GMX is a decentralized perpetual-futures exchange launched on Arbitrum in 2021. Learn how its GLP and GM vaults, GMX token, Chainlink oracles, 2025 exploit, and multichain expansion work.

- x.com9

- gmxio.substack.com5

- dlnews.com2

- leviathannews.substack.com1

- snapshot.box1

- snapshot.org1

- youtube.com1

+2 sources across the wider coverage universe

GMX launches 24/7 gold and silver perps with up to 100x leverage, powered by Chainlink2026-04

GMX launches 24/7 gold and silver perps with up to 100x leverage, powered by Chainlink2026-04 GMX traders pay 65% less funding after late-April changes flatten long-tail perp rates2026-05

GMX traders pay 65% less funding after late-April changes flatten long-tail perp rates2026-05 GMX goes live on MegaETH with 50x leverage perps and 10ms execution via Chainlink2026-03

GMX goes live on MegaETH with 50x leverage perps and 10ms execution via Chainlink2026-03 Arthur Hayes sells $9.6m of GMX as newer protocols eat market share with point systems2024-04

Arthur Hayes sells $9.6m of GMX as newer protocols eat market share with point systems2024-04 GMX to receive largest share of Arbitrum's $40 million grant, Lido misses out.2023-10

GMX to receive largest share of Arbitrum's $40 million grant, Lido misses out.2023-10 GMX introduces GLV - GMX Liquidity Vaults 2024-09

GMX introduces GLV - GMX Liquidity Vaults 2024-09

GMX is a decentralized perpetual-futures exchange that lets users trade leveraged positions on crypto and other assets directly from a self-custodial wallet, with liquidity supplied by on-chain pools rather than a traditional order book. First deployed on Arbitrum in 2021, it became one of the defining protocols of the "real yield" era of decentralized finance (DeFi).

What GMX Is and How It Works

GMX is an on-chain venue for trading perpetual futures—derivatives that track an asset's price without an expiry date—using leverage of up to 50x or higher depending on the market and chain (GMX docs, tastycrypto). Unlike a centralized exchange, GMX settles trades through smart contracts, so users retain custody of their funds and counterparties are not other individual traders matched on an order book but a shared liquidity pool.

The protocol's defining design choice is that liquidity providers act as the collective counterparty to traders. When a trader opens a leveraged long or short, the pool takes the other side. Traders pay fees and funding to the pool; in return, liquidity providers absorb trader profit and loss. Asset prices are not discovered internally but imported from external oracles—primarily Chainlink and, in newer deployments, Chainlink Data Streams—which has made oracle integration central to how GMX expands to new markets and chains.

Two generations of the protocol coexist conceptually but the second has become the standard. GMX V1 used a single multi-asset pool called GLP, holding a basket such as ETH, BTC, LINK, USDC, USDT, DAI and FRAX; providers minted GLP and earned a large share of fees while bearing exposure to the basket and to net trader winnings (Coinhouse). GMX V2, now the actively supported version on Arbitrum and Avalanche, replaced the monolithic pool with isolated GM markets. Each GM pool backs a specific market and accrues only that market's fees, letting liquidity providers choose their risk exposure and limiting contagion between markets (beincrypto). V2 also added stronger oracle protections and more granular fee mechanics.

GMX launches 24/7 gold and silver perps with up to 100x leverage, powered by Chainlink

100x on gold perps when CME caps you at ~15x on GC futures — DeFi leverage on commodities is now multiples beyond TradFi. GMX pricing these 24/7 via Chainlink Data Streams while COMEX closes for 45 minutes daily and shuts entirely on weekends means the oracle is quoting prices during thin liquidity windows with no reference market backing it. Previous XAUT launch was capped at 25x, so if commodity pairs are actually getting 100x now, GMX LPs are absorbing a completely different risk profile than what they signed up for with crypto perps.

Readers follow GMX not as a static DeFi blue-chip but as a live accountability ledger — they click every stage of the exploit-to-recovery arc and treat insider exits like Arthur Hayes's $9.6m sale as hard evidence that newer incentive models are winning the perp DEX war.

