Deep dive explainer on how earnings work across crypto exchanges, stablecoins, DeFi protocols and users, linking revenue, profit, macro cycles, security risks and prediction markets to the evolving digital asset economy.

+16 sources across the wider coverage universe

MiniMax and Zhipu secured CSRC approval for Hong Kong IPOs planned in early 2026, marking major moves for China’s AI sector. Meanwhile, U.S. AI stocks slid after Oracle’s earnings miss spooked investors.2025-12

MiniMax and Zhipu secured CSRC approval for Hong Kong IPOs planned in early 2026, marking major moves for China’s AI sector. Meanwhile, U.S. AI stocks slid after Oracle’s earnings miss spooked investors.2025-12 SoFi's Bank Q2 earnings report discloses $166M in cryptocurrency holdings, a significant increase from last quarter2023-08

SoFi's Bank Q2 earnings report discloses $166M in cryptocurrency holdings, a significant increase from last quarter2023-08 Trump's family secures the majority stake in World Liberty’s profits, claiming 75% of token sale earnings and $400M in fees, leaving just 5% of the $550M raised for development, according to Reuters estimates2025-03

Trump's family secures the majority stake in World Liberty’s profits, claiming 75% of token sale earnings and $400M in fees, leaving just 5% of the $550M raised for development, according to Reuters estimates2025-03 Coinbase reported Q1 2025 earnings with total revenue of $2.0 billion and EPS of $0.24, missing the consensus estimate of $1.98 by approximately 88%2025-05

Coinbase reported Q1 2025 earnings with total revenue of $2.0 billion and EPS of $0.24, missing the consensus estimate of $1.98 by approximately 88%2025-05 SoFi CEO Anthony Noto highlights crypto growth and future product plans during ‘Squawk Box’ as part of the company’s latest earnings breakdown.2025-04

SoFi CEO Anthony Noto highlights crypto growth and future product plans during ‘Squawk Box’ as part of the company’s latest earnings breakdown.2025-04- MakerDAO's revenue soars as crypto loans become the dominant profit generator for the protocol. "The bull market is driving users to seek leverage, resulting in increased earnings for Maker," says Phoenix Labs CEO, Sam MacPherson.2024-01

Earnings in Crypto: From Onchain Fees to Wall Street Seasons

In financial language, the word earnings usually describes the profit left after costs and taxes, while revenue is the gross inflow of money and income can refer to money earned either before or after expenses depending on context. In crypto, the same idea runs through everything from Coinbase’s quarterly results to a DeFi farmer’s yield: earnings are the portion of value that actually sticks, whether it sits on a corporate balance sheet, a protocol treasury, or in a user’s wallet.

Foundations: What “Earnings” Means in Finance and Crypto

Earnings, income and revenue in traditional finance

The starting point for understanding earnings in crypto is the way the term is used in traditional finance and accounting. In corporate reporting, revenue is the total amount of money a company receives from its core operations, such as trading fees for an exchange or payment processing charges for a fintech. It appears at the top of the income statement and is often called the top line because it is the first, gross measure of business activity before any costs are deducted. By contrast, income or net income is the money left over after all expenses, interest, depreciation, and taxes have been subtracted from revenue, which is why it is called the bottom line. In most corporate contexts, earnings and net income are used interchangeably to mean this final profit figure, although the word “earnings” is also reused in intermediate metrics such as earnings before interest and taxes (EBIT) or earnings before interest, taxes, depreciation and amortization (EBITDA).

For individuals, the language is fuzzier but the underlying logic is similar. Personal income typically refers to the total money received from wages, investments, and other sources, before taxes and living expenses, whereas earnings in a household context usually means what remains once taxes have been paid and mandatory deductions are taken out. Some tax guidance explicitly frames earnings as money left after the tax system has done its work, aligning it with the idea of disposable income. Public policy debates often center on this notion of “keeping more of what you earn,” as seen in recent discussions around U.S. tax rules and refund data showing larger average refunds, which effectively increase households’ post‑tax earnings and may free up capital for savings or speculative investments such as crypto. That framing, while political, underscores that earnings are about what is truly retained rather than what is merely received.

The importance of this distinction becomes clear when looking at how markets value companies. Investors are aware that a firm can grow revenue rapidly while still burning cash if costs run ahead of inflows, or it can post strong earnings even in a period of flat revenue if it manages expenses carefully. This is why earnings, not just revenue, are central to stock valuation, and why measures like earnings per share (EPS) are widely followed. EPS is simply net income divided by the number of shares outstanding, expressed as \( \text{EPS} = \frac{\text{Net income}}{\text{Shares outstanding}} \). Although the exact accounting details can be complex, the conceptual link is straightforward: earnings represent the economic surplus generated by a firm over a period, and EPS scales that surplus to the unit of ownership.

Berkshire Hathaway’s reporting illustrates how nuanced this can become. The conglomerate regularly highlights operating earnings as a better measure of performance than headline net income because the latter can swing dramatically with unrealized gains and losses on its equity portfolio. In one recent report, Berkshire disclosed more than 11 billion USD in operating earnings while simultaneously emphasizing the role of a very large cash pile and warning that tariffs could disrupt parts of its business. This underscores that even in traditional markets, “earnings” is not a single, simple concept but a family of related measures that analysts interpret in context. The same complexity is now migrating into crypto, where both centralized companies and decentralized protocols are learning to present their economic performance in ways investors can understand.

How crypto imported and reshaped the earnings concept

When crypto assets were young, much of the conversation revolved around price charts, hash rate, and onchain activity, rather than income statements. Bitcoin had no issuing company and no concept of corporate earnings; its “performance” was measured entirely by market price and network security. As tokenized businesses, centralized exchanges, and DeFi protocols emerged, they gradually imported the language of revenue and earnings from Wall Street but adapted it to a new environment where value flows can be visible directly onchain.

Centralized exchanges such as Coinbase sit at the most familiar end of this spectrum. Coinbase earns revenue from transaction fees on spot and derivatives trades, spreads on retail conversions, and growing streams from subscription and services lines such as custody, staking, and interest on customer balances. In its first‑quarter 2026 results, the company reported approximately 1.4 billion USD of total revenue but still posted a net loss near 394 million USD under GAAP, while at the same time highlighting more than 300 million USD in positive adjusted EBITDA as a measure of underlying profitability. This combination of metrics mirrors the toolkit used by high‑growth tech firms: investors look beyond headline net income to see whether the core business is generating cash, while discounting temporary charges or non‑cash accounting adjustments.

