In‑depth explainer on UNI, the token behind Uniswap’s DeFi ecosystem. Covers governance, fee switch, UNIfication, Unichain staking, regulatory backdrop, institutional adoption, RWA narrative and key risks shaping UNI’s long‑term role in crypto markets.

+92 sources across the wider coverage universe

Uniswap DAO voted to activate its long-awaited fee switch, redirecting a portion of protocol revenue into a buyback-and-burn mechanism that could destroy up to 100M UNI (~$600M), while Uniswap Labs stops interface fees and the Foundation winds down.2025-12

Uniswap DAO voted to activate its long-awaited fee switch, redirecting a portion of protocol revenue into a buyback-and-burn mechanism that could destroy up to 100M UNI (~$600M), while Uniswap Labs stops interface fees and the Foundation winds down.2025-12 BlackRock brings its $1.8 billion tokenized Treasury fund to Uniswap and buys UNI, marking Wall Street’s first major foray into DeFi trading.2026-02

BlackRock brings its $1.8 billion tokenized Treasury fund to Uniswap and buys UNI, marking Wall Street’s first major foray into DeFi trading.2026-02 $UNI jumps 40% on announcements Blackrock is buying2026-02

$UNI jumps 40% on announcements Blackrock is buying2026-02 Uniswap Labs has relegated the governance rights of UNI token holders in a controversial suite of decisions that favor Optimism.2024-10

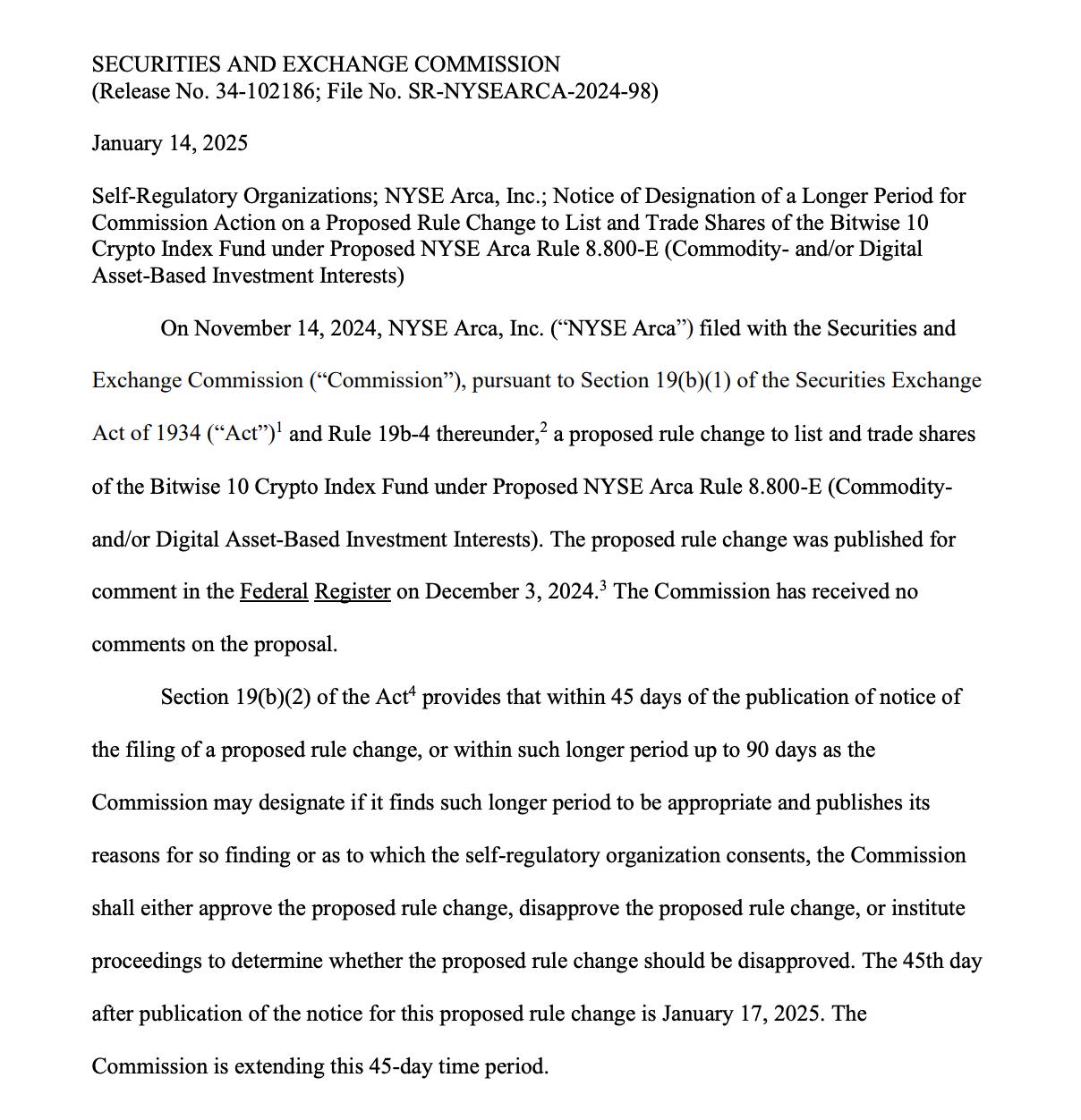

Uniswap Labs has relegated the governance rights of UNI token holders in a controversial suite of decisions that favor Optimism.2024-10 SEC delays Bitwise 10 crypto index ETF (BTC, ETH, SOL, XRP, ADA, AVAX, LINK, BCH, DOT, UNI)2025-01

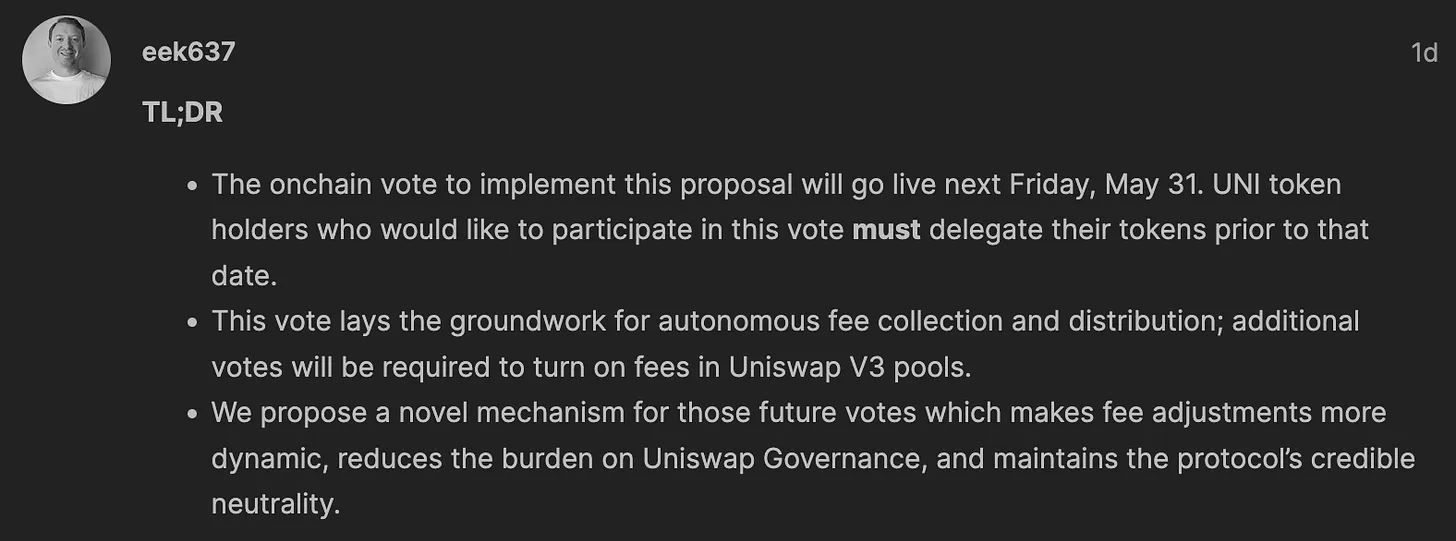

SEC delays Bitwise 10 crypto index ETF (BTC, ETH, SOL, XRP, ADA, AVAX, LINK, BCH, DOT, UNI)2025-01 Uniswap Foundation announces $UNI holders interested in voting on the "fee switch" must have their token delegated before Friday, May 31st to be eligible2024-05

Uniswap Foundation announces $UNI holders interested in voting on the "fee switch" must have their token delegated before Friday, May 31st to be eligible2024-05

UNI: Governance, Tokenomics, and the Future of Uniswap’s Native Token

As the native token of the Uniswap protocol, UNI sits at the intersection of decentralized exchange infrastructure, on-chain governance, and a rapidly evolving model for fee capture and network value accrual. Initially launched as a pure governance asset, UNI is now being reshaped by protocol fee activation, the planned Unichain layer‑2 network, and a series of high‑stakes governance and legal experiments that could define how major DeFi tokens function in the next phase of crypto adoption.

