Deep explainer on DAI, MakerDAO’s original overcollateralized dollar stablecoin, covering how it works, its Sky/USDS migration, collateral and risk, DeFi and CeFi use, and how it compares to USDC, USDT, USDe and other rivals.

+16 sources across the wider coverage universe

Crypto whale sues Coinbase over refusal to return stolen DAI tied to $55M phishing hack, despite exchange freezing funds and demanding court order to verify ownership2026-05

Crypto whale sues Coinbase over refusal to return stolen DAI tied to $55M phishing hack, despite exchange freezing funds and demanding court order to verify ownership2026-05 Bybit to auto-swap DAI balances for USDS at 1:1, joining Binance in adopting Sky Protocol's stablecoin rebrand2026-04

Bybit to auto-swap DAI balances for USDS at 1:1, joining Binance in adopting Sky Protocol's stablecoin rebrand2026-04 Liquity’s BOLD became the first decentralized stablecoin to earn an A- rating from Bluechip, scoring perfect 1.0 marks in Management, Decentralization, and Governance. Unlike USDC or DAI, BOLD cannot be frozen, has no admin keys, and is fully crypto-backed—highlighting the tradeoff between counterparty risk and smart-contract risk.2026-01

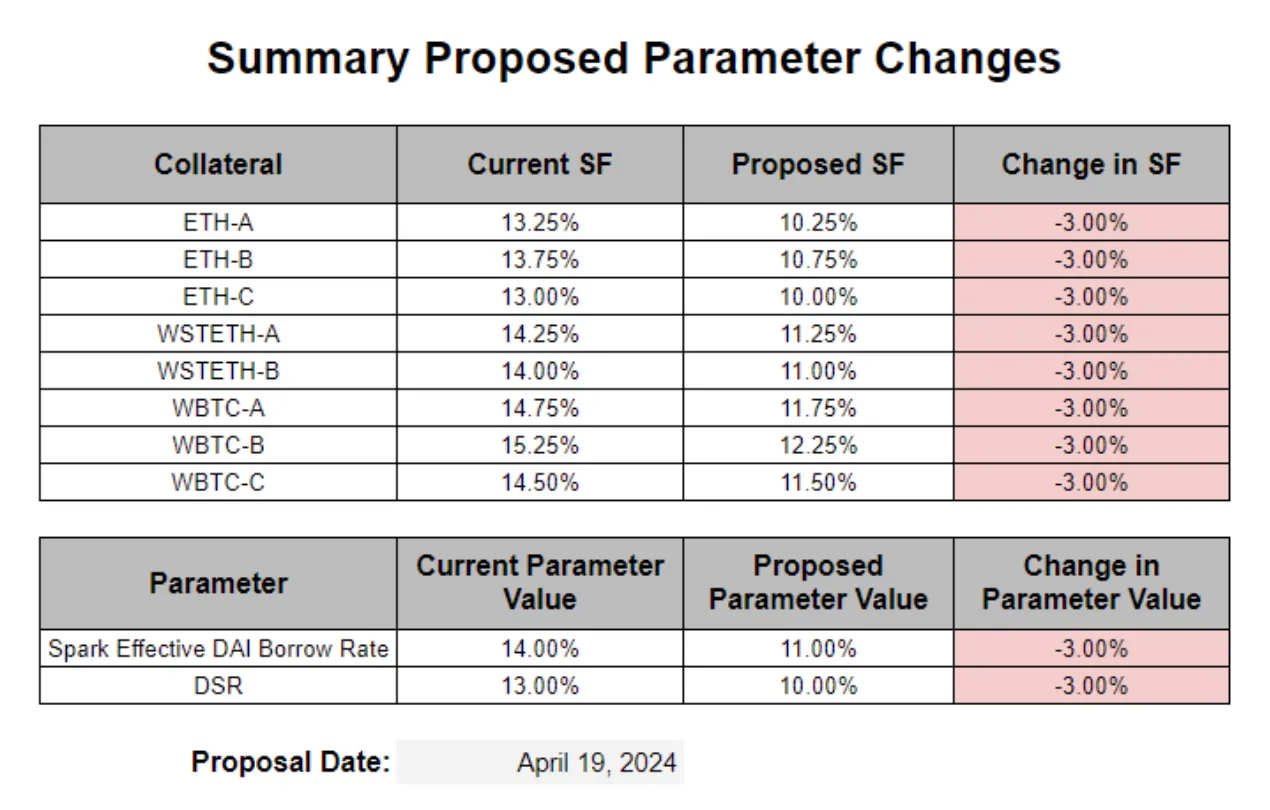

Liquity’s BOLD became the first decentralized stablecoin to earn an A- rating from Bluechip, scoring perfect 1.0 marks in Management, Decentralization, and Governance. Unlike USDC or DAI, BOLD cannot be frozen, has no admin keys, and is fully crypto-backed—highlighting the tradeoff between counterparty risk and smart-contract risk.2026-01 BA Labs recommends Maker DAO decrease rates 3%, which would drop the Dai Savings Rate to 10%2024-04

BA Labs recommends Maker DAO decrease rates 3%, which would drop the Dai Savings Rate to 10%2024-04 Ethereum's stablecoin volume has soared to a record $1.46 trillion, doubling from $650 billion earlier this year. DAI leads with $960 billion, reflecting strong demand for DeFi, but ranks behind USDT and USDC when adjusted for potential wash trading and high transfer frequency.2024-09

Ethereum's stablecoin volume has soared to a record $1.46 trillion, doubling from $650 billion earlier this year. DAI leads with $960 billion, reflecting strong demand for DeFi, but ranks behind USDT and USDC when adjusted for potential wash trading and high transfer frequency.2024-09- MakerDAO Boosts Dai's Yield to 8%, Implements VPN Restriction for Front-End Access2023-08

DAI Stablecoin Explained: Legacy MakerDAO Dollar in the Sky Protocol Era

A decentralized, overcollateralized dollar stablecoin on Ethereum, DAI was the first large‑scale proof that crypto could synthesize a “dollar” without a bank account, using smart contracts and collateral instead of cash in a custody account. Over time, DAI evolved from a purely ETH‑backed experiment into a system largely supported by a mix of crypto collateral, tokenized U.S. Treasuries, and centralized stablecoins like USDC, governed by MakerDAO and, more recently, its successor brand Sky Protocol. Today, DAI sits at the intersection of DeFi innovation and traditional finance exposure: it remains widely used as a neutral unit of account and borrowing asset, even as its own issuer has launched a successor stablecoin, USDS, and centralized exchanges migrate liquidity toward the new token. Understanding DAI therefore means understanding not only how an overcollateralized stablecoin works on Ethereum, but also how governance, collateral composition, regulation, and competition from tokens like USDC, Ethena’s USDe, and Sky’s USDS shape the future of decentralized dollars. This explainer walks through DAI’s mechanics, history, risk profile, and role in today’s multi‑trillion‑dollar stablecoin economy, with an eye to what still makes it unique—and where it may be overtaken by its own successor.

What Is DAI?

DAI is a crypto‑collateralized stablecoin, issued as an ERC‑20 token on the Ethereum blockchain, whose smart contracts aim to keep its value as close as possible to one United States dollar. Unlike fiat‑backed stablecoins such as USDC or USDT, which are issued by centralized companies holding dollars and Treasuries in bank or trust accounts, DAI is generated when users lock other crypto assets into Maker Protocol vaults, taking on overcollateralized debt that is denominated in DAI. The protocol is governed by a decentralized autonomous organization, originally MakerDAO, whose participants hold a governance token (MKR, now evolving into SKY) and vote on risk parameters, collateral types, and system upgrades. That governance structure, combined with the onchain visibility of collateral and liabilities, has long positioned DAI as one of the clearest examples of a non‑bank, market‑based stablecoin described in research by institutions like the World Economic Forum’s “Stablecoin Toolkit.”

