Deep explainer on PYUSD, PayPal’s regulated dollar stablecoin issued by Paxos, covering its design, reserves, global rollout, multi‑chain and DeFi integrations, competition with USDC/USDT, risks, and role in future stablecoin payments.

+7 sources across the wider coverage universe

Spark seeds Uniswap v4 with $150M in USDS-PYUSD and USDS-USDT liquidity for stablecoin FX layer2026-06

Spark seeds Uniswap v4 with $150M in USDS-PYUSD and USDS-USDT liquidity for stablecoin FX layer2026-06 PayPal takes PYUSD global, expanding its stablecoin from two countries to 70 in one shot2026-03

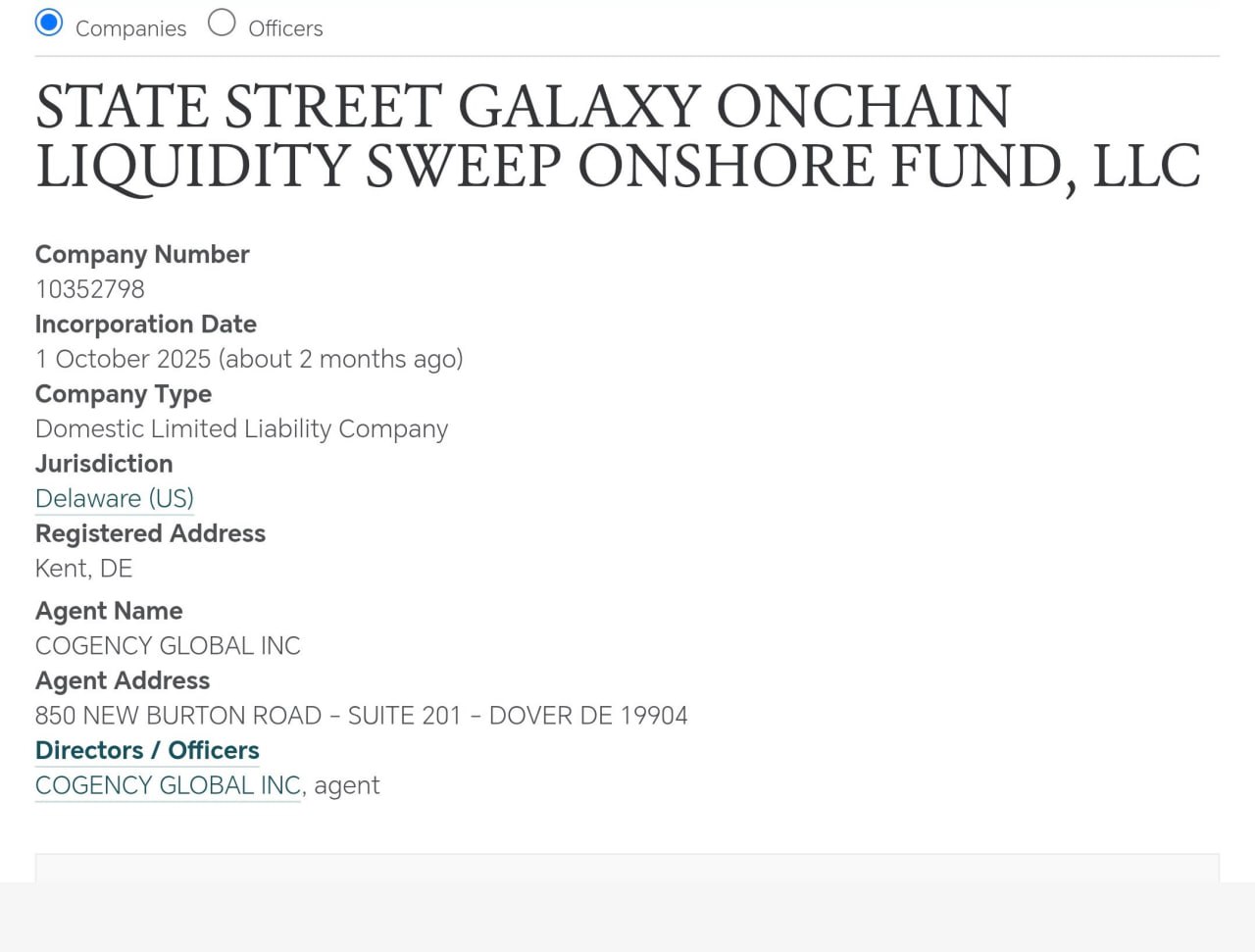

PayPal takes PYUSD global, expanding its stablecoin from two countries to 70 in one shot2026-03 State Street and Galaxy to launch tokenized liquidity fund, SWEEP on Solana in 2026. The fund will run on Solana at launch and use PYUSD. Ondo Finance committed about $200 million to seed the tokenized liquidity fund, which will later expand to other chains.2025-12

State Street and Galaxy to launch tokenized liquidity fund, SWEEP on Solana in 2026. The fund will run on Solana at launch and use PYUSD. Ondo Finance committed about $200 million to seed the tokenized liquidity fund, which will later expand to other chains.2025-12 Paypal's $pyUSD goes cross chain with a Layer Zero integration2024-11

Paypal's $pyUSD goes cross chain with a Layer Zero integration2024-11 PayPal Ventures utilizes stablecoin for investment in Mesh crypto transfer platform as PYUSD deploys on Aave and Curve.2024-01

PayPal Ventures utilizes stablecoin for investment in Mesh crypto transfer platform as PYUSD deploys on Aave and Curve.2024-01 PayPal USD has launched on Solana, 2nd blockchain to support PYUSD after Ethereum2024-05

PayPal USD has launched on Solana, 2nd blockchain to support PYUSD after Ethereum2024-05

PYUSD: PayPal’s Dollar Stablecoin, Explained

PayPal USD (ticker: PYUSD) is a U.S. dollar stablecoin issued by Paxos Trust Company and distributed through PayPal and Venmo, designed to maintain a 1:1 value with the U.S. dollar while moving natively on public blockchains. Backed by cash, U.S. dollar deposits, and short‑term U.S. Treasuries with regular third‑party attestations, it sits at the intersection of mainstream fintech payments and on‑chain finance, expanding across multiple networks, integrating into card settlement and DeFi infrastructure, and raising new questions about how regulated stablecoins will reshape digital payments worldwide.

Introduction: Why PYUSD Matters

Stablecoins have evolved from a niche trading tool on crypto exchanges into one of the core building blocks of digital finance, underpinning remittances, DeFi lending markets, tokenized treasuries, and cross‑border commerce. Within that landscape, PYUSD is distinctive because it is the first major U.S. dollar stablecoin launched in partnership with a global consumer payments brand that already serves hundreds of millions of users. Unlike crypto‑native issuers that built their user bases from scratch, PayPal can introduce PYUSD directly into its existing wallet, merchant, and checkout rails, and then extend the same token onto open blockchains where it can be used alongside USDC, USDT, and decentralized stablecoins. That dual identity, both inside a closed consumer app and as an on‑chain asset, is what makes PYUSD strategically important.

