Deep dive on Brazil’s evolving crypto landscape, covering regulation, taxes, Drex CBDC, Pix, stablecoins, crime, tokenized RWAs, mining and talent trends for investors, builders and policymakers.

+15 sources across the wider coverage universe

Brazil bans prediction markets like Polymarket and Kalshi, citing investor protection risks and rising gambling concerns under new betting regulations2026-04

Brazil bans prediction markets like Polymarket and Kalshi, citing investor protection risks and rising gambling concerns under new betting regulations2026-04 Brazil Postpones Crypto Tax Plan Until After October Presidential Election2026-03

Brazil Postpones Crypto Tax Plan Until After October Presidential Election2026-03 Brazil central bank bans crypto use in regulated cross-border eFX payment rails, forcing providers to rely on FX transactions and tightening control over stablecoin flows2026-05

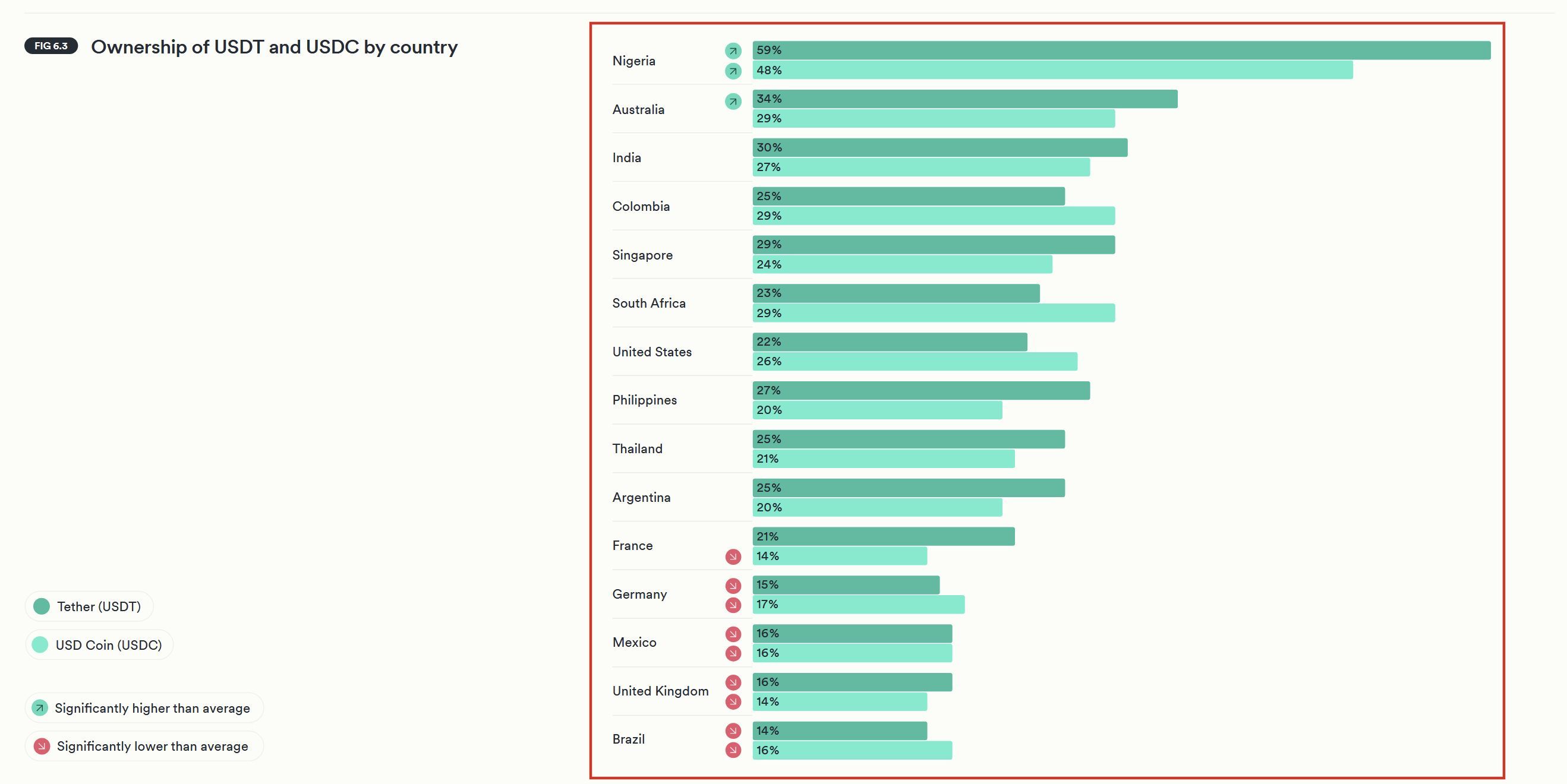

Brazil central bank bans crypto use in regulated cross-border eFX payment rails, forcing providers to rely on FX transactions and tightening control over stablecoin flows2026-05 USDT still leads global stablecoin ownership, but USDC is gaining ground across markets like the U.S., Germany and Brazil, signaling a shift toward regulated stablecoins.2026-03

USDT still leads global stablecoin ownership, but USDC is gaining ground across markets like the U.S., Germany and Brazil, signaling a shift toward regulated stablecoins.2026-03 Brazil's B3 exchange rolls out bitcoin event contracts restricted to investors with $1.9M+ in assets2026-04

Brazil's B3 exchange rolls out bitcoin event contracts restricted to investors with $1.9M+ in assets2026-04 Brazil advances Bill 4308 banning algo stables like USDe and FrxUSD, requiring segregated reserves and 8-year jail terms for issuers2026-02

Brazil advances Bill 4308 banning algo stables like USDe and FrxUSD, requiring segregated reserves and 8-year jail terms for issuers2026-02

Brazil and Crypto: Regulation, Markets, and Innovation

As Latin America’s largest economy, Brazil has quietly become one of the world’s most important testbeds for digital assets, combining high retail adoption with ambitious experiments in payments, tokenization, and central bank digital currency. At the same time, policymakers are building one of the most comprehensive regulatory and tax frameworks in the Global South, tightening controls on crime and cross‑border flows while trying to keep room for innovation.

Brazil’s Place in Global Crypto Adoption

Brazil’s rise in the digital asset landscape is best understood against its broader economic and financial backdrop. The country has a long history of financial innovation driven by inflation episodes, a large unbanked population, and a highly concentrated banking system, all of which created strong incentives to modernize payments and expand access to financial services. The rollout of the instant payments system Pix gave almost every Brazilian with a smartphone access to real‑time, low‑cost transfers, and that experience with digital money has made it easier for users to understand and engage with cryptocurrencies as another layer on top of their financial lives. Together, a large tech‑savvy youth population, widespread mobile internet, and an active fintech sector have made Brazil fertile ground for both speculative and utilitarian crypto use.

On‑chain data helps quantify this position. Chainalysis’ Global Crypto Adoption Index for 2025 ranks Brazil among the top five countries worldwide, behind India, the United States, Pakistan, and Vietnam, reflecting a strong combination of retail usage and institutional activity. Over the twelve months ending in mid‑2025, Latin America as a region saw crypto adoption grow by roughly 63%, and Brazil accounts for a significant share of that growth in both transaction volume and the diversity of use cases. Chainalysis estimates that between July 2024 and June 2025, Brazil alone received about 318 billion U.S. dollars’ worth of cryptocurrency on‑chain, representing roughly one‑third of all crypto value flowing into Latin America over that period. These figures underscore that Brazil is not merely a regional follower; it is one of the global hubs where the next phase of digital asset regulation, infrastructure, and business models is being worked out in real time.

