Explainer on how short-term U.S. Treasury bills underpin stablecoins, tokenized RWAs and DeFi yields, covering T-bill basics, tokenized funds, T-bill-backed stablecoins, risks, regulation and the growing competition to share risk-free yield on-chain.

+3 sources across the wider coverage universe

Aave founder Kulechov addresses $9B idle liquidity critique, unveiling V4 auto-reinvestment into T-bills to optimize sub-par yield2026-02

Aave founder Kulechov addresses $9B idle liquidity critique, unveiling V4 auto-reinvestment into T-bills to optimize sub-par yield2026-02 Canada’s central bank says stablecoins must be fully redeemable at par, backed by liquid assets like T-bills, with clear, fee-free exit rules. Ottawa plans a federal stablecoin framework in 2025 to support payments modernization.2025-12

Canada’s central bank says stablecoins must be fully redeemable at par, backed by liquid assets like T-bills, with clear, fee-free exit rules. Ottawa plans a federal stablecoin framework in 2025 to support payments modernization.2025-12 CoinGecko's 2023 Q3 Crypto Industry Report: Tokenized T-bills take the lead in on-chain RWA assets, reaching a staggering $665 million2023-10

CoinGecko's 2023 Q3 Crypto Industry Report: Tokenized T-bills take the lead in on-chain RWA assets, reaching a staggering $665 million2023-10- OpenEden launches tokenized T-Bills on XRP Ledger2024-08

Tether's Q2 2024 attestation reveals a record $5.2 billion profit, highest treasury bill ownership, and nearly $12 billion in consolidated equity.2024-07

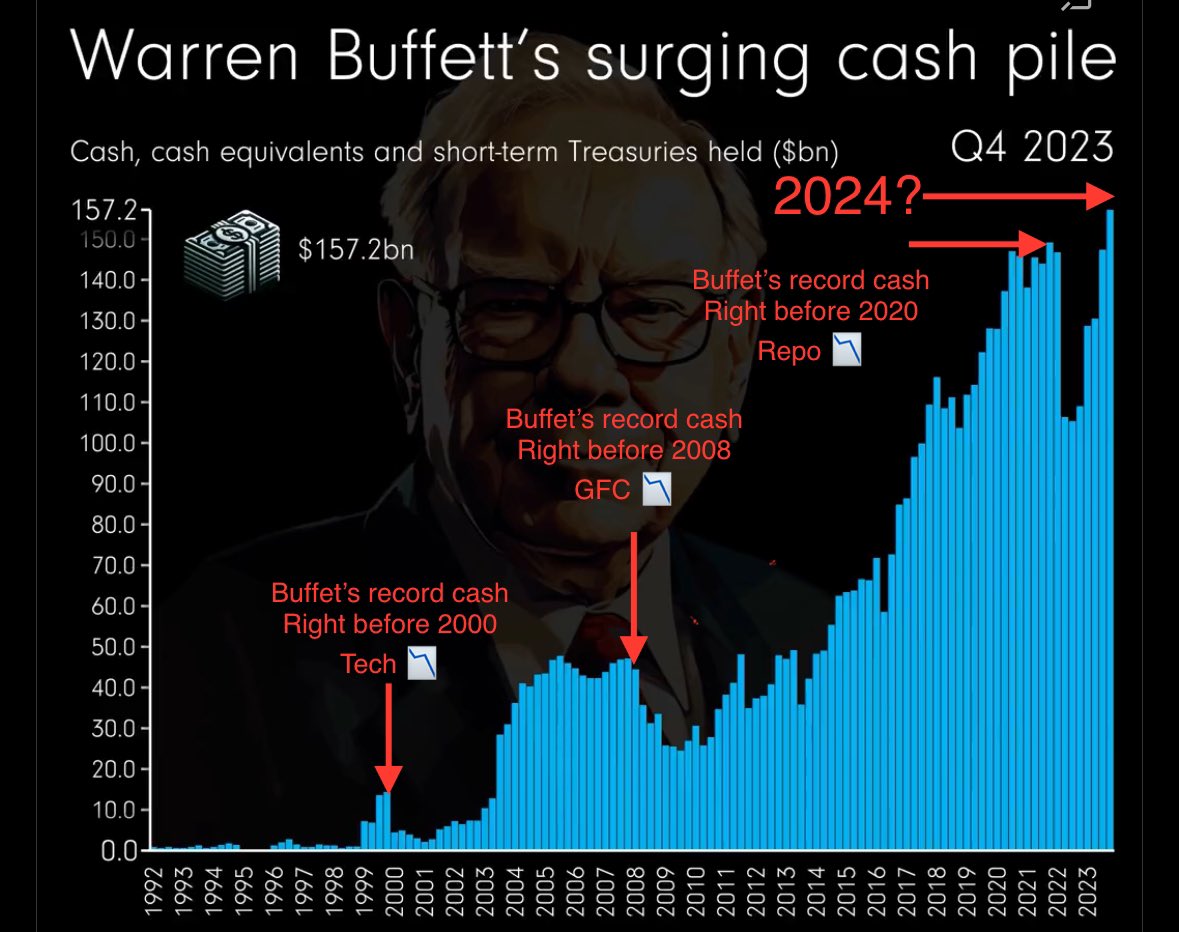

Tether's Q2 2024 attestation reveals a record $5.2 billion profit, highest treasury bill ownership, and nearly $12 billion in consolidated equity.2024-07 Buffett is hoarding $188 billion in cash in short term U.S. T-bills collecting 5.4% rate.2024-05

Buffett is hoarding $188 billion in cash in short term U.S. T-bills collecting 5.4% rate.2024-05

T-Bills, Stablecoins, and DeFi: How U.S. Treasuries Became Crypto’s Safe Yield

Short-term U.S. government debt known as Treasury bills has quietly become one of the most important building blocks behind today’s stablecoins, tokenized real‑world assets, and yield strategies across crypto. As on-chain finance matures, T‑bills and the money market funds that hold them are increasingly serving as the risk‑free anchor for digital dollars, protocols, and even AI infrastructure.

At their core, Treasury bills, or T‑bills, are ultra‑short‑term IOUs issued by the U.S. government, sold at a discount and redeemed at face value in a year or less, providing a low‑risk yield pegged to dollar interest rates. As global demand for safe, liquid assets has surged, T‑bills have become the default cash management tool for corporations, asset managers, and now stablecoin issuers and DeFi protocols. On-chain, this has produced a rapid expansion in tokenized T‑bill funds, yield‑bearing stablecoins backed by short‑dated Treasuries, and composable money‑market tokens like BlackRock’s BUIDL, Matrixdock’s STBT, Mountain Protocol’s USDM, and a growing range of similar products. The result is a new, layered financial stack in which U.S. Treasury exposure sits beneath stablecoins like USDC, Tether, and FDUSD, beneath lending protocols such as Aave, and beneath RWA platforms integrating everything from tokenized high‑yield bonds to GPU‑backed loans. This explainer unpacks how T‑bills work, why they matter so much to crypto, how tokenized Treasury exposure is structured, and what risks and regulatory questions lie ahead as DeFi converges with the world’s primary safe‑asset market.

