Deep dive on how interest rates shape crypto: from Fed and ECB policy to DeFi lending curves, perp funding, stablecoin revenue models, and user-set rates in Liquity-style designs, plus macro and fiscal-dominance risks ahead.

- x.com11

- leviathannews.substack.com3

- dlnews.com2

- truthsocial.com1

- snapshot.org1

- vendorfinance.medium.com1

- thedefiant.io1

+5 sources across the wider coverage universe

Private credit stress spreads as BNPL loans and fintech lending weaken, with funds limiting withdrawals amid rising defaults and pressure from higher interest rates2026-03

Private credit stress spreads as BNPL loans and fintech lending weaken, with funds limiting withdrawals amid rising defaults and pressure from higher interest rates2026-03 Borrowers raise rate rigging flags on Morpho as hard kink model allows deposit-withdraw loops, sparking curve redesign review2026-03

Borrowers raise rate rigging flags on Morpho as hard kink model allows deposit-withdraw loops, sparking curve redesign review2026-03 Fed's Waller went in ready to cut rates, but Iran war oil spike forced a hold — says cuts still possible later in 20262026-03

Fed's Waller went in ready to cut rates, but Iran war oil spike forced a hold — says cuts still possible later in 20262026-03 Crypto’s post-2021 stagnation comes down to tight liquidity, high interest rates, and weakening USD stability, keeping risk-on assets capped despite visible progress. Stablecoins stand out as the only sector with real institutional traction, while AI has absorbed most speculative capital and broader crypto awaits a clear macro or regulatory shift.2026-02

Crypto’s post-2021 stagnation comes down to tight liquidity, high interest rates, and weakening USD stability, keeping risk-on assets capped despite visible progress. Stablecoins stand out as the only sector with real institutional traction, while AI has absorbed most speculative capital and broader crypto awaits a clear macro or regulatory shift.2026-02 In today’s The Tentacle, we explore the USD0++ depeg drama that shook DeFi this weekend. Usual Money’s abrupt redemption changes sent ripples through Morpho, Pendle, and beyond—trapping leveraged farmers, spiking interest rates, and raising eyebrows over MEV Capital’s role in the chaos. Is this a case of mismanagement, bad comms, a calculated play, or all three?

We break down the mechanics, the fallout, and what this means for DeFi’s future in our latest newsletter. Don’t miss it—stay informed, stay ahead.2025-01

In today’s The Tentacle, we explore the USD0++ depeg drama that shook DeFi this weekend. Usual Money’s abrupt redemption changes sent ripples through Morpho, Pendle, and beyond—trapping leveraged farmers, spiking interest rates, and raising eyebrows over MEV Capital’s role in the chaos. Is this a case of mismanagement, bad comms, a calculated play, or all three?

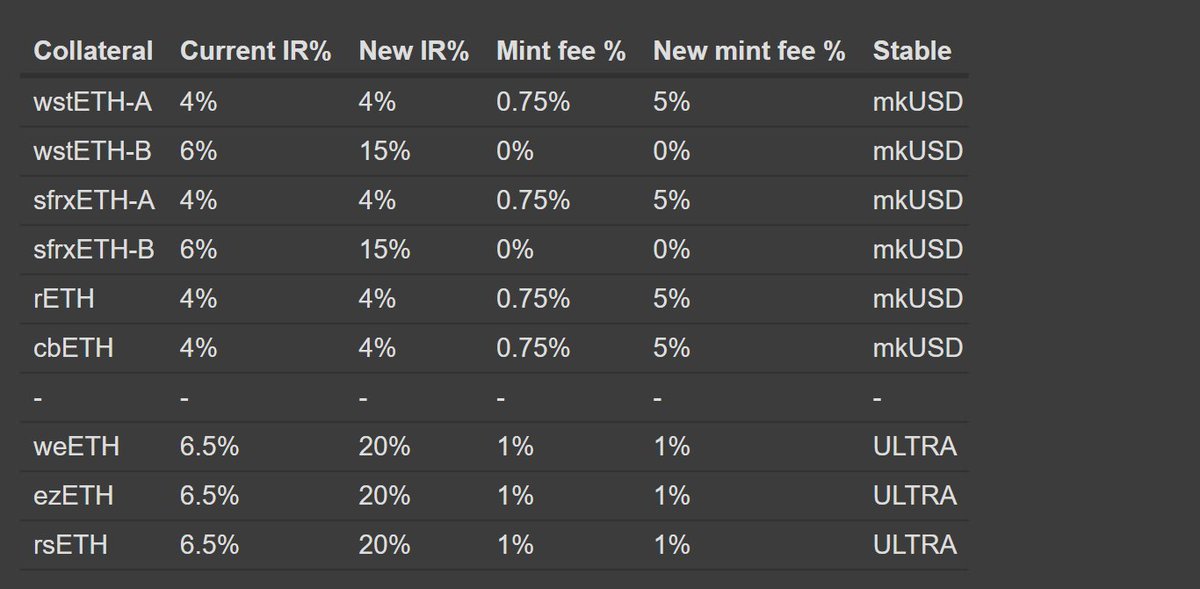

We break down the mechanics, the fallout, and what this means for DeFi’s future in our latest newsletter. Don’t miss it—stay informed, stay ahead.2025-01 First MakerDao, now Prisma proposes a 5% mint fee or 15% interest rates for minting its stablecoin2024-03

First MakerDao, now Prisma proposes a 5% mint fee or 15% interest rates for minting its stablecoin2024-03

Interest Rates in Crypto and DeFi: An Evergreen Guide

Interest rates are the price of money over time: the percentage you pay to borrow or earn to lend, usually quoted per year. In crypto, that same idea shows up everywhere from Federal Reserve policy to DeFi lending pools, perpetual futures funding rates, and the yield that backs stablecoins, making rates one of the quiet forces that shape every market cycle.

What Do We Mean by “Interest Rates”?