From a user’s perspective, however, DAI behaves like most other dollar‑pegged tokens. It can be sent between Ethereum addresses in seconds, integrated into decentralized exchanges (DEXes) as a base trading pair against assets like ETH, or deposited into DeFi lending protocols as collateral or as a yield‑earning asset. Because DAI conforms to the ERC‑20 standard, it is natively interoperable across the Ethereum ecosystem and can be bridged to layer‑2 networks and sidechains, or wrapped for use on other blockchains, often forming part of multi‑chain liquidity networks that also include USDC, USDT, and now USDS. As a result, DAI functions as both a transactional currency in DeFi and a balance‑sheet asset for traders, DAOs, and treasuries that want exposure to a crypto‑native dollar without fully trusting a single centralized issuer.

At the level of design, DAI represents a specific answer to the core stablecoin design problem identified by researchers: how to maintain a stable unit of account without a central bank, using economic incentives, collateral, and governance rather than discretionary intervention. Maker’s answer has always been to combine overcollateralized debt positions, automated liquidations, and fee mechanisms with a backstop governance token (MKR, transitioning to SKY) that can be diluted to recapitalize the system in extreme stress. That framework gives DAI a different risk profile than asset‑backed stablecoins like USDC, which concentrate risk in the solvency and regulatory status of a single issuer, or algorithmic designs like the failed UST, which attempted to rely primarily on market incentives without robust collateral. In practice, DAI’s performance over several major crypto cycles has made it a benchmark for decentralized stablecoin design, even as new entrants like Liquity’s BOLD and Ethena’s USDe explore more extreme versions of crypto‑collateralization and synthetic dollar construction.

Crypto whale sues Coinbase over refusal to return stolen DAI tied to $55M phishing hack, despite exchange freezing funds and demanding court order to verify ownership

Leviathan readers click DAI stories not as passive stablecoin observers but as yield arbitrageurs and governance stakeholders — the dominant signal is 'who set this rate, why, and is it sustainable?', revealing that DAI's audience tracks it as a monetary-policy instrument rather than a simple dollar peg.↗

Historical Background: From Sai to DAI to Sky

The story of DAI begins with Maker as a smart‑contract platform on Ethereum that aimed to back and stabilize a dollar‑pegged token using collateralized debt positions. The earliest version, known as Sai or “Single‑Collateral DAI,” allowed users to lock only ETH as collateral in order to generate the stablecoin, reflecting a purist vision that Ethereum’s native asset could underwrite a decentralized dollar. This first iteration proved the concept but was constrained in scale and flexibility, since ETH’s volatility demanded high collateralization ratios and limited how much Sai could safely be minted relative to the size of the ETH market. Over time, developers and governance participants converged on a more flexible design that could accept multiple collateral types, including tokenized real‑world assets and other stablecoins.

In 2019, MakerDAO launched Multi‑Collateral DAI (MCD), which replaced Sai and became the DAI most users know today. MCD introduced the notion of Vaults—generalized smart contracts where different asset types could be deposited, each with its own risk parameters such as minimum collateralization ratio and stability fee. This upgrade allowed collateral beyond ETH, including tokenized assets and centralized stablecoins like USDC, enabling DAI supply to grow while distributing risk across multiple markets. The system’s architecture was captured in Maker’s 2020 white paper, which emphasized that every DAI in circulation is directly backed by excess collateral, with the value of that collateral exceeding the outstanding DAI debt. It also formalized the two‑token model of DAI as the stablecoin and MKR as the governance and recapitalization asset.

As DeFi expanded, DAI became one of the default “base monies” for lending protocols, DEXs, and yield strategies on Ethereum. Research on Maker observed that users generated DAI by depositing collateral into Maker Vaults and used it across the ecosystem, contributing to Maker’s total value locked (TVL) reaching billions of dollars. DAI’s growth accelerated during the “DeFi summer” boom, where traders deployed leverage by borrowing DAI against ETH or LP tokens in order to farm governance tokens across protocols. At the same time, Maker’s risk governance apparatus was stress‑tested by events like the March 2020 market crash, which revealed the challenges of liquidating collateral in highly volatile, gas‑constrained environments; these events spurred improvements in auction mechanisms and collateral management but did not fundamentally change DAI’s design.

The Endgame for Maker began to crystallize in the early 2020s, as founder Rune Christensen argued that the protocol needed to evolve toward a more modular, brandable, and politically resilient structure. On August 27, 2024, MakerDAO announced a major rebranding to Sky, reflecting a broader shift in governance and product strategy rather than a simple cosmetic rename. This change included the introduction of a new governance token, SKY, to supersede MKR over time, and the design of a new flagship stablecoin, USDS, intended to carry forward DAI’s functions with a cleaner brand and upgraded savings mechanics. As analysis of the rebranding notes, DAI became increasingly framed as a “legacy issuance” within the Sky ecosystem, continuing to exist but no longer the primary focus of growth efforts.

By 2026, the new architecture had largely taken shape. Documentation and support materials describe DAI as decentralized and collateralized by a mix of crypto and tokenized real‑world assets through Sky, while USDS is presented as Sky Protocol’s flagship dollar stablecoin and explicit successor to DAI. Eco’s infrastructure guide, for instance, summarizes that MakerDAO rebranded to Sky in late 2024, and that DAI has become roughly a multi‑billion‑dollar legacy issuance running in parallel with the newer USDS, which has grown more rapidly. Sky’s own materials emphasize that USDS is the native stablecoin of Sky Protocol, designed to hold its peg, backed onchain, and tightly integrated with a new Sky Savings Rate module that replaces the older DAI Savings Rate as the main yield product. The rebrand did not switch off DAI overnight; instead, it initiated a gradual migration, with Sky‑run converters and centralized exchange token swaps encouraging users to rotate into USDS while preserving DAI’s existing DeFi integrations.

How DAI Works Under the Hood

At the core of DAI’s design lies the Maker Protocol, a set of Ethereum smart contracts that allow anyone to generate DAI by locking approved collateral into Vaults. Technically, a Vault is a smart contract instance parameterized by collateral type: users deposit collateral tokens such as ETH, liquid staking derivatives, or tokenized Treasuries, and in return they can draw DAI up to a governance‑defined collateralization limit. The system enforces a minimum collateralization ratio, typically greater than \(100\%\), so that the value of the locked assets exceeds the value of the DAI debt, measured using onchain price oracles. For example, if a particular Vault requires a \(150\%\) collateralization ratio, a user must lock at least \(150\) units of value in collateral to borrow \(100\) DAI; if the ratio falls below the threshold due to price movements, the position becomes liquidatable. This structure makes DAI a form of overcollateralized credit money, where stability emerges from a combination of conservative leverage, automated liquidations, and governance‑set fees.

The collateralization ratio of a Vault can be described with a simple expression. If \(V_{collateral}\) denotes the market value of the collateral and \(V_{debt}\) denotes the outstanding DAI debt, then the ratio is \(CR = \frac{V_{collateral}}{V_{debt}}\). Maker governance sets a minimum allowed \(CR_{min}\) for each collateral type; whenever \(CR < CR_{min}\), liquidation mechanisms can trigger to auction the collateral. These auctions sell collateral for DAI to cancel the outstanding debt, with any surplus returned to the Vault owner and any shortfall absorbed by the system, ultimately backstopped by the potential dilution of the governance token. In this way, DAI’s solvency is continuously enforced by smart contracts that adjust individual Vault positions in response to market prices, rather than by discretionary decisions of a centralized issuer.