At a technical level, PYUSD is a fiat‑backed, custodial stablecoin: for each PYUSD token in circulation, Paxos holds an equivalent amount of U.S. dollar cash, bank deposits, and short‑term U.S. Treasury instruments in segregated reserves. The token is minted and burned through a traditional “mint‑and‑redeem” mechanism rather than an algorithmic structure, aiming to keep its market price anchored near one dollar by allowing large holders to arbitrage deviations via issuance and redemption. Legally, it is issued by Paxos Trust Company, a nationally chartered trust company supervised by the U.S. Office of the Comptroller of the Currency (OCC), which also issues the USDP stablecoin and previously issued BUSD for Binance. PayPal, for its part, operates as a distributor and user interface, integrating PYUSD into the PayPal and Venmo apps while leaving reserve management and token issuance to Paxos.

Since its launch in August 2023, PYUSD has progressed from a single‑chain, U.S.‑only product to a multi‑chain, multi‑region stablecoin with a circulating supply that peaked above four billion dollars before retracing, even as stablecoin market growth overall has slowed. It debuted on Ethereum, expanded to Solana in 2024, and then to Stellar and additional networks via cross‑chain messaging frameworks, while PayPal broadened access from the United States and United Kingdom to around seventy markets across Asia‑Pacific, Europe, Latin America, and North America. That expansion coincides with deeper integration into payment and capital‑markets infrastructure, from being spendable anywhere WalletConnect Pay is supported to being included in Mastercard’s stablecoin settlement program and targeted for a one‑billion‑dollar liquidity partnership with Maker‑aligned protocol Spark.

At the same time, PYUSD enters a competitive field dominated by Tether’s USDT and Circle’s USDC, with decentralized alternatives like DAI and newer dollar‑pegged designs vying for mindshare and liquidity. Stablecoin supply has surpassed three hundred billion dollars, but growth has decelerated, and recent data show Tether adding billions in supply while other stablecoins, including USDC and PYUSD, have contracted over shorter windows. This dynamic underscores that even for a brand as large as PayPal, success in stablecoins is not guaranteed; it will depend on trust, liquidity, regulatory clarity, and compelling use cases that go beyond simple dollar substitution.

The following sections examine PYUSD in depth: its technical and legal architecture, reserve design, network expansion, integration into PayPal’s ecosystem and DeFi, its position relative to USDC and USDT, and the risks and policy debates surrounding its rapid global rollout. The goal is to provide an evergreen, critical explainer that can serve as a reference point as PYUSD and stablecoin payments continue to evolve.

How Paypal Is Racing To Keep Its Lead In Stablecoins With PYUSD

Less than 1% of stablecoin activity is actual payments, so PayPal has the one distribution channel most issuers are still trying to fake: merchant checkout. PYUSD is only ~$2.7B outstanding on DeFiLlama, mostly Ethereum/Solana/Arbitrum, but a 4% in-app reward and rollout to ~70 markets can turn dormant wallet balances into subsidized settlement inventory. DeFi adoption is the weak leg; without deeper routing, lending, and collateral markets, PYUSD remains PayPal balance-sheet plumbing with a token wrapper.

Readers click every new PYUSD chain or country launch as a discrete event — yet the skepticism pieces (sluggish Nansen growth, 90% exchange-held supply, usability concerns) also land, revealing that our audience is tracking distribution velocity while actively questioning whether any of it translates to real circulation.↗

From Concept to Launch: How PYUSD Emerged

PayPal’s Stablecoin Strategy

PayPal’s entry into stablecoins reflects a broader strategic shift among payment networks and large financial platforms: instead of viewing crypto as a separate asset class, they increasingly see tokenized dollars and treasuries as infrastructure for faster, more flexible settlement. PayPal had already added buy‑and‑sell functionality for major cryptocurrencies like Bitcoin and Ethereum before moving to create a branded dollar token that could underlie payments, remittances, and crypto trading within its ecosystem. By working with a regulated issuer rather than directly issuing the token itself, PayPal adopted a model that leverages its consumer distribution while outsourcing the regulated custody and reserve management to a specialist.

The decision to partner with Paxos was not incidental. Paxos had already established credibility as a regulated trust company issuing fiat‑backed stablecoins, including USDP and the now‑wound‑down BUSD, and had experience dealing with both crypto‑native and institutional clients. In December 2025, Paxos converted its New York limited‑purpose trust charter into a national trust charter supervised by the OCC, formalizing its status as a national trust company and allowing it to operate under a single federal charter across the United States. For PayPal, this arrangement created a neatly separated risk profile: Paxos would hold the reserves as segregated customer property and manage issuance and redemptions, while PayPal would focus on user experience, distribution, and tying PYUSD into its other products.

From a regulatory narrative standpoint, launching a stablecoin under this model allowed PayPal to emphasize that PYUSD is “U.S. federally regulated,” backed 1:1, and subject to monthly attestation, positioning it as a conservative design relative to algorithmic or partially collateralized stablecoins that have suffered de‑pegging events. This framing aimed both at regulators wary of systemic risk and at mainstream users who may be less familiar with on‑chain risks but intuitively understand the concept of a digital dollar stored with a regulated trust company.

Launch on Ethereum

PYUSD launched in August 2023 as an ERC‑20 token on the Ethereum mainnet, which remains the canonical chain for issuance. Ethereum offered a mature ecosystem of exchanges, wallets, and DeFi protocols, as well as robust infrastructure for compliance features like blacklisting and snapshotting balances when needed. From a technical perspective, using Ethereum as the primary issuance chain enabled Paxos to build on its existing experience issuing USDP on Ethereum, including how to design smart contracts with appropriate administrative controls and monitoring.

In the early months, most PYUSD activity remained tied to PayPal’s own interface. Users in the United States could buy PYUSD with dollars in their PayPal balance or linked payment methods, send it to other PayPal users, and transfer it out to external crypto wallets supporting Ethereum. Venmo integration followed, creating another on‑ramp to the token for a younger and more social user base, although that rollout occurred gradually across user segments and geographies. Meanwhile, centralized exchanges such as Coinbase listed PYUSD trading pairs, creating off‑PayPal avenues for price discovery and liquidity against other stablecoins and cryptocurrencies.

Technically, each time a PayPal user buys PYUSD, PayPal routes dollars to Paxos, which then mints an equivalent amount of PYUSD tokens and sends them either to PayPal’s omnibus wallets or directly on‑chain as appropriate. When users redeem, the reverse process occurs: tokens are burned, and dollars are released back to PayPal or the user’s bank account. This mint‑and‑burn mechanism is the core stabilizing force behind PYUSD’s dollar peg; as long as arbitrageurs can profitably mint or redeem when market prices deviate from one dollar, the token should gravitate back toward parity.

Expansion to Solana, Stellar, and Beyond

After establishing a base on Ethereum, PayPal and Paxos began extending PYUSD across faster and cheaper networks to support consumer‑grade payments and DeFi use cases where Ethereum’s fees and latency could be a barrier. In May 2024, PayPal announced that PYUSD would be available on the Solana blockchain, emphasizing Solana’s high throughput and low transaction costs as an advantage for smaller retail transactions. Crypto.com, Phantom, and Paxos were among the first partners to provide on‑ramps to PYUSD on Solana, enabling users to acquire and transfer the token natively on that chain.