At its core, an interest rate is the fee paid on top of an amount of money, called the principal, for the right to use that money for a period of time. When you borrow, the rate is a cost; when you lend or deposit, the rate is your compensation for giving up liquidity and taking risk. In traditional finance, rates are normally expressed as an annual percentage rate, even if interest is charged or credited more frequently, which lets you compare different loans or investments on a common basis. This concept underpins everything from mortgages and credit cards to bond yields and bank savings accounts, and it is exactly the same logic that sits under crypto lending protocols and stablecoin treasuries.

Economists often distinguish between nominal and real interest rates to capture the difference between quoted returns and purchasing-power–adjusted returns. The nominal rate is the sticker number you see on a loan or a bond, while the real rate subtracts expected inflation to show how much your money is actually growing in terms of what it can buy. For example, if a stablecoin issuer earns 4% on Treasury bills while inflation runs at 3%, its real return is roughly 1% before fees and operating costs. Crypto markets are deeply exposed to these real rates because they shape the relative appeal of holding risky tokens versus earning essentially risk-free yields in government securities or high-grade money market instruments.

There is also an important distinction between policy rates and market rates. Policy rates are set or targeted by a central bank, such as the Federal Reserve’s federal funds target range in the United States or the European Central Bank’s deposit and refinancing rates in the euro area. Market rates, by contrast, are determined by supply and demand across many buyers and sellers and include yields on government and corporate bonds, interbank lending rates, and consumer borrowing costs. Even in DeFi, where there is no central bank, you can think of lending protocol rates, derivatives funding rates, and protocol-controlled “user-set” rates as different market rates emerging from specific mechanisms and incentives. Understanding how these fit together is the first step to seeing how changes in interest rates ripple into crypto.

Finally, interest rates are the mathematical expression of the time value of money, the idea that a dollar today is worth more than a dollar tomorrow because you can invest it, earn a return, or simply enjoy the flexibility of having it now. Every discounted cash-flow model used to value growth stocks or real-world assets on-chain embeds an interest rate that converts future cash flows into today’s value. In practice, when central banks raise rates, the discount rate used across markets tends to rise, pulling down valuations on long-duration assets such as tech equities and speculative crypto tokens. When they cut, the opposite is true: future narratives become more valuable, and capital hunts for risk and growth again.

Private credit stress spreads as BNPL loans and fintech lending weaken, with funds limiting withdrawals amid rising defaults and pressure from higher interest rates

Higher rates exposing all the garbage lending that happened 2020-2022. Private credit party is over

Readers click interest-rate stories not for the rate number itself but for the power struggle over who sets it — governance attacks on lending curves, protocol designs that hand rate control to borrowers, and Fed decisions that cascade into DeFi collateral mechanics collectively dominate the top of the click chart, revealing that 'rate risk' in crypto is fundamentally a control and accountability story.↗

Central Banks, Policy Rates, and the Global Macro Backdrop

In traditional finance, the most important interest rate is usually the central bank’s policy rate, because it anchors the entire curve of short-term borrowing costs and heavily influences longer-term yields. In the United States, the Federal Reserve targets a range for the federal funds rate, the overnight rate at which banks lend reserves to each other, and it achieves that target by adjusting the supply of reserves and using tools such as interest on reserve balances and open market operations. When the Fed raises this target range, it becomes more expensive for banks to fund themselves, which tends to push up rates on everything from business loans to credit cards, and when it cuts, the opposite happens. During the post-pandemic tightening cycle, the Fed raised the federal funds range aggressively and, according to J.P. Morgan’s commentary, held it in a 4.25% to 4.5% band at the May 2025 meeting as it waited for clearer inflation data.

Other sources track the realized and expected path of these rates in detail. Market data from one forecasting service shows the effective federal funds rate—that is, the actual average overnight rate paid in the market—around 3.63% at one point, with futures pricing a modestly higher path toward roughly 3.8% by late 2026 and about 4% thereafter. This kind of forecast reflects traders’ expectations for growth, inflation, and Fed policy over several years, and it feeds back into how longer-term yields are priced. Strategists at J.P. Morgan expect that by the end of 2026, 10‑year U.S. Treasury yields could trade near 4.35%, with similar upward pressure on German Bunds and UK gilts, and they argue that most developed‑market central banks are likely to be on hold through much of that year, with the Fed and the Bank of England only cutting slightly further. For crypto investors, those expectations are not academic; they shape the prospective returns on safe assets that compete directly with stablecoins and DeFi yields.

In Europe, the European Central Bank sets three key policy rates: the deposit facility rate, the main refinancing operations rate, and the marginal lending facility rate. At a recent meeting, the ECB raised its deposit rate by 0.25 percentage points to 2.25%, with corresponding increases in its other key rates, after having kept them on hold for several prior meetings. ECB staff simultaneously revised their inflation projections upward, expecting headline inflation to average around 3% in 2026 before drifting closer to the 2% target later in the decade. Market pricing implied a few more small hikes further out, though many analysts believed the ECB was near the end of its tightening phase, with limited appetite for aggressive moves either way. These dynamics matter for euro‑denominated stablecoins and for European banks and fintechs whose interest income is tied to the ECB’s rate path.

To summarize these policy stances in a purely illustrative way, consider the following snapshot of recently discussed or forecast rates and narratives:

| Institution / Rate | Level / Forecast (Illustrative) | Recent Stance and Commentary |

|---|---|---|

| Federal Reserve – Fed funds | Target 4.25–4.5% (May 2025); effective ≈3.63% | Held steady as inflation cooled but remained above target; markets priced modest future cuts. |

| European Central Bank | Deposit 2.25%; main refi 2.40%; marginal 2.65% | Raised rates slightly amid renewed inflation pressures; signaled data‑dependent, gradual path. |

| Global DM bond markets | 10‑year UST ≈4.35%, Bund ≈2.75%, gilt ≈4.75% (2026 forecast) | Strategists see yields “grinding higher” and easing cycles largely concluded by early 2026. |

Central banks also shape expectations rather than just current levels. Tools like the CME FedWatch dashboard translate futures prices into explicit probabilities that the Fed will hike, hold, or cut at upcoming meetings, and these probabilities are widely watched in both TradFi and crypto trading rooms. It is common to see headlines about FedWatch probabilities rising or falling after CPI releases or geopolitical shocks, and in our own coverage we have highlighted moments where the tool showed around a two‑thirds chance of a 25‑basis‑point cut at a particular meeting. Those shifting odds are quickly reflected in dollar strength, Treasury yields, and risk assets, including bitcoin and major altcoins.