A second crucial component of the system is the stability fee, effectively the interest rate charged to Vault users on their outstanding DAI debt. Stability fees accrue over time and must be paid in DAI to close or reduce a Vault, functioning as a monetary policy tool analogous to an interest rate set by a central bank. When DAI trades above its one‑dollar target, governance can increase stability fees to make borrowing more expensive, incentivizing Vault users to repay DAI and thereby reducing supply; when DAI trades below a dollar, fees can be lowered to encourage additional borrowing and expansion of supply. Historically, these rates have been adjusted through onchain governance votes, reflecting Maker’s decentralized approach: MKR (and now SKY) holders propose and decide on parameter changes, acting as the system’s de facto monetary authority.

In addition to stability fees on borrowers, DAI has also used a savings rate mechanism to influence demand. The DAI Savings Rate (DSR) is an interest rate paid to DAI holders who lock their tokens into a specific smart contract module, earning yield funded from system revenues such as stability fees. Santiment’s overview notes that DSR allows DAI holders to earn an onchain interest rate by depositing DAI into these contracts, turning idle balances into income‑generating positions while steering the demand side of DAI’s market. When DSR is high, more users may choose to hold and lock DAI, tightening circulating supply and supporting the peg; when DSR is low or zero, demand can weaken, making DAI more likely to trade below one dollar without other supporting mechanisms. In the Sky era, this concept has evolved into the Sky Savings Rate (SSR) for USDS, with sUSDS as a yield‑bearing wrapper; nonetheless, the DSR remains a conceptual milestone in DAI’s monetary toolkit.

Perhaps the most important later‑stage upgrade to DAI’s peg mechanics has been the Peg Stability Module (PSM). The PSM is a special contract that allows users to swap certain fiat‑backed stablecoins, most notably USDC, into and out of DAI at a near‑fixed rate of one‑for‑one, subject to small fees. Maker’s MIP29 proposal describes the PSM as a tool to “restore the peg and utility of DAI” by enabling arbitrageurs to mint or redeem DAI directly against centralized stablecoin reserves when the market price deviates from one dollar. If DAI trades above one dollar, users can deposit USDC into the PSM to mint DAI and sell it, increasing DAI supply and pushing the price down; if DAI trades below one dollar, users can do the opposite, buying cheap DAI and redeeming it for USDC. Over time, this mechanism has led to a large portion of DAI’s effective backing being held in USDC and related real‑world asset strategies, which simultaneously strengthened the peg but introduced new dependencies on centralized issuers.

The final structural backstop in DAI’s design is the role of the governance token—originally MKR, now transitioning to SKY—in absorbing losses. Maker’s white paper explains that if collateral auctions cannot fully cover bad debt after liquidations, the system can mint and sell additional MKR to recapitalize the protocol, diluting existing holders. This mechanism is intended to align governance incentives: MKR and SKY holders have a direct financial interest in setting prudent collateral parameters and monitoring systemic risk, because reckless policies increase the probability of future dilution. At the same time, this backstop creates a complex nexus between governance, token price, and system safety, since a sharp decline in MKR or SKY value could impair the market’s ability to absorb new issuances in a crisis. In practice, DAI’s survival through multiple stress events has reinforced market perception that the combination of overcollateralization, liquidations, PSM support, and governance‑token backstop is robust, but not risk‑free.

- 01DSR yield sustainability debate↗

The top story by a factor of 3.5x was a rate-cut recommendation, and multiple follow-on headlines about 8% yields, EDSR arbitrage, and supply skyrocketing showed readers tracking whether MakerDAO's high-yield era could hold or was being gamed.

- 02Endgame rebrand and DAI phase-out↗

Multiple headlines covering Rune's endgame vision, NewStable/USDS replacement tokens, and Sky Protocol strategy signaled readers were watching whether DAI itself would survive or be superseded by its own issuer.

- 03Ethena USDe rivalry and integration risk↗

USDe overtaking DAI as third-largest stablecoin and proposals to back DAI/USDS with Ethena collateral — despite governance concerns — drew readers tracking whether MakerDAO was compromising its decentralization model for yield competitiveness.

- 04Collateral quality and peg defense↗

Stories about the $250M Coinbase emergency transfer, WBTC removal, Centrifuge pool default risk, and Aave zeroing DAI LTV showed readers monitoring the real backing behind the peg, not just the price.

- 05DAI as hack-laundering rail

Several exploit stories — the $24M stETH hack repayment in DAI, Orbit Chain losses, Lazarus Group DAI swaps — showed readers noticing DAI's recurrent role as the settlement layer of choice for stolen-fund negotiations and laundering.

- 06Regulatory threat to yield-bearing stablecoins

The GENIUS vs STABLE Act breakdown drew clicks specifically because both bills directly constrain decentralized yield-bearing stablecoins like DAI, putting MakerDAO's core business model in legislative crosshairs.

Collateral, Backing and Risk

One of the most consequential evolutions in DAI’s history has been the transformation of its collateral base. Originally, Sai and early DAI issuance were almost entirely backed by ETH, meaning that both the value and the political risk profile of the stablecoin were tied closely to Ethereum’s native asset. As Multi‑Collateral DAI expanded, Maker governance approved a growing range of collateral types, from other crypto assets to tokenized real‑world assets (RWAs) like short‑term U.S. Treasuries, as well as fiat‑backed stablecoins such as USDC. Pharos Watch’s risk profile now describes DAI as minted from “crypto and RWA vaults and supported by stablecoin PSM liquidity,” indicating that its backing combines volatile crypto collateral, centralized stablecoins, and real‑world credit exposures. Eco’s 2026 analysis similarly notes that DAI is “decentralized and collateralized by a mix of crypto and tokenized RWAs through Sky,” underscoring the hybrid nature of its contemporary backing.

The overcollateralization principle nonetheless remains central. Maker’s white paper stresses that every DAI in circulation is directly backed by excess collateral, meaning that the value of the collateral is higher than the value of the DAI debt. Collateral types are assigned minimum collateralization ratios that reflect their risk: more volatile assets like ETH require higher ratios, while assets considered safer or more liquid can be allowed lower thresholds. Pharos documents that the system uses auto‑liquidations if a Vault’s ratio falls below the minimum, selling collateral and burning DAI to restore solvency, with MKR or SKY acting as a backstop against unresolvable bad debt. In principle, this architecture ensures that DAI is always backed by more assets than liabilities, although that assurance depends on accurate price oracles, functioning liquidations, and the real‑world solvency of any offchain collateral issuers or custodians.

The introduction and growth of the Peg Stability Module significantly altered DAI’s effective risk profile. Because the PSM allows near‑par swaps between USDC and DAI, large amounts of USDC have accumulated as backing for DAI, particularly during periods when market participants arbitraged small peg deviations. Over time, Maker has deployed a substantial share of these stablecoin reserves into U.S. Treasury bill strategies via the Sky Allocator system, earning yield on the PSM‑backed USDC and similar assets. Sky’s USDS documentation describes how the protocol parks a large share of its PSM‑backed USDC into Treasuries, capturing the government bond yield and feeding it into the Sky Savings Rate. While the same allocator architecture supports both USDS and, indirectly, DAI’s backing, the result is that DAI is now heavily exposed to the credit and regulatory risks of U.S. Treasuries and USDC, in addition to traditional crypto volatility.

This CeFi‑dependent aspect is explicitly highlighted in risk analyses. Pharos classifies DAI’s backing model as “Crypto‑Collateralized” but notes that governance is “CeFi‑Dependent,” with freeze exposure inherited through upstream collateral, custody, or wrapper dependencies. In practice, this means that if a centralized issuer like Circle were forced by regulators to freeze USDC held in Maker’s PSM, or if custodians involved in RWA strategies faced legal or solvency issues, DAI could suffer sudden impairment of a significant portion of its backing. Maker’s design attempts to mitigate these risks through diversification, governance oversight, and legal structuring of RWA deals, but it cannot fully eliminate dependence on regulated institutions as long as DAI (and now USDS) earn much of their yield from Treasuries and centralized stablecoins. This stands in contrast to designs like Liquity’s LUSD or BOLD, which emphasize pure crypto collateral and the absence of freezeable assets, at the cost of higher volatility and potential liquidity constraints.