The Uniswap protocol itself is one of the most widely used decentralized exchanges, allowing users to swap tokens directly from their own wallets without relying on centralized intermediaries, and it has become a foundational liquidity layer for DeFi across multiple blockchains. Uniswap’s automated market maker design lets anyone supply liquidity to trading pools and earn fees, helping bootstrap deep markets in thousands of tokens and driving billions of dollars in cumulative trading volume. UNI was introduced as a way to decentralize control over this infrastructure, enabling token holders to govern parameters such as fee structures, protocol upgrades, and treasury spending via the Uniswap DAO. Over time, as the protocol generated more than a billion dollars in fees in a single year with none of that revenue flowing directly to UNI holders, pressure mounted to align the token’s economics with the protocol’s usage and profitability. The DAO’s decision to activate a long‑debated “fee switch,” combined with the proposed UNIfication roadmap and the launch of Unichain, marks a turning point: UNI is evolving from simple governance wrapper into a multi‑faceted asset that can be burned against protocol revenue, staked to validate a dedicated scaling network, and potentially benefit from MEV and settlement fees. At the same time, regulatory outcomes like the SEC’s decision to close its investigation into Uniswap Labs without action, and divergent moves such as Prometheum treating UNI as a digital asset security, underscore the legal uncertainty that still surrounds major DeFi tokens. Added to this are strong opinions from Wall Street—Standard Chartered’s high‑profile forecast that UNI could reach 100 USD by 2030 if tokenized real‑world assets migrate on‑chain—and large institutional forays from players like BlackRock and Grayscale, which collectively frame UNI as one of the leading bellwethers for how DeFi, regulation, and traditional finance will converge. This explainer traces UNI’s role, tokenomics, governance, regulatory context, and market narrative, with a focus on developments that are likely to matter over the long term rather than short‑term price moves.

What Is UNI? Definition and Core Role

UNI is the governance and native incentive token of the Uniswap protocol, a non‑custodial decentralized exchange (DEX) system built primarily on Ethereum that enables peer‑to‑peer token swaps without traditional order books. The protocol uses smart contracts to allow users to provide liquidity to token pairs and set prices algorithmically, with traders interacting directly with liquidity pools instead of centralized market makers. UNI’s original purpose was to decentralize control over key aspects of this system, giving token holders the power to vote on protocol upgrades, parameter changes, and treasury allocations through the Uniswap DAO. In this sense, holding UNI has historically meant holding governance rights over a critical piece of DeFi infrastructure rather than a direct claim on protocol revenue or equity in Uniswap Labs, the company that develops much of the software.

When UNI launched, the token was distributed to early Uniswap users, liquidity providers, and community members, with a fixed initial supply of 1 billion tokens and a multi‑year vesting schedule for team and investor allocations. This airdrop-based launch was widely seen as a watershed moment for DeFi, both because it rewarded early adopters and because it cemented UNI as one of the first large‑scale governance tokens tied to a protocol that already had substantial product‑market fit. Over time, UNI became listed on major centralized exchanges and integrated into a range of DeFi products, cementing its status as a top‑tier crypto asset by market capitalization and trading volume. UNI’s governance role includes decisions about deploying Uniswap to new blockchains, adjusting protocol fee parameters, and funding ecosystem initiatives via the DAO treasury, making it central to the way Uniswap evolves.

For several years after its launch, however, UNI’s functionality remained almost entirely confined to this governance domain, with no direct mechanism by which protocol revenues flowed to token holders. While Uniswap was generating significant trading fees for liquidity providers, the protocol itself did not accrue revenue, and thus UNI holders were effectively stewards of a public good rather than beneficiaries of a cash‑flow‑generating asset. This divergence between the ubiquity of the protocol and the relatively limited economic rights of the token became a central theme in both community debates and external analyst coverage, setting the stage for recent governance moves aimed at aligning UNI more closely with protocol usage. The current evolution of UNI—from a governance‑only token to one that participates in fee burns, network validation, and potentially MEV capture—represents an attempt to reconcile that gap without undermining Uniswap’s open, permissionless design.

Uniswap DAO voted to activate its long-awaited fee switch, redirecting a portion of protocol revenue into a buyback-and-burn mechanism that could destroy up to 100M UNI (~$600M), while Uniswap Labs stops interface fees and the Foundation winds down.

"The fee switch will maintain the current swap fees. But it will divert between one quarter and one-sixth of those fees to a smart contract known as the token jar. Anyone who burns UNI tokens — using a smart contract called “fire pit” — would be able to withdraw an equivalent amount of crypto from the token jar. In order to compensate liquidity providers, the DAO approved development of a new feature, the Protocol Fee Discount Auction. That would “add a new source of protocol fees by internalizing MEV that would otherwise go to searchers or validators,” according to the UNIfication proposal."

Readers click UNI stories to track governance legitimacy, not protocol mechanics — the dominant question across every top headline is who actually controls the fee switch, the treasury, and the right to define UNI's legal status, revealing that the core risk is political capture, not smart-contract failure.↗

How Uniswap Works: Context for UNI

From AMMs to Multi‑Chain Liquidity Hub

Understanding UNI requires a clear picture of the protocol it governs. Uniswap pioneered a form of decentralized exchange based on automated market makers (AMMs), where liquidity pools hold reserves of two tokens and prices are determined algorithmically rather than by matching individual buy and sell orders. Liquidity providers deposit token pairs into these pools and earn a share of the trading fees, which are charged as a small percentage of each swap and accrue directly to LPs in proportion to their contribution to the pool. This model enabled always‑on liquidity and permissionless token listings, in contrast to centralized exchanges where assets must be curated and order books maintained, and it helped drive the explosion of DeFi activity on Ethereum and other EVM‑compatible chains.

Over time, Uniswap evolved from a simple constant‑product AMM (v1 and v2) into a more sophisticated “concentrated liquidity” design with Uniswap v3, where LPs can allocate capital to specific price ranges and thus deploy liquidity more efficiently. This architecture allows for deeper liquidity near the current market price while avoiding idle capital in far‑out price ranges, which in turn improves price execution for traders and can increase fee income for LPs willing to actively manage their positions. Uniswap v3 has been deployed across multiple chains, including Ethereum, various layer‑2 networks, and some alternative L1s, turning Uniswap into a multi‑chain liquidity hub rather than a single‑chain DEX. In aggregate, the protocol has supported large volumes of trading that translate into substantial fee generation across chains.

Recent data cited in governance and research discussions indicate that Uniswap generated on the order of 1.3 billion USD in fees across five chains in a single year, a figure that underscores the protocol’s centrality to DeFi despite periods of market volatility. Crucially, almost all of these fees have historically gone to LPs rather than to the protocol treasury or UNI holders, meaning that the protocol itself did not directly capture revenue even as it facilitated enormous volumes of trading. This “LP‑only” fee model reflected the original design choice to prioritize liquidity and permissionless usage over value extraction at the protocol layer, but it also created a tension: the UNI token, which governed this increasingly important piece of infrastructure, had no native claim on its economic output. As alternative DeFi projects began experimenting with fee sharing and protocol‑owned liquidity, Uniswap’s community faced growing pressure to consider mechanisms—such as a fee switch or staking rewards—that could channel some of this economic activity back to the protocol and its tokenholders.

The forthcoming Uniswap v4, and especially the planned Unichain network, are part of a broader strategy to position Uniswap not just as a DEX, but as a modular liquidity and settlement layer for a wide range of tokenized assets. While v4 preserves the core concentrated liquidity model of v3, it introduces new architectural features like “hooks” that allow developers to customize pool behavior, potentially opening up new forms of order flow, fee structures, and MEV mitigation. Unichain, in turn, is designed as a DeFi‑centric layer‑2 built on Optimism’s OP Stack, aiming to provide fast, low‑cost settlement for Uniswap and other financial applications while giving UNI holders a direct economic role in securing and governing the network. This expansion of Uniswap’s technical footprint is tightly linked to UNI’s evolving utility and tokenomics, as the protocol seeks to align its governance token with its increasingly complex economic landscape.

Governance and the Uniswap DAO

The Uniswap DAO is the on‑chain governance system through which UNI holders propose and vote on changes to the protocol, treasury allocations, and major ecosystem initiatives. Governance proposals typically go through an off‑chain discussion phase in the Uniswap governance forum, followed by on‑chain voting where UNI holders or their delegates can cast votes proportional to their token holdings. This model allows for community control over critical decisions but also depends heavily on active participation and delegation, as many individual UNI holders lack the time or expertise to evaluate complex technical and economic proposals.

