Deep dive on integration in crypto: how blockchains, stablecoins, RWAs, AI, exchanges, and regulations connect. Explains oracles, cross‑chain, tokenization, AI agents, and policy trends shaping onchain finance.

+30 sources across the wider coverage universe

The US may have banned a CBDC, but through stablecoin regulation, 1:1 reserves, & institutional integration, stablecoins become America's de-facto digital dollar.2025-12

The US may have banned a CBDC, but through stablecoin regulation, 1:1 reserves, & institutional integration, stablecoins become America's de-facto digital dollar.2025-12 Aave Chan Initiative Accuses Aave Labs of Diverting DAO Revenues and Privatizing Protocol Economics, Demands Clarity on CowSwap Integration, Vault Fees, Horizon Deals, and V4 Liquidation Engine Incentives.2025-12

Aave Chan Initiative Accuses Aave Labs of Diverting DAO Revenues and Privatizing Protocol Economics, Demands Clarity on CowSwap Integration, Vault Fees, Horizon Deals, and V4 Liquidation Engine Incentives.2025-12 US Regulator Clears Banks to Intermediate Crypto Transactions, Marking Another Step Toward Tighter Integration of TradFi and Digital Assets2025-12

US Regulator Clears Banks to Intermediate Crypto Transactions, Marking Another Step Toward Tighter Integration of TradFi and Digital Assets2025-12 LlamaRisk Insights: GHO’s backing and RWA integration, a portfolio analysis.2025-12

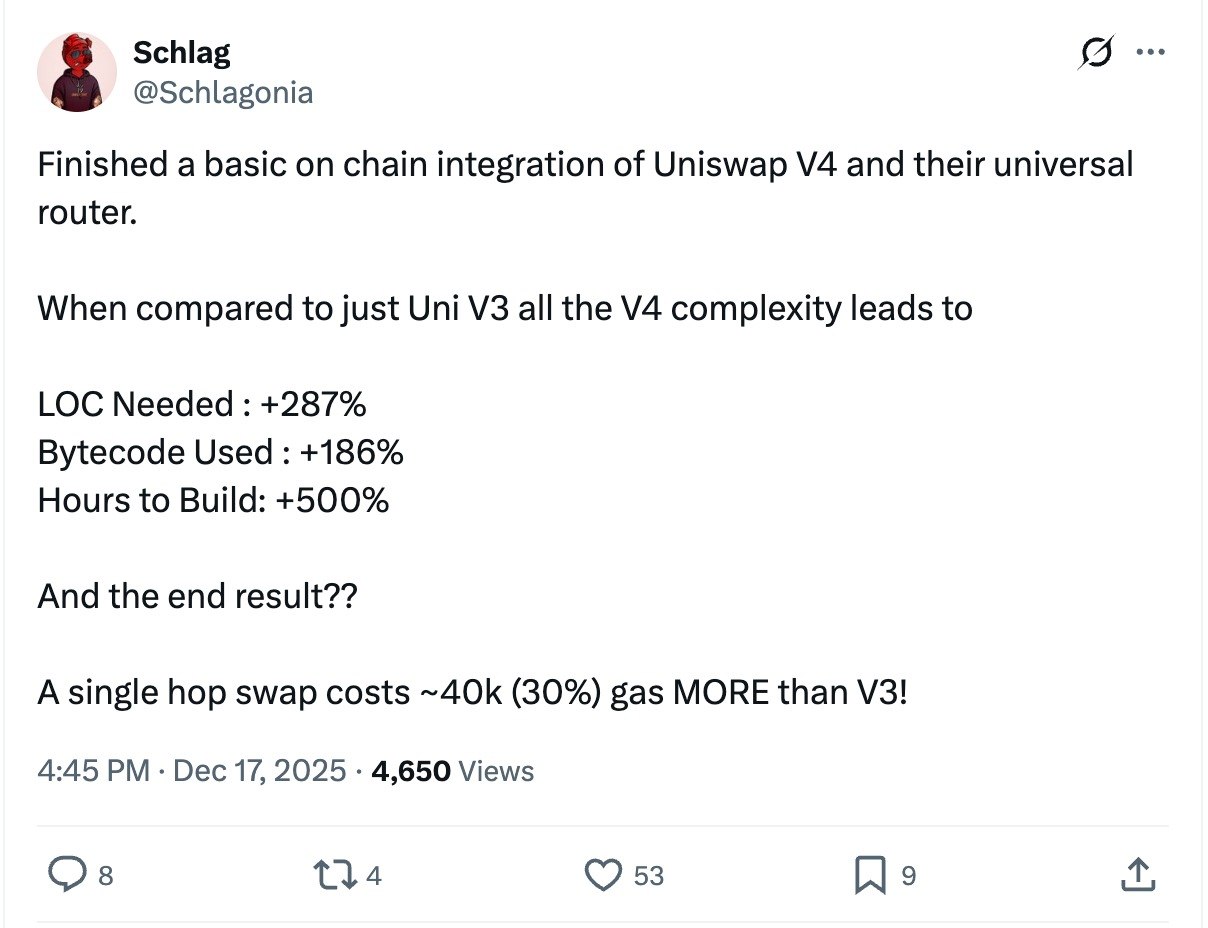

LlamaRisk Insights: GHO’s backing and RWA integration, a portfolio analysis.2025-12 Yearn developer Schlag gives feedback on basic onchain integration of Uniswap V4 and their universal router2025-12

Yearn developer Schlag gives feedback on basic onchain integration of Uniswap V4 and their universal router2025-12 Woori Bank has become the first Korean commercial bank to display Bitcoin prices in its main trading room, signaling BTC’s growing role in market sentiment. The move comes as Korean banks deepen digital asset integration and prepare for tighter regulations.2025-12

Woori Bank has become the first Korean commercial bank to display Bitcoin prices in its main trading room, signaling BTC’s growing role in market sentiment. The move comes as Korean banks deepen digital asset integration and prepare for tighter regulations.2025-12

Integration in Crypto: How Everything Connects

In digital assets, integration describes the process of connecting blockchains, protocols, data sources, institutions, and users so they function as a coherent financial and technological system rather than isolated silos. It is the quiet infrastructure work behind every “launch,” from a stablecoin going live on a new chain to an AI agent executing trades across DeFi.

What Integration Means in Crypto

In traditional software, integration usually refers to plugging one application into another through an API. In crypto, the concept is broader and more layered: it encompasses how smart contracts interact with offchain data, how liquidity moves across chains and venues, how tokenized assets are recognized in legal systems, and how national regulators embed digital assets into existing capital markets. Oracles feeding prices into Ethereum, a wallet adding a new DeFi protocol, or a central bank clarifying stablecoin rules are all examples of integration work, even if they look very different on the surface.