One of the deeper macro debates of this cycle is whether advanced economies are drifting into an era of fiscal dominance, where high public‑debt burdens constrain central banks’ willingness or ability to keep rates high enough to fully control inflation. Research from the Boston Fed describes fiscal dominance as a situation where an increasing debt‑to‑GDP ratio makes it politically or financially difficult for the central bank to raise rates, because doing so would cause government interest costs to spike, threatening debt sustainability. Survey evidence from German households suggests that when people hear news implying higher future debt ratios, many revise their inflation expectations upward, especially if they already believe that fiscal resources are tight. In a New Keynesian model with heterogeneous beliefs, such expectations of future fiscal dominance can push up inflation today, forcing the central bank into a trade‑off between tightening policy now at the cost of weaker growth or tolerating somewhat higher inflation. For crypto markets, which often frame bitcoin and some stablecoins as hedges against monetary or fiscal excess, this debate is not merely academic; it feeds narrative cycles about debasement, “hard money,” and the relative appeal of on‑chain dollars versus fiat.

How Interest Rates Shape Crypto Market Cycles

Crypto markets sit at the intersection of high‑beta technology exposure and alternative monetary experimentation, which makes them unusually sensitive to shifts in interest rates and global liquidity conditions. During periods of low rates and abundant liquidity, such as 2020–2021, investors are more willing to allocate to long‑duration, speculative assets where most of the expected payoff lies in the distant future. In traditional terms, higher-growth, higher‑risk cash flows get discounted at a lower rate, inflating present valuations, while the opportunity cost of holding non‑yielding assets (like a pre‑yield bitcoin) is relatively low. When the Fed and other central banks tighten aggressively, that calculus reverses: safe yields become more attractive, discount rates rise, and risk assets sell off. Many analysts argue that the post‑2021 stagnation in crypto prices, despite continued technical progress, reflects this regime shift toward higher real rates and tighter dollar liquidity.

This macro link runs not only through valuations but also through the plumbing of leverage and credit. Higher policy rates drive up funding costs for banks, prime brokers, and non‑bank lenders, and those higher costs make their way into margin lending, derivatives financing, and stablecoin borrowing. Private credit and fintech lenders that expanded aggressively in the low‑rate era have faced growing stress as rates rose, particularly in unsecured or lightly underwritten areas such as buy‑now‑pay‑later (BNPL) loans. Federal Reserve research suggests that BNPL users tend to carry higher outstanding debt balances, although they have historically shown lower default rates, which complicates the risk picture. As borrowing costs rise and growth slows, however, the margins on such lending compress, and we have already seen funds gating withdrawals and tightening standards in parts of the private credit market. Crypto is not insulated from this dynamic: centralized finance (CeFi) firms that relied on cheap short‑term funding and risky long‑term lending imploded in 2022, and DeFi protocols now operate in an environment where traditional credit is more expensive and risk appetite more constrained.

Interest rates also shape flows into and out of crypto through the lens of opportunity cost. When investors can earn 4% or 5% on risk‑free Treasuries, the hurdle rate for allocating to a volatile asset like ETH or a DeFi governance token rises. J.P. Morgan’s global research desk expects developed‑market yields to remain relatively elevated through 2026, with only limited further easing from the Fed and Bank of England and essentially flat policy from the ECB, Riksbank, Reserve Bank of Australia, and others. In such a world, the relative attractiveness of simply holding a tokenized T‑bill or a fiat‑backed stablecoin backed by short‑term government debt is quite high compared with chasing illiquid DeFi yield strategies. This helps explain the growing institutional interest in tokenized cash and Treasuries and the way stablecoins have continued to gain traction as payments and settlement infrastructure even as speculative crypto activity cooled.

At the same time, crypto markets increasingly trade on interest‑rate expectations rather than just current levels. Policy communications from figures like the Fed chair, other governors, and regional presidents are dissected for hints about the trajectory and speed of future moves. In the last cycle, we saw episodes where a governor like Christopher Waller signaled openness to cutting rates only to be forced into a hold by an oil‑price spike tied to geopolitical tensions, illustrating how quickly the macro backdrop can shift. In the political arena, officials have pressured central bankers to cut faster to avoid slowing the economy, while critics have accused them of being too slow to respond to inflation. Crypto traders follow these dynamics closely because a dovish pivot or a surprise hold can move the dollar, bond yields, and high‑beta tech equities in ways that feed directly into bitcoin and altcoin prices. Even prediction markets like Polymarket have hosted large bets on specific FOMC outcomes, with whales wagering on whether there will be rate changes at particular meetings, turning monetary policy into a tradable event for on‑chain participants.

- 01User-set DeFi borrowing rates↗

Liquity v2's BOLD stablecoin and Asymmetry's USDaf both let borrowers fix their own rates, inverting the protocol-controlled model readers had grown skeptical of — the design itself was the news.

- 02Protocol rate governance attacks↗

Morpho's hard-kink deposit-withdraw loop exploit, Abracadabra's governance vote jacking CRV loan rates to 200%, and Prisma's 15% mint-rate proposal showed readers that on-chain rate governance is a live attack surface, not a safety feature.

- 03Fed/ECB macro decisions rippling into DeFi↗

FOMC holds, Waller's oil-shock pivot, and FedWatch probability shifts directly moved collateral yields and stablecoin revenues, making traditional monetary policy a front-page DeFi story.

