MakerDAO, rebranded as Sky in 2024, is Ethereum's pioneering decentralized stablecoin and DAO behind DAI and USDS. Explore its mechanics, SKY governance, 2026 treasury reform, real-world-asset collateral, and risks.

Former MakerDAO and Chronicle Labs contributor Marc-André Dumas joins The Graph Council, reinforcing leadership across protocol governance and treasury management2026-04

Former MakerDAO and Chronicle Labs contributor Marc-André Dumas joins The Graph Council, reinforcing leadership across protocol governance and treasury management2026-04 OpenZeppelin co-founder Manuel Aráoz now considers all of DeFi unsafe and is urging friends and family to exit every position, including blue-chips like Aave, MakerDAO, and Compound.2026-05

OpenZeppelin co-founder Manuel Aráoz now considers all of DeFi unsafe and is urging friends and family to exit every position, including blue-chips like Aave, MakerDAO, and Compound.2026-05 $10B exits Aave as capital rotates to Maker’s Spark, USDC and safer DeFi yields2026-04

$10B exits Aave as capital rotates to Maker’s Spark, USDC and safer DeFi yields2026-04 Sky, formerly MakerDAO, proposes treasury overhaul to shift from governance-led capital deployment to fixed, rules-based spending model, simplifying allocations across security, buybacks and staking rewards2026-04

