In‑depth explainer on Sky Protocol, covering its MakerDAO origins, USDS and sUSDS design, Sky Savings Rate, Agent Network, governance and S&P rating, integrations across CeFi/DeFi, risk profile, and how it compares with USDC, DAI and other stablecoins.

+1 sources across the wider coverage universe

Bybit to auto-swap DAI balances for USDS at 1:1, joining Binance in adopting Sky Protocol's stablecoin rebrand2026-04

Bybit to auto-swap DAI balances for USDS at 1:1, joining Binance in adopting Sky Protocol's stablecoin rebrand2026-04 Aave votes to remove Sky Protocol's USDS as collateral, citing it "generates negligible revenue while its issuance model introduces asymmetric risks that could impact Aave's stablity"2025-12

Aave votes to remove Sky Protocol's USDS as collateral, citing it "generates negligible revenue while its issuance model introduces asymmetric risks that could impact Aave's stablity"2025-12 Sky guts buybacks 87% after S&P rates its reserves on par with DRC bonds, Rune warns 'massive oil shock' is coming2026-03

Sky guts buybacks 87% after S&P rates its reserves on par with DRC bonds, Rune warns 'massive oil shock' is coming2026-03 There’s a “third way” emerging in DeFi lending. Beyond monolithic and isolated models, SubDAO-based lending—pioneered by Sky and Spark—is quietly outperforming, combining unified liquidity with specialized execution and strong margins. A different blueprint for scaling DeFi credit.2026-01

There’s a “third way” emerging in DeFi lending. Beyond monolithic and isolated models, SubDAO-based lending—pioneered by Sky and Spark—is quietly outperforming, combining unified liquidity with specialized execution and strong margins. A different blueprint for scaling DeFi credit.2026-01 BA Labs recommends Maker DAO decrease rates 3%, which would drop the Dai Savings Rate to 10%2024-04

BA Labs recommends Maker DAO decrease rates 3%, which would drop the Dai Savings Rate to 10%2024-04 Introducing Sky Aave Force: An initiative by Rune and Stani to drive mass adoption and close the gap between DeFi and TradFi 2024-09

Introducing Sky Aave Force: An initiative by Rune and Stani to drive mass adoption and close the gap between DeFi and TradFi 2024-09

Sky Protocol and the Evolution of Stablecoin Yield

Emerging from MakerDAO’s pioneering experiment with the DAI stablecoin, Sky Protocol is a decentralized credit and stablecoin platform that issues the USDS dollar-pegged stablecoin and its yield-bearing counterpart sUSDS, governed by the SKY token and backed largely by real‑world assets and onchain collateral. At its core, the system aims to connect idle stablecoin liquidity to institutional‑grade yields via a network of capital allocators, while preserving the overcollateralized, transparent design that characterized MakerDAO’s original architecture.

Stablecoins, Yield, and Why Sky Protocol Matters

Understanding Sky Protocol begins with the broader role of stablecoins in crypto markets. Stablecoins are digital tokens designed to track the value of fiat currencies such as the U.S. dollar, providing a relatively stable unit of account and medium of exchange inside highly volatile crypto ecosystems. Early designs split into two broad camps: centrally issued tokens such as USDC and USDT backed by bank deposits and Treasuries, and decentralized, collateral‑backed designs like DAI that allowed anyone to lock crypto collateral onchain and mint a corresponding amount of stablecoin against it. The second model, pioneered by MakerDAO, promised censorship resistance and transparency, but it also faced persistent questions about scalability, risk management, and the ability to generate sustainable yield for users in a low‑rate environment.

As decentralized finance matured, the search for yield became one of its defining themes. During periods of extremely low interest rates in traditional finance, onchain protocols sometimes offered double‑digit returns, but these were often subsidized by token emissions rather than supported by durable cash flows, leading to cycles of boom and bust. The collapse of under‑collateralized or algorithmic stablecoins reinforced the idea that sustainable yields must be funded by real economic activity rather than reflexive token incentives. Sky Protocol positions itself as a response to this lesson: a system that channels stablecoins into diversified portfolios of real‑world assets, DeFi lending, and other credit exposures, and then returns a portion of the resulting income to holders of its savings token sUSDS.

Another important background element is the convergence between traditional finance and crypto capital markets. Large asset managers and banks increasingly experiment with tokenized Treasuries, credit portfolios, and money‑market strategies, while crypto protocols seek access to those same instruments to back stablecoins with transparent, short‑duration, dollar‑denominated assets. Sky’s design explicitly leans into this convergence: it uses an “Agent Network” of institutional and protocol‑level allocators to deploy capital into off‑chain and on‑chain opportunities under onchain governance constraints. This structure sits between the fully centralized model of a corporate issuer and the purely algorithmic model of an onchain stablecoin, making Sky an important test case for hybrid designs.

Finally, the stablecoin landscape is increasingly competitive and scrutinized by regulators and ratings agencies. The fact that Sky Protocol and its savings product sUSDS have been assigned a public credit rating of B‑ with a stable outlook by S&P Global underscores both the protocol’s institutional ambitions and the perceived risks in its model. At the same time, Sky emphasizes its nearly decade‑long track record, inherited from MakerDAO, of operating without core exploits or losses to stablecoin holders, arguing that time‑tested transparency and resilience are its real moat. The tension between these narratives—robust historical performance versus forward‑looking risk assessments—frames much of the current debate around Sky.

Bybit to auto-swap DAI balances for USDS at 1:1, joining Binance in adopting Sky Protocol's stablecoin rebrand

Bybit will auto-swap user DAI balances to USDS at 1:1, completing its catch-up to Sky Protocol's stablecoin rebrand that Binance already processed months back. USDS is MakerDAO's successor stablecoin — same $1 peg, but holders earn Sky Token Rewards that DAI never paid. Combined DAI+USDS supply now sits at $13.4B, keeping Sky the third-largest stablecoin issuer behind Tether and Circle.