Launch and Early Growth

The protocol's roots trace to Gambit Exchange, which launched in 2021 before relaunching as GMX on Arbitrum, the Ethereum layer-2 rollup, in September 2021 (Coinhouse). In January 2022 it expanded to Avalanche, an EVM-compatible chain. GMX's arrival coincided with Arbitrum's own growth, and the two became closely associated: GMX was for a time the largest source of fees and trading activity on the network, and it remains one of the leading derivatives venues across Arbitrum and Avalanche, with cumulative trading volume reported in the range of $130 billion and several hundred thousand users (beincrypto).

Its rise helped popularize the "real yield" narrative—the idea that a DeFi protocol should distribute revenue earned from actual usage (trading fees) rather than emit inflationary token rewards. That framing shaped how a generation of derivatives protocols marketed themselves and how investors evaluated them.

- 01Exploit accountability arc

The $42m V1 GLP reentrancy hack generated three separate high-click articles — the breach, the white-hat bounty offer, and the fund return — showing readers stayed engaged through every accountability beat, not just the initial shock.

- 02Arbitrum grant competition

Readers wanted to know who captured the largest slice of Arbitrum's $40m ecosystem grant, signaling that protocol-level capital allocation races matter as much as product news.

- 03Arthur Hayes exit as signal

A named insider dumping $9.6m while citing point-system competitors framed GMX's competitive decline as a concrete, attributable event rather than vague market pressure.

- 04V2 evolution and new products

GMX V2 mainnet launch, GLV vaults, TWAP orders, and gold/silver perps each drew clicks, reflecting reader appetite for evidence that the protocol was iterating against faster rivals.

- 05Whale liquidation tracking

A $13m GMX whale liquidation featured in the weekly roundup alongside Hyperliquid whale cross-platform positioning shows readers use large-position unwinds as real-time market-health indicators.

- 06Multichain and infrastructure bets

Expansion to Base, MegaETH, and the LayerZero partnership each generated clicks, reflecting reader interest in whether GMX's cross-chain strategy could offset share lost on Arbitrum.

The GMX Token, Vaults and Tokenomics

GMX uses a two-token economic structure that separates governance/value capture from liquidity provision.

- GMX is the protocol's utility and governance token, with a supply historically capped near 13.25 million (GMX docs). Staking GMX confers voting power and a claim on protocol revenue.

- GLP (V1) and GM tokens (V2) represent liquidity-provider positions in the vaults that back trading. GM holders earn the fees generated by their specific market.

- esGMX (escrowed GMX) is a reward token distributed to stakers and via referrals; it can be vested into liquid GMX over roughly one year or staked for additional rewards (GMX docs).

GMX's value-accrual mechanism has evolved. Historically, stakers earned a direct share of fees paid in ETH and AVAX. More recently, the DAO approved a buyback model in which a portion of protocol fees—commonly cited around 27%—is used to repurchase GMX on the open market, with repurchased tokens directed to the treasury or removed from circulation (tokenomics.com). In 2026, governance pursued a more aggressive program: the DAO launched buyback-transparency tooling and "staking power" upgrades, and reporting describes a strategy that accumulates bought-back GMX in the treasury for later distribution to stakers, with "power" accrual that began on March 4, 2026 (CryptoRank). These mechanics are set by token-holder vote and change over time, so current parameters should be confirmed against live governance and documentation rather than assumed fixed.

Stablecoins—particularly USDC—are foundational to the system. USDC is a core collateral and settlement asset in GMX vaults, and newer markets frequently pair assets directly against USDC. The protocol's RIZ v2 market framework, for example, lists isolated markets such as GMX/USDC and a range of other token-versus-USDC pairs that can be deployed in minutes rather than weeks, reflecting a shift toward faster, permissionless market creation.