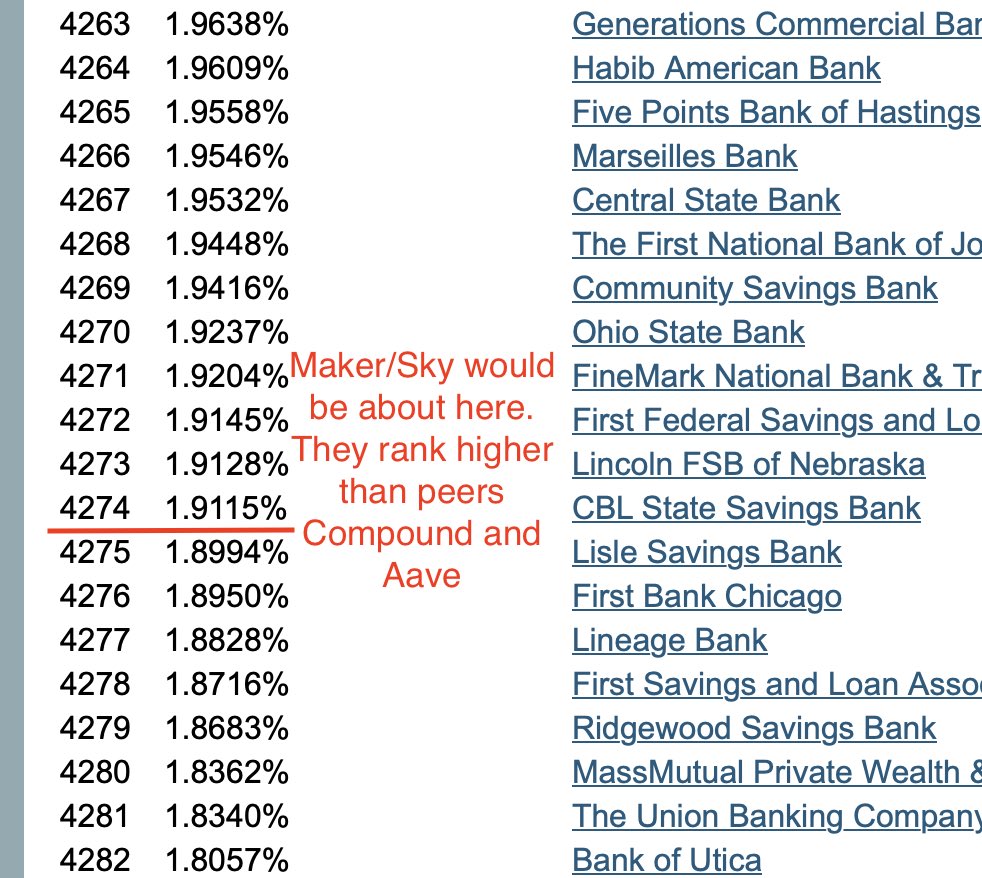

Sky, formerly MakerDAO, proposes treasury overhaul to shift from governance-led capital deployment to fixed, rules-based spending model, simplifying allocations across security, buybacks and staking rewards2026-04 DeFi lending protocols like Aave, Compound, and Maker currently operate as some of the least efficient “banks” in the US by net interest margin—far behind even average credit unions—highlighting how primitive their lending economics and product design still are despite huge room for improvement.2026-02

DeFi lending protocols like Aave, Compound, and Maker currently operate as some of the least efficient “banks” in the US by net interest margin—far behind even average credit unions—highlighting how primitive their lending economics and product design still are despite huge room for improvement.2026-02 Crypto market-maker Wintermute is reportedly paying more than $1m per employee amid a boom in high-profit digital asset trading.2026-01

Crypto market-maker Wintermute is reportedly paying more than $1m per employee amid a boom in high-profit digital asset trading.2026-01

MakerDAO is the Ethereum-based protocol that pioneered decentralized, overcollateralized stablecoins and on-chain governance; in August 2024 its community rebranded the system to Sky, introducing the USDS stablecoin and SKY governance token alongside the original DAI and MKR (The Block).

For most of its history it has been one of decentralized finance's foundational pieces of infrastructure: a smart-contract network that lets users lock crypto collateral and mint a dollar-pegged stablecoin without a bank or custodian.

Origins and Core Mechanism

The project launched in December 2017 with DAI, a stablecoin soft-pegged to the U.S. dollar but backed entirely by crypto assets held in smart contracts rather than by dollars in a bank. The mechanism is overcollateralization: a user deposits collateral (originally only ETH) worth more than the DAI they want to borrow, and the protocol mints new DAI against it. If the collateral's value falls below a required ratio, the position is automatically liquidated through on-chain auctions to keep the system solvent.

Three concepts anchor the design. A vault (originally called a Collateralized Debt Position, or CDP) is the individual loan a user opens against deposited collateral. The stability fee is the interest rate charged on minted DAI, set by governance. The liquidation ratio defines how much collateral must back each unit of debt. Together these levers let the protocol expand or contract DAI supply and defend the peg without a central operator.

This made MakerDAO an early proof that a stablecoin could be decentralized — governed by token holders and executed by code on Ethereum — rather than relying on a company holding reserves, the model used by USDT and USDC.

Former MakerDAO and Chronicle Labs contributor Marc-André Dumas joins The Graph Council, reinforcing leadership across protocol governance and treasury management

Dumas covered MakerDAO revenue analysis during the surplus buffer debates, then Chronicle Labs where the oracle stack secures $5B+ of Maker/Sky collateral. Graph Council picks him up as Horizon Mainnet rolls out Q1 2026, with query volume down 15.9% QoQ and indexer unit economics decoupling from the 15,087 active subgraphs. GRT issuance math has to account for Base flipping Ethereum as the dominant query chain — having someone with Maker-grade scar tissue on collateral rebalancing is overdue.

Readers click MakerDAO stories most when their own money is at stake in the next 48 hours — rate cuts that reprice savings, a named whale facing liquidation, a governance vote that could lock in bad collateral — abstract protocol debates rank far below actionable position risk.

Governance and the DAO

Maker is also one of the original examples of a DAO (decentralized autonomous organization): an entity whose decisions are made by token-holder voting rather than by executives. Holders of the governance token — historically MKR, now optionally upgraded to SKY — vote on risk parameters, which collateral types to accept, interest rates, and treasury spending.

The economics tie governance to system health. When the protocol earns more in fees than it spends, surplus revenue is used to buy back and burn the governance token, reducing supply. When liquidations fail to cover bad debt, the protocol can mint and sell new governance tokens to recapitalize, diluting holders. This creates a direct incentive for governance to manage risk prudently: token holders are effectively the backstop of last resort.

