Deep explainer on crypto apps: how exchange, wallet, DeFi, gaming, AI and “superapps” front-end onchain finance, balance custody and UX, rely on banks and stablecoins, and face growing security and regulatory pressures.

+84 sources across the wider coverage universe

Tempo releases Accounts SDK enabling passkey-based wallets with 1-line integration, bringing Face ID logins, transaction simulation, and gas sponsorship to apps2026-04

Tempo releases Accounts SDK enabling passkey-based wallets with 1-line integration, bringing Face ID logins, transaction simulation, and gas sponsorship to apps2026-04 OpenAI mandates macOS app updates after Axios supply chain attack exposes code signing certificates2026-04

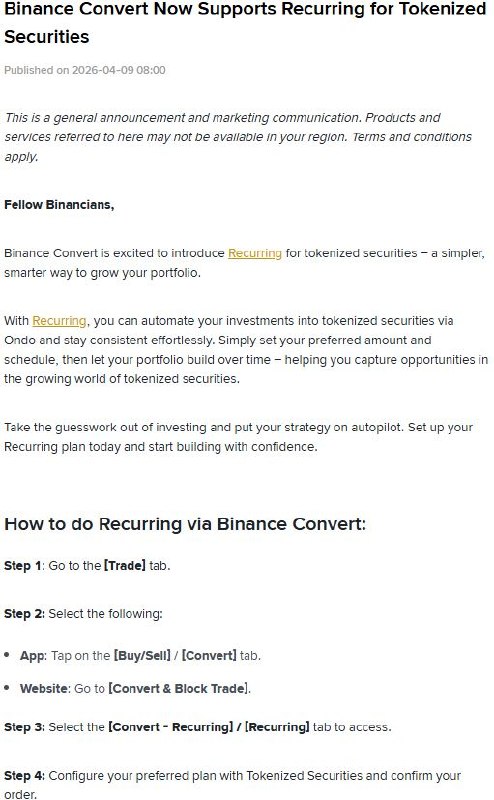

OpenAI mandates macOS app updates after Axios supply chain attack exposes code signing certificates2026-04 Binance Convert adds recurring buys for Ondo tokenized securities across app and web2026-04

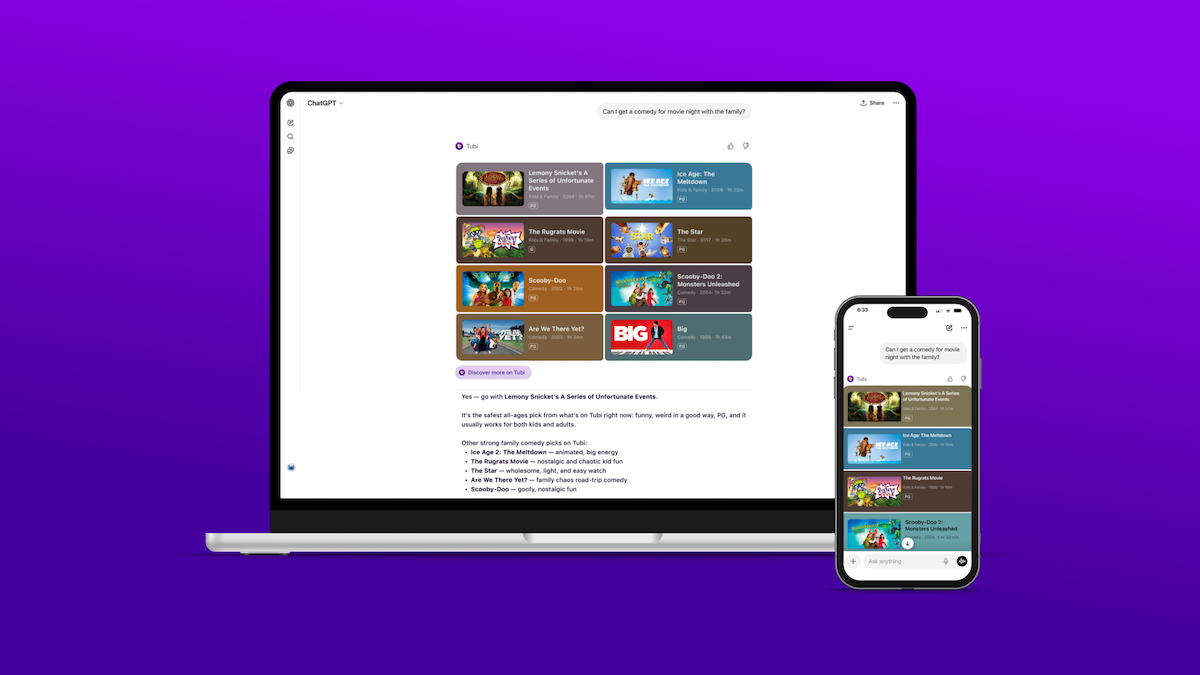

Binance Convert adds recurring buys for Ondo tokenized securities across app and web2026-04 Tubi becomes first streamer to launch native app inside ChatGPT, unlocking discovery across 300K+ movies and TV episodes2026-04

Tubi becomes first streamer to launch native app inside ChatGPT, unlocking discovery across 300K+ movies and TV episodes2026-04 Nansen integrates MoonPay fiat on-ramp, enabling seamless in-app crypto purchases via card, Apple Pay, and Google Pay without leaving platform2026-04

Nansen integrates MoonPay fiat on-ramp, enabling seamless in-app crypto purchases via card, Apple Pay, and Google Pay without leaving platform2026-04 Polymarket launches $5M bug bounty on Cantina, exposing full-stack prediction market infra including smart contracts, oracles, and web app to security researchers2026-04

Polymarket launches $5M bug bounty on Cantina, exposing full-stack prediction market infra including smart contracts, oracles, and web app to security researchers2026-04

In digital finance, an app is the primary interface through which everyday users encounter blockchains, tokens, and onchain services. In crypto, the term covers everything from centralized exchange portals to non-custodial wallets, DeFi dashboards, NFT games, AI-powered agents, and increasingly, “superapps” that try to bundle all of those functions into a single experience.

