Deep dive on VanEck’s role in crypto, covering its Bitcoin and BNB ETFs, Solana and Avalanche products, tokenized VBILL fund, DeFi and Avalanche partnerships, and research shaping institutional access to digital assets.

+10 sources across the wider coverage universe

Bitwise locks in 0.67% fee and BHYP ticker for Hyperliquid ETF as Grayscale, VanEck chase HYPE exposure2026-04

Bitwise locks in 0.67% fee and BHYP ticker for Hyperliquid ETF as Grayscale, VanEck chase HYPE exposure2026-04 Blockworks launches the Transparency Alliance with Coinbase, Kraken, Ripple, and VanEck to standardize token disclosures ahead of looming US crypto regulation2026-05

Blockworks launches the Transparency Alliance with Coinbase, Kraken, Ripple, and VanEck to standardize token disclosures ahead of looming US crypto regulation2026-05 VanEck launches the first US spot BNB ETF, giving investors regulated exposure to Binance-linked BNB through physically backed exchange-traded shares2026-05

VanEck launches the first US spot BNB ETF, giving investors regulated exposure to Binance-linked BNB through physically backed exchange-traded shares2026-05 VanEck's VBILL Treasury fund goes live on Euler as tokenized collateral for DeFi loans2026-05

VanEck's VBILL Treasury fund goes live on Euler as tokenized collateral for DeFi loans2026-05 VanEck pitches BNB's $160M revenue and 33M monthly users as VBNB ETF edge2026-06

VanEck pitches BNB's $160M revenue and 33M monthly users as VBNB ETF edge2026-06 VanEck publishes 2050 price predictions for Bitcoin...

Bear - $130k

Base - $2.9m

Bull - $52.3m (give me whatever they are smoking plz)2024-07

VanEck publishes 2050 price predictions for Bitcoin...

Bear - $130k

Base - $2.9m

Bull - $52.3m (give me whatever they are smoking plz)2024-07

VanEck and Crypto: How a Traditional Asset Manager Became a Key Player in Digital Assets

VanEck is a long‑standing global asset manager best known for commodity and gold funds that has become one of the most aggressive traditional finance firms pushing into bitcoin, altcoin ETFs, tokenized funds, and on‑chain products. By combining regulated exchange‑traded vehicles with DeFi integrations and research-heavy macro views on Bitcoin and other networks, it now sits at the center of how institutional and retail capital access crypto markets.

VanEck’s Evolution: From Gold Specialist to Digital Asset Gatekeeper

VanEck’s crypto story makes more sense when you understand its roots in commodities and hard assets. For decades the firm built its brand around giving investors exposure to difficult‑to‑access markets such as gold, natural resources, and emerging markets, often via specialized mutual funds and ETFs. In its own marketing, VanEck emphasizes that it has historically been “at the forefront of gold investing,” positioning itself as comfortable operating at the frontier of new asset classes where infrastructure, regulation, and investor understanding are still developing. That positioning created a natural bridge to Bitcoin, which many early adopters framed as “digital gold” and as a hedge against monetary debasement.

As crypto markets matured, VanEck increasingly presented digital assets as a new asset class that could sit alongside commodities inside diversified portfolios. The firm’s educational materials on “crypto investing” are explicitly designed to help investors understand Bitcoin, cryptocurrencies and other digital assets, as well as the portfolio role they might play. That combination of explanatory content and product launches is a familiar playbook from commodity ETFs, where VanEck and peers had to teach investors about underlying markets before those funds could scale. From the start, the firm’s messaging has stressed long‑term adoption rather than speculative trading, which resonates with both institutional allocators and retail investors looking for regulated access.

Crucially, VanEck also chose to compete on first‑mover status in U.S. and European regulation. It describes itself as the first established ETF issuer to file in the United States for both a Bitcoin‑linked ETF and a spot ether ETF, underscoring a willingness to test the boundaries of what the Securities and Exchange Commission (SEC) would allow. In practice, that meant multiple years of filings, amendments, and rejections before spot Bitcoin ETFs were finally approved, but it also cemented the firm’s reputation as one of the issuers most committed to bringing crypto under the ETF umbrella. That reputation is now central to its brand in digital assets.

The firm’s internal culture around crypto has also been carefully signaled to the market. When U.S. spot Bitcoin ETFs were finally approved, VanEck’s CEO Jan van Eck marked the moment with the line “We celebrate Bitcoin builders – not tourists,” framing the firm as aligned with long‑term protocol contributors rather than short‑term price chasers. That public stance matters because it differentiates VanEck from issuers that treat Bitcoin and altcoins as just another product line, and it helps explain why the firm has committed a share of profits from some products to ecosystem development. In short, VanEck is trying to look less like a late‑cycle tourist and more like a “crypto‑native” ally from traditional finance.

Notably, the firm’s move into digital assets has not been limited to a single jurisdiction or product type. In Europe, VanEck has leaned heavily on exchange‑traded products (ETPs) and exchange‑traded notes (ETNs) tied to specific coins like Bitcoin, ether, Solana, Avalanche and others. In the United States, where the regulatory regime is stricter and more fragmented, it has focused on fully registered ETFs and trusts that hold Bitcoin and, more recently, Binance’s BNB token. This multi‑jurisdiction, multi‑structure strategy reflects a view that crypto adoption will not unfold uniformly, and that a global asset manager must be willing to meet regulators where they are.

Taken together, VanEck has repositioned itself from a commodity‑focused specialist into a broader access provider for scarce or complex assets, with crypto now one of the most important frontiers. Its credibility in gold and emerging markets gives institutional allocators a familiar counterparty as they move into digital assets, while its willingness to experiment with tokenization and DeFi integrations appeals to a more crypto‑native audience. That dual identity explains why VanEck has become a central name in stories about Bitcoin ETFs, altcoin ETPs, the tokenization of Treasuries, and on‑chain payment experiments.

Bitwise locks in 0.67% fee and BHYP ticker for Hyperliquid ETF as Grayscale, VanEck chase HYPE exposure

0.67% fee with 85% staking pass-through sounds competitive until you consider that the ETF's Anchorage-delegated stake could dominate an active set of just 24 validators — that's a centralization vector nobody's pricing in. Only 27% of HYPE supply is circulating right now, so four issuers racing to launch spot exposure against that float is going to create some wild supply dynamics once AUM starts stacking. Bitwise already soft-launched the staking ETP on Xetra two days ago, which means they're battle-testing custody and staking infra in production before the SEC even signs off — smart sequencing given how many crypto ETF launches have fumbled the operational side.

Readers use VanEck filings as a real-time radar for which assets are next in line for TradFi legitimization — each S-1, 8-A, or Delaware trust registration is clicked not for the fund itself but as a signal that an asset class is being institutionally de-risked.↗

Building the Bitcoin Franchise: HODL, On‑Chain Research, and Macro Theses

The HODL Spot Bitcoin ETF: Structure and Purpose

VanEck’s flagship crypto product in the United States is its spot Bitcoin ETF, branded under the memorable ticker HODL. The fund is structured as a passive investment vehicle designed to hold Bitcoin directly and track the asset’s price, offering investors regulated exposure without the need to manage private keys, navigate exchanges, or worry about self‑custody and on‑chain operations. According to the fund documentation, the trust does not seek to generate returns beyond simply reflecting Bitcoin’s market price, which means it does not use leverage, derivatives, or yield‑enhancing strategies. This plain‑vanilla approach aligns with SEC expectations for commodity‑style ETPs and helps distinguish HODL from more complex structured products.