Over time, Maker governance evolved an elaborate apparatus of delegates, risk teams, and "core units" that functioned like decentralized departments. Critics long argued the structure was slow and bureaucratic, with low voter turnout concentrating effective power among a handful of large holders and professional delegates — a recurring tension across the DAO landscape.

The Endgame and the Sky Rebrand

In 2022, co-founder Rune Christensen proposed "Endgame," a multi-year plan to make the protocol more resilient, more decentralized, and easier to govern. The most visible result arrived in August 2024, when MakerDAO rebranded to Sky and shipped a new token set (Blockworks).

Under the rebrand, USDS became the upgraded stablecoin, convertible from DAI at a fixed 1:1 rate through an on-chain converter, while SKY replaced MKR as the governance token at a fixed ratio of 1 MKR to 24,000 SKY (The Block). Importantly, the upgrade was designed to be optional and coexistent: DAI and MKR continue to circulate alongside USDS and SKY, and the converter contracts run in both directions indefinitely.

Endgame also introduced semi-autonomous units originally called SubDAOs and now branded Stars — each with its own focus, token, and treasury but tied to the core protocol through shared reserves and USDS integration. The lending front-end Spark is the most prominent of these, operating as a borrowing-and-savings layer built on Sky's liquidity.

By 2026, USDS supply had grown above $9 billion, and Sky's total value locked reached roughly $7.5 billion in March 2026, ranking it among the largest DeFi protocols (Eco). Major exchanges scheduled automatic DAI-to-USDS conversions, with Binance migrating balances on April 7, 2026 and Coinbase following in early May (BlockEden).

OpenZeppelin co-founder Manuel Aráoz now considers all of DeFi unsafe and is urging friends and family to exit every position, including blue-chips like Aave, MakerDAO, and Compound.

DefiLlama's April hack table shows $635M lost across 27 incidents, with Kelp + Drift alone at $578M and tagged as infrastructure. That doesn't make Aave/MakerDAO/Compound risk-free; it means the failure mode has moved into collateral onboarding, bridge trust, admin keys, oracle assumptions, and guardian latency. Blue-chip DeFi probably survives this, but only with tighter caps, faster quarantine paths, and an explicit risk premium for every external dependency it lets onto the balance sheet.

- 01BA Labs rate governance power

The single most-clicked story by a wide margin revealed that one advisory firm can move the Dai Savings Rate by 3 percentage points, making readers acutely aware of how concentrated rate-setting influence actually is inside MakerDAO.

- 02Whale liquidation mechanics

A massive named ETH position nearing liquidation drew readers who wanted to understand the cascade mechanics and track it in real time, exposing how a single leveraged borrower can threaten protocol solvency.

- 03WBTC collateral control risk

BA Labs flagging an emergency governance vote over WBTC custody change risk hit readers who understood that collateral quality, not just collateral quantity, determines whether DAI stays solvent.

- 04DeFi lending economics critique

The comparison of Maker, Aave, and Compound to inefficient banks by net interest margin resonated with readers questioning whether the yield premium DeFi promises actually materialises at scale.

- 05Sky rebrand governance conflict

The emergency proposal renaming the protocol while key community members were banned surfaced fears that Endgame governance could be captured by insiders under the cover of a rebrand.

- 06Stablecoin regulation exposure

MiCA frontend licensing threats and competing US stablecoin bills (GENIUS vs STABLE) pulled in readers who recognised DAI's decentralised model as a specific regulatory target, not just background noise.

How DAI/USDS Stays Pegged Today

The peg mechanism has changed substantially since 2017. Early DAI was backed almost entirely by ETH. Today the collateral mix is far more diversified and, controversially, far less crypto-native. As of early 2026, Sky's backing was roughly 40% real-world assets (mostly short-term U.S. Treasury bills allocated through institutional partners), about 35% USDC routed through the Peg Stability Module, and the remainder in ETH, staked ETH, and other crypto collateral (Eco).

