Deep explainer on Stellar’s payments-first blockchain, covering XLM, Soroban smart contracts, USDC and MGUSD stablecoins, MoneyGram and DTCC ties, cross-border payments, tokenization, quantum security, and key risks for onchain finance.

+9 sources across the wider coverage universe

Alchemy brings Stellar ecosystem to its platform, enabling builders to scale RWA platforms, cross-border payments, and financial apps with enterprise integrations2026-04

Alchemy brings Stellar ecosystem to its platform, enabling builders to scale RWA platforms, cross-border payments, and financial apps with enterprise integrations2026-04 Circle expands CCTP to Stellar, enabling developers and institutions to move USDC across 23 blockchains using canonical burn-and-mint infrastructure2026-05

Circle expands CCTP to Stellar, enabling developers and institutions to move USDC across 23 blockchains using canonical burn-and-mint infrastructure2026-05 Stellar plans quantum-safe signers for all accounts by 2027 as QPP targets Ed25519 risk2026-06

Stellar plans quantum-safe signers for all accounts by 2027 as QPP targets Ed25519 risk2026-06 MoneyGram and Stellar extend partnership to scale global stablecoin adoption, expanding USDC-powered cash on/off-ramps and app balances across Latin America2026-04

MoneyGram and Stellar extend partnership to scale global stablecoin adoption, expanding USDC-powered cash on/off-ramps and app balances across Latin America2026-04 Stellar CMO urges crypto to abandon hype cycles for “get rich slow” mindset, emphasizing long-term value creation as key to mainstream trust2026-04

Stellar CMO urges crypto to abandon hype cycles for “get rich slow” mindset, emphasizing long-term value creation as key to mainstream trust2026-04 CME Group says crypto futures suite now covers over 75% of total market cap after adding Cardano, Chainlink, and Stellar contracts2026-03

CME Group says crypto futures suite now covers over 75% of total market cap after adding Cardano, Chainlink, and Stellar contracts2026-03

Stellar: A Comprehensive Guide to the Payments‑First Blockchain

Stellar is an open-source blockchain network designed primarily for payments, asset issuance, and tokenization, with a particular focus on connecting traditional financial institutions to onchain infrastructure. At its core, Stellar aims to make moving value as simple and reliable as sending an email, while supporting regulated stablecoins, institutional-grade tokenization, and programmable payments.

Origins and Design Philosophy

Stellar emerged in 2014 with an explicit mission to improve access to affordable financial services by creating a neutral, interoperable payment layer that could sit between existing financial systems. From the outset, the network’s design prioritized speed, low fees, and direct integration with banks, money transmitters, and fintechs rather than focusing solely on permissionless speculation or complex DeFi. That institutional and payments-centric orientation remains visible today in Stellar’s positioning as a blockchain built for enterprises and institutions, supporting smart contracts, fast payments, and asset tokenization. This starting point helps explain why the network has become a home for use cases such as cross-border remittances, regulated stablecoins, and tokenized securities.

Unlike many general-purpose smart contract platforms, Stellar’s early architecture placed built-in payments primitives at the center of the protocol. The base layer included native support for multiple issued assets, path payments, and a decentralized exchange, allowing users to move between currencies without needing external smart contracts. This design reflected a conviction that real-world financial flows require predictable behavior, transparent fees, and clear asset semantics. Over time, the ecosystem has layered more programmability on top of these primitives, culminating in the Soroban smart contract platform, while maintaining compatibility with the original payments-focused ledger. This evolution illustrates Stellar’s attempt to combine the reliability of a payment network with the flexibility demanded by modern onchain finance.

The network’s governance model has also been shaped by its financial-inclusion origins. The Stellar Development Foundation (SDF), a non-profit entity, stewards protocol development and ecosystem growth rather than operating as a for-profit issuer or centralized service provider. While SDF holds significant influence through its control of part of the XLM supply and its role in shaping protocol upgrades, the network’s validation and consensus are handled by a decentralized set of validators that choose their own trust relationships. This distinction matters for regulators and institutional partners who need clarity about who operates the infrastructure and where responsibilities lie, especially in the context of stablecoin issuance, securities tokenization, and cross-border payment channels.

Alchemy brings Stellar ecosystem to its platform, enabling builders to scale RWA platforms, cross-border payments, and financial apps with enterprise integrations

Alchemy is an EVM shop — ERC-4337 smart wallets, Solidity tooling, gas sponsorship — and Stellar runs Rust on Soroban with a completely different account model. Franklin Templeton's BENJI parking $651M on XLM pushed Stellar's RWA past $1.8B, which is why Alchemy showed up after QuickNode and Ankr already had Horizon support. Watch whether Soroban RPC gets the same SLA tier as their Ethereum endpoints — RWA issuers measure infra in 9s of uptime, not gas savings.

Readers click Stellar not for DeFi speculation but for TradFi legitimacy signals — every high-performing headline is a name-brand institution (CME, MoneyGram, Mastercard, Societe Generale) treating Stellar as settlement infrastructure, which means reader appetite is really a proxy for 'is this network safe enough for real money.'↗

How the Stellar Network Works

Accounts, Assets, and the Built-In DEX

At the technical level, Stellar organizes activity around accounts that hold balances of different assets and maintain configuration data such as signers and thresholds. Each account can hold both the native asset, Stellar Lumens (XLM), and an arbitrary number of issued assets representing fiat currencies, stablecoins, commodities, or other tokenized instruments. These issued assets exist as credit from an issuing account, and other users hold them under a system of trustlines that explicitly opt in to each asset. That trustline model is central to how Stellar implements asset risk management: users must signal their willingness to accept exposure to each issuer, which provides a straightforward way to differentiate regulated stablecoins from more experimental tokens.

One of Stellar’s distinctive features is a native orderbook-based decentralized exchange built directly into the protocol. Rather than relegating asset swaps to smart contracts, Stellar’s core operations include the creation, cancellation, and matching of limit orders between assets. This orderbook underpins path payments, which allow a user to send one asset and have the recipient receive another, with the protocol finding conversion paths across orderbooks and issued assets. For cross-border payments, this means a sender can pay in their local currency, route through stablecoins or XLM, and deliver a different fiat currency to the recipient, all in a single transaction. That functionality is particularly relevant when combined with regulated stablecoins such as USDC and MGUSD, which can serve as liquid intermediaries in these paths.

The account model also supports multi-signature configurations, sequence numbers for replay protection, and time bounds on transactions. These features are not unique to Stellar, but they are tightly integrated into its transaction semantics in ways that matter for compliance and institutional integration. For example, asset issuers can freeze or claw back tokens when required by regulation if they opt into those capabilities at issuance time, allowing them to meet obligations around sanctions or court orders. This balance between programmable control and user autonomy is a recurring theme in how Stellar has approached asset issuance and tokenization.

Anchors and Fiat On/Off-Ramps

Anchors are a foundational concept in the Stellar ecosystem, serving as regulated gateways that connect onchain assets to off-chain accounts such as bank balances or mobile money wallets. In practice, an anchor issues a tokenized representation of a currency or deposit claim on Stellar and agrees to redeem that token 1:1 for the corresponding off-chain asset. Users can deposit fiat with an anchor, receive the tokenized version onchain, transfer it across the network, and eventually withdraw into local bank accounts or cash-out partners, with the anchor handling the off-chain settlement. This model allows Stellar to interoperate with a diverse set of banking and payment systems without requiring changes to those systems’ core infrastructure.

Anchors can be banks, licensed money transmitters, stablecoin issuers, or other regulated entities. Their responsibilities extend beyond issuance and redemption; they often handle KYC, AML checks, and transaction screening, which is why Stellar ecosystem standards (SEPs) define common APIs and data formats for these interactions. This anchor model is critical for cross-border payments, where funds commonly move from a local payment method into a tokenized asset on Stellar, traverse the network, and then exit through an anchor on the receiving side. For remittance providers and fintechs, this architecture offers a way to build global corridors without negotiating bilateral relationships in every market.