- 04Stablecoin depeg from rate mechanic failures↗

USD0++'s abrupt redemption-policy change spiked borrow rates, trapped leveraged Morpho and Pendle farmers, and exposed how a single protocol's rate decision can cascade into a sector-wide liquidity crisis.

- 05Private credit and RWA rate arbitrage↗

Rising TradFi rates drove companies to blockchain-based private credit (55% sector surge) and tokenized Treasuries (ONDO), while simultaneously stressing funds that had lent at locked rates, creating both opportunity and withdrawal pressure.

- 06Rate-dependent business model risk↗

Circle's S-1 revealing 99% of revenue tied to Fed rates, and Robinhood/Revolut earnings pressure from rate compression, made readers confront that the most 'crypto-native' firms are deeply exposed to central bank decisions.

Interest Rates in DeFi Lending Markets

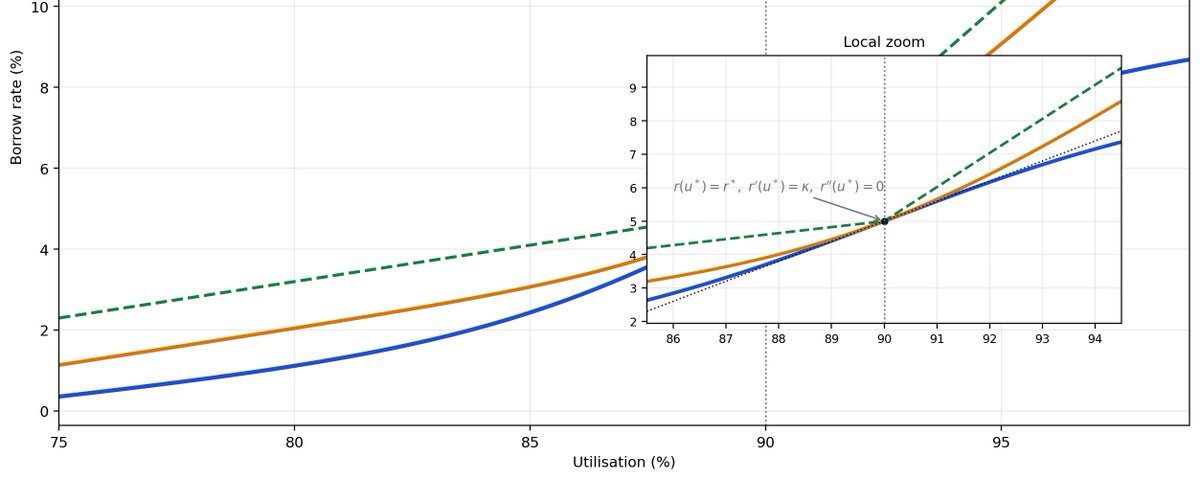

If central banks are the main architects of policy rates in TradFi, smart contracts are the architects of interest rates in DeFi. On leading DeFi lending platforms, such as Aave and Compound, interest rates on loans and deposits are not set by a committee but by algorithms encoded in the protocol’s smart contracts. These algorithms typically link the interest rate for each asset to the pool’s utilization ratio, which is the share of supplied liquidity that is currently borrowed. When utilization is low, rates tend to be low, encouraging borrowing and discouraging additional supplying; as utilization rises, rates increase, making borrowing more expensive and attracting more suppliers until a new equilibrium is reached. The Banque de France, which examined major DeFi platforms, found that these algorithmic rates can be quite volatile and sometimes appear surprisingly disconnected from traditional money market rates, underscoring how DeFi can follow its own micro‑dynamics even as it remains indirectly influenced by macro policy.

Academic researchers have started to analyze how these mechanisms play out in practice by studying granular transaction data from large protocols. A study of Aave v2, for instance, seeks to uncover the main drivers of DeFi intermediation, examining who supplies and borrows, how sensitive they are to interest rate changes, and how liquidity migrates between pools. One key insight is that DeFi lenders and borrowers are often sophisticated, actively arbitraging rate differences between pools and platforms, which can amplify rate volatility as liquidity chases the best yields. Another is that collateral composition and governance decisions, such as listing a new asset or changing a risk parameter, can have major effects on interest rate paths and utilization, sometimes creating feedback loops that are reminiscent of bank funding squeezes or repo market dislocations in TradFi, but playing out entirely on‑chain.

Not all DeFi rate curves are simple, smooth functions. Some protocols employ nonlinear designs with distinct “kinks” where the interest rate jumps more aggressively once utilization crosses a particular threshold, in order to strongly discourage further borrowing and protect liquidity for withdrawals. The Morpho ecosystem, for example, has used an AdaptiveCurve interest rate model with a so‑called hard kink, which can produce very steep increases in borrow rates near full utilization. Risk analysts at LlamaRisk have highlighted that when such curves are combined with complex vault structures, they can create odd incentives and potential attack vectors, including the possibility of “rate rigging” where sophisticated participants loop deposits and withdrawals to manipulate yields or to stress the system. These concerns have sparked design reviews and discussions about how to preserve protective rate features without enabling abusive strategies, illustrating how central interest rate design is to DeFi protocol safety and fairness.

The volatility and at times disconnection of DeFi rates from traditional benchmarks raise the question of how much monetary policy actually matters for on‑chain lending. The Banque de France analysis suggests that traditional rate moves can affect DeFi rates through several channels: by changing the returns on alternative safe assets, by influencing risk sentiment and thus demand for leverage, and by affecting the cost of off‑chain funding for market makers who interact with DeFi. However, because DeFi protocols mostly deal in overcollateralized loans and are funded by crypto‑native assets, their short‑term rate dynamics are more strongly driven by internal factors such as protocol incentives, liquidity mining programs, and the speculative cycles of underlying tokens. This means that you can see very high DeFi rates even when TradFi policy rates are low, and vice versa, creating a mosaic of yield opportunities and risks that is unique to on‑chain markets.

