In crypto, “manipulation” spans price games, protocol exploits, and AI‑driven narrative tricks that distort markets. This explainer unpacks how schemes work, why regulators care, and how traders and builders can spot and mitigate manipulation risks.

+7 sources across the wider coverage universe

Uniswap emphasizes robust technical design and product-focused approach as other crypto projects repeatedly fail, blaming users for exploits, airdrop sniping, and oracle manipulation2025-12

Uniswap emphasizes robust technical design and product-focused approach as other crypto projects repeatedly fail, blaming users for exploits, airdrop sniping, and oracle manipulation2025-12 Aiming to curtail market manipulation and misconduct, the SEC charges 9 phony market makers and crooked promoters with fraud and warns, "Crypto market investors should be mindful that the deck may be stacked against them"2024-10

Aiming to curtail market manipulation and misconduct, the SEC charges 9 phony market makers and crooked promoters with fraud and warns, "Crypto market investors should be mindful that the deck may be stacked against them"2024-10- MakerDAO community divided over high yields as Dai supply skyrockets 25%, sparking concerns over sustainability and potential manipulation2023-08

Bitget flags irregular VOXEL/USDT activity after volume soars to $12.7B, freezing accounts and planning rollbacks amid manipulation concerns.2025-04

Bitget flags irregular VOXEL/USDT activity after volume soars to $12.7B, freezing accounts and planning rollbacks amid manipulation concerns.2025-04 LegalBlock’s Dr. Rasit Tavus warns crypto market makers could face charges as some liquidity tactics blur into price manipulation amid sharp token declines.2025-04

LegalBlock’s Dr. Rasit Tavus warns crypto market makers could face charges as some liquidity tactics blur into price manipulation amid sharp token declines.2025-04- Arbitrum DeFi project Ede Finance confesses to price manipulation after alleged white hat hack.2023-05

Manipulation in Crypto: How It Works, Why It Matters, and How to Navigate It

Deliberately distorting prices, data, narratives, or emotions to gain an unfair edge is what “manipulation” means in crypto, whether it plays out on centralized exchanges, in DeFi protocols, or across social and media channels. In a market defined by volatility, thin liquidity, and pseudonymous actors, manipulation is not an edge case but a structural risk that both traders and builders must understand in detail.

Manipulation in digital asset markets blends classic securities and commodities abuses with new, protocol-level and algorithmic attack surfaces, from pump‑and‑dump schemes and wash trading to oracle exploits and AI‑driven social engineering. Regulators such as the SEC and CFTC increasingly treat many of these behaviors as forms of fraud or market manipulation, but the global, fragmented nature of crypto trading makes enforcement uneven and slow. At the same time, design choices in automated market makers, concentrated liquidity, and tokenomics can unintentionally create manipulation “traps,” where a small number of actors can move prices or drain value with modest capital. Off‑chain narratives and information flows, amplified by large language models and deepfake tools, add another layer of risk by turning tweets, fake ETF announcements, and orchestrated community campaigns into powerful levers on price and sentiment. Understanding how these different forms of manipulation interact, where the law draws lines, and what technical and behavioral defenses are emerging is now essential for anyone participating seriously in crypto markets.

The Many Faces of Manipulation in Crypto

Manipulation in financial markets predates blockchains by centuries, but crypto markets have amplified old tactics and enabled entirely new ones. In traditional securities law, “market manipulation” usually refers to conduct that creates an artificial or misleading appearance of active trading, or an artificial price for a security, often through coordinated trades, false statements, or abusive order strategies. The same basic idea applies in crypto: when a token’s price, volume, or perceived demand is driven by contrived activity rather than genuine supply and demand, the market is being manipulated. That manipulation can be overtly fraudulent, as with fabricated announcements or insider trading, or it can exploit gray zones in market structure, such as aggressive but technically “legal” high‑frequency strategies on illiquid pairs.

Regulators increasingly treat at least some crypto assets as securities or commodities and see manipulation through that lens. The SEC’s cyber and crypto assets enforcement teams explicitly target schemes involving deceptive or manipulative trading in digital asset securities, while the CFTC has brought manipulation and fraud cases in Bitcoin, Ether, and derivatives markets, often under its anti‑fraud authority in spot commodity markets. These agencies emphasize that efforts to mislead investors, distort prices, or abuse information asymmetries in crypto are not exempt from existing law simply because the underlying assets live on a blockchain. Yet enforcement resources are finite and jurisdictional reach is limited, leaving large swaths of activity in a legal gray area that sophisticated actors can exploit.

What sets crypto apart is how deeply manipulation risks are embedded in the technology stack itself. On centralized exchanges, the familiar toolkit of spoofing, layering, wash trading, and cross‑exchange arbitrage games operates in an environment of limited transparency, under‑regulated market making, and often thin liquidity, especially for new listings. On decentralized exchanges, automated market makers (AMMs) and on‑chain oracles make pricing and execution rules transparent in code, but that very transparency creates predictable patterns that arbitrageurs and attackers can exploit, including sandwich attacks, flash‑loan‑driven price manipulation, and targeted oracle distortions. Above that, governance mechanisms, cross‑chain bridges, and consensus protocols introduce higher‑layer manipulation risks, such as timestamp manipulation, collusive validator behavior, or governance “attacks” where a coordinated bloc forces through self‑serving changes.

Another important difference from traditional finance is the central role of narrative and community. Social channels and crypto media do not just report on markets; they actively shape them, especially for small‑cap tokens. A single tweet from a prominent investigator, influencer, or protocol founder can trigger panic selling or frenzied buying within minutes, as seen when on‑chain sleuths traced suspicious RAVE token flows or exposed opaque insider dealings in the LAB token that allegedly left as much as 95% of supply in the hands of insiders. In this environment, information manipulation—ranging from coordinated shilling and astroturfing to deepfake videos and fake war footage—is part of the same continuum as order‑book manipulation. Both work by exploiting information asymmetry and trust gaps in audiences that are hungry for alpha but lack reliable ground truth.

