Deep explainer on Kraken’s evolution from early Bitcoin exchange to multi‑asset trading hub, covering its history, products, DeFi and AI pushes, tokenized equities, regulation, and how it stacks up against Coinbase and other rivals.

+31 sources across the wider coverage universe

Kraken wins first-ever crypto Fed master account as banks and lawmakers sound alarm over systemic risk2026-04

Kraken wins first-ever crypto Fed master account as banks and lawmakers sound alarm over systemic risk2026-04 Kraken opens spot trading for Quai Network, merged-mined PoW chain claiming 50,000+ TPS2026-04

Kraken opens spot trading for Quai Network, merged-mined PoW chain claiming 50,000+ TPS2026-04 Kraken unveils Ink Points with Season 1 rollout, marking major shift toward gamified trading and long-term user retention strategy2026-04

Kraken unveils Ink Points with Season 1 rollout, marking major shift toward gamified trading and long-term user retention strategy2026-04 Deutsche Börse takes $200M stake in Kraken at $13.3B valuation, 33% below prior round2026-04

Deutsche Börse takes $200M stake in Kraken at $13.3B valuation, 33% below prior round2026-04 Kraken says no systems breached and client funds safe after extortion attempt2026-04

Kraken says no systems breached and client funds safe after extortion attempt2026-04 Kraken weighs $71M Aave Group deal for 15% stake at $385M valuation as Payward expands DeFi bets2026-06

Kraken weighs $71M Aave Group deal for 15% stake at $385M valuation as Payward expands DeFi bets2026-06

Kraken: From Early Bitcoin Exchange To Multi‑Asset Trading Platform

Kraken is a United States–based cryptocurrency exchange, legally known as Payward, Inc., that has evolved from a 2011 Bitcoin trading venue into a multi‑asset platform spanning crypto, tokenized equities, derivatives, banking services and emerging DeFi and AI‑driven tools. Positioned as both a centralized exchange and a bridge into tokenized capital markets, Kraken now sits at the intersection of crypto, traditional finance and on‑chain innovation, competing directly with Coinbase, Robinhood and global offshore exchanges for order flow, listings and investor mindshare.

What Kraken Is And Why It Matters

Kraken is best understood as a centralized exchange, or CEX, meaning it is a company that matches buyers and sellers of digital assets via internal order books while generally acting as the custodian of client funds. Customers deposit fiat currencies or cryptocurrencies into accounts, then trade spot pairs such as bitcoin–dollar, ether–euro or hundreds of altcoin combinations, with Kraken maintaining infrastructure, security controls and regulatory compliance around those markets. Unlike purely crypto‑native venues, Kraken also operates under a US corporate structure as Payward, Inc., and has pursued conventional licensing regimes, including a US state banking charter and European investment firm registration, in an effort to make crypto trading feel more like mainstream brokerage. For a crypto news audience tracking market structure, Kraken is important because it serves as one of the longest‑running, deeply liquid venues for Bitcoin and other major coins, while simultaneously pushing into new domains such as tokenized equity IPO access and US‑regulated crypto perpetual futures.

The exchange competes most directly with Coinbase in the United States retail market, with both companies offering simple buy‑and‑sell interfaces for newcomers alongside pro‑grade trading tools, but Kraken has historically leaned more toward lower fees and advanced features like margin and futures trading. Outside the US, Kraken has built a broader multi‑asset offering by adding tokenized stocks, an NFT marketplace, yield products and interconnections with DeFi protocols and Solana‑based decentralized exchanges, effectively turning the platform into an access point for several layers of the crypto stack. Its strategy now involves acquisitions of traditional futures brokers, derivatives clearinghouses and token management firms to round out an institutional‑grade suite that covers spot, derivatives, custody and token lifecycle services. In parallel, the company has become a prominent voice in regulatory debates, both through its SEC settlement over staking services and through its participation in global advisory bodies and US tech initiatives focused on blockchain security and infrastructure.

Kraken opens Bending Spoons IPO access to eligible users via xStocks with 24/5 trading.

Kraken says eligible customers in the EEA and many global markets can register non-binding interest in Bending Spoons' Nasdaq IPO, bringing pre-listing access to the company behind WeTransfer, Evernote, Vimeo, AOL and Eventbrite. Allocated users receive BSPx on listing day, a 1:1-backed tokenized equity representation that trades 24/5 on Kraken, xStocks Alliance platforms and compatible DeFi venues. This is useful IPO access, but it is still price exposure rather than direct ownership; allocation can be full, partial or zero, and US, UK, Canadian and Australian users are out.

Readers click Kraken stories as a behavioral intelligence feed — the 10x engagement spike on Australian market-preference data versus SEC filings or security breaches reveals that audiences use Kraken's exchange-level data to read crypto culture, not just to track the company.↗

Origins, Growth And Corporate Structure

Kraken traces its origins to the very early days of Bitcoin trading, when market infrastructure was fragile and dominated by exchanges such as Mt. Gox. Founded in San Francisco in 2011 by Thanh Luu, Michael Gronager and Jesse Powell, the company initially focused on providing a more reliable and compliant alternative for Bitcoin trading following repeated outages and security issues at rival venues. From those beginnings, Kraken expanded its spot markets to add Litecoin, namecoin and other early altcoins before gradually evolving into a full multi‑asset exchange with fiat currency rails in US dollars, euros, yen and other major currencies. The company’s early emphasis on security, proof‑of‑reserves‑style transparency and conservative listing standards helped it attract users seeking stability amid periodic exchange failures and hacks across the industry.

Legally, Kraken operates through Payward, Inc., which serves as the parent for various regulated subsidiaries in different jurisdictions. One of the more distinctive elements of this structure is Kraken’s decision to apply for and secure a Special Purpose Depository Institution, or SPDI, charter in the state of Wyoming, creating what it brands as Kraken Bank. The Wyoming SPDI framework is a bespoke banking regime designed for digital asset companies: it allows Kraken to operate a bank that can take deposits and provide custody for digital assets under state and, indirectly, federal oversight, while being prohibited from lending customer deposits in the manner of a fractional‑reserve bank. Kraken has described Kraken Bank as the first digital asset company in US history to receive such a bank charter recognized under both state and federal law, positioning it as a regulated bridge between crypto holdings and traditional deposit‑taking services.

The firm’s growth trajectory has reflected broader boom‑and‑bust cycles in crypto markets. By 2025, Kraken was reported to have reached roughly 207 billion dollars in quarterly trading volume and to rank as the fourteenth‑largest global crypto exchange by volume, highlighting both its scale and the degree of competition from Asian and offshore platforms. The user base has expanded into the many millions, with marketing materials and press announcements referencing more than 15 million clients worldwide, spanning retail traders, high‑net‑worth investors, family offices and, increasingly, institutional and professional market participants. Kraken serves this diverse audience partly through its main retail interface and partly through Kraken Pro, a dedicated professional trading environment that offers lower fees, deeper order types and connectivity options more familiar to traditional market participants.