MoneyGram’s adoption of Stellar provides a clear illustration of how anchors and off-ramps operate in practice. The company has launched MGUSD, a U.S. dollar stablecoin designed to power its own network, with tokens minted and burned using smart contracts provided by infrastructure provider M0 and initially deployed on Stellar. By combining MGUSD issuance with its extensive global payout network, MoneyGram can allow users to hold and transfer a tokenized dollar on Stellar and cash out through retail locations or bank partners, effectively bridging between onchain balances and physical or local banking cash-out options. This model points toward a future in which traditional money transfer brands act as anchors and stablecoin issuers, rather than being displaced by blockchain-native startups.

Fees, Throughput, and Scalability

Stellar’s fee model is intentionally conservative and predictable. Every operation on the network incurs a base fee denominated in XLM, with the minimum set at 0.00001 lumen per operation. This extremely low fee is primarily designed as an anti-spam mechanism rather than a significant source of revenue, reflecting the network’s goal of facilitating high-volume, low-value transactions such as remittances and micro-payments. At typical market prices, the cost of sending a payment is often measured in fractions of a cent, which makes the network feasible for retail transfers and machine-sized payments that would be uneconomical on more expensive chains.

From a supply perspective, there are approximately 50 billion lumens in existence, and the protocol no longer creates new XLM. Earlier in the network’s history, a portion of the supply was burned to reduce inflationary overhang, and the remaining tokens are used for fees, account minimums, and ecosystem support. The absence of ongoing issuance at the protocol level simplifies long-term economic analysis for institutions that need to forecast their cost base for onchain operations. It also means that fee revenue does not accrue to miners or validators in the same way it does on proof-of-work or many proof-of-stake chains, which influences the incentives around network participation and governance.

In terms of throughput, Stellar’s consensus protocol is optimized for relatively fast finality at the scale required for global payments rather than the very high transaction volumes targeted by some high-performance chains. The network can settle transactions in a matter of seconds in typical conditions, which is sufficient for most remittance, retail, and institutional payment flows. Because many payment paths can be executed in a single multi-operation transaction, the effective capacity for complex cross-asset payments is higher than a simple transactions-per-second metric might suggest. However, as Soroban smart contracts gain adoption, the network will need to continue optimizing for computational load and state growth, balancing programmability with the deterministic performance expected by payments partners.

Stellar Lumens (XLM): The Native Asset

Role of XLM in the Network

Stellar Lumens (XLM) serves as the network’s native asset, but it is intentionally designed as a utility token rather than a claim on revenues or equity of the Stellar Development Foundation. One of XLM’s primary roles is to act as a fee token, with every transaction consuming a small amount of lumens to deter spam and denial-of-service attacks. In addition, accounts must maintain a minimum XLM balance that scales with the number of trustlines and offers they create, which further discourages excessive use of network resources. This approach ties resource allocation to a scarce asset while keeping the absolute costs low enough to preserve accessibility.

XLM can also function as a bridge asset in the network’s built-in decentralized exchange and path payment system. When direct liquidity between two issued assets is thin, the protocol can route through XLM orderbooks, effectively using lumens as an intermediate currency to facilitate conversion paths. This bridging role is more prominent in corridors where regulated stablecoins are not yet deeply liquid or where local currency tokens are relatively new. XLM thus supports the broader ecosystem of issued assets by improving liquidity and routing options, although its importance as a bridge asset may diminish over time as more fiat-backed stablecoins and tokenized currencies become liquid on Stellar.

The asset also plays a symbolic and governance-related role. While XLM does not entitle holders to formal on-chain voting rights over protocol parameters, it is central to ecosystem funding programs and grants administered by the SDF. Many community initiatives, including infrastructure, wallets, and developer tooling, have been funded in XLM, aligning contributors’ incentives with network growth. This distribution model has, however, attracted regulatory scrutiny in some jurisdictions, where authorities are still considering how to classify native tokens that power public blockchains.

Tokenomics and Supply Characteristics

Stellar’s tokenomics are deliberately conservative compared with some newer networks. The total number of lumens is fixed at around 50 billion, and the protocol does not create additional XLM. Earlier phases of the network involved inflationary issuance and community distributions, but those policies were revised, and a large portion of the supply was destroyed to align long-term incentives. The remaining XLM is held by a combination of users, exchanges, institutions, and the Stellar Development Foundation, which uses its holdings for ecosystem growth and operational expenses.

The fixed supply and extremely low protocol fees mean that future demand for XLM will primarily be driven by its role as a utility asset rather than by expectations of fee-based yield or staking rewards. Unlike proof-of-stake chains, Stellar validators do not receive block rewards or fee shares, and there is no native staking yield for lumens. This design simplifies the economic model for institutional partners who may be wary of implicit securities-like features or yield mechanisms embedded in protocol tokens. It also places greater weight on the intrinsic utility of XLM for payments, liquidity, and account management.

For retail market participants, these characteristics have implications for how XLM is perceived as an investment. Without native yield or governance rights, XLM’s value is largely tied to expectations about network usage, institutional adoption, and the scarcity of the token supply. Price movements can be influenced by developments such as new stablecoin launches, tokenization partnerships, or major protocol upgrades like Soroban and the Quantum Preparedness Plan. However, as with other infrastructure tokens, there is no guarantee that increased network activity will translate directly into proportional price appreciation, especially given the relatively large existing supply.

Market Positioning and Institutional Perception

XLM occupies a somewhat distinct niche in the broader crypto asset universe. It is closely associated with cross-border payments, remittances, and institutional partnerships rather than purely speculative DeFi or NFT activity. That positioning is reinforced by collaborations with firms such as MoneyGram, which has chosen Stellar as the launch platform for its MGUSD stablecoin, and by tokenization initiatives involving infrastructure providers like DTCC. For institutions evaluating blockchain options, the network’s emphasis on compliance, stablecoin support, and integration with existing payment rails can be more salient than the presence of retail-focused yield farms or gaming applications.

At the same time, XLM competes for attention and liquidity with native tokens from other payment-oriented networks and with stablecoins themselves. As regulated stablecoins such as USDC and MGUSD become more prominent on Stellar, many users may choose to hold those assets rather than maintaining large XLM balances, especially for day-to-day transactions. In this sense, XLM’s role is somewhat analogous to that of a utility commodity in a financial market, necessary for operations but not always the primary vehicle for savings or investment. This dynamic underscores why ecosystem health for Stellar is as much about the diversity and quality of issued assets, anchors, and institutional integrations as it is about XLM’s market capitalization.

- 01Foundation strategic backing race↗

Splyce's simultaneous backing from Sui, Stellar, and Solana foundations signaled a competitive war for DeFi developer mindshare, pulling readers who track which L1s are winning builder loyalty.

- 02TradFi derivatives coverage expansion

CME adding Stellar futures alongside Cardano and Chainlink — hitting 75% of total crypto market cap — told readers that institutional hedging infrastructure was catching up to spot markets faster than expected.

- 03Stablecoin payment rails buildout↗

MoneyGram's USDC-powered cash on/off-ramps and Wirex's native Stellar payment cards represent the specific use case Stellar was designed for, drawing readers tracking whether the network's decade-long remittance thesis is finally closing.

- 04USDC cross-chain infrastructure↗

Circle's CCTP expansion making Stellar domain 27 across 23 chains turned Stellar into a canonical USDC corridor, which readers recognized as a structural liquidity upgrade with institutional weight behind it.

