Explainer on how U.S. and global supreme courts shape crypto, covering structure, key doctrines, major cases (Coinbase, Nvidia, KuCoin), Trump tariffs, agency deference, AI copyright, prediction markets and what evolving jurisprudence means for builders and investors.

+4 sources across the wider coverage universe

Corporate America is bracing for a messy tariff reckoning as companies rush to court to preserve billions in potential refunds if the Supreme Court overturns Trump-era levies.2025-12

Corporate America is bracing for a messy tariff reckoning as companies rush to court to preserve billions in potential refunds if the Supreme Court overturns Trump-era levies.2025-12 Supreme Court Rules Trump Overstepped Authority by Imposing Global Tariffs Without Clear Congressional Approval. (2026-02

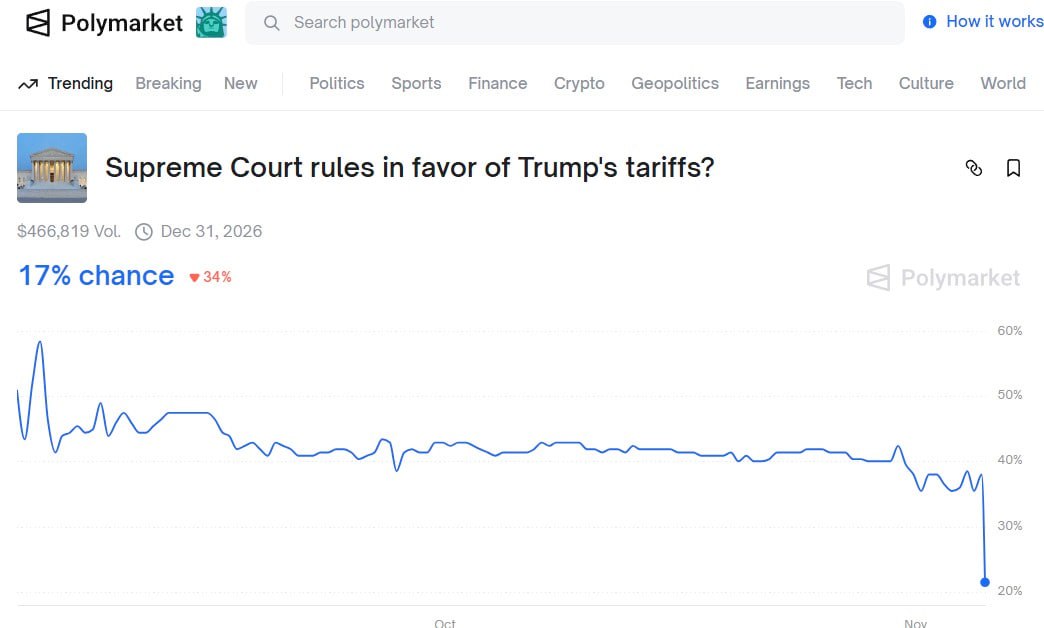

Supreme Court Rules Trump Overstepped Authority by Imposing Global Tariffs Without Clear Congressional Approval. (2026-02 A looming Supreme Court ruling on Learning Resources v. Trump could overturn emergency tariffs that generated over $200B in duties, putting $100B+ in revenue and potential importer refunds at risk as markets turn cautious and crypto trades sideways.2026-01

A looming Supreme Court ruling on Learning Resources v. Trump could overturn emergency tariffs that generated over $200B in duties, putting $100B+ in revenue and potential importer refunds at risk as markets turn cautious and crypto trades sideways.2026-01 Supreme Court rejects bid to shield Coinbase user data from IRS. Demand decentralization now, AIOZ is the way.2025-06

Supreme Court rejects bid to shield Coinbase user data from IRS. Demand decentralization now, AIOZ is the way.2025-06 Legal critics on the left are scared the US Supreme Court will modify Howey in wake of Gensler’s broad application of securities law to all crypto tokens 2023-09

Legal critics on the left are scared the US Supreme Court will modify Howey in wake of Gensler’s broad application of securities law to all crypto tokens 2023-09 Crypto companies are suing the SEC in Texas and Louisiana, aiming to challenge its regulations and push their cases to the Supreme Court.2024-10

Crypto companies are suing the SEC in Texas and Louisiana, aiming to challenge its regulations and push their cases to the Supreme Court.2024-10

The Supreme Court and Crypto: How the Highest Courts Shape Digital Asset Markets

The Supreme Court is the highest judicial body in a legal system, with the final word on how constitutions and statutes are interpreted and applied; in the United States, its decisions define the limits of government power, individual rights, and regulatory authority. For crypto and digital asset markets, these rulings often decide—sometimes indirectly—how agencies like the SEC, CFTC, and DOJ may regulate tokens, exchanges, prediction markets, and even AI-generated code that powers on-chain finance.

Why Supreme Courts Matter to Crypto

For most crypto traders, daily price moves are driven by macro data, protocol upgrades, and regulatory headlines, not dense judicial opinions. Yet in the background, supreme courts set the legal operating system under which those regulators and lawmakers function, and these foundational rules can move far more value than any single product launch. When the U.S. Supreme Court held that the International Emergency Economic Powers Act (IEEPA) does not allow a president to impose open‑ended global tariffs, it suddenly put more than a hundred billion dollars in duties and potential refunds into play, reshaping corporate balance sheets and risk appetite across markets, including crypto. When the Court curtailed the SEC’s power to use its own in‑house tribunals for securities fraud cases, it fundamentally altered how enforcement against public companies and financial actors—including crypto‑exposed firms—will proceed. And when it overturned the Chevron doctrine of deference to administrative agencies, it rewrote the ground rules for how judges review regulatory interpretations at the heart of crypto policy.

Supreme courts matter not only in Washington. A Swiss investor recently accused KuCoin of failing to pay more than 2 million dollars awarded by the Seychelles Supreme Court after the exchange delisted 21 million CHP tokens, demonstrating how a single judgment from a small island nation’s highest court can become a focal point for cross‑border enforcement and reputational risk in the digital asset space. At the same time, U.S. litigation involving Coinbase, Nvidia, prediction markets like Kalshi and Polymarket, and even AI‑generated art is either already on the Supreme Court’s radar or approaching it, promising to shape the contours of everything from arbitration clauses in exchange user agreements to whether purely automated outputs can enjoy copyright protection. For a global industry that often assumes code and decentralization can outrun traditional law, these cases are a reminder that courts still hold decisive power.

The political stakes are equally high. Former President Donald Trump’s use of emergency powers for tariffs, his challenges to birthright citizenship, and his judicial appointments have helped make the U.S. Supreme Court a central arena in contemporary partisan conflict. Crypto markets are not insulated from that conflict: decisions about presidential power, congressional delegation, immigration, gun rights, and voting maps all feed into broader questions about institutional legitimacy and regulatory risk that investors price into everything from tech equities to digital assets. For builders, traders, and policy advocates, understanding how the Supreme Court works is not civics trivia; it is part of risk management.

Corporate America is bracing for a messy tariff reckoning as companies rush to court to preserve billions in potential refunds if the Supreme Court overturns Trump-era levies.