Corporate governance and ownership remain private, setting Kraken apart from Coinbase, which completed a direct listing on Nasdaq in 2021. Market speculation around a Kraken IPO has circulated for several years, with internal and external commentary at times suggesting a possible listing window in the mid‑2020s. More recent reporting has indicated that Kraken’s US public listing may be slipping toward 2027, reflecting both volatile crypto valuations and the company’s desire to strengthen its regulated derivatives, banking and tokenization businesses before entering public markets. Valuation markers have emerged through M&A activity: for example, Banking Dive reported that the 2026 agreement to acquire derivatives firm Bitnomial in a deal worth up to 550 million dollars implied an equity valuation for Payward of about 20 billion dollars, though such figures are inherently sensitive to market conditions.

Strategy Through Acquisitions And Product Expansion

Kraken’s evolution from a pure crypto spot exchange into a multi‑asset platform has been driven in large part by a deliberate acquisition strategy focused on three pillars: derivatives infrastructure, tokenization and token management, and trading technology. On the derivatives side, the most consequential deals involve NinjaTrader and Bitnomial, both US‑based firms that operated in the traditional futures and derivatives ecosystem before coming under Kraken’s umbrella. NinjaTrader is a leading retail futures trading platform, known for its charting tools, algorithmic trading support and connection to commodity and financial futures markets; in March 2025, Kraken agreed to acquire NinjaTrader for approximately 1.5 billion dollars, in what was described as one of the largest combinations of traditional and crypto finance to date. The strategic rationale was to leverage NinjaTrader’s CFTC‑registered futures commission merchant, or FCM, license to offer both traditional and crypto futures to US clients under a unified, 24/7 “always‑on” professional trading platform.

Bitnomial, by contrast, is a derivatives company that bills itself as the first US crypto‑native business to hold all three Commodity Futures Trading Commission licenses required to operate as a brokerage, exchange and clearinghouse. In April 2026, Kraken announced an agreement to acquire Bitnomial for up to 550 million dollars, with the deal expected to close by June of that year, marking a significant step toward full US‑regulated crypto derivatives offerings, including spot margin, perpetuals and options. Kraken’s co‑CEO Arjun Sethi framed the acquisition in infrastructure terms, arguing that the shape of a market is determined by its clearing infrastructure and that the US had lacked clearing systems built specifically for digital assets; Bitnomial, in his view, spent a decade building capabilities that could not simply be bolted onto legacy systems, and would serve as the regulated foundation Kraken needed. Together, NinjaTrader and Bitnomial give Kraken a vertically integrated derivatives stack, from user interface to FCM to exchange and clearing, that can support crypto and eventually other asset classes under CFTC oversight.

On the tokenization and token management front, Payward has pursued smaller but strategically important acquisitions. It has partnered with and reportedly acquired interests in tokenization platform Backed Finance, which specializes in issuing tokenized versions of real‑world assets such as equities and ETFs on blockchain rails, and it has bought Magna, a token management firm that helps crypto projects handle vesting schedules, investor distributions and governance mechanics. Fortune reported in 2026 that Kraken’s acquisition of Magna, for an undisclosed sum, marked its sixth deal over the prior year and strengthened its ability to support issuers along the entire token lifecycle, from launch to secondary trading. These moves align with Kraken’s broader xStocks initiative, under which Payward plans to offer tokenized IPO access to retail investors, giving them the ability to participate in US‑listed initial public offerings at the same price as institutional buyers via tokenized shares. CryptoNews described Payward’s model as one where investors submit non‑binding indications of interest before an IPO, Kraken aggregates demand across participating exchanges in the xStocks Alliance, and then works with underwriting syndicates to secure allocations that can be distributed via tokenized representations.

The result of this acquisition‑driven strategy is that Kraken is no longer just a Bitcoin and altcoin exchange. It is increasingly configured as what its own materials describe as a “24/7, always‑on technology platform built for professional traders,” one that integrates traditional futures, crypto derivatives, tokenized equities and sophisticated token management tooling into a single ecosystem. This has important implications for both competition and regulation, since Kraken now competes not just with Coinbase and other crypto exchanges, but also with futures brokers, online stock brokers and, via its bank charter, even some banking services. For a crypto‑savvy audience, this evolution underscores the way exchanges are positioning themselves as full‑stack venues for markets that blend crypto and traditional assets rather than as isolated crypto islands.

Core Spot Markets And Crypto Trading

At the heart of Kraken’s business remain its spot markets for cryptocurrencies and fiat currency pairs. Kraken offers trading in major coins such as Bitcoin, Ether, Solana and a wide range of altcoins, alongside stablecoins and, in some jurisdictions, tokenized versions of traditional assets. Users can fund accounts with various fiat currencies or stablecoins via bank transfer and other rails, and then execute market, limit and more complex order types through both basic and professional interfaces. Kraken’s Pro platform emphasizes lower fees, deeper charting and analytics tools, and more granular order controls, appealing to experienced traders who care about execution quality and cost as much as about ease of use. For many retail participants and small crypto funds, Kraken functions as a primary fiat on‑ramp into Bitcoin and other digital assets, particularly in Europe and parts of North America where it has long maintained strong banking relationships.

Kraken’s fee structure and interface design have made it a natural comparator to Coinbase, particularly for US users deliberating where to execute trades. Independent comparisons generally characterize Coinbase as easier for complete beginners due to its streamlined mobile interface and very simple buy‑and‑sell flows, while noting that Coinbase’s convenience is often offset by higher fees on retail trades. A 2025 comparison by Coin Bureau, for instance, found that Kraken Pro typically offers lower entry‑tier spot trading costs than Coinbase’s retail platform, and highlighted Kraken’s support for spot margin and futures as differentiators for more advanced users. A popular YouTube review echoed this assessment, describing Coinbase as the simplest choice for new users but recommending Kraken for those who place priority on lower‑cost trades, more responsive customer support and access to margin and futures trading. In practice, many sophisticated traders maintain accounts on both platforms to arbitrage liquidity, fee tiers and listing coverage, but the general perception is that Kraken is more trader‑oriented while Coinbase is somewhat more beginner‑oriented.

Liquidity and market integrity are critical components of any exchange’s value proposition, and Kraken has worked to differentiate itself through conservative risk management and transparency measures. Following years of industry debate over hidden leverage, opaque reserves and off‑balance‑sheet exposures at some exchanges, Kraken implemented what it called next‑generation proof‑of‑reserves audits, enabling clients to cryptographically verify that their bitcoin and ether balances are backed by real assets held in custody. In a February 2022 announcement, Kraken explained that these audits use Merkle trees and independent third‑party verification to demonstrate that aggregate client balances match or are exceeded by assets held, without revealing individual user holdings to the auditor. While proof of reserves is not a panacea—since it does not, for example, directly address liabilities beyond customer deposits—it has become an important trust signal in a post‑FTX landscape, and Kraken’s adoption of regular audits in this area has been widely covered as a positive step for exchange transparency.