A useful way to understand integration is to distinguish it from related terms like interoperability and composability. Interoperability is the ability of two chains or systems to exchange data or value at all; composability is the ability to stack protocols like Lego bricks so the output of one becomes the input of another. Integration is the deliberate, often incremental process of making those connections reliable, secure, regulated where necessary, and usable at scale. Ethereum’s role as a hub chain illustrates this: its smart-contract standards and liquidity depth made it the default venue for stablecoins, DeFi, and tokenized assets, and much of “integration” over the past decade has meant adapting other chains, institutions, and tools to plug into that ecosystem.

Integration is also the bridge between the crypto-native and the offchain world. Fiat‑backed stablecoins such as USDC, which is issued by Circle and fully backed by reserves to maintain a one‑to‑one value with the U.S. dollar, are designed explicitly to integrate traditional money with blockchain‑based payment and trading rails. At the same time, regulators are attempting to integrate digital assets into policy frameworks: the United States has directed a federal working group to design a regulatory framework for digital assets and stablecoins while explicitly prohibiting federal agencies from launching a U.S. CBDC, illustrating a preference to integrate private stablecoins rather than issue a public tokenized dollar. Thailand, for its part, is shifting its crypto regulation toward market expansion and institutional integration, focusing less on pure speculation and more on embedding digital assets in capital markets and defining investor access.

In the mid‑2020s, integration has become the dominant theme shaping crypto’s trajectory. Institutions are experimenting with tokenization of real‑world assets (RWAs), with estimates that tokenized RWAs could reach 3–12% of global GDP by 2030 under bullish scenarios. Onchain liquidity is consolidating in sophisticated venues such as Hyperliquid, which has bootstrapped its way to becoming one of the largest decentralized exchanges with trillions in cumulative volume and billions in net inflows, in part by deeply integrating derivatives, cross‑margining, and onchain governance. At the same time, AI‑blockchain projects, AI‑linked tokens, and AI‑powered agents are forcing developers to think about how to integrate machine intelligence, verifiable data, and programmable finance without introducing new systemic risks.

For a crypto news audience, “integration” is often the story behind the headline. When Coinbase announces tokenized stocks and AI integrations, or a new DeFi protocol launches on Ethereum with USDC support, what is really happening is a complex integration effort that touches technical standards, legal structures, market microstructure, and user experience. Understanding integration as a multi‑dimensional process rather than a one‑off switch flip helps explain why some initiatives—like stablecoins or core DeFi blue chips—embed themselves quickly across the ecosystem while others, such as many tokenized RWA experiments, struggle to move beyond pilot status despite impressive issuance numbers.

The US may have banned a CBDC, but through stablecoin regulation, 1:1 reserves, & institutional integration, stablecoins become America's de-facto digital dollar.

Totally agree with this. Very soon, it will just be a total regulation

Readers click 'integration' stories not for the technical plumbing but for the access unlock — the top headlines are all about a previously gated capability (orderbook trading, yield pools, cross-chain liquidity, wallet on-ramps) becoming reachable for the first time through a new protocol connection.↗

Technical Integration: From Oracles to Cross‑Chain Liquidity

Smart Contracts, Oracles, and the Data Integration Layer

Public blockchains are deliberately sealed environments: smart contracts cannot natively query web APIs or arbitrary offchain systems. This isolation is crucial for security and consensus, but it creates what is known as the oracle problem: contracts need external data—prices, interest rates, corporate actions, even weather feeds—but have no built‑in way to trust that data. Oracles are the integration layer that solves this gap by connecting blockchains to offchain resources and performing verifiable computation on behalf of smart contracts.

Leading oracle networks like Chainlink operate as decentralized oracle networks (DONs), in which multiple independent node operators fetch data from multiple sources, aggregate it, and deliver it onchain, reducing single points of failure and manipulation risk. This architecture allows oracles not only to supply price feeds for DeFi but also to perform more advanced tasks such as cross‑chain messaging, compliance checks using identity data, and privacy‑preserving computations that would be too expensive to run directly onchain. Chainlink’s Cross‑Chain Interoperability Protocol (CCIP) is one example of integration infrastructure, enabling secure messaging and token transfers between public and private blockchains with integrated risk management and monitoring.

In practice, oracle integration is now foundational to most onchain finance. Without it, lending protocols could not adjust collateral requirements to market prices; insurance contracts could not pay out on real‑world events; and tokenized RWAs could not synchronize onchain records with offchain legal and accounting systems. This is why enterprise‑scale integrations—such as the integration of major market infrastructures like DTCC with oracle networks to support tokenized securities settlement—are closely watched: they represent a deepening integration between traditional financial plumbing and DeFi infrastructure, rather than isolated pilots.

At a more granular level, integrating an oracle into a DeFi protocol or application is itself a non‑trivial engineering task. Developer‑oriented guides around projects like Tellor, an L1 oracle chain designed to provide subjective or harder‑to‑validate data, emphasize workflows for contract design, dispute and verification mechanisms, and monitoring, underscoring that integration is not merely about wiring an endpoint but about aligning incentives and security assumptions. The quality of this data integration layer directly determines not just protocol safety but also its ability to support more complex instruments, from leveraged derivatives to structured RWA products.

Cross‑Chain Integration, DEXs, and Liquidity Flows

As the L1 and L2 landscape has fragmented, technical integration has increasingly meant cross‑chain integration. Users now expect to move assets and positions between Ethereum, alternative L1s, rollups, and app‑specific chains with minimal friction, and they want to trade across this multi‑chain universe in a unified way. Yet research on blockchain adoption in fields like supply chain management highlights that scalability, interoperability, and the lack of robust cross‑chain standards remain major barriers to widespread deployment. The same frictions appear in DeFi when protocols try to expand beyond a single chain.

One pattern has been the rise of multi‑chain protocols and specialized bridges, combined with DEX and aggregator integrations. The Tria x Aptos integration, for example, brought hundreds of thousands of users and over one hundred million dollars of transaction volume to the Aptos ecosystem by enabling cross‑chain spend, trade, and earn across multiple networks, illustrating how integration can act as a demand catalyst when done securely. Likewise, Coinbase’s DEX integration going live in dozens of countries is less about launching a single interface and more about tying together centralized KYC funnels, onchain liquidity pools, and cross‑border compliance into a single user experience.

On purely onchain venues, DEXs like Hyperliquid demonstrate how aggressive integration can help a protocol escape the gravity well of low initial liquidity. Hyperliquid’s growth to multi‑trillion‑dollar trading volumes and billions in net inflows has depended on tightly integrating order books, perpetual swaps, collateral management, and governance into a single, performant onchain system. That kind of integration is technically demanding—it requires careful choices about settlement layers, sequencer design, and risk engines—but it enables the kind of deep liquidity and product diversity that makes an exchange a natural integration partner for wallets, aggregators, and institutional traders.