Because manipulation in crypto can occur at many layers at once, it is useful to think of it as a spectrum running from price and liquidity manipulation, through protocol and data manipulation, to narrative and emotional manipulation. At the price layer, actors may pump and dump illiquid tokens, spoof order books, or structure OTC deals that hide true float and concentration. At the protocol layer, they may manipulate AMM prices to exploit lending platforms, abuse supply caps or token minting functions, or exploit oracle design weaknesses to drain vaults. At the narrative layer, they may fabricate endorsements, amplify false rumors about ETF approvals, or deploy AI agents that build parasocial relationships with users to steer them toward dubious investments. Often, these layers reinforce one another: a fake announcement triggers a price spike, which creates on‑chain price deviations that make protocols vulnerable, which in turn produce liquidations or exploits that feed back into panic in social channels.

It is also important to distinguish between manipulation that is clearly unlawful and behavior that is morally dubious but legally ambiguous. A market maker that shorts a token it is also providing liquidity for, especially if it has superior information about upcoming unlocks or client activity, may be viewed as predatory but not necessarily illegal, as long as it is not engaging in deceptive conduct such as wash trades or spoofing. Conversely, insiders who coordinate to pump a token they control by disseminating misleading statements or by faking demand through related accounts are likely crossing lines that regulators treat as fraud or manipulation, even if the token itself has unclear legal status. In practice, crypto participants cannot rely solely on legal definitions; they must develop their own sense of manipulation risk based on market structure, incentives, and transparency.

To make these distinctions concrete, it helps to map typical manipulation patterns to the layers they affect, the tools they use, and the harms they create. The following table summarizes some of the most common categories that recur in enforcement actions, academic analyses, and on‑chain investigations.

| Layer | Typical Tactic | Mechanism | Example Pattern |

|---|---|---|---|

| Price & Liquidity | Pump‑and‑dump, wash trading, spoofing | Fake volume, spoofed orders, insider‑driven pumps | Illiquid token rallies 900% then crashes 90% in days |

| Protocol & Data | Oracle manipulation, supply‑cap exploits | Push DEX price, bypass caps, exploit TWAP lags | Flash‑loan attack drains lending protocol via oracle skew |

| Narrative & Social | Fake news, AI bots, astroturfed campaigns | Deepfakes, bot armies, fake ETF or listing claims | Compromised official account falsely announces ETF |

Each of these categories has distinct technical and legal countermeasures, but all rest on the same foundation: exploiting some combination of opacity, complexity, and human cognitive bias. That is why any robust understanding of manipulation in crypto must move beyond simple moral labels and examine the mechanics of how value and trust are actually created and destroyed in these markets.

Uniswap emphasizes robust technical design and product-focused approach as other crypto projects repeatedly fail, blaming users for exploits, airdrop sniping, and oracle manipulation

He already said what needs to be said

Readers most reliably click manipulation stories when there is a named institutional actor — a market maker, an exchange, a regulator — revealing that the real draw is accountability and power asymmetry, not the mechanics of the scheme itself.↗

How Market and Liquidity Manipulation Works

Price and liquidity manipulation remain the most visible and emotionally charged forms of abuse in crypto, largely because they are so easy to experience directly. Traders see the effects of manipulation in the form of sudden wicks, unexplained rallies, flash crashes, and order books that vanish at critical moments. Under the hood, however, many of these phenomena are variations on relatively well‑understood tactics from traditional markets—with a twist: in crypto, they often unfold on assets with minuscule free floats, highly concentrated ownership, and fragmented liquidity across multiple exchanges.

One of the canonical examples is the pump‑and‑dump scheme. In its classic form, a group acquires a stake in a thinly traded asset, hypes it aggressively with misleading or exaggerated claims, and then sells into the buying pressure it has created, leaving latecomers with steep losses. Crypto’s 24/7, global, and largely unregulated trading environment has made such schemes far easier to execute and scale. Because many new tokens launch with only a small fraction of total supply circulating, insiders can effectively dictate price by deciding how much of their own supply to release, while outsized fully diluted valuations mask how little real liquidity exists. That dynamic was on display when nearly six billion dollars of nominal market value evaporated from RAVE DAO in less than two days, even though on‑chain data suggested only a small fraction of that amount ever passed through actual liquidations. The gap between notional capitalization and realizable liquidity is fertile ground for manipulative campaigns.

Insider control of supply can supercharge these pumps. Investigators analyzing the LAB token, for example, flagged that a tiny group of insiders appeared to control as much as 95% of the supply, based on transfer patterns and the absence of non‑insider flows after the token generation event. According to on‑chain analysis, these insiders allegedly used opaque private loans and heavily discounted over‑the‑counter deals, some offering up to a 60% discount with multi‑month lockups, to concentrate tokens off‑exchange while still orchestrating a 915% rally from pre‑launch prices to a peak that attracted retail attention. When such a structure unwinds—due to investigations, sentiment shifts, or liquidity providers pulling back—the resulting crash can be just as dramatic, as seen in the subsequent double‑digit percentage drop in LAB’s price when manipulation concerns went mainstream.

Centralized exchanges add their own manipulation vectors. Spoofing and layering, where traders place large orders they never intend to execute in order to mislead others about supply and demand, remain technically feasible on many crypto venues, especially those without robust surveillance. Wash trading, in which the same entity trades with itself to simulate volume and interest, can artificially boost a token’s ranking on dashboards and exchange lists, making it appear safer or more “blue chip” than it really is. Crypto market makers, who often operate with bespoke contracts that allow them to short client tokens or receive large option packages, sometimes straddle an uneasy line between providing liquidity and exploiting asymmetric information. Reports have described situations where market makers allegedly profited from shorting the very tokens they were hired to support, contributing to price collapses while still collecting fees from issuers. Whether or not such behavior meets the legal definition of manipulation, it clearly raises conflict‑of‑interest concerns for token teams and retail traders.