Kraken has also invested in the breadth of its spot listings, including both established large‑cap coins and more niche assets, albeit with somewhat stricter listing standards than some offshore competitors. Recent examples include the listing of AVA, the token associated with the Travala travel platform, with trading pairs denominated in USD and EUR; that listing was accompanied by promotional campaigns such as an AVA trading challenge and associated travel discounts, highlighting Kraken’s willingness to co‑market with token issuers under defined terms and eligibility criteria. For a crypto news readership, these listings are relevant not only as trading opportunities but also as signals of which ecosystems Kraken deems credible enough to support, given its reputational stake in the assets it lists.

Derivatives: Futures, Perpetuals And Options

Beyond spot markets, derivatives are increasingly central to Kraken’s competitive strategy. Internationally, Kraken offers crypto futures and perpetual contracts that allow users to take leveraged long or short positions on major cryptocurrencies, with margin requirements and risk controls calibrated by asset and jurisdiction. Perpetual futures, or “perps,” are a particularly important instrument for crypto traders: they resemble futures contracts but do not have a fixed expiry date, instead using a funding rate mechanism to keep contract prices anchored to underlying spot markets. Kraken’s derivatives platforms support leverage levels that vary by asset and user eligibility, with Coin Bureau reporting that US customers can access retail perpetuals with up to 10‑times leverage, while eligible non‑US users may receive up to 50‑times leverage in some markets. These derivatives are crucial for hedging, arbitrage and speculative strategies, and they position Kraken against established futures venues such as CME Group as well as offshore giants like Binance and Bybit.

In Europe, Kraken launched regulated crypto derivatives offerings in May 2025 after acquiring a license in Cyprus under the European Union’s Markets in Financial Instruments Directive, or MiFID II. This license allows Kraken’s Cyprus‑based arm to provide investment services, including the operation of a multilateral trading facility for derivatives, to clients across much of the European Economic Area, subject to local implementation of EU rules. The launch of regulated derivatives in Europe was framed as part of a broader push to bring crypto derivatives under conventional investor protection and market integrity standards, complementing the more lightly regulated futures products available in some offshore jurisdictions. For European institutions, this regulatory clarity matters, since many are restricted to using venues that operate under recognized licenses and meet certain capital and governance thresholds.

The US derivatives strategy has been more complex, due to the strict jurisdiction of the CFTC and the need for comprehensive licensing across exchange, clearinghouse and brokerage functions. This is where the acquisitions of NinjaTrader and Bitnomial become particularly important. NinjaTrader’s FCM license allows Kraken to act as a futures commission merchant, handling customer accounts and interfacing with exchanges under CFTC oversight, while Bitnomial’s suite of licenses enables it to operate as an exchange and clearinghouse specifically tailored for crypto derivatives. Banking Dive noted that buying Bitnomial adds regulated US derivatives to Kraken’s existing capabilities in crypto trading, tokenized equities, staking and on‑ and off‑ramps, and that the combined platform opens a new channel for partners such as fintechs, banks and brokerages to offer derivatives to their users via a single integration. Recent coverage has highlighted that Kraken has begun rolling out CFTC‑regulated US crypto perpetual futures on Kraken Pro using this infrastructure, allowing eligible US traders to access perps in a framework that regulators can supervise more closely than offshore platforms.

Importantly, derivatives expansion is not only about speculative risk‑taking. For institutional investors and sophisticated funds, futures and options are risk management tools that allow them to hedge spot exposures, implement basis trades and manage portfolio volatility across Bitcoin and broader crypto holdings. Kraken’s stated ambition is to become a leading US futures venue for both traditional and crypto markets, using its 24/7 trading technology and combined clearing infrastructure to serve participants who are accustomed to weekday trading hours and legacy exchange technology. Whether Kraken can fully realize that ambition will depend on regulatory developments, competition from established futures giants and its ability to integrate its acquisitions smoothly, but its trajectory places it squarely at the center of the derivatives arms race in crypto.

- 01exchange as market sentiment mirror↗

The Australian preferences story dominated all others by a factor of ten, showing readers treat Kraken data as a proxy for retail crypto psychology and cultural momentum across regions.

- 02SEC lawsuit & regulatory warfare↗

Multiple headlines spanning the initial suit, Kraken's dismissal motion, state AG amicus briefs, and Binance settlement comparisons pulled consistent clicks, signaling readers tracking the regulatory endgame closely.

- 03security breach accountability

The CertIK exploit and the North Korean fake-engineer sting both drew strong clicks not for the technical details but for the resolution arc — who got caught, whether funds came back, and how Kraken handled exposure.

- 04TradFi convergence plays↗

NinjaTrader acquisition, xStocks tokenized equities, TradeStation Crypto purchase, and tokenized VC funds (SpaceX/OpenAI/Anthropic exposure) collectively map Kraken's push to blur the line between exchange and broker-dealer.

- 05European regulatory localization

Germany Lightning withdrawal, German government BTC sales routed through Kraken, Tether MiCA delisting review, and Quantoz MiCA-compliant stablecoin partnership show readers tracking how Kraken navigates EU fragmentation.

- 06Jesse Powell legal exposure

The FBI raid on the founder pulled nearly 300 clicks, reflecting reader interest in whether founder-level legal risk bleeds into platform trust and regulatory standing.

Staking, Yield And The Aftermath Of SEC Enforcement

One of the more visible regulatory flashpoints for Kraken has been its US crypto staking program. Staking, in this context, refers to the process by which holders of proof‑of‑stake cryptocurrencies such as Ethereum or Solana delegate their coins to validators in order to secure the network and earn block rewards, usually in the form of additional tokens. Exchanges like Kraken simplify this by offering staking‑as‑a‑service, pooling user assets, running validators and passing along rewards in exchange for a fee. From 2019 onward, Kraken offered such staking services to US customers, with advertised annual yields that in some cases reached about 21 percent, depending on the asset.

In February 2023, the US Securities and Exchange Commission charged Payward Ventures, Inc. and Payward Trading Ltd., both operating under the Kraken brand, with failing to register the offer and sale of these staking‑as‑a‑service programs as securities. The SEC’s complaint alleged that the staking program involved investment contracts under the Howey test, because investors transferred crypto assets to Kraken in expectation of profits based on Kraken’s efforts, without sufficient disclosure of terms and risks. To settle the charges, Kraken agreed, without admitting or denying the allegations, to immediately cease offering or selling securities through crypto asset staking‑as‑a‑service programs to US clients and to pay 30 million dollars in disgorgement, prejudgment interest and civil penalties. The settlement also included a permanent injunction against Kraken and controlled entities offering or selling such staking services that would constitute securities, highlighting the SEC’s view that centrally managed staking products fall under its remit.

Outside the US, Kraken continues to offer staking and yield products, but the enforcement action reshaped how the company structures yield‑generating services. A notable recent launch is Bitcoin Vault, a product within the Kraken Earn suite designed for long‑term Bitcoin holders who want to earn yield while maintaining BTC‑denominated exposure. According to Kraken’s own announcement, Bitcoin Vault allows customers to earn up to roughly 2.5 percent in BTC‑denominated rewards by deploying deposits into curated strategies that allocate to well‑known on‑chain lending and liquidity protocols such as Aave, Morpho and Tydro. The product is powered by external platforms Veda and Sentora, which design strategies and manage risk, with Kraken aiming to abstract away complexity so that users simply hold Bitcoin, opt in to the vault and receive rewards in BTC without needing to handle DeFi interactions directly. Bitcoin Vault is available through Kraken Earn in most jurisdictions where Kraken operates, with exceptions such as the UK, UAE and Australia, reflecting local regulatory constraints on yield products.