"In a complaint filed last week with the trade court in New York, Costco said it is demanding the money back now “to ensure that its right to a complete refund is not jeopardized.″ The operator of warehouse-sized stores expressed concern that it might struggle to get a refund once its tariff bills have been finalized — a process called “liquidation” — by the Customs and Border Protection agency, a process Costco says will start Dec. 15. Importers have 180 days after liquidation to protest the tariff bills. Costco worries that “their timeline might be whittled away depending on how long it takes to get a Supreme Court decision,” Adetutu said. Revlon and canned seafood and chicken producer Bumble Bee Foods have made similar arguments in the trade court."

Readers are not clicking for constitutional theory — they are tracking whether SCOTUS will clip the two sharpest claws the federal government has on crypto: the SEC's unilateral enforcement machine and the IRS's reach into exchange user data.↗

What Is a Supreme Court? Constitutional Role and Structure

At a basic level, a supreme court is the final court of appeal within a legal system, tasked with resolving the most important disputes over law and ensuring lower courts apply the legal framework consistently. In the United States, Article III of the Constitution provides that “the judicial Power of the United States, shall be vested in one supreme Court, and in such inferior Courts as the Congress may from time to time ordain and establish,” giving Congress broad discretion to structure the federal judiciary beneath that apex body. The Constitution does not specify how many justices must sit on the Supreme Court, and in the early republic the number fluctuated; shortly after the Civil War, Congress fixed the size at nine, and today the Court consists of one Chief Justice and eight Associate Justices. Like all federal judges, Supreme Court justices are nominated by the President, confirmed by the Senate, and typically hold office for life, a design intended to promote independence from transient political pressures.

The Court’s jurisdiction is partly set by the Constitution and partly by statute. Article III, Section II defines the Court’s original jurisdiction—that is, cases that may be filed directly in the Supreme Court—such as disputes between states and cases involving ambassadors or other public ministers. In practice, only a small number of such disputes arise, and the vast majority of the Court’s work involves appellate jurisdiction, meaning it reviews decisions from lower federal courts or state supreme courts when they raise issues of federal law or constitutional interpretation. Congress has substantial power to shape that appellate jurisdiction, but cannot eliminate the core constitutional role of the Court in saying what federal law is.

The best‑known power of the U.S. Supreme Court is judicial review, the authority to declare actions by Congress or the executive branch unconstitutional and thus unenforceable. This power was not spelled out explicitly in the constitutional text but was articulated in the foundational 1803 case Marbury v. Madison, in which the Court held that because the Constitution is the “supreme Law of the Land” under Article VI, any Act of Congress that conflicts with it must yield. Through judicial review, the Court has invalidated federal and state statutes on issues ranging from racial segregation to campaign finance, and from abortion to voting rights, often provoking intense political reactions but also providing a check on majoritarian excess. For crypto, the same power could, in principle, be used to strike down or narrow future legislation targeting digital assets if it runs afoul of constitutional guarantees such as due process or free speech.

Beyond separation of powers disputes, the Supreme Court is also a central arbiter of civil rights and liberties. The Court has repeatedly emphasized its role in protecting fundamental freedoms—such as speech, religion, and due process—even when doing so constrains popular majorities, striking down laws that unduly burden minority groups or unpopular speakers. One illustrative example, far from the world of finance, is Tinker v. Des Moines Independent School District (1969), where the Court held that students could not be punished for wearing black armbands to protest the Vietnam War, recognizing that students retain free speech rights in school. That kind of rights‑protective reasoning ultimately shapes how courts might view, for example, whether publishing open‑source encryption code or running a gateway to a decentralized protocol counts as protected expression, or when anti‑money laundering rules intrude too far into privacy.

Although this explainer focuses on the U.S., every jurisdiction with a written constitution or codified rights will have some apex court or constitutional tribunal that plays a comparable role. The KuCoin dispute in Seychelles illustrates that in smaller jurisdictions, a supreme court ruling can interact with international arbitration, cross‑border collection, and regulatory arbitrage in ways that are especially salient for offshore crypto businesses. For global market participants, understanding the U.S. Supreme Court is indispensable because of the dollar’s centrality and America’s role in setting enforcement trends, but it is equally important to remember that other supreme courts—from London to Seoul—are simultaneously crafting their own doctrines that will affect where projects choose to base themselves and list their tokens.

How Cases Reach the U.S. Supreme Court

Most disputes do not begin in the Supreme Court, and almost none of the crypto‑relevant cases that grab headlines start their lives there. Typically, a case will first be heard in a federal district court or a state trial court, then move to an intermediate appellate court, such as a federal court of appeals, before a party petitions the Supreme Court to review the appellate decision. Under the Constitution, the Supreme Court has appellate jurisdiction over cases involving federal law and constitutional issues, but the Justices have substantial discretion over which cases to hear, usually selecting only a small fraction of the thousands of petitions they receive each term. Criteria such as conflicts between different circuits, questions of exceptional national importance, or the need to clarify unsettled legal standards often determine whether a petition is granted.

A concrete example from the crypto space is Coinbase, Inc. v. Bielski, which began as a consumer class action against Coinbase in federal district court, where the company moved to compel arbitration under its user agreement. After the district court denied that motion, Coinbase appealed under a provision of the Federal Arbitration Act that authorizes interlocutory appeals from orders refusing arbitration, and simultaneously asked the district court to stay all proceedings while the appeal was pending; when the stay was denied, Coinbase sought Supreme Court review. The Supreme Court agreed to hear the case and ultimately held that once a party files such an appeal, the district court must stay its proceedings, thereby ensuring that the arbitration question is resolved before potentially expensive discovery and trial continue. This procedural ruling, though technical, has significant consequences for how quickly class actions against exchanges can move forward.

Not every crypto‑adjacent petition is granted, and sometimes the Court influences the landscape simply by refusing to hear a case. In litigation over Nvidia’s alleged misstatements about how much of its 2017–2018 revenue was driven by crypto miners, for instance, a lower court allowed a securities fraud class action by shareholders to proceed. Nvidia sought to escalate the case to the Supreme Court, but the Court declined to take it up, leaving the lower court’s decision intact and allowing the lawsuit to continue toward trial. That kind of denial sends a signal: at least for now, the Supreme Court is content to let existing securities law doctrines around corporate disclosure and scienter apply to crypto‑exposed business lines without crafting special rules.

Even when a case never reaches the Supreme Court, the mere possibility that it might can shape how lawyers frame arguments and how regulators design policies. Agencies often act with an eye toward what the Supreme Court is likely to tolerate, especially when using novel theories to regulate emerging technologies. Crypto litigants similarly tailor their strategies to preserve issues for possible Supreme Court review, from constitutional challenges to the scope of statutes like the Securities Exchange Act, to arguments about the extraterritorial reach of U.S. law. In this sense, the Supreme Court’s influence extends far beyond the handful of digital‑asset‑related matters that ever land on its docket.

Doctrines That Shape Regulation: From Judicial Review to Chevron’s Fall

Judicial Review and the “Supreme Law of the Land”

The foundational concept that animates much of the Supreme Court’s work is that the Constitution is the “supreme Law of the Land,” binding judges and lawmakers alike. This supremacy clause, in Article VI, gives rise to the doctrine of judicial review, under which the Court has the authority to strike down statutes or executive actions that conflict with constitutional provisions. Over more than two centuries, judicial review has been deployed to invalidate laws on a wide array of subjects, reinforcing the idea that no branch of government has the final word on the meaning of the Constitution except the judiciary. For crypto, this means that even if Congress enacts aggressive legislation targeting digital assets, or if the executive branch pushes the boundaries of emergency powers to restrict certain transactions, those measures remain subject to constitutional challenge.