- 05Quantum safety timeline↗

Stellar's 2027 quantum-safe signer roadmap and its architectural advantage — account identity separated from signing keys — gave readers a concrete answer to an abstract threat that other chains have not yet addressed.

- 06RWA and tokenized fund adoption↗

Franklin Templeton's BENJI and Amundi's $100M tokenized fund choosing Stellar over Ethereum-first alternatives told readers that regulated asset managers were vetting the network's compliance posture, not just its throughput.

Smart Contracts on Stellar: Soroban

From Simple Operations to Full Smart Contracts

For much of its history, Stellar deliberately avoided general-purpose smart contracts in favor of a limited set of built-in operations. Complex workflows were composed by chaining multiple operations in a single transaction rather than by deploying custom code on-chain. This approach reduced the attack surface and made transaction behavior more predictable, which aligned well with the network’s payments-first philosophy. However, as DeFi, programmable stablecoins, and institutional tokenization grew in sophistication, demand increased for a more flexible execution environment that could still meet Stellar’s security and performance requirements.

Soroban is Stellar’s answer to this challenge, introduced as a smart contract platform integrated into the existing Stellar blockchain. Rather than launching a separate chain, Soroban is an additive feature that lives alongside the classic set of Stellar operations and interacts with the same ledger. Contracts are written in Rust and compiled to WebAssembly (Wasm), which provides a well-understood, sandboxed execution environment and allows developers to leverage Rust’s strong type system and tooling. This architecture aims to bring the programmability associated with platforms like Ethereum to Stellar while retaining its deterministic, payments-focused core.

The decision to integrate Soroban into the existing chain rather than spinning up a parallel environment has significant implications for user experience and institutional adoption. Assets issued on classic Stellar are directly usable in Soroban contracts, and payments logic can combine native operations with contract calls without requiring complex cross-chain bridges. For anchors and stablecoin issuers, this means they can add programmable features such as conditional transfers, escrow, or compliance checks without migrating to a different ledger. For institutions evaluating tokenization strategies, the combination of a mature payments layer and a new, auditable contract environment is a core part of Stellar’s value proposition.

Soroban Architecture and Developer Experience

Soroban’s architecture builds on a set of host functions that expose safe, bounded operations to contract code running in Wasm. Developers write Rust code that interacts with these host functions to read and write contract storage, manipulate assets, and interact with accounts and other contracts. The environment enforces deterministic execution and resource metering, so that contracts cannot consume unbounded computation or memory. These controls are particularly important for a payments network, where predictable fees and performance are more critical than maximum expressiveness.

From a developer-experience standpoint, Soroban provides SDKs, testing frameworks, and tooling that align with modern Rust and WebAssembly workflows. Contracts can be developed and tested locally before being deployed to testnet and eventually mainnet, with clear guidance on best practices for security and gas optimization. The Stellar ecosystem has also funded early Soroban projects through programs such as the Stellar Community Fund, which offers grants to teams building DeFi protocols, wallets, and infrastructure that leverage the new smart contract capabilities. This funding helps bootstrap onchain liquidity and use cases, which are essential for any smart contract platform.

One compositional advantage of Soroban is its ability to coexist with SEPs and other off-chain standards that anchors use. For instance, a stablecoin issuer could maintain existing deposit and withdrawal APIs while adding Soroban contracts to handle programmable features like streaming payments or invoice reconciliation. Payment facilitators might deploy contracts that encode routing rules or revenue splits, while still settling the underlying transfers through classic Stellar payments. This hybrid model allows institutions to adopt programmability incrementally rather than being forced into a complete migration to a new stack.

Use Cases: DeFi, Programmable Payments, and Compliance Tooling

Soroban opens the door to a range of use cases that extend beyond Stellar’s original remittance focus while still aligning with its institutional and compliance-aware ethos. On the DeFi side, developers can build automated market makers, lending protocols, and tokenized yield products that natively use Stellar-issued assets and stablecoins. These protocols can operate alongside the built-in orderbook DEX, potentially offering both orderbook and AMM liquidity for the same asset pairs. Stablecoins like USDC and MGUSD can serve as core collateral assets and settlement currencies within these protocols, provided that their issuers are comfortable with the contract risk exposure.

Programmable payments represent another important application area. With Soroban, it becomes possible to encode conditional transfers, multi-party escrow, subscription billing, or milestone-based disbursements directly into contracts. For example, a humanitarian organization could deploy a contract that releases funds to beneficiaries only when certain onchain or off-chain conditions are met, while funding the contract with onchain stablecoins. Retail-focused applications could implement pay-per-use models or time-locked rewards using Soroban, with settlement occurring in tokenized fiat or regulated stablecoins rather than volatile cryptocurrencies.

Compliance tooling is perhaps the most distinctive potential use case for Soroban in the context of Stellar’s institutional strategy. Contracts can be designed to enforce whitelist-based access, region-specific restrictions, or dynamic risk checks before allowing transfers of certain tokenized securities or institutional stablecoins. Coupled with the network’s anchor model and SEPs, this allows issuers and financial institutions to encode parts of their regulatory obligations directly into onchain logic. While such designs must be carefully audited and remain subject to evolving regulations, they illustrate how programmable compliance could differentiate Stellar from less regulated environments.

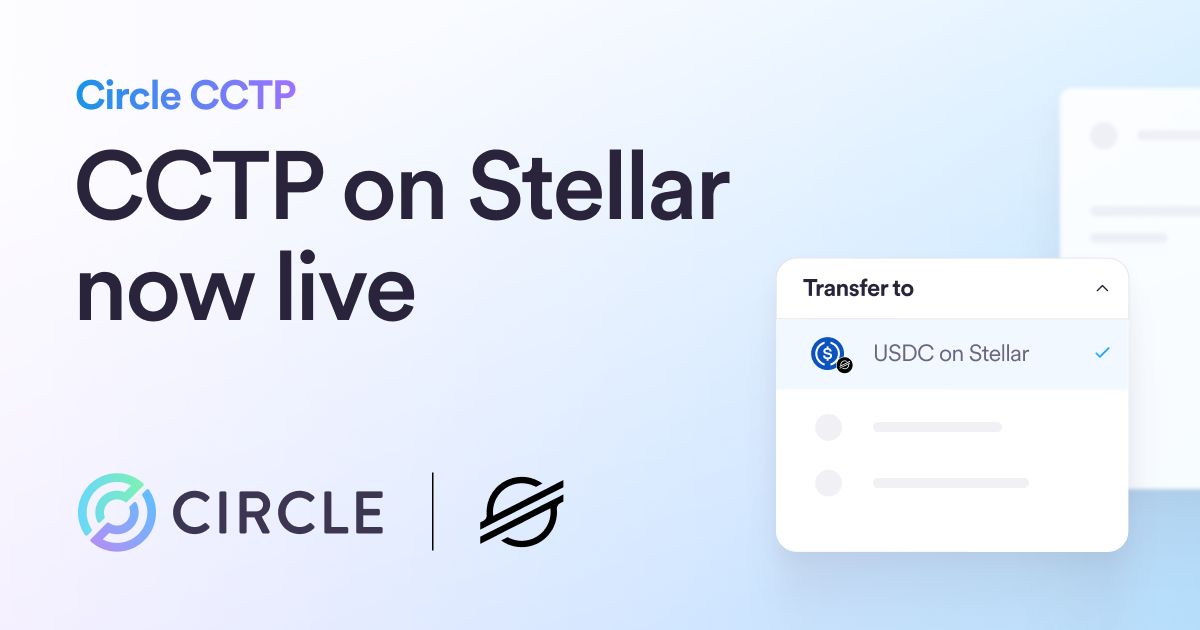

Circle expands CCTP to Stellar, enabling developers and institutions to move USDC across 23 blockchains using canonical burn-and-mint infrastructure

$284M of USDC on Stellar is tiny next to Ethereum's $50B+ pool, but it was also stuck in a payments lane with weak composability into EVM/Solana flow. CCTP turns Stellar into usable inventory for treasury desks, payment apps, and on/off-ramp routing, especially with MoneyGram's 475k cash locations at the edge. The footgun is very Stellar-specific: Circle's docs require CctpForwarder for inbound mints because raw 32-byte addresses don't distinguish accounts from contracts, so sloppy integrations can still strand funds even with canonical burn-mint.