These integration patterns are not without risk. Every additional bridge, cross‑chain messaging layer, or exchange connector increases the attack surface, and the industry has seen multiple high‑profile bridge exploits. That is why there is growing emphasis on using hardened cross‑chain standards, such as decentralized oracle‑based messaging and risk‑managed bridging, rather than bespoke bridges for each integration. Integration is shifting from ad hoc connections to shared infrastructure primitives, much as internet connectivity eventually standardized around a small set of robust protocols.

Stablecoins, USDC, and Integration of Money Itself

Stablecoins are arguably the most impactful integration vector between crypto and the traditional financial system. Fiat‑backed stablecoins like USDC are fully reserved tokens designed to maintain a steady value, typically pegged one‑to‑one to a fiat currency such as the U.S. dollar, and are redeemable for that underlying fiat via the issuer’s banking relationships. Their design makes them natural units of account for DeFi, practical payment instruments for onchain commerce, and low‑friction settlement assets for cross‑border transfers.

Empirical data underscores how deeply stablecoins have integrated into crypto activity. TRM Labs estimated that stablecoins accounted for roughly thirty percent of all crypto transaction volume between January and July 2025, reflecting their dominant role in trading, lending, and remittances. Other market coverage suggests that on some networks and venues, stablecoins now comprise the overwhelming majority of transactions, with Tether’s USDT in particular becoming the default medium for value transfer in many emerging‑market user bases. Integrations such as Kaia’s USDT support, which aim to unlock secure, high‑speed transaction opportunities by embedding Tether directly into network infrastructure, illustrate how core stablecoin integrations can materially change a chain’s usage profile.

USDC plays a complementary role as a more institutionally oriented stablecoin. Circle emphasizes transparent reserves and regulatory engagement, positioning USDC as a trust‑minimized bridge asset that can move seamlessly across chains like Ethereum and into regulated payment and banking channels. Its integration into DeFi money markets, centralized exchanges, and fintech payment platforms allows users to treat it as a programmable dollar while still maintaining access to the legacy banking system. News coverage of products like PumpBTC exploring integration with Circle’s Bitcoin‑backed cirBTC instrument shows how stablecoin‑style tokens are now being applied to other underlying assets, turning integration of “money” into integration of yield‑bearing or synthetic exposures as well.

Stablecoin integration is also a regulatory project. The U.S. presidential directive on digital financial technology calls for a federal framework to govern the issuance and operation of digital assets including stablecoins, while explicitly barring agencies from issuing a CBDC absent specific legal mandate. This framing effectively recognizes private stablecoins as the primary vehicle through which tokenized dollars will be integrated into markets, payments, and DeFi, and it shifts the integration challenge toward ensuring that these tokens fit within existing prudential, AML, and consumer‑protection regimes. Integration, in this sense, is as much about licensing, capital rules, and disclosure standards as it is about smart‑contract code.

Institutional and Market Integration: Tokenization, Exchanges, and National Strategies

Tokenized Real‑World Assets and Their Struggle to Integrate

Tokenization of real‑world assets refers to converting ownership or economic rights in traditional assets—such as bonds, equities, real estate, commodities, or intellectual property—into digital tokens recorded and transferred on a blockchain. In technical terms, the tokens represent claims on offchain asset structures, often wrapped in special‑purpose vehicles or trusts, while the onchain contracts encode transfer rules, payout logic, and sometimes governance rights. The promise is that tokenization brings the programmability and global reach of DeFi to the vast pool of traditional assets, enhancing liquidity, reducing settlement times, and allowing fractional ownership.

By mid‑2025, more than twenty‑one billion dollars’ worth of tokenized RWAs (excluding stablecoins) had been deployed across various chains and protocols, covering government bonds, private credit, real estate, and more. Yet academic analysis and market data emphasize a persistent gap between issuance and integration: many of these tokens trade thinly, see limited acceptance as collateral in DeFi money markets, and remain siloed in specialized platforms. In other words, tokenization is happening, but integration into the broader DeFi stack is lagging, leaving tokenized RWAs more like walled gardens than fully composable building blocks.

The tokenization process itself contains multiple integration points. The initial asset selection and valuation must align with investors’ risk appetites and regulatory constraints, and the legal structuring phase must create wrappers—such as SPVs or trusts—that courts will recognize and that can support token transferability across jurisdictions. Smart contracts must then be deployed with programmable rules around ownership, transfer permissions, and payment waterfalls, while a compliance and identity layer embeds KYC, AML, and accreditation requirements, increasingly using privacy‑preserving schemes such as zero‑knowledge proofs. Only after all of this can tokens be listed and traded in onchain or permissioned markets, ideally with near‑instant settlement. Each of these steps is an integration challenge with its own failure modes.

Recent market moves show how large platforms are trying to close the gap between tokenization and integration. Coinbase’s launch of tokenized stocks that represent actual equity shares and can be traded twenty‑four hours a day, margined, and transferred with far fewer frictions than traditional brokerage models represents a significant integration of tokenized assets into mainstream trading flows. These products must simultaneously integrate with traditional custodians, clearing systems, and corporate‑action feeds, while also plugging into DeFi‑style interfaces and collateral engines. Similarly, AIxCrypto’s engagement with Faraday Future to explore RWA‑related applications underscores that experimentation is moving beyond simple token wrappers toward richer integrations between industrial assets, AI analytics, and onchain financing structures.

And yet, as the RWA liquidity literature stresses, fragmented laws across jurisdictions, uncertainty over digital custody and secured rights, and unresolved questions about bankruptcy treatment all constrain cross‑border token trading and DeFi integration. Integration, in the RWA context, often means slow, negotiated harmonization between securities law, insolvency regimes, and smart‑contract‑based markets, rather than the rapid, permissionless composability that DeFi users are accustomed to.

Exchange, Wallet, and Protocol Integration in the Retail Front End

For most users, “integration” is experienced not in legal documents or back‑office plumbing but in the front‑end interfaces they touch. When a centralized exchange adds a new token or supports a new chain, or when a wallet plugs into an options protocol or prediction market, it is enabling new behaviors with a familiar user experience. Recent coverage of KuCoin’s Web3 wallet integrating with prediction platform Polymarket is a clear example: users can interact with a previously niche DeFi vertical directly from a mainstream exchange‑branded wallet, without manually configuring RPC endpoints or bridging assets.

