A token launch encompasses the full lifecycle of creating, distributing, and establishing a market for a crypto asset — from tokenomics design and airdrops to exchange listings, governance structure, and regulatory risk.

- x.com37

- theblock.co13

- thedefiant.io5

- coindesk.com3

- decrypt.co3

- cryptonews.com2

- leviathannews.substack.com2

+9 sources across the wider coverage universe

OpenSea delays $SEA token launch indefinitely just two weeks before planned March 30 event, offers fee refunds for seasons 3-6 participants2026-03

OpenSea delays $SEA token launch indefinitely just two weeks before planned March 30 event, offers fee refunds for seasons 3-6 participants2026-03 Paradex signals upcoming $DIME Token Generation Event2026-03

Paradex signals upcoming $DIME Token Generation Event2026-03 Real Finance blockchain gears up for token launch after $25 million raise from Nimbus Capital2026-04

Real Finance blockchain gears up for token launch after $25 million raise from Nimbus Capital2026-04 Goldfish prepares GFIN governance token launch and ecosystem airdrop as GGBR expands across DeFi. By introducing a gold-backed stablecoin, Goldfish aims to bridge physical gold and DeFi.2026-03

Goldfish prepares GFIN governance token launch and ecosystem airdrop as GGBR expands across DeFi. By introducing a gold-backed stablecoin, Goldfish aims to bridge physical gold and DeFi.2026-03 Man snipes 70% of $WET presale using 1,000+ wallets, demands refund; HumidiFi cancels bot allocations, issues pro-rata airdrop, and announces new audited token launch to protect legitimate investors.2025-12

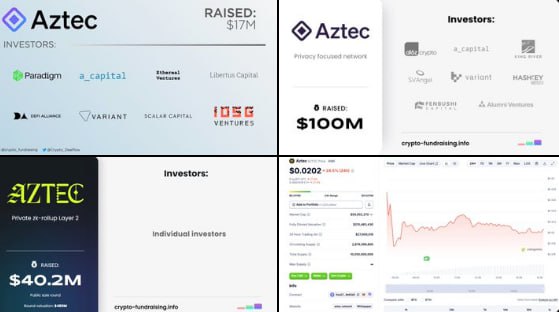

Man snipes 70% of $WET presale using 1,000+ wallets, demands refund; HumidiFi cancels bot allocations, issues pro-rata airdrop, and announces new audited token launch to protect legitimate investors.2025-12 Crypto investor slams Aztec’s token launch as a VC-inflated fiasco that left retail holders with 50%+ losses and a fraction of its prior $480M valuation.2026-02

Crypto investor slams Aztec’s token launch as a VC-inflated fiasco that left retail holders with 50%+ losses and a fraction of its prior $480M valuation.2026-02

Arrr, hoistin' me quill to chart these token launch waters for ye — here be the pillar page, shipshape and ready for the crew:

A token launch is the process by which a blockchain project creates, distributes, and establishes a market for a new cryptographic asset — encompassing everything from smart contract deployment to exchange listing strategy and community allocation.

The mechanics have grown considerably more complex since Bitcoin demonstrated in 2009 that a native asset could bootstrap a decentralized network from zero. Today a token launch involves legal structuring, tokenomics design, exchange relationships, market-maker agreements, airdrop campaigns, and governance frameworks that must all cohere before a single token trades publicly. Getting any one of these wrong — as a string of high-profile delays and controversies has shown — can sink a project before it finds its footing.

What a Token Actually Is

Before examining a launch, it helps to be precise about what is being launched. A token is a unit of account on a blockchain that encodes some set of rights or functions: it might represent a governance vote, a share of protocol revenue, access to a service, collateral for a stablecoin, or speculative exposure to a network's growth. This is distinct from a coin, which is the native asset of a layer-1 blockchain (ETH on Ethereum, SOL on Solana).

Most tokens today are issued on programmable smart-contract platforms. Ethereum's ERC-20 standard remains the dominant format, but Solana's SPL token program, BNB Chain's BEP-20, and newer environments like Base and Monad have expanded the landscape. Cross-chain launches — where the same token is simultaneously deployed on multiple networks — are increasingly common, as projects chase liquidity wherever it pools.

OpenSea delays $SEA token launch indefinitely just two weeks before planned March 30 event, offers fee refunds for seasons 3-6 participants

What went wrong. Indefinitely shouldn't be in the conversation

Readers click token launches not for the tokenomics — they click for personal extraction angles: airdrop eligibility to farm, pre-launch price signals to trade, or insider selling evidence to front-run the dump.

Tokenomics: Design Before Deployment

The most consequential decisions in a token launch happen before any public sale. Tokenomics — the economic design of a token's supply, distribution, and incentive structure — determines whether a token can sustain value or will collapse under early selling pressure.