Kraken has emphasized that these yield offerings differ from the earlier US staking‑as‑a‑service program, both in terms of structure and jurisdiction. Nevertheless, they illustrate the regulatory tightrope exchanges must walk as they try to offer competitive crypto yield opportunities while avoiding classification as unregistered investment products. For a sophisticated audience, the key takeaway is that yield on Kraken is increasingly mediated through curated DeFi strategies rather than simple pass‑through staking, and that regulatory scrutiny has pushed the company to tailor products at a much more granular, jurisdiction‑specific level.

Kraken weighs $71M Aave Group deal for 15% stake at $385M valuation as Payward expands DeFi bets

CoinDesk says Kraken parent Payward is in talks to buy 15% of Aave Group at a $385M valuation, with a proposed structure of 35,000 ETH for 250,000 $AAVE plus common equity. The roughly $71M deal would push Payward Asset Management deeper into DeFi ahead of Kraken's expected IPO, following Payward's April agreement to buy Bitnomial for up to $550M. Timing is messy: Aave is still rebuilding from the KelpDAO bridge exploit, where Lazarus-linked attackers minted $292M of unbacked rsETH, left $190M-$230M in bad debt, and triggered more than $8B in withdrawals without compromising Aave's own contracts.

NFTs, Web3 And Solana DEX Integration

Kraken has also moved into the non‑fungible token and broader Web3 space, albeit with a measured approach compared to some rivals. In December 2022, the company opened a public beta for Kraken NFT, a marketplace for collectors to explore, discover and trade NFTs on Ethereum and Solana. At launch, the platform featured a curated set of more than 110 of the highest‑trading‑volume NFT collections, reflecting a strategy of focusing on blue‑chip projects rather than listing every possible series. Kraken NFT was designed to address some of the friction points of early NFT markets by offering zero gas fees for NFTs held on Kraken, meaning users could trade without directly incurring network gas costs or worrying about congestion on the underlying blockchain during peak activity. The marketplace also included creator earnings mechanisms to route a portion of sale value back to original creators, rarity rankings to help users assess the relative scarcity of specific NFTs, and support for listing and bidding in eight fiat currencies and over 200 cryptocurrencies.

While Kraken’s NFT marketplace does not match the volume of specialized platforms like OpenSea or Blur, it fits into a broader strategy of offering a one‑stop shop for major crypto use cases. For users whose primary relationship is with Kraken as a trading venue and custodian, having integrated NFT capabilities lowers the barrier to experimenting with Web3 assets, especially when combined with fiat on‑ramps and portfolio views that show fungible and non‑fungible holdings together. In this sense, Kraken NFT is less about chasing speculative NFT trading volumes and more about gradually normalizing NFTs within the broader crypto investing experience.

The more recent and structurally significant Web3 move is Kraken’s integration of Solana‑based decentralized exchange trading into its mobile app. According to reporting from CryptoRank and other outlets, Kraken has launched a feature that allows mobile users to trade thousands of tokens available on major Solana DEX protocols directly from within the Kraken interface, using either USD or USDC as the funding currency. This integration relies on a built‑in Privy wallet that automatically manages keys and transactions on behalf of the user, with holdings integrated into the existing Kraken portfolio screen, giving the appearance of a unified account even though trades are executed on decentralized venues. Kraken has described this approach as part of a “DeFi mullet” strategy, meaning that users experience the front end of a familiar centralized exchange, but under the surface, execution and custody leverage decentralized infrastructure and self‑custody principles.

The DeFi mullet framing is significant for market structure. It allows Kraken to offer access to a much wider universe of tokens than it could reasonably list on its own centralized order books, since listing on a CEX entails legal, technical and reputational due diligence. By routing orders to Solana DEXs through a smart contract‑controlled wallet, Kraken can give users exposure to long‑tail tokens while mitigating some of the compliance and listing liabilities it would otherwise face. At the same time, abstracting away private key management and transaction signing lowers the learning curve for users unfamiliar with self‑custody and DeFi wallet operations. Kraken has indicated that it plans to expand this DEX support to other blockchains beyond Solana, though it has not yet disclosed specific timelines or networks, leaving the integration roadmap as an area to watch.

Tokenized Equities, IPO Access And SpaceX

One of the most ambitious parts of Kraken’s roadmap is its push into tokenized equities and initial public offering access. Tokenized equities are digital tokens that represent claims on underlying shares of publicly traded companies, typically issued under a legal structure that allows the token to be redeemed or economically tied to the real‑world stock. In 2025, Kraken began allowing trading in tokenized equities for non‑US customers, initially including large‑cap names like Apple, Tesla and Nvidia, with the tokens recorded on its digital ledger and tradable alongside cryptocurrencies on the exchange. This offering is limited by jurisdictional constraints and is typically unavailable to US persons due to securities regulations, but it signals Kraken’s intention to blur the boundary between traditional stocks and crypto assets within a single platform.

Building on that, Payward announced plans to offer tokenized IPO access through the xStocks program. CryptoNews reported that Payward will soon allow Kraken customers and other members of the xStocks Alliance to participate in US‑listed initial public offerings via tokenized shares, giving eligible investors the ability to receive allocations at the IPO price, similar to institutional investors, rather than buying in the aftermarket once public trading begins. Under this model, investors submit non‑binding indications of interest for specific IPOs, Kraken aggregates demand across participating platforms and works with underwriting syndicates to secure an allocation, which is then distributed as tokenized representations tied to the underlying shares. The aim is to democratize primary market access, which has historically been limited to large institutions and select brokerage clients, by leveraging blockchain rails to fractionalize and distribute IPO allocations globally.

A particularly high‑profile case is the SpaceX IPO. Kraken has launched an offering that allows eligible users to participate in the SpaceX IPO via xStocks, using a tokenized instrument known as SPCXx as the ticker. Documentation on Kraken’s support site explains that users with verified accounts in eligible regions can submit pre‑orders for the SpaceX IPO by specifying the amount they wish to participate with; funds in USD, USDG or USDC are reserved, not debited, during the pre‑order window, and participants ultimately receive allocations at the offering price, inclusive of a five percent spread to account for fees and slippage. The SpaceX IPO via xStocks is explicitly unavailable to clients located in the US, UK, Canada, Australia or to US persons, reflecting the complexity of securities law and offering restrictions. Despite these limitations, demand for SpaceX exposure has reportedly far exceeded the allocation Kraken secured from underwriters, illustrating both the appeal of marquee private tech names and the constraints of working within traditional IPO syndication structures.