The Brazilian market is also distinctive in that crypto exists alongside a deeply successful public digital payments project rather than in its absence. Pix has achieved near‑universal adoption across income segments and regions, demonstrating that state‑led infrastructure, if designed well, can deliver instant settlement, strong interoperability, and low fees at scale. This raises the bar for private crypto payment solutions, which must compete not with slow legacy rails but with Pix’s convenience. As a result, many Brazilian crypto users gravitate toward crypto primarily as an investment, a hedge, or exposure to new asset classes like tokenized real‑world assets, while relying on Pix and traditional banking for everyday domestic payments. Understanding this layered landscape is essential for appreciating why Brazilian regulators have simultaneously embraced innovation like central bank digital currency and hardened their stance on certain forms of private crypto use, particularly in cross‑border contexts.

Brazil bans prediction markets like Polymarket and Kalshi, citing investor protection risks and rising gambling concerns under new betting regulations

Polymarket saw heavy Brazilian flow during the 2022 Lula-Bolsonaro election, so what matters is whether Polygon onchain access stays open or gets DNS-blocked at the ISP level. Brazil legalized fixed-odds sports betting last year and the public health backlash has been intense — prediction markets are getting bucketed with sportsbooks regardless of how the CFTC classifies Kalshi-style derivatives. Watch for Brazilian banks to start flagging fiat-to-crypto rails for wallets with prediction market history; that's the actual chokepoint, not the front-end ban.

Brazilian readers click heaviest on state-mediated access stories — CBDC pilots, PIX-rails stablecoin integration, and exchange licensing — revealing that the dominant reader concern is not whether crypto works in Brazil, but whether the Brazilian government will let it.↗

Regulatory Architecture: Who Oversees Crypto in Brazil?

The New Crypto Asset Framework and SPSAV Licensing

Brazil’s regulatory regime for crypto is transitioning from patchwork guidance to a comprehensive framework that treats major crypto activities as part of the mainstream financial sector. At the heart of this shift is a new authorization pathway under which custodians, exchanges, and intermediaries must apply to become Sociedades Prestadoras de Serviços de Ativos Virtuais (SPSAVs), or “virtual asset service provider companies,” supervised by the Central Bank of Brazil (BCB). This regime effectively extends the same standards that apply to traditional financial institutions to core crypto businesses, including prudential requirements, governance expectations, and conduct rules. The choice of the central bank as lead supervisor underscores the perception that crypto markets can impact financial stability and payment system integrity, rather than being treated solely as a niche technology or speculative phenomenon.

Under the SPSAV framework, both domestic and foreign firms face stringent entry conditions. Overseas companies that wish to operate in the Brazilian market may not simply serve Brazilian residents from offshore platforms; they must either establish a physical local presence, such as a subsidiary, or partner with a licensed local entity before commencing operations. This requirement is designed to give regulators jurisdictional leverage and to ensure that Brazilian consumer protection and AML rules apply effectively, rather than being circumvented by cross‑border digital business models. Licensed SPSAVs must meet minimum capital thresholds ranging from roughly 10.8 million to 37.2 million Brazilian reais, depending on the type and scale of activities they conduct, aligning prudential expectations with the risk profile of each business model. They are also required to segregate client assets from their own balance sheets, prohibit the use of customer funds for proprietary purposes, appoint responsible individuals for each area of activity, and submit to independent audits and comprehensive public disclosure obligations around their business models, fees, and risks. These measures collectively aim to reduce the likelihood of FTX‑style collapses hurting Brazilian users and to integrate crypto service providers more tightly into the country’s regulatory perimeter.

The implementation of this framework has significant implications for global exchanges and service providers that see Brazil as a strategic growth market. Firms that previously operated on a largely cross‑border basis must now plan for domestic licensing, capital allocation, and localized compliance, often hiring country managers with strong regulatory backgrounds to navigate the process. Industry coverage has highlighted how some major exchanges have reshuffled leadership to emphasize regulatory expertise in Brazil, anticipating that SPSAV authorization will become a de facto license to operate in one of the world’s largest crypto economies. In parallel, domestic fintechs that previously offered crypto alongside broader digital banking services are having to decide whether to spin off dedicated SPSAV entities or significantly upgrade compliance functions within their existing corporate structures. The result is a steady professionalization of the sector, as crypto operations begin to resemble other regulated financial businesses in terms of governance and oversight, even if the underlying tech remains novel.

Dividing Lines: Central Bank, Securities Regulator, and Tax Authority

The Central Bank of Brazil is not the only public institution shaping the country’s crypto landscape. The securities regulator, Comissão de Valores Mobiliários (CVM), has issued detailed guidelines clarifying when crypto assets qualify as securities under Brazilian law, thereby falling within its jurisdiction. In its consolidated guidance, CVM emphasizes that tokens representing debt, equity, or investment contracts with an expectation of profit derived from the efforts of others are treated as securities, regardless of the technological form they take. This classification pulls many tokenized real‑world assets—such as tokenized debentures or fund shares—into the realm of traditional securities regulation, requiring registration, disclosure, and ongoing reporting consistent with existing capital markets rules. CVM’s stance provides a legal foundation for Brazil’s experiments with tokenized bonds and investment funds, while also drawing a clear line between pure payment tokens or certain utility tokens and regulated securities.

Alongside these financial regulators stands the Federal Revenue Service, known locally as the Receita Federal do Brasil (RFB), which is responsible for administering crypto taxation and reporting obligations. RFB has already introduced a flat 15% tax rate on income from crypto assets held abroad by Brazilian residents, effective from early 2024, marking an effort to bring offshore and self‑custodied holdings into the tax net. Later, the government announced a shift to a 17.5% flat tax on crypto capital gains more broadly, including gains from offshore and self‑custodial holdings, with the policy taking effect in mid‑2025. According to reporting, plans for further adjustments or tightening of crypto tax rules were subsequently frozen ahead of a contentious presidential election, underscoring how politically sensitive digital asset taxation has become in Brazil. The RFB has also put forward a consultation to revise Normative Instruction 1888/2019, dramatically expanding the scope and granularity of reporting required from both Brazilian entities and residents engaging in crypto transactions. This proposed regime, discussed in more detail below, gives the tax authority a central role in monitoring the crypto economy, not just for revenue collection but also as a source of data for financial crime enforcement.

Taken together, Brazil’s institutional architecture for digital assets is relatively clear by emerging‑markets standards. The central bank oversees core VASPs and payment‑related implications; the securities regulator governs tokenized securities and investment contracts; and the tax authority tracks income, capital gains, and transactional activity, increasingly in coordination with global standards like the FATF Travel Rule. Additional actors such as ANBIMA, the capital markets association, and SERPRO, the federal data processing service, play important supporting roles as industry coordinators and public‑sector technology partners. This networked approach does not eliminate regulatory uncertainty, particularly for new DeFi or multi‑chain business models, but it provides a comparatively coherent starting point as Brazil continues to refine how crypto fits into its broader financial system.

Digital Payments, CBDC, and Stablecoins

Pix: The Foundation of Digital Money in Brazil

Any explanation of Brazil’s crypto ecosystem must start with Pix, the instant payment system that has transformed how Brazilians move money. Launched by the Central Bank of Brazil, Pix provides 24/7, real‑time transfers between accounts using simple identifiers like phone numbers, email addresses, or randomly generated keys, at very low or zero cost to end users. An IMF analysis of Pix highlights design features such as mandatory participation for major banks, open access for non‑bank institutions, and the use of standardized messaging that together foster strong competition and interoperability among providers. These choices reduced frictions that had historically limited electronic payments, rapidly increasing both the volume and value of digital transactions across the country. As small merchants, gig workers, and informal businesses adopted Pix en masse, cash usage declined and digital account ownership expanded, particularly among lower‑income and previously unbanked segments.

