In-depth explainer on AERO, the governance and rewards token powering Aerodrome and the upcoming cross-chain Aero DEX, covering tokenomics, buybacks, governance, Predictive Allocation, Base/Coinbase ties, risks, and long-term outlook for DeFi users.

+13 sources across the wider coverage universe

Aerodrome’s Ethereum expansion could transform AERO into cross-chain exchange infrastructure, but sustainable growth hinges on reducing subsidy-driven liquidity2026-06

Aerodrome’s Ethereum expansion could transform AERO into cross-chain exchange infrastructure, but sustainable growth hinges on reducing subsidy-driven liquidity2026-06 Aerodrome and Velodrome to merge in July, with $VELO fungible for 0.55 $AERO2026-03

Aerodrome and Velodrome to merge in July, with $VELO fungible for 0.55 $AERO2026-03 Aerodrome is introducing a Market-Aware buyback model through its upcoming Momentum Fund, using algorithmic, volatility-responsive rules to acquire AERO more efficiently than fixed schedules or discretionary buys. The pilot showed strong results, accumulating 8.7M AERO and scaling buy pressure during high volatility, with plans to consolidate capital programs and introduce buyback-and-burns to strengthen long-term protocol economics.2026-01

Aerodrome is introducing a Market-Aware buyback model through its upcoming Momentum Fund, using algorithmic, volatility-responsive rules to acquire AERO more efficiently than fixed schedules or discretionary buys. The pilot showed strong results, accumulating 8.7M AERO and scaling buy pressure during high volatility, with plans to consolidate capital programs and introduce buyback-and-burns to strengthen long-term protocol economics.2026-01 Aerodrome updates its Flight School program, which buys back AERO, locks as veAERO and distributes as rewards to lockers, increased its bonus to its highest ever rate of 60%2024-06

Aerodrome updates its Flight School program, which buys back AERO, locks as veAERO and distributes as rewards to lockers, increased its bonus to its highest ever rate of 60%2024-06 Dromos announces Aero, an expansion to mainnet via a merger between Aerodrome and Velodrome, with a token distributed to current VELO & AERO holders spilt 94.5/4.5 based on annual revenue2025-11

Dromos announces Aero, an expansion to mainnet via a merger between Aerodrome and Velodrome, with a token distributed to current VELO & AERO holders spilt 94.5/4.5 based on annual revenue2025-11 Aerodrome's AERO added as collateral for MAI Stablecoin on Base2024-04

Aerodrome's AERO added as collateral for MAI Stablecoin on Base2024-04

Understanding AERO: Token, DEX, and Liquidity Hub for the Superchain

As the governance and rewards token behind Aerodrome Finance and the forthcoming cross-chain Aero exchange, AERO sits at the center of an increasingly influential piece of decentralized finance infrastructure on Ethereum layer 2. It anchors a vote-escrow incentive system, revenue-sharing model, and buyback-and-lock programs that collectively aim to turn Aerodrome into a sustainable liquidity hub for the Base ecosystem and beyond.

At its core, AERO ties together the economic incentives of traders, liquidity providers, protocol builders, and long-term token lockers. Aerodrome already functions as the dominant automated market maker (AMM) on Coinbase’s Base network, routing a large share of that chain’s volume and fees through its pools and gauges. Plans to merge Aerodrome with its sister protocol Velodrome into a unified cross-chain DEX called Aero, coupled with new mechanisms such as Predictive Allocation and an expanded buyback-and-burn “Momentum Fund,” are set to reshape how AERO emissions, locks, and revenues interact. This article explains how AERO works today, how it is evolving, how its economics compare to other DeFi tokens, and what risks and opportunities sophisticated crypto users should consider.

The DeFi Context: From AMMs to Vote-Escrow Liquidity Hubs

To understand AERO, it helps to situate Aerodrome and Aero within the broader history of decentralized exchanges. The first generation of Ethereum AMMs, typified by Uniswap v2, focused on simple constant-product liquidity pools where liquidity providers earned a share of trading fees in proportion to their stake. In that design, LPs funded most of the protocol’s economics: they provided capital, accepted impermanent loss risk, and were compensated directly from trader fees. Governance tokens, when they existed, often had weak or indirect links to protocol cash flows.

The second generation of AMM designs introduced more specialized pools and more explicit tokenomics. Curve Finance pioneered the vote-escrow model with veCRV, in which users lock governance tokens for long periods to gain boosted rewards and voting power over which pools receive emissions. This transformed liquidity incentives into a political and economic game: tokens could be locked to direct incentives, protocols could pay for votes via “bribes,” and long-term lockers gained leverage over both emissions and fee distribution.

A subsequent evolution came with Solidly-style designs, sometimes dubbed ve(3,3), in which the gauge and bribe mechanics were adapted to newer ecosystems like Optimism and Fantom. Velodrome Finance on Optimism became one of the most successful implementations of this model, emphasizing deep, protocol-directed liquidity and aggressive incentive markets for builders seeking efficient liquidity routing. Aerodrome Finance then transplanted and refined this design on Base, Coinbase’s Ethereum layer-2, with AERO as its governance and rewards token.

The central idea behind these systems is that the DEX is not just a passive venue for swaps. Instead, it becomes a liquidity marketplace where emissions, bribes, and fee flows are actively negotiated through governance. AERO is the asset that prices these negotiations on Aerodrome and, soon, on the unified Aero DEX. This explains why its tokenomics, governance, and buyback policies are crucial to understanding both the protocol’s health and the broader markets it touches.

Base, Optimism, and the OP Superchain

Aerodrome operates today on Base, an Ethereum layer-2 network incubated by Coinbase that uses optimistic rollup technology and is part of the broader Optimism “Superchain” ecosystem. Base aims to provide low-cost, high-throughput infrastructure for applications that can tap Coinbase’s large user base, while still ultimately settling on Ethereum mainnet. Because of its close association with Coinbase and its focus on consumer-facing use cases, Base has quickly become a focal point for DeFi experimentation, memecoins, and novel protocols.

Velodrome, in contrast, was originally built on Optimism, another rollup within the same Superchain family. Dromos Labs, the team behind both Velodrome and Aerodrome, has positioned these DEXs as native liquidity engines for their respective chains. Aerodrome’s own documentation and dashboards describe it as the central trading and liquidity marketplace on Base, and on-chain data aggregators have reported substantial liquidity, fees, and total value locked (TVL) centered on its pools. Aerodrome’s team has highlighted that the DEX has generated tens of billions of dollars in cumulative volume on Base, more than twice the volume of the next-largest DEX on that chain over comparable periods.

The planned merger of Aerodrome and Velodrome into Aero is explicitly designed to move beyond a single-chain focus and unify liquidity, governance, and incentives across Base, Optimism, Ethereum mainnet, and Circle’s institutional Arc network. In that expanded context, AERO is intended to serve not only as the token of the dominant Base DEX but as the governance and rewards asset of a cross-chain AMM operating across the Superchain and key mainnet environments.

