, or mainnet launches thus requires a precise sense of what “genesis” denotes in each case.

ZachXBT says law enforcement seized $18.9M from actors tied to Genesis creditor theft

ZachXBT pushed back on claims that several detained Dubai-based “crypto entrepreneurs” were just tech operators, saying they were threat actors tied to high-profile social engineering fraud and data extortion. He says law enforcement seized $18.9M in stolen funds, with the alleged network linked to Danish Zulfiqar Khan, SIM swaps, breaches, and the $243M Genesis creditor theft.

Readers clicked Genesis not to understand the bankruptcy itself but to follow the accountability chain radiating outward from it — who missed which payment, which regulator filed what complaint, who stole $243M from creditors while it was failing, and whether the recovery percentage was fair — treating the collapse as an ongoing legal drama with named defendants, not a closed financial event.↗

Genesis Blocks: Where Blockchains Begin

In blockchain engineering, the genesis block is the unique starting point of a chain’s ledger. It is typically numbered as block 0, although some early implementations treated it as block 1. Unlike every subsequent block, the genesis block does not reference a previous block hash, because there is nothing earlier in the chain’s history. Instead, it is hard-coded into the node software of the blockchain implementation and distributed to all participants as a shared point of reference. The data within the genesis block specifies the network’s initial parameters, such as the version, timestamp, and often an initial distribution of coins or state entries.

Bitcoin’s genesis block illustrates why this matters in practice. Satoshi Nakamoto embedded a headline from a British newspaper into the coinbase data of the first block, anchoring Bitcoin’s launch in a specific political and economic moment and signaling the project’s critique of the traditional banking system. Technically, the block also included a subsidy for the miner, but that subsidy is unspendable in Bitcoin’s code, making the genesis block a special case that defines protocol rules rather than enriching its creator. Because it is hard-coded, any node that attempts to join the Bitcoin network with a different genesis block will be rejected as incompatible, underscoring the role of the genesis block as a constitutional document in code form.

Other proof-of-work and proof-of-stake networks have adopted similar mechanisms, even when their governance models and token distributions differ markedly from Bitcoin’s. A new chain generally publishes a “genesis file” alongside its node software, specifying initial validator sets, token balances, and sometimes vesting schedules. In proof-of-stake systems, this genesis configuration determines which entities can participate in block production from day one and how voting power is distributed. For example, when modular data-availability networks such as Celestia launched, they defined a genesis validator set and TIA token allocation that encoded the outcomes of their pre-launch testing, airdrop criteria, and investor allocations. Although implementation details vary, the structural role of the genesis block or genesis state remains constant: it is the irreversible origin point for the canonical chain.

The relationship between genesis and mainnet launch is particularly important. In many modern networks, the “genesis” state is prepared and audited off-chain before any blocks are produced. Once the chain starts producing blocks from that genesis state, the mainnet is considered live. Governance proposals, airdrop claims, and vesting contracts all reference balances and entitlements that exist in the genesis snapshot. This is why disputes over genesis allocations can be so fraught: any error or controversy baked into genesis is hard to unwind without a contentious hard fork. The term “genesis” thus has concrete implications for BTC holders, TIA recipients, and other token communities whose future distribution and governance are locked in at launch.

Genesis NFTs and Collectibles

As NFTs emerged, creators and platforms quickly borrowed the language of genesis to highlight the primacy of early works. A Genesis NFT typically refers to the first non-fungible token issued within a specific collection, project, or ecosystem. It occupies a unique position because it marks the origin point from which all later NFTs in that series are derived, giving it symbolic and historical significance beyond its aesthetic traits. Many teams intentionally design their genesis piece to embody the project’s identity or long-term vision and often distribute it to early supporters as recognition for being present at the beginning.

This pattern can be seen in curated art platforms and gaming ecosystems alike. On SuperRare, for instance, a “genesis” auction might accompany the launch of a new token or project, positioning the first piece as a one-of-one artifact tied to the platform’s narrative arc. When the artist Yigit Duman’s “Panorama” series launched, the event combined a PANO token launch with a Genesis NFT auction, explicitly linking ownership of the inaugural NFT to the project’s broader token economy. In move-to-earn ecosystems like STEPN, genesis sneakers are minted in limited numbers and marketed as premium assets, sometimes resurfacing in promotional collaborations such as Rabbids-themed Genesis Sneakers and Dreamland Genesis Sneakers distributed through GGBox drops.

