Comprehensive explainer on Ether.Fi, covering its liquid restaking tokens, DeFi vaults, OP Mainnet neobank stack, Plume RWA partnership, ETHGas validator deal, card program, and the risks and opportunities of onchain yield.

+8 sources across the wider coverage universe

OP Mainnet logs largest TVL surge in history as Etherfi migrates $200M, bringing 70K cards and 300K users to Optimism to scale real-world crypto payments2026-04

OP Mainnet logs largest TVL surge in history as Etherfi migrates $200M, bringing 70K cards and 300K users to Optimism to scale real-world crypto payments2026-04 Ether.fi commits $3B in ETH to ETHGas in exclusive three-year preconfirmation deal2026-04

Ether.fi commits $3B in ETH to ETHGas in exclusive three-year preconfirmation deal2026-04 Fluid rolls out $1B-cap aWETH Redemption Protocol with Lido Finance, EtherFi, and 1inch to reduce systemic DeFi risk and unlock trapped ETH liquidity on Aave2026-04

Fluid rolls out $1B-cap aWETH Redemption Protocol with Lido Finance, EtherFi, and 1inch to reduce systemic DeFi risk and unlock trapped ETH liquidity on Aave2026-04 Ether.fi re-enables weETH bridging via LayerZero across all chains with liquid minting and redemption, boosting security by increasing DVNs to four and tightening rate limits2026-04

Ether.fi re-enables weETH bridging via LayerZero across all chains with liquid minting and redemption, boosting security by increasing DVNs to four and tightening rate limits2026-04 Aave alongside EtherFi, KelpDAO, and Compound propose unlocking ETH frozen by Arbitrum Security Council, aiming to channel funds into DeFi United to restore rsETH backing after April exploit2026-04

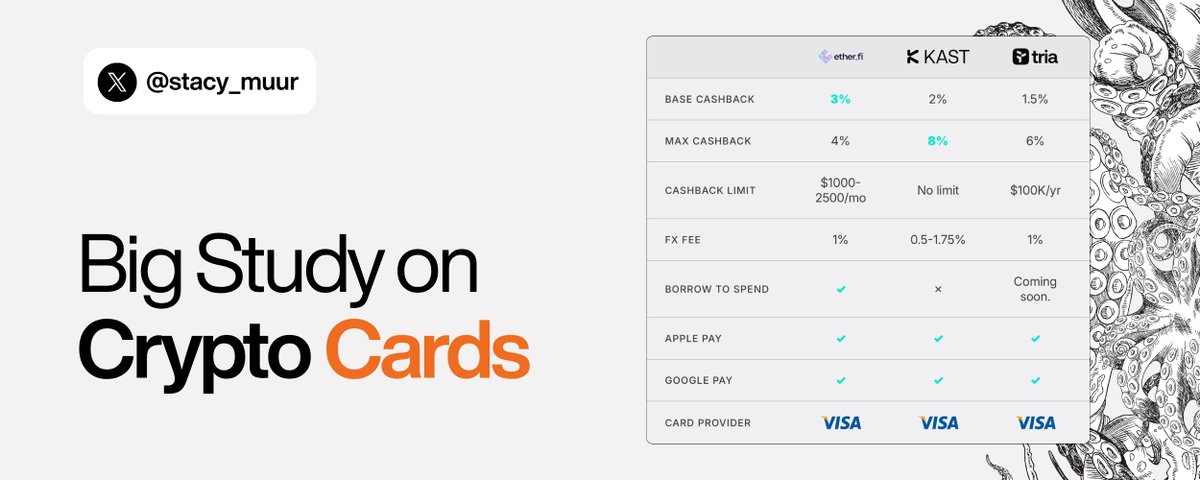

Aave alongside EtherFi, KelpDAO, and Compound propose unlocking ETH frozen by Arbitrum Security Council, aiming to channel funds into DeFi United to restore rsETH backing after April exploit2026-04 Crypto card competition heats up in 2026 as Tria, EtherFi and KAST battle traditional neobanks with stablecoin payments and onchain banking features2026-05

Crypto card competition heats up in 2026 as Tria, EtherFi and KAST battle traditional neobanks with stablecoin payments and onchain banking features2026-05

Ether.Fi: Liquid Restaking and Onchain Banking on Ethereum

A non‑custodial liquid restaking protocol and onchain “crypto neobank” built on Ethereum, Ether.Fi combines liquid staking, automated DeFi vaults, and a self‑custodial Visa card so users can save, earn yield, and spend without giving up control of their assets.

