In‑depth explainer on how oil shapes crypto markets, from macro shocks and CME futures to onchain perps, tokenized barrels, stablecoin‑financed trade, and Ethereum’s “digital oil” role in the emerging commodities‑DeFi nexus.

+29 sources across the wider coverage universe

The Evolution of Commodities - state of commodities and a quantitative analysis of the growth of commodities markets onchain

A new research report by Castle Labs2026-03

The Evolution of Commodities - state of commodities and a quantitative analysis of the growth of commodities markets onchain

A new research report by Castle Labs2026-03 Infinityhedge breaks down Hormuz crisis: 9 supertankers left, EU diesel up 50%, $200 oil looms, and Trump unwinds Russia sanctions to fuel his own war2026-03

Infinityhedge breaks down Hormuz crisis: 9 supertankers left, EU diesel up 50%, $200 oil looms, and Trump unwinds Russia sanctions to fuel his own war2026-03 Fed's Waller went in ready to cut rates, but Iran war oil spike forced a hold — says cuts still possible later in 20262026-03

Fed's Waller went in ready to cut rates, but Iran war oil spike forced a hold — says cuts still possible later in 20262026-03 Hyperliquid HIP-3 hits record weekend volume at $720M as geopolitical turmoil and surging oil prices drive traders to onchain derivatives2026-03

Hyperliquid HIP-3 hits record weekend volume at $720M as geopolitical turmoil and surging oil prices drive traders to onchain derivatives2026-03 Citigroup faces $1 Billion lawsuit over alleged role in orchestrating and concealing fraud at Mexican Oil company Oceanografia, as U.S. appeals court revives case.2025-05

Citigroup faces $1 Billion lawsuit over alleged role in orchestrating and concealing fraud at Mexican Oil company Oceanografia, as U.S. appeals court revives case.2025-05 Ostium introduces its v2 - the only place onchain to long or short the S&P, Nasdaq, gold, oil, & JPY at up to 200x leverage2025-03

Ostium introduces its v2 - the only place onchain to long or short the S&P, Nasdaq, gold, oil, & JPY at up to 200x leverage2025-03

Oil, Macro, and Crypto: How a Legacy Commodity Is Going Onchain

Few assets shape the macro backdrop for digital assets as profoundly as crude oil, and the line between barrel markets and blockchains is getting thinner every year. This explainer traces oil’s role as a macro benchmark, its growing presence in onchain derivatives and tokenization, the rise of stablecoin‑based commodity financing, and why Ethereum itself is increasingly framed as “digital oil” alongside Bitcoin’s “digital gold.”

Oil as a Commodity and Macro Benchmark

Physical Oil and Its Role in the Global Economy

Crude oil is first and foremost an industrial input, not a financial product. It is the feedstock for transportation fuels, petrochemicals, plastics, fertilizers, and countless industrial processes, which means its price ripples through everything from airline tickets to food costs. Because modern economies still depend heavily on hydrocarbon energy, oil functions as a de facto tax or subsidy on global growth: when prices spike, consumers and businesses feel an immediate squeeze; when they fall, real purchasing power rises.

Oil is also stratified into grades such as Brent, West Texas Intermediate (WTI), and various regional blends, each with its own sulfur content and density profile that determines refining economics. Benchmarks like Brent and WTI serve the same role that major equity indices do for stock markets, acting as reference prices upon which an enormous tower of futures, swaps, and options is built. These benchmarks are central to risk management for producers, refiners, airlines, shipping firms, and macro hedge funds that trade oil as a cross‑asset macro variable.

For crypto market participants, oil matters precisely because it anchors the global inflation and growth outlook that drives central bank policy. When energy is cheap and abundant, inflation pressure often fades and central banks can cut interest rates more easily, a context that has historically been constructive for risk assets, including Bitcoin and Ethereum. By contrast, oil shocks tend to push inflation higher, keep rates elevated, and tighten financial conditions, which can weigh on speculative assets even as they strengthen the case for “hard‑asset” hedges.

In recent years, the vulnerability of global supply chains to geopolitical shocks has become painfully clear. The acute disruption around the Strait of Hormuz, a maritime choke point that normally carries a large share of Middle Eastern exports, has been described as the worst supply shock in modern oil market history. Yet prices have remained below earlier doomsday forecasts of \(200\) dollars a barrel, partly because record United States exports, a pre‑war surplus, and an unexpected slowdown in Chinese demand have absorbed part of the shock. This kind of complex, adaptive response is precisely what makes oil such a rich macro signal for traders across both TradFi and crypto.

Price Formation: Supply, Demand and Geopolitics

Oil pricing is ultimately a story of marginal barrels and expectations. On the supply side, OPEC and its allies (often referred to as OPEC+) still exert meaningful influence by managing production quotas, but they operate within a broader ecosystem that includes US shale producers, Russian exports under varying sanctions regimes, and non‑OPEC countries such as Brazil and Norway. When OPEC+ chooses to increase output despite softening demand, as reflected in recent production hikes of several hundred thousand barrels per day, it can cap prices and compress volatility even in otherwise tense macro environments.

Demand, meanwhile, is tied to global growth, transportation patterns, and structural efficiency gains. A slowdown in Chinese crude imports, with inbound shipments reportedly slashed by close to forty percent over a given month relative to the prior year’s average, can offset a significant share of supply lost to war‑related disruptions. That reduction in demand helped cool prices after an early surge in the current Middle Eastern conflict and contributed to benchmark Brent crude retreating below \(100\) dollars a barrel after briefly spiking above \(140\). For macro‑focused crypto traders, such shifts in the physical market can be as important as onchain news.

Financial flows amplify these fundamentals. Hedge funds and commodity trading firms regularly express macro views through large futures positions, while commodity index products channel passive capital into long‑only exposure. Dislocations can appear when physical and financial markets diverge—such as sharp contango or backwardation in the futures curve—creating opportunities for sophisticated basis and arbitrage trades. Episodes like the Abraxas Capital oil trade, where the firm reportedly maintained a \(130\) million‑dollar short exposure in crude and at one point was paying funding equivalent to roughly \(600\) million dollars per year, illustrate how aggressive positioning can generate huge carry costs when the market structure breaks from expectations.

Geopolitics is the final, often dominant layer. Conflict involving major producers, sanctions regimes, and shipping disruptions can all manifest as extreme volatility in oil prices. During a recent Iran‑related escalation, for example, crude prices spiked to around \(100\) dollars a barrel amid fears of supply interruptions. Policymakers responded with measures such as temporary sanction waivers and the release of emergency reserves, highlighting how energy security and foreign policy are tightly interwoven. Each such episode feeds into the reflexive loop between oil, inflation expectations, and monetary policy that crypto traders increasingly watch alongside onchain metrics.