At the other end of the spectrum, decentralized finance protocols talk about protocol revenue, treasury income, and tokenholder earnings even though there is no corporate entity in the traditional sense. Protocols may charge transaction fees, interest spreads, or liquidation penalties and direct this revenue to a treasury governed by tokenholders, to liquidity providers, or to a burn mechanism that reduces token supply. In these cases, “earnings” often means the flow of value captured by tokenholders or contributors over time and measured through onchain data rather than audited financial statements. Although the terminology is still evolving, the fundamental intuition is the same as in corporate finance: earnings are what is left after paying the costs required to operate and secure the system.

This convergence of language means that a crypto news audience increasingly has to think in parallel about different layers of earnings: the results of public companies exposed to crypto markets, the revenue and profitability of private infra providers such as stablecoin issuers, the protocol‑level cash flows of DeFi systems, and the individual earnings of users from staking, yield strategies, or creator platforms. All of these interact with each other and with the broader macroeconomic environment, shaping both the price of tokens and the health of the ecosystem.

MiniMax and Zhipu secured CSRC approval for Hong Kong IPOs planned in early 2026, marking major moves for China’s AI sector. Meanwhile, U.S. AI stocks slid after Oracle’s earnings miss spooked investors.

"The planned listings would mark significant capital market entries for China’s artificial intelligence sector as the industry continues to attract investor attention amid global competition in AI development. Meanwhile, in the U.S., investors fled AI-related tech names on Thursday after Oracle posted an earnings miss, raising alarms about how quickly companies can monetize their AI investments."

Readers treat 'earnings' as a legitimacy test: when crypto entities — from TradFi banks disclosing crypto holdings to DeFi protocols reporting on-chain revenue — publish financial results, the click spike reveals an audience asking whether crypto has graduated from speculation to accountable, auditable income generation.↗

Listed Crypto Companies and the Earnings Cycle

Exchanges, brokers and miners: Coinbase, Schwab, DMG and Bullish

Quarterly earnings announcements for crypto‑exposed public companies have become key calendar events for the sector, analogous to how bank or semiconductor earnings shape sentiment in traditional markets. Coinbase is the most prominent example. Its Q1 2026 earnings release showed total revenue of about 1.4 billion USD, below Wall Street expectations of roughly 1.49 billion USD, leading to an initial sell‑off in the stock despite positive signals in other parts of the business. Transaction revenue came in around 756 million USD, also under consensus estimates, highlighting how sensitive the exchange’s top line remains to spot trading volumes and volatility. Yet the company also guided for flat adjusted operating expenses year over year and pointed to growing subscription and services revenue expected in the following quarter, suggesting a strategic pivot toward more stable income streams. The reaction underscored a basic earnings‑season dynamic: the market weighs not only absolute earnings but also how they compare to expectations and what they imply about the trajectory of future profitability.

Schwab offers another angle on this dynamic. Long known as a discount broker, it has reported strong earnings growth while simultaneously preparing to roll out a new spot crypto trading platform branded as Schwab Crypto, which will give retail clients direct access to bitcoin and ether trading through linked accounts custodied at Charles Schwab Premier Bank. The firm’s recent earnings surge of roughly 30 percent, as noted in contemporary coverage, is partly tied to its ability to monetize client balances and expand fee‑based services. By integrating spot crypto trading into its broader ecosystem, Schwab is positioning digital asset activity as another contributor to brokerage earnings, not an isolated speculative experiment. The result is that crypto markets are increasingly influenced by the earnings cycles of large, diversified financial institutions, not only pure‑play exchanges.

Mining and infrastructure companies add a further twist. DMG Blockchain Solutions, for instance, announces dates and conference call details for its quarterly earnings, emphasizing not only bitcoin production and hash rate but also power costs, hosting revenue, and hedging strategies. Although the specific figures vary from quarter to quarter, miners’ earnings are structurally leveraged to both bitcoin price and energy markets. High electricity costs or adverse difficulty adjustments can compress margins even in a rising price environment, while innovations in firmware, cooling, or energy procurement can boost earnings by lowering the cost base. This means that miner earnings season often functions as a barometer for the sustainability of network security under current economic conditions.

Institutional exchanges like Bullish, which operate order books and liquidity pools for professional clients, reflect yet another pattern. Recent fund flows show investors such as ARK Invest increasing their positions in Bullish shares even as the stock has occasionally traded lower, signalling a view that the exchange’s current valuation does not fully reflect its earnings potential once volumes normalize and more institutions adopt digital asset trading. Because these venues often have different fee structures and counterparty profiles compared to retail‑heavy platforms, their earnings may respond differently to market cycles, giving attentive investors additional signals about where institutional demand is heading.

Fintech and payments: Block, Circle and the “payments chains” thesis

Fintech conglomerates that straddle card payments, point‑of‑sale systems, and crypto services provide another critical lens on earnings in the digital asset era. Block, the parent of Square and Cash App, offers perhaps the most intricate case study. In its first quarter of 2026, Block reported net revenue of roughly 6.06 billion USD, up from about 5.77 billion USD in the prior year, yet swung to a net loss of around 308–309 million USD compared with a prior profit close to 190 million USD. The company’s gross profit, however, rose to about 2.91 billion USD, with strong contributions from both Cash App and Square, and adjusted diluted earnings of 0.85 USD per share beat analyst estimates by more than 25 percent.

The divergence between revenue growth, positive adjusted earnings, and a GAAP net loss was driven by factors such as restructuring charges, higher credit losses, and a roughly 172.8 million USD bitcoin remeasurement loss associated with revaluing its digital asset holdings. Bitcoin‑related revenue itself declined about 26 percent year over year, even as the company’s underlying transaction and software businesses performed strongly. This illustrates how crypto exposure can both augment and obscure a firm’s earnings profile. On the one hand, Bitcoin‑linked products can add revenue and attract users. On the other, accounting rules that require fair‑value adjustments for crypto holdings can inject significant volatility into reported earnings, even if the core cash‑generating business remains robust.

Circle, the issuer of USDC, has begun to surface its own earnings profile more explicitly as it matures. The company recently reported adjusted EBITDA of about 151 million USD in the first quarter of 2026, a 24 percent increase that reflects the profitability of its stablecoin and payments infrastructure business. At the same time, it disclosed that a presale of its ARC token raised approximately 222 million USD at a fully diluted network valuation of 3 billion USD, signalling investor confidence in its institutional blockchain strategy. Commentary such as the “Payments Chains” analysis has framed Circle, Stripe, and similar companies as building hyperscale infrastructure for payments in a manner analogous to how AWS reshaped computing, with Circle’s “first earnings season” marking a shift from pure growth story to visible cash generator. In Circle’s case, a significant portion of earnings is linked to the interest income earned on reserves backing USDC, as well as fees for APIs, treasury services, and onchain settlement, tying its profitability directly to both onchain activity and prevailing interest rates.