Industry coverage has noted that the tokenized equity market has grown to an estimated 5.5 billion dollars, with exchanges like Kraken and Bybit opening access to tokenized SpaceX IPO exposure as key catalysts for this figure. While such numbers are still small relative to global equity markets, they suggest a trajectory where tokenized representations of stocks and pre‑IPO shares become a meaningful bridge asset class between crypto and traditional securities. For investors and observers, Kraken’s role in this space highlights both the technical feasibility of tokenized equities and the regulatory and operational frictions that still constrain their global rollout.

Banking, Custody And Kraken Bank

Kraken’s decision to secure a bank charter in Wyoming reflects a strategic bet that combining exchange and banking functions under a regulated entity will be a competitive differentiator as crypto matures. The Wyoming SPDI charter, granted in 2020, authorizes Kraken Bank to provide deposit‑taking and digital asset custody services within a framework that is recognized under both state and federal law. As a special purpose depository institution, Kraken Bank is required to maintain full reserves against deposits rather than engaging in fractional‑reserve lending, which means it must hold safe assets equal to customer deposits at all times, a structure intended to minimize solvency risk. In its announcement, Kraken described plans for the bank’s first year to include enabling US clients to deposit US dollars and custody digital assets at a regulated state‑chartered bank, with services integrated into existing exchange accounts for smoother funding and withdrawal flows.

Over time, Kraken has expressed ambitions to expand Kraken Bank’s services to include enhanced digital asset custody products, demand deposit accounts, wire transfer services, online and mobile banking capabilities, debit cards that let clients spend crypto, and a suite of corporate services such as account management, bank comfort letters and proof‑of‑funds attestations. The bank is headquartered in Cheyenne, Wyoming, with a permanent physical presence housing back‑office teams, while operations are designed to be online‑ and mobile‑first, consistent with Kraken’s overall digital nature. Customer service is advertised as being available around the clock, in keeping with the 24/7 character of crypto markets, and the bank is intended to eventually support additional asset classes such as securities as regulatory and business conditions permit.

While the full build‑out of Kraken Bank has taken longer than some initial commentary anticipated, the charter positions Kraken differently from most crypto exchanges, which rely on third‑party partner banks for fiat services and cannot themselves offer deposit products. In an era where stablecoins, tokenized bank deposits and on‑chain representations of money are proliferating, having a bank license gives Kraken a platform from which to experiment with new forms of tokenized cash and integrated treasury services, subject to regulatory approval. It also gives regulators a more conventional entity through which to supervise certain aspects of Kraken’s operations, potentially easing concerns about off‑shore or lightly regulated activities, even if the bank and the exchange still operate as distinct legal entities.

SEC charges Kraken over unregistered staking-as-a-service; $30M settlement, staking shut down for US users

- 2024-06exploit

CertIK researchers exploit Kraken bug, refuse to return ~$3M, route funds through Tornado Cash

- 2024-07governance

German government moves 400 BTC to Kraken and Coinbase to liquidate seized assets

SEC files second, expanded lawsuit against Kraken as unregistered securities exchange

Kraken acquires NinjaTrader, a retail futures and trading platform, to bridge TradFi and crypto

Kraken and Solana Foundation launch xStocks, bringing tokenized US equities and ETFs on-chain

Kraken receives Wyoming Special Purpose Depository Institution charter, becoming first crypto-native digital asset bank

Kraken acquires Magna token management platform to support institutional asset issuance

AI Trading Agents, Research Copilots And Market Structure

A newer and rapidly evolving dimension of Kraken’s strategy involves the integration of artificial intelligence agents into trading, research and portfolio management workflows. Across the industry, exchanges are experimenting with “copilot” features that connect AI models to market data, news flow, portfolio holdings and execution interfaces, allowing users to query markets in natural language, generate strategies and, in some cases, delegate certain trading tasks to autonomous or semi‑autonomous agents. Recent coverage has highlighted that Coinbase, Robinhood and Kraken are all moving in this direction, turning AI agents into trading copilots that tie together research, risk analytics and order placement within a single platform.

The clearest example of this trend is Robinhood’s “Agentic Trading” product, which provides a dedicated agentic account where users can connect AI agents to their Robinhood brokerage, with built‑in safety controls that keep trades segregated and require user oversight. Robinhood emphasizes that these agentic accounts allow users to stay in control of every trade their agent makes, while the platform enforces guardrails around risk and compliance. While Kraken has not publicly rolled out an identical product, industry reporting suggests that it is building similar infrastructure to let users and third‑party developers connect AI agents to Kraken’s trading APIs in a controlled manner. The goal is to enable AI‑driven research, portfolio rebalancing and execution strategies while ensuring that users retain visibility and veto power over orders, much like the way algorithmic trading strategies are supervised in traditional markets.

For crypto markets, where 24/7 trading, fragmentation across venues and high volatility create both opportunity and risk, AI agents promise to further blur the line between retail and professional trading. Retail traders equipped with AI copilots may soon be able to scan dozens of markets, backtest strategies and execute cross‑venue arbitrage trades that previously required specialized skills and infrastructure. At the same time, exchanges like Kraken will need to manage new forms of operational risk, including the potential for AI agents to exacerbate flash crashes or trigger feedback loops if many agents respond similarly to market signals. Kraken’s push into AI‑mediated trading, combined with its derivatives and tokenized equities offerings, positions it as a likely test bed for how AI changes behavior in crypto and hybrid markets, but the contours of that change remain uncertain.

DeFi L2s, Bridging And Institutional On‑Chain Access

Kraken’s Solana DEX integration is one piece of a broader strategy to embed itself more deeply into DeFi and on‑chain capital markets. A notable component of this strategy involves layer‑two networks and specialized chains designed for institutional use. Social media posts and early communications from Across Protocol, for instance, have referenced “Ink,” described as Kraken’s layer‑two network for the next generation of DeFi, with bridging support from protocols like Across helping users move assets to this environment. While detailed public documentation on Ink remains limited, the concept aligns with a broader industry trend in which major exchanges and custodians launch their own L2s or app‑chains as controlled environments for on‑chain trading, lending and settlement.

In parallel, Kraken has begun supporting new asset formats on permissioned networks that target institutional adoption of tokenized finance. Recent coverage from the company and industry observers has noted that Kraken is opening deposits and withdrawals of USDCx on Canton, a permissioned network designed for regulated financial institutions to issue and trade tokenized assets. By enabling clients to move tokenized dollars into and out of Canton, Kraken is positioning itself as a gateway between public crypto markets and private institutional tokenization platforms, which are increasingly used for experiments in tokenized bonds, funds and structured products. This kind of connectivity could become crucial if large banks and asset managers continue to build on permissioned chains while crypto‑native liquidity remains concentrated on public networks.