Aerodrome’s Ethereum expansion could transform AERO into cross-chain exchange infrastructure, but sustainable growth hinges on reducing subsidy-driven liquidity

DefiLlama has Aerodrome at roughly $527M 24h volume and $18B 30d volume on Base against about $314M TVL, so the venue already has enough turnover to matter before the multi-chain thesis kicks in. The hard part on Ethereum is not just porting Slipstream; it is winning orderflow where Uniswap v4 hooks, Curve/Convex gauge wars, and aggregator routing already crush lazy LP margins. If veAERO emissions keep buying mercenary TVL, mainnet becomes a bigger subsidy sink; if fees and external incentives follow organic volume, AERO starts looking less like a Base beta trade and more like DEX coordination infrastructure.

Leviathan readers most reliably click when Aerodrome's tokenomics machinery produces structural supply removal — buyback-and-lock programs, veAERO max-lock saturation, and emission-versus-lock ratios — revealing that the community is stress-testing whether the ve(3,3) flywheel is self-sustaining or subsidy-dependent.↗

What Is AERO?

Aerodrome Finance and the AERO Token

Aerodrome Finance is an automated market maker and decentralized exchange deployed on the Base network that aims to be that ecosystem’s central liquidity hub. It combines a range of AMM pools with an incentive system based on vote-escrowed governance tokens and gauge-directed emissions. AERO is the protocol’s native token and plays several roles simultaneously: it is the unit of liquidity incentives paid to LPs, the governance token that controls emissions and protocol parameters, and the asset through which holders can claim a share of the DEX’s fee revenue via locking into veAERO.

In practical terms, users encounter AERO in three main ways. Traders interact with Aerodrome’s pools when swapping tokens on Base, indirectly generating fees and volume that feed into AERO’s revenue flywheel. Liquidity providers deposit token pairs into Aerodrome’s pools and receive LP tokens that entitle them to AERO emissions, which are allocated based on governance votes but are decoupled from point-in-time trading fees. Governance participants acquire AERO, lock it into veAERO for a specified duration, and use this locked position to direct emissions to specific pools (gauges), collect trading fees and bribes, and participate in protocol decision-making.

Aerodrome’s design makes AERO structurally central to how liquidity is directed across the Base ecosystem. Protocols and projects launching on Base that want deep liquidity are incentivized to court veAERO voters, either by accumulating locked AERO themselves or by paying bribes to existing veAERO holders to vote for their pools. This positions AERO as a kind of meta-asset that protocols must reckon with if they want to efficiently source liquidity on Base and, in the future, on Aero’s broader cross-chain environment.

Evolution Toward Aero: Merger with Velodrome

The most significant structural change on AERO’s roadmap is the planned merger of Aerodrome with Velodrome into a unified cross-chain DEX called Aero. Announced initially in late 2025 and slated to go live around July 2026, this merger will consolidate governance and liquidity from both platforms under a single protocol architecture and token. The goal is to end internal competition between Aerodrome and Velodrome, unify incentives, and create a more capital-efficient liquidity layer spanning multiple chains.

According to public materials and aggregated coverage, the new Aero protocol will deploy on Ethereum mainnet and Circle’s permissioned Arc blockchain, while maintaining deep deployments on Base and Optimism. This expansion targets both the liquidity depth and composability of Ethereum and the more regulated, USDC-centric environment of Arc, which is designed for institutional users and compliant financial applications. The codebase will evolve into what Dromos Labs describes as a MetaDEX operating system, sometimes referred to as MetaDEX03, designed to orchestrate liquidity, routing, and incentives across chains.

A key aspect of the merger is token consolidation. The plan, as described in third-party coverage, is to introduce a new unified AERO token that will replace the existing Aerodrome AERO and Velodrome VELO tokens. The initial distribution is expected to be heavily weighted toward the existing Aerodrome ecosystem, reflecting the larger share of revenue that Aerodrome has generated relative to Velodrome. One widely cited breakdown allocates roughly 94.5% of the new token supply to current AERO holders and 5.5% to VELO holders, although the precise implementation and any subsequent governance changes will ultimately be determined by the protocol.

This merger and rebranding will not change AERO’s functional role as the governance and reward token of the core DEX. Rather, it is intended to extend that role across multiple chains, broaden the set of assets and users that interact with AERO, and introduce new mechanisms—such as Predictive Allocation and enhanced buybacks—to make the tokenomics more efficient.

AERO’s Utility: Beyond Simple Governance

Even before the Aero launch, AERO’s utility extends beyond simple voting rights. By design, veAERO lockers capture 100% of Aerodrome’s protocol revenues, since the DEX routes all swap fees and related income to voters rather than LPs in what its designers describe as a “zero-leak” model. This means that AERO, when locked, entitles holders not only to influence emissions but also to claim a pro-rata share of the DEX’s fee-based revenue stream.

In addition, veAERO holders earn AERO emissions themselves and can collect “bribes” paid by external protocols seeking to attract votes for their liquidity pools. In combination, these flows—fees, emissions, and bribes—turn veAERO into a yield-bearing governance asset. Liquidity providers, meanwhile, gain AERO emissions and may also receive project-specific incentives or additional rewards attached to particular pools. Because AERO emissions are decoupled from point-in-time trading fees, LPs can sometimes earn significant yield even in lower-volume pools, provided governance votes direct emissions to those gauges.

As Aerodrome evolves into Aero, this utility is expected to expand to include cross-chain fee capture, potentially enhanced revenue from more sophisticated routing and MEV-resistant pool designs, and new buyback-and-burn mechanisms funded by the protocol’s cash flows. At the same time, these mechanisms introduce complexity and risk, making it important for users to understand how AERO’s incentive structures interact with underlying market conditions.

Aerodrome’s Design: AMMs, Gauges, and Emissions

AMM Architecture and Pool Types

Aerodrome’s core is a set of automated market maker pools that facilitate token swaps on Base. Like many modern DEXs, it supports different pool types optimized for various assets: “stable” pools for closely correlated assets, such as two stablecoins or different forms of tokenized dollars, and “volatile” pools for more uncorrelated pairs such as governance tokens against ETH. While the precise implementation can evolve, the underlying design draws heavily from the Solidly and Velodrome architectures, which use a mix of curve formulas to balance capital efficiency with robustness.

In this architecture, pricing is algorithmic, with the shape of the bonding curve determining how the marginal price changes as traders consume liquidity. Traders pay a fee on each swap, typically denominated as a percentage of trade volume. Unlike in Uniswap v2, those fees do not automatically accrue to LPs; instead, they are collected as protocol revenue and later distributed to veAERO voters according to governance rules. This design allows the protocol to treat fee revenue as a flexible resource that can fund buybacks, grants, or other programs, rather than tying it mechanically to LP positions.

Aerodrome has also begun transitioning some of its pools to MEV-resistant designs as part of its preparation for the Aero launch. MEV, or miner/maximal extractable value, refers to the value that block builders can extract by reordering, inserting, or censoring transactions, often at the expense of traders and LPs. MEV-resistant pools attempt to reduce or redirect this extraction, for example by batching trades or using specialized routing logic, which can improve execution quality and increase the portion of value that accrues to the protocol and its stakeholders. By integrating such designs, Aerodrome aims to make its pools more competitive on execution quality, particularly as it prepares to compete with established DEXs like Uniswap on Ethereum mainnet.