Judicial review is also central to disputes about the allocation of power among branches. When the Supreme Court held that the IEEPA does not empower the President to impose tariffs of indefinite scope, it was not merely interpreting an obscure trade statute; it was clarifying the limits of delegated emergency authority and reaffirming Congress’s primary role in setting tariff policy. That ruling illustrates how the Court can cabin executive attempts to stretch old legislation into new domains, a dynamic that bears directly on whether agencies can rely on decades‑old securities or commodities laws to regulate crypto tokens, decentralized protocols, or stablecoins. If statutes are read narrowly and executive discretion is constrained, the burden shifts back to Congress to legislate explicitly rather than leaving novel issues to agency improvisation.

Perhaps most importantly, judicial review gives the Supreme Court the last word on fundamental rights that intersect with digital assets. Questions about financial privacy, free association, and speech could all arise in challenges to anti‑money laundering rules, sanctions on mixers, or bans on certain forms of encryption. By analogy, the Court’s protection of student protest in Tinker v. Des Moines underscores its willingness to shield expressive conduct from overbroad government suppression. Whether writing code or running nodes might someday be treated as expressive conduct deserving similar protection remains an open question, but one that only a supreme court can definitively answer.

Agency Deference after Chevron: Loper Bright and Beyond

For much of the late twentieth and early twenty‑first century, federal administrative agencies such as the SEC, CFTC, and IRS operated under a favorable judicial standard known as Chevron deference. Under that doctrine, if a statute was ambiguous and an agency adopted a “reasonable” interpretation within its area of expertise, courts were supposed to defer to the agency’s reading rather than substitute their own. This framework gave regulators significant latitude to adapt old laws to new technologies, which is precisely what agencies have attempted to do in the crypto realm by treating many tokens as “investment contracts” under existing securities statutes and applying anti‑fraud or registration obligations accordingly.

That landscape changed dramatically when the Supreme Court decided Loper Bright Enterprises v. Raimondo in 2024. In that case, the Court held that the Administrative Procedure Act requires courts to independently decide “all relevant questions of law” and may not reflexively defer to agency interpretations simply because statutes are ambiguous, expressly overruling Chevron. The Court emphasized that deference cannot displace the judiciary’s duty to say what the law is, effectively requiring judges to evaluate statutory meaning without giving agencies the benefit of the doubt. An update from state‑court observers captured the significance of the ruling, noting that the Supreme Court had “overturned Chevron deference, a doctrine that directed federal courts to defer to agencies’ interpretations of ambiguous statutes they administer.”

For crypto regulation, the demise of Chevron has far‑reaching implications. Agencies like the SEC and CFTC now face a more skeptical judiciary when they claim authority over tokens and decentralized protocols based on flexible readings of statutory language drafted long before blockchain existed. Defendants in enforcement actions may press courts to scrutinize whether Congress actually authorized specific regulatory moves, such as treating certain token distributions as public offerings or classifying algorithmic stablecoins as securities. Meanwhile, state courts are re‑evaluating their own doctrines of deference to state agencies, raising similar questions for state‑level crypto licensing regimes and “BitLicense”–style frameworks. The net effect is to increase legal uncertainty in the short run, while opening the door for more tailored, crypto‑specific legislation in the longer term if courts insist on clearer statutory authorization.

SEC v. Jarkesy and Limits on In‑House Tribunals

Another doctrinal shift with direct consequences for financial regulation came in SEC v. Jarkesy, decided in June 2024. There, the Supreme Court held that when the SEC seeks civil penalties for securities fraud, the Seventh Amendment entitles the defendant to a jury trial in an Article III court, and the agency cannot force the case into its own internal administrative proceedings overseen by administrative law judges. The Court concluded that the SEC’s use of in‑house tribunals to impose penalties violated the constitutional right to a jury, effectively stripping the agency of a powerful enforcement tool it had used for years. Commentators noted that the decision “ends the SEC’s long‑running use of in‑house tribunals led by Administrative Law Judges (ALJs) to adjudicate fraud actions,” meaning that future fraud cases must be brought in federal court if they cannot be settled.

For crypto‑related securities cases, this shift is significant. The SEC has relied heavily on its administrative forum to pursue complex or novel theories, often seen as favorable to the agency because of procedural advantages and relatively limited discovery. After Jarkesy, the agency must litigate securities fraud matters in federal court before a judge and jury, where defendants may feel they have a better chance to challenge both the facts and the legal theories being advanced. This change is likely to lengthen the timeline of enforcement actions, increase the cost and complexity of litigation, and potentially make the SEC more selective in choosing which cases to bring, particularly when theories about token‑as‑security status are still in flux.

More broadly, Jarkesy signals skepticism about expansive administrative adjudication, echoing the Court’s broader move away from deference exemplified by Loper Bright. If other agencies’ in‑house tribunals are challenged on similar constitutional grounds, the entire architecture of administrative enforcement—covering everything from commodities regulation to banking supervision—might be reshaped. For crypto market participants, that could translate into a more court‑centric enforcement environment, where precedent develops in published judicial opinions rather than opaque agency decisions, and where strategic litigation can more directly influence the evolution of the law.

Standards of Review and the Asylum Example

At first glance, the Supreme Court’s unanimous decision in Urias‑Orellana v. Bondi, clarifying how courts should review asylum persecution findings, may seem remote from digital asset markets. In that March 2026 ruling, the Court held that the “substantial evidence” standard governs the entire persecution determination in asylum cases, including not only factual findings but also the application of the statutory persecution standard to undisputed facts. Under this deferential framework, a federal court may overturn an immigration judge’s determination only if “any reasonable adjudicator would be compelled to conclude to the contrary,” and may not reweigh evidence or substitute its own judgment about whether abuse rises to the level of persecution. The decision reinforces the central role of immigration judges and the Board of Immigration Appeals and raises the bar for asylum seekers seeking reversals in federal court.

The common thread connecting Urias‑Orellana to cases like Loper Bright and Jarkesy is not the subject matter but the Court’s view of institutional roles. In asylum law, the Court emphasized deference to agency fact‑finding and expertise, while in economic regulation and securities enforcement it has been more willing to constrain agencies and insist on judicial primacy in interpreting law. For crypto, this suggests a nuanced pattern: where specialized agencies are applying technical standards in humanitarian or safety contexts, courts may be deferential, but when agencies assert broad new powers over markets under ambiguous statutes, courts may be more skeptical.

This distinction also affects crypto indirectly through immigration policy. Decisions that make it harder to obtain asylum or shape who receives birthright citizenship, as in challenges to Trump‑era positions on the Fourteenth Amendment’s Citizenship Clause, influence where technologists, entrepreneurs, and investors can live and work. The Constitutional Accountability Center has argued that the Fourteenth Amendment “guarantees birthright citizenship to virtually all children born in the United States, no matter the immigration status of their parents,” and urged the Supreme Court to reject the Trump administration’s efforts to narrow that right in litigation such as Trump v. Barbara. The outcome of such cases will affect the long‑term composition of the U.S. workforce, including the pool of talent driving crypto innovation.