Borrowers raise rate rigging flags on Morpho as hard kink model allows deposit-withdraw loops, sparking curve redesign review

Deposit-withdraw loops to game kink-based IRMs are as old as Compound v2 — the difference is Morpho's immutable AdaptiveCurveIRM can't be patched via governance vote the way Aave just tweaks slope parameters. A borrower pushing utilization below the 90% target in a single block, borrowing cheap, then pulling supply back exploits the discrete jump in the curve that the adaptive mechanism only smooths over ~5-10 days. Any redesign has to choose between a smoother curve (less capital efficient, weaker incentive to repay) or shorter adaptation windows (more volatile rates for passive LPs) — there's no free lunch here, and Morpho V2's push toward fully market-driven rates might just move the manipulation surface from the IRM to the curator layer.

Fixed vs Variable Rates and New DeFi Rate Models

Most early DeFi lending protocols offered purely variable rates, exposing borrowers and lenders to the full volatility of utilization‑driven curves. As markets matured, demand grew for more predictable borrowing costs and returns, similar to fixed‑rate mortgages or corporate bonds in TradFi. Some protocols responded by introducing pseudo‑fixed structures, such as time‑bound lending markets where users lock in a rate until a maturity date, or interest rate swaps that let participants exchange floating for fixed cash flows. Others, especially in the stablecoin space, began to experiment with mechanisms that make the borrowing cost itself a user‑defined parameter rather than a purely algorithmic outcome.

An example of this trend is Asymmetry Finance’s USDaf, a stablecoin that markets itself as allowing borrowers to set their own fixed interest rates when minting against collateral such as bitcoin or yield‑bearing assets. Rather than taking whatever variable rate a pool offers, a user chooses a rate that balances their desire for cheap funding against the likelihood that other market participants will be willing to provide capital at that rate. This turns interest rate discovery into a marketplace in its own right, where users negotiate, implicitly or explicitly, about the fair cost of leverage. The design promises more customization and transparency but also raises questions about how to prevent adverse selection, ensure sufficient liquidity, and handle scenarios where market rates move far from previously chosen fixed rates.

At a more structural level, new research and whitepapers have proposed “variable fixed rate” (VFR) frameworks that layer fixed‑rate experiences on top of utilization‑based models. These designs often draw inspiration from protocols like Liquity, which in its first version offered interest‑free loans against ETH with a one‑time fee, and in its upcoming v2 iteration is exploring user‑set interest rates for a new stablecoin backed by multiple types of collateral. The idea of VFR is to let users lock in a borrowing cost for a period while the protocol manages the underlying variable‑rate exposure through hedging or internal buffers. In effect, the protocol becomes an interest rate transformer, turning volatile DeFi yields into something that feels more like a bond coupon for end‑users, while still being rooted in on‑chain liquidity conditions.

These experiments highlight an important distinction between who sets interest rates and how risk is shared. In centralized finance, banks and lenders largely dictate rates, adjusting them in response to competition, funding costs, and regulatory constraints. In first‑generation DeFi, protocols embedded a mathematical rule and let market conditions drive the outcome. In the new wave of user‑set–rate systems, borrowers have more control up front, but they must convince others to fund them, shifting some of the rate‑setting function to peer‑to‑peer negotiation, mediated by smart contracts. Each approach comes with trade‑offs in transparency, predictability, and systemic resilience, and their coexistence is likely to give on‑chain users a richer but more complex menu of interest‑bearing strategies.

Liquity v2 announced: user-set rates, BOLD stablecoin, multi-collateral CDPs

USD0++ depeg: Usual Money changes redemption rules, spikes Morpho/Pendle borrow rates, traps leveraged farmers

Polymarket whale bets $1.3M on Fed no-change at July FOMC; CME FedWatch tracks 69% cut probability for December

FedWatch shows 69.4% probability of 25bp Fed cut in December

FOMC holds rates at 4.25%–4.5% range; Asymmetry Finance launches USDaf with user-fixed borrow rates

Fed's Waller holds rates citing Iran war oil-price spike, signals cuts remain possible later in 2026

Perpetual Futures Funding Rates: Crypto’s Synthetic Interest

One of the most visible “interest rates” in crypto is not a loan rate at all but the funding rate on perpetual futures contracts. Perpetual futures, or perps, are derivatives that track the price of an underlying asset, such as BTC or ETH, without an expiry date. To keep the perp price anchored to the spot price, exchanges use a funding mechanism where traders on one side of the market pay a periodic fee to traders on the other side, usually every few hours. When the perp is trading above spot, long positions pay shorts; when it trades below spot, shorts pay longs. The funding payment is effectively an interest rate on the leveraged exposure that incentivizes traders to bring the perp back in line with the underlying spot market.

The funding rate can be annualized to give a sense of the implied yield or cost of holding a perpetual position. For example, a funding payment of 0.01% every eight hours translates, roughly, into an annualized rate in the mid‑teens, depending on compounding assumptions. During speculative frenzies, funding rates can spike to extremely high levels as traders crowd into long positions, effectively paying large interest to remain leveraged. Conversely, in fearful or bearish markets, funding can go deeply negative, rewarding contrarian longs who are willing to hold exposure while most participants are short. These swings make funding rates a key barometer of positioning and sentiment in the derivatives market, and they create opportunities for basis trades where investors arbitrage differences between spot yields and perp funding.

Exchanges and DeFi derivatives protocols can adjust funding mechanics over time. An example is the decision by one venue to shift certain stock‑indexed perps, such as contracts linked to HOOD, INTC, AMZN, SNDK, and MU, to an eight‑hour funding interval while simultaneously reducing the interest rate component to zero. Changes like this affect how quickly imbalances between longs and shorts get corrected and how attractive it is for market makers and arbitrageurs to provide liquidity. For protocol designers, there is a balance to strike between keeping the perp closely anchored to spot, minimizing manipulative behavior, and avoiding excessive costs that could deter participation. For traders, monitoring funding rates across venues is akin to tracking short‑term interest rates in FX or fixed income markets; it reveals where leverage is concentrated and what it costs to be on each side of the trade.