What is Ether.Fi?

Ether.Fi is a decentralized finance platform that sits at the intersection of Ethereum staking, restaking, and everyday onchain banking. At its core, it is a non‑custodial liquid restaking protocol: users deposit ETH and receive liquid tokens that represent staked and restaked positions, which continue to earn rewards while remaining usable throughout DeFi. Over time, the project has expanded into a broader product suite that includes automated yield vaults and a crypto‑backed Visa card, positioning itself as an onchain neobank for digital asset management. The unifying idea is that users should be able to save, grow, and spend crypto from a single interface, while keeping keys and onchain ownership under their own control.

From a technical standpoint, Ether.Fi builds on Ethereum’s proof‑of‑stake architecture and emerging restaking ecosystems such as EigenLayer, offering users exposure to base ETH staking yield plus additional restaking and DeFi rewards through its main tokens eETH and weETH. The protocol also operates a marketplace for node operators and validators, using deposited ETH to run validators while sharing rewards among stakers, node operators, and the protocol itself. On top of this, Ether.Fi routes liquidity into strategy vaults and real‑world‑asset products, while extending credit lines against staked collateral so users can spend via a credit card without selling their crypto. This blend of infrastructure‑level staking plus consumer‑facing banking features is what makes Ether.Fi notable in both the restaking and neobank narratives.

In terms of scale, Ether.Fi has grown quickly. The project describes itself as the leading onchain neobank, citing more than 6 billion dollars in assets under management across its Cash (card), Stake (restaking), and Liquid (strategy vault) products. It has also built a sizable user base; when the platform migrated to the Optimism OP Mainnet, it reported more than 70,000 active cards, over 300,000 accounts, and more than 200 million dollars in total value locked moving with it. These numbers are fluid by design—onchain TVL and user metrics shift with market conditions—but they illustrate that Ether.Fi has become one of the largest liquid restaking players on Ethereum.

Crucially, Ether.Fi is architected as non‑custodial. Users interact with smart contracts and hold their own private keys rather than depositing into a centralized exchange or lender. This means that risk shifts away from exchange insolvency or off‑chain mismanagement and toward smart contract security, validator performance, bridge safety, and market volatility. As the rest of this explainer will show, understanding Ether.Fi therefore requires looking not just at headline yields, but at how staking, vaults, cards, bridges, and institutional partnerships all connect in one onchain stack.

OP Mainnet logs largest TVL surge in history as Etherfi migrates $200M, bringing 70K cards and 300K users to Optimism to scale real-world crypto payments

Scroll just lost 28K daily spend transactions and over 25% of all crypto card volume (per Dune) to OP Mainnet — that's not a minor reshuffling. OP Mainnet's been bleeding mindshare to Base on pure DeFi, so leaning hard into payments infrastructure is a smart way to carve out a lane. 70K non-custodial cards pushing $2M/day in real spend is the kind of sticky activity that yield-farming TVL never produces.

Readers track EtherFi as a full-stack financial institution bet rather than a restaking protocol — the neobank pivot and Visa card generated comparable engagement to LRT yield mechanics, revealing that readers are stress-testing whether crypto-native banking can survive regulatory and competitive pressure, not just whether eETH beats competitors on APY.↗

Architecture and Core Tokens: ETH, eETH and weETH

Ether.Fi is built around Ethereum’s native asset, ETH, and two closely related tokens: eETH and weETH. Understanding how these tokens work, and how they interact with Ethereum’s proof‑of‑stake and restaking ecosystems, is essential to understanding the protocol itself.

Ethereum staking, liquid staking, and restaking

Ethereum’s proof‑of‑stake design allows anyone with at least 32 ETH, plus the technical capability to run validator hardware, to help secure the network and earn rewards. In practice, most users access staking via pooled solutions that accept smaller deposits and handle validator operations on their behalf. Liquid staking protocols go a step further by issuing liquid tokens that represent staked positions. Instead of locking ETH and waiting through withdrawal queues, users receive a token they can hold, trade, or deploy across DeFi while their underlying ETH continues to earn staking rewards.

