Comprehensive explainer on Celsius Network’s rise, 2022 collapse, Chapter 11 bankruptcy, creditor recoveries, Ionic Digital spin-off, Alex Mashinsky’s fraud cases, and the lasting impact on crypto lending, regulation, Bitcoin and ETH holders.

+3 sources across the wider coverage universe

Ex-Celsius CEO Mashinsky files pro se motion to vacate 12-year fraud sentence, blames SBF for CEL manipulation2026-05

Ex-Celsius CEO Mashinsky files pro se motion to vacate 12-year fraud sentence, blames SBF for CEL manipulation2026-05 Celsius gains approval to sell off Altcoins for BTC and ETH beginning July 1st 2023-06

Celsius gains approval to sell off Altcoins for BTC and ETH beginning July 1st 2023-06 Celsius returns as Ionic, ‘$20’ shares now worth $02025-02

Celsius returns as Ionic, ‘$20’ shares now worth $02025-02- Crypto lenders Voyager and Celsius are slowly working their ways towards making customers whole2023-07

Celsius Files Lawsuit Against Tether, Demands Restitution of $2.4b Worth of BTC

Tether Vows To Defend Itself Against The Litigation, Calling It A "Shake Down"2024-08

Celsius Files Lawsuit Against Tether, Demands Restitution of $2.4b Worth of BTC

Tether Vows To Defend Itself Against The Litigation, Calling It A "Shake Down"2024-08- Celsius creditors demand crypto return amidst bankruptcy as ETH sales fuel suspicions of prioritizing corporate needs.2023-12

Celsius Network: Collapse, Bankruptcy, and the Future of a Fallen Crypto Lender

Celsius Network was a centralized crypto lending platform that promised high yields on Bitcoin, ETH, and other digital assets, but ultimately collapsed in 2022, entered Chapter 11 bankruptcy, and re-emerged in 2024 as a creditor-owned Bitcoin mining business after one of the most consequential failures in crypto finance. Its downfall triggered years of litigation, regulatory actions, and clawbacks, turning Celsius into a case study in counterparty risk, crypto lending, and the legal status of customer assets in insolvency.

What Celsius Was Supposed To Be

Celsius Network launched in 2017 as a crypto “banking alternative” that aimed to let users “unbank” themselves by depositing digital assets and earning yield, or by borrowing against those assets without selling them. The company, founded by entrepreneur Alex Mashinsky and partners, positioned itself as a kind of crypto-native savings-and-loans provider, built on the idea that it could generate returns by lending crypto to institutions, engaging in market-making, and participating in DeFi protocols, while sharing a portion of those returns with retail depositors.

The core offering revolved around its Earn product, which allowed customers to transfer cryptocurrencies to Celsius and receive periodic “rewards” denominated either in-kind or in the platform’s native CEL token. Promotional material and public statements emphasized unusually high yields, often far above traditional savings accounts, and portrayed Celsius as a safer, more transparent alternative to conventional banks, despite the lack of formal deposit insurance and the speculative nature of its underlying activities. Over a few intense years of a bull market, Celsius attracted hundreds of thousands of customers globally and billions of dollars’ worth of Bitcoin, ETH, and other digital assets under management.

To many retail users, Celsius appeared to sit somewhere between a crypto exchange and a bank, with its mobile app interface, simple onboarding, and seemingly stable interest payouts. However, legally and structurally it operated more like an unsecured lending scheme: customers transferred ownership or control of their assets to the platform in exchange for a contractual promise of yield, while Celsius retained broad discretion to rehypothecate those assets, deploy them into leveraged strategies, and pledge them as collateral for its own borrowing. That gap between the perception of safe deposit-like accounts and the reality of unsecured claims became the central fault line when the firm failed.

Ex-Celsius CEO Mashinsky files pro se motion to vacate 12-year fraud sentence, blames SBF for CEL manipulation

Mashinsky filed a pro se motion in SDNY on Tuesday to vacate his 144-month sentence, citing ineffective counsel and "fruit of the poisonous tree" after his lawyers stopped communicating with him. The ex-Celsius CEO now pins the CEL token manipulation he was convicted for on SBF — alleging the former FTX boss "intended to destroy Celsius" — and accuses former Celsius CRO Roni Cohen-Pavon of attempting a hostile takeover. Judge Koeltl sentenced him in May 2025 for commodities and securities fraud, and Mashinsky has been representing himself since announcing the switch on May 5.

Readers clicked Celsius stories not for the collapse itself but for the drawn-out accountability chain — who got arrested, who got sentenced, whether creditors actually recovered money, and whether the legal system could claw back losses from a founder who publicly misled depositors.↗

Business Model: Earn, Borrow, CEL, and Hidden Risks

Celsius’s business model had several pillars that created both its rapid growth and its fragility. On the asset side, the company lent customer crypto to institutional borrowers such as hedge funds and market-makers, and also deployed funds into various yield-generating strategies, including DeFi protocols and arbitrage trades. On the liability side, it owed yield and eventual principal repayment to its customers, whose deposits were used to fund these activities. The spread between what Celsius earned and what it paid users was meant to sustain the platform and, in theory, generate profits for equity holders.