Perp funding also connects back to macro rates through relative value. When cash rates on dollars are near zero, earning a modest but steady positive funding rate by being short perps can look attractive, especially for market‑neutral funds. When risk‑free rates are 4% or 5%, that same strategy must clear a higher hurdle to be worthwhile. Similarly, protocols that share funding revenues with token holders effectively turn those tokens into claims on a stream of interest‑like cash flows, whose value will be sensitive to both crypto‑specific volatility and the broader rate environment. As with DeFi lending, the interplay between perp funding and macro rates will likely grow more complex as more sophisticated traders bring fixed‑income and volatility‑arbitrage techniques on‑chain.

Stablecoins, Tokenized Treasuries, and Rate‑Sensitive Business Models

Stablecoins are arguably the clearest bridge between traditional interest rates and crypto. Fiat‑backed stablecoins like USDC and USDT hold reserves in cash, bank deposits, and short‑term government securities, and the interest earned on those reserves can be a massive revenue source when policy rates are high. Analysis of Circle, the issuer of USDC, shows just how rate‑sensitive this model is: in 2024, Circle generated on the order of $1.6–$1.7 billion in revenue, with roughly 99% of that coming from interest income on USDC reserves rather than transaction fees or other services. As USDC’s outstanding supply rebounded toward around $60 billion, the company’s fortunes became tightly intertwined with the yields available on U.S. Treasuries and bank deposits. If the Fed were to cut rates back toward zero, the interest income underpinning this business would shrink dramatically, raising questions about sustainability and competition.

This dependence on rates has strategic implications as stablecoin issuers move toward public markets and as large corporations consider launching their own tokenized cash instruments. Circle’s plans to go public, described in filings and analyses, are unfolding just as major firms like JPMorgan, Walmart, PayPal, and Meta explore their own stablecoin or tokenized deposit offerings, many of which also rely on earning interest on customer balances. McKinsey has argued that tokenized cash can serve as a next‑generation payments infrastructure, enabling peer‑to‑peer transfers between blockchain wallets without the need for traditional bank accounts. But if multiple issuers are chasing the same pool of rate‑driven revenue, the competitive pressure to share more of that yield with users, either through rewards or integration benefits, will grow. In a low‑rate world, some business models that look lucrative today could compress to thin margins, prompting consolidation or strategic pivots.

On the DeFi side, protocols like Ondo Finance have built products that offer tokenized exposure to U.S. Treasuries, effectively bringing money market‑fund–like yields on‑chain. These products are most compelling when Treasury yields are relatively high, because they offer a simple, regulated path for on‑chain investors to earn a steady return backed by government securities, while taking on some smart contract and custody risk. J.P. Morgan’s forecast that 10‑year Treasuries could sit around 4.35% in 2026 suggests that yields might remain appealing for such strategies in the medium term, although the exact path of short‑term bills, which stablecoin issuers prefer, will depend on Fed policy. If and when the rate cycle turns decisively lower, the yield advantage of tokenized Treasuries over non‑yielding stablecoins and DeFi blue chips will narrow, forcing RWA protocols to differentiate on other dimensions such as access, liquidity, and regulatory clarity.

Stablecoin design is also evolving in response to interest‑rate volatility. Projects like Liquity v2, which introduces a new stablecoin backed by user‑set interest rates and an adaptive redemption mechanism, and Asymmetry’s USA.d, which aims to borrow against a very large base of crypto assets while allowing users to set their own loan rates, point toward a world where stablecoins are not just passive containers of external yields but active participants in on‑chain credit markets. In these systems, interest rates become a core governance variable: they influence how much demand there is to mint the stablecoin, how attractive it is to hold, and how resilient the peg will be under stress. When these mechanisms work well, they can produce more tailored and transparent interest‑bearing instruments; when they fail, they can contribute to depeggings, liquidity squeezes, and cascading liquidations.

Fed's Waller went in ready to cut rates, but Iran war oil spike forced a hold — says cuts still possible later in 2026

All talk but no action. What is we are ready but oil spike forced a hold. Just say you aren't ready

Morpho's hard-kink utilization model allowed deposit-withdraw loops that let large depositors manipulate the effective borrow rate paid by smaller borrowers, triggering a curve redesign review.

- Centralization / governance captureHigh

Abracadabra governance voted to push CRV loan rates to 200%, which a core Fraxlend developer publicly called a 'rug,' illustrating how token-weighted governance can weaponize rate levers against minority borrowers.

USD0++ redemption-rule changes and private-credit fund withdrawal limits both demonstrated that rate-shock events can simultaneously freeze exit routes and spike borrow costs, compressing the window for leveraged positions to unwind safely.

Fed rate holds driven by geopolitical shocks (Iran war oil spike, 2026) rather than domestic inflation data introduce unpredictable timing risk for DeFi yield strategies that price in consensus-driven cut schedules.

Stablecoin issuers earning Treasury yields (Circle, Usual Money) and RWA protocols (ONDO) face direct revenue compression if the Fed cuts to near-zero, a structural fragility Circle's S-1 quantified as near-total revenue exposure.

With global debt at $307 trillion and credible warnings of fiscal dominance forcing central banks to suppress rates regardless of inflation, DeFi protocols built on high-yield RWA collateral face a regime-change tail risk that has no on-chain hedge.

User‑Set Interest Rates and the Liquity/Asymmetry Design Space

The idea of letting users set their own interest rates flips the traditional lender–borrower relationship on its head. In protocols inspired by Liquity v2 or Asymmetry’s USDaf and USA.d, a user seeking to borrow stablecoins against collateral such as ETH, BTC, or liquid staking tokens specifies the interest rate they are willing to pay, often as a fixed rate for a given term. On the other side, capital providers choose which loans to fund based on their desired return and risk tolerance, effectively creating a marketplace where rates are discovered through many micro‑negotiations. The smart contract enforces collateralization and payment terms, but it does not centrally dictate the rate; instead, it mediates a decentralized matching process.