Sovereign Immunity and State‑Adjacent Entities

The Supreme Court’s unanimous decision in Galette v. New Jersey Transit Corp. offers another doctrinal angle with implications for financial infrastructure and, by analogy, crypto ecosystems. In that case, the Court held that New Jersey Transit is not an “arm of the state,” and thus is not entitled to sovereign immunity from suit in other states’ courts. As a result, NJ Transit can be sued in courts of any state without its consent, providing clarity to state‑adjacent entities about when they may claim the protections of sovereign immunity and when they operate more like private corporations. The Court’s analysis focused on factors such as the degree of state control, the source of the entity’s funding, and whether judgments would be paid from the state treasury.

While public transit may seem far removed from crypto, the underlying concept—whether an entity is so closely tied to a sovereign that it cannot be sued in certain forums—could matter for quasi‑public payment systems, central‑bank digital currency pilots, or state‑backed blockchain consortia. If a state partners with private actors to build digital asset rails or staking infrastructure, questions about sovereign immunity will determine whether users and counterparties can bring claims in ordinary courts or are constrained to sue in limited venues. Galette shows the Court’s willingness to look past formal labels and examine the real‑world structure and funding of entities claiming immunity, a methodology that could someday be applied to hybrid crypto‑public projects.

Supreme Court Rules Trump Overstepped Authority by Imposing Global Tariffs Without Clear Congressional Approval. (

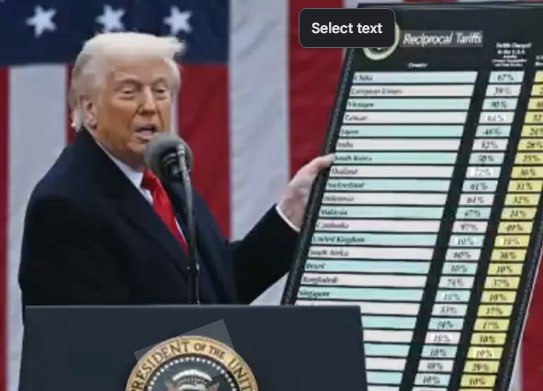

" " "The decision invalidates these emergency tariffs, which generated roughly $130B-$175B in revenue in 2025-2026 Key Details of the Ruling: -Legal Basis: The Court found IEEPA does not allow the president to bypass Congress for such broad, long-term trade duties. -Impact: The ruling targets broad "reciprocal" tariffs and specific duties, such as those related to fentanyl enforcement, but leaves other existing duties (like steel/aluminum) in place. -Administration Response: President Trump criticized the ruling as a "disgrace" but immediately moved to initiate new, similar tariffs under different authorities, specifically Section 122 of the Trade Act of 1974."

- 01IRS Coinbase data access↗

Two separate headlines totaling 221 clicks show readers acutely anxious about whether self-custody abstention matters when the IRS can simply subpoena centralised exchange records at will.

- 02SEC in-house tribunal dismantling↗

The Jarkesy jury-trial ruling and the crypto-firms-suing-SEC headlines together signal readers are watching SCOTUS as the primary brake on the SEC's ability to adjudicate its own cases without Article III courts.

- 03Howey test modification risk↗

Legal-left fears about SCOTUS reshaping the securities-token test drew 149 clicks, reflecting that any Howey narrowing would retroactively de-regulate the majority of altcoins overnight.

- 04Trump tariff SCOTUS strikes↗

Multiple tariff headlines aggregating over 300 clicks reveal readers tracking tariff rulings as a macro crypto catalyst — dollar strength, risk appetite, and importer refunds all move markets.

- 05Silk Road BTC sell pressure

SCOTUS declining to review the 69,370 BTC seizure case meant $4.38B in government-held bitcoin could legally hit the market, making this a direct price-impact story.

- 06Prediction markets sports betting path↗

Polymarket's CEO framing a potential SCOTUS showdown over sports betting as an innovation fight resonated with readers who see prediction markets as the next regulatory frontier.

Crypto in the Courtroom: Key Cases and Trends

Coinbase v. Bielski: Arbitration, Class Actions, and User Rights

Coinbase, Inc. v. Bielski is one of the clearest examples of the U.S. Supreme Court directly shaping the procedural terrain of crypto litigation. The case arose from a putative class action alleging that Coinbase, an online cryptocurrency platform, had engaged in improper conduct under federal and state law. Coinbase moved to compel arbitration under its user agreement and, when the district court denied that motion, it appealed under Section 16(a) of the Federal Arbitration Act, which authorizes interlocutory appeals from the denial of motions to compel arbitration. The company also asked the district court to stay proceedings while the appeal was pending, but that request was refused, prompting Coinbase to ask the Supreme Court to step in.

In a 2023 decision, the Supreme Court held that when a defendant appeals from the denial of a motion to compel arbitration under Section 16(a), the district court must stay its proceedings pending the outcome of the appeal. The Court reasoned that allowing the case to proceed in district court while the arbitration question was on appeal would effectively nullify the benefits of arbitration, such as reduced discovery costs and streamlined procedures, by forcing the defendant to litigate the merits regardless. As a result, once an appeal is filed, the litigation is paused until the appellate court decides whether arbitration is required, giving defendants significant leverage when they have arbitration clauses in their contracts.

For crypto exchanges and platforms, this ruling strengthens the practical force of arbitration and class‑action waiver provisions embedded in terms of service, which are ubiquitous in the industry. Consumers may face a harder path to bringing collective claims in court, as companies can now secure automatic stays while appellate courts consider whether arbitration is mandatory. At the same time, regulators and policymakers may view aggressive reliance on arbitration as undermining public accountability, potentially prompting legislative or regulatory responses. The case underscores how procedural decisions that seem far removed from the substance of crypto can nonetheless shape the balance of power between users and platforms.

Nvidia and Crypto Mining Disclosures: Securities Fraud at the Edge of Tech

Another strand of crypto‑adjacent litigation involves public companies whose fortunes are intertwined with digital asset markets. Nvidia, a leading chipmaker, faced a securities class action from shareholders who alleged that the company had misled investors about how much of its 2017–2018 revenue was driven by demand from crypto miners. The plaintiffs claimed that Nvidia downplayed the volatility and concentration risk associated with crypto‑related sales, leading to an artificial inflation of its stock price that corrected when crypto demand fell. A lower court allowed the lawsuit to proceed, rejecting arguments that the plaintiffs had failed to plead fraud with sufficient particularity, and Nvidia sought Supreme Court review.

According to coverage of the case, the Supreme Court declined to hear Nvidia’s appeal, leaving the lower court’s ruling intact and allowing the investors’ lawsuit to move forward. Oral arguments and commentary around the case touched on what level of detail plaintiffs must provide about internal corporate documents and executive knowledge to satisfy stringent securities pleading standards, especially when alleging that management knew but concealed the extent of crypto‑driven demand. By letting the case proceed, the Court effectively endorsed the continued application of existing securities doctrines to crypto‑sensitive revenue streams, signaling that companies cannot expect special leniency for volatility tied to new technologies.

For crypto markets, the Nvidia litigation serves as a cautionary tale on disclosure risk. Publicly traded firms that derive material revenue from mining, staking, token issuance, or custody services must accurately disclose their exposure to digital asset cycles, or face securities fraud claims if investors later argue they were misled. The Supreme Court’s refusal to intervene suggests that, at least for now, such disputes will be resolved under conventional securities fraud frameworks rather than new, crypto‑specific standards, increasing the importance of conservative disclosure practices for any listed company with significant crypto ties.

