Deep explainer on spreads in crypto, covering bid-ask, yield, funding and swap spreads, DeFi money markets, tokenized stocks, and malware propagation, with a focus on liquidity, risk, and how pricing gaps shape modern digital asset markets.

+7 sources across the wider coverage universe

Microsoft warns Tor-based crypto clipper spreads via USB shortcuts to steal seed phrases and swap wallet addresses2026-06

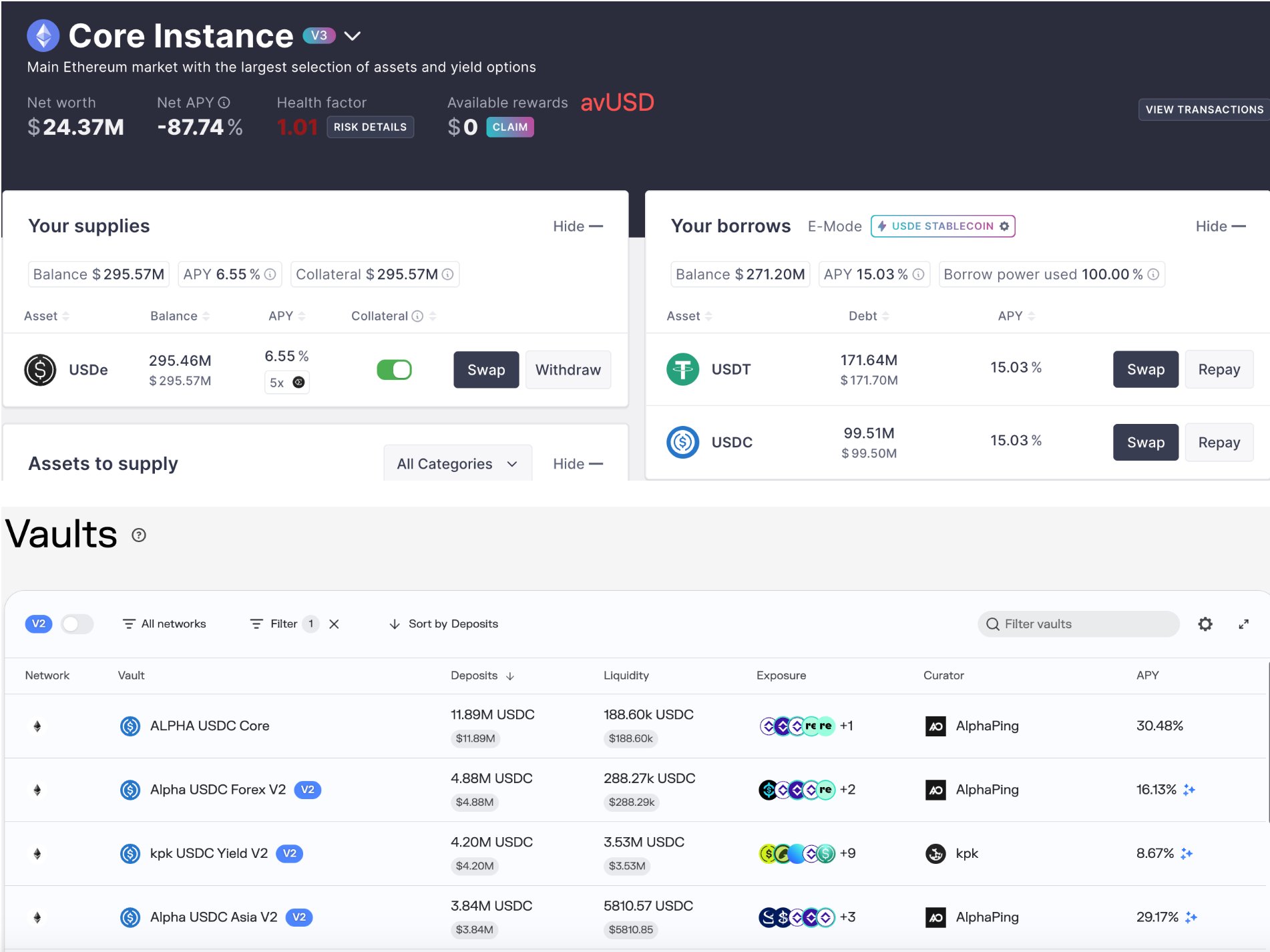

Microsoft warns Tor-based crypto clipper spreads via USB shortcuts to steal seed phrases and swap wallet addresses2026-06 Avant's avUSD hits -87% interest rate on Aave as contagion spreads to Morpho2026-04

Avant's avUSD hits -87% interest rate on Aave as contagion spreads to Morpho2026-04 Spreads is live, offering users to trade tokenized stocks, and copy trade politicians, funds, and social media equities portfolio in one click2026-03

Spreads is live, offering users to trade tokenized stocks, and copy trade politicians, funds, and social media equities portfolio in one click2026-03 Binance expands Spot Altcoin Liquidity Boost Program to 40 pairs, improving spreads, reducing slippage, and enhancing trading efficiency across supported altcoins2026-04

Binance expands Spot Altcoin Liquidity Boost Program to 40 pairs, improving spreads, reducing slippage, and enhancing trading efficiency across supported altcoins2026-04

Spreads in Crypto: Liquidity, Pricing Gaps, and How Risk Travels

In crypto, a spread is most often the gap between two related prices or yields, such as the difference between the best bid and best ask on an exchange, or the yield difference between two lending markets, and it functions as a compact measure of liquidity, risk, and market stress. The same word also appears in security coverage when malware “spreads” between wallets or platforms, so understanding spreads in crypto today means tracking both how prices diverge across markets and how threats propagate through the ecosystem.

Understanding “Spreads” in Crypto

The concept of a spread predates digital assets by decades, but crypto markets have made it far more visible to everyday traders. At its core, a spread is simply a difference: between two prices, between two yields, or between a synthetic rate and a benchmark. In spot markets, traders usually encounter the bid‑ask spread, defined as the difference between the highest price a buyer is willing to pay for an asset and the lowest price a seller is willing to accept. In yield markets, they encounter yield spreads, defined as the difference between yields on two debt or interest‑bearing instruments with different maturities, credit profiles, or risk characteristics. In derivatives and macro markets, they meet swap spreads, basis spreads between spot and futures, and option credit spreads, all of which encode information about risk and liquidity into a single number.

Crypto adds yet another layer, because the word “spreads” also appears in coverage of security incidents and malware campaigns, such as Microsoft’s warnings about Tor‑based crypto clippers that propagate via USB drives and attempt to hijack wallet addresses. This dual usage can be confusing, especially for new entrants who see headlines about “spreads widening” in bitcoin markets alongside warnings that “malware spreads” through wallets and exchanges. The unifying idea is that spreads, in both senses, describe how something moves through a system: one refers to how prices diverge across an order book or across venues, the other to how malicious code propagates across devices and users. Thinking in terms of flows—of orders, of capital, of risk, or of exploits—helps make sense of why journalists, exchanges, and security teams use the term so frequently.