Stellar for Cross-Border Payments

Traditional Remittances vs Blockchain Rails

Cross-border payments and remittances have long been characterized by high fees, long settlement times, and fragmented correspondent banking relationships. In the traditional model, funds often pass through multiple intermediaries, each of which charges fees and introduces additional settlement risk. Pre-funding of nostro accounts ties up capital, and opaque FX spreads make it difficult for consumers to understand the true cost of a transfer. These frictions are particularly painful for migrants sending relatively small amounts home, as fixed costs represent a large percentage of the transfer.

Blockchain-based rails attempt to streamline this process by enabling direct, near-instant value transfers that settle on a shared, auditable ledger. Stellar was designed from the outset to serve this role, providing a way to represent different fiat currencies as tokens and move them across borders with transparent fees and deterministic settlement. Instead of maintaining bilateral relationships in every corridor, payment companies can integrate with a small number of anchors and use the Stellar network to handle the routing and settlement between currencies. Stablecoins and tokenized fiat act as the vehicle for value transfer, while local payouts occur through existing banking and payment systems.

This model does not eliminate the need for regulation or compliance; on the contrary, it places anchors at the center of KYC and AML processes. However, it can reduce the number of intermediaries involved in each transfer and make FX conversion more competitive by leveraging onchain orderbooks and stablecoin liquidity. For many corridors, especially those involving emerging markets, the ability to avoid pre-funding multiple currencies and correspondent banks can materially improve the economics of remittances.

Cross-Border Flows on Stellar Today

On Stellar, cross-border payments typically follow a pattern where a user’s local currency is converted into a stablecoin or tokenized representation, routed across the network, and then converted into the recipient’s currency at the destination. The process can be orchestrated using Stellar’s path payment operation, which allows a sender to specify the maximum amount they are willing to spend in their asset and the minimum amount the recipient should receive in theirs. Along the way, the protocol automatically finds conversion paths through orderbooks and liquid assets, which may include XLM and stablecoins like USDC or MGUSD.

The network’s cross-border capabilities are not limited to consumer remittances. Institutional flows, such as treasury transfers between subsidiaries or wholesale FX settlements, can also benefit from the same infrastructure. For example, a fintech operating in multiple countries might hold working capital in USDC on Stellar and use it to fund local disbursements via anchors, managing FX exposure more dynamically than with pre-funded bank accounts. The low transaction fees and relatively fast settlement make such flows operationally feasible, though institutions must still weigh custody, regulatory, and counterparty considerations.

Stellar’s role in cross-border payments is also reinforced by partnerships with large money transfer operators. MoneyGram’s decision to issue MGUSD on Stellar reflects a strategy of integrating blockchain rails into its existing network rather than replacing it. Users can potentially send MGUSD across Stellar and cash out through MoneyGram’s global distribution network, effectively turning any MGUSD-compatible wallet into an interface for cross-border transfers funded and settled in tokenized dollars. As other remittance providers experiment with stablecoins on different chains, Stellar’s ability to offer both onchain settlement and regulated off-ramps will be a key differentiator.

Anchors, Corridors, and Institutional Partnerships

The success of cross-border payments on Stellar ultimately depends on the depth and reliability of its anchor network. Each corridor requires at least one anchor on both the sending and receiving side that can handle fiat deposits and withdrawals. Anchors must maintain sufficient liquidity, manage FX exposures, and comply with local regulations, which is why Stellar’s institutional outreach emphasizes partnerships with regulated financial institutions and payment companies. The network’s formal documentation and SEPs provide standardized ways for anchors and wallets to interoperate, reducing integration friction.

Institutional partnerships extend beyond remittance firms. On the capital markets side, the integration of Stellar into DTCC’s tokenization service shows how the network can support tokenized securities while maintaining investor protections and entitlements equivalent to traditionally held assets. In this context, Stellar serves not just as a payment rail but as a settlement and record-keeping layer for securities that may be traded and settled across multiple chains. This convergence of payments and capital markets infrastructure underscores why network design choices around compliance, asset controls, and governance are critical for institutional adoption.

As major payment networks like Mastercard expand their settlement capabilities to include regulated stablecoins such as USDC, PYUSD, and others, the broader market is shifting toward a world where card transactions and other retail payments can settle onchain, even on weekends and holidays. Although Mastercard’s current stablecoin program spans several networks, the principles it demonstrates—programmable, always-on settlement and interoperability with traditional cards—align closely with Stellar’s long-term vision for payments. In such an environment, networks that can offer both robust stablecoin support and direct institutional connectivity will be well-positioned.

MoneyGram USDC corridor launched on Stellar

Franklin Templeton BENJI tokenized fund goes live on Stellar

Societe Generale-FORGE deploys EURCV euro stablecoin on Stellar

- 2025-11milestone

CME Group adds Stellar futures, pushing crypto futures market cap coverage past 75%

Circle expands CCTP to Stellar as domain 27 across 23 chains

DTCC tokenization service connects to Stellar public blockchain

Mastercard expands intraday stablecoin settlement to Stellar network

Quantum Preparedness Plan targets Ed25519 migration, quantum-safe signers by 2027

Stablecoins on Stellar: USDC, MGUSD, and Beyond

Why Stablecoins Matter for Stellar

Stablecoins are digital tokens designed to maintain a stable value relative to a reference asset, most commonly a national currency such as the U.S. dollar. On Stellar, fiat-backed stablecoins play a crucial role in bridging traditional financial systems and onchain settlement. They allow users and institutions to hold and transfer dollar or euro exposure without dealing with the volatility of cryptocurrencies such as XLM, while still benefiting from the speed, transparency, and programmability of blockchain transactions. For cross-border payments, stablecoins can serve as a neutral settlement asset between different local currencies, reducing FX complexity and pre-funding requirements.

Stellar’s architecture is particularly well-suited to stablecoins because it treats them as first-class assets issued by regulated entities, with clear mechanisms for trustlines, asset controls, and redemption. Anchors and issuers can configure their tokens to support features such as freeze, clawback, and KYC-enforced access, which are often mandated in regulated contexts. This makes the network attractive not only to crypto-native stablecoin issuers but also to traditional financial institutions considering launching tokenized deposits or fund shares. In practice, much of the network’s activity is likely to center on a handful of high-quality, fully backed stablecoins that carry strong legal and regulatory assurances.

At the same time, a stablecoin-centric ecosystem introduces new dependencies and risks. The stability of onchain payments and DeFi protocols built on Stellar will increasingly depend on the risk management practices of stablecoin issuers and the regulatory regimes under which they operate. This is why understanding the specifics of major stablecoins on Stellar—such as USDC and MGUSD—is essential for assessing the network’s long-term resilience.

USDC on Stellar and Circle’s CCTP Integration

USDC is a fully reserved digital dollar stablecoin issued by Circle, backed by high-quality liquid assets such as cash and short-term U.S. Treasuries. When deployed on Stellar, USDC can function as a digital representation of a U.S. dollar deposit, enabling onchain transfers and programmable payments while preserving a clear 1:1 redemption path into the traditional banking system. Circle and Stellar emphasize that using USDC on the network can help reduce pre-funding and counterparty risk in cross-border flows, since value can be moved and settled in real time rather than relying on dormant nostro accounts.