Liquidity Provisioning and LP Returns

Liquidity providers on Aerodrome deposit pairs of tokens into pools and receive LP tokens that represent their proportional share of the pool’s reserves. These LP tokens are typically staked in associated gauges to earn AERO emissions. A distinctive feature of Aerodrome’s model, emphasized in its documentation, is that LPs do not receive the ongoing trading fees from the pools directly; instead, their primary direct compensation from the protocol comes in the form of AERO emissions and any attached incentives.

This structure decouples LP returns from the immediate fee revenue of their pools. In traditional AMMs, LPs earn more when their pools see high volume and fee generation; on Aerodrome, LPs can still benefit from volume indirectly—since higher volume can attract more governance votes and bribes—but their direct reward stream is determined by how many AERO emissions their pool’s gauge receives in a given epoch. In other words, LP returns are a function of governance dynamics and emissions policy rather than fee generation alone.

LPs still bear standard AMM risks, including impermanent loss when the relative prices of the tokens in their pool change. In volatile pools, this can be substantial if one asset appreciates or depreciates sharply against the other. LPs must therefore weigh the value of AERO emissions and any accompanying incentives against the possibility of impermanent loss and the opportunity cost of deploying their capital elsewhere. Because AERO’s own price can be volatile, the real-world yield expressed in dollars or stablecoins can fluctuate significantly as market conditions change.

The decoupling of fees and LP rewards allows Aerodrome to implement a zero-leak revenue model in which all protocol revenue flows to governance participants rather than LPs. This is intended to align the interests of long-term AERO lockers with the protocol’s overall growth and fee generation. It also means that the sustainability of LP incentives depends heavily on the value of AERO emissions and the competitiveness of Aerodrome’s incentive system relative to other DEXs.

Gauges, Bribes, and Emissions Routing

The gauge system is where AERO’s tokenomics come to life. Each liquidity pool on Aerodrome is associated with a gauge that can receive a portion of the protocol’s AERO emissions. At regular intervals (epochs), veAERO holders vote on how to distribute emissions across gauges, effectively deciding which pools receive more or fewer AERO tokens as rewards for their LPs. The more veAERO voting power allocated to a given gauge, the higher the AERO rewards for LPs in that pool during the next epoch.

This mechanism turns emissions into a scarce resource that protocols must compete for. Projects launching tokens on Base can try to acquire veAERO themselves, enabling them to vote for their own pools, or more commonly they can pay “bribes” to veAERO voters, offering additional tokens or incentives in exchange for votes. These bribes supplement the fee and emission income that veAERO holders receive, often making vote-locking AERO attractive for yield-focused participants.

The result is a complex marketplace in which emissions, bribes, and vote power interact. A pool that generates high trading fees may attract votes organically, as veAERO holders seek to maximize their fee income. A project that wants liquidity but has lower natural volume may attempt to overcome this disadvantage by paying bribes to veAERO voters. Over time, this can result in an equilibrium where emissions are spread across pools in a way that reflects both underlying activity and external demand for liquidity.

To prevent extreme concentration of emissions in a few pools and to reduce strategic manipulation, the protocol can introduce gauge caps, limiting the maximum share of total emissions a single gauge can receive in an epoch. Although implementation details can change over time, the general purpose of gauge caps is to encourage diversification of incentives, reduce the impact of any one pool’s governance coalition, and mitigate the risk of emissions being captured entirely by a small set of insiders. These caps are particularly important at launch and during major upgrades, when new pools and chains come online and the emissions landscape is still forming.

Aerodrome and Velodrome to merge in July, with $VELO fungible for 0.55 $AERO

$260M vs $15M in trailing revenue — the 94.5/5.5 split prices Velodrome's Optimism origination and ve(3,3) pioneering at zero premium. This is an acquisition wearing a merger's clothing. Embedded MEV auctions in METADEX03 are what to watch: if Dromos can internalize searcher flow when they hit Ethereum mainnet, they'll have a structural fee edge against Uniswap's $4.9B TVL moat where most MEV still bleeds to block builders.

- 01Flight School buyback-and-lock mechanics↗

The 1,023-click lead article shows readers are tracking the specifics of programmatic AERO removal — bonus rates, lock ratios, and whether the flywheel compounds or stalls.

- 02Aerodrome–Velodrome merger into Aero↗

The Dromos/Aero announcement attracted 435 clicks because the 94.5/4.5 VELO-to-AERO token split and MetaDEX03 architecture directly reset holder value expectations.

- 03veAERO lock saturation and supply compression↗

Multiple articles on near-total max-lock of veAERO supply, plus the Momentum Fund's algorithmic buybacks, collectively drew readers evaluating whether circulating supply can meaningfully decline.

- 04AERO collateral and DeFi composability↗

Headlines on MAI stablecoin collateral and QiDao veAERO relays pulled readers interested in whether vote-escrowed positions can be productively deployed rather than sitting idle.

- 05AERO 2024 performance and Base ecosystem leverage↗

The 3,139% annual gain headline framed AERO as a high-beta Base derivative, prompting debate about whether the move was structural or a liquidity-driven overshoot.

- 06Institutional recognition via Grayscale↗

Grayscale's Q3 portfolio addition of AERO alongside IP signaled to readers a potential legitimacy threshold, lifting the 82-click story above raw DeFi coverage.

AERO Tokenomics: Revenue, Buybacks, and Locks

Zero-Leak Revenue Model and Fee Flows

A defining feature of Aerodrome’s tokenomics is its zero-leak fee model, in which all protocol revenue is routed to governance token holders rather than to LPs. According to tokenomics analyses and monitoring dashboards, the DEX collects swap fees and other sources of income and channels them to veAERO voters as “holders’ revenue,” with no direct fee share allocated to LPs. This is in contrast to many other DEX designs, where LPs receive a fixed portion of trading fees and the protocol or token holders capture only a fraction of the revenue.

Conceptually, Aerodrome’s cash flows can be summarized as follows:

| Role | Main inflows from protocol | Main outflows / costs | Primary risks |

|---|---|---|---|

| veAERO holders | Share of swap fees and protocol revenue; AERO emissions; bribes from external protocols | Cost of locking AERO (illiquidity, price risk) | Governance uncertainty; smart contract risk |

| Liquidity providers (LPs) | AERO emissions from gauges; potentially extra incentives attached to pools | Capital committed to pools; impermanent loss | IL, token volatility, dependence on emissions |

| Protocol treasury / funds | Swap fees (temporarily); potential yield on holdings; ability to direct incentives | Buybacks, grants, emissions funding | Misallocation, sustainability, governance |

Because all fees accrue to veAERO holders, AERO’s value proposition is directly linked to the DEX’s trading volume and fee rates. When volumes are high, the protocol can generate substantial revenue, which can be distributed to veAERO lockers, used for buybacks, or both. For example, monitoring tools have reported weeks in which Aerodrome earned more than a million dollars in revenue, while net locks of AERO exceeded new emissions, effectively shrinking circulating supply over that period. In such conditions, the token behaves in a way that resembles a revenue-sharing equity-like instrument, though without legal ownership rights.

The zero-leak model has implications for LP economics. Since LPs receive no direct fee share, their returns depend heavily on the value of AERO emissions and supplemental incentives. If the AERO price is high, emissions can provide attractive returns; if the price falls, LP yields can diminish rapidly, potentially leading to a decline in liquidity that then feeds back into lower volumes and fee generation. This feedback loop can be virtuous in growth periods but fragile in downturns, which is one reason Aerodrome invests heavily in buybacks, locks, and new mechanisms like Predictive Allocation to stabilize incentives.