Key variables include:

Total supply and emission schedule. A fixed supply (like Bitcoin's 21 million cap) signals scarcity; an inflationary schedule funds ongoing protocol incentives but dilutes holders. Neither is inherently superior — the design must match the protocol's actual needs.

Allocation splits. Industry practice has converged around categories: team and early contributors (typically 15–25%, subject to multi-year vesting), investors (10–20%, also vested), ecosystem and treasury reserves (20–40%), and community distributions including airdrops and liquidity incentives (15–30%). Distortions in these splits — unusually large team or investor allocations, thin community pools — are a common early warning sign.

Vesting and lockup schedules. Team and investor tokens locked for one to four years prevent immediate dumping. When those cliffs expire, supply can spike suddenly. Savvy analysts track unlock schedules as a market timing tool; several data services publish these calendars.

Utility versus speculation. Tokens with genuine protocol utility — fee payment, collateral, governance rights with real stakes — tend to develop more durable demand than pure governance tokens for protocols where governance decisions have little economic consequence.

Real Finance, which raised $25 million from Nimbus Capital before its token launch, and Goldfish, which paired its GFIN governance token with a gold-backed stablecoin, illustrate two different tokenomics philosophies: one anchored in institutional fundraising, one attempting to link the token to a real-world asset price.

The Token Generation Event (TGE)

A Token Generation Event — sometimes called a TGE or token launch proper — is the moment the smart contract that creates the token is executed on-chain. It is distinct from the public sale or exchange listing, though these often happen in close sequence.

Common TGE structures include:

Initial DEX Offerings (IDOs). Tokens are sold and immediately paired with a base asset (ETH, SOL, USDC) in a decentralized exchange liquidity pool. Price discovery happens in real time, without a centralized intermediary setting an opening price. This approach democratizes access but can produce violent early price action if the liquidity pool is thin.

Launchpad sales. Platforms like Binance Launchpad, or newer category-specific venues like SafuSkill on BNB Chain, pre-screen projects and conduct structured sales to allowlisted participants before broader trading opens. These offer more controlled conditions but concentrate gatekeeping power.

Genesis NFT + token auctions. Some projects combine an NFT auction with a token launch, as Panorama did with its $PANO token in April — sequencing a token launch, allowlist NFT mint, and public NFT mint across two days. This creates a multi-phase demand event but also multiplies operational complexity and regulatory exposure.

Fair launches. No pre-sale, no investor allocation; tokens are distributed entirely through mining, liquidity provision, or community participation. This model, popularized by early DeFi projects, is rare today for well-capitalized teams but retains ideological cachet.

Paradex has signaled an upcoming Token Generation Event for its $DIME token, and Polymarket — the prediction market platform — has been the subject of active speculation about a 2026 token launch. Both represent the pattern of mature protocols delaying launches until market and regulatory conditions feel favorable.

- 01airdrop farming speculation

Rumors of unannounced token launches triggered immediate farming behavior, making speculation itself the story — readers wanted allocation strategies, not product analysis.

- 02team and insider dumping

Onchain evidence of founders selling into launch liquidity — epitomized by $500M in TRUMP team sells — drew readers seeking early warning of exit behavior.

- 03TradFi tokenization pilots

Announcements from DBS, BlackRock, Société Générale, and Bitfinex framed tokenization as institutional validation, pulling readers who track the legitimization arc of the asset class.

- 04NFT projects pivoting to tokens

Doodles and Pudgy Penguins converting community goodwill into fungible tokens raised questions about whether NFT holders or new buyers capture value.

- 05governance token redesigns

MakerDAO's Endgame restructuring — replacing MKR with new stable and governance tokens — attracted readers weighing dilution risk against promised incentive alignment.

- 06cross-chain UX at launch

Magic Accounts' unified-balance architecture at launch set a new benchmark, attracting readers evaluating whether token utility was real or bridging complexity was just hidden.

Airdrops and Community Distribution

An airdrop is a retroactive or prospective distribution of tokens to a defined group of addresses, typically to reward early users, bootstrap a governance community, or generate awareness. It is one of the most powerful — and most gamed — tools in the token launch toolkit.

Retroactive airdrops distribute tokens to past users based on on-chain activity: transaction counts, volume, protocol-specific interactions. Uniswap's 2020 airdrop, which sent 400 UNI to every historical address, set the template. Since then, projects have added progressively more sophisticated criteria to filter out "airdrop farmers" — accounts that mimic organic usage solely to capture distributions.

Points programs and seasons have emerged as a middle layer. Projects like OpenSea (which eventually delayed its $SEA token launch indefinitely amid market challenges) ran multi-season points programs that implied future token distributions. When OpenSea postponed without a new date and offered refunds for seasons 3–6 participants, the episode became a case study in how points programs create implicit commitments that are painful to walk back.