In June 2025, PayPal followed with plans to make PYUSD available on the Stellar network, positioning Stellar as a platform for new use cases such as cross‑border payments and business‑to‑business settlement. Stellar has long focused on remittances and fiat‑backed tokens, and bringing PYUSD there signaled an intent to plug into existing corridors and partners already leveraging Stellar for dollar‑linked transfers. Around the same time, Paxos and PayPal also pursued cross‑chain expansion via LayerZero’s messaging protocol, which by 2026 connected PYUSD to additional networks including Arbitrum and other high‑throughput chains.

An ecosystem of secondary integrations grew in parallel. Flow, a network originally known for NFT applications such as NBA Top Shot, emerged as a growing hub for dollar stablecoins, with on‑chain data showing that PYUSD had become one of the significant stablecoin positions there. Public metrics highlighted that Flow’s stablecoin supply reached new highs and that Flow had become a notable network for PYUSD activity, underscoring how the token was being picked up beyond its original Ethereum and Solana contexts. This multi‑chain distribution allows users and protocols to choose the network that best fits their needs while still settling in the same branded dollar asset.

Global Rollout Across Seventy Markets

On the distribution side, the biggest milestone came in March 2026, when PayPal announced that PYUSD would be available to users in around seventy markets through the PayPal account. Previously, access had been largely limited to U.S. users and, later, to the United Kingdom and Singapore, with differing functionality by region. The expansion added coverage across Asia‑Pacific, Europe, Latin America, and North America, including countries such as Colombia, Peru, Singapore, Guatemala, and the Faroe Islands, among many others. PayPal indicated that users in the remaining supported markets would gain access over the following weeks, effectively transforming PYUSD from a two‑country product into a global one in a single strategic move.

The details of what users can do with PYUSD still vary by jurisdiction, reflecting local regulatory constraints and PayPal’s risk assessments. In the United States, users can buy, sell, send, receive, move PYUSD via crypto transfers, and earn rewards on their balances if they opt in and meet eligibility criteria. In the United Kingdom, functionality is more limited, currently focusing on buy and sell without the ability to send or receive PYUSD to external wallets. Singapore supports buying, selling, sending, and receiving, while a number of smaller markets support buying, sending, receiving, and PYUSD rewards but no ability to sell back into local currency. This patchwork reflects the complexity of offering a regulated stablecoin across diverse legal regimes, but the overarching message is that PYUSD is transitioning from a U.S.‑centric experiment to a global payment and savings instrument.

The global expansion coincided with PYUSD’s market capitalization topping four billion dollars, according to contemporaneous reporting, before later settling closer to three and a half billion. That growth represented more than a fivefold increase in supply over the prior year, highlighting both organic user adoption and increased on‑chain liquidity as more exchanges, DeFi protocols, and institutional partners integrated the token. However, subsequent months saw net outflows from several non‑Tether stablecoins, including PYUSD, underscoring that growth is not linear and that users actively rotate between stablecoins based on yields, perceived safety, and utility.

Issuer, Reserves, and Regulatory Architecture

Paxos as Issuer and Custodian

A central feature of PYUSD’s design is the separation between issuer and distributor. Paxos Trust Company, not PayPal, is the legal issuer of PYUSD and the entity that holds the reserves backing the token. Structured as a national trust company under an OCC charter, Paxos operates under U.S. federal oversight, with fiduciary obligations to safeguard customer assets and to segregate them from its own corporate balance sheet. This structure is similar to how regulated custodians handle securities and other client assets, and it is meant to ensure that PYUSD reserves would be treated as customer property in the event of Paxos’s insolvency.

Paxos’s track record with stablecoins is a key part of PYUSD’s story. It issues USDP (Pax Dollar), another U.S. dollar‑backed stablecoin, and it previously issued BUSD in partnership with Binance before winding that token down after regulatory scrutiny. This history gives Paxos operational experience with reserve management, minting and redemption flows, and the compliance obligations that come with being a U.S.‑regulated fiat token issuer. At the same time, it means that Paxos and its products are on regulators’ radar, which can be both a source of scrutiny and a signal of legitimacy.

For PYUSD, Paxos is responsible for minting new tokens when it receives dollars for issuance, burning tokens when users redeem, managing the investment of reserves, and publishing monthly transparency reports and attestations. PayPal, by contrast, is a large customer and distributor: it funnels user orders to Paxos, integrates PYUSD into its UI and APIs, and handles much of the end‑user onboarding, KYC/AML, and customer support. This delineation has legal consequences: PYUSD tokens held in self‑custody wallets represent direct claims on Paxos’s reserves, whereas PYUSD held inside a PayPal or Venmo account is also subject to PayPal’s own terms of service and risk controls.

Reserve Composition and Transparency

The credibility of any fiat‑backed stablecoin rests on the quality and transparency of its reserves. Paxos and PayPal describe PYUSD as being fully backed 1:1 by cash, U.S. dollar deposits, and short‑term U.S. Treasuries and Treasury reverse repurchase agreements, with no exposure to commercial paper, corporate bonds, or crypto collateral. This is a deliberately conservative reserve profile, mirroring the trend among U.S.‑regulated stablecoins to avoid riskier assets in response to past controversies over opaque reserves.

Paxos publishes monthly reserve reports and third‑party attestations for the digital assets it issues, including PYUSD, USDP, and others. These reports break down the composition of holdings and confirm that total notional reserves exceed or match the outstanding token supply on each reporting date. The use of short‑term U.S. Treasuries and overnight reverse repos allows Paxos to earn interest on the backing assets while maintaining high liquidity, since those instruments can be liquidated quickly in normal market conditions to meet redemption requests. Cash and bank deposits, meanwhile, cover shorter‑term needs and provide operational flexibility.

The absence of commercial paper and longer‑duration credit instruments is significant given that some earlier stablecoins came under scrutiny for holding opaque or risky corporate debt. By emphasizing a narrow set of high‑quality, short‑duration U.S. government instruments and cash, PYUSD aligns itself with a “narrow bank” style of reserve management, where capital preservation and liquidity are prioritized over yield. That does not mean there is no yield to capture; short‑term Treasury rates have been elevated in recent years, which in turn creates room for Paxos and PayPal to share some of the interest income with users via reward programs while retaining a margin for themselves.

Peg Mechanism and Contrast with Algorithmic Stablecoins

PYUSD’s peg to the U.S. dollar is enforced through a straightforward fiat‑collateralized model. When demand for PYUSD rises, users can bring dollars to PayPal or directly to Paxos, which in turn mints new tokens and adds the incoming dollars to the reserve portfolio. When demand falls or users wish to exit, they can redeem tokens for dollars, at which point Paxos burns the corresponding tokens and draws on reserves to satisfy the redemption. This linear relationship between supply and reserves is the core of the 1:1 backing claim.

In liquid markets, the existence of this mint‑and‑redeem pathway helps keep the secondary market price of PYUSD close to one dollar. If PYUSD trades below one dollar, arbitrageurs can buy tokens at a discount and redeem them with Paxos or via PayPal at par, capturing the spread and reducing circulating supply. If it trades above one dollar, they can mint new tokens for one dollar each and sell them on the open market at a slight premium, increasing supply until the price returns toward parity. While frictions such as fees, KYC requirements, and redemption minimums can prevent perfect arbitrage, this mechanism has historically been effective at stabilizing fiat‑backed stablecoins under normal conditions.