What Treasury Bills Are and How They Work

Treasury bills are short‑term debt securities issued by the U.S. Department of the Treasury to finance government operations and manage short‑term funding needs. Unlike longer‑dated Treasury notes and bonds, which pay semiannual coupons, T‑bills are issued at a discount to their face (par) value and mature at par, with the investor’s return entirely captured in the price difference between purchase and redemption. Maturities are typically very short, commonly four, eight, 13, 26, or 52 weeks, and the market is deep and liquid, with primary issuance conducted through regular auctions and a robust secondary market where bills can be traded before maturity. Because they are backed by the full faith and credit of the U.S. government and carry negligible credit risk under normal conditions, T‑bills are widely treated as the closest practical approximation to a risk‑free asset in U.S. dollars.

The pricing and yield mechanics of T‑bills are straightforward but differ from coupon‑bearing bonds in ways that matter for both traditional and on‑chain investors. When an investor buys a bill with a face value of \(F\) at price \(P\) and a maturity of \(n\) days, the investor pays less than \(F\) and receives \(F\) at maturity, with the approximate annualized yield often described by the simple discount yield formula \( \text{yield} \approx \frac{F - P}{P} \times \frac{365}{n} \). In practice, the U.S. Treasury and money market funds use more precise conventions, but the intuition remains the same: the shorter the maturity and the closer the purchase price is to par, the lower the yield; the deeper the discount, the higher the implied yield. Because the maturities are so short, duration risk is minimal, and mark‑to‑market volatility is generally low compared with longer‑dated bonds, especially when bills are held to maturity rather than traded actively.

From a portfolio construction perspective, T‑bills sit at the very bottom of the risk spectrum, alongside overnight reverse repurchase agreements and government‑only money market funds. They are widely used as “cash equivalents” in corporate treasuries and institutional portfolios, a classification reflecting both their safety and their high market liquidity. Large investors can buy and sell multi‑billion‑dollar blocks of T‑bills with tight bid‑ask spreads, and settlement conventions are predictable and standardized. This combination of safety, liquidity, and yield makes bills natural backing for instruments that promise stable nominal value in dollars, such as stablecoins, and a natural target for protocols seeking to earn a low‑risk base yield on idle capital. It is precisely this trifecta that explains their importance to the evolving crypto RWA landscape.

The current interest rate environment has only increased the appeal of T‑bills as a core yield instrument. Following the rate‑hiking cycle in the early to mid‑2020s, short‑term Treasury yields rose into the mid‑single digits, and large investors responded by dramatically increasing their T‑bill allocations. Berkshire Hathaway, for example, ended the first quarter of 2026 with roughly 397.4 billion U.S. dollars in cash and short‑term T‑bills on its balance sheet, substantially higher than in prior years and earning a rate on bills reported around 5.4 percent during this period. When such conservative capital allocators choose to hold record amounts in T‑bills instead of bank deposits or riskier assets, it sends a strong signal to both traditional and on‑chain markets about where the perceived safe yield lies.

Aave founder Kulechov addresses $9B idle liquidity critique, unveiling V4 auto-reinvestment into T-bills to optimize sub-par yield

Interesting move by Aave to address idle liquidity. On-chain data shows a significant portion of Aave's TVL has been underutilized, with yields lagging behind other DeFi protocols. This auto-reinvestment strategy into T-bills could boost protocol revenue and attract more liquidity. It will be important to monitor how this impacts Aave's risk profile and user adoption.

Readers click T-bill stories not to learn what T-bills are, but to audit whether a specific protocol's T-bill backing is real, independently attested, and large enough to matter — click volume tracks trust-verification anxiety, not yield curiosity.↗

T-Bills in Traditional Finance: Safe Asset, Liquidity Anchor, Yield Benchmark

In traditional finance, T‑bills serve three intertwined roles: they are the primary U.S. dollar safe asset, a core source of liquidity for institutional portfolios, and a benchmark for short‑term risk‑free yields. Banking systems, fund managers, and corporate treasurers rely on them to park cash, manage liquidity gaps, and satisfy regulatory or internal risk limits that require holdings of high‑quality liquid assets. Government‑only money market funds, which invest primarily in T‑bills and overnight repos backed by Treasuries, offer investors diversified exposure to this short‑term government debt, and have become a standard tool for households and institutions seeking slightly higher yields than bank deposits while still maintaining daily liquidity and a strong safety profile.

The money market fund structure matters because it is the template many tokenized T‑bill products and stablecoin reserve portfolios follow. Funds governed under U.S. Securities and Exchange Commission Rule 2a‑7, for example, must adhere to strict rules on portfolio credit quality, weighted average maturity, liquidity buffers, and diversification, designed to ensure that their net asset value remains stable and redemptions can be honored under stress. Circle, the issuer of USDC, explicitly emphasizes that the majority of the USDC reserve is held in the Circle Reserve Fund (USDXX), an SEC‑registered 2a‑7 government money market fund composed of highly liquid cash and cash‑equivalent assets such as short‑dated U.S. Treasuries and overnight repurchase agreements. The remaining portion of USDC reserves sits in cash at large banks, but the structure underscores how T‑bills and related government instruments provide the baseline safety for even ostensibly “crypto‑native” dollars.

Asset management giants have also moved to package T‑bill exposure into structures that are now being mirrored on‑chain. BlackRock’s BUIDL fund, for example, is a tokenized money market fund available through Securitize that invests investors’ U.S. dollars into overnight repurchase agreements and Treasury bills in order to earn short‑term yield. At its core, BUIDL is a conventional institutional government money market fund; what is novel is that investors receive tokenized representations of their shares that can move on public blockchains within a controlled, whitelisted environment. This approach allows investors to enjoy the safety and regulatory oversight of a traditional fund while gaining some of the composability and programmability of blockchain‑based assets.

The behavior of conservative investors such as Berkshire Hathaway reinforces the centrality of T‑bills in this ecosystem. The firm’s record cash and T‑bill position approaching four hundred billion dollars in 2026 demonstrates that even when equities and risk assets are available, large pools of capital may choose to prioritize liquidity and capital preservation, particularly in higher‑rate environments. For crypto participants trying to understand why so much money is suddenly flowing into stablecoins, tokenized T‑bill funds, and yield‑bearing dollars, this context is critical: the goal is not necessarily to maximize return but to earn a safe, transparent, policy‑driven yield on dollar cash without taking on bank credit risk, duration risk, or opaque leverage.

As a result, short‑term Treasuries now define the opportunity cost of “cash” both off‑chain and on‑chain. When the yield on T‑bills is near zero, parking stablecoins in a wallet or lending them at a modest rate may be acceptable. But when the risk‑free rate rises to several percent, the pressure intensifies to capture that income. Traditional finance layers such as money market funds and corporate treasuries naturally respond; crypto protocols, stablecoin issuers, and DeFi users are now doing the same by seeking direct or indirect exposure to T‑bills and the money market instruments built on top of them.

Why Crypto Cares About T-Bills

The crypto ecosystem has historically revolved around volatile assets such as Bitcoin and Ether and around native yield sources like perpetual futures funding, margin lending, and liquidity provision in automated market makers. As the market has matured and institutional participation has increased, however, there has been growing demand for instruments that behave more like cash or high‑grade bonds than speculative tokens. T‑bills have become central to this shift because they satisfy three core requirements: they are denominated in dollars, they are highly liquid and broadly accepted, and they offer what is widely perceived as the “risk‑free” yield in the U.S. dollar system.