Emissions, Epochs, and Gauge Caps

AERO emissions follow an epoch-based schedule governed by smart contracts and subject to parameter changes via governance. Each epoch, a fixed amount of AERO is emitted and allocated across gauges according to veAERO votes, subject to any gauge caps or protocol-level constraints. Over time, emissions are generally designed to decay, reducing inflation and encouraging long-term holding, though the exact shape of the emissions curve can evolve as the protocol matures.

Gauge caps play an important role in preventing runaway concentration. In a purely vote-weighted system with no caps, a coalition controlling a large share of veAERO could direct a disproportionate share of emissions to its preferred pools, potentially starving other parts of the ecosystem. Caps introduce a ceiling on how much any one gauge can receive, forcing large veAERO holders to diversify their votes or accept diminishing marginal returns to concentration.

From a markets perspective, gauge caps and emissions schedules influence the launch rewards that LPs can expect when new pools or chains go live. At the Aero launch, for example, emissions will likely need to be allocated across Base, Optimism, Ethereum mainnet, and possibly Arc, as well as across many asset pairs. Caps can ensure that strategically important pools—such as core ETH, stablecoin, and major governance token pairs—receive substantial but not absolute shares of emissions, while long-tail assets still have a path to attract liquidity through targeted bribes and ecosystem grants.

It is important to recognize that emissions are both an incentive and a liability. They create supply overhang that must be absorbed by buyers or sinks such as locks and burns. AERO’s tokenomics therefore rely heavily on programs that reduce circulating supply and on mechanisms that encourage locked, long-term positions.

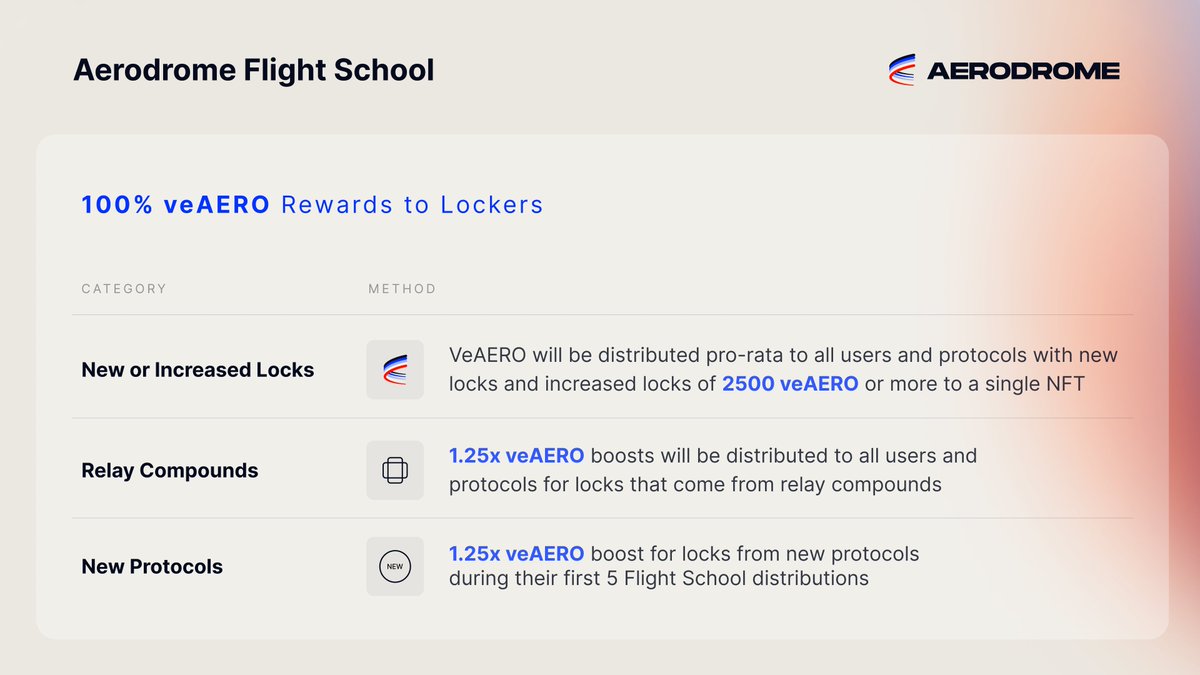

Buybacks, Locks, and Flight School

One of Aerodrome’s most distinctive features is the scale and structure of its buyback-and-lock programs. The protocol’s Public Goods Fund (PGF), alongside initiatives such as Flight School and Relay, has acquired large quantities of AERO on the open market and “max-locked” them into veAERO positions, effectively removing them from liquid circulation for extended periods. In a widely cited update, the Aerodrome team reported that cumulative AERO bought back and locked across these programs had surpassed 180 million tokens, with individual PGF acquisitions of hundreds of thousands of AERO at a time.

Flight School, in particular, has been framed as a program that rewards lockers and ecosystem participants with additional AERO while encouraging long-duration locks. Updates from the project have emphasized that Flight School changes give AERO lockers opportunities to receive the full share of the program’s rewards, further incentivizing veAERO positions over liquid holdings. By tying rewards to locked positions, the protocol attempts to convert speculative demand into committed, governance-aligned ownership.

These buyback and lock programs serve several purposes. First, they reduce circulating supply by moving tokens into long-term lockups, which can offset ongoing emissions and mitigate inflationary pressure. Second, they concentrate voting power in programmatic or community-directed entities like the PGF, which can then steer emissions toward pools deemed strategically important for the ecosystem. Third, they signal confidence and alignment by directing protocol revenue and treasury resources into the token itself, rather than into unrelated expenditures.

However, these programs also create governance and concentration risks. If a large fraction of veAERO is controlled by protocol-run funds, the effective decentralization of governance can be reduced, even if the nominal token distribution is broad. Decisions about how these locked tokens vote—whether via transparent policies, delegated governance, or discretionary management—can significantly shape the DEX’s long-term direction. The balance between supply reduction and governance centralization is therefore a key factor for AERO holders to monitor.

The Momentum Fund and Future Burn Mechanics

Looking ahead to the Aero launch, Dromos Labs has outlined plans for a Momentum Fund that will further integrate buybacks and burns into the protocol’s economics. Public statements indicate that this fund will have mandates that include forward-looking allocation of emissions or incentives to strategically important pools, delegation or extension of allocation power to ecosystem builders, and explicit use of protocol resources to buy back and burn AERO. In effect, this adds a deflationary lever on top of the existing buyback-and-lock mechanisms.

The introduction of a burn component is significant. Whereas locking removes AERO from liquid circulation but leaves it as a claim on future revenue and governance, burning permanently reduces supply. If implemented at scale and funded by sustainable revenue, buyback-and-burn programs can turn an inflationary emissions model into a net-deflationary one, especially once emissions have decayed from their initial high-growth phase. In such a regime, the combination of revenue share, reduced supply, and cross-chain growth could make AERO resemble a quasi-equity instrument in a growing fee-generating platform.

