Deep dive into MegaETH, a real‑time Ethereum L2 targeting 10ms blocks and 100k+ TPS, covering its architecture, MEGA and USDm tokenomics, DeFi ecosystem, security trade‑offs, exchange listings, and its role in the evolving L2 competition.

- x.com22

- theblock.co6

- leviathannews.substack.com1

- thedefiant.io1

- gmxio.substack.com1

- crypto.news1

- megaeth.com1

+5 sources across the wider coverage universe

Brix raises $5.5M to bring institutional-grade emerging market yield onchain via MegaETH, backed by Circle Ventures and ConsenSys2026-04

Brix raises $5.5M to bring institutional-grade emerging market yield onchain via MegaETH, backed by Circle Ventures and ConsenSys2026-04 Grayscale adds HYPE, PENDLE, VIRTUAL, and MegaETH among 30 assets to Q2 consideration list2026-04

Grayscale adds HYPE, PENDLE, VIRTUAL, and MegaETH among 30 assets to Q2 consideration list2026-04 MegaETH-based futures exchange MNX raised $6.4M at a $40M valuation to build trading markets around AI company valuations, compute resources, equities, and prediction markets2026-06

MegaETH-based futures exchange MNX raised $6.4M at a $40M valuation to build trading markets around AI company valuations, compute resources, equities, and prediction markets2026-06 Avon halts MegaETH deployment, announces shutdown of MegaVault with users urged to withdraw funds immediately as project pivots amid uncertainty2026-04

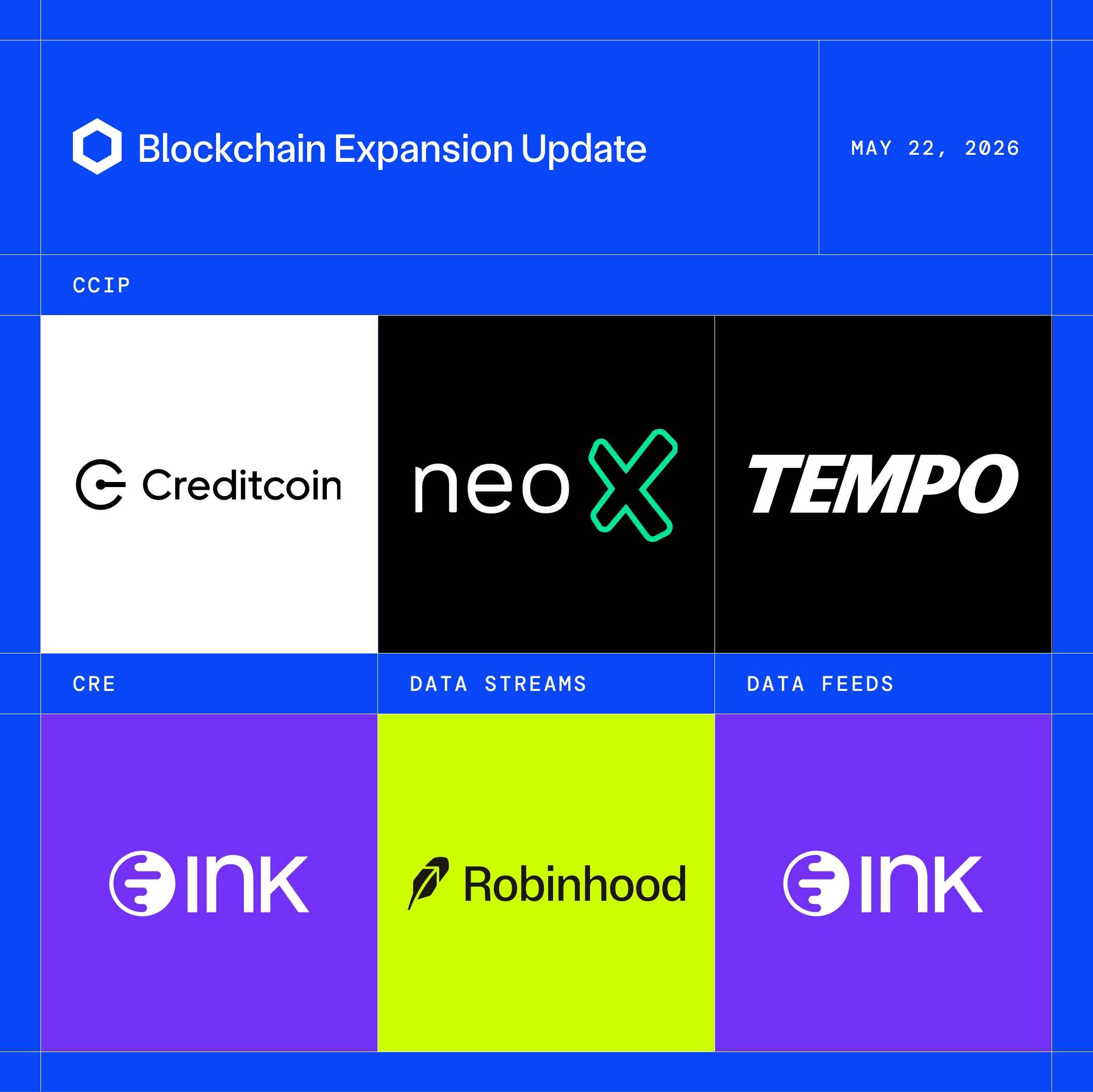

Avon halts MegaETH deployment, announces shutdown of MegaVault with users urged to withdraw funds immediately as project pivots amid uncertainty2026-04 Chainlink expands CCIP, CRE, and Data Feeds to Robinhood Chain testnet, MegaETH, Plasma, and more2026-05

Chainlink expands CCIP, CRE, and Data Feeds to Robinhood Chain testnet, MegaETH, Plasma, and more2026-05 MegaETH TGE in 1 week after chain achieves necessary KPIs2026-04

MegaETH TGE in 1 week after chain achieves necessary KPIs2026-04

MegaETH: A Real-Time Ethereum Layer‑2 Explained

As an Ethereum Layer‑2 built explicitly for real‑time performance, MegaETH is a high‑throughput blockchain that targets block times under 10 milliseconds and throughput above 100,000 transactions per second while remaining compatible with the Ethereum Virtual Machine and settling to Ethereum for security. It combines a heterogeneous node architecture, a performance‑linked token model, and a native stablecoin called USDm to create a low‑latency environment aimed at high‑frequency trading, gaming, and other latency‑sensitive onchain applications.

What MegaETH Is Trying To Solve

At its core, MegaETH is positioned as a response to the persistent performance gap between traditional Web2 systems and public blockchains, particularly in the Ethereum ecosystem. Ethereum mainnet is designed for decentralization and security rather than speed, and in practice it processes roughly 15 transactions per second, which makes it unsuitable for high‑frequency trading or real‑time gaming at global scale. Even the leading Layer‑2 networks, such as Arbitrum and Base, tend to operate in the tens of transactions per second in normal conditions, leaving a wide gulf between onchain user experience and centralized exchanges or fintech applications. MegaETH’s design goal is to close this gap by providing an environment where onchain transactions feel as fast and responsive as using a centralized order book, while still inheriting trust from Ethereum and preserving EVM compatibility.

The project’s founders frame MegaETH as the “first real‑time blockchain,” a phrase that is meant to convey both very low latency and continuous state streaming rather than the traditional model of discrete, multi‑second blocks. To make this feasible, MegaETH targets block times under 10 milliseconds, with an ambition of eventually approaching 1 millisecond confirmation for many user interactions. In concrete terms, that means transactions can be ordered and executed in timeframes comparable to high‑frequency trading systems, where the speed of state updates is often measured in milliseconds. The goal is not simply to increase theoretical throughput, but to enable categories of applications that have historically been forced offchain, such as high‑frequency derivatives trading, real‑time prediction markets, and fast‑twitch gaming economies.

Crucially, MegaETH insists on remaining fully compatible with Ethereum’s tooling and smart contract environment, which means it runs an EVM‑compatible execution layer despite its unconventional architecture. This allows existing Ethereum developers to port or deploy their applications with minimal code changes, and it preserves the composability that has historically made DeFi and NFT ecosystems on Ethereum so powerful. The project emphasizes that developers can scale their apps using “real‑time state streaming” while maintaining full Ethereum composability, a promise intended to differentiate MegaETH from non‑EVM high‑performance chains that require different tooling and contract languages. At the same time, the chain is marketed as being secured by Ethereum, with settlement of transaction batches and dispute resolution anchored to Ethereum mainnet, even as execution happens offchain at very high speed.

From an industry‑wide perspective, MegaETH is attempting to test an important hypothesis about user priorities: whether traders, gamers, and other active users care more about strict decentralization guarantees or about the user experience of low fees and near‑instant execution. The team has been explicit that they are willing to prioritize speed and developer experience over maximal decentralization in the early stages, challenging the prevailing narrative around “Stage 1” rollups that aim for rigorous trust minimization from the outset. This has made MegaETH a focal point in debates about how Ethereum’s scaling roadmap should balance performance, trust assumptions, and economic sustainability, and whether a more “Web2‑like” blockchain can still be meaningfully considered part of the Ethereum trust model.

