Explainer on crypto delisting: how and why exchanges remove tokens, impacts on liquidity and pricing, differences from stock delistings, effects on USDT pairs, WBTC and stablecoins, legal and EU angles, and how traders can navigate and manage delisting risk.

+5 sources across the wider coverage universe

With Maker's recent delisting of WBTC, dlcBTC could emerge as a safer wrapped Bitcoin—hear insights from Aki, dlcBTC's CEO, on the Unchained podcast.2024-08

With Maker's recent delisting of WBTC, dlcBTC could emerge as a safer wrapped Bitcoin—hear insights from Aki, dlcBTC's CEO, on the Unchained podcast.2024-08 Coinbase, Binance, and other EU Crypto Asset Service Providers are phasing out and delisting stablecoins not regulated under MiCA2024-10

Coinbase, Binance, and other EU Crypto Asset Service Providers are phasing out and delisting stablecoins not regulated under MiCA2024-10 DefiLlama's 0xngmi rebuts critiques on the delisting of Aster2025-10

DefiLlama's 0xngmi rebuts critiques on the delisting of Aster2025-10 Bit Global sues Coinbase for $1 billion over WBTC delisting2024-12

Bit Global sues Coinbase for $1 billion over WBTC delisting2024-12 Anchorage Digital’s Stablecoin Safety Report draws criticism for alleged inaccuracies and undisclosed Paxos ties, as Agora’s CEO accuses firm of “Pay to Play” tactics in delisting USDC and AUSD2025-06

Anchorage Digital’s Stablecoin Safety Report draws criticism for alleged inaccuracies and undisclosed Paxos ties, as Agora’s CEO accuses firm of “Pay to Play” tactics in delisting USDC and AUSD2025-06 Binance’s pivot to USDC is a calculated move, not panic, with USDC’s market share on the exchange jumping from 0.48% to 8.26% year-to-date, as upcoming EU regulations drive the delisting of USDT and fuel a $351B DeFi boom where compliance, liquidity, and stablecoin infrastructure are king.2025-03

Binance’s pivot to USDC is a calculated move, not panic, with USDC’s market share on the exchange jumping from 0.48% to 8.26% year-to-date, as upcoming EU regulations drive the delisting of USDT and fuel a $351B DeFi boom where compliance, liquidity, and stablecoin infrastructure are king.2025-03

Delisting in Crypto: How Token Removals Reshape Markets

Delisting is the process by which an exchange or platform removes an asset from trading, meaning users can no longer buy or sell that asset there, even though the token or share itself usually continues to exist elsewhere. In crypto, delisting decisions by major venues such as Binance and Coinbase can instantly transform liquidity, pricing, and even the perceived legitimacy of a token, making it crucial for traders to understand how and why delistings happen, what they signal, and how to respond.

What “Delisting” Really Means

Delisting sounds simple on the surface—an asset disappears from an exchange’s trading screen—but the underlying mechanics and consequences are more nuanced. In its most basic sense, delisting refers to the removal of an asset from a trading venue’s order book so that it can no longer be traded there. When a cryptocurrency is delisted on a centralized exchange, all active spot and margin trading pairs for that token are typically suspended and removed, and users are given a limited window to withdraw their holdings or convert them into other assets before full support ends. After that window closes, the exchange may no longer allow deposits or withdrawals of the asset at all, even though the token continues to exist on its native blockchain.

This core structure closely mirrors how delisting works in traditional equity markets. When a stock is delisted from a venue like the NYSE or Nasdaq, the shares are removed from the exchange’s board and no longer trade there, although shareholders still own their stock. In both contexts, delisting is fundamentally about the relationship between an asset and a particular marketplace, not about destroying the underlying asset itself. The key difference is that blockchain-based tokens remain natively transferable on-chain even if every centralized exchange delists them, while delisted stocks typically migrate to less regulated over-the-counter (OTC) markets rather than a public, permissionless ledger.

It is also important to distinguish between full asset delisting and narrower actions such as removing specific trading pairs. Binance, for example, sometimes delists individual spot trading pairs that have poor liquidity or very low volume, while leaving the underlying tokens tradable against other bases like USDT or BTC. In that case, the exchange is pruning specific markets rather than expelling the asset entirely, and the same token might continue to trade robustly in other pairings. Traders who see a headline such as a “USDT pair delisting” therefore need to read the details carefully to understand whether the token itself is being removed or only a particular market configuration is disappearing.

Comparing Crypto and Stock Delistings

A side‑by‑side comparison helps clarify the shared logic and key differences between delisting in crypto and in traditional stock markets:

| Dimension | Crypto exchange delisting | Stock exchange delisting |

|---|---|---|

| What is removed | Trading pairs and often deposit/withdrawal support on a centralized exchange | Trading of the company’s shares on a regulated exchange such as NYSE or Nasdaq |

| Asset existence | Token continues to exist on its blockchain; may trade on other exchanges or DEXs | Shares continue to exist but usually migrate to OTC markets if at all |

| Common reasons | Low liquidity, regulatory pressure, project risk, security incidents, strategic changes | Failure to meet listing standards (price, market cap), regulatory violations, corporate actions |

| Investor outcome | Users retain on‑chain ownership if they withdraw before support ends; market value often falls, liquidity collapses | Shareholders still own stock but may face steep devaluation and harder trading conditions; some lose everything in bankruptcies |

| Typical recourse | Move tokens to another venue or self‑custody; search for alternative liquidity | Trade OTC, accept losses, or wait for corporate events (acquisitions, restructurings) |

Regulated stock exchanges operate with detailed listing standards—covering minimum prices, market capitalisation, reporting obligations, and governance—backed by securities law and supervisory agencies. For instance, both NYSE and Nasdaq enforce a minimum price rule of around 1 USD, and companies that trade below that threshold for a sustained period can face accelerated delisting unless they regain compliance. This dynamic is evident in real cases such as the Chinese company Cango, which received an NYSE non‑compliance notice over its sub‑1‑dollar share price and must now raise its price or risk delisting entirely. Once delisted, a stock may trade OTC, but liquidity tends to be thin, spreads wide, and long‑term value uncertain.

Crypto exchanges borrow some of this logic but operate in a much more fragmented and lightly regulated environment. There is no single authority equivalent to the SEC or an exchange’s listing committee overseeing token listings across the entire market, and each venue sets its own standards and delisting criteria. As a result, a project can be delisted on one platform while remaining fully listed on dozens of others, or vice versa, and tokens can continue to circulate on decentralized exchanges even if every major centralized venue removes them. This mixture of similarities and differences makes understanding delisting a core part of reading the health of a crypto asset and the venues it trades on.

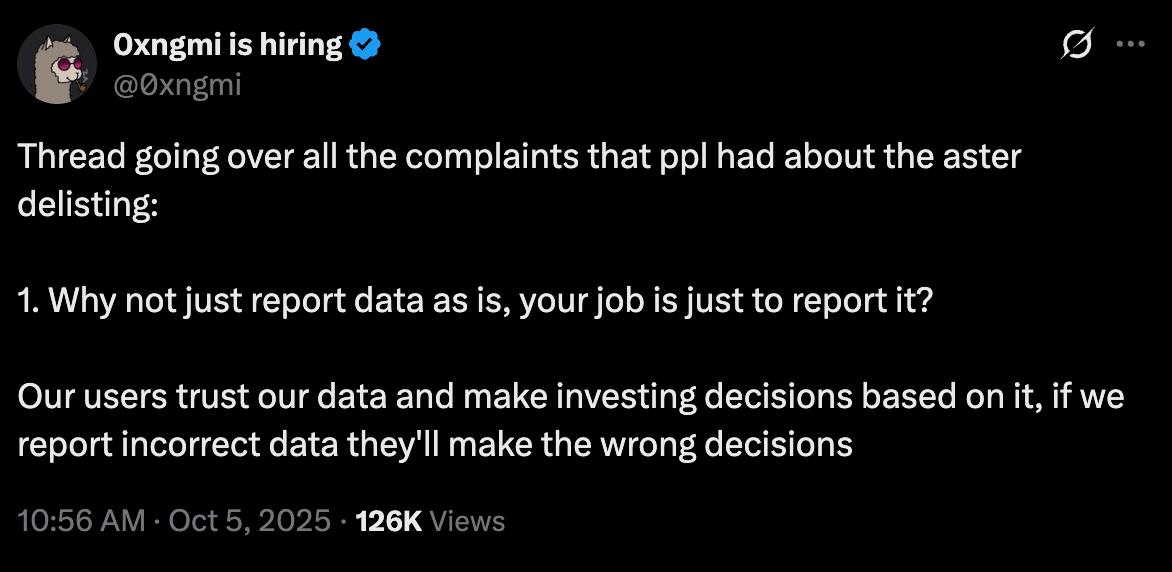

DefiLlama's 0xngmi rebuts critiques on the delisting of Aster

Should've delisted quietly again. If there is more to the story than just "wash trading", DeFiLlama causing unnecessary FUD.

Readers do not click delistings for the token price impact — they click because high-profile delistings expose who actually controls which assets survive: exchanges and protocols wielding unilateral listing power trigger billion-dollar lawsuits, regulatory realignments, and accusations of pay-to-play curation that reveal listing decisions as de facto industry gatekeeping.↗

How Delisting Works on Centralized Crypto Exchanges

The mechanics of delisting on centralized crypto exchanges (CEXs) follow a fairly recognizable pattern, even though the exact rules vary from platform to platform. Major exchanges typically have internal listing committees or risk teams that periodically review existing assets against a set of standards, such as liquidity, compliance posture, security record, and development activity. When a token begins to fall short—for instance, due to vanishing volumes, regulatory scrutiny, or project abandonment—the exchange might first flag it for heightened monitoring, then impose restrictions, and ultimately announce a full delisting.

Binance, the world’s largest crypto exchange by volume, makes this process visible through its “Monitoring Tag” system, under which it marks certain assets as needing enhanced due diligence by users. Tokens that carry the tag might have issues such as low liquidity, project risk, or regulatory uncertainty, and Binance explicitly warns that these assets are at higher risk of delisting if they fail to improve their metrics or address identified concerns. Periodic review announcements and lists of extended monitoring tags give traders an early indication of which markets might be on the chopping block, even before a formal delisting notice is published.

From Watchlist to Removal: The Delisting Lifecycle

Once an exchange decides to delist an asset, it usually follows a staged process designed to protect users while allowing an orderly wind‑down of trading. Both educational resources and concrete announcements from exchanges reveal a broadly similar lifecycle across platforms. First, the exchange publishes a public announcement describing the planned delisting, including the token or trading pairs affected, the exact dates and times when trading will cease, and any deadlines for deposits and withdrawals. This announcement may also provide a high‑level reason such as poor liquidity, regulatory requirements, or security concerns.

Next, trading on the impacted markets is disabled at the specified time. Binance’s notices, for example, routinely state that spot trading in certain pairs—such as ADX/BTC or WBTC/ETH in one recent update—will cease at a precise UTC time because a periodic review found insufficient liquidity or volume. After trading stops, the exchange may cancel all open orders on the delisted markets automatically to prevent stale orders from lingering and confusing users. Coinbase explicitly notes in its market rules that orders associated with delisted assets or disabled markets can be cancelled at its discretion, underscoring that the platform controls which markets remain active.

For a transitional period after trading ends, users are typically allowed to withdraw delisted tokens or, in some cases, swap them into other supported assets. Paybis and CoinMarketCap both emphasize that investors are normally given a specific time window to withdraw their funds before the exchange fully stops supporting the asset. Binance likewise highlights that platforms often provide a transition period during which users can withdraw or convert their tokens before the delisting becomes final. If users miss those deadlines, they may lose the ability to move those assets off the platform entirely, even though the tokens still exist on‑chain, because the exchange stops processing transactions for them.

The way this final step is handled varies by business model. Some platforms, such as the Dutch brokerage Finst, have announced that if users still hold delisted assets like WBTC or stETH past the withdrawal deadline, the platform will automatically sell those positions on the users’ behalf at the best available market price and credit the proceeds, minus fees. That approach reduces the risk of stranding illiquid assets on custodial accounts but exposes users to forced sales at potentially unfavourable prices. Others simply freeze unsupported assets in place, leaving them inaccessible until, if ever, the platform reintroduces support.

Spot, Margin, and Derivatives Delistings

Delisting takes different forms across spot markets, margin trading, and derivatives such as perpetual futures. Spot delisting is the most straightforward: the exchange removes one or more trading pairs for an asset from its spot order books, meaning users cannot submit new buy or sell orders for that pair. In many cases, this is combined with disabling new margin positions or collateral use for that asset to avoid runaway risk as liquidity dries up. Margin positions that remain open may be given a grace period to close, or they might be force‑liquidated or converted at the delisting price.

Derivatives platforms, particularly those offering perpetual futures, follow more specialised procedures because they must ensure fair settlement of outstanding contracts. Bybit, for example, states in its delisting announcements that when it delists a perpetual contract such as SKYAIUSDT, open positions will be settled at a final index price at the delisting time, and the contract will then cease trading. Users are urged to close or adjust positions before the deadline to manage their risk, as leveraged positions can move rapidly in thin markets approaching delisting. Similar procedures apply to other derivatives venues, with variations in how funding, margin, and final settlement are handled.

Recent market events show how derivatives delistings can create ripple effects across the broader ecosystem. When perpetual futures referencing smaller tokens like NFP/USDT or SkyAI/USDT approach delisting, liquidity can collapse quickly as arbitrageurs and market‑makers wind down their exposure, sometimes leading to sharp, erratic price moves. In DeFi, the threat of delisting an asset that is widely used as collateral—for example, certain restaking tokens in lending protocols—can create concerns about liquidity lockups and bad debt if the market for that collateral dries up faster than positions can be unwound. These linkages make it vital for traders using leverage or borrowing against niche tokens to watch delisting calendars closely and understand how their positions might be affected.

Partial Delistings: Trading Pairs versus Full Asset Support

A subtle but critical distinction in crypto is between delisting a trading pair and completely removing an asset from an exchange’s ecosystem. Binance explicitly notes in some announcements that removing certain spot trading pairs does not affect the availability of the underlying tokens on Binance Spot; users can still trade those tokens through other pairs that remain listed. For example, delisting a WBTC/ETH pair does not necessarily mean that WBTC or ETH itself is being delisted; they may each remain tradable against USDT, BTC, or fiat currencies. In these situations, the exchange is optimising its market structure by shutting down illiquid or redundant pairs, not signalling a lack of confidence in the asset itself.

By contrast, a full asset delisting shuts down all trading pairs and typically ends deposits and withdrawals for that token on the platform. When Finst decided to delist Wrapped Bitcoin (WBTC) and Lido staked Ether (stETH), it announced a firm cutoff time after which buying, selling, and swapping these assets would cease, and it also informed users that any remaining balances at that time would be liquidated on their behalf. That pattern resembles a traditional stock delisting more closely, because the asset is being removed from the platform altogether rather than just from one particular market.

Stablecoin support changes add a further nuance. Some institutions have launched formal processes to phase out support for particular stablecoins and automatically convert user balances into alternatives that better meet the firm’s regulatory or risk criteria. Anchorage Digital, for instance, published a “Stablecoin Safety Matrix” evaluating fiat‑backed stablecoins by the regulatory status of their issuers and announced a guided phase‑out of USDC, Agora USD (AUSD), and Usual USD (USD0), with a transition window for institutional clients to convert into stablecoins that meet specified benchmarks. Kraken, meanwhile, has adjusted its stablecoin offerings for clients in the European Economic Area in response to evolving regulatory pressures over euro‑area stablecoins. These moves are not always framed explicitly as “delistings,” but for end users the effect is similar: certain stablecoins become harder or impossible to use on specific platforms, while others are favoured.

Why Tokens Get Delisted

Behind every delisting is a decision that the continued listing of a token or trading pair no longer meets the exchange’s standards or commercial priorities. In practice, the reasons tend to fall into recurring categories: market quality, regulatory or legal pressure, project‑level risks, security and data integrity concerns, and broader strategic shifts by platforms. While exchanges sometimes publish detailed rationales, they often provide only high‑level explanations, leaving traders to infer the underlying drivers from context.

Low Liquidity, Low Volume, and Market Quality

Low liquidity and negligible trading volume are among the most routine reasons that crypto trading pairs and even entire tokens are delisted. Exchanges bear operational costs for maintaining order books and market‑making programmes, and illiquid pairs can be thinly traded, easy to manipulate, and unappealing to serious investors. Binance explicitly states that it removes certain spot trading pairs after periodic reviews that consider factors such as poor liquidity and low trading volume, in order to “maintain a high quality trading market.” When a pair consistently fails to attract enough orders, the venue may simply decide that the market is not worth keeping.

Educational resources from CoinMarketCap and others note that delisting often occurs when a project no longer meets an exchange’s listing standards, which can include liquidity thresholds and other performance metrics. As speculative interest cycles through narratives—DeFi summer, meme coins, AI tokens—many assets enjoy brief bursts of activity before fading into near‑zero volume. Exchanges, especially those serving a broad retail base, may list a wide tail of such tokens, but over time they prune back the least active markets. The steady stream of announcements delisting obscure USDT pairs on major venues illustrates this ongoing housekeeping, even when the underlying issuers remain operational.

For traders, low‑liquidity delistings are double‑edged. On one hand, they are a sign that the market has largely lost interest in the token, which may presage sustained underperformance. On the other, the lead‑up to delisting can produce intense volatility as holders rush to exit positions through narrow order books, creating sharp spikes and crashes that short‑term traders sometimes try to exploit. Having a realistic understanding of how difficult it will be to trade a token before and after delisting is therefore crucial, particularly when positions are large relative to market depth.

Regulatory and Legal Pressure

Regulatory and legal considerations are increasingly important drivers of delisting decisions, especially for assets that might be classified as securities or for stablecoins that must comply with emerging frameworks. Some exchanges have proactively restructured their offerings in particular jurisdictions rather than waiting for direct enforcement. Kraken’s decision to change its stablecoin offerings for clients in the European Economic Area is one notable example, reflecting the influence of European regulatory developments on which digital assets can be offered to retail users. Such moves can amount to a de facto delisting of certain assets for users in that region, even if the same stablecoins remain available elsewhere.

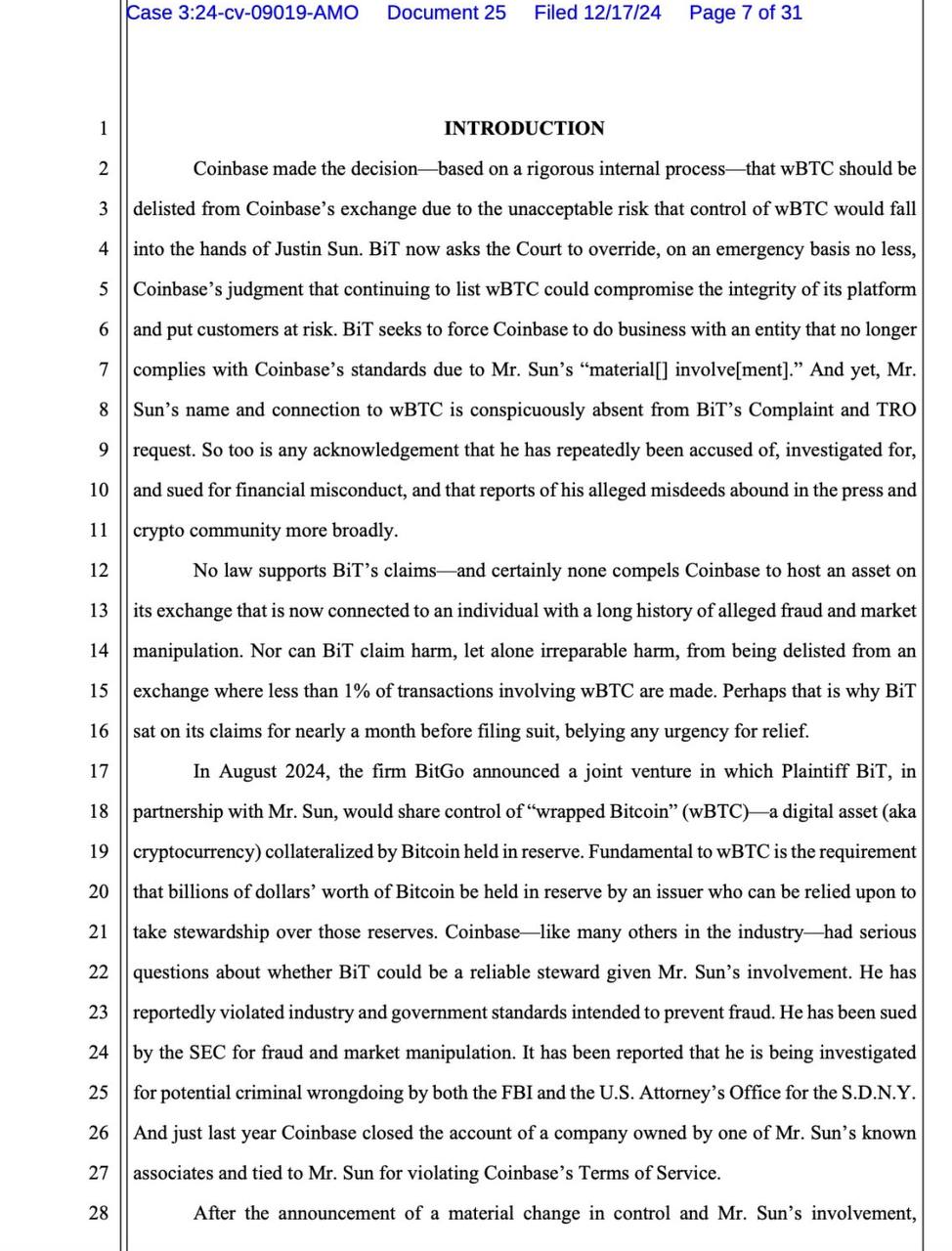

Legal disputes can also arise when issuers or large holders object to delistings. A high‑profile recent case involved BiT Global Digital Ltd., associated with Wrapped Bitcoin (WBTC), which sought a temporary restraining order in US federal court to prevent Coinbase from delisting WBTC from its platform. The judge denied the request, allowing Coinbase to proceed with delisting a token reportedly linked to billions of dollars in underlying Bitcoin value. This outcome underscores the wide discretion that exchanges typically retain in their terms of service to list or delist assets as they see fit, and it illustrates how delisting decisions can become flashpoints between exchanges, issuers, and large stakeholders.

Stablecoins are at the centre of another regulatory nexus. Anchorage Digital’s publication of a Stablecoin Safety Matrix and its parallel announcement of plans to phase out support for certain dollar‑pegged stablecoins demonstrate how institutional custodians are evaluating regulatory status, oversight, and operational robustness when deciding which stablecoins to support. In practice, such assessments may result in the gradual delisting or de‑emphasis of stablecoins seen as falling short of evolving regulatory or risk standards, even absent direct government pressure. As global frameworks such as the EU’s Markets in Crypto‑Assets Regulation (MiCA) are implemented, exchanges serving European users are likely to adjust their listings accordingly, leading to more regional delisting patterns.

Project Risk: Hacks, Abandonment, and Governance Failures

Exchanges also delist tokens when the underlying projects exhibit signs of severe distress, abandonment, or outright fraud. CoinMarketCap notes that assets may be delisted when they no longer meet an exchange’s listing standards, which can include criteria related to project team responsiveness, transparency, and ongoing development. If a project’s team disappears from public communication channels, fails to provide required disclosures, or is implicated in fraud or misconduct, exchanges will often remove the token to protect users from further harm and reputational risk.

Security breaches are another common trigger. News coverage has repeatedly shown that tokens associated with hacked or compromised smart contracts often find themselves under “trading caution” designations or delisting threats, especially when the exploit undermines confidence in the token’s supply or functionality. For example, when the security of a protocol like IoTeX (IOTX) is threatened by hacking incidents, exchanges and data platforms may flag the asset, restrict trading, or weigh delisting as they assess the risk to users. In on‑chain lending markets, the possibility that a collateral asset might be delisted from major venues can also raise fears of cascading liquidations and bad debt if liquidators cannot realise collateral at expected prices.

These dynamics were visible in the case of certain restaking tokens and synthetic assets whose potential delisting could have trapped positions on protocols like Aave or Spark. Even when a delisting is ultimately averted, the mere possibility can spark stress within communities and concentrate attention on the need for diversified collateral and robust risk parameters. From an exchange’s perspective, delisting tokens associated with exploited or abandoned projects is a defensive move to limit ongoing exposure; from investors’ standpoint, it is a reminder that listing on a major venue is not a permanent seal of approval.

Security and Data Integrity: Oracles, Indexes, and Metrics

Not all delistings are about the token’s intrinsic risk; some are about the integrity of the data used to measure and present trading activity. DeFiLlama’s decision to remove reported volume for Aster’s perpetual futures from its platform after uncovering suspicious trading patterns is a case in point. According to coverage, DeFiLlama observed that Aster’s reported perp volume closely mirrored Binance’s, raising questions about whether the volumes were genuine or manipulated, and chose to delist that volume data to preserve the credibility of its metrics. Here, the delisting is not of the asset itself but of a particular feed or representation of trading activity, aimed at defending data quality.

In a broader sense, oracles, indexes, and analytics platforms increasingly act as gatekeepers for which tokens and protocols are visible to investors. When a major data provider delists a token’s price feed or removes it from volume rankings due to concerns about wash trading or market manipulation, that can reduce interest and liquidity even if the token remains technically tradable. Stablecoin safety matrices, such as Anchorage Digital’s, play a similar role on the institutional side by categorising assets according to perceived risk and thereby influencing which tokens find support in custodial and trading platforms. In both cases, delisting becomes a tool for shaping the informational environment of the market.

Corporate Actions and Strategic Decisions

Finally, some delistings arise from corporate events or strategic shifts by either the issuing project or the exchange itself. In traditional markets, voluntary delistings can occur when a company chooses to go private, merge, or move to another exchange; shareholders may receive cash buyouts or shares in an acquiring entity. In crypto, comparable events include token migrations to new chains, protocol restructurings, and decisions by exchanges to focus on fewer, higher‑volume assets. When a token migrates, exchanges may delist the old contract and relist a new one, while providing users with conversion mechanisms; in other cases, they may simply delist tokens associated with outdated or redundant projects.

Exchanges also periodically refocus their listings to align with strategic priorities or regulatory realities. A venue might decide, for example, to reduce exposure to certain categories such as privacy coins or algorithmic stablecoins, leading to a wave of delistings even for tokens that remain actively developed. Similarly, the CFTC’s evolving framework for perpetual futures referencing different asset classes signals that derivatives venues must consider regulatory expectations when listing or maintaining certain products. In such cases, delisting is less about the immediate health of an individual token and more about the platform’s portfolio‑wide positioning.

Anchorage Digital’s Stablecoin Safety Report draws criticism for alleged inaccuracies and undisclosed Paxos ties, as Agora’s CEO accuses firm of “Pay to Play” tactics in delisting USDC and AUSD

- 01WBTC custody war↗

Coinbase's WBTC removal and the ensuing $1B Bit Global lawsuit forced readers to confront that the risk was Justin Sun's custodian control, not the token's mechanics — a trust-in-custody question disguised as a delisting story.

- 02MiCA stablecoin compliance purge↗

EU MiCA rules turned non-compliant stablecoin delistings from isolated exchange decisions into a coordinated, systemic event that reshaped stablecoin market share and DeFi liquidity across Europe.

- 03DeFi data integrity disputes↗

DefiLlama removing Aster over volume data concerns showed that on-chain analytics platforms now exercise listing power comparable to centralized exchanges, and that the community will litigate that power publicly.

- 04Pay-to-play safety rankings↗

Anchorage's stablecoin safety matrix drew accusations from Agora's CEO that safety scores double as paid delisting instruments, exposing commercial incentives behind institutional curation of which stablecoins survive.

- 05Wrapped Bitcoin alternatives post-delisting

Maker's WBTC collateral removal created immediate reader demand for trust-minimized wrapped BTC alternatives like dlcBTC, framing the delisting as a market opening rather than just a loss.

What Delisting Means for Traders and Projects

For traders, the immediate impact of a delisting is operational: markets disappear from their preferred platform, forcing decisions about whether and how to exit, transfer, or hold positions. For projects, the effects are reputational and economic, as delisting on a large venue can dramatically reduce liquidity and perceived legitimacy. Understanding these consequences is crucial for both individual portfolio management and project‑level strategy.

Ownership, Custody, and Access

One of the most important points—repeated in both equity and crypto contexts—is that delisting does not, by itself, erase ownership. Robbins LLP emphasises that shareholders still own their stock after a delisting, even though the shares may become far less valuable and harder to trade. Similarly, CoinSwitch notes that when a company’s shares are removed from the stock exchange, investors still technically hold their shares, but their ability to realise value is constrained. In crypto, because tokens exist on a public ledger rather than in a centralised registry, delisting on a particular exchange does not extinguish the tokens themselves; users can still hold them in self‑custody wallets and, if other venues support them, continue to trade them.

The catch is that access depends on timely action. Paybis and CoinMarketCap both stress that exchanges typically provide a limited timeframe during which investors can withdraw delisted tokens before the assets are no longer supported by that platform. Binance echoes this point, urging users to act quickly when a delisting is announced so that they do not lose the ability to recover tokens held in custodial accounts. If a user fails to withdraw before support ends, the exchange may freeze the asset in place or, in some cases, liquidate it on the user’s behalf, as Finst does with WBTC and stETH after its announced delisting deadline. Either outcome can effectively separate users from their assets, even if those assets continue to exist on‑chain.

The situation is different for derivatives and other synthetic exposures. When a perpetual contract is delisted, users do not own the underlying token directly; they hold a contractual exposure that must be settled according to the platform’s rules. Once final settlement occurs, their position disappears, replaced by a realised profit or loss in the margin asset. In lending protocols, borrowing and collateral positions may remain open even if a token is delisted on major centralized exchanges, increasing the risk that on‑chain liquidations will struggle to find sufficient buyers in secondary markets. In all these scenarios, timely awareness of delisting plans and their implications for different product types is essential.

Liquidity Shocks, Price Impact, and Slippage

Delisting announcements often trigger acute liquidity and price dynamics. Binance warns that delistings can carry several risks, including immediate volatility and the possibility that users who do not withdraw in time may lose access to their tokens on the platform. As markets anticipate the removal of a trading pair, spreads tend to widen and depth thins out, especially for smaller tokens. This environment can produce sharp, seemingly irrational price moves as traders rush to close positions, leading to both steep losses for late sellers and occasional outsized gains for those who can provide liquidity at opportune moments.

Over longer horizons, delisted assets frequently experience significant or even total devaluation. Robbins LLP notes that once a stock is delisted, its price often falls sharply, and in some cases stockholders can lose everything, particularly when the delisting is associated with bankruptcy or severe corporate distress. CoinSwitch likewise emphasises that delisted shares usually suffer diminished liquidity and value, and that options tied to delisted stocks can become worthless because the underlying security no longer trades on the primary venue. Analogous patterns are visible in crypto: tokens that lose listings on major exchanges often see their market capitalisation shrink as liquidity migrates to smaller, less reputable venues or to thin on‑chain pools.

These liquidity shocks are especially pronounced for trading pairs against dominant stablecoins like USDT. Because so much crypto liquidity is denominated in USDT pairs, the delisting of an illiquid token’s USDT market can effectively cut it off from the main arteries of the ecosystem. Even when the token remains listed in BTC or other pairs, the loss of the primary USDT market can significantly constrain dollar‑denominated trading. Interestingly, this can happen even when USDT itself is not under threat; the stablecoin remains widely supported, but exchanges remove USDT pairs for tokens that no longer justify the overhead of maintaining them.

Reading USDT Pair Delistings and Other Signals

USDT pair delistings are easy to misinterpret. Headlines announcing that a particular “XYZ/USDT” trading pair is being delisted may sound as if USDT itself is being de‑emphasised, when in fact the stablecoin remains central to the exchange’s market structure. Binance’s notice that the delisting of specific spot trading pairs does not affect the availability of the tokens on Binance Spot clarifies that most such moves are targeted rather than systemic. In many cases, the removal of a USDT pair simply reflects that the token’s USDT market has become too thin to warrant keeping it active, while more liquid pairs—perhaps against BTC or another stablecoin—remain available.

For traders, the key is to read beyond the headline. If the delisting announcement covers only one or two pairs for a given token and explicitly states that the token will remain tradable in other markets, the immediate impact is mostly about convenience and specific liquidity routes. However, if the notice indicates that all spot, margin, and derivatives markets for a token will be removed and deposits and withdrawals disabled, the situation is more serious: the token is being fully delisted from that platform. Patterns across exchanges also matter. When multiple major venues delist the same token within a short window, that is a stronger signal of structural issues than an isolated pair removal on one platform.

Reputational and Funding Impacts on Projects

For projects, delisting carries both practical and symbolic consequences. Practically, losing a listing on a large exchange like Binance or Coinbase means reduced liquidity, fewer market‑making relationships, and a smaller potential investor base. Symbolically, it can be perceived as a vote of no confidence from a key gatekeeper, even if the official rationale emphasizes neutral factors like liquidity thresholds or regulatory caution. Token teams may find it harder to raise capital, attract partners, or maintain community morale once delisting news spreads.

High‑profile cases like Coinbase’s delisting of WBTC illustrate this dynamic. WBTC represents a wrapped form of Bitcoin issued by a consortium, and the token is embedded in numerous DeFi protocols and trading strategies. When Coinbase decided to delist WBTC, BiT Global Digital Ltd. attempted to block the move but failed in court, highlighting both the importance of centralized exchange listings to wrapped assets and the limited recourse issuers have when platforms change direction. For WBTC holders, Coinbase’s decision altered a key liquidity venue; for the consortium, it underscored the risks of relying on a small number of centralized gateways for a token that represents billions of dollars of value.

Projects whose tokens are widely used as collateral on lending platforms or as components in yield strategies face additional complexities. A threatened delisting can force protocols to reassess risk parameters and potentially freeze or phase out collateral types to avoid bad debt if liquidity vanishes. When a restaking token used in protocols like Spark or Aave comes under delisting pressure, governance forums must weigh how quickly they can unwind positions without triggering cascading liquidations. In this sense, delisting decisions by centralized venues can propagate into on‑chain risk management, reinforcing the intertwined nature of centralized and decentralized markets.

Delisting in DeFi: Protocols, Front‑Ends, and Data

On decentralized exchanges and protocols, the concept of delisting is more subtle. Because anyone can deploy a token and create a liquidity pool on a permissionless DEX like Uniswap, there is no central listing committee to approve or remove assets. However, DeFi still experiences analogous processes when protocols, front‑ends, or data providers choose to stop supporting or displaying certain tokens or markets.

Why DeFi Cannot “Delist” in the Traditional Sense

In a pure smart contract context, there is no central authority that can erase an existing liquidity pool or prevent users from trading a token, as long as the contracts remain live and the chain continues to function. If a project is abandoned, its token can still be swapped in the corresponding DEX pool, although liquidity providers might withdraw and slippage may become extreme. This is fundamentally different from a centralized exchange, where delisting literally removes the order book and prevents any further trades on that venue.

However, most users interact with DeFi through front‑ends, aggregators, and wallets that curate which tokens and pools are prominently displayed. When these interfaces decide to hide or “delist” a token from their default views, effective access for mainstream users can decline dramatically, even though power users can still interact directly with the contracts. Additionally, governance processes can alter or remove incentives for providing liquidity, such as farming rewards, which can make pools economically unviable and thereby shrink liquidity over time. These kinds of decisions mirror centralized delisting in their impact, even if they are implemented through different mechanisms.

Lending Markets and Collateral Delistings

Lending protocols like Aave, Compound, and newer platforms such as Spark layer another dimension of delisting onto DeFi. When a token is accepted as collateral, borrowers can take leveraged positions against its value, and the protocol’s solvency depends on the ability to liquidate that collateral if prices fall. If a collateral token loses major centralized exchange listings or experiences severe on‑chain liquidity problems, the protocol may decide to “delist” it as collateral—that is, to prevent new borrowing against it and encourage or require existing positions to be unwound.

This dynamic came to the fore in the context of restaking derivatives and other complex assets that tie into Ethereum’s broader staking ecosystem. When one such token faced potential delisting and liquidity concerns, governance debates in protocols like Spark centred on the risk of liquidity lockup and potential bad debt if undercollateralized positions could not be liquidated at fair prices. Even when a full delisting was ultimately avoided, the episode highlighted how reliance on illiquid or structurally complex collateral can expose protocols to the knock‑on effects of centralized delisting decisions and shifts in market infrastructure.

From users’ perspective, collateral delisting can be as consequential as spot delisting. If a token is no longer accepted as collateral, borrowers may be forced to repay loans or add other collateral, while lenders might worry about the protocol’s exposure to illiquid assets. Yield farming strategies built on looping collateral and debt positions become harder or impossible to maintain. Thus, while DeFi cannot simply “turn off” a token’s existence, its governance choices about collateral eligibility and risk parameters can functionally delist assets from key roles in the on‑chain financial system.

Indexes, Explorers, and Data Platforms

Data and analytics platforms play a major gatekeeping role in DeFi visibility. DeFiLlama’s decision to delist Aster’s perpetual futures volume over data integrity concerns shows how information providers can shape perceptions of an asset’s activity. By observing that Aster’s reported volume appeared to mirror Binance’s in suspicious ways, DeFiLlama concluded that the data might not be reliable and opted to remove it, thereby preventing that volume from boosting Aster’s apparent market standing. Other platforms may follow similar policies when they detect wash trading, fake volume, or other anomalies.

Token explorers, portfolio trackers, and on‑chain analytics tools likewise choose which tokens to index and highlight. When they delist or de‑prioritize a token—perhaps due to spam filtering, security issues, or inactivity—the asset can become harder for users to monitor and value. Stablecoins that fall lower in institutional safety matrices may also receive less analytical attention and slower integration into new protocols, which in turn can reduce their practical utility relative to better‑rated competitors. In aggregate, these informational delistings can have effects comparable to the removal of a token from a centralized exchange, even though they technically only concern data.

Vaults, Structured Products, and Indirect Exposure

Yield vaults and structured products constitute another layer where delisting manifests indirectly. Strategies that allocate capital into centralized exchange markets or into on‑chain pools for specific tokens may have to suspend new deposits or unwind positions if underlying assets face severe liquidity or delisting risks. When a vault such as a Kronos QLS strategy is suspended from trading and flagged for eventual delisting, depositors are typically given a window to claim their shares or underlying assets before the strategy is fully terminated. For users, this can feel similar to an exchange delisting: a previously accessible product disappears, and the default behaviour may shift from growth to capital return.

Because many of these vaults provide leveraged or derivative‑like exposures, their delisting can propagate risk. If a vault holds a token that is being delisted from major exchanges, its ability to exit positions at fair prices may be impaired, potentially leading to losses that are passed on to depositors. Conversely, vault providers may pre‑emptively close strategies and return funds to avoid being trapped in illiquid assets. In both cases, the web of connections between CeFi, DeFi, and structured products amplifies the significance of delisting decisions beyond the narrow scope of a single order book.

Coinbase and BiT Global have settled their dispute over the delisting of wBTC, with BiT Global dismissing its lawsuit filed in the Northern District of California.

MiCA Title III stablecoin provisions enter force across EU

Sky (MakerDAO) governance votes to delist WBTC as collateral citing Justin Sun custodian risk

Coinbase delist WBTC; Bit Global files $1B lawsuit in Northern District of California

Binance and other EU CASPs begin phased delisting of USDT and non-MiCA stablecoins for EEA users

Anchorage Digital publishes stablecoin safety matrix; Agora CEO alleges pay-to-play delisting of USDC and AUSD

- 2025-04milestone

Coinbase and Bit Global settle WBTC delisting lawsuit; case dismissed in Northern District of California

Legal and Regulatory Dimensions of Delisting

Delisting is not just a market or technology event; it is deeply intertwined with legal frameworks and regulatory objectives. In traditional finance, delisting rules are codified in exchange regulations and overseen by securities regulators. In crypto, the landscape is more fragmented, but trends in enforcement and regulation are gradually shaping how exchanges list and delist assets.

Investor Protection in Stock Markets versus Crypto

In stock markets, delisting is explicitly framed as an investor protection tool. Robbins LLP describes delisting as a mechanism to shield investors from failing companies that no longer meet exchange standards, with exchanges sometimes giving companies time to cure deficiencies but ultimately removing them if milestones are not met. CoinSwitch similarly explains that when companies fall short of requirements related to minimum share price, market capitalisation, or financial reporting, they may be delisted, and that this process is considered an important event for both companies and investors. The NYSE and Nasdaq enforce detailed rules in this regard, including minimum price requirements and processes for regaining compliance.

For example, under recently approved rules, Nasdaq and the NYSE require listed companies to maintain a minimum share price of at least 1 USD, with typical compliance periods of around six months. If a stock trades below that threshold for an extended period and fails to recover, the exchange can accelerate the delisting process, narrowing the options available to struggling companies. Nasdaq’s announcement of its decision to delist the securities of Four Leaf Acquisition Corporation, after those securities had already been suspended from trading, illustrates how the process unfolds in practice: the exchange notifies the market and executes the delisting when conditions are not remedied.

In crypto, there is no single, comprehensive investor‑protection regime governing delisting across all exchanges. Instead, each exchange sets its own policies, often emphasizing the need to protect users and maintain “quality markets” but without the same degree of standardisation or regulatory oversight. Some tokens are listed or delisted with minimal transparency, and recourse for investors is generally limited to withdrawing assets or moving to other venues. Nevertheless, as regulators focus more closely on digital assets, especially where they resemble securities or derivatives, the gap between traditional and crypto delisting practices may narrow.

Litigation and Disputes over Delisting Decisions

Delisting decisions can provoke legal disputes, particularly when large sums are at stake or when issuers feel blindsided. The Coinbase–WBTC case is a notable example: BiT Global Digital Ltd. sought a temporary restraining order in a US federal court to prevent Coinbase from delisting wrapped Bitcoin (WBTC) from its platform, arguing that the move would harm users and markets linked to the token. The court denied the request, effectively confirming Coinbase’s contractual right to delist assets in accordance with its platform rules. Coinbase’s own market rules make clear that it can disable trading or cancel orders involving delisted assets, reinforcing the wide discretion exchanges retain.

Such cases highlight the asymmetry between exchanges and token issuers. While issuers and large stakeholders can object to delistings, they typically sign or implicitly accept terms of service that give exchanges broad authority over listings. Investors, too, have limited recourse; their main protections lie in being informed early and acting within withdrawal windows. In the absence of specific statutory protections around crypto listings, courts are often reluctant to second‑guess exchanges’ risk‑management and compliance decisions.

That said, as cryptoassets increasingly overlap with regulated financial products, including tokenized securities, the legal regime around delisting may evolve. The Securities Industry and Financial Markets Association (SIFMA) has been exploring investor protection in the context of tokenized securities, including issues around custody, regulation, and marketplace integrity, suggesting that future tokenized listings might inherit aspects of traditional delisting frameworks. Where crypto tokens are reclassified as securities or traded on regulated alternative trading systems, issuers and exchanges may face more formalised duties around delisting disclosures and processes.

EU Perspective and Stablecoin Rules

Europe’s regulatory trajectory illustrates how regional frameworks can shape delisting behaviour. Kraken’s adjustments to its stablecoin offerings for EEA clients reflect the pressures of aligning operations with evolving European rules governing digital assets and payment instruments. Under regimes such as MiCA, stablecoin issuers and service providers face requirements around reserves, governance, and authorisation, which in turn influence which assets exchanges are willing to support. If a stablecoin or token cannot satisfy those criteria, exchanges serving European customers may choose to delist it in that region rather than risk non‑compliance.

Anchorage Digital’s Stablecoin Safety Matrix, while not a regulatory document, is explicitly oriented around the regulatory status of stablecoin issuers and the robustness of their frameworks. By categorising stablecoins according to criteria that mirror regulatory expectations—such as transparency, oversight, and reserve management—Anchorage signals which stablecoins it views as safer from a regulatory and operational perspective. Its decision to phase out support for USDC, AUSD, and USD0, with a guided transition toward other stablecoins, shows how institutional players may drive de facto delisting of assets they see as falling short of these benchmarks, particularly when servicing regulated clients.

As other jurisdictions implement their own digital asset rules, including stablecoin‑specific regulations, regional patchworks of delisted and supported assets are likely to emerge. An asset might be delisted for European users but remain freely tradable in other regions, creating a heterogeneous landscape that traders must navigate carefully.

Tokenized Securities and Grey Zones

The emergence of tokenized securities and hybrid instruments further complicates the legal landscape of delisting. SIFMA’s discussions on tokenized securities emphasise investor protection, custody rules, and regulatory sandboxes as central topics, highlighting that tokenized forms of traditional assets still need to comply with securities law and exchange rules. If equities, bonds, or funds are tokenized and traded on digital platforms, their listing and delisting could fall under more familiar regulatory frameworks, including formal delisting procedures akin to those on the NYSE or Nasdaq.

At the same time, there is a grey zone of cryptoassets that are not clearly classified as securities but still raise regulatory concerns. For these, delisting often becomes a tool of risk management rather than a formal regulatory outcome. Exchanges might delist tokens they fear could later be deemed unregistered securities or that operate in regulatory no‑man’s‑land, pre‑empting enforcement actions. Over time, as more tokens are explicitly brought under securities or commodities frameworks—such as through CFTC oversight of certain perpetual futures or SEC guidance on tokenized instruments—delisting may increasingly be governed by statutory and rule‑based processes rather than purely contractual discretion.

How to Navigate a Delisting as a Crypto User

For individual traders and investors, knowing how to respond to a delisting announcement can make the difference between a controlled exit and a scramble through illiquid markets. While each situation is unique, there are recurring patterns and best practices reflected in exchange guidance and independent analyses.

Reading and Understanding Delisting Announcements

The first step is always to read the official announcement carefully. Binance advises users to consult the delisting calendar and pay close attention to deadlines for trading cessation and withdrawal support, noting that missing those deadlines can result in loss of access to funds on the platform. SDLCCorp similarly recommends that investors note key details such as the exact date and time of delisting, withdrawal deadlines, and any suggested alternatives to manage positions. Announcements from venues like Finst and Bybit show how specific these details can be, specifying times down to the minute and clarifying whether open orders will be cancelled and whether positions will be auto‑settled.

Understanding whether the delisting concerns a single trading pair, multiple pairs, or the entire asset is crucial. As Binance explains, removal of a particular spot trading pair does not necessarily affect the availability of the tokens on the exchange; only a full asset delisting terminates all markets and typically leads to the end of deposit and withdrawal support. For derivatives, announcements will often specify the methodology for final settlement, the index price to be used, and the treatment of funding payments near delisting time. Only by absorbing these details can a trader craft an appropriate response.

Deciding Whether to Sell, Transfer, or Hold

Once the parameters are clear, investors must decide whether to sell their tokens on the delisting exchange, transfer them to another platform or wallet, or hold them and ride out the uncertainties. Binance’s guidance acknowledges that some users will prefer to sell on the existing platform before trading is frozen, especially if they have lost confidence in the project or wish to avoid future complications. Others may opt to transfer tokens to another exchange that still lists them or to a self‑custody wallet if they believe in the asset’s long‑term potential and are prepared to manage liquidity risk.

SDLCCorp expands on this decision framework, urging users to check whether other exchanges still support the token, for example via aggregators such as CoinMarketCap, and to evaluate the project’s future viability. If the delisting stems from regulatory pressure or serious project issues, holding may be a high‑risk bet; if it is primarily due to low liquidity on a single venue, the token might still have life on alternative platforms. For stablecoins, investors should also consider the implications of institutional safety evaluations and regulatory trends highlighted by entities like Anchorage Digital, especially if they rely on those stablecoins for treasury management or on‑chain operations.

Operational Execution and Avoiding Forced Outcomes

After choosing a course of action, timely execution is paramount. Exchanges and advisors stress acting well before deadlines to avoid congestion, high on‑chain fees, or technical glitches that can occur when many users attempt to withdraw simultaneously. Ensuring that withdrawal addresses are compatible with the token’s network and that destination exchanges actually support the asset is critical; mis‑sent tokens may be unrecoverable. Binance specifically warns users to follow the platform’s instructions carefully when withdrawing delisted tokens to avoid sending funds to the wrong address or network.

Users should also be aware of the consequences of inaction. Finst’s policy of selling remaining delisted assets like WBTC and stETH on behalf of users after the deadline demonstrates that some platforms will enforce forced liquidation to prevent stranded balances. On derivatives venues such as Bybit, failure to close or adjust positions before delisting can lead to automatic settlement at a final price that may not align with a trader’s expectations. In margin and lending contexts, collateral or debt positions tied to a delisted asset can be subject to accelerated liquidations or parameter changes. Monitoring all these moving parts is demanding but necessary for anyone with complex exposure.

Portfolio Construction and Delisting Risk Management

Over the longer term, investors can reduce delisting‑related risks through thoughtful portfolio construction and monitoring. SDLCCorp advises against concentrating portfolios in tokens that are only listed on a single exchange or that exhibit clear signs of regulatory or project risk, recommending diversification into more stable assets with multiple exchange listings. Monitoring official announcements from both exchanges and token projects, as well as keeping wallets organised and funds spread across multiple, reputable venues and self‑custody solutions, can provide flexibility when delistings occur.

Choosing exchanges with transparent delisting policies and reliable communication channels also matters. Platforms that routinely explain the reasons for delistings, provide ample notice, and offer clear instructions for withdrawal or conversion are easier to navigate during stressful events. For larger portfolios, engaging advisors familiar with digital asset risk and tax implications can be helpful, particularly when delistings involve complex products, cross‑jurisdictional issues, or potential classification changes (for example, from utility token to security). In a maturing but still volatile market, delisting risk is an unavoidable reality; managing it is an integral part of professional‑grade crypto investing.

MiCA stablecoin provisions required EU exchanges to delist non-approved tokens like USDT by hard compliance deadlines, setting a template for jurisdiction-driven forced delistings that will expand to other regions.

Exchange delisting authority is unilateral and legally opaque — Coinbase removed WBTC with no advance remedy path, prompting a $1B lawsuit that underscored how unchecked centralized venue gatekeeping is.

Phased delistings of widely-held assets such as USDT across EU CASPs simultaneously compress on-chain liquidity pools, force asset migration at scale, and can reprice collateral positions across lending protocols.

Smaller-cap token delistings (SPELL, TRX on Binance US; IOTX under caution status) routinely cause sharp price dislocations as liquidity fragments across remaining venues with no guaranteed off-ramp.

- Counterparty / LegalMedium

Projects and custodians whose tokens are removed face asymmetric legal options — Bit Global's lawsuit against Coinbase ultimately settled, but the litigation risk deters smaller projects from challenging exchange decisions at all.

- Smart-contract / ProtocolLow

Protocol-level delistings (e.g., Spark's rsETH removal) are governance-triggered by on-chain liquidity or bad-debt risk rather than smart-contract exploits, but can still leave collateral locked during wind-down periods.

Outlook

Delisting has become a structural feature of crypto markets rather than an occasional anomaly. As the ecosystem has expanded to thousands of tokens and a proliferation of derivatives, yield strategies, and tokenized instruments, exchanges and protocols must constantly refine which assets they support and under what conditions. This process is driven by a mix of market quality considerations, regulatory pressures, project‑level developments, and strategic positioning by both centralized and decentralized platforms.

Going forward, several trends are likely to shape the delisting landscape. First, as regulation of digital assets deepens—particularly around stablecoins, tokenized securities, and derivatives—regional differences in listings and delistings will likely widen, requiring traders to pay closer attention to jurisdictional nuances. Second, the interplay between centralized delisting decisions and DeFi risk management will intensify, as protocols adjust collateral and exposure parameters in response to shifting liquidity conditions across venues. Third, data and analytics platforms will continue to act as informal gatekeepers, delisting questionable volume and highlighting safer assets, thereby influencing where attention and liquidity flow.

For Bitcoin and other blue‑chip assets, the main impact of these trends may be indirect, manifesting through changes in wrapped representations like WBTC or in the composition of derivatives and structured products. For long‑tail tokens, however, delisting will remain a central risk, capable of transforming a seemingly active market into a thin, fragmented, or effectively dead one overnight. For informed traders and builders, understanding delisting is not merely about avoiding unpleasant surprises; it is about reading the deeper signals of a market that is gradually, unevenly, but unmistakably maturing.

Latest Delisting news

DefiLlama's 0xngmi rebuts critiques on the delisting of AsterAnchorage Digital’s Stablecoin Safety Report draws criticism for alleged inaccuracies and undisclosed Paxos ties, as Agora’s CEO accuses firm of “Pay to Play” tactics in delisting USDC and AUSDCoinbase and BiT Global have settled their dispute over the delisting of wBTC, with BiT Global dismissing its lawsuit filed in the Northern District of California.Binance’s pivot to USDC is a calculated move, not panic, with USDC’s market share on the exchange jumping from 0.48% to 8.26% year-to-date, as upcoming EU regulations drive the delisting of USDT and fuel a $351B DeFi boom where compliance, liquidity, and stablecoin infrastructure are king. Coinbase legal responds to BiT Global’s attempt to block wBTC delisting, declares lawsuit baseless and seeks denial of TRO.Bit Global sues Coinbase for $1 billion over WBTC delisting

Coinbase legal responds to BiT Global’s attempt to block wBTC delisting, declares lawsuit baseless and seeks denial of TRO.Bit Global sues Coinbase for $1 billion over WBTC delistingSources

- https://paybis.com/blog/glossary/delisting/

- https://www.binance.com/en/support/announcement/list/161

- https://www.coinbase.com/legal/trading_rules

- https://robbinsllp.com/my-stock-was-delisted/

- https://coinswitch.co/switch/personal-finance/delisting-of-shares-and-stocks/

- https://support.kraken.com/articles/stablecoin-offerings-for-eea-clients

- https://finst.com/en/blog/articles/delist-wbtc-and-steth

- https://www.binance.com/en/square/post/17787587546521

- https://hselaw.com/news-and-information/legalcurrents/the-dust-has-settled-a-comparison-of-the-new-nasdaq-1-00-minimum-bid-price-and-nyse-1-00-minimum-price-rules/

- https://cryptorank.io/news/feed/51e1a-cango-nyse-delisting-notice-stock-price

- https://coinmarketcap.com/academy/glossary/delisting

- https://www.binance.com/en/square/post/22464359008538

- https://www.sifma.org/news/podcasts/tokenized-securities-the-case-for-investor-protection

- https://sdlccorp.com/post/how-to-handle-delisting-of-tokens-on-crypto-exchange-platforms/

- https://katten.com/perpetual-futures-come-onshore-the-cftcs-new-regulatory-framework

- https://www.anchorage.com/insights/anchorage-digital-publishes-stablecoin-safety-matrix-enables-auto-conversions-to-safe-stablecoins

- https://unchainedcrypto.com/defillama-delists-aster-perp-volume-over-data-integrity-concerns/

- https://ir.nasdaq.com/news-releases/news-release-details/delisting-securities-nasdaq-stock-market-5

- https://www.binance.com/en/support/announcement/detail/965d2d68914b4f95b57ac426ea9e497e

- https://announcements.bybit.com/en/article/delisting-of-skyaiusdt-perpetual-contract-blt428b3a5df12fc452/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…