The earliest and still dominant expression of this demand is in fiat‑backed stablecoins. CoinGecko’s research indicates that the vast majority of on‑chain real‑world assets by market value are USD‑pegged stablecoins, and that the top three—Tether’s USDT, Circle’s USDC, and MakerDAO’s DAI—collectively account for roughly ninety‑five percent of the RWA stablecoin market. As of early 2024, USDT alone had a market capitalization of around 96.1 billion U.S. dollars and commanded roughly 71.4 percent of the USD stablecoin market, with USDC at about 26.8 billion and DAI at 4.9 billion. These tokens function as the primary medium of exchange and unit of account in much of DeFi, and their issuers hold substantial reserve portfolios largely composed of cash and short‑term U.S. government securities such as T‑bills and Treasury‑backed repos.

USDC’s reserve structure is explicit: the stablecoin is described as a digital dollar backed one hundred percent by highly liquid cash and cash‑equivalent assets, always redeemable 1:1 for U.S. dollars, and with the majority of reserves held in the Circle Reserve Fund, an SEC‑registered 2a‑7 government money market fund. This implies that a significant share of USDC’s backing is ultimately short‑dated U.S. Treasuries and closely related government obligations, with the remainder held as cash at highly regulated global banks. First Digital’s FDUSD stablecoin follows a similar model, with reserves comprising cash and a basket of highly liquid U.S. Treasury bills of very short‑dated maturity and overnight reverse repurchase agreements, and each token intended to be fully backed by one U.S. dollar or an asset of equivalent fair value. FDUSD can be redeemed for fiat by qualified clients who complete anti‑money‑laundering and counter‑terrorism‑financing checks, with the stablecoin taken out of circulation upon redemption.

Tether, the largest USD stablecoin issuer by market capitalization, has likewise shifted heavily into Treasuries and cash‑equivalent instruments. Its first‑quarter 2024 attestation reported a record‑breaking profit of approximately 4.52 billion U.S. dollars and highlighted the highest percentage ownership of Treasury bills in its history, along with expanded total group equity. Public disclosures from Tether emphasize that a large portion of its reserves are held in U.S. T‑bills and related highly liquid assets, positioning the company as a significant holder of U.S. government debt and aligning its fortunes closely with short‑term interest rates and the stability of the U.S. Treasury market. For stablecoin users, this means that when they hold USDT, they indirectly rely on the safety and liquidity of T‑bills and related instruments, even if they never directly see those securities.

Beyond stablecoins, protocol treasuries and centralized exchanges have begun to treat T‑bills as a natural destination for idle U.S. dollar liquidity. WOO X, for instance, partnered with institutional RWA platform OpenTrade to launch RWA‑backed “Earn Vaults” that allow clients’ idle USDC balances to earn yields around 4–5 percent annualized by channeling funds into high‑quality real‑world financial assets. While the underlying portfolio can include a mix of instruments, short‑term U.S. government securities are a key component, and the structure effectively transforms what would otherwise be unproductive stablecoin balances into T‑bill‑anchored yield streams for exchange clients. This mirrors traditional brokerage cash sweep programs but with stablecoins as the funding currency and tokenized rails for settlement and accounting.

DeFi protocols are going further by integrating T‑bill exposure directly into their core lending markets. Aave’s forthcoming Version 4, for example, introduces a Reinvestment Module designed to automatically deploy excess idle liquidity from its lending pools into low‑risk yield strategies, including short‑term Treasuries, without imposing lock‑ups or withdrawal restrictions on depositors. According to Aave Labs, this module aims to address longstanding criticism about the opportunity cost of idle liquidity by connecting on‑chain capital to off‑chain yield rates, thereby allowing depositors to earn more than they would in comparable traditional instruments while still being able to exit instantly back into stablecoins or other crypto assets. Here again, T‑bills function as the anchor for yield: the protocol seeks to capture the risk‑free rate and pass some of it through to depositors, with the additional protocol revenue used to strengthen the DAO’s finances.

Taken together, these developments reveal why T‑bills are so important to crypto: they are the asset that underpins the “dollar” side of the crypto economy. Stablecoins, lending markets, and new RWA protocols all ultimately compete for access to the short‑term Treasury yield, deciding how to slice it between issuers, tokenholders, and protocol treasuries. As rates and regulation evolve, this competition over who captures the T‑bill yield will shape both stablecoin design and DeFi business models.

- 01tokenized RWA market milestones↗

The single highest-clicked headline was a quantified market-size moment — $665M on-chain — giving readers a concrete benchmark for how fast institutional assets were moving into DeFi rails.

- 02stablecoin reserve attestations↗

Multiple Tether attestation headlines and the FDUSD/Justin Sun solvency dispute drew sustained clicks because readers wanted proof, not promises, that dollar-pegged coins were actually backed by T-bills.

- 03DeFi protocol T-bill integration↗

Aave V4 auto-reinvestment, BlackRock BUIDL into Aave GHO, MakerDAO's $100M allocation proposal, and frxUSD's USTB reserve all signaled that blue-chip DeFi was routing idle liquidity into T-bill wrappers as a yield floor.

- 04institutional and TradFi T-bill signals↗

Buffett's $188B T-bill hoard and BofA's stablecoin-driven Treasury demand forecast let crypto readers triangulate whether on-chain T-bill demand was a blip or part of a macro rotation into short-duration safety.

- 05multi-chain tokenization launches↗

OpenEden on XRP Ledger, Spiko on Arbitrum, and Woo X's retail T-bill product each marked a new chain or audience segment unlocked, making each launch a credible 'first' story readers tracked as market expansion.

- 06stablecoin regulatory frameworks↗

Canada's proposed mandatory T-bill backing and BofA's warning that tokenized T-bills threaten money market funds more than sovereign bond markets signaled that regulators and banks were starting to price in on-chain T-bill competition.

Tokenized T-Bills and On-Chain Money Market Funds

The most direct way T‑bills appear on‑chain is through tokenized products that represent a claim on either the bills themselves or on shares of a fund that invests in them. These are often categorized under the broader umbrella of real‑world assets (RWAs), a term that refers to the tokenization of tangible or off‑chain financial assets that are brought onto blockchain networks. CoinGecko’s research shows that tokenized T‑bill products have been among the fastest‑growing segments of the RWA space: in 2023, tokenized U.S. Treasury bills were the largest driver of on‑chain RWA assets, with market capitalization rising from about 114 million U.S. dollars in January to 665 million by the end of September, a roughly 5.84‑fold increase. A broader category of tokenized Treasury products is estimated to have grown by about 782 percent in 2023 to reach over 931 million dollars, marking a significant institutionalization of on‑chain safe‑asset exposure.

Direct T-Bill-Backed Tokens

Some of the most straightforward tokenized products are directly backed by short‑term U.S. Treasury bills held in custody by a regulated entity, with the token representing a pro‑rata share of a bankruptcy‑remote pool. Matrixdock’s Short‑Term Treasury Bill Token (STBT) is one prominent example: it is marketed as being backed by short‑term U.S. Treasury bills, pegged 1:1 to the U.S. dollar, and designed to provide low volatility and diversification for digital asset portfolios. Each STBT token is described as equivalent to one U.S. dollar of net asset value in underlying short‑term Treasuries, and holders receive daily interest through an on‑chain rebasing mechanism that increases token balances to reflect accrued yield. From the user’s perspective, STBT functions much like a tokenized government money market fund share with automated reinvestment and clear linkage to specific T‑bill holdings.