At the same time, relying on USDC and U.S. Treasuries has materially strengthened DAI’s peg stability. The WEF’s “Stablecoin Toolkit” points out that most stablecoins in practice are pegged to the U.S. dollar and backed by instruments like Treasury bills, and DAI’s shift toward RWA strategies moves it closer to that mainstream model. The PSM ensures that as long as USDC is redeemable for dollars at par, DAI remains tightly anchored through arbitrage, leading metrics providers like Pharos to rate its peg performance in the high nineties despite recording more individual depeg events than many peers. In other words, DAI has experienced frequent but typically small deviations from one dollar, which are quickly corrected by market participants using the PSM, lending markets, and onchain arbitrage. The trade‑off is that DAI’s resilience to extreme crypto market volatility has improved, while its vulnerability to offchain regulatory and custodial actions has increased.

In the Sky era, these risk trade‑offs are being re‑expressed through USDS and the Sky Savings Rate rather than through DAI’s own DSR, but the underlying collateral system is shared. USDS holders who wrap into sUSDS to earn the SSR are indirectly exposed to the same RWA and stablecoin strategies that back DAI’s PSM reserves, with Sky emphasizing that the yield comes from stability fees, USDC‑based T‑bill allocations, and curated RWA vaults operated by professional asset managers. For DAI, this means that its role is increasingly that of a legacy token sitting atop a modernized collateral stack designed primarily for USDS, with governance carefully trying to preserve DAI’s solvency and utility even as new products take center stage. Users and treasuries must therefore assess DAI’s risk not only through onchain metrics like collateralization ratios and peg deviations, but also through the evolving political and regulatory landscape governing USDC, Treasuries, and cross‑border stablecoin regulation.

Bybit to auto-swap DAI balances for USDS at 1:1, joining Binance in adopting Sky Protocol's stablecoin rebrand

Bybit will auto-swap user DAI balances to USDS at 1:1, completing its catch-up to Sky Protocol's stablecoin rebrand that Binance already processed months back. USDS is MakerDAO's successor stablecoin — same $1 peg, but holders earn Sky Token Rewards that DAI never paid. Combined DAI+USDS supply now sits at $13.4B, keeping Sky the third-largest stablecoin issuer behind Tether and Circle.

DAI in Practice: Use Cases, Liquidity and Integrations

In day‑to‑day crypto markets, DAI serves as a versatile building block across decentralized finance and centralized exchanges. On Ethereum, it is a common base asset for DEX trading pairs against ETH and other tokens, enabling users to swap into a dollar‑denominated unit of account without leaving the chain. Lending protocols such as Aave, Compound, and Maker itself accept DAI as both collateral and a borrowable asset, allowing traders to lever up long or short positions in ETH or other assets via DAI‑denominated debt. Research on Maker underscores that generating DAI by depositing collateral into Vaults is itself a form of borrowing, with loans used for everything from speculative leverage to liquidity provision in DeFi pools. As a result, DAI liquidity and borrowing rates are closely intertwined with broader Ethereum market conditions, including ETH’s price and staking yields.

Recent onchain activity provides vivid illustrations of DAI’s role as both a hedging and speculation tool. A wallet linked to Ethereum co‑founder Joseph Lubin reportedly moved over one hundred thousand ETH to defend a large DAI debt position, highlighting how major ETH holders use DAI as a structured leverage instrument rather than simply as a payments token. In another example, the Pando Rings hacker bought a large amount of ETH using around ten million DAI during a market dip, and later sold the ETH back for over ten million DAI, capturing hundreds of thousands of dollars in profit and demonstrating DAI’s utility as a neutral trading currency even in the hands of adversarial actors. Similarly, the UXLink exploiter has been observed repeatedly selling stolen ETH into DAI on DEXs like CoWSwap, taking advantage of DAI’s deep onchain liquidity to launder or reposition funds. These cases, alongside investigations linking North Korea’s Lazarus Group to hacks where stolen BTC and ETH were swapped into DAI and dispersed, reveal that DAI’s composability makes it attractive to both legitimate traders and illicit actors.

On centralized exchanges, DAI historically appeared as a secondary stablecoin behind USDT and USDC but still formed an important part of the liquidity ecosystem. Over time, major venues including Binance and Bybit listed DAI spot pairs against BTC, ETH, and other assets, as well as supporting margin and derivatives products denominated in DAI. As Sky Protocol launched USDS, these exchanges announced and executed automatic DAI‑to‑USDS migrations, converting user balances at a one‑for‑one ratio and delisting DAI trading pairs in favor of USDS pairs. Binance’s announcement explains that it completed the DAI token swap and rebranding to USDS, opened deposits and withdrawals for the new USDS tokens, and launched BTC/USDS, ETH/USDS, and USDS/USDT spot pairs, while ceasing withdrawals of old DAI tokens and offering only conversion of remaining BEP‑20 DAI. Bybit similarly pledged to auto‑convert all DAI balances to USDS at a rate of 1 DAI = 1 USDS and to delist DAI markets in favor of USDS pairs. For centralized‑exchange users, this means that DAI’s practical role is fading, replaced by USDS, even though DAI remains alive onchain.

In the broader stablecoin market, DAI is now one of many options. Data aggregated by DefiLlama shows that the total stablecoin market cap has exceeded hundreds of billions of dollars, with Tether’s USDT and Circle’s USDC dominating, and DAI occupying a much smaller share in the low single‑digit billions. At the same time, new contenders like Ethena’s USDe have rapidly climbed the rankings by offering synthetic yield backed by delta‑hedged ETH and BTC positions, while more conservative decentralized designs like Liquity’s BOLD have positioned themselves as non‑freezable, fully crypto‑backed alternatives to DAI and USDC. Against this competitive backdrop, DAI’s proposition is less about scale and more about its unique governance and collateral mix: it offers a decentralized issuance model with transparent onchain accounting, but with meaningful reliance on centralized assets like USDC and Treasuries via the PSM and RWA vaults.

Beyond trading and leverage, DAI functions as a payments and treasury asset across DAOs, web3 startups, and increasingly, non‑crypto native entities experimenting with onchain finance. Because it is not issued by a single corporate entity, some organizations perceive DAI as a more neutral settlement asset than USDC or USDT, particularly for cross‑jurisdictional arrangements where counterparties may prefer not to rely on a U.S.‑regulated issuer. DAOs have historically denominated their budgets and salaries in DAI, and multi‑sig treasuries often hold DAI as part of a diversified stablecoin portfolio that also includes USDC, USDT, and now sUSDS for yield. Eco’s analysis emphasizes that “DAI‑compatible infrastructure in 2026 has to do four things at once,” including settling DAI and USDS one‑for‑one across chains, surfacing deterministic pricing for treasury teams, and staying neutral across issuers—indicating that DAI remains an important part of multi‑stablecoin routing systems.

However, DAI’s presence on regulated platforms has also underscored the interface between decentralization and compliance. A notable example is the lawsuit against Coinbase in which a whale sought the return of approximately fifty‑five million dollars in DAI that had been frozen by the exchange after being tied to a large phishing scam. Court filings and reporting indicate that the stolen DAI was traced to Coinbase, which then froze the associated accounts, prompting a dispute over whether and under what conditions the exchange should release or return the assets. This episode demonstrates that while DAI itself does not have blacklisting capabilities at the token contract level, once it enters centralized venues like Coinbase, it becomes subject to traditional controls, including account freezes geared toward anti‑money‑laundering and fraud prevention. The fact that the asset in question was DAI rather than USDC did little to change the regulatory dynamics, reinforcing that decentralization at the protocol level does not insulate users from compliance frictions when they rely on custodial intermediaries.