For crypto, Pix is both a complement and a competitor. On the one hand, it dramatically lowers the barriers for people to move fiat into and out of crypto platforms, since users can fund exchange accounts or P2P trades instantly from their bank accounts without paying card or boleto fees. On the other hand, Pix already delivers key value propositions often advertised by crypto payment projects, such as instant settlement and low transaction costs, but with state backing and bank‑grade consumer protections. This reduces the immediate need for cryptocurrencies as a domestic payment medium, steering most users toward treating crypto primarily as an investment, a speculative asset, or a tool for specific use cases like cross‑border transfers or access to dollar‑linked stablecoins. In effect, Pix has set a high baseline for digital money, meaning that crypto projects seeking adoption in Brazil must either provide clearly differentiated features—such as censorship‑resistance, synthetic dollar exposure, or programmable settlement—or focus on asset classes and services that go beyond simple person‑to‑person payments.

The success of Pix also shapes how regulators evaluate new payment‑related crypto services. Since BCB already operates a widely trusted instant settlement system, it is less likely to tolerate parallel, unregulated payment rails that could fragment liquidity, undermine AML controls, or expose consumers to hidden risks. This helps explain why the central bank has been comparatively assertive in its oversight of stablecoin‑based cross‑border payments and crypto‑settled foreign exchange, as discussed in the next subsection. At the same time, Pix’s architecture and governance provide a blueprint for how public infrastructure can coexist with private innovation, an experience that informs Brazil’s approach to its central bank digital currency project, Drex.

Drex: Brazil’s CBDC and Tokenized Financial Infrastructure

Brazil’s central bank digital currency initiative, known as Drex, is not simply a digital version of the real but an ambitious attempt to build a shared tokenization infrastructure for the entire financial system. The BCB’s official materials describe Drex as a platform where tokenized deposits, government securities, and potentially other financial instruments can coexist on a distributed ledger, enabling programmable transactions and new forms of financial intermediation. In early 2023, the central bank revised Drex’s guidelines and set out directives for a pilot project—“Piloto Drex”—with the goal of completing this phase by the end of 2024. The pilot involves a consortium of banks, fintechs, and market infrastructure providers testing use cases such as tokenized bank deposits for retail payments, delivery‑versus‑payment for tokenized securities, and other on‑chain operations that require coordination among multiple institutions.

Commentary on Drex in the context of “convergent digital infrastructure” emphasizes that Brazil’s CBDC project reflects a shift from experimental cryptography toward productive financial infrastructure. Rather than positioning Drex as a standalone retail CBDC that competes with bank deposits, the BCB has framed it as a platform where commercial bank money, tokenized government instruments, and potentially other assets can be represented as tokens and transacted via smart contracts. This architecture blurs the line between CBDC, tokenized deposits, and tokenized securities, allowing for more integrated settlement of complex financial transactions. For example, a consumer credit contract could be programmed to automatically deduct payments from tokenized deposits, while collateral is represented as tokenized debentures or government bonds, all settled instantly on the Drex ledger. In the longer term, such a system could make it easier to launch programmable savings products, automated escrow arrangements, or more efficient repo and securities lending markets.

From a crypto industry perspective, Drex presents both an opportunity and a challenge. On the opportunity side, the existence of a programmable, regulator‑endorsed tokenization platform could lower barriers for building compliant DeFi‑like applications that plug into mainstream financial assets and payment rails, using on‑chain logic while relying on regulated intermediaries for KYC and asset custody. On the challenge side, Drex may crowd out certain private stablecoin or payment token use cases, especially if it offers cheap, interoperable access to tokenized deposits that function much like a domestic stablecoin fully backed by commercial bank money and overseen by the central bank. The design choices Brazil makes around governance, access for non‑bank fintechs, and interoperability with public blockchains will therefore shape whether Drex becomes a closed club for incumbents or a public‑private bridge between traditional finance and open crypto networks.

Stablecoins and Cross‑Border Payment Rails

If Pix and Drex dominate the domestic digital money conversation, stablecoins loom large in the cross‑border and offshore dimension of Brazil’s crypto economy. Stablecoins, particularly those pegged to the U.S. dollar, are attractive to Brazilians as a way to hold dollar exposure, hedge against local currency volatility, or transact in global markets without going through traditional FX channels. However, the Central Bank of Brazil has taken a firm stance against allowing stablecoins and other cryptocurrencies to serve as settlement instruments within regulated cross‑border payment rails. In a notable move, the BCB banned the use of stablecoins and crypto for settlement in regulated cross‑border electronic foreign exchange (eFX) payment systems used by fintechs and payment institutions, effectively closing the back‑end crypto rail for such flows. Providers participating in those regulated cross‑border systems are required to settle transactions using fiat currency and conventional FX operations, with compliance deadlines set over a multi‑year horizon extending to the latter half of the decade.

This policy signals several regulatory priorities. First, it reflects concerns that stablecoin‑based settlement could obscure the true nature and routing of cross‑border flows, complicating AML and capital controls enforcement. Second, it indicates a desire to preserve the central bank’s ability to monitor and manage foreign exchange markets, avoiding a scenario in which large volumes of cross‑border trade and remittances bypass official FX channels via stablecoins. Third, by limiting stablecoin usage in regulated rails while tolerating it in more open crypto markets, the BCB is effectively creating a distinction between speculative or investment uses of stablecoins and their use as quasi‑banking infrastructure. In practice, cross‑border payment providers serving Brazilian customers now need to rely on more traditional FX arrangements, even if they use crypto at other parts of their stack, which may reduce demand for stablecoins in this specific segment.

At the same time, stablecoins remain central to many Brazilians’ self‑directed crypto activity. Some users acquire dollar‑pegged tokens via local or offshore exchanges as a hedge or to access DeFi yields, while others use them informally for cross‑border transfers, even if those flows fall outside regulated payment schemes. Regulators are aware that these parallel channels can be exploited for money laundering and capital flight, which is why the RFB’s proposed reporting rules explicitly cover transactions through foreign providers, decentralized platforms, and direct peer‑to‑peer channels when they exceed certain thresholds. The interaction between the BCB’s settlement ban in formal cross‑border rails and the tax authority’s attempt to bring offshore stablecoin use into view illustrates Brazil’s broader strategy: accept that private stablecoins exist and will be used, but ensure that large‑scale, systemic payment and FX functions remain under public oversight and that data about significant activity is available to authorities.

Crypto Taxation and Reporting Obligations

Capital Gains, Offshore Holdings, and Policy Politics

Tax policy is a crucial lens through which to understand Brazil’s approach to crypto as both a source of revenue and a locus of political debate. The Federal Revenue Service has moved gradually from treating crypto as a niche asset to explicitly taxing it, particularly when held abroad or in self‑custody. A key step was the introduction of a fixed 15% income tax on earnings from crypto assets held overseas by Brazilian taxpayers, effective from the beginning of 2024. This measure targeted a growing practice whereby wealthier Brazilians held substantial digital assets in foreign exchanges or self‑hosted wallets, potentially outside the domestic reporting system. By setting a clear rate and requiring disclosure, the RFB signaled that crypto‑denominated income would be treated similarly to other foreign investment income, even in the absence of traditional custodians.

In mid‑2025, Brazil then moved to a 17.5% flat tax on crypto capital gains more generally, encompassing gains realized on both offshore and self‑custodied holdings. According to reporting, this change simplified what had been a more complex, tiered system of capital gains taxation, but it also expanded the reach of the tax net to capture a broader spectrum of crypto investors, not just those with foreign accounts. The political sensitivity of these changes became apparent as additional crypto tax proposals were floated and then shelved ahead of a presidential election, with officials reportedly opting to postpone any further tax “storms” until after the vote. This sequence underscored that crypto taxation in Brazil is no longer a technocratic issue; it is entangled with broader debates about fiscal policy, fairness, and the state’s relationship with a growing cohort of crypto‑savvy citizens.

Another component of the tax landscape is Brazil’s treatment of other financial operations that intersect with crypto, such as betting and certain foreign exchange transactions. Broader tax reforms have included adjustments to the Tax on Financial Transactions (IOF), which historically applied to certain FX and credit operations. For example, the government has pursued a gradual reduction of IOF rates on many FX operations, with the ultimate goal of lowering the rate to zero, in line with commitments under the OECD Code of Liberalisation of Capital Movements. These changes affect the relative attractiveness of using regulated FX channels versus crypto‑based alternatives, and they interact with the BCB’s efforts to maintain control over cross‑border settlement mechanisms. While IOF is not a crypto tax per se, its evolution forms part of the overall picture of how Brazil calibrates taxes on financial flows in which crypto is increasingly implicated.