The Earn product was the headline feature. Customers could deposit Bitcoin, ETH, stablecoins, and other tokens and receive returns often in the range of several percentage points annually, sometimes boosted by opting to receive rewards in CEL, the platform’s own token. These yields were marketed as relatively stable and recurring, with promotional messaging emphasizing that Celsius did the hard work of yield generation on behalf of users, while they simply enjoyed “rewards” for HODLing. Regulators later argued that, economically, these arrangements resembled interest-bearing securities offered to the public without registration or adequate disclosure.

On the borrowing side, users could post crypto as collateral and take out loans in fiat or stablecoins, usually with conservative loan-to-value ratios. The ability to borrow against Bitcoin and ETH without triggering taxable events was particularly appealing during the bull market. Yet this also created leverage within the system, as Celsius had to manage collateral values, market volatility, and liquidity for both its institutional loan book and its retail margin lending.

CEL, the platform’s utility token, added another layer of complexity. Celsius used CEL to offer enhanced yields and benefits to users, encouraging them to buy and hold the token. Prosecutors and regulators later alleged that Mashinsky and Celsius executives supported CEL’s price through manipulative trading and used misleading statements about demand and tokenomics to support its valuation. When market conditions deteriorated and confidence in Celsius’s solvency evaporated, CEL’s price crashed, undermining a key part of the firm’s capital and incentive structure.

Underneath the marketing language about safety and transparency, the business depended heavily on maturity and liquidity transformation. Short-term, on-demand liabilities to retail depositors were funded by longer-term, often illiquid positions in loans and DeFi strategies. When crypto markets were rising and liquidity was abundant, this mismatch remained hidden. When markets turned, the same structure created a classic run risk: once doubts surfaced, customers rushed to withdraw funds that Celsius could not quickly recover from its counterparties or unwind from complex positions.

From Bull Market Darling To Bankruptcy Debtor

The collapse of Celsius cannot be understood in isolation from the broader boom-and-bust cycle that hit crypto in 2021–2022. During the bull market, high-yield lending and DeFi strategies proliferated, with platforms like Celsius, BlockFi, and Voyager competing to offer the most attractive rates. At the same time, large institutional players and hedge funds, such as Three Arrows Capital (3AC), used leverage and borrowed funds to pursue aggressive directional bets. This created an interconnected web of credit exposure and rehypothecation across both centralized lenders and on-chain protocols.

In 2022, a series of shocks destabilized this ecosystem. The collapse of the TerraUSD (UST) stablecoin and the Anchor protocol, which had offered unsustainably high yields on UST deposits, destroyed tens of billions of dollars in value and undermined confidence in high-yield crypto products. Major funds such as 3AC failed, dragging down lenders with exposure to them. The failure of FTX later in 2022 further damaged trust in centralized platforms, but Celsius was already in deep crisis by mid-year.

Celsius’s trouble became impossible to hide in June 2022, when it froze withdrawals, swaps, and transfers, citing “extreme market conditions.” That move signaled that the company could not meet customer withdrawal demands in full and in real time, raising immediate fears of insolvency. As more details later emerged in court filings, it became clear that Celsius had suffered substantial trading and lending losses, held significant exposure to failed or stressed counterparties, and had engaged in complex transactions that impaired its liquidity position.

On July 13, 2022, Celsius Network LLC and several affiliates filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Southern District of New York. Chapter 11 allowed the company to continue operating under court supervision while it developed a plan to reorganize or liquidate in an orderly fashion. Importantly, it also centralized all creditor claims and disputes in one forum and imposed an automatic stay on many lawsuits and collection efforts. For crypto users, this marked a key turning point: coins they thought of as “on deposit” became part of a bankruptcy estate, subject to U.S. insolvency law and creditor priority rules.

A central legal question was whether customer deposits, especially in the Earn program, remained the property of users or had become the property of Celsius upon transfer, leaving customers with only unsecured claims for dollar-denominated value. The bankruptcy court ultimately concluded that, under Celsius’s Terms of Use, assets in the Earn program were indeed property of the estate, giving Celsius legal title to those coins and demoting users to unsecured creditors for their dollar-equivalent claims. This ruling was devastating for those who believed they still “owned” their Bitcoin and ETH, and it set a precedent for similar cases involving centralized yield platforms.

Tether settled its Celsius lawsuit with a $299.5M payment—far less than the $4.5B originally sought—closing disputes over Bitcoin liquidations before Celsius’s collapse.

How is Alex, former CEO, faring now in prison.. Update should be made and why did Tether pay almost $300m compared to the original payment?

- 01creditor recovery and distributions↗

Readers with money trapped in Celsius closely tracked each court milestone, partial withdrawal window, and actual dollar amounts paid out to 251,000+ creditors.

- 02Mashinsky arrest and sentencing↗

The arc from arrest to guilty plea to 12-year sentence to pro-se appeal gave readers a rare complete accountability narrative in crypto fraud.

- 03Celsius vs. Tether lawsuit↗

A $2.4B–$4.5B lawsuit against one of crypto's most powerful entities — and its eventual $299.5M settlement — made for a high-stakes legal drama readers followed start to finish.

- 04bankruptcy reorganization into Ionic Digital↗

Readers were skeptical of the restructuring plan that converted creditor claims into shares of a new mining firm, which then cratered to near zero.

- 05altcoin liquidation and asset sales

Court-approved altcoin-to-BTC/ETH conversions and large ETH transfers to exchanges raised creditor suspicions about who benefited from the timing and sequencing.

- 06clawback lawsuits against users↗

Celsius suing its own customers to recover withdrawals made 90 days before bankruptcy was a deeply personal affront that drove clicks from affected depositors.

The Chapter 11 Case: Claims, Clawbacks, and Creditor Recoveries

Structure of the Plan and Emergence from Bankruptcy

The Celsius Chapter 11 case evolved into one of the most complex bankruptcies in crypto history, involving more than 600,000 account holders and billions of dollars in claims. Over time, a court-appointed unsecured creditors’ committee became a central player, negotiating with the estate, litigating key issues, and eventually co-developing a reorganization strategy. After extensive negotiations and multiple plan iterations, Celsius and the committee proposed a plan centered on returning a combination of cash, crypto, and equity in a new Bitcoin mining company to creditors.

In late 2023, the bankruptcy court confirmed Celsius’s plan of reorganization, which was then overwhelmingly approved by account holders, with approximately 98 percent voting in favor. Under the confirmed plan, Celsius would distribute more than US$3 billion in cryptocurrency and fiat to creditors and spin off a new Bitcoin mining company, Ionic Digital, Inc., owned by creditors and free of funded debt. This structure aimed to provide immediate, liquid value through BTC, ETH, and cash distributions, while also giving creditors upside exposure to future mining revenues via equity.

On January 31, 2024, Celsius announced that it had successfully emerged from Chapter 11 by consummating the transactions under the plan. Emergence meant that the debtor entities were no longer operating under Chapter 11 protection and that the reorganized business, focused on Bitcoin mining and related activities, could proceed under a new governance and capital structure. From a legal standpoint, this also triggered the finalization of certain claim reconciliations, the establishment of post-confirmation administrators, and the beginning of plan distributions to eligible creditors.

Distributions: BTC, ETH, Cash, and Ionic Equity

The Celsius plan contemplated several streams of recovery: cryptocurrency distributions primarily in Bitcoin and Ethereum, fiat distributions for certain creditors, and shares in Ionic Digital for eligible account holders. Crypto distributions were limited to BTC and ETH, even for users whose original deposits included a wider range of tokens, reflecting both the estate’s available assets and a desire to streamline the process. For most retail Earn creditors, recoveries were calculated on a dollarized basis as of a specified petition-date valuation, with distributions made in BTC and ETH at current market prices based on that claim amount.

The first waves of distributions began shortly after emergence, with Celsius and its distribution agents sending BTC and ETH to eligible creditors and fiat payments where applicable. A portion of the recovery also took the form of equity in Ionic Digital, which was allocated to creditors based on their allowed claims and was intended to be eventually tradable once Ionic became a publicly listed company. In practice, the timing of Ionic’s listing and the ultimate value of those shares remained uncertain, fueling frustration and debate among creditors who had expected more immediate or predictable equity value.

As distributions proceeded, Celsius and its agents issued detailed guidance about calculation methodologies, partners, and logistical issues. For example, a limited number of corporate accounts received cryptocurrency distributions through Coinbase, while most individual creditors used other designated platforms. For creditors with multiple claim types—such as Earn claims, Withhold claims, or Retail Borrower claims—distributions were aggregated, and the combined recovery was delivered in the form of BTC, ETH, or U.S. dollars, depending on the class and plan provisions.

The process continued in multiple rounds. By early 2026, Celsius had announced a forthcoming fourth distribution, projected to begin in February 2026, indicating that the estate was still monetizing assets and resolving disputes in order to fund additional creditor recoveries. For creditors whose distributions had been attempted but remained unclaimed, Celsius established deadlines; for instance, those with attempted distributions on or before February 29, 2024, were given until March 31, 2025, to redeem their funds before they might be treated as unclaimed property under applicable law.

Clawbacks, Withdrawal Preference Exposure, and EU Consumers

A particularly contentious aspect of the Celsius bankruptcy involved so-called “clawback” or preference actions. Under U.S. bankruptcy law, the estate can, in certain circumstances, seek to recover transfers made to creditors within a defined pre-bankruptcy period, on the theory that such transfers unfairly prefer those recipients over other creditors. For Celsius, this meant that customers who withdrew more than a threshold amount of crypto in the 90 days before the July 2022 filing could face lawsuits demanding the return of some or all of those withdrawals.

Celsius’s confirmed plan introduced the concept of Withdrawal Preference Exposure (WPE) as a way to quantify the extent to which a creditor’s prepetition withdrawals might be subject to clawback. WPE was used in a settlement framework that allowed many customers to resolve potential preference liability on standardized terms, often by agreeing to reduced recoveries or other adjustments rather than litigating. However, subsequent court rulings made clear that WPE did not cap the estate’s statutory avoidance rights. In a key Phase One decision, the court held that the definition of WPE in the plan applied only to the Account Holder Avoidance Action Settlement and did not limit the Litigation Administrator’s ability to pursue the full amount recoverable under sections 547 and 550 of the Bankruptcy Code against non-settling defendants.

The court also addressed threshold issues that had significant implications for foreign customers. It found that it had personal jurisdiction over all defendants who had been properly served, including non-U.S. customers, because Celsius’s Terms of Use included a New York choice-of-law clause and a mandatory forum selection provision. Furthermore, the court determined that the transfers at issue were domestic in nature, since they originated from U.S.-based accounts controlled by Celsius Network LLC, thereby sidestepping complex questions about the extraterritorial reach of U.S. avoidance law.

For European users and policymakers, these clawback lawsuits became a real-world test of how EU consumer protection and conflict-of-law rules would interact with U.S. bankruptcy preference actions. Scholars and advocates questioned whether EU consumers fully understood that they were submitting to New York law and courts when clicking through Celsius’s terms, and whether aggressive clawback actions against ordinary retail customers were consistent with European notions of fairness and consumer protection. The Celsius case thus highlighted not only the risks of using offshore or foreign crypto platforms, but also the legal leverage that U.S. courts can exert over global participants in dollar- and New York–centered financial structures.

Ongoing Litigation: The Tether Lawsuit and Settlement

Beyond disputes with its own users, Celsius also pursued litigation against third parties, seeking to enlarge the estate for the benefit of creditors. One of the most prominent cases targeted Tether, the issuer of the USDT stablecoin and operator of related entities such as Bitfinex. The dispute centered on a large margin lending relationship in which Celsius had pledged roughly 39,000 Bitcoin as collateral to Tether. In June 2022, amid Celsius’s financial distress and falling Bitcoin prices, Tether liquidated this collateral.

Celsius alleged that Tether’s liquidation was improper and violated the lending agreement. According to Celsius’s complaint, Tether failed to honor a contractual ten-hour waiting period after a margin call and sold the pledged Bitcoin at an average price of around \$20,656, allegedly below contemporaneous market rates. Celsius further claimed that Tether transferred the liquidated Bitcoin to Bitfinex accounts as partial repayment of Celsius’s outstanding debt of over \$800 million and that these actions constituted not only a breach of contract but also fraudulent and preferential transfers under U.S. bankruptcy law.

Tether, for its part, characterized the lawsuit as a baseless shakedown and argued that it had acted within the terms of the parties’ agreements, including the right to liquidate when Celsius failed to meet margin requirements. Tether also challenged the jurisdictional and domesticity aspects of the case, emphasizing that it was an offshore company. However, the U.S. Bankruptcy Court concluded that Celsius had alleged a plausible claim involving domestic activity, noting that the relevant communications and financial flows had sufficient U.S. nexus, and it denied Tether’s motion to dismiss key causes of action, including breach of contract and fraudulent transfers.

Initially, Celsius sought damages that, based on then-current Bitcoin valuations, could exceed \$4 billion. Eventually, after extensive litigation and in the context of broader estate recovery efforts, the parties reached a settlement. Tether agreed to pay approximately \$299.5 million to the Celsius bankruptcy estate, via the Blockchain Recovery Investment Consortium (BRIC), a joint recovery vehicle formed to pursue claims against various collapsed crypto firms. This amount was far less than the nearly \$4.5 billion in Bitcoin Celsius originally sought, but it effectively ended one of the most contentious adversary proceedings of the case and added a substantial cash infusion to the estate for creditor distributions.

Alex Mashinsky: From Crypto Promoter To Convicted Fraudster

Public Face of Celsius and Alleged Misconduct

Alex Mashinsky, a serial entrepreneur known for his role in early internet telephony, became the public face of Celsius Network, frequently appearing in interviews, AMAs, and promotional content to tout the platform’s advantages over traditional finance. He positioned Celsius as a trusted guardian of customer funds, asserting that the company took fewer risks than banks, that user deposits were always accessible, and that the firm generated yield through sound and transparent strategies rather than hidden leverage. These statements would later be scrutinized in detail by regulators and prosecutors.

Regulators alleged that many of Mashinsky’s claims were false or misleading. In a complaint filed in the U.S. District Court for the Southern District of New York, the Commodity Futures Trading Commission (CFTC) charged Celsius Network and Mashinsky with fraud and material misrepresentations in connection with operating a digital asset–based finance platform. The CFTC asserted that they falsely promoted the platform as generating high profits with minimal risk, inducing customers to deposit digital asset commodities such as Bitcoin and ETH based on misleading assurances about safety, liquidity, and risk management.

State-level regulators had already raised red flags before the collapse. For example, the New Jersey Bureau of Securities issued an order against Celsius in 2021, alleging that its Earn Rewards accounts constituted unregistered securities offerings and that Celsius had failed to provide investors with necessary disclosures about how funds were deployed, what risks were involved, and how rewards were generated. These actions foreshadowed the broader regulatory backlash that would follow the platform’s failure and provided early indications that authorities viewed Celsius’s Earn product as functionally similar to interest-bearing securities, not simply a “rewards” program.

Criminal Case, Sentence, and Attempts to Vacate

Following Celsius’s collapse and the civil regulatory actions, U.S. criminal authorities brought charges against Mashinsky, accusing him of orchestrating a scheme to defraud customers by misrepresenting the safety and profitability of Celsius’s business and by manipulating the price of the CEL token. Prosecutors alleged that he misused customer funds, obscured the company’s true financial condition, and supported CEL’s price in ways that created a misleading impression of demand and value. These actions, they argued, allowed Celsius to continue attracting deposits and growing its liabilities even as its balance sheet deteriorated.

In 2024, Mashinsky was sentenced to 12 years in prison after being found guilty of fraud and market manipulation. The sentence reflected both the scale of the losses suffered by Celsius customers and the perceived culpability of its leadership in misrepresenting the platform’s risks and misusing user funds. As part of the criminal proceedings and parallel civil cases, Mashinsky agreed to forfeit any claims to assets from the Celsius bankruptcy estate, ensuring that he could not personally benefit from the reorganized company or distributions intended for creditors.

Subsequently, Mashinsky continued to contest aspects of his conviction and sentence. After his legal team withdrew, he filed a motion to vacate his sentence pro se, arguing without counsel that various procedural and substantive errors justified overturning or reducing his punishment. Among other arguments, he sought to shift blame toward broader market conditions and the actions of other crypto figures, including claims about external manipulation of CEL’s price. These efforts, however, faced a high legal bar, as courts are generally reluctant to disturb jury verdicts and sentences absent clear evidence of constitutional or procedural violations.

CFTC Settlement and Permanent Trading Ban

Parallel to the criminal case, the CFTC pursued its enforcement action against Celsius and Mashinsky. In resolving the case against the company, Celsius agreed to a permanent injunction prohibiting future violations of the Commodity Exchange Act and related CFTC regulations. For the individual case, the CFTC ultimately reached a settlement that imposed significant personal consequences on Mashinsky.

Under the settlement, Mashinsky accepted a permanent ban on trading in CFTC-regulated markets and on registering with the agency, effectively barring him from serving as a principal or operator in regulated derivatives and commodity markets. He also agreed to forfeit over \$48 million and pay a civil monetary penalty, although the precise structure of these obligations interacted with his criminal forfeiture and restitution liabilities. The CFTC publicly emphasized that this was its first-ever action against a crypto lending platform and its leadership, sending a signal that it viewed misrepresentations in centralized lending as within its enforcement scope.

These sanctions, combined with the criminal sentence, marked a dramatic reversal for a figure who had spent years portraying himself as a champion of financial fairness and transparency. For the broader crypto industry, the Mashinsky outcome underscored that founders and executives of crypto platforms could face penalties comparable to those imposed on traditional financial fraudsters, particularly when retail investors bore the brunt of the losses.

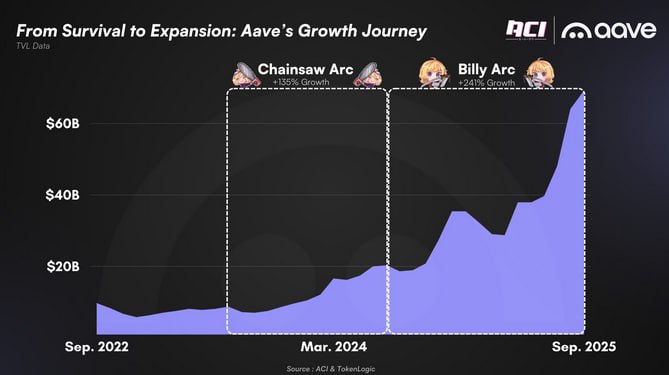

Aave DAO’s “State of the Union” recalls late 2022 chaos—FTX, Celsius & 3AC collapsed, Anchor wiped $6B, stETH depegged, TVL sank to $5B, and treasury raiders drained funds. With V3 struggling, many declared DeFi dead—but ACI launched to “Make Aave Great Again.”

New Jersey cease-and-desist order against Celsius

Celsius freezes all customer withdrawals

Celsius files Chapter 11 bankruptcy

CFTC, SEC, FBI, SDNY announce charges against Mashinsky

Celsius emerges from bankruptcy; Ionic Digital formed

Celsius begins distributing $3B+ to creditors

Mashinsky pleads guilty to fraud

Mashinsky sentenced to 12 years in prison

Celsius in the Broader Crypto and DeFi Ecosystem

CeFi vs DeFi: Perception and Reality

Celsius’s rise and fall have become a touchstone in the debate over centralized finance (CeFi) versus decentralized finance (DeFi). On the surface, Celsius offered a user experience similar to DeFi yield platforms: deposit tokens, earn yield, borrow against collateral. However, unlike protocols such as Aave or Compound, Celsius was a black box where key operations, risk management decisions, and counterparty exposures were opaque to users. All meaningful decisions were made by a centralized team, and customers had little recourse or visibility into how their assets were actually used.

The 2022 crisis exposed this difference starkly. While some DeFi protocols suffered losses or depeggings, many core lending platforms such as Aave remained solvent and functioning, precisely because their rules were on-chain, collateralized positions were transparently monitored, and liquidations occurred according to predefined logic rather than discretionary management. In a “State of the Union” reflection, contributors to the Aave DAO recalled the late 2022 chaos, including the collapses of FTX, Celsius, and 3AC, as well as the UST/Anchor implosion and the stETH depeg, noting that total value locked in DeFi fell sharply and that many pronounced DeFi “dead” at the time.

Yet the key point was that the failures most damaging to retail users were heavily concentrated in centralized platforms like Celsius and FTX, where governance was opaque and legal structures turned depositors into unsecured creditors. This distinction has informed both regulatory conversations and user behavior. Some investors have become more cautious about CeFi platforms that offer high yields without clear on-chain collateralization or audited transparency, while others continue to use centralized lenders despite the risks, attracted by convenience and branding.

Regulatory and Policy Implications

Regulators have used the Celsius case as a catalyst for scrutinizing crypto lending and staking products more broadly. The New Jersey enforcement action against Celsius in 2021, which argued that Earn Rewards accounts were unregistered securities, foreshadowed later actions against other platforms offering similar products. In the wake of Celsius’s bankruptcy, both the U.S. Securities and Exchange Commission (SEC) and state regulators intensified their focus on whether yield-bearing crypto accounts constituted securities or investment contracts subject to registration and investor protection requirements.

The CFTC’s case against Celsius and Mashinsky further expanded the regulatory perimeter by framing misrepresentations about crypto lending and yield-generation as commodity fraud, especially where underlying assets such as Bitcoin and ETH are treated as commodities under U.S. law. Taken together, these actions indicate that multiple agencies assert jurisdiction over different aspects of centralized crypto lending, increasing the compliance burden for any platform seeking to operate in the U.S. market.

Policy debates have also centered on the treatment of customer assets in insolvency. The Celsius ruling that Earn assets were property of the estate, rather than customer property held in trust or custody, highlights the importance of precise contractual language and custodial structures. Regulators and lawmakers have begun to explore clearer requirements for segregation of customer assets, explicit disclosures about ownership and rehypothecation, and possibly special regimes for “crypto custodians” analogous to those for broker-dealers or futures commission merchants.

Internationally, the Celsius clawback actions against EU consumers have sparked discussion about the intersection of U.S. bankruptcy law with foreign consumer protection regimes. Some European commentators argue for stronger local safeguards against the enforcement of foreign forum selection clauses against retail consumers in complex financial products, especially where the consumers may not fully understand the implications of such terms.

Market Memory and the Return of Crypto Lending

Despite the cautionary lessons of Celsius, crypto lending has not disappeared. As markets recovered and Bitcoin prices climbed, lending and yield products began to re-emerge, both on centralized exchanges and within DeFi protocols. Bloomberg’s coverage has noted that crypto lending volumes and total value locked (TVL) have risen again, even as the memory of Celsius, BlockFi, and Voyager’s bankruptcies remains fresh. This cyclical pattern raises the question of whether market participants are sufficiently pricing in counterparty risk or whether yield hunger is driving a return to similar structures under new branding.

DeFi communities have responded by emphasizing risk controls, decentralization, and transparency. For example, the Aave DAO’s reflections on the post-2022 period included efforts to strengthen protocol governance, risk parameters, and the resilience of liquidity pools, under slogans like “Make Aave Great Again.” Yet even in DeFi, new forms of complexity—such as liquid staking derivatives and cross-chain bridges—introduce risks that can be difficult for ordinary users to evaluate.

Celsius thus functions as both a historical event and an ongoing reference point. When new centralized platforms advertise double-digit yields on crypto deposits, market observers routinely compare them to Celsius and ask whether the underlying business model has truly changed or merely been rebranded. For regulators and policy advocates, the case provides concrete evidence of the harms that can arise when retail investors treat unsecured claims on opaque entities as if they were insured deposits or segregated custodial holdings.

Ionic Digital: The Post-Bankruptcy Mining Spin-Off

Structure, Ownership, and Strategy

A distinctive feature of Celsius’s reorganization plan was the creation of Ionic Digital, Inc., a new Bitcoin mining company owned by Celsius creditors. The idea was to convert part of the creditors’ recovery into equity in a going-concern business that could, in theory, benefit from Bitcoin’s long-term price appreciation and mining economics. This approach contrasted with a pure liquidation, which would simply sell all assets and distribute the proceeds in cash or crypto, potentially locking in depressed market values.

Under the plan, Celsius’s mining assets, including data center operations, mining rigs, and related infrastructure, were transferred into Ionic Digital. The company was structured to have no funded debt, meaning it did not emerge with pre-existing leverage, which was intended to improve its resilience in the inherently volatile mining sector. Creditors received shares in Ionic proportionate to their allowed claims, turning them into shareholders collectively holding the entire equity of the new company.

Ionic’s business strategy centered on operating Bitcoin mining facilities in regions with access to relatively low-cost electricity, such as West Texas, where abundant energy infrastructure and, in some cases, favorable grid dynamics have attracted miners. The company also held a material amount of Bitcoin on its balance sheet, effectively functioning as both a mining operation and a BTC treasury vehicle, which aligned its fortunes with the broader Bitcoin market.

Listing, Valuation, and Creditor Expectations

From the outset, a key question for creditors was whether and when Ionic would achieve a public listing, such as on Nasdaq, to allow them to trade their shares and realize value. Commentary around Ionic’s transition suggested an expectation, or at least an aspiration, to list the company on a public exchange, thereby converting illiquid private shares into tradable equity. However, the process of preparing audited financials, meeting listing requirements, and navigating regulatory reviews proved more complex and time-consuming than some creditors had hoped.

Discussions among creditors and observers have highlighted the gap between the plan-era notional valuation of Ionic shares and their perceived realizable value in practice. At confirmation, plan documents and communications sometimes referenced reference values or suggested that the equity component could be worth a specific per-share figure under certain assumptions. Over time, however, delays in listing, uncertainties about mining profitability, and broader market volatility led many creditors to fear that their Ionic stake might be worth significantly less—or even effectively zero—if the company could not access public markets or generate sufficient cash flows.

It is important to distinguish between the book value of Ionic, as reflected in its assets and accounting, and the market value that equity might command if and when the shares become freely tradable. Mining company valuations tend to be highly sensitive to Bitcoin price, network difficulty, energy costs, and investor sentiment about the sector. For Celsius creditors, this means that the ultimate value of their Ionic equity could vary dramatically over time. In the meantime, the lack of liquidity leaves many in a holding pattern, with their recovery partly tied to a venture they did not voluntarily choose.

Governance, Transparency, and the Legacy of Celsius

Ionic’s governance structure and transparency practices are closely watched by former Celsius users who now hold its equity. Given the history of misrepresentation and opaque risk-taking at Celsius, creditors have pressed for stronger disclosure, oversight, and accountability in the mining company. While Ionic is structurally separate from the old Celsius lending business, its origin in a bankruptcy reorganization and its unusual shareholder base—tens of thousands of former creditors rather than traditional institutional investors—make its governance challenges unique.

The mining business also introduces its own risk profile. Electricity prices can change, regulatory attitudes toward mining can evolve, and Bitcoin’s halving cycles can compress margins. Ionic’s choice to maintain a Bitcoin treasury exposes it to BTC price volatility, which can amplify both upside and downside scenarios for equity holders. For some creditors, this exposure is a feature rather than a bug—they wanted to retain Bitcoin upside rather than be fully cashed out in fiat. For others, it represents an additional layer of risk imposed on them long after they believed they were simply holding assets on a lending platform.

Nonetheless, the creation of Ionic reflects a broader trend in crypto bankruptcies: rather than purely liquidating, some estates attempt to preserve or create going-concern value in related businesses (such as mining, technology, or IP) and distribute that value to creditors. Whether this model ultimately benefits Celsius creditors will depend on Ionic’s execution and market conditions in the years ahead.

Celsius operated as a fully custodial, opaque lender where a single founder controlled asset deployment and publicly misrepresented the platform's health to depositors.

Celsius and Mashinsky faced simultaneous enforcement from the CFTC, SEC, FBI, SDNY, and New York AG, resulting in criminal conviction, a permanent trading ban, and ongoing civil litigation.

Celsius froze withdrawals for all 1.7 million users in June 2022 with no warning, exposing the fatal mismatch between illiquid yield strategies and on-demand withdrawal promises.

Celsius deployed customer funds into DeFi protocols including Aave and used stETH as collateral; the stETH depeg in mid-2022 accelerated its insolvency spiral.

The collapse of LUNA/UST in May 2022 triggered cascading losses across Celsius's leveraged positions, turning a liquidity stress into a solvency crisis within weeks.

While over $3B was ultimately distributed to creditors, the Ionic Digital share component — meant to represent upside — collapsed to near zero, leaving many creditors with less than expected.

Ongoing Effects: Asset Sales, Creditor Tensions, and Data Risks

Even after emergence from Chapter 11, the Celsius saga continues to influence crypto markets and creditor behavior. One area of ongoing attention is the estate’s management and unwinding of remaining crypto holdings, including ETH and other assets that are not immediately distributed. On-chain analysts have tracked movements from addresses associated with Celsius, including transfers of large amounts of staked ETH to exchanges and trading firms, sparking debates about whether these sales are depressing prices or favoring certain counterparties over others.

Some creditors have expressed concern that ETH and other token sales are being executed in ways that prioritize institutional or corporate interests, such as liquidity providers or structured counterparties, rather than maximizing net recovery for ordinary users. These tensions reflect a broader theme in bankruptcies: decisions about when, how, and at what price to sell assets are inherently judgment calls, and different stakeholders may disagree about how to balance speed, market impact, and risk.

There have also been operational and security incidents that further strain trust. Reports of a data breach affecting Celsius creditors, involving exposure of personal information such as names, contact details, or account identifiers, highlight the ongoing risks that linger even after the financial questions are nominally resolved. For affected individuals, such breaches can create vulnerabilities to phishing, scams, or identity theft, underscoring that the consequences of engaging with a failed platform can extend well beyond financial losses.

At the same time, the estate and its administrators continue to pursue recoveries, manage unclaimed property, and address disputes over preference liability and claim classification. For some creditors, particularly those located outside the U.S. or with relatively small claims, the administrative burden of engaging with these processes can feel disproportionate to the potential recovery. Others remain actively involved, participating in creditor groups, following court filings, and advocating for particular strategies in ongoing litigation and asset sales.

Conclusion and Outlook

The Celsius story encapsulates many of the central tensions in crypto finance: the allure of high yields versus the reality of counterparty risk; the promise of decentralization versus the convenience of centralized platforms; and the collision between crypto-native business models and traditional legal frameworks like securities regulation and bankruptcy law. From its origins as a user-friendly lending app to its collapse in 2022, its complex Chapter 11 process, and its rebirth as a creditor-owned Bitcoin miner, Celsius has left a deep mark on both market practices and regulatory thinking.

For Bitcoin and ETH holders, the core lesson is that where assets are held and under what legal terms matters as much as the assets themselves. Customers who believed they were simply “earning yield” on coins held in accounts discovered that, legally, they were unsecured creditors of a distressed company, with their recovery dependent on court decisions, estate recoveries, and negotiated plans rather than immediate access to their tokens. The status of those assets in insolvency turned on dense contractual language and jurisdictional clauses that few retail users had fully digested.

Regulators have responded by pushing for clearer rules and stronger enforcement. Actions by state securities regulators, the SEC, and the CFTC against Celsius and similar platforms signal a view that many high-yield crypto products are, in substance, securities or commodities-related investment schemes requiring registration, disclosure, and supervision. The Mashinsky prosecutions and sanctions demonstrate that executives who mislead investors or misuse funds can face criminal exposure and lifetime bans from regulated markets. At the same time, policymakers are grappling with how to design regimes for crypto custodians and lenders that adequately protect consumers without stifling innovation.

For DeFi and protocols like Aave, Celsius’s failure has served as both a warning and an opportunity. It highlighted the dangers of opaque leverage and the reputational contagion that centralized failures can inflict on the broader crypto ecosystem. Yet it also underscored the relative resilience of well-designed on-chain protocols, whose rules are transparent and whose liquidations are algorithmic rather than discretionary. This contrast has informed rebranding efforts, risk parameter tuning, and community governance reforms within DeFi.

Looking forward, Celsius’s legacy will likely be felt in three main arenas. First, in market behavior, where memories of the collapse may temper enthusiasm for unregulated high-yield products, even as new variants continue to appear in each bull cycle. Second, in law and regulation, where the precedents set on asset ownership, clawbacks, and cross-border consumer exposure will inform future cases and rulemaking. Third, in the fortunes of Ionic Digital, whose success or failure as a creditor-owned Bitcoin miner will determine whether Celsius’s reorganization strategy ultimately delivers meaningful upside to those who once simply thought they were depositing Bitcoin and ETH to earn interest.

The Celsius saga is therefore not just a story about one failed company. It is an evolving case study in how crypto intersects with traditional legal and financial systems, how narratives of decentralization can obscure very centralized risks, and how the industry, regulators, and users adapt after a high-profile collapse. For anyone participating in crypto lending—whether through centralized platforms, DeFi, or hybrid models—understanding what happened at Celsius is essential to understanding the risks and responsibilities of the space today.

Latest Celsius news

Ex-Celsius CEO Mashinsky files pro se motion to vacate 12-year fraud sentence, blames SBF for CEL manipulationTether settled its Celsius lawsuit with a $299.5M payment—far less than the $4.5B originally sought—closing disputes over Bitcoin liquidations before Celsius’s collapse.Aave DAO’s “State of the Union” recalls late 2022 chaos—FTX, Celsius & 3AC collapsed, Anchor wiped $6B, stETH depegged, TVL sank to $5B, and treasury raiders drained funds. With V3 struggling, many declared DeFi dead—but ACI launched to “Make Aave Great Again.” NY bankruptcy judge greenlights $4.3 billion dollar Celsius lawsuit against Tether

NY bankruptcy judge greenlights $4.3 billion dollar Celsius lawsuit against Tether Celsius founder Alex Mashinsky sentenced to 12 years.

Celsius founder Alex Mashinsky sentenced to 12 years. Celsius founder Alex Mashinsky heads into sentencing

Celsius founder Alex Mashinsky heads into sentencingSources

- https://en.wikipedia.org/wiki/Celsius_Network

- https://frblaw.com/celsius-bankruptcy-litigation-update-key-phase-one-rulings-and-strategic-considerations-for-defendants-in-phase-two-and-beyond/

- https://www.cftc.gov/PressRoom/PressReleases/8749-23

- https://www.whitecase.com/news/press-release/white-case-leads-celsius-creditors-committee-successful-chapter-11-exit-and

- https://celsiusdistribution.stretto.com/support/solutions/articles/153000252038-fourth-distribution

- https://todaysgeneralcounsel.com/celsius-lawsuit-against-tether-for-allegedly-improper-bitcoin-liquidation-to-proceed/

- https://bitcoinmagazine.com/business/tether-pays-300-million-to-settle-4-5-billion-celsius-bankruptcy-claims

- https://www.tradingview.com/news/cointelegraph:9e28a96a4094b:0-celsius-mashinsky-gets-permanent-trading-ban-in-cftc-settlement/

- https://policyreview.info/articles/analysis/celsius-clawbacks-against-eu-consumers

- https://celsiusdistribution.stretto.com/support/solutions/articles/153000147044-distribution-calculation-partners-reporting-and-other-questions

- https://www.tradingview.com/news/cointelegraph:173df8786094b:0-ex-celsius-ceo-files-motion-to-vacate-sentence-after-lawyers-withdraw/

- https://www.nasdaq.com/press-release/celsius-emerges-from-chapter-11-and-commences-distributions-of-over-$3-billion-of

- https://celsiusdistribution.stretto.com/support/solutions/articles/153000234707-unclaimed-property

- https://www.youtube.com/watch?v=9ufbqV_MTGU

- https://www.coinbase.com

- https://www.facebook.com/bloombergbusiness/posts/crypto-lending-is-on-the-rise-again-among-exchanges-despite-the-risks/751562973496465/

- https://www.law360.com/articles/2489216/cftc-secures-trading-ban-against-celsius-mashinsky

- https://governance.aave.com/t/aave-dao-s-state-of-the-union-by-aci/23124

- https://www.nj.gov/oag/newsreleases21/Celsius-Order-9.17.21.pdf

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…