Apps in Crypto: How Software Became the Front Door to Onchain Finance

Apps sit at the center of the modern crypto experience, shaping how people discover markets, move money, and interact with onchain protocols. While blockchains provide a neutral, open infrastructure for digital value, most users never touch that infrastructure directly. Instead, they tap, swipe, and scroll through mobile and web applications that abstract away key management, transaction formatting, and protocol complexity. These apps have evolved from simple price trackers into multi-service platforms that offer trading, stablecoin payments, NFTs, tokenized stocks, AI agents, private DeFi, and yield strategies—all while competing on user experience, regulatory coverage, and security. At the same time, concentration of activity inside a handful of major apps raises concerns about centralization, app store gatekeeping, malware, and the ethics of promotion. Understanding what “app” really means in a crypto context is increasingly essential for making sense of how the next phase of onchain finance will be built, governed, and used.

What “App” Means in a Crypto Context

From generic software to the crypto “front end”

In general computing, an application is simply software that helps users perform tasks on a device or over the internet. Crypto apps are no different at a technical level, but their purpose is more specific: they provide a human-friendly front end to cryptographic networks that were never designed for mainstream users. A blockchain like Bitcoin or Ethereum can be accessed using raw command-line tools, but the vast majority of people interact with these networks via mobile apps, browser extensions, and web dashboards that bundle many services into a familiar, account-based environment. Cryptocurrency itself is typically defined as a digital payment system that uses cryptography and peer-to-peer networking to validate transactions without relying on banks or traditional intermediaries. Crypto apps translate that fairly abstract idea into actions like “buy,” “send,” “stake,” or “borrow” that users can perform with a tap.

In crypto media and product marketing, the word “app” often serves as shorthand for an entire service stack. A single app can incorporate fiat onramps, KYC verification, trading interfaces, custody, DeFi integrations, NFT galleries, social feeds, and customer support. That differs from the more modular architecture of early Web3, where “dapps” were lightweight front ends pointing at one or two smart contracts, and users stitched their own workflows together across multiple sites and wallets. Today’s “all-in-one money apps” promise to collapse that complexity into a single login. Examples range from App Store offerings like Bolt, which markets itself as a secure all-in-one finance app for sending, receiving, and spending digital value in one place, to more crypto-native entrants that combine wallets, trading, and rewards under one brand.

Apps also mediate the relationship between user devices and remote infrastructure. A mobile trading app is more than just a set of screens; it also coordinates calls to backend services that query order books, route trades, or assemble onchain transactions. The rise of cloud services, API-driven markets, and managed custody means that an “app” can be only the visible tip of a much larger architecture, yet for users it remains the single point of contact. This concentration of functionality reinforces why app design, performance, and reliability are central to how crypto is perceived and adopted.

Apps, dapps, and protocols: clarifying the stack

Crypto discourse often blurs the lines between “app,” “dapp,” and “protocol,” but they describe different layers of the stack. A protocol is a set of rules implemented in smart contracts or consensus mechanisms that define how a network behaves—for example, the ERC-20 standard for fungible tokens or the logic of a lending pool contract. A dapp (decentralized application) is a user-facing interface that interacts directly with such contracts, typically using a non-custodial wallet and letting users sign transactions themselves. By contrast, many mainstream “apps” in crypto are custodial or semi-custodial, where user actions are translated into backend operations that the provider executes on their behalf.

The boundaries are soft. A “DeFi app” might present itself as a neutral dashboard for protocols but also route orders through its own smart contracts or enforce proprietary routing logic. Centralized exchange apps like those from Coinbase or Binance offer access to spot and derivatives markets that are mostly offchain order books, while also providing gateways into onchain features such as staking or L2 withdrawals. Hybrid architectures are becoming common, where an app presents both custodial accounts and integrated onchain services from the same interface. Kraken’s rollout of onchain token trading directly inside its main app is an example: users can now access thousands of Solana-based tokens while still using the same credentials and fiat rails they rely on for centralized spot markets.

For users, the distinction between protocol and app matters because it determines who holds the keys, who controls the rules, and who can change or censor what. A protocol encoded in smart contracts has governance and upgrade processes, but its behavior is transparent and verifiable onchain. An app can change its terms, remove tokens, or alter reward schemes with a backend update. The tension between user-friendly apps and trust-minimized protocols is one of the defining issues of this era of crypto adoption.

Onchain, offchain, and the rise of hybrid apps

One of the most important conceptual divides in crypto is between onchain and offchain activity. Onchain operations are those recorded on a blockchain ledger—for example, sending USDC on Ethereum or swapping tokens on a decentralized exchange. Offchain operations happen in databases controlled by app providers, such as internal ledger transfers between users of a centralized exchange. Apps often mix both types of activity in order to achieve speed, reduce fees, and deliver a smoother experience.

Kraken’s Solana DEX integration illustrates how hybrid architectures are evolving. In this model, the app exposes Solana-based tokens that actually trade via decentralized exchanges, but the user’s entry point is the same interface they use for ordinary spot trades. The app abstracts away network RPC configuration, token verification, and wallet management. Users see estimated tokens, fees, and a guaranteed minimum amount before confirming, but the underlying execution is onchain. Binance has pursued a similar direction with its Binance Wallet and the Binance Alpha interface, encouraging users to trade tokens like ETHGas (GWEI) onchain while still inside the familiar exchange environment.

At the other end of the spectrum, non-custodial apps like Base’s onchain wallet and browser are built from the ground up for direct interaction with smart contracts and NFTs. These apps reinforce the original Web3 model: the app is a thin client that helps users sign transactions, while most of the logic and state live on the blockchain. As app competition intensifies, the question is no longer whether an app is “onchain” or “offchain,” but how it blends the two modes to balance user experience, security, and sovereignty.

Coinbase’s Base app launches desktop web version for trading and payments.

$4.8B in stables and ~$4.1B of DeFi TVL already sit on Base, so desktop Base App is less about screen size than letting Coinbase own the default route from fiat balance to swap, payment, and mini-app. If the web app makes Base accounts feel closer to a brokerage tab than a wallet extension, Uniswap/Phantom/MetaMask lose some top-of-funnel while Base gets cleaner orderflow and payment volume. The tradeoff is obvious: better UX and distribution, but more onchain retail passing through Coinbase’s policy layer before it ever touches a protocol.

Readers click 'App' stories not for feature launches but for access battles: who controls the on-ramp door — Apple, Google, Telegram, or a fraudster — determines whether crypto reaches the next billion users or loses them to a fake app.

Core Building Blocks of a Crypto App

Identity, keys, and custody

Underneath every crypto app lies a fundamental question: who controls the private keys that authorize onchain transactions? In cryptography, a private key is a secret number that proves control over a wallet or account. Losing it means losing access to associated assets. Many non-custodial apps derive keys from a seed phrase, a human-readable list of words that can recreate the keypair. Security practitioners emphasize that seed phrases should be stored offline, encrypted where appropriate, backed up, and never shared in plain text, since anyone with the phrase can drain the wallet.