Liquidity mining programs, listing campaigns, and trading festivals can also interact with manipulation in subtle ways. When exchanges or protocols incentivize high turnover in a specific asset—perhaps by offering raffle tickets or bonus rewards for hitting volume targets—they create conditions that favor high‑frequency traders and wash‑trading bots over genuine investors. Thin‑order‑book tokens subject to such campaigns can experience periods of hyperactive trading that dissolve once incentives end, leaving behind illiquidity and disoriented holders. This is not manipulation in the legal sense if disclosed properly, but it can generate price paths that resemble manipulated markets and can be exploited by sophisticated players who know when incentives will start and stop.

The fragmentation of liquidity across centralized exchanges and DeFi platforms adds yet another layer. A manipulator can, for example, build a large position on one exchange while pushing price on a less liquid venue that feeds into widely used price trackers, creating arbitrage gaps that entice other traders to move the price further in their favor. They may also coordinate between centralized exchanges and DEXs, pushing price on low‑liquidity AMM pools to influence oracles used by perps platforms, then shorting those contracts on centralized venues. Because there is no consolidated tape in crypto, and because cross‑exchange surveillance is limited, these cross‑venue feedback loops are hard for retail traders to spot.

Not all extreme price moves, of course, are manipulative. High volatility is a feature of speculative markets, and genuine shifts in information—such as major protocol updates, regulatory announcements, or macroeconomic news—can justify rapid repricing. The line between sharp but legitimate repricing and manipulative conduct often turns on intent and disclosure: are actors deliberately creating a false or misleading impression, or simply trading aggressively based on real information? That question is challenging enough in regulated equity markets; in crypto, where many key actors are anonymous or offshore, it can be almost impossible to answer in real time.

- 01market maker misconduct↗

SEC charges against fake market makers, DWF Labs allegations on Binance, and Cobie's post on opaque loan-and-option deals collectively dominated clicks because readers sense market makers hold structural pricing power with almost no public accountability.

- 02exchange intervention as manipulation↗

Bitget freezing accounts and planning rollbacks over VOXEL, and Hyperliquid force-delisting JELLY, forced readers to confront whether a centralized venue's 'protective' intervention is itself a form of manipulation against traders.

- 03DeFi oracle and price exploit vectors↗

Sturdy Finance's 1,100 ETH loss and Venus Protocol's $3.7M supply-cap risk showed readers that price manipulation is the primary attack surface against DeFi lending protocols, not a purely trading-desk phenomenon.

- 04insider token rugging

The YZY sniping video boast and Movement's market-maker agreement scandal resonated because they showed insiders openly flaunting manipulation with zero apparent fear of consequence.

- 05DAO and governance vote gaming

Sushiswap's $40M treasury vote passing amid manipulation allegations and MakerDAO's yield-driven Dai surge raised the question of whether token-weighted governance is as gameable as a spot order book.

- 06regulatory enforcement escalation↗

The SEC fraud charges, CFTC actions, and an Alabama man's prison sentence for the SEC X-account SIM swap provided the accountability narrative that manipulation coverage rarely delivers — proof that consequences occasionally land.

DeFi, Oracles, and Protocol‑Level Manipulation

Decentralized finance adds a new frontier of manipulation risk by moving market infrastructure into smart contracts. Automated market makers, lending protocols, and derivatives platforms are open, transparent, and programmable, which makes them auditable but also predictable. Attackers can study their code, simulate scenarios off‑chain, and deploy capital with surgical precision to distort prices or exploit design flaws that would be impossible—or illegal—to replicate on traditional exchanges.

Automated market makers such as Uniswap, Curve, and many forks rely on deterministic pricing functions, such as the constant‑product formula \(x \cdot y = k\), where \(x\) and \(y\) are the reserves of two tokens in a pool and \(k\) is a constant. In a simple constant‑product AMM with equal weights, the price of one token relative to the other is essentially the ratio of reserves, so a trade that significantly changes this ratio will move price accordingly. For large pools with deep liquidity, this price impact is moderate for most trade sizes; for smaller or concentrated pools, even modest trades can move prices sharply. Because anyone can trade against these pools, an attacker can deliberately push the AMM price far away from the global market price, especially if they can temporarily marshal large capital through flash loans.

This ability to distort AMM prices becomes dangerous when other protocols rely on those prices as oracles. Oracle manipulation occurs when an attacker deliberately moves the price reported by a data source used for critical protocol decisions—such as determining collateral values, liquidation thresholds, or minting rates—to trigger favorable outcomes for themselves. Many early DeFi hacks followed a pattern in which an attacker took out a flash loan, used it to push the price of a token in a thin AMM pool, and then interacted with a lending or stablecoin protocol that treated that distorted price as truth, allowing the attacker to borrow more, drain collateral, or mint under‑collateralized assets. After closing their positions and repaying the flash loan, the attacker walked away with profit, while the protocol and its users absorbed the losses.

The Venus Protocol exploit on BNB Chain illustrates how subtle design decisions can open doors to such attacks. In that incident, attackers manipulated the protocol’s supply cap mechanisms around a particular token, enabling them to borrow against an artificially inflated position and extract approximately 3.7 million dollars. Although details vary across cases, the core idea is consistent: protocol parameters such as supply caps, collateral factors, and interest rate curves can be gamed when combined with manipulable price oracles and flash‑loan‑enabled capital. Once attackers identify such a vector, they can script it into a single atomic transaction that leaves no time for human intervention.