Brix raises $5.5M to bring institutional-grade emerging market yield onchain via MegaETH, backed by Circle Ventures and ConsenSys

$5.5M is modest but the cap table tells the story — FRWRD (Yapi Kredi's venture arm) and Is Asset Management (Is Bank subsidiary) are two of Turkey's largest financial institutions backing a protocol that packages their own country's ~40% sovereign carry into composable DeFi yield. That's not just "institutional adoption" marketing, it's local TradFi actively piping domestic MMF returns into onchain rails via RedStone's hybrid FX oracle. Circle Ventures in the mix likely means a USDC/iTRY pair is coming, which would make parking stables in Turkish carry as simple as a swap on MegaETH.

Readers proxy-bet on MegaETH by clicking its DeFi tenants first — GTE alone drove more clicks than the $50M token sale and TGE combined, revealing that institutional confidence in the chain is being read through blue-chip protocol migrations rather than the chain's own milestones.

Origins, Launch, And Early Market Traction

MegaETH’s conceptual roots trace back to 2022, when founder Yilong Li began formulating an approach to Ethereum scaling that would break from the standard rollup pattern of homogeneous full nodes. Rather than having every node perform ordering, execution, and full state validation, MegaETH’s whitepaper proposed specializing node roles and optimizing the execution environment for parallelism and real‑time responsiveness. The project moved into active development around mid‑2024 following an initial fundraise, with the stated goal of building a high‑performance Layer‑2 that solved Ethereum’s scalability bottlenecks without breaking EVM compatibility or abandoning Ethereum as a settlement layer. During this period, MegaETH’s team began releasing research materials and technical writings that outlined their approach to “real‑time blockchain” design, positioning the chain as a kind of laboratory for next‑generation Web3 infrastructure.

The mainnet went live on 9 February 2026, marking the first production deployment of MegaETH’s real‑time architecture. From launch, the network aimed at block times under 10 milliseconds and throughput exceeding 100,000 transactions per second, though the actual realized performance would depend on network conditions and the level of adoption at any given moment. This launch timing roughly matched earlier expectations that the mainnet and token generation event would land between December 2025 and early 2026, reflecting the team’s deliberate approach to shipping the underlying protocol and developer tooling before aggressively marketing the token. The early mainnet phase was characterized by a focus on attracting high‑frequency trading and derivatives applications, which are among the most sensitive to latency and therefore most likely to benefit from MegaETH’s design choices.

One of the most distinctive aspects of MegaETH’s early trajectory was its performance‑based token launch model. Instead of announcing a fixed token generation date and inflation schedule, the team tied the MEGA token’s TGE to specific onchain key performance indicators (KPIs), such as transaction throughput and real usage metrics, and committed to triggering the TGE seven days after any one of these KPIs was reached. This structure led to what some observers described as the industry’s first KPI‑triggered token generation event, designed to align token issuance with actual network performance rather than speculative timelines. When those criteria were met, the MEGA token went live on 30 April 2026 and was simultaneously listed on Binance, Coinbase, and eleven other centralized exchanges, which some commentators characterized as one of the largest token launches of the year in terms of distribution breadth and market attention. This extensive listing footprint was later complemented by availability on Robinhood’s Legend platform, further broadening access to retail traders in the United States.

MegaETH’s team also made a deliberate choice to launch without the aggressive incentive programs that had become standard in the Layer‑2 space. Public statements emphasized that the project had not run airdrops, points campaigns, or other “InfoFi” driven user acquisition schemes before launch, framing this as a rejection of inflated short‑term metrics in favor of slower, organic growth based on real usage. Instead, token distribution leaned heavily on the performance‑gated emission framework and on rewarding users who committed capital or activity in ways aligned with the protocol’s long‑term KPIs. This stance has been both praised and criticized: supporters see it as a healthier model for bootstrapping sustainable ecosystems, while skeptics question whether a high‑performance chain can build network effects quickly enough without the usual incentive playbook, especially in a cautious or “weak” crypto market.

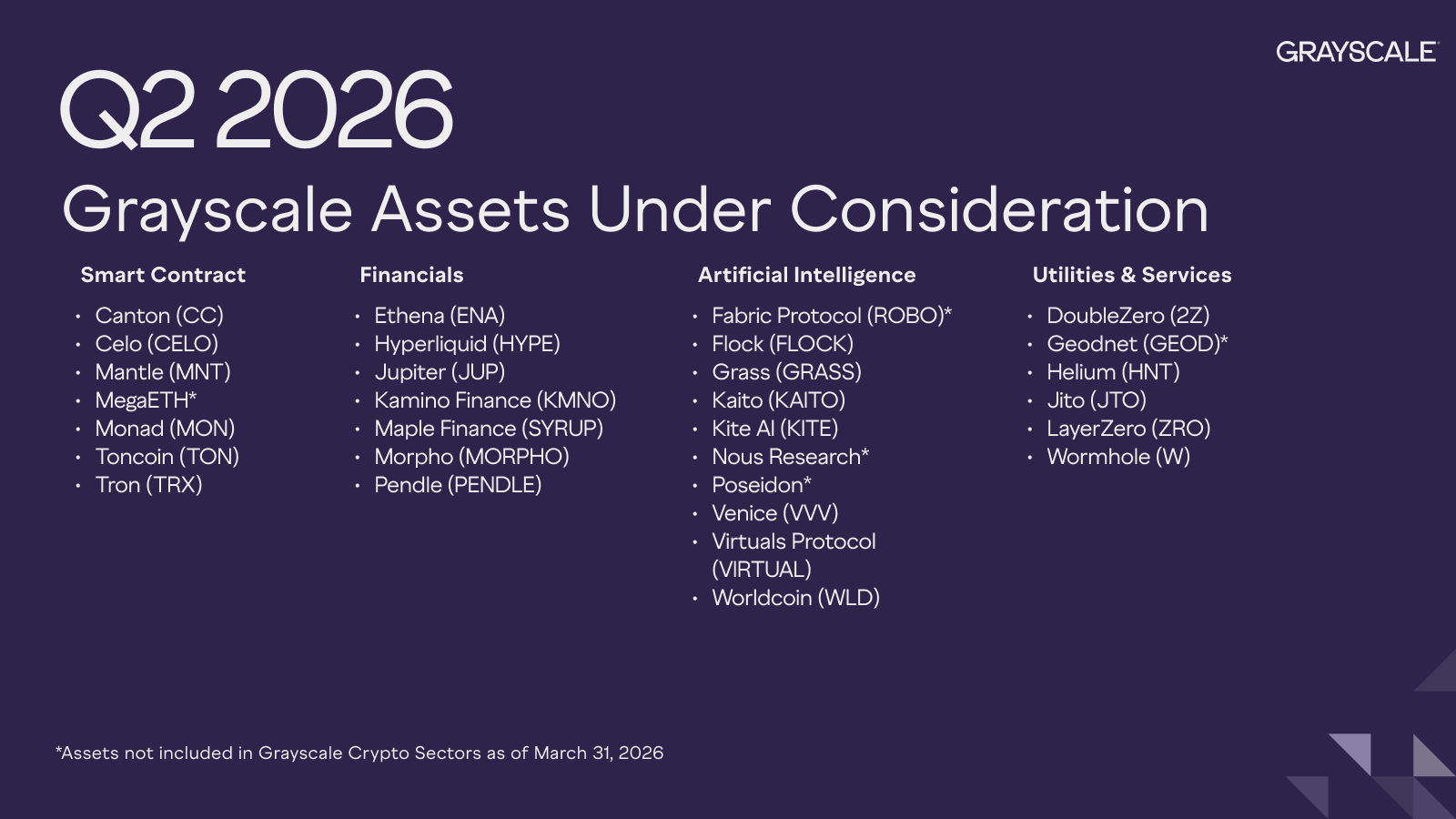

As with any new chain and token, early market conditions have been shaped by infrastructure decisions and upgrade cycles. For example, the Korean exchange Upbit announced a temporary suspension of MEGA deposits and withdrawals starting on 4 June, citing a necessary network upgrade and leaving the resumption time unspecified. Such pauses are relatively common when exchanges manage protocol upgrades to avoid user deposits landing on incompatible chain versions, but they can constrain short‑term liquidity and arbitrage opportunities while the upgrade is in progress. At the same time, institutional and quasi‑institutional actors have begun to take notice: Grayscale, one of the largest crypto asset managers, added MegaETH to its Q2 2026 list of digital assets under consideration for future investment products, signaling that MEGA could eventually feature in structured products alongside more established Layer‑1 and Layer‑2 tokens. These early signals point to a project that is simultaneously pushing technical boundaries and learning to operate within the risk frameworks of major exchanges and asset managers.