On the user‑experience side, DAI’s widespread adoption has also created new security pitfalls. One striking case involved a victim who lost one hundred thousand dollars by mis‑copying an address and sending three hundred thousand DAI to a malicious account that mimicked the intended address’s starting and ending characters. This illustrates how the ease of moving DAI on Ethereum, without intermediaries or chargeback mechanisms, amplifies the consequences of small operational errors. In another incident, a temporary pricing bug on a bridge and swapping service briefly made ETH behave like a “stablecoin” against DAI, enabling a user to arbitrage an artificially fixed rate before returning the funds for a bounty—an amusing reminder that while 1 DAI is designed to equal 1 USD, it is certainly not meant to equal 1 ETH. Altogether, these stories show that DAI’s role in practice extends far beyond the abstract idea of a “decentralized dollar”: it is the grease in the gears of everything from exploit monetization and law‑enforcement tracking to yield farming and DAO payroll.

Single-collateral DAI (Sai) launched on Ethereum

Multi-Collateral DAI replaces Sai; DSR introduced

- 2022-09exploit

Profanity tool flaw compromises L2 DAI deployer addresses

DSR raised to 8%; VPN geo-block added to front-end

- 2024-02governance

MakerDAO proposes $600M DAI allocation into Ethena USDe via Morpho

Ethena USDe surpasses DAI as third-largest stablecoin at $5.8B

MakerDAO removes WBTC collateral; DSR cut to 6%

Sky Protocol launches; DAI begins migration to USDS branding

From DAI to USDS: The Sky Protocol Transition

The rebranding of MakerDAO to Sky Protocol and the introduction of USDS mark a pivotal shift in the ecosystem that created DAI. Sky is not simply a new logo; it reflects a restructuring of governance and product lines, including the rollout of a new governance token (SKY), a revamped savings mechanism (the Sky Savings Rate), and USDS as the protocol’s headline stablecoin. OAK Research’s governance investigation notes that on August 27, 2024, MakerDAO officially announced its rebranding to Sky, which set in motion the migration of roles, incentives, and branding from the legacy MakerDAO/MKR/DAI triad to the new Sky/SKY/USDS structure. In this model, DAI remains, but increasingly as an inherited liability and liquidity base whose economic future is being carefully managed but not aggressively expanded.

Sky’s own materials describe USDS as the native stablecoin of Sky Protocol, explaining how it holds its peg, what backs it onchain, and how it powers the Sky Savings Rate. Eco’s 2026 guide calls USDS “Sky Protocol’s flagship dollar stablecoin and the successor to DAI,” noting that two years after the rebrand, USDS supply had exceeded nine billion dollars, with the Sky Savings Rate printing between roughly 3.75 and 4.5 percent APY in early 2026 and sUSDS—the yield‑bearing wrapper—becoming a default treasury allocation for onchain funds seeking passive dollar yield. Holders can swap USDS one‑for‑one for legacy DAI through Sky’s official converter, and most major exchanges and DeFi protocols now treat USDS as the canonical dollar token of the Sky ecosystem. This one‑for‑one swapability and shared collateral backing mean that, economically, DAI and USDS sit on the same balance sheet, even if their branding and incentive structures differ.

Centralized exchanges have been key in operationalizing the transition. Blockeden’s coverage of the DAI‑to‑USDS migration recounts that in early April 2026, Binance and several other exchanges planned coordinated DAI delistings and auto‑conversions to USDS. Binance’s official announcement confirms that it completed the DAI token swap and rebranding to USDS, converting user balances at a ratio of 1 DAI = 1 USDS and opening new trading pairs such as BTC/USDS, ETH/USDS, and USDS/USDT. The exchange discontinued withdrawals of old DAI tokens, while allowing users to deposit remaining DAI on Binance’s internal networks and convert them to USDS through its Convert function. Bybit likewise announced support for the token swap and automatic conversion of all DAI balances to USDS at the same one‑for‑one rate, with timelines for delisting DAI spot pairs and introducing USDS‑denominated markets. For everyday traders, these moves mean that USDS has effectively replaced DAI in centralized exchange order books, even though DAI persists in DeFi.

Onchain, the transition is more nuanced. Eco’s analysis describes DAI as “a $4.6B legacy issuance running alongside the newer USDS,” emphasizing that most new “MakerDAO alternatives” or “DAI stablecoin providers” are really shopping for compatibility with the broader Sky stablecoin stack rather than with DAI specifically. Sky’s USDS yield guide explains that USDS itself does not pay yield—holding the bare token yields zero, similar to USDC—but that depositing USDS into the SSR module mints sUSDS, an ERC‑4626 vault token whose exchange rate against USDS increases over time at the SSR, currently in the low‑to‑mid single digits. The yield backing sUSDS comes from three revenue streams: stability fees on collateralized Vaults, USDC reserves earning T‑bill yield via Sky’s allocator system, and direct deployments into RWA strategies run by institutional managers. Although DAI can still access legacy DSR‑style yields in some contexts, Sky’s design clearly channels new economic benefits and governance attention toward USDS and sUSDS.

For DAI holders and integrators, this raises practical questions. One is whether to proactively convert DAI to USDS using Sky’s official converter or through exchange auto‑swaps, effectively embracing the new token as the default. Another is whether DAI’s legacy status poses any heightened risk of underinvestment in its peg and risk‑management infrastructure. So far, Sky’s governance appears intent on maintaining DAI’s stability and honoring its convertibility, as evidenced by the one‑for‑one swaps and the continued presentation of DAI as a supported asset in infrastructure guides. However, strategic discussions within Sky, including brainstorming on how to establish USDS as the primary trading pair against ETH on DEXes, suggest that liquidity, incentives, and branding will increasingly favor USDS over DAI. For integrators building new products in 2026 and beyond, the default choice is more likely to be USDS, with DAI supported for backward compatibility.

The transition also interacts with regulatory and market positioning. By concentrating user‑facing yield in sUSDS and the Sky Savings Rate, Sky may be seeking to navigate potential U.S. regulatory restrictions on interest‑bearing stablecoins, which have been a focal point in debates over legislation like the STABLE Act and the GENIUS Act. Policy discussions around whether stablecoin issuers can pay interest, what licensing they require, and how to classify decentralized issuers directly impact DAI’s legacy positioning and USDS’s future strategy. While DAI itself, as an older design, may end up shielded from some new constraints by virtue of lower growth, USDS will likely be the focus of regulatory scrutiny for the Sky ecosystem, with DAI’s existence offering a kind of escape valve for users or jurisdictions that prefer the legacy token’s legal treatment.

Governance, Transparency and Regulation

DAI’s defining feature relative to many other stablecoins is its decentralized governance model. Maker Protocol is managed by a decentralized autonomous organization, originally MakerDAO and now reorganizing under the Sky umbrella, whose governance token holders propose, debate, and vote on key system parameters. MKR (and, as migration proceeds, SKY) holders decide which collateral types to whitelist, what collateralization ratios and debt ceilings to set, how to calibrate stability fees and savings rates, and when to implement major architectural upgrades such as the PSM or the shift to multi‑chain deployments. This governance happens via onchain voting contracts, often preceded by extensive offchain discussion in forums, calls, and research papers, with successful proposals formalized as Maker Improvement Proposals (MIPs). In effect, MKR and SKY holders act as the board and monetary policy committee of a decentralized central bank for DAI and now USDS.

The transparency of DAI’s reserves and liabilities is another core selling point. Because DAI is generated through smart contracts on Ethereum, anyone can inspect the aggregate and per‑Vault collateralization in real time, track the amount of DAI outstanding, and verify liquidation events and system health dashboards. Maker’s white paper emphasizes that every DAI is directly backed by excess collateral, with the value of that collateral onchain exceeding the DAI debt, and that automated mechanisms enforce this property through liquidations and debt auctions. Pharos’s static profile for DAI records its peg mechanism as overcollateralized CDP Vaults with auto‑liquidations below minimum ratios, a Lite PSM enabling 1:1 USDC–DAI swaps, and MKR acting as a backstop that can be minted and sold to cover bad debt. The combination of onchain accounting and independent analytics providers like Pharos allows users, regulators, and researchers to treat DAI as a relatively transparent system compared with opaque centralized issuers that disclose reserves only via periodic attestations.