In practice, governance power in Uniswap has often been concentrated among large holders and specialized delegate organizations, including venture capital firms, DAO‑native governance shops, and ecosystem partners. To improve participation and expertise, the DAO has experimented with delegation programs that allocate treasury UNI to selected delegates, giving them voting power in exchange for a commitment to actively engage with proposals and the broader community. Recent governance efforts include a plan to delegate up to 18 million UNI from the treasury to a set of active delegates, aimed at strengthening governance engagement and reducing voter apathy. At the same time, the DAO has also moved to reclaim UNI that had been loaned to delegates in earlier programs, including a proposal to retrieve approximately 12.5 million UNI—worth around 42 million USD at the time—from third‑party organizations that had been entrusted with governance power between 2022 and 2023. This vote, which saw a majority in favor of reclaiming tokens, reflected a desire to rebalance power back toward the DAO’s own treasury and ensure that delegation structures remain aligned with community interests.

From a conceptual standpoint, there is an ongoing debate within the Uniswap community about what kind of entity the DAO should be. Some participants argue that Uniswap governance should be a relatively “neutral” body that sets high‑level rules and parameters while leaving day‑to‑day operations and execution to specialized teams, rather than becoming a sprawling organization that tries to run everything on‑chain. This view emphasizes the DAO’s role in governing protocol primitives and high‑level resource allocation, while avoiding over‑centralization of execution within the DAO itself. Others push for a more proactive, quasi‑corporate DAO that can direct product strategy, manage multi‑chain deployments, and even negotiate with external partners. The creation of legal and organizational structures like the Uniswap Foundation and, more recently, the proposed DUNI entity in Wyoming’s Decentralized Unincorporated Nonprofit Association (DUNA) framework, reflects attempts to balance on‑chain governance with off‑chain legal and operational needs. UNI sits at the center of these debates, because control over UNI—and the mechanisms for delegating it—effectively determine who shapes the future of the Uniswap protocol.

UNI Tokenomics: Supply, Distribution, and Economic Design

Supply, Inflation, and Burns

UNI launched with a fixed total supply of 1 billion tokens, allocated among community members, team, investors, and a governance treasury, with vesting schedules intended to align long‑term incentives. For several years, this 1 billion cap defined market expectations around UNI’s supply, and there was no active minting or burning mechanism at the protocol level. However, the UNI token contract was designed with the possibility of future inflation: after January 1, 2024, it became technically possible for governance to mint additional UNI, subject to strict constraints. Specifically, the contract allows new tokens to be minted only once every 365 days, with a hard cap of 2% of the total supply per mint event, effectively limiting potential annual inflation to a maximum of around 2% if governance chooses to use the full allowance. This design gives the DAO flexibility to fund long‑term development and ecosystem programs while preserving a relatively low upper bound on dilution, at least at the base layer of the token contract.

The recent UNIfication proposal from Uniswap Labs and the Uniswap Foundation explicitly builds on this minting capability by suggesting a recurring “growth budget” funded via new UNI issuance. Under the plan, governance would authorize an annual budget of 20 million UNI, beginning in 2026, to be distributed quarterly using a vesting contract to support protocol growth and development. In percentage terms, 20 million UNI corresponds to roughly 2% of the original 1 billion supply, aligning with the token contract’s minting cap. This means that if the growth budget is fully utilized each year, UNI would experience modest but ongoing inflation, at least from this source, though the net effect on supply will also depend on the scale of future burns. The UNIfication proposal also calls for a retroactive burn of 100 million UNI from the treasury, an amount intended to approximate what might have been burned had the protocol fee mechanism been active over the previous few years. Burning 100 million tokens represents a 10% reduction of the original supply, more than offsetting multiple years of the proposed 20 million annual issuance if viewed in aggregate.

More importantly, UNIfication links future protocol usage directly to UNI supply by directing protocol fees into a buyback‑and‑burn mechanism. When the DAO voted to activate the long‑discussed “fee switch,” it adopted a model whereby a portion of the trading fees generated by Uniswap is diverted into a smart contract known as a “token jar.” Rather than distributing these fees directly to token holders, the system allows UNI holders to burn their tokens in exchange for withdrawing an equivalent share of the assets accumulated in the jar. Because burning UNI reduces the total supply, this mechanism is designed to create a deflationary pressure on the token when protocol usage is high, while also giving holders an option to exit into a basket of accumulated protocol fees. Governance parameters currently envision diverting between one‑sixth and one‑quarter of eligible protocol fees into this jar, though this can be adjusted over time.

The net effect of these mechanisms is that UNI’s supply dynamics are now path‑dependent and tied to protocol success. If trading volumes and Unichain activity generate substantial protocol and sequencer fees, and if a meaningful fraction of UNI holders choose to redeem and burn tokens, UNI could become net deflationary even after accounting for the 20 million annual growth budget. Conversely, if trading activity stagnates or the fee switch is configured conservatively, new issuance could dominate burns, leading to moderate inflation that functions as a “tax” on token holders to fund development. Some analysts and community researchers have argued that the combination of buyback‑and‑burn with a fixed growth budget could, in certain scenarios, operate like a “tax on success,” because as the protocol grows and more UNI is burned, the relative impact of newly minted tokens on the circulating supply could become larger. Still, others note that the retroactive 100 million burn and ongoing burns funded by fees can significantly offset dilution, especially if Uniswap maintains or grows its share of DeFi trading volumes. These debates are central to UNI’s investment case and will likely continue as governance refines the parameters in response to market conditions.

Utility: Governance, Fee Capture, and Staking

For much of its history, UNI’s utility consisted almost entirely of governance rights, with no direct link to cash flows or network security, and community members often emphasized that purchasing UNI was not equivalent to buying equity in Uniswap Labs or a revenue share in the DEX. In forum discussions, prominent contributors have repeatedly clarified that UNI is best understood as a token conferring voting power over protocol governance, not as a claim on Uniswap’s corporate profits. This distinction was important both for regulatory reasons and for setting expectations among token holders. However, as DeFi matured and competition intensified, the limitations of a governance‑only token model became more apparent, especially given Uniswap’s substantial fee generation and growing role in on‑chain finance.

The activation of protocol fees and the UNIfication roadmap materially expand UNI’s functional role. First, the fee switch and token jar mechanism give UNI a direct, if indirect, relationship to protocol revenue: instead of periodic dividend‑like distributions, revenue is accumulated in the jar, and token holders can burn UNI to redeem underlying assets. This is structurally different from a conventional profit share, but economically it links UNI’s value to the scale and composition of protocol fees. Second, the UNIfication proposal directs all Unichain sequencer fees—net of Ethereum data costs and a 15% share allocated to Optimism—to this same UNI burn mechanism. That means UNI will not only be tied to Uniswap’s trading fees but also to the settlement economics of the dedicated layer‑2, especially if Unichain achieves significant adoption.

Beyond fee burns, UNI is expected to play an active role in Unichain’s security and operation. Unichain is designed around a “Unichain Validation Network,” in which UNI holders will be able to stake their tokens to help validate Unichain transactions and, in return, earn a share of network sequencer fees. This turns UNI into a staking asset: rather than simply governing parameter changes, staked UNI will participate in the economic security of the layer‑2 and receive on‑chain rewards for doing so. This shift is significant because it adds an explicit yield component tied to network usage, altering UNI’s risk–reward profile compared to its governance‑only past. It also introduces new design questions around staking centralization, slashing, and the interplay between staked and liquid UNI in governance.

A third dimension of UNI’s emerging utility involves MEV (maximal extractable value), the profit that can be captured by reordering, inserting, or censoring transactions within blocks. Uniswap, as a major venue for on‑chain trading, is a large source of MEV opportunities, and recent analysis suggests that MEV associated with Uniswap trades amounts to roughly 10% of total fees paid on the protocol, or around 100 million USD over the past year. Roadmaps and governance discussions around Unichain and Uniswap v4 envision mechanisms to capture some portion of this MEV at the protocol level, rather than leaving it entirely to external searchers and block builders. While the exact distribution is still subject to governance, there is a clear possibility that some share of captured MEV will flow into the same burn and staking mechanisms that benefit UNI holders, reinforcing the token’s link to the protocol’s economic “surface area.” Together, these developments mark UNI’s transition from a purely political token to a multi‑faceted asset that governs, secures, and economically participates in the Uniswap ecosystem.

Market Presence and Institutional Access

UNI’s prominence in the crypto asset landscape is reflected not only in its market capitalization and trading volumes but also in its integration into institutional products and mainstream financial platforms. Market data aggregators consistently list UNI among the largest crypto assets by market cap, with hundreds of millions of dollars in daily trading volume and widespread availability across centralized and decentralized exchanges. Although prices fluctuate, UNI has generally traded in the single‑digit to low double‑digit USD range in recent years, placing it among the more liquid and widely held DeFi tokens. Its role as the native token of the largest DEX by volume has made it a natural component of thematic DeFi indices and funds.

