Deep dive explainer on OpenSea’s evolution from NFT marketplace to multi‑chain crypto hub, covering OS2, fees, creator royalties, SEA token plans, perps via Hyperliquid, competition with Blur, and key risks and outlook.

+6 sources across the wider coverage universe

OpenSea says it’s evolving beyond NFTs into a broader crypto ownership platform, betting on onchain assets and verifiable digital property across Web32026-05

OpenSea says it’s evolving beyond NFTs into a broader crypto ownership platform, betting on onchain assets and verifiable digital property across Web32026-05 OpenSea delays $SEA token launch indefinitely just two weeks before planned March 30 event, offers fee refunds for seasons 3-6 participants2026-03

OpenSea delays $SEA token launch indefinitely just two weeks before planned March 30 event, offers fee refunds for seasons 3-6 participants2026-03 OpenSea product marketing lead teases perps on NFT marketplace with Hyperliquid support2026-06

OpenSea product marketing lead teases perps on NFT marketplace with Hyperliquid support2026-06 FIFA transitions to Polygon blockchain, unveils NFTs for World Cup final tickets. "For the first drop, 100 digital collectibles will be made available ... and will feature the rarest collectibles that offer the chance to secure 2026 FIFA World Cup final tickets," the statement said. "A total of 900 other digital collectibles will be issued on the Polygon network and made available on the OpenSea platform."2023-12

FIFA transitions to Polygon blockchain, unveils NFTs for World Cup final tickets. "For the first drop, 100 digital collectibles will be made available ... and will feature the rarest collectibles that offer the chance to secure 2026 FIFA World Cup final tickets," the statement said. "A total of 900 other digital collectibles will be issued on the Polygon network and made available on the OpenSea platform."2023-12- OpenSea advises users to rotate API keys following third-party security breach2023-09

- Former OpenSea Head of Product Nathaniel Chastain sentenced to 3 months home arrest, 200 community service hours and reliquishing the 16 ETH earned front running2023-08

OpenSea: From NFT Marketplace To Multi‑Chain Crypto Trading Hub

The largest NFT trading platform by historical volume, OpenSea is a multi‑chain marketplace that lets users buy, sell and create non‑fungible tokens while also swapping fungible crypto tokens through integrated liquidity providers. As it evolves beyond collectibles into broader crypto markets, the platform sits at the center of Web3’s experiment with verifiable digital ownership, creator monetization, and onchain financial products ranging from token swaps to planned perpetual futures. This explainer traces how OpenSea works, how its OS2 upgrade and delayed SEA token fit into the wider crypto landscape, and what risks and opportunities that creates for traders, creators and investors.

Origins, Founders, and the Rise of NFT Marketplaces

OpenSea emerged in 2017 as one of the first dedicated marketplaces for non‑fungible tokens, building on the early wave of Ethereum‑based digital collectibles such as CryptoKitties. The company was founded by Devin Finzer and Alex Atallah, software entrepreneurs who saw NFTs as a new primitive for digital property and not merely a niche for speculative JPEGs. Initially headquartered in New York before later moving its headquarters to Miami, OpenSea set out to be a neutral marketplace protocol layered on top of public blockchains rather than a custodial platform holding user assets itself. That design choice reflected a core Web3 ethos: users connect their own wallets, sign transactions, and retain control of their keys, while the marketplace provides discovery, order‑matching and user experience.

The broader NFT boom of 2020–2021 turned OpenSea from a niche startup into one of crypto’s best‑known consumer brands. High‑profile drops in art, music, gaming and profile‑picture (PFP) collections drew mainstream attention, and OpenSea became the default venue where new collections launched and secondary trading concentrated. At the peak of the mania, blue‑chip NFT collections saw daily volumes measured in tens or hundreds of millions of dollars, and OpenSea’s fee revenue helped propel it to “unicorn” status with valuations in the billions of dollars. This period also entrenched a perception of OpenSea as synonymous with NFTs, even though the underlying technology was more general: a marketplace for any tokenized asset that could be represented onchain.

As competition grew, particularly from Polygon‑based and alternative‑chain marketplaces, OpenSea began supporting multiple blockchains beyond Ethereum mainnet. In July 2021, it added Polygon with gas‑free trading for buyers, allowing users to trade NFTs without paying Ethereum’s often‑volatile transaction fees. This move foreshadowed the multi‑chain direction that would later be formalized with OS2, where OpenSea presents itself as an aggregator of onchain markets across dozens of networks rather than a single‑chain venue. It also signaled a willingness to abstract away blockchain complexity so that mainstream users could access digital collectibles without worrying about gas optimization or bridging.

From the outset, OpenSea’s core economic model was straightforward: charge a take‑rate on successful trades while enabling creators to set optional or enforced royalties on secondary sales. Unlike centralized exchanges, OpenSea did not custody user funds; instead, it integrated with Web3 wallets such as MetaMask, Ledger and others, using smart contracts to manage listings and transfers. This architecture helped the platform sidestep some regulatory obligations associated with custodial intermediaries, but it also meant that users bore most of the responsibility for key management, transaction security and understanding the risks of interacting with smart contracts. Over time, this tension between usability, decentralization and regulation has shaped many of OpenSea’s product decisions.

The rise of NFTs also brought scrutiny. Questions emerged about wash trading, insider trading, and the speculative nature of many collections, culminating in legal cases such as that of former OpenSea executive Nathaniel Chastain, whose NFT “insider trading” conviction was later overturned on appeal over issues with jury instructions. The case spotlighted how thin the line can be between traditional securities‑style insider trading and information asymmetries in token markets, even when the underlying assets are collectibles rather than regulated financial instruments. That controversy, and others around stolen NFTs and fake collections, pushed OpenSea to strengthen compliance, moderation, and security tooling even as it tried to preserve the openness of NFT minting.

By the mid‑2020s, with NFT trading volumes cycling through boom and bust phases, OpenSea’s leadership began talking less about NFTs in isolation and more about “the tokenization of everything.” In Finzer’s public comments and interviews, he framed onchain ownership as a general‑purpose technology for representing culture, identity, finance and physical assets, and not merely a speculative trading game. That narrative shift underpins the OS2 overhaul and the planned SEA token: OpenSea is repositioning itself as a general crypto ownership and trading hub, of which NFT collectibles are only “chapter one.”