Crypto also magnifies the importance of spreads because the market structure is fragmented, always on, and heavily retail‑driven. Unlike traditional equity markets, where a small set of exchanges and market makers dominate volumes, crypto liquidity is split across centralized exchanges, a growing number of on‑chain automated market makers (AMMs), orderbook‑style decentralized exchanges (DEXs), and a patchwork of derivatives venues. This fragmentation means that spreads can vary dramatically between venues at the same moment, and arbitrageurs must continuously work to keep them aligned. At the same time, DeFi lending protocols and derivatives platforms make yield and funding spreads visible at a granularity that would be unusual in traditional finance, with dashboards showing live net interest margins between protocols and negative funding rates in perpetual futures markets.

For a crypto news audience, spreads matter because they sit at the intersection of several major storylines: the push to tighten bid‑ask spreads and reduce slippage through liquidity programs and new AMM designs; the evolution of DeFi money markets and net interest spreads as platforms like Morpho, Aave, Compound, Spark, and others compete for deposits; the rise of tokenized equities and protocols literally branded “Spreads” that promise CEX‑like trading conditions inside DeFi; and the security battles in which Microsoft and other firms document how malware spreads through wallet infrastructure to steal crypto. Each of these domains uses the same word, but each tells us something different about how crypto markets function, how they break, and how they might evolve.

Hypercall brings S&P 500 options live next to SPCX with calls, puts, spreads, and strategy templates

Promoting from Tsunami auto-feed. Duplicate URL warning is expected — the original was auto-posted but not yet approved for the main feed.

Readers click 'spreads' for two opposite reasons that rarely overlap: platform alpha (a new venue letting retail copy-trade political portfolios in one click) and contagion alarm (a spread blowing out on Aave signals systemic stress) — meaning the word itself is a sentiment barometer, not a single topic.↗

Bid‑Ask Spreads and Market Liquidity

Defining the bid‑ask spread in crypto order books

In everyday trading, the most important spread is the bid‑ask spread, which quantifies the gap between the best available buying price and the best available selling price at a given moment. On a centralized exchange, the bid is the highest price any participant is currently willing to pay for a given coin, while the ask (or offer) is the lowest price any participant is willing to accept. The bid‑ask spread is simply the difference between these two prices, and it is often expressed either in absolute terms, such as \( \text{Spread} = \text{Ask} - \text{Bid} \), or as a percentage of the mid‑price, which approximates the asset’s fair value. In microstructure terms, the bid side of the book reflects demand, while the ask side reflects supply, and the spread is the price at which these two forces fail to meet.

Market makers sit at the heart of this process. They post both bids and asks, effectively standing ready to buy at the bid and sell at the ask, earning the spread as compensation for providing liquidity and bearing inventory risk. For a price taker, the spread acts as an invisible transaction cost: they must buy at the ask and sell at the bid, so simply turning over a position results in a loss equal to the spread, even before fees. For professional market makers, the spread is their primary revenue source, though in crypto they also earn exchange rebates or on‑chain rewards, and they must weigh this income against the risk of adverse selection if the market moves sharply against them. This balance between compensation and risk is why spreads tend to widen in volatile conditions and compress in calm markets.

Bid‑ask spreads also behave differently on various trading infrastructures, and crypto’s mix of centralized and decentralized venues makes this visible in a way that few other asset classes exhibit. Centralized exchanges like Binance, Coinbase, or smaller regional venues typically display order books where spreads in highly liquid pairs such as BTC‑USDT or ETH‑USD can narrow to a fraction of a basis point during peak hours. On the other hand, thinly traded altcoins or newly launched tokens may show spreads of several percent or more, reflecting both the lack of depth and the higher risk market makers perceive. When orderbook‑style DEXs launch on new chains, such as early deployments on a mainnet like Pharos for real‑world asset tokens, they often start with relatively wide spreads that narrow over time as more professional market makers engage and seeded liquidity deepens.

Spreads as a measure of liquidity and market health

Because the spread represents the marginal cost of immediately trading, it is one of the most intuitive metrics of liquidity. Investopedia notes that when the spread between bid and ask prices tightens, the market is more liquid, while a growing spread signals deteriorating liquidity. CoinMarketCap similarly emphasizes that the bid‑ask spread serves as a key measurement of market liquidity, with narrower spreads indicating that buyers and sellers can transact at prices closer together, and wider spreads indicating that the market is thin or stressed. In practice, traders often monitor both the spread and the depth behind it, since a tight spread backed by very little volume may vanish quickly when a larger order hits the book, resulting in hidden slippage.

Academic work on order book microstructure adds nuance to this view, examining how exchange fee structures and maker‑taker incentives shape spreads and depth. One such study shows that both spreads and price impact tend to decrease when the fee paid to market makers is close to the fee charged to market takers, implying that more symmetric fee schedules encourage tighter markets. For crypto, where fee tiers and rebate structures are often used to attract volume, this insight helps explain why some exchanges achieve tighter spreads than others in similar pairs. It also illustrates why on‑chain protocols that adjust fees dynamically, or offer concentrated liquidity incentives in particular price ranges, can materially improve realized spreads even if headline trading fees seem similar.

Beyond individual venues, there is also evidence of liquidity commonality across cryptocurrencies, meaning that liquidity conditions tend to move together across major assets. A study of the crypto market’s microstructure finds that liquidity, including measures like bid‑ask spreads, co‑moves across coins and exhibits seasonality, suggesting that broader market conditions, not just asset‑specific news, drive much of the variation. This implies that when volatility spikes or funding conditions tighten, spreads are likely to widen simultaneously across many tokens, reducing the benefits of diversification from a liquidity standpoint. For traders, this commonality underscores the need to monitor systemic indicators such as aggregate market depth and cross‑venue spreads, not just the micro metrics of a single asset.

Centralized exchanges, liquidity programs, and tight spreads

Centralized exchanges devote considerable resources to managing spreads because tight markets are both a competitive advantage and a regulatory expectation in many jurisdictions. They rely heavily on professional market makers, often offering fee discounts, rebate programs, and other incentives to keep spreads in flagship pairs extremely tight. Research on order book markets suggests that when fees for makers and takers converge, spreads and price impact can fall, which aligns with the design of some modern exchange fee schedules that aim to reduce asymmetric incentives. In crypto, this might take the form of volume‑based tiers where high‑frequency liquidity providers face very low net fees, enabling them to quote tighter spreads while still earning a positive net return.

Liquidity programs targeting specific altcoin pairs have become particularly visible as exchanges compete to offer better execution. Binance, for example, has promoted an Altcoin Liquidity Boost program that adds depth and aims to tighten spreads in selected spot markets, including pairs like CGPT/USDT, marketing these efforts as a way to reduce slippage and improve trading efficiency for users. While the details vary by platform, the underlying logic is consistent: by attracting more capital and more active quoting to a pair, the exchange can compress spreads, making the market more attractive, which in turn draws more volume and further improves liquidity. This feedback loop is powerful but can also reverse quickly if incentives are withdrawn or if broader market interest fades.