Ether.Fi extends this idea into the emerging field of restaking. Restaking allows the same staked ETH to secure additional services built on top of Ethereum, sometimes called Actively Validated Services (AVSs), in exchange for extra yield. Rather than just earning the base staking reward, users who restake can earn supplementary rewards from these AVSs, plus protocol incentives and points. Ether.Fi’s liquid restaking tokens (LRTs) are designed to represent this layered exposure, wrapping base ETH staking plus restaking and DeFi strategy rewards into a single asset.

In this model, Ether.Fi sits between users and validators. Deposited ETH is allocated to validator nodes, either run by professional node operators or by users who wish to run their own validators through the platform’s node services marketplace. Rewards are then split according to a predefined sharing model, with a portion going to stakers, a smaller share to node operators, and a protocol fee retained by Ether.Fi. The protocol can also deploy validator capacity in structured ways, as seen in its three‑year agreement with Ethereum infrastructure provider ETHGas, under which ETHGas will supply 3 billion dollars’ worth of ETH validator liquidity to Ether.Fi’s liquid restaking token eETH to increase capital efficiency and network security.

Restaking amplifies both potential yields and potential risks. Users gain access to more diverse reward streams, but their capital is now linked not only to Ethereum’s consensus layer, but also to the performance and security of AVSs and any DeFi strategies layered on top. Ether.Fi’s architecture is therefore a complex stack: staked ETH at the base, restaking services in the middle, and DeFi vaults, RWA products, and credit lines at the top.

eETH: the rebasing liquid restaking token

The core user‑facing token in this stack is eETH. eETH is described as a rebasing ERC‑20 liquid staking token and the primary product of the Ether.Fi protocol. When users deposit ETH into Ether.Fi’s staking contracts, they receive eETH in return, representing a claim on staked and restaked ETH plus accumulated rewards. Because it is a rebasing token, the number of eETH tokens in a user’s wallet can increase over time as staking rewards are periodically distributed, rather than their price drifting upward relative to ETH.

Rebasing design has trade‑offs. On the one hand, it allows eETH to remain closely pegged to ETH in price terms, while the balance adjusts to reflect yield. This can simplify certain accounting and integration scenarios, particularly where protocols or wallets assume a 1:1 relationship between deposit token and underlying asset. On the other hand, rebasing can be challenging for some DeFi integrations, especially where smart contracts do not expect token balances to change without a direct transfer. This is one reason Ether.Fi also offers a wrapped, non‑rebasing version of its staking token.

From a yield perspective, holding eETH entitles users to the composite reward stream generated by Ether.Fi’s validator set and restaking activity. Sources describe current base yields in the low single digits, with additional restaking and incentive rewards on top; for example, community estimates shared with institutional partners referenced roughly 3.5 percent rewards plus protocol points, with total returns projected toward 7 percent as AVSs begin paying for blockspace and security. Those numbers are indicative rather than guaranteed, and actual yields vary with network conditions, reward structures, and protocol decisions. Nonetheless, they illustrate Ether.Fi’s goal: to package multiple yield sources into a single liquid token that behaves like staked ETH.

weETH: wrapped eETH for DeFi and cross‑chain use

To address integration challenges and improve composability, Ether.Fi offers weETH, a wrapped version of eETH that is non‑rebasing and designed as a value‑accruing token for DeFi. When users wrap eETH into weETH, they effectively lock the rebasing token in a smart contract and receive a fixed balance of weETH whose price gradually increases relative to ETH and eETH as rewards accrue. This pattern is familiar from other liquid staking ecosystems: the rebasing token is optimized for simple staking exposure, while the wrapped token is optimized for integration into lending platforms, AMMs, derivatives, and bridges.

Descriptions from centralized venues listing weETH emphasize its role as a DeFi‑native asset. Holding weETH allows users to gain native ETH staking rewards and EigenLayer restaking rewards, while also using the token as collateral or liquidity across DeFi protocols on Ethereum and compatible layer‑2 networks. Because it does not rebase, weETH can be more easily integrated into contracts that assume static balances, such as money markets, structured products, or cross‑chain messaging systems.