OpenSea says it’s evolving beyond NFTs into a broader crypto ownership platform, betting on onchain assets and verifiable digital property across Web3

26 chains, perps, token swaps, Apple Pay-style onboarding, and an MCP/API for agent trades puts OpenSea closer to Phantom + Rabby + Coinbase Wallet territory than Blur territory. The weak spot is DeFi: without lending, LP positions, restaking receipts, or vault exposure, “own everything onchain” still stops at spot inventory and collectibles. SEA only works if that unified portfolio starts producing sticky routing/marketplace fees; another points-to-token cycle gets farmed and forgotten.

Readers click OpenSea stories not for NFT market mechanics but for institutional failure: they want the insider caught, the executive named, the token delayed again, and the valuation gutted — OpenSea functions as the NFT cycle's accountability ledger.↗

NFTs and Onchain Ownership Basics

To understand OpenSea’s evolution, it is useful to clarify what NFTs are and how they differ from fungible tokens. A non‑fungible token is a unique digital asset recorded on a blockchain, typically following standards such as ERC‑721 or ERC‑1155 on Ethereum and compatible networks. Unlike fungible tokens such as ETH or USDC, where each unit is interchangeable, NFTs are designed to represent distinct items: a specific artwork, an in‑game item, a music track license, or a membership credential. The token acts as a pointer to metadata and often to off‑chain media, combined with an immutable ownership record that anyone can verify onchain.

Fungible tokens, by contrast, behave more like traditional currencies or shares. Each unit of a fungible token is identical to any other, and they are used to represent money, governance rights, or claims on protocol revenue in decentralized finance (DeFi). When OpenSea speaks of “tokens” alongside NFTs in OS2, it is mainly referring to these fungible ERC‑20‑style assets that can be swapped via decentralized exchanges. Both NFTs and fungible tokens rely on blockchain mainnets such as Ethereum, Polygon or newer chains like Berachain and Soneium to settle transactions and secure state. A mainnet, in this context, is the production network of a blockchain where real economic value is transferred, as opposed to testnets used for development.

The distinction between NFTs and fungible tokens is central to OpenSea’s value proposition because it has historically specialized in the former while now aggregating the latter. NFT markets are typically thinner, with unique items, less standardized pricing and more emphasis on cultural value than on yield. Fungible token markets, as seen on centralized exchanges and DeFi platforms, tend to be deeper, faster and more arbitrage‑driven, with established pricing on major pairs. By integrating fungible token swaps through third‑party liquidity aggregators, OS2 blurs this boundary, letting a user move from buying a PFP to swapping into governance tokens or stablecoins within the same interface.

The concept of “ownership” in NFTs also differs from the ownership of underlying intellectual property. Buying an NFT on OpenSea does not usually give the buyer copyright in the artwork; rather, it conveys a provably scarce digital token that may carry usage rights defined by license terms. This nuance is critical in legal debates and in how creators structure drops, whether for 10,000‑piece PFP collections or 1‑of‑1 fine art. OpenSea’s role is to display metadata, enforce or respect creator‑defined rules where technically possible, and provide transaction rails; it is not the arbiter of underlying legal rights, which remain governed by off‑chain law.

As NFTs spread beyond art into gaming, ticketing and real‑world assets, OpenSea found itself at the crossroads of different communities and use cases. Gaming projects launching new mainnets or sidechains often list their in‑game skins and characters on OpenSea to reach a broader audience, while artists and entertainment brands use the platform for limited‑edition digital releases. High‑profile examples, such as projects spearheaded by well‑known creatives like animation director Ralph Sosa or gaming ecosystems whose NFTs can be used both in‑game and on secondary markets, highlight how OpenSea functions as an attention gateway where cultural and financial value intersect. This dual nature makes the platform both a market and a media layer, which in turn shapes the rest of its product roadmap.

How OpenSea Works: Wallets, NFTs, and Token Swaps

At a mechanical level, OpenSea is a non‑custodial web application that orchestrates interactions between user wallets and smart contracts deployed on various blockchains. To use the marketplace, a user connects a compatible wallet, such as MetaMask, Rainbow, Phantom or a hardware wallet, and authorizes the OpenSea interface to read public addresses and request transaction signatures. OpenSea does not take custody of the private keys that control those wallets; instead, it builds transaction payloads that users approve or reject using their own keys, with final settlement occurring on the relevant blockchain. This architecture means funds and NFTs remain in user‑controlled addresses until a smart contract call transfers them to a buyer or seller according to the trade’s terms.

NFT trading on OpenSea revolves around listings, offers, and auctions. Sellers can list an NFT at a fixed price or create time‑bounded auctions, while buyers can place offers either on specific items or on entire collections at a floor price. The platform indexes these orders, surfaces them through search and discovery algorithms, and matches buyers and sellers when transaction conditions are met. Under the hood, most newer listings use OpenSea’s Seaport protocol, an open‑source smart contract system that supports complex order types, including trades involving multiple items or partial fills. By making Seaport permissionless and without a privileged “owner” address, OpenSea has tried to position the protocol as shared infrastructure rather than a proprietary lock‑in.

OS2 extends this familiar NFT trading workflow by adding fungible token swaps through integrated liquidity aggregators. Instead of building its own automated market maker (AMM), OpenSea connects to third‑party aggregators that route orders across major decentralized exchanges and AMMs to source best prices. This means that when a user initiates a token swap from OS2’s interface, the underlying trade may be executed on Uniswap, SushiSwap or other DEXs, with OpenSea acting as a unified front‑end and analytics layer. OS2 initially charges 0% fee on swaps at the marketplace level, although third‑party liquidity providers may charge their own protocol fees and standard network gas still applies. At times, the platform has explicitly used temporary 0% swap fees as a promotional tool to increase OS2 adoption, especially around key reward or token announcements.

One of OS2’s hallmark features is cross‑chain purchasing. Historically, users would have to bridge assets between chains or hold native tokens on each network to participate in NFT drops and token markets across ecosystems like Ethereum, Polygon, Arbitrum or newer chains. OS2 aims to abstract this away by allowing users to pay with a single asset, such as ETH on one chain, while the platform and its partners handle the necessary swaps, bridges and settlements behind the scenes. For example, a user with ETH on Ethereum mainnet can buy an NFT minted on a supported alternative chain, with the system automatically performing the cross‑chain operations needed to complete the purchase. This design tries to make multi‑chain markets feel more like a unified “onchain internet” rather than a fragmented set of separate silos.