This model stands in contrast to algorithmic or partially collateralized stablecoins that rely on mint‑and‑burn relationships with volatile crypto assets or on reflexive demand dynamics. Those designs can offer higher capital efficiency but have proven vulnerable to death spirals when confidence is lost, as seen in the collapse of TerraUSD. By tying PYUSD’s obligations to a concrete reserve of cash and Treasuries managed by a regulated trust company, Paxos and PayPal seek to minimize such reflexive risk and present PYUSD as a low‑volatility, high‑trust instrument anchored firmly in the traditional financial system.

Relationship Between Paxos and PayPal

The division of roles between Paxos and PayPal has practical implications for risk, user experience, and even the token’s survival scenarios. Since reserves are held by Paxos as segregated customer property, PYUSD tokens should remain redeemable even if PayPal were to exit the business or suffer financial distress. In that scenario, users holding PYUSD in self‑custody could interface directly with Paxos for redemption, while users whose tokens are custodied by PayPal would need to rely on PayPal’s solvency and operational continuity until transfers could be made.

In everyday use, however, most retail users will interact only with PayPal and Venmo. They will trust these brands to reflect their on‑chain PYUSD balances correctly, to process transfers and redemptions, and to manage issues like fraud, disputes, or mistaken payments. From their perspective, PYUSD inside PayPal behaves less like a bearer token and more like a balance entry in a regulated financial app, even though under the hood it corresponds to actual ERC‑20 or equivalent tokens on various networks. This dual layering—on‑chain token plus platform ledger—creates both flexibility and complexity in how ownership and legal claims are structured.

The Paxos‑PayPal architecture also shapes how compliance features are implemented. As a regulated trust company, Paxos retains the ability to freeze or blacklist specific PYUSD addresses at the smart‑contract level when required by law, much like other fiat‑backed stablecoin issuers do. PayPal adds another layer of control at the account level, where it can restrict accounts suspected of fraud, sanction violations, or other prohibited activity, independently of Paxos’s on‑chain controls. Understanding these layers is important for users and developers who might assume that a dollar stablecoin on a public blockchain is as censorship‑resistant as native assets like ETH or BTC, which is not the case for PYUSD.

- 01Cross-chain expansion velocity↗

Each new chain (Solana, Arbitrum, nine LayerZero chains via PYUSD0) was treated as a standalone news event, generating repeated clicks and signaling readers are monitoring PYUSD's multichain footprint in real time.

- 02DeFi protocol integrations↗

Aave onboarding, Curve pool additions, Spark's $1B liquidity deal, and Llama Risk's crvUSD review collectively show readers care whether PYUSD earns real DeFi legitimacy, not just brand placement.

- 03Adoption vs. distribution gap↗

The Nansen 'sluggish growth / 90% exchange-held' headline and usability/gas-fee concern pieces drew strong clicks despite being contrarian, confirming readers distinguish between supply issuance and actual on-chain usage.

- 04Global retail reach and rewards↗

The 70-country expansion and 3.7% annual rewards program headlines show readers are watching whether PayPal can convert its 400M-user base into stablecoin holders, not just crypto-native adopters.

- 05Regulatory clearance signal

The SEC closing its PYUSD inquiry without enforcement action was a clear market-structure signal that drew clicks from readers assessing whether PayPal's stablecoin faces existential legal risk.

- 06Institutional and TradFi rails

State Street/Galaxy's $200M-seeded tokenized fund on Solana using PYUSD, plus Visa and Coinbase partnerships, attracted readers tracking whether PYUSD can bridge traditional finance infrastructure.

PYUSD Inside PayPal and Venmo

User Experience and Core Functions

Within the PayPal and Venmo apps, PYUSD is presented as a familiar, dollar‑denominated asset that users can buy, hold, send, and sometimes spend, sitting alongside balances in local currency and other cryptocurrencies. PayPal’s product pages emphasize that PYUSD is redeemable 1:1 for U.S. dollars and that users can move between dollars, PYUSD, and other crypto assets within the PayPal wallet. For users accustomed to fiat balances, PYUSD functions like a crypto‑enabled dollar balance that can be extended onto public blockchains when needed.

Buying PYUSD typically involves funding a PayPal account with a linked bank account, card, or existing balance and then converting those dollars into PYUSD at a quoted rate, which should track very close to one dollar per token under normal conditions. Users can then send PYUSD to other PayPal users, often using only an email address or phone number, which abstracts away the complexity of blockchain addresses. For more crypto‑savvy users, PayPal allows transfers of PYUSD to and from external wallets on supported networks, enabling participation in DeFi, trading on decentralized exchanges, or custody with hardware wallets.

Venmo’s integration operates similarly but is designed around social payments and younger demographics. Users can pay friends back, split bills, and share payment activity in social feeds, with PYUSD appearing as just another funding or settlement option once enabled in the app. This integration matters because it normalizes stablecoin usage in everyday contexts, moving it beyond trading and into casual peer‑to‑peer payments, albeit behind a user interface that hides many of the underlying complexities.

Rewards and Yield on PYUSD Balances

One of the notable features PayPal added to PYUSD is a rewards program that pays users a variable rate on their PYUSD balances held within the PayPal and Venmo apps. In April 2025, PayPal introduced rewards starting at an advertised annual rate of around 3.7 percent, later increasing the advertised rate to about 4 percent by 2026. The rate is variable, set by PayPal, viewable inside the app, and subject to change at any time, much like an interest rate on a high‑yield savings product. Rewards accrue on the average daily PYUSD balance and are paid out monthly in PYUSD, compounding users’ holdings over time.

These rewards are not universally available. As of 2026, PYUSD rewards are offered only to U.S. customers outside New York who opt in and hold at least one dollar in PYUSD, with additional regional restrictions for other markets. Some markets where users cannot sell PYUSD back into local currency nonetheless allow them to earn PYUSD rewards on their holdings, making the token function almost like a dollar‑denominated savings product within the PayPal ecosystem. This design raises interesting questions about how regulators classify such reward programs and whether they resemble deposit products, money market funds, or something new.

Economically, the rewards are funded from the interest income generated by PYUSD’s underlying reserves, which consist largely of short‑term U.S. government securities. Paxos, as reserve manager, earns this interest and can share it with PayPal as part of their commercial arrangement, after which PayPal can decide how much to pass through to users as rewards and how much to retain as revenue. The presence of a yield differentiates PYUSD from many cash balances in traditional payment apps that earn nothing for the user, but it also situates PYUSD within a broader “yield competition” among stablecoins, where DeFi yields, tokenized treasuries, and centralized platforms vie to offer the most attractive return on digital dollars.

Geographic Availability and Feature Fragmentation

Because stablecoins intersect with money transmission, securities law, and banking regulation, PayPal’s PYUSD rollout is necessarily fragmented by geography. The PayPal help center provides a matrix of markets and supported features, making clear that not all PYUSD functionality is available everywhere. In some countries, users can buy, sell, send, receive, and earn rewards on PYUSD, offering a near‑complete experience that mirrors the U.S. product. In others, only buy and sell are supported, with no ability to transfer externally or earn rewards, effectively limiting PYUSD to a speculative asset or a trading pair inside the app.