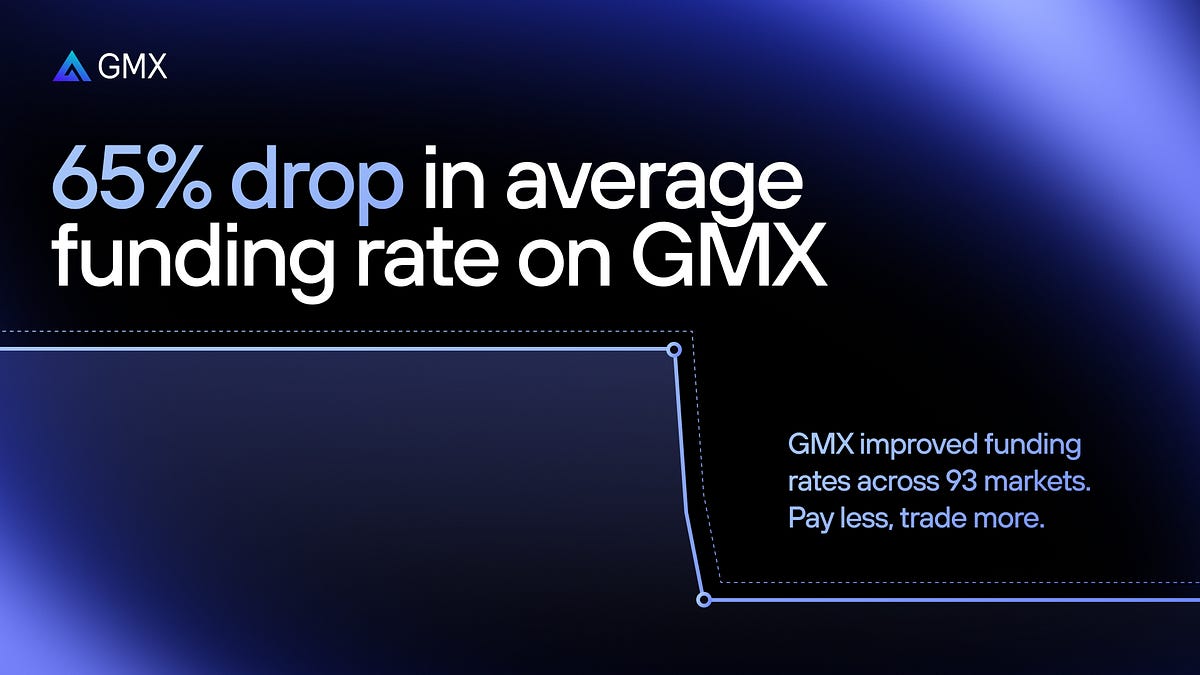

GMX traders pay 65% less funding after late-April changes flatten long-tail perp rates

GMX says funding-paying side median rates are down over 65% versus the pre-update baseline since late-April funding parameter changes, with 93 of 109 markets posting lower rates. The long-tail perp markets that used to run above 50% funding have basically disappeared, making positions cheaper to carry and giving GMX cleaner room to list larger, deeper markets. Team frames this as the first pass, with more funding-mechanism refinements already queued.