A significant recent development is the integration of Circle’s Cross-Chain Transfer Protocol (CCTP) with Stellar. CCTP is designed to allow users and applications to move USDC natively across supported blockchains by burning tokens on the source chain and minting an equivalent amount on the destination chain. With Stellar now supported as domain 27 within CCTP, developers can programmatically move USDC between Stellar and other networks such as Ethereum or various rollups without relying on third-party token bridges. The integration introduces considerations specific to Stellar’s address format and contract environment, which are addressed through components like the CctpForwarder contract.

From a strategic standpoint, CCTP support reinforces Stellar’s role as part of a multi-chain stablecoin ecosystem rather than an isolated environment. Applications can choose the network that best suits their needs for a given workflow, moving USDC onto Stellar when they require low-cost payments or anchor connectivity and off of it when they need access to DeFi protocols or users on other chains. However, this cross-chain mobility also introduces additional risk surfaces, as failures or exploits in CCTP-integrated systems could propagate across networks. That is why robust risk management and careful contract design are critical for both Circle and Stellar-aligned developers.

MoneyGram’s MGUSD: Onchain Dollars with Off-Chain Reach

MGUSD is MoneyGram’s own U.S. dollar stablecoin, launched to power its global network of payment services and initially deployed on Stellar. The token is minted and burned using smart contract infrastructure provided by M0, an onchain platform for issuing fully collateralized tokens, with MGUSD issued on Stellar at launch. MoneyGram holds the underlying fiat reserves backing MGUSD, positioning the token as a representation of a claim on funds custodied by one of the world’s largest money transfer companies. This structure allows MoneyGram to integrate MGUSD into its existing compliance and treasury systems while exposing the token to Stellar’s onchain ecosystem.

The strategic logic of MGUSD is to combine the reach of MoneyGram’s global cash-out and bank payout network with the efficiency of onchain settlement. Users can potentially receive MGUSD in a wallet, send it across Stellar, and then cash out at a MoneyGram location or partner bank, effectively enabling global transfers mediated by a tokenized dollar. For MoneyGram, MGUSD also provides a programmable settlement asset for internal and B2B flows, allowing the firm to manage liquidity across corridors more dynamically. The choice of Stellar aligns with the network’s focus on cross-border payments and anchors, as well as its low transaction fees and built-in asset support.

However, MGUSD also illustrates some of the key risks and constraints inherent in stablecoin-based payments. Users must trust MoneyGram’s reserve management, regulatory compliance, and operational resilience, and any issues affecting the company could spill over into MGUSD’s stability. The token’s usability also depends on the breadth of wallet and protocol integrations on Stellar and potentially other chains if MGUSD becomes multi-chain over time. For regulators and policymakers, MGUSD is part of a broader trend in which traditional financial institutions issue their own stablecoins, raising questions about competition, consumer protection, and systemic risk.

Mastercard Settlement, DTCC Tokenization, and Institutional Stablecoin Flows

The growing use of regulated stablecoins by mainstream financial infrastructure providers underscores the strategic importance of networks like Stellar. Mastercard, for example, has announced plans to expand its settlement capabilities to include on-chain card settlement using regulated stablecoins such as Circle’s USDC, as well as Paxos-issued stablecoins like PYUSD, USDG, and USDP, Ripple’s RLUSD, and SoFiUSD. These stablecoins will be enabled across a range of supported blockchain networks, illustrating how card networks are experimenting with programmable, always-on settlement outside the constraints of banking hours. This development reflects a convergence between stablecoin-based payments and traditional card rails.

In parallel, DTCC’s integration of its tokenization service with Stellar illustrates how tokenized securities and stablecoins may coexist on the same network. DTCC has stated that DTC-tokenized assets will have the same investor protections, entitlements, and safeguards as traditionally held securities, and that Stellar connectivity is part of a broader multi-chain strategy for its digital assets and tokenization initiatives. In this context, stablecoins on Stellar can serve as settlement assets or collateral for tokenized securities transactions, while the network itself provides the ledger for ownership records and corporate actions. This arrangement situates Stellar within the evolving architecture of onchain capital markets.

For institutional users, these developments raise both opportunities and challenges. On the one hand, stablecoins like USDC and MGUSD offer a way to move value quickly between different parts of the financial system, from card networks and remittance providers to tokenized securities platforms. On the other hand, the growing interconnectedness increases the importance of robust risk management, transparency, and regulatory oversight, as problems in one part of the stablecoin ecosystem could propagate through multiple infrastructure layers. Stellar’s emphasis on compliance, anchor standards, and institutional partnerships is partly a response to this complexity.

Stablecoin Risks and Limitations

While stablecoins can improve payment efficiency and broaden access to digital dollars, they also pose distinct risks that must be understood in the context of Stellar’s strategy. Analysts such as the Bank Policy Institute have highlighted how even fully backed stablecoins can create vulnerabilities for retail investors, borrowers, lenders, and the broader financial system. For example, if stablecoin issuers rely on short-term funding or hold reserves in instruments that become illiquid during stress, they may face run risk as users rush to redeem. The need to liquidate reserves quickly can exacerbate market stress, particularly in Treasury or money market instruments.

Stablecoins also raise regulatory and legal questions, including how redemption rights are structured, what protections exist in insolvency, and how stablecoin activities intersect with banking and securities regulation. Inconsistent or incomplete regulation can leave users exposed to counterparty risk that is not immediately apparent from onchain behavior. Additionally, the rise of cross-chain stablecoin transfer protocols like CCTP introduces operational and smart contract risks, as bugs or exploits in the bridging logic can lead to losses or disruptions even if the underlying reserves remain intact. For networks like Stellar that rely heavily on stablecoins for payments and tokenization, these systemic risks cannot be ignored.

Another limitation is that stablecoin-based payments still depend on off-chain infrastructure for key functions such as KYC, AML, and access to the banking system. Anchors and issuers may face regulatory changes that constrain their ability to serve certain markets or user segments, which can fragment stablecoin liquidity and reduce the network effects that make stablecoins effective settlement assets. For developers and institutions building on Stellar, a realistic assessment of these risks is essential when designing products that rely on USDC, MGUSD, or other stablecoins as core components.

Tokenization and Real-World Assets on Stellar

Asset Issuance Model and Tokenization Mechanics

Tokenization refers to the process of representing ownership or claims on real-world assets—such as cash deposits, securities, or funds—using digital tokens on a blockchain. Stellar’s core design has always supported the issuance of arbitrary assets by any account, which makes it a natural platform for real-world asset (RWA) tokenization. Issuers create an asset by defining a code and setting themselves as the issuing account, while other users establish trustlines and hold balances of that asset. Depending on the asset type and regulatory requirements, issuers can configure controls like freezing, clawback, and authorization flags.

Stellar’s official materials emphasize that the network is designed to tokenize real-world assets in a secure, compliant, and global manner, with tooling and standards that help institutions meet their obligations. Issuers can use account-level flags to restrict who can hold or trade an asset, implement blacklists or whitelists, and integrate KYC processes via anchors and SEPs. These features make Stellar attractive for tokenizing not only stablecoins but also fund shares, private credit instruments, or other financial products where investor eligibility and transfer restrictions are critical.

The tokenization model also leverages Stellar’s built-in DEX and path payments. Once an asset is issued, it can be listed in orderbooks against stablecoins, XLM, or other tokenized instruments, allowing secondary market trading within the constraints set by the issuer. For regulated securities, this might involve restricting trading to KYC’d counterparties or specific jurisdictions. For more open assets, such as tokenized commodities or public fund shares available to retail investors, liquidity can be broader. In all cases, tokenization on Stellar aims to preserve the legal rights and protections associated with the underlying asset, rather than creating purely synthetic representations.