Crypto‑native analytics around specific tokens illustrate what “tight spreads” look like in practice. Weekly updates from protocols like ZeroBase have highlighted periods where its ZBT token maintained average top‑of‑book bid‑ask spreads around 0.45 percent while trading in a relatively narrow price band, signaling healthy liquidity conditions for a mid‑cap asset. CoinGecko data show that ZBT has at times posted daily trading volumes in the multimillion‑dollar range, with price moves over a week in the mid‑single‑digit percentage range, a profile consistent with reasonably deep markets for a token of its size. Commentary around ZBT frequently describes its tight spreads as both a sign of strong market‑maker engagement and a potential indicator of resilience, even when broader crypto markets turn choppy. The underlying message is that for traders, tight spreads reduce the cost of entering and exiting positions, making it easier to manage risk in volatile environments.

On‑chain AMMs, prop AMMs, and CEX‑tight execution

On the decentralized side, AMMs initially traded off tight spreads for simplicity, but new designs increasingly promise CEX‑like execution. In constant‑product AMMs, the shape of the pricing curve means that effective spreads widen as trade size grows relative to pool depth; small swaps may see negligible differences between execution and mid‑price, while larger trades experience significant price impact. As DeFi matured, protocol designers and professional market makers sought ways to narrow effective spreads while preserving the non‑custodial benefits of on‑chain trading. Concentrated‑liquidity AMMs and proactive‑market‑maker (prop AMM) designs emerged as key innovations, allowing liquidity providers to place capital in tighter price bands and enabling algorithms to update quotes in response to oracle prices.

Recent coverage of Solana‑based prop AMMs, for example, emphasizes sub‑second quote updates, oracle‑driven pricing, and resistance to MEV as tools to deliver “top execution” and “CEX‑tight spreads” on‑chain. These AMMs update pool parameters based on external price feeds, collapsing the wedge between on‑chain and off‑chain prices more quickly than earlier, purely passive designs. In parallel, new orderbook DEXs are launching on L2s and app‑chains specifically for real‑world asset tokens such as pAlpha, with teams explicitly positioning tighter spreads and deeper on‑chain liquidity as key value propositions for institutions looking to trade tokenized credit or private assets. By coordinating with professional market makers and seeding initial liquidity, these launches aim to start life with spreads that resemble a mature centralized market rather than a thinly traded altcoin pair.

Prediction markets and the economics of fixed‑width spreads

Prediction markets add a distinctive twist to the spread story because many platforms standardize outcomes on a \$0–\$1 price range, allowing analysts to talk about spreads in cents rather than percentages. MetaMask’s research into prediction markets notes that a 5‑cent spread is commonly observed in mid‑tier markets with daily volumes in the tens of thousands of dollars, and that such a spread typically signals moderate liquidity rather than extreme thinness. In a market where contracts settle at \$1 if an event occurs and \$0 otherwise, a bid‑ask spread of \$0.05 around a mid‑price of \$0.50 corresponds to a 10 percent spread relative to the mid‑price, which is wider than in major spot crypto pairs but often acceptable for retail traders seeking exposure to idiosyncratic events.

However, as on‑chain prediction platforms scale and as exchanges like Coinbase discuss launching new prediction markets alongside tokenized U.S. stocks, attention has turned to the risk that wide spreads signal thin seas, to borrow the language of some recent coverage. In illiquid markets, a nominal 5‑cent spread might conceal very shallow depth, meaning that a slightly larger order could move the implied probability sharply and offer free arbitrage to better‑informed traders. Conversely, when market makers or specialized firms come in to tighten spreads around key events such as elections or macro data releases, they help transform prediction markets from speculative casinos into more reliable aggregators of information. The interplay between listing breadth, market‑maker engagement, and spread width in these new Coinbase and DeFi prediction venues will be one of the key determinants of whether they evolve into deep markets or remain niche side‑pools.

Yield, Interest and Funding Spreads in DeFi

Yield spreads: from bonds to stablecoin markets

Outside of spot trading, the most important spreads are yield spreads, which measure the difference between the yields on two interest‑bearing instruments. Investopedia defines a yield spread as the difference between yields on debt instruments of varying maturities, credit ratings, issuers, or risk levels, and emphasizes that these spreads are closely watched indicators of credit risk and macro sentiment. In traditional finance, investors track spreads such as the difference between corporate bonds and Treasuries, or between high‑yield and investment‑grade indices, to gauge how much extra compensation the market demands for bearing default risk. The absolute level of yields matters, but the spread relative to a benchmark often conveys more information about perceived vulnerability and the availability of credit.

In crypto, that logic translates into the difference between yields on different DeFi lending protocols, stablecoins, or strategies. Instead of comparing a BBB‑rated corporate bond to a sovereign bond, a stablecoin lender might compare the APY for depositing USDC on Aave v3 versus a Morpho vault, or the yield on a governance‑backed “super‑saver” stablecoin like Spark SSR versus a more conservative protocol like Compound. Eco’s 2026 overview of DeFi lending platforms reports that USDC supply rates on Aave v3 typically sit in the 3–6 percent range depending on chain and utilization, while Morpho’s top vaults often deliver around 4–8 percent on USDC or USDT, with specific yields depending on the curator and strategy. Spark SSR is described as providing relatively predictable mid‑single‑digit yields on its native USDS, while Compound v3 tends to offer 3–5 percent, reflecting a more conservative, narrower set of markets. These differences are exactly the kind of yield spreads that capital allocators watch closely.

The existence of yield spreads across similar assets reflects differences in risk, design, and incentives. A vault that delivers higher yield on the same stablecoin often does so because it is taking additional smart contract risk, rehypothecating collateral, concentrating exposure in a smaller set of borrowers, or relying on governance to backstop losses. Conversely, a protocol that offers lower yields may be providing more conservative collateral policies or benefiting from stronger implicit guarantees. In DeFi, where risk disclosures are often minimal and on‑chain activity can be complex, yield spreads serve as one of the clearest market signals about perceived risk and about how aggressively platforms are competing for deposits.

Interest spreads, net interest margin, and token economics

Within a single protocol, the notion of interest spreads mirrors the net interest margin that banks earn: the difference between the interest rate paid to depositors and the rate charged to borrowers. In DeFi, this spread is often captured partly by the protocol treasury, partly by liquidity providers or token holders, and partly by external stakeholders such as liquidators or insurance funds. For example, when a money market like Aave or Compound charges borrowers a variable rate that floats above the deposit APY, the difference contributes to protocol reserves or is redirected to governance token stakers, aligning token value with platform usage.