The OS2 interface is also built to function as a data and analytics console for NFT and token markets. It offers improved search, filtering and trait‑based discovery so that users can find specific NFT attributes or explore trending collections more efficiently. Color‑coded rarity indicators, real‑time floor price updates and in‑depth statistics on volume, holders and listing behavior are built into collection pages, reducing the need for third‑party analytics dashboards. For fungible tokens, OS2 surfaces price charts, liquidity metrics and trade history, helping users understand slippage, volatility and potential counterparty risks before executing swaps. This increasing emphasis on analytics reflects a shift toward more active traders and investors rather than purely casual collectors.

Crucially, OS2 aggregates marketplace listings beyond OpenSea’s own order flow. The platform ingests and displays orders from competing NFT marketplaces where possible, allowing users to see and in some cases execute the best available prices without leaving the OS2 interface. This aggregation approach is similar to how some DeFi front‑ends aggregate DEX liquidity, and it positions OpenSea less as a single standalone market and more as a generalized discovery and routing layer for onchain assets. For users, this means that “shopping around” across marketplaces is gradually replaced by a unified browsing experience, even as liquidity remains fragmented at the contract level.

The wallet experience is another pillar of how OpenSea works, and one area where it has made strategic acquisitions. In 2025, OpenSea acquired Rally, a company behind a mobile‑first Web3 wallet and user‑friendly crypto app, and brought its co‑founders into leadership roles including chief technology officer. The goal is to integrate Rally’s wallet technology and mobile design philosophy into OpenSea’s products, reducing friction in onboarding and making it easier for non‑crypto‑native users to move from discovering a collection on social media to owning it in a self‑custodial wallet. Combined with OS2’s wallet sidebar and real‑time notifications, this reflects a broader trend: major crypto applications are morphing into multi‑purpose “super apps” where wallets, marketplaces and social features converge.

OpenSea delays $SEA token launch indefinitely just two weeks before planned March 30 event, offers fee refunds for seasons 3-6 participants

What went wrong. Indefinitely shouldn't be in the conversation

- 01Insider misconduct and named executives↗

Two separate named-executive scandals — Chastain's front-running conviction and Pawlak's alleged pump-and-dump pseudonym — pulled readers who wanted real accountability attached to real people.

- 02$SEA token saga and repeated delays↗

The cycle of announcement, valuation leak, confirmed Q1 2026 launch, and then indefinite delay generated repeated click waves as each reversal reset reader expectations.

- 03Platform security breaches and phishing

A third-party API key breach and parallel phishing campaigns against developers signaled that OpenSea's security posture was a live liability for its user base.

- 04Market decline and executive exodus↗

Layoffs cutting 50% of staff, a 76% Tiger Global valuation cut, three C-suite departures in three months, and an acquisition hint composed a coherent story of platform collapse readers tracked serially.

- 05OS2 evolution and royalty policy reversal↗

OpenSea's pivot to an XP-gated OS2 beta, community backlash forcing a points system revamp, and the removal of royalty enforcement showed readers a company iterating under competitive pressure from Blur.

- 06NFT brand partnerships and institutional adoption↗

FIFA's Polygon-based World Cup ticket NFTs distributed via OpenSea signaled that despite platform struggles, OpenSea remained the default venue for high-profile institutional NFT drops.

Fees, Creator Earnings, and the Seaport Protocol

Any marketplace is defined not just by what can be traded, but also by how fees and incentives are structured. OpenSea’s fee model has evolved, but at the OS2 stage it typically charges a 1% fee on NFT sales, included in the price displayed to buyers. For primary drops minted through OpenSea Studio, the platform can charge a 10% fee on the mint, reflecting the additional infrastructure and distribution support involved in launching a new collection. Token swaps via integrated DEX aggregators carry a 0% fee from OpenSea itself, although external liquidity providers may charge their own fees and the user always pays blockchain gas to validators. These platform fees are in addition to any creator earnings set at the collection level.

Gas fees are separate from OpenSea’s business model and are paid to blockchain validators for processing transactions on the underlying network, such as Ethereum or Polygon. When users list NFTs, accept offers, or transfer items between wallets, they sign transactions that incur gas costs commensurate with network congestion and contract complexity. OpenSea does not control, receive, or directly influence these gas fees, although it can optimize smart contract design to reduce unnecessary gas consumption. For some chains and phases of its product, OpenSea has used gasless listing strategies or meta‑transactions, but in general users should expect that any onchain action carries a cost independent of the marketplace’s own fee schedule.

Creator royalties, rebranded on OpenSea as “creator earnings,” have been one of the most contentious issues in NFT markets. Originally, many NFT platforms allowed creators to specify a royalty percentage on secondary sales, often in the 5–10% range, which the marketplace then enforced at the UI and smart contract level. Over time, as competition intensified, some marketplaces began making royalties optional or allowing sellers to toggle them off in order to attract traders who preferred lower total fees. OpenSea’s current framework distinguishes between optional creator earnings and enforceable earnings at the smart contract level.

On OpenSea, collection owners can set a preferred creator earnings percentage, along with the payout address, via OpenSea Studio’s Creator Earnings tab. For standard ERC‑721 and ERC‑1155 contracts, these earnings are optional: sellers can choose whether to honor them when creating listings or accepting offers, and the platform presents a toggle in the UI. If the underlying NFT smart contract is compatible with ERC‑721C or ERC‑1155C—a standard that encodes enforceable onchain creator earnings—the collection owner can go a step further and “enforce” earnings through OpenSea. When enforced, the earnings toggle is locked in the “on” position and cannot be disabled by sellers on OpenSea or on other marketplaces that support the same enforcement standard.

There are important caveats to this enforcement model. Only collections deployed or upgraded after certain dates, and using compatible contract architectures, can enable enforcement; older collections or non‑upgradable contracts must rely on optional earnings. Moreover, enforcing creator earnings via ERC‑721C and ERC‑1155C typically restricts trading to OpenSea and other marketplaces that integrate Limit Break’s payment processor, such as Magic Eden, narrowing where those NFTs can be sold. For creators and communities, this trade‑off is non‑trivial: enforceable royalties can secure revenue streams and align incentives, but they may also reduce liquidity by locking out marketplaces that do not support or honor the enforcement standard.