Mountain Protocol’s USDM is another influential design that brings T‑bill exposure on‑chain but presents it as a yield‑bearing stablecoin rather than a security token. USDM is described as a fully compliant, yield‑bearing, institutional‑grade stablecoin backed by U.S. Treasury bills held as part of the USDM reserves. Mountain Protocol emphasizes that T‑bills are generally regarded as the safest U.S. dollar asset and widely used by institutions to manage their own treasuries, and it extends this model to stablecoin users by incorporating the underlying T‑bill yield into the token’s behavior rather than retaining it solely for the issuer. In practice, USDM behaves like a stablecoin whose backing assets are short‑dated Treasuries and whose holders earn a yield that tracks T‑bill rates, positioning it as a competitor to traditional non‑yielding stablecoins.

While T‑bill‑backed tokens originally focused on Ethereum, the tokenization trend is now expanding to other chains and asset classes. OpenEden, a regulated RWA platform based in Bermuda, has launched HYBOND, a tokenized product that offers eligible investors on‑chain access to BNY Investments’ Global Short‑Dated High Yield Bond strategy. HYBOND initially targets selected institutional clients, with broader institutional availability planned, and is supported on the Ethereum network with plans to extend to the XRP Ledger, BNB Smart Chain, and other networks. Although HYBOND itself is backed by short‑dated high‑yield corporate bonds rather than T‑bills, it illustrates how RWA platforms that began with tokenized Treasuries are now moving up the risk curve, using the same tokenization infrastructure that was first proven with safe government securities.

Tokenized Money Market Funds and Institutional Vehicles

A second major category consists of tokenized money market funds that hold T‑bills and overnight government repos as part of a diversified portfolio, with tokenholders effectively owning fund shares rather than specific T‑bill allocations. BlackRock’s BUIDL fund is the flagship example. Managed by BlackRock and made available through Securitize, BUIDL invests investor U.S. dollars into overnight repurchase agreements and Treasury bills to generate yield, while representing investor positions as tokens on the Ethereum blockchain. Each token corresponds to an interest in the underlying fund, and because the fund is structured under conventional securities law, the tokens themselves are generally treated as securities, restricted to qualified investors and subject to regulated transfer regimes. This design marries BlackRock’s money market expertise with on‑chain settlement and opens the door for BUIDL tokens to be used as collateral or settlement assets in permissioned DeFi environments.

Spiko’s tokenized money market funds extend this model to both U.S. and European markets and focus explicitly on making risk‑free interest rates in euros and dollars accessible to individuals, small and medium‑sized enterprises (SMEs), and startups. The funds are designed to give such users easy access to euro and dollar money market yields, which typically derive from holdings of government T‑bills and related instruments, while leveraging blockchain rails for faster, more transparent ownership tracking and transfer. By bringing regulated U.S. and EU T‑bill exposure onto a Layer‑2 ecosystem like Arbitrum, tokenized funds such as those offered by Spiko aim to combine institutional‑grade asset management with the cost and composability advantages of modern L2 networks.

These tokenized money market funds do more than simply mirror off‑chain structures. Because they issue closed‑end or open‑ended tokens that can be integrated into DeFi protocols, they enable new forms of composability. For example, a DAO treasury might hold BUIDL or a similar token as a core reserve asset and then deposit those tokens into a lending protocol that supports them as collateral, effectively chaining together traditional money market risk with on‑chain credit risk. While such integrations are still in early stages and often limited by KYC and securities law constraints, the direction of travel is clear: tokenized T‑bill funds are becoming building blocks in their own right, not just static warehouse receipts.

Hybrid Designs: Synthetic Dollars, T-Bills, and Real-World Credit

A third, more experimental wave of products blends T‑bill exposure with other real‑world assets to create synthetic dollar instruments that balance safety and growth. USD.AI’s design is a prominent example that combines Treasuries with GPU‑backed loans to finance AI infrastructure while offering different risk–return profiles to tokenholders. The protocol uses a two‑token system in which USDai functions as a fully backed synthetic U.S. dollar, one hundred percent collateralized by U.S. Treasuries and cash equivalents, while sUSDai represents a yield‑bearing version of USDai that earns income from both Treasury yields and interest on loans secured by real GPU hardware. At present, the protocol reports that roughly ninety‑nine percent of sUSDai’s backing comes from Treasuries, with the remainder from GPU loans, reflecting a cautious ramp‑up in credit exposure on top of a T‑bill foundation.

The loan underwriting framework at USD.AI illustrates how deeply traditional asset evaluation can be integrated into on‑chain products. Before any GPU‑backed loan is originated, the protocol’s curators verify the specific GPUs being pledged, the location and insurability of the hardware, and the revenue‑generating offtake or service agreements that will allow the borrower to service the debt. This includes confirming custody at verified, insurable data centers, obtaining warehouse receipts acknowledging physical custody, and ensuring full replacement‑value insurance coverage that names both the bailee and the lender. Credit analysis models hardware depreciation, expected resale values, income stability, and utilization rates before funding first‑loss tranches. In this architecture, T‑bills provide the core stability and liquidity for both USDai and sUSDai, while GPU loans offer incremental yield; together they create a structured product that resembles a cross between a stablecoin, a T‑bill fund, and an asset‑backed security.

Such hybrid designs underscore a broader point: in the emerging RWA stack, T‑bills are not the end of the story but the base layer. Once that base is tokenized and accessible on‑chain, protocols can use it as collateral or as a reference asset to support riskier lending, structured products, or real‑economy financing. The safety and liquidity of T‑bills make them uniquely suited to this role, giving them a central place in the evolving intersection of crypto, capital markets, and sectors like AI infrastructure.

Canada’s central bank says stablecoins must be fully redeemable at par, backed by liquid assets like T-bills, with clear, fee-free exit rules. Ottawa plans a federal stablecoin framework in 2025 to support payments modernization.

What they mean is they want us all to buy their debt

Stablecoins, Reserves, and the Battle for T-Bill Yield

While tokenized T‑bill funds are important, the biggest driver of Treasury exposure in crypto remains fiat‑backed stablecoins. Their scale means that decisions about reserve composition and yield distribution reverberate far beyond individual protocols, affecting both the U.S. Treasury market and the competitive dynamics among stablecoin issuers.

Reserve Composition and Transparency

USDC highlights a transparency‑first model: Circle states that USDC and its euro counterpart, EURC, are fully backed by highly liquid fiat reserves held separately from the company’s operating funds at leading financial institutions for the benefit of stablecoin holders. The majority of the USDC reserve is held in the Circle Reserve Fund (USDXX), an SEC‑registered 2a‑7 government money market fund, with the remainder held in cash at a small group of globally significant banks with high capital, liquidity, and supervisory standards. USDC is described as always redeemable 1:1 for U.S. dollars, making its stability contingent on the liquidity and safety of short‑dated Treasuries and related government instruments inside the Reserve Fund and on regulated banking relationships for the cash portion.

FDUSD adopts a similar but not identical approach. First Digital Labs notes that each FDUSD is intended to be fully backed by one U.S. dollar or an asset of equivalent fair value, with reserves comprising cash and a basket of highly liquid U.S. Treasury bills of very short‑dated maturity and overnight reverse repurchase agreements. Unlike some competitors, FDUSD redemption is not entirely open to any holder: to redeem directly, a user must become a client of First Digital Labs, meeting specific requirements including AML and CTF checks. Once onboarded, the client can exchange FDUSD for fiat currency, with redeemed tokens removed from circulation. The stablecoin is nonetheless widely accessible through secondary markets, as many major cryptocurrency exchanges list FDUSD and provide liquidity for users who may never interact with First Digital directly.