Despite these best practices, seed phrases remain a major usability and security bottleneck. New users are frequently phished into entering their phrase into fake apps or support chat windows. Devices are lost without backups. Physical storage can be damaged or stolen. Some wallet-focused apps and specialist providers advocate encrypted digital backups, secure physical notebooks, and multi-location redundancy to mitigate these risks. Others avoid exposing seed phrases to users altogether, instead using multi-party computation (MPC), hardware-backed keys, or “keyless” architectures where the app coordinates signature fragments without ever revealing a single point of failure.

Binance’s “Keyless” wallet approach, used in the Binance Wallet and associated Alpha interface, exemplifies this move away from visible seed phrases. In its GWEI trading promotion, Binance explicitly restricts eligibility to trades executed via Binance Wallet (Keyless) or Binance Alpha, highlighting a preference for users to operate inside this managed key environment rather than through third-party dapps. Kraken’s onchain trading rollout likewise abstracts seed management by letting users access Solana DEX markets with no separate wallet or seed phrase workflow at all. These models trade some self-sovereignty for convenience and risk reduction, but they also concentrate trust in the app operator.

Custody is therefore not only a technical but also a legal and regulatory category. When an app holds user keys or maintains an internal ledger, it effectively functions as a financial intermediary, with corresponding obligations and risks. Non-custodial apps, by contrast, position themselves as software providers rather than custodians. The spectrum between those poles—shared custody, MPC, smart contract wallets with social recovery—defines much of the current innovation in wallet apps and onchain accounts.

Networks, tokens, and markets

Crypto apps are gateways to many different networks and asset types. At the base layer are blockchains like Bitcoin, Ethereum, Solana, and newer L2s and appchains. On top of those networks, tokens represent everything from infrastructure governance assets to stablecoins, memecoins, NFTs, and real-world assets. Stablecoins such as USDC function as digital dollars that move on open networks and settle across borders in seconds, offering bank-account-like behavior without the limitations of domestic banking hours. Apps that support USDC and similar tokens can therefore serve as global payment tools, remittance channels, and trading collateral.

Trading-focused apps usually present this complexity as a list of markets rather than a graph of protocols. Users see pairs like BTC/USDC or HYPE/USDC, even if the underlying liquidity is provided by deeply onchain venues. Infinex’s perps app integrating Hyperliquid spot markets is one example of this model: users continue using the same derivatives interface, but now can trade spot pairs sourced from an onchain order book, including high-volume pairs like HYPE/USDC. The SODAX SDK similarly lets app developers expose tokenized stocks such as TSLAx, NVDAx, SPYx, or COINx held natively on Solana, while giving users a familiar “xStocks” market list within their preferred front-end. In both cases, the app is a distribution layer for tokenized exposures that live on specific networks.

As token universes expand, curation and verification become critical app responsibilities. Kraken’s Solana DEX integration launched with nearly 2,500 verified Solana tokens available in its app, including early-stage assets not yet listed on any centralized exchange. That curation shields users from some scams but does not eliminate market risk. Apps must decide which tokens to list, how to signal risk, and how to handle controversial or illiquid assets. For stablecoins, apps must consider issuer risk and regulatory classification, especially when supporting assets used for payroll, lending, or savings.

Markets themselves are not just price charts but also functional building blocks. Apps integrate swaps, perpetual futures, options, NFTs, and credit markets into a cohesive experience. Underneath, each of these market types may rely on different protocols and liquidity models. The choice of networks and tokens an app supports has immediate consequences for latency, fees, and available strategies. That is why many of the latest onchain-first apps build multi-chain support from the start and market themselves as “built to trade and earn” across networks, as Base’s app framing makes clear.

Payments, onramps, offramps, and cards

For most users, apps are where crypto meets traditional money. Onramps let users buy crypto using bank transfers or cards; offramps convert crypto back into fiat or card-based spending. Behind these flows are sponsor banks, card networks, and payment processors that enable apps to bridge between stablecoins, card balances, and bank accounts. Industry observers have noted that sponsor banks previously known for supporting fintech brands like Chime or Cash App could become the backbone of stablecoin adoption, as regulation and demand for tokenized dollars increase. Apps that integrate stablecoins with everyday payments therefore sit on a complex intersection of bank compliance and open networks.

EarnOS offers a good example of this convergence. It positions itself as a platform where users can earn rewards online and get instant payouts in real money, not points or gift cards, with a dedicated Visa card for spending those rewards on everyday purchases. At the same time, EarnOS promotes onchain mechanics behind the scenes, and has raised venture funding from investors like 1kx and Coinbase to build a more “verifiable and rewarding” internet. Such apps rely on stablepayments rails and card issuers to deliver a familiar user experience, while using crypto infrastructure for settlement, rewards, or yield behind the scenes.

Other money apps emphasize peer-to-peer payments, global transfers, and spending in multiple currencies. Bolt’s “crypto superapp” positioning as an all-in-one tool for sending, receiving, and spending digital assets illustrates the competitive push to own not just trading but also everyday financial activity. Yet most of these apps still depend on legacy rails somewhere in the stack. Even crypto neobanks that market themselves as “bankless” often rely on banking partners, card issuers, and centralized payment networks, making them vulnerable to account freezes and policy shifts despite their onchain components. Apps that integrate direct stablecoin rails and permissionless markets may have more resilience, but still operate in a regulatory environment that can change their status abruptly.

Major Categories of Crypto Apps

Exchange and trading apps

Exchange apps are still the primary way most people interact with crypto markets. These include global platforms like Coinbase, Binance, Kraken, and region-specific venues. Their apps usually offer fiat onramps, custodial wallets, spot and derivatives trading, staking services, and market data. Coinbase’s app, for example, lets users buy, sell, convert, send, and store a growing list of assets; new token listings such as the Re (RE) asset are frequently promoted as becoming available on coinbase.com and through the Coinbase app at the same time, reinforcing the app as the default entry point.