As of mid‑2026, HODL had grown to more than one billion dollars in net assets, with total net assets reported at roughly 1.03 billion dollars. The share price around that time was quoted at 17.74 dollars, reflecting Bitcoin’s price over the relevant measurement period, and performance data showed that investors had experienced a drawdown of more than 25 percent over a specified period despite the fund’s growth in assets. Those numbers illustrate two important dynamics. First, the ETF wrapper did not insulate investors from Bitcoin’s volatility; HODL moves up and down with the underlying market. Second, large asset growth alongside negative recent returns indicates that investors have been willing to allocate capital even in less bullish market conditions, reinforcing the “long‑term thesis” narrative VanEck emphasizes.

Operationally, HODL functions like other physically backed commodity ETFs. Authorized participants create and redeem ETF shares in large blocks by delivering or receiving Bitcoin, with a regulated custodian holding the underlying coins on behalf of the trust. VanEck’s materials stress that the fund’s objective is price tracking rather than active trading, implying that portfolio turnover is limited to creation/redemption activity and any operational rebalancing. For many investors, this provides a compromise between self‑custodied Bitcoin – which offers sovereignty but requires technical expertise and security practices – and exposure via derivatives like futures, which introduce basis risk and potential roll costs.

One of the interesting market‑structure consequences of spot Bitcoin ETFs, including HODL, is the way they re‑channel demand for Bitcoin into traditional brokerage and retirement accounts. Rather than opening accounts at crypto exchanges, many investors can simply buy or sell the ETF through existing platforms, potentially broadening the investor base. Although daily flow data are volatile, there have been periods where the broader U.S. spot Bitcoin ETF complex recorded net outflows while HODL booked net inflows, suggesting that certain investor cohorts may prefer VanEck’s product based on fees, brand, or distribution channels. Over time, the aggregate Bitcoin holdings of such funds can become systemically significant for the asset’s supply‑demand dynamics, especially given the fixed supply schedule of Bitcoin itself.

Bitcoin ChainCheck: On‑Chain Signals and Market Health

VanEck has not limited its Bitcoin franchise to product issuance; it has also invested in on‑chain and macro research that informs both its own positioning and public narratives. In a mid‑March 2026 “Bitcoin ChainCheck” note, the firm highlighted that selling by long‑term holders appeared to be slowing, which it interpreted as a potentially constructive signal for the market’s medium‑term outlook. The same analysis observed that on‑chain transfer volumes had declined month‑over‑month across every age cohort of coins, indicating a generalized slowdown in spending activity. For VanEck, such patterns suggest that “strong hands” may be re‑accumulating or simply holding through volatility, which historically has often preceded new uptrends.

These ChainCheck reports blend blockchain data – such as coin age distributions, realized capitalization measures, and transfer volumes – with ETF flow information and macro indicators like interest rates and liquidity conditions. By publishing them under the VanEck brand, the firm attempts to translate complex on‑chain analytics into a language that portfolio managers and investment committees already use. This serves two purposes. First, it helps justify Bitcoin allocations not just on speculative grounds but as part of a data‑driven thesis about network adoption and investor behavior. Second, it positions VanEck as more than a product factory; it becomes an interpreter of crypto‑native data for traditional capital allocators.

On‑chain analytics also connect directly to ETF flows in feedback loops. If ChainCheck suggests that long‑term holders are distributing coins into ETF demand, one might infer that regulated products like HODL are gradually internalizing an increasing share of Bitcoin’s free float. Conversely, if on‑chain data show renewed accumulation among long‑term holders while ETFs see outflows, analysts might infer that wealth is migrating from brokerage accounts to self‑custody. VanEck’s decision to publicly track these metrics underscores its belief that Bitcoin’s maturation can and should be measured using a blend of crypto‑native and traditional indicators.

Exuberant Long‑Term Targets: One Million and Beyond

Perhaps the most headline‑grabbing aspect of VanEck’s Bitcoin research has been its aggressive long‑term price scenarios. In one widely discussed forecast, the firm suggested that Bitcoin could reach one million dollars per coin within five years, presenting that level as its “base case” outcome based on an adoption‑curve framework. That analysis, summarized by the Bitcoin Foundation, argued that Bitcoin’s role as a global store of value and its increasing penetration among younger generations could support such a trajectory. Importantly, VanEck framed the projection not as a guarantee but as the central scenario in a distribution of potential outcomes, with both lower and higher paths possible depending on regulatory, technological, and macroeconomic developments.