The market assigns value to genesis NFTs for several reasons. First, there is genuine historical scarcity: only one first token can exist for a given smart contract or collection. Second, genesis holders are often promised ongoing perks such as boosted in-game earnings, higher staking multipliers, or access to allowlists for future mints. Third, collectors attribute cultural cachet to being “early,” especially in ecosystems where early adopters of BTC, TIA, or landmark NFT collections have been financially rewarded. This creates a feedback loop: projects emphasize the “genesis” branding to attract speculators, and speculators pay a premium in the hope that future demand will validate their bet on the project’s origin story.

However, the same features that make genesis NFTs appealing also heighten risk. Their value is usually more tightly coupled to the long-term success of a project than later, more utility-focused assets. If a move-to-earn game fails to sustain user growth or a curated art platform loses momentum, the market premium attached to the genesis NFT may evaporate. Moreover, the opacity of rights and benefits can create misunderstandings: some buyers read “genesis” as implying equity-like upside or governance privileges that are never actually encoded in the underlying smart contract. In the wake of broader market drawdowns and the collapse of centralized firms like FTX, the legal status of such implied promises has become an increasingly active area of regulatory interest, even if enforcement actions have so far focused more on token sales than on discrete NFTs.

Draper Dragon opens $80M OrionFund for Cardano builders across Genesis and Apex tracks

Promoting from Tsunami auto-feed. Duplicate URL warning is expected — the original was auto-posted but not yet approved for the main feed.

- 01Creditor recovery rate scrutiny↗

The 64% average restitution figure on a $4B distribution gave readers a concrete number to evaluate whether bankruptcy justice was actually served.

- 02DCG-Gemini payment warfare

The $630M missed payment, NYAG complaint alleging a covered-up $1B hole, and DCG's counterattack calling the settlement 'subversive' turned a corporate dispute into a high-stakes public feud readers could track.

- 03$243M creditor theft prosecution

The audacity of stealing from bankruptcy creditors while the case was live — followed by arrests, eXch seizure, and a $91M follow-on social engineering scam — made this a criminal subplot readers tracked separately from the civil proceedings.

- 04GBTC redemption as bankruptcy exit

Eric Balchunas framing Genesis's GBTC-to-spot-BTC conversion as net neutral reframed a market panic narrative and gave readers a cleaner mental model of what Genesis was actually doing with $2.1B in shares.

- 05FTX-Genesis cross-claims tangle

The mutual billion-dollar claims between two simultaneously bankrupt entities — each alleging the other enabled fraud — offered readers a rare look at how contagion settlements work when both sides are insolvent.

- 06Protocol 'genesis' launch events

Hyperliquid HYPE, Celestia TIA, Taiko, and Plume each used 'genesis' as a launch branding term, creating a secondary click cluster from readers tracking early-participation airdrop opportunities unrelated to the lender collapse.

Genesis Phases, Programs and Points

Beyond discrete tokens, “genesis” has evolved into a standard label for launch-phase campaigns aimed at rewarding early adopters before a protocol is fully live. These programs often appear in the form of points systems, time-limited liquidity windows, or “Genesis Month” events wrapping around a mainnet rollout. The RXUSD Genesis Points Program is a clear example of this pattern. It is designed to reward early community participation and ecosystem loyalty, allowing users to register their wallets, hold RXUSD, and eventually stake into sRXUSD to accumulate Genesis Points over time. Participants who register before the mainnet launch receive additional Early Bird bonus points and a unique access code providing testnet access, explicitly framing the program as a way to become a founding member of the ecosystem.

A similar dynamic operates in the Monetrix Genesis event, which is described as a pre-mainnet farming window in which users deposit capital to earn GEMs, a non-transferable points currency. According to Monetrix’s guide, Genesis distributes a fixed number of GEMs per day to depositors based on a time-weighted and size-weighted model, meaning that both how much a user deposits and how long it remains in the pool matter. The event is structured to reward early and patient participants more heavily than late, short-term depositors, reinforcing the idea that “genesis” is about being present before the token and the hype arrive. Monetrix even issues a Pioneer Genesis Soulbound Token, an on-chain marker of early participation that cannot be transferred and may later serve as a criterion for token airdrops or governance roles.

Other projects have adopted similar language. Cancore, for instance, rolled out its mainnet alongside a Genesis program geared toward early adopters and contributors, positioning this phase as a bridge between testnet experimentation and full network operation. In the Ethereum ecosystem, initiatives such as ERC‑8004 have used the concept of “Genesis Month” around mainnet launch, creating a time-bounded narrative that encourages users to participate in trustless contracts or new infrastructure as it goes live. Stablecoin and DeFi initiatives like RXUSD are experimenting with Genesis Points that convert into future rewards or influence, while staking-oriented projects are launching “Genesis Boosts” to incentivize early delegation before their staking products open to the wider public.