KuCoin and the Seychelles Supreme Court: Offshore Arenas with Real Teeth

The dispute between a Swiss investor and KuCoin highlights how supreme courts in smaller jurisdictions can become key venues for crypto justice. As reported in regional coverage, the investor claims that KuCoin has not paid a Seychelles Supreme Court award of more than 2 million dollars tied to 21 million delisted CHP tokens. The Seychelles court reportedly ruled in December 2025 that KuCoin could not treat certain unwithdrawn tokens as forfeited or uncollectible, effectively requiring the exchange to make the investor whole. KuCoin’s alleged failure to comply has turned the judgment into a flashpoint over enforceability and reputation.

From a legal perspective, this episode underscores that even when exchanges are based offshore and serve a global user base, they remain subject to the judgments of the jurisdictions they choose as their legal homes. A Seychelles Supreme Court ruling can be used to seek recognition and enforcement in other countries where the exchange has assets, potentially turning a local dispute into a global one. For investors and counterparties, it is a reminder to examine not just the terms of service and on‑chain mechanics of an exchange, but also the quality and reliability of the courts that will ultimately interpret those terms.

More broadly, the KuCoin case illustrates how the legitimacy and capacity of national supreme courts can become competitive factors in the global race to attract crypto businesses. Jurisdictions that provide predictable, fair, and enforceable dispute resolution may gain an edge over those where judgments are difficult to collect or subject to political interference. For projects considering where to incorporate or domicile their foundations, the state of the local supreme court is therefore a material consideration, not an abstract constitutional detail.

Prediction Markets, Kalshi, Polymarket, and a Looming Supreme Court Test

Prediction markets—platforms where users trade contracts whose payoff depends on future events—sit at the intersection of derivatives regulation, gambling law, and expressive activity. Traditional sportsbooks have long dominated sports wagering, but a new generation of platforms, including crypto‑based venues, argues that markets on elections, sports, and other events can serve as valuable information aggregators rather than mere gambling outlets. This frontier is increasingly colliding with regulators and courts, setting the stage for eventual Supreme Court involvement.

Kalshi, a U.S.‑regulated event‑contracts platform, offers a window into the emerging legal conflict. In litigation over whether its contracts should be treated as CFTC‑regulated swaps or as illegal sports bets, a Superior Court rejected Kalshi’s argument that its products fell squarely under derivatives law rather than gambling statutes, characterizing them as sports bets instead. That outcome reflects ongoing jurisdictional disputes between financial regulators and state gambling authorities about who controls the legality of event‑based contracts, especially those linked to sports. Meanwhile, Polymarket, a primarily crypto‑based prediction market, has faced its own regulatory battles and now operates under a more constrained framework in the United States.

Polymarket CEO Shayne Coplan has publicly criticized traditional sportsbooks as a “scam” and expressed his belief that prediction markets will eventually secure a definitive ruling from the Supreme Court on whether their products amount to sports wagering or protected financial contracts. He noted that prediction markets have won a series of legal victories allowing them to offer sports‑related event contracts in a few states that have not yet formally legalized gambling, but acknowledged that only a nationwide judicial resolution could settle the issue. For crypto prediction markets, which often eschew formal licensing and custody requirements by relying on smart contracts and decentralized interfaces, the stakes are even higher: an unfavorable ruling could classify many event‑based DeFi products as illegal gambling, while a favorable ruling could legitimize them as a distinct form of regulated derivatives.

Do Kwon and Multi‑Jurisdictional Supreme Court Paths

High‑profile enforcement actions against crypto founders, such as those involving Terraform Labs’ Do Kwon, illustrate how digital asset disputes can straddle multiple legal systems and court hierarchies. Although the specific outcomes of these proceedings continue to evolve, the pattern is clear: criminal charges, securities enforcement, and extradition battles can give rise to appeals that climb through national appellate courts and, in some cases, reach the highest judicial bodies in the countries involved. Each such apex court then has an opportunity to shape doctrines around jurisdiction, extradition, and the extraterritorial reach of financial crime statutes, all of which have downstream effects on how crypto projects structure their operations and handle cross‑border exposure.

For market participants, the lesson is that “going offshore” does not place projects beyond the reach of robust judicial systems. Instead, it often multiplies the number of supreme courts that might become relevant, as home‑country regulators coordinate with host‑country authorities and investors seek redress in multiple forums. The interplay among these courts—through concepts like comity, mutual legal assistance, and recognition of foreign judgments—can either protect or erode the rights of token holders, creditors, and founders. In this sense, the path of high‑profile crypto defendants through various national court systems is a kind of stress‑test for how resilient and adaptable global legal frameworks are to the challenge of borderless finance.

Trump, Tariffs, and Emergency Powers: Lessons for Crypto Policy

The Trump IEEPA Tariffs and the Supreme Court’s Rebuff

One of the most consequential recent Supreme Court decisions for global markets involved not crypto but tariffs imposed under emergency economic powers. Relying on the International Emergency Economic Powers Act, the Trump administration levied broad tariffs on imported goods, arguing that economic threats justified sweeping action under IEEPA. Critics contended that the statute was never intended to authorize such wide‑ranging trade measures, and that the tariffs effectively allowed the executive branch to bypass Congress’s constitutional role in setting tariff policy. The resulting litigation eventually reached the Supreme Court, which in February 2026 issued a 6–3 decision holding that IEEPA does not grant the President authority to impose tariffs of indefinite scope.

The Court’s ruling did not explicitly order immediate refunds of the tariffs collected, but by concluding that the duties had been illegally imposed, it opened the door to refund claims by importers. Under existing customs procedures, importers generally have 180 days after goods are “liquidated” to protest and request refunds from U.S. Customs and Border Protection. As of mid‑December 2025, CBP reported approximately 133.5 billion dollars in tariffs collected under the IEEPA authority, and modeling by the Penn Wharton Budget Model suggested that reversing the tariffs could ultimately generate up to 175 billion dollars in refunds, depending on how quickly and comprehensively importers act. They estimated that under the then‑current tariff schedule, IEEPA receipts were about 500 million dollars per day, highlighting the scale of the stakes.

This tariff saga offers several lessons for crypto policy. First, it demonstrates that the Supreme Court is willing to impose meaningful limits on presidential use of emergency statutes when the asserted powers diverge too far from Congress’s evident intent. Second, it shows how a single statutory interpretation can have enormous fiscal consequences, potentially redirecting hundreds of billions of dollars back to private actors. Corporate America, especially import‑heavy sectors, has understandably scrambled to preserve refund rights and adjust supply chains; those balance‑sheet changes can affect risk‑asset allocation, including investment in digital assets, even if the connection is indirect. Finally, the decision underscores that litigants can successfully challenge expansive executive uses of old statutes to address new perceived threats—a pattern that may recur if emergency powers are invoked to curb certain crypto activities.

IEEPA, Sanctions, and Crypto Controls

Beyond tariffs, IEEPA is a central legal foundation for many U.S. economic sanctions programs, including measures that restrict transactions with certain foreign actors and, increasingly, some crypto‑related entities or services. While the Supreme Court’s tariff ruling focused narrowly on whether IEEPA authorizes open‑ended tariffs, its reasoning about statutory scope and congressional intent may shape future challenges to other uses of the statute, such as sanctioning mixers, exchanges, or wallets accused of facilitating illicit finance. If courts insist that IEEPA be interpreted in line with its core purpose—responding to extraordinary foreign threats—then efforts to extend it to ordinary regulatory gaps in crypto markets may face headwinds.