Underpinning much of OpenSea’s trading logic is the Seaport protocol, introduced as an open‑source marketplace protocol for safely and efficiently buying and selling NFTs. Seaport’s core smart contract is intentionally decentralized, with no contract owner or upgradeability hooks that would give OpenSea privileged power over it. This means that, in principle, any other marketplace or application can build on Seaport, and the protocol cannot be unilaterally altered to change fee structures or introduce backdoors. By making Seaport permissionless, OpenSea has tried to position itself both as a steward of shared infrastructure and as one of many potential front‑ends, even as it remains by far the largest Seaport integrator.

Seaport supports advanced order types that go beyond simple “buyer pays X, seller receives Y” trades. It allows for multi‑asset bundles, where one order can specify a combination of NFTs and fungible tokens on each side, as well as partial fills where a large order can be gradually executed by multiple counterparties. These features open the door to more complex market structures, such as NFT index baskets or structured trades involving both tokens and collectibles. For OS2, Seaport serves as the foundation for future features that blur the line between collectibles and DeFi, particularly as the platform moves toward integrating perpetual futures and other derivatives through external providers.

From a revenue perspective, OpenSea remains one of the higher‑earning protocols in DeFi and NFT infrastructure, with annualized fees measured in the tens of millions of dollars according to analytics sites that track onchain fee flows. However, net revenue after incentives, buybacks and rewards is smaller, especially as the platform dedicates portions of its fee stream to user rewards, prize vaults, and future SEA token‑related programs. This shift toward sharing fee revenue with the community mirrors trends across crypto, where protocols use tokens and onchain incentives to bootstrap liquidity and user loyalty, particularly when facing competitors that already have aggressive token reward schemes.

OS2, XP, and the SEA Token: Incentives and Governance

The OS2 platform is not merely a user interface overhaul; it also introduces a new incentive architecture centered on experience points (XP), seasonal “Voyages,” and a planned native token, SEA. When OS2 was launched in private beta, OpenSea granted priority access to holders of Gemesis NFTs—a collection tied to its earlier acquisition of the Gem NFT aggregator—which was determined by taking a snapshot of nearly fifty thousand wallets. From the outset, OS2 users could earn XP by performing onchain activities such as listing NFTs, placing collection offers, swapping tokens, and even providing feedback via official channels. XP updates dynamically and is displayed in the interface, turning everyday marketplace actions into a gamified progression system.

Over time, OpenSea layered structured missions called Voyages on top of the base XP accrual. Voyages incentivize users to explore new features, chains, and collections, with tasks that range from minting on newly supported networks to sharing galleries or participating in specific campaigns. Completing Voyages and maintaining activity levels allows users to upgrade “Treasure Chests,” tiered reward containers that were initially designed to determine a share of future SEA token distributions. During the final pre‑token generation event (TGE) reward phases, users could level up chests from lower tiers to higher ones by trading more, completing missions, and claiming surprise shipments, with higher‑tier chests expected to yield larger allocations.

The SEA token, as announced by the OpenSea Foundation, is envisioned as a governance and utility token intended to reward loyal users and support the underlying Seaport protocol. Early public statements and documentation outlined a tokenomics design where 50% of the total supply would be allocated to the community, including historical users, XP earners, and other stakeholders, while the remaining portion would go to other categories such as the foundation, contributors and investors. In parallel, OpenSea indicated that 50% of platform revenue at launch would be committed to SEA buybacks, creating a direct link between protocol usage and token demand. Holders would be able to stake SEA behind their preferred tokens and NFT collections, aligning themselves with specific communities and potentially influencing rewards distribution.

Utility‑wise, SEA has been described as providing governance rights over protocol parameters, including fee structures and potentially certain aspects of the Seaport roadmap. OpenSea has also hinted that holding SEA could unlock trading discounts, enhanced features on OS2, or privileged access to campaigns and drops, echoing how exchange tokens like BNB or OKB function on centralized platforms. Importantly, the SEA distribution is designed to avoid a private sale; instead, tokens are to be airdropped based on XP, treasure chest tiers and historical usage, with U.S. residents explicitly included in eligibility in contrast to many DeFi airdrops that excluded them because of regulatory concerns. This open, usage‑based distribution model is partly a response to OpenSea’s loss of market share to Blur, whose token incentives aggressively rewarded high‑volume traders and liquidity providers.

The roadmap for SEA has, however, been repeatedly revised in response to market conditions and community feedback. Initial expectations coalesced around a TGE in late 2025, with snapshots of XP and chest levels planned for early October and token distribution to follow in Q4. Later, OpenSea’s leadership publicly targeted Q1 2026 for the token’s debut, with the CEO highlighting that the platform was already seeing billions in monthly trading volume, much of it from token trading rather than pure NFTs, which would underpin SEA’s economic base. Throughout these phases, OpenSea ramped up reward programs and introduced a “prize vault” funded by a share of platform fees, seeded with assets like OP and ARB tokens, which would be distributed alongside SEA.

Community sentiment toward OS2’s points and rewards programs has been mixed. On one hand, active users appreciate transparent, on‑platform accounting of XP and chest levels, and the prospect of meaningful retroactive rewards for years of activity. On the other hand, some traders have criticized shifting rules, perceived under‑rewarding of volume, or retroactive changes to how different actions count toward XP. Periodic adjustments to the XP formula and the balance between genuine usage and farmed activity have sparked debates reminiscent of those around other points‑based systems in DeFi, where protocols struggle to deter sybil attacks while still rewarding organic behavior. OpenSea has responded at times by revising its OS2 rewards design, promising to focus SEA distribution on users who contribute long‑term value rather than short‑term wash trading.

A pivotal turning point came when OpenSea announced that the SEA TGE, originally scheduled around March 30, 2026, would be delayed due to “challenging” market conditions, with no new date provided. The OpenSea Foundation communicated that it would wait for more favorable conditions before launching the token, effectively postponing the culmination of XP, chest, and prize vault programs that users had been engaging with for months or years. As part of the same announcement, OpenSea declared that the current Treasure rewards wave would be the last, and that users from specific seasons could claim refunds for platform fees paid during those periods, but only if they forfeited accumulated Treasure. To soften the blow and encourage OS2 adoption, the platform also set token‑swap trading fees to 0% for a limited period beginning March 31.