Oil, Inflation and Central Banks

Because of oil’s centrality to transportation and manufacturing, sustained price increases typically bleed directly into headline inflation prints. Central banks, particularly the Federal Reserve, monitor these dynamics closely when calibrating interest rate policy. When energy prices spike, they face a difficult trade‑off: tighten policy to prevent an inflation spiral, at the risk of slowing growth, or look through the shock in the hope that price pressures will prove transitory.

Recent policy communications have underscored how acute this tension can be. In one episode, Federal Reserve Governor Christopher Waller reportedly went into a policy meeting inclined to support rate cuts, only to reverse course after a war‑induced oil spike raised near‑term inflation risks. That shift helped postpone easing, even though the Fed still signaled that cuts later in the year remained possible. For digital asset markets accustomed to trading on the trajectory of real yields and liquidity expectations, such oil‑driven pivots are highly consequential.

The interplay between oil and inflation also shapes narratives around store‑of‑value assets. Investors like Robert Kiyosaki, author of “Rich Dad Poor Dad,” have long argued that fiat currencies are structurally inflationary, urging holders to accumulate hard assets like gold, silver, oil, Bitcoin, and Ethereum as a hedge against monetary debasement. In this view, oil’s role is twofold: it is both a real asset with intrinsic utility and a barometer of inflationary pressure that can justify broader hard‑asset allocation, including into digital currencies.

Forecasts from traditional banks provide a baseline for these debates. J.P. Morgan, for example, currently expects Brent crude to average around \(60\) dollars per barrel in 2026, citing “soft supply‑demand fundamentals” and visible surpluses in early‑year data. Their analysts project that oil demand will grow by roughly \(0.9\) million barrels per day, but supply is likely to outpace demand absent production cuts, which would otherwise lead to inventory build‑ups and lower prices. They still flag geopolitical risks as a wild card, but the central scenario is one of moderate prices and manageable inflation. Crypto traders overlay these macro baselines onto their own theses about Bitcoin’s halving cycle, Ethereum’s fee dynamics, and broader risk sentiment.

The Evolution of Commodities - state of commodities and a quantitative analysis of the growth of commodities markets onchain A new research report by Castle Labs

Hyperliquid's CL-USDC oil contract pulling $1.62B in daily volume with $170M OI — while only 7 of the top 30 HIP-3 markets are even crypto pairs — tells you where the actual demand is heading. Onchain commodities aren't a nice-to-have RWA narrative anymore; they're filling a structural gap that CME can't: weekend price discovery during geopolitical shocks like the Iran strikes, when trad markets are dark and the spot move has already happened by Monday open. The composability unlock is still underpriced though — once Aave or Morpho start accepting tokenized commodity positions as collateral (Ostium, Hyperliquid perps, even PAXG), you get a leverage loop on real-world vol that didn't exist 12 months ago, and that $3.1B tokenized commodity market starts compounding a lot faster.

Readers click 'OIL' not as a DeFi yield primitive but as a geopolitical pressure valve — they want to know when real-world oil shocks force macro hands (Fed holds, war risk), and whether crypto provides an alternative settlement rail or leveraged expression that traditional markets cannot.↗

Oil in Traditional Financial Markets

Futures, Options and Benchmarks

Modern oil markets rely on derivatives infrastructure that predates Bitcoin by decades. Futures contracts on crude and refined products allow producers and consumers to lock in prices months or years ahead, smoothing cash flows and protecting against adverse moves. A refinery might buy futures to hedge its input costs, while an airline could hedge jet fuel exposure. Speculators and market‑makers intermediate between hedgers, providing liquidity and taking directional risk.

Options add a further layer, enabling participants to buy downside insurance or express asymmetric views on volatility. Structured products, such as collars and swaps tied to oil benchmarks, are commonplace in corporate risk management. At the institutional level, commodity index funds and exchange‑traded products allow asset managers and pension funds to include commodities in diversified portfolios, often with systematic roll strategies along the futures curve.

This pre‑existing toolkit is important context for crypto because many of the instruments now emerging onchain—perpetual futures, tokenized commodities, synthetic exposure—consciously mirror or extend these structures. Oil perps on decentralized exchanges owe a clear intellectual debt to centralized futures markets, even as they introduce innovations like real‑time, algorithmic funding rates. Understanding the benchmark‑driven nature of oil pricing also clarifies why most tokenized oil instruments reference specific grades or indices: without a trusted benchmark, the entire hedging and speculation edifice would lack an anchor.

Market structure also shapes how shocks propagate. During severe disruptions such as the Hormuz crisis, spreads between physical prices and nearby futures can blow out, creating opportunities and risks for basis traders and arbitrage desks. Large commodity firms and hedge funds may use leverage to exploit these spreads, but financing and margin requirements can become punitive if trends move against them. The Abraxas example—where traders shorted crude in size and found themselves paying extraordinarily high funding to maintain the position—captures the way derivatives market structure can magnify the cost of being wrong on macro direction.

CME Group, Market Hours and the 24/7 Debate

CME Group sits at the center of traditional oil derivatives trading, offering benchmark crude, refined product, and energy futures that serve as the primary venue for institutional hedging and speculation. Historically, these contracts have traded nearly around the clock on weekdays but paused on weekends, reflecting the legacy rhythms of global commodity markets rather than the 24/7 tempo of crypto exchanges.

Recently, CME sought to push that boundary by proposing fully 24‑hours‑a‑day, seven‑days‑a‑week trading in certain crude and gold futures contracts. The idea is straightforward: macro risk is now continuous, and market participants would prefer the ability to adjust hedges and positions in real time, including over weekends when geopolitical events and crypto markets may be most active. For crypto‑native traders who are accustomed to perpetual access and gap‑less charts, the traditional weekend closure of major futures markets can feel increasingly anachronistic.

However, the United States Commodity Futures Trading Commission (CFTC) has reportedly considered blocking CME’s 24/7 oil contract bid, raising questions about how far regulators are willing to go in aligning legacy market hours with the always‑on paradigm of digital assets. Concerns range from the operational burden on intermediaries and clearinghouses to the potential for thinly traded off‑hours sessions to amplify volatility. For crypto participants, this regulatory tug‑of‑war is instructive: it illustrates both the demand for continuous commodity trading and the institutional constraints that may slow its adoption on traditional venues.

The more regulators hesitate, the more attractive onchain alternatives may become. Decentralized derivatives protocols are already offering round‑the‑clock oil exposure via perpetual swaps, and they do so without the institutional frictions of legacy clearing systems. This creates a dynamic where onchain venues can serve as price discovery arenas when traditional markets are closed, feeding back into Monday‑morning gaps and cross‑venue arbitrage. If CME cannot move to 24/7 trading, the center of gravity for marginal oil price discovery during stress episodes may continue shifting toward crypto‑native platforms.