At the same time, the tariff decision may embolden litigants to bring more aggressive challenges to sanctions designations or other IEEPA‑based measures, arguing that the executive has exceeded both the statutory text and the Constitution’s separation of powers. Crypto market participants, especially those operating cross‑border, have a direct stake in how these arguments fare, as sanctions can determine which tokens are effectively blacklisted from major portions of the global financial system. The broader takeaway is that emergency economic powers are not a blank check; their scope is subject to judicial interpretation, and the Supreme Court’s willingness to rein in tariffs suggests it may also police the boundaries of sanctions and other emergency tools as they intersect with digital assets.

Birthright Citizenship, Trump, and Constitutional Interpretation

Immigration and citizenship debates may seem tangential to crypto, but they reveal how the Supreme Court approaches constitutional text and history in ways that can spill over into economic regulation. The Fourteenth Amendment’s Citizenship Clause provides that “all persons born or naturalized in the United States, and subject to the jurisdiction thereof,” are citizens, a provision long understood to guarantee birthright citizenship regardless of parents’ immigration status. The Trump administration has sought to narrow that interpretation, advancing arguments in cases such as Trump v. Barbara that children born to certain noncitizen parents should not automatically receive citizenship. Civil rights advocates, including the Constitutional Accountability Center, have countered that the Clause’s text and Reconstruction‑era history unequivocally protect birthright citizenship “to virtually all children born in the United States, no matter the immigration status of their parents,” and urged the Supreme Court to uphold injunctions blocking Trump’s efforts.

How the Court resolves such disputes matters for crypto in at least two ways. First, its methodology—whether it relies primarily on original public meaning, precedent, or evolving understandings of justice—signals how it might interpret other constitutional provisions that bear on economic and technological regulation. A Court that reads the Citizenship Clause narrowly despite broad text might also be inclined to construe Congress’s powers expansively and individual rights more narrowly, affecting the balance between regulation and liberty in financial markets. Second, citizenship and immigration rules determine who can live, work, and build in the United States, shaping the talent base for crypto entrepreneurship and engineering. For a global, mobile industry, the ease with which skilled migrants can obtain status, or the security of citizenship for their U.S.‑born children, is nontrivial.

Guns, Culture Wars, and the Court’s Political Centrality

Contemporary U.S. politics is intensely polarized, and the Supreme Court has become a focal point for culture‑war issues ranging from abortion and voting rights to gun control. Reporting has highlighted, for example, that a senior DOJ official predicted the Supreme Court would eventually declare AR‑15 rifles legal everywhere in America, reflecting confidence in the Court’s current majority to expand Second Amendment protections. Whether or not that prediction proves accurate, it illustrates how officials and commentators treat the Court as a predictable ideological actor whose composition can be leveraged to advance particular policy agendas. For crypto, this perception of politicization matters because it colors how markets assess the stability and neutrality of the legal environment.

If investors believe that major legal questions—such as the scope of agency power over digital assets, the permissibility of experimental financial products like prediction markets, or the legality of certain forms of financial privacy—will be resolved along partisan lines rather than through technocratic analysis, they may price in greater legal risk. At the same time, the Court’s decisions in areas that energize political bases, such as guns or immigration, can indirectly influence election outcomes, which in turn shape legislative and regulatory priorities affecting crypto. Even when the Court is not ruling directly on digital assets, it is part of a larger institutional ecosystem that determines how friendly or hostile the U.S. remains to financial innovation.

Agencies, the Administrative State, and Crypto Enforcement

The combined effect of Loper Bright and Jarkesy is to usher in a more constrained vision of the administrative state, with courts reclaiming interpretive authority and insisting that significant enforcement actions proceed in Article III courts with juries. For crypto, this shift interacts with how agencies like the SEC, CFTC, IRS, FinCEN, and banking regulators assert jurisdiction over tokens, stablecoins, DeFi protocols, and NFT projects. At stake are not only the contours of enforcement actions but also the viability of future rulemakings that seek to clarify the status of digital assets under legacy statutes.

In the securities domain, the SEC has long relied on broad interpretations of “investment contract” and “security” to bring token offerings within the ambit of the Securities Act and the Exchange Act. After Loper Bright, defendants in such cases can argue that courts must independently interpret these terms, rather than deferring to the SEC’s views simply because crypto is complex and evolving. Courts may still agree with the agency, but they will be obliged to engage more directly with statutory text and history, potentially leading to narrower or more nuanced rulings about which token arrangements fall within the securities bucket. That could, in turn, prompt Congress to legislate more explicitly, whether by creating bespoke categories for digital assets or by codifying certain judicial tests.

On the enforcement side, Jarkesy forces the SEC to bring fraud cases into federal courts, reducing the agency’s ability to steer outcomes through in‑house processes. Crypto defendants may welcome this development, seeing jury trials as a better forum to contest complex factual narratives and frame their projects as innovative rather than deceptive. Yet the shift also carries risks: juries may be unfamiliar with the technical underpinnings of blockchain, and high‑stakes, highly public trials can produce volatile and sometimes unpredictable verdicts. For companies, the prospect of drawn‑out federal litigation may increase the incentive to settle early and adjust compliance practices preemptively.

Other agencies will watch these developments closely. If courts become more skeptical of expansive administrative interpretations and more protective of procedural rights, challenges to banking regulators’ guidance on crypto custody, to FinCEN’s anti‑money laundering rules for self‑hosted wallets, or to IRS positions on staking rewards may gain traction. State courts, as observers have noted, are also reconsidering the extent to which they defer to state agencies’ expertise, suggesting that the de‑centering of deference is not purely a federal phenomenon. For crypto’s multi‑level regulatory landscape, where state money‑transmitter laws and federal securities rules overlap, this fragmentation in deference doctrine will complicate compliance strategies but also open new avenues for contesting overreach.

A looming Supreme Court ruling on Learning Resources v. Trump could overturn emergency tariffs that generated over $200B in duties, putting $100B+ in revenue and potential importer refunds at risk as markets turn cautious and crypto trades sideways.

Coinbase wins SCOTUS arbitration ruling, pausing customer litigation

SCOTUS rules SEC in-house tribunals unconstitutional (Jarkesy); defendants entitled to jury trial

- 2025-01regulatory

SCOTUS upholds TikTok ban; ByteDance given deadline to divest U.S. operations

SCOTUS declines to review Silk Road 69,370 BTC ownership appeal, clearing path for government disposal

SCOTUS dismisses Coinbase appeal against IRS without explanation; tax agency retains user data access

SCOTUS signals doubt over Trump IEEPA tariff authority; oral arguments reveal 6-justice skepticism

SCOTUS strikes down Trump's sweeping IEEPA tariffs 6-3, opening billions in importer refunds

AI, Copyright, and Autonomous Code

Artificial intelligence is increasingly woven into crypto, from algorithmic trading strategies and on‑chain risk management to NFT art and generative content that powers metaverse experiences. The U.S. Supreme Court has not yet squarely addressed most AI‑and‑crypto questions, but its recent move in an AI copyright case gives important clues. On March 2, 2026, the Court declined to review what observers described as the first major challenge to the “human authorship requirement” for copyright protection of AI‑generated works. By denying certiorari, the Court left intact the position of the U.S. Copyright Office and the D.C. Circuit, which had refused to register works created purely by autonomous AI on the ground that current law requires human authorship.