Expanding Reporting: From Exchanges to DeFi and NFTs

If tax rates define how much is owed, reporting rules determine what the government can actually see. Brazil’s RFB has proposed a major expansion of crypto reporting requirements that would significantly increase transparency across centralized and decentralized platforms alike. The proposal to revise Normative Instruction 1888/2019 broadens the categories of entities and transactions that must report detailed data to the tax authority. Brazilian‑domiciled crypto service providers are required to submit comprehensive monthly reports on all transactions they process, including dates, types, values, and the identities of the parties involved, with precision down to the tenth decimal place for both crypto‑to‑crypto and fiat‑to‑crypto trades. Brazilian residents and entities that transact through foreign providers, decentralized platforms, or direct peer‑to‑peer arrangements are also brought into the reporting net when their monthly transaction volume exceeds 30,000 reais, regardless of whether those transactions occur on regulated exchanges or in DeFi protocols.

The scope of covered activities is notably broad. In addition to conventional buying and selling, the RFB’s proposal explicitly includes staking and yield farming, airdrops, loans, donations, payments in kind, and even more complex operations such as the fractionalization of non‑fungible tokens. This means that typical DeFi behaviors—such as providing liquidity to a protocol, claiming governance token rewards, or splitting an NFT into multiple fungible shares—become taxable events that must be recorded and reported if they surpass relevant thresholds. The regulation also contemplates the inclusion of transactions executed through decentralized platforms that operate without significant influence over the distributed ledger technology or smart contracts, a clear attempt to ensure that “non‑custodial” and protocol‑level activity does not escape oversight simply because there is no centralized intermediary.

To implement this vision, the RFB expects both service providers and users to maintain detailed records of transaction purposes, asset origins, and collateral arrangements. The proposal mandates that virtual asset service providers document the intended purpose of each transaction—for example, whether it represents a purchase, a loan, a service payment, or another category—and report year‑end balances in both fiat and crypto, including acquisition costs in Brazilian reais. It also requires disclosure of assets used as collateral, staking rewards, mining income, and transfers such as airdrops or loans. For individual users, especially those active in DeFi, such requirements can be onerous, as they imply tracking and categorizing complex multi‑step interactions that are not easily mapped onto traditional accounting concepts. Nonetheless, the direction of travel is clear: Brazil is moving toward a tax regime in which crypto transactions are tracked with granularity similar to or exceeding that of traditional securities trading.

Alignment with FATF Travel Rule and AML Objectives

Underlying these tax reporting reforms is a broader concern with anti‑money‑laundering (AML) compliance and international standards. The RFB explicitly frames its proposals as aligned with the Financial Action Task Force’s (FATF) “Travel Rule,” which calls on virtual asset service providers to collect and transmit identifying information about the originators and beneficiaries of crypto transactions above certain thresholds. In line with this guidance, Brazilian regulations emphasize collecting detailed client information, including names, addresses, tax domiciles, and national identification numbers such as CPF or CNPJ, not only for domestic users but also in the context of foreign or cross‑border transactions. Service providers are expected to develop systems capable of tracking complex chains of custody and ownership, ensuring that they can identify controlling individuals even when transactions pass through multiple wallets or protocols.

This alignment has several implications. For one, it pushes Brazilian‑based exchanges and custodians to adopt more sophisticated compliance infrastructure, including blockchain analytics tools and transaction monitoring systems that can map on‑chain activity onto real‑world identities. It also puts pressure on foreign platforms that wish to serve Brazilian customers, since they may be required to share customer information or adapt their systems to accommodate Brazilian reporting standards, especially if they wish to comply with SPSAV licensing in the future. For DeFi protocols, the situation is more complex, as there may be no obvious entity to hold liable for non‑compliance; however, regulators can still target front‑end operators, developers, or local intermediaries that facilitate access, especially when they market services to Brazilian residents. In the longer term, Brazil’s embrace of the Travel Rule and detailed reporting requirements may encourage the emergence of permissioned DeFi and regulated on‑chain financial products that incorporate identity verification by design, even as purely permissionless systems continue to exist in parallel.

Brazil Postpones Crypto Tax Plan Until After October Presidential Election

We all know why they decided to pick this route. Bunch of people you can't just trust

- 01CBDC and digital real rollout↗

The Drex pilot naming Visa, Microsoft, and major local banks signaled Brazil moving from experiment to infrastructure, pulling readers tracking sovereign digital money adoption.

- 02Stablecoin access via banking rails↗

USDC landing inside PIX and local bank accounts — then the central bank banning stablecoins from cross-border eFX rails — created a push-pull readers closely followed as a proxy for how open Brazil's on-ramp would actually be.

- 03Regulatory licensing and exchange legitimacy↗

Binance's broker-dealer license and Coinbase's expansion filings showed readers tracking whether Brazil's framework would produce a licensed, stable market or remain a gray zone.

- 04Crypto tax regime shape-shifting↗

Repeated pivots — election-linked postponement, offshore 15% flat tax, exemption removal — told readers the tax rulebook was still live and consequential for their holdings.

- 05Central bank system breach and crypto laundering↗

A $2,770 insider bribe unlocking a $148M heist with funds routed through LATAM OTC desks hit readers at the accountability angle: how exposed is Brazil's financial plumbing to crypto-facilitated crime.

- 06Algo stablecoin and prediction market bans↗

Bill 4308 targeting USDe and FrxUSD with 8-year jail terms, plus the Polymarket/Kalshi ban, showed Brazil drawing hard lines around specific DeFi primitives that readers in those products needed to track.

Trading, Derivatives, and Investment Products

B3 and the Institutionalization of Bitcoin Exposure

Brazil’s principal stock exchange, B3, has played a notable role in bringing crypto exposure into the regulated capital markets domain. The exchange has listed a Bitcoin futures contract that allows investors to gain exposure to the price fluctuations of the leading cryptocurrency through a regulated, exchange‑traded product, rather than holding the underlying asset directly. According to B3’s own materials, this futures contract is designed to provide yet another alternative for investors seeking crypto exposure in a safe and regulated environment, with the contract structure and margin requirements anchored in existing derivatives market practices. The availability of such products gives institutional investors, family offices, and sophisticated retail traders a familiar vehicle for participating in crypto markets while relying on the exchange’s clearinghouse, risk management systems, and regulatory oversight.

Beyond futures, B3 has also experimented with bitcoin‑linked event contracts and other structured products, often restricting access to accredited or professional investors with substantial assets under management. These limitations reflect regulators’ ongoing concerns about leverage, volatility, and the potential for retail investors to suffer outsized losses in highly speculative markets. At the same time, they signal a willingness to integrate crypto themes into mainstream financial instruments when adequate safeguards are in place. The broader effect is to normalize Bitcoin and other digital assets as part of the investment universe, even as spot trading on offshore exchanges and decentralized platforms continues in parallel. For many Brazilian investors, particularly those already active in equities and derivatives, B3‑listed products offer a bridge between traditional portfolios and the world of crypto, without requiring them to manage private keys or navigate unregulated platforms.

This institutionalization of crypto exposure also intersects with retirement and wealth management. Brazilian asset managers have launched investment funds with crypto allocations, sometimes using exchange‑traded products or regulated futures as their underlying exposure, in order to comply with CVM and Central Bank guidelines on custody and risk management. In this way, crypto becomes one more asset class that can be wrapped in familiar fund structures, subject to existing investor protection and disclosure frameworks. While the proportion of assets allocated to crypto in most portfolios remains relatively modest, the presence of such offerings signals that Brazilian capital markets infrastructure is adapting to client demand for digital asset exposure, and not simply relegating crypto to the realm of speculative retail trading.