Newer money markets and governance tokens explicitly foreground these spreads in their economic design. Coverage of ZentraFinance’s launch of its $ZNT token on the Citrea ecosystem, for instance, highlights that 90 percent of fees, interest spreads, liquidation proceeds, flash loan revenues, and external rewards will accrue to ZNT stakers, effectively turning net interest margin into a direct yield stream for token holders. This approach is conceptually similar to how banks monetize spreads between funding and lending, but in DeFi it is codified in smart contracts and mediated by governance. By making the interest spread an explicit source of token value, such designs aim to align incentives around long‑term protocol health rather than short‑term emissions.

At the same time, these tokenized interest spreads can introduce new risks. If governance has strong incentives to maximize spreads, it may be tempted to underpay depositors or overcharge borrowers, pushing users to competing platforms and triggering liquidity flight. Conversely, if the spread is narrowed too aggressively in pursuit of growth, the protocol may lack resources to build reserves or cover unforeseen losses. The fact that DeFi yield curves and spreads are visible in real time, often aggregated across platforms by dashboards like DeFiLlama, creates both an opportunity for sophisticated cross‑protocol arbitrage and a risk that abrupt shifts in spreads will spark rapid capital flows that stress the system. Yield spreads in DeFi thus serve as both an income opportunity and an early warning indicator of platform‑level or market‑wide stress.

Negative rates, inverted spreads, and contagion

Sometimes yield and interest spreads tell a more alarming story, especially when they turn negative or behave in ways that contradict economic intuition. Traditional finance offers a parallel in the form of negative interest rate swap spreads, where the fixed rate on an interest rate swap trades below the yield on a government bond of the same maturity, signaling unusual pressures in the government bond or derivatives markets. The Bank for International Settlements describes a swap spread as the difference between the interest rate swap rate and the yield on a government bond with the same maturity, and notes that negative spreads in some currencies have been interpreted as signs of balance sheet constraints or safe‑asset scarcity.

In DeFi, analogously odd phenomena appear when stablecoin lending rates crash or turn sharply negative on specific assets, sometimes because of incentive programs, sometimes because of structural imbalances. Recent coverage from crypto newsrooms has described episodes where tokens like Avant’s avUSD posted highly negative effective interest rates on Aave, with on‑chain data showing double‑digit negative APYs as deleveraging and liquidity flight cascaded across integrated platforms like Morpho. While the precise numbers and causes vary, the general pattern is clear: when a platform’s design or incentive structure allows yields to turn sharply negative, capital will likely flee, and the damage can “spread” to connected protocols through shared collateral, rehypothecated positions, or integrated vaults. In this sense, yield spreads between platforms become a channel for contagion, not just a signal of it.

Narratives around contagion in DeFi echo those in traditional markets, but with a twist: smart contracts can amplify or accelerate feedback loops. If a rapidly falling stablecoin yield drives depositors away from one platform, the resulting drop in liquidity can spike utilization and borrowing costs for remaining users, prompting further outflows. Where positions are cross‑collateralized or auto‑rebalanced through protocols like Morpho vaults, these shifts can cascade into other protocols, changing yield spreads elsewhere. Journalistic metaphors describing this process often borrow imagery from disease dynamics, reminiscent of MIT research that modeled how airports like New York, Los Angeles, and Honolulu would disproportionately accelerate the spread of pandemics through air travel networks. In DeFi, major stablecoin lending platforms play a similar role, serving as hubs through which yield and liquidity shocks spread to the rest of the ecosystem.

Liquidity spirals in money markets

Yield spreads and liquidity are tightly intertwined in DeFi money markets, and in stressed conditions they can generate liquidity spirals. When liquidity is ample and borrowers are healthy, yields tend to cluster within a moderate range across major platforms, reflecting competition but also shared risk constraints. However, when collateral prices fall or when a protocol suffers reputational damage, lenders may withdraw funds, pushing utilization higher and forcing the protocol to raise borrowing rates. Higher borrowing costs can lead to deleveraging, which may depress collateral prices further, undermining confidence and prompting additional withdrawals. Along the way, yield spreads between this protocol and its competitors widen, signaling stress.

Crypto coverage of episodes like the avUSD rate crisis often uses the language of contagion “spreading” from one protocol to another, but underneath that metaphor is a mechanical story of interest spreads and collateral dynamics. As deposit yields collapse on the troubled platform and spike on safer alternatives, rational capital moves, but in so doing it can destabilize interlinked structures such as leveraged farming strategies or cross‑margin positions. Smart contracts that automatically chase the highest yield can exacerbate these moves, turning what might have been a contained event into a system‑wide repricing of risk. For traders and long‑term investors, monitoring yield spreads across platforms is therefore not just an optimization exercise but a key part of risk management.

- 01Spreads.fi tokenized equity copy-trading↗

The platform's pitch — trade tokenized stocks and mirror politicians' or funds' portfolios in one click — hit a nerve with readers primed for RWA and social-trading narratives simultaneously.

- 02avUSD Aave contagion blowout↗

An -87% interest rate on a stablecoin inside a top lending protocol is a systemic stress signal; readers treat it as an early-warning spread for broader DeFi contagion.

- 03Binance altcoin liquidity program↗

A centralized exchange actively subsidizing tighter spreads across 40 pairs signals that thin altcoin liquidity is a recognised structural problem, not a fringe edge case.

- 04USB malware hijacking wallet addresses

Microsoft's warning about a Tor-routed clipper that spreads via USB shortcuts tied 'spreads' to a real, deniable attack vector that hits non-technical holders hardest.

- 05PropAMM oracle-driven spread compression↗

Oracle-priced AMMs promising CEX-tight spreads and MEV resistance represent the leading structural alternative to constant-product pools, drawing readers tracking execution quality.

- 06Prediction market bid-ask efficiency↗

Wide spreads in prediction markets directly erode expected value for informed bettors, making spread width a proxy for market maturity and manipulation resistance.

Spreads in Derivatives and Cross‑Asset Markets

Basis spreads between spot and futures

Beyond spot and lending markets, crypto derivatives introduce basis spreads, the difference between the price of a futures contract and the underlying spot price. In bitcoin and ether markets, perpetual futures dominate volumes, and their prices rarely deviate far from spot because funding payments incentivize convergence. Nevertheless, when funding becomes persistently positive or negative, the implied basis represents a spread that traders can harvest through basis trades. CV5 Capital, for example, has highlighted periods where bitcoin perpetual futures funding rates remained negative on a 30‑day average around minus 5 percent despite a rally in the underlying token, creating opportunities for institutional funds to earn yield by buying spot and shorting perps.

In such a trade, the fund is effectively long the underlying asset and short the derivative, collecting the funding payments that perpetual shorts pay to longs when funding is negative. The spread here is the difference between the implied carry on the perp and the financing cost of holding spot, adjusted for exchange risk, leverage, and margin requirements. If markets remain backwardated (with futures trading below spot) for an extended period, this funding spread can deliver sizable returns without directional exposure, at least in theory. But in practice, basis trades involve significant risks: exchange counterparty risk, liquidity risk if positions must be unwound quickly, and basis risk if the spread does not behave as expected.