Liquidity and redemption mechanics matter in this context. According to a review prepared for Nexus Mutual governance, stakers can redeem ETH out of eETH or weETH without waiting through the Ethereum validator exit queue, as long as Ether.Fi has sufficient liquid ETH available in its contracts. This feature softens one of the main frictions of native staking, although it depends on Ether.Fi maintaining adequate buffers and market liquidity. In typical conditions, users can move between ETH, eETH, and weETH with minimal delay, and then deploy weETH throughout DeFi for leverage, yield farming, or hedging strategies.

Because weETH circulates widely, bridge and cross‑chain design are significant. Ether.Fi supports weETH bridging using infrastructure such as LayerZero, allowing the token to move to other Ethereum‑compatible chains. Following the broader industry’s bridge security concerns, Ether.Fi has periodically paused and then re‑enabled weETH bridge routes while hardening security parameters, such as pinning decentralized verification network (DVN) configurations and raising thresholds so that inbound messages must be validated by all participating DVNs. This design underscores the dual nature of weETH: an instrument of yield and liquidity, but also a vector through which cross‑chain risks can propagate if not carefully constrained.

Reward flows and protocol economics

Beneath the user experience of “Stake ETH, receive eETH/weETH, earn yield” lies a specific revenue‑sharing model. Ether.Fi’s own materials and community‑facing documentation describe a split in which 90 percent of staking rewards go to stakers, 5 percent to node operators, and 5 percent to the protocol. In this model, node operators are compensated for running and maintaining validators, while the protocol’s share funds development, operations, and risk management. There are no additional protocol fees on top of this revenue share, apart from standard Ethereum gas costs associated with staking and unstaking.

This baseline reward stream is augmented by restaking rewards from AVSs, protocol incentives, and point programs. For example, Ether.Fi and EigenLayer have both run points systems that reward early or sustained participation; one institutional analysis noted that these point programs had, at times, boosted annualized returns into much higher ranges than base staking alone. Such point programs are discretionary and may be convertible into tokens or other benefits, but they also add complexity and speculation to the yield stack.

On top of staking and restaking, Ether.Fi’s Liquid vaults deploy collateral into DeFi strategies that earn additional yield, while its RWA partnerships plug deposits into off‑chain assets such as credit pools, securitized loans, or bond ETFs. The resulting yield is then reflected in the value of vault shares or in the value growth of tokens like weETH when used as vault collateral. Because these strategies can involve borrowing, leverage, or exposure to off‑chain counterparties, their risk‑return profile can diverge significantly from vanilla ETH staking.

Finally, Ether.Fi’s broader business model involves consumer products and institutional services. On the consumer side, the Cash card extension and onchain banking features aim to generate interchange, interest spread, or ancillary revenue while still remaining non‑custodial. On the institutional side, the protocol has struck multi‑billion‑dollar deals such as its three‑year, 3‑billion‑dollar validator liquidity arrangement with ETHGas, effectively pre‑purchasing validator capacity to support eETH liquidity and blockspace market experiments. Together, these layers make Ether.Fi more than just a staking wrapper; it becomes a vertically integrated stack spanning validators, DeFi vaults, payments, and institutional blockspace markets.

Product Pillars: Stake, Liquid, and Cash

Ether.Fi organizes its offering into three main product lines: Stake, Liquid, and Cash. These correspond broadly to staking and restaking services, automated DeFi vaults, and consumer spending products. The platform’s marketing condenses this into a simple promise—save, grow, and spend from one onchain interface—aimed at both crypto‑native users and those coming from traditional neobank apps.

Stake: liquid restaking for ETH, stablecoins, and BTC

The Stake pillar is the foundation of Ether.Fi’s stack. Here, users deposit core assets such as ETH, stablecoins, or BTC and receive liquid restaking tokens that can be used across the wider ecosystem. For ETH, the primary exposure is via eETH and weETH, which encode the staking and restaking mechanics discussed above. For stablecoins and BTC, Ether.Fi offers analogous products, such as eUSD for staked stablecoins and eBTC for BTC‑denominated strategies.