This indefinite delay has significant implications. For one, it underscores how tightly token launches are now linked to market cycles; even large, well‑funded platforms hesitate to introduce new governance tokens during periods of low liquidity or regulatory uncertainty. It also raises questions about the durability of points‑based incentive schemes: users who optimized their activity for SEA eligibility must now reassess the opportunity cost of that behavior versus trading on other platforms. At the same time, by not launching SEA into a weak market, OpenSea may be trying to avoid replicating the pattern of over‑distributed tokens that rapidly lose value and fail to sustain aligned governance. For now, SEA remains an announced but unlaunched token, and OS2’s XP system functions more as a reputational and internal‑reward metric than as a clear claim on immediate token allocations.

OpenSea product marketing lead teases perps on NFT marketplace with Hyperliquid support

Zack Brenner asked who wanted early access to perps on OpenSea, then replied “yes” when asked if the feature would be powered by Hyperliquid. This is still a tease, not a formal launch announcement, but it signals OpenSea is pushing further beyond NFTs into crypto trading infrastructure. CoinGecko’s latest marketplace ranking has OpenSea third by monthly NFT volume with 19.9% share, so the interesting part is less NFT dominance and more distribution meeting Hyperliquid rails.

Nathaniel Chastain front-runs OpenSea homepage NFT listings

Chastain convicted of wire fraud and money laundering

Chastain sentenced to 3 months home arrest, forfeits 16 ETH

OpenSea lays off 50% of workforce, CEO announces OS2 plan

OpenSea removes mandatory royalty enforcement, switches to voluntary creator fees

SEC issues Wells Notice to OpenSea over NFT securities classification

OS2 private beta launches with XP system and Gemesis NFT holder priority access

OpenSea confirms $SEA token for Q1 2026 with 50% community supply and revenue buyback

Competition, Market Cycles, and OpenSea’s Position in Crypto

OpenSea does not operate in a vacuum; its strategy and product choices are best understood in relation to competing marketplaces and shifting NFT market cycles. The most prominent rival in the Ethereum NFT ecosystem has been Blur, a marketplace and aggregator that aggressively targeted professional traders with low fees, fast execution, and a token‑incentive program that rewarded high‑volume activity and liquidity provision. According to contemporary analyses and commentary, OpenSea’s loss of market share to Blur’s token‑driven model was a key factor in its decision to introduce XP, prize vaults and the SEA token as mechanisms to realign user incentives and share more value with the community. In effect, OpenSea transitioned from a purely fee‑based business to a hybrid model where a significant share of fees is recycled back to users through rewards and future token buybacks.

Beyond Blur, marketplaces like Magic Eden, originally focused on Solana, have expanded cross‑chain and now compete with OpenSea in areas such as enforceable creator royalties and curated drops. Magic Eden’s integration of Limit Break’s payment processor, which supports ERC‑721C and ERC‑1155C royalty enforcement, positions it as an important counterpart in the debate over how to sustain creator earnings in a race‑to‑zero‑fee environment. Meanwhile, older platforms and niche marketplaces serve specific ecosystems, such as gaming‑centric chains or art‑focused platforms that differentiate through curation rather than liquidity. In this landscape, OpenSea’s OS2 pivot to aggregate NFTs and tokens across roughly twenty‑plus blockchains aims to differentiate on breadth and convenience: it wants to be the place where users go first, even if liquidity is technically fragmented under the hood.

The competitive dynamics can be illustrated with a simplified comparison of key marketplaces.

| Marketplace | Primary Focus | Native Token | Incentive Model | Notable Features |

|---|---|---|---|---|

| OpenSea | NFTs plus fungible token swaps (OS2) | SEA (planned) | XP, prize vaults, future buybacks, airdrops | Multi‑chain, Seaport, creator earnings options |

| Blur | High‑frequency NFT trading, aggregation | BLUR | Points and token rewards for volume/liquidity | Pro‑trader UI, deep integration with aggregators |

| Magic Eden | NFTs, especially gaming and PFPs | None (core) | Campaign‑based rewards, partner incentives | Early Solana focus, royalty enforcement options |

OpenSea’s strengths lie in brand recognition, early‑mover network effects, and an increasingly sophisticated technical stack, including Seaport and OS2’s cross‑chain and analytics capabilities. Its challenges include retaining high‑volume traders who may be more motivated by immediate token incentives elsewhere, and convincing creators that its evolving royalty and rewards systems will reliably support their long‑term revenue models. Periods of lower NFT volumes have also tested the resilience of its business model; nevertheless, the platform has consistently ranked among the higher fee‑generating protocols tracked by DeFi analytics, suggesting a durable user base even in down markets.

Market cycles add another layer of complexity. During bull runs, NFT trading volumes and floor prices can surge across major collections, leading to spikes in OpenSea’s activity and revenue. In bear phases, volumes compress, speculative interest wanes, and many collections see illiquidity or dramatic price declines, which erode fee income and can push platforms into more aggressive churn‑reduction strategies. Recent data points to a rebound in NFT trading volumes after prior downturns, driven by top collections and renewed activity on platforms like OpenSea, Blur and Magic Eden, illustrating how sentiment and liquidity can rotate back into NFTs when broader crypto markets recover. For OpenSea, this cyclicality reinforces the value of expanding into fungible token markets and derivatives, which tend to have more continuous demand.

Competition is no longer limited to NFT marketplaces. New consumer‑facing crypto applications, such as streaming‑adjacent trading platforms and meme‑coin launchpads, compete for the same user attention and transaction volume that OpenSea targets. Projects like Pump.fun that combine live streaming, social features and token launches, or AI‑driven information‑finance platforms that reward content engagement with tokens like KAITO, are reframing what a “crypto app” can be. In that context, OpenSea’s strategy to become a one‑stop “home” for onchain culture, art, tokens and eventually derivatives is as much about defending screen time and mindshare as it is about capturing trading fees.