That said, sustainability is the critical question. Buybacks and burns that outpace genuine, fee-based profitability can only be funded by drawing down treasuries or diverting emissions, which may not be durable in adverse market conditions. Moreover, the market may eventually discount buybacks that are perceived as defensive, especially if they are used mainly to support the token price rather than to reflect long-term value creation. For AERO, the success of the Momentum Fund will depend on whether cross-chain expansion, MEV-resistant routing, and Predictive Allocation can drive enough incremental revenue to fund meaningful buybacks without undermining other parts of the ecosystem.

Governance and Predictive Allocation

Vote-Escrow Governance and veAERO

AERO uses a vote-escrow governance model in which users lock their tokens for a specified period to obtain veAERO, a non-transferable token that represents voting power and revenue share. The longer the lock duration and the larger the underlying AERO balance, the greater the veAERO voting power. This model is inherited from Curve and refined by Velodrome and Aerodrome, but adapted to the zero-leak revenue approach and buyback-heavy strategy.

veAERO holders have three primary economic rights. They receive a pro-rata share of the DEX’s protocol revenue, primarily composed of swap fees. They earn additional AERO emissions distributed to voters, which can be viewed as a form of staking yield. And they can collect bribes from external protocols that pay veAERO voters to support specific gauges, effectively turning governance into a marketplace for votes.

These incentives are meant to encourage long-term alignment. Locking AERO reduces sell pressure by removing tokens from the liquid market, while giving lockers a stream of income that depends on the protocol’s health. The illiquidity risk and price volatility of the underlying token, however, mean that locking is not without cost. If AERO’s price falls sharply or if revenue and bribes decline, veAERO holders may find that their locked positions underperform more flexible strategies such as farming emissions and selling them periodically.

The vote-escrow model also shapes the political economy of the protocol. Large veAERO holders, including PGF and other programmatic funds, can exert significant influence over emissions and, by extension, over which protocols on Base and other chains receive subsidized liquidity. This can be positive if used to support genuine ecosystem growth, but it also raises concerns about favoritism, capture, and resistance to new competitors.

Classical Gauge Voting vs Predictive Allocation

Under the classical gauge voting system, veAERO holders cast votes during discrete epochs, often weekly. At the end of each epoch, the distribution of votes determines how AERO emissions are allocated across gauges for the next period. This system introduces a lag between changes in market conditions and changes in emissions. For example, if a new pool suddenly sees a surge in volume and fees, it may have to wait until the next epoch before voters can respond and redirect emissions toward it.

Moreover, the weekly cadence and relatively coarse granularity can lead to misallocation and stale votes. Voters may not update their preferences frequently, especially if transaction costs are non-trivial or if they are satisfied with existing yields. Protocols may overpay for bribes in one epoch and underpay in another, and the system can be gamed by short-term coalitions that concentrate votes in ways that are not reflective of sustainable demand. These frictions can reduce the efficiency of emissions, meaning that a significant share of AERO rewards may go to pools that are not generating commensurate fees or strategic value.

Recognizing these limitations, Dromos Labs has proposed and begun implementing a new mechanism called Predictive Allocation, which will debut fully with the Aero launch. In this system, token voting is made effectively continuous rather than discrete. veAERO holders can update their votes in real time, and the emissions allocation adapts dynamically, with the aim of aligning emissions more closely with current and expected future fee generation.

Predictive Allocation as a New Incentive Primitive

Predictive Allocation reframes gauge voting as a kind of prediction market on future fees. As described by Dromos Labs and summarized by independent commentators, the idea is that casting a vote becomes akin to placing a bet on which pools will generate the most fees in the near future. If a veAERO holder correctly predicts which pools will outperform, their votes will earn more in fees and bribes; if they allocate votes to underperforming pools, their returns will be lower.

This introduces asymmetric payoffs and more immediate feedback into the governance process. Instead of waiting for weekly epochs, voters can monitor fees and yields continuously and reallocate their voting weight as conditions change. In principle, this responsiveness can improve the efficiency of emissions by directing them toward pools that are actually generating value, rather than toward those that happen to have secured votes in a prior epoch. Dromos Labs has suggested that this system could improve the efficiency of rewards distribution by up to 80%, though real-world results will depend on market behavior and implementation details.

From a mechanism design perspective, Predictive Allocation creates several interesting dynamics. It rewards voters who invest in information and monitoring, since better predictions translate into higher returns. It can also reduce the profitability of naive bribery strategies, since paying voters to support an underperforming pool becomes more expensive if those voters can earn more by reallocating to better-performing pools. On the other hand, it may increase complexity for casual participants and could amplify volatility in emissions, as rapid shifts in voting patterns could cause yields on different pools to swing more rapidly.

For AERO, Predictive Allocation may make veAERO an even more active management asset. Holders who simply set-and-forget their votes may see their relative returns decline compared to those who actively rebalance their allocations in response to signals like fee generation, market news, and protocol incentives. This could encourage the emergence of professional vote managers, DAOs, or automated strategies that specialize in optimizing veAERO positions, further deepening the financialization of governance.

Security, Governance Capture, and Centralization Concerns

Any system that ties significant economic value to governance decisions must grapple with security and centralization risks. AERO is no exception. The combination of fee revenue, emissions, and bribes flowing to veAERO elevates the stakes of governance and could make the protocol a target for governance attacks, smart contract exploits, or social engineering campaigns.

On the smart contract side, Aerodrome and the future Aero protocol inherit the standard risks of DeFi. Protocols rely on complex smart contracts to manage pools, gauges, emissions, locking, and cross-chain routing. Vulnerabilities in these contracts—whether due to logic errors, integration bugs, or unforeseen interactions—can lead to loss of funds, misallocation of emissions, or governance failures. As security specialists have emphasized, DeFi protocols must invest heavily in formal audits, continuous monitoring, and defensive design to mitigate these risks. Users, in turn, should recognize that even audited contracts can harbor undiscovered vulnerabilities and that interacting with DeFi carries inherent technical risk.

Governance capture is another concern. Large veAERO holders, including protocol-controlled entities like the PGF and future Momentum Fund, can wield outsized influence over emissions and policy. While these entities are designed to support ecosystem growth—by funding public goods, strategically allocating incentives, and using buybacks to align interests—their control also creates a single point of failure. Disagreements over how these funds are managed, or over their transparency and accountability, could become flashpoints within the community.

Bribes and external incentives complicate this further. While they are a core feature of the model, enabling protocols to pay for liquidity rather than rely solely on organic demand, they can also distort decision-making if voters prioritize short-term bribe income over long-term protocol health. Predictive Allocation may mitigate some of this by tying returns more tightly to fee outcomes, but it will not eliminate the possibility of coordinated campaigns to direct emissions to politically favored pools.

Finally, cross-chain expansion raises additional governance and security challenges. As Aero integrates deployments on Ethereum mainnet, Arc, and potentially other chains like Tron via its SuperSwaps and MetaDEX architecture, it will need robust mechanisms for cross-chain message passing, state synchronization, and governance coordination. Each additional chain introduces its own trust model, security assumptions, and regulatory context, increasing the surface area for potential attacks or failures. For AERO holders, this expansion promises new revenue opportunities but also new vectors of risk.

Aerodrome is introducing a Market-Aware buyback model through its upcoming Momentum Fund, using algorithmic, volatility-responsive rules to acquire AERO more efficiently than fixed schedules or discretionary buys. The pilot showed strong results, accumulating 8.7M AERO and scaling buy pressure during high volatility, with plans to consolidate capital programs and introduce buyback-and-burns to strengthen long-term protocol economics.