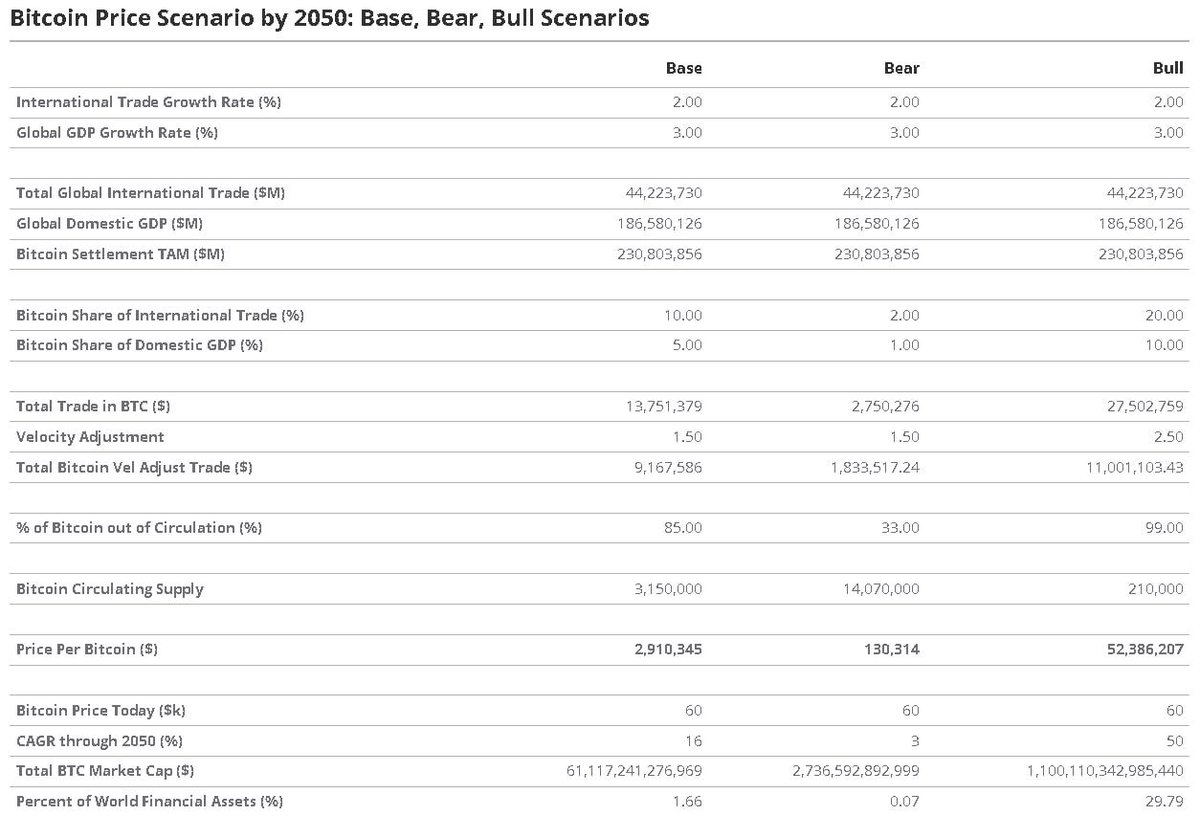

In a separate, more formal capital market assumptions report, VanEck modeled Bitcoin out to 2050 and arrived at a base‑case valuation of roughly 2.9 million dollars per coin by that year. From prevailing prices at the time of publication, that implied an expected compound annual growth rate of about 15 percent, which the firm argued could make Bitcoin competitive with, or superior to, many traditional asset classes on a risk‑adjusted basis. The report tied these projections to assumptions about Bitcoin’s eventual share of global financial wealth, its role as a “digital gold,” and its diversification properties relative to equities and bonds. While the numbers are striking, the more significant point for institutional investors is that a major asset manager is explicitly embedding Bitcoin into the same capital market modeling frameworks used for stocks and bonds.

Such forecasts serve multiple functions. They obviously help market VanEck’s products to investors seeking high‑growth opportunities, but they also provide a conceptual bridge for fiduciaries who must justify allocations in terms of expected returns, volatility, and correlations. By articulating a structured long‑term thesis, VanEck effectively argues that Bitcoin is not just a speculative bet but a macro asset that belongs in strategic asset allocation models. At the same time, the firm typically emphasizes the inherent uncertainty of these projections and the importance of sizing positions appropriately given Bitcoin’s volatility and regulatory risk.

Government Bitcoin Mining and the Institutionalization of Hashrate

Beyond price targets and ETF flows, VanEck has explored how Bitcoin’s mining ecosystem intersects with geopolitics, energy markets, and state behavior. In a research piece summarized by CryptoRank, the firm revealed that at least thirteen national governments were already engaged in Bitcoin mining activities, signifying a shift from being passive observers of the network to active participants. Although the specific countries were not enumerated in the summary, the key takeaway is that sovereign entities now see Bitcoin mining as sufficiently important – whether for economic, strategic, or energy‑management reasons – to warrant direct involvement.

This trend has several implications. First, it further undermines the narrative that Bitcoin is purely an adversarial technology vis‑à‑vis states; instead, some governments are experimenting with using the protocol as a buyer of last resort for stranded or surplus energy. Second, state participation in mining may change the political calculus around heavy‑handed regulation or bans. If government‑linked entities are accumulating mining revenue or even BTC reserves, their incentives may align more with supporting network stability than suppressing it. VanEck’s decision to highlight these developments reflects its broader thesis that Bitcoin is becoming entangled with real‑world energy systems and fiscal strategies, making it harder to dismiss as a fringe asset.

For ETF investors, state mining participation is not an immediate pricing input, but it contributes to a broader story about Bitcoin’s durability and integration into global systems. An institution deciding whether to allocate to HODL or a competing Bitcoin fund may take comfort from evidence that governments are no longer uniformly hostile. Conversely, skeptics may worry about centralization of hashrate or the potential for governments to wield outsized influence in certain mining‑heavy regions. VanEck’s research does not settle those debates, but by surfacing the issue it helps frame Bitcoin as an increasingly political – not just technological – asset.

Beyond Bitcoin: Ethereum, Solana, Avalanche and the “Onchain Economy”

Early Ether Filings and the Onchain Economy ETF

VanEck’s push beyond Bitcoin began with Ethereum and the broader “onchain economy” theme. The firm emphasizes that it was the first established ETF issuer to file for a spot ether ETF in the United States, again aiming to secure first‑mover advantage in a new segment of the market. Ether occupies a distinct position relative to Bitcoin: while Bitcoin is increasingly viewed as digital gold, ether is usually framed as the fuel of a programmable smart‑contract platform that supports DeFi, NFTs, and other decentralized applications. For an asset manager, that creates an opportunity to offer differentiated exposure that tracks not only macro narratives but also the growth of on‑chain usage and transaction fees.

Alongside direct ETH exposure, VanEck launched an Onchain Economy ETF that takes a more traditional approach: rather than holding tokens, it invests in publicly traded companies that derive a significant share of their business from digital assets and blockchain technology. This actively managed fund gives investors indirect crypto exposure through equities such as exchanges, mining firms, infrastructure providers, and fintech companies that are building on or integrating blockchains. By structuring the fund as an equity ETF rather than a token ETP, VanEck sidesteps some of the regulatory challenges around holding digital assets directly, particularly in the U.S. market where securities law treatment of many tokens remains contested.

From a portfolio‑construction perspective, the Onchain Economy ETF can compliment direct coin exposure by offering a different risk and return profile. Equity prices incorporate not only crypto market cycles but also company‑specific execution, regulatory risk, and broader stock market dynamics. VanEck’s choice to manage this ETF actively reflects a belief that there is alpha to be captured by selecting winners and avoiding losers in a fast‑moving industry. It also mirrors earlier commodity strategies, where the firm offered both physical‑backed products and equity funds targeting miners and related companies, giving investors multiple ways to express a theme.

Solana ETPs and the Path Toward Staking‑Based ETFs

Solana has become another focal point for VanEck’s multi‑asset crypto lineup. In Europe, the firm launched a spot Solana ETP in November 2025, giving investors direct exposure to SOL, the network’s native asset, via regulated exchanges. ETPs of this kind typically hold the underlying token in custody and issue exchange‑traded certificates or notes to investors, who thereby avoid dealing with wallets and self‑custody while still tracking SOL’s price. For many European investors, ETPs have become the default way to gain crypto exposure in regulated accounts, mirroring the ETF role in the U.S. market.

In the United States, VanEck has gone further by filing with the SEC for a Solana ETF structure. A registration statement on Form S‑1 for a VanEck Solana ETF describes a trust that would issue shares representing fractional undivided beneficial interest in a pool of SOL, again using a physically backed model. As with Bitcoin and the proposed ether ETFs before it, the Solana filing requires the issuer to persuade regulators that the market is sufficiently mature, surveilled, and resistant to manipulation to support a spot product. The SEC’s treatment of Solana is complicated by its evolving views on whether certain tokens might be unregistered securities, so the fate of this filing carries broader implications for altcoin regulation in the U.S.