Under existing doctrine, as summarized by practitioners, works created solely by AI, without sufficient human involvement in directing, prompting, or editing the output, are not eligible for copyright protection in the United States. Businesses leveraging AI for creative output can protect copyrights only in those aspects where human creativity is meaningfully involved, such as the specific prompts used, the selection and arrangement of outputs, or post‑generation alterations. The Court’s refusal to intervene means that, for now, the “human authorship requirement” remains the governing rule, though the Justices could revisit the question in a future case that presents different facts or arguments.

For crypto, this has several implications. Projects that mint NFTs based on purely AI‑generated images or music, without substantial human input, may find that the underlying works are not protected by copyright, undermining the scarcity and exclusivity that NFTs often promise. Conversely, NFTs representing works where human creativity is heavily involved in curating or editing AI outputs may still qualify for protection, provided they satisfy traditional authorship standards. This distinction could influence how NFT platforms structure their creation tools and smart contracts, perhaps nudging them toward designs that foreground human collaboration with AI rather than full automation.

The AI authorship rule also intersects with smart contracts and autonomous agents. While copyright deals with creative works, the broader reluctance to recognize purely machine‑generated artifacts as rights‑bearing could foreshadow similar caution in other legal domains, such as contract formation, liability, or even personhood. Courts may be slow to treat an AI‑driven trading bot or self‑executing DeFi protocol as an independent legal actor, instead looking for human entities—developers, deployers, governance token holders—who can be held accountable. For builders who hope that decentralization and automation can shield them from legal risk, the Court’s stance in the AI copyright context is a reminder that human involvement remains central to how law allocates rights and responsibilities.

Power, Legitimacy, and Reform Debates

Because the U.S. Supreme Court has immense power and its Justices enjoy life tenure, debates about its legitimacy and structure have intensified in recent years. Some reformers argue that lifetime appointments allow Justices to wield influence long after the presidents who appointed them have left office, leading to a democratic deficit. One prominent proposal, developed by institutions such as the Brennan Center for Justice, calls for Supreme Court term limits, typically eighteen years, with Justices serving staggered terms of active service such that a new vacancy would open every two years. Under this system, each president would be guaranteed two appointments per four‑year term, promoting regular turnover and reducing incentives for strategic retirements or delayed confirmations.

Proponents contend that term limits would preserve judicial independence while enhancing democratic accountability and reducing the temperature of confirmation battles. Critics worry that imposing term limits might require a constitutional amendment or destabilize settled expectations about judicial tenure. For crypto, these structural debates matter because they influence how predictable and stable the Court’s jurisprudence will be over the long term. A Court whose membership changes more regularly might adjust more nimbly to technological change, but it might also produce more doctrinal swings as different cohorts of Justices revisit prior rulings.

The Court’s legitimacy is also contested along partisan lines. During and after the Trump administration, appointments to the Supreme Court became lightning rods, and the Court’s decisions on issues such as abortion, voting maps, and religious liberty have drawn both praise and intense criticism. Recent coverage, for example, has noted that the Court cleared Alabama to use a GOP‑friendly congressional map for an upcoming election and that state‑level supreme courts, such as Virginia’s, have struck down gerrymanders, prompting celebratory statements from political figures like Trump. These episodes reinforce perceptions that courts are deeply enmeshed in partisan battles, which can erode public trust in their neutrality.

Yet for markets, including crypto, the more important question is often not whether a particular outcome is ideologically balanced, but whether the Court articulates clear, administrable rules that allow actors to plan. Uncertainty about whether the Court might suddenly revisit doctrines central to financial regulation—such as the scope of administrative power, the extraterritorial application of U.S. law, or the enforceability of arbitration clauses—can deter investment and innovation. For a sector that already faces volatile prices and evolving technology, legal instability adds another layer of risk. Conversely, even decisions that industry participants dislike substantively can be beneficial if they deliver clarity that enables consistent compliance and business planning.

How Supreme Court Decisions Ripple Through Digital Asset Markets

Supreme Court decisions rarely mention Bitcoin, Ethereum, or DeFi by name, but their effects cascade through legal and economic systems in ways that ultimately reach digital asset markets. The tariff ruling under IEEPA illustrates how a statutory interpretation can transfer enormous resources between the public and private sectors, affecting corporate balance sheets and macroeconomic conditions that shape appetite for risk assets. If importers succeed in reclaiming tens or hundreds of billions of dollars in refunds, those funds may be used for debt reduction, capital expenditures, dividends, buybacks, or increased risk‑taking, each of which has different implications for correlated assets, including crypto. Even absent direct causal links, such large fiscal shifts alter the backdrop against which crypto trades.

At the micro level, cases like Coinbase v. Bielski and the Nvidia securities litigation influence the cost and availability of capital for crypto‑exposed firms. By making it easier for exchanges to halt class‑action litigation while arbitration appeals proceed, the Supreme Court has reduced some of the immediate litigation drag on large platforms, potentially making them more attractive to investors but also limiting users’ ability to seek collective redress. By letting securities fraud claims tied to crypto mining disclosures proceed against Nvidia, the Court signaled that plaintiffs can test traditional securities theories in the context of crypto‑driven demand cycles, raising disclosure stakes for any public company with significant digital asset exposure. Together, these developments shape how boards, general counsels, and investors evaluate crypto strategies.

In the regulatory sphere, the combination of Chevron’s demise and Jarkesy’s jury‑trial requirement reshapes the risk calculus for agencies contemplating aggressive crypto enforcement. Agencies must now anticipate more intrusive judicial review of their statutory interpretations and the prospect of longer, more resource‑intensive jury trials when pursuing fraud penalties. This may slow some enforcement initiatives, encourage more targeted cases, or push regulators to seek clearer legislative mandates. For crypto, that could mean a temporarily less certain but ultimately more democratically grounded regulatory framework, as courts and Congress negotiate the contours of authority rather than leaving them primarily to agency discretion.

Beyond the United States, supreme courts in other jurisdictions are beginning to assert themselves in crypto matters, as the KuCoin Seychelles case shows. Investors and counterparties increasingly recognize that winning a judgment in one country may require navigating enforcement proceedings in others, depending on where an exchange holds assets or where its affiliates operate. Over time, patterns will emerge about which courts are more protective of investors, which prioritize contractual freedom, and which are more receptive to arguments about decentralization and technological neutrality. These comparative dynamics will influence where projects choose to incorporate, how they draft dispute resolution clauses, and which jurisdictions emerge as hubs for crypto litigation.

SCOTUS is actively reshaping SEC enforcement authority — Jarkesy stripped in-house tribunal power, and pending Howey challenges could redraw which tokens qualify as securities entirely.

SCOTUS rejecting Coinbase's IRS shield confirms that third-party doctrine applies to exchange records, meaning KYC data at any U.S.-regulated exchange is reachable by federal agencies without user consent.

The IEEPA tariff strikes create short-term dollar and risk-asset volatility that correlates with crypto price action, as evidenced by reader interest in tariff rulings tracking alongside crypto sideways trading.

- LiquidityMedium

Government-held Silk Road BTC (~69,370 BTC) moving toward potential disposal after SCOTUS declined review creates a quantified, time-uncertain sell-pressure overhang on bitcoin spot markets.