DTCC Integration and Tokenized Capital Markets

The integration between Stellar and DTCC’s tokenization service is a landmark development for the network’s role in capital markets. DTCC, a central player in U.S. securities infrastructure, has announced that its tokenization service will connect to the Stellar public blockchain as part of a multi-chain strategy. In this arrangement, DTC-tokenized assets will have the same investor protections, entitlements, and safeguards as traditionally held securities, while Stellar connectivity provides one of the rails for tokenized holdings and transactions. This combination suggests a future where major securities, such as components of the Russell 1000 index, ETFs, or U.S. Treasuries, could be represented on Stellar under DTCC’s custodial umbrella.

For Stellar, being chosen as a connectivity layer for a systemically important market infrastructure provider signals confidence in its technical design and governance. DTCC’s cautious approach to tokenization, which includes maintaining investor protections and managing onchain risks carefully, aligns with Stellar’s compliance-focused ethos. It also positions the network to support institutional-grade tokenization use cases, where issuers and asset managers expect robust legal frameworks and operational resilience. In such scenarios, Stellar’s features—such as asset controls, anchor standards, and Soroban smart contracts—can be used to model corporate actions, interest payments, and other lifecycle events.

This integration does not mean that all securities activity will migrate to Stellar, nor that tokenized assets will be freely tradable in DeFi protocols. Rather, it illustrates a hybrid model where traditional custodians and market infrastructures leverage blockchain rails to improve transparency, settlement efficiency, and programmability, while keeping regulatory and investor protection frameworks intact. Within that model, Stellar is one of several networks providing connectivity, and its ongoing relevance will depend on security, performance, and the richness of its institutional ecosystem.

Compliance, KYC, and Institutional Controls

A recurring theme in Stellar’s tokenization strategy is the emphasis on compliance and institutional-grade controls. Issuers can require authorization before an account is allowed to hold or trade their asset, implement region-based restrictions, and revoke authorization if needed. Combined with off-chain KYC and AML processes managed by anchors or custodians, this allows tokenized assets to operate within existing regulatory frameworks. For example, a fund manager could tokenize shares of a private credit fund on Stellar while ensuring that only accredited or qualified investors in allowed jurisdictions can hold the tokens.

Soroban smart contracts further expand the range of compliance tools by enabling programmable access controls and dynamic restrictions. Contracts can check attributes associated with an account, such as KYC status or risk scores, before allowing specific operations. They can also model complex workflows like investor onboarding, subscription and redemption processes, or secondary transfers requiring issuer approval. For highly regulated assets, such as tokenized securities under DTCC’s umbrella, these capabilities can be used to codify large parts of the compliance and settlement logic into onchain code, while leaving ultimate control and oversight with regulated entities.

This compliance-oriented design has trade-offs. It may limit the composability of certain tokenized assets with open DeFi protocols or restrict their availability to global retail investors. However, for institutions that view regulatory certainty and investor protection as non-negotiable, Stellar’s approach can be an advantage. It allows them to explore tokenization and stablecoin-based payments without adopting fully permissionless models that might conflict with their obligations. For crypto-native developers and users, this means that Stellar’s RWA ecosystem may look more controlled and institutional than those on some other chains, but potentially more aligned with mainstream financial integration.

Stellar plans quantum-safe signers for all accounts by 2027 as QPP targets Ed25519 risk

Stellar Development Foundation introduced QPP, a roadmap to move the network toward quantum-safe signing without forcing users to abandon existing G-addresses. Soroban contract accounts are slated to get post-quantum signature verification in 2026 via ML-DSA-44 and ML-DSA-65 host functions, while a 2027 protocol upgrade would let every classic account add a quantum-safe signer. The hard part is activation: deprecating Ed25519 could freeze dormant accounts, so SDF is pushing that cutoff into community design and threat-timeline decisions.

Soroban smart contracts are live on mainnet but the ecosystem is nascent; oracle incidents (RedStone's $10M exploit highlighting feed risks) show Stellar DeFi inherits the same composability attack surface as other chains.

The Stellar Development Foundation controls protocol upgrades, the community fund, and a large share of XLM supply, creating meaningful governance concentration even as validator diversity has grown.

Stellar's compliance-first design — built around KYC-compatible stablecoins and regulated partners like Mastercard and Societe Generale — reduces regulatory risk compared to permissionless DeFi chains, though stablecoin reserve and issuer oversight rules remain unsettled globally.

RWA TVL crossing $1B and then $2B is a headline milestone, but thin secondary-market liquidity for tokenized assets on Stellar means large redemptions face friction if institutional holders exit simultaneously.

Transaction fees and spam-prevention reserves are denominated in XLM, so a sustained price decline can make the network economically unviable for micropayment use cases that define Stellar's core value proposition.

NIST places the practical quantum threat to Ed25519 at 2029 and beyond; Stellar's 2027 quantum-safe signer target gives a meaningful runway, and its key-account separation architecture makes migration less disruptive than chains where account identity is derived directly from the signing key.

Security, Governance, and Quantum Preparedness

Network Governance and the Role of the Stellar Development Foundation

Stellar’s governance is a blend of open-source development, community input, and leadership by the Stellar Development Foundation. The SDF coordinates protocol upgrades, ecosystem funding, and strategic partnerships, but it does not control block production in the way that a centralized operator might. Consensus is achieved through the Stellar Consensus Protocol (SCP), which relies on nodes selecting their own quorum slices and reaching agreement without proof-of-work or proof-of-stake. This design aims to provide fast finality and resilience while avoiding some of the centralization concerns associated with delegated staking systems.

Community participation is facilitated through initiatives such as the Stellar Community Fund (SCF), which offers grants to developers and entrepreneurs building on the network. The SCF provides crypto grants in the range of tens to hundreds of thousands of dollars equivalent, supporting DeFi, NFT, and Web3 projects that leverage Stellar and Soroban. Over 656 projects have been funded through the SCF, indicating a broad base of experimental and production use cases across different verticals. The fund’s rounds, such as Round 43 that awarded millions of dollars in XLM to 29 projects, also serve as periodic checkpoints for ecosystem priorities and innovation themes.

Governance also encompasses protocol-level decisions, such as fee changes, new operations, or major upgrades like Soroban and the Quantum Preparedness Plan. These changes are typically proposed, discussed, and refined in public forums, with SDF playing a central role in coordination but ultimately relying on validator adoption to activate changes. For institutional partners, understanding this governance process is important for assessing upgrade risk, backward compatibility, and the predictability of the network’s evolution.

Security Model, Upgrades, and Smart Contract Risk

Stellar’s security model is multifaceted, combining the safety properties of SCP with conservative protocol design and cautious rollout of new features. The classic layer of the protocol includes a limited set of operations whose behavior is well understood and extensively audited, which has historically reduced the likelihood of catastrophic bugs affecting payments or asset balances. Security best practices for anchors and issuers, such as using hardware security modules for key storage and implementing multi-signature controls, are encouraged through documentation and ecosystem standards.

The introduction of Soroban adds a new dimension to the security landscape. Smart contracts inherently increase the attack surface, and vulnerabilities in contract code can lead to loss of funds or systemic disruptions. To mitigate these risks, Soroban’s design employs a sandboxed execution environment, deterministic resource metering, and a curated set of host functions that limit the ways in which contracts can interact with the underlying ledger. Nonetheless, developers must follow secure coding practices, undergo audits, and consider upgrade mechanisms carefully, especially for protocols that will custody user funds or interact with stablecoins and tokenized assets.

Upgrades to the Stellar protocol are handled through well-defined release cycles and network votes, with extensive testing on testnets before mainnet adoption. This process is designed to balance innovation with stability, particularly given the network’s use in regulated contexts and by institutions that require predictable behavior. However, as with any public blockchain, there is no central authority that can unilaterally reverse transactions or roll back the ledger in response to an incident, so ex ante security and risk controls remain paramount.