Bitcoin Vault, mentioned earlier, also illustrates Kraken’s approach to connecting users with DeFi in a curated fashion. Rather than requiring users to learn protocol interfaces, gas management and risk parameters, Kraken partners with strategy providers like Veda and Sentora, which in turn allocate capital to lending markets and yield strategies on protocols such as Aave, Morpho and Tydro. Kraken’s role becomes that of a distributor and risk curator, translating complex on‑chain positions into simple BTC‑denominated yield products for end users, while absorbing some of the operational burden of protocol selection and monitoring. This is analogous to how traditional finance offers packaged mutual funds or structured products that wrap underlying exposures in a simplified wrapper, but in this case, the underlying exposures are DeFi protocols and liquidity pools rather than conventional securities.

For institutions, these developments matter because they provide a pathway to on‑chain exposure that aligns with risk, compliance and custody requirements. An asset manager that cannot directly hold DeFi tokens on self‑custodied wallets might still be able to participate in yield strategies or tokenized assets via a regulated intermediary like Kraken, especially when that intermediary can demonstrate proof of reserves, bank‑level custodial controls and compliance with securities and derivatives regulations in relevant jurisdictions. In this way, Kraken’s DeFi integrations, L2 initiatives and tokenization efforts are not just technology experiments; they are part of a larger attempt to make on‑chain finance compatible with institutional scale and regulatory oversight.

Maple and Kraken close landmark onchain warehouse facility for digital asset-backed loans. But onchain lending facility raises questions about default risks and regulatory gaps.

DeFiLlama has Maple around $2B TVL while its own front-end shows low-single-digit yield on the main USDC products, so this is credit plumbing with regulated-CeFi counterparty risk attached. The concentration is the hard part: Kraken affiliates originate, sell, and service the loans while Kraken Financial custodies the BTC/ETH, putting lenders on Kraken’s margin engine, SPV waterfall, and liquidation discipline. Onchain performance data helps after origination; a weekend BTC wick or borrower default still gets resolved through legal recourse, bankruptcy-remoteness, and jurisdictional plumbing.

Regulation, Compliance And Policy Engagement

Kraken’s regulatory posture is complex and evolving, shaped by its multi‑jurisdictional activities and the still‑fluid status of many crypto assets under law. In the United States, Kraken must navigate overlapping oversight from the SEC, CFTC, FinCEN and state regulators, in addition to its obligations under the Wyoming Division of Banking as a SPDI. The SEC staking settlement underscored the commission’s view that many centrally managed yield products constitute securities offerings requiring registration or exemption, while the Bitnomial acquisition highlighted Kraken’s recognition that operating crypto derivatives exchanges in the US requires full CFTC licensing. Through its banking subsidiary, Kraken also engages with prudential regulators and bank examiners, adding an additional layer of compliance requirements related to capital, liquidity, operational risk and consumer protection.

In Europe, Kraken’s MiFID II license in Cyprus enables it to offer investment services, including derivatives trading, under a relatively clear regime that treats certain crypto instruments as financial instruments akin to traditional derivatives. This license serves both as a passport for services across the European Economic Area and as a signal to regulators and clients that Kraken is willing to subject itself to conventional investment firm rules, including conduct of business, best execution and investor protection obligations. As the EU’s Markets in Crypto‑Assets Regulation (MiCA) continues to be implemented, Kraken and other exchanges will need to adapt their token listing, stablecoin and custody practices to align with MiCA’s new categories of crypto‑asset service providers and issuance requirements.

Beyond formal regulation, Kraken has sought to shape policy and public understanding of crypto through participation in initiatives and advisory groups. Its parent Payward has reportedly joined US tech‑focused coalitions such as the US Tech Force Initiative, which aims to advance crypto security and blockchain adoption in federal technology upgrades, positioning Kraken as a stakeholder in national infrastructure modernization. Internationally, Kraken has been named as one of the members of the United Nations Development Programme’s Blockchain Advisory Group, alongside networks such as Ethereum, Cardano and Sui, with the group tasked with advising on the use of blockchain in sustainable development and public sector applications. These roles do not confer regulatory authority, but they give Kraken a voice in how blockchain technology is framed for policymakers, development agencies and the public.

Of course, regulatory exposure also brings risk. Kraken, like Coinbase and other US exchanges, faces the possibility of future enforcement actions or rule changes that could affect its business lines, particularly around token listings that might be deemed securities, stablecoin operations and cross‑border derivatives offerings. The company must also manage anti‑money‑laundering and know‑your‑customer compliance across jurisdictions, including the implementation of travel rule requirements for crypto transfers and sanctions screening. For market participants, Kraken’s regulatory trajectory offers a case study in how a large, long‑standing crypto exchange attempts to professionalize and institutionalize without losing the flexibility that initially made crypto markets innovative.

Brand, Sponsorships And Ecosystem Positioning

Kraken’s brand has historically emphasized security, transparency and a somewhat more technical, trader‑centric identity than some of its competitors. In recent years, however, it has also embraced mainstream marketing and sponsorships to broaden its recognition. A particularly high‑profile example is Kraken’s multi‑year partnership with FIFA, under which Kraken has been named the Official Crypto Exchange of the FIFA World Cup 2026. This sponsorship gives Kraken prominent visibility during one of the world’s most watched sporting events, with branding opportunities across stadiums, broadcasts and digital channels, and reflects a broader trend of crypto exchanges using sports sponsorships to reach mass audiences.

These marketing moves sit alongside more targeted ecosystem campaigns. The AVA listing mentioned earlier, for instance, was accompanied by a Kraken marketing campaign that included a trading challenge and associated travel discounts for the top AVA traders, highlighting how Kraken uses token listings as opportunities for co‑branded promotions. By tying token campaigns to tangible benefits, such as travel vouchers, Kraken aims to deepen engagement with specific token communities while also demonstrating its platform’s reach to potential issuers. Similar strategies have been evident in NFT promotions, yield product launches and regional marketing pushes, though the company tends to avoid the more aggressive retail leverage advertising that has drawn criticism for some competitors.

Within the crypto ecosystem, Kraken occupies a somewhat distinct niche. It is often seen as more conservative and compliance‑oriented than offshore exchanges that offer extremely high leverage, extremely rapid listing of new tokens and minimal KYC requirements. At the same time, it is more experimentally inclined than strictly regulated brokerages, as evidenced by its DeFi integrations, tokenized equities and AI agent initiatives. This positioning allows Kraken to act as a bridge, not just between crypto and traditional finance, but also between the risk‑tolerant, innovation‑driven segments of crypto and the more cautious institutional world. For Bitcoin markets specifically, Kraken remains one of the key price discovery venues, especially in euro and other non‑US dollar pairs, and its support for proof of reserves and SPDI banking have made it a reference point in debates over exchange solvency and transparency.

Kraken faces active SEC litigation, multi-jurisdiction compliance pressure from India's FIU, German BaFin-driven service restrictions, and EU MiCA forcing product delisting reviews including Tether.

- Security / OperationalMedium

The June 2024 CertIK exploit exposed a critical bug; funds were ultimately returned but the researcher conduct and Tornado Cash routing created reputational and compliance risk beyond the technical breach.

- CentralizationMedium

Kraken custodies assets and controls listing decisions unilaterally — evidenced by Monero delisting in Canada and Lightning Network disabling in Germany — concentrating withdrawal and access risk in a single operator.