In yet other markets, PayPal allows users to buy, send, receive, and earn rewards on PYUSD but does not permit selling back to local currency, a configuration that can be puzzling at first glance. One interpretation is that this reflects regulatory comfort with inbound dollarization and on‑chain inflows but greater caution about enabling easy conversion from a dollar‑linked token back into local fiat, which might raise policy concerns about capital controls or monetary sovereignty. From a user’s perspective, it means they must think carefully about their exit options before accumulating large PYUSD balances in such jurisdictions.

Despite this fragmentation, the overall direction of travel is toward broader access. The March 2026 expansion to around seventy markets underscores that PayPal sees PYUSD as a global product, even if the feature set and compliance rules will remain heterogeneous. For cross‑border users, this can enable interesting patterns: for example, a user in one country may buy PYUSD via PayPal, send it to a relative in another country that supports receiving, and then that relative can move it to a self‑custody wallet or a local exchange, sidestepping some of the friction of traditional remittance channels.

Relationship to Other PayPal Crypto Features

PYUSD sits alongside Bitcoin, Ethereum, and other cryptocurrencies that PayPal offers for trading and payments, but it plays a different role. Whereas volatile cryptocurrencies are generally used for speculation or, in limited cases, as high‑beta collateral, PYUSD is designed as the stable leg of the portfolio that can be used to denominate value, settle purchases, and provide a less volatile store of value. PayPal’s interface makes it easy to convert between PYUSD and these other assets, encouraging users to treat PYUSD as a base currency inside their crypto experience.

From a merchant perspective, PayPal can also allow customers to pay with PYUSD at checkout while settling the merchant in local currency or in PYUSD, depending on their preference and the capabilities of the merchant’s acquirer. Over time, as card networks like Mastercard begin supporting stablecoin settlement for card transactions, there is a plausible path for PYUSD to be used not only inside PayPal’s own checkout but also as a settlement asset between banks and processors in the background. That distinction—consumer‑facing use versus infrastructural settlement use—will be critical in assessing how deeply PYUSD penetrates the payments stack.

On-Chain Integrations, Networks, and Liquidity

Multi-Chain Footprint and LayerZero Expansion

On the open blockchain side, PYUSD has moved from a single‑chain ERC‑20 to a multi‑chain asset, reflecting both user demand for cheaper settlement and a strategic desire to be available wherever DeFi and tokenized assets migrate. Ethereum remains the primary issuance chain, but Solana offered a compelling alternative for high‑throughput, low‑fee transfers, especially in consumer and trading contexts. The move to Solana also aligned with broader market narratives about Solana as a fast, cost‑efficient chain for payments and market‑making, and coincided with renewed regulatory clarity around SOL as a digital commodity.

Stellar, which has historically been used for remittances and fiat‑linked tokens, provided another natural home for PYUSD, particularly for cross‑border payment corridors and business‑to‑business flows. PayPal’s announcement that PYUSD would be made available on Stellar explicitly framed it as enabling new wallets, platforms, and business use cases across global payments, suggesting that this integration is as much about institutional partners as about retail users. Additional EVM networks such as Arbitrum have become supported settlement environments for PYUSD through bridges and LayerZero’s messaging stack, enabling the token to be wrapped or mirrored across chains without fragmenting its core supply.

LayerZero’s cross‑chain messaging plays an important role in this expansion. Rather than deploying completely independent token contracts on each chain and managing separate reserves, PayPal and Paxos can use LayerZero to create canonical and wrapped representations of PYUSD that maintain a consistent supply picture and can be bridged under controlled conditions. This helps mitigate some of the fragmentation risk seen in earlier multi‑chain stablecoin deployments, where different bridges created multiple incompatible versions of the same token. In theory, a more unified cross‑chain design makes it easier for protocols to integrate PYUSD and for users to understand what they are holding.

WalletConnect Pay and Merchant Acceptance

A key step in moving PYUSD from trading to everyday spending was its integration with WalletConnect Pay, a checkout experience that lets users pay merchants directly from their crypto wallets. With PYUSD now spendable wherever WalletConnect Pay is accepted, users can hold PYUSD in any supported self‑custody wallet and then pay participating merchants without first moving funds back into PayPal or a centralized exchange. This enables PYUSD to straddle the line between Web2 fintech and Web3 commerce, allowing a user who acquired PYUSD through PayPal or an exchange to spend it in a decentralized wallet context.

WalletConnect’s framing of PYUSD emphasizes its regulated nature and backing, describing it as a fully regulated, 1:1 USD‑backed stablecoin issued by Paxos Trust Company, regulated by the OCC. The messaging also highlights that PYUSD was the first stablecoin issued in partnership with a major U.S. payments company, with native integration across PayPal and Venmo, placing it “directly in front of hundreds of millions of users from day one.” For merchants, accepting PYUSD via WalletConnect Pay abstracts away most of the complexity of dealing with different networks and wallets, presenting the token more like any other payment method, albeit one settled on‑chain.

This form of integration is particularly important for the narrative of “stablecoins as real money.” PayPal executives have publicly discussed PYUSD in those terms, stressing that for many users, the meaningful difference is not between different stablecoins but between whether digital dollars can be spent easily at merchants and moved globally. By building pathways from PayPal’s custodial product to non‑custodial wallets and then to merchant checkout, PYUSD attempts to close the loop from traditional finance into Web3 and back again.

Mastercard Settlement and Institutional Use

Beyond consumer‑facing payments, PYUSD is also being integrated into card and bank settlement infrastructure. Mastercard announced in 2026 that it would expand its settlement capabilities to support regulated stablecoins, including Circle’s USDC and Paxos‑issued stablecoins such as PYUSD, USDG, and USDP. The program is designed to support intraday, weekend, and holiday settlement, allowing card issuers, acquirers, and other partners to settle obligations using stablecoins on networks like Arbitrum, Base, Canton, Ethereum, Polygon, Solana, Tempo, and XRPL.

Mastercard’s announcement named several early adopters, including ARQ (formerly DolarApp), CBW Bank, Cross River, Lead Bank, and Nuvei, who are expected to support stablecoin settlement options in the United States and Latin America. For PYUSD, being included alongside USDC in such an initiative signals that card networks view it as sufficiently regulated and liquid to serve as a settlement asset between financial institutions. It also underscores a broader thesis: stablecoins are not just for crypto exchanges or DeFi; they can become rails for traditional card transactions, payroll, and cross‑border bank transfers.

In practice, this could mean that a consumer paying with a traditional card might never see PYUSD, but their bank and the acquiring bank could settle net positions in PYUSD over a public blockchain rather than via slower, legacy correspondent banking systems. For issuers and processors, using PYUSD in this way might reduce settlement risk windows and enable more flexible liquidity management, especially during weekends and holidays when traditional rails are constrained. For PayPal and Paxos, it represents an expansion of PYUSD’s role from retail stablecoin to wholesale settlement asset.

DeFi Liquidity: Spark, Ethena, and Beyond

On the DeFi side, PYUSD has begun to feature in liquidity strategies, lending markets, and structured products. One prominent initiative is PayPal’s partnership with Spark, an on‑chain asset allocator launched by Sky (formerly MakerDAO), to expand liquidity for PYUSD by targeting a one‑billion‑dollar liquidity reserve deal. The plan, as reported, is to use Spark’s framework to build sustainable, deep markets for PYUSD across DeFi, potentially including automated market maker (AMM) pools, lending markets, and stablecoin‑stablecoin pairs. This could increase PYUSD’s presence on decentralized exchanges and as collateral in lending protocols, making it more competitive with USDC and USDT in DeFi contexts.