Quantum Preparedness Plan (QPP) and Post-Quantum Signatures

One of Stellar’s more forward-looking initiatives is its Quantum Preparedness Plan (QPP), which addresses the risk that future quantum computers could break current cryptographic schemes such as Ed25519 signatures. The QPP lays out a multi-stage roadmap for migrating the network to quantum-safe cryptography, with an emphasis on minimizing disruption and preserving account identities. This plan is notable because NIST and other authorities have indicated that the quantum threat to today’s widely deployed cryptography may become more acute in the 2030s, and every blockchain will eventually need a migration strategy.

In Stage 1 of the QPP, scheduled for 2026, Stellar plans to add post-quantum signature verification to Soroban as native host functions, supporting ML-DSA-44 and ML-DSA-65, which are enterprise-grade NIST signature standards. With these primitives in place, contract accounts can implement quantum-safe authentication through Soroban’s account abstraction layer, without requiring protocol-level changes to classic accounts. This means that enterprise wallets and high-value users can begin migrating to quantum-safe contract accounts as early as 2026, well before a hard cutoff is required.

Stage 2, targeted for 2027, involves protocol-level enshrinement of quantum-safe signer types as first-class signers on classic accounts. A Core Advancement Proposal will introduce these new signer types, allowing every existing account to add a quantum-safe signer alongside its existing Ed25519 key using standard operations. Importantly, this migration model does not require creating a new account type, changing addresses, or migrating balances; instead, it allows wallets, SDKs, and anchors to gradually update to support quantum-safe key generation, signing, and verification. Stage 3 contemplates eventual deprecation of Ed25519 for new transaction authorization, with timing determined by the actual progress of quantum computing and ecosystem readiness.

A key advantage of Stellar’s design in this context is the separation between account identity and signing keys. Because account addresses are not tightly bound to a specific cryptographic scheme, it is possible to update signer types without forcing users to abandon their existing account identifiers. This contrasts with some systems where account addresses are directly derived from public keys that would need to change in a post-quantum world. For institutions and long-term asset holders, the QPP offers a credible path to maintaining security over multi-decade horizons, which is particularly important for tokenized securities, long-duration bonds, and other assets that may remain on-chain for extended periods.

Ecosystem, Funding, and Developer Experience

Stellar Community Fund and Ecosystem Growth

The Stellar Community Fund (SCF) is a central mechanism through which the ecosystem supports new projects, infrastructure, and applications. The SCF offers grants ranging from roughly 15,000 to over 150,000 dollars’ worth of crypto to teams building DeFi, NFT, and Web3 projects on Stellar, including those targeting Soroban smart contracts. According to official figures, more than 656 projects have been funded through the SCF, covering a wide range of use cases and contributing to the network’s diversity and resilience. These grants often support early-stage experimentation that might not yet be commercially viable but could lay the groundwork for future institutional or mainstream adoption.

Recent SCF rounds have highlighted themes such as onchain payments, stablecoin infrastructure, wallet experiences, and tools for anchors and compliance. For example, Round 43 awarded approximately 3.139 million dollars’ worth of XLM to 29 projects across multiple tracks, reflecting an emphasis on both Soroban-native applications and improvements to the classic payments stack. Demo days and ecosystem showcases provide visibility for these projects, allowing institutional partners, developers, and the broader community to track innovation trends and identify potential collaborators.

Beyond direct funding, the SCF serves as a signal of ecosystem priorities and the maturity of different verticals. The increasing share of Soroban-related grants, for instance, suggests a deliberate push to expand the network’s programmable finance capabilities. At the same time, continued support for anchors, wallets, and off-ramp tooling underscores Stellar’s original focus on real-world financial connectivity. For developers considering where to build, the presence of a structured, recurring grant program can make Stellar a more attractive option compared with chains where ecosystem funding is less organized or more ad hoc.

Tooling, SDKs, and Onboarding Developers

Developer experience is a critical factor in the long-term viability of any blockchain ecosystem. Stellar offers official documentation, SDKs in multiple programming languages, and reference implementations for common patterns such as asset issuance, anchor integrations, and Soroban contracts. The Soroban developer documentation, in particular, provides an overview of the smart contract platform, its integration into the existing Stellar blockchain, and the Rust-based development model. This documentation is complemented by guided tutorials, code examples, and testing frameworks that help developers get started with contract deployment and interaction.

On the classic side, Stellar provides strongly defined ecosystem standards (SEPs) that specify how wallets, anchors, and other services should interoperate. These standards cover areas such as deposit and withdrawal flows, KYC data exchange, and cross-border payment APIs. For developers building wallets or payment applications, adhering to SEPs can dramatically reduce integration work and ensure compatibility with a broad range of anchors and stablecoin issuers. For institutional partners, the existence of these standards simplifies due diligence and technical assessments.

The combination of Soroban and classic Stellar operations also offers developers a layered approach to application design. Simple payment flows and asset transfers can rely entirely on classic operations, minimizing complexity and cost, while more complex logic can be implemented in Soroban contracts where necessary. This flexibility allows teams to match the complexity of their implementation to the requirements of their use case, rather than forcing everything into a one-size-fits-all contract environment. Over time, as tooling matures and best practices emerge, this hybrid model may prove to be one of Stellar’s differentiating strengths.

Comparing Stellar to Other Payment-Focused Networks

In the broader landscape of payment-focused blockchains, Stellar competes and collaborates with networks such as Ripple’s XRP Ledger, various stablecoin-oriented layer-1s, and high-throughput general-purpose chains. While a detailed comparison is beyond the scope of this explainer, a few high-level distinctions are relevant. Stellar’s emphasis on open, public infrastructure combined with compliance-oriented asset controls sets it apart from more walled-garden or consortium-based architectures. Its anchor model and SEPs provide standardized ways to connect to banks and payment systems, which can be more flexible than relying on a small number of centralized gateways.

At the same time, Stellar must contend with the rapid growth of stablecoins and tokenization on other chains, particularly those with large DeFi ecosystems and deep liquidity. For example, stablecoin-based remittances and cross-border payments are also being built on networks like Solana, where Western Union has launched its USDPT stablecoin, and on Ethereum scaling solutions used by card networks and fintechs. Stellar’s differentiation rests less on being the only network capable of supporting stablecoins and more on offering a tailored combination of low fees, institutional integrations, compliance-friendly asset models, and a clear roadmap for long-term security and post-quantum readiness.

From a developer’s perspective, the choice between Stellar and other payment-focused chains often hinges on the specific corridors, partners, and regulatory regimes involved. Projects that require deep integration with MoneyGram’s MGUSD flows, DTCC tokenization, or specific anchors may find Stellar particularly compelling. Conversely, those seeking immediate access to large DeFi liquidity pools or certain NFT communities may gravitate toward other ecosystems. The reality is that many sophisticated applications will operate across multiple chains, using Stellar where its strengths in payments and compliance are most valuable and relying on other networks for complementary features.

Key Risks and Critiques

Technical and Operational Risks

Despite its focus on reliability and institutional use cases, Stellar is not immune to technical and operational risks. The SCP consensus mechanism, while designed for resilience and safety, depends on the correct configuration of quorum slices and the honest behavior of validators. Misconfigurations or concentrated control among a small group of validators could, in theory, undermine liveness or decentralization. While there have been no widely publicized catastrophic failures of SCP, ongoing monitoring and governance vigilance are required to maintain network health.

The introduction of Soroban significantly expands the potential attack surface. Smart contract vulnerabilities, mispriced gas costs, or unexpected interactions between Soroban and classic operations could lead to incidents affecting user funds or network stability. As with other smart contract platforms, there is a risk that early DeFi protocols on Soroban may be exploited due to coding errors or design flaws. The presence of regulated stablecoins and tokenized assets adds stakes to these risks, as a hack involving USDC or MGUSD pools on Soroban-based DeFi could have repercussions beyond the crypto-native community.