Another dimension of competition is regulatory positioning and user trust. As centralized exchanges face tightening regulations around custody, leverage and token listings, non‑custodial marketplaces like OpenSea may benefit from users who prefer retaining control over their assets. However, as OpenSea steps into areas such as perpetual futures trading through partners, it may attract a different class of regulatory scrutiny similar to that facing derivatives platforms. At the same time, controversies such as insider‑trading allegations, security incidents around malicious collections, and debates over stolen NFTs have highlighted that even non‑custodial platforms must invest heavily in compliance, risk management and user education to maintain trust.

Beyond NFTs: Perpetual Futures, Mobile, and the “Everything” Platform Vision

OpenSea’s move into perpetual futures trading marks one of its most ambitious steps beyond the conventional NFT marketplace model. The company has confirmed plans to integrate perpetual futures via Hyperliquid, a high‑performance decentralized exchange built on its own Layer‑1 blockchain, inviting users to sign up for early access through social media. Perpetual futures, or “perps,” are derivative contracts that allow traders to speculate on the price of an underlying asset without an expiration date, using a funding rate mechanism to keep the contract price anchored to spot markets. Unlike spot trading of NFTs or tokens, perps typically involve leverage, margin requirements, and more complex risk profiles, bringing OpenSea closer to the feature set of centralized and decentralized exchanges that cater to advanced traders.

The integration with Hyperliquid is significant for several reasons. First, it signals that OpenSea is not building a derivatives engine from scratch but rather plugging into existing infrastructure that already processes billions in daily trading volume. This approach allows the marketplace to focus on front‑end experience, onboarding and cross‑asset integration while outsourcing core matching‑engine and risk management logic to a specialized protocol. Second, by giving OS2 users the ability to trade perps alongside spot NFTs and tokens, OpenSea effectively turns its interface into a multi‑product trading terminal, where collectors might hedge exposure to certain tokens or speculate on market moves without leaving the platform. Third, the move underscores OpenSea’s belief that the future of onchain markets will involve a continuum from collectibles to purely financial instruments, all accessible through unified user experiences.

The details of OpenSea’s perpetual futures offering are still emerging. Key questions include which assets will be covered—major cryptocurrencies, NFT floor‑price indexes, or perhaps tokens tied to flagship collections—and how leverage limits and margin requirements will be set. Geographic availability is another open issue, as derivatives are subject to stricter regulatory regimes in many jurisdictions, and platforms often geofence certain countries from accessing leveraged products. Regardless of specifics, the decision to enter perps aligns with OpenSea’s stated goal of evolving into a broader crypto ownership platform where users can manage portfolios across spot and derivatives markets without having to grant custody of their assets to centralized exchanges.

Mobile and wallet strategies are the other pillars supporting this “everything” platform vision. As noted earlier, the acquisition of Rally brought in a mobile‑first wallet and a team experienced in building socially‑oriented web3 products. OpenSea has since been testing mobile trading experiences, including closed‑alpha features that allow token trading from smartphones, complementing existing NFT browsing apps. This mobile emphasis recognizes that mainstream users increasingly expect to manage digital assets from phones, and that future growth will depend on lowering onboarding friction, abstracting seed phrases where safe, and integrating social discovery with trading and ownership.

OpenSea’s rhetoric around “tokenization of everything” encapsulates a broader rebrand from an NFT marketplace to a comprehensive onchain asset platform. In interviews, Finzer and other leaders have described NFTs as “chapter one,” with subsequent chapters encompassing fungible tokens, physical‑digital hybrids, and other forms of verifiable property documented on blockchains. OS2’ support for new chains such as Flow, ApeChain, Berachain and Soneium, with more chains slated for integration, is a concrete manifestation of this vision, positioning OpenSea as an aggregator across gaming‑centric, DeFi‑heavy and experimental networks alike. Initiatives like establishing an NFT reserve with a million‑dollar pledge to digital art, and sweeping tokens and NFTs into a prize vault funded by platform fees, further highlight its desire to straddle both cultural patronage and financialized incentives.

The planned SEA token sits at the intersection of these initiatives. By tying token economics to platform revenue, staking and governance, OpenSea aims to create a unifying incentive layer that can span NFTs, fungible tokens, perps and whatever else the platform integrates in the future. If implemented effectively, SEA could allow users to express preferences over fee allocation, listing rules, or even which chains and products to prioritize, making OpenSea more of a community‑steered protocol than a conventional startup. At the same time, any such token must navigate securities‑law considerations, avoid being construed as a pure profit‑sharing instrument, and remain robust across market cycles—challenges that arguably contributed to the decision to delay its launch until conditions improve.

Taken together, these moves suggest that OpenSea is positioning itself as a central node in the emerging onchain economy—one that aspires to bundle NFTs, tokens, perps, wallets, analytics, rewards and governance into a single coherent product experience. Whether users, regulators and competitors accept that bundling will determine how far this “everything” platform vision can go.

The SEC issued a Wells Notice threatening legal action over NFTs listed on OpenSea, treating them as unregistered securities — a precedent-setting threat to the entire NFT marketplace model.

OpenSea lost NFT market share dominance to Blur's pro-trader model, and its OS2 platform centralizes access controls via a 49,785-wallet Gemesis snapshot, creating privileged tiers.

Thirdweb disclosed a critical vulnerability targeting NFT collections using OpenSea's Seaport-adjacent contracts, requiring coordinated emergency patching across multiple collections.

Tiger Global marked down OpenSea's valuation by 76% from its $13.3B peak, and trading volume concentration in competitors like Blur reduced OpenSea's fee revenue base substantially.

The $SEA token was delayed indefinitely two weeks before its scheduled March 30 launch, with fee refunds offered to seasons 3–6 participants, undermining trust in the tokenomics roadmap.

Three executives including former COO Shiva Rajaraman departed within three months, and insider misconduct by the former Head of Product created reputational and legal liability that required federal prosecution.

Risks, Critiques, and What Users Should Watch

Despite its prominence, OpenSea carries the same underlying risks as other non‑custodial crypto platforms, along with some that are specific to NFT markets. On the technical side, users are exposed to smart contract risks in Seaport and other contracts used for listings, offers and token swaps; while Seaport is open‑source and designed without upgradeable backdoors, any sufficiently complex contract system may harbor undiscovered bugs or vulnerabilities. Integrations with third‑party liquidity aggregators and protocols like Hyperliquid add additional attack surfaces, as failures or exploits in those systems can indirectly affect OpenSea users executing trades through its interface. Because users maintain custody in their own wallets, they must also guard against phishing, malicious approvals and compromised devices, which remain among the leading causes of loss in DeFi and NFT ecosystems.