However, transparency does not equate to regulatory immunity. The World Economic Forum’s stablecoin analysis notes that the term “stablecoin” itself lacks a consensus legal definition, and that jurisdictions are converging on diverse frameworks that distinguish between custodial, algorithmic, and crypto‑collateralized designs. DAI fits the WEF’s working definition of a stablecoin as a publicly available, non‑central‑bank‑issued digital asset that aims to serve as a stable unit of account through economic mechanisms. Yet, because DAI’s backing now includes substantial exposure to U.S. Treasuries and USDC, it intersects with traditional regulations around investment funds, securities, and money transmission, even if the issuer is a DAO rather than a corporation. Lawmakers considering bills such as the STABLE Act and the GENIUS Act have grappled with how to treat non‑custodial, overcollateralized stablecoins and whether to impose bank‑like regulations, cap interest payments, or create bespoke categories that recognize the role of decentralized governance.

The Coinbase lawsuit over frozen DAI provides a concrete lens on this tension. In that case, the crypto whale’s DAI was allegedly stolen in a phishing attack, moved across wallets, and ultimately ended up on Coinbase, which froze the funds pending clarity on ownership and potential regulatory obligations. While DAI itself does not implement blacklist functions at the token level, Coinbase—as a regulated exchange—must follow know‑your‑customer and anti‑money‑laundering rules, including freezing or rejecting deposits believed to be proceeds of crime. The resulting lawsuit, in which the victim sought the return of the frozen DAI and contested Coinbase’s conditions, illustrates that even decentralized stablecoins become entangled in traditional legal processes once they intersect with custodial services and offchain identity. For DAI users, this means that the choice between holding DAI in self‑custody or on exchanges like Coinbase is not just a technical one but also a regulatory and legal risk decision.

Internally, Sky’s governance changes are also reshaping DAI’s regulatory posture. OAK Research’s governance investigation highlights that the rebranding to Sky came with shifts in governance structures and the introduction of new tokens, which may alter how regulators view the system’s accountability and control. A decentralized governance model that is too concentrated among a few large MKR or SKY holders might be seen as functionally equivalent to a centralized issuer, especially if those holders are identifiable entities in specific jurisdictions. Conversely, a sufficiently distributed and pseudonymous governance set presents challenges for enforcement, pushing regulators to target access points like centralized exchanges, fiat on‑ramps, and RWA custodians instead. In all cases, DAI’s future is tied not only to its onchain mechanics but also to the evolving global legal framework for stablecoins, a framework in which decentralized designs are still a relatively new and controversial category.

Liquity’s BOLD became the first decentralized stablecoin to earn an A- rating from Bluechip, scoring perfect 1.0 marks in Management, Decentralization, and Governance. Unlike USDC or DAI, BOLD cannot be frozen, has no admin keys, and is fully crypto-backed—highlighting the tradeoff between counterparty risk and smart-contract risk.

On-chain data shows BOLD's TVL has grown 18% since the rating announcement, now at $245M. However, daily minting volume remains modest at ~$2M, indicating adoption is still early-stage compared to DAI's $5B supply. The perfect decentralization score is validated by zero admin-controlled contracts, a key differentiator from USDC's blacklist risk.

MakerDAO's shift to real-world assets and Coinbase custody for backing, VPN-gated front-end access, and BA Labs' outsized rate-setting influence represent a steady drift away from trustless issuance that its own governance community has flagged repeatedly.

The addition of USDe as collateral drew immediate risk-parameter cuts from Nostra and Aave (LTV to 0%), and prior incidents with Centrifuge credit pools and WBTC removal illustrate that DAI's collateral basket has repeatedly required emergency triage.

- RegulatoryHigh

Proposed U.S. stablecoin legislation (STABLE Act) would ban yield on stablecoins outright, directly threatening the DSR — DAI's primary demand driver — and the decentralized issuance model has no obvious compliance path under either bill.

- Smart-contractMedium

The Profanity-tool compromise of the L2 DAI vanity-address deployer in 2022 exposed a systemic keygen vulnerability across multiple networks, and DAI's reliance on a complex multi-collateral vault system with numerous third-party integrations keeps attack surface broad.

- Liquidity / peg stabilityMedium

DAI has historically maintained its peg but required a $250M emergency Coinbase transfer to defend it during a collateral crunch; the USDR depeg (DAI-backed real estate stablecoin) also illustrated second-order contagion risk from tokens using DAI as reserve.

Ethena's USDe overtook DAI as the third-largest decentralized stablecoin by offering yields more than double the DSR; Sky Protocol's own pivot toward USDS signals that even MakerDAO has acknowledged DAI's declining competitive position.

Comparing DAI with Other Stablecoins and New Competitors

Within the expanding stablecoin universe, DAI occupies a middle ground between fiat‑backed and fully crypto‑collateralized designs. The World Economic Forum’s research emphasizes that most people think of stablecoins as digital assets pegged one‑to‑one to the U.S. dollar and backed by Treasury bills in a bank account, which accurately describes leading tokens like USDC and USDT. These centralized stablecoins maintain pegs by promising redeemability for dollars on demand through the issuer, relying on trust in the issuer’s solvency, reserve quality, and regulatory compliance. DAI, by contrast, maintains its peg through a combination of collateralized debt positions, liquidation mechanisms, and now stablecoin arbitrage via the PSM, without a legal promise of redemption from a single entity. In practice, the presence of USDC backing within the PSM makes DAI partly reliant on the same underlying Treasuries and bank accounts as USDC itself, but with added layers of onchain governance and overcollateralization.

Compared to purely crypto‑backed stablecoins like Liquity’s LUSD and BOLD, DAI takes a more hybrid stance. Liquity’s ecosystem, as referenced in Eco’s 2026 guide, issues LUSD and BOLD as ETH‑collateralized stablecoins with no exposure to centralized assets or RWAs, prioritizing censorship resistance and the absence of freezeable collateral. BOLD’s recent rating by independent assessors—earning high marks in management, decentralization, and governance and marketing itself as non‑freezable and fully crypto‑backed—highlights a design philosophy that deliberately avoids the CeFi dependencies that Pharos flags in DAI’s backing. The trade‑off is that such designs may face more severe peg volatility in extreme ETH drawdowns and may be less scalable due to limited safe leverage on volatile collateral. DAI, by allowing stablecoins and RWAs into its collateral set, sacrifices some censorship resistance and increases regulatory exposure in exchange for a stronger peg, higher scalability, and the ability to tap traditional fixed‑income yields.

Newer entrants like Ethena’s USDe complicate the picture further. Eco’s infrastructure analysis lists Ethena among key stablecoin issuers, describing USDe as a synthetic dollar backed by delta‑hedged ETH and other collateral, where the “peg” is maintained through derivatives positions rather than traditional collateralization alone. USDe has grown rapidly by offering attractive yields funded by basis trading and funding‑rate capture, making it a popular choice for speculative treasuries and traders seeking higher returns than typical stablecoins provide. In contrast, DAI’s yield opportunities historically came from the DAI Savings Rate and now indirectly via conversion into USDS and sUSDS, where the Sky Savings Rate tracks U.S. Treasury yields and stability fees rather than derivatives funding. This positions DAI (and USDS) as “real‑yield” products linked to credit and interest‑rate markets, whereas USDe and similar designs rely more on trading profits and may face different systemic risks.