Goldfish's planned GFIN ecosystem airdrop alongside its governance token launch, targeting DeFi participants across its platform, illustrates the current norm: airdrops paired with governance tokens to simultaneously distribute ownership and reward engagement.

Paradex signals upcoming $DIME Token Generation Event

Goodluck to them on their endeavors

Market Making, Exchange Listing, and the Binance Question

A token can be technically launched but economically inert if it lacks liquidity. Market makers — firms that continuously quote buy and sell prices — are essential to functioning secondary markets. Their contracts with projects have attracted increasing scrutiny.

In 2024 and into 2025, investigations revealed that some market-maker agreements included "loan-with-option" structures: the project lent tokens at no cost, and the market maker could return them or pocket them after an agreed period, depending on price movement. This created perverse incentives for market makers to suppress prices and profit on the option rather than support the token.

Binance publicly tightened its rules on market makers and token launch trading in response to these concerns, requiring greater transparency about market-maker agreements from projects seeking listings. The exchange's listing decisions remain enormously consequential for a token's liquidity profile — a Binance spot listing can multiply trading volume by orders of magnitude — which means its new requirements effectively set a due-diligence floor for major launches.

Exchange listing sequencing matters: listing on a centralized exchange before sufficient decentralized liquidity exists can lead to price manipulation; listing too late, after DEX price discovery has run for months, can disadvantage exchange investors who pay a premium relative to earlier participants.

- 2024-01launch

Jupiter JUP token launches on Solana at ~$0.65 implied price

- 2024-03launch

BlackRock Ethereum tokenized fund (BUIDL) launches on-chain

- 2024-07governance

MakerDAO Endgame launch begins with new stablecoin and governance token plan

- 2024-11launch

Tether USDT and XAUT go live on TON blockchain

- 2024-12launch

Pudgy Penguins $PENGU token launches before year-end

- 2025-01milestone

TRUMP team sells ~$500M in tokens into launch liquidity per onchain data

- 2025-02launch

Berachain mainnet launches with 15.75% BERA community airdrop

Governance Tokens and the Question of Real Power

Many modern token launches are nominally for governance: token holders vote on protocol parameters, treasury allocations, fee structures, and upgrade proposals. The substance behind this power varies enormously.

At one end, governance tokens for major DeFi protocols like Uniswap, Compound, or Aave control billions of dollars of protocol parameters and treasury funds — genuine economic stakes. At the other end, tokens sold as "governance" for protocols with immutable contracts or centralized admin keys offer effectively no power.

Regulatory agencies, particularly the U.S. Securities and Exchange Commission, have increasingly focused on whether governance tokens constitute unregistered securities. The logic: if token holders expect to profit from the efforts of others (the issuing team building the protocol), the Howey test for a security may be satisfied regardless of the "governance" label. This has made legal structuring a central element of modern token launches, with projects seeking to demonstrate genuine decentralization before distributing tokens.

The $PANO launch's regulatory scrutiny warnings and SafuSkill Launchpad's acknowledgment of regulatory risks illustrate that even smaller launches now grapple openly with this exposure.

The Role of AI and Autonomous Agents

An emerging frontier in token launches involves autonomous agents — AI systems capable of executing on-chain transactions without direct human intervention. Flap's modular token launch infrastructure, integrated into the BitAgent ERC-8183 Agent Marketplace, enables builders to wire launch mechanics directly into agents: automated sales, liquidity provisioning, and distribution logic that runs without a human clicking "confirm" at each step.

This creates new efficiencies and new risks. An agent that can autonomously execute a token launch can also autonomously make mistakes that are immediately on-chain and often irreversible. The intersection of AI compute — itself increasingly tokenized — with autonomous launch infrastructure is nascent but moving quickly, particularly on Solana and Base where lower transaction costs make iteration cheaper.

Velvet's integration with Printr, enabling unified discovery and trading of token launches across Solana, Base, BNB Chain, and Monad, points toward a future where multi-chain launches are orchestrated through AI-assisted interfaces rather than manual cross-chain monitoring.

Real Finance blockchain gears up for token launch after $25 million raise from Nimbus Capital

"On-chain data shows Real Finance's testnet had 12k daily active wallets last month - strong traction pre-launch. But Nimbus Capital's $25M raise came with a 2-year vesting schedule (trackable via Etherscan), tempering immediate sell pressure. Smart money wallets already accumulating on DEXs - 5 key addresses hold 18% of circulating supply. TVL at $47M suggests organic demand beyond VC hype." (280 chars) Key metrics referenced: - Testnet adoption (12k DAU) - Vesting terms (2-year lock)

- Smart ContractMedium

New token contracts deployed at launch — especially cross-chain or multi-protocol designs like Magic Accounts — expand the attack surface before audits can cover live conditions.