Tether’s disclosures, although historically more contentious, now underscore a heavy emphasis on Treasuries as well. In its Q1 2024 attestation, Tether reported a record‑breaking profit of about 4.52 billion dollars, attributing much of this performance to the yield generated on its reserves, and highlighted that it held the highest percentage ownership of Treasury bills in its history, with total group equity exceeding 11 billion. Supplemental public communications have stressed that Tether’s U.S. Treasury exposure is now so large that the company ranks among the major holders of T‑bills globally, surpassing several nation‑states. For USDT holders, this means that their stablecoin is effectively a claim on a portfolio whose key risk factors are the safety of U.S. government debt and the company’s operational and legal robustness.

These reserve structures have macro implications. S&P Global Ratings, in its analysis of stablecoins and Treasuries, estimates that U.S. dollar stablecoin issuers’ net purchases of T‑bills may reach 50–55 billion dollars by the end of 2025, up from an estimated 36 billion in 2024. While this remains a small fraction of the overall Treasury market, it is non‑trivial, particularly in the short‑dated segment, and contributes to a growing ecosystem in which stablecoin issuers and tokenized funds are meaningful participants in U.S. government debt demand. CoinGecko’s observation that most on‑chain RWAs are stablecoins further underscores that, indirectly, a significant share of crypto’s real‑world asset exposure is to T‑bills and related government instruments.

Who Captures the Yield?

One of the most contentious questions in the stablecoin market is who should capture the underlying T‑bill yield: the issuer, the tokenholder, or some combination via protocol incentives. Historically, most fiat‑backed stablecoins did not pass through any interest to users. When interest rates were near zero, this was widely accepted. But as T‑bill yields have risen into the mid‑single digits, the economics have shifted dramatically. Tether’s multi‑billion‑dollar quarterly profits, for instance, reflect the fact that the company earns risk‑free T‑bill yield on tens of billions of dollars in reserves while paying no explicit interest to stablecoin holders; the spread accrues to Tether’s equity. This has prompted debate over whether such profits are justified by operational and regulatory burdens or whether more of the yield should flow back to tokenholders.

Yield‑bearing stablecoins and tokenized T‑bill funds are a direct response to this debate. Mountain Protocol’s USDM explicitly positions itself as a yield‑bearing stablecoin backed by short‑term U.S. government securities, sharing the treasury yield with tokenholders instead of keeping it entirely at the issuer level. Frax’s frxUSD stablecoin is described as fully backed by bankruptcy‑remote, tokenized U.S. Treasury funds managed by institutions such as BlackRock, Superstate, and WisdomTree, with minting and redemption available 1:1 via partner institutions across more than twenty blockchain networks. While the details of how yield is distributed can vary, frxUSD’s architecture makes the connection between tokenized Treasury funds and a stablecoin explicit, paving the way for more direct pass‑through of T‑bill returns to DeFi stablecoin users.

The USD.AI design goes even further by splitting the stable value and yield components into two separate tokens, USDai and sUSDai, the latter of which receives income from both T‑bill yields and interest on GPU‑backed loans. This two‑token system allows risk‑averse users to hold USDai, fully backed by Treasuries and cash equivalents, while more yield‑seeking users can opt into sUSDai, bearing additional exposure to real‑world credit risk in exchange for higher returns. Aave’s Reinvestment Module similarly aims to boost yields for depositors by automatically deploying idle protocol liquidity into short‑term Treasuries and similar low‑risk strategies, thereby letting depositors capture a portion of the risk‑free yield that would otherwise be foregone.

Centralized platforms also recognize this competitive pressure. WOO X’s RWA‑backed Earn Vaults use OpenTrade’s infrastructure to put idle USDC to work in high‑quality real‑world assets, offering clients yields in the 4–5 percent range and helping the exchange respond to criticism that customer stablecoin balances were not being managed efficiently. As more tokenized T‑bill products and yield‑bearing stablecoins become available, the expectation that stablecoin providers “share the T‑bill yield” with users is likely to grow, driving innovation in both product design and revenue‑sharing models.

Regulatory Perspectives on T-Bill-Backed Stablecoins

Regulators are increasingly attentive to the role of T‑bills in stablecoin reserves, viewing them as both a source of stability and a potential conduit for systemic risk. Canada offers an illustrative case. A C.D. Howe Institute analysis notes that Canada’s 2025 federal budget announced plans for legislation to regulate fiat‑currency‑backed stablecoins as part of a broader digital payments modernization initiative. The emerging Canadian framework emphasizes that stablecoins should be fully redeemable at par and backed by liquid assets such as T‑bills, with clear, fee‑free exit rules to protect consumers and maintain confidence. This reflects a view that backing with high‑quality government securities and segregated cash is essential for making stablecoins safe enough to integrate into mainstream payments systems.

Global ratings agencies share similar concerns about stability and asset quality. S&P Global Ratings argues that while stablecoins could add some incremental demand for Treasuries, their larger significance lies in their potential impact on financial stability and the safe‑asset ecosystem. By projecting that stablecoin issuers’ net T‑bill purchases may grow significantly by 2025, S&P highlights a scenario in which stablecoins become notable buyers of short‑term government debt, potentially affecting money market fund dynamics and bank deposit bases even if they do not substantially move Treasury yields themselves. In this view, T‑bill‑backed stablecoins are both an opportunity and a risk: they can improve payment efficiency and broaden access to safe assets, but they may also disintermediate traditional banks and money market funds, shifting liquidity and risk into new, less regulated channels.

For T‑bill‑backed tokens that are clearly securities—such as many tokenized money market funds—regulatory treatment is more straightforward: they generally fall under existing securities law and must comply with restrictions on who can invest, where tokens can trade, and how information is disclosed. The complexity intensifies with stablecoins that resemble bank deposits or payment instruments more than securities. Policymakers are actively grappling with whether to treat them as e‑money, deposit substitutes, investment products, or a new category altogether, with backing by T‑bills often seen as a mitigating factor but not a complete solution.

Tokenized T-bills hit $665M on-chain per CoinGecko Q3 report

Mountain Protocol launches USDM, yield-bearing stablecoin backed by short-dated Treasuries

Tether Q1 2024 attestation: $4.52B profit, highest-ever T-bill ownership percentage

Tether Q2 2024 attestation: $5.2B record profit, $72.5B T-bill exposure, ranked 22nd-largest Treasury buyer

Spiko launches regulated US and EU tokenized T-bill funds on Arbitrum

Aave V4 auto-reinvestment module proposal: idle liquidity routed into T-bill products

Canada proposes federal stablecoin framework requiring full T-bill or liquid-asset backing

- 2026-05launch

Pendle lists USDG T-Bill RWA stablecoin, anchoring institutional fixed-income markets on-chain

Mechanics: How On-Chain Access to T-Bills Actually Works

Behind every T‑bill‑linked token or stablecoin sits a set of legal, operational, and technical arrangements that determine what users really own and what risks they bear. Understanding these mechanics is crucial for evaluating the safety and utility of such products.

At the legal level, most tokenized T‑bill offerings rely on a special purpose vehicle (SPV), trust, or regulated fund that holds the underlying securities in a segregated account. In the case of Matrixdock’s STBT, for example, short‑term U.S. Treasury bills are held in custody, and the STBT token is designed to represent an interest in that pool with a stable net asset value of one U.S. dollar per token. Yield accrues as the underlying T‑bills generate interest, and the token’s supply is adjusted through a daily on‑chain rebasing process that increases balances in holders’ wallets rather than changing the price per token. Redemptions typically involve burning tokens and receiving fiat or bank transfers from the issuer, with secondary market trading enabling many users to enter and exit positions without interacting directly with the issuer.