- 2023-08launch

GMX V2 beta launches on Arbitrum and Avalanche

- 2023-10milestone

GMX receives largest share of Arbitrum's $40m STIP grant

- 2023-11exploit

$42m reentrancy exploit hits GMX V1 GLP; attacker bridges funds to Ethereum

- 2023-11governance

GMX offers 10% white-hat bounty (~$4.2m) for return of stolen funds

- 2023-11milestone

Hacker returns $37.5m; retains $5m ETH as negotiated bounty

- 2024-01exploit

Abracadabra MIM-GMX strategy exploited for 6,260 ETH

- 2024-06launch

GMX introduces GLV — GMX Liquidity Vaults — as new LP product

- 2024-09milestone

Arthur Hayes sells $9.6m of GMX, citing point-system protocol competition

The July 2025 Exploit

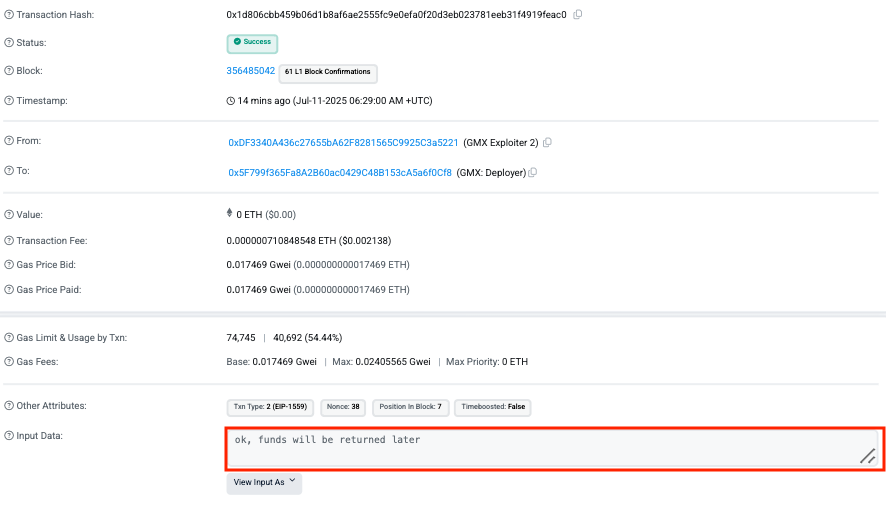

In July 2025, GMX suffered the most serious security incident of its history. On July 9, an attacker exploited a reentrancy vulnerability in GMX V1, draining more than $40 million—figures across analyses cluster around $42 million (Halborn, QuillAudits). Reentrancy is a class of bug in which a malicious contract re-enters a function before the first invocation finishes updating its internal state.

The mechanics were specific to V1's accounting. By re-entering through the order-execution path, the attacker caused the list of short positions to update while the global average short price did not, leaving that price artificially low. The system then treated shorts as if opened at those depressed values, inflating the protocol's calculated assets under management and the perceived value of GLP, which the attacker exploited to extract funds (Sherlock, CertiK).

GMX responded with a public bounty offer: return the funds within a set window for a white-hat payment exceeding 10% of the stolen amount and no legal pursuit. The attacker accepted. Within days, the bulk of the funds—initially over $10 million in FRAX, then the remainder—was returned to GMX-controlled wallets, while the exploiter retained roughly $5 million in ETH as the agreed bounty (CoinDesk, DL News). The episode reinforced two recurring DeFi lessons: that older, less-maintained contract versions carry concentrated risk even after a protocol's primary development has moved on, and that negotiated bounties have become a common, if uncomfortable, recovery path.

- Smart-contractHigh

GMX V1 suffered a $42m GLP reentrancy exploit, a separate Abracadabra/MIM strategy exploit for 6,260 ETH, and an earlier exploit where the hacker ultimately kept $5m as a bounty — a pattern of material on-chain losses.

- Market / CompetitiveHigh

Arthur Hayes's public $9.6m sale explicitly cited point-system protocols eating GMX's market share, signaling that liquidity-mining incumbents face structural user-acquisition disadvantage against newer incentive designs.

- LiquidityMedium

GLP pools are the counterparty to all trades, meaning large directional trader wins directly drain liquidity provider returns; the $13m whale liquidation and recurring large open-interest events amplify this dynamic.

- Centralization / InfrastructureMedium

GMX depends on Chainlink Data Streams for real-time perp execution and selected LayerZero as its sole cross-chain messaging layer, creating concentrated oracle and bridge dependency risk.

- GovernanceLow

The DAO successfully voted to direct 10% of revenues to treasury with no apparent controversy, and the Chaos Labs V2 Risk Portal added granular controls, suggesting governance is functional if not deeply contested.

- RegulatoryLow

No regulatory enforcement actions appear in the most-clicked GMX coverage; the protocol's permissionless perp model carries latent jurisdiction risk but has not yet drawn direct regulator attention based on reader-signal headlines.

Multichain and New Markets

After years anchored to Arbitrum and Avalanche, GMX has pushed into a multichain footprint and a broader set of tradable assets.

- Base. GMX expanded onto Coinbase's Ethereum layer-2, Base, marking an early step in its multichain strategy beyond its original two networks.

- MegaETH. GMX went live on MegaETH, a high-throughput chain marketed around roughly 10-millisecond execution. The deployment pairs MegaETH's speed with Chainlink Data Streams to offer up to 50x leverage perps and a USDm liquidity vault, positioning fast block times as a way to reduce liquidation risk and improve execution. GMX's own messaging frames this as a "real-time blockchain" deployment for BTC, ETH and SOL perps, with a GLV (GMX Liquidity Vault) backed by the USDm stablecoin.