For crypto markets, basis spreads also encode macro sentiment. When futures trade at a premium to spot and funding is strongly positive, it often signals bullish leverage and speculative froth. Conversely, persistent negative funding and discounted futures prices can signal either hedging demand from long spot holders or skepticism about sustained price levels. News stories emphasizing that negative funding has persisted “despite” rallies often imply that institutional hedgers or cautious market makers are skeptical of the move, using perps to hedge while maintaining spot exposure. Understanding these basis spreads is therefore critical not just for arbitrageurs but for anyone trying to read the positioning of different market participants.

Funding spreads, directional crowding, and liquidity

Funding spreads also intersect with liquidity and order book dynamics. When funding is very positive, going long perpetual futures is costly, and traders may switch to spot or to other derivatives such as dated futures or options, reducing liquidity in perps and potentially widening their bid‑ask spreads. When funding is very negative, as in the CV5 example, traders are incentivized to go long futures and short spot, which can concentrate liquidity in derivatives venues and thin out spot markets. These shifts can widen spreads in the less favored venue and create cross‑venue dislocations that arbitrageurs must work to close.

In DeFi, on‑chain perpetual protocols replicate this dynamic, but with additional layers such as oracle latency and AMM mechanics. Funding rates in AMM‑based perps adjust based on differences between the AMM’s mark price and the oracle price, creating implicit spreads within the pricing curve. If liquidity providers withdraw capital when volatility rises, the effective depth of the AMM shrinks, widening the execution spread between small and large trades in a self‑reinforcing way. Protocols that integrate prop AMM features, sub‑second quotes, and CEX‑grade oracles aim to stabilize these spreads by keeping on‑chain prices tightly anchored to off‑chain markets, reducing the scope for extreme funding dislocations.

Credit spreads and options strategies

Options markets bring yet another category: credit spreads as an options strategy, not to be confused with credit spreads in bond markets. Charles Schwab defines a credit spread strategy as one in which a trader simultaneously buys and sells options of the same class—both calls or both puts—on the same underlying with the same expiration date but different strike prices. The trader receives a net credit upfront because the option sold is more expensive than the one purchased, and this credit represents the maximum potential profit, while the difference between strikes minus the credit defines the maximum loss. Schwab notes that such strategies are often used to reduce risk by accepting a limited profit in exchange for a defined and typically smaller potential loss, and that in many cases, traders can calculate the exact risk at entry.

In crypto, option credit spreads are increasingly used to express views on volatility and directional movement while capping worst‑case losses. For example, a trader who believes that bitcoin will remain below a certain level might sell a call at that strike and buy a higher‑strike call, collecting a net premium. The spread between the two strike prices defines the risk window, while the premium spread defines the payoff. Market makers and vol desks watch the spreads between implied volatility across strikes and maturities, constructing complex positions that resemble traditional equity derivatives strategies. As centralized venues expand their crypto options suites and DeFi protocols experiment with on‑chain options and structured products, credit spreads and other multi‑leg strategies are likely to become more important in hedging and yield generation.

Swap spreads, rising yields, and macro stress

In macro markets, swap spreads are a key barometer of stress, especially in bond and rates markets. The BIS defines a swap spread as the difference between the interest rate on an interest rate swap and the yield on a government bond of the same maturity, and its research has pointed out that negative spreads can signal pressures in government bond markets, balance sheet constraints, or changes in demand for safe assets. When swap spreads widen, it may indicate growing credit concerns or reduced willingness of dealers to warehouse risk; when they compress or turn negative, it can reflect either demand for swaps as hedging tools or anomalies at the sovereign bond level.

Crypto news coverage has increasingly drawn parallels between swap spreads in traditional markets and stress indicators in digital assets, especially during episodes of rising Treasury yields linked to geopolitical events or conflicts. Commentators note that if swap spreads widen sharply in response to events such as conflicts in the Middle East, it could herald broader financial “squalls” that eventually hit risk assets, including bitcoin and other cryptocurrencies. In such environments, spreads of many kinds tend to widen: corporate bond spreads over Treasuries, cross‑currency basis spreads in FX markets, and bid‑ask spreads in less liquid crypto pairs. The language of “squalls” and “storms” used in crypto media captures this idea that changes in macro spreads can propagate into digital asset markets, challenging assumptions about bitcoin’s role as an uncorrelated asset.

For a crypto trader or investor, tracking macro spreads alongside crypto‑specific spreads offers a more complete picture of risk. Bitcoin has been dubbed a “canary in the coal mine” for risk‑off moves by research from firms like Bitwise, which argue that crypto often reacts more quickly than equities or credit to shifts in liquidity conditions or risk appetite. If swap spreads begin to widen and equity volatility picks up, while bitcoin’s bid‑ask spreads widen and basis spreads in futures shift from positive to negative, the combination paints a picture of tightening financial conditions that could affect everything from DeFi lending spreads to tokenized equity markets.

Tokenized Equities, RWAs and DeFi Platforms Named Spreads

Coinbase, tokenized stocks, and liquidity fragmentation

One of the more ambitious developments at the intersection of crypto and traditional finance is the push to list tokenized equities and build full‑fledged securities markets on crypto rails. Coinbase has announced that it is increasing its bitcoin holdings and plans to launch tokenized U.S. stocks and prediction markets, effectively bringing thousands of traditional securities into a crypto‑native trading environment. Reports suggest that Coinbase is preparing to support thousands of tokenized stocks, potentially numbering in the high four digits, alongside new on‑chain prediction venues linked to macro events and corporate outcomes.

This expansion raises immediate questions about spreads and liquidity. Traditional equity markets are already fragmented across exchanges and dark pools, but they benefit from consolidated tape, regulatory market‑making obligations, and large institutional participants. In contrast, tokenized stocks on a crypto venue may lack both regulatory obligations for market makers and deep pools of natural order flow, especially in long‑tail names. If Coinbase and similar platforms list thousands of names without corresponding market‑maker commitments, many could trade with very wide bid‑ask spreads, exposing retail traders to significant transaction costs and price gaps. Crypto news commentary has already warned that taking on 8,000‑plus tokenized stocks entails navigating substantial “liquidity risks and widening spreads,” particularly if the listing pace outstrips the capacity of market makers to quote tight markets.

On the other hand, tokenization could also bring new forms of liquidity and spread compression. If tokenized equities can be used as collateral in DeFi protocols, integrated into copy‑trading strategies, or combined with yield‑bearing stablecoins in structured products, the resulting capital flows might support tighter spreads even in mid‑cap names. The key question is whether on‑chain venues can attract enough professional liquidity providers and whether fee structures and incentive programs will mirror the tight‑spread conditions of established equities markets. As with crypto spot markets, spreads will be the first and most visible indicator of whether tokenized equity trading is functioning efficiently or merely providing a thin, speculative overlay.