Binance’s mobile and web apps have evolved into comprehensive trading environments that increasingly blur the boundary with onchain. The platform’s promotion around ETHGas (GWEI) trading explicitly ties participation in a trading competition to use of its own Binance Wallet (Keyless) and Binance Alpha interfaces, excluding third-party dapps from eligibility. Users interested in the GWEI trading leaderboard must click a “Join” button on the Binance app event page, update their app version, create and back up their Keyless wallet, and then trade GWEI within the app to accumulate valid volume. This structure draws usage toward Binance’s proprietary app ecosystem and demonstrates how trading apps design incentives around in-app behavior.

Kraken’s app, long associated with centralized spot and derivatives markets, is now also an onchain trading interface. The firm has integrated Solana DEX access into its main app, allowing eligible U.S. users and customers in over 100 other countries to trade more than 2,500 Solana-based tokens directly, including many not yet on centralized exchanges. DEX-tradable assets are labeled differently from Kraken-listed tokens, and the order flow exposes estimated tokens, fees, and guaranteed minimums before users confirm. This is a clear instance of a centralized trading app morphing into a hybrid front end for onchain liquidity.

Smaller platforms and specialized venues follow similar patterns. Infinex’s perps app, by integrating Hyperliquid’s onchain order book for spot markets, allows users to trade spot and derivatives in the same UI. Fee rebates, liquidity mining, and trading competitions across these platforms further incentivize trading inside their apps. For a typical retail user, “crypto app” still often means “the exchange app where I bought my first BTC,” but under the hood these are increasingly multi-protocol, multi-chain products.

Wallet and self-custody apps

Wallet apps, in contrast, center around key management and direct onchain interaction. They can be browser extensions, mobile apps, or embedded experiences within other services. Base’s “Built to Trade & Earn” app described in app store listings is framed as a secure onchain wallet and browser that puts users in control of their crypto, NFTs, DeFi activity, and digital assets. By combining wallet functionality with a built-in browser, it acts as both key manager and dapp portal. Users can connect to DeFi protocols, interact with NFTs, and access multiple chains from one interface, while still holding their own keys.

Bolt’s finance app illustrates another variation on the wallet concept. Although marketed as an all-in-one finance app, its ability to send, receive, and spend instantly across crypto and fiat modes makes it function as a hybrid wallet. The app emphasizes security and speed, signaling to users that self-directed transfers and payments are primary use cases rather than only speculation. Other wallets—both open-source and commercial—layer in features like multi-chain support, NFT galleries, and direct integration with DeFi services, all while navigating the trade-off between security and convenience in key management.

One emerging theme is the move toward “super wallets” that act as operating systems for onchain life. These apps aim to integrate trading, DeFi, gaming, and social components while still presenting as a wallet. Base’s app, some versions of Trust Wallet, and other ecosystem-specific wallets are moving in this direction. In parallel, app stores themselves are evolving; platforms like ONE Store, backed by tens of millions of installs, are pitching themselves as game hubs where users can discover, play, and connect, including with blockchain-enabled titles. Crypto wallet and gaming apps built for these stores must satisfy both user expectations and app store policies, adding another layer of gatekeeping to onchain access.

DeFi, lending, and “bankless” money apps

DeFi apps provide interfaces to non-custodial lending, borrowing, swaps, and structured products. At first these were primarily browser-based dashboards built by protocol teams. Today, entire “money apps” exist that market themselves as bank alternatives, where users can deposit stablecoins, earn yield, borrow against their holdings, or participate in governance. Many of these apps still rely on underlying banks and card networks for fiat connectivity, as highlighted in research on how sponsor banks that powered fintech brands like Chime and Cash App could similarly underpin stablecoin adoption. The irony is that some apps marketing “bankless” finance remain dependent on banks behind the scenes.

COTI’s Privacy Portal introduces another layer to DeFi apps: privacy. COTI promotes “Private DeFi on any chain, token, wallet and use case,” with its flagship privacy app powering private lending, payroll, and other DeFi functions. The portal supports live private ERC-20 tokens and positions itself as programmable privacy infrastructure for ERC-20 tokens, trading, NFTs, and AI agents, allowing developers to build applications where specific aspects of transactions are hidden while others remain verifiable. Apps integrating these capabilities could offer users more confidentiality while still preserving compliance and auditability at necessary points, a key challenge for DeFi as it encroaches on traditional financial functions.

EarnOS sits in the adjacent category of “earn apps,” which blend DeFi mechanics with consumer rewards. Its flagship app promises instant payouts in real money, with users able to load earnings onto an EarnOS Visa card for everyday spending. Backed by funding from investors such as 1kx and Coinbase, EarnOS positions itself as an infrastructure for turning online activity into verifiable, spendable earnings. To achieve that, its app needs to handle identity, reputation, reward calculation, and settlement, much of which may involve tokenized incentives and onchain accounting. At the same time, it must remain legible to regulators and merchants, who will see only fiat card charges and fiat settlements.

As DeFi protocols expand into real-world assets, credit scoring, and institutional markets, the apps built on top of them will resemble more traditional financial apps in layout and compliance, but differ in what happens behind the scenes. Yield generation might come from lending stablecoins into onchain markets; collateral might be tokenized treasury bills; and under-collateralized loans might be governed by DAOs. The app, however, will likely present a familiar interface of balances, yields, and repayment schedules.

Gaming, NFT, and social apps

Crypto’s cultural and entertainment layer is dominated by gaming, NFTs, and social apps. These range from NFT marketplace apps to fully onchain games and prediction platforms. A recent example from sports is the Tria app, which introduced “Tria FC” for football season, allowing users to predict World Cup matches, earn bonus points, and compete for prize pools, all inside the app. Such experiences often blend traditional gaming UX with tokenized rewards, leaderboards, and occasionally onchain settlement of winnings, though the users’ view is simply a game interface.

Gaming apps also illustrate the darker side of distribution. A security report from Kaspersky’s Securelist described how attackers exploited Steam’s Workshop platform via Wallpaper Engine, a popular live wallpaper app, to distribute malicious downloads disguised as animated wallpapers. These wallpapers, shared freely by users, contained malware that could steal Steam account credentials, plant backdoors, deploy crypto miners, or even install ransomware, often without obvious signs until damage was done. Some malicious wallpapers launched additional executables that modified system libraries, hijacked active Steam sessions, and sent account data to attacker-controlled servers, enabling the upload of even more malicious wallpapers. While this specific campaign targeted gamers and Steam accounts, the techniques—bundling malware into “application wallpapers,” abusing trusted platforms, and distributing crypto-stealing tools—are directly relevant to the broader crypto app ecosystem, where users regularly download wallet and trading apps from app stores.