- Solana adjacency. GMTrade, which began as a GMX deployment on Solana before becoming an independent protocol, illustrates how the GMX model has been forked and adapted—using a pooled trading model, Chainlink oracle integration, and LP-yield mechanics on a non-EVM chain.

The asset menu has also broadened well beyond crypto. GMX launched 24/7 gold and silver perpetuals with leverage advertised up to 100x, powered by Chainlink price feeds, and has listed pre-IPO equity exposure such as SpaceX (SPCX) perpetuals. These products extend on-chain derivatives into commodities and private-company valuations, but they introduce distinct risks: commentary around the metals markets flagged liquidity concerns, since thin pools can widen slippage and complicate liquidations during volatile, round-the-clock trading.

Beyond new chains and assets, GMX has positioned itself as infrastructure for other platforms. It serves as an execution venue for on-chain prop-trading and structured products—cited as a liquidity backbone for platforms like Doji—reflecting a strategy in which GMX supplies depth that third parties build atop.

GMX goes live on MegaETH with 50x leverage perps and 10ms execution via Chainlink

$363B lifetime volume across 8 chains sounds impressive until you remember MegaETH's entire TVL was sitting around $66M a week after mainnet launch. 50x leverage perps live and die on counterparty depth — GLV pool sizing on a chain this young is the real bottleneck, not 10ms execution. Anyone who traded GMX V1 on Arbitrum early knows oracle architecture matters way less than whether there's enough LP cushion in the USDm vault to absorb a $BTC wick without getting drained. Chainlink Scale subsidizing oracle costs is a nice bootstrap, but the second that subsidy ends, the fee math for LPs changes fast.

Governance, Operations and Open Questions

GMX is governed by a DAO whose token holders vote on fee parameters, buyback policy, treasury use and market launches. In 2026, governance addressed two structural themes. The first was price discovery and supply overhang: the DAO approved measures to manage concentrated holdings and centralized-exchange supply, including a temporary buy-wall liquidity plan, in an effort to stabilize the token's market. The second was operational maturity: GMX Labs proposed creating a formal CEO role to lead strategic growth, explicitly framing the move around scaling risks and governance concerns. A search for an experienced operator to lead expansion signals a shift from a purely community-stewarded protocol toward more conventional organizational structure—a transition that often surfaces tension between decentralization ideals and the demands of running a large, multichain business.

Other recent operational changes have been incremental but telling: lower funding costs after late-April adjustments flattened long-tail perpetual rates (one report cited roughly 65% lower funding for traders), a redesigned trading interface, in-app chat support, and an overhauled referrals page with guild-based rebates. Separately, Coinbase suspended its own GMX-PERP and a basket of other perpetual contracts in March 2026—a reminder that the token's listing footprint on centralized venues moves independently of the protocol's own product roadmap.

Outlook

GMX's trajectory now hinges on whether it can convert a strong DeFi-native brand into durable advantage as the on-chain derivatives field grows more crowded and faster. Its bets—isolated GM vaults, expansion to high-speed chains like MegaETH and Base, non-crypto markets such as metals and pre-IPO equities, and a buyback-centric token model—each carry an offsetting risk: new markets can be thinly liquid, multichain deployments enlarge the security surface that the 2025 V1 exploit showed can be costly, and aggressive tokenomics tie holder rewards to price targets that may or may not be met. The proposed move toward formal executive leadership suggests the project itself recognizes that the next phase is less about pioneering a category and more about operating reliably at scale. Readers should treat specific parameters—fee splits, leverage caps, buyback percentages and reward schedules—as governance-dependent and subject to change, and verify them against current GMX documentation before acting.

Latest GMX news

GMX launches 24/7 gold and silver perps with up to 100x leverage, powered by ChainlinkGMX traders pay 65% less funding after late-April changes flatten long-tail perp ratesGMX goes live on MegaETH with 50x leverage perps and 10ms execution via Chainlink GMX goes multichain, starting with an expansion into Base

GMX goes multichain, starting with an expansion into Base GMX hacker have returned $37.5m and keep $5m in ETH as bounty

GMX hacker have returned $37.5m and keep $5m in ETH as bounty GMX hacker agrees to return the stolen funds

GMX hacker agrees to return the stolen fundsCommunity notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…