Oil in Crypto Narratives and Macro Positioning

Hard Assets: Oil, Gold, Bitcoin and Ethereum

In the crypto community, oil is often grouped with gold, real estate, and other “hard assets” as part of a broader narrative about inflation hedging and currency debasement. Voices like Robert Kiyosaki explicitly advocate owning gold, silver, oil, Bitcoin, and Ethereum as protection against what they see as a structurally inflationary fiat system managed by “criminal” central banks. Whether or not one agrees with this rhetoric, the framing reveals how commodity and crypto markets coexist in many investors’ mental models.

The analogy between Bitcoin and gold is now mainstream. The Industrial and Commercial Bank of China (ICBC), the world’s largest bank by assets, released research explicitly describing Bitcoin as “digital gold,” citing its scarcity and store‑of‑value characteristics. In the same report, ICBC called Ethereum “digital oil,” underscoring its role as a utility asset that fuels decentralized applications and smart contract execution. This pairing is conceptually neat: Bitcoin is the inert, scarce reserve asset, while Ethereum is the energy source that powers an onchain economy, much as oil powers industrial activity.

Gold’s onchain trajectory reinforces this narrative. Tokenized gold products like Tether Gold (XAUT) and Pax Gold (PAXG) now account for the vast majority of the commodity tokenization market by value, with estimates suggesting they represent roughly seventy‑plus percent of total commodity token capitalization. One analysis notes that tokenized gold volumes in 2025 reached approximately \(178\) billion dollars, surpassing every major gold ETF by trading volume except GLD and ranking as the world’s second‑largest gold investment product by volume. This success has led some researchers to describe tokenized gold as a blueprint for broader commodity tokenization, including energy markets.

Oil fits naturally into this template, but with an important twist. Unlike gold, which is primarily held as a store of value or adornment, oil is consumed. It is both a speculative asset and an input into production, which means its value is tied to the real economy in a more direct way. For crypto investors who want exposure to macro growth, inflation, and energy security, oil can serve as a complement to Bitcoin and gold rather than a substitute. Ethereum, with its “digital oil” moniker, sits interestingly at this intersection, embodying both a scarce asset profile and a utility‑like role as gas for computation.

Risk Sentiment, Volatility and Cross‑Asset Correlations

Beyond narratives, oil functions as a practical macro hedge or risk factor in quantitative crypto strategies. During periods of geopolitical tension—such as the Hormuz crisis, which saw only a handful of supertankers still navigating the choke point, European diesel prices spike by around fifty percent, and fears of \(200\) dollar crude—volatility tends to rise across global markets. Crypto is not immune: liquidity can thin, funding rates can flip, and correlations to traditional risk assets often increase as portfolios de‑risk.

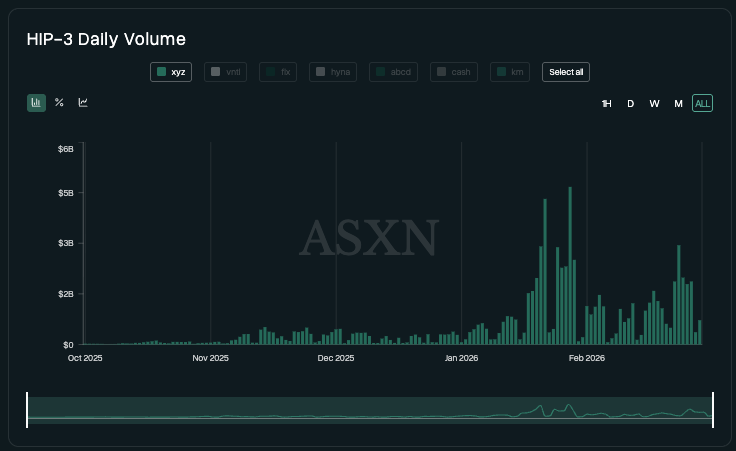

One recent pattern has been a surge in onchain derivatives activity during oil shocks, as traders look for high‑beta proxies to express macro views. Hyperliquid, a decentralized derivatives platform, registered a record weekend volume of roughly \(720\) million dollars in one episode, driven largely by oil and silver‑linked trades as geopolitical tensions flared and crude prices climbed above \(110\) dollars per barrel. More than \(160\) million dollars in oil perpetual contracts reportedly changed hands within a single 24‑hour period, demonstrating how quickly onchain venues can become focal points for macro speculation.

At the same time, oil‑driven growth or inflation shocks feed into expectations for central bank policy, which in turn influence Bitcoin and Ethereum valuations through the discounting of future cash flows and the availability of leverage. When oil spikes force policymakers like Fed Governor Waller to delay expected rate cuts, as recently occurred, the resulting higher‑for‑longer rates can pressure Bitcoin toward lower price levels, such as the \(60,000\) dollar region highlighted in some market commentary. For traders running multi‑asset portfolios, oil thus becomes a key input into cross‑asset positioning: long or short energy exposure may be paired with offsetting Bitcoin or ETH trades depending on the macro thesis.

Crypto‑native markets also respond in idiosyncratic ways. In one recent macro squall marked by renewed oil volatility and broader risk jitters, Solana’s ecosystem was noted for showing surprising internal strength despite the turbulent backdrop. This suggests that while oil shocks tend to tighten financial conditions across the board, their impact on specific digital assets can be mediated by ecosystem‑specific factors such as protocol revenues, DeFi usage, and narrative momentum. For sophisticated participants, oil is not simply a linear risk‑off trigger but a variable to be incorporated into nuanced, cross‑asset strategies.

- 01Geopolitical oil-crypto macro link↗

Iran war risk, Hormuz blockade scenarios, and OPEC+ supply hikes forcing Fed rate decisions pulled readers who track how energy shocks ripple into crypto markets and onchain leverage demand.

- 02Onchain oil derivatives access↗

Ostium v2 offering 200x leverage on oil and Elmnts tokenizing mineral royalties on Solana attracted readers seeking direct onchain exposure to energy markets previously locked in TradFi.

- 03ETH-as-digital-oil narrative↗

ICBC calling Ethereum 'digital oil' — a framing from the world's largest bank — gave institutional legitimacy to a thesis that crypto maps onto the global energy economy.

- 04Sanctions evasion via crypto oil trade↗

Venezuela's PDVSA pivoting to digital currency for crude exports and Tether threatening wallet freezes framed oil-crypto intersection as a live sanctions battleground, not a hypothetical.

- 05Digital yuan oil settlement↗

PetroChina settling crude with digital yuan at a state exchange signaled that petrodollar alternatives are operational, not theoretical — directly relevant to crypto's reserve-currency narrative.