One notable example is the Grayscale DeFi Fund, which holds a basket of leading DeFi tokens that includes UNI alongside assets such as AAVE, MKR, and others. By incorporating UNI into a regulated investment product targeted at accredited and institutional investors, Grayscale has helped broaden access to UNI exposure for market participants who prefer traditional fund wrappers over direct token custody. Another development that underscores UNI’s institutional relevance is its inclusion in the composition of proposed and pending exchange‑traded funds (ETFs). The Bitwise 10 Crypto Index ETF, for instance, has filed with the U.S. Securities and Exchange Commission to include UNI alongside large‑cap assets like BTC, ETH, SOL, and others, although the SEC has delayed decisions on such products.[news: Bitwise filings] These moves signpost UNI’s maturation from a purely crypto‑native governance token into an asset that sits alongside Bitcoin and Ethereum in multi‑asset portfolios.

At the same time, other institutions have begun offering regulated custody services for UNI. Prometheum Capital, a FINRA‑member firm and SEC‑registered special purpose broker‑dealer for digital asset securities, launched a custody platform that supports several crypto assets, including Ethereum, Uniswap’s UNI, Arbitrum’s ARB, Optimism’s OP, and The Graph’s GRT. In Prometheum’s framework, these assets are treated as “digital asset securities,” and the firm offers custodial services that allow institutions to hold them under a regulated broker‑dealer regime. This classification diverges from Uniswap Labs’ interpretation of UNI’s regulatory status, but it demonstrates that UNI is now part of the conversation around institutionally managed digital asset portfolios.

UNI is also increasingly accessible to retail users via mainstream fintech platforms. Brazilian neobank Nubank, which serves more than 100 million customers across Latin America, has expanded a USDC rewards program that allows customers to earn yield and trade selected crypto assets, including UNI. Within this offering, users can swap Bitcoin (BTC), Ethereum (ETH), Solana (SOL), and Uniswap (UNI) for USDC and vice versa at reduced fees, making UNI one of a small set of supported crypto assets. This kind of integration positions UNI as a familiar option for users who encounter crypto primarily through their banking app rather than specialized exchanges, and it may enhance the token’s liquidity and recognition in emerging markets. Together, these institutional and retail on‑ramps indicate that UNI is no longer a niche governance token, but a widely accessible asset embedded in both DeFi and traditional financial channels.

- 01Labs sidelining token holders↗

The top-clicked headline exposed Uniswap Labs unilaterally favouring Optimism while stripping governance rights from UNI holders, making decentralisation feel like a post-hoc label rather than a design guarantee.

- 02Fee switch control and timing↗

Multiple high-click headlines tracked delegation deadlines, buyback-and-burn mechanics, and whether the fee switch would actually make UNI deflationary — readers wanted the exact stake and the exact calendar.

- 03SEC and securities classification↗

Headlines spanning SEC filings, Prometheum classifying UNI as a security, and the eventual SEC retreat drew repeat clicks because each update directly changed whether UNI could be legally held or listed.

- 04MEV and oracle lag exploitation

A $3M bad-debt event caused by oracle latency during UNI price volatility pulled readers who track how AMM design limitations translate into real, measurable losses across interconnected lending protocols.

- 05Treasury delegation power concentration↗

The $113M, 18M-token delegation plan raised immediate reader concern that handing governance influence to select delegates replicates the same capture problem UNI holders already face with Labs.

- 06TradFi institutional entry via DeFi↗

BlackRock parking $1.8B of tokenized Treasuries on Uniswap and buying UNI validated DeFi as infrastructure, not speculation — a signal readers found surprising enough to click despite being bullish.

Governance in Practice: Fee Switch, UNIfication, and DUNI

The Long‑Awaited Fee Switch

The “fee switch” has been one of the most debated topics in Uniswap governance since the days of v2. From the outset, Uniswap’s smart contracts included a mechanism that would allow a portion of pool trading fees to be redirected from liquidity providers to the protocol, but this switch remained turned off for years amid concerns about competitiveness and regulatory implications. Liquidity providers have historically earned the full trading fee—commonly 0.3% or lower depending on pool configuration—with no share going to the protocol treasury, and any change to that arrangement risks affecting LP incentives and the attractiveness of Uniswap compared to rival DEXs. Meanwhile, some community members worried that explicitly directing fees to token holders might increase the risk of UNI being classified as a security under U.S. law, although others argued that carefully designed mechanisms could mitigate this risk.

In late 2025, Uniswap governance finally voted to activate a version of the fee switch, following a governance process shaped by a joint proposal from Uniswap Labs and the Uniswap Foundation under the banner of UNIfication. The adopted design does not send protocol fees straight to UNI holders like a dividend. Instead, a portion of fees—variously described as between one‑sixth and one‑quarter of applicable pool fees—is diverted into the “token jar,” a smart contract that accumulates these revenues over time. UNI holders then have the option to burn their tokens in exchange for a proportional share of the jar’s assets, effectively redeeming UNI for a basket of tokens generated by the protocol’s activity. This mechanism attempts to balance several objectives: it ties UNI’s value to protocol usage, avoids continuous cash distributions that might resemble traditional securities dividends, and preserves LP incentives by diverting only a fraction of fees away from liquidity providers.

Another important aspect of the fee switch activation is the change in how Uniswap Labs monetizes its products. Prior to UNIfication, Uniswap Labs earned revenue by charging interface fees on the official Uniswap website and wallet, adding a small surcharge on top of the underlying protocol fees for users who accessed Uniswap through Labs‑built frontends. As part of the new model, Uniswap Labs agreed to cease charging these interface fees and instead rely on its role as a core development company, funded by the DAO’s growth budget and other arrangements. This change aligns revenue capture more closely with the protocol and UNI holders rather than with a single corporate frontend, reinforcing the narrative that Uniswap is a decentralized public good whose economics are governed by the DAO.

The activation of the fee switch does not settle all debates. Some LPs worry that even a modest diversion of fees could gradually erode Uniswap’s edge if competing DEXs offer higher net returns to liquidity providers. Others counter that Uniswap’s network effects, brand, and deep liquidity may allow it to sustain a protocol fee, especially if LPs benefit indirectly from a stronger, better‑funded protocol. Regulatory observers are watching closely to see whether routing fees into a burn‑and‑redeem mechanism affects how UNI is viewed by agencies like the SEC, particularly in the wake of the SEC’s decision to close its investigation into Uniswap Labs without enforcement. In practice, the long‑term impact of the fee switch will depend on how aggressively the DAO configures fee parameters and how the market responds to the new balance between LP returns and protocol value capture.

UNIfication: Aligning Labs, Foundation, and Tokenholders

UNIfication is more than a fee switch; it is an attempt to rationalize Uniswap’s long‑term governance, funding, and incentive structure. Announced as a joint governance proposal by Uniswap Labs and the Uniswap Foundation, UNIfication lays out a model in which protocol usage drives UNI burns while a predictable growth budget funds development and ecosystem initiatives. The key components include turning on protocol fees and channeling them into the UNI burn mechanism, directing Unichain sequencer fees to the same burn contract, performing a one‑time retroactive burn of 100 million UNI from the treasury, and establishing an annual growth budget of 20 million UNI starting in 2026.

Under this framework, Uniswap Labs focuses on building and improving the core protocol and related infrastructure, funded indirectly via grants and programs supported by the DAO’s growth budget. The Uniswap Foundation, which previously managed grants and ecosystem growth, is expected to wind down or significantly change its role as governance consolidates around this new model, although details depend on subsequent votes. The aim is to reduce overlapping structures, make funding more transparent, and tie ecosystem spending to a clear, capped issuance schedule rather than ad hoc requests. By linking the size of the growth budget to a fixed UNI amount rather than a percentage of fees, the DAO can plan expenses while letting protocol usage determine the pace of buybacks and burns.

Market analysts and community researchers have dissected the UNIfication plan in detail. Some argue that the combination of fee‑driven burns and a capped growth budget could make UNI structurally deflationary, especially if Uniswap’s volumes and Unichain activity grow substantially. Others are more cautious, noting that as UNI is burned and the circulating supply shrinks, a fixed 20 million annual issuance could represent an increasing share of the remaining supply, functioning like a “tax on success” that dilutes holders precisely when the protocol is performing well. Internal and external modeling has suggested that maintaining certain market valuations under this framework would require ambitious growth in protocol fees—for example, sustaining 30% annual fee growth over several years to justify specific price levels implied by market prices at the time of the proposal. These analyses highlight the sensitivity of UNI’s valuation to governance decisions about fee levels, burn rates, and issuance.

Despite differing views on the exact parameters, UNIfication is notable for explicitly linking the fortunes of Uniswap Labs, Unichain, and UNI holders. By routing both protocol and sequencer fees into the same burn mechanism, and by tying Labs’ funding to a DAO‑controlled UNI budget, the proposal seeks to align incentives across builders, tokenholders, and network users. Whether this alignment holds in practice will depend on execution, including how Unichain competes in a crowded layer‑2 ecosystem, how Uniswap v4’s new features attract liquidity and order flow, and how the DAO responds to market and regulatory feedback.