Architecture: How MegaETH Works Under The Hood

Heterogeneous Real‑Time Design

MegaETH departs from traditional rollup architectures by splitting the responsibilities of ordering, execution, and verification across specialized node roles, rather than requiring every node to do everything. Broadly, the network distinguishes between sequencers, which order transactions in real time; executors, which process those transactions in parallel; and verifiers or provers, which confirm results and maintain the integrity of the global state. This separation allows each node type to be optimized for its specific function, much as modern distributed systems allocate different tasks to specialized services or microservices rather than relying on monolithic servers. In principle, this enables MegaETH to scale horizontally—by adding more executor capacity, for example—while keeping the latency of transaction ordering extremely low through a carefully managed sequencer set.

Sequencers sit at the heart of MegaETH’s real‑time story. They are responsible for accepting incoming transactions, organizing them into a canonical order, and broadcasting this order to execution nodes with block intervals measured in milliseconds rather than seconds. Public commentary from the team has emphasized that MegaETH intentionally uses a small number of “beefy” sequencer machines, capable of very high throughput, to minimize network overhead and latency. Around these core sequencers, the protocol is designed to support a semi‑exclusive cohort of servers that can be rented by traders and market makers seeking extremely low‑latency connectivity, forming the basis for what MegaETH calls Proximity Markets. By shortening the time between transaction submission and ordering to under 10 milliseconds in many cases, MegaETH aims to give onchain applications the feel of a high‑speed centralized matching engine, while still anchoring finality to Ethereum.

Executors and verifiers handle the bulk of the computational work, processing ordered transactions and updating the network’s state in a way that can be efficiently audited and reconstructed. MegaETH’s technical literature highlights the use of concurrency and parallel execution, allowing independent transactions or state segments to be processed simultaneously rather than strictly sequentially. This is critical to achieving the network’s stated target of more than 100,000 transactions per second, which would be unattainable under purely sequential execution even on powerful hardware. The protocol also employs an approach termed Stateless Validation, which minimizes the local state that a node needs to hold in order to verify blocks; instead, nodes can fetch required state data on demand, making it possible for validators to operate using relatively modest hardware such as consumer laptops. This design is intended to counterbalance the centralizing effects of high‑performance sequencers by broadening the set of participants who can independently verify the chain’s correctness.

From a user perspective, the result of this architecture is meant to be real‑time interactivity. Instead of submitting a transaction and waiting several seconds for it to be included in a block and then several more blocks for confirmation, users on MegaETH can often see their transactions reflected in the network state essentially instantly. This enables use cases like ultra‑fast perpetual futures trading, where a price movement on an oracle feed can be acted upon and executed onchain without the delays that would normally drive traders back to centralized venues. It also opens up possibilities for interactive onchain games, streaming payments, and real‑time bidding systems, where each user action can be recorded and responded to onchain in human‑perceptible real time. In this sense, MegaETH is not just about raw TPS numbers but about trying to reconceptualize blockchain state as a continuously streaming medium.

Data Availability And Security Model

MegaETH is built as a Layer‑2 on Ethereum, meaning that its security model is ultimately meant to rest on Ethereum mainnet, even though day‑to‑day execution happens offchain. In practice, this involves periodically committing transaction data and state roots from MegaETH to Ethereum, where they can be challenged or audited through fraud proofs or validity proofs, depending on the specific rollup configuration. MegaETH’s public materials emphasize that the chain is “secured by Ethereum,” a phrase that signals it is not a sovereign Layer‑1 but instead relies on Ethereum for final settlement and dispute resolution. This approach is consistent with the broader rollup thesis in Ethereum’s roadmap, which holds that most user activity will eventually migrate to Layer‑2s while Ethereum serves as a high‑security base for data availability and consensus.

Data availability is a central concern for any rollup, because users need to be confident that they can reconstruct the state even if all Layer‑2 operators disappear or become malicious. While MegaETH’s core marketing focuses on latency and execution speed, the chain still must ensure that transaction data is posted somewhere accessible, whether directly to Ethereum or to a data‑availability layer that ultimately anchors to Ethereum. The project’s documentation and terms of use also make clear that the team reserves the right to monitor transactions for regulatory compliance and to suspend bridge operations in certain circumstances, for example when a security or compliance issue is detected. This kind of administrative control over bridging is not unique to MegaETH and is common for young Layer‑2s, but it underscores the extent to which early‑stage rollups often lean on social governance and operational discretion while their trust models are still evolving.

The trade‑off between performance and decentralization is particularly visible in MegaETH’s early security posture. The network currently relies on a relatively small set of sequencers and a project‑controlled multisignature for critical operations, reflecting an explicit choice to prioritize execution speed and developer experience in the short term. Critics argue that this places MegaETH closer to the “trusted operator” end of the spectrum, at least until the sequencer set and governance are further decentralized, and that users should treat the chain more like a high‑performance sidechain than a fully trust‑minimized rollup in its early years. Proponents counter that many applications benefiting most from MegaETH—such as high‑frequency derivatives trading—already rely on centralized or semi‑centralized infrastructure, and that the incremental trust placed in a well‑audited multisig is acceptable given the gains in latency and throughput. Over time, MegaETH’s evolution toward more distributed sequencer sets and permissionless validation will be a key indicator of how far it moves along the decentralization spectrum.

Real‑Time Oracles And Onchain Data Flows

For a real‑time blockchain, the speed of its oracle infrastructure is just as important as the speed of block production, because trading and lending protocols depend on external price feeds. MegaETH has leaned heavily into integrations with Chainlink, particularly Chainlink Data Streams, which are designed to deliver high‑frequency, low‑latency pricing data suitable for derivatives and other latency‑sensitive applications. When GMX, one of the largest onchain perpetual futures platforms, deployed on MegaETH, it specifically highlighted the combination of MegaETH’s 10‑millisecond block times and Chainlink’s high‑speed data feeds as a way to offer users near real‑time execution with reduced risk of oracle lag. In this setup, prices are updated and consumed onchain in sub‑second intervals, allowing liquidations and position updates to more closely track underlying markets than would be possible with slower feeds.

Chainlink has also broadened its presence on MegaETH beyond Data Streams, extending services such as cross‑chain interoperability (CCIP), proofs, and other data products to the network. This expansion is part of a broader strategy by oracle providers to support emerging Layer‑2 ecosystems and ensure that developers have access to the same tooling they expect on more established networks. For MegaETH, this means that builders can rely on familiar oracle primitives even as they experiment with novel execution patterns, bridging some of the perceived risk of deploying to a newer chain. At the same time, MegaETH’s real‑time orientation has attracted interest from other oracle projects and pricing networks that are exploring similarly low‑latency designs, creating a competitive landscape for how market data is delivered and standardized across DeFi protocols.

The reliance on fast, centralized oracle infrastructure introduces its own set of systemic risks. When most major derivatives protocols on a high‑speed chain use the same oracle provider and are updated on nearly identical timeframes, a sudden price spike or oracle malfunction can trigger tightly synchronized liquidations and cascading unwinds across the entire ecosystem. Observers have noted that as oracle network effects standardize pricing and risk models across protocols, it becomes more difficult to isolate or slow down cross‑protocol contagion during extreme events. MegaETH’s design, by minimizing latency between oracles, sequencers, and execution, amplifies these dynamics; the same qualities that make trading fairer and more responsive can make systemic events unfold more quickly. Designing circuit breakers, differential update intervals, and other risk‑management layers will therefore be an important part of building robust DeFi infrastructure on MegaETH.

Validation, Statelessness, And Decentralization

MegaETH’s concept of Stateless Validation is key to its claim that ordinary users can still meaningfully validate the network despite the presence of high‑performance sequencers. In traditional full nodes, validators must store the entire state—accounts, balances, contract storage—to verify new blocks, which can be resource‑intensive as the chain grows. MegaETH instead allows validators to operate without maintaining the full state locally; they can request the necessary state fragments on demand or rely on cryptographic proofs that a given state transition is valid. This reduces hardware requirements and opens the door for validation from consumer devices such as laptops, which in theory broadens participation and reduces the risk that only data‑center operators can verify the chain. If implemented and adopted widely, stateless validation could help address criticisms that high‑performance chains inevitably centralize verification.

At the same time, MegaETH’s architecture is candid about the fact that early‑stage block production and ordering are not as decentralized as on Ethereum mainnet or on more mature rollups. The small number of sequencers and the need for sophisticated infrastructure to run them mean that block production is, at least initially, concentrated among a limited set of operators, likely including the core team and strategic partners. Over time, the protocol roadmap envisions staking of MEGA tokens to decentralize sequencer rotation, allowing additional participants to join the sequencer set by bonding tokens and meeting hardware requirements. MEGA’s role in staking, governance, and incentive alignment is therefore tightly intertwined with the decentralization trajectory: as more MEGA holders stake to become sequencers or to vote on sequencer policies, the network’s operational control can gradually move away from the founding team.