Readers engage Sky/MakerDAO coverage primarily as rate-watchers with skin in the game — the dominant click signal is not protocol curiosity but yield-sustainability anxiety: who controls the DSR lever, can elevated rates hold, and what breaks in the collateral stack when they fall.↗

From MakerDAO and DAI to Sky, USDS, and SKY

Sky Protocol did not emerge in a vacuum; it is the result of a multi‑year transformation of the MakerDAO ecosystem. MakerDAO’s original DAI stablecoin, introduced in 2017 and formalized in its 2020 white paper, was a decentralized, collateral‑backed cryptocurrency soft‑pegged to the U.S. dollar. Users locked assets such as ETH into collateralized debt positions (CDPs) and minted DAI against that collateral, subject to overcollateralization ratios and stability fees. This design proved remarkably resilient through multiple market cycles, and DAI became a foundational asset for DeFi lending, trading, and liquidity provision.

Over time, however, DAI’s growth and MakerDAO’s own economics became increasingly tied to real‑world assets and off‑chain yield strategies. The protocol began allocating collateral into short‑term U.S. Treasuries and other dollar‑linked credit exposures, gradually inverting its economics so that more than 60% of protocol revenue came from real‑world asset positions rather than purely crypto‑native collateral. Governance debates around how to manage this RWA exposure, scale the system, and adapt to evolving regulation culminated in Rune Christensen’s “Endgame” roadmap, which envisaged a reorganization of MakerDAO into a broader “Sky” ecosystem. This roadmap aimed to create specialized SubDAOs, a revamped governance token, and a modernized stablecoin brand more suited to institutional adoption.

The formal pivot arrived in August 2024, when Christensen unveiled Sky Protocol as a rebrand and evolution of MakerDAO, with two new flagship tokens: USDS as the successor to DAI, and SKY as the successor to the MKR governance token, with an approximate 1:24,000 conversion ratio. Under this plan, USDS would gradually replace DAI as the primary stablecoin, while sUSDS would become the dominant savings vehicle, receiving the interest generated by the protocol’s diversified collateral portfolio. Existing MKR holders were given a path to upgrade into SKY, with governance incentives and, later, a “Delayed Upgrade Penalty” to encourage migration within a defined timeframe, signaling a controlled but firm transition to the new governance regime.

The migration from DAI to USDS accelerated dramatically once major centralized exchanges began to support the new stablecoin. In early April 2026, Binance announced that it would automatically convert all exchange DAI balances to USDS at a 1:1 ratio, delist DAI trading pairs, and introduce new USDS pairs such as BTC/USDS and ETH/USDS shortly thereafter. Other exchanges, including Bitunix, BIT (Matrixport), Coinmetro, and CoinJar, enacted similar auto‑conversion policies, effectively making USDS the primary representation of Maker‑origin stablecoin liquidity on centralized platforms. For users holding DAI on these exchanges, the change required no action; balances converted automatically, and value was preserved at parity, but the branding and ticker they interacted with shifted to USDS.

This exchange‑level migration reflects a deeper reality: Sky Protocol is designed as the new operational center of gravity for what began as MakerDAO. USDS is now the focus of new liquidity mining programs, SubDAO allocations, and savings rate incentives, while legacy DAI positions and systems are being wound down or integrated into the new framework. From the perspective of stablecoin markets, this means that analyzing DAI without considering Sky and USDS increasingly misses the point; the risk profile, governance, and growth trajectory of the Maker‑Sky ecosystem are now bound to Sky’s architecture and decision‑making, not the legacy MakerDAO branding.

USDS, sUSDS, and the Sky Savings Rate

The heart of Sky Protocol’s product offering is a two‑token stablecoin design: USDS as the base dollar‑pegged asset and sUSDS as the yield‑bearing savings token that accrues the Sky Savings Rate (SSR). USDS itself functions much like DAI did, aiming to maintain a soft peg to the U.S. dollar, backed by a mix of onchain collateral and real‑world asset exposures, and redeemable through protocol mechanisms designed to keep its market price anchored near one dollar. What differentiates Sky’s current model is less the existence of a collateral‑backed stablecoin and more the explicit integration of a savings layer, sUSDS, that is positioned as “the world’s largest yield‑generating stablecoin” with real‑time verifiability of backing.

USDS can be supplied into a dedicated module within Sky to mint sUSDS, effectively “staking” the stablecoin to earn the Sky Savings Rate. In return, users receive sUSDS tokens that represent a claim on an expanding pool of protocol surplus; over time, the exchange rate between sUSDS and USDS increases as yield is accrued, rather than distributing interest in the form of periodic payouts. This design mirrors the earlier DAI Savings Rate (DSR) but is now central to the product identity of Sky, rather than a secondary feature. Unlike many money‑market tokens whose yields are driven by pool utilization or algorithmic interest rate models, the SSR is an administered rate set explicitly by Sky governance and funded by protocol revenue streams.

The mechanics of the Sky Savings Rate are deliberately transparent. According to documentation and independent analyses, the SSR is funded from three primary internal yield sources: returns on real‑world asset collateral such as short‑term Treasuries, the borrow rate paid by users who take USDS loans through the Spark lending SubDAO, and stability fees on USDS minted via the original collateralized debt position system. Governance, through the SKY token holders, calibrates the SSR so that these cash flows cover payouts to sUSDS holders, operating costs, and a surplus buffer intended as a backstop for the stablecoin, leaving some margin for buybacks or other capital decisions. Because the SSR is tied to discrete governance decisions and underlying revenue capacity, it tends to move in steps rather than continuous small adjustments, tracking broader interest rate environments and protocol performance rather than short‑term market utilization.

In its early years, the DAI Savings Rate occasionally exceeded 8%, as Maker deployed collateral into higher‑yielding environments and used the rate as a tool to manage DAI supply. Under Sky, the emphasis has shifted toward sustainable, institutionally acceptable yields. As of mid‑2026, governance materials and the sUSDS product page indicate that the Sky Savings Rate has been set in the mid‑single‑digit range, with recent adjustments bringing it to around 3.60% annualized. This rate is framed as a conservative yield relative to money‑market benchmarks, designed to remain viable across market cycles rather than maximizing short‑term attractiveness. Because there are no lock‑ups or withdrawal penalties for sUSDS—users can redeem back into USDS at any time, subject to usual onchain constraints—the SSR acts more like a non‑custodial savings account within the Sky ecosystem than a fixed‑term bond.