The table below summarizes, at a high level, how selected firms’ recent quarterly figures illustrate different relationships between revenue and earnings in a crypto context.

| Company | Recent quarter (2026) | Revenue (approx.) | Net result (GAAP) | Key crypto-related driver |

|---|---|---|---|---|

| Coinbase | Q1 2026 | 1.4B USD | Net loss ~394M USD | Trading fees, subscriptions, staking |

| Block | Q1 2026 | 6.06B USD | Net loss ~308–309M USD | Bitcoin trading revenue, bitcoin remeasurement |

| Circle | Q1 2026 | Not disclosed | Adjusted EBITDA 151M USD | USDC reserves income, payments infra |

| Schwab | Recent FY/quarter | Not specified | Earnings +30% vs prior period (coverage) | Upcoming spot bitcoin & ether trading |

This diversity reveals an important point for a crypto news audience: even when multiple firms operate in or around digital assets, their earnings can respond in very different ways to the same market conditions. Coinbase’s earnings are directly tied to trading volume and fee take rates; Block’s are influenced by Bitcoin prices through both transactional revenue and balance‑sheet revaluations; Circle’s depend on USDC circulation and interest rates; Schwab’s are shaped by a broad brokerage franchise into which crypto may be a relatively small but high‑growth component. Understanding these nuances is essential for interpreting earnings headlines.

Earnings expectations, prediction markets and volatility

Earnings do not exist in a vacuum; they are always measured against expectations and priced through market mechanisms. Traditionally, those expectations were dominated by Wall Street analysts and sell‑side research. In recent years, however, decentralized prediction markets have emerged as alternative aggregators of earnings forecasts. Platforms like Polymarket allow users to bet on whether companies will beat or miss EPS or revenue estimates, effectively crowdsourcing probabilities from traders willing to risk capital. An analysis of Polymarket’s earnings contracts found that when users collectively bet that companies were likely to miss earnings estimates, those firms actually did so at a rate of around 44 percent—more than double the historical baseline miss rate—suggesting that the prediction market’s odds contained actionable information beyond conventional analyst consensus.

This has drawn attention from quantitative hedge funds and other professional investors eager to incorporate market‑implied signals into their models. For the crypto ecosystem, it is particularly notable that these forecast venues are themselves crypto‑native, settling positions onchain and using stablecoins or other tokens for collateral and payouts. The phrase “The market is the analyst: Polymarket earnings eats Wall Street research” captures the idea that, at least around earnings events, aggregated onchain bets may rival or exceed the informational value of traditional research notes. For traders in crypto‑linked equities like Coinbase or Block, as well as in tokens whose prices are sensitive to these companies’ results, monitoring such markets can offer early hints about whether upcoming earnings calls will surprise to the upside or downside.

This interplay becomes even more visible when macro events cluster. Ahead of weeks packed with major earnings from mega‑cap technology companies, traders often re‑assess risk across both equities and digital assets. News that Bitcoin and XRP were climbing into a pivotal week characterized by expectations of a Federal Reserve rate cut, a steady Bank of Japan, and a series of “Magnificent Seven” tech earnings, alongside a highly anticipated Trump–Xi summit, illustrates how macro, geopolitics, and earnings narratives weave together to shape cross‑asset flows. In such environments, crypto markets may respond more to changes in risk appetite and liquidity triggered by big‑tech or bank earnings than to crypto‑specific headlines, underscoring the importance of following the broader earnings season.

Onchain Earnings: Protocol Revenue, Stablecoins and Payment Rails

Stablecoin issuers and USDC as an earnings engine

Stablecoins have quietly become one of the most important earnings engines in crypto. USDC, issued by Circle, is fully reserved and redeemable at par, but the reserves backing it—generally a mix of cash and short‑term U.S. government securities—generate interest income. Circle, not USDC holders, retains most of this interest, which can translate into substantial earnings when short‑term rates are elevated and the stablecoin’s circulating supply is large. The company’s reported adjusted EBITDA growth in early 2026 reflects this dynamic, as it monetizes both the float from USDC and fee‑based services for institutions building on its infrastructure.

This model is explicitly infrastructural rather than speculative. As commentators have observed, Circle and peers such as Stripe are building “payments chains” reminiscent of how cloud providers built the backbone of internet computing. In this analogy, USDC is not merely a token but a settlement layer for dollar payments across exchanges, DeFi protocols, and off‑chain businesses. The more volume that flows through USDC rails, the greater the potential earnings from transaction fees and reserve income. At the same time, because the reserves are mostly invested in highly rated, short‑duration securities, the issuer’s earnings are sensitive to central bank policy: higher policy rates increase the yield on reserves and thus boost earnings; rate cuts compress them.

This sensitivity creates an interesting alignment between macro and crypto. For example, when Fed officials signal an increased likelihood of rate cuts, as they did in recent speeches that contributed to shifting market odds toward an imminent reduction, the immediate market reaction might support risk assets like Bitcoin due to looser expected financial conditions. Yet those same cuts could, over time, reduce the interest income that stablecoin issuers earn on their reserves, potentially trimming a key source of their earnings. For a crypto news audience, this double‑edged effect is important: macro events that are bullish for token prices may be mildly negative for certain crypto businesses’ earnings, and vice versa.

DeFi, DEXs and protocol‑level earnings

In decentralized finance, earnings are not reported in glossy quarterly decks but accrued continuously onchain. Automated market makers, lending protocols, derivatives platforms, and liquid staking systems all charge some form of fee, whether on swaps, borrow interest, liquidations, or staking rewards. Protocol revenue is typically defined as the share of these fees that accrues to tokenholders or to a protocol treasury, whereas the portion paid to liquidity providers or market makers is considered an expense of running the system. In that sense, a DeFi protocol’s earnings can be conceptualized as the surplus left after compensating users who supply capital or perform work, analogous to a firm’s net income after paying wages and cost of goods sold.

What makes this different from corporate earnings is the transparency and immediacy. Because the flows are visible on the blockchain, analytics platforms can compute daily or even real‑time “earnings” figures for protocols, decomposing them by product line, user segment, or token pair. This has led to new valuation frameworks in which tokens are priced using multiples of protocol earnings, mirroring equity valuation techniques such as price‑to‑earnings (P/E) ratios but applied to onchain cash flows. It also means that protocol governance can adjust fee structures dynamically in response to competitive pressures or market cycles, for example by raising fees when demand is strong to boost earnings or lowering them to gain market share.