Designers of major DEXs have tried to harden their protocols against simple oracle attacks. Uniswap v2, for instance, introduced cumulative price tracking that allows external contracts to compute time‑weighted average prices (TWAPs) by reading cumulative price values and dividing by elapsed time. Because each block adds the current end‑of‑block price to a cumulative variable, the cost of manipulating the TWAP over a meaningful period becomes the cumulative cost of pushing price in each block during that period. For large pools and longer averaging windows, this cost can exceed the profit attainable from most exploits, making manipulation economically irrational in normal conditions. However, if liquidity is shallow, averaging windows are short, or network congestion reduces arbitrage efficiency, even TWAP‑based oracles can be vulnerable, which is why many protocols now combine multiple data sources or add circuit breakers.

Impermanent loss and concentrated liquidity introduce additional manipulation dynamics for liquidity providers. Impermanent loss is the opportunity cost a liquidity provider experiences when the relative price of the two assets in a pool diverges compared to simply holding them. For a 50/50 constant‑product pool, a standard formula for impermanent loss as a function of the price ratio change \(d = \frac{p_1}{p_0}\) is \(\text{IL} = \frac{2\sqrt{d}}{1+d} - 1\). This expression shows that impermanent loss depends only on the magnitude of price change, not its direction; a double in price or a halving produces the same relative underperformance versus hodling. In traditional, “full‑range” AMMs, IL is largely a function of market volatility, but with concentrated liquidity designs like Uniswap v3, liquidity providers can choose narrow price ranges, which increases capital efficiency but also amplifies both fee income and IL.

An attacker who can temporarily push price outside of popular liquidity ranges can effectively “strand” LP capital, causing positions to go out of range and stop earning fees while traders route through the small portion of active liquidity that remains. If that active liquidity is controlled by the attacker, they can earn outsized fees or execute toxic flow against stale LPs, a pattern some analysts describe as a manipulation trap in concentrated liquidity pools. These dynamics are not necessarily illegal, since they arise from the rules of the protocol and market forces, but they illustrate how design choices can shift bargaining power toward sophisticated actors and away from passive participants. Builders and regulators must therefore consider not only explicit exploits but also structural features that enable value extraction in ways that most users do not fully understand.

Beyond prices and liquidity, protocol‑level manipulation can target consensus and time itself. Audits of CometBFT and other consensus engines have highlighted potential vulnerabilities in timestamp handling, where malicious or colluding validators could manipulate block timestamps within allowed tolerances to influence time‑dependent logic, such as interest accrual, auction durations, or TWAP windows. Such manipulation might not directly change transaction ordering, but it can subtly bias economic outcomes in favor of those who control validation. Ethereum co‑founder Vitalik Buterin has stressed that while the base blockchain may be resilient to overt 51% attacks in practice, off‑chain trust assumptions around validators, bridges, and oracles create new avenues for collusion and manipulation that cryptography alone cannot eliminate. Bridged assets, cross‑chain oracles, and optimistic rollups all depend on honest behavior from small sets of actors, which means governance and incentive design become as important to manipulation resistance as code.

Tokenomics choices around supply caps, emission schedules, burns, and buybacks also play a central role in manipulation dynamics. Projects that announce large token burns, such as Venice Token’s destruction of roughly 42.8% of its supply followed by a sharp price surge, tout scarcity as a driver of value. Yet if circulating supply remains tightly held by insiders or liquidity is thin, these events can create volatile conditions where a small amount of net buying leads to outsized price moves, attracting momentum traders who may not appreciate how little they would be able to sell if sentiment turns. Similarly, buyback programs and staking schemes can concentrate tokens in treasuries or smart contracts controlled by a few entities, raising concerns that those entities could later dump or reallocate tokens in ways that surprise the market.

The Venus Protocol exploit underscores how supply caps and collateral limits, if poorly calibrated, can be manipulated to synthesize leverage beyond what designers intended. When combined with governance mechanisms that allow token holders to adjust these parameters, there is a risk that self‑interested whales could push through changes that set the stage for future manipulation of lending and borrowing markets. Some recent cases in Vietnam and other jurisdictions, where executives associated with crypto platforms were arrested on allegations of fraud and manipulation tied to token distributions and lending schemes, show how quickly tokenomics experiments can cross into legal trouble when opacity and self‑dealing are involved.

Ethereum co-founder Vitalik Buterin warned that blockchain security only protects on-chain assets, cautioning that off-chain trust in validators exposes users to collusion and manipulation beyond cryptographic safeguards.

Isn't this the whole issue with proof of stake?

Sturdy Finance loses 1,100 ETH to oracle price manipulation exploit

CFTC brings enforcement actions targeting manipulation and fraud in crypto derivatives

DWF Labs alleged to have conducted coordinated spot manipulation on Binance

SEC X account hijacked via SIM swap; false Bitcoin ETF approval tweet spikes BTC price over $1,000

- 2025-03governance

Hyperliquid force-delists JELLY token after coordinated manipulation of HLP vault exposes systemic risk

Bitget freezes accounts and announces rollbacks after VOXEL/USDT futures volume hits $12.7B amid manipulation allegations

SEC charges 9 fake market makers and promoters with coordinated crypto fraud

Narrative, AI, and Social Manipulation

While price and protocol manipulation often hinge on technical expertise and capital, narrative manipulation thrives on attention. Crypto markets are unusually sensitive to headlines, tweets, and rumors because information asymmetry is high, regulatory guidance is opaque, and many participants trade more on sentiment than on discounted cash flows. This has made official accounts, influential personalities, and now AI‑generated content into powerful levers for moving markets, sometimes with only a few words.

The compromise of the SEC’s official X account in early 2024 illustrates how fragile market trust can be. In that incident, an unknown party gained control over the phone number associated with the @SECGov account and posted a false announcement claiming that spot Bitcoin ETFs had been approved, followed quickly by another post simply saying “$BTC.” The SEC later confirmed that these posts were unauthorized, that the account had been compromised for a brief period, and that there was no evidence of broader system intrusion. Nevertheless, the fake news triggered an immediate spike in Bitcoin’s price, as traders took the message at face value and rushed to buy in anticipation of institutional inflows, before the truth emerged and the market retraced. Subsequent criminal proceedings against an individual accused of orchestrating a SIM swap to hijack the account underscored how market‑moving even a short‑lived narrative manipulation can be when it appears to come from an official source.