These designs deliberately blur the line between marketing and mechanism. By labeling something a “Genesis Points Program” or “Genesis Capital Allocation,” teams signal that this is a privileged phase during which participants may earn outsized upside relative to later users. Venture and ecosystem funds have adopted similar language, as seen in accelerator tracks that distinguish between Genesis and Apex cohorts for builders at different stages. In each case, the idea is that Genesis participants bear more uncertainty—technical, regulatory, or market-related—and are therefore entitled to a differentiated share of tokens, governance rights, or fee streams once the protocol matures. Yet these entitlements are rarely guaranteed in contractual terms; they are often aspirational, contingent on later token launches, governance votes, or revenue that may never materialize.

Corporate “Genesis”: Lenders, Miners and Legal Risk

Complicating matters further, “Genesis” is not just a descriptor but also a brand. Genesis Global Capital, a major crypto lending arm associated with the Genesis Trading group, became one of the emblematic casualties of the 2022–2023 market downturn. After suffering heavy losses tied to counterparties such as Three Arrows Capital and being exposed to the FTX collapse, Genesis Global Capital entered restructuring proceedings. By early 2024, the firm had completed a debt restructuring that sought to resolve its obligations to creditors, an outcome documented by legal advisors involved in the process. For many market participants, headlines about a “Genesis unit” facing lawsuits over asset sales or bankruptcy claims signaled the end of an era for centralized institutional lenders that once dominated OTC BTC and ETH markets.

It is important to separate this corporate “Genesis” from the technical concept of a genesis block or the various genesis points programs discussed earlier. The lender’s problems stemmed from maturity mismatches, opaque risk management, and concentrated exposures, not from any flaw in Bitcoin’s genesis design or NFT issuance mechanics. Yet the shared branding can still mislead less experienced readers, especially when news reports juxtapose Genesis Global Capital’s restructuring, FTX creditor claims, and on-chain airdrop “claims” in a single news cycle. Understanding that Genesis in this context refers to a company—and that its obligations are mediated through bankruptcy and restructuring law, not through smart contracts—helps clarify what recourse creditors and counterparties actually have.

Genesis Digital Assets, a Bitcoin mining firm, provides another example where the brand intersects with legal and reputational risk. The FTX Recovery Trust has sued Genesis Digital Assets and two of its co-founders, alleging that Sam Bankman‑Fried directed more than 1.15 billion dollars in commingled and misappropriated FTX customer funds into the company and related entities. According to the complaint, these transfers constituted a misuse of customer deposits intended to fund high-risk equity investments in mining rather than maintain the safety and liquidity of exchange balances. The case is part of a broader effort to claw back assets after FTX’s collapse and to maximize recoveries for creditors whose claims are now being processed through formal bankruptcy channels.

Separately, law enforcement agencies have pursued actors who targeted Genesis-related entities and their stakeholders. Reports have detailed investigations into hackers who allegedly stole tens or hundreds of millions of dollars from Genesis creditors or related platforms, with subsequent seizures of on-chain funds and coordination with blockchain investigators like ZachXBT. While these incidents are distinct from the corporate restructuring and the FTX-related lawsuit, they share a common theme: the name “Genesis” surfaces in headlines not only as a symbol of early opportunity but also as a shorthand for some of the industry’s most visible failures and enforcement actions. For readers parsing discussions of BTC price moves, NFT auctions, FTX claims, and TIA airdrops, distinguishing between “genesis” the concept and “Genesis” the corporate actor is essential to avoid conflating protocol-level risk with counterparty risk.

Cancore launches Genesis program to reward early adopters and contributors as Mainnet rolls out.