SPSAV Licensing and the Future of Exchanges

For spot exchanges, custodians, and intermediaries, the SPSAV licensing regime marks a turning point in how they must operate in Brazil. Under the new framework, these entities must meet minimum capital requirements, maintain robust risk management and compliance functions, and ensure strict separation between client assets and corporate funds. Requirements for independent audits, designated responsible officers for each business line, and clear public disclosure of business models and fee structures further align crypto platforms with the standards expected of banks and broker‑dealers. The practical effect is to raise the barrier to entry for new platforms, while giving licensed entities a stamp of regulatory credibility that may become increasingly important as consumers learn to differentiate between regulated and unregulated offerings.

Foreign platforms that see Brazil as a key growth market face an additional decision: whether to establish local subsidiaries to pursue SPSAV authorization or to operate informally-with greater legal and reputational risk. The requirement for a physical presence or partnership with a locally licensed entity is intended to prevent a situation in which large offshore exchanges serve Brazilian customers without any meaningful accountability to domestic regulators. In practice, this means that global exchanges must invest in local compliance teams, build relationships with the BCB and CVM, and adapt their products—particularly derivatives and leveraged offerings—to align with local rules. Industry developments already show senior executives with regulatory expertise being appointed to oversee Brazil strategies for major exchanges, reflecting the importance and complexity of this market.

The shift toward licensing also has implications for innovation. On the one hand, compliance costs and capital requirements may deter smaller startups or purely experimental projects from entering the regulated market, potentially concentrating activity among larger incumbents. On the other hand, a clear licensing pathway may encourage more traditional financial institutions, such as banks and brokerages, to add crypto services, confident that they can do so within a well‑defined regulatory perimeter. Over time, this dynamic could lead to a Brazilian market where regulated, SPSAV‑licensed platforms dominate fiat on‑and‑off‑ramps and custody, while a more experimental ecosystem of DeFi protocols and offshore platforms continues to operate at the periphery, often accessed via VPNs or cross‑border services.

AI‑Powered Derivatives and the Next Frontier

Brazil’s crypto derivatives landscape is not limited to domestic exchanges and B3. International platforms specializing in futures and perpetual swaps also court Brazilian traders, often emphasizing advanced features such as algorithmic strategies and artificial intelligence. One example is OneBullEx, a self‑described AI futures exchange that has actively engaged with Brazilian academia by participating in a Web3 career event at the University of São Paulo. During this event, the platform’s Brazil country manager delivered a keynote presentation and joined a panel discussion on career paths, skills, and regional opportunities in the Web3 market, signaling the company’s long‑term interest in cultivating local talent and market knowledge. OneBullEx positions itself as a provider of AI‑integrated futures trading infrastructure, including tools for creating and subscribing to systematic trading strategies, with the stated goal of making futures trading more structured and verifiable.

For Brazilian regulators, such offerings raise questions that go beyond traditional market risk. AI‑driven strategies may introduce new forms of model risk and opacity, making it harder for retail traders to understand the behaviors of strategies they subscribe to, especially if algorithms are proprietary. Additionally, the bundling of trading infrastructure with strategy creation and subscription services could blur the lines between execution venues, asset managers, and investment advisers, triggering different sets of regulatory obligations. While these issues are not unique to Brazil, the country’s efforts to modernize its securities and derivatives regulations, including CVM’s guidelines on cryptoasset securities, suggest that AI‑powered derivatives will be scrutinized through both a technology and conduct‑of‑business lens. How Brazil balances the promise of AI for more efficient markets with the need to protect less sophisticated traders will be another chapter in its evolving crypto story.

Tokenization, Real‑World Assets, and Market Infrastructure

ANBIMA’s DLT Pilot for Tokenized Assets

Brazil is emerging as a global testbed for tokenization of real‑world assets (RWAs), particularly in its capital markets. ANBIMA, the Brazilian Financial and Capital Markets Association, has launched the country’s first distributed ledger technology (DLT) network pilot focused on tokenized assets, with an initial emphasis on investment funds and debentures, which are corporate bonds. The pilot simulates the full lifecycle of a tokenized asset, from issuance and primary distribution to secondary trading, corporate actions, and eventual redemption or maturity. By running these end‑to‑end simulations, ANBIMA and participating institutions aim to evaluate the legal, operational, and technological implications of moving traditional securities onto blockchain‑based registries, as well as the potential efficiency gains in settlement, reconciliation, and investor servicing.

The pilot’s focus on investment funds is particularly significant because funds are a dominant vehicle for retail and institutional investment in Brazil. Tokenizing fund shares could, in principle, enable fractional ownership, faster settlement, and more direct distribution channels, potentially reducing intermediary layers and fees. Similarly, tokenized debentures could make it easier for corporate issuers to reach a broader base of investors, including overseas participants, while enabling on‑chain automation of interest payments and covenant monitoring. However, these potential benefits must be balanced against regulatory and operational considerations, such as ensuring that tokenholders’ rights are legally recognized, that on‑chain records can interoperate with existing registries, and that KYC/AML requirements are maintained even in more decentralized ownership structures. ANBIMA’s pilot is therefore as much a regulatory sandbox as it is a technology testbed, providing data and experience that will inform future rules issued by the CVM and the central bank.

In the broader context, Brazil’s tokenization initiatives position it at the forefront of a global trend where financial institutions experiment with DLT to modernize legacy market infrastructure. By focussing on debentures and investment funds—a core part of corporate finance and household investment—the Brazilian pilot goes beyond the narrow use case of tokenized government bonds seen in some other jurisdictions. It aligns with the vision of Drex as a convergent infrastructure where tokenized deposits and securities can be transacted via smart contracts, pointing toward an ecosystem in which issuance, trading, and settlement of many asset classes occur on interoperable networks rather than in siloed systems. For the crypto industry, this suggests that Brazil may become a leading market for compliant RWA tokens that bridge traditional financial assets and on‑chain liquidity, offering a regulated alternative to the more experimental RWA projects seen in DeFi.

Public‑Sector Blockchain: The Cardano–SERPRO Partnership

Beyond private capital markets, Brazil’s public sector is also exploring blockchain technology as a tool for digital transformation and education. A notable example is the partnership between the Cardano Foundation and SERPRO, Brazil’s Federal Data Processing Service, which is responsible for a wide range of IT services across public administration. The partnership aims to combine SERPRO’s expertise in public sector processes with Cardano’s blockchain technology, with the stated goal of driving digital transformation in government services and building capacity in blockchain education. Although specific use cases have not yet been fully detailed, the collaboration suggests interest in exploring blockchain for purposes such as secure record‑keeping, identity management, or transparent procurement, among others.

The educational component of the partnership is particularly important in a country where both public servants and the general population are still building fluency in blockchain concepts. By collaborating with a well‑known blockchain foundation, SERPRO can access technical resources, training materials, and possibly pilot platforms that help demystify how distributed ledgers work and how they can be applied beyond cryptocurrencies. For Cardano, the partnership offers an opportunity to showcase its technology in a real‑world, large‑scale public sector context, potentially catalyzing broader use of its ecosystem in Brazil. The alignment with Brazil’s broader digital agenda, including Pix and Drex, suggests that public authorities view blockchain as one of several tools for modernizing infrastructure, not as a panacea but as a complementary technology where appropriate.

For the crypto community, public‑sector blockchain initiatives like this can have knock‑on effects even if they do not directly involve cryptocurrencies. They help legitimize the underlying technology in the eyes of policymakers, encourage the development of local talent and service providers, and create opportunities for cross‑pollination between public‑sector projects and private innovation. Over time, these efforts may contribute to a more nuanced regulatory environment, where regulators distinguish between speculative crypto activities that require strict oversight and infrastructural uses of blockchain that can be encouraged under appropriate governance and security standards.