"This pilot serves as the prologue to a larger structural shift. The Public Goods Fund and Flight School programs will soon be consolidated into the Momentum Fund, a unified capital allocation engine. Once active, this engine will apply the same market-aware framework at an institutional scale, pairing governance influence with disciplined capital deployment. The objective is to support strategic pools, reduce floating supply, and strengthen the Aerodrome economy. Furthermore, the Momentum Fund will introduce buyback-and-burns, permanently removing AERO from circulation when specific market conditions are met."

Aerodrome launches on Base mainnet

Predictive Allocation feature announced

AERO posts 3,139% annual gain; user activity up ~800%

Grayscale adds AERO to Q3/Q4 portfolio alongside Story (IP)

Flight School bonus reaches record 60%; total buybacks exceed 180M AERO

Dromos Labs announces Aero merger of Aerodrome and Velodrome on MetaDEX03

Aerodrome–Velodrome merger scheduled; VELO convertible at 0.55 AERO

AERO in Practice: Markets, Integrations, and Use Cases

Trading Venues and Access

AERO’s primary on-chain home is Aerodrome itself on Base, where it trades in various pools against USDC, ETH, and other assets. As Aerodrome has grown into Base’s central liquidity hub, AERO’s markets on-chain have become relatively deep and integrated into the broader Base ecosystem. Traders can access AERO via decentralized interfaces, aggregators, and Base-native wallets.

Off-chain, AERO has begun to appear on centralized and hybrid platforms as well. Robinhood has announced that AERO is available for trading on its Robinhood Legend platform alongside other assets like QNT and ZRO, signaling growing retail accessibility through familiar brokerage-style interfaces. This expanded access can increase liquidity and price discovery but also exposes AERO to a wider base of users who may be less familiar with DeFi’s underlying risks and mechanisms.

Perhaps more structurally significant is the way Coinbase has integrated Base tokens into its main consumer app. Upgrades to Coinbase’s interface have effectively allowed users of the main app—not just the Coinbase Wallet—to access and trade tokens that live on the Base network, including those listed primarily on DEXs like Aerodrome. Commentators have described this as Coinbase having “de facto listed” every Base token, since users can route trades through underlying DEX liquidity without each token undergoing a traditional exchange listing process. For AERO, this means that a substantial portion of Coinbase’s user base can, in principle, gain exposure to the token via Base DEX liquidity, even if AERO is not explicitly listed as a conventional spot asset on the central limit order book.

As Aero rolls out on Ethereum mainnet and other chains, AERO’s trading venues are likely to diversify further. Integration into on-chain routing aggregators, cross-chain bridges, and potentially more centralized exchanges will play a role in determining its liquidity profile and accessibility to different classes of investors.

Market Structure, Liquidity, and Volume

Aerodrome’s position as the leading DEX on Base has translated into substantial trading volumes and fee generation, which in turn underpin AERO’s revenue-sharing model. The project has highlighted that Aerodrome has processed more than 70 billion dollars in trading volume on Base over a single year, more than double the volume of the next-best DEX on that chain over the same period. Data platforms tracking Aerodrome’s total value locked, daily volumes, and accumulated fees have consistently ranked it as one of the top protocols in the Base ecosystem.

This market structure has several implications for AERO. When large volumes flow through Aerodrome’s pools, swap fees accumulate and are distributed to veAERO holders as revenue. High volume also tends to attract more protocols to launch liquidity on Aerodrome, which can increase demand for AERO via bribes and emissions competition. The combination of volume-driven revenue and demand for governance influence can create reinforcing flywheels in favorable markets.

At the same time, Aerodrome’s liquidity is not monolithic. It spans everything from core blue-chip pairs like ETH–USDC to more experimental or niche pools, including governance tokens from emerging protocols (such as TEA or PROS) and even fan tokens associated with major football clubs like PSG and Arsenal’s AFC, which have launched USDC pools eligible for AERO emissions. These pools allow diverse assets to tap into Aerodrome’s incentive engine, but they also introduce varying levels of risk. Some asset pairs may be relatively stable and liquid; others may be thinly traded or highly volatile, with LPs heavily reliant on AERO emissions and external incentives to justify their risk exposure.

Coverage of individual pools has underscored that AERO emissions can create both opportunities and hazards. For example, pools that become eligible for emissions—such as certain OFC–USDC, WETH, or KAT–USDC pairs—may attract capital seeking high yields, but also face sell pressure as farmers harvest and dump AERO rewards or underlying tokens. In such cases, the interplay between emissions, token price dynamics, and LP behavior can be fragile, leading to sudden shifts in liquidity and market depth if conditions change.

AERO as Yield and Collateral

From an investor’s perspective, AERO can be thought of as a yield-bearing governance asset when locked and as a speculative token when held liquid. Locking AERO into veAERO gives access to fee revenue, emissions, and bribes, which together can produce attractive yields in favorable conditions. These yields are not guaranteed and depend on factors such as trading volume on Aerodrome, the intensity of bribe competition among protocols, and the AERO emissions schedule.

In addition, AERO’s integration into wider DeFi can allow it to be used as collateral in lending protocols, staked in derivative strategies, or pooled in structured products. The specifics of these integrations vary over time and across platforms and are sensitive to risk assessments, oracle availability, and regulatory considerations. In general, protocols that accept AERO as collateral must grapple with its governance-linked nature: a large leveraged position in AERO could give the holder both financial exposure and disproportionate voting power, raising the stakes of liquidation cascades or governance-driven market moves.

For yield-focused participants, the trade-off is between locking vs. farming vs. trading. Locking AERO into veAERO sacrifices liquidity but can generate a relatively predictable stream of protocol revenue and bribe income, especially for those who actively manage their votes under Predictive Allocation. Farming emissions by providing liquidity to AERO pairs allows users to accumulate more AERO but exposes them to impermanent loss and the risk that emissions lose value if AERO’s price declines. Trading or holding AERO liquid keeps options open but forfeits direct participation in protocol revenue and governance.

Institutional and Retail Positioning

AERO’s emergence has not gone unnoticed by institutional and structured products. At various points, AERO exposure has appeared in DeFi-focused investment vehicles, such as diversified funds that rebalance among major protocol tokens. In some cases, these funds have added AERO during periods of strong growth and reduced or removed exposure when seeking to rotate into other opportunities, reflecting an ongoing reassessment of where DeFi value accrues over time. These shifts underscore that AERO is competing not only with other DEX tokens but also with newer primitives in areas like real-world assets, restaking, or stablecoin infrastructure.

On the retail side, the inclusion of AERO on platforms like Robinhood Legend and its indirect availability via Coinbase’s Base integration expand the token’s audience beyond DeFi-native users. This can deepen liquidity and broaden participation in Aerodrome’s economics, but it also puts a premium on clear, accessible explanations of the token’s risks and mechanics. Retail users who buy AERO on a centralized platform may not immediately realize that the core value proposition lies in locking into veAERO, directing emissions, and capturing protocol revenue—activities that typically require on-chain interactions.