This architecture echoes peer‑to‑peer lending platforms in TradFi, but with important differences. Collateralization levels are typically much higher in DeFi, reducing credit risk, while smart contracts handle custody and execution automatically, reducing operational overhead. However, the absence of a central underwriter or balance sheet also means that liquidity can fragment across many small positions, and interest rates can diverge across similar risk exposures if market information is incomplete. To mitigate this, user‑set rate protocols often incorporate automated redemption or refinancing mechanisms: if market rates fall below the rate on an existing loan, other users can repay that loan and take over the collateral, or borrowers can refinance at a lower rate, ensuring that stale, above‑market rates do not persist indefinitely.

These systems must also grapple with coordination and systemic‑risk questions. If most borrowers try to set unrealistically low rates, they may find no funding, causing minting of the stablecoin to stall and potentially undermining its liquidity and utility. Conversely, if borrowers are willing to pay very high rates during a bull market, the protocol may appear to thrive in the short term as interest revenue surges, but it could become brittle as users become over‑leveraged at expensive rates just as macro conditions tighten. Governance plays a critical role in setting bounds, defaults, and safety valves to prevent runaway dynamics. In a sense, the community becomes a miniature central bank, deciding how flexible or constrained the rate‑setting process should be, and when to intervene to protect the system’s integrity.

From a broader perspective, user‑set interest rates express a key ethos of crypto: shifting control from institutions to markets and individuals, while relying on code to enforce rules. Whether this approach will yield more efficient, fair, and resilient credit markets remains an open question. On the one hand, it promises a more granular and participatory form of price discovery; on the other, it demands a level of financial literacy and risk management from users that cannot be assumed. Over time, we are likely to see layered architectures where sophisticated participants provide liquidity and risk transformation behind the scenes, smoothing out some of the extremes, while retail‑facing interfaces present simplified choices that still respect the underlying user‑set rate logic.

Credit Stress, BNPL, and Lessons for DeFi Risk

Higher interest rates do not merely change prices; they expose weaknesses in credit structures that were built for a different regime. In traditional finance, the rise of BNPL and other fintech lending models during the low‑rate years was fueled by cheap funding and aggressive growth targets. Research indicates that BNPL users often carry higher overall debt loads, yet they historically showed lower default rates, likely reflecting both selection effects and the still‑benign credit environment during the early growth phase. As policy rates climbed and inflation eroded real incomes, the stress in these segments intensified, leading some funds and lenders to tighten credit, raise fees, or restrict withdrawals from vehicles exposed to illiquid or deteriorating loans.

These developments offer useful analogies for DeFi. On‑chain lenders often extend so‑called riskless leverage, where loans are fully collateralized by volatile assets such as ETH or governance tokens. This structure avoids the problem of unsecured defaults but introduces the risk of cascading liquidations when collateral prices fall and interest rates spike simultaneously. Events like the sudden change in redemption rules and subsequent depeg of a stablecoin such as USD0++, which reportedly sent shockwaves through protocols like Morpho and Pendle, illustrate how quickly on‑chain credit conditions can tighten when confidence is shaken. As leveraged farmers rush to unwind positions and speculators flee, utilization ratios can surge, algorithmic rate curves can push borrowing costs sharply higher, and liquidity for withdrawals can evaporate temporarily, creating a feedback loop eerily reminiscent of bank runs or gated funds in TradFi.

The Morpho case study, where concerns were raised about the possibility of rate manipulation via deposit‑withdrawal loops exploiting a hard‑kinked rate model, underscores another lesson: interest rate design can itself be a source of risk. Just as flawed reference rates like LIBOR were vulnerable to manipulation in traditional markets, poorly designed on‑chain curves or oracle mechanisms can incentivize behavior that undermines the fairness or solvency of the system. Risk frameworks such as those developed by LlamaRisk aim to identify these vulnerabilities in advance, but as protocols compete for yields and users, the temptation to push more exotic or fragile rate structures into production can be strong. Builders and users alike must recognize that high headline yields often come with hidden structural risks that may only become apparent when macro rates move abruptly or when liquidity dries up.

For DeFi, learning from BNPL, private credit, and fintech stress means thinking in terms of cycles and buffers. Protocols that are calibrated for a world of low vol, low inflation, and abundant liquidity may perform poorly in a high‑rate, high‑uncertainty environment. Those that bake in conservative collateral requirements, robust liquidation mechanisms, and stress‑tested rate models are more likely to survive. From a user’s perspective, assessing not only the current yield but also the sustainability of that yield under different interest rate scenarios is crucial. A 20% APY funded by leveraged bets on short‑term rates staying low is very different from a 5% APY backed by short‑duration Treasuries and overcollateralized loans.

Frameworks for Traders and Builders: Thinking in Rates

For traders, incorporating interest rates into a crypto thesis starts with monitoring the global rate cycle. Tools like the CME FedWatch, which translates futures pricing into probabilities for upcoming Fed moves, provide a concise view of market expectations. When the probability of cuts rises, risk assets often rally as investors anticipate easier financial conditions; when the odds of hikes or extended holds increase, the opposite tends to occur. Overlaying these expectations with J.P. Morgan’s forecasts for bond yields and central bank policy—such as their expectation that most developed‑market central banks will be on hold through 2026, with only modest further easing by the Fed and Bank of England—helps frame the likely range of scenarios for the risk‑free rate backdrop. Within crypto, that backdrop influences the fair value of stablecoin issuers, tokenized T‑bill products, DeFi lending yields, and even perp funding regimes.