Strategic integrations can materially reshape a protocol’s metrics. Plasma Blockchain’s climb into the top tier of total value locked (TVL) rankings following the integration of Tether in its native wallet demonstrates how a widely used stablecoin can act as a liquidity magnet once deeply embedded in a chain’s tooling and UX. In a similar vein, Hyperliquid’s expansion has been amplified by tight integration with onchain wallets and portfolio tools that allow traders to manage complex derivatives positions while still retaining self‑custody over their assets. Each partnership or connector reduces switching costs and makes it more likely that users will treat these platforms as default venues.

Developer‑facing integrations are equally important. Upbit’s launch of a software development kit (SDK) designed to make API integration faster and easier for third‑party builders highlights how exchanges now compete not just for end‑users but for developer mindshare. By lowering the friction to connect bots, analytics tools, or even AI trading agents to its order books, an exchange effectively integrates itself into the broader crypto software ecosystem, increasing stickiness and order flow. Similarly, Coinbase’s DEX integration, which unlocks global trading opportunities in dozens of countries, represents a convergence of centralized and decentralized liquidity under a single brand, with the integration work happening at the API, compliance, and settlement layers simultaneously.

Wallet‑level integrations in the emerging AI agent economy also illustrate integration’s double edge. The partnership between Claw Wallet and security provider GoPlus to embed a dedicated SafuSkill integration aims to create a foundational security layer for AI agents that will manage onchain assets autonomously. By integrating security checks deeply into the wallet‑agent stack, the goal is to make AI‑driven operations safer by design. But such integrations also centralize certain trust assumptions: if a large share of AI agents rely on a small number of integrated security services, failures or compromises in those services can propagate widely.

National Strategies and Regulatory Integration

At the macro level, governments and regulators are making their own integration choices. Thailand’s latest regulatory pivot showcases a move away from viewing crypto purely as a speculative asset class and toward designing rules that allow integration into national capital markets and institutional portfolios. Policymakers are now wrestling with practical questions: how to list tokenized assets on local exchanges, how to structure investor access tiers, and how to align digital‑asset custody models with existing securities‑law protections. These integration questions are more complex than simply authorizing or banning crypto trading; they require coordination between securities regulators, central banks, and tax authorities.

In Europe, the rollout of the Markets in Crypto‑Assets Regulation (MiCA) has been followed by high‑stakes consultations on how, and to what extent, decentralized finance should be integrated under that framework. Policymakers are debating whether onchain protocols can be supervised via requirements on front ends and governance token holders, and how to handle inherently borderless, permissionless liquidity pools. These debates are effectively about integration: whether DeFi will be partially absorbed into the existing regulatory perimeter or remain largely parallel.

The United States is taking a distinct path. The presidential directive on digital financial technology explicitly bans agencies from establishing, issuing, or promoting CBDCs unless required by law, while instructing a working group to propose a federal regulatory framework for digital assets, with a focus on stablecoins and market integrity. This signals a strategy of integrating private digital assets into existing regulatory regimes rather than building a state‑run tokenized currency system. TRM Labs’ global policy review notes that across jurisdictions, enforcement themes are converging on stablecoins, illicit‑finance controls, and consumer protection, even as details diverge. Integration is happening through supervisory practice and enforcement as much as through new statutes.

Jurisdictional competition also shapes how projects plan their own integration roadmaps. Startale’s expansion into Abu Dhabi as part of the UAE’s broader crypto push, albeit with significant regulatory and integration risks, is an example of projects aligning themselves with jurisdictions that promise more predictable onramps for digital‑asset‑driven business models. Conversely, ambitious visions such as Sui’s trillion‑dollar AI agent economy, which may require significant changes to network architecture to support agent‑centric workloads, face both technical integration pitfalls and the challenge of fitting these novel constructs into still‑evolving regulatory categories.

Aave Chan Initiative Accuses Aave Labs of Diverting DAO Revenues and Privatizing Protocol Economics, Demands Clarity on CowSwap Integration, Vault Fees, Horizon Deals, and V4 Liquidation Engine Incentives.

🍿

- 01Hyperliquid as integration magnet

DEX Screener, Ethena, and MetaMask each integrated with Hyperliquid L1 in rapid succession, making it the single most-clicked integration destination and signalling readers see it as the emerging liquidity hub to plug into.

- 02DeFi yield pool unlocks

Liquity BOLD stability pools, Curve-Lite auto-deployment, and Curve LLAMMA integration all promise new yield access contingent on broader DeFi adoption, and readers engaged heavily with the 'what rate do I get?' framing.

- 03Cross-chain stablecoin reach↗

LayerZero powering pyUSD, CCTP landing USDC on Cosmos, and USDV launching with LayerZero all hit the same nerve: a stablecoin becoming natively multi-chain multiplies the addressable yield and trading surface readers can access.

- 04Consumer wallet on-ramps↗

PayPal + MetaMask, MetaMask adding Bitcoin, Visa/Transak withdrawals to 145 countries, MoonPay/PayPal, and Revolut Lightning all map to the same reader desire: moving between fiat rails and self-custody without leaving familiar apps.

- 05Institutional TradFi bridges↗

Kraken + EigenLayer restaking, Lido institutional via Crypto Finance AG, Italian banks exploring Bitcoin wallets with Coinbase, and Sberbank structured bonds signal that custody-grade integration into TradFi is the next unlock readers are tracking.

- 06DAO integration politics

The Aave Chan Initiative's accusations around CowSwap and vault fee routing show readers are alert to integrations that quietly redirect protocol revenue away from token holders — governance capture dressed as technical partnership.

AI–Crypto Integration: Beyond the Buzzwords

Why AI and Blockchains Are Being Integrated

The convergence of AI and crypto is often marketed as inevitable, but the underlying integration logic is specific. Blockchains provide tamper‑resistant data stores, programmable value transfer, and transparent execution, while AI systems excel at extracting patterns, making predictions, and automating decisions under uncertainty. When combined thoughtfully, AI can act on verifiable onchain data and assets, while blockchains can provide audit trails for AI decisions and constrain what AI agents are permitted to do.

Enterprise‑focused commentary increasingly frames AI‑blockchain integration as a “strategic imperative” rather than an experiment, pointing to use cases in supply chains, healthcare, and finance where AI models can analyze blockchain‑verified data to drive automated workflows while the chain ensures verifiable integrity of the underlying records. In the crypto‑native world, AI‑powered trading agents and portfolio managers are already beginning to execute onchain strategies, while AI‑driven analytics tools interpret governance proposals, protocol risk, and onchain behavior for investors.