- 06Tokenized commodity market growth↗

Castle Labs' quantitative report on onchain commodities gave data-oriented readers a framework for evaluating whether tokenized oil and gas assets represent a structurally new market layer.

Onchain Oil Exposure: Derivatives

Perpetual Swaps, Funding and Basis Trades

Perpetual futures, or perps, are the primary way crypto traders gain synthetic oil exposure onchain today. Unlike traditional futures, perps have no fixed expiry date. Instead, they use a funding mechanism in which long and short traders periodically pay each other based on the difference between the perp price and a reference index. When the perp trades above spot, longs pay shorts; when it trades below, shorts pay longs. This funding rate aligns perps with spot prices over time and serves as a real‑time barometer of positioning.

In the context of oil, this structure can generate substantial carry costs, especially when speculative positioning becomes one‑sided. The Abraxas Capital trade is illustrative: the firm maintained approximately \(130\) million dollars in short crude exposure via derivatives and, at the height of the dislocation, was reportedly paying funding equivalent to around \(600\) million dollars per year to keep the position open. That implies a funding rate that, annualized, exceeded the notional size of the position several times over, a level that is unsustainable except for short windows or highly hedged strategies. While details remain partly opaque, this episode underscores how mispriced basis and extreme funding can inflict large mark‑to‑market and cash‑flow pain even on professional desks.

Crypto‑native oil perps can exhibit similar dynamics, albeit with differences in counterparty structure and collateral. When geopolitical news drives crude sharply higher over a weekend, onchain oil perps may gap up, liquidating over‑levered shorts and driving funding rates deeply positive as late longs pile in. Traders who enter short positions to capture rich funding must carefully manage the risk that prices continue to rise; a \(4\) million‑dollar short in an onchain OIL‑denominated perp can face severe risk if volatility remains elevated and funding flips back and forth. In this environment, oil perps become not just instruments for expressing directional views but tools for sophisticated carry and volatility strategies.

Perps also facilitate cross‑market arbitrage between onchain and traditional venues. When CME oil futures trade at a different implied yield than decentralized perps, arbitrageurs can construct long‑short baskets to capture the spread, using stablecoins like USDT as margin. However, regulatory and operational frictions—such as limited 24/7 trading on CME and differing margin rules—mean that these arbitrages are not always straightforward. The fact that the CFTC is hesitant about 24/7 CME oil trading further reinforces the role of onchain markets as a separate, sometimes leading, arena for energy price discovery.

Onchain Platforms and Liquidity

Several platforms have emerged as hubs for onchain commodity derivatives. Hyperliquid is a prominent example, offering perpetual contracts on macro assets including oil and silver. During a recent oil shock, Hyperliquid’s HIP‑3 product posted a record weekend volume of roughly \(720\) million dollars, driven primarily by oil and silver volatility and increased onchain macro trading demand. According to analytics cited at the time, oil‑linked contracts generated more than \(160\) million dollars in volume over a 24‑hour period when crude climbed above \(110\) dollars per barrel. These statistics highlight how quickly liquidity can concentrate in a few key venues when macro events dominate the narrative.

Another notable platform is Ostium, whose V2 upgrade has positioned it as an onchain gateway to a broad spectrum of traditional markets. Ostium allows users to long or short major US and global equity indices, foreign exchange pairs, single‑name equities, commodities such as oil, gold, and copper, and cryptocurrencies like Bitcoin and Ethereum—all directly from a self‑custodied wallet, with leverage as high as 200x in some markets. The protocol advertises low trading fees, with total round‑trip costs for foreign exchange pairs as low as two basis points and funding rates designed to reflect underlying volatility. For oil traders, this means the ability to run multi‑asset macro strategies entirely within DeFi, collateralizing positions with stablecoins or crypto rather than fiat.

Research outfits like Castle Labs have begun to quantify the growth of onchain commodities trading, framing oil perps and related products as part of an “evolution of commodities” toward more transparent and accessible markets. Their analyses highlight rising onchain open interest, the concentration of liquidity in a handful of leading protocols, and the tendency for commodity volumes to spike during macro stress—mirroring the behavior seen historically on centralized venues. Together, platforms like Hyperliquid and Ostium illustrate how oil is becoming a first‑class citizen in DeFi’s emerging macro stack.

Infinityhedge breaks down Hormuz crisis: 9 supertankers left, EU diesel up 50%, $200 oil looms, and Trump unwinds Russia sanctions to fuel his own war

Trump is a dictator

Tokenized Commodities and Tokenized Oil

From Gold Tokens to a Broader Commodity Stack

Beyond derivatives, tokenization is bringing real‑world commodities onto blockchains as programmable assets. In a tokenized commodity structure, a custodian or issuer holds physical assets—such as gold bars or barrels of oil—and issues digital tokens that represent ownership claims on those assets. Holders can trade the tokens 24/7, use them as collateral in DeFi, or redeem them for the underlying commodity or cash equivalent, subject to issuer policies.

Gold has been the clear early leader in this market. According to research by Tiger, the total commodity tokenization market grew roughly four‑fold in one year, from about \(1.9\) billion dollars in early 2025 to roughly \(7.13\) billion dollars by February 2026. Approximately seventy‑three percent of that value is in gold‑linked products, with the top two tokens—XAUT and PAXG—accounting for over seventy percent of the entire commodity tokenization market by capitalization. A separate analysis by DWF Labs similarly notes that the tokenized commodities market exceeded \(1\) billion dollars in early 2025 and was on track to approach roughly \(8\) billion dollars by early 2026, reinforcing the picture of rapid growth from a small base.

Gold’s success has provided a concrete blueprint for other commodities. In a typical architecture, an institutional client wires fiat to the issuer, who then purchases London Bullion Market Association (LBMA)‑approved bars, stores them in a professional vault (for example, a Brink’s facility in London), and mints tokens only after the physical gold has been secured. Each minted token represents a fractional claim on specific bars, and redemptions reverse the flow: tokens are burned, and physical gold or cash proceeds are delivered to the redeemer. This mint‑on‑demand, redeem‑on‑burn model ensures that token supply tracks physical inventory and that onchain representations remain fully backed.

Other sectors are emerging, though at smaller scale. Energy‑linked tokens exist, such as JMWH, which tokenizes megawatt‑hours of electricity, and agricultural tokens like JSOY_OIL, structured with a one‑token‑per‑ton soybean oil mapping. However, onchain activity in many of these products remains thin, with some showing onchain traces mainly of mint and burn operations rather than active trading. Researchers point to fragmented regulation, the complexities of physical logistics, and limited venue listings as reasons why gold has so far captured the lion’s share of tokenized commodity liquidity.