Experimenting with Legal Wrappers: DUNI and the Wyoming DUNA

As Uniswap’s economic and governance complexity has grown, so too has the need for clearer legal structures that can interface with off‑chain systems. One of the more innovative responses is the proposal to create “DUNI,” an in‑real‑life entity for Uniswap governance organized under Wyoming’s Decentralized Unincorporated Nonprofit Association (DUNA) statute. If adopted, this would make Uniswap Governance the largest DAO to leverage the DUNA framework, which was specifically designed to give decentralized communities a formal legal status while preserving much of their on‑chain governance structure.

The DUNA statute allows DAOs to exist as legally recognized nonprofit associations, capable of signing contracts, holding assets, and interacting with courts, while treating tokenholders as members of the association. In the context of Uniswap, DUNI would serve as a legal wrapper around the DAO, potentially providing limited liability protection for participants, clarifying tax and compliance obligations, and enabling more straightforward engagement with service providers, regulators, and counterparties. This could be particularly important as Uniswap expands into areas like tokenized real‑world assets (RWAs) and institutional partnerships, where traditional legal entities are often required to handle certain functions.

However, formalizing DAO governance in this way raises important questions. Some community members worry that creating a legal entity could centralize power or expose the DAO to new forms of regulatory oversight that conflict with its decentralized ethos. Others see it as a pragmatic step that allows Uniswap to operate at scale in a world where significant parts of finance and regulation remain off‑chain. The DUNI proposal emphasizes that on‑chain governance via UNI would remain the core decision‑making mechanism, with the legal entity implementing those decisions in the off‑chain world. How this dual structure plays out in practice—especially in relation to the SEC, CFTC, and international regulators—will be an important case study for other large DAOs considering similar paths.

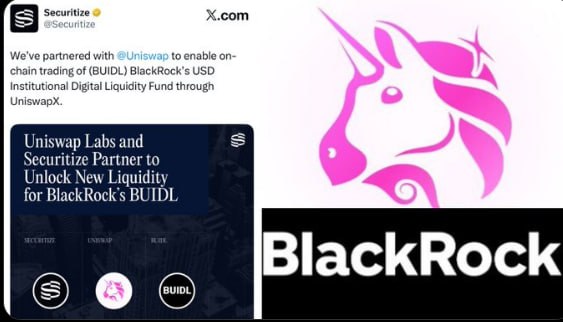

BlackRock brings its $1.8 billion tokenized Treasury fund to Uniswap and buys UNI, marking Wall Street’s first major foray into DeFi trading.

/c eth 15m

Legal and Regulatory Landscape

SEC Investigation and “Win for DeFi”

Uniswap’s regulatory status has been a focal point for the broader DeFi industry, particularly after the U.S. Securities and Exchange Commission issued a Wells Notice to Uniswap Labs alleging that the company might be operating an unregistered securities exchange, engaging in unregistered broker or clearing activity, or issuing an unregistered security through UNI. This notice signaled that the SEC’s enforcement division was seriously considering charges related to how Uniswap functions and how UNI was distributed and used. The Wells process allowed Uniswap Labs to respond with legal and factual arguments before the SEC made a final decision on whether to bring an enforcement action.

After a multi‑year investigation, the SEC ultimately decided to close the investigation into Uniswap Labs without recommending any enforcement action. In a public blog post titled “A Win for DeFi,” Uniswap Labs characterized this outcome as a significant validation of its position that the Uniswap protocol is a non‑custodial set of smart contracts and that Labs does not operate as a traditional broker, exchange, or clearing agency. The post emphasized that, by closing the case without charges, the SEC staff effectively acknowledged that Uniswap Labs is not currently violating securities laws in the ways alleged in the Wells Notice, and that the protocol and its token do not neatly fit within the categories the SEC had initially suggested.

While Uniswap Labs and much of the DeFi community interpreted this as a positive signal, it is important to recognize the limits of what the SEC’s decision means. The closure of an investigation without enforcement does not constitute a formal rulemaking, a court decision, or even a published legal interpretation; it simply means that, at this time, the Commission chose not to pursue the specific case. Future SEC leadership could revisit similar issues, perhaps under different factual circumstances or legal theories, and other regulators—both in the U.S. and abroad—may adopt different views of how DeFi protocols and tokens should be regulated. Nonetheless, the decision provides Uniswap Labs and UNI holders with some measure of relief, reducing the immediate overhang of a potentially precedent‑setting enforcement action.

Diverging Classifications: Prometheum, ETFs, and Global Access

Even as the SEC pulled back from enforcement against Uniswap Labs, other actors have taken a more expansive view of UNI’s status as a regulated asset. Prometheum Capital, which operates as a special purpose broker‑dealer for digital asset securities under SEC and FINRA oversight, launched a custody platform that includes UNI among its supported assets, alongside Ethereum, Arbitrum, Optimism, and The Graph. As part of this offering, Prometheum effectively treats UNI as a “digital asset security” subject to securities law requirements in the context of its broker‑dealer operations. While this classification is Prometheum’s interpretation rather than a formal SEC designation, it illustrates how different participants in the regulatory ecosystem may arrive at varying conclusions about the same token.

At the same time, UNI has appeared in the composition of proposed crypto index ETFs, including the Bitwise 10 Crypto Index ETF that would hold a diversified basket of major digital assets such as BTC, ETH, SOL, XRP, ADA, AVAX, LINK, BCH, DOT, and UNI.[news: Bitwise filings] The SEC has delayed decisions on these multi‑asset ETFs, reflecting both caution and the complexity of evaluating baskets that include tokens beyond Bitcoin and Ethereum. UNI’s inclusion in such proposals underscores its status as a “blue‑chip” DeFi asset in the eyes of product designers, but it also highlights regulatory challenges: if some components of an index are later deemed to be unregistered securities, the product structure may need to change. The process for approving or denying these ETFs will shape how easily traditional investors can gain exposure to UNI alongside assets like BTC, which is increasingly accessible through approved spot ETFs.

Globally, platforms like Nubank complicate the regulatory picture further. Nubank’s decision to support BTC, ETH, SOL, and UNI trading and USDC swaps for its more than 100 million customers required navigating Brazilian and regional regulations around crypto asset offerings. In many jurisdictions, DeFi governance tokens occupy a gray area between commodities, payment tokens, and securities, and regulatory frameworks are still evolving. UNI’s growing presence in bank apps, custody platforms, and prospective ETFs suggests that regulators will increasingly need to articulate coherent positions on DeFi tokens, not just on Bitcoin and Ethereum.

Governance Power and Centralization Debates

Regulation is not the only systemic risk facing UNI; governance centralization is another. On‑chain data and governance records show that a relatively small set of large holders—founding teams, early investors, specialized funds, and a handful of whales—control a significant fraction of UNI’s voting power. High‑profile episodes, such as venture firm a16z unstaking tens of millions of UNI before key votes or a Chinese fund reportedly acquiring a large UNI position ahead of governance debates, have fueled concerns that a few actors can disproportionately shape outcomes. The DAO’s decision to reclaim around 12.5 million UNI that had been loaned to external delegates, as well as its plan to re‑delegate up to 18 million UNI to a broader set of active participants, can be seen as attempts to manage these power dynamics.

The planned introduction of Unichain complicates governance further. Because Unichain is built using Optimism’s OP Stack, Uniswap Labs and the DAO must coordinate with another major ecosystem and its token, OP. Critics have argued that recent governance decisions, including aspects of UNIfication and Unichain’s design, may favor Optimism’s interests or infrastructure choices in ways that dilute direct UNI holder control. Proposals to route Unichain sequencer fees into the UNI burn mechanism and to treat UNI as the staking token for Unichain are partly intended to reassure UNI holders that the new network will enhance, rather than erode, their economic and governance position. However, the actual distribution of decision‑making power between UNI governance, Unichain validators, and Optimism’s own governance remains a subject of active discussion.

These centralization concerns intersect with regulatory risk. If regulators perceive that a handful of insiders effectively control a DAO and its token, they may be more inclined to treat the token as a security or the DAO as an unregistered issuer. Conversely, if Uniswap can demonstrate robust, broad‑based governance and legally compliant structures like DUNI, it may strengthen arguments that UNI functions more like a commodity‑like governance token for a decentralized protocol. UNI’s governance and regulatory stories are thus tightly interwoven, and both will evolve as the protocol scales and as more institutional capital and traditional financial products incorporate UNI.