On the creative side, studios and infrastructure teams are building tools to integrate agentic workflows, onchain assets, and gameplay. Portal Studio, for instance, is presented as a tool for visualizing agent workflows, with a forthcoming “Portal Nexus” superapp designed to power complex game agents and experiences. By combining AI agents with onchain economies, such apps could allow NPCs or game systems to interact autonomously with DeFi protocols, marketplaces, or governance, while players interface through a traditional game app. Grants programs like Celo’s Prezenti Season 2 explicitly encourage “agentic apps & infra” within their ecosystem, signaling growing interest in applications where AI agents are first-class users of blockchains and DeFi.

NFT and social apps also experiment with identity, reputation, and creator monetization. While many early NFT wallets were bare-bones galleries, newer apps integrate messaging, feed-style content, and offchain data. The overlap with social networks and politics is increasingly visible, as exemplified by controversies over political figures promoting or praising apps to their audiences, raising questions about disclosure, conflicts of interest, and the ethics of such endorsements.

Arc launches open-source stablecoin FX app on testnet, pitching a flagship multi-currency hub for global stablecoin finance

25 bps is already baked into the sample app’s env, so the repo is closer to a monetizable FX checkout template than a toy demo. USDC/EURC/cirBTC on Arc gives Circle a clean wedge into the same stable-swap surface Curve and Uniswap fought over, but with Wallets, CCTP/Gateway, and sub-second USDC-gas settlement bundled at the platform layer. Bullish for fintech distribution; less clean for DeFi purists, because routing, custody, and fee capture sit inside Circle’s stack unless builders deliberately break them back out.

- 01Telegram as Web3 super-app

Multiple high-click headlines show readers tracking whether Telegram's 900M-user base becomes the dominant crypto distribution layer via TON mini-apps, USDT integration, and BNB Chain partnerships.

- 02App store gatekeeping crypto

MetaMask's removal and return, Wallet of Satoshi's US exit, and Apple blocking/allowing crypto apps made readers acutely aware that Apple and Google hold veto power over self-custody.

- 03Fake apps stealing real funds↗

The fraudulent Rabby Wallet ($1.6M stolen) and fake Ledger Live on Microsoft Store (16.8 BTC) revealed that app stores are actively exploited to launder phishing tools as trusted brands.

- 04Mainstream fintech crypto integration↗

Uniswap+Robinhood, Revolut X, Binance adding Apple/Google Pay, and China's Digital Yuan for tourists signaled that legacy finance apps are absorbing crypto rather than competing with it.

- 05DEX and protocol app launches

Uniswap v4's multi-chain web app launch and Curve's Telegram mini-app drew readers interested in whether DeFi UX is finally closing the gap with centralized exchange apps.

Centralized, Onchain, and Hybrid Architectures

Custodial “walled garden” apps

The earliest mainstream crypto apps were custodial. Users opened accounts, passed KYC checks, deposited fiat, and received an internal balance denominated in crypto. In these setups, most activity—including transfers between users—occurred on centralized ledgers. Withdrawals and some large transfers were processed onchain by the exchange. This model remains dominant in large exchange apps like Coinbase, Binance, and Kraken, despite their growing onchain feature sets.

Custodial apps have clear advantages. They can offer familiar login mechanisms, password recovery, and fraud monitoring. They can hold assets in cold storage, pool liquidity, and process high-frequency trades without congesting public networks. They can also enforce compliance measures like freezing accounts, reversing certain internal transfers, or geofencing services. On the downside, users must trust the provider to secure keys, maintain solvency, and respect withdrawal requests. Regulatory actions, lawsuits, or internal mismanagement can put users at risk, as seen in multiple exchange failures over the past decade.

Branding and intellectual property issues are also prominent in custodial app ecosystems. Crypto.com, for example, has filed lawsuits over trademark use of community slogans like “Crofam” in connection with sites and apps, highlighting the tension between corporate branding and grassroots community language. Apps are not just technical tools; they are also brand touchpoints, and companies may aggressively defend how their names and logos are used in app contexts. This complicates the landscape for third-party developers who want to reference brands or integrate with existing platforms.

Onchain-native apps and ecosystem hubs

Onchain-native apps attempt to minimize backend custody and place as much logic as possible on blockchains or L2 networks. Wallet-centric apps like Base’s wallet and browser frame themselves as ways to “trade and earn” directly onchain, often prioritizing speed, low fees, and deep integration with specific ecosystems. These apps see themselves as “ecosystem hubs,” where users can discover dapps, participate in governance, and bridge between chains. The Base app, for example, places emphasis on fast, onchain access rather than delayed transfers, highlighting that users can deploy assets across networks immediately rather than waiting for bank settlements.

Kraken’s integration of Solana DEX trading into its main app can be seen as a hybrid step toward onchain-native paradigms. Rather than listing all Solana tokens on a centralized order book, Kraken surfaces DEX liquidity through its interface, with dedicated labeling for DEX tokens and transparent fee breakdowns. Users tap “Buy,” enter an amount, and see an estimated output and guaranteed minimum before confirming. Although Kraken remains the venue orchestrating the trade flow, execution relies on Solana’s onchain infrastructure. This approach allows Kraken to offer early access to tokens before they are centrally listed, while relying on the DEX for price discovery and settlement.

Celo’s grants for “apps bringing real transactions, usage & volume” and “agentic apps & infra” point to another flavor of onchain-native applications. Here, the app is intended as an interface to a broader ecosystem where real-world transactions—like merchant payments, remittances, or microloans—are recorded onchain. The emphasis is on usage and volume, not only speculative trading. Apps funded in such programs may integrate SMS onboarding, local-currency ramps, and agent networks while still settling onchain, blurring the lines between web2-style distribution and web3-style settlement.

Hybrid and white-label apps

Between pure custodial models and fully onchain-native apps lies a large spectrum of hybrids. Many fintech and neobank apps use white-label banking and payment infrastructure provided by sponsor banks, while also incorporating stablecoin rails. Tempo’s research on sponsor banks suggests that the same institutions that powered consumer-facing apps like Chime and Cash App could similarly underwrite stablecoin-based platforms, handling compliance and fiat flows while the front-end apps focus on user experience. In such cases, the app may be a thin layer on top of banking-as-a-service APIs, card processors, and stablecoin issuers.