One concrete example is the partnership between infrastructure provider DGrid and the Stable ecosystem, where DGrid is supplying LLM infrastructure to power AI integration across applications built on Stable, with the stated goal of unlocking real‑world AI use cases that operate onchain. This kind of integration embeds AI inference directly into dapps, allowing, for example, conversational interfaces for DeFi protocols, automated risk scoring for wallets, or intelligent routing of trades across venues. On centralized platforms, Coinbase’s AI integrations signal a similar direction, adding AI‑driven insights, assistance, or risk alerts into exchange interfaces that already handle fiat, crypto, and, increasingly, tokenized securities.

However, research into AI‑linked crypto tokens injects a note of caution. Many so‑called “AI tokens” promise decentralized AI infrastructure or governance but rely heavily on centralized compute providers, closed‑source models, or small teams that retain effective control over parameter updates and system behavior. From an integration perspective, this means that while tokens may be deeply integrated into DeFi markets and exchanges, the underlying AI systems they purport to decentralize may not be meaningfully integrated into the trustless guarantees that blockchains provide.

Infrastructure, Energy, and Vertical Integration

On the infrastructure side, AI‑crypto integration is driving a form of vertical integration that looks different from financial integrations but is just as significant. Training and running large AI models require enormous amounts of energy and compute capacity, and there is growing interest in colocating AI data centers with renewable energy sources, a pattern familiar from Bitcoin mining. Soluna’s acquisition of the Briscoe wind farm for fifty‑three million dollars, which gave it full ownership of the renewable generation feeding its Project Dorothy data center, is a prime example. By owning both the power source and the data‑center infrastructure, Soluna aims to provide competitively priced, sustainable compute capacity for AI workloads while retaining tighter control over operating costs and risk.

Vertical integration of this kind creates new linkages between energy markets, carbon policy, AI infrastructure, and potentially crypto mining or rollup sequencer operations that share the same facilities. If AI training jobs, proof‑of‑work mining, and DeFi transaction sequencing all run on the same vertically integrated infrastructure, failures or regulatory interventions in one domain can spill over into others. Integration at the physical and energy level, in other words, complements digital integration but also creates new systemic dependencies.

Token projects promising onchain access to AI compute, data, or models must integrate these realities. Claims about “decentralized AI” that do not grapple with the concentration of data‑center ownership, model governance, and regulatory obligations around AI safety risk misrepresenting the actual trust model. Proper integration would involve not only wiring payments and access control through smart contracts but also aligning transparency about model behavior, safety constraints, and offchain infrastructure resilience with onchain governance mechanisms.

Risks: Security, Scalability, and Disinformation

AI‑blockchain integration also magnifies familiar risks. From a security standpoint, delegating control of wallets, trading strategies, or governance votes to AI agents increases the blast radius of model errors and adversarial attacks. Projects experimenting with AI‑built Monero integrations, where AI tools generate or manage code for privacy‑focused cryptocurrencies, are already encountering both security vulnerabilities and regulatory pushback, given that errors in privacy tooling or compliance logic can have severe consequences. These challenges echo more general concerns in the AI‑security community about automated code generation and autonomous agents.

Scalability is another friction point. Sophisticated AI agents that monitor onchain data in real time, evaluate complex strategies, and coordinate across multiple chains and protocols impose heavy computational and bandwidth demands on both offchain infrastructure and onchain networks. Analyses of AI‑blockchain integration highlight that without careful design—such as offloading heavy computation offchain while keeping minimal, verifiable commitments onchain—systems can become either too slow or too expensive to be practical. Network‑level visions, such as Sui’s ambition to re‑architect parts of its stack to support a trillion‑dollar AI agent economy, underline both the opportunity and the risk: tailoring base‑layer architectures too aggressively around one integration thesis can create compatibility and governance challenges later.

The information environment is a third area where AI and blockchains intersect in complicated ways. The World Economic Forum has warned that advanced AI and synthetic media are accelerating disinformation, creating a global crisis that undermines trust in democracies and institutions. As AI‑generated video integrates natively into social media feeds, the risk of deepfakes and cognitive manipulation rises dramatically, prompting calls for “narrative inoculation” strategies and better verification tools. Blockchains are often proposed as part of the solution, through content provenance systems that record hashes of media at creation time, enabling verification of later copies or edits. But integrating such verification infrastructure into user platforms, identity systems, and legal frameworks is a major challenge in itself.

Crypto projects working on AI‑video provenance or reputation systems are therefore engaged in a complex integration exercise: they must connect AI content detection, onchain identity attestations, oracle‑fed real‑world data, and platform moderation policies in ways that preserve privacy and free expression while mitigating harm. This is a far cry from merely “tokenizing AI”; it is a socio‑technical integration problem that spans multiple domains.

Compliance, Data, and Workflow Integration

Blockchain as Compliance Infrastructure

One of the less glamorous but most important integration frontiers is compliance. As regulatory expectations around digital assets mature, institutions are exploring how to integrate blockchains into their compliance architectures rather than treating them as opaque risk pools. Commentary from the regtech sector emphasizes that blockchains’ tamper‑proof records can help organizations maintain the integrity of compliance data and reduce the risk of fraud and errors in areas like shareholder voting, transaction monitoring, and audit trails. In effect, the ledger itself becomes part of the compliance system, not just a transaction log.

However, integrating DeFi and crypto activity into compliance workflows is challenging. A major OECD study on the limits of DeFi for financial inclusion notes that despite DeFi’s theoretical openness, barriers such as technical complexity, volatility, and weak consumer protections currently limit its usefulness for underserved populations. From a compliance perspective, pseudonymity and composability complicate KYC and transaction‑monitoring obligations, while the global, permissionless nature of DeFi protocols makes enforcement inherently cross‑border. Integration, therefore, often means building layered identity and analytics services on top of open protocols, rather than trying to retrofit traditional banking compliance models directly onto them.

Stablecoins again sit at the intersection of these forces. TRM Labs’ analysis of stablecoin usage and its global crypto policy review highlight that regulators and law‑enforcement agencies are increasingly focusing on stablecoin flows, given their central role in onchain activity and their potential use for both legitimate payments and illicit finance. Integrating stablecoins into regulated payment and banking frameworks requires robust travel‑rule compliance, sanctions screening, and transaction‑monitoring capabilities, often delivered by specialized analytics firms that ingest onchain data and offchain identities. In this sense, regtech providers themselves are becoming integration layers between transparent blockchain data and traditional compliance dashboards.

Data Fabrics, Zero‑Copy Integration, and Crypto Analogies

The enterprise software world is grappling with similar integration problems around data access, governance, and AI. ServiceNow’s expansion of its Workflow Data Fabric through a new integration with Oracle’s Autonomous Database illustrates emerging patterns: zero‑copy data sharing and bi‑directional data exchange allow real‑time, secure access to data across transactional, analytical, vector, document, spatial, and graph formats, all governed by rules and guardrails on how data is accessed, used, and monitored. Oracle’s converged database platform, in turn, enforces strong security and access controls while automating functions such as encryption, logging, and threat detection.