For money market fund‑based tokens like BUIDL, the structure is similar but maps directly onto a regulated fund. Investors subscribe to fund shares through a transfer agent such as Securitize, which conducts know‑your‑customer checks and ensures eligibility. Once admitted, investors receive BUIDL tokens on Ethereum that correspond to their fund shares, with the tokens subject to on‑chain transfer restrictions so they can only move between whitelisted wallets. The fund itself invests in overnight repos and Treasury bills according to its prospectus, and yield is delivered via traditional fund accounting mechanisms, often reflected as an increasing net asset value per share. Because the tokens are merely a representation of conventional fund shares, their legal status as securities is clear, and they integrate with DeFi mainly via permissioned protocols that can handle security tokens.

Stablecoins backed by T‑bills but not structured as securities present more varied designs. Mountain Protocol’s USDM, for instance, treats the T‑bill reserve as the backing for a payment‑oriented stablecoin whose on‑chain behavior includes yield accrual. Users interact primarily with the token in DeFi, while the reserve portfolio is managed off‑chain to meet regulatory requirements and maintain full backing with short‑term government securities. Frax’s frxUSD similarly uses tokenized U.S. Treasury funds such as those managed by BlackRock, Superstate, and WisdomTree as the underlying collateral, with frxUSD minted and redeemed 1:1 via partner institutions. In these cases, the on‑chain token is not itself a security token representing fund shares but a liability of the issuer or protocol, backed by a combination of tokenized fund interests and cash.

USD.AI’s USDai and sUSDai introduce another twist by using an explicitly dual‑token structure. USDai is minted against a pool of U.S. Treasuries and cash equivalents, giving it characteristics similar to a fully collateralized stablecoin whose backing assets are T‑bills and related instruments. sUSDai is then issued as a claim on the yield generated by that pool plus interest from GPU‑backed loans, with its value and risk profile tied to both interest rates and loan performance. The protocol’s careful documentation of collateral verification, data center oversight, insurance, and offtake agreements illustrates how much traditional legal and operational infrastructure is required to transform real‑world assets into on‑chain collateral while maintaining credible backing.

Technically, these systems rely on smart contracts to track token balances, manage rebasing or interest accrual, and sometimes enforce transfer restrictions. For example, a rebasing token like STBT adjusts balances across all holders within a contract function, distributing yield in proportion to holdings without changing the nominal 1:1 peg. A permissioned token like BUIDL, by contrast, implements smart‑contract logic that only allows transfers between addresses flagged as eligible under the fund’s compliance rules. More complex architectures, such as Aave’s Reinvestment Module, route idle liquidity from DeFi markets into off‑chain yield strategies like short‑term Treasuries, with smart contracts and oracles coordinating deposits and withdrawals to maintain real‑time liquidity on‑chain.

From a user’s perspective, the key questions are: what exactly do I own when I hold this token; who is legally responsible for the underlying T‑bills; how does yield flow to me; and how can I redeem or exit under normal and stressed conditions? The answers vary widely across products, even when all of them reference T‑bills as their ultimate asset.

Risks: What Can Go Wrong with T-Bills in Crypto?

Although T‑bills are often described as “risk‑free,” their integration into crypto introduces several layers of risk beyond the U.S. government’s creditworthiness. Evaluating T‑bill‑linked tokens requires looking past the comforting phrase “backed by Treasuries” to the specifics of duration, custody, legal claims, smart contracts, and regulatory context.

On the market side, T‑bills carry minimal but non‑zero interest rate risk. Because maturities are short, price sensitivity to rate changes is limited compared with longer‑term bonds, especially if bills are held to maturity rather than traded. However, tokenized T‑bill funds typically mark portfolios to market daily, and their net asset value can fluctuate modestly with moves in short‑term rates. For rebasing tokens pegged to one dollar, issuers may absorb some volatility to maintain a stable peg, but this is not guaranteed, particularly under severe market stress. If projects extend beyond pure T‑bills into slightly longer‑dated notes or high‑yield bonds, as with OpenEden’s HYBOND, duration and credit risks become materially more significant.

Credit and sovereign risk, though widely considered remote for U.S. Treasuries, are not zero. Political standoffs over the U.S. debt ceiling or fiscal sustainability could, in extreme scenarios, disrupt Treasury markets or raise questions about the risk‑free status of U.S. bills. Investors like Berkshire Hathaway signal strong confidence in T‑bills by holding hundreds of billions of dollars in them, but that confidence rests on expectations about U.S. governance and economic strength. Stablecoin issuers and tokenized funds are implicitly betting on the continued reliability of U.S. government obligations; users of T‑bill‑backed tokens share that exposure, even if they experience it only as stable dollar balances.

Custody and legal structure pose more immediate risks. The safety of a tokenized T‑bill product depends heavily on whether the underlying securities are held in segregated, bankruptcy‑remote accounts and whether tokenholders have a clear legal claim to those assets. Some products, such as regulated money market funds, operate under well‑established frameworks like the Investment Company Act, offering investors clearer protections and disclosure standards. Others rely on offshore SPVs or bespoke trust arrangements that may be less tested in court. If an issuer fails, becomes insolvent, or is targeted by regulators, tokenholders need to know whether they are senior claimants on the T‑bill pool, general creditors, or something in between. Stablecoins like FDUSD, which require users to become clients of First Digital Labs and pass AML/CTF checks before redeeming, also introduce operational and counterparty risk: redemption is contingent not only on asset backing but on the issuer’s continued willingness and ability to process exits.

Smart contract and technical risks are layered on top. Tokens deployed on public blockchains are subject to bugs, key‑management failures, and potential exploits in both core contracts and surrounding infrastructure. Permissioned tokens with whitelisting logic can become stuck or frozen if governance keys are compromised or misused. Multi‑chain deployments introduce bridge risk, as wrapped representations of T‑bill‑backed tokens may depend on third‑party bridges that have historically been attractive targets for hackers. Even where underlying T‑bills are safe, a malfunction or attack in the tokenization layer could temporarily or permanently disrupt on‑chain access and pricing.

Regulatory risk is perhaps the most complex. Policymakers are still debating how to classify and regulate stablecoins, tokenized funds, and RWA platforms. Canada’s emerging framework, for example, emphasizes full backing by liquid assets like T‑bills and par‑value redeemability for fiat‑backed stablecoins, but other jurisdictions may impose different requirements or restrict retail access to T‑bill‑backed products if they are deemed investment securities rather than payment instruments. In the United States and Europe, regulatory scrutiny of stablecoin reserves, disclosure practices, and consumer protections is intense and evolving, and tokenized T‑bill funds like BUIDL are navigating securities law compliance on top of blockchain‑specific considerations. Changing rules could affect who can buy these tokens, where they can trade, and how they can be integrated into DeFi.

There are also systemic considerations. S&P Global Ratings points out that stablecoin issuers’ growing demand for T‑bills could reach 50–55 billion dollars by 2025, raising questions about how this demand interacts with traditional money market funds and bank funding models. While S&P does not expect stablecoins to materially disrupt Treasury market dynamics in the near term, they may pose a larger competitive threat to money market funds and banks by drawing savers into on‑chain instruments that offer comparable or higher yields with greater programmability. As more tokenized T‑bill and stablecoin products emerge, the line between traditional and decentralized money markets may blur, complicating oversight and crisis‑management planning.