UNI token launched with retroactive airdrop to historical users

Uniswap v3 launches concentrated liquidity positions

Fee switch governance debate formally opened on Uniswap forum

- 2024-05governance

Foundation sets May 31 delegation deadline for fee switch vote eligibility

SEC drops all claims against Uniswap Labs; UNI ruled not a security

DAO votes to activate fee switch with buyback-and-burn of up to 100M UNI

UNI in the Market: Pricing, Forecasts, and Trading Dynamics

Historical Performance and Volatility

UNI’s market performance has reflected both the broader crypto cycle and protocol‑specific developments. After its launch and airdrop in 2020, UNI quickly appreciated as traders and investors priced in Uniswap’s dominant position in DeFi and the novelty of a major protocol governance token. During the 2021 bull market, UNI reached high double‑digit prices in USD terms, before declining alongside the broader crypto market in subsequent drawdowns. More recently, UNI has generally traded in the single‑digit USD range, with periodic spikes tied to governance news, institutional moves, or macro‑driven rallies in the wider crypto complex. Its market capitalization has typically kept it within the top 50 crypto assets, making it liquid and widely followed by traders.

Like many altcoins, UNI tends to correlate with BTC and ETH during broad risk‑on or risk‑off phases, but its idiosyncratic news flow can drive significant deviations. Approval or delay of multi‑asset ETFs that include UNI, as well as regulatory news affecting DeFi more broadly, can trigger sharp re‑pricings. For instance, reports that the SEC had closed its investigation into Uniswap Labs without enforcement were widely seen as reducing tail risk for UNI, even if the immediate price reaction was muted. Conversely, episodes where large token holders capitulate or accumulate—on‑chain records of whales selling UNI at substantial realized losses or accumulating millions of tokens in a short period—have been interpreted by traders as sentiment signals, sometimes prompting short‑term volatility even when fundamentals are unchanged.

UNI’s liquidity is spread across centralized exchanges, Uniswap itself, and other DEXs, with deep order books and pools enabling sizable trades with relatively low slippage under normal conditions. However, during periods of extreme volatility, liquidity can fragment and spreads can widen, particularly in less liquid trading pairs. The emergence of tokenized RWAs and institutional pools on Uniswap, including BlackRock’s BUIDL fund and other on‑chain funds, introduces new sources of liquidity and demand that may affect UNI over time. As UNI becomes more integrated into structured products and institutional portfolios, its trading dynamics may gradually shift from purely speculative flows to a mix of speculative, hedging, and yield‑driven behavior.

Standard Chartered’s 100 USD Target and the RWA Thesis

One of the most discussed recent developments in UNI’s market narrative is Standard Chartered’s decision to initiate coverage of the token with a long‑term price forecast tied to the growth of tokenized real‑world assets. According to reporting on the bank’s research, Standard Chartered projects a potential trajectory in which UNI could reach 6.50 USD in 2026, 20 USD in 2027, 40 USD in 2028, 65 USD in 2029, and 100 USD by the end of 2030, contingent on a bullish scenario for RWA tokenization and DeFi adoption. The bank emphasizes that this is an analyst model rather than a guarantee, and that the path depends heavily on how quickly traditional assets like bonds, funds, and other financial products migrate on‑chain and whether decentralized exchanges like Uniswap capture a meaningful share of that flow.

The core thesis behind this forecast is that a large portion of future on‑chain trading volume could come from tokenized RWAs, representing trillions of dollars in assets, rather than from purely crypto‑native tokens. Standard Chartered reportedly cites projections of a 4 trillion USD RWA tokenization market by 2028 and argues that if Uniswap becomes a key venue for trading these assets—either directly or via permissioned pools and compliance‑layer integrations—UNI could benefit from the associated fee volume and protocol prominence. In this view, UNI’s evolving tokenomics, particularly the fee switch and the integration of Unichain sequencer fees and MEV capture, create a structural link between the token’s value and the growth of on‑chain finance beyond the current crypto ecosystem.

BlackRock’s move to list its BUIDL tokenized U.S. Treasury fund on Uniswap and to acquire UNI tokens provides a concrete example of the RWA thesis in action. BUIDL represents shares in a roughly 2 billion USD tokenized Treasury fund, and its listing on Uniswap positions the protocol as a venue where institutional‑grade, yield‑bearing RWAs can trade alongside traditional crypto assets. BlackRock’s acquisition of UNI has been interpreted by some as a strategic bet on Uniswap’s centrality to this tokenized asset future, while others caution that it could simply be a governance or hedging position. Regardless, the combination of Standard Chartered’s coverage and BlackRock’s on‑chain activity has strengthened the narrative that UNI is a key token to watch in the context of Wall Street’s gradual embrace of blockchain‑based trading.

It is important to treat such forecasts with skepticism and nuance. The 100 USD target is explicitly framed as a scenario model, not a promise, and it assumes both robust growth in the RWA tokenization market and Uniswap’s success in capturing a significant share of that market. There are many reasons why these assumptions might not fully materialize: RWAs could gravitate toward permissioned, KYC‑only platforms; regulatory regimes might limit the use of public DEXs for certain asset classes; or competing protocols could out‑innovate Uniswap in specialized market segments. Nonetheless, Standard Chartered’s coverage is notable as one of the first detailed, institutionally branded valuation frameworks for a major DeFi token, and it has contributed to renewed investor interest and price volatility in UNI when announced and updated.

Whales, Liquidity, and Market Microstructure

Beyond macro narratives and institutional coverage, UNI’s day‑to‑day market behavior is heavily influenced by on‑chain whale activity and liquidity conditions. Blockchain analytics frequently highlight wallets that make large purchases or sales of UNI within short time windows, sometimes involving tens of millions of dollars in notional value. Episodes in which a whale capitulates—selling large holdings of UNI and possibly other DeFi tokens like COMP at substantial realized losses—can be interpreted as risk‑off signals, particularly if they occur in conjunction with negative macro or regulatory news. Conversely, reports of wallets accumulating hundreds of thousands or millions of UNI within hours are often framed as bullish accumulation, although the ultimate intent of these buyers (governance influence, speculative trading, hedging) may not be fully known.

Whale flows matter not only because of their immediate price impact but also because they affect governance dynamics. UNI holdings confer voting power, and large token holders can significantly sway outcomes on proposals related to fee parameters, treasury spending, or even the creation of entities like DUNI. When major institutional players, such as BlackRock or large crypto funds, acquire UNI, they may also be positioning themselves to participate in or shape governance debates. Recent governance sagas, including the DAO’s efforts to reclaim loaned UNI and to delegate treasury tokens to a curated set of active delegates, can be seen as attempts to manage and channel whale influence rather than eliminate it entirely.

From a microstructure perspective, the advent of Unichain and potential future integrations with order flow auctions and MEV‑aware routing could change how UNI and other tokens trade on Uniswap. If Unichain centralizes a significant portion of DeFi trading activity, including trades in UNI itself, then block builders and searchers on that network will play a larger role in determining trade execution, spreads, and slippage. This could make UNI’s liquidity more resilient in some scenarios but may also introduce new forms of complexity as market participants adjust to a MEV‑aware, cross‑domain trading environment. For now, UNI remains one of the more liquid DeFi tokens, but its future trading dynamics will be shaped by both human decisions in governance and algorithmic behavior in MEV markets.

Integrations with CeFi and TradFi

UNI’s growing presence in centralized finance (CeFi) and traditional finance (TradFi) channels is a key part of its long‑term story. In addition to institutional funds and ETF proposals, retail‑focused platforms like Nubank illustrate how UNI can reach users who do not self‑custody crypto or interact directly with DEXs. Nubank’s crypto product now allows customers to swap between BTC, ETH, SOL, and UNI and USDC with reduced fees, and to earn a fixed annual return on USDC holdings, effectively using these assets as entry points into digital dollar savings and trading. By placing UNI alongside BTC and ETH in a mainstream banking app, Nubank signals that it views Uniswap’s token as part of a core set of crypto assets relevant to everyday users in Latin America.

On the institutional side, regulated custody from firms like Prometheum, and UNI’s inclusion in baskets like the Grayscale DeFi Fund, make it easier for funds, corporates, and high‑net‑worth individuals to gain exposure without needing to manage private keys or account for on‑chain governance themselves. These products often treat UNI as a component of a broader DeFi or crypto theme, diversified across several tokens, which can dampen idiosyncratic volatility while still exposing investors to the sector’s growth. At the same time, they can also propagate regulatory interpretations: if a major custodian treats UNI as a security, for example, that may influence how other financial institutions classify and handle the token.

These integrations also tie UNI more closely to Bitcoin and other large‑cap assets in investor portfolios. When BTC rallies on macro news—such as rate cut expectations or ETF approvals—cross‑asset flows often lift altcoins like UNI, especially if they are components of the same index products. Conversely, when BTC suffers sharp drawdowns, forced deleveraging and risk‑off positioning can lead to heavier percentage losses in UNI as investors rotate into perceived “safer” assets. Over time, as UNI’s fee capture, staking returns, and RWA exposure become more concrete, its correlation profile with BTC may evolve, but for now it remains part of the broader crypto beta complex.

Unichain, MEV, and the Future Utility of UNI

What Is Unichain?