White-label crypto apps also exist that provide exchanges or wallets for brands without deep technical stacks. These apps can be reskinned for different markets, with the underlying custody and compliance handled by the provider. In parallel, infrastructure SDKs like SODAX enable app developers to integrate cross-network assets such as xStocks from nineteen integrated networks, meaning any partner app can offer users exposure to tokenized stocks without building the full stack themselves. The result is an application ecosystem where many different brands share similar underlying infrastructures, differing mainly in brand, UX, and geographic focus.

Hybrid apps present both opportunities and risks. On the one hand, they can onboard users quickly by leaning on regulated intermediaries, familiar payment methods, and app store distribution. On the other, they can create hidden dependencies that undermine the rhetoric of decentralization. Apps may market themselves as “onchain” or “bankless” while still being subject to unilateral account shutdowns, policy-induced service changes, or deplatforming by banks, card networks, or app stores.

AI, Agents, and “Agentic” Crypto Apps

AI inside trading, UX, and operations

Artificial intelligence is becoming an integral part of crypto app design and operation. At the simplest level, AI models assist with support chat, fraud detection, and personalized recommendations. More advanced usage includes AI agents that monitor markets, propose portfolio rebalances, or automatically execute strategies within user-defined constraints. Apps are increasingly marketing themselves as “agent-ready,” meaning they expose APIs or workflows that can be orchestrated by AI systems rather than only by human users.

Portal Studio, for instance, is pitched as a tool for visualizing agent workflows, especially in gaming contexts, with a forthcoming “Portal Nexus” superapp that promises to provide powerful tools for agents to build complex games and experiences. In such a vision, the “user” of an app may not be a human directly, but a constellation of AI agents acting on their behalf or interacting with each other in a virtual world that ties into real crypto markets. These agents might query onchain data, trade assets, or participate in governance through programmable interfaces. The human sees a game or dashboard; the agents see APIs and state machines.

Celo’s focus on “agentic apps & infra” within its grants programs points to similar trends. Developers are encouraged to build applications where agents mediate user interactions with DeFi protocols or perform background tasks like payment routing, risk management, or compliance checks. COTI’s programmable privacy for ERC-20 tokens, trading, NFTs, and AI agents adds another dimension; AI agents might interact with privacy-preserving contracts to execute confidential trades or payroll, while still enabling selective disclosure for audits or tax reporting. Apps that integrate such capabilities must balance UX clarity with the opacity inherent in both AI models and privacy tech.

Trading apps have also begun integrating AI-driven research feeds, sentiment indicators, and copy-trading recommendations. While these features can help users navigate noisy markets, they also raise questions about transparency, conflicts of interest, and over-reliance on opaque models. If an app’s AI nudges users toward certain tokens or strategies, the line between tool and advisor becomes blurred.

Content verifiability and anti-AI “slop”

The rise of generative AI has created another problem for apps: content quality and authenticity. As synthetic media floods feeds, platforms struggle to distinguish high-quality human contributions from low-value “AI slop.” EarnOS’s launch of an “anti-AI slop” app, backed by funding from investors including 1kx, Circle, and Coinbase, is a notable response. The company’s broader mission, as described in its public materials, is to make the internet more verifiable and rewarding, partly by turning online activity into measurable, rewardable contributions. Its app aims to reward human-created, verifiable participation with real-money payouts accessed via its Visa card, rather than abstract points.

In this model, a crypto app is not only a financial interface but also a verification layer. It must assess whether content or actions are genuine, attach cryptographic or reputational proofs, and allocate rewards accordingly. Stablecoins and onchain accounting ensure that rewards are transparent and portable, while the app serves as the arbiter of value in a noisy content landscape. The “anti-AI slop” framing hints at a future where apps compete not only on tools and yields, but also on the quality and trustworthiness of the content they surface.

Privacy, onchain data, and programmable access

AI and agents intensify long-standing privacy concerns in crypto. Onchain data is transparent by default; agents and analytics tools can aggregate and analyze it at scale. At the same time, many onchain use cases—payroll, lending, health-related data, enterprise transactions—require confidentiality. Apps like COTI’s Privacy Portal attempt to square this circle by offering programmable privacy primitives. Developers can build DeFi or agentic apps where certain fields are encrypted or hidden, while others remain public or selectively revealable under specified conditions.

Private DeFi apps complicate regulatory discussions but open new possibilities for enterprise and consumer applications that could not be built on fully transparent ledgers. Payroll apps that run on COTI’s infrastructure, for example, could allow companies to pay workers in stablecoins or other tokens while keeping individual salaries private but provably compliant with tax and reporting obligations. Lending apps might hide borrower identities while exposing collateralization ratios. AI agents operating in such environments could manage nuanced policies about what to reveal and when, but the user’s view remains that of a simple, intuitive app.

Sophon shutters L2 chain after failing to find product-market fit, shifts focus to app studio and Base deployments

DeFiLlama has Sophon TVL at about $294k, down from a ~$20.1m May 2025 high; keeping a dedicated ZK Stack chain alive for that base is treasury theater. The sharper move is stripping SOPH of gas/staking utility, moving the LayerZero OFT adapter to Ethereum, and kicking off a 46.5m+ burn while Pyre tries to fund future buybacks from interchange, vault fees, and stablecoin reserve yield. For the ZKsync Elastic Chain crowd, Base is the uncomfortable scoreboard: apps want shared liquidity and distribution more than sovereignty once subsidies wear off.

- 2021-08regulatory

Apple allows Axie Infinity on App Store

- 2023-09milestone

Uniswap front-end fee hits $1M in first month

- 2023-11regulatory

Wallet of Satoshi exits US app stores citing regulatory pressure

- 2023-11exploit

Fake Ledger Live on Microsoft Store steals 16.8 BTC

- 2024-02exploit

Fraudulent Rabby Wallet on Apple App Store steals $1.6M

- 2024-11launch

Tether USDT and XAUT launch on TON blockchain for Telegram's 900M users

- 2025-01launch

Uniswap v4 launches web app across 10 chains including Ethereum, Base, Arbitrum

- 2025-03milestone

Uniswap and Robinhood partner to offer in-app crypto swaps with $10 USDC promotion

Security, Risks, and User Protection

Malware, app stores, and supply-chain attacks

As apps become the primary gateway to crypto, they are increasingly attractive targets for attackers. The Steam Wallpaper Engine campaign uncovered by security researchers illustrates how attackers leverage trusted platforms and seemingly innocuous applications to distribute malware. In this case, malicious “application wallpapers” were uploaded to Steam Workshop, a popular platform for sharing custom content, and downloaded thousands of times by users. Once a user applied an infected wallpaper, hidden executables would run, dropping backdoors, infostealers, crypto miners, or ransomware on the victim’s machine. Some variants even modified system libraries to hijack Steam sessions and harvest credentials, which were sent to attacker-controlled servers for account takeover and further malware dissemination.