- Market / LiquidityMedium

BTC exchange wallet outflows tracked across Kraken, Coinbase, Binance, and OKX indicate structural liquidity thinning; this reduces the exchange's fee revenue base while potentially amplifying price dislocations during stress.

Acquiring NinjaTrader, launching tokenized equities via xStocks on Solana, and pursuing a Wyoming digital asset bank charter introduce regulatory capital requirements and counterparty complexity that a pure crypto exchange does not face.

- Smart-Contract / ProductLow

Kraken is primarily a centralized custodial exchange; EigenLayer restaking integration and xStocks tokenization add smart-contract surface area, but core custody and settlement risk remains off-chain and exchange-controlled.

Kraken Versus Coinbase And Other Competitors

For many crypto users, the practical question is how Kraken compares to Coinbase, Binance, Bybit, Robinhood and other exchanges as a venue for trading, investment and market access. Coinbase, as the only major US crypto exchange currently publicly listed, enjoys strong brand recognition and regulatory scrutiny, but its retail platform is often criticized for relatively high fees on simple buy‑and‑sell transactions. Kraken, by contrast, has built its value proposition around lower fees, particularly on Kraken Pro, and around advanced features such as margin trading and futures that Coinbase offers in more limited forms. A snapshot comparison based on publicly available analyses illustrates some of these differences.

| Feature | Kraken | Coinbase |

|---|---|---|

| Founded | 2011, San Francisco | 2012, San Francisco |

| Primary focus | Multi‑asset crypto, derivatives, tokenized equities | Retail crypto brokerage, ecosystem apps |

| Fees (entry tiers) | Generally lower spot fees on Kraken Pro | Higher retail fees, simpler UI |

| Derivatives | Margin, futures, perps in eligible regions | Limited derivatives, expanding slowly |

| Bank charter | Wyoming SPDI (Kraken Bank) | None (relies on partner banks) |

Coin Bureau’s in‑depth comparison concludes that Kraken is best suited for advanced, global or cost‑conscious traders who value deeper tools and access to margin and futures, while Coinbase is better for those who prioritize the fastest, simplest onboarding into crypto, even at higher cost. A 2025 YouTube analysis adds that Coinbase’s consumer‑friendly interface and fast transactions make it ideal for beginners, but that Kraken offers better customer support, more advanced features and lower fees for those who intend to trade actively. The choice between the two often comes down to user sophistication, geographical location, desired products and tolerance for interface complexity.

Against offshore exchanges like Binance and Bybit, Kraken’s differentiation rests more on regulatory posture and tokenized equities than on sheer breadth of spot listings or maximum leverage. Offshore platforms typically offer a wider array of small‑cap tokens and extremely high leverage on derivatives, but they also carry higher jurisdictional and regulatory risks, with some markets blocking access or warning against their use. Kraken, with its bank charter, MiFID license, US derivatives licensing and public proof‑of‑reserves audits, presents itself as a safer, more institutionally compatible choice, even if that means offering a more curated set of products. In tokenized equities and IPO access, Kraken’s xStocks initiative has few direct analogues, though Bybit has followed its lead by offering tokenized access to pre‑IPO SpaceX exposure via the same underlying tokenization source, underscoring Kraken’s role as an early mover in that segment.

Risks, Challenges And Open Questions

Despite its strengths, Kraken faces significant risks and challenges that a discerning crypto audience should consider. Regulatory risk remains foremost, particularly in the US, where the classification of many tokens, stablecoins and crypto‑based yield products is unsettled. The SEC’s staking case demonstrates that even long‑standing products can suddenly fall afoul of enforcement priorities, forcing rapid business model adjustments. Future actions related to specific token listings, stablecoin operations or cross‑border derivatives could similarly affect Kraken’s product lineup and geographic reach, and increased scrutiny of tokenized securities could complicate its xStocks and tokenized equity offerings.

Competitive pressure is another major challenge. Kraken must compete simultaneously with highly capitalized public companies like Coinbase, agile offshore exchanges that can iterate rapidly without the same regulatory burdens, fintech platforms like Robinhood that integrate crypto alongside stocks and options, and traditional exchanges like CME that are moving into Bitcoin and Ethereum futures. Each of these competitors brings different strengths, from distribution and brand to regulatory licenses and technological capabilities. Kraken’s acquisition‑driven strategy, while providing rapid capability expansion, also introduces integration risk, as it must meld cultures, systems and regulatory frameworks across NinjaTrader, Bitnomial, Magna and other acquired entities.

Technological and operational risks are amplified by Kraken’s push into DeFi, AI agents and on‑chain tokenization. Integrating Solana DEX trading via a built‑in wallet raises questions about smart contract security, key management and the handling of protocol‑level failures or exploits. Bitcoin Vault’s reliance on third‑party DeFi protocols such as Aave, Morpho and Tydro exposes users indirectly to protocol‑level risks, even if Kraken and its partners engage in careful risk curation. AI trading agents add another layer of complexity, as exchanges must design robust guardrails to prevent runaway algorithms, ensure transparency around decision‑making and manage potential conflicts when AI models are trained on proprietary order flow or user behavior.

Finally, the timing and structure of Kraken’s potential IPO remain uncertain. While a public listing could provide capital for further expansion and give investors direct equity exposure to Kraken’s growth, it would also subject the company to quarterly reporting pressures, expanded disclosure obligations and market scrutiny that may constrain its willingness to experiment. Reporting from Finance Magnates suggests that Kraken’s IPO timeline may now extend toward 2027, and that recent acquisitions are part of an effort to present a more diversified, multi‑asset profile to public markets. How investors value a hybrid exchange–bank–derivatives–tokenization platform in an environment of shifting regulation and crypto sentiment is an open question, and Kraken’s leadership will need to balance growth ambitions with resilience against regulatory and market shocks.

Outlook

Kraken’s trajectory over the past decade and a half reflects the broader evolution of crypto itself, from a niche Bitcoin exchange ecosystem into a sprawling, multi‑asset financial landscape that spans spot trading, derivatives, NFTs, DeFi, tokenized securities and AI‑mediated strategies. Having started as a relatively conservative, security‑focused alternative to early exchanges, Kraken has become one of the most diversified players in the sector, combining a US bank charter, European investment firm licensing, global spot and derivatives markets, tokenized equity and IPO access, curated DeFi yield products and experimental DEX and L2 integrations. Its ongoing acquisitions of NinjaTrader, Bitnomial and Magna suggest a desire to own the full stack of trading, clearing and token management infrastructure, positioning it as a potential hub for both retail and institutional participation in crypto and tokenized capital markets.

Looking ahead, Kraken’s success will hinge on its ability to manage regulatory relationships, integrate complex acquisitions, and deliver on the promise of AI‑assisted trading and DeFi access without compromising security or user trust. Its rivalry with Coinbase and the emergence of hybrid platforms like Robinhood’s agentic trading environment will shape user expectations around fees, features and the integration of stocks, crypto and tokenized assets. At the same time, macro factors such as Bitcoin’s role in portfolios, the pace of tokenization of real‑world assets, and the regulatory treatment of stablecoins and securities‑like tokens will determine the ceiling for Kraken’s multi‑asset ambitions. For crypto market observers, Kraken offers a compelling case study in how an early exchange can attempt to reinvent itself as a bridge between legacy finance and the on‑chain economy, while navigating the risks that come with operating at the frontier of both technology and regulation.