Similarly, protocols like Ethena have begun to treat PYUSD as a borrowing and collateral asset. Updates to Ethena’s market structure included adding PYUSD liquidity and enabling a “Debt Swap” tool that allows users to move USDG debt to PYUSD without manually unwinding positions. This sort of integration shows how PYUSD can become embedded in more complex DeFi strategies, such as synthetic dollar systems and yield‑bearing stablecoin portfolios, where users might borrow against or swap between multiple dollar tokens based on interest rates and risk preferences.

Elsewhere in the Solana and Flow ecosystems, PYUSD is being used in yield vaults, automated strategies, and cross‑chain bridging protocols. Risk‑managed vaults curated by on‑chain risk managers allocate PYUSD into lending markets and liquidity pools, seeking to generate yield while controlling counterparty risk. These activities sit alongside more speculative uses of PYUSD as collateral for derivatives and leveraged positions, highlighting that even a conservatively backed stablecoin can end up in riskier structures once it enters permissionless finance.

Spark seeds Uniswap v4 with $150M in USDS-PYUSD and USDS-USDT liquidity for stablecoin FX layer

Spark deployed about $150 million into two Ethereum Uniswap v4 pools, pairing USDS with PYUSD and USDT as the first phase of its Stablecoin FX Layer. The initial rollout uses standard v4 pools, with Spark planning a later Shared Liquidity Layer and DualPool hook after separate security review. The pitch is simple: stablecoin issuers get shared onchain liquidity instead of each rebuilding market makers, inventory, and venues from scratch.

PYUSD launched on Ethereum by Paxos / PayPal

PYUSD deployed on Solana, second supported blockchain

- 2024-08milestone

Aave v3 onboards PYUSD as borrowable mainnet asset

- 2024-10milestone

PYUSD surpasses $1B market cap, roughly one year post-launch

PayPal announces plans to deploy PYUSD on Stellar for remittances and PayFi

PYUSD access expanded from 2 countries to 70 markets globally

Spark and PayPal announce $1B PYUSD DeFi liquidity initiative

- 2026-06launch

PYUSD0 launched via LayerZero/Stargate Hydra, extending to nine new blockchains

PYUSD Versus Other Stablecoins: USDC, USDT, and Beyond

Market Share and Growth Dynamics

In the broader stablecoin market, PYUSD remains a mid‑sized player relative to giants like Tether’s USDT and Circle’s USDC. Its supply grew rapidly from launch, reaching roughly three and a half billion dollars in circulation by May 2026, more than five times its level a year earlier. Around the time of its global PayPal rollout, PYUSD’s market capitalization briefly topped four billion dollars, underscoring strong initial growth. Nonetheless, total stablecoin supply across the market has plateaued around the low‑hundreds‑of‑billions range, and recent periods have seen USDT adding billions in supply while other stablecoins, including USDC, USDe, and PYUSD, have collectively shrunk, resulting in muted net growth.

This suggests that PYUSD is gaining relevance but still competes in a crowded field where liquidity, integration depth, and user trust determine which dollar token dominates. USDT remains heavily used on offshore exchanges and in emerging markets, USDC is deeply integrated into U.S.‑regulated venues and DeFi, and decentralized stablecoins like DAI and newer entrants provide alternatives that reduce reliance on centralized issuers. PYUSD’s differentiator is less its raw market share and more its direct tie‑in to PayPal’s consumer network and its emerging role in card settlement and institutional liquidity structures.

Comparative Design and Regulation

Comparing PYUSD with USDC and USDT reveals both similarities and differences. Like USDC, PYUSD is issued by a U.S.‑regulated entity that publishes regular attestations and holds reserves primarily in cash and short‑term U.S. Treasuries. Both emphasize transparency and conservative reserve management, and both have been accepted by mainstream financial institutions and payment networks as relatively low‑risk, fiat‑backed tokens. USDT, by contrast, has historically faced more questions about reserve transparency and composition, though it has also published attestations and increased disclosure over time.

A simplified comparison can be expressed as follows:

| Token | Issuer | Primary Backing | Regulatory Regime | Core Distribution |

|---|---|---|---|---|

| PYUSD | Paxos Trust Company | Cash, USD deposits, short‑term U.S. Treasuries, reverse repos | OCC‑chartered national trust company; U.S. federal oversight | PayPal/Venmo apps, exchanges, DeFi |

| USDC | Circle (with partners) | Cash and short‑term U.S. Treasuries | U.S. state‑regulated money transmitter and partners; evolving global licensing | Exchanges, DeFi, institutional rails |

| USDT | Tether Limited | Mix of cash, Treasuries, other assets as disclosed | Offshore; limited direct U.S. oversight | Global exchanges, OTC, emerging markets |

PYUSD’s regulatory story is tightly bound to Paxos’s OCC trust charter and PayPal’s own licensing as a money transmitter and payments provider, giving it a strong U.S. regulatory footprint. USDC likewise operates under U.S. regulation but via a different legal structure, while USDT is issued by an offshore entity and is more distant from direct U.S. prudential oversight. For risk‑sensitive institutional users and card networks, these distinctions matter, which is why Mastercard’s settlement initiative focuses on “regulated stablecoins” like USDC and those issued by Paxos, including PYUSD.

Distribution and Ecosystem Positioning

Another key difference lies in distribution. PYUSD is uniquely integrated into PayPal and Venmo, giving it immediate exposure to a large installed base of consumer and business accounts worldwide. USDC and USDT, by contrast, are primarily distributed through crypto exchanges, institutional OTC desks, and smart‑contract interfaces, with relatively little direct presence in mainstream consumer wallets. That said, USDC has been integrated into certain neobanks and fintech apps, and USDT is widely used on regional payment rails in some countries via third‑party apps.

For developers and DeFi protocols, USDC and USDT currently enjoy deeper and broader liquidity across decentralized exchanges and lending markets, a legacy of their earlier launch and entrenched dominance. PYUSD is working to close this gap through initiatives like the Spark liquidity partnership, Ethena integration, and listings on major centralized exchanges, but it still lacks the sheer ubiquity of USDC/USDT pairs in DeFi. Over time, if PYUSD can leverage PayPal’s consumer flows into DeFi, it may build thicker liquidity, but this remains an open competitive question.

User-Facing Differences

For end users, the differences between PYUSD, USDC, and USDT often come down to where they can be acquired, how easy it is to cash out, and what use cases each token unlocks. Someone deeply embedded in DeFi may prefer USDC because of its pervasive integration with protocols, while a PayPal user who wants a simple yield on a dollar‑denominated balance may find PYUSD more accessible due to in‑app rewards and seamless conversion from bank accounts. Users in emerging markets without direct access to PayPal might still rely on USDT as the most liquid and accessible dollar proxy on local exchanges.