Even more ambitious is VanEck’s proposed JitoSOL ETF, which would hold a Solana‑based liquid staking token rather than SOL itself. A separate S‑1 lays out the structure of the VanEck JitoSOL ETF, describing it as an exchange‑traded fund issuing common shares representing beneficial interest in a trust that would hold JitoSOL tokens. Nasdaq, which would list the fund, has filed a proposed rule change to support trading, explicitly characterizing the product as a fund designed to hold the Solana‑based liquid staking token. This is notable because JitoSOL represents staked SOL that accrues staking rewards and is subject to slashing risk if validators misbehave, meaning ETF shareholders would indirectly bear protocol‑level staking risks alongside price volatility.

The JitoSOL proposal raises novel regulatory and risk‑management questions. Because the token is yield‑bearing, regulators must consider whether the ETF structure inadvertently wraps an investment contract, and investors must understand that on‑chain events could impact both principal and yield. Nasdaq’s filing and media coverage have highlighted concerns about slashing, validator concentration, and the complexity of liquid staking protocols, all of which could feed into the SEC’s deliberations. VanEck’s willingness to pursue such a product underscores its intent to push beyond simple “price tracker” ETPs into structures that capture native on‑chain yield within regulated wrappers, even if that means navigating uncharted regulatory territory.

Avalanche Exposure: ETNs, ETFs, and the Payments Collective

Avalanche is another network where VanEck has experimented with both traditional and on‑chain exposures. In Europe, the firm offers a VanEck Avalanche ETN, marketed as an exchange‑traded note that provides direct access to AVAX, the native token of the Avalanche blockchain. The product is fully collateralized and invests in AVAX, with notes traded on regulated exchanges, giving investors a way to gain price exposure without engaging directly with the Avalanche network. As with other ETNs, investors take on both the market risk of AVAX and the credit risk of the note’s issuer, though full collateralization is intended to mitigate the latter.

In its global crypto timeline, VanEck notes that it launched a spot Avalanche ETF in January 2026, extending its single‑asset altcoin ETF strategy beyond Bitcoin and ether. However, early reception appears to have been lukewarm. Coverage on Binance’s Square platform reported that the VanEck spot Avalanche ETF saw zero net cash inflow and only about 330,000 dollars in trading volume on its first day, prompting commentary about “haunting silence” at launch. At the same time, the underlying AVAX token was trading in a depressed range around 11–15 dollars, with only a modest recovery of a few percent after the ETF listing. This episode illustrates a key lesson: simply wrapping an altcoin in an ETF does not guarantee investor demand, especially if broader market sentiment is cautious.

VanEck’s Avalanche strategy is not limited to listed products. It is also a founding participant in the Avalanche Payments Collective, announced by the Avalanche team as a collaborative effort to build a full‑stack payments ecosystem on the network. According to Avalanche, companies like VanEck, OpenTrade, and Grove will contribute treasury, liquidity, and yield‑bearing financial products to the collective’s asset‑management layer, while other participants focus on stablecoins, settlement, and merchant services. For VanEck, this is an opportunity to embed its expertise in treasuries and yield products into a native on‑chain payments environment, potentially supplying tokenized cash‑equivalent and yield‑bearing instruments that sit underneath consumer and B2B payment flows.

This multi‑pronged Avalanche approach underscores VanEck’s broader thesis that value will migrate not just into tokens but into real‑world assets and financial primitives issued directly on blockchains. The Avalanche ETN and ETF give investors familiar, regulated exposure to AVAX price action, while the Payments Collective experiments with making tokenized funds and liquidity instruments part of everyday payments infrastructure. Whether or not the initial ETF launch gains traction, these initiatives position VanEck as a recurring partner in Avalanche’s institutional narrative.

Blockworks launches the Transparency Alliance with Coinbase, Kraken, Ripple, and VanEck to standardize token disclosures ahead of looming US crypto regulation

42 filings on the live TTF board and only 13 marked complete is a cleaner tell than the logo wall. If Coinbase/Kraken/Binance.US pipe B-1/B-2 status into listing reviews, disclosure stops being PR and becomes a liquidity gate: market-maker contracts, insider unlocks, entity structure, buybacks. The catch is obvious from the partials: Morpho, Jito, AERO, JUP, DYDX all still have gaps, so the first serious market reaction comes when venues start penalizing opacity instead of just applauding participation.

- 01ETF filing race sequencing↗

Readers tracked the precise timing of VanEck's 8-A and 19b-4 filings as predictive signals for launch dates, treating regulatory paperwork as a countdown clock.

- 02Altcoin ETF frontier↗

SOL, BNB, AVAX, stETH, and Hyperliquid filings generated repeated engagement because each one tested how far the SEC's post-Bitcoin ETF tolerance actually extends.

- 03Long-range Bitcoin price research↗

The 2050 scenario analysis with a $52.3M bull case drew the most clicks of any single headline, revealing strong appetite for extreme-upside institutional modeling regardless of credibility.

- 04Novel index and basket products

The MarketVector MEMECOIN index signaled that VanEck is willing to package speculative retail culture into structured products, which readers found both surprising and telling.

- 05DeFi and on-chain integration↗

VBILL tokenized treasuries deployed as DeFi collateral on Euler and the Onchain Economy ETF filing showed VanEck bridging TradFi and DeFi rails, a genuinely novel move for a legacy asset manager.

- 06International ETF expansion

Australia listings and the French pension ETN deal signaled that global regulatory arbitrage is accelerating, with VanEck as a leading indicator of where institutional crypto flows next.

The BNB ETF and the Race for Altcoin Spot Exposure

Why BNB Became the Next ETF Battleground

After the approval of spot Bitcoin and, later, spot ether ETFs in the United States, market attention turned to which altcoin might be next. Binance Coin (BNB), the native token of the BNB Chain ecosystem and closely associated with the Binance exchange, emerged as a leading candidate due to its large market capitalization, trading liquidity, and extensive user base. At the time of intensive filing activity in May 2025, reporting noted that BNB was trading around 657 dollars and ranked as the fourth‑largest cryptocurrency by market capitalization, underscoring its prominence. Those metrics made it an obvious focal point for issuers looking to extend the crypto ETF universe beyond Bitcoin and Ethereum.

From VanEck’s standpoint, BNB offered an additional attraction: strong underlying network economics and user adoption that could be framed as fundamentals in marketing materials. In public pitches and research discussed in the crypto press, VanEck emphasized that BNB Chain generated hundreds of millions of dollars in annual revenue and supported tens of millions of monthly active users, which it presented as evidence of durable demand for block space and token utility. While those specific figures come from secondary reporting, they echo a broader narrative that BNB is not just a speculative token but a core economic asset for a high‑activity smart‑contract platform. For investors comparing potential altcoin ETFs, that combination of size, revenue, and user metrics is an important differentiator.

At the same time, BNB carries unique regulatory and reputational baggage because of its association with Binance, a centralized exchange that has faced multiple enforcement actions and investigations in various jurisdictions. For the SEC, assessing a BNB ETF thus involves not only token‑level questions about market manipulation and decentralization but also exchange‑level issues around compliance and governance. VanEck’s decision to pursue a BNB ETF despite these complications signals, again, a willingness to operate at the frontier of what regulators may allow, betting that demand for regulated exposure to a major altcoin will justify the effort.