A key differentiator for sUSDS is its positioning as a rated credit product. S&P Global has assigned Sky Protocol—and by extension its savings token—a B‑ long‑term issuer credit rating with a stable outlook, and the protocol highlights sUSDS as the first DeFi savings product to achieve such a rating. The rating reflects S&P’s view of Sky’s operational track record, collateral quality, governance, and risk controls, while also emphasizing the low‑probability but high‑severity risks inherent in using smart contracts to hold and manage collateral. For institutions considering exposure to yield‑bearing stablecoins, this combination of onchain transparency and traditional credit analysis is central to Sky’s pitch, even if the rating itself is still in “junk grade” territory by conventional standards.

- 01DSR yield rate decisions↗

The single highest-clicked headline was BA Labs recommending a 3-point rate cut, signaling readers treat DSR governance as a live financial event that directly affects their own stablecoin yield positions.

- 02MakerDAO-to-Sky rebrand confusion↗

Multiple high-click headlines spanning the Endgame identity shift — DAI to USDS, MKR to SKY — and the subsequent community push to revert the name revealed persistent reader skepticism about whether the pivot served token holders or just insiders.

- 03Collateral and peg fragility↗

Headlines about WBTC removal over Justin Sun custody concerns, a $250M emergency Coinbase transfer to defend DAI's peg, and Centrifuge credit defaults drew readers tracking whether DAI's backing was structurally sound.

- 04Ethena USDe competitive threat↗

Stories about USDe surpassing DAI as the third-largest stablecoin and Sky allocating $600M to Ethena captured readers anxious about DAI losing market share to a rival offering more than double its yield.

- 05Sky-Aave strategic alliance↗

Both the Sky Aave Force launch and Aave's subsequent move to strip DAI's LTV to 0% generated significant clicks, showing readers follow this partnership as a bellwether for USDS institutional adoption — and its reversibility.

- 06Governance capture and insider control↗

The Deco core unit going AWOL while collecting nearly 2M DAI annually, community fractures over unsustainable yields, and Rune's top-down Endgame restructuring all fed a consistent reader thread: who actually controls this protocol.

The Sky Agent Network, Collateral, and Real‑World Assets

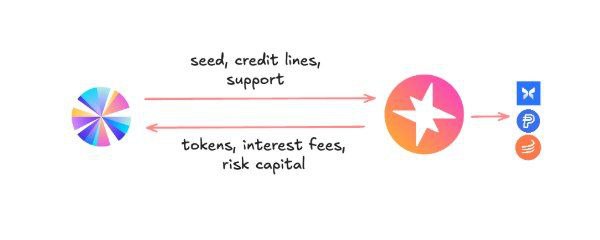

Central to Sky’s economic model is the way it sources and manages collateral backing USDS and sUSDS. Over the last several years, Maker and now Sky have increasingly relied on real‑world assets—particularly tokenized or structured exposure to U.S. Treasuries and other fixed‑income instruments—to generate yields that can be passed through to sUSDS holders. Governance materials and third‑party analyses describe how the protocol’s revenue mix has flipped from mostly crypto‑native to predominantly real‑world asset driven, with more than 60% of total income now coming from these off‑chain allocations. This shift has been instrumental in supporting a stable, administratively controlled savings rate without resorting to inflationary token subsidies.

The operational mechanism for these allocations is the Sky Agent Network, a collection of independent capital allocators—both onchain protocols and traditional financial institutions—that manage portions of Sky’s collateral under governance‑approved mandates. Agents might include DeFi lending protocols like Spark and Morpho, which channel USDS into overcollateralized loans, as well as traditional asset managers that invest in Treasuries, tokenized credit portfolios, or structured products such as collateralized loan obligations (CLOs). For example, Sky has been associated with deploying approximately one billion dollars into a tokenized CLO structure, illustrating the scale and complexity of some of these strategies. Each Agent operates within risk parameters set by Sky governance, and their aggregate performance feeds into the protocol’s surplus and, ultimately, the SSR.

One of the more visible recent developments in the Agent Network is Osero, a new Sky Agent that has raised around $13.5 million to integrate the Sky Savings Rate directly into neobanks, wallets, and custodial platforms. Osero’s mandate is not only to allocate capital but also to expand distribution channels for USDS and sUSDS, effectively embedding Sky’s yield into front‑end products that ordinary users of fintech apps might already be using. This speaks to Sky’s ambition to become part of mainstream financial plumbing, using the Agent model to bridge between conservative, regulated financial institutions and the composable, permissionless world of DeFi smart contracts.

Real‑world asset exposure comes with significant benefits and risks. On the one hand, short‑duration government securities and investment‑grade credit instruments can offer relatively predictable yields that track macro interest rates, providing a solid foundation for a stable savings rate. On the other hand, these exposures introduce counterparty, jurisdictional, and regulatory risks that do not exist for strictly onchain collateral. If a custodian, issuer, or jurisdiction freezes or seizes assets, USDS and sUSDS holders could face losses or temporary illiquidity even if the onchain mechanisms function correctly. S&P’s rating reports explicitly identify these structural and legal uncertainties, as well as the cyber risk associated with smart contracts themselves, as key factors behind the B‑ rating. For users, this means that while Sky’s collateral is “institutional‑grade” in terms of underlying assets, the overall risk profile remains meaningfully above that of insured bank deposits or top‑tier sovereign debt.

To increase transparency around these dynamics, Sky has supported the development of a public risk and analytics dashboard, operated by third‑party analytics firm Block Analitica and accessible via info.sky.money. The dashboard presents real‑time data on collateral composition, leverage, protocol surplus, the SSR, and even valuation metrics like a price‑to‑earnings ratio for SKY based on protocol profits. This kind of continuous, onchain‑informed disclosure is part of Sky’s argument that stablecoins can be more transparent than traditional money‑market funds, even if they carry different risks. However, it also exposes the protocol to market scrutiny when metrics like surplus buffers or concentration in particular RWAs raise concerns, as seen in the wake of recent credit rating actions and geopolitical volatility.