The presence of multiple robust stablecoins can be healthy, spreading issuer risk and giving users options. At the same time, fragmentation can complicate liquidity and settlement if different tokens are not interoperable or if cross‑stablecoin liquidity dries up during stress. PYUSD’s strategy of deep integration with one large consumer platform plus expansion into multi‑chain DeFi and card rails aims to carve out a unique niche in this landscape rather than directly displacing existing leaders.

Risks, Incidents, and Critiques

Operational and Smart Contract Risks

Even with conservative reserves, stablecoins face operational and technical risks. One high‑profile but ultimately harmless incident reported in 2026 involved Paxos mistakenly minting an extraordinarily large amount of PYUSD during an internal transfer as part of its treasury operations. The error was caught quickly, and the excess tokens were burned before they could affect circulating supply or customer balances, but the notional scale of the mis‑mint underscored how powerful administrative controls are and how much trust users place in issuer discipline and internal controls.

Smart contract design also introduces risk. Like other fiat‑backed stablecoins, PYUSD’s contracts include functions that allow the issuer to pause transfers, freeze specific addresses, or upgrade the contract logic. These controls are essential for compliance and for responding to bugs, but they create a central attack surface: if keys were compromised, or if an insider went rogue, an attacker could in principle disrupt transfers or attempt to misallocate tokens. Paxos mitigates this through multi‑sig control, key management procedures, and audits, but from a purist decentralization perspective, PYUSD remains a highly permissioned asset.

Multi‑chain deployments and bridges add further complexity. If PYUSD exists in wrapped form on certain chains via third‑party bridges, vulnerabilities in those bridges can lead to situations where wrapped PYUSD becomes under‑collateralized relative to canonical supply. LayerZero’s involvement is designed to create a more unified cross‑chain representation, but like any cross‑chain infrastructure, it must defend against message‑forgery and contract‑exploitation risks. Users holding PYUSD on non‑canonical chains need to understand which contract they are dealing with and what assurances exist about its linkage to Paxos’s mint‑and‑burn process.

Regulatory and Policy Risks

Regulation is both PYUSD’s selling point and a source of uncertainty. Being issued by an OCC‑regulated trust company and distributed by a globally regulated payments firm gives PYUSD a strong compliance posture, but it also means it is directly exposed to evolving U.S. and international policy on stablecoins. Legislators and regulators are actively debating how to categorize and supervise stablecoins, with proposals ranging from bank‑like regulation for issuers to more specific stablecoin charters. Changes in these rules could alter capital requirements, permitted reserve assets, or even the feasibility of certain reward programs.

PayPal’s aggressive expansion of PYUSD to seventy markets in one step has also drawn commentary about potential regulatory scrutiny and operational risk. Rolling out a regulated dollar stablecoin across such a wide array of jurisdictions raises questions about how consistently local rules are being interpreted and enforced, how cross‑border flows are monitored for money laundering and sanctions compliance, and how local supervisors will react to increased use of dollar‑linked tokens in their economies. Critics caution that missteps in any one jurisdiction could result in fines, product restrictions, or forced rollbacks.

In emerging markets, policymakers may worry that easily accessible dollar stablecoins accelerate informal dollarization, undermining local currencies and complicating monetary policy. While this concern applies to USDT and USDC as well, PYUSD’s connection to a household brand like PayPal—and to card networks like Mastercard—could bring the issue more squarely into mainstream policy debates. The more PYUSD is used in everyday payments and savings, the more likely it is to attract attention from central banks and finance ministries weighing the implications of private digital dollars versus central bank digital currencies.

Counterparty and Concentration Risk

From a user’s standpoint, PYUSD embodies several layers of counterparty risk. At the base layer is Paxos, which must remain solvent and operationally sound to honor redemptions and manage reserves. Above that sits PayPal, which controls access for users who hold PYUSD inside its apps and whose own financial health and regulatory standing shape the availability of services. On top of those issuers and distributors stand the banks and custodians that hold the underlying cash and Treasuries backing PYUSD. While each of these entities is regulated, the overall structure concentrates risk in a specific cluster of U.S. financial institutions.

This concentration is not unique to PYUSD; most fiat‑backed stablecoins rely heavily on the U.S. Treasury market and a small set of global custodians. However, it does raise systemic questions. In a stress scenario where short‑term Treasury markets are dislocated, stablecoin issuers may face challenges in liquidating assets quickly without incurring losses. While U.S. government securities are widely considered risk‑free in credit terms, they are not immune to liquidity or interest rate risk. For a stablecoin that promises par redemptions, ensuring sufficient cash buffers and access to liquidity lines is critical.

Market Risk and Depeg Scenarios

Although PYUSD is designed to hold its peg, market conditions could in theory produce temporary depegs. If confidence in Paxos or PayPal were undermined—due to regulatory action, negative publicity, or actual losses in reserves—secondary markets might discount PYUSD relative to other stablecoins or to the dollar. In such situations, arbitrage may be constrained by limited access to mint‑and‑redeem pathways, particularly if large holders fear getting stuck in a redemption queue or if regulators restrict new issuance or redemptions.

Moreover, PYUSD’s integration into DeFi leverage and derivative structures can amplify the impact of even small price deviations. If PYUSD is widely used as collateral in leveraged strategies, a modest depeg could trigger liquidations, which in turn could put further pressure on its price or on related markets. This is not hypothetical; similar dynamics have occurred with other stablecoins during market stress. The presence of deep liquidity, robust risk management by protocols, and transparent communication by issuers can mitigate but not eliminate these risks.

PYUSD is issued solely by Paxos under PayPal's direction; both entities can freeze or destroy tokens unilaterally, and the $300 trillion accidental mint incident — caught and burned internally — illustrates how much operational control rests with a single custodian.

- LiquidityMedium

Nansen data showed exchanges holding approximately 90% of PYUSD supply with sluggish organic DeFi circulation, meaning on-chain liquidity depth is thin relative to USDC or USDT despite a $1B+ market cap.

The Paxos $300 trillion erroneous mint during an internal transfer — immediately identified and burned with no customer impact — demonstrates that minting infrastructure errors are possible, even if controls caught this one quickly.

- RegulatoryLow

The SEC closed its PYUSD inquiry without enforcement action, reducing near-term U.S. federal securities-law risk, though evolving stablecoin legislation could impose new reserve, redemption, or licensing requirements on PayPal and Paxos.

- Market / CompetitionMedium

PYUSD competes against deeply entrenched incumbents (USDC, USDT) and yield-bearing newcomers; rewards programs and DeFi incentive spending (e.g., $132K to Stake DAO's Curve Votemarket) indicate PayPal is paying for liquidity rather than winning it organically.

- Counterparty / RedemptionLow

JP Koning's analysis argued PYUSD is structurally safer than USD held in PayPal's traditional e-money wallet because stablecoin holdings are backed by segregated reserve assets, not commingled customer funds subject to PayPal insolvency risk.

Ecosystem, Developers, and Use Cases

Building with PYUSD: APIs and On-Chain Integrations

For developers, PYUSD offers several integration paths. Within the PayPal ecosystem, developers and merchants can use PayPal’s existing APIs to accept PYUSD as a funding source or payout method, often without needing to directly handle blockchain interactions. This is particularly attractive for merchants who want the benefits of digital dollars without the complexity of on‑chain custody, key management, and compliance monitoring. PayPal can abstract these details, settling merchants in fiat or PYUSD as appropriate.