Although the immediate victims in that campaign were gamers, the tactics are applicable to crypto apps and app stores. A malicious wallet app might pass initial store reviews but later update to include credential-stealing code. An attacker could publish a fake version of a popular exchange app with almost identical branding, tricking users into entering passwords or seed phrases. Even legitimate apps can be compromised through supply-chain attacks, where third-party libraries or advertising SDKs are injected with malicious code. Stories like the Steam wallpaper malware remind users and developers that “trusted platforms” are not immune to abuse and that content which appears as mere aesthetics—a wallpaper, a theme, a browser extension—can hide powerful attack vectors.

App providers must therefore invest heavily in security: code audits, secure build pipelines, dependency vetting, runtime protections, and anomaly detection. They must also guide users toward safe behaviors, such as downloading apps only from official sources, verifying publisher identities, and keeping operating systems updated. Users, for their part, must treat their devices as critical infrastructure; a single infection can compromise all keys stored on a device, regardless of the quality of the wallet app itself.

Seed phrases, keyless models, and user practices

User-side security practices remain crucial, especially for non-custodial apps. Guidance from security-focused providers emphasizes several principles: keep seed phrases offline, consider encrypting any digital backups, maintain multiple backups in separate secure locations, and never type a seed phrase into a website or chat window. Users are encouraged to consider the physical security of their storage (for example, fire and water resistance) and to plan for inheritance or emergency access in case of death or incapacitation. These considerations turn a simple “twelve words” into a long-term operational challenge.

Keyless and MPC-based wallet models seek to reduce the burden on users by eliminating visible seed phrases. As seen in Binance’s Keyless wallet and Kraken’s integrated onchain trading, these apps manage key material behind the scenes, often distributed across devices or servers, and present a more familiar login flow. Users may log in with email, passwords, or device-biometrics; recovery may involve multi-factor authentication rather than retrieving a phrase. This can dramatically reduce cases of lost access due to misplaced seed phrases, but it also increases dependence on the provider’s infrastructure and recovery policies.

Education within apps is a delicate balance. Overwhelming new users with security warnings can drive them back to custodial services, while under-emphasizing risks can lead to catastrophic losses. Some apps attempt to segment users by sophistication, offering “basic” and “expert” modes, or gating advanced features behind comprehension checks. Others build gradual onboarding flows where users start custodial and are later encouraged to migrate to self-custody once balances or usage justify the added responsibility.

Social engineering, political promotion, and ethics

Security is not only technical. Social engineering—tricking users into trusting the wrong person or interface—is a leading cause of loss. Prominent figures endorsing apps can blur the line between personal recommendation and paid promotion, complicating user perception. Coverage around political figures praising specific apps, such as Donald Trump’s public praise for his “great daughter” using a particular app, has sparked debate over promotion ethics, disclosure, and the potential for undue influence in app adoption decisions. When a political figure or celebrity lauds an app without transparent disclosure of financial or personal interests, users may overestimate the app’s safety or regulatory status.

Family members of political figures also feel the reputational effects of such associations. Kai Trump, for instance, has spoken publicly about how half the world dislikes her because of her last name, underscoring how political identity can color everyday interactions, including perceptions of apps linked to those figures. When combined with financially risky products like levered trading or speculative tokens, endorsement by polarizing figures can intensify both regulatory scrutiny and public backlash.

Brand conflicts also arise in community-driven spaces. Crypto.com’s litigation over “Crofam” trademarks for its site and app illustrates how community language and corporate branding can collide. Communities may feel a sense of ownership over slogans or memes, while companies seek exclusive rights for marketing and legal reasons. Apps are where these disputes become visible, as logos, names, and taglines appear on home screens and in app stores. Clear disclosure, careful marketing, and respect for communities become part of an app’s security and trust profile, even if they are not coded in software.

Regulation, Banks, and Stablecoin Infrastructure Behind Apps

Sponsor banks, card networks, and “bankless” dependence

Behind many crypto apps sits a layer of traditional finance. Sponsor banks provide regulated accounts, payment processing, and card issuance for fintechs and crypto platforms, often through banking-as-a-service arrangements. Research into this space has highlighted that the same sponsor banks that powered the rise of fintech giants like Chime and Cash App could become crucial to stablecoin-based platforms, as these banks are already skilled at managing compliance, deposit flows, and integrations with card networks. As stablecoin adoption accelerates, apps that integrate USDC or similar tokens may require sponsor banks to hold fiat reserves, manage settlement, and bridge between onchain and offchain balances.

Card networks like Visa and Mastercard remain central to many crypto app value propositions. EarnOS’s promise of instant payouts in “real money” that can be spent via an EarnOS Visa card is only possible because of tight integration with these networks. Bolt, Crypto.com, and other money apps similarly rely on card issuers and processors to allow users to spend crypto-derived balances at ordinary merchants. This dependency contradicts narratives of complete disintermediation: even when crypto is used under the hood, the last mile to merchants and ATMs passes through legacy rails.

Apps that try to circumvent banks entirely face challenges in fiat conversion, regulatory licensing, and consumer protection frameworks. Some attempt to route around these issues by focusing on stablecoin-only ecosystems or by restricting themselves to “utility token” features, but regulators have increasingly signaled that functional equivalence to traditional money will invite comparable oversight. As a result, many “bankless” apps are in practice deeply entangled with bank and card infrastructures, but present a more radical image to users.

Compliance, KYC, and app permissions

Regulatory compliance is embedded in app flows. Identity verification, sanctions screening, transaction monitoring, and reporting obligations must be implemented at the app level, even if some checks are delegated to third-party providers. Exchange and neobank apps typically require users to provide identification documents and personal data before enabling full functionality. Wallet-only apps may avoid KYC by dealing solely with onchain interactions, but risk being swept into broader regulatory nets if they integrate fiat ramps or certain DeFi services.

Campaigns like Binance’s GWEI trading competition showcase how compliance and marketing intersect. Participation requires users to click “Join” in the app, thereby linking the competition to identifiable accounts. Trading volume is tracked via Binance Wallet (Keyless) and Alpha, excluding third-party dapps. Rewards are claimable within specified time windows, and unclaimed tokens are forfeited. Such detailed rules require the app to manage eligibility, calculate payouts, and enforce terms—in effect, embedding a mini-regulatory regime around a marketing event.