DAI also competes in the realm of interest‑bearing stablecoins and wrappers. Sky’s USDS guide explains that USDS itself does not pay yield; instead, users deposit USDS into the SSR vault to receive sUSDS, an ERC‑4626 token whose exchange rate to USDS increases at the Sky Savings Rate, currently in the 3.75–4.5 percent APY range in early 2026. The yield flows from stability fees on USDS‑minting Vaults, PSM‑backed USDC deployed into T‑bill strategies, and curated RWA vaults managed by institutional asset managers. Historically, DAI’s DSR fulfilled a similar role, but as governance attention and revenue structures shift to USDS, DAI’s own savings opportunities may be less competitive. Meanwhile, other protocols have launched their own yield‑bearing stablecoins and vault tokens, including those that auto‑compound DeFi yields or wrap USDC into tokenized T‑bill portfolios. In this environment, DAI’s value proposition as a yield‑bearing asset is increasingly overshadowed by sUSDS and specialized yield products, while its core role as a widely accepted, overcollateralized dollar persists.

Eco’s 2026 infrastructure report synthesizes these dynamics by arguing that teams searching for “MakerDAO alternatives” or “DAI stablecoin providers” are rarely shopping for a single replacement issuer; instead, they need an issuance protocol, a routing rail, and a liquidity network. Within that framework, Sky serves as the issuance protocol for DAI and USDS, while neutral routing rails like Eco and LI.FI handle multi‑stablecoin swaps, and liquidity networks aggregate depth across DEXes and offchain venues. The report cautions against locking into a single issuer at the application layer, describing that as the failure mode which produced earlier “DAI vs USDC” debates, and instead recommends neutral orchestration layers that allow treasuries to hold whatever mix of USDC, USDT, DAI, USDS, or USDe best fits their risk and regulatory constraints. In such a multi‑issuer world, DAI’s relevance stems less from being the dominant stablecoin and more from being one component of a diversified, over‑collateralized segment of the market.

Risks, Depegs and Attack Scenarios

Despite its track record, DAI is not risk‑free, and understanding its failure modes is essential for informed use. Pharos’s risk profile points out that DAI has more recorded depeg events than many other major stablecoins, though its overall peg score still sits in the high nineties, indicating that most deviations have been small and short‑lived. These depegs can arise from several sources: sharp collateral price moves that stress liquidations, liquidity imbalances on DEXes, changes in stability fees and savings rates, or disruptions in the PSM’s ability to arbitrage between DAI and USDC. For example, if ETH were to crash rapidly and liquidations failed to keep pace due to gas congestion or oracle lags, some Vaults could become undercollateralized, potentially resulting in bad debt that must be absorbed by MKR or SKY dilution. While such events have been managed in the past, they reveal the complex interplay between onchain mechanics and broader market conditions.

The Peg Stability Module is both a stabilizer and a potential single point of failure. Because the PSM holds large balances of USDC and similar stablecoins as backing for DAI, any impairment of those assets—whether through regulatory action against the issuer, reserve losses, or technical failures—could directly weaken DAI’s solvency. Pharos warns that freeze exposure is inherited through upstream collateral, custody, or wrapper dependencies, meaning that if USDC in Maker’s PSM were frozen by its issuer, DAI would suddenly lose a key backstop for redemptions and arbitrage. In that scenario, DAI might trade at a persistent discount to one dollar, and governance would face the difficult choice of whether and how to write down the frozen collateral, recapitalize via MKR or SKY issuance, and reorient the system toward non‑freezeable assets. Such a shock would test not only DAI’s technical design but also Sky’s capacity to navigate cross‑jurisdictional legal disputes.

Governance risk is another critical dimension. Because MKR and SKY holders control parameter settings and collateral onboarding, concentrated governance power or malicious actors could push the system into dangerous territory by whitelisting low‑quality collateral, lowering collateralization ratios too aggressively, or misallocating RWA exposures. The incentive alignment mechanism—where bad debt is covered by diluting governance token holders—is meant to discourage such behavior, but it assumes rational and long‑term oriented governance participants. In reality, token price swings, activist campaigns, or regulatory pressures could distort governance decisions, and the complexity of RWA deals may make it difficult for the broader community to fully assess risks. Debates over the rebranding to Sky and the introduction of USDS illustrate that even major strategic shifts can be contentious, with trade‑offs between simplicity, decentralization, and growth.

DAI is also deeply embedded in the attack surface of the broader crypto ecosystem. As noted earlier, major hacking operations and exploitation campaigns often involve DAI as an intermediate or final asset: stolen ETH or BTC is swapped into DAI to take advantage of its liquidity and relative price stability, after which funds may be bridged to other chains or dispersed across mixers and DeFi protocols. Investigations linking Lazarus Group to a $23 million hack on a UK startup, where stolen BTC and ETH were laundered via DAI swaps and spread across wallets, underscore this pattern. Similarly, the Pando Rings hacker and UXLink exploiter have actively traded between ETH and DAI in sophisticated patterns, even capturing market dips for profit. While these uses do not reflect flaws in DAI’s own design, they highlight how its neutrality and composability can be exploited, thereby attracting regulatory and law‑enforcement scrutiny that may, indirectly, affect its reputation and usage.

Operational risks at the user level are also non‑trivial. The case of the victim who lost $100,000 due to a copy‑paste mistake when sending 300,000 DAI to a deceptive address demonstrates that the irreversible nature of Ethereum transfers magnifies human error. Similarly, temporary bugs in bridging or swapping services can create misleading price signals involving DAI, as in the brief episode where ETH was effectively priced like a stablecoin relative to DAI on a routing service before the glitch was corrected and funds were returned for a bounty. Users who borrow DAI against volatile collateral like ETH face liquidation risk if prices move sharply, as seen when large holders like Joseph Lubin move substantial amounts of ETH to shore up Vault positions and avoid forced liquidations. These patterns underscore that DAI’s safety depends not only on protocol‑level design but also on user behavior, interface quality, and ecosystem hygiene.

How to Use DAI Safely: Practical Considerations

For traders, treasuries, and individuals considering DAI, a practical risk framework can help structure usage. First, it is useful to distinguish between holding DAI as an asset, borrowing DAI against collateral, and routing DAI through centralized exchanges. In self‑custody, DAI exposes holders primarily to protocol‑level risks such as collateral volatility, PSM dependencies, and governance decisions, as well as to Ethereum’s smart‑contract and network risks. These risks can be monitored through onchain dashboards, stability metrics, and governance communications, and mitigated by diversifying across multiple stablecoins such as USDC, USDT, USDS, and possibly newer decentralized tokens like LUSD or BOLD, depending on risk appetite. Treasuries often combine DAI with sUSDS for yield and USDC for fiat on‑ramps, using orchestration layers like Eco to route between them without bespoke integrations to each protocol.

Borrowing DAI via Maker Vaults or integrated protocols adds leverage risk. Users who lock ETH or other volatile assets to mint DAI must carefully manage their collateralization ratios, taking into account potential price swings, oracle delays, and liquidation penalties. Maintaining a conservative buffer above the minimum ratio, monitoring ETH and market conditions, and understanding the liquidation process are essential, particularly during periods of high volatility. Large actors like the Lubin‑linked wallet defending a $259 million DAI debt position by moving 110,000 ETH illustrate the scale at which these dynamics can operate. For smaller users, leveraging DAI for yield farming or speculative strategies requires similar discipline, as cascading liquidations during market crashes can quickly wipe out positions that were only marginally overcollateralized.

Using DAI on centralized exchanges introduces a different set of considerations. As the Coinbase phishing‑related lawsuit shows, exchanges may freeze DAI deposits they suspect are linked to illicit activity or fraud, even though DAI itself is non‑freezeable at the contract level. Moreover, as Binance and Bybit’s token swap announcements highlight, exchanges can unilaterally decide to delist DAI pairs and convert balances to USDS, affecting users’ asset mix and trading options. For traders who wish to maintain DAI exposure specifically, this means increasingly relying on DeFi venues or specialized platforms that preserve DAI markets, while accepting that mainstream exchanges are converging on USDS and other stablecoins for liquidity and product support. Whenever DAI is held in custodial accounts, users must also consider the counterparty risk of the exchange itself, including insolvency and rehypothecation risks that go beyond DAI’s protocol design.