In sum, T‑bills remain among the safest assets in the financial system, but tokenizing them does not eliminate the familiar risks of custody, legal claims, operational failures, and regulatory change. Crypto users must distinguish between the underlying asset’s risk profile and the additional layers introduced by issuers, protocols, and blockchains.

A new analysis looks at how USD.ai uses GPUs, T-bills, and asset-backed securities to fund non-hyperscaler AI infrastructure while offering stablecoin holders new yield sources. With its two-token model and the Allo Game bootstrapping liquidity, the protocol is positioning itself as a bridge between DeFi and the massive AI capex cycle.

Tokenized T-bill wrappers (BUIDL, STBT, USDM) add at least one smart-contract layer between the investor and the underlying Treasury, creating upgrade, oracle, and redemption-logic risk absent from direct T-bill ownership.

Every major tokenized T-bill product relies on a single permissioned issuer for custody and redemption; KYC-gating means on-chain transfers do not guarantee actual liquidity access for secondary holders.

Tokenized T-bill shares are treated as securities in most jurisdictions, creating cross-border compliance friction and leaving retail DeFi integrations in a legal grey zone that no major regulator has fully resolved.

On-chain secondary market depth for T-bill tokens is thin relative to the underlying Treasury market; a coordinated redemption wave could force issuers to liquidate T-bill positions at unfavorable prices if settlement windows don't align.

Short-dated T-bills carry near-zero duration risk and are backed by the full faith and credit of the U.S. government, making the underlying asset the most credit-stable collateral class in existence.

Stablecoin issuers holding T-bills as reserves (Tether, First Digital) introduce a second counterparty layer — the issuer itself — whose solvency, attestation quality, and custodian relationships become systemic risks for the peg.

Case Studies: How T-Bills Are Reshaping Crypto in Practice

A few concrete examples illustrate the range of ways T‑bills now underpin crypto instruments, from stablecoins to lending protocols and AI‑financing platforms.

Mountain Protocol’s USDM represents the straightforward yield‑bearing stablecoin model. Backed by a reserve of U.S. Treasury bills and designed to be fully compliant and institutional‑grade, USDM wraps the T‑bill yield into a stablecoin that can circulate in DeFi while offering holders a return linked to short‑term government rates. For users, this reduces the need to choose between a non‑yielding payment token and a separate tokenized T‑bill fund; USDM aims to be both in one. At the same time, its reliance on T‑bills as primary backing aligns its risk profile with that of U.S. government debt, plus issuer and regulatory risk, making it a relatively conservative choice within the crypto landscape.

First Digital’s FDUSD demonstrates a more traditional custodial stablecoin approach with a T‑bill‑heavy reserve. The stablecoin is intended to be fully backed by U.S. dollars or equivalent assets, with reserves consisting of cash, highly liquid short‑term U.S. Treasury bills, and overnight reverse repos. FDUSD emphasizes accessibility via secondary markets—many major exchanges list it and provide liquidity—while maintaining controlled direct redemption via a client onboarding process with AML/CTF checks. External risk reviewers, such as LlamaRisk in independent analyses, have scrutinized this structure, highlighting both its strengths in asset quality and the trade‑offs inherent in a custodial model that layers counterparty risk on top of the underlying T‑bill exposure.

Frax’s frxUSD takes the route of anchoring a decentralized stablecoin in tokenized U.S. Treasury funds. According to its documentation, frxUSD is fully backed by bankruptcy‑remote tokenized U.S. Treasury funds, managed by firms like BlackRock, Superstate, and WisdomTree, and can be minted and redeemed 1:1 at each partner institution. The stablecoin operates across more than twenty blockchain networks, bringing the backing of institutional Treasuries into a highly composable, multi‑chain DeFi environment. Community proposals to use additional tokenized T‑bill funds, such as USTB, as part of the reserve structure reflect the protocol’s intent to deepen its integration with the tokenized Treasury ecosystem, blurring the line between DeFi liquidity and traditional government debt markets.

On the protocol side, Aave’s forthcoming Reinvestment Module shows how core DeFi infrastructure is evolving to treat T‑bill yield as a base layer of returns. By automatically deploying unused protocol liquidity into governance‑approved, low‑risk strategies including short‑term Treasuries, the module aims to increase returns for depositors and boost revenue for the Aave DAO. Crucially, it is designed so that there are no lock‑up periods or withdrawal restrictions for depositors: capital can flow back from T‑bill strategies into on‑chain pools in response to user withdrawals, preserving the instant‑liquidity expectations of DeFi while tapping into off‑chain yields. This reinvestment architecture turns idle stablecoin deposits into a dynamic bridge between the Treasury market and on‑chain lending, effectively reconciling the world of U.S. government bills with the world of composable smart contracts.

USD.AI’s USDai and sUSDai present perhaps the most ambitious integration of T‑bills into an on‑chain credit platform. By fully collateralizing USDai with Treasuries and cash equivalents and then using that base to support GPU‑backed loans, the protocol seeks to fund non‑hyperscaler AI infrastructure while offering stablecoin holders exposure to safe yields. sUSDai holders, in turn, receive a combination of Treasury yields and loan interest, with the protocol reporting that roughly ninety‑nine percent of sUSDai’s backing is currently Treasuries, the remaining share coming from GPU loan exposure. The design leverages T‑bills as a stabilizing anchor that can absorb shocks and provide liquidity even if some GPU loans underperform, reflecting a sophisticated use of government securities as the foundation for more speculative real‑world credit.

These case studies demonstrate that T‑bills are no longer peripheral to crypto; they are central. Whether as the hidden reserve backing behind USDT and USDC, the explicit collateral in USDM and STBT, the yield engine in Aave v4’s Reinvestment Module, or the stabilizing asset in USD.AI’s AI‑funding experiments, short‑term U.S. government debt has become a key pillar of the on‑chain financial system.

How Crypto Investors Can Think About T-Bill Exposure

For a crypto‑native audience, T‑bill‑linked products may at first glance all look similar: they promise dollar stability and some connection to safe government debt. In practice, the differences are substantial and matter for both risk and usability.

One useful way to frame the landscape is to distinguish between payment‑oriented stablecoins, tokenized T‑bill or money market funds, and hybrid or structured products. Payment‑oriented stablecoins like USDC, USDT, and FDUSD prioritize broad exchange support, deep liquidity, and ease of use in DeFi and CeFi. Their backing portfolios often contain large allocations to T‑bills, but most of the yield accrues to issuers, not users. Tokenized funds like BUIDL, STBT, and Spiko’s products prioritize transparent exposure to T‑bills and related instruments, offer more direct pass‑through of yield, and often impose investor eligibility and transfer restrictions because they are structured as securities or sophisticated investment products. Hybrid products such as USDM, frxUSD, USDai, and sUSDai sit somewhere in between, combining stablecoin functionality with more generous yield‑sharing and, in some cases, additional real‑world credit risk.