As Aero launches on Ethereum and other chains, and as Predictive Allocation and the Momentum Fund shift the dynamics of emissions and buybacks, institutional and retail investors alike will have to reassess how AERO fits into their portfolios. Its role as a cross-chain liquidity governance token, rather than a simple DEX reward token, may make it more attractive to some classes of sophisticated investors while increasing complexity for others.

Risks and Considerations

Smart Contract, MEV, and Cross-Chain Risks

Engaging with AERO and Aerodrome entails exposure to the standard array of DeFi smart contract risks. Protocols like Aerodrome rely on intricate smart contracts to manage liquidity pools, gauge voting, locking schedules, fee accounting, and emissions. Vulnerabilities in these contracts—ranging from reentrancy bugs to logical errors in accounting—can result in loss of funds, misallocation of rewards, or governance malfunctions. Security research has repeatedly shown that even well-audited contracts can harbor subtle vulnerabilities, and that updates, integrations, or new deployments can introduce fresh attack surfaces.

The shift to MEV-resistant pools, while potentially improving execution quality and fee efficiency, adds its own layer of complexity. Designs that involve batch auctions, specialized routing logic, or interaction with off-chain order flow must be carefully vetted to ensure they do not create unexpected failure modes or centralization points. For example, reliance on specific relayers or block builders could give those actors undue influence over trade ordering, while poorly implemented MEV mitigation could be circumvented by sophisticated actors.

Cross-chain expansion compounds these challenges. Aero’s plans to operate across Base, Optimism, Ethereum mainnet, Arc, and potentially other chains imply the need for robust cross-chain messaging and state synchronization. Bridges and cross-chain messaging protocols are historically among the most attacked components in the DeFi stack, with numerous high-profile exploits resulting from compromised validators, misconfigured contracts, or mismatched security assumptions. While designs like “SuperSwaps” and MetaDEX architectures aim to abstract away some of these concerns by managing liquidity routing at the DEX level, the underlying cross-chain infrastructure remains subject to the usual risks.

For AERO holders and LPs, these risks manifest as potential loss of funds in pools, disruption of fee and emission flows, or dilution of governance if malicious actors can exploit cross-chain vulnerabilities to manipulate state. Diversification, risk management, and careful attention to the protocol’s security posture and incident response plans are therefore important considerations.

Emissions Dependence and Flywheel Fragility

AERO’s model relies heavily on emissions to compensate LPs and to incentivize locking and governance participation. Emissions are a powerful growth tool: they can bootstrap liquidity, attract protocols to launch pools, and reward early adopters. However, they also create a flywheel that can spin in both directions.

In the positive direction, rising token prices make emissions more valuable. Higher emissions value attracts more LPs, increasing liquidity and tightening spreads, which attracts more trading volume. Greater volume leads to higher fee revenue and more bribes from protocols competing for liquidity, which in turn increases the yields available to veAERO lockers, driving demand to lock more AERO and reinforcing price support and supply reduction.

In the negative direction, falling token prices reduce the real-world value of emissions. LPs who were attracted by high nominal yields may withdraw liquidity when those yields collapse in dollar terms, leading to wider spreads and reduced execution quality. Lower liquidity can cause trading volumes and fees to decline, reducing revenue available for veAERO holders and buybacks. Protocols may cut back on bribes if they perceive that emissions are no longer delivering sufficient liquidity. This can weaken demand for veAERO, reduce locking, and increase sell pressure as emissions and unlocked tokens hit the market, potentially triggering further price declines.

Analysts have highlighted this flywheel fragility in the context of specific Aerodrome pools, where high AERO emissions have temporarily supported liquidity in niche pairs, only for that liquidity to evaporate when emissions or prices changed. Pools involving thinly traded or experimental assets are particularly susceptible: they may attract opportunistic capital chasing AERO rewards, but face rapid outflows and price dislocations when those rewards decline or when token prices move adversely. For LPs, this underscores the importance of evaluating not just headline yields but also the sustainability of emissions, the underlying asset quality, and the broader market context.

Base Dependency and Regulatory Overhang

Although Aero aims to be cross-chain, Aerodrome’s current footprint and AERO’s economic base are heavily tied to Base, which is operated in close conjunction with Coinbase. This confers both advantages and risks. On the positive side, Base’s association with Coinbase provides access to a large existing user base, integration into mainstream platforms, and potential regulatory and compliance expertise. The network has benefited from Coinbase-led promotion and from being a natural venue for Coinbase-originating projects and assets.

On the risk side, concentration on a single L2 with a prominent centralized sponsor exposes Aerodrome and AERO to platform, regulatory, and business-model risk. Changes in Coinbase’s strategic priorities, regulatory environment, or risk appetite could affect Base’s trajectory and, by extension, the activity on Aerodrome. For example, more stringent regulatory scrutiny of DeFi, tighter controls on off-ramp access, or shifting policy positions on token listings could influence the flow of capital into and out of Base and protocols like Aerodrome.

Moreover, Base itself is subject to the technical and governance risks of optimistic rollups, including delays and complexity in withdrawals, reliance on specific sequencer and validator arrangements, and evolving decentralization roadmaps. While the OP Superchain vision aims to distribute governance and security across multiple stakeholders, the path and timeline for that distribution remain subjects of ongoing work.

Aero’s planned deployments on Ethereum mainnet and Arc diversify some of this chain-specific risk but introduce their own regulatory complexities. Arc, in particular, is a permissioned network geared toward institutions and compliant USDC flows; operating a DEX in that environment will require careful navigation of KYC, AML, and securities law considerations. How AERO’s governance and revenue-sharing features intersect with those regimes is an open question that may evolve as regulators and market participants gain more experience with such hybrid structures.

Governance, Buyback Concentration, and Sustainability

Finally, AERO’s heavy reliance on protocol-run funds and buyback programs raises questions about governance concentration and long-term sustainability. The PGF, Flight School, Relay, and future Momentum Fund collectively control a significant and growing share of locked AERO, giving them substantial influence over emissions, gauge configurations, and strategic priorities. While these entities are positioned as stewards of the ecosystem, the concentration of voting power in a relatively small set of hands can be at odds with decentralization ideals.

The sustainability of buyback-heavy strategies also depends on robust, recurring revenue. If fee income and bribes are sufficient to fund buybacks and burns without compromising other investments, the model can support long-term value accrual to AERO holders. If, however, buybacks are funded primarily by emissions or by drawing down treasuries accumulated under different assumptions, the dynamic may resemble financial engineering more than sustainable profitability. Market observers have noted that periods of reduced buyback activity or shifts in buyback policy can coincide with increased price volatility or breaks of technical support levels, underscoring the market’s sensitivity to these programs.

For token holders and potential investors, these dynamics highlight the importance of looking beyond headline metrics like total buybacks or locks and toward deeper indicators: the ratio of revenue to emissions, the share of supply controlled by protocol entities, the transparency of governance, and the adaptability of the tokenomics to changing market conditions.

Aerodrome inherits the Velodrome ve(3,3) codebase with incremental upgrades (MetaDEX03 in progress); the merger migration path introduces new upgrade surface before audits on the unified architecture are complete.

Virtually all TVL and fee revenue originates on Base; a slowdown in Base user activity or a competing L2 incentive program would directly compress AERO emissions value and veAERO yield.