IRS subpoena victories against Coinbase reinforce that holding assets on centralised U.S. exchanges is a privacy and legal-exposure risk, accelerating structural pressure toward self-custody and DEXs.

- Smart-contract / Legal RecognitionLow

No SCOTUS case has yet directly addressed on-chain contract enforceability; the court's engagement with crypto remains confined to securities classification and government data access rather than protocol-layer legality.

Practical Implications for Builders, Investors, and Policy Advocates

For builders, the Supreme Court’s evolving jurisprudence on administrative power, arbitration, and AI authorship translates into concrete design and governance choices. Smart contract developers and protocol DAOs must assume that agencies will face more judicial scrutiny when asserting jurisdiction over novel products, but that when enforcement does come, it is increasingly likely to play out in federal court with juries and robust discovery. That combination makes it prudent to invest early in compliance, documentation, and governance structures that can withstand adversarial examination rather than relying on informal understandings or opaque multisig control.

Exchanges and platforms should treat Coinbase v. Bielski as validation of arbitration clauses’ procedural force, but not as immunity from scrutiny. Arbitration provisions should be drafted clearly, fairly, and in ways that courts are likely to uphold, given that unconscionable or deceptive terms can still be invalidated. At the same time, companies should be aware of reputational and regulatory pushback against hard‑to‑challenge arbitration regimes, particularly in an environment where policymakers are concerned about consumer protection in crypto. Balancing legal defensibility with user trust will be an ongoing challenge.

Investors, for their part, should integrate Supreme Court risk into their thesis for crypto‑exposed equities and token projects. Decisions on tariffs, birthright citizenship, asylum standards, and gun rights may seem remote from digital assets, but they affect macroeconomic conditions, labor markets, political polarization, and institutional trust—all inputs into risk premia for speculative assets. Closer to home, rulings on agency deference, in‑house tribunals, and AI authorship directly affect the regulatory and IP landscape for crypto projects and AI‑driven trading or NFT platforms. Monitoring the Court’s docket, reading key opinions, and understanding their implications should be part of any sophisticated crypto investor’s research process.

Policy advocates and industry groups have opportunities to shape how future cases are framed and decided. Amicus briefs in cases with indirect crypto relevance—such as those involving administrative law, economic emergency powers, or AI—can educate the Court about how its decisions will impact digital asset innovation. Engaging in legislative advocacy to clarify statutes in light of Supreme Court doctrine may also prove more fruitful than attempting to push agencies to stretch old laws to cover new technologies, particularly in a post‑Chevron environment. As the Supreme Court continues to assert its role in defining the boundaries of government power, crypto stakeholders will need to become more sophisticated constitutional actors, not merely reactive defendants.

Outlook

In the coming years, the Supreme Court is likely to encounter more cases that touch directly on crypto, from prediction markets and stablecoins to the classification of tokens under securities and commodities law. Platforms like Kalshi and Polymarket are already on trajectories that could force the Court to decide whether event‑based contracts are regulated as derivatives, treated as gambling, or recognized as a distinct category, with significant implications for on‑chain prediction markets. As agencies refine their enforcement priorities in light of Loper Bright and Jarkesy, disputes over the limits of their authority to police decentralized protocols and overseas exchanges may also rise through the appellate courts.

At the same time, broader constitutional battles over immigration, emergency powers, and the structure of the administrative state will continue to shape the environment in which crypto develops. Whether the Court adopts term limits, how it navigates calls for institutional reform, and the extent to which it remains perceived as a neutral arbiter rather than a partisan actor will influence investor confidence in the durability of legal rules. For a technology premised on disintermediation and distrust of centralized authority, the paradox is that its long‑term success may depend on the credibility and clarity of one of the most centralized institutions of all: the Supreme Court.

Latest Supreme Court news

Corporate America is bracing for a messy tariff reckoning as companies rush to court to preserve billions in potential refunds if the Supreme Court overturns Trump-era levies.Supreme Court Rules Trump Overstepped Authority by Imposing Global Tariffs Without Clear Congressional Approval. (A looming Supreme Court ruling on Learning Resources v. Trump could overturn emergency tariffs that generated over $200B in duties, putting $100B+ in revenue and potential importer refunds at risk as markets turn cautious and crypto trades sideways. Polymarket CEO Shayne Coplan blasts traditional sportsbooks as a “scam,” arguing they stifle innovation and limit winning bettors as prediction markets edge toward a potential Supreme Court showdown over sports betting legality.

Polymarket CEO Shayne Coplan blasts traditional sportsbooks as a “scam,” arguing they stifle innovation and limit winning bettors as prediction markets edge toward a potential Supreme Court showdown over sports betting legality. Supreme Court signals doubt over legality of Trump’s global and fentanyl tariffs, questioning whether the former president overstepped Congress’s taxing authority.

Supreme Court signals doubt over legality of Trump’s global and fentanyl tariffs, questioning whether the former president overstepped Congress’s taxing authority. U.S. Begins Quiet Retreat From Trump-Era Tariffs, weighing exemptions for goods not made domestically as officials acknowledge the economic strain of reciprocal duties — a shift that could see hundreds of products, from farm goods to aircraft parts, spared ahead of a key Supreme Court review.

U.S. Begins Quiet Retreat From Trump-Era Tariffs, weighing exemptions for goods not made domestically as officials acknowledge the economic strain of reciprocal duties — a shift that could see hundreds of products, from farm goods to aircraft parts, spared ahead of a key Supreme Court review.Sources

- https://www.uscourts.gov/about-federal-courts/educational-resources/about-educational-outreach/activity-resources/about

- https://statecourtreport.org/our-work/analysis-opinion/judicial-deference-agency-expertise-states

- https://www.gibsondunn.com/securities-litigation-2025-mid-year-update/

- https://www.supremecourt.gov/opinions/22pdf/22-105_5536.pdf

- https://www.youtube.com/watch?v=fhQDGuwimO8

- https://www.hklaw.com/en/insights/publications/2026/02/prediction-markets-at-a-crossroads-the-continued-jurisdictional-battle

- https://budgetmodel.wharton.upenn.edu/p/2026-02-20-supreme-court-tariff-ruling/

- https://www.morganlewis.com/pubs/2026/03/us-supreme-court-declines-to-consider-whether-ai-alone-can-create-copyrighted-works

- https://www.quarles.com/newsroom/publications/unanimous-supreme-court-decision-clarifies-how-appeals-courts-review-asylum-persecution-findings

- https://www.theusconstitution.org/litigation/trump-v-barbara/

- https://www.supremecourt.gov/opinions/23pdf/22-451_7m58.pdf

- https://www.whitecase.com/insight-alert/supreme-court-rules-sec-use-house-tribunals-unconstitutional-potentially-far-reaching

- https://www.axios.com/2025/11/18/polymarket-ceo-sportsbooks-gambling

- https://x.com/WuBlockchain/status/2065442960984965517

- https://www.supremecourt.gov/opinions/25pdf/24-777_9ol1.pdf

- https://www.quarles.com/newsroom/publications/supreme-court-rules-new-jersey-transit-is-not-entitled-to-sovereign-immunity

- https://www.youtube.com/watch?v=UXq8Wb59Jhc

- https://www.brennancenter.org/our-work/policy-solutions/supreme-court-term-limits

- https://cdn.ca9.uscourts.gov/datastore/opinions/2023/12/05/22-15566.pdf

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…