The Peg Stability Module (PSM) lets users swap USDC for DAI/USDS at a fixed rate, which keeps the peg tight but means a large share of the "decentralized" stablecoin is ultimately backed by a centralized, freezable asset. The pivot into Treasury bills, meanwhile, transformed the protocol into one of the larger on-chain holders of U.S. government debt, generating most of its revenue but exposing it to traditional-finance counterparties and interest-rate cycles.

To pass yield back to users, Sky operates the Sky Savings Rate (SSR), a contract that pays holders who deposit USDS a variable return — between roughly 3.75% and 4.5% APY in early 2026 — funded largely by the protocol's Treasury-bill income (Eco). This savings rate has become a key competitive lever for attracting deposits and stablecoin float.

Treasury Reform and Capital Rotation

In 2026 the protocol moved to overhaul how it manages money. Founder Rune Christensen proposed simplifying the Treasury Management Function after the transfer of Genesis Capital to a unit called Grove marked the end of the protocol's bootstrap "Genesis Capitalization" phase (Cryptopolitan).

The proposal collapses a five-step conditional spending waterfall into four fixed allocations — security and maintenance, aggregate backstop capital, the Smart Burn Engine (which funds token buybacks), and USDS staking rewards — and caps expenses at a fixed percentage of revenue (The Defiant). The intent is to shift from ad hoc, governance-decided outflows to rules-based, predictable spending. The reform reflects a broader maturation: less improvisation, more mechanical policy.

That discipline coincided with notable capital rotation across DeFi. Reporting in 2026 described billions of dollars flowing out of competing lender Aave toward Sky's Spark, USDC, and other lower-risk venues as yields compressed and capital sought safer parking (Blockworks). Sky governance simultaneously pruned Spark's exposure — offboarding certain Aave-deployed positions and adjusting supply caps on Bitcoin-pegged collateral — illustrating how actively the protocol now reallocates capital across markets.

$10B exits Aave as capital rotates to Maker’s Spark, USDC and safer DeFi yields

Aave's USDC and USDe pools hit 100% utilization during the outflow, meaning lenders literally couldn't withdraw — calling this "rotation to safer yields" is generous when it was forced liquidation pressure from $196M in rsETH bad debt. Same pattern as the stETH depeg stress in 2022, except LRTs don't have Lido's track record when a bridge gets drained. Spark catches the flow because sUSDS yield is backed by T-bills and DAI collateral, not restaking tokens with bridge-dependent pegs.

- 2017-12launch

Single-collateral DAI (SAI) launches on Ethereum mainnet

- 2019-11launch

Multi-Collateral DAI launches; MKR governance token activated

- 2020-03exploit

Black Thursday: ETH crash triggers $4M bad debt; emergency MKR dilution auction

- 2023-06milestone

$1B allocated into tokenized US Treasuries via Securitize, Superstate, Centrifuge

- 2023-12milestone

Maker records $200M+ annual revenue driven by US Treasury yield integration

- 2024-08governance

Emergency vote to limit WBTC exposure after custody control-change risk flagged by BA Labs

- 2024-08governance

Rune announces Sky rebrand: $USDS replaces DAI branding, Sky.money launched

- 2025-01milestone

Sky (MakerDAO) unveils 2026 roadmap including rules-based treasury spending model

Risks and Criticisms

For all its longevity, the protocol carries real and debated risks. Centralization of collateral is the most cited: heavy reliance on USDC and Treasury bills means regulators or counterparties could, in theory, freeze assets that back a supposedly decentralized stablecoin. The 2023 USDC depeg, when Circle's reserves were briefly trapped at a failing bank, temporarily dragged DAI off its peg and underscored that dependency.

Governance risk is structural. Because token holders control collateral onboarding and risk parameters, a concentrated or compromised vote could alter the system's safety profile. Smart-contract risk persists as well — the entire edifice runs on Ethereum code, and the broader DeFi sector continues to suffer hacks and exploits, a reminder that even battle-tested contracts are not risk-free.