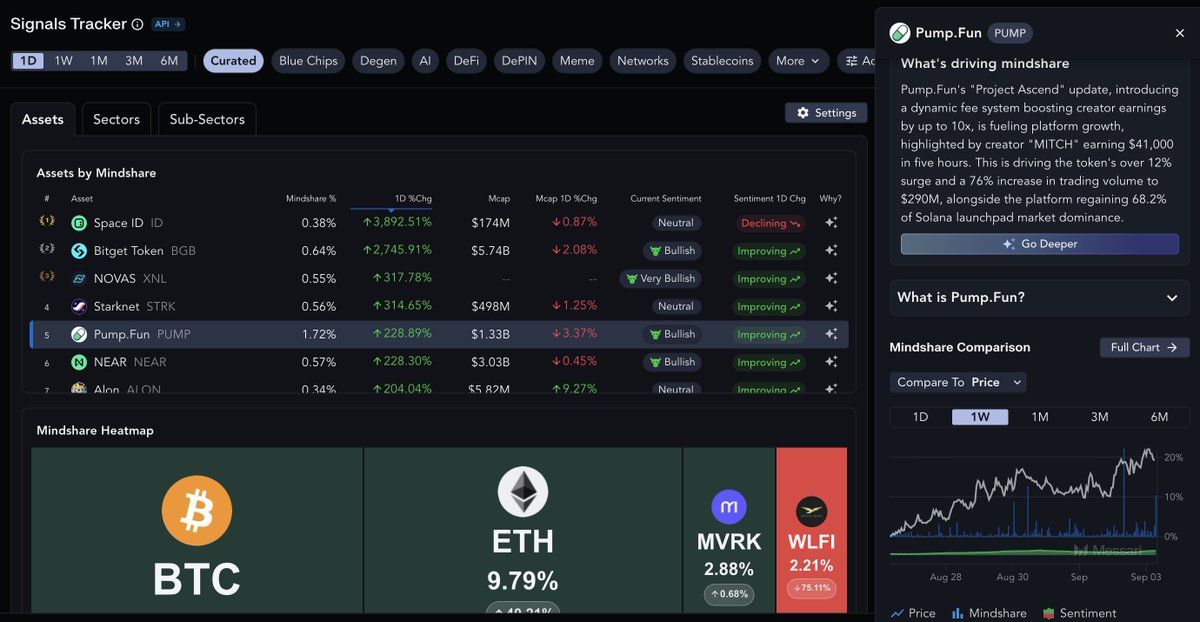

Project‑specific experiments highlight the creativity and risk of this space. Pump.fun’s “Project Ascend,” for instance, introduced a revenue‑sharing model that aimed to deliver up to ten times more creator earnings through dynamic fee structures, while also accelerating the processing of creator fees. By redesigning how fees are collected and distributed onchain, the project sought to align the incentives of platform operators and creators in a more granular way than traditional platforms typically allow. Similarly, the emergence of onchain contests where AI agents earn tokens such as BEAT for achieving specified outcomes illustrates how protocol‑level incentives can be directed not just at liquidity providers but at autonomous software that performs useful tasks. In these cases, “earnings” are being generated by non‑human agents whose actions are governed by code but whose rewards ultimately accrue to human developers and tokenholders.

Payment gateways and partner earnings: NOWPayments, Korbit and beyond

Payment gateways and exchanges that share revenue with partners and users represent a hybrid between centralized corporate earnings and onchain revenue distribution. NOWPayments, for example, positions itself as a global crypto payment gateway that enables businesses to accept and send payouts in various cryptocurrencies. It has promoted a zero‑fee, near‑instant payout infrastructure specifically designed to enhance partner earnings, emphasizing that merchants and affiliates can receive their share of transaction revenue in as little as one second. While the gateway itself earns via spreads, optional fees, or ancillary services, its messaging underscores that a significant portion of payment‑related earnings can be streamed directly to partners rather than accumulating solely at the corporate level.

Exchanges in different jurisdictions are experimenting with similar ideas. Campaigns promising users the ability to “unlock steady deposit fee payouts” exemplify a trend where platforms redistribute some portion of their earnings from deposit fees or lending spreads back to depositors as a quasi‑dividend. Although the details vary by platform and regulatory regime, the underlying logic is to treat user balances as not just passive capital but as co‑productive assets that deserve a share of the platform’s earnings. This mirrors traditional finance mechanisms such as mutual ownership structures or profit‑sharing arrangements but executes them via smart contracts and promotional campaigns.

Projects like Codatta push the concept further into the “agentic economy,” where identity verification, data contributions, and automated task execution are compensated with onchain earnings. In such models, users—or their AI agents—might perform actions such as verifying counterparties, supplying data, or interacting with protocols, and receive ongoing earnings streams in return. These schemes blur the lines between wages, dividends, and royalties, but they all hinge on the same core principle: earnings are the share of value that accrues to a given stakeholder after the costs of running a system have been met.

Ark Invest bought $10.2M worth of Bullish shares across three ETFs even as the stock fell 4.5%. The firm continues expanding its crypto exposure ahead of key earnings.

Good move from the team

- 01TradFi crypto balance-sheet disclosures

SoFi's $166M crypto holdings disclosure and CEO earnings commentary pulled the most clicks, signaling readers watch for when regulated banks treat crypto as a material, reportable asset class.

- 02Coinbase quarterly earnings scrutiny↗

Multiple Coinbase earnings cycles — Q1 2023, Q2 2024 on-chain NFT, Q2 2024 breach impact, Q1 2025 miss — generated sustained reader interest in the flagship public crypto company as a proxy for sector health.

- 03Insider profit extraction from token sales

The World Liberty story (Trump family claiming 75% of token sale earnings) revealed how protocol revenue can be captured by insiders before it reaches builders or the community, which readers found alarming.

- 04DeFi protocol revenue vs. speculation↗

MakerDAO's bull-market loan revenue, PumpFun's 2.58M SOL lifetime earnings, and Solana DApp fee dominance showed readers that on-chain protocols can generate real, measurable income — not just token price gains.

- 05Prediction markets beating analyst research↗

Polymarket's crowd-sourced earnings forecasts outperforming Wall Street models attracted readers interested in decentralized intelligence replacing traditional financial research.

- 06Macro earnings crossover into crypto↗

Berkshire, Apple, Amazon, and Fed-meeting weeks moving crypto markets showed readers that crypto prices are now meaningfully correlated with TradFi earnings cycles and macro policy.