These architectural choices have clear analogues in crypto. Onchain data layers, indexing services, and subgraphs function as a kind of open data fabric for DeFi, while offchain analytics and AI tools query that fabric for risk, compliance, and business intelligence. The move toward zero‑copy data access—in which multiple applications can act on the same underlying datasets without pulling and replicating them—mirrors the blockchain ethos of a single shared source of truth, even as privacy and data‑sovereignty concerns force developers to blend public and permissioned data sources. As AI agents become more prominent in crypto, integrating them with these data fabrics while maintaining strong access controls and audit capabilities will become critical.

The ServiceNow‑Oracle integration also underscores the importance of granular governance around data access, something that will be essential as onchain financial data becomes more sensitive. Governance tokens and DAOs focusing on privacy‑preserving identity solutions, RWA registries, or compliance‑oriented infrastructure will need to encode detailed access policies and monitoring logic into their contracts and offchain legal agreements. Integration, in this sense, is as much about embedding governance norms into code as it is about linking APIs.

Workflow Automation and AI Agents in Financial Operations

As integration layers mature, the next step is workflow automation. In enterprise settings, AI‑driven platforms orchestrate processes across CRM systems, ERP databases, and communication tools, using data fabrics as the backbone. In crypto, the analogous vision involves AI agents that manage wallets, rebalance DeFi portfolios, respond to governance proposals, or optimize tax positions, all while coordinating between onchain protocols and offchain information sources.

Projects like Stable, which is integrating LLM infrastructure from DGrid to power AI across its applications, are early attempts to operationalize this vision. By providing a unified AI layer integrated with onchain state, such ecosystems aim to let developers build agents and interfaces that can reason about portfolios, market conditions, and user preferences in natural language, then execute transactions or governance actions via smart contracts. The Claw Wallet–GoPlus SafuSkill integration, which focuses on embedding security checks into the AI agent stack, reflects growing recognition that automation must be paired with safety mechanisms to prevent reckless or malicious actions.

However, these integrations raise deep questions about accountability and decision‑making. If an AI agent misallocates a portfolio or votes for a harmful governance proposal, where does responsibility lie—with the model developers, the protocol integrators, or the user who deployed the agent? Research on AI‑linked tokens warns that many systems marketed as decentralized retain strong centralized control over model updates and access, meaning that real‑world accountability may rest with a small set of organizations even if governance tokens are widely distributed. Integrating AI into onchain workflows responsibly will require transparency about these control points and mechanisms for human override.

US Regulator Clears Banks to Intermediate Crypto Transactions, Marking Another Step Toward Tighter Integration of TradFi and Digital Assets

"The Office of the Comptroller of the Currency issued new guidance saying that banks can engage in what are known as "riskless principal" transactions that involve crypto assets and would not receive scrutiny from the regulator."

- 2023-08launch

PayPal launches pyUSD stablecoin on Ethereum

Circle deploys USDC natively on Cosmos via CCTP on Noble

- 2023-08launch

Alchemy debuts Account Kit for smart-account + social-login integration

- 2024-04milestone

EigenLayer mainnet opens restaking; Kraken completes integration

- 2024-11launch

Hyperliquid L1 mainnet launches, triggering wave of protocol integrations

- 2025-01launch

DEX Screener integrates Hyperliquid L1 orderbook

- 2025-02governance

Ethena governance proposal to integrate USDe and hedging engine on Hyperliquid EVM

- 2025-03launch

pyUSD goes cross-chain via LayerZero integration

Integration Challenges: Fragmentation, Liquidity, and Governance

Interoperability Limits and Technical Immaturity

Despite the proliferation of integration efforts, technical limitations remain a central bottleneck. Studies of blockchain deployment in supply chains, for example, note that scalability constraints, weak interoperability between different blockchain platforms, regulatory uncertainty, and the absence of common standards all inhibit widespread adoption, even when pilots succeed in controlled environments. The same structural issues affect DeFi and digital‑asset markets: different chains use different virtual machines, consensus mechanisms, and security assumptions, and bridges between them are often ad hoc, brittle, or insecure.

Efforts like Chainlink’s CCIP aim to provide standardized, risk‑managed cross‑chain messaging and token transfers, but the ecosystem is still early in converging on shared integration primitives. Experiments at the base‑layer level, such as Linea’s decision to chart a new course from an Ethereum‑compatible virtual machine toward a RISC‑V‑based architecture, illustrate both the possibilities and hazards of rapid innovation. While alternative architectures may offer performance or flexibility benefits, they also risk breaking compatibility with existing tooling, slowing integration with established DeFi protocols, and introducing complex migration challenges for users and developers accustomed to EVM semantics.

Technical immaturity also shows up in offchain‑onchain integration. Real‑world data feeds can be noisy, incomplete, or subject to manipulation, and even decentralized oracle networks must contend with data‑source selection, update frequency, and adversarial behavior. Integrations like “Using Tellor: Integration Workflow” emphasize robust verification and dispute mechanisms precisely because subjective data—such as credit scores, ESG metrics, or real‑world event classifications—cannot be treated as purely objective truths. Integrating such data into financial contracts requires not just technical bridging but also governance processes for handling disagreement.

Liquidity Fragmentation and Market Structure

Liquidity is the lifeblood of integration. Tokenization and protocol launches mean little if the resulting assets cannot be traded at scale or used as collateral. The RWA liquidity literature stresses that while tokenized asset issuance has grown rapidly, with more than twenty‑one billion dollars of RWAs deployed onchain by mid‑2025, most of this value remains fragmented across small pools and niche platforms, with limited use in mainstream DeFi protocols. Tokenized government bonds may trade reliably on a dedicated platform, but they are rarely accepted as collateral in high‑profile lending markets or integrated into automated portfolio allocators.

Stablecoins and blue‑chip DeFi tokens stand out as exceptions. Their deep integration across chains, exchanges, and applications creates a self‑reinforcing network effect: because they are accepted everywhere, they become even more liquid. TRM Labs’ estimate that stablecoins comprised about thirty percent of total crypto transaction volume in early 2025 highlights how dominant they have become as the medium of exchange and settlement asset in the crypto economy. Where widely used stablecoins like USDC and USDT are not integrated, users often perceive platforms as incomplete or high friction. This dynamic helps explain why integrating Tether into a chain’s native wallet, as in Plasma’s case, can significantly boost TVL and activity by making it easier for users to park and mobilize liquidity.