SpreadsFi as a composability layer for tokenized stocks

Perhaps unsurprisingly, one of the high‑profile projects in this area has chosen to call itself SpreadsFi, signaling just how central spreads are to its vision. Alea Research describes SpreadsFi as a composability layer built on top of tokenized equity infrastructure, adding a stock terminal, copy‑trading features, and vaults such as sprUSD so that tokenized equities can be farmed and traded entirely within DeFi without routing back to a traditional brokerage. According to this research, SpreadsFi aims to let users follow the portfolios of politicians, funds, and social media personalities in a single click, effectively turning on‑chain tokenized stocks into a social trading environment.

In this context, spreads play several roles at once. At the execution level, the platform must keep bid‑ask spreads in tokenized equities tight enough for copying and rebalancing portfolios to be economical, especially for smaller users. At the strategy level, the vaults and structured products must manage yield and funding spreads across tokenized assets, stablecoins, and DeFi lending markets, attempting to harvest net interest margin or basis spreads while controlling risk. At the governance level, any protocol token associated with SpreadsFi or similar platforms may stake claims on fee income, spreads from routing and execution, or interest spreads from integrated money markets. Each of these layers depends on tight operational control of spreads in the underlying markets, without which the user experience and risk profile would deteriorate.

The naming of a platform after spreads underscores something deeper about DeFi’s evolution: spreads are no longer just background microstructure statistics but explicit design parameters and sources of value. Whether in money markets that route interest spreads to token holders, derivatives platforms that package funding spreads into basis‑trading products, or equity‑focused projects like SpreadsFi that foreground execution and yield spreads in their branding, the decomposition of financial returns into spreads is becoming part of the user‑facing story. This is a sign that crypto markets are maturing, but it also raises the bar for transparency and education, since misunderstandings about how spreads are generated and who bears the risk can lead to misplaced trust.

Orderbook DEX launches and RWA liquidity

Real‑world asset (RWA) platforms face similar spread challenges as tokenized equities but often under tighter regulatory and institutional constraints. When a protocol launches the first orderbook DEX for RWA tokens like pAlpha on a chain such as Pharos, the explicit goal is to enable secondary trading, tighter spreads, and deeper on‑chain liquidity for assets that might otherwise be locked in siloed structures. To support healthy price discovery from day one, project teams like Agra have indicated that they will seed initial liquidity, coordinate with professional market makers, and partner with other DeFi protocols to drive participation. The hope is that by starting with relatively tight spreads and solid depth, the DEX can attract organic, institution‑grade volume and avoid the perception of being a lightly traded, high‑spread niche venue.

For RWAs, spreads are not just a matter of trader convenience but of institutional viability. Asset managers accustomed to bond or syndicated loan markets expect to transact within relatively narrow spreads around evaluated prices, and they often face internal or regulatory constraints on what they can accept. If an on‑chain RWA market posts spreads that are several percent wide for moderately sized trades, institutions may treat that as a signal that the venue is not yet suitable for serious business. Conversely, if an orderbook DEX can demonstrate stable, tight spreads with minimal slippage for block‑sized trades, it bolsters the case for on‑chain settlement of assets like private credit, real estate claims, or structured products. As in other areas, spreads become the visible interface between legacy financial norms and the experimental architecture of DeFi.

ZEROBASE and ZBT: a case study in tight spreads

ZeroBase’s ZBT token offers a concrete example of how mid‑cap crypto assets can use spreads as a narrative and performance indicator. Weekly updates from the project have documented periods in which ZBT traded within relatively narrow price ranges—for instance, oscillating between roughly \$0.148 and \$0.166 in one week—while maintaining tight average top‑of‑book spreads around 0.5 percent. In later periods, ZBT reportedly navigated more volatile ranges, such as \$0.067 to \$0.080, yet still held spreads near 0.45 percent, signaling that liquidity providers remained engaged even as price action grew choppier.

CoinGecko data confirm that ZBT has, at various times, sustained daily trading volumes around \$7–8 million while posting modest percentage price moves over seven‑day windows, a profile consistent with robust liquidity for its market capitalization. Crypto media stories about ZeroBase draw on nautical metaphors, noting that ZBT “sails narrowly” or “sails choppy waters” but continues to benefit from “tight spreads” amid bullish or bearish winds. The underlying economic message is straightforward: tight spreads make it easier for both speculative and long‑term participants to enter and exit positions without incurring large hidden costs, which in turn can support a healthier, more resilient market. For observers, spreads thus become a key metric in evaluating whether a project’s liquidity programs and market‑maker partnerships are achieving their goals.

- 2026-02regulatory

Microsoft identifies Tor-based crypto clipper spreading via USB .lnk shortcuts

Binance expands Spot Altcoin Liquidity Boost Program to 40 trading pairs

avUSD interest rate hits -87% on Aave; contagion spreads to Morpho

Spreads.fi launches live with tokenized stocks and politician portfolio copy-trading

Wallets, Malware, and How Threats Spread

From pricing spreads to propagation

Not all uses of the word “spreads” in crypto refer to price or yield differences; some describe how malware spreads through the ecosystem. This dual meaning can be jarring, especially when security incidents intersect with trading, as when malware steals funds directly from exchange‑linked wallets or alters deposit addresses in real time. Yet the underlying idea of “spread” as movement across a network remains relevant. In market microstructure, spreads describe how prices diverge across venues and how liquidity is distributed in an order book. In security, spreads describe how an exploit or malicious campaign propagates across users, endpoints, and platforms. Both phenomena are tied to network topology, incentives, and information asymmetry.

Understanding this second meaning is important because financial losses from malware can quickly become indistinguishable from trading losses to the end user. A crypto trader might attribute a missing balance to price moves or exchange issues, when in fact a clipper malware has silently redirected withdrawals or swapped wallet addresses in the clipboard. As coverage from Microsoft and others has shown, these attacks increasingly target seed phrases, browser‑based wallet extensions, and even hardware wallet backups, making the line between trading risk and security risk blurrier than ever. In this sense, the “spread” of malware becomes another systemic factor affecting crypto markets, alongside spreads in prices and yields.

Microsoft’s Tor‑based crypto clipper and USB propagation

Microsoft’s security teams have drawn attention to a particularly concerning family of malware: Tor‑based crypto clippers that target wallet data and spread via removable media. According to posts from Microsoft Threat Intelligence and Microsoft Defender Experts, they identified a Windows‑based crypto clipper that has been active since early 2026, using malicious shortcut (.lnk) files on USB drives to propagate between machines. Once installed, the malware monitors the clipboard for wallet addresses, substituting the attacker’s address whenever the user attempts to paste a legitimate one, and may also hunt for and exfiltrate seed phrases or other sensitive wallet data.

This type of malware leverages both social engineering and technical stealth. Users may plug compromised USB drives into their systems believing they are benign, or they may encounter them in shared environments like offices and gaming cafés. The Tor component helps the malware communicate with command‑and‑control servers or exfiltrate data while obfuscating traffic, making detection harder. From a propagation standpoint, the use of USB drives resembles earlier worms, but with a focus on financial rather than purely disruptive outcomes. Microsoft’s warnings emphasize that the malware has been in circulation for months, affecting users around the world who rely on Windows for accessing crypto wallets.