How Crypto Users Earn: Trading, Yield, Work and Creation

Trading profits and speculative earnings

At the user level, the most visible form of crypto earnings remains trading profits. When a trader buys an asset like Bitcoin at one price and sells it later at a higher price, the difference constitutes earnings, albeit often highly volatile and subject to taxation as capital gains. The last few years have shown how tightly such earnings are intertwined with macro conditions. During periods when Bitcoin has been down more than 20 or 30 percent from recent peaks and the entire crypto market has shed nearly a third of its aggregate market capitalization, as reported in recent coverage, many traders see their paper gains evaporate and realized earnings turn negative. Conversely, sharp rallies driven by shifts in expectations for Fed rate cuts or changes in ETF flows can rapidly restore profitability for active market participants.

The growing influence of derivatives, leverage, and structured products complicates the picture. Many crypto traders now earn not only from directional moves but from basis trades, options strategies, or liquidity provision to perpetual swaps. These techniques can generate earnings even in sideways markets, but they also introduce counterparty and liquidation risks. For individuals, the distinction between revenue and earnings is crucial here: gross trading volume or notional exposure says little about actual earnings; what matters is the net result once fees, funding costs, and losses on losing trades are taken into account.

Staking, lending, and yield as earnings streams

Beyond trading, staking and lending yields constitute a large share of crypto users’ earnings. In proof‑of‑stake networks, validators and delegators earn rewards for securing the network, which can be understood as a combination of newly issued tokens and protocol fees redistributed to stakers. From an economic perspective, these are earnings allocated in proportion to capital contributed and risk borne. In DeFi lending protocols, lenders earn interest from borrowers, while liquidity providers earn fees and sometimes token incentives from supplying assets to pools. These yields are often advertised in annualized percentage yield (APY) terms, but the underlying earnings depend on utilization, market conditions, and smart contract risk.

Yield strategies can be structured to approximate more traditional financial products. For instance, some liquidity pools behave similarly to fixed‑income instruments, generating predictable cash flows from trading fees, while others introduce significant price risk. Stablecoin lending can feel analogous to money market fund investing, with earnings tied to short‑term borrowing rates in stablecoins. Yet all of these earnings remain subject to smart contract bugs, governance attacks, or regulatory changes, which can abruptly alter or wipe out expected cash flows. Hence, crypto earnings are often “high beta” relative to traditional fixed‑income yields.

Creator platforms, referral programs and AI agents

Creator‑centric and affiliate earnings models are gaining prominence in crypto. Platforms like Pump.fun that share a substantial portion of fee revenue with creators illustrate how token issuance, content creation, and social engagement can be combined into an earnings engine. When a new token or campaign is launched, fees from trading or minting can be split between the platform, the creator, and in some cases the broader community. With dynamic fee schedules and instant onchain distribution, creator earnings become transparent and programmable, potentially motivating higher quality contributions and longer‑term alignment.

Referral and partnership programs from payment gateways or exchanges similarly tie user behavior to earnings. If a gateway like NOWPayments shares fees with merchants and affiliates in near real time, participants can treat their referral networks or merchant customer base as productive assets that yield ongoing earnings streams. The difference from Web2 affiliate models is the composability and settlement infrastructure: payouts can be automated via smart contracts, denominated in multiple tokens, and integrated into broader DeFi strategies.

The rise of AI agents takes this logic into a new domain. In onchain contests where developers deploy autonomous agents that execute strategies, solve tasks, or interact with protocols, the agents’ performance directly translates into token earnings such as BEAT. These contests demonstrate a future where a meaningful share of onchain earnings comes not from human workload but from the deployment of algorithms that operate within specified constraints, with humans collecting the surplus. Projects like Codatta, which focus on identity verification and practical earnings in the agentic economy, suggest that verifying who or what is entitled to earnings will become a central challenge as machine agents take on a larger role.

Taxation and “keeping what you earn”

No discussion of earnings is complete without considering taxes. For individuals, the distinction between pre‑tax and post‑tax earnings is pivotal. Tax authorities generally treat crypto earnings—whether from trading, staking, or yield—as taxable income or capital gains, depending on jurisdiction and the nature of the activity. From the perspective of everyday investors, what matters is net earnings after satisfying these obligations. That is why debates about tax policy often revolve around how much of one’s earnings can actually be retained.

Recent U.S. data have highlighted that average tax refunds have increased, with the average refund in a recent filing season exceeding 3,400 USD and standing more than 10 percent higher than the prior year and almost 20 percent above the pre‑existing baseline. Government communications have framed this as evidence that Americans are “keeping more of what they earn,” linking it to policy choices including expansions of key credits and, historically, the effects of Trump‑era tax reforms. Regardless of one’s political view, the practical impact is that higher refunds and lower effective tax rates on certain income brackets can increase disposable earnings, potentially boosting household demand for savings, investment, and risk assets like crypto.

For companies, including crypto exchanges and fintechs, tax considerations influence after‑tax earnings and strategic decisions. Jurisdictional arbitrage, such as locating certain operations in lower‑tax regimes or designing token issuance structures with specific tax treatments, can materially affect reported net income. Thus, both at the individual and corporate level, the final step of the earnings journey is filtering gross inflows through the tax code to determine what truly remains.

Earnings, Macro and Market Sentiment

Earnings optimism, drawdowns and rebounds

Markets often move in anticipation of earnings as much as in response to realized results. Periods described as “market pauses after slump, then surges on earnings optimism” illustrate a familiar pattern: after significant drawdowns, investors seek evidence that corporate earnings remain healthy or are poised to recover, and when enough companies beat expectations or offer upbeat guidance, risk appetite returns. For crypto, which is highly sensitive to shifts in global risk sentiment, such episodes can catalyze sharp rallies even in the absence of crypto‑specific news.

Bitcoin’s behavior around shifts in Fed expectations is a case in point. When Federal Reserve officials hint at forthcoming rate cuts, as in recent remarks that led market odds for a cut in the near term to jump markedly, investors often infer a friendlier liquidity environment and bid up risk assets, including Bitcoin and large‑cap altcoins. At the same time, high‑frequency data such as ETF inflows and outflows show that institutional adoption can ebb and flow rapidly; recent periods have seen some of the worst monthly outflows on record from Bitcoin ETFs, with roughly 3.5 billion USD pulled over a few weeks even as spot prices attempted to stabilize. Earnings optimism in equities can sometimes counterbalance such crypto‑specific headwinds by improving overall risk tolerance, but the relationship is far from linear.

AI, big tech and spillovers into crypto

The rise of AI mega‑caps has added a new layer of complexity to the earnings landscape. Corporate events like Nvidia’s quarterly earnings are viewed as litmus tests for the sustainability of the AI boom, with analysts scrutinizing data center revenue, order backlogs, and capex plans by hyperscalers. When expectations are high, an earnings miss—such as the one reported by Oracle that recently spooked U.S. AI stocks—can trigger a broad de‑risking across tech, compressing valuations and dragging down correlated assets. This, in turn, can spill over into crypto, particularly for tokens associated with AI narratives or for crypto‑linked equities held in the same thematic portfolios.