Design of Tokenized Oil RWAs

Tokenized oil builds on this blueprint, but introduces unique challenges and opportunities given oil’s role as a consumable and logistically complex commodity. Chainlink, which provides oracle infrastructure for bringing offchain data onchain, has outlined a conceptual framework for tokenized oil as part of the broader real‑world asset (RWA) movement. In this framework, tokenized oil refers to digital tokens that represent ownership rights to crude oil, refined products, or even energy infrastructure and production capacity.

Two broad categories of tokenized oil are commonly discussed. The first is straightforward commodity tokens, where each token maps to a fixed quantity of physical oil, such as one barrel of West Texas Intermediate crude stored at a specified facility. These tokens can be used for trading, hedging, or as a stable store of value pegged to energy prices. The second category comprises tokens that represent equity or revenue rights in energy production, such as a claim on a share of a field’s output or a pipeline’s throughput revenues. These behave more like securities than simple commodity receipts and raise distinct regulatory issues.

The lifecycle of a tokenized oil commodity token begins with origination. A regulated custodian or energy producer verifies the existence, quality, and storage location of the oil inventory. Once verification is complete, a smart contract mints digital tokens, each corresponding to a defined unit of the underlying—often one token per barrel. The physical oil is held in secure storage facilities, while the tokens circulate globally on public or permissioned blockchains. Crucially, the token is designed as a programmable claim, not a mere tracking identifier: it can embed legal rights, redemption rules, and even conditional logic for interest or storage fees.

Trading occurs on centralized exchanges, decentralized exchanges (DEXs), or peer‑to‑peer, with settlement happening onchain at near‑instant speed. Traditional oil trades often settle on a T+2 or T+3 basis, tying up capital and introducing counterparty risk. Tokenized oil settles effectively at T+0, improving capital efficiency and enabling more agile risk management. When a holder wishes to redeem, they send tokens back to the issuer’s smart contract, which burns them and triggers either a release of physical barrels at a specified location or a cash payout based on prevailing prices. This redeemability is central to maintaining the peg between token and underlying asset.

Fractionalization is one of the key benefits emphasized by tokenization advocates. Buying and storing physical oil or investing directly in drilling operations typically requires substantial capital and operational sophistication. By splitting these exposures into smaller digital units, tokenization opens energy markets to a wider pool of investors who might otherwise be shut out. At the same time, tokenized oil can integrate with DeFi as collateral, enabling borrowing and lending against energy assets, constructing structured products, or building index‑like baskets that mix oil with gold, Bitcoin, and other onchain assets.

Case Studies: Mineral Rights and Infrastructure

Not all oil‑linked tokenization focuses on inventory; some target the upstream economics of production. Elmnts, a project built on Solana, is an example of this approach. Rather than tokenizing barrels in storage, Elmnts aims to tokenize oil and gas royalties and other mineral rights, opening up what it estimates to be a more than \(700\) billion‑dollar market in mineral rights in the United States alone to a global pool of investors. Mineral rights entitle owners to a share of revenue from oil and gas production, making them akin to long‑duration cash‑flow streams rather than pure commodity exposure.

By representing these rights as tokens, Elmnts seeks to make them divisible, tradable, and composable within Solana’s DeFi ecosystem. That could allow crypto investors to gain exposure to the economics of energy production without directly managing leases, contracts, or physical operations. At the same time, it offers mineral rights owners a potential new avenue for liquidity, as they can sell fractionalized interests rather than entire parcels. For Solana, which has been noted for its resilience during recent macro squalls, such RWA projects also demonstrate how a high‑performance L1 can host complex financial products linked to legacy sectors like oil and gas.

The intersection of crypto culture and fossil fuel majors is also visible in governance debates. For instance, former Gitcoin co‑founder Kevin Owocki publicly commented on his former DAO’s partnership with Shell, a major oil company, sparking discussion about whether Web3 public‑goods funding should engage with legacy hydrocarbon firms. This controversy illustrates that oil’s presence in crypto is not purely financial; it also raises questions about environmental impact, reputational risk, and the alignment between Web3 values and fossil fuel industries.

ICBC labels ETH 'digital oil', BTC 'digital gold'

Tether engages commodity traders on USDT lending

- 2025-01milestone

Russia ruble surges 40%, defying oil-sanction pressure

PetroChina settles crude trade in digital yuan at SHPGX

Ostium v2 launches onchain oil/commodity perpetuals at 200x

OPEC+ accelerates production hike, adds 411k bbl/day

CFTC considers blocking CME 24/7 oil futures contract

Hyperliquid HIP-3 hits $720M weekend record on oil-driven volatility

Stablecoins, CBDCs and Oil Trade Settlement

USDT and the Plumbing of Onchain Dollars

Stablecoins are the connective tissue between crypto capital and real‑world markets, and oil trading is no exception. Tether’s USDT is the largest dollar‑pegged stablecoin, with circulating supply roughly \(190\) billion dollars as of April 2026, up from about \(118\) billion at the start of 2025 and having crossed \(100\) billion in mid‑2024. Each USDT is designed to trade at one US dollar and is redeemable at par by verified institutional clients who pass Tether’s know‑your‑customer checks, while retail users rely on secondary markets and onchain liquidity to access the peg.

Tether’s reserves have evolved over the years, with the current mix dominated by short‑dated US Treasury bills and other cash‑like instruments. A recent attestation indicates that roughly seventy‑seven percent of reserves are in cash and short‑term US Treasuries, about six percent in other cash and equivalents, five percent in Bitcoin, four percent in gold, and small single‑digit percentages in secured loans and other investments. Auditing firm BDO provides quarterly attestations, and Tether has emphasized its non‑EU regulatory posture and the existence of a US‑regulated sibling stablecoin to serve American users. This balance sheet composition means that USDT is indirectly backed by some of the same safe‑asset instruments that traditional commodity traders use for collateral and margin.

The scale and liquidity of USDT make it de facto plumbing for onchain dollars, widely used as collateral and settlement currency in derivatives platforms like Hyperliquid and Ostium. When traders open or close oil perps, settle arbitrage trades, or collateralize positions that mix oil with Bitcoin or gold, USDT often sits at the center of the transaction. This ubiquity has led Tether to explore lending its “crypto billions” to commodities trading companies, considering US dollar lending opportunities as a way to deploy profits and diversify revenue streams beyond swap fees and seigniorage. Such lending could provide an alternative source of credit for commodity traders, who have traditionally relied heavily on banks and specialized trade‑finance houses.

Tether, Commodity Financing and Sanctions Compliance

Tether’s expanding footprint in commodity finance has drawn regulatory attention, particularly where oil exports intersect with sanctions regimes. In Venezuela, for example, the state‑run oil firm PDVSA has reportedly planned to increase the use of digital currencies in its crude and fuel exports after the United States reimposed sanctions and pressured intermediaries. Using digital assets for settlement can theoretically help circumvent restrictions on dollar‑based banking channels, though it also introduces new layers of traceability and risk.