Decentralization is not only a technical question but also a social and economic one. MegaETH’s governance will eventually have to address questions like who controls protocol upgrades, how fees and proximity‑market revenues are distributed, and how to manage emergency powers such as bridge suspension in transparent ways. The team’s research portal and public communications suggest an intention to evolve toward more open participation and formalized governance, but the path and timing remain open questions. For users and developers, understanding MegaETH’s current position on the decentralization spectrum—and how it plans to move along that spectrum—is critical for determining appropriate risk tolerances. In practice, many projects may treat MegaETH as a high‑beta, high‑performance environment suitable for certain types of trading and experimentation, while continuing to rely on more conservative rollups for long‑term asset storage and mission‑critical protocols.

Grayscale adds HYPE, PENDLE, VIRTUAL, and MegaETH among 30 assets to Q2 consideration list

Grayscale filed the S-1 for a spot HYPE ETF three weeks ago — adding it to the "consideration list" now is just catching the paperwork up to the product pipeline. PENDLE making the financials cut alongside Hyperliquid and Ethena is a deliberate play: yield tokenization is the closest DeFi primitive to TradFi interest rate derivatives, and that's exactly the kind of institutional pitch Grayscale knows how to package. Four competing HYPE ETF filings (Grayscale, Bitwise, 21Shares, VanEck) in under a month — that's the altcoin ETF race that actually has legs right now.

- 01GTE DEX institutional backing

Two separate GTE funding rounds — Echo/Cobie seed and Paradigm Series A — generated the top two most-clicked headlines, signaling readers treat GTE's fundraise as a bellwether for MegaETH's legitimacy as a DeFi venue.

- 02MEGA token sale mechanics and chaos↗

The $50M raise hitting $1B valuation, the botted predeposit campaign forcing a cap raise, outage-triggered refunds, and the eventual TGE formed a multi-part drama readers tracked as a stress test of the team's competence.

- 03Performance claims vs live benchmarks↗

Publication of real L2 performance numbers against the 100k TPS seed-round marketing drew readers hungry to verify whether the speed narrative held up under production conditions.

- 04USDm sequencer economics flywheel↗

Readers engaged with the novel model of funding sequencer operations via stablecoin reserve yield rather than fee markup, especially as Ethena's backing and the pre-deposit bridge gave it a concrete capital path.

- 05Ecosystem accelerator protocol buildout↗

MegaMafia 2.0 raising $40M+ for cohort projects, GMX deploying with 50x perps, MNX building AI-valuation futures, and Brix bringing EM yield collectively signaled whether the chain could attract serious builders beyond hype.

- 06Decentralization tradeoff and multisig risk

The Avon MegaVault shutdown, the rogue multisig that triggered early deposits and forced refunds, and the Stage 1 rollup debate crystallized the tension between speed-first design and trust assumptions readers expect on Ethereum L2s.

Tokens, Stablecoins, And The MegaETH Economic Model

MEGA Token Design And Tokenomics

The MEGA token is the native asset of the MegaETH network, serving as both the gas token for paying transaction fees and a governance and staking asset for the protocol. MegaETH’s documentation describes MEGA as the core of a “token business,” reflecting the view that the chain should generate and capture economic value in ways that are transparently linked to token holders rather than relying solely on venture capital or sequencer margins. MEGA has a fixed maximum supply of 10 billion tokens, placing it in the category of capped‑supply Layer‑2 tokens rather than inflationary models. At the time of the token generation event, approximately 1.13 billion MEGA—about 11.3% of the total supply—entered circulation, with the remainder locked and subject to performance‑based unlocks tied to network milestones and KPI achievements.

MegaETH’s tokenomics depart from standard vesting schedules in several ways. Instead of emitting tokens on a fixed linear or exponential curve, the protocol ties emissions to objective network milestones; when specific KPIs are achieved and independently attested, tokens are released to holders of so‑called commit positions. This design is intended to discourage purely speculative participation and instead reward those who are willing to commit capital or usage based on confidence in the protocol’s ability to hit real adoption metrics. In addition, a portion of MEGA’s supply is reserved for community contributors and early supporters through mechanisms such as The Fluffle, a soulbound NFT collection that recognizes early community builders and is linked to about 5% of the token supply. By using soulbound NFTs rather than transferable points, MegaETH aims to tie those allocations more closely to identities and contributions rather than purely to capital size.

From a market structure perspective, MEGA’s broad initial listing across major centralized exchanges, including Binance and Coinbase, gave it immediate liquidity and visibility that many Layer‑2 tokens do not have at launch. Later inclusion as a supported asset on Robinhood’s Legend platform further expanded access to retail investors in regulated markets. At the same time, the absence of a large retroactive airdrop or points campaign meant that there was less immediate selling pressure from sybil‑farmed wallets or short‑term incentive farmers. This created a somewhat unusual launch dynamic: a liquid, widely listed token with relatively constrained free float and a distribution geared toward performance‑linked emissions rather than upfront giveaways. Over time, as more KPIs are met and additional tranches of MEGA unlock, the token’s supply curve will increasingly reflect actual network activity levels rather than an exogenously set schedule.

Within the protocol, MEGA is designed to play multiple roles that go beyond gas. It is expected to be used for staking to participate in sequencer rotation, giving token holders a direct role in the block production process. It also functions as a governance asset, allowing holders to vote on protocol parameters, fee structures, and treasury usage once onchain governance is fully implemented. Moreover, MEGA is earmarked for ecosystem incentives such as developer grants, liquidity mining for key protocols, and community reward programs that align user growth with long‑term protocol health. The combination of capped supply, performance‑based unlocks, and multi‑role utility places MEGA among the more structurally complex Layer‑2 tokens, making its long‑term value heavily dependent on the success of MegaETH’s onchain economy and the credibility of its KPI framework.

USDm: Native Stablecoin And Yield Flywheel

Alongside MEGA, MegaETH introduces USDm, a native U.S. dollar‑pegged stablecoin designed specifically to power its real‑time economy. USDm is issued through a partnership with Ethena, a project focused on synthetic dollar products and yield‑bearing stable assets. At a technical level, USDm is backed by Ethena’s USDtb, which is described as a yield‑bearing asset linked to tokenized U.S. Treasury reserves, allowing USDm to maintain a 1:1 dollar peg while also generating offchain yield from traditional financial instruments. This structure effectively embeds a yield component into the stablecoin stack, with the underlying treasury yield flowing up from USDtb to Ethena and then, through a revenue‑sharing arrangement, to the MegaETH ecosystem.

MegaETH’s design leverages this structure to rewire how the network is funded. Instead of charging significant margins on sequencer fees—a common monetization model for other Layer‑2s—MegaETH aims to “redirect value from financial yield rather than users” by capturing a portion of the yield generated by USDm’s backing assets. The MegaETH Foundation receives rewards from the USDm issuer and uses those net rewards to buy back MEGA tokens on the market, creating a buyback flywheel that links stablecoin adoption directly to MEGA demand. As more applications denominate their activity in USDm and as users hold or transact in USDm, the aggregate yield from the backing Treasuries grows, increasing the funds available for MEGA buybacks. In May 2026, the foundation executed its first MEGA token buyback using all net rewards accrued from the USDm issuer up to that point, an event described as a test of the “USDm flywheel” and associated buyback flow.

In addition to buybacks, USDm is intended to serve as the primary unit of account and transactional medium within the MegaETH ecosystem. Protocols are encouraged to denominate liquidity pools, lending markets, and derivatives collateral in USDm, aligning user balances with the network’s native yield‑bearing stable asset. This stands in contrast to chains where U.S. dollar exposure is fragmented across multiple third‑party stablecoins issued offchain, often with little or no integration into the chain’s economic model. By embedding USDm as a first‑class citizen, MegaETH aims to build a real‑time onchain economy where payments, collateral, and incentives all revolve around a single, yield‑connected stable asset. Experiments like Avon’s MegaVault and USDmY concept—intended to keep stablecoin yield onchain and redirect it to users and network activity—reflect the broader ambition of knitting stablecoin yield into the fabric of MegaETH’s DeFi landscape, even though not all such experiments have persisted.

The USDm design, however, introduces exposure to offchain risks. Because the stablecoin’s backing ultimately depends on tokenized U.S. Treasury reserves and Ethena’s synthetic dollar machinery, any regulatory action, custody issue, or hedging failure in those layers could affect USDm’s stability or yield. MegaETH’s reliance on USDm for its economic model therefore implicitly imports traditional financial and regulatory risk into the chain’s core monetary system. This is not unique to MegaETH—many stablecoin ecosystems depend on offchain treasuries—but it underscores that the chain’s promise of funding itself from “yield instead of users” is contingent on the continued smooth functioning of these underlying instruments. For users and developers, understanding USDm’s risk profile is as important as understanding MEGA’s tokenomics, especially when designing protocols that rely on USDm as their primary collateral or settlement asset.