Skepticism reaches the protocol's own peers. In recent commentary, OpenZeppelin co-founder Manuel Aráoz said he now regards all of DeFi — including blue chips such as Aave, Compound, and Maker/Sky — as carrying systemic risk he was no longer comfortable with, urging a broad retreat from on-chain exposure. Such views are not consensus, but they capture an ongoing debate about whether DeFi's complexity has outrun its safety guarantees. Users should treat any stablecoin, custodied in a wallet or not, as carrying counterparty and contract risk rather than a guaranteed dollar.

Why It Matters

Maker/Sky occupies an unusual position in crypto: simultaneously one of the most decentralized stablecoin systems and one of the most entangled with traditional finance. DAI and USDS function as base money across DeFi — used as collateral, trading pairs, and yield instruments throughout the Ethereum ecosystem. Changes to its parameters ripple outward, which is why governance votes draw intense scrutiny.

It also remains a live experiment in whether a DAO can manage a multibillion-dollar balance sheet responsibly over years, not months. The 2026 treasury reforms — trading discretionary governance for fixed rules — suggest the answer the community reached: at scale, predictability beats improvisation.

- Smart ContractMedium

An OpenZeppelin co-founder publicly urged exiting MakerDAO alongside other blue-chip DeFi protocols, citing systemic smart-contract risks that have not been resolved despite years of audits.

- CentralizationHigh

BA Labs commands enough governance weight to single-handedly recommend 300-basis-point rate swings, and the emergency Sky governance proposal showed the core team can act unilaterally while banning dissenting voices.

- Collateral / CounterpartyHigh

The WBTC custody-change episode demonstrated that off-chain custodial risk can force emergency governance votes; a single large ETH borrower can simultaneously threaten protocol liquidity.

- RegulatoryHigh

EU MiCA interpretations could ban standard DeFi frontends, and US stablecoin bills explicitly debate whether decentralised stablecoins like DAI can legally pay interest, threatening the Dai Savings Rate model.

- LiquidityMedium

Capital rotation into Spark and safer DeFi yields shows Maker can attract TVL in bull markets, but revenue is explicitly tied to users seeking leverage, making income highly cyclical.

- Market / RevenueMedium

Over $200M in annual revenue was driven by rising US Treasury yields and crypto loan demand; a simultaneous rate compression and bear market would sharply reduce both income streams.

Outlook

The protocol's trajectory points toward consolidation rather than reinvention. The Sky rebrand, the rules-based treasury, and the Stars/Spark architecture all aim to make a sprawling system simpler to govern and more resilient to shocks. The central tension is unlikely to resolve soon: deepening reliance on Treasury bills and USDC stabilizes the peg and funds the savings rate, but at the cost of the censorship-resistance that originally defined DAI. How Sky balances yield, decentralization, and regulatory exposure — while DAI and USDS coexist through a multi-year migration — will shape not just its own future but the template other stablecoin issuers follow.

Latest Maker DAO news

Former MakerDAO and Chronicle Labs contributor Marc-André Dumas joins The Graph Council, reinforcing leadership across protocol governance and treasury managementOpenZeppelin co-founder Manuel Aráoz now considers all of DeFi unsafe and is urging friends and family to exit every position, including blue-chips like Aave, MakerDAO, and Compound.$10B exits Aave as capital rotates to Maker’s Spark, USDC and safer DeFi yieldsSky, formerly MakerDAO, proposes treasury overhaul to shift from governance-led capital deployment to fixed, rules-based spending model, simplifying allocations across security, buybacks and staking rewardsDeFi lending protocols like Aave, Compound, and Maker currently operate as some of the least efficient “banks” in the US by net interest margin—far behind even average credit unions—highlighting how primitive their lending economics and product design still are despite huge room for improvement.Crypto market-maker Wintermute is reportedly paying more than $1m per employee amid a boom in high-profit digital asset trading.Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…