According to third‑party platform reviews, users who deposit ETH into Stake receive weETH, which earns an advertised base APY in the range of roughly 4 percent plus additional reward programs. Stablecoin deposits into eUSD have been associated with higher nominal yields, reflecting both DeFi lending conditions and the risk profile of underlying strategies; one snapshot put eUSD’s APY around 6 percent plus rewards. BTC strategies via eBTC remain more nascent, with yields described as “to be determined” and reliant on the evolution of BTC‑based DeFi. All of these rates are illustrative, not fixed; they respond to Ethereum fee markets, validator rewards, leverage availability, and market demand for borrowing or hedging.

Stake is also where users interface with Ether.Fi’s node services marketplace. Users or institutions that want to run validators can plug into the protocol, supplying infrastructure in exchange for a cut of rewards and participation in blockspace markets. The ETHGas agreement is a notable example: by committing three billion dollars of validator liquidity to Ether.Fi’s eETH over a three‑year period, ETHGas provides a predictable supply of validator slots, while Ether.Fi commits to consuming that liquidity to boost capital efficiency and network security. Together, such arrangements underpin the yield that Stake can offer to retail users.

Liquid: automated DeFi strategy vaults

Above the base staking layer sits Liquid, a suite of automated DeFi vaults designed to deploy user assets across vetted protocols and strategies. Instead of manually chasing yields, users can deposit into themed vaults—such as ETH yield, market‑neutral stablecoin strategies, or BTC yield—and receive vault tokens that track their share of the strategy. The vault smart contracts then route capital into pools, money markets, or other protocols, auto‑compounding rewards and periodically rebalancing to maintain target risk profiles.

Data aggregators describe Liquid as a simple access point for using eETH in the DeFi ecosystem, with average APYs in the low single digits for ETH‑denominated vaults and higher yields for more complex USD strategies. For example, one review reported a “Liquid ETH Yield” vault offering around 3.45 percent APY plus additional rewards, while a “Market‑Neutral USD” vault posted near‑double‑digit yields by combining lending, borrowing, and hedging. These figures should be read as snapshots; they change with market volatility, protocol incentives, and risk assumptions.

Because Liquid sits at the center of Ether.Fi’s strategy layer, risk management has been a recurring theme in the project’s communications. During the fallout from a high‑profile exploit affecting another restaking token, rsETH, Ether.Fi publicly stated that its Liquid vaults were architecturally isolated and that users would not experience any drawdowns as a result of that incident. At the same time, the protocol proactively paused some of its bridge operations and cross‑protocol flows, before re‑enabling them with tightened security parameters, in order to minimize contagion risk and protect vault yields.

Liquid has also participated in coordinated ecosystem responses to systemic risk. When a major lending protocol froze a large WETH pool amid concerns about concentration and risk, a coalition including Fluid, Lido, Ether.Fi, 1inch, 0x, and Kyber launched an “aWETH Redemption Protocol” that allowed users to redeem out of the frozen pool, processing more than 136 million dollars in redemptions within 48 hours. Ether.Fi’s involvement in such efforts is part of a broader pattern in which large liquid staking and restaking providers are increasingly expected to contribute to DeFi’s financial stability, not just to extract yield.

Cash: crypto‑backed credit and real‑world spending

The Cash pillar translates onchain yield into everyday spending power. Ether.Fi Cash is a self‑custodial Visa credit card that lets users borrow against their staked ETH—specifically eETH or weETH—without selling, allowing their crypto collateral to continue earning staking and restaking rewards while they spend. This distinguishes Ether.Fi’s card from many competing crypto cards, which typically require users to sell crypto into fiat before loading a prepaid balance.

Reviews of the Cash program highlight several key features. The card operates on the Visa credit network and can be used at over 100 million locations worldwide, with support for digital wallets such as Apple Pay and Google Pay. It offers four membership tiers—Core, Luxe, Pinnacle, and VIP—with public tiers advertising around 3 percent cashback on purchases, a 1 percent foreign exchange fee, and varying requirements in terms of Ether.Fi points or staked ETHFI tokens. Availability currently spans major markets such as the US, UK, and European Economic Area, subject to regulatory and compliance checks.

From a risk and design perspective, Cash is essentially a secured credit line backed by onchain collateral. Users lock eETH or weETH, which continue to earn staking and restaking yield, and receive a revolving credit line that can be