Proximity Markets And Monetization Of Low Latency

One of MegaETH’s most distinctive economic design choices is the concept of Proximity Markets, a mechanism for monetizing the chain’s low‑latency capabilities by selling prioritized network access to traders who value it most. Instead of charging users uniformly higher gas fees or extracting value through opaque sequencer surcharges, MegaETH proposes to “tax proximity to the sequencer” by offering tiers of low‑latency connectivity that can be rented by market makers, high‑frequency traders, and other latency‑sensitive actors. In practice, this might involve a tiered bidding system where participants pay for privileged placement in the network’s topology—for example, co‑locating their servers physically or logically closer to sequencers, or gaining access to lower‑latency transaction relays. The central assumption is that traders who can profit from microsecond‑scale advantages are willing to pay for them, creating a revenue stream that does not directly penalize ordinary users making standard transactions.

This approach mirrors, in some respects, the way traditional exchanges monetize co‑location and low‑latency connections for high‑frequency trading firms. Exchanges sell rack space in their data centers and premium connection services to firms that compete on speed, generating revenue that subsidizes the broader platform. MegaETH’s proximity markets attempt to transplant this model into an onchain context, with the added twist that the underlying blockchain itself is designed to operate at extremely low latency. The economic implication is that the value of MegaETH’s speed becomes an explicit, priced resource rather than an unpriced externality. Traders pay for access to latency advantages, and the proceeds can be routed to the protocol treasury, MEGA buybacks, or other forms of value accrual for token holders.

The proximity‑market model raises important questions about fairness and market structure. Critics worry that formalizing paid access to low‑latency connectivity could entrench advantages for large, well‑capitalized trading firms and increase informational asymmetries between them and retail users. Proponents counter that such asymmetries already exist in practice, given the realities of network geography and infrastructure, and that by making them transparent and protocol‑mediated, MegaETH at least allows the resulting revenue to be captured and redistributed rather than leaking to private infrastructure providers. In any case, MegaETH’s willingness to design monetization around low‑latency services rather than purely around gas suggests a broader rethinking of how blockchains can generate sustainable revenue while keeping basic transaction fees low. The success or failure of proximity markets will likely be a key case study in whether real‑time chains can balance efficiency with perceived fairness.

Buybacks, Treasury, and The “Token Business” Narrative

The first MEGA token buyback on 7 May 2026, funded entirely from net USDm issuer rewards, was symbolically important for MegaETH’s self‑presentation as a “token business.” Rather than relying on governance proposals or manual treasury interventions, the chain’s design effectively automates a pathway from ecosystem growth to token demand: as USDm usage increases and generates more yield, the foundation accumulates more rewards, which can then be used to repurchase MEGA on the open market. This mechanism is meant to create structural buy pressure that scales with the success of MegaETH’s stablecoin economy, thereby aligning tokenholder interests with the growth of onchain activity in a direct, quantifiable way. At the time of that first buyback, commentary highlighted that the MEGA supply in circulation was approaching approximately 480 million tokens, giving some concrete sense of the scale at which these buybacks might operate.

More broadly, MegaETH’s leadership has argued that one of the core issues facing the crypto industry is the lack of clear economic rationale for many tokens—hence the rhetorical emphasis that “MegaETH is a token business.” By tying MEGA’s value accrual to concrete revenue streams such as USDm yield capture and proximity‑market fees, the project attempts to distinguish itself from tokens whose value rests primarily on speculative demand or vague governance rights. In this framing, MEGA is akin to an equity‑like claim on the cash flows generated by a real‑time blockchain platform, though without the legal rights of actual equity. This narrative has resonated with some investors and analysts who are increasingly focused on onchain cash flow models and token products that approximate traditional business fundamentals.

At the same time, the success of this model depends on disciplined treasury management and transparent reporting. Token buybacks funded from USDm rewards need to be conducted in ways that do not unduly distort markets or favor particular counterparties, and the governance process around how much revenue is allocated to buybacks versus ecosystem grants or reserves must be clearly articulated. As MegaETH matures, the interaction between MEGA’s supply curve, buyback schedule, and treasury strategy will be watched closely by both traders and long‑term holders, especially as more sophisticated institutional investors, such as those behind products like potential Grayscale vehicles, evaluate whether MEGA fits within their risk and valuation frameworks. In this sense, MegaETH is not only a technical experiment in real‑time execution but also a financial experiment in how a Layer‑2 can be run like an onchain business.

Ecosystem, Applications, And Use Cases

High‑Speed Trading And Derivatives: GMX, MNX, And Beyond

Trading and derivatives are the most immediately obvious beneficiaries of MegaETH’s real‑time performance. The deployment of GMX, one of the most battle‑tested perpetual futures platforms in DeFi, onto MegaETH marked an important vote of confidence in the chain’s suitability for serious trading. On MegaETH, GMX users can trade perpetual swaps on major assets such as BTC, ETH, and SOL with up to 50x leverage, benefiting from deep liquidity, competitive fees, and high‑speed onchain execution that makes use of the chain’s 10‑millisecond block times. GMX’s integration leverages Chainlink’s data standard and Data Streams for asset pricing, meaning that the combination of a real‑time oracle feed and a real‑time execution environment can offer near‑instant execution and pricing updates for leveraged positions. This setup allows traders to experience something much closer to centralized exchange responsiveness while retaining the non‑custodial, transparent attributes of DeFi.

The MegaETH deployment is GMX’s eighth chain integration, following earlier expansions to networks such as Arbitrum and Avalanche, and it is framed as an opportunity to test “MegaETH‑specific optimizations” that unlock the full potential of real‑time onchain execution. Initially, GMX prioritized reliability by porting its existing, time‑tested architecture—responsible for over 360 billion dollars in cumulative trading volume—to MegaETH with minimal changes. Over time, the plan is to roll out features that are uniquely enabled by MegaETH’s low latency, such as more granular liquidation logic, advanced order types, or tighter spreads based on faster price propagation. The presence of GMX also provides a template for other derivatives projects evaluating MegaETH: it shows that a flagship perp venue can run on the chain using existing infrastructure while gradually layering in real‑time features.

Another high‑profile ecosystem project is MNX, a decentralized futures exchange focused on the AI economy and built natively on MegaETH. MNX raised 6.4 million dollars in a pre‑seed funding round led by Village Global, with a reported 40 million dollar valuation, to build specialized futures and prediction markets tied to AI‑related assets such as computing power, AI lab valuations, and equity‑like perpetual contracts. By using MegaETH as its base chain, MNX aims to provide a fast, efficient trading environment tailored to technology professionals and crypto market participants who want to speculate on or hedge AI‑linked exposures, ranging from GPU rental prices to the implied valuations of private AI companies. MegaETH’s high throughput and low latency are particularly relevant here, since markets for AI resources can be highly volatile and require rapid re‑pricing to reflect real‑world developments. The MNX case illustrates how MegaETH’s performance profile can attract niche but potentially large categories of derivatives that are difficult to host on slower chains.

The broader trading ecosystem on MegaETH is likely to extend beyond major platforms like GMX and MNX. Experimental trading games and social‑trading products have begun to appear on the network, taking advantage of rapid state updates to create arcade‑like experiences around speculation and price discovery. These range from “tap trading” interfaces that gamify micro‑positioning in markets, to experimental competitions that reward users for rapid decision‑making in low‑latency environments. While such initiatives are still early and may not all persist, they demonstrate the breadth of applications that become feasible when onchain responsiveness is measured in milliseconds rather than seconds. In aggregate, they reinforce the idea that MegaETH is emerging as a specialized venue for real‑time financial experiments.

Real‑World Assets, Yield, And Institutional Onboarding

Beyond pure trading, MegaETH’s economic architecture and USDm stablecoin create a natural fit for real‑world asset (RWA) protocols that want to tokenize yield‑bearing securities and plug them into a high‑speed DeFi environment. Projects like Brix, for instance, have raised multi‑million‑dollar rounds to build institutional‑grade yield products on MegaETH, backed by entities such as Circle Ventures and ConsenSys, with a focus on tokenizing emerging‑market sovereign or corporate debt and making those yields accessible onchain. While such efforts are still in their early phases, they align closely with MegaETH’s narrative of redirecting traditional financial yield into onchain economies, whether through USDm’s Treasury‑linked backing or through dedicated RWA platforms that issue tokenized claims on yield streams.

In this context, MegaETH serves as both a settlement layer and an execution environment for complex fixed‑income strategies. Institutional users or sophisticated DeFi participants might deposit capital into RWA vaults that hold tokenized treasuries, corporate bonds, or structured credit, receiving onchain tokens that accrue yield over time. These tokens can then be used as collateral in MegaETH‑based lending markets, traded on DEXs, or integrated into structured products like leveraged yield vaults. The chain’s low fees and high throughput make it easier to rebalance positions, roll over maturities, or implement algorithmic yield strategies without incurring prohibitive gas costs. As more traditional institutions experiment with tokenization, MegaETH’s ability to offer fast, composable DeFi integration may become a differentiating factor.