On the open blockchain side, integrating PYUSD works much like integrating any other ERC‑20 or SPL (Solana) token. Protocols can treat PYUSD as a base asset in AMM pools, as collateral in lending markets, or as a settlement asset in cross‑chain bridges. The key design questions for developers are which chain’s version of PYUSD to support, how to handle bridging, and how to manage regulatory exposure if they facilitate flows into or out of regulated platforms like PayPal. For example, a DeFi protocol that directly markets itself as a way to arbitrage PayPal’s PYUSD rewards could attract scrutiny if regulators view it as facilitating regulatory arbitrage.

The availability of PYUSD on chains like Solana and potentially other high‑performance networks also creates opportunities for low‑latency, high‑frequency trading strategies, market‑making, and real‑time micropayments. Developers building gaming, social, or content‑monetization apps might choose PYUSD as a medium of exchange precisely because users can easily acquire it through PayPal, spend it on‑chain, and, in some regions, earn rewards while holding it.

Network-Specific Ecosystems: Solana, Flow, and Stellar

Different networks provide different niches for PYUSD. On Solana, PYUSD can participate in high‑throughput DeFi, such as order‑book‑based decentralized exchanges, perps markets, and lending protocols that capitalize on Solana’s low fees and fast block times. It can serve as a base stablecoin for these markets, complementing or competing with USDC on Solana. Solana’s growing role in tokenized treasuries and RWAs also creates room for PYUSD to act as a transactional layer between tokenized funds and end users.

Flow’s evolution from an NFT‑centric chain into a broader stablecoin and consumer‑app platform may position PYUSD as a key dollar token in that ecosystem, particularly as Flow develops EVM equivalence and on‑chain automation tools for consumer yield apps. If a significant share of Flow’s stablecoin supply is in PYUSD, as on‑chain metrics suggest, then applications built on Flow might naturally standardize on PYUSD for payments, rewards, and savings features. This would give PYUSD a role across digital collectibles, gaming, and consumer finance on Flow.

On Stellar, PYUSD can plug into existing corridors for remittances and fiat token transfers. Stellar’s design and ecosystem are tailored to fast, low‑cost cross‑border transactions, and PYUSD’s arrival there opens the door for wallet providers and remittance services to offer PYUSD as a settlement and payout currency. For developers building in these contexts, PYUSD offers the familiarity of a branded, regulated U.S. dollar token backed by major incumbents.

Tokenized Funds and Institutional Structures

Beyond retail and DeFi, PYUSD is being woven into institutional tokenization projects. State Street and Galaxy’s planned tokenized liquidity fund, reportedly to be launched on Solana under the name SWEEP, is one example where a tokenized fund uses PYUSD as part of its operational plumbing. In such structures, institutions can use PYUSD to subscribe to and redeem from tokenized funds, settle trades, and move liquidity between fund tokens and stablecoins in on‑chain money markets.

PYUSD’s attractiveness in these contexts lies in its conservative reserve backing, regulatory pedigree, and multi‑chain presence. Institutions that are already comfortable with PayPal and Paxos as counterparties may find it easier to approve PYUSD for use in tokenized asset projects than more opaque or offshore stablecoins. As more asset managers, custodians, and banks experiment with tokenization, PYUSD could be one of several stablecoins used as the “cash leg” in on‑chain security settlements and fund operations.

Outlook

PYUSD sits at the intersection of three converging trends: the maturation of fiat‑backed stablecoins as core crypto infrastructure, the entry of mainstream payment companies into on‑chain finance, and the integration of stablecoins into traditional card and banking rails. Its architecture—Paxos as a federally regulated issuer, PayPal as a global distributor, reserves in cash and short‑term Treasuries, and a mint‑and‑redeem peg mechanism—positions it as a conservative, compliance‑friendly stablecoin that can appeal to regulators, institutions, and everyday users alike.

The token’s future trajectory will depend on several factors. One is the depth and quality of its on‑chain liquidity relative to USDC and USDT; if initiatives like the Spark partnership and Ethena integration succeed, PYUSD could become a first‑class DeFi asset rather than a peripheral one. Another is the extent to which PayPal can convert its installed base into active PYUSD users for payments, savings, and remittances, especially in the seventy markets where PYUSD access has recently been opened. A third is the evolving regulatory environment, which could either codify PYUSD’s model as a template for others or impose constraints that slow growth.

Risks remain. Operational errors, while so far contained, remind us that stablecoins are only as robust as their governance and internal controls. Regulatory backlash against dollarization or private stablecoins could curtail PYUSD’s use in certain jurisdictions or force changes to its reserve, yield, or distribution models. Competition from CBDCs, other stablecoins, and tokenized bank deposits could fragment the digital dollar space further. Yet, despite these uncertainties, PYUSD has already demonstrated that a large consumer payments company can launch a regulated, multi‑chain stablecoin, integrate it into both Web2 and Web3 rails, and scale it into the multi‑billion‑dollar range within a few years.

For developers and advanced users, the practical question is less whether PYUSD will “win” outright and more how to incorporate it as one component in a diversified stablecoin and liquidity strategy. It may be particularly well‑suited for use cases that value regulatory clarity, PayPal integration, and card‑rail interoperability, while USDC, USDT, and decentralized stablecoins continue to dominate in other niches. As stablecoin payments move from narrative to practice—from buying pizza with Bitcoin anecdotes to paying merchants directly with on‑chain dollars—PYUSD will likely remain one of the key experiments to watch in bridging regulated finance and open blockchain networks.

Latest PYUSD news

Sources

- https://www.paypal.com/us/digital-wallet/manage-money/crypto/pyusd

- https://www.paxos.com/pyusd-transparency

- https://eco.com/support/en/articles/12270549-what-is-pyusd-paypal-s-stablecoin-in-2026

- https://newsroom.paypal-corp.com/2024-05-29-PayPal-USD-Stablecoin-Now-Available-on-Solana-Blockchain,-Providing-Faster,-Cheaper-Transactions-for-Consumers

- https://newsroom.paypal-corp.com/2025-06-11-PayPal-USD-PYUSD-Plans-to-Use-Stellar-for-New-Use-Cases

- https://fortune.com/2026/03/17/paypal-expands-pyusd-stablecoin-access-to-68-more-countries/

- https://www.mastercard.com/global/en/news-and-trends/press/2026/june/mastercard-expands-settlement-capabilities-to-include-stablecoin.html

- https://walletconnect.com/blog/your-pyusd-on-walletconnect-pay

- https://blockworks.com/news/paypal-and-spark-target-1b-liquidity-boost-for-pyusd

- https://x.com/kamino/status/2061910551790285238

- https://x.com/flow_blockchain/status/2065551904655192319

- https://www.facebook.com/SwyftxNZ/posts/weekly-crypto-news-time-bitcoin-breaks-50kthe-big-event-this-week-was-bitcoin-br/898049922321262/

- https://www.mexc.com/news/109518

- https://x.com/WalletConnect/status/2055274532240289944

- https://www.prnewswire.com/news-releases/paypal-brings-paypal-usd-to-users-across-70-markets-302715503.html

- https://x.com/DecryptMedia/status/2033993333651939646

- https://www.paypal.com/us/cshelp/article/where-is-pyusd-available-help1326

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…