Influencers, investigators, and project insiders also shape narratives in ways that can border on manipulation. Investigative threads by on‑chain sleuths like ZachXBT, alleging that insiders controlled over 90% of the circulating supply of tokens like RAVE and used that control to orchestrate pump‑and‑dump schemes, have triggered panic sell‑offs and giant percentage drawdowns in a matter of hours. While exposing hidden risks is generally in the public interest, the timing, phrasing, and amplification of such revelations can themselves become market events that sophisticated actors might trade around. Conversely, insiders boasting on social media about “sniping” their own token launches or orchestrating rugs, as seen in some recent controversies, can normalize manipulative behavior and dampen fear of repercussions, encouraging copycats.

Political and geopolitical narratives bleed into crypto manipulation as well. Statements by high‑profile figures about media manipulation in conflict zones, or platforms revising creator monetization policies to combat AI‑generated war footage and propaganda, highlight how information warfare now extends across social and economic domains. In an environment where viral videos and AI‑produced commentary about wars, elections, or sanctions can move traditional markets and cryptocurrencies simultaneously, distinguishing genuine intelligence from orchestrated narrative pushes becomes part of trading risk management.

Artificial intelligence has dramatically increased the scale and speed of narrative and social manipulation. TRM Labs and other analysts have documented how fraudsters deploy large language models, deepfake generators, and automation scripts to enhance traditional scam tactics rather than replacing them. AI can generate convincing phishing emails, impersonate support agents in chat interfaces, craft tailored investment pitches that mirror a target’s writing style, and even create video or audio deepfakes of trusted figures endorsing a token or platform. When combined with on‑chain data and open social graphs, AI systems can prioritize high‑value targets, A/B‑test messaging strategies, and coordinate thousands of fake accounts to give the appearance of organic community enthusiasm.

The emergence of AI “companions” and agents that maintain ongoing, emotionally charged conversations with users adds a subtler form of manipulation risk. These systems can influence user beliefs and behaviors over time, sometimes nudging them toward particular financial choices, products, or political views without explicit disclosure of conflicts of interest. In the context of crypto, where many users already interact with bots for trading signals, portfolio tracking, or community management, the line between helpful automation and emotionally manipulative persuasion is thin. Platforms and regulators are only beginning to grapple with questions about disclosure, consent, and the psychological impacts of such AI agents, especially on minors and vulnerable populations.

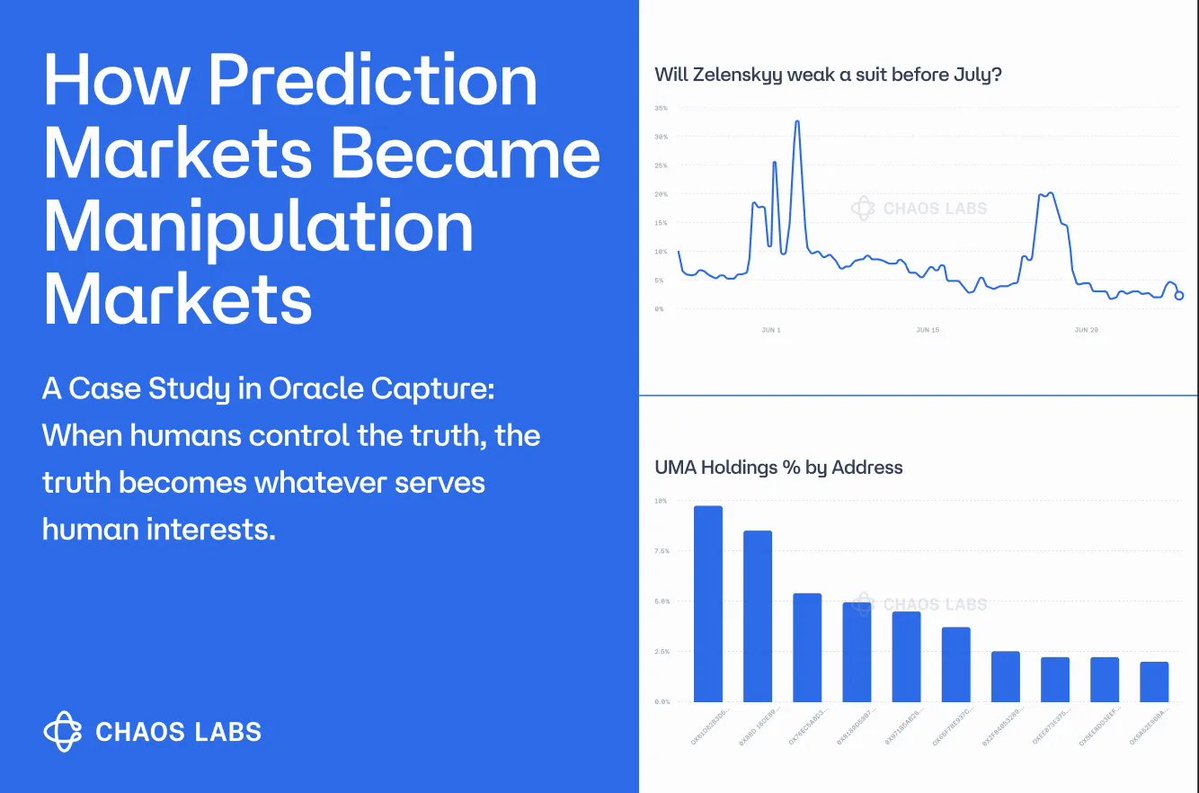

Prediction markets add another twist to narrative manipulation by directly monetizing beliefs about real‑world events. Crypto‑native prediction platforms, which allow users to stake tokens on outcomes ranging from elections to protocol upgrades, promise more accurate forecasting by aggregating dispersed information. However, they also create incentives for participants to influence the underlying events or at least the perception of those events. An individual with a large position on a prediction market about a regulatory decision, for instance, may be tempted to spread rumors or selectively leak documents to move both market odds and related token prices in their favor. As some builders have acknowledged, prediction markets can devolve into “manipulation markets” when rules for settlement are vague, oracle sources are contestable, or large players can simultaneously influence both the events and the oracles that report them.