This is generous of them! I hope this continues for those who stay with the project

- 2022-06exploit

Three Arrows Capital collapse exposes Genesis's $2.4B exposure

- 2022-11milestone

FTX collapse triggers Genesis withdrawal suspension

- 2023-01regulatory

Genesis Global Capital files Chapter 11 bankruptcy

- 2023-01regulatory

NYAG files complaint against Gemini, Genesis, and DCG for fraud

- 2024-02governance

DCG reaches in-principle deal with creditors at 65–90% recovery

- 2024-08exploit

$243M stolen from Genesis creditors via social engineering

- 2024-11regulatory

Genesis settles with NYAG: $8M fine and BitLicense forfeiture

Genesis completes restructuring, begins $4B creditor distribution at 64% average

Genesis, Launches and Mainnet: How The Pieces Fit

Across L1s, L2s, and application-layer protocols, “genesis” is now tightly woven into narratives about launches and mainnet transitions. Technically, a chain’s genesis block or genesis state is the first mainnet state; conceptually, however, teams often stretch the “genesis” label backward to encompass the weeks or months of pre-launch activity that set the stage for the mainnet. This is apparent in cases such as RXUSD, where the Genesis Points Program begins before the mainnet goes live and explicitly promises testnet access and bonus points for wallets that register in advance. The result is a multi-phase rollout in which testnet usage, points farming, and early community building are all framed as part of the genesis journey rather than mere pre-production testing.

Monetrix offers a similar example from the DeFi infrastructure side. Its Genesis event is positioned as a pre-mainnet farming window, but the points and soulbound tokens earned during this period are intended to carry forward into the mainnet environment, influencing token allocations, access, or governance once the protocol fully launches. By structuring rewards on a time-weighted basis, Monetrix reinforces the idea that the true genesis participants are those who were willing to commit capital before there was any liquid token to sell or stake. In governance forums, this kind of pre-mainnet involvement is often used to justify special treatment for early users, whether in the form of claim multipliers in a TIA-style airdrop, priority access to liquid staking products, or whitelisting for NFT mints associated with protocol branding.

For infrastructure standards like ERC‑8004, the notion of a “Genesis Month” around mainnet launch further entrenches this temporal framing. During such periods, developers and early adopters are encouraged to deploy contracts, test integrations, and participate in orchestrated on-chain events that demonstrate the protocol’s capabilities. The genesis label serves both as a call to action and as a promise that participation in this window may be rewarded differently than activity after the network is widely adopted. This is consistent with broader crypto culture, where early users of systems ranging from Bitcoin to Celestia have, in retrospect, captured outsized gains compared with later entrants.

At the application layer, NFT projects and gaming ecosystems integrate genesis concepts directly into their launch playbooks. A curated art platform might coordinate a token generation event, a genesis NFT auction, and an allowlist mint over a forty‑eight hour period, marketing each step as part of a unified genesis narrative. Move‑to‑earn apps might seed their in‑game economy with a limited drop of Genesis Sneakers, followed by seasonal distributions through lootbox‑style mechanisms such as GGBoxes. Protocols experimenting with new staking or restaking frameworks may introduce “Genesis Boosts” that reward early delegators ahead of a broader public release. In each scenario, the line between mainnet launch and genesis activity is deliberately blurred so that the project can tell a cohesive story about early commitment, future upside, and community formation.

Risks, Rewards and How To Evaluate “Genesis” Opportunities

For participants deciding whether to engage with a “genesis” opportunity—whether it is a BTC genesis narrative, a TIA airdrop, a Genesis NFT auction, or a Genesis Points campaign—the key questions are less about branding and more about structure. The primary advantage of genesis participation is straightforward: early users often face less competition for rewards and may secure claim positions that are difficult or impossible to replicate later. In points‑based schemes like RXUSD’s Genesis Points or Monetrix’s GEM distribution, time‑weighted models explicitly favor those who show up first and stay longest. For genesis NFTs, supply is capped at a single token or a very small series, ensuring that later entrants cannot acquire the same status directly from the issuer.

However, with higher potential upside comes elevated risk. Genesis phases tend to coincide with the least proven stage of a project’s lifecycle. Smart contracts may not have been fully audited, tokenomics can change through governance proposals, and regulatory interpretations are still being tested. The FTX‑Genesis Digital Assets lawsuit illustrates how capital flows around high‑growth ventures can later be characterized as misappropriation or fraudulent conveyance when underlying institutions fail. Creditors in FTX’s bankruptcy, including those whose funds allegedly ended up in Genesis Digital Assets, must now navigate a complex landscape of claims, clawbacks, and litigation rather than simply relying on automated on‑chain redemption. Even in less dramatic cases, changes in macro conditions or protocol governance can retroactively dilute or restructure genesis‑phase promises.