DEXs such as Hyperliquid show that integration‑driven liquidity growth is possible for newer venues as well. By tightly integrating derivatives markets, risk management, and onchain governance, and by connecting to broader ecosystems of wallets and analytics tools, Hyperliquid has drawn billions in net inflows and trillions in cumulative trading volumes in a relatively short period. But the broader market still suffers from fragmentation: many chains and protocols host isolated pools of liquidity that cannot be easily accessed or aggregated by users who do not wish to navigate complex bridging and wrapping steps.

Governance design influences these patterns. Proposals like TIP‑8, which introduces weETH into a tETH strategy to improve yield efficiency using existing post‑strategy capital, show how governance can drive deeper integration of liquid staking tokens and restaking strategies into protocol designs. Integrating assets like weETH into lending or restaking frameworks can unlock new collateral options and yield paths, but it also creates new dependencies and risk vectors, tying protocol health to the behavior of underlying staking and restaking markets.

Governance, Regulation, and Social Integration

Integration is not purely technical or economic; it also depends on governance structures and social adoption. The OECD’s work on DeFi and financial inclusion highlights that, despite the openness of DeFi protocols, their complexity, risk profile, and lack of consumer protections mean they are currently used mostly by relatively sophisticated, wealthier users, limiting their inclusion impact. Integrating DeFi into mainstream financial lives therefore requires governance choices that prioritize usability, education, and safety, not only composability and yield.

Regulatory integration shapes these choices. TRM Labs’ global crypto policy review notes that across 2025 and beyond, regulators are increasingly converging on themes such as stablecoin regulation, enforcement against illicit use, and the extension of travel‑rule requirements to VASPs and certain DeFi touchpoints. At the same time, jurisdictions differ in their tolerance for experimentation, resulting in a patchwork landscape where some projects gravitate toward more permissive hubs, while others seek the legitimacy of stricter regimes. Startale’s move into Abu Dhabi reflects a bet on the UAE’s efforts to position itself as a crypto‑friendly jurisdiction, even as integration risks and regulatory details remain to be fully resolved.

The rise of AI‑driven disinformation adds another layer. The WEF’s analysis of cognitive manipulation via AI stresses that resilience requires not just technical verification tools but also investment in community‑level systems of verification, deliberation, and accountability. Educational efforts that teach users to ask who is communicating with them, how they were targeted, what the sender stands to gain, and whether sharing a message could harm others are as much a part of “integration” as code changes. Crypto’s own history of scams and misinformation suggests that integrating robust social and educational frameworks into user experiences is essential if onchain systems are to serve broader populations safely.

How Builders Approach Integration in Practice

Designing Integration Paths for Oracles and Data

For developers, integration begins at the design stage. When building a DeFi protocol or application, teams must decide what data they need, which oracles to trust, and how to architect contracts so they can be safely upgraded and extended. Chainlink’s educational materials emphasize that oracles are not simply utilities but critical infrastructure whose correctness, availability, and security are mission‑critical because they determine payouts and application safety. Developers are encouraged to treat oracle integration as a first‑class design problem, evaluating node diversity, data‑source quality, update frequencies, and fallback mechanisms.

Guides like “Using Tellor: Integration Workflow” underscore similar priorities. Integrating an oracle that delivers subjective or dispute‑prone data requires protocols for challenging data, staking by reporters, and slashing ineffective or malicious actors. From a user’s perspective, these mechanisms may be invisible, but they shape the reliability of the protocol’s outputs—whether a liquidation occurs at the right price, whether an insurance payout is warranted, or whether a DAO resolution triggers. Good integration design therefore blends cryptoeconomic incentives with clear governance, not just APIs.

Builders also think ahead about future integrations. Architecting contracts with modularity in mind—for example, by separating core logic from oracle adapters—makes it easier to swap or add data providers over time. This is particularly relevant as more sophisticated data feeds, such as ESG scores, credit models, or AI‑generated risk metrics, become available. Integrating such feeds raises new questions about model governance and bias, which will need to be addressed both onchain and offchain.

Integrating with Ethereum and Other Base Layers

Launching a protocol on Ethereum or another base layer is itself an integration process. Developers must decide how deeply to integrate with existing DeFi primitives, which versions of token standards to support, and whether to target only one chain or multiple. Ethereum’s rich ecosystem of ERC‑20 and ERC‑1400‑style security tokens, or institutional‑grade standards for RWAs, means that new projects can often integrate with existing interfaces but must also ensure compatibility with evolving norms. On other chains, teams may need to build or port standards and liquidity pools from scratch, trading off speed against ecosystem depth.

Cross‑chain expansions introduce additional complexity. The Tria x Aptos integration shows how a protocol can bring hundreds of thousands of users and significant transaction volume into a new ecosystem by enabling cross‑chain spend, trade, and earn features that bridge multiple networks. But such integrations require careful handling of bridging risks, synchronizing state across chains, and adapting to different virtual machines and fee structures. When Linea, for instance, moves from an EVM‑centric design to a RISC‑V architecture, integrators will need to reassess tooling, auditing practices, and compatibility with existing smart contracts.

Governance decisions around asset integration also matter. The TIP‑8 proposal to integrate weETH into a tETH strategy, designed to improve yield efficiency by redeploying existing capital, shows how DAOs can use governance to deepen integration with liquid staking ecosystems. Similarly, PumpBTC’s interest in integrating Circle’s cirBTC, a tokenized Bitcoin product, highlights that base‑layer protocols, DeFi strategies, and custodial wrappers are becoming intertwined. Each integration delivers new yield or collateral options but also entangles protocols with the technical and regulatory profiles of those underlying assets.

Integrating AI into Crypto Products Responsibly

The current wave of AI‑crypto experimentation places additional responsibilities on builders. Integrating LLMs or other AI models into wallets, exchanges, or DeFi dashboards can dramatically improve user experience by providing conversational interfaces, risk summaries, or automated strategy suggestions. Projects like Stable, with DGrid providing the AI infrastructure layer, exemplify a model where a shared AI backend powers features across an ecosystem of applications. But integration must be done with clear boundaries: AI agents should be constrained in what they can execute without explicit user approval, and high‑risk actions should require additional safeguards.

Security‑oriented integrations like Claw Wallet’s SafuSkill collaboration with GoPlus show one path: embedding security checks as first‑class components in the AI agent stack. Before an AI agent signs a transaction or approves a contract interaction, the integrated security layer can assess contract risk, phishing signatures, or anomalous behavior patterns. Yet these systems themselves must be audited and subject to oversight, because flaws or biases in the security layer could block legitimate activity or, worse, provide a false sense of safety.