Filing Wars: VanEck vs. Grayscale and SEC Negotiations

The path to a BNB ETF was neither quick nor straightforward. Both VanEck and Grayscale first filed registration statements for spot BNB ETFs with the SEC in May 2025, initiating what quickly became a competitive race to market. Over the following year, each issuer submitted multiple amendments in response to SEC feedback, refining disclosures around custody, pricing, and risk factors. By May of the following year, Bloomberg Intelligence ETF analyst James Seyffart highlighted that VanEck had filed its fifth amended S‑1, while Grayscale had submitted a second amended S‑1, interpreting the synchronized activity as a sign that both firms were actively engaging with regulators and potentially preparing for a near‑term launch. Parallel media coverage described this as evidence that BNB could become the next crypto asset to receive spot ETF approval after Bitcoin and Ethereum.

The filings laid out broadly similar product designs. Both VanEck and Grayscale proposed physically backed BNB trusts that would hold BNB directly and list on Nasdaq under the Commodity‑Based Trust Shares rules, specifically Nasdaq Rule 5711(d). The funds would track BNB’s price using reference indices; in VanEck’s case, the proposal specified the use of the MarketVector BNB Index as the pricing benchmark. This structure mirrors that of spot Bitcoin ETFs, which also rely on exchange‑based indices and operate as commodity‑style trusts rather than registered investment companies. By framing BNB as a commodity for ETF purposes, the issuers seek to avoid treating it as a security and to align with the legal model that prevailed for Bitcoin.

One contentious issue in the BNB filings was staking. Early versions of VanEck’s proposal contemplated staking BNB held by the trust to earn additional yield, which could then be distributed or reinvested. However, by November 2025 the firm had removed staking from its filing, citing unresolved U.S. regulatory questions about whether staking rewards might constitute a separate security or raise additional investor‑protection concerns. The amended filings for both VanEck and Grayscale explicitly stated that the ETFs would not engage in staking at launch, though they retained conditional language allowing for the possibility if and when regulatory clarity emerged. This reflects a broader pattern: U.S. regulators have been far more cautious about yield‑bearing crypto activities than about straightforward price‑tracking strategies.

The iterative amendment process also required detailed discussion of market surveillance and manipulation risks. To satisfy SEC concerns, the issuers emphasized that BNB trading was concentrated on large, surveilled exchanges and that the listing exchange would have surveillance‑sharing agreements to monitor for suspicious trading patterns. They also had to address the unique risks associated with BNB’s relationship to Binance, including potential conflicts of interest and concentration of liquidity. While many of these details are technical, they illustrate how the BNB ETF race became a test case for how far the SEC was willing to extend the Bitcoin ETF template to other large‑cap crypto assets.

Launching VBNB: Structure, Market Access, and Reaction

The culmination of this process came when VanEck announced the launch of the VanEck BNB ETF (VBNB) in late May 2026. In a press release dated May 28, 2026, VanEck described VBNB as the first U.S. spot BNB exchange‑traded product designed to provide investors with direct, physically backed exposure to BNB through regulated exchange‑traded shares. The fund lists on Nasdaq and allows investors to buy and sell shares during market hours like any other ETF, with each share representing a fractional interest in a pool of BNB held in custody. As with HODL, the fund is designed as a passive vehicle that simply tracks the underlying asset’s price without using leverage or yield‑enhancing strategies.

Structural details mirror the Bitcoin ETF template. Authorized participants create and redeem shares in large blocks by delivering BNB to or receiving it from the trust, with the custodian responsible for the secure storage of the tokens. Pricing is tied to the MarketVector BNB Index, which aggregates BNB trading across selected exchanges to produce a representative spot price. Investors thus obtain exposure to BNB’s price movements without facing the operational challenges of opening accounts on offshore exchanges or managing BNB wallets. For institutions with mandates that restrict direct token holdings but allow ETFs, VBNB offers a way to express a BNB thesis within existing compliance frameworks.

Market reaction to the launch highlighted both excitement and caution. Crypto media reported that BNB’s price rose in the wake of the ETF’s debut, echoing the “buy the rumor, sell the news” patterns observed around Bitcoin and ether ETF approvals, though causality is always hard to prove. Other coverage emphasized that VanEck aggressively marketed the ETF’s link to BNB Chain’s user base and fee revenue, presenting those metrics as a kind of “fundamental” underpinning for the asset. At the same time, analysts noted that ETF approval did not magically erase ongoing legal and regulatory issues facing Binance itself, and that investors still needed to consider those risks when allocating to VBNB.

The combination of these factors makes VBNB an important milestone in the evolution of crypto ETFs. It demonstrates that U.S. regulators are, at least in some cases, willing to extend spot ETF approval beyond Bitcoin and Ethereum to other large‑cap tokens, and it shows how issuers like VanEck and Grayscale are jockeying to become the default gateways for each major asset. Whether altcoin ETFs ultimately attract the same kind of sustained inflows as Bitcoin products remains an open question, but VBNB’s launch suggests that the race is very much underway.

Tokenization, VBILL, and VanEck’s DeFi and Infrastructure Bets

From ETFs to Tokenized Funds: Real‑World Assets On‑Chain

In parallel with its ETF business, VanEck has begun issuing tokenized versions of traditional funds, reflecting a broader industry trend toward bringing real‑world assets (RWAs) onto public blockchains. Tokenization, in this context, refers to the creation of blockchain‑based tokens that represent legal claims on off‑chain assets such as U.S. Treasuries, money market funds, or equity portfolios. The underlying assets remain in traditional custody and are managed under existing regulatory regimes, but ownership interests are recorded and transferred using blockchain rails rather than legacy systems.

VanEck’s most prominent example is VBILL, a tokenized share class of a U.S. Treasury fund that invests in short‑term government bills. While full technical and legal details are not in the public snippets, reporting and social media posts describe VBILL as a tokenized U.S. Treasury fund whose tokens can circulate on public blockchain networks. Economically, VBILL holders earn the underlying fund’s yield, which is driven by short‑term interest rates, while beneficial ownership is represented by on‑chain balances. This makes VBILL one of a growing cohort of tokenized Treasury products that offer crypto users access to dollar‑denominated yield from traditional markets.

Tokenized funds like VBILL differ from ETFs in several respects. They are typically issued under private‑placement or offshore regimes rather than being registered under the 1940 Act or ’33 Act, and they often impose transfer restrictions to ensure that only eligible, KYC‑verified investors can hold them. At the same time, they offer advantages that ETFs cannot easily match, such as 24/7 settlement, programmable composability with DeFi protocols, and the ability to move positions between on‑chain platforms without going through a broker. For VanEck, this represents a bet that some portion of future capital markets activity will occur directly on public blockchains and that being an early RWA issuer will confer strategic advantages.