Unichain is Uniswap’s planned DeFi‑centric scaling solution, designed as a dedicated layer‑2 network built on Ethereum using Optimism’s OP Stack and integrated with the Flashbots block builder infrastructure. Its stated goal is to serve as a universal liquidity hub for financial applications, providing faster transactions and lower fees while preserving the security and composability of the Ethereum base layer. By leveraging the OP Stack, Unichain inherits a battle‑tested rollup architecture and plugs into Optimism’s broader “Superchain” vision, where multiple rollups share infrastructure and liquidity while maintaining their own governance and economics.

The design of Unichain reflects Uniswap’s ambition to move beyond being just a protocol deployed on external chains to operating its own execution environment tailored to DeFi’s needs. In principle, a dedicated L2 allows Uniswap to optimize block production, transaction ordering, and data availability for trading and liquidity provision use cases, potentially improving slippage, latency, and MEV mitigation compared to general‑purpose L2s. It also provides a native platform on which Uniswap v4 and other DeFi primitives can run with more predictable performance, making it easier to experiment with advanced order types, hooks, and cross‑pool routing strategies. The testnet for Unichain launched in October, with a mainnet launch targeted for a subsequent period, and community materials emphasize that UNI will be integral to Unichain’s validation and fee distribution mechanisms.

UNI as a Staking and Validation Asset

A core innovation of Unichain is its “Unichain Validation Network,” which will use UNI as the staking asset for validators who help secure the network and sequence transactions. In this model, UNI holders will be able to delegate or stake their tokens to validators, who in turn will earn sequencer fees generated by transaction activity on Unichain. These fees, after covering Ethereum data costs and fulfilling a 15% revenue share obligation to Optimism, will feed into the same UNI burn mechanism established for Uniswap protocol fees. This arrangement creates a feedback loop: higher transaction volumes on Unichain generate more sequencer fees, increasing both staking rewards and the pace of UNI burns, which could, in theory, support UNI’s price and incentivize further staking and usage.

This staking role marks a significant expansion of UNI’s function. Whereas Ethereum’s ETH and other base‑layer tokens secure their networks through proof‑of‑stake, UNI has historically not been used to secure consensus or validation in any network. By making UNI the staking token for Unichain, Uniswap effectively transforms UNI into a security‑critical asset, whose distribution and governance directly affect the safety and performance of the layer‑2. This change brings both opportunities and risks. On the opportunity side, UNI holders can earn on‑chain yields tied to real network usage, potentially making UNI more attractive to long‑term investors and less purely speculative. On the risk side, validator centralization, slashing conditions, and cross‑chain bridge security become more salient, and any major exploit or censorship issue on Unichain could feed back into UNI’s perceived value.

The precise mechanics of staking—such as lock‑up periods, delegation models, slashing rules for misbehavior, and the interplay between staked and liquid UNI in governance—will be determined through governance and technical design decisions. Balancing security, decentralization, and economic efficiency will be crucial. If staking rewards are too low, few holders may lock their tokens, compromising decentralization; if they are too high, UNI’s inflation and burn dynamics might become unstable. Because Unichain also sits within Optimism’s broader ecosystem, coordination between UNI and OP holders and governance systems may also be needed to align incentives and avoid conflicts.

MEV Capture and Revenue Sharing

Maximal extractable value has become a central topic in blockchain economics, and Uniswap is one of the largest sources of MEV opportunities because its pools and routers intermediate a large fraction of on‑chain trading volume. MEV arises when block builders or validators can profit from arbitrage, liquidations, or sandwiching strategies by reordering or inserting transactions. Historically, much of this MEV has been captured by searchers and validators rather than by the protocols that generate the underlying transaction flow. Uniswap’s roadmap, particularly in the context of Unichain, aims to change that by integrating MEV capture into protocol‑level mechanisms that can direct a share of this value back to users and tokenholders.

Recent estimates suggest that MEV associated with Uniswap may amount to roughly 10% of the total fees paid on the protocol, or approximately 100 million USD over a recent one‑year period. If even a portion of this value can be captured through protocol‑integrated order flow auctions, MEV‑aware routing, or collaborative mechanisms with block builders like Flashbots, it represents a substantial new revenue stream. Governance discussions have floated the idea that some of this captured MEV could be routed into the same token jars that fund UNI burn and buyback, while other portions could be used to subsidize traders or enhance LP yields. In the context of Unichain, where Uniswap has more control over the sequencing and settlement environment, it may be easier to implement sophisticated MEV policies that are hard to coordinate across multiple independent L1s and L2s.

How MEV is shared among stakeholders will have important implications for UNI. If UNI holders receive a meaningful share of MEV‑funded burns or staking rewards, UNI’s value may become more tightly correlated with trading intensity and arbitrage activity. If most MEV is used to improve user experience—through better execution prices or lower net fees—UNI holders may benefit more indirectly via higher protocol adoption and competitive positioning. In either case, Uniswap’s approach to MEV, and the decisions made by UNI governance around it, will help determine whether UNI evolves into a token whose value is primarily tied to governance symbolism or one that is underpinned by measurable, diversified cash‑flow‑like streams from fees, sequencer revenue, and MEV.

$UNI jumps 40% on announcements Blackrock is buying

Good for $uni holders..need my own bags to pump

Uniswap v4's hook architecture materially expands the composable attack surface relative to v3, and oracle lag during UNI volatility has already produced $3M in protocol bad debt across connected lending markets.

Uniswap Labs has unilaterally redirected governance rights toward Optimism, controls interface fee monetisation, and is positioning to capture v4 order flow revenue without token-holder consent, making on-chain governance votes structurally advisory.

The SEC formally dropped its broker, exchange, and security claims against Uniswap Labs, but Prometheum has independently classified UNI as a security within its custody platform, leaving legal status contested at the infrastructure layer.

- LiquidityMedium

UNI's use as collateral in Compound and Aave means sharp price dislocations propagate cross-protocol: a single UNI liquidity crunch triggered AaveDAO to cut stablecoin borrowing power across the board, demonstrating systemic contagion risk.

The UNIfication plan's fixed 20M-UNI annual budget becomes a rising dilution tax as price appreciates, and the $9 market price at proposal time implied sustaining 30% fee growth for five consecutive years to justify fair value.

Risks, Critiques, and Open Questions

Governance and Decentralization Trade‑offs

Despite Uniswap’s reputation as a decentralized protocol, governance risks remain front and center for UNI. Token distribution is skewed toward early participants, investors, and large funds, and even with delegation programs, many UNI holders do not actively participate in voting. This raises concerns that a relatively small group of technically sophisticated or capital‑rich actors—venture capital firms, specialized DAOs, or whales—may effectively control key decisions, from fee parameters to treasury spending and network design. Events like the DAO’s decision to reclaim previously loaned UNI from delegates show both the risks of concentrated power and the community’s attempts to rebalance it. However, such actions can also be controversial, especially if affected delegates argue that they were fulfilling their mandates or that sudden changes undermine governance continuity.

The introduction of Unichain adds further complexity. Because Unichain relies on Optimism’s OP Stack and participates in a broader “Superchain” ecosystem, certain decisions about its architecture and cross‑chain interactions may involve governance processes beyond UNI holders’ direct control. Critics have expressed concern that Uniswap Labs and Optimism’s governance could strike arrangements that favor the OP token or centralize operational control in ways that are not fully transparent to UNI holders. The UNIfication proposal’s promise to direct Unichain sequencer fees into UNI’s burn mechanism and to use UNI for staking is partly a response to these concerns, but the balance of influence between the Uniswap DAO, Unichain validators, and Optimism’s institutions will only become clear over time.

The creation of DUNI under the Wyoming DUNA statute may mitigate some risks by giving the DAO a legal voice and framework, but it may also introduce new tensions between on‑chain votes and off‑chain legal obligations. For example, if an on‑chain vote directs DUNI to pursue an action that conflicts with regulatory requirements or fiduciary duties defined in the DUNA framework, whose decision prevails? These kinds of questions are new territory not only for Uniswap but for DAOs generally. UNI holders, especially large ones, will need to weigh not just the economic implications of proposals but their institutional and legal ramifications.

Regulatory Uncertainty

The SEC’s decision to close its investigation into Uniswap Labs without enforcement has been widely celebrated in DeFi circles, but it does not eliminate regulatory risk for UNI. Future SEC leadership could adopt a more aggressive posture toward DeFi or reinterpret existing facts under different legal theories. Other U.S. agencies, such as the CFTC, FinCEN, or state regulators, may also assert jurisdiction over aspects of Uniswap’s activity, particularly if RWAs and more traditional financial products are increasingly traded via the protocol. International regulators may take divergent approaches; what is acceptable in Brazil, where Nubank offers UNI to retail customers, may not be acceptable in the EU or in certain Asian jurisdictions.