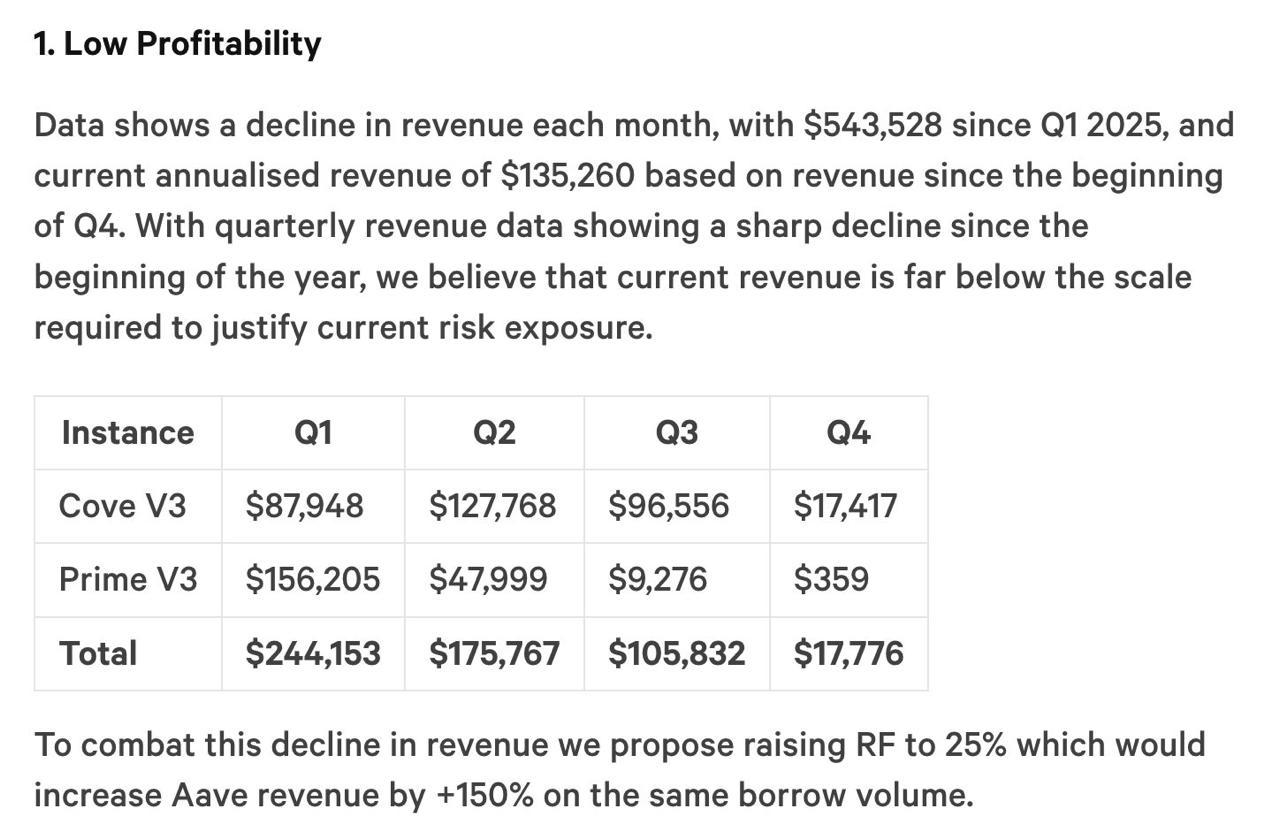

Aave votes to remove Sky Protocol's USDS as collateral, citing it "generates negligible revenue while its issuance model introduces asymmetric risks that could impact Aave's stablity"

"1. Low Profitability Data shows a decline in revenue each month, with $543,528 since Q1 2025, and current annualised revenue of $135,260 based on revenue since the beginning of Q4. With quarterly revenue data showing a sharp decline since the beginning of the year, we believe that current revenue is far below the scale required to justify current risk exposure."

Governance, the SKY Token, and Capital Policy

Governance in the Sky ecosystem revolves around the SKY token, which replaced MKR as the primary voting token under the Endgame roadmap. Holders of SKY participate in onchain governance processes that determine core parameters such as the Sky Savings Rate, collateral onboarding and risk limits, Agent mandates, and capital allocation between surplus buffers, buybacks, and other strategic initiatives. Proposals are typically authored by specialized core units—such as the Stability Scope, which focuses on monetary policy and risk—and executed via timelocked smart contracts that provide time for community review and, if necessary, emergency responses. This structure builds on years of Maker governance practice while trying to streamline decision‑making for a more complex, multi‑agent environment.

Tokenomics for SKY incorporate both governance power and value‑accrual mechanisms. One of the key features is the “Smart Burn Engine,” a systematic buyback‑and‑burn program that historically deployed approximately one million dollars per day of protocol surplus to purchase SKY on the open market and permanently destroy it. At that scale, the mechanism could retire on the order of $102 million in SKY per year, assuming sufficient surplus, creating a deflationary pressure that links protocol profitability to token scarcity. For investors, this structure resembles the share repurchase programs of traditional companies, with the twist that decisions about buyback intensity are themselves governed onchain by token holders.

Recent events, however, illustrate how flexible and politically charged this capital policy can be. Following S&P’s assignment of a B‑ credit rating and amid heightened geopolitical tensions—particularly concerns about the economic impact of conflict in the Middle East—Sky governance voted to slash its buyback program by roughly 87%, cutting daily buybacks from about $300,000 to around $37,600 for at least a three‑month period. The stated rationale was to bolster the protocol’s reserves and backstop capital for USDS and DAI in light of increased macro risk, prioritizing the stability of the stablecoin over immediate tokenholder value extraction. Governance communications emphasized that the surplus “buffer” had remained roughly flat at around $50 million and that temporarily diverting cash flows away from buybacks would help rebuild this safety margin.