Jurisdictional differences manifest in feature availability. Kraken’s onchain Solana trading is restricted to “eligible customers” in the U.S. and over 100 other countries, implying that some regions are excluded due to sanctions, licensing, or local restrictions. Local app stores may also block certain apps or disable features based on government directives. Apps must therefore maintain complex configurations about what features are available where, which tokens can be shown, and what disclosures are required in each jurisdiction.

Jurisdictional fragmentation and app competition

Because crypto markets are global but regulation is local, app competition is often segmented by geography. Some apps prioritize U.S. compliance and list only assets deemed acceptable under that regime. Others focus on markets in Asia, Europe, or emerging economies, tailoring token offerings, languages, and fiat ramps accordingly. Local regulators may issue licenses for virtual asset service providers, with stringent requirements on capital, custody, and reporting. Apps that operate across borders must navigate overlapping frameworks, decide where to base legal entities, and manage complex corporate structures.

Fragmentation influences not just what users can access, but also how quickly they can access new markets. Kraken’s ability to expose Solana DEX listings rapidly through its app gives it an advantage in serving early-stage token demand in eligible markets. Coinbase’s listing cadence and geographical coverage for new tokens like RE determine which users can buy them within their app. Binance’s design of wallet and Alpha features signals where the company expects regulatory space for onchain trading promotions. As more onchain-first apps emerge, jurisdictional arbitrage may favor those who can deliver a mostly uniform experience globally, but the long-term trend points toward continued fragmentation.

- Smart-contract / protocolMedium

Odos Protocol lost ~$50k via an arbitrary call vulnerability in its app-facing contracts, illustrating that front-end aggregator integrations add novel attack surfaces beyond core protocol code.

- RegulatoryHigh

Wallet of Satoshi's full US app-store exit and MetaMask's temporary removal demonstrate that regulators can effectively de-platform crypto apps without passing new legislation simply by pressuring Apple and Google.

- CentralizationHigh

Telegram's TON-only mini-app strategy drew explicit backlash for concentrating Web3 distribution through a single messaging platform with limited liquidity and a single blockchain dependency.

Fake Ledger Live on Microsoft Store and a fraudulent Rabby Wallet on the Apple App Store collectively stole millions, showing that official app marketplaces provide insufficient protection against impersonation attacks.

- LiquidityMedium

yield.app's bankruptcy and Friend.tech's mass exodus to rival apps highlight that app-layer liquidity is fragile — user assets and TVL can evaporate faster than protocol fundamentals change.

- Market / platform dependencyMedium

Projects built as Telegram mini-apps or Robinhood integrations inherit the market and policy risk of their host platform, as seen when TON's limited liquidity was flagged as an existential concern for TON-only apps.

Outlook

Crypto apps are consolidating an extraordinary range of functions—trading, payments, savings, gaming, AI agents, and identity—into single interfaces that increasingly resemble operating systems for digital value. The immediate trajectory points toward more hybrid architectures, where onchain and offchain components are tightly coupled but abstracted from users. Exchange apps will continue to fold in DEX access and cross-chain routes; wallet apps will evolve into ecosystem hubs; and “superapps” will vie to own the full spectrum of onchain life, from DeFi to gaming and social.

At the same time, underlying tensions will sharpen. Custody and key management models must reconcile user safety with sovereignty. AI and agentic apps must balance automation with transparency and fairness, especially when recommending trades or allocating rewards. Privacy-preserving DeFi apps must prove they can deliver both confidentiality and compliance. Security will remain a moving target, as attackers exploit app stores, user trust, and the expanding attack surface of complex app stacks. Regulatory scrutiny will keep intensifying, particularly around stablecoins, neobank-style apps, and cross-border payments.

For a crypto news audience, the key is to understand that “app” is no longer a simple label for a downloadable program. It now encapsulates business models, governance choices, regulatory strategies, and infrastructural dependencies. The next decade of onchain finance will likely be defined less by isolated protocols and more by the apps that orchestrate them—shaping who gets access to which markets, under what rules, and with what trade-offs between convenience, control, and openness.

Latest App news

Coinbase’s Base app launches desktop web version for trading and payments.Arc launches open-source stablecoin FX app on testnet, pitching a flagship multi-currency hub for global stablecoin financeSophon shutters L2 chain after failing to find product-market fit, shifts focus to app studio and Base deployments RedStone charts new oracle waters for Daml, letting Canton apps anchor shared prices while keeping each ledger hidden below the surface

RedStone charts new oracle waters for Daml, letting Canton apps anchor shared prices while keeping each ledger hidden below the surface Uniswap lets teams launch CCA token auctions from web app on Ethereum, Base, Arbitrum, and Unichain

Uniswap lets teams launch CCA token auctions from web app on Ethereum, Base, Arbitrum, and Unichain Meta reportedly builds points-based Arena prediction market app to rival Polymarket and Kalshi

Meta reportedly builds points-based Arena prediction market app to rival Polymarket and KalshiSources

- https://blog.kraken.com/product/onchain-trading/now-built-into-the-kraken-app

- https://www.kaspersky.com/resource-center/definitions/what-is-cryptocurrency

- https://apps.apple.com/us/app/bolt-finance-crypto-superapp/id6714480612

- https://apps.apple.com/us/app/base-built-to-trade-earn/id1278383455

- https://www.kraken.com/features/onchain

- https://securelist.com/dozens-of-malicious-wallpapers-found-on-steam-workshop/120186/

- https://x.com/COTInetwork/status/2067614954467869071

- https://x.com/TheBlockCo/status/2067260316652638718

- https://x.com/jevgenijs/article/2067206267806822416

- https://earnos.com

- https://www.youtube.com/watch?v=uAtkedvJibU

- https://www.binance.com/en/support/announcement/detail/6da78dd5f06c441ba03f974321dc46f3

- https://x.com/leviathan_news/status/2067818223861694549

- https://x.com/earnos_io?lang=en

- https://x.com/Portalcoin/status/2066826523089203677

- https://x.com/Celo/status/2066620906898927846

- https://www.facebook.com/TheRawStory/posts/kai-trump-the-granddaughter-of-president-donald-trump-revealed-that-half-the-wor/1400863745401915/

- https://shieldfolio.com/blogs/crypto-security-blog/seed-phrase-storage-guide

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…