Prometheum’s classification of UNI as a digital asset security within its broker‑dealer framework underscores that some regulated entities are already treating UNI as if it were a security, even absent a formal SEC pronouncement. If more brokers, custodians, or exchanges follow suit, UNI may become subject to a patchwork of compliance regimes that complicate its listing and trading. On the other hand, broader inclusion in regulated products, such as the Bitwise 10 Crypto Index ETF or other multi‑asset funds that include BTC, ETH, and UNI, could also normalize UNI as an investable asset and drive demand, depending on how these products are ultimately approved and structured.[news: Bitwise filings]

As UNI’s tokenomics evolve—particularly with fee capture and staking—it may draw closer scrutiny under securities law frameworks that focus on expectations of profit from the efforts of others. Uniswap’s governance design, the decentralized nature of its protocol, and legal wrappers like DUNI will all play a role in determining how regulators ultimately view the token. UNI holders should therefore consider regulatory outcomes as a key risk factor, alongside technical and market risks.

Economic Sustainability and Competition

Finally, UNI’s long‑term value depends on whether Uniswap can maintain and extend its competitive edge in a rapidly evolving DeFi landscape. Competitors are experimenting with alternative AMM designs, order book models, cross‑chain liquidity systems, and aggressive token incentives. If Uniswap’s fee switch reduces LP returns too far or if Unichain fails to attract sufficient activity, liquidity and users may migrate to rival platforms. Conversely, if Uniswap’s brand, depth of liquidity, and integration with RWAs and institutional flows prove decisive, it may continue to dominate DeFi volumes and make UNI’s fee burn and staking economics attractive.

The Standard Chartered forecast for UNI, while optimistic, implicitly assumes that Uniswap will capture a meaningful share of a multi‑trillion‑dollar RWA market. This outcome is far from guaranteed. RWAs may gravitate toward permissioned, KYC‑only networks run by consortia of banks and custodians, with limited use of public DEXs. Regulatory constraints may limit which assets can trade on protocols like Uniswap and under what conditions. And even within DeFi, liquidity may fragment across multiple specialized DEXs, each optimized for different asset classes or trading styles. In such a world, UNI’s value would be determined more by Uniswap’s share of crypto‑native trading and the success of Unichain than by RWA flows.

The UNIfication tokenomics, with their combination of growth budget, fee burns, and sequencer fee integration, represent a bold attempt to craft a sustainable economic model that aligns builders, tokenholders, and users. Whether this model proves sustainable or requires substantial revision will depend on empirical results: how much fee and MEV revenue is actually generated, how aggressively UNI is burned, how developers and projects respond to Unichain, and how regulators treat the protocol. The risk is that miscalibration—too much issuance, too little fee capture, or misaligned incentives—could undermine UNI’s value, even if Uniswap remains widely used at the protocol level.

Conclusion

UNI has traveled a long way from its origins as a retroactive airdrop and a simple governance token for an experimental automated market maker. It now anchors the governance, economics, and—soon—security of one of the most important pieces of DeFi infrastructure. The activation of the fee switch and the adoption of the UNIfication roadmap mark a fundamental shift in how Uniswap captures and distributes value, tying UNI’s supply to trading fees, Unichain sequencer revenue, and potentially MEV, while introducing a predictable but non‑trivial growth budget funded by new issuance. Institutional developments, from BlackRock’s BUIDL listing and UNI purchases to Standard Chartered’s long‑term valuation model and the inclusion of UNI in Grayscale funds and proposed ETFs, signal that UNI has become a central asset in the conversation about how traditional finance will intersect with DeFi.

At the same time, UNI remains exposed to significant uncertainties. Governance remains concentrated among large holders and key institutions, and the introduction of Unichain and DUNI will test the DAO’s ability to coordinate complex technical, economic, and legal decisions. Regulatory risk is far from resolved, despite the SEC’s decision to close its investigation into Uniswap Labs without enforcement, as divergent interpretations like Prometheum’s classification of UNI as a digital asset security illustrate. Economic competition is intense, with rival DEXs and layer‑2s vying for liquidity, order flow, and RWA integrations, and UNI’s tokenomics will need to prove themselves in a live environment rather than in theoretical models.

For a crypto‑news audience, UNI is likely to remain one of the most important tokens to watch—not just for its price action, but as a barometer of how DeFi protocols are governed, how they capture value, how they interact with regulators, and how they interface with the traditional financial system. Whether Standard Chartered’s 100 USD scenario ever materializes is less important than the underlying question it poses: can a decentralized exchange token evolve into a durable, cash‑flow‑linked asset at the heart of a multi‑trillion‑dollar on‑chain economy? UNI’s next chapters—shaped by Unichain’s launch, ongoing governance battles, and the global regulatory response—will go a long way toward answering that question.

Outlook

Looking ahead, UNI’s trajectory will hinge on a few key developments. The rollout and adoption of Unichain will test whether a DeFi‑specific layer‑2, secured and governed by UNI, can attract enough activity to meaningfully augment fee and MEV‑driven burns and staking yields. The implementation details of the fee switch and MEV capture mechanisms will determine whether UNI becomes structurally deflationary, as some analysts suggest, or whether the growth budget behaves more like a persistent tax on holders. Regulatory outcomes, including decisions on multi‑asset ETFs that include UNI and evolving guidance on DeFi tokens, will shape how easily mainstream investors can access UNI alongside BTC and ETH and how issuers structure products around it.[news: Bitwise filings]

On the adoption side, the extent to which RWAs migrate to public chains and, crucially, to Uniswap‑based venues will be a central driver of UNI’s long‑term narrative, particularly in light of institutional moves from BlackRock and Standard Chartered’s RWA‑driven valuation thesis. Meanwhile, integrations with platforms like Nubank and the continued inclusion of UNI in institutional products such as the Grayscale DeFi Fund suggest that, regardless of market cycles, UNI is likely to remain a core DeFi exposure for both retail and professional investors. For now, UNI should be understood as a high‑beta, governance‑driven asset whose value is tightly coupled to the success of Uniswap’s evolving protocol stack, the robustness of its DAO, and the broader experiment of bringing financial markets on‑chain.

Latest UNI news

Uniswap DAO voted to activate its long-awaited fee switch, redirecting a portion of protocol revenue into a buyback-and-burn mechanism that could destroy up to 100M UNI (~$600M), while Uniswap Labs stops interface fees and the Foundation winds down.BlackRock brings its $1.8 billion tokenized Treasury fund to Uniswap and buys UNI, marking Wall Street’s first major foray into DeFi trading.$UNI jumps 40% on announcements Blackrock is buying Cryptocondom Intern research suggests the UNI fee switch will make it deflationary

Cryptocondom Intern research suggests the UNI fee switch will make it deflationary Uniswap’s UNIfication plan risks turning a fixed 20M-UNI annual budget into a rising “tax on success,” diluting value as UNI grows and treasury burns tighten supply.

Uniswap’s UNIfication plan risks turning a fixed 20M-UNI annual budget into a rising “tax on success,” diluting value as UNI grows and treasury burns tighten supply. Analysis of Uniswap's UNification plan suggests the market pricing of $9 requires sustaining 30% fee growth over the next 5 years

Analysis of Uniswap's UNification plan suggests the market pricing of $9 requires sustaining 30% fee growth over the next 5 yearsSources

- https://coinmarketcap.com/currencies/uniswap/

- https://www.findas.org/tokenomics-review/coins/the-tokenomics-of-uniswap-uni/r/581DwifCMJFX7eLsofUR56

- https://castlerock.org/uniswap-decentralized-exchange-core-features-and-how-they-work-2/

- https://www.dlnews.com/articles/defi/uniswap-dao-votes-to-take-back-loaned-uni-tokens/

- https://gov.uniswap.org/t/brief-thoughts-on-how-the-dao-could-grow/24749

- https://gov.uniswap.org/t/layer-2-is-upon-us-back-to-discussing-the-fee-switch/13419

- https://developers.uniswap.org/docs/protocols/v4/concepts/v4-vs-v3

- https://gov.uniswap.org/t/the-uni-token-and-its-future/16044

- https://www.tradingview.com/news/newsbtc:ee2c4ba0d094b:0-standard-chartered-sees-uniswap-rising-to-100-by-2030-on-rwa-growth/

- https://www.kavout.com/market-lens/what-does-blackrock-s-uniswap-move-signify-for-defi

- https://www.dlnews.com/articles/defi/uniswap-dao-to-activate-fee-switch-and-burn-100m-uni-tokens/

- https://blog.uniswap.org/unification

- https://x.com/JustDeauIt/status/1845565893050270134

- https://blog.uniswap.org/a-win-for-defi

- https://uniswapfoundation.org/blog/duni-an-irl-entity-for-uniswap-governance

- https://www.21shares.com/en-us/insights/newsletter-issue-246

- https://x.com/Grayscale/status/1942337972315292127

- https://www.prometheum.com/press-releases/prometheum-capital-launches-its-custody-platform-for-digital-asset-securities

- https://international.nubank.com.br/consumers/nubank-expands-usdc-rewards-program-to-all-customers/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…