The table below illustrates some of these distinctions for a few representative products.

| Product | Type | Primary Underlying Assets | Yield to Holder | Access / Constraints |

|---|---|---|---|---|

| USDC | Fiat‑backed stablecoin | Cash and short‑dated government money market fund holding U.S. Treasuries and repos | No direct yield; interest retained by issuer | Widely available; no direct redemption for some users but broad secondary liquidity |

| FDUSD | Fiat‑backed stablecoin | Cash, highly liquid short‑term U.S. T‑bills, overnight reverse repos | No explicit yield pass‑through; issuer retains reserve income | Exchange‑listed; direct redemption requires onboarding and AML/CTF checks |

| STBT | Tokenized T‑bill token | Short‑term U.S. Treasury bills held in custody | Yes; daily interest distributed via rebasing | Typically restricted to qualified investors and whitelisted addresses |

| BUIDL | Tokenized money market fund | Government money market portfolio investing in overnight repos and T‑bills | Yes; fund yield reflected in token value or balance | Security token; available to eligible investors via Securitize |

| USDM | Yield‑bearing stablecoin | Short‑term U.S. Treasury bills as reserves | Yes; stablecoin structure passes T‑bill yield to holders | Institutional‑grade; availability depends on jurisdiction and platform |

| frxUSD | DeFi stablecoin backed by tokenized Treasuries | Bankruptcy‑remote tokenized U.S. Treasury funds from managers like BlackRock, Superstate, WisdomTree | Designed to share underlying yield via protocol mechanics | Multi‑chain DeFi integration; minting/redeeming via partner institutions |

| USDai / sUSDai | Synthetic dollar and yield token | U.S. Treasuries and cash equivalents; plus GPU‑backed loans for sUSDai | USDai: stable; sUSDai: receives Treasury yield and loan interest | On‑chain; subject to protocol risk and evolving market depth |

For investors and builders, key due‑diligence questions include: the precise composition and maturity profile of the underlying assets; the legal structure and bankruptcy protections; the identity and jurisdiction of custodians; the mechanism and frequency of yield distribution; the redemption terms and any gating; and the regulatory status of the token (security or not). While it may be tempting to treat all T‑bill‑backed tokens as interchangeable “on‑chain cash,” these details can make the difference between a smooth exit and a protracted legal battle in adverse scenarios.

From a portfolio standpoint, T‑bill‑linked tokens can play multiple roles. For conservative users, they can serve as a low‑risk store of value and base currency, particularly when used in place of non‑yielding stablecoins. For active DeFi users and DAOs, they can be used as collateral in lending and derivatives protocols, reducing reliance on volatile assets and improving the safety of leveraged strategies. For developers, they provide a dependable, transparent reference rate that can underpin new forms of interest‑rate derivatives, fixed‑income vaults, and structured products. In all cases, the growing integration of T‑bills into crypto suggests that the boundary between “Web3” and “TradFi” is increasingly porous, with U.S. government debt now circulating, in tokenized form, through the same networks as NFTs and governance tokens.

Outlook

T‑bills have evolved from an obscure corner of the U.S. federal funding apparatus into a central pillar of the crypto financial stack. What began as a quiet shift in stablecoin reserve composition—away from opaque commercial paper and toward short‑dated U.S. government securities—has grown into a full‑fledged tokenized Treasury ecosystem encompassing stablecoins, money market funds, structured yield products, and protocol‑level reinvestment strategies. CoinGecko’s data on the rapid growth of tokenized Treasury products and S&P Global Ratings’ projections of rising stablecoin demand for T‑bills both suggest that this trend is still in its early stages.

Looking ahead, competition over who captures the T‑bill yield is likely to intensify. Traditional stablecoin issuers that retain most of the reserve income may face pressure from yield‑bearing alternatives like USDM, frxUSD, and structured products such as sUSDai, as well as from CeFi and DeFi platforms that channel idle stablecoin balances into tokenized money market funds and T‑bill strategies. At the same time, regulatory developments—such as Canada’s push for a federal stablecoin framework emphasizing full backing with liquid assets like T‑bills and par‑value redemption—will shape which models are viable in mainstream payments and which remain confined to crypto‑native niches. Large asset managers like BlackRock, through vehicles such as BUIDL, are likely to play an increasingly important role as bridges between institutional Treasury markets and on‑chain liquidity, catalyzing new integrations across lending, collateral management, and cross‑border payments.

For now, the core insight is simple: behind many of the dollars moving on public blockchains sit U.S. Treasury bills and the money market funds that hold them. Understanding how those T‑bills are owned, managed, and tokenized is essential for anyone who wants to navigate the emerging world of RWA‑driven DeFi with eyes open to both the opportunities and the risks.

Latest T-Bills news

Aave founder Kulechov addresses $9B idle liquidity critique, unveiling V4 auto-reinvestment into T-bills to optimize sub-par yieldCanada’s central bank says stablecoins must be fully redeemable at par, backed by liquid assets like T-bills, with clear, fee-free exit rules. Ottawa plans a federal stablecoin framework in 2025 to support payments modernization.A new analysis looks at how USD.ai uses GPUs, T-bills, and asset-backed securities to fund non-hyperscaler AI infrastructure while offering stablecoin holders new yield sources.

With its two-token model and the Allo Game bootstrapping liquidity, the protocol is positioning itself as a bridge between DeFi and the massive AI capex cycle. BofA says stablecoin demand for Treasuries projected at $25–$75B in the next year won’t shift T-bill dynamics but poses a bigger threat to money market funds, where tokenization and yield competition are forcing banks to adapt.

BofA says stablecoin demand for Treasuries projected at $25–$75B in the next year won’t shift T-bill dynamics but poses a bigger threat to money market funds, where tokenization and yield competition are forcing banks to adapt. First Digital responded firmly to Justin Sun’s accusations, stating, “This is a dispute with TUSD, not $FDUSD. First Digital is fully solvent—every dollar is backed by U.S. Treasury Bills, with ISIN numbers publicly detailed in our attestation report.”

First Digital responded firmly to Justin Sun’s accusations, stating, “This is a dispute with TUSD, not $FDUSD. First Digital is fully solvent—every dollar is backed by U.S. Treasury Bills, with ISIN numbers publicly detailed in our attestation report.” $150M in tokenized money market funds go live on Arbitrum as Spiko brings regulated US and EU T-Bills to the Layer-2 ecosystem.

$150M in tokenized money market funds go live on Arbitrum as Spiko brings regulated US and EU T-Bills to the Layer-2 ecosystem.Sources

- https://www.investopedia.com/terms/t/treasurybill.asp

- https://www.coingecko.com/research/publications/rwa-report-2024

- https://www.circle.com/transparency

- https://x.com/tokenterminal/status/1775814359236653304

- https://realinvestmentadvice.com/resources/blog/buffett-cash-hoard-why-373-billion-sits-on-the-sidelines/

- https://www.coingecko.com/research/publications/2023-q3-crypto-report

- https://www.matrixdock.com/stbt

- https://mountainprotocol.com/usdm/

- https://openeden.com/news/openeden-bny-hybond-tokenized-high-yield-bond-fund/

- https://www.opentrade.io/case-studies/woo-x

- https://cdhowe.org/publication/the-window-is-closing-how-canada-can-shape-the-future-of-stablecoins-and-digital-payments/

- https://www.spglobal.com/ratings/en/regulatory/article/stablecoins-financial-stability-and-treasuries-whats-next-for-money-and-safe-assets-s101659822

- https://www.firstdigitallabs.com/fdusd

- https://tether.io/news/tether-releases-q1-2024-attestation-reports-record-breaking-4-52-billion-profit-highest-treasury-bill-ownership-percentage-ever-total-group-equity-of-11-37-billion/

- https://docs.frax.com/frxusd

- https://www.spiko.io/blog/spiko-launches-the-worlds-first-tokenized-money-market-funds

- https://aave.com/blog/aave-v4-reinvestment-module

- https://securitize.io/blackrock/buidl

- https://usd.ai/insights/how-gpu-loans-work

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…