Latest Kraken news

Kraken opens Bending Spoons IPO access to eligible users via xStocks with 24/5 trading.Kraken weighs $71M Aave Group deal for 15% stake at $385M valuation as Payward expands DeFi betsMaple and Kraken close landmark onchain warehouse facility for digital asset-backed loans. But onchain lending facility raises questions about default risks and regulatory gaps. Kraken brings Centrifuge-tokenized Janus Henderson JAAA into qualified custody for institutional collateral

Kraken brings Centrifuge-tokenized Janus Henderson JAAA into qualified custody for institutional collateral Squid (@squidrouter) reveals their public token sale just weeks after announcing their $6m private round.

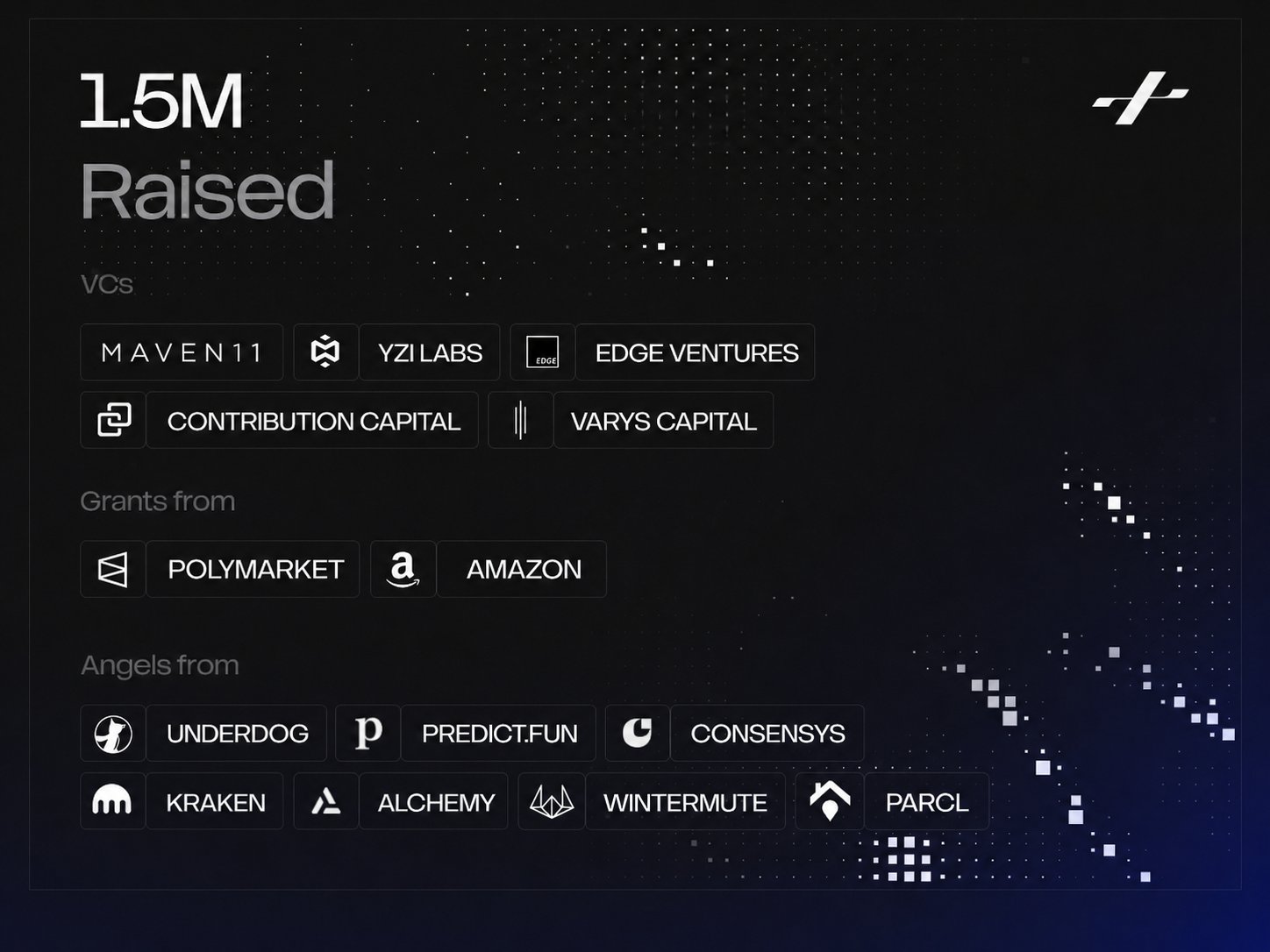

Squid (@squidrouter) reveals their public token sale just weeks after announcing their $6m private round. AI analytics platform Polysights raises $1.5M pre-seed funding to combat insider trading in prediction markets. The raise was backed by YZi Labs S3, Maven 11 Capital, and angels from Kraken and Consensys, plus grants from Polymarket and AWS.

AI analytics platform Polysights raises $1.5M pre-seed funding to combat insider trading in prediction markets. The raise was backed by YZi Labs S3, Maven 11 Capital, and angels from Kraken and Consensys, plus grants from Polymarket and AWS.Sources

- https://www.kraken.com

- https://en.wikipedia.org/wiki/Kraken_(cryptocurrency_exchange)

- https://www.bloomberg.com/profile/company/0965294D:US

- https://www.financemagnates.com/cryptocurrency/kraken-ipo-slides-toward-2027-four-weeks-after-sethi-publicly-reaffirmed-filing/

- https://www.youtube.com/watch?v=Y5pHdGSvpXM

- https://www.sec.gov/newsroom/press-releases/2023-25

- https://robinhood.com/us/en/agentic-trading

- https://cryptorank.io/news/feed/49500-kraken-solana-dex-mobile-app

- https://x.com/AcrossProtocol/status/2066841887625900356

- https://support.kraken.com/articles/spacex-ipo

- https://cryptonews.net/news/finance/32959980/

- https://ninjatrader.com/news/kraken-to-acquire-ninjatrader-introducing-the-next-era-of-professional-trading/

- https://www.bankingdive.com/news/kraken-buy-derivatives-firm-bitnomial-550-million-deal/817839/

- https://fortune.com/2026/02/18/kraken-acquires-magna-token-management-platform/

- https://blog.kraken.com/news/kraken-wyoming-first-digital-asset-bank

- https://blog.kraken.com/product/bitcoin-vault/introducing-bitcoin-vault

- https://www.kraken.com/press/releases/kraken-opens-nft-marketplace

- https://www.kraken.com/press/releases/kraken-launches-proof-of-reserves-audits-allowing-clients-to-verify-crypto-balances

- https://coinbureau.com/analysis/kraken-vs-coinbase

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…