At the same time, developments in AI elsewhere, such as MiniMax and Zhipu securing regulatory approval for Hong Kong IPOs in the AI sector, signal that capital markets are globalizing around these themes. As more AI firms list and report earnings in Asia, Europe, and North America, and as prediction markets list contracts tied to their results, cross‑regional flows may influence both AI equities and AI‑branded tokens. Crypto’s own “agentic economy,” where AI agents earn tokens onchain, further tightens the linkage between AI and digital asset earnings streams, even if the underlying cash flows remain modest relative to big‑tech giants.

Geopolitics, tariffs and the Trump–Xi factor

Geopolitical events can influence earnings both directly, through trade and regulation, and indirectly, through their impact on risk sentiment. Berkshire Hathaway’s warning that tariffs could disrupt various businesses while it sits on a record multi‑hundred‑billion‑dollar cash pile speaks to the way corporate leaders factor policy risk into capital allocation decisions. Companies with global supply chains or customer bases may see earnings compressed by tariffs, sanctions, or currency volatility, and those concerns often show up in earnings guidance.

For crypto, which is not bound by traditional borders but is heavily influenced by regulatory regimes and macro policy, summits such as a Trump–Xi meeting carry symbolic weight. Market narratives often frame such events as potential catalysts for shifts in trade policy, financial regulation, or geopolitical stability. When such meetings occur alongside major central bank decisions and mega‑cap earnings releases, as occurred in a recent “pivotal week” where Bitcoin and XRP climbed in anticipation of a possible Fed rate cut, investors must parse multiple overlapping signals. In such weeks, the phrase “earnings” refers simultaneously to corporate profits that justify valuations, to traders’ realized gains or losses, and to the broader economic earnings power of entire regions shaped by policy choices.

Bitcoin and XRP climb ahead of a pivotal week as markets brace for a Fed rate cut, steady BOJ policy, Mag 7 earnings, and the highly anticipated Trump–Xi summit.

Maybe it's not yet over 😕😕

- 2019-08launch

Curve StableSwap AMM launched by Michael Egorov

- 2023-05milestone

Coinbase Q1 2023 earnings report released

- 2024-08milestone

Coinbase Q2 2024 earnings published on-chain as $COIN NFT

Coinbase Q2 2024 earnings absorb $307M hit from data breach

Berkshire Hathaway Q2 operating earnings fall 4% amid tariff warnings

- 2025-05milestone

Coinbase Q1 2025 earnings: $2.0B revenue, EPS misses consensus

- 2025-07regulatory

SoFi Q2 earnings disclose $166M in cryptocurrency holdings

Polymarket earnings forecasts cited by Bloomberg as edge over Wall Street analysts

Accounting, Security and One-Off Shocks to Earnings

Crypto accounting: remeasurement, impairment and volatility

The treatment of crypto assets under accounting standards has direct implications for reported earnings. Under many regimes, companies holding crypto on their balance sheets must remeasure those holdings at fair value each reporting period, recognizing gains or losses through the income statement. Block’s roughly 172.8 million USD bitcoin remeasurement loss in Q1 2026 is a concrete example of how such rules can convert price volatility into earnings volatility, even when operational performance is strong. If Bitcoin prices rebound in subsequent quarters, the same holdings may contribute to gains, but the net effect is that earnings become more sensitive to market swings.

Other crypto exposures, such as tokenized equity or DeFi positions, can introduce even more complexity. Companies may have to decide whether to treat these positions as financial instruments, intangible assets, or inventory, each with different implications for earnings recognition. For investors evaluating earnings, it becomes important to distinguish between core operating results and fair‑value adjustments on crypto holdings. Adjusted metrics that exclude such remeasurement effects, like adjusted EPS or EBITDA, are attempts to provide a clearer view of underlying earnings power, though they also open the door to subjective judgment.

Security breaches, outages and their financial impact: the Coinbase case

Security incidents and operational outages can impose significant, sometimes irregular, costs that weigh on earnings. Coinbase’s recent experience with a major data breach illustrates this vividly. Cybercriminals bribed a small group of overseas customer support agents to exfiltrate data from internal tools, affecting less than 1 percent of the company’s monthly transacting users but creating material risk of targeted social engineering attacks. The attackers then attempted to extort Coinbase for 20 million USD in exchange for not disclosing the breach and for ceasing their activities, an offer the company refused. Instead, Coinbase launched an investigation, reinforced its controls, notified affected customers, and committed to reimbursing retail users who were tricked into sending funds to the attackers as a result of the incident.

In addition to reimbursing users, Coinbase chose to establish a 20 million USD reward fund for information leading to the arrest and conviction of the attackers, while also introducing additional safeguards such as extra identity checks on large withdrawals and more prominent scam‑awareness prompts. The company disclosed that the same period also included significant service disruptions due to an AWS outage that caused over three hours of degraded performance, further affecting user experience. Subsequent earnings reports indicated that the combined impact of the breach, associated reimbursements, and remediation efforts produced a hit of more than 300 million USD to quarterly results, contributing to both lower net income and reduced investor confidence.

From an earnings analysis perspective, the key issue is how to classify these costs. Many investors and analysts treat them as one‑off, non‑recurring items—akin to restructuring charges or legal settlements—arguing that they should not heavily influence assessments of ongoing earnings power. However, repeated or severe incidents can change this calculus, leading markets to demand a higher risk premium and to discount future earnings more heavily. For crypto firms, whose core value proposition hinges on security and trust, the reputational damage from such events may linger beyond the quarter in which the earnings hit is recognized.

Regulatory, legal and restructuring charges

Legal and regulatory risks are another recurring source of earnings volatility for crypto‑exposed firms. Block’s swing to a net loss in Q1 2026, despite strong revenue growth and rising gross profit, was partly attributed to restructuring charges and accruals related to investigations, including inquiries from the U.S. Department of Justice. These accruals, while non‑cash in the short term, represent expected future outflows that reduce reported earnings today. Similarly, exchanges and fintechs facing enforcement actions, settlements, or compliance overhauls must often book provisions that weigh on net income.

Restructuring costs also arise from strategic shifts such as layoffs or business line exits. Coinbase’s announcement of a 14 percent workforce reduction, cutting around 700 staff as it pivoted toward AI and efficiency, is expected to generate restructuring expenses in the range of 50–60 million USD in the short term. While such moves are framed as efforts to improve long‑term earnings by lowering the cost base, they can depress near‑term net income and complicate quarter‑to‑quarter comparisons. Investors must therefore parse earnings reports with an eye toward separating recurring operating items from non‑recurring charges, while also evaluating whether the latter signal deeper structural issues.