Centralized intermediaries add another layer of complexity. The collapse and restructuring of Genesis Global Capital offer a cautionary example of how “early access” to institutional yield products, often marketed under prestigious brands, can leave depositors exposed when risk management fails. Unlike on‑chain genesis allocations governed by deterministic smart contracts, claims against a centralized lender depend on bankruptcy law, negotiation, and court‑approved reorganization plans. Participants in on‑chain genesis programs should ask whether their “claims” are enforced by code or depend on the solvency and goodwill of an off‑chain entity. The contrast between on‑chain claim mechanisms, such as automatic airdrop eligibility based on wallet activity, and off‑chain creditor claims, such as those in the FTX and Genesis cases, underscores the importance of understanding where enforcement actually resides.

Evaluating any genesis opportunity therefore requires careful due diligence that goes beyond the allure of being early. Participants should analyze who controls the genesis configuration or points ledger, how changes can be made, and whether there is any legal documentation backing the implied benefits. In pre‑mainnet phases, it is prudent to treat points and soulbound tokens as signals rather than guarantees of future TIA, BTC, or governance token distributions. Similarly, collectors considering a Genesis NFT or Genesis Sneaker should distinguish between hard‑coded rights (for example, royalty splits or access keys embedded in the token’s metadata) and soft promises conveyed in marketing materials. Finally, it is essential to recognize that the reputational weight of the term “Genesis” does not immunize a company or protocol from failure. The same industry that celebrates iconic origin stories also documents, in detail, the collapses, lawsuits, and enforcement actions tied to entities that once branded themselves as genesis‑era leaders.

Genesis Global Capital's collapse demonstrated that crypto lenders extending billions to under-collateralized borrowers like Three Arrows Capital face total loss events with no traditional bankruptcy safety net for creditors.

- RegulatoryHigh

The NYAG's complaint and forced BitLicense forfeiture established that crypto lending platforms serving retail customers face the same fraud and disclosure standards as licensed financial institutions, with operational shutdown as a penalty.

- LiquidityHigh

Genesis suspended withdrawals within days of the FTX collapse, illustrating how crypto lenders operating on fractional reserves can face bank-run dynamics the moment a major counterparty fails.

- Custody / TheftHigh

The $243M social engineering theft from Genesis creditors during active bankruptcy proceedings exposed that claimants holding large documented crypto positions become high-value targets for coordinated criminal operations.

- Governance / FiduciaryMedium

DCG's accusation that Genesis's bankruptcy plan showed selective favoritism toward certain creditor classes reflects systemic risk in crypto bankruptcy proceedings where governance structures lack the independent oversight of traditional Chapter 11 processes.

- Market / ContagionMedium

Genesis's forced liquidation of over 32,000 BTC in GBTC shares during restructuring created measurable ETF outflow signals, demonstrating how a single distressed entity can generate misleading macro market reads.

Comparative Uses Of “Genesis”

The multiplicity of meanings attached to “genesis” can be summarized by comparing how the term functions in different contexts. While each usage invokes the idea of a beginning, the underlying mechanics and risk profiles differ significantly.

| Genesis usage | Context | What begins | Typical incentives or effects | Example reference |

|---|---|---|---|---|

| Genesis block/state | Layer‑1 or Layer‑2 blockchain | Canonical ledger and initial token state | None directly; defines BTC, TIA, or other supply and governance from day one | Bitcoin genesis block hard‑coded in clients |

| Genesis NFT/collectible | NFT collections, gaming, art | First token(s) in a collection | Scarcity premium, cultural status, potential ongoing perks | Genesis NFTs in curated auctions and STEPN Genesis Sneakers |

| Genesis phase/program | DeFi, stablecoins, staking, infra | Early participation window around launch | Points, boosted yields, airdrop eligibility, testnet access | RXUSD Genesis Points, Monetrix Genesis farming, Cancore Genesis program |

| “Genesis” as a company | Centralized lenders, miners | Corporate ventures and finance operations | Institutional yield, BTC mining exposure; also counterparty and legal risk | Genesis Global Capital restructuring and Genesis Digital Assets lawsuit |

This diversity helps explain why headlines referencing “genesis” can range from deeply technical discussions of BTC’s block history to coverage of NFT auctions, mainnet points races, or FTX‑related claims against a Bitcoin miner. For a crypto‑native readership, recognizing which row of this table a given use of “genesis” belongs to is a prerequisite for understanding the real mechanics and risks behind the story.

Outlook

As crypto matures, “genesis” is likely to remain a central term in both protocol design and narrative framing. On the technical side, new L1s, modular data‑availability networks, and specialized appchains will continue to hard‑code genesis states that encode token distributions, validator sets, and governance baselines. The controversies already seen around initial allocations for BTC successors and TIA‑style launches suggest that communities will keep debating who deserves what at genesis and how transparent that process should be. On the cultural side, genesis NFTs, sneakers, and collectibles will persist as status symbols in NFT and gaming circles, with premium valuations attached to verifiable early participation.