VBILL as Collateral on Euler: A New DeFi–TradFi Bridge

The most striking manifestation of VBILL’s on‑chain utility came when DeFi lending protocol Euler announced that VBILL could be used as collateral for loans. Social media posts from Euler and industry observers noted that “VanEck’s tokenized VBILL U.S. Treasury fund can now be used as collateral on Euler,” framing it as a new path for tokenized securities in DeFi lending. Euler explained that assets like VBILL and STAC would be accepted as collateral in dedicated vaults where transfer and eligibility checks are enforced at the vault level, ensuring only compliant addresses can interact with these tokenized securities. In effect, this creates a walled‑garden within DeFi where regulated RWAs can be rehypothecated in ways analogous to traditional repo markets but powered by smart contracts.

This integration is significant for several reasons. First, it shows that tokenized funds are not merely static representations of off‑chain assets; they can be embedded into programmable financial systems where they serve as building blocks for lending, leverage, and other activities. Second, it demonstrates that compliance‑aware DeFi is possible: Euler’s vault‑level checks enable it to respect securities law constraints while still offering some of DeFi’s composability benefits. Third, it connects VanEck’s traditional client base, which cares about yield, liquidity, and regulatory certainty, with a new class of DeFi users who want dollar‑denominated yield but prefer on‑chain instruments.

For VanEck, the Euler integration is both a proof of concept and a marketing asset. It allows the firm to position itself not just as an ETF issuer, but as a provider of tokenized collateral that DeFi protocols and institutional on‑chain lenders can rely on. In the long run, if tokenized Treasuries and similar instruments become standard collateral in DeFi, asset managers like VanEck could become significant liquidity providers and gatekeepers in these markets. That possibility aligns with the firm’s participation in broader industry efforts to standardize token disclosures and build institutional‑grade infrastructure for on‑chain assets.

Avalanche Payments Collective: Embedding Treasuries and Yield in Payments

VanEck’s role in the Avalanche Payments Collective further illustrates its ambition to integrate traditional financial products into on‑chain ecosystems. According to Avalanche’s own description, the Payments Collective is designed to bring together payment companies, fintechs, financial institutions, and infrastructure providers to build a comprehensive payments stack on the Avalanche network. Founding participants include Franklin Templeton, VanEck, Anchorage Digital, Paxos, Agora, Ethena, Rain, Axiym, Tassat, and others that collectively span stablecoins, settlement, treasury management, and yield products. Within this framework, VanEck, OpenTrade, and Grove are highlighted as contributors to the asset‑management layer, bringing treasury, liquidity, and yield‑bearing financial products to the ecosystem.

This initiative suggests a vision where tokenized Treasuries and similar instruments become native components of payment flows. For example, a business using Avalanche‑based payment rails might park working capital in a tokenized Treasury fund like VBILL or analogous products from other issuers, earning yield between payment cycles while still being able to move funds instantly when needed. Merchants and payroll providers could similarly integrate yield‑bearing stable or near‑stable assets into their operations. VanEck’s role would then mirror its traditional function as a manager of cash and short‑term fixed‑income products, but with the added dimension of on‑chain programmability and global, 24/7 settlement.

The Payments Collective also highlights how VanEck sees its competitive set expanding. Rather than competing only with ETF issuers, it is now collaborating and competing with stablecoin issuers, on‑chain treasuries, and DeFi protocols to define what “on‑chain cash management” looks like. By aligning with Avalanche and other infrastructure providers, VanEck positions itself as a trusted brand that can reassure institutions wary of purely crypto‑native teams. At the same time, its involvement signals to crypto users that not all RWAs are created equal; those managed by established asset managers may carry different risk profiles than those issued by newer, less regulated entities.

Transparency Alliance: Standardizing Token Disclosures

VanEck’s RWA and DeFi initiatives are complemented by its participation in efforts to standardize token disclosures and improve transparency. Blockworks announced the launch of the Transparency Alliance, an industry group designed to establish standardized transparency around tokens via an open‑source Token Transparency Framework. The framework aims to provide structured, comparable data on token economics, supply schedules, governance, and other key characteristics for every digital asset that participates. Founding members include firms such as Coinbase, Kraken, Ripple, and VanEck, reflecting a mix of exchanges, issuers, and infrastructure providers.

For an asset manager, participation in such an alliance serves multiple objectives. It helps mitigate regulatory concerns about opaque token structures and information asymmetries, which have been at the heart of many enforcement actions and investor protection debates. It also gives VanEck a say in how “good disclosure” is defined in crypto, which in turn shapes which tokens are considered suitable for ETFs, ETPs, and tokenized fund strategies. If the Transparency Alliance’s frameworks become widely adopted, tokens that follow them could enjoy easier paths to inclusion in regulated products, while those that do not may face higher hurdles.

From an investor’s perspective, standardized token disclosures can make it easier to compare assets across dimensions such as inflation rate, insider allocations, lockup schedules, and governance rights. This is particularly important for products like the Onchain Economy ETF and potential future multi‑asset crypto funds that must explain and justify their holdings to regulators and clients. VanEck’s advocacy for transparency in token markets thus aligns with its strategic interest in expanding the universe of assets that can be safely and credibly packaged into exchange‑traded and tokenized vehicles.

VanEck launches the first US spot BNB ETF, giving investors regulated exposure to Binance-linked BNB through physically backed exchange-traded shares

39 bps plus no staking makes VBNB a convenience wrapper, not the cleanest way to own $BNB; direct holders still keep validator yield and actual gas utility on BSC. AP creations can still pull spot supply into Anchorage cold storage while BNB Chain is already doing 14M+ tx/day, 2.5M DAUs, $16B stablecoins and $3.6B RWAs. Clean first-week spreads matter more than a day-one pump: they give Grayscale’s GBNB and the rest of the alt ETF queue a working comp.

- 2023-10launch

VanEck ETH futures ETF launches with $400K first-day volume

VanEck spot Bitcoin ETF (HODL ticker) approved and listed

- 2024-05regulatory

SEC acknowledges VanEck and ARK spot Ethereum ETF applications

- 2024-07launch

VanEck spot Ethereum ETF launches at 0.20% fee

VanEck and 21Shares file 19b-4s for spot Solana ETF

VanEck files Delaware trust for BNB ETF

- 2025-04regulatory

VanEck files for stETH ETF following SEC liquid-staking guidance

VanEck VBILL tokenized treasury fund goes live on Euler as DeFi collateral

Risks, Challenges, and the Market Impact of VanEck’s Crypto Strategy

Demand Risk and Product–Market Fit: Lessons from the AVAX ETF

One of the clearest lessons from VanEck’s crypto expansion is that not every product will find immediate traction, even if it is “first.” The launch of the spot Avalanche ETF in January 2026 exemplifies this. As noted earlier, commentary on Binance’s Square platform reported that the ETF debuted with zero net cash inflows and only about 330,000 dollars in trading volume on its first day, in stark contrast to the blockbuster launches of some Bitcoin ETFs. The underlying AVAX token, meanwhile, remained under pressure, trading near the lower end of an 11–15 dollar range with only a modest, roughly two‑percent bounce after the ETF listing. This muted response suggests that investor appetite for single‑asset altcoin ETFs is far more conditional than for Bitcoin.