Case Studies: Earnings Across the Crypto Landscape

Coinbase: revenue mix, security shocks and strategic pivots

Coinbase sits at the intersection of many of the themes discussed above. Its Q1 2026 earnings underscored the sensitivity of its revenue to trading volumes, with total revenue of 1.4 billion USD and transaction revenue of 756 million USD falling short of analyst expectations. Yet the company also highlighted growth in subscription and services revenue, including custody fees, staking income, and interest on customer balances, and guided for this segment to reach 565–645 million USD in the second quarter. This diversification reflects a strategic effort to reduce dependence on volatile spot trading fees and to build more predictable earnings streams.

The subsequent data breach and extortion attempt, together with the AWS outage, tested this strategy by introducing significant one‑off costs and reputational challenges. Coinbase’s decision to reimburse affected customers voluntarily and to create a substantial bounty for information on the attackers signalled a commitment to protecting user earnings even at the expense of short‑term corporate earnings. At the same time, the company’s workforce reductions and investment in AI tools for support and risk management were framed as measures to improve efficiency and build resilience, with the aim of strengthening future earnings despite near‑term restructuring expenses. For investors, Coinbase’s earnings trajectory now reflects a complex interplay between core trading activity, high‑margin services, security and operational risks, regulatory developments, and strategic bets on new technologies.

Circle and USDC: from growth story to earnings engine

Circle’s evolution from a venture‑backed fintech to a profitable infrastructure provider illustrates how stablecoin businesses transform over time. In its initial years, Circle’s value was tied more to USDC’s growth in circulation and ecosystem adoption than to visible profitability. As interest rates rose and USDC became deeply embedded in both centralized exchanges and DeFi protocols, the interest income on reserves and fee‑based revenues from APIs and institutional services began to generate substantial earnings. The company’s reported adjusted EBITDA of 151 million USD in Q1 2026 represents the crystallization of that model, while the successful ARC token presale underscores investor appetite for exposure to its expanding institutional blockchain network.

At the same time, Circle’s earnings profile remains sensitive to macro variables such as rates and to competition from other stablecoins, some of which may share more of the underlying earnings with users. The “payments chains” thesis suggests that as more commerce and financial flows move onto tokenized rails, infrastructure providers like Circle could capture a disproportionate share of the resulting earnings through economies of scale and network effects. However, this also puts them under increasing regulatory scrutiny, which may affect capital requirements, reserve composition, and, by extension, earnings volatility.

Block: marrying fintech growth with crypto exposure

Block’s case study highlights both the promise and pitfalls of combining high‑growth fintech businesses with crypto offerings. Its Square merchant services and Cash App consumer ecosystem have continued to produce robust gross profit growth, with overall gross profit reaching about 2.91 billion USD and Cash App’s segment delivering particularly strong gains. Yet the company’s net loss in Q1 2026, driven by restructuring charges, credit losses, and bitcoin remeasurement, reminds investors that earnings are not a simple function of top‑line growth.

Bitcoin revenue, which declined 26 percent year over year, remains a relatively low‑margin business for Block because the company treats the bulk of the gross inflows from Bitcoin sales to customers as pass‑through revenue, recognizing only a thin spread as gross profit. This accounting approach inflates revenue figures while leaving earnings more dependent on core fintech operations and on fair‑value adjustments to Bitcoin holdings than a cursory reading of the top line might suggest. For a crypto‑savvy audience, the lesson is clear: headline revenue contributions from crypto may not translate into commensurate earnings unless the business model captures significant spreads or fee income.

Schwab: integrating spot crypto into a profitable brokerage

Schwab’s decision to launch spot crypto trading under the Schwab Crypto brand appears against the backdrop of a highly profitable core brokerage business whose earnings recently surged by around 30 percent. Rather than betting the franchise on crypto, Schwab is integrating bitcoin and ether trading as additional asset classes available to retail clients through a separate, but linked, account structure. Charles Schwab Premier Bank will serve as the custodian for clients’ digital assets, responsible for safekeeping and record‑keeping, aligning the product with existing regulatory and operational frameworks.

This approach suggests that Schwab views crypto more as an incremental earnings opportunity than as a transformational gamble. Trading fees, payment for order flow or spreads, and cross‑selling of other services can all augment earnings, but the company’s overall profitability will remain anchored in its broader suite of investment products and cash management offerings. For crypto markets, the more interesting implication is that as large brokers and banks integrate spot crypto into their platforms, the earnings cycles of these diversified institutions will increasingly influence the availability and cost of crypto services for retail investors.

Berkshire: illustrating operating earnings and cash as strategic optionality

Although Berkshire Hathaway has no direct crypto operations, its reporting on operating earnings and cash reserves offers a useful counterpoint for understanding earnings quality. The company’s disclosure of roughly 11.35 billion USD in operating earnings and a record cash pile, followed by later reports of operating earnings around 11.16 billion USD alongside warnings about tariff risks and a cash war chest exceeding 300 billion USD, illustrates a deliberate focus on earnings that come from ongoing operations rather than volatile investment gains. Warren Buffett’s emphasis on operating earnings as the right metric for evaluating business performance, and his willingness to let cash accumulate when valuations are unattractive, exemplify a conservative approach to capital allocation.

For crypto participants, the lesson is not that Berkshire’s model should be copied wholesale but that distinguishing between recurring, high‑quality earnings and highly variable mark‑to‑market gains is crucial. Just as Berkshire investors discount unrealized equity gains and focus on the earnings power of subsidiaries, crypto investors may need to look past short‑term token price movements and ask whether exchanges, protocols, and stablecoin issuers are generating durable earnings streams that justify their valuations.

- Smart-contract / protocolMedium

DeFi protocols like MakerDAO and AMM LP strategies generate real revenue, but earnings are fully exposed to smart-contract exploits that can wipe accrued yield instantly.

- CentralizationHigh

The World Liberty structure — where Trump family entities claimed 75% of token sale earnings and $400M in fees, leaving 5% for development — exemplifies how protocol earnings can be legally but asymmetrically extracted by controlling parties.

- RegulatoryMedium

Brazil's pending 15% tax on offshore crypto earnings, and evolving IRS treatment of staking and DeFi yield, signal that jurisdictions are moving to tax on-chain income more like ordinary earnings.

Coinbase Q2 2024 earnings absorbed a $307M breach-related hit while spot trading volumes fell, illustrating that crypto-native company earnings are highly sensitive to both market sentiment and one-time operational shocks.