Economically, the trend toward genesis points, soulbound tokens, and structured pre‑mainnet campaigns is likely to become more sophisticated. As regulators scrutinize token launches and centralized lenders, teams may lean more heavily on non‑transferable markers of participation, retroactive airdrops, and community‑driven allocation frameworks rather than upfront sales. Experiments like RXUSD’s Genesis Points or Monetrix’s time‑weighted farming windows hint at an environment in which “being early” is quantified through on‑chain behavior rather than off‑chain commitments. At the same time, the legal fallout from FTX and its dealings with Genesis‑branded entities will continue to shape how courts treat clawbacks, misappropriation claims, and the relationship between centralized balance sheets and decentralized protocols.

For readers navigating this landscape, the core discipline remains the same: separate genesis as a technical and economic concept from “Genesis” as a marketing term or corporate brand. Evaluate launch‑phase incentives on their actual mechanics and enforceability, not on the implicit promise that all genesis participation is rewarded equally or safely. The industry’s history shows that genesis moments can be extraordinarily generative, producing enduring protocols and communities around BTC, novel L1s, and influential NFT collections. It also shows that some ventures bearing the Genesis name have become focal points for creditor claims, lawsuits, and enforcement actions. Understanding both sides of that history is the best preparation for whatever the next generation of genesis blocks, genesis NFTs, and genesis programs brings.

Latest Genesis news

ZachXBT says law enforcement seized $18.9M from actors tied to Genesis creditor theftDraper Dragon opens $80M OrionFund for Cardano builders across Genesis and Apex tracksCancore launches Genesis program to reward early adopters and contributors as Mainnet rolls out.British Hacker Behind Genesis Creditor Heist Likely Arrested as $18.6M in Crypto Seized After Dubai Raid Tether's technology arm, Tether Data, launched decentralized AI App, dataset, QVAC Genesis I, the world’s largest open STEM AI dataset, and a privacy-focused local AI app, QVAC Workbench to decentralize intelligence and challenge Big Tech’s control of AI data.

Tether's technology arm, Tether Data, launched decentralized AI App, dataset, QVAC Genesis I, the world’s largest open STEM AI dataset, and a privacy-focused local AI app, QVAC Workbench to decentralize intelligence and challenge Big Tech’s control of AI data. The FTX Recovery Trust has sued Bitcoin miner Genesis Digital Assets for $1.15B, alleging Sam Bankman-Fried funneled misappropriated FTX customer deposits to the firm and its founders. The case is part of efforts to claw back funds after FTX’s 2022 collapse.

The FTX Recovery Trust has sued Bitcoin miner Genesis Digital Assets for $1.15B, alleging Sam Bankman-Fried funneled misappropriated FTX customer deposits to the firm and its founders. The case is part of efforts to claw back funds after FTX’s 2022 collapse.Sources

- https://www.ledger.com/academy/glossary/genesis-block

- https://en.bitcoin.it/wiki/Genesis_block

- https://coinmarketcap.com/currencies/genesis/

- https://www.clearygottlieb.com/news-and-insights/news-listing/genesis-completes-debt-restructuring

- https://www.facebook.com/cointelegraph/posts/%EF%B8%8F-new-the-hacker-who-stole-300m-from-coinbase-users-sent-a-taunting-message-onch/1012705271036301/

- https://www.binance.com/en/square/hashtag/ftx

- https://baxity.com/glossary/genesis-nft

- https://getrxusd.com/incentives

- https://www.mometrix.com/academy/

- https://x.com/SkyEcosystem/status/2033187385215766649

- https://www.mometrix.com/academy/reconstruction/

- https://www.tradingview.com/news/coindar:8188d4b1e094b:0-superrare-to-hold-panorama-genesis-nft-auction-on-april-23rd/

- https://aixbt.tech/projects/Cancore-69d0aff698fbde5610ed6aae

- https://x.com/Stepnofficial/status/2038551832750961019

- https://t.me/s/airdrops_io?before=7627

- https://fsl.com/updates/march-26

- https://www.mexc.com/news/1090572

- https://www.weex.com/news/detail/the-dao-reboot-backpack-prepares-for-tge-whats-the-overseas-crypto-community-talking-about-today-570171

- https://airdrops.io/blog/monetrix-airdrop-genesis-guide/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…