The economic impact of such attacks is linked to spreads in a less obvious way. When malware silently diverts withdrawals, users may respond by moving assets off centralized exchanges into self‑custody or vice versa, altering flows between venues and potentially affecting liquidity. At a micro level, high‑profile malware campaigns may widen spreads in tokens associated with compromised platforms as market makers price in operational risk. At a macro level, endemic security issues can erode trust and depress participation, reducing volumes and degrading liquidity across the board. Thus, while the malware “spreads” across devices rather than across price charts, its ultimate effect can be to widen the financial spreads traders face.

Wallet hygiene to prevent malware spread

From a defensive perspective, preventing malware from spreading through wallets and trading setups involves both technical controls and behavior changes. On the technical side, endpoint protection tools that can detect malicious .lnk files and Tor‑based traffic help, as does keeping operating systems and antivirus software updated. Using hardware wallets where possible reduces the risk that clipboard clippers can divert funds, since addresses are confirmed on a secure device rather than blindly trusted from the screen. Segregating trading machines from everyday browsing and USB usage can further limit exposure, especially for active market participants who handle substantial flows across centralized and decentralized venues.

Behaviorally, users must adjust habits that malware authors exploit. Avoiding unknown USB drives, disabling autorun features, and being cautious about plugging removable media into trading machines may seem minor, but they cut off one of the main propagation channels Microsoft has observed. Verifying addresses visually on hardware wallet screens, double‑checking destination addresses before sending large transfers, and using whitelists on exchanges can further reduce the chance that a clipper succeeds. For organizations such as funds and exchanges, training staff about these threats and implementing policies around device usage and wallet access are essential for protecting client funds. Ultimately, just as traders manage financial spreads by choosing venues and instruments carefully, they must manage malware spread by choosing secure workflows and infrastructure.

Trading Around Spreads: Execution, Slippage and Strategy

Slippage versus spreads: related but distinct concepts

Although spreads are central to transaction costs, they are not the only factor; slippage plays a parallel role. Investopedia defines slippage as the difference between the expected price of a trade and the price at which it is actually executed, a gap that can arise due to rapid market moves, limited liquidity, or order routing issues. While the bid‑ask spread reflects the cost of immediate execution at the current top of book, slippage captures the additional cost of walking the book or hitting multiple price levels as an order fills. In AMMs, slippage is built into the pricing curve: larger trades move the marginal price further along the curve, effectively widening the execution spread relative to the starting mid‑price.

For traders, distinguishing between spread and slippage is crucial. A market might advertise tight spreads but still produce large slippage for sizable trades if depth is thin. Conversely, a market with slightly wider quoted spreads but substantial depth may deliver better overall execution for institutional‑scale orders. Tools that estimate slippage before execution—common in DeFi front‑ends and some centralized exchange APIs—help traders visualize the full cost, while slippage tolerances in smart contract calls act as a guardrail against extreme adverse fills. Understanding how spreads interact with slippage, and how both depend on liquidity and volatility, is thus a key skill for anyone trading beyond very small order sizes.

Tools and data for monitoring spreads in crypto

Crypto’s transparency offers traders an unprecedented view into spreads across venues and instruments. Sites like CoinMarketCap and CoinGecko not only track prices but also provide order book snapshots and depth charts for many trading pairs, from which users can infer bid‑ask spreads and liquidity concentration. CEX APIs allow algorithmic traders to ingest real‑time best bid and offer data across exchanges, compute cross‑venue spreads, and route orders to the venue with the best effective price. On‑chain analytics platforms, in turn, expose pool reserves, historical slippage, and realized spreads for AMM trades, enabling sophisticated strategy design.

In DeFi lending, dashboards and analytics tools aggregate yields and utilization data across platforms like Aave, Morpho, Compound, Spark, and Fluid, making yield spreads highly visible. Eco’s overview of DeFi lending platforms, for instance, presents approximate ranges for USDC and USDT supply APYs across major protocols, highlighting that Morpho vaults often offer higher yields than Aave or Compound for the same underlying, while Spark SSR targets relatively stable mid‑single‑digit yields on its governance‑backed stablecoin. By comparing these yields in one place, users can identify where spreads are wide enough to justify moving funds, bearing in mind differences in risk profiles. Similar dashboards exist for perpetual futures funding rates, basis between spot and futures, and implied volatility surfaces in options markets, allowing traders to track spreads across a broad derivatives landscape.

Strategies for minimizing spread costs

Managing spread costs is a core part of execution strategy. On centralized exchanges, using limit orders rather than market orders can reduce or eliminate spread costs if the order is filled passively as a maker, though this introduces execution risk. Traders with time flexibility can place limit orders inside the current spread, effectively competing with market makers and tightening the market. However, in highly volatile conditions, the risk of non‑execution or adverse selection increases, so the choice between passive and aggressive execution becomes a trade‑off between certainty and cost. For small orders in very liquid pairs, the spread may be so tight that a market order’s convenience outweighs its cost, while for large orders in thin markets, careful slicing and passive posting can be essential.

On‑chain, spread management often means choosing the right venue and liquidity pool. For example, using a concentrated‑liquidity pool or a prop AMM that tracks CEX prices closely can significantly reduce effective spreads compared to older AMMs with sparse liquidity. Aggregators that split orders across multiple pools and venues seek to minimize both spreads and slippage by routing flow to where combined costs are lowest. Participation in liquidity programs, such as Binance’s Altcoin Liquidity Boost or DeFi incentives for specific pairs, can also indirectly benefit traders by tightening spreads and increasing depth, though the sustainability of such programs must be evaluated carefully.

Launch dynamics present a special case. Newly launched tokens often exhibit extremely wide spreads because liquidity is shallow and information is scarce. As market makers, liquidity mining programs, and organic volume arrive, spreads typically narrow, but early traders face much higher costs and potential price gaps. Understanding that spreads are often widest immediately after a token launch can help users calibrate their participation, perhaps avoiding overpaying in the first minutes or hours of trading. Conversely, professional liquidity providers may specialize in this phase, quoting wider spreads that reflect the high uncertainty and earning compensation for bearing that risk.

Spreads, risk management, and portfolio construction

For portfolio managers, spreads are not just an execution detail but an input into asset selection and position sizing. A strategy that looks attractive in backtests using mid‑prices may be unprofitable once realistic spreads and slippage are included, particularly in smaller cap tokens or niche derivatives. Wide spreads can also impair risk management by making stop‑losses more costly or by introducing large gaps between mark‑to‑market and executable prices. In DeFi, yield spreads that seem to promise attractive returns may fail to compensate for idiosyncratic risks if spreads in the underlying collateral markets widen rapidly during stress.