At a more micro level, traders can view every on‑chain yield as a combination of a base risk‑free component and a risk premium. Tokenized T‑bill products and fiat‑backed stablecoins invested in government securities approximate the risk‑free leg, subject to smart contract and custody risk. DeFi lending yields add protocol risk, collateral volatility, and utilization‑driven variability. Perp funding rates add directional and volatility risk tied to leveraged positioning. Understanding how these components respond to changes in macro rates can reveal mispricings. For example, if tokenized T‑bill yields fall quickly after a Fed cut while some DeFi lending markets still reflect much higher rates because of slow rate‑sensitive capital migration, there may be opportunities to supply liquidity on‑chain and hedge off‑chain, or vice versa, depending on your access and risk appetite.

Builders, meanwhile, should treat interest rate design as a first‑class protocol primitive, not an afterthought. This means rigorously stress‑testing rate curves under extreme utilization, modeling how they respond to rapid price moves, and considering how they interact with incentives such as liquidity mining or fee rebates. It also means thinking about how the protocol’s revenue model behaves under different macro scenarios. A lending protocol that depends on chronically high borrow rates may look attractive at the top of a cycle but could suffer greatly when competition, deleveraging, or lower policy rates compress margins. Conversely, a protocol that can operate sustainably through a range of rate environments, perhaps by dynamically adjusting spreads or by offering both variable and pseudo‑fixed options, is more likely to build long‑term trust.

Finally, both traders and builders must recognize that interest rates are not merely numbers on a dashboard; they are embedded in a larger political and social context. The emerging debate over fiscal dominance, the pressure on central banks to balance inflation control with debt sustainability, and the experiments with user‑set on‑chain rates all reflect deeper questions about who should control the price of money and on what terms. Crypto’s promise is to offer alternative answers to those questions, but it cannot escape the gravitational pull of the broader rate environment. Integrating macro literacy with protocol‑level understanding is no longer optional; it is a prerequisite for serious participation in the space.

Outlook

Over the next several years, the most plausible baseline is a world of moderately positive real interest rates, with major central banks either at or near the end of their easing cycles and long‑term yields “grinding higher” rather than collapsing back to the near‑zero levels of the 2010s. In such a setting, on‑chain money markets, stablecoin issuers, and tokenized T‑bill products are poised to remain central pillars of the crypto ecosystem, while pure speculative leverage may face a higher hurdle. At the same time, the risk of fiscal dominance and policy error persists, creating periodic windows where narratives about debasement and “hard money” could return to the forefront. DeFi rate innovation—whether in algorithmic curves, user‑set stablecoin borrowing, or more sophisticated perp funding designs—will continue, offering richer tools but also new failure modes.

For a crypto audience, the key is to stop treating interest rates as an external curiosity and to start viewing them as part of the core state of the system, just like block times or gas fees. The future of stablecoins, DeFi lending, tokenized real‑world assets, and even the next bitcoin cycle will all be shaped by how global rate regimes evolve—and by how well on‑chain protocols internalize and respond to that reality.

Latest Interest rates news

Private credit stress spreads as BNPL loans and fintech lending weaken, with funds limiting withdrawals amid rising defaults and pressure from higher interest ratesBorrowers raise rate rigging flags on Morpho as hard kink model allows deposit-withdraw loops, sparking curve redesign reviewFed's Waller went in ready to cut rates, but Iran war oil spike forced a hold — says cuts still possible later in 2026Crypto’s post-2021 stagnation comes down to tight liquidity, high interest rates, and weakening USD stability, keeping risk-on assets capped despite visible progress. Stablecoins stand out as the only sector with real institutional traction, while AI has absorbed most speculative capital and broader crypto awaits a clear macro or regulatory shift. FedWatch shows a 69.4% rise in the probability of the Federal Reserve cutting interest rates by 25 basis points in December.

FedWatch shows a 69.4% rise in the probability of the Federal Reserve cutting interest rates by 25 basis points in December. Investors warn of ‘Fiscal Dominance’ era as soaring debt and rising rates pressure Central Banks to ease policy.

Global markets may be entering a phase of fiscal dominance, where central banks face growing pressure to keep interest rates low to offset record government borrowing costs—most notably in the U.S., U.K., and Japan.

Investors warn of ‘Fiscal Dominance’ era as soaring debt and rising rates pressure Central Banks to ease policy.

Global markets may be entering a phase of fiscal dominance, where central banks face growing pressure to keep interest rates low to offset record government borrowing costs—most notably in the U.S., U.K., and Japan.Sources

- https://www.investopedia.com/terms/i/interestrate.asp

- https://www.investopedia.com/ask/answers/031115/how-do-central-banks-impact-interest-rates-economy.asp

- https://streetstats.finance/rates/fedfunds

- https://www.pbs.org/newshour/politics/watch-live-powell-speaks-after-fed-committee-makes-decision-on-interest-rates-as-trump-demands-cut

- https://www.bostonfed.org/publications/research-department-working-paper/2025/household-beliefs-about-fiscal-dominance.aspx

- https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

- https://global.morningstar.com/en-gb/economy/ecb-raises-interest-rates-lifts-inflation-forecasts

- https://www.richmondfed.org/publications/research/economic_brief/2026/eb_26-05

- https://www.sciencedirect.com/science/article/abs/pii/S1042957325000348

- https://www.banque-france.fr/en/publications-and-statistics/publications/interest-rates-decentralised-finance

- https://www.llamarisk.com/research/morpho-vaults-risk-disclaimer

- https://home.asymmetry.finance/usdaf

- https://metamask.io/news/perpetual-futures-funding-frequency-strategies

- https://coinmetrics.substack.com/p/state-of-the-network-issue-307

- https://lex.substack.com/p/analysis-our-circle-ipo-primer-16b

- https://www.mckinsey.com/industries/financial-services/our-insights/the-stable-door-opens-how-tokenized-cash-enables-next-gen-payments

- https://www.jpmorgan.com/insights/global-research/outlook/market-outlook

- https://x.com/Aster_DEX/status/2028369694449910091

- https://www.jpmorgan.com/insights/outlook/economic-outlook/fed-meeting-may-2025

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…