Operationally, anchors and stablecoin issuers represent potential single points of failure for specific corridors and assets. If an anchor experiences technical outages, regulatory sanctions, or financial distress, users may temporarily or permanently lose access to deposit and withdrawal channels for the associated tokens. While the network itself would continue operating, the real-world utility of affected assets could be severely impaired. This dependency on off-chain entities is not unique to Stellar but is particularly salient in an ecosystem so focused on real-world payment flows.

Regulatory and Policy Uncertainties

Regulatory uncertainty is a pervasive challenge for all public blockchains, and Stellar is no exception. Questions remain about how different jurisdictions will classify native tokens like XLM, stablecoins such as USDC and MGUSD, and tokenized securities issued on public networks. In some markets, regulators may require stablecoin issuers and anchors to hold banking licenses or adhere to bank-like prudential standards, which could limit the number of entities able to participate. In others, restrictions on cross-border data flows and KYC requirements may complicate the operation of global anchor networks.

In the United States, debates around legislative proposals such as the Clarity Act highlight the tension between regulatory clarity and innovation. Stellar’s leadership has suggested that while clearer rules would be helpful, tokenization and onchain payments are not entirely contingent on a specific legislative outcome, especially given the network’s global reach. However, for institutions subject to U.S. oversight, the evolution of stablecoin and securities regulation will materially affect their willingness to deploy significant assets on Stellar or any other public chain. This is particularly relevant for initiatives like DTCC’s tokenization service, which must operate within a strictly regulated environment.

Cross-border regulatory fragmentation presents another layer of complexity. Anchors operating in different jurisdictions face diverse licensing, reporting, and compliance requirements, which must be harmonized or at least made interoperable at the application layer. Divergent approaches to data privacy, sanctions, and consumer protection can increase the cost and complexity of building global payment solutions on Stellar. For the network to realize its full potential as a neutral payment rail, ongoing dialogue with regulators, clear standards, and robust compliance tooling will be essential.

Systemic and Market Structure Risks around Stablecoin-Based Payments

The increasing reliance on stablecoins as settlement assets in payment systems and capital markets raises systemic concerns. Analysts have noted that even fully backed stablecoins can transmit stress into underlying markets if mass redemptions force issuers to liquidate large volumes of reserves quickly. If stablecoins become deeply integrated into payment networks, remittance flows, and card settlement systems, disruptions in a major stablecoin could have knock-on effects for merchants, consumers, and financial institutions. Stellar’s alignment with regulated stablecoins like USDC and MGUSD may mitigate some risks but does not eliminate them.

Market structure is also evolving in ways that may concentrate power in the hands of a few large stablecoin issuers and infrastructure providers. If most onchain payments and tokenized asset settlements rely on a small number of dollar stablecoins, then the issuers of those tokens, and the banks holding their reserves, become critical nodes in the financial system. This concentration could raise competition concerns and make it harder for smaller issuers, alternative currencies, or decentralized stablecoin designs to gain traction. For a network like Stellar that aspires to support a diverse set of assets and anchors, maintaining openness and interoperability will be an ongoing challenge.

Finally, there is a risk that enthusiasm for tokenization and stablecoin-based payments could lead to projects that are technologically impressive but economically or socially marginal. As some industry participants have noted, tokenizing assets “just to tokenize” is unlikely to create lasting value; tokenization must solve concrete problems, such as improving liquidity, transparency, or access, to be worthwhile. Stellar’s alignment with institutions like DTCC and MoneyGram suggests an emphasis on substantive use cases, but developers and policymakers will need to remain critical and discriminating as the ecosystem grows.

Conclusion and Outlook

Stellar occupies a distinctive position in the evolving landscape of blockchain-based finance. Built from the ground up as a payments-first network, it has gradually expanded to support sophisticated smart contracts, regulated stablecoins, and institutional tokenization while retaining a focus on compliance, low fees, and real-world connectivity. Partnerships with firms like MoneyGram and DTCC, along with the deployment of stablecoins such as USDC and MGUSD, illustrate how Stellar is being woven into the fabric of cross-border payments and capital markets. At the same time, initiatives like the Quantum Preparedness Plan show an awareness of long-term security challenges and a proactive approach to preserving trust in the network’s cryptographic foundations.

The outlook for Stellar will depend on several interlocking factors. The continued maturation of Soroban and the growth of a robust ecosystem of DeFi and programmable payments applications will shape how attractive the network is to developers and users seeking more than basic transfers. The depth and resilience of the anchor network, along with the success of institutional stablecoins and tokenization efforts, will determine whether Stellar can become a standard rail for cross-border payments and onchain settlement at scale. Regulatory developments around stablecoins, securities, and public blockchains will influence how quickly and extensively banks, asset managers, and payment processors are willing to build on Stellar’s public infrastructure.

In the broader competition among payment-focused chains, Stellar’s strengths lie in its combination of institutional partnerships, compliance-aware design, and a clear roadmap for long-term security. Its challenges include differentiating itself in a crowded stablecoin and tokenization landscape, managing the risks introduced by cross-chain interoperability and smart contracts, and maintaining decentralization and openness while accommodating regulatory demands. For crypto-native users, Stellar offers a way to interact with regulated dollars and tokenized assets in a low-cost, programmable environment. For institutions, it presents a path to bring existing financial products and payment flows onchain without abandoning the safeguards and controls that underpin today’s markets. How successfully Stellar navigates these trade-offs will determine its role in the next decade of digital finance.

Latest Stellar news

Alchemy brings Stellar ecosystem to its platform, enabling builders to scale RWA platforms, cross-border payments, and financial apps with enterprise integrationsCircle expands CCTP to Stellar, enabling developers and institutions to move USDC across 23 blockchains using canonical burn-and-mint infrastructureStellar plans quantum-safe signers for all accounts by 2027 as QPP targets Ed25519 riskMoneyGram and Stellar extend partnership to scale global stablecoin adoption, expanding USDC-powered cash on/off-ramps and app balances across Latin AmericaStellar CMO urges crypto to abandon hype cycles for “get rich slow” mindset, emphasizing long-term value creation as key to mainstream trustCME Group says crypto futures suite now covers over 75% of total market cap after adding Cardano, Chainlink, and Stellar contractsSources

- https://stellar.org

- https://blog.bitpanda.com/en/what-stellar-xlm-guide-stellar-network-and-its-stablecoin-ecosystem

- https://x.com/circle/status/2067721402095206425

- https://www.prnewswire.com/news-releases/moneygram-launches-mgusd-a-stablecoin-to-power-its-own-global-network-302787799.html

- https://www.mastercard.com/us/en/news-and-trends/press/2026/june/mastercard-expands-settlement-capabilities-to-include-stablecoin.html

- https://www.dtcc.com/news/2026/may/27/tokenization-service-to-connect-with-stellar-public-blockchain-as-dtc-advances-multi-chain-strategy

- https://communityfund.stellar.org

- https://stellar.org/blog/foundation-news/introducing-the-quantum-preparedness-plan

- https://stellar.org/learn/what-are-stablecoins

- https://stellar.org/use-cases/tokenization

- https://stellar.org/learn/cross-border-payments

- https://developers.stellar.org/docs/build/smart-contracts/overview

- https://stellar.org/learn/lumens

- https://bpi.com/stablecoin-risks-some-warning-bells/

- https://www.youtube.com/watch?v=v8Z77ZWCfkc

- https://www.facebook.com/Innovationvillage/posts/moneygram-launches-mgusd-stablecoin-on-stellarglobal-payments-company-moneygram-/1753637176194078/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…