In response, Tether has stated that it will freeze wallets using USDT to evade sanctions on Venezuelan oil exports, signaling a willingness to enforce compliance obligations and cooperate with regulators. This underscores a critical nuance: although stablecoins live on public blockchains and can be transferred peer‑to‑peer, centralized issuers like Tether retain the ability to blacklist addresses and freeze tokens at the contract level. That capacity turns stablecoins into a kind of programmable middleware where monetary policy, sanctions enforcement, and private issuer discretion collide.

The broader landscape of commodities and sanctions is evolving in tandem. The United States has temporarily lifted some sanctions on Russian oil during periods of acute supply stress, allowing other countries, such as India, to purchase previously stranded cargoes as part of a strategy to cool global prices. At the same time, lawsuits and allegations of fraud involving oil companies, such as the revived case against Citigroup over its alleged role in the Oceanografia scandal, show how legal risks and governance failures can sit alongside pure market risks in the commodity complex. Crypto‑based settlement and financing, whether via stablecoins or future tokenized credit instruments, will have to navigate this dense thicket of compliance and legal exposure.

Digital Yuan and the Multipolar Oil Payments System

Central bank digital currencies (CBDCs) add another layer to the future of oil settlement. China has been a first mover with its digital yuan, or e‑CNY, piloting transactions across various sectors. In a notable milestone, PetroChina reportedly purchased around one million barrels of crude oil at the Shanghai Petroleum and Natural Gas Exchange, settling the transaction in digital yuan. This was described as the first crude oil trade settled with e‑CNY on that platform, marking a symbolic step toward a multipolar energy payments system where the US dollar faces competition from state‑backed digital currencies.

Such experiments have implications for both geopolitics and crypto. On one hand, they demonstrate that digital representations of money—whether CBDCs or stablecoins—are increasingly being tested for large‑scale commodity trades, breaking the monopoly of traditional correspondent banking rails. On the other hand, CBDCs like e‑CNY are centrally controlled and permissioned, contrasting with the open, programmable nature of onchain stablecoins and tokenized commodities. The coexistence of these systems raises questions about interoperability, capital controls, and surveillance.

For crypto markets, the rise of CBDC‑settled oil trades is a double‑edged sword. It could accelerate the normalization of digital asset‑based settlement in commodity markets, making it easier for tokenized oil and gold products to find institutional acceptance. At the same time, state‑backed digital currencies could crowd out private stablecoins in certain corridors, especially where governments prefer tight control. The interplay between USDT, e‑CNY, and potential future CBDCs from other major economies will shape the architecture of cross‑border oil trade settlement over the coming decade.

Ethereum, “Digital Oil” and the Network Gas Metaphor

Gas Fees and Economic Energy

The metaphor of Ethereum as “digital oil” is rooted in the concept of gas. On Ethereum, every transaction or smart contract interaction consumes a certain amount of computational effort, measured in units called gas. Users pay for this gas in Ether (ETH), the network’s native token, with prices typically denominated in gwei, where one gwei equals one billionth of an ETH. Gas fees compensate validators for processing transactions and securing the network.

Three main variables determine a user’s total gas fee: the complexity of the transaction (how much gas it requires), the base fee per gas unit (which adjusts dynamically based on block congestion), and an optional priority fee or “tip” that users can add to incentivize faster inclusion in a block. The total fee is calculated by multiplying the sum of the base fee and priority fee by the amount of gas used. This structure is analogous to paying both a standard toll and an express‑lane surcharge to navigate a congested highway.

In this context, ETH functions as the fuel that powers a decentralized computational machine. DeFi protocols, NFT mints, DAO governance votes, and token transfers all consume ETH as gas, much as trucks and planes consume oil to move goods and people. When usage spikes—during NFT booms, memecoin manias, or high‑stakes governance episodes—gas prices can soar, mirroring how physical oil prices spike when demand surges or supply is constrained. Conversely, during quiet periods or after scaling improvements, gas prices typically fall, lowering the cost of transacting and deploying contracts.

For macro‑minded crypto investors, the gas economy introduces an internal “energy” dynamic distinct from external commodities like crude oil. ETH is both a speculative asset whose price is influenced by global liquidity and a utility token whose value is tied to the demand for blockspace. This dual identity is one reason ICBC’s research found the analogy of Ethereum as “digital oil” compelling: it captures both the productive and consumptive aspects of the asset within a broader digital economy.

ICBC’s “Digital Gold” and “Digital Oil” Framing

ICBC’s report categorizing Bitcoin as “digital gold” and Ethereum as “digital oil” is notable not just for its content but for its source. As the largest bank in the world by assets, ICBC serves a vast institutional clientele, and its framing helps legitimize narratives that have long circulated in crypto circles. Bitcoin’s fixed supply and halving schedule make the gold comparison intuitive: both are scarce, non‑yielding assets that many investors hold as long‑term stores of value and hedges against inflation or currency devaluation.

Ethereum’s comparison to oil, by contrast, emphasizes its role in facilitating productive activity. As a generalized smart contract platform, Ethereum is the base layer for a wide range of applications, from decentralized exchanges to lending platforms and NFT marketplaces. ETH is required to run all of these, much as oil is required to run physical industrial and transportation systems. Furthermore, Ethereum’s post‑EIP‑1559 fee‑burn mechanism means that a portion of gas fees are permanently removed from supply, introducing a “consumption” element that further strengthens the analogy: some ETH is continuously “burned” as the network is used, just as oil is burned as fuel.

Voices like Kiyosaki’s, which group oil, gold, Bitcoin, and Ethereum as recommended holdings, tap into this conceptual alignment between physical and digital assets. From a portfolio‑construction perspective, one could imagine a “macro hard‑asset basket” that includes tokenized gold, Bitcoin, Ethereum, and tokenized oil, perhaps financed in USDT and actively rebalanced based on macro indicators like oil prices, real yields, and onchain activity. While such products remain mostly hypothetical today, the building blocks—stablecoins, tokenized commodities, onchain derivatives, and smart‑contract platforms—already exist.

Fed's Waller went in ready to cut rates, but Iran war oil spike forced a hold — says cuts still possible later in 2026

All talk but no action. What is we are ready but oil spike forced a hold. Just say you aren't ready

CFTC actively considered blocking CME's 24/7 oil futures contract in June 2026, signaling aggressive regulatory posture toward commodity derivatives in both TradFi and onchain venues.