This decision highlights the trade‑offs inherent in Sky’s model. On one side, tokenholders benefit financially from aggressive buybacks and burns, especially when the protocol is profitable and growth opportunities appear abundant. On the other side, stablecoin holders and risk‑averse participants prefer a thicker capital cushion and more conservative policies, particularly when ratings agencies and major DeFi protocols flag concerns about resilience. S&P’s rating commentary explicitly referenced Sky’s exposure to low‑probability, high‑severity cyber risks and the potential for losses if smart contracts fail or if real‑world asset arrangements break down, reinforcing the case for a robust surplus buffer. Balancing these constituencies is an ongoing governance challenge, and the recent pivot toward reserve accumulation suggests that, at least for now, Sky is leaning toward the safety‑first side of that spectrum.

The ongoing migration from MKR to SKY adds another layer of complexity. To encourage timely migration and reduce the surface area of legacy governance structures, Sky introduced a “Delayed Upgrade Penalty,” under which MKR holders who postpone upgrading their tokens to SKY face an increasing penalty over time, starting at around 1% and stepping up periodically according to the Sky Atlas governance blueprint. This mechanism is intended to avoid a long tail of dormant or unengaged MKR that could complicate governance and risk management, but it also raises questions about fairness to passive holders and the optics of effectively taxing late movers. For observers, it is a reminder that while Sky builds on Maker’s legacy, it is also willing to adopt more assertive policy tools to shape its governance base.

- 2022-09exploit

L2 DAI vanity-address deployer compromised via Profanity tool key vulnerability

- 2023-08governance

MakerDAO raises DAI Savings Rate to 8%; implements VPN geo-restriction on front end

- 2023-11milestone

MakerDAO transfers $250M from Coinbase custody to defend DAI peg amid collateral shortfall

Endgame plan formally introduces NewStable (USDS) and NewGovToken (SKY) to replace DAI and MKR

MakerDAO rebrands to Sky Protocol; DAI-to-USDS migration begins

- 2024-10governance

Sky removes WBTC as DAI collateral and disables WBTC borrowing on SparkLend over Justin Sun custody concerns

Sky Aave Force initiative launched by Rune Christensen and Stani Kulechov to drive USDS adoption

Sky community debates reverting brand identity back to MakerDAO amid persistent SKY token utility confusion

Integrations Across CeFi, DeFi, and Multiple Chains

Sky Protocol’s influence depends not only on its internal design but also on how widely USDS and sUSDS are integrated across centralized exchanges, DeFi platforms, and blockchains. The migration from DAI to USDS on major centralized exchanges is one of the clearest signals of this integration. As noted earlier, Binance’s decision to auto‑convert all user DAI balances to USDS at a 1:1 ratio and delist DAI trading pairs effectively elevated USDS to a first‑class stablecoin on the world’s largest crypto exchange. Similar moves by Bitunix and other platforms have amplified this effect, ensuring that new inflows and trading pairs are denominated in USDS rather than DAI. Other exchanges, including Bybit and large Asian platforms such as Upbit, have moved to list both USDS and the SKY governance token in key markets, expanding liquidity in fiat pairs like KRW as well as in USDT and BTC pairs, though details of these listings come primarily from ongoing news coverage rather than core protocol documentation.

In the DeFi arena, Sky leverages both its own SubDAOs and partnerships with external lending protocols. Spark, the first SubDAO launched under the Endgame roadmap, operates as a lending market closely aligned with Sky’s collateral framework, allowing users to borrow USDS against approved collateral and contributing directly to protocol revenue via the Spark borrow rate. Beyond its internal ecosystem, Sky has taken on a “curator” role on Morpho, a lending layer that allows curated entities to create lending markets with optimized matching between lenders and borrowers. Through this role, Sky‑native assets such as USDS serve as collateral in over $400 million of lending, extending the reach of the stablecoin into broader credit markets. This “third way” of DeFi lending—combining unified liquidity at the protocol level with specialized SubDAOs and curated markets—contrasts with both monolithic platforms like Aave and purely isolated pool designs.

Not all DeFi integrations have been frictionless, however. In a notable governance move, Aave’s community recently advanced a proposal to set USDS loan‑to‑value ratios to zero across all Aave deployments, effectively removing USDS as acceptable collateral while simultaneously increasing reserve factors. The rationale, as discussed in the Aave governance forum, was that USDS as a collateral asset generated negligible revenue for Aave while introducing asymmetric risks linked to its issuance model and RWA exposure, potentially affecting Aave’s own stability. The snapshot vote reached quorum with a decisive majority in favor of removing USDS collateral, underscoring that major DeFi protocols are actively reassessing their risk appetites toward newer RWA‑backed stablecoins even when those coins have robust track records elsewhere.

Sky is also pursuing a multi‑chain strategy, with USDS available on several networks via bridging technologies. On Solana, USDS is implemented as an Omnichain Fungible Token (OFT), allowing it to move between Ethereum and Solana through cross‑chain messaging frameworks. In early 2026, USDS bridging on Solana was temporarily paused while Sky and its partners conducted a security review related to an exploit in rsETH, another protocol in the broader ecosystem. Importantly, Sky emphasized that USDS contracts and Sky’s own systems were unaffected, and that USDS remained fully collateralized and verifiable onchain throughout the review period. Once the security review concluded, bridging resumed, illustrating both the fragility of cross‑chain connectivity and Sky’s willingness to halt functionality pre‑emptively in response to potential systemic risks.

Distribution partnerships further entrench Sky in centralized channels. Governance updates have highlighted initiatives to distribute the Sky Savings Rate through platforms like Binance and through newly created Agents like Osero, which target neobanks and custodians. This model envisions retail users accessing SSR‑backed yield not directly through DeFi interfaces but via familiar centralized platforms that integrate sUSDS or USDS into their product stacks. For regulators and traditional institutions, such arrangements raise questions about custody, disclosure, and the legal status of yield‑bearing stablecoins, but they also hint at a future where the line between DeFi protocols and fintech front‑ends becomes increasingly blurred.

Security, Risk Management, and Credit Ratings

Security and risk management are central to any stablecoin protocol, and Sky is acutely aware that its ambitions hinge on maintaining trust through both technical resilience and capital adequacy. From a historical perspective, the Sky team emphasizes that the protocol—counting its MakerDAO origins—has operated for nearly a decade without core smart contract exploits or losses to stablecoin holders. This track record spans multiple boom‑and‑bust cycles, including the 2020 DeFi summer, the 2022 credit unwinds, and various market dislocations, during which DAI and now USDS maintained their pegs with manageable deviations. For many in DeFi, this longevity and stress‑tested performance are powerful arguments in favor of Sky’s design.