AERO relies on continuous buyback-and-lock programs (Flight School, PGF, Momentum Fund) to offset protocol emissions; if buy pressure softens relative to emissions, circulating supply expands and voter yields fall.

The Public Goods Fund and Flight School are team-directed capital programs; veAERO voting power concentration among max-lockers further narrows effective governance to long-term insiders.

AERO's use as collateral for the MAI stablecoin on Base and its listing on Robinhood increase regulatory surface area, particularly as U.S. regulators scrutinize DeFi yield products and stablecoin collateral structures.

The Aerodrome–Velodrome consolidation into Aero requires migrating two live protocols, a new token distribution (94.5/4.5 split), and adoption of MetaDEX03 architecture simultaneously, creating a multi-month execution risk window.

Conclusion

AERO represents a sophisticated attempt to align the incentives of traders, liquidity providers, protocol builders, and long-term token holders around a central liquidity hub in the Ethereum layer-2 ecosystem. Through Aerodrome on Base and the forthcoming cross-chain Aero DEX, AERO underpins a design that combines Solidly-style vote-escrow governance, gauge-directed emissions, a zero-leak revenue model, and aggressive buyback-and-lock strategies. This architecture has allowed Aerodrome to capture a large share of Base’s trading volume and fees, while positioning AERO as a key governance asset for protocols seeking liquidity within the OP Superchain and beyond.

The merger of Aerodrome and Velodrome into Aero, the rollout of Predictive Allocation, and the establishment of the Momentum Fund mark the next phase in AERO’s evolution. These changes aim to make emissions more capital-efficient, direct liquidity incentives more precisely toward value-generating pools, and enhance long-term value accrual to AERO holders via buybacks and burns. At the same time, they increase the complexity of the system and raise new questions about governance centralization, cross-chain security, and the sustainability of subsidy-driven liquidity.

From a market perspective, AERO is both a yield-bearing governance token and a bet on the success of a particular DEX architecture as a dominant liquidity layer across multiple chains. Its value is linked to trading volume on Aerodrome and future Aero deployments, to the robustness of its smart contracts and cross-chain infrastructure, and to the continued relevance of vote-escrow and bribe-driven models in an increasingly competitive DeFi landscape. As with any crypto asset, especially one deeply intertwined with experimental mechanism design, the upside potential is matched by material technical, economic, and governance risks.

For sophisticated participants, the key to engaging with AERO is understanding these trade-offs. veAERO can provide exposure to protocol revenue and bribes but requires locking and active governance participation. LP positions can earn attractive emissions but are exposed to impermanent loss and flywheel fragility. Holding AERO liquid offers flexibility but foregoes direct participation in the protocol’s cash flows. Navigating these choices requires not only a grasp of AERO’s current mechanics but also an appreciation of how its tokenomics may evolve as Aero launches, cross-chain expansion progresses, and DeFi market structure continues to change.

Outlook

Looking ahead, AERO’s trajectory will be shaped by three intertwined developments. First, the Aero launch and cross-chain expansion will test whether Aerodrome’s model can compete effectively on Ethereum mainnet and in institutional environments like Arc, alongside incumbents such as Uniswap and Curve. Success would deepen AERO’s fee base and solidify its role as a cross-chain liquidity governance token; setbacks could expose the limits of emissions- and bribe-driven designs in more mature markets.

Second, the practical impact of Predictive Allocation will reveal whether continuous, prediction-market-like governance can meaningfully improve the efficiency of emissions and reduce wasteful liquidity subsidies. If the mechanism works as intended, it could become a template for other DEXs seeking to refine their incentive systems. If it proves too complex or prone to new forms of manipulation, it may require further iteration or complementing mechanisms.

Third, the long-term sustainability of buybacks, locks, and the Momentum Fund will depend on the protocol’s ability to generate durable, fee-based profitability and to manage governance concentration responsibly. AERO’s appeal as a quasi-equity-like asset rests on the idea that it can capture a significant share of DeFi trading revenue across chains while gradually reducing its circulating supply through economically justified buybacks and burns. Whether that vision is realized will be determined over years, not months, and will require careful balancing of growth, risk management, and community governance.

For now, AERO stands as one of the more ambitious experiments in DEX tokenomics and cross-chain liquidity infrastructure. It offers a rich case study for anyone interested in how incentives, governance, and market structure intersect in DeFi—and a reminder that the most promising designs often carry the most intricate trade-offs.

Latest AERO news

Aerodrome’s Ethereum expansion could transform AERO into cross-chain exchange infrastructure, but sustainable growth hinges on reducing subsidy-driven liquidityAerodrome and Velodrome to merge in July, with $VELO fungible for 0.55 $AEROAerodrome is introducing a Market-Aware buyback model through its upcoming Momentum Fund, using algorithmic, volatility-responsive rules to acquire AERO more efficiently than fixed schedules or discretionary buys. The pilot showed strong results, accumulating 8.7M AERO and scaling buy pressure during high volatility, with plans to consolidate capital programs and introduce buyback-and-burns to strengthen long-term protocol economics. Aerodrome releases FAQ with more details on the previously announced AERO product

Aerodrome releases FAQ with more details on the previously announced AERO product Dromos Labs announce Aero, the new liquidity hub meant to unite and bring together the best of both Aerodrome and Velodrome, built on the new MetaDEX03 architectureDromos announces Aero, an expansion to mainnet via a merger between Aerodrome and Velodrome, with a token distributed to current VELO & AERO holders spilt 94.5/4.5 based on annual revenue

Dromos Labs announce Aero, the new liquidity hub meant to unite and bring together the best of both Aerodrome and Velodrome, built on the new MetaDEX03 architectureDromos announces Aero, an expansion to mainnet via a merger between Aerodrome and Velodrome, with a token distributed to current VELO & AERO holders spilt 94.5/4.5 based on annual revenueSources

- https://coinmarketcap.com/currencies/aerodrome-finance/

- https://aerodrome.finance/docs

- https://x.com/AerodromeFi?lang=en

- https://x.com/0xchainink/status/2066883582447210617

- https://coinmarketcap.com/cmc-ai/velodrome-finance/latest-updates/

- https://x.com/valueverse_ai/status/2038947103603327306

- https://vansairforce.net/threads/aero-momentum-engines.233126/

- https://x.com/AerodromeFi/status/2034287278475133122

- https://tokenomics.com/articles/aerodrome-tokenomics-how-aero-captures-100-of-protocol-fees

- https://dune.com/0xkhmer/aerodrome

- https://www.dlnews.com/articles/defi/aerodrome-creator-announces-predictive-allocation-feature/

- https://x.com/wagmiAlexander/status/1998865700157534573

- https://defillama.com/protocol/aerodrome

- https://www.youtube.com/watch?v=3LgExmfNwXg

- https://www.facebook.com/robinhoodapp/posts/aero-qnt-and-zro-are-now-available-to-trade-on-robinhood-legend/1299260275715441/

- https://www.facebook.com/jhunter101/posts/bitcoin-hitting-100k-isnt-the-biggest-storyits-what-smart-money-is-doing-behind-/3508598382774382/

- https://x.com/lachlanalextodd/status/1863772357418156408

- https://x.com/AerodromeFi/status/1807049888271896977

- https://x.com/wagmiAlexander/status/2052843303843008744

- https://salusec.io/blog/3_defi-security

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…