The intersection of RWAs and MegaETH also has regulatory implications. Bringing tokenized treasuries and similar instruments onto a high‑speed, globally accessible chain raises questions about securities compliance, KYC/AML, and jurisdictional risk, particularly if assets are offered to retail users. MegaETH’s terms of use acknowledge that the network may monitor transactions for compliance and suspend bridge operations when necessary, suggesting an awareness that regulatory interfaces will be part of its operating reality. For RWA protocols, MegaETH’s willingness to engage with these issues may be a positive signal, but it also means that the platform sits at the frontier of how traditional financial regulation interacts with real‑time, programmable markets.

Identity, Naming, And Agent‑Driven Infrastructure

While trading and RWAs dominate early narratives, MegaETH’s real‑time architecture also opens interesting possibilities in identity and naming. The emergence of services like MegaName Market, which offers a fully onchain, cross‑chain .mega naming system, illustrates how high‑speed chains can become hubs for identity infrastructure. By making name registration, resolution, and updates happen nearly instantaneously, MegaETH can support naming systems that feel as responsive as Web2 DNS while offering the composability and transparency of smart contracts. Builders of such systems have reported using AI agents to significantly accelerate development, pointing to the growing interplay between AI tooling and blockchain engineering in fast‑moving ecosystems.

In practice, onchain naming systems on MegaETH might be used for wallet aliases, application‑specific identifiers, or cross‑chain routing of messages and assets. The low latency allows for interactive flows—such as auctions for premium names or time‑sensitive name‑based rewards—that would be clunky on slower chains. Over time, such naming and identity primitives could also be integrated with reputation systems, KYC attestations, or social graphs, turning MegaETH into a substrate for real‑time identity‑aware applications. This complements the network’s financial focus by enabling more granular access control, credit scoring, and personalized UX, all anchored to fast‑updating onchain identifiers.

The use of AI agents in building MegaETH infrastructure hints at another frontier: agentic onchain systems. As developers increasingly rely on AI assistants to write and audit smart contracts, it becomes easier to experiment with complex protocols that respond dynamically to real‑time data. On a chain like MegaETH, AI agents could even interact directly with onchain markets, executing trading or rebalancing strategies in milliseconds based on external signals. While this raises its own concerns about systemic risk and coordination, it underscores the possibility that MegaETH could become a preferred environment for AI‑driven autonomous agents, precisely because its latency profile matches the time horizons at which those agents operate.

Stablecoin Yield, Vaults, and Experimental DeFi Primitives

MegaETH’s stablecoin‑centric design has already inspired a wave of experimental DeFi primitives aimed at capturing and redistributing USDm yield. Avon’s MegaVault and USDmY initiatives, for example, were designed to keep stablecoin yield onchain within the MegaETH ecosystem, turning USDm into a native, yield‑bearing asset whose returns flow back to users, applications, and network activity. The logic is straightforward: if USDm’s backing assets already generate yield, and if part of that yield is shared with the MegaETH foundation, why not build vaults and structured products that allocate a portion of that yield directly to users rather than intermediaries? By doing so on a real‑time chain, such vaults can rebalance and distribute returns more frequently, potentially offering finer‑grained yield products.

However, the subsequent decision by Avon to halt its MegaETH deployment and shut down MegaVault, urging users to withdraw funds as the project pivoted, highlights the experimental and sometimes fragile nature of early‑stage DeFi on new chains. While the core idea of yield‑bearing USDm remains intact, specific implementations may fail for reasons ranging from product‑market fit to risk management challenges. For MegaETH, the lesson is that even in a high‑speed environment, the usual DeFi caveats apply: users must consider smart contract risk, protocol governance, and the possibility that apps may be discontinued or restructured. The chain’s low latency does not magically eliminate business or execution risk; it simply changes the tempo at which such risks materialize.

Despite such setbacks, the direction of travel is clear: DeFi builders on MegaETH are exploring ways to harness USDm’s yield and integrate it into lending markets, leveraged yield strategies, and liquidity vaults. Over time, one can expect to see USDm‑denominated liquidity vaults, similar to those already supporting GMX’s perp markets, expand in sophistication, providing diversified portfolios of stablecoin strategies that rebalance in real time. The combination of fast execution, onchain composability, and embedded yield creates fertile ground for complex, automated products that would be impractical on slower or more expensive networks.

Tooling, Research, And Developer Experience

On the developer side, MegaETH has invested in a research‑driven culture and a suite of tools aimed at making real‑time development as accessible as possible. The project’s research portal aggregates papers and technical notes on topics such as real‑time blockchain design, stateless validation, and heterogeneous execution, giving builders insight into the protocol’s inner workings and roadmap. This emphasis on open research helps attract technically sophisticated teams that are comfortable navigating a fast‑moving, experimental environment. At the same time, MegaETH maintains full EVM compatibility, meaning developers can use familiar languages like Solidity and standard Ethereum tooling such as MetaMask, Hardhat, and common libraries without significant modification.

Developer experience is further enhanced by MegaETH’s low fees and fast confirmation times. For teams used to iterating on testnets or slower mainnets, deploying to a chain where transactions confirm in milliseconds can significantly speed up the development and debugging cycle. Real‑time state streaming also opens up new patterns in frontend design, where applications can subscribe to live feeds of state changes rather than polling or waiting for multiple block confirmations. This enables richer, more interactive UX, such as real‑time dashboards, collaborative onchain tools, and streaming payments interfaces. As more developers experiment with these paradigms, MegaETH could become a hub for onchain real‑time app design patterns, influencing how other chains think about their own developer ergonomics.

Chainlink’s expansion of services like CCIP, proof systems, and data feeds to MegaETH also improves the developer experience by ensuring that critical middleware is available from day one. When combined with other infrastructure providers—indexers, RPC providers, analytics platforms—this ecosystem support makes it easier for teams to treat MegaETH as a first‑class deployment target rather than a secondary experiment. Over time, the richness of the tooling ecosystem may be as important as raw TPS in determining whether MegaETH attracts and retains high‑quality applications.

MegaETH-based futures exchange MNX raised $6.4M at a $40M valuation to build trading markets around AI company valuations, compute resources, equities, and prediction markets

200ms batch auctions plus a team-run HLP vault is a Hyperliquid/Lighter-shaped way to bootstrap liquidity, but AI exposure makes adverse selection nastier than perps on BTC or SOL. Compute perps tied to SemiAnalysis indices and markets on benchmark scores/product launches run straight into the same insider-flow problem Kalshi is now trying to patch with employer disclosures; add leverage and the oracle/resolution layer becomes the risk surface. If MNX can make those contracts cleanly collateralizable, MegaETH gets native non-crypto order flow instead of another farmed perp venue.

- 2024-11milestone

$20M seed round announced; 100k TPS claim publicized

- 2025-03launch

Public testnet launched March 6; user onboarding March 10

- 2025-03milestone

The Fluffle NFT collection sold, generating $28M

$50M MEGA token sale closes in minutes at $1B valuation

- 2025-05governance

Pre-deposit campaign botted; cap raised to $1B; outages and rogue multisig trigger full refund

Frontier mainnet pre-deposit bridge launched with $250M USDC→USDm cap

GMX deploys on MegaETH with 50x leverage perps and Chainlink 10ms execution

- 2025-06governance

Avon halts MegaETH deployment; MegaVault shutdown announced, users urged to withdraw

Trading, Liquidity, And Market Infrastructure

Listings, Exchange Support, And Institutional Interest

From a markets perspective, MegaETH and MEGA have achieved unusually broad exchange support relative to their age. The MEGA token’s initial listing on Binance, Coinbase, and eleven other centralized exchanges at the time of the TGE gave it a global footprint and deep order books from the outset. This broad distribution was later complemented by listing on Robinhood Legend, which added MEGA to a curated set of digital assets available to U.S. users on a mainstream trading app. The combination of Tier‑1 exchange support and retail platforms means that MEGA trades in a relatively mature market structure compared to many newer Layer‑2 tokens that initially rely on a handful of regional exchanges or DEXs.

Institutional interest has also started to surface. Grayscale’s decision to add MegaETH to its Q2 2026 list of assets under consideration for future investment products suggests that analysts at large asset managers see MEGA as a candidate for inclusion in trusts or ETFs that target Ethereum scaling or broader DeFi exposure. While “under consideration” does not guarantee that a product will be launched, the inclusion itself often signals that the asset has reached a threshold of liquidity, infrastructure support, and regulatory plausibility. Combined with venture funding into MegaETH‑native projects like MNX and RWA platforms, this points to a growing ecosystem of stakeholders whose business models and products depend on MegaETH’s long‑term viability.