However, past resilience does not eliminate forward‑looking risks. S&P Global’s B‑ rating for Sky Protocol, with a stable outlook, is a reminder that even well‑designed DeFi systems sit within a high‑risk category from a traditional credit perspective. S&P’s research update notes that Sky is exposed to “low‑probability, high‑severity” cyber risks because it uses smart contracts to hold and manage assets, and that a significant exploit could rapidly destabilize the system and cause losses to stablecoin holders. The rating also reflects concerns about the legal and operational complexities of real‑world asset arrangements, including questions about enforceability, counterparty risk, and jurisdictional exposure. In the language of ratings, a B‑ denotes a materially speculative credit profile, comparable to lower‑rated sovereign and corporate issuers, even if the underlying collateral quality is often higher than that association might suggest.

Capital buffers and contingency mechanisms are therefore critical to Sky’s risk story. Governance materials and external reporting suggest that Sky maintains an aggregate backstop in the form of surplus capital—essentially retained earnings—that can be used to stabilize USDS or absorb losses in the event of undercollateralization. As of recent updates, this surplus buffer has been in the vicinity of $50 million, a non‑trivial sum but modest relative to Sky’s multi‑billion‑dollar stablecoin liabilities. In addition, Sky has the ability to claw back some of the crypto capital allocated to subsidiaries such as Spark, providing an additional, though limited, source of emergency funds—on the order of tens of millions of dollars according to governance commentary. Finally, the protocol can issue and sell new SKY tokens to recapitalize itself in extreme scenarios, effectively diluting governance token holders to protect stablecoin users. These mechanisms collectively form Sky’s capital stack, but they also highlight the reliance on market confidence: the willingness of investors to buy SKY in times of stress is not guaranteed.

The decision to drastically curtail buybacks and redirect cash flows toward strengthening reserves, discussed earlier, reflects both internal prudence and external pressure. Ratings agencies, institutional counterparties, and large DeFi protocols like Aave have all sent signals that they view current buffers as lean relative to systemic importance. Critically inclined commentators describe Sky’s situation as one where “security vows face stormy seas,” arguing that the protocol’s promises of safety sit uneasily alongside a junk‑grade rating and relatively thin surplus capital. Supporters counter that Sky’s onchain transparency and conservative collateral profile—including heavy use of short‑term government securities—make it more robust than many opaque off‑chain credit structures with similar ratings. In practice, the truth likely lies somewhere in between: Sky is neither a near‑risk‑free substitute for insured bank deposits nor an inherently unstable experiment, but rather a high‑yield, moderate‑risk credit platform experimenting with unprecedented degrees of transparency.

Smart contract risk remains an omnipresent concern. Although Sky’s core contracts and those inherited from MakerDAO have a strong track record, the expanding web of integrations—Agents, SubDAOs, bridges, and external protocols—introduces new attack surfaces. The temporary pause of USDS bridging on Solana after an exploit in rsETH, even though Sky’s contracts were unaffected, shows how contagion risk in composable DeFi can force conservative responses. Security reviews, audits, bug bounties, and defense‑in‑depth strategies are ongoing necessities rather than one‑time hurdles. For users and institutions, the existence of formal ratings, public dashboards, and transparent governance processes provides tools to monitor these risks, but not guarantees that they will never crystallize.

Sky guts buybacks 87% after S&P rates its reserves on par with DRC bonds, Rune warns 'massive oil shock' is coming

- Smart-contractMedium

The L2 DAI vanity-address deployer was generated with the compromised Profanity tool, exposing multiple chains (excluding Optimism and Arbitrum) to private-key extraction risk.

BA Labs holds outsized influence over DSR rate-setting recommendations, and the entire Endgame restructuring — including the Sky rebrand and token replacement — was driven by a founding-team vision over significant community objection.

- RegulatoryMedium

MakerDAO implemented VPN geo-restrictions on its front end concurrent with the 8% DSR announcement, signaling active sensitivity to jurisdictional enforcement risk around high-yield stablecoin products.

- LiquidityMedium

A $250M emergency transfer from Coinbase custody was required to defend DAI's peg during a collateral shortfall episode, exposing reliance on rapid, large-scale manual rebalancing to maintain the $1 anchor.

DAI/USDS collateral exposure spans WBTC custody risk linked to Justin Sun, Centrifuge real-world credit defaults, and over $600M allocated to Ethena USDe/sUSDe — each carrying distinct and correlated tail-risk profiles in a risk-off scenario.

- Market / CompetitiveHigh

Ethena's USDe overtook DAI as the third-largest stablecoin while offering yields more than double USDS's rate, forcing Sky into aggressive yield competition that risks degrading collateral quality to defend market share.

How Sky Compares to Other Stablecoins and Yield Models

To place Sky Protocol in context, it is helpful to compare USDS and sUSDS with other major stablecoins and yield‑bearing assets. Traditional centralized stablecoins like USDC are issued by regulated entities that hold fiat reserves and Treasuries in custody accounts, providing 1:1 redemption and relying on banking and securities infrastructure for safety. Decentralized stablecoins like the original DAI, and now USDS, rely on overcollateralized onchain positions and, increasingly, RWA allocations overseen by onchain governance. Yield‑bearing tokens such as aUSDC or similar lending‑market receipts derive their interest from protocol‑level lending activity, with rates fluctuating based on loan demand and pool utilization, whereas sUSDS receives an administered savings rate directly from protocol revenue.