Recent efforts by projects like GoPlus to build more transparent and rule‑driven prediction market infrastructure reflect an awareness of these dangers. By clarifying settlement rules, diversifying oracle sources, and making dispute processes more accessible, designers hope to reduce the scope for narrative manipulation to distort prediction market outcomes. Yet as long as markets trade on real‑world information, they cannot fully insulate themselves from the broader information ecosystem, including the influence of AI‑generated content, platform policies, and political actors.

Wash trading, spoofing, and coordinated pump-and-dump schemes remain endemic across crypto spot and futures markets, with the SEC identifying a systemic pattern of fake market-making used to inflate token prices before retail exit.

Price oracle manipulation is a primary DeFi attack vector — artificially inflating collateral values to drain lending pools — as demonstrated concretely by Sturdy Finance's 1,100 ETH loss.

Opaque market-maker agreements structured as token loans with call options create incentives for market makers to short the very tokens they are contracted to support, quietly draining on-chain depth.

Centralized exchanges and hybrid DeFi venues can freeze accounts, force liquidations, or delist assets unilaterally, creating a second-order manipulation surface that disadvantages ordinary traders relative to insiders.

- GovernanceMedium

Token-weighted DAO votes are vulnerable to last-minute whale accumulation and quorum gaming, enabling small coordinated groups to pass proposals controlling tens of millions in treasury funds.

SEC and CFTC enforcement against market makers, promoters, and exchange operators is accelerating, but jurisdictional gaps and the pseudonymous nature of most on-chain activity leave the majority of manipulation in a deterrence gray zone.

Regulation, Enforcement, and Platform Accountability

Legal systems traditionally address manipulation through a combination of prohibitions on deceptive conduct, requirements for fair trading, and enforcement against egregious cases. In the United States, the SEC focuses primarily on securities, while the CFTC oversees derivatives and certain spot commodity markets, including some aspects of crypto. Both agencies have expanded their cyber and crypto units in recent years, signaling that manipulative schemes in digital assets are a priority.

The SEC’s Division of Enforcement maintains a Cyber Unit, renamed and expanded to cover crypto assets and emerging technologies, that specifically targets misconduct involving digital asset securities, as well as cyber‑related threats. This includes not just classic Ponzi schemes or unregistered offerings, but also manipulative trading activity, market‑moving false statements, and undisclosed promotional campaigns involving tokens that qualify as securities. Separately, the Commission has repeatedly cited concerns about market manipulation in its decisions on Bitcoin exchange‑traded products. In its 2022 order rejecting Grayscale Investments’ bid to convert its Bitcoin trust into a spot ETF, the SEC argued that the sponsoring exchange had not demonstrated adequate surveillance‑sharing agreements or other protections to detect and deter manipulation in underlying Bitcoin markets, many of which trade on offshore platforms with limited oversight. The order emphasized that approving a spot ETF under those conditions could invite further manipulation, undermining investor protection.

The CFTC, for its part, has brought numerous cases alleging fraud and manipulation in crypto derivatives and spot markets, and reported 96 enforcement actions in fiscal year 2023 across all markets, many of which involved digital assets. It has also created a Cybersecurity and Emerging Technologies Task Force within its Division of Enforcement to address risks tied to AI, cyber intrusions, and new financial technologies, including crypto. This task force approach reflects recognition that novel forms of manipulation—such as oracle exploits, algorithmic trading abuses, or AI‑enabled social engineering—require specialized expertise and coordination with other agencies. The CFTC has also emphasized whistleblower programs and hotlines for reporting suspicious activity in commodity and derivatives markets, including those involving crypto assets.

ETF and product approval debates showcase how manipulation concerns shape regulatory decisions even when outright fraud is not alleged. The SEC has historically distinguished between Bitcoin futures ETFs, which it allowed under the premise that CME futures markets are subject to robust surveillance, and spot Bitcoin ETFs, which it resisted for years on the grounds that underlying spot markets remained vulnerable to manipulation on unregulated exchanges. Although the regulatory landscape continues to evolve, the underlying issue remains: how to ensure that the reference prices for widely distributed financial products are not easily distorted by wash trading, spoofing, or cross‑venue schemes. Even as regulators gradually acknowledge certain crypto assets as commodities rather than securities, they stress that commodities markets are not exempt from anti‑manipulation rules, and that fraud in commodity spot markets can fall under CFTC jurisdiction.

Regulators are also grappling with new frontiers of manipulation involving official communications and social media. The SEC’s own experience with the compromised @SECGov X account has forced the agency to confront how its digital presence can become a vector for market manipulation when hacked. In its public statements about the incident, the SEC acknowledged that unauthorized access to its account created confusion and raised concerns about the security of its communications channels, and committed to working with law enforcement to investigate both the intrusion and any related misconduct. Such episodes may spur stricter security requirements for official accounts, as well as clearer guidance for investors on how to verify regulatory announcements.

Enforcement against cross‑border fraud and manipulation remains challenging. Cases in jurisdictions such as Vietnam, where authorities have arrested executives linked to crypto platforms on allegations of fraud and manipulation tied to token issuance and lending schemes, underscore that local regulators may step in aggressively when retail investors suffer large losses. Yet the decentralized and global nature of crypto means that perpetrators can often operate from jurisdictions with weak enforcement or extradition mechanisms. This mismatch between the global reach of manipulative schemes and the local scope of law enforcement is one reason why industry self‑regulation and platform accountability have become central themes.