Several factors likely contributed to this outcome. Avalanche, while technologically sophisticated and supported by an active DeFi and gaming ecosystem, does not yet have the same brand recognition or narrative resonance as Bitcoin or Ethereum among mainstream investors. Its token has experienced significant drawdowns from prior cycle highs, and regulatory clarity for altcoins remains weaker than for Bitcoin. Moreover, the ETF arrived in a risk‑off macro environment, where investors were already cautious about adding new exposures. VanEck’s experience with the AVAX ETF underscores that product timing, market sentiment, and the perceived fundamental story of the underlying asset are all critical to ETF success.

This case also raises questions about how far the single‑asset altcoin ETF model can scale. If only a handful of large‑cap tokens attract sufficient demand to support liquid, economically viable ETFs, issuers will need to be selective and strategic. For VanEck, the AVAX launch may still be valuable as an option on future adoption and as a signal of commitment to the network’s ecosystem, especially given its involvement in the Avalanche Payments Collective. However, it also illustrates that the ETF wrapper does not, by itself, create a market; it can only channel demand that already exists or that can be cultivated through credible narratives and use cases.

Regulatory and Structural Risks: SEC Scrutiny, Staking, and Tokenization

VanEck’s crypto strategy exposes it to a wide range of regulatory and structural risks. In the ETF arena, every new filing must navigate the SEC’s evolving views on what constitutes a commodity versus a security, how to ensure adequate market surveillance, and whether certain token features – such as pre‑mines, insider allocations, or governance structures – pose investor‑protection concerns. The BNB filings, for example, had to address not only BNB’s market characteristics but also its deep ties to Binance, a company under intense regulatory scrutiny in multiple jurisdictions. Approval of VBNB does not eliminate those underlying issues; it simply indicates that the SEC found the specific ETF structure acceptable under current law.

Staking presents another layer of complexity. As noted earlier, VanEck removed staking from its BNB ETF proposal due to unresolved questions about whether staking yields might count as securities or trigger additional regulatory obligations. Similar concerns hover over the JitoSOL ETF filing, where the underlying asset is a yield‑bearing liquid staking token subject to protocol‑level slashing risk. If regulators ultimately take a stricter view of staking as a regulated activity or of staking tokens as securities, products built around them could face delays, forced restructuring, or even delisting. VanEck’s cautious approach – preserving optionality to add staking in the future without using it at launch – reflects an attempt to balance investor demand for yield with regulatory pragmatism.

Tokenization initiatives such as VBILL also operate in a gray area. While the underlying assets are familiar and regulated (e.g., U.S. Treasuries), representing them as on‑chain tokens raises questions about how securities laws apply to secondary trading on public blockchains, especially across borders. Euler’s decision to enforce transfer and eligibility checks at the vault level is an attempt to square this circle, but regulators could still decide that certain on‑chain interactions constitute unregistered distribution or that DeFi protocols need to register as alternative trading systems or broker‑dealers when dealing with tokenized securities. As a high‑profile issuer, VanEck will likely be at the center of these debates.

Structural risks are not limited to regulation. ETF investors must also consider custody and operational risks, including the possibility of hacks, key mismanagement, or failures at custodial partners. While VanEck and other issuers work with specialized crypto custodians and tout robust security practices, the history of crypto markets provides many examples of infrastructure failures. Similarly, tokenized funds depend on smart contract security and correct mapping between on‑chain tokens and off‑chain legal claims; any discrepancy or exploit could lead to complex disputes. VanEck’s reputation as a conservative, institutional‑grade manager may mitigate perceived risk, but it cannot eliminate the underlying technological and operational uncertainties inherent in crypto.

ETF Versus Direct Ownership: Trade‑Offs for Crypto Investors

VanEck’s products crystallize the trade‑offs between holding crypto directly and accessing it through ETFs or tokenized funds. On the one hand, ETFs like HODL and VBNB offer regulated, familiar vehicles that fit seamlessly into brokerage accounts, IRAs, and institutional platforms. Investors avoid dealing with private keys, hardware wallets, or exchange hacks, and they benefit from protections like audited financial statements, standardized disclosures, and oversight by securities regulators. For many institutions, these features are not optional; mandates simply do not allow direct token purchases.

On the other hand, ETF investors sacrifice some of the core features that attract many to crypto in the first place. They do not control the underlying coins and cannot use them in DeFi, move them across chains, or participate in governance and staking directly. Fees, while falling in many ETFs, still represent a drag relative to holding the asset outright, especially in long‑term strategies predicated on large price appreciation. There is also basis risk: while physically backed ETFs are designed to track spot prices closely, discrepancies can still arise due to creation/redemption frictions, custody costs, and trading dynamics.

Tokenized funds like VBILL occupy an intermediate space. They preserve some on‑chain functionality, allowing investors to plug into DeFi protocols or move tokens between wallets, while still abstracting away underlying asset management and custody. However, they bring their own layers of legal and operational complexity, including transfer restrictions and the need to trust that off‑chain fund administration is accurately reflected on‑chain. VanEck’s portfolio of ETFs, ETPs, ETNs, and tokenized funds thus offers a menu of exposure types, each with its own mix of convenience, control, risk, and regulatory posture.

Reputational and Concentration Risks in a Fast‑Moving Market

Finally, VanEck’s deep involvement in crypto exposes it to reputational and concentration risks. If a major product experiences a security incident, severe tracking error, or regulatory sanction, the damage could spill over to the firm’s broader brand as a responsible asset manager. Similarly, if aggressive price targets like one million or 2.9 million dollars for Bitcoin are widely publicized but fail to materialize over long periods, critics may question whether the firm contributed to speculative excess. Balancing bold theses that attract attention with sober risk disclosures is an ongoing challenge.

There is also a concentration risk in terms of personnel and narratives. Much of VanEck’s public crypto research is associated with a small group of executives and analysts, whose views may or may not represent consensus within the firm. If these individuals leave or their views are discredited, VanEck may need to recalibrate its messaging. Moreover, as more traditional asset managers enter the crypto ETF and tokenization space, VanEck’s first‑mover advantage could erode, forcing it to compete more on fees and distribution than on innovation alone.

Despite these challenges, VanEck’s strategy has undeniably shaped how mainstream investors access crypto. Its early and persistent efforts helped normalize the idea of physically backed crypto ETFs, its tokenization projects offer a template for integrating RWAs with DeFi, and its research has contributed to framing Bitcoin and other assets as legitimate components of long‑term portfolios. The question is not whether VanEck matters in crypto today, but how its role will evolve as the industry and regulatory environment continue to change.

Conclusion

VanEck’s journey from a gold‑focused asset manager to a central player in digital asset markets encapsulates the broader convergence of traditional finance and crypto. Leveraging its experience with commodities and emerging markets, the firm has systematically built a suite of products that span U.S. spot Bitcoin ETFs like HODL, European ETPs and ETNs for assets such as Solana and Avalanche, and more experimental structures like the BNB ETF and proposed JitoSOL staking ETF. This product stack is complemented by tokenized funds such as VBILL and on‑chain collaborations like the Avalanche Payments Collective, which together signal a conviction that both investment exposure and financial infrastructure are migrating onto blockchains.