The following simplified table summarizes some of these differences:

| Asset | Issuer / Governance | Backing and Yield Source | Peg Mechanism | User Yield Model |

|---|---|---|---|---|

| USDC | Centralized (Circle) | Fiat and Treasuries; yield retained by issuer | Direct redemption at $1 via issuer | None to user; yield kept by issuer |

| DAI (legacy) | MakerDAO governance | Onchain collateral plus increasing RWA exposure | Overcollateralized CDPs and arbitrage | Optional DSR (now largely superseded) |

| USDS | Sky Protocol governance | Mix of onchain collateral and RWAs | Overcollateralized positions and RWA portfolio; arbitrage | Base token; no inherent yield |

| sUSDS | Sky Protocol governance | Protocol surplus from RWAs, Spark borrowing, stability fees | Indirect via USDS backing and SSR policy | Administered Sky Savings Rate (currently mid‑single digits) |

| aUSDC‑style tokens | DeFi lending protocols | Onchain loans and collateral | Redemption via lending protocol share accounting | Market‑driven variable APY based on utilization |

In this landscape, USDS sits between USDC and purely algorithmic experiments: it is not redeemable through a single centralized issuer, but its heavy reliance on RWAs and institutional Agents brings it closer to traditional finance than earlier crypto‑only designs. sUSDS is even more distinctive, effectively transforming Sky into a transparent, onchain analog of a money‑market fund or short‑duration bond fund, with an explicit, governance‑set yield and a public credit rating. For users who are willing to accept the additional smart contract and governance risks, sUSDS may offer a more attractive risk‑adjusted yield than simply holding USDC or USDT, and with clearer visibility into collateral composition than many off‑chain funds.

At the same time, centralized stablecoins currently enjoy advantages in terms of regulatory clarity, fiat on‑ramps, and, often, perceived safety. They benefit from bank‑grade custody and, in some jurisdictions, explicit or implicit regulatory oversight, even if they lack the programmability and open governance of protocols like Sky. On the yield side, tokenized Treasuries and onchain money‑market funds issued by regulated entities compete directly with sUSDS for investors seeking dollar‑denominated yield, albeit usually with higher minimums and less composability. Sky’s competitive edge therefore rests on its combination of permissionless access, composability within DeFi, and the ability to integrate with both CeFi exchanges and fintech front‑ends via Agents.

Ultimately, Sky’s positioning can be summarized as a “third way” in stablecoin design: not purely centralized, not purely decentralized and crypto‑only, but a hybrid structure where governance‑directed Agents connect onchain capital to off‑chain yield. This makes its risk profile more complex to analyze than that of either USDC or a simple crypto‑collateralized stablecoin, and it is precisely this complexity that both excites proponents and worries skeptics. The success or failure of Sky’s approach will likely influence how future stablecoins balance decentralization, regulatory engagement, and real‑world asset exposure.

User Experience, Use Cases, and Who Sky Is For

From the perspective of an individual user, interacting with Sky Protocol generally involves three levels of engagement: holding USDS as a simple dollar‑pegged asset, staking USDS into sUSDS to earn the Sky Savings Rate, or participating more deeply in governance and DeFi integrations around the ecosystem. Holding USDS alone resembles holding any other onchain stablecoin; it can be used to trade, provide liquidity, or serve as collateral in supported lending markets, and its peg stability is underpinned by the protocol’s collateral and risk management framework. For users whose primary concern is transactional convenience or integration with specific platforms—such as CeFi exchanges that have standardized on USDS—this level of engagement may be sufficient.

Users seeking yield can supply USDS to the SSR module and receive sUSDS in return, gaining exposure to the administered savings rate without locking up funds or paying explicit fees. Because sUSDS is itself a transferable ERC‑20‑style token, it can be used across DeFi as a yield‑bearing asset, though each protocol integration entails separate smart contract and composability risks. The appeal of sUSDS lies in the combination of relatively stable, macro‑linked yield with full onchain transparency and flexibility. Unlike staking in validator sets or locking funds in ve‑style tokenomics, sUSDS holders do not take protocol‑specific slashing risk or commit to long‑dated lock‑ups; their primary risk is the overall solvency and operational integrity of Sky and its Agents.

More sophisticated users and institutions may engage with Sky as governance participants or as Agents themselves. Holders of the SKY token can propose and vote on changes to SSR, collateral parameters, and Agent mandates, influencing both risk and returns. Active governance participation requires a deep understanding of macro conditions, credit risk, and DeFi mechanics, as decisions about, for example, increasing RWA allocations or adjusting surplus buffer targets can have complex downstream effects. Institutional counterparties might seek to become Agents, managing portions of Sky’s collateral to earn fees while providing specialized expertise in areas like structured credit, tokenized securities, or regional regulatory environments. In this sense, Sky functions both as a public money protocol and as an allocation platform for professional asset managers.

Use cases for USDS and sUSDS span trading, payments, treasury management, and credit intermediation. Traders may use USDS as a quote currency on exchanges such as Binance and others that have migrated from DAI, while DeFi users deploy USDS or sUSDS as collateral in lending markets or as a base asset in liquidity pools. DAOs and crypto‑native treasuries may treat sUSDS as part of their reserve strategy, earning yield while maintaining nominal dollar exposure and onchain transparency. Fintech apps and neobanks integrating via Agents like Osero might eventually offer users “savings accounts” implicitly backed by sUSDS, abstracting away the complexity of DeFi while relying on Sky’s infrastructure under the hood. Each of these use cases, however, requires users to understand that they are exposed to a set of protocol‑level risks different from those associated with bank deposits or centralized stablecoins.

For risk‑conscious investors, the B‑ rating and the presence of an explicit surplus buffer provide some reference points, but they do not substitute for independent due diligence. Users must assess whether the additional yield offered by sUSDS over holding USDC or parking cash in a traditional savings account adequately compensates for smart contract risk, governance risk, and RWA‑related uncertainties. They must also consider liquidity and market structure: while USDS and sUSDS enjoy growing exchange and DeFi support, they do not yet match the ubiquity of USDT or USDC across all platforms and fiat on‑ramps. As with any financial product, suitability depends on individual risk tolerance, investment horizon, and the specific ways in which the assets will be used.

Conclusion

Sky Protocol represents one of the most ambitious attempts to redesign a large, battle‑tested stablecoin system around a new set of economic and governance principles. Building on the foundation laid by MakerDAO and DAI, it introduces USDS as a next‑generation stablecoin, sUSDS as a yield‑bearing savings token backed by protocol revenues, and SKY as a governance and value‑accrual token tied to the system’s long‑term performance. The protocol’s architecture—centered on the Sky Agent Network, real‑world asset allocations, and SubDAOs like Spark—seeks to connect onchain liquidity to institutional‑grade yield opportunities in a structured, transparent way. In doing so, it positions itself as a bridge between DeFi and traditional credit markets.