Crime, Enforcement, and Investor Protection

Brazil’s Crypto Crime Challenge and Law Enforcement Response

As crypto adoption has grown, Brazil has also grappled with the darker side of digital assets: their use in fraud, money laundering, and organized crime. Chainalysis reports that between mid‑2024 and mid‑2025, Brazil received approximately 318 billion U.S. dollars in on‑chain value, with a portion of this activity associated with high‑risk or illicit services, including global money laundering networks that route funds through Brazilian platforms and intermediaries. These networks often exploit the country’s size, its interconnected financial system, and its role as a gateway to other Latin American markets to obscure the origin of funds and integrate them into the legitimate economy. The nature of these schemes ranges from ransomware payouts and darknet market proceeds being laundered through Brazilian exchanges to domestic scams that promise high returns on crypto investments but operate as pyramid or Ponzi schemes.

Despite these challenges, law enforcement has made significant strides in identifying and dismantling major laundering operations. TRM Labs’ 2026 Crypto Crime Report highlights Brazil as one of the jurisdictions where authorities took down industrial‑scale money laundering networks in 2025, using a combination of on‑chain analytics, traditional investigative techniques, and international cooperation. These cases often involve coordinated actions by federal police, financial intelligence units, and regulators, resulting in asset seizures, arrests, and the freezing of accounts associated with illicit activity. The visibility provided by public blockchains, when combined with robust data and analytics, has thus become a double‑edged sword: while criminals attempt to exploit the pseudonymous nature of addresses, investigators can trace flows over time and link them to real‑world entities once a single point of exposure is identified.

Anti‑Gang Law and Seized Crypto for Public Security

Brazil has recently taken a step further by explicitly integrating seized crypto into its public security funding mechanisms. A new anti‑gang law signed by President Luiz Inácio Lula da Silva empowers authorities to seize, confiscate, or freeze digital or virtual assets, including cryptocurrencies like Bitcoin, when there is strong evidence that they are linked to serious criminal activity. Crucially, the law allows such seized assets, once adjudicated, to be liquidated and the proceeds used to finance public security resources, including equipment, technology, and operations. This move formalizes what had previously been a more ad hoc approach to handling seized crypto, which posed practical challenges related to custody, valuation, and liquidation.

By turning seized crypto into a funding source for public security, Brazil is attempting to “turn the tables” on criminal organizations, channeling their digital spoils into resources that strengthen the capacity of law enforcement agencies. This approach also addresses the problem of seized crypto assets sitting idle in wallets while their value fluctuates, as prompt liquidation can lock in value and reduce volatility risk for the state. However, it raises its own set of operational and ethical questions, such as how to manage auction processes, how to ensure transparency in the conversion of crypto to fiat, and how to avoid creating perverse incentives for agencies to overemphasize seizures as a revenue source. Nonetheless, the law sends a strong signal that the state not only aims to deter crypto‑enabled crime but also to repurpose its proceeds in a way that visibly benefits public safety.

Prediction Markets, Betting Regulations, and Consumer Risks

Another area where Brazil has tightened its stance is the intersection of crypto and betting. Authorities have blocked access to major prediction market platforms like Polymarket and Kalshi, characterizing their offerings as illegal betting on events such as elections and sports results. The decision comes amid a broader regulatory push to formalize and tax sports betting and gambling, while protecting consumers from addiction and fraud. By treating decentralized or offshore prediction markets as unauthorized betting operations, regulators aim to prevent circumvention of domestic rules and to curb the growth of unregulated online gambling channels that might be marketed as “investing” or “information markets.”

This crackdown occurs against a backdrop where crypto has already permeated gaming, sports fandom, and speculative contests, including football‑themed prediction pools and token‑based rewards campaigns. While such innovations can increase engagement and introduce new forms of fan participation, they also blur the boundaries between entertainment, speculation, and investing, particularly for younger users. Brazil’s actions suggest that authorities are increasingly attentive to these blurred lines, especially when platforms offer leveraged or binary outcomes that resemble betting rather than investment. In the longer term, the regulatory treatment of prediction markets could influence how other event‑linked crypto products are designed and marketed, including whether they must be offered only to sophisticated investors or under explicit gambling licenses. For a crypto industry eager to tap into Brazil’s passion for sports and gaming, navigating these regulatory sensitivities will be essential.

AML Controls, the Travel Rule, and DeFi Challenges

The earlier discussion of tax reporting and the FATF Travel Rule also has clear implications for AML enforcement. By requiring virtual asset service providers to collect and report detailed information on clients, including ultimate beneficial owners, the Brazilian authorities aim to create a data environment where suspicious patterns can be more easily detected and investigated. The emphasis on including decentralized platforms and peer‑to‑peer transactions within reporting obligations, at least above certain thresholds, is a recognition that illicit actors may migrate toward these channels as centralized exchanges become more tightly regulated. AML compliance programs in Brazil therefore increasingly rely on a combination of KYC procedures, transaction monitoring, blockchain analytics, and cooperation with law enforcement to flag and act upon high‑risk activity.

DeFi presents a particular set of challenges in this regard. Protocols that operate autonomously on public blockchains and lack a central operator do not fit neatly into traditional regulatory categories. The RFB’s proposals hint at an emerging approach: instead of attempting to regulate protocols themselves, authorities focus on the human touchpoints—front‑end operators, aggregators, wallet providers, or localized interfaces—that connect Brazilian users to these systems. By imposing reporting obligations on Brazilian residents who transact through DeFi platforms beyond certain volumes, regulators seek to maintain visibility even when there is no custodial intermediary. However, enforcement in this area is likely to be uneven and iterative, as authorities test what is feasible and proportionate, and as technological developments such as privacy‑enhancing tools, cross‑chain bridges, and rollups complicate attribution further. Brazil’s experience in this field will contribute to global debates on how to regulate DeFi without stifling innovation or driving activity entirely into less transparent jurisdictions.

Brazil central bank bans crypto use in regulated cross-border eFX payment rails, forcing providers to rely on FX transactions and tightening control over stablecoin flows

Brazil enacts crypto asset regulatory framework (Law 14,478)

Central Bank launches Drex CBDC pilot with 14 institutions including Visa and Microsoft

Brazil postpones offshore crypto capital gains tax ahead of October presidential election

Brazil enforces 15% flat tax on offshore crypto earnings

Central bank bans stablecoin settlement in cross-border eFX payment rails

C&M Software insider breach exposes six bank reserve accounts; ~$148M taken, $30–40M laundered via crypto OTCs

Lula signs Anti-Gang Law authorizing seizure and liquidation of crypto for public security funding

Brazil bans prediction markets including Polymarket and Kalshi under new betting regulations

Mining, Energy, and Sustainability

Renewable Energy Context and Bitcoin Mining

Brazil’s energy landscape, characterized by a high share of renewables such as hydroelectric power and bioenergy from sugarcane, creates an intriguing context for Bitcoin mining. The environmental criticism often leveled at proof‑of‑work mining hinges on its carbon footprint, which is heavily dependent on the energy mix used to power mining rigs. In Brazil, the availability of relatively clean and sometimes underutilized energy sources opens the possibility that Bitcoin mining could be framed not as an environmental liability but as a way to monetize surplus renewable energy and stabilize grids in certain regions. This narrative aligns with a broader global trend of miners seeking locations where renewable or stranded energy can be converted into digital assets, potentially supporting both local economic development and the security of the Bitcoin network.

Tether‑Backed Adecoagro Sugarcane Mining Project

A high‑profile example of this dynamic is the Bitcoin mining project announced by Adecoagro, a South American agribusiness company in which stablecoin issuer Tether is a major shareholder. Adecoagro plans to launch Bitcoin mining operations in Brazil using electricity generated from burning sugarcane waste, a form of biomass energy that is already part of the company’s operations. The project is based in Ivinhema, in the state of Mato Grosso do Sul, and is set to begin with an initial capacity of about 10 megawatts and roughly 1,280 Bitcoin mining machines. This initial deployment represents only a fraction of Adecoagro’s installed energy generation capacity, positioning the initiative as a commercial test of whether Bitcoin mining can scale as a complementary use for surplus energy alongside existing power sales.