Oil price volatility driven by geopolitical events (Iran war risk, Hormuz crisis) directly amplifies liquidation risk in leveraged onchain oil positions at up to 200x, compressing time to insolvency.

Onchain perpetual platforms offering oil exposure (Ostium, Hyperliquid) carry oracle manipulation risk since oil price feeds from illiquid or geopolitically disrupted markets can be gamed during stress events.

Tokenized oil royalty platforms (Elmnts) and digital yuan settlement (PetroChina) both depend on centralized custodians or state actors controlling the underlying asset, undermining permissionless claims.

Onchain oil derivative markets remain thin relative to CME volumes; Hyperliquid's $720M weekend record during geopolitical turmoil shows demand spikes but also that liquidity is event-driven rather than structural.

Tether's commitment to freeze wallets used to evade Venezuela oil sanctions establishes that stablecoin infrastructure can be weaponized as a compliance chokepoint in energy trade flows.

Risks, Regulation and Market Structure

Commodity Law and Onchain Oil

As oil and other commodities migrate onchain through perps and tokenization, they enter a legal landscape that was not designed with decentralized networks in mind. In the United States, the CFTC oversees derivatives on commodities, while the Securities and Exchange Commission (SEC) focuses on securities and certain investment contracts. Many tokenized commodity products straddle these categories, and jurisdictional boundaries can be blurry. European frameworks like MiCA add another layer, with their own definitions and licensing regimes.

Research by Tiger highlights that roughly half of the nearly forty tokenized commodity products it tracks are unregulated, despite representing claims on physical assets. Even for gold, where practices and audits are relatively mature, proof‑of‑reserve mechanisms often fall short of the standards used in traditional markets. Some issuers provide regular attestations, but chain‑of‑custody documentation, insurance details, and legal enforceability of claims can vary widely. For oil and other energy products, which involve more complex logistics and higher storage costs, these challenges are even more pronounced.

Regulatory unease is also evident in the CFTC’s consideration of CME’s push for 24/7 oil and gold futures. While the core issue there is trading hours rather than tokenization per se, the reluctance to extend traditional market structures to an always‑on model hints at broader concerns about operational risk, liquidity fragmentation, and systemic stability. Onchain oil derivatives, with their global accessibility, permissionless participation, and leverage, may draw heightened scrutiny as they scale, particularly if they begin to influence price discovery in the underlying physical markets.

From a policy standpoint, authorities are likely to focus on three main areas: investor protection, market integrity, and financial stability. Investor protection concerns arise when retail traders access high‑leverage oil perps without fully understanding the risks of funding, liquidations, and volatility. Market integrity issues include the potential for manipulation via wash trading, spoofing, or oracles. Financial stability worries emerge if large, interconnected players in both TradFi and DeFi build substantial oil exposures that could transmit shocks across systems. Balancing innovation with these concerns will be a central regulatory challenge over the next decade.

Liquidity, Custody and Oracle Risk

Beyond regulation, tokenized oil and onchain oil derivatives face structural risks tied to liquidity, custody, and data feeds. Liquidity in most non‑gold tokenized commodities remains thin. Tiger’s analysis notes that outside gold, energy and agricultural tokens often show limited secondary trading, with some products recording mostly mint and burn transactions but little actual liquidity on exchanges. Thin liquidity exacerbates slippage, widens spreads, and increases the risk of price manipulation, all of which can deter institutional participation.

Custody is particularly complex for oil. Unlike gold bars, which can sit in vaults for years with relatively low handling risk, oil requires ongoing management of tanks, pipelines, and environmental safeguards. Ensuring that each token genuinely corresponds to high‑quality, unencumbered barrels in specific storage locations is non‑trivial. Any mismatch between token supply and physical inventory, whether due to fraud, operational failures, or legal disputes, could break pegs and undermine trust in the product class.

Oracle risk is another critical vector. Tokenized oil and oil perps depend on reliable price feeds to determine collateral values, funding rates, and redemption terms. Oracle providers like Chainlink aggregate price data from multiple sources and publish it onchain, but they must guard against manipulation, outages, and delays. In highly stressed markets—such as sudden embargoes, shipping disruptions, or extreme volatility—the availability and accuracy of reference prices can be compromised. If onchain protocol logic relies on stale or erroneous data, it may trigger cascading liquidations or mispriced redemptions.

Systemic risk is further amplified by concentration at the issuer and protocol level. Tether’s dominance in stablecoin collateral means that any shock to its reserves or reputation could have outsized effects on commodity trading that relies on USDT as margin or settlement currency. In the tokenized commodity space, the fact that a handful of gold tokens represent most of the market cap and volume concentrates custody and legal risk in a small number of entities. These are solvable problems—through diversification, robust audits, and redundant oracles—but they require deliberate design and governance choices.

How Crypto Traders Use Oil Today

Macro Hedges and Event Trades

For crypto‑native traders, oil serves both as a macro indicator and a direct trading venue. During geopolitical crises, traders may go long oil perps on platforms like Hyperliquid or Ostium while shorting equity indices or high‑beta altcoins, constructing cross‑asset hedges that straddle onchain and offchain markets. In scenarios like the Hormuz disruption—where key shipping lanes are blocked, supply losses exceed ten million barrels per day, and fears of \(200\) dollar oil circulate—these cross‑hedges help portfolios weather extreme moves.

Some traders pursue relative‑value strategies that exploit divergences between oil and other macro assets. For example, if oil prices spike but gold and Bitcoin lag, a trader might go long gold or BTC and short oil, betting on normalization of historical correlations. Conversely, if Bitcoin sells off sharply on fears that higher energy prices will prolong restrictive monetary policy, while oil remains elevated, traders might position for a catch‑up rally in BTC once macro panic subsides. These strategies rely heavily on quantitative models that monitor correlations, betas, and volatility regimes across time.

Onchain derivatives make it easier to express such views around the clock, especially during weekends when traditional futures markets are closed. Episodes like Hyperliquid’s record weekend volumes during oil shocks show that onchain venues can become primary outlets for event‑driven macro trades. The presence of high leverage and composable collateral means that even relatively small capital pools can deploy significant notional exposure, which both enhances opportunity and magnifies risk.

Macro commentators like Infinityhedge have also used oil events as teaching moments, breaking down the mechanics of supply chains, shipping, and policy responses. During the Hormuz crisis, for instance, analysts highlighted details like the reduced number of supertankers transiting the strait, sharp increases in European diesel prices, and policy maneuvers by the US administration, such as unwinding certain Russian oil sanctions to augment supply. These narratives give crypto traders a more granular understanding of the real‑world levers behind the price action they see on charts.