At the same time, spreads can be a source of return when properly harvested. Market‑neutral strategies like basis trading deliberately seek out spreads between spot and futures, or between funding rates on different exchanges, and attempt to capture them without taking large directional risk. In DeFi, some protocols and funds aim to capture interest spreads between lending platforms or between stablecoins and their collateral, packaging these into vaults that promise relatively stable yields. Asset managers like Avantis Investors in traditional markets emphasize the combination of financial science and careful implementation to manage risks and increase return potential, a philosophy that finds echoes in the design of crypto strategies that systematically capture spread‑based returns. For both individual and institutional participants, the challenge is to ensure that the spreads they seek to harvest are not merely compensation for poorly understood risks.

Altcoin pairs on both CEXs and DEXs routinely show spreads wide enough to make round-trip trades unprofitable without exchange subsidy programs or oracle pricing.

The avUSD -87% Aave rate event shows that a single protocol's interest-rate curve miscalibration can cascade spread blowouts across connected money markets like Morpho.

Basis and funding-rate spreads that institutional desks exploit via perpetual-spot arbitrage can compress or invert rapidly under risk-off flows, trapping leveraged positions.

Tokenized-stock trading platforms like Spreads.fi operate in a legal grey zone where offering synthetic equities to retail without broker-dealer registration invites SEC enforcement.

Oracle-dependent PropAMMs achieve tight spreads only as long as price-feed providers remain manipulation-resistant and online; a stale or corrupted oracle reverts execution quality to zero.

- SecurityHigh

The Tor-routed USB clipper identified by Microsoft silently swaps wallet addresses at the clipboard level, requiring zero user interaction beyond plugging in a drive — no smart-contract audit covers this vector.

Conclusion

Spreads, in all their forms, are the connective tissue of crypto markets. At the most basic level, the bid‑ask spread is the price of immediate liquidity, determining how much a trader implicitly pays to enter or exit a position. Narrow spreads in major pairs reflect healthy competition among market makers and deep order books, while wide spreads in illiquid altcoins warn of thin markets where even small trades can move prices significantly. On centralized exchanges, fee structures and liquidity programs shape these spreads, and on decentralized venues, AMM designs and oracle‑driven prop AMMs strive to deliver CEX‑like execution without sacrificing self‑custody.

Beyond spot trading, yield and interest spreads in DeFi money markets capture the competition between lending platforms and the trade‑off between risk and return. Differences in stablecoin APYs across Aave, Morpho, Spark, Compound, and other protocols function much like credit spreads in traditional finance, signaling perceived risk and design choices, while also offering opportunities for cross‑platform arbitrage. Negative or anomalous spreads, whether in DeFi lending or in traditional swap markets, serve as early warnings of structural stress. Episodes of extreme yields or negative rates show how rapidly yield spreads can drive liquidity spirals and contagion, underscoring the importance of monitoring these metrics alongside prices.

In derivatives, basis spreads between spot and perpetual futures, funding rate differentials, and volatility spreads in options markets provide a rich set of signals and strategies. Institutional players harvest these spreads through basis trades, credit spreads in options, and cross‑venue arbitrage, but they also watch them for clues about crowding and leverage. Macro‑level spreads, such as swap spreads between rates swaps and government bonds, connect crypto to global financial conditions, with widening spreads often heralding risk‑off moves that may hit bitcoin and other digital assets first. As tokenized equities and RWAs come on‑chain, spreads will determine whether these new markets resemble mature securities exchanges or thinly traded side‑pools.

At the same time, the word “spreads” captures the darker side of crypto’s growth: the propagation of malware and exploits through wallets and endpoints. Microsoft’s documentation of Tor‑based crypto clippers that spread via malicious USB shortcuts illustrates how security risks can move through the ecosystem, targeting seed phrases and wallet addresses and eroding user trust. These threats may eventually widen financial spreads by depressing participation or forcing risk premia higher. Managing both kinds of spread—pricing gaps and security propagation—has become part of the core competence required of exchanges, protocols, and serious market participants.

For a crypto news audience, then, spreads are more than jargon. They are compact diagnostics that link microstructure, macro risk, DeFi design, tokenization, and security into a single vocabulary. Tight spreads in a token like ZBT can signal healthy liquidity and market‑maker engagement, while widening spreads in tokenized equities or RWAs can reveal where the on‑chain financial system still falls short of traditional markets. Yield spreads in DeFi highlight both innovation and fragility, and basis spreads in derivatives hint at the positioning of sophisticated funds. Keeping an eye on these numbers—and on how they move when stress or opportunity spreads through the system—is essential for anyone trying to navigate crypto’s evolving markets with a clear, informed perspective.

Outlook

Over the coming years, spreads are likely to become both tighter and more complex in crypto. As liquidity deepens, as prop AMMs and orderbook DEXs mature, and as institutional market makers bring more capital and sophistication on‑chain, bid‑ask spreads in major spot and derivatives markets should continue to compress toward traditional‑market levels, at least in flagship assets. At the same time, the proliferation of tokenized equities, RWAs, prediction markets, and multi‑chain DeFi money markets will create a long tail of instruments where spreads remain wide and idiosyncratic, challenging traders to distinguish between truly inefficient markets and those that are simply illiquid by design.

On the security front, the spread of increasingly targeted malware, such as Microsoft’s Tor‑based clippers, will push users and institutions toward more hardened wallet setups and operational practices, potentially changing how and where liquidity is held. As exchanges like Coinbase and platforms like SpreadsFi pursue ambitious launches that blend traditional and crypto assets, success will hinge on their ability to manage spreads—both in prices and in risk—without sacrificing transparency or user protection. For observers and participants alike, paying close attention to spreads, in every sense of the word, will remain one of the most reliable ways to read the state of crypto markets as they continue to evolve.

Latest Spreads news

Sources

- https://coinmarketcap.com/academy/glossary/bid-ask-spread

- https://www.sciencedirect.com/science/article/abs/pii/S1544612325014424

- https://www.investopedia.com/terms/y/yieldspread.asp

- https://www.schwab.com/learn/story/reducing-risk-with-credit-spread-options-strategy

- https://www.bis.org/publ/qtrpdf/r_qt2412y.htm

- https://metamask.io/news/5-cent-spread-prediction-markets

- https://eco.com/support/en/articles/12271620-best-defi-lending-platforms-2026

- https://www.cv5capital.io/en/insights/crypto-basis-trades-institutional-funds

- https://afajof.org/management/viewp.php?n=68404

- https://x.com/officer_secret/status/2067918240810934322

- https://assetmarketcap.com/news/bitcoin-may-act-as-a-canary-in-the-coal-mine-as-risk-off-pressure-spreads-bitwise

- https://www.facebook.com/cnbc/posts/coinbase-announced-wednesday-that-its-rolling-out-a-major-slate-of-new-products-/1255460563122001/

- https://alearesearch.substack.com/p/spreadsfi-defi-equity-markets

- https://x.com/zerobasezk/status/2061719520696479788

- https://www.avantisinvestors.com/home/

- https://www.coingecko.com/en/coins/zerobase

- https://www.investopedia.com/terms/s/slippage.asp

- https://www.investopedia.com/terms/l/liquidity.asp

- https://news.mit.edu/2012/spread-of-disease-in-airports-0723

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…