At the same time, exchange‑level operational decisions remind users that infrastructure risk is part of the picture. Upbit’s temporary suspension of MEGA deposits and withdrawals for a network upgrade, with no fixed resumption time, highlights how layer‑2 protocol changes can affect centralized exchange operations and, by extension, the ability of users to move tokens in and out of those venues. During such windows, onchain activity may diverge from exchange pricing, and arbitrageurs may be constrained in their ability to realign markets. For traders and liquidity providers, understanding the upgrade cadence and communication practices of both MegaETH and the exchanges that list MEGA is therefore essential to managing operational and liquidity risk.

Onchain Liquidity, Bridges, And Settlement

Onchain, MegaETH supports a growing array of liquidity pools, DEXs, and bridges that facilitate movement of assets between MegaETH, Ethereum, and other chains. GMX’s deployment, backed by USDm‑denominated liquidity vaults, provides one anchor for derivatives liquidity, while spot DEXs and lending markets build around USDm and MEGA as core assets. Bridges play a crucial role in moving assets from Ethereum and other ecosystems into MegaETH, enabling users to bring collateral and liquidity into the high‑speed environment. MegaETH’s terms of use explicitly note that the team may monitor transactions and suspend bridge operations for security or compliance reasons, which has implications for how bridges are designed and governed. In practice, this means that while bridges are critical to liquidity, they may operate under more centralized oversight than in fully permissionless environments, at least in the early stages.

Chainlink’s expansion of CCIP and other cross‑chain services to MegaETH also influences the shape of onchain liquidity. By providing standardized messaging and transfer primitives, these services make it easier for protocols to move value across chains in a composable way, potentially using MegaETH as an execution layer while settling or collateralizing positions elsewhere. For example, a protocol could accept collateral on Ethereum, tokenize claims on that collateral via CCIP, and trade or hedge those claims on MegaETH’s real‑time markets. This kind of architecture blurs the distinction between “home” and “foreign” chains, positioning MegaETH as part of a multi‑chain liquidity fabric rather than an isolated island.

Settlement dynamics on MegaETH are shaped by its real‑time nature. For traders, the difference between “soft” and “hard” finality may feel less pronounced, because transactions appear and are executed almost instantly, even if their ultimate settlement onto Ethereum takes longer. However, during stress events or in the presence of bugs, the ability to roll back or challenge batches on Ethereum remains crucial. Users relying on MegaETH for high‑value settlement must therefore understand both the chain’s internal finality guarantees and the timeline and mechanisms for rolls‑up to Ethereum. The presence of centralized bridge and sequencer controls adds another layer of complexity: in some scenarios, social consensus or administrative intervention could override purely technical finality, which is important to consider when using MegaETH for large transfers or long‑term storage.

Market Structure, Liquidity Risks, and User Behavior

MegaETH’s choice to forgo large airdrops and points campaigns has implications for market structure and liquidity. Without a broad base of airdrop farmers and sybil accounts dumping tokens at TGE, the initial MEGA market may have had a different profile, with a higher proportion of tokens held by committed participants and fewer immediately sellable “free” allocations. On the other hand, this also means there may be fewer small holders, and liquidity can be more concentrated among early investors, strategic partners, and those who acquired tokens on exchanges. As performance‑based emissions unlock more MEGA to users with commit positions, the token’s float and holder distribution will evolve, potentially smoothing liquidity over time.

Liquidity risk on MegaETH is not limited to the MEGA token. Stablecoins, RWAs, and derivatives positions all carry their own liquidity profiles, which can be stress‑tested in unusual ways by the chain’s real‑time design. For instance, in a sudden market move, a combination of fast oracle updates and fast block times can trigger rapid cascades of liquidations in perp markets, which in turn force the selling of collateral assets into potentially thin liquidity. If bridges are congested or temporarily suspended due to upgrades or security measures, participants may be unable to move collateral off MegaETH to other venues, exacerbating local volatility. Designing robust risk management—such as throttled liquidation mechanisms, adaptive fee models, and circuit breakers—will therefore be crucial for protocols operating in MegaETH’s environment.

User behavior is shaped by these dynamics. Traders attracted by 10‑millisecond execution and high leverage may cluster on MegaETH precisely because it offers advantages not available elsewhere, but they need to be aware that the same speed can magnify both gains and losses. Long‑term holders and DeFi users must weigh the benefits of yield and composability against the risks of a relatively young chain whose security and governance are still maturing. Over time, the balance of speculative trading, yield farming, and long‑term utility usage will determine whether MegaETH becomes primarily a high‑frequency trading hub or evolves into a more broadly diversified ecosystem.

Security, Risks, And Controversies

Rollup Security, Centralization, And Trust Assumptions

By branding itself as a real‑time Ethereum Layer‑2, MegaETH implicitly invites scrutiny of its security model and trust assumptions. The core claim is that MegaETH is “secured by Ethereum” in the sense that transaction data and state commitments are posted to Ethereum, enabling users to reconstruct the chain and challenge invalid state transitions if necessary. However, as with many young rollups, the degree of actual trust minimization can differ significantly from the long‑term ideal. In MegaETH’s current form, the small set of powerful sequencers and the presence of project‑controlled multisigs for key operations mean that users are, to a nontrivial extent, trusting the operator set not to censor or reorder transactions maliciously, and to manage upgrades and bridge operations responsibly.

This reality has led some commentators to argue that MegaETH is effectively challenging the relevance of “Stage 1” rollups—which prioritize full decentralization and trustless operation from day one—by demonstrating that many users may be willing to accept more centralized trust assumptions in exchange for better user experience. From this perspective, MegaETH is testing whether user preference for speed, low fees, and smooth developer tooling can outweigh concerns about who controls sequencers or how quickly fraud/validity proofs are enforced. The outcome of this experiment will have implications beyond MegaETH: if real‑time chains gain significant market share, other Layer‑2s may feel pressure to optimize for performance and UX even at the cost of stricter decentralization, leading to a more heterogeneous landscape of security models.

MegaETH’s terms of use and early governance structure reflect an awareness of these trade‑offs. By explicitly reserving the right to monitor transactions for regulatory compliance and suspend bridge operations for security reasons, the project acknowledges that human judgment and centralized decision‑making are part of its operational reality. Over time, the challenge will be to migrate these powers into transparent, accountable governance frameworks without undermining the chain’s ability to respond quickly to threats. For users, the key is to treat MegaETH’s trust model as an evolving spectrum rather than a binary, and to align their exposure and use cases accordingly. High‑frequency trading or experimental DeFi strategies may be appropriate, while long‑term cold storage of large balances might remain on Ethereum mainnet or more conservative rollups until MegaETH’s decentralization matures.

Wallet‑Level Risks, Hacks, and User Safety

Not all security incidents on MegaETH reflect on the protocol itself; some arise from user‑level vulnerabilities such as compromised private keys. A widely discussed case involved the draining of a MegaETH wallet belonging to a well‑known DeFi educator, whose address reportedly lost around 42,000 dollars worth of assets in what appeared to be a private key hack. Available reports suggest that this was not the result of a protocol exploit or MegaETH‑specific vulnerability, but rather a standard key compromise, which can happen through phishing, malware, or reuse of keys across insecure platforms. Nevertheless, incidents like this can shape perceptions of a new chain’s safety, especially when they involve prominent community members.

The lesson is that traditional self‑custody best practices remain essential, perhaps even more so on high‑speed chains where malicious actors can move stolen funds through multiple protocols in milliseconds. Users should be cautious about connecting wallets to unfamiliar dApps, signing arbitrary messages, or using browser extensions that may be compromised. Hardware wallets, multi‑sig setups, and other security measures are just as valuable on MegaETH as on any other chain. Given MegaETH’s role as a hub for high‑frequency trading, some users may also maintain separate wallets for trading and long‑term holding, reducing the blast radius if a hot wallet is compromised. Educating users about these practices will be an important part of the ecosystem’s maturation.

Real‑Time Risk, Liquidations, and Oracle Dependencies

MegaETH’s defining characteristic—its real‑time execution—creates unique risk dynamics, particularly in leveraged markets. In a typical DeFi environment with multi‑second block times and slower oracle updates, there is often a small buffer between rapid price moves and onchain reactions, allowing some slippage and delay but also giving participants time to respond. On MegaETH, by contrast, 10‑millisecond block times combined with high‑frequency oracle feeds can cause liquidations and margin calls to cascade almost instantaneously, with little room for manual intervention. For traders, this increases the importance of robust risk management, such as conservative leverage, hedging strategies, and monitoring tools that can keep pace with onchain changes.

The dependence on centralized oracle providers like Chainlink further concentrates risk, even as it improves user experience. If a Chainlink Data Stream for a particular asset were to malfunction, be attacked, or experience a sudden delay, the resulting mispricing could propagate rapidly across multiple MegaETH protocols that rely on that feed. In real‑time environments, such disruptions could lead to mass liquidations or arbitrage opportunities that are exploited by bots faster than human users can react. Designing redundancy into oracle architectures—such as multi‑oracle setups, sanity checks, and dynamic update intervals—will be critical for mitigating these risks on MegaETH. The same is true for alternative oracle networks that are optimizing for real‑time chains; as their network effects grow, the potential for cross‑protocol contagion during oracle anomalies increases.