Research into AI‑linked tokens suggests that many projects overstate the degree of decentralization in their AI infrastructure, highlighting that token distribution alone does not guarantee decentralized control over models or data. Builders who aim to integrate AI into onchain governance or financial decision‑making need to be transparent about where control and responsibility actually reside: who can update the model, who can shut it down, and how disputes over AI behavior will be resolved. In some cases, the appropriate integration model may involve retaining significant human oversight and offchain governance processes rather than fully automating decisions onchain.

Every integration adds a new dependency path; a single vulnerable adapter in a multi-protocol stack (e.g. Curve LLAMMA + lending market + bridge) can cascade losses across all composing protocols.

LayerZero underpins pyUSD cross-chain, USDV, and Libre Capital's 120-chain reach simultaneously — a single exploit or censorship event in that messaging layer would freeze liquidity across all three ecosystems at once.

Visa, PayPal, Revolut, and Italian bank integrations bring stablecoin flows under existing payment-services law in the EU and US, increasing the probability of mandatory KYC cutoffs propagating into formerly permissionless DeFi surfaces.

- Liquidity concentrationMedium

Multiple protocols routing liquidity through Hyperliquid L1 creates a single-venue concentration risk; a liquidity crisis or governance failure on Hyperliquid would simultaneously impair DEX Screener data, Ethena's hedging engine, and MetaMask swap routes.

- Counterparty / protocol dependencyMedium

Integrations like Convergence + Convex + Frax create deep dependency chains where a governance decision or token-incentive change by one protocol directly breaks the economics of its downstream integrators.

Google Cloud GCUL and Meta stablecoin exploration signal big-tech entry, which historically accelerates regulatory intervention; the US executive order framework for digital financial technology sets the stage for compliance requirements that could gate institutional integration pipelines.

Outlook

Integration has always been crypto’s underlying story, but the stakes are now significantly higher. Stablecoin integration has turned blockchains into serious contenders for global payments and settlement, with fiat‑backed tokens like USDC and USDT acting as the connective tissue between traditional banking systems and DeFi. Tokenization efforts are rapidly wrapping real‑world assets in onchain form, even if integration of those tokens into mainstream DeFi remains stubbornly incomplete. In parallel, AI‑driven agents and analytics are beginning to integrate with wallets, exchanges, and protocols, promising new efficiencies but also introducing fresh security and governance risks.

Regulators are moving from reactive enforcement toward more structured integration strategies. Thailand’s pivot to market expansion and institutional integration, the EU’s MiCA framework and DeFi consultations, and the United States’ emphasis on stablecoin regulation without a CBDC all point to a future in which digital assets are neither fully outside nor fully inside the traditional system but integrated selectively into specific functions. How these integrations are designed—who can issue which tokens, how disclosures and safeguards are enforced, and how cross‑border activity is handled—will shape whether crypto’s benefits diffuse broadly or remain confined to specialized niches.

By 2030, if optimistic projections hold, tokenized real‑world assets could represent a non‑trivial share of global GDP, and integrated AI‑crypto systems could underpin everything from supply‑chain finance to retail investment platforms. But realizing that vision will require sustained work on the unglamorous parts of integration: standardizing data and token formats, hardening cross‑chain messaging, embedding robust compliance and identity layers, and educating users about both the power and the limits of autonomous, AI‑enhanced finance. Integrations that prioritize resilience, transparency, and user agency are likely to endure; those that chase short‑term hype while ignoring governance and risk will probably falter.

For builders, investors, and policymakers, the key question is no longer whether to integrate with crypto, but how. The answers will determine whether Ethereum, stablecoins, AI agents, and platforms from Hyperliquid to Coinbase and beyond coalesce into a more open, efficient financial and information infrastructure—or fragment into incompatible, risky silos. Watching the next wave of integration headlines with this deeper lens will help distinguish structural change from surface‑level marketing.

Latest Integration news

The US may have banned a CBDC, but through stablecoin regulation, 1:1 reserves, & institutional integration, stablecoins become America's de-facto digital dollar.Aave Chan Initiative Accuses Aave Labs of Diverting DAO Revenues and Privatizing Protocol Economics, Demands Clarity on CowSwap Integration, Vault Fees, Horizon Deals, and V4 Liquidation Engine Incentives.US Regulator Clears Banks to Intermediate Crypto Transactions, Marking Another Step Toward Tighter Integration of TradFi and Digital AssetsLlamaRisk Insights: GHO’s backing and RWA integration, a portfolio analysis.Yearn developer Schlag gives feedback on basic onchain integration of Uniswap V4 and their universal routerWoori Bank has become the first Korean commercial bank to display Bitcoin prices in its main trading room, signaling BTC’s growing role in market sentiment. The move comes as Korean banks deepen digital asset integration and prepare for tighter regulations.Sources

- https://www.circle.com/usdc

- https://www.proxymity.io/views/the-future-of-compliance-emerging-regtech-trends/

- https://chain.link/education/blockchain-oracles

- https://www.hilbert.group/en/tokenization-of-real-world-assets/

- https://www.instagram.com/reel/DZFr_pmBIyD/

- https://www.oecd.org/content/dam/oecd/en/publications/reports/2024/03/the-limits-of-defi-for-financial-inclusion_11aad057/f00a0c7f-en.pdf

- https://arxiv.org/html/2505.07828v1

- https://www.trmlabs.com/reports-and-whitepapers/2025-crypto-adoption-and-stablecoin-usage-report

- https://www.crowdfundinsider.com/2026/06/286035-coinbase-announces-new-features-tokenized-stocks-ai-integration-more/

- https://www.sciencedirect.com/science/article/pii/S2772503025000192

- https://arxiv.org/html/2508.11651v1

- https://newsroom.servicenow.com/press-releases/details/2025/ServiceNow-expands-Workflow-Data-Fabric-capabilities-with-new-Oracle-integration-01-29-2025-traffic/default.aspx

- https://x.com/Stable/status/2044787438531580147

- https://aptosnetwork.com/currents/tria-decibel-perpetuals

- https://www.trmlabs.com/reports-and-whitepapers/global-crypto-policy-review-outlook-2025-26?scLang=en

- https://sisgain.com/blogs/blockchain-ai-future-of-business

- https://www.solunacomputing.com/news/soluna-acquires-briscoe-wind/

- https://www.weforum.org/stories/2026/03/how-cognitive-manipulation-and-ai-will-shape-disinformation-in-2026/

- https://www.whitehouse.gov/presidential-actions/2025/01/strengthening-american-leadership-in-digital-financial-technology/

- https://www.crowdfundinsider.com/2026/06/285124-thailands-crypto-regulation-shifts-toward-market-expansion-and-institutional-integration/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…