Structured Strategies Across Onchain and TradFi

More sophisticated players, including funds and proprietary trading firms, increasingly design structured strategies that integrate both onchain and TradFi oil markets. One template involves using CME futures to hedge directional risk while exploiting funding or basis differentials in onchain perps. For instance, a trader might short an oil perpetual swap on a DeFi platform where funding is extremely positive, while taking an offsetting long position in CME futures or in a tokenized oil product that closely tracks spot. The goal is to harvest funding income or basis mean reversion while remaining hedged in terms of net directional exposure.

Stablecoins like USDT are instrumental in these strategies, functioning as the primary margin asset on DeFi protocols and as an intermediate settlement medium when moving capital between exchanges. Tether’s exploration of direct lending to commodity traders points toward a future where stablecoins not only facilitate trading but also provide working capital for physical operations. This would blur the boundaries between speculative DeFi activity and real‑world commodity logistics, with stablecoin issuers effectively playing roles traditionally filled by trade‑finance banks.

Commodity tokenization unlocks additional paths. A fund could, in principle, hold tokenized gold, tokenized oil, and Bitcoin in a single onchain vault, dynamically rebalancing based on systematic signals or discretionary views. DeFi protocols might accept such tokens as collateral, allowing traders to borrow stablecoins against them for leverage or to fund other operations. In energy‑linked projects like Elmnts, investors can gain cash‑flow exposure to oil and gas production royalties, adding a quasi‑equity component to the mix.

Finally, national currencies of commodity exporters can play into these strategies. Recent performance of the Russian ruble, which reportedly surged over forty percent in a single year despite ongoing war, sanctions, falling oil prices, and economic headwinds, illustrates how complex the relationship between oil, macro fundamentals, and currency valuations can be. A sophisticated macro‑crypto strategy might involve long or short positions in tokenized forex, oil perps, and Bitcoin, all designed around specific hypotheses about how energy prices and sanctions will affect different economies and asset classes.

Outlook

Oil’s entanglement with crypto is deepening along multiple axes at once. At the macro level, crude remains a central driver of inflation, growth, and monetary policy, ensuring that Bitcoin, Ethereum, and other digital assets will continue to trade in its shadow whenever geopolitical shocks erupt. In market structure, crypto‑native derivatives platforms already offer 24/7 oil exposure, sometimes outpacing traditional venues in responsiveness and accessibility, especially as regulators hesitate to fully embrace always‑on trading on legacy exchanges.

In tokenization, the path blazed by gold shows that real‑world commodities can function as programmable, onchain collateral at meaningful scale. Oil is a more complex test case, but projects ranging from tokenized barrels to mineral‑rights platforms like Elmnts demonstrate growing experimentation across the value chain. The broader commodity tokenization market has already grown from under \(2\) billion dollars to over \(7\) billion dollars in approximately a year, with analysts projecting continued expansion as energy and agriculture follow gold’s lead.

Stablecoins and CBDCs add a geopolitical dimension. USDT’s role as the dominant onchain dollar, combined with Tether’s willingness to lend to commodity firms and freeze sanctioned wallets, positions stablecoins squarely in the middle of future oil financing and compliance debates. Meanwhile, digital‑yuan oil trades at venues like the Shanghai Petroleum and Natural Gas Exchange signal that state‑backed digital currencies will play an increasing role in energy settlement, potentially challenging the dollar’s hegemony and creating new competitive pressures for private stablecoins.

For crypto traders and builders, the key is to internalize oil not as an external curiosity but as an integral part of the onchain macro landscape. Oil perps, tokenized barrels, mineral‑rights tokens, and stablecoin‑denominated trade finance are all converging into a new, hybrid market structure where real‑world commodities and digital assets co‑exist on the same rails. Whether one is a DeFi protocol designer, a macro fund, or a retail trader, understanding how oil prices echo through funding rates, stablecoin flows, and ETH gas dynamics will become an increasingly necessary part of operating in the crypto economy.

Latest OIL news

The Evolution of Commodities - state of commodities and a quantitative analysis of the growth of commodities markets onchain

A new research report by Castle LabsInfinityhedge breaks down Hormuz crisis: 9 supertankers left, EU diesel up 50%, $200 oil looms, and Trump unwinds Russia sanctions to fuel his own warFed's Waller went in ready to cut rates, but Iran war oil spike forced a hold — says cuts still possible later in 2026Hyperliquid HIP-3 hits record weekend volume at $720M as geopolitical turmoil and surging oil prices drive traders to onchain derivatives Rich Dad Poor Dad author Robert Kiyosaki says schools “brainwash kids” to work for inflationary fiat, calling central banks “criminals” while urging investors to hold gold, silver, oil, Bitcoin, and Ethereum.

Rich Dad Poor Dad author Robert Kiyosaki says schools “brainwash kids” to work for inflationary fiat, calling central banks “criminals” while urging investors to hold gold, silver, oil, Bitcoin, and Ethereum. Wall St week ahead U.S. attack on Iran fuels stock market jitters as investors eye oil price spikes and retaliation risks

Wall St week ahead U.S. attack on Iran fuels stock market jitters as investors eye oil price spikes and retaliation risksSources

- https://dailyhodl.com/2024/06/11/biggest-bank-in-the-world-says-ethereum-is-digital-oil-bitcoin-digital-gold-report/

- https://www.mexc.com/news/888274

- https://www.ostium.com/blog/introducing-ostium-v2

- https://solanacompass.com/projects/elmnts

- https://x.com/CoinDesk/status/1783235018552234072

- https://www.facebook.com/our.today.news/posts/venezuelas-state-run-oil-company-pdvsa-plans-to-increase-digital-currency-usage-/401393602778796/

- https://blockworks.com/news/china-digital-yuan-oil

- https://www.bloomberg.com/news/articles/2026-06-12/cftc-considers-blocking-cme-s-24-7-oil-contract-bid

- https://x.com/arkham/status/2042550127752286309

- https://www.youtube.com/watch?v=OFaznAZFfOA

- https://x.com/castle_labs/status/2052037426206408892

- https://fortune.com/2026/06/06/oil-prices-biggest-supply-shock-history-china-imports-inventories-us-exports/

- https://www.youtube.com/watch?v=YtFDA3cePE0

- https://www.dwf-labs.com/research/how-tokenized-gold-turns-into-a-blueprint-for-the-commodities-market

- https://eco.com/support/en/articles/11819134-what-is-tether-usdt-2026-guide

- https://www.jpmorgan.com/insights/global-research/commodities/oil-prices

- https://reports.tiger-research.com/p/2026-commoditymarket

- https://chain.link/article/tokenized-oil-blockchain-energy-assets

- https://www.britannica.com/money/ethereum-gas-fees-eth

- https://www.bloomberg.com/news/articles/2024-10-14/tether-talking-to-commodity-traders-about-lending-its-crypto-billions-usdt

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…