Security hygiene remains paramount for self‑custody and DeFi interaction. Users sending DAI should verify addresses carefully, ideally by using hardware wallets, address books, and ENS names where possible to reduce the risk of copy‑paste attacks or look‑alike addresses. Interacting with Vaults, lending protocols, or DEXs requires verifying contract addresses and frontends to avoid phishing or interface hijacking, which can trick users into approving malicious transfers of DAI and other tokens. Since DAI runs on Ethereum, general best practices—such as keeping private keys offline, using multi‑signature setups for large treasuries, and limiting approvals to trusted contracts—apply. The irreversible nature of Ethereum transactions and the composability of DAI with almost any contract mean that mistakes can propagate quickly and be difficult to unwind, as seen in several high‑profile DAI loss incidents.

Finally, users weighing whether to hold DAI or USDS should consider their goals and constraints. DAI offers a long track record and broad DeFi support, but its growth prospects and yield opportunities are increasingly overshadowed by USDS and sUSDS within the Sky ecosystem. USDS, for its part, is designed to be the primary Sky stablecoin, with better exchange support and direct access to the Sky Savings Rate via sUSDS, but it is newer and more explicitly tied to Sky’s branding and governance. Treasuries that prioritize neutrality and backward compatibility with older DeFi integrations may continue to hold DAI alongside other stablecoins, whereas those seeking yield and tight integration with Sky’s RWA strategies may favor USDS and sUSDS. In all cases, sizing positions according to explicit assessments of protocol, collateral, regulatory, and custody risk—and avoiding over‑concentration in any single design—remains the most robust approach.

Outlook

The future of DAI is inseparable from the evolution of Sky Protocol and the broader stablecoin regulatory landscape. As Sky continues to promote USDS as its flagship stablecoin, strengthen the Sky Savings Rate, and expand RWA strategies, DAI is likely to persist as a significant but gradually diminishing share of the ecosystem’s liabilities. Its onchain contracts, legacy integrations, and convertibility into USDS at one‑for‑one parity give it a long tail of relevance, particularly in DeFi protocols and treasuries that value continuity. At the same time, the center of gravity for innovation, governance, and yield within the Sky universe is clearly shifting toward USDS and sUSDS, suggesting that future research and regulation will focus more on these tokens while treating DAI as a mature, somewhat static instrument.

In the wider stablecoin market, DAI will continue to serve as a reference point for decentralized, overcollateralized design, even as competition from USDC, USDT, USDe, BOLD, and others intensifies. Debates over the GENIUS Act, the STABLE Act, and similar legislation will shape what is permissible for stablecoin issuers in terms of interest payments, backing assets, and licensing requirements, potentially favoring or disadvantaging models like DAI’s relative to fully custodial or purely crypto‑backed alternatives. As Ethereum itself positions to become a core settlement and coordination layer not only for DeFi but also for emerging “machine economy” use cases, there may be renewed demand for decentralized units of account like DAI and USDS that are native to Ethereum’s trust model.

For now, DAI remains a cornerstone of DeFi’s history and a live instrument whose behavior continues to inform how builders and regulators think about “stable” crypto dollars. Its journey from ETH‑only Sai, through multi‑collateral DAI, to legacy token within Sky’s USDS ecosystem encapsulates the trade‑offs between decentralization, scalability, regulatory exposure, and user experience that all stablecoin designs must navigate. Whether DAI ultimately fades into a purely historical artifact or maintains a durable niche alongside its successor will depend on how well Sky manages the transition, how resilient the collateral stack proves under future stress, and how the crypto industry balances its appetite for yield against its tolerance for complex, multi‑layered risk.

Latest DAI news

Crypto whale sues Coinbase over refusal to return stolen DAI tied to $55M phishing hack, despite exchange freezing funds and demanding court order to verify ownershipBybit to auto-swap DAI balances for USDS at 1:1, joining Binance in adopting Sky Protocol's stablecoin rebrandLiquity’s BOLD became the first decentralized stablecoin to earn an A- rating from Bluechip, scoring perfect 1.0 marks in Management, Decentralization, and Governance. Unlike USDC or DAI, BOLD cannot be frozen, has no admin keys, and is fully crypto-backed—highlighting the tradeoff between counterparty risk and smart-contract risk. Layerswap briefly turned ETH into a “stablecoin” thanks to a wild pricing bug that a user quickly farmed before returning funds for a 10% bounty. Glitch fixed—though the dream of 1 DAI = 1 ETH is gone again.

Layerswap briefly turned ETH into a “stablecoin” thanks to a wild pricing bug that a user quickly farmed before returning funds for a 10% bounty. Glitch fixed—though the dream of 1 DAI = 1 ETH is gone again. Ethereum Foundation launches dAI Team to make Ethereum the core settlement and coordination layer for AIs—bridging decentralized infrastructure with the machine economy to build a more open, verifiable, and censorship-resistant AI future.

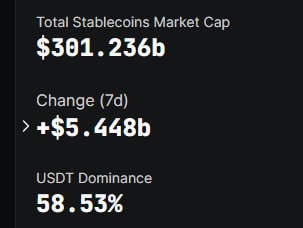

Ethereum Foundation launches dAI Team to make Ethereum the core settlement and coordination layer for AIs—bridging decentralized infrastructure with the machine economy to build a more open, verifiable, and censorship-resistant AI future. The stablecoin market cap has surged past $300B for the first time, hitting $301B on DeFiLlama data amid a crypto rebound. Tether’s USDT leads with a 58% share at $176B, followed by Circle’s USDC at $74B, Ethena’s USDe at $14.8B, and MakerDAO’s DAI at $5B.

The stablecoin market cap has surged past $300B for the first time, hitting $301B on DeFiLlama data amid a crypto rebound. Tether’s USDT leads with a 58% share at $176B, followed by Circle’s USDC at $74B, Ethena’s USDe at $14.8B, and MakerDAO’s DAI at $5B.Sources

- https://en.wikipedia.org/wiki/Dai_(cryptocurrency)

- https://makerdao.com/en/whitepaper/sai/

- https://blockeden.xyz/blog/2026/04/03/dai-usds-migration-makerdao-sky-protocol-stablecoin-rebrand/

- https://sky.money

- https://defillama.com/stablecoins

- https://announcements.bybit.com/en/article/token-swap-and-rebranding-of-dai-dai-to-usds-usds--blte886c207d75dcc94/

- https://www.binance.com/en/support/announcement/detail/3c4abe4314554c9592d9a2f433c34c8d

- https://docs.makerdao.com

- https://arxiv.org/pdf/2210.16899.pdf

- https://mips.makerdao.com/mips/details/MIP29

- https://academy.santiment.net/metrics/makerdao-dai-savings-rate/

- https://oakresearch.io/en/analyses/investigations/investigation-on-governance-maker-dao-rebranding-influence-founder

- https://x.com/arkham/status/2034883129488417047

- https://www.tradingview.com/news/cointelegraph:7a11888d9094b:0-coinbase-faces-lawsuit-over-frozen-funds-from-55m-crypto-theft/

- https://www.weforum.org/stories/2026/02/new-research-answers-fundamental-questions-about-stablecoins/

- https://makerdao.com/whitepaper/

- https://eco.com/support/en/articles/14542897-best-dai-compatible-infrastructure-2026

- https://eco.com/support/en/articles/11752998-usds-sky-protocol-2026-yield-guide

- https://www.youtube.com/watch?v=xXXJxAqMGxY

- https://pharos.watch/stablecoin/dai-makerdao/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…