The partnership between Adecoagro and Tether, formalized through a memorandum of understanding signed previously, aims to leverage Tether’s expertise in digital assets and sustainable mining, including its proprietary Mining OS, which will manage operations at the site. Tether has indicated an intention to open‑source this Mining OS, potentially contributing to broader industry efforts around efficient, renewable‑powered mining. The initiative’s stated goals include monetizing surplus energy that might otherwise go unused, improving grid stability by providing a flexible load that can ramp up or down as needed, and supporting decentralized networks by contributing hash power from renewable sources. If successful, the project could provide a template for how agricultural and energy companies in Brazil might integrate Bitcoin mining into their business models, transforming what would otherwise be waste energy into a revenue stream.

From a regulatory and tax standpoint, mining operations in Brazil are subject to general rules on income and corporate taxation, as well as the expanded reporting obligations that cover mining income and other crypto‑related revenues. As the sector grows, energy regulators and environmental agencies may also develop specific guidelines for crypto mining, addressing issues such as grid impact, emissions reporting, and land use. In any case, the combination of a renewable‑heavy energy matrix, large agribusiness players, and an increasingly sophisticated crypto regulatory framework suggests that Brazil could become an important node in the global conversation about sustainable Bitcoin mining.

Talent, Education, and Ecosystem Development

Universities, Careers, and the Web3 Workforce

The long‑term health of Brazil’s crypto ecosystem depends not only on regulation and infrastructure but also on the availability of skilled developers, designers, lawyers, and regulators who understand digital assets. Universities and educational institutions are increasingly engaging with these topics, often in partnership with industry players. The Web3 career event at the University of São Paulo, which featured participation from OneBullEx, exemplifies this trend. At that event, the company’s Brazil country manager delivered a keynote on emerging career paths, skill requirements, and regional opportunities in the Web3 market, followed by a panel discussion with multiple speakers on how students and young professionals can prepare for roles in decentralized finance, trading, and blockchain development. Such initiatives help bridge the gap between academic knowledge and industry practice, exposing students to real‑world use cases and the regulatory and ethical challenges that accompany them.

Engagements of this kind are also strategically important for companies. For OneBullEx, Brazil is described as an important user market and a key part of the next stage of global Web3 talent, application, and community development. By building relationships with university communities and local ecosystem partners, the company aims to create a pipeline of skilled professionals who can contribute to its AI‑integrated futures platform and to Brazil’s crypto landscape more broadly. Other exchanges, protocols, and infrastructure providers similarly invest in hackathons, workshops, and sponsorships of meetups in cities such as São Paulo, Rio de Janeiro, and Brasília. These grassroots efforts complement more formal training programs and signal that Brazil is viewed as a strategic hub for human capital in the global crypto industry.

Public‑Private Knowledge Building

On the public‑sector side, partnerships like the one between SERPRO and the Cardano Foundation also play an educational role. By collaborating on pilot projects and training, public servants gain hands‑on exposure to blockchain technologies, the design of smart contracts, and the governance models that underpin public and private networks. This knowledge can improve the quality of regulation, as policymakers who understand the technical realities are better equipped to craft rules that are both effective and innovation‑friendly. It can also help identify appropriate use cases for blockchain in government services, such as verifiable credentials, transparent procurement processes, or secure registries for property and corporate ownership.

The combination of university‑industry collaborations and public‑sector partnerships contributes to an ecosystem where knowledge circulates across boundaries. Legal scholars engage with regulators on questions of token classification; computer scientists work with startups on protocol design; and economists and sociologists study the social impacts of crypto adoption, including financial inclusion, debt, and behavioral changes. Over time, this cross‑disciplinary engagement may produce a cadre of Brazilian experts whose work influences not only domestic policy but also international debates on digital assets.

Culture, Speculation, and Retail Engagement

Brazil’s mainstream culture also shapes its crypto story. Football fandom, gaming, and social media play an important role in how many Brazilians encounter crypto for the first time, often through fan tokens, NFT collectibles, or prediction games tied to major tournaments. Recent promotions and contests that rewarded users for predicting match outcomes or engaging with branded Web3 experiences illustrate how crypto projects tap into national passions to drive engagement. While such campaigns can be effective marketing tools and help demystify wallets and tokens for newcomers, they also carry risks: they can encourage speculative behavior, conflate entertainment with investment, and expose users to scams or poorly designed tokenomics.

Regulators have responded by paying closer attention to marketing practices, especially those that target young people or present complex financial products in gamified formats. The crackdown on unlicensed prediction markets, alongside stricter rules for sports betting and gambling, reflects a growing awareness that the border between gaming and investing is increasingly porous in the digital age. In this environment, investor education becomes critical. Industry associations, consumer protection agencies, and independent media play important roles in explaining the differences between investing, trading, and gambling, as well as the tax and legal implications of various activities. As Brazil’s crypto market matures, the interplay between cultural enthusiasm and sober risk assessment will remain a central theme.

Brazil in Regional and Global Context

Latin American Comparisons and Influence

Within Latin America, Brazil stands out not only because of its size but also because of its relatively advanced regulatory and infrastructural approach to digital assets. Chainalysis data shows that Latin America as a region has seen strong growth in crypto adoption, with a 63% increase in on‑chain activity over a recent twelve‑month period, but Brazil accounts for a disproportionate share of that activity. Other large economies such as Mexico and Argentina also have vibrant crypto communities, driven by remittances and inflation concerns respectively, yet Brazil’s combination of Pix, Drex, SPSAV licensing, and RWA tokenization pilots gives it a unique profile. In effect, Brazil is experimenting with a comprehensive model in which public digital infrastructure, strict but clear regulation, and private innovation in tokenization and trading coexist, offering lessons for other emerging markets.

Brazil’s regulatory stance on issues like stablecoin settlement in cross‑border rails and the application of the FATF Travel Rule is likely to influence regional and global peers. As a member of the G20 and an active participant in multilateral forums, Brazil can share its experiences with instant payments, CBDC design, and crypto regulation, potentially shaping norms adopted by other central banks and securities regulators. The IMF’s analysis of Pix already positions it as a success story that other countries may learn from, and Drex may similarly become a reference point for CBDC architectures that integrate tokenized deposits and securities. For countries in Africa and Asia that share some of Brazil’s challenges—large informal sectors, financial exclusion, and demand for digital innovation—the Brazilian model may be particularly compelling.

Trade Policy, Geopolitics, and Digital Assets

Brazil’s position in global trade and geopolitics also interacts with its crypto policies. As it negotiates trade agreements with major partners, including discussions around tariffs and market access, issues of digital trade, data localization, and financial services can shape how cross‑border digital asset flows are treated. While recent reports on talks between Brazilian and U.S. leaders have focused primarily on tariffs and goods, the broader relationship between the two countries’ financial systems and regulatory approaches could impact cross‑border fintech and crypto businesses in the future. For instance, alignment or divergence in stablecoin and CBDC standards, data sharing for AML purposes, and tax information exchange will affect how easily Brazilian and foreign firms can operate across borders.

Brazil’s relationships within blocs such as BRICS and Mercosur also matter. Discussions about de‑dollarization, regional payment systems, and alternative reserve assets can create both opportunities and constraints for crypto adoption. On one hand, crypto and tokenized assets can serve as tools for diversifying away from traditional currencies; on the other, governments may see certain forms of private digital money as undermining efforts to develop their own public infrastructures, such as regional settlement systems or digital currencies. Brazil’s careful stance on stablecoins in regulated rails, combined with its push for Drex, reflects this tension: the country is open to innovation but intent on preserving monetary sovereignty and regulatory control over systemic financial functions.