Centralized exchanges, market makers, and large protocols occupy gatekeeper roles that give them both the power and the responsibility to mitigate manipulation risks. Exchanges like Bitget, for example, are directly affected when tokens listed on their platforms are accused of insider manipulation or when price crashes trigger large liquidations and user outcry. They must balance listing demand and trading volume against reputational and regulatory risks, implementing surveillance systems to detect wash trading, spoofing, and suspicious cross‑account activity. Some market makers, responding to growing criticism, have begun to emphasize transparency in their client agreements, promising not to engage in predatory shorting of client tokens or to use confidential information for proprietary trading. However, such commitments are still far from standardized, and many issuers and traders have limited visibility into the real behavior of their liquidity providers.

DeFi protocols face analogous questions, albeit framed in code and governance. Designers must decide how conservative to be in their oracle choices, whether to integrate off‑chain data that might be manipulated by a few actors, and how to structure governance to resist capture by large token holders who might push through self‑serving parameter changes. Tooling that uses machine learning, including large language models, to detect anomalies in oracle price patterns or transaction flows is emerging as a way to automate some aspects of manipulation detection. Yet reliance on AI brings its own challenges, including the risk of false positives, adversarial adaptation by attackers, and potential over‑reliance on opaque models.

TransCrypts raises $15M Pantera Capital backed seed round to redefine digital identity verification. The funding comes amid growing global concern over AI-driven fraud and deepfake manipulation. This becomes key as individuals and enterprises seek new ways to protect sensitive personal data.

Great news. Privacy has been a major concern these days, hopefully something gets done about it

Navigating Manipulation Risks as a Participant

For traders and investors, manipulation is not an abstract legal concept but a constant background hazard. Managing that hazard requires a combination of market literacy, technical understanding, and skepticism about narratives. One of the most practical starting points is to analyze token distribution and liquidity. If on‑chain data shows that a small number of addresses control the vast majority of supply, as alleged in the LAB case where insiders were said to hold up to 95% of tokens with minimal non‑insider transfers after launch, then the token is inherently vulnerable to large, sudden price moves driven by those insiders. Similarly, if a token’s fully diluted valuation implies billions of dollars in “market cap” but only a few tens of millions of dollars in real liquidity, as RAVE DAO’s case suggested, then the nominal market value can evaporate much faster than most participants realize.

Understanding where and how a token trades is equally important. Tokens that rely heavily on thin DEX pools for price discovery, or that are listed on only a handful of lightly regulated centralized exchanges, are easier to manipulate through coordinated buy or sell campaigns. Evaluating order‑book depth, historical volatility, and the presence of credible market makers can provide clues. Reputable market makers are not a guarantee against manipulation—indeed, some have been accused of shorting client tokens or engaging in murky practices—but clear, publicly disclosed terms between issuers and liquidity providers are generally a good sign. Conversely, tokens with opaque market‑making arrangements, large “marketing wallets,” or frequent unexplained spikes in reported volume warrant extra caution.

DeFi users need to understand the specific manipulation vectors of the protocols they engage with. Providing liquidity to a concentrated range in an AMM, for instance, can be profitable when volatility is moderate and fees are high, but it also exposes LPs to the risk that price will be pushed out of range, either by natural market moves or by exploitative trading, leaving them earning no fees and facing concentrated asset exposure. Lending against volatile collateral that depends on DEX‑based oracles, especially those with short TWAP windows or single‑source price feeds, carries the risk that a flash‑loan‑enabled attack will distort prices just long enough to trigger liquidations or allow an attacker to borrow against inflated collateral. Reading protocol documentation, audits, and governance discussions—and paying attention to how protocols respond to past incidents of manipulation—is essential.

At the narrative level, cultivating healthy skepticism toward attention‑grabbing headlines and social media posts is crucial. The SEC X account hack showed how even seemingly authoritative sources can be compromised, and how quickly markets can overreact to unverified information. Traders should develop habits such as cross‑checking major announcements on multiple official channels, looking for corresponding filings or website updates, and being wary of messages that urge immediate action based on time‑sensitive claims. AI‑generated content makes it harder to rely on surface cues such as writing style or video quality to assess authenticity, so verifying sources and context becomes more important than ever.

Builders and protocol designers have their own responsibilities and tools for mitigating manipulation. On the technical side, they can adopt oracle designs that make manipulation uneconomical, such as longer TWAP windows, multi‑source aggregators, and fallback mechanisms that pause critical functions when price feeds diverge beyond reasonable thresholds. They can parameterize lending and margin systems conservatively, limiting collateral factors for illiquid or volatile tokens and setting supply caps that take into account the risk of concentrated ownership. They can also incorporate monitoring tools, including anomaly detection algorithms and LLM‑based systems that scan for suspicious transaction patterns or governance proposals, to catch early signs of manipulation.

On the governance side, protocols can reduce capture risk by avoiding overly plutocratic designs, where a few token holders can unilaterally push through changes that favor their own positions. Mechanisms such as quorum requirements, time‑locks on parameter changes, and delegated voting with transparency around delegates’ incentives can improve resilience. Vitalik Buterin’s warnings about off‑chain trust and collusion risks in oracles and bridges underscore that governance is not just about voting mechanics but also about choosing and overseeing the human or institutional actors who maintain critical infrastructure. Transparent criteria for oracle providers, bridge operators, and validators can help align incentives.