At the same time, VanEck has invested heavily in research that frames Bitcoin and other digital assets within familiar institutional paradigms. Its ChainCheck reports translate on‑chain metrics into actionable signals, while long‑term capital market assumptions place Bitcoin alongside equities and bonds in strategic asset allocation models, even projecting million‑dollar‑plus price levels under certain scenarios. Analyses of government Bitcoin mining, token transparency, and staking risks further underscore an effort to engage with crypto’s technological and geopolitical complexity rather than treating it as a mere speculative fad. This research serves both as marketing for VanEck’s products and as a bridge for institutional investors still learning the space.

Yet VanEck’s aggressive strategy also highlights the limits and risks of the ETF‑ and tokenization‑driven approach. The lukewarm reception of the Avalanche ETF shows that not every altcoin can support a thriving single‑asset ETF, while the regulatory uncertainty around staking‑based products and tokenized securities cautions against assuming that today’s structures will remain viable tomorrow. Investors using VanEck’s products must weigh the convenience and regulatory comfort of ETFs and tokenized funds against the loss of direct control, composability, and, in some cases, economic features like staking rewards. As the crypto market matures and new entrants proliferate, VanEck will need to continue balancing innovation with prudence to maintain its position as a trusted gateway rather than a fair‑weather tourist.

VanEck's entire crypto product pipeline depends on SEC discretion — delays or rejections on SOL, BNB, AVAX, and stETH ETFs could stall the firm's digital-asset revenue roadmap for years.

- Market / AUM fragilityMedium

The ETH futures ETF launched with only $400K in first-day volume, demonstrating that SEC approval does not guarantee demand, and thin AUM products risk closure as the Onchain Economy ETF replacement of the ETH futures fund showed.

VBILL tokenized treasuries deployed as collateral on Euler introduce direct smart-contract risk to an otherwise TradFi product, exposing institutional investors to protocol exploits.

- CentralizationLow

As a regulated asset manager, VanEck's custodial and governance structure is conventionally centralized; this is a feature for institutional clients and not a systemic DeFi-style risk.

- Competitive / fee compressionMedium

VanEck entered the spot ETH ETF at 0.20%, but fee wars with BlackRock and Franklin below 30bps risk compressing margins on a product category where AUM scale determines viability.

VanEck filed an AVAX ETF while AVAX was down 55% year-to-date and holds BTC price scenarios spanning $130K to $52.3M by 2050, reflecting the extreme range of outcomes baked into its product suite.

Outlook

Looking ahead, VanEck is likely to remain a prominent architect of how traditional capital interacts with crypto, but the contours of that role will evolve as regulation, competition, and technology change. On the listed‑product side, the BNB ETF’s launch opens the door to a broader universe of altcoin ETFs, yet the mixed experience of the AVAX ETF suggests that only a subset of large‑cap tokens will attract sufficient demand to justify stand‑alone products. Future developments around Solana and staking‑based ETFs like JitoSOL will be key tests of how far regulators are willing to extend the spot ETF template beyond Bitcoin‑style assets, and VanEck’s filings position it at the forefront of that experimentation. Success will depend not only on regulatory outcomes but also on whether these networks can sustain compelling usage and fee‑generation narratives that resonate with both crypto‑native and traditional investors.

In tokenization and DeFi, initiatives such as VBILL on Euler and the Avalanche Payments Collective are still early, but they point toward a future where tokenized Treasuries, money market funds, and other RWAs become standard collateral and liquidity sources in on‑chain financial systems. If this vision plays out, asset managers like VanEck could become core infrastructure providers for DeFi, supplying the high‑quality, yield‑bearing assets that underwrite lending, payments, and derivative markets. At the same time, this will likely invite closer regulatory scrutiny of DeFi protocols and tokenized securities, requiring careful design of access controls, disclosures, and governance to balance innovation with investor protection.

For a crypto‑savvy audience, the practical takeaway is that VanEck is more than just one more ticker in the sea of ETFs; it is an influential actor whose decisions about which assets to list, how to structure products, and which on‑chain experiments to back will shape the evolution of regulated access to digital assets. Whether you hold HODL in a retirement account, borrow against VBILL in DeFi, or track the progress of VBNB and future altcoin ETFs, understanding VanEck’s strategy and constraints offers insight into how traditional finance is absorbing – and being reshaped by – the crypto economy.

Latest VanEck news

Bitwise locks in 0.67% fee and BHYP ticker for Hyperliquid ETF as Grayscale, VanEck chase HYPE exposureBlockworks launches the Transparency Alliance with Coinbase, Kraken, Ripple, and VanEck to standardize token disclosures ahead of looming US crypto regulationVanEck launches the first US spot BNB ETF, giving investors regulated exposure to Binance-linked BNB through physically backed exchange-traded sharesVanEck's VBILL Treasury fund goes live on Euler as tokenized collateral for DeFi loansVanEck pitches BNB's $160M revenue and 33M monthly users as VBNB ETF edge VanEck CEO Jan van Eck concerned about Bitcoin's encryption and privacy, says firm could walk away and that some longtime Bitcoin holders are examining Zcash as the market reassesses long-term assumptions.

VanEck CEO Jan van Eck concerned about Bitcoin's encryption and privacy, says firm could walk away and that some longtime Bitcoin holders are examining Zcash as the market reassesses long-term assumptions.Sources

- https://www.vaneck.com/us/en/education/investment-ideas/crypto-investing/

- https://www.vaneck.com/offshore/en/investments/bitcoin-etf-hodl/

- https://www.vaneck.com/us/en/press-releases/vaneck-launches-first-us-spot-bnb-etp-vbnb/

- https://www.vaneck.com/lu/en/investments/avalanche-etp/

- https://www.sec.gov/Archives/edgar/data/2028541/000202854125000002/vanecksolanaetfs-1a1.htm

- https://www.sec.gov/Archives/edgar/data/2082189/000162828025041000/vaneckjitosoletfs-1.htm

- https://x.com/TheBlockCo/status/2060022763041980525

- https://www.avax.network/about/blog/avalanche-payments-collective

- https://blockworks.com/insights/blockworks-launches-transparency-alliance

- https://bitcoinfoundation.org/news/bitcoin/bitcoin-price-hit-1m-vaneck/

- https://www.vaneck.com/us/en/blogs/digital-assets/matthew-sigel-vaneck-mid-march-2026-bitcoin-chaincheck/

- https://cryptorank.io/news/feed/784e6-vaneck-government-bitcoin-mining-nations

- https://www.tradingview.com/news/cointelegraph:42f04bbe5094b:0-sec-approval-sought-for-jitosol-solana-based-liquid-staking-token-etf/

- https://coinmarketcap.com/academy/article/%20bnb-etf-race-vaneck-grayscale

- https://www.binance.com/en/square/post/35700992329897

- https://www.vaneck.com/us/en/investments/bitcoin-etf-hodl/

- https://www.vaneck.com/us/en/blogs/digital-assets/matthew-sigel-vaneck-bitcoin-long-term-capital-market-assumptions/

- https://www.marketsmedia.com/blockworks-launches-transparency-alliance-for-tokens/

- https://x.com/eulerfinance/status/2061483778833285182

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…