At the same time, Sky’s design choices expose it to a multifaceted risk profile. Heavy reliance on RWAs introduces legal and jurisdictional uncertainties, while smart contract and composability risks remain ever‑present despite a strong historical track record. The B‑ credit rating from S&P Global codifies these concerns in traditional financial language, classifying Sky as a speculative‑grade credit even as it receives praise for transparency and risk management practices. Governance tensions between maximizing short‑term tokenholder value via aggressive buybacks and prioritizing long‑term resilience through surplus accumulation have already surfaced in high‑profile decisions to slash buybacks and build reserves, especially in response to geopolitical shocks and external scrutiny.

Sky’s growing integration across CeFi exchanges, DeFi lending platforms, and multi‑chain environments suggests that it is becoming a significant piece of crypto market infrastructure, particularly as DAI liquidity transitions into USDS and sUSDS. Yet the reaction of other protocols, exemplified by Aave’s move to remove USDS as collateral, shows that this integration is not automatic or uncontested. Whether Sky ultimately becomes a dominant, broadly trusted stablecoin and savings layer, or remains a high‑yield niche product with constrained systemic reach, will depend on its ability to maintain its peg and solvency through future stress events while satisfying both regulators and market participants that its risk controls are adequate.

In sum, Sky Protocol stands at a crossroads where decentralization, real‑world finance, and algorithmic governance intersect. Its success or failure will carry lessons far beyond a single protocol, informing how future stablecoins balance transparency and complexity, yield and safety, and onchain autonomy and off‑chain regulation.

Outlook

Looking ahead, Sky Protocol’s trajectory will likely be shaped by three intertwined forces: macroeconomic conditions, regulatory developments, and the evolving competitive landscape of stablecoins and tokenized credit. If global interest rates remain elevated, the protocol’s RWA‑driven revenues should continue to support a moderate Sky Savings Rate without resorting to aggressive risk‑taking, reinforcing its positioning as a conservative yield instrument within DeFi. Conversely, a sharp decline in rates would test Sky’s ability to manage user expectations around yield and maintain surplus buffers while remaining attractive relative to competing products.

Regulation and ratings will also play a decisive role. As jurisdictions refine their approaches to stablecoins and tokenized securities, Sky will need to navigate a patchwork of rules affecting its Agents, custodians, and distribution partners, from CeFi exchanges to neobanks integrating sUSDS. Future revisions to S&P’s rating—upward or downward—will signal how traditional credit analysts view the protocol’s risk trajectory and may influence which institutions are willing to engage. Finally, competition from both centralized issuers and other RWA‑backed protocols will intensify, forcing Sky to differentiate through transparency, governance quality, and execution. For a crypto news audience, Sky Protocol will remain a critical story to watch, not only as a major stablecoin platform but as a bellwether for the broader experiment of merging decentralized infrastructure with institutional‑grade capital markets.

Latest Sky Protocol news

Bybit to auto-swap DAI balances for USDS at 1:1, joining Binance in adopting Sky Protocol's stablecoin rebrandAave votes to remove Sky Protocol's USDS as collateral, citing it "generates negligible revenue while its issuance model introduces asymmetric risks that could impact Aave's stablity"Sky guts buybacks 87% after S&P rates its reserves on par with DRC bonds, Rune warns 'massive oil shock' is comingThere’s a “third way” emerging in DeFi lending. Beyond monolithic and isolated models, SubDAO-based lending—pioneered by Sky and Spark—is quietly outperforming, combining unified liquidity with specialized execution and strong margins. A different blueprint for scaling DeFi credit. Private equity firm Bridgepoint to buy majority of crypto audit specialist ht.digital. Bridgepoint did not disclose the financial terms of the deal. Sky News cited a figure of 200 million pounds ($262 million).

Private equity firm Bridgepoint to buy majority of crypto audit specialist ht.digital. Bridgepoint did not disclose the financial terms of the deal. Sky News cited a figure of 200 million pounds ($262 million). Obex raises $37M to build 'Y Combinator' for RWA-backed stablecoins, led by Framework, Sky and LayerZero. $2.5B will also be deployed by Sky into projects incubated by Obex.

Obex raises $37M to build 'Y Combinator' for RWA-backed stablecoins, led by Framework, Sky and LayerZero. $2.5B will also be deployed by Sky into projects incubated by Obex.Sources

- https://sky.money

- https://blockeden.xyz/blog/2026/04/03/dai-usds-migration-makerdao-sky-protocol-stablecoin-rebrand/

- https://solana.com/es/podcasts/talking-tokens/episodes/how-sky-is-building-the-future-of-stablecoin-yield-with-usds-rune-christensen-e3hkhcb

- https://eco.com/support/en/articles/15254003-sky-savings-rate-deep-dive-2026-ssr-susds-usds-mechanics

- https://x.com/SkyEcosystem/status/2067251346391048701

- https://www.spglobal.com/ratings/en/products/solutions/digital-assets

- https://x.com/SkyEcosystem/status/2064041172796948616

- https://x.com/SkyEcosystem/status/2053852668536246329

- https://governance.aave.com/t/arfc-remove-usds-as-collateral-and-increase-rf-across-all-aave-instances/23426

- https://morpho.org/stories/sky/

- https://x.com/SkyEcosystem/status/2054218216553980254

- https://sky.money/susds

- https://www.spglobal.com/ratings/en/regulatory/article/-/view/type/HTML/id/3421145

- https://www.youtube.com/watch?v=Kby78i-bg9M

- https://www.spglobal.com/ratings/en/regulatory/article/-/view/sourceId/101638334

- https://www.dlnews.com/articles/defi/sky-slashes-buybacks-to-boost-reserves-of-usds-stablecoin/

- https://tokenomics.com/articles/sky-tokenomics-how-the-smart-burn-engine-destroys-102m-in-sky-per-year

- https://blockanalitica.substack.com/p/the-sky-risk-and-analytics-dashboard

- https://makerdao.com/whitepaper/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…