Regulators, auditors, and researchers also play key roles in navigating and reducing manipulation risks. Enforcement actions, public advisories, and litigated cases all contribute to a body of precedent that clarifies which behaviors cross legal lines and which remain in gray zones. Independent security audits and code reviews can surface manipulation vectors before they are exploited, as seen in the identification of timestamp manipulation vulnerabilities in consensus engines like CometBFT. Academic and industry research on AMM design, MEV mitigation, and oracle robustness provides theoretical and empirical foundations for more resilient protocols. At the same time, collaborations between forensic analysts, compliance firms, and law enforcement, often augmented by AI‑driven blockchain analytics, are improving the detection of coordinated manipulation campaigns and the tracing of illicit gains.

Ultimately, navigating manipulation in crypto is less about finding definitive safe harbors and more about understanding the contours of risk. Markets where information is abundant, incentives are aligned, and infrastructure is robust will always be harder to manipulate than those characterized by opacity, concentration, and complexity. For traders, builders, and regulators alike, the task is to push crypto markets toward the former and away from the latter, recognizing that technological innovation will continue to open new battlefields in the struggle over fair and efficient price discovery.

Outlook

Manipulation is not a temporary aberration in crypto markets; it is a structural byproduct of open, permissionless systems interacting with human incentives, regulatory gaps, and rapidly advancing technologies. As DeFi matures, oracles harden, and more liquidity concentrates in blue‑chip assets and well‑governed protocols, some of the most egregious manipulation tactics may become less profitable or more easily detected. At the same time, however, AI‑assisted social engineering, cross‑chain exploits, and sophisticated market‑making strategies will likely create new forms of abuse that blur the lines between legitimate trading and manipulation.

Regulatory responses are likely to remain uneven and reactive, with high‑profile enforcement actions in clear cases of fraud or insider manipulation, and cautious, sometimes contradictory guidance in gray areas such as ETF approvals and commodity classifications. Over time, jurisdictions that combine clear rules with pragmatic oversight may attract more compliant capital and infrastructure, while those that swing between laxity and crackdowns could see manipulative actors migrate there. Industry‑driven standards around market‑making, token distribution, and oracle design, if widely adopted and enforced by market discipline, could reduce some manipulation risks without stifling innovation.

For participants, the core challenge will be to internalize manipulation risk as a normal part of crypto exposure, much like smart contract risk or regulatory risk. That means pricing it into decisions about which tokens to hold, which platforms to use, and how much leverage to take. It also means demanding more transparency from exchanges, issuers, and protocols, and rewarding those that design with manipulation resistance in mind. In the long run, markets that can credibly claim to be less manipulable—through a combination of robust technical design, effective oversight, and resilient information ecosystems—are likely to attract deeper, more durable liquidity. Until then, understanding how manipulation works, and recognizing its telltale patterns across price, protocol, and narrative layers, remains one of the most valuable skills in crypto.

Latest Manipulation news

Uniswap emphasizes robust technical design and product-focused approach as other crypto projects repeatedly fail, blaming users for exploits, airdrop sniping, and oracle manipulationEthereum co-founder Vitalik Buterin warned that blockchain security only protects on-chain assets, cautioning that off-chain trust in validators exposes users to collusion and manipulation beyond cryptographic safeguards.TransCrypts raises $15M Pantera Capital backed seed round to redefine digital identity verification. The funding comes amid growing global concern over AI-driven fraud and deepfake manipulation. This becomes key as individuals and enterprises seek new ways to protect sensitive personal data. Beanie, VC with Gm Capital, laments the sad state of crypto & shares IG video someone "part of insider team" posted boasting about sniping and rugging $YZY token. "There’s literally no fear of repercussions anymore."

Beanie, VC with Gm Capital, laments the sad state of crypto & shares IG video someone "part of insider team" posted boasting about sniping and rugging $YZY token. "There’s literally no fear of repercussions anymore." Cobie's latest X-post highlights opaque market-maker deals fueling crypto collapses—calls grow for transparency and standardized terms to protect token buyers and issuers from hidden risks.

Cobie's latest X-post highlights opaque market-maker deals fueling crypto collapses—calls grow for transparency and standardized terms to protect token buyers and issuers from hidden risks. Omer Goldberg, founder of Chaos Labs, on how prediction markets became manipulation markets

Omer Goldberg, founder of Chaos Labs, on how prediction markets became manipulation marketsSources

- https://econone.com/resources/blogs/cryptocurrency-market-manipulation/

- https://en.wikipedia.org/wiki/Pump_and_dump

- https://www.sec.gov/about/divisions-offices/division-enforcement/cyber-crypto-assets-emerging-technology

- https://www.bitget.com/news/detail/12560605414809

- https://www.bis.org/publ/qtrpdf/r_qt2112v.htm

- https://speedrunethereum.com/guides/impermanent-loss-math-explained

- https://arxiv.org/html/2502.06348v2

- https://www.cftc.gov/PressRoom/PressReleases/8822-23

- https://www.trmlabs.com/resources/blog/how-ai-is-changing-the-scale-and-speed-of-crypto-fraud

- https://www.chainalysis.com/blog/crypto-prediction-markets/

- https://www.tradingview.com/news/newsbtc:43fe3da3d094b:0-rave-token-crashes-95-as-manipulation-allegations-trigger-panic/

- https://www.ccn.com/analysis/crypto/venice-token-vvv-price-outlook-ai-token-burn/

- https://www.kelleydrye.com/viewpoints/client-advisories/with-regulation-in-flux-the-sec-disapproves-proposed-grayscale-investments-spot-bitcoin-etf

- https://www.cftc.gov/PressRoom/PressReleases/8736-23

- https://thedefiant.io/news/hacks/venus-protocol-3-7m-supply-cap-exploit-6072ly

- https://www.sec.gov/secgov-x-account

- https://developers.uniswap.org/docs/protocols/v2/concepts/oracles

- https://www.bitget.com/news/detail/12560605031671

- https://www.dlnews.com/articles/markets/market-makers-short-tokens-but-one-firm-wants-transparency/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…