Brazil has simultaneously issued a broker-dealer licensing regime, banned stablecoins from cross-border eFX rails, outlawed algorithmic stablecoins under Bill 4308, and imposed new AML rules — leaving operators navigating a fast-changing, multi-regulator environment.

Itaú recommending 1–3% BTC allocations and Mercado Bitcoin's Wormhole cross-chain integration signal maturing institutional demand, but B3's bitcoin event contracts restricted to $1.9M+ investors limits retail market depth.

- Smart-contract / ProtocolMedium

Bill 4308's ban on algorithmic stablecoins with segregated-reserve mandates creates a direct legal risk surface for any DeFi protocol issuing or integrating algo-collateralized assets targeting Brazilian users.

The C&M Software breach demonstrated that Brazil's central bank reserve infrastructure is accessible through a single third-party contractor credential, concentrating systemic risk in lightly audited service-provider access points.

The central bank's ban on stablecoin settlement within regulated cross-border eFX rails forces crypto-to-fiat flows onto non-bank corridors, constraining on-ramp liquidity and increasing slippage for large transfers.

Lula's Anti-Gang Law now authorizes law enforcement to seize and liquidate Bitcoin and other digital assets as public-security funding, introducing a novel confiscation vector absent from most comparable jurisdictions.

Conclusion

Brazil’s crypto landscape is marked by paradoxes that make it both challenging and fascinating for observers and participants. It is a country where crypto adoption is among the highest in the world, yet where everyday domestic payments are dominated by a state‑run instant payment system that renders many crypto payment pitches redundant. It is a jurisdiction where regulators are simultaneously building one of the most comprehensive regulatory frameworks for virtual asset service providers, experimenting with a cutting‑edge CBDC and tokenization platform, and cracking down hard on certain uses of crypto, from cross‑border stablecoin settlement to unlicensed prediction markets. It is also a country where the proceeds of crypto‑enabled crime, once seized, can be converted into funds for public security, even as law enforcement partners with blockchain analytics firms to dismantle industrial‑scale money laundering networks.

For investors, builders, and policymakers, the Brazilian experience underscores several key lessons. First, crypto does not exist in a vacuum; it interacts with and is shaped by existing financial infrastructures like Pix, as well as by broader political and fiscal dynamics, such as debates over tax policy and crime. Second, clear but demanding regulation—exemplified by SPSAV licensing, CVM guidance, and RFB reporting rules—can both professionalize the industry and raise barriers to entry, potentially favoring better‑capitalized incumbents while pushing more experimental activity offshore or into DeFi. Third, tokenization and CBDCs represent not just new types of money but new architectures for entire financial systems, and Brazil’s Drex project and ANBIMA’s DLT pilot show how ambitious such transformations can be. Finally, the human dimension—talent development, cultural engagement, and investor education—remains critical for ensuring that the benefits of crypto and blockchain technologies are widely shared and that risks are understood and managed.

As Brazil continues to refine its regulatory approach and scale its digital infrastructure, it will likely remain a bellwether for how large emerging markets can integrate crypto into their financial systems without ceding control over key policy levers. For a crypto news audience, following Brazil means tracking not just coin prices or headline‑grabbing enforcement actions, but the deeper institutional and infrastructural changes that will shape what “crypto in the real economy” actually looks like over the coming decade.

Outlook

Looking ahead, Brazil appears poised to deepen, not retreat from, its engagement with digital assets and blockchain technology. The Drex project is likely to enter more advanced piloting and possibly early production phases, testing how tokenized deposits and securities can coexist on shared ledgers and how smart contracts can automate complex financial arrangements. ANBIMA’s tokenization pilot may expand beyond investment funds and debentures into other asset classes, including potentially real estate or trade finance, as regulators grow more comfortable with DLT‑based registries. At the same time, the SPSAV licensing regime will sort the market, as some platforms secure authorization and integrate deeply into Brazil’s financial system while others either adapt as offshore‑only options or exit the market.

Crypto taxation and reporting will remain contested terrain, especially as the RFB’s expanded reporting requirements begin to bite and as policymakers revisit shelved tax plans after electoral cycles. The balance between robust AML enforcement and a welcoming environment for innovation will be tested repeatedly, particularly in relation to DeFi, privacy‑enhancing technologies, and cross‑border stablecoin use. Meanwhile, projects like Tether‑backed sugarcane‑powered mining, Cardano’s partnership with SERPRO, and ongoing university‑industry collaborations suggest that new forms of public‑private experimentation will continue to emerge, reinforcing Brazil’s status as a laboratory for sustainable mining, public‑sector blockchain, and advanced derivatives.

For global crypto participants, Brazil will likely remain a market that cannot be ignored. Its regulatory rigor may deter some actors, but for those willing to engage seriously with compliance, tokenization, and integration with public digital infrastructure, Brazil offers the prospect of scale, innovation, and a relatively clear path to legitimacy. As Latin America’s crypto adoption continues to grow and as other countries watch Brazil’s experiments with Pix and Drex, the choices made in Brasília, São Paulo, and beyond will help shape the contours of the next phase of digital finance worldwide.

Latest Brazil news

Brazil bans prediction markets like Polymarket and Kalshi, citing investor protection risks and rising gambling concerns under new betting regulationsBrazil Postpones Crypto Tax Plan Until After October Presidential ElectionBrazil central bank bans crypto use in regulated cross-border eFX payment rails, forcing providers to rely on FX transactions and tightening control over stablecoin flowsUSDT still leads global stablecoin ownership, but USDC is gaining ground across markets like the U.S., Germany and Brazil, signaling a shift toward regulated stablecoins.Brazil's B3 exchange rolls out bitcoin event contracts restricted to investors with $1.9M+ in assetsBrazil advances Bill 4308 banning algo stables like USDe and FrxUSD, requiring segregated reserves and 8-year jail terms for issuersSources

- https://www.chainalysis.com/blog/brazil-crypto-asset-regulatory-framework-2025/

- https://glenbrook.com/payments_news/brazils-central-bank-bans-stablecoin-and-crypto-settlement-in-cross-border-payments/

- https://www.dlnews.com/articles/regulation/brazil-signs-antigang-law-to-use-seized-crypto/

- https://coinmarketcap.com/academy/article/brazil-freezes-crypto-tax-plans-ahead-of-october-vote-reports-reuters

- https://international.anbima.com.br/news/anbima-launches-brazil-s-first-dlt-network-pilot-for-tokenized-assets

- https://clientes.b3.com.br/en/w/futuro-de-bitcoin

- https://www.bloomberg.com/news/articles/2026-04-24/brazil-moves-to-ban-prediction-markets-on-elections-sports

- https://www.chainalysis.com/blog/brazil-crypto-crime-money-laundering-regulation/

- https://bitcoinmagazine.com/news/tether-backed-adecoagro-bitcoin-mining

- https://www.prnewswire.com/news-releases/onebullex-joins-usp-web3-career-opportunities-panel-to-support-brazils-blockchain-talent-ecosystem-302779322.html

- https://www.mmerge.io/on-stage/tokenized-money-and-cbdcs-convergent-digital-infrastructure

- https://www.chainalysis.com/blog/2025-global-crypto-adoption-index/

- https://www.elibrary.imf.org/view/journals/002/2023/289/article-A004-en.xml

- https://globaltaxnews.ey.com/news/2025-1243-brazilian-government-announces-substantial-tax-changes-affecting-interest-on-net-equity-financial-investments-betting-operations-and-iof-regulations

- https://www.taxbit.com/blogs/crypto-tax-compliance-in-focus-brazils-federal-revenue-service-consultation-explained

- https://www.machadomeyer.com.br/en/recent-publications/publications/capital-markets/cvm-guidelines-for-the-cryptoasset-market

- https://www.trmlabs.com/reports-and-whitepapers/2026-crypto-crime-report

- https://www.bcb.gov.br/en/financialstability/digital_brazilian_real

- https://cardanofoundation.org/blog/strategic-partnership-serpro

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…