Another dimension of real‑time risk is MEV (miner or maximal extractable value). On a chain where block times are measured in milliseconds, MEV bots and sequencers have more granular opportunities to reorder or insert transactions around user trades, liquidations, or arbitrage. MegaETH’s proximity markets and controlled sequencer set provide tools to manage these dynamics—by, for example, aligning incentives between sequencers and the protocol—but they also raise questions about how MEV is captured and distributed. If low‑latency access is sold to traders, the distinction between MEV extraction and latency arbitrage can blur. Over time, MegaETH will need to articulate a clear MEV policy, whether through auctions, rebates, or other mechanisms, if it wants to avoid opaque or unfair value extraction.

Regulatory, Compliance, And Governance Challenges

Given its focus on real‑time trading and yield‑bearing stablecoins, MegaETH sits squarely at the intersection of DeFi and traditional financial regulation. USDm’s backing by tokenized U.S. Treasuries and Ethena’s synthetic dollar mechanisms means that part of MegaETH’s core monetary system depends on access to U.S. securities markets and compliant custody arrangements. Regulatory changes that affect tokenized treasuries, synthetic dollars, or yield‑bearing stablecoins could therefore have direct implications for USDm’s operation. Similarly, derivatives platforms like GMX and AI‑focused futures exchanges like MNX raise questions about the classification of perpetual swaps and prediction markets under various jurisdictions’ securities and commodities laws. While these issues are not unique to MegaETH, the chain’s positioning as a high‑speed trading venue may attract particular scrutiny.

MegaETH’s terms of use, which reserve the right to monitor transactions and suspend bridge operations for compliance reasons, reflect a pragmatic acceptance that regulatory interfaces will be part of the chain’s life. This could involve cooperating with law enforcement in cases of clear criminal activity, implementing sanctions screening at the bridge level, or adjusting protocol parameters in response to regulatory guidance. The challenge is to do so in ways that maintain user trust and avoid arbitrary or opaque interventions. As governance decentralizes, token holders may play a larger role in setting the boundaries of compliance, potentially through onchain votes about how and when to respond to legal demands.

Governance itself is another area of risk and controversy. MegaETH’s roadmap envisions MEGA‑based governance over sequencer selection, protocol upgrades, and treasury usage, but the details of how this will be implemented—and how quickly control will shift from the founding team to the community—remain in development. Poorly designed governance can lead to capture by large token holders, voter apathy, or decision‑making that prioritizes short‑term price appreciation over long‑term security and resilience. For MegaETH, whose economic model ties token value closely to protocol revenue and ecosystem growth, aligning governance with sustainable business practices will be particularly important.

- CentralizationHigh

MegaETH relies on a single sequencer for real-time execution and a small multisig for governance; a rogue multisig action directly caused the pre-deposit early-trigger incident requiring full refunds.

- Smart Contract / ProtocolMedium

Avon's MegaVault was shut down and users were urged to withdraw immediately mid-deployment, demonstrating that ecosystem protocols on MegaETH can fail or pivot abruptly, leaving depositors exposed.

The $50M MEGA token sale closed at a $1B valuation within minutes before the mainnet was live, a structure that prices in near-perfect execution and leaves token holders holding illiquid upside against a still-maturing chain.

- LiquidityMedium

The pre-deposit campaign attracted botted demand forcing a cap increase to $1B, and subsequent outages required a full refund — indicating fragile liquidity coordination mechanisms ahead of Frontier mainnet.

MEGA's listing on Robinhood and inclusion on Grayscale's Q2 consideration list, combined with a public token sale structure, increases the surface area for securities classification scrutiny in the US.

MegaETH has integrated Chainlink CCIP, Data Feeds, and CRE alongside RedStone Bolt as a latency-optimized oracle, reducing single-oracle dependency risk, though 10ms block times push oracle update assumptions to their limits.

MegaETH In The Layer‑2 Landscape

Performance Comparisons and Design Trade‑Offs

To understand MegaETH’s position among Ethereum scaling solutions, it is helpful to compare its performance targets with those of other networks. Ethereum mainnet processes around 15 transactions per second under typical conditions, with block times of roughly 12 seconds. Leading general‑purpose rollups such as Arbitrum process on the order of 20 transactions per second, while Base handles slightly more, though both can spike higher under load. MegaETH, by contrast, targets throughput exceeding 100,000 transactions per second and block times under 10 milliseconds, putting it in a different performance category altogether. While these are target metrics rather than constant realized values, they illustrate the magnitude of MegaETH’s ambition.

A simplified comparison can be summarized as follows:

| Network | Approx. TPS (typical) | Block Time (approx.) | Execution Environment |

|---|---|---|---|

| Ethereum L1 | ~15 | ~12 seconds | Monolithic, EVM |

| Arbitrum | ~20 | ~0.25–0.5 seconds | Rollup, EVM |

| Base | Slightly above 20 | ~0.25–0.5 seconds | Rollup, EVM |

| MegaETH | Target >100,000 | <10 milliseconds | Real‑time L2, EVM |

Figures for Ethereum, Arbitrum, and Base are drawn from typical operational numbers; MegaETH’s figures are targets reported in its documentation and ecosystem analyses. While the exact TPS realized in production can vary, the relative differences are stark. MegaETH achieves this by embracing a specialized architecture, high‑performance sequencer hardware, and a willingness to centralize certain functions in the short term. The trade‑off is clear: higher performance at the cost of stricter trust assumptions, at least until the network’s decentralization roadmap progresses.

For developers and users, the choice between MegaETH and other L2s will often come down to application requirements. A lending protocol primarily concerned with capital efficiency and composability might prefer a more conservative rollup if its users value strong censorship resistance and smoother decentralization trajectories. A high‑frequency derivatives platform, by contrast, might find MegaETH’s latency profile irresistible, even if it entails more operator trust. In this sense, MegaETH contributes to a broader diversification of the rollup ecosystem, where different chains optimize for different points on the performance‑decentralization spectrum rather than converging on a single design.

Stage‑1 Rollups, User Preferences, and Competitive Dynamics

MegaETH’s explicit prioritization of speed, low fees, and developer experience over maximal decentralization has sparked debate about the relevance of so‑called “Stage 1” rollups, which strive to be fully trustless and permissionless from the outset. Some argue that MegaETH’s popularity—or lack thereof—will be a real‑world referendum on whether users truly value the strongest decentralization guarantees when given a compelling alternative. If traders, gamers, and DeFi users flock to a real‑time chain with a small sequencer set and centralized upgrade paths, it might suggest that for many use cases, user experience is paramount, and that decentralization beyond a certain threshold yields diminishing perceived returns.

On the other hand, it is possible that MegaETH will occupy a niche without displacing more conservative rollups. Just as traditional finance has both high‑frequency trading venues and slower, highly regulated exchanges, the Ethereum scaling ecosystem may evolve into tiers of chains optimized for different functions. In such a world, MegaETH could be the go‑to venue for latency‑sensitive applications, while other rollups handle long‑term settlement, high‑value transfers, or politically sensitive use cases where censorship resistance is paramount. The presence of multi‑chain middleware, such as Chainlink CCIP, makes it easier for applications to straddle multiple chains, using MegaETH for execution and other networks for storage or settlement.

Competitive dynamics will also play a role. Other Layer‑2s may respond to MegaETH by optimizing their own performance, experimenting with specialized subnets, or integrating low‑latency features within a more conservative trust framework. Conversely, MegaETH may feel pressure to accelerate its decentralization roadmap and reduce reliance on centralized controls as it matures and competes for more risk‑averse users. The interplay between these strategic choices will shape the broader trajectory of Ethereum scaling and influence how developers allocate their attention and capital.

Token Business Versus Public Infrastructure

Finally, MegaETH raises important questions about how we conceptualize Ethereum Layer‑2s: as public infrastructure or as token‑driven businesses. By emphasizing that it is a “token business,” MegaETH foregrounds the idea that its primary stakeholders are MEGA holders, and that its design choices—from USDm integration to proximity markets—are meant to generate sustainable value for that group. This is not inherently at odds with providing public infrastructure; many public companies operate critical infrastructure while also serving shareholders. However, it does contrast with narratives that treat rollups primarily as public goods whose tokens are secondary or purely governance‑oriented.

This framing has practical implications. When evaluating protocol changes, MegaETH’s governance will have to balance user interests, developer needs, and tokenholder value. For example, decisions about how much of USDm’s yield to allocate to MEGA buybacks versus grants or fee subsidies will reflect a view about whether MegaETH is more like a business optimizing revenue or a platform optimizing for ecosystem growth. For some users, the clarity of the “token business” model may be appealing; for others, it may raise concerns about fee extraction or misalignment with user interests. In any case, MegaETH’s experiment in building a Layer‑2 as an explicitly token‑centric business will provide valuable data for the broader industry.

Outlook