- CentralizationHigh

Team and early-backer token allocations routinely enable nine-figure unlocked sells into launch liquidity, as the TRUMP team's ~$500M onchain outflow illustrates.

- RegulatoryHigh

Stablecoin and tokenized-asset launches from Société Générale, DBS, and Tether face divergent jurisdictional treatment, with euro-backed and TON-native instruments sitting in unsettled legal categories.

- LiquidityHigh

Low float at launch combined with large locked supplies — Jupiter launched 1.35B circulating against a much larger total — creates violent price discovery and thin exit depth for late buyers.

- Market ManipulationHigh

Aerodrome's suspension of contributors for insider trading of $VVV at launch confirms that pre-launch information asymmetry regularly translates into front-running rather than exception.

- GovernanceMedium

Protocols like Friendtech and MakerDAO highlight that teams can issue governance tokens with no binding obligations toward buyers, leaving holders exposed to unilateral parameter changes.

What Goes Wrong: Common Failure Modes

Token launch problems tend to concentrate in predictable categories:

Pre-launch information asymmetry. Insiders — team members, early investors, advisors — sometimes trade on advance knowledge of launch timing or tokenomics details. The Milei-LIBRA affair, in which phone records revealed seven calls between the Argentine president and a LIBRA token backer on launch night, illustrated how political and financial conflicts can intersect around token launches with enormous consequences.

Operational failures under pressure. A tight mint schedule, as flagged in the $PANO launch analysis, creates windows where bugs, network congestion, or front-running can cause cascading problems. Grvt delayed its token launch to late June citing market consolidation, reflecting the rational calculation that a bad launch in poor conditions is worse than a delayed launch in better ones.

Tokenomics that front-load insiders. High team and investor allocations with short vesting periods produce predictable sell pressure at cliff dates. Community participants who bought at launch or airdrop can find themselves holding an asset whose largest holders are incentivized to exit.

Regulatory ambiguity. Projects that launch without clear legal structuring face retroactive enforcement risk, particularly in U.S. markets. This has pushed many launches to use foundation structures in crypto-friendly jurisdictions, exclude U.S. participants from public sales, or delay launches until regulatory clarity improves.

Market timing. Circle's exploration of an Arc Network token launch, highlighted by its CEO, is an example of a well-capitalized issuer carefully managing the timing signal — floating the idea publicly to gauge reception before committing to a date. OpenSea's repeated delays, eventually indefinite, show the downside of committing publicly to a date before conditions are right.

Stablecoins and the Token Launch Ecosystem

Stablecoins play an infrastructure role in token launches that is easy to underestimate. The vast majority of token sales are denominated in stablecoins — USDC and USDT being the dominant pair assets — rather than in ETH or BTC. This pricing convention insulates both issuers and buyers from base-asset volatility during the sale period, standardizes accounting, and simplifies post-launch treasury management.

Goldfish's pairing of a governance token launch with a gold-backed stablecoin (GGBR) represents a more integrated approach: the stablecoin is not just a sale denomination but a core protocol asset, designed to give the governance token a fundamental utility floor.

Projects raising funds in stablecoins also hold more predictable treasury reserves, an advantage when planning multi-year development budgets in volatile markets.

Outlook

The token launch landscape is consolidating around higher standards of transparency and rigor, partly driven by market experience with failures and partly by regulatory pressure that — whatever its pace — is clearly moving toward more structured oversight of digital asset issuance.

Several trends are likely to define launches in the coming years. Multi-chain launches, where tokens are simultaneously live on Solana, Ethereum, Base, and BNB Chain from day one, will become the norm rather than the exception. Autonomous agent infrastructure will handle more of the mechanical execution. Vesting and unlock schedules will face more sophisticated community scrutiny, with on-chain analytics making it harder to obscure insider allocations.

The most durable token launches will be those where the token has genuine utility within a functioning product, where tokenomics distribute ownership broadly enough to sustain a governance community, and where the team has thought carefully about what it is asking the market to value. That combination remains rare — and that is precisely why it commands a premium when it appears.

Latest Token Launch news

OpenSea delays $SEA token launch indefinitely just two weeks before planned March 30 event, offers fee refunds for seasons 3-6 participantsParadex signals upcoming $DIME Token Generation EventReal Finance blockchain gears up for token launch after $25 million raise from Nimbus CapitalGoldfish prepares GFIN governance token launch and ecosystem airdrop as GGBR expands across DeFi. By introducing a gold-backed stablecoin, Goldfish aims to bridge physical gold and DeFi.Man snipes 70% of $WET presale using 1,000+ wallets, demands refund; HumidiFi cancels bot allocations, issues pro-rata airdrop, and announces new audited token launch to protect legitimate investors.Crypto investor slams Aztec’s token launch as a VC-inflated fiasco that left retail holders with 50%+ losses and a fraction of its prior $480M valuation.Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…