Market‑structure risks are equally important. NFTs are notoriously illiquid and susceptible to sharp price swings, especially in thinly traded collections where a few large holders dominate supply. Floor prices can collapse rapidly when sentiment turns, and wash trading can distort volume metrics, making it difficult for casual users to assess genuine demand. While OpenSea has implemented measures to detect and label suspicious trading behavior, it cannot fully eliminate the possibility that certain collections’ volumes and prices are inflated by non‑economic trades. Fungible token swaps through OS2 may be more liquid but still carry slippage, impermanent loss (when using LP tokens elsewhere), and exposure to volatile assets with little intrinsic value beyond speculative narratives.

Regulatory and legal risks are in flux. NFTs historically occupied a grey area relative to securities law, with many regulators focusing first on fungible token offerings and centralized exchanges. However, enforcement actions and court cases increasingly reference NFTs, as seen in the prosecution and subsequent overturning on appeal of the former OpenSea executive’s insider‑trading conviction, which hinged on whether information about featured collections constituted property and whether NFT trading fell under certain fraud statutes. As OpenSea expands into perps and token markets, it may encounter stricter regulatory regimes that govern derivatives, leverage and cross‑border solicitation, particularly in the United States, the European Union and other major jurisdictions. Users should be alert to evolving terms of service, region‑specific restrictions and the possibility that some features may be geofenced or modified in response to legal developments.

The SEA token adds another layer of uncertainty. While usage‑based airdrops and community allocations are popular in crypto, they often attract speculative users who game points systems or farm activity without contributing long‑term value. OpenSea’s XP and Treasure programs already faced scrutiny over whether they favored high‑volume traders or those with sophisticated farming strategies, and the indefinite delay of the SEA TGE has sparked frustration among users who optimized for rewards that may not materialize on the original timeline. Moreover, the promise that 50% of platform revenue at launch would fund SEA buybacks raises expectations that could prove difficult to sustain in the face of volatile fee income and changing regulatory views on buyback‑like mechanisms for tokens.

There are also critiques around centralization and gatekeeping. Even though Seaport is decentralized as a protocol, OpenSea’s web interface, discovery algorithms and policy decisions effectively determine which collections get surfaced, which are verified, and how issues such as stolen assets are handled. Decisions to de‑list certain collections, honor takedown requests, or enforce specific creator earnings structures can shape market outcomes, sometimes in ways that feel opaque to users and creators. As OpenSea evolves into a more multi‑product platform, these governance questions will become more acute, making transparent and credible community input mechanisms increasingly important, whether or not SEA eventually becomes the formal governance vehicle.

Finally, users should be attentive to how OpenSea balances user experience with the ethos of self‑custody and permissionlessness. Features that abstract away complexity, such as cross‑chain purchasing or simplified mobile flows, can improve accessibility but may also obscure what is happening under the hood in terms of bridges, contract approvals and counterparty risk. For sophisticated traders, this abstraction might be a welcome convenience; for newcomers, it can make it harder to build a mental model of their risk exposure. The challenge for OpenSea—and for any platform operating at this intersection of culture and finance—is to design interfaces that are both intuitive and honest about the irreducible risks of onchain markets.

Outlook

OpenSea stands at a pivotal juncture in its evolution from a pioneering NFT marketplace to a comprehensive onchain asset platform. The OS2 rebuild, with its integration of fungible token swaps, cross‑chain purchasing, enhanced analytics and gamified XP system, has already transformed the user experience into something closer to a multi‑asset trading terminal than a simple collectibles storefront. Plans to add perpetual futures via Hyperliquid and to eventually launch the SEA token further underscore a strategic ambition to sit at the center of Web3 markets, where NFTs, tokens and derivatives coexist under one cohesive interface. At the same time, delays to the SEA TGE and adjustments to rewards programs show that OpenSea is willing to course‑correct when market conditions or community feedback warrant it, even at the cost of short‑term user frustration.

For creators, OpenSea will likely remain a crucial distribution and monetization channel, especially as enforceable creator earnings standards like ERC‑721C mature and as marketplaces coordinate around royalty enforcement. The platform’s investment in initiatives such as an NFT reserve and prize vaults, and its ongoing role in high‑profile drops across art, entertainment and gaming, signal that culture remains central to its identity even as it leans into more financialized products. How effectively it can align creator revenue models with trader incentives—especially in a world of optional royalties and intense competition from token‑rich rivals—will be a key determinant of its long‑term cultural relevance.

For traders and investors, OpenSea’s trajectory offers both opportunities and risks. OS2’s multi‑chain, multi‑asset aggregation could make it a powerful hub for onchain portfolio management, particularly if SEA eventually delivers meaningful governance rights, fee discounts and staking‑based alignment with favored collections and tokens. However, the expansion into perps, the complexity of cross‑chain abstractions, and the evolving regulatory environment mean that risk‑management and due diligence will remain essential. Users should monitor how OpenSea handles jurisdictional restrictions, disclosures around leverage and derivatives, and the interplay between its non‑custodial architecture and any potential compliance obligations.

Looking ahead, OpenSea’s biggest challenge may be navigating the tension between being an open protocol steward and a consumer‑facing brand in increasingly politicized and regulated crypto markets. As competitors experiment with new models that blend social media, streaming, AI‑driven curation and tokenized rewards, OpenSea will need to continually iterate on its product, incentives and governance to maintain relevance and user loyalty. Whether SEA eventually launches into a more favorable market or is re‑scoped entirely, the deeper trend is clear: marketplaces like OpenSea are no longer just venues for buying and selling JPEGs; they are becoming operating systems for digital ownership, where culture, capital and code converge in real time on blockchain mainnets across the world.

Latest OpenSea news

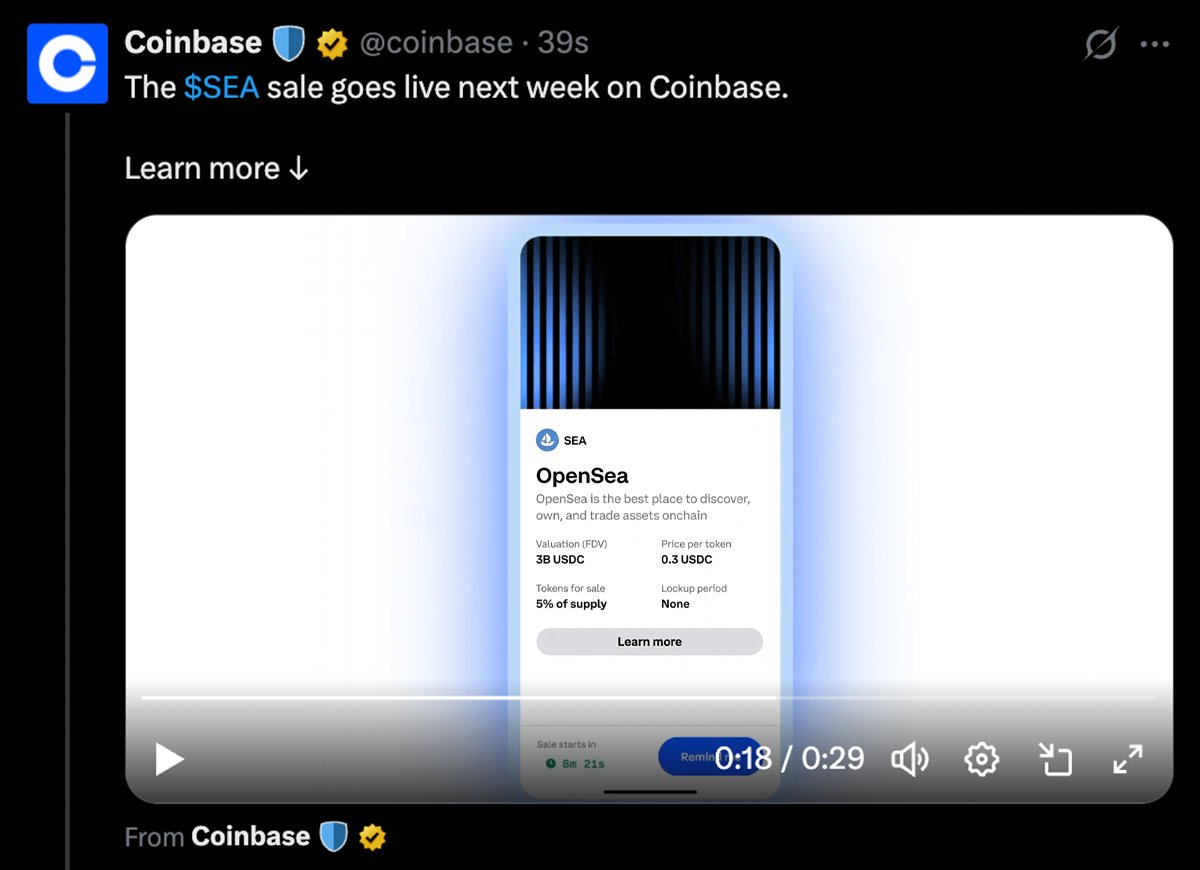

OpenSea says it’s evolving beyond NFTs into a broader crypto ownership platform, betting on onchain assets and verifiable digital property across Web3OpenSea delays $SEA token launch indefinitely just two weeks before planned March 30 event, offers fee refunds for seasons 3-6 participantsOpenSea product marketing lead teases perps on NFT marketplace with Hyperliquid support Coinbase briefly posted — then deleted — a notice about an OpenSea SEA token sale valuing the project at $3.8B with 5% of supply priced at 0.3 USDC, according to doomerfied, though neither company has commented and SEA is still slated for a Q1 2026 launch with half the supply going to the community.

Coinbase briefly posted — then deleted — a notice about an OpenSea SEA token sale valuing the project at $3.8B with 5% of supply priced at 0.3 USDC, according to doomerfied, though neither company has commented and SEA is still slated for a Q1 2026 launch with half the supply going to the community. OpenSea confirms its SEA token will launch in Q1 2026, with 50% of supply for users and a buyback plan using half of its revenue. Trading volume tops $2.6B this month.

OpenSea confirms its SEA token will launch in Q1 2026, with 50% of supply for users and a buyback plan using half of its revenue. Trading volume tops $2.6B this month. OpenSea unveils first NFT reserve by pledging $1 million to digital art, teases SEA token update. As part of the SEA token launch, OpenSea will “start sweeping millions in tokens and NFTs into a massive prize vault” using 50% of all platform fees beginning Sept. 15.

OpenSea unveils first NFT reserve by pledging $1 million to digital art, teases SEA token update. As part of the SEA token launch, OpenSea will “start sweeping millions in tokens and NFTs into a massive prize vault” using 50% of all platform fees beginning Sept. 15.Sources

- https://opensea.io

- https://en.wikipedia.org/wiki/OpenSea

- https://defillama.com/protocol/opensea

- https://support.opensea.io/en/articles/8867026-how-do-i-set-creator-earnings-on-opensea

- https://coinmarketcap.com/academy/article/openseas-os2-platform-launches-with-new-xp-system-and-exclusive-access-for-gemesis-nft-holders

- https://x.com/TheBlockCo/status/2055629052782792782

- https://opensea.io/blog/articles/opensea-digest-july-10-2025

- https://www.dlnews.com/articles/people-culture/opensea-delays-sea-token-airdrop/

- https://www.tradingview.com/news/cryptobriefing:d34c31043094b:0-opensea-plans-sea-token-launch-in-q1-2026-with-50-supply-for-users-and-50-revenue-for-buybacks/

- https://x.com/TheBlockCo/status/1965112113413706159

- https://whale-alert.io/stories/ea98012535090c/OpenSea-delays-SEA-token-launch-indefinitely-last-Treasure-rewards-wave-refunds-offered-forfeiting-Treasure-and-0-OS2-trading-fees-for-60-days

- https://cryptorank.io/news/feed/63d24-opensea-perpetual-futures-hyperliquid

- https://opensea.io/blog/articles/introducing-os2

- https://iq.wiki/wiki/opensea

- https://www.youtube.com/watch?v=85hbgjImbZc

- https://cryptorank.io/news/kaito

- https://cryptonews.net/news/altcoins/31726375/

- https://support.opensea.io/en/articles/8867091-what-fees-do-i-pay-on-opensea

- https://opensea.io/blog/articles/introducing-seaport-protocol

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…