- Liquidity / rate sensitivityMedium

Robinhood, Revolut, and Monzo face earnings compression as lower interest rates erode the net interest income that has underpinned neobank profitability, a structural risk shared by any yield-dependent crypto product.

Coinbase's Q2 2024 breach — where offshore staff were bribed to expose customer data — shows that even exchange-reported earnings can be materially impaired by insider counterparty failure, not just market moves.

Conclusion

Across both traditional finance and the crypto ecosystem, earnings serve as the primary measure of economic surplus. For public companies like Coinbase, Block, Circle‑backed entities, Schwab, and crypto‑adjacent conglomerates such as Berkshire, earnings distill the complex interplay of revenue, costs, accounting choices, macro conditions, and one‑off events into a single bottom‑line figure that markets use to allocate capital. In crypto, this framework has been extended to decentralized protocols, stablecoin issuers, payment gateways, and even AI agents onchain, all of which now speak, implicitly or explicitly, in the language of earnings and profitability.

The details, however, differ markedly across contexts. Corporate earnings can be buffeted by bitcoin remeasurement losses, security breaches, restructuring charges, or shifts in interest rates, as seen in the experiences of Block and Coinbase. Protocol‑level earnings are transparent and continuous but exposed to smart contract risk, governance decisions, and competitive fee wars, as with DeFi platforms and creator‑focused projects like Pump.fun. User‑level earnings—from trading, staking, yield, referrals, or creator economies—are often high‑beta and must be evaluated net of fees and taxes, in light of broader policy developments such as changes in tax credits or Trump‑era tax reforms that alter how much of one’s earnings can be retained.

At the same time, prediction markets and onchain data are reshaping how expectations about earnings are formed and priced. Platforms like Polymarket show that market‑implied probabilities of earnings beats or misses can sometimes out‑predict traditional analysts, offering crypto‑native traders a new set of tools to navigate earnings season. Macro events, from Fed rate decisions to AI mega‑cap earnings and Trump–Xi summits, increasingly influence both corporate and crypto earnings, underscoring the need for holistic analysis rather than siloed thinking.

For a crypto news audience, the practical takeaway is that following “earnings” now means tracking multiple layers of economic performance: corporate earnings of listed and private firms, onchain earnings of protocols and stablecoins, and personal earnings opportunities and risks in trading, yield, and creation. The more these layers are understood in relation to each other, the better positioned investors, builders and users will be to interpret headlines, assess sustainability, and navigate the next phase of digital asset growth.

Outlook

Looking forward, earnings in crypto are likely to become more transparent, more programmable, and more intertwined with traditional finance. Stablecoin issuers and payments infrastructure providers are on a trajectory toward becoming the “AWS of money,” with earnings driven by onchain settlement volume and interest rates. Exchanges and brokers, from Coinbase to Schwab, will continue to diversify their earnings away from pure transaction fees toward subscriptions, custody, and structured products, even as they grapple with security, regulatory, and macro risks. DeFi protocols will refine their fee and revenue‑sharing models, experimenting with ways to align tokenholder earnings with sustainable usage rather than short‑term incentives.

Macro forces will remain decisive. Shifts in Fed policy will alter both the discount rate applied to future earnings and the interest income of stablecoin issuers, while AI‑driven productivity gains and sector rotations around big‑tech earnings will shape risk appetite in crypto and beyond. Geopolitical developments, including trade policy and high‑level summits, will continue to influence the earnings power of global firms and the regulatory climate for digital assets. In this environment, understanding earnings—not just prices—will be essential for anyone seeking to navigate the evolving intersection of crypto, onchain infrastructure, and the broader financial system.

Latest Earnings news

MiniMax and Zhipu secured CSRC approval for Hong Kong IPOs planned in early 2026, marking major moves for China’s AI sector. Meanwhile, U.S. AI stocks slid after Oracle’s earnings miss spooked investors.Ark Invest bought $10.2M worth of Bullish shares across three ETFs even as the stock fell 4.5%. The firm continues expanding its crypto exposure ahead of key earnings.Bitcoin and XRP climb ahead of a pivotal week as markets brace for a Fed rate cut, steady BOJ policy, Mag 7 earnings, and the highly anticipated Trump–Xi summit. The market is the analyst: Polymarket earnings eats Wall Street research.

The market is the analyst: Polymarket earnings eats Wall Street research. PumpFun’s “Project Ascend” sent mindshare soaring 228%—because nothing says innovation like charging creators differently.

PumpFun’s “Project Ascend” sent mindshare soaring 228%—because nothing says innovation like charging creators differently. Nvidia earnings report set to test Wall Street’s faith in AI boom on Wednesday

Nvidia earnings report set to test Wall Street’s faith in AI boom on WednesdaySources

- https://www.investopedia.com/ask/answers/070615/what-difference-between-earnings-and-income.asp

- https://corporatefinanceinstitute.com/resources/accounting/income-vs-revenue-vs-earnings/

- https://www.youtube.com/watch?v=d7BeHWXcLYE

- https://www.youtube.com/watch?v=hKUG2P_Eqjc

- https://www.coinbase.com/blog/protecting-our-customers-standing-up-to-extortionists

- https://www.circle.com/pressroom/circle-reports-first-quarter-2026-results

- https://www.stocktitan.net/sec-filings/XYZ/10-q-block-inc-quarterly-earnings-report-e5533e74dbf0.html

- https://pressroom.aboutschwab.com/press-releases/press-release/2026/Charles-Schwab-Announces-Details-of-Spot-Crypto-Trading-Launch/default.aspx

- https://www.facebook.com/cnn/posts/berkshire-hathaway-on-saturday-reported-1135-billion-in-operating-earnings-and-a/1347394440586537/

- https://www.investing.com/news/cryptocurrency-news/nowpayments-redefines-crypto-payouts-zerofee-1second-infrastructure-built-for-partner-earnings-4719837

- https://financefeeds.com/block-inc-jumps-8-after-strong-q1-earnings/

- https://polymarket.com/predictions/earnings

- https://www.whitehouse.gov/releases/2026/04/this-tax-day-americans-are-keeping-more-of-what-they-earn/

- https://www.bloomberg.com/news/articles/2026-04-16/wall-street-quants-see-an-edge-in-polymarket-earnings-forecasts

- https://www.fintechbrainfood.com/p/payments-chains

- https://cryptorank.io/news/feed/805f0-pump-fun-project-ascend-unveiled-heres-who-will-get-major-rewards

- https://www.youtube.com/watch?v=1vw0G9du1Lc

- https://www.facebook.com/Benzinga/posts/on-tuesday-cathie-wood-led-ark-invest-made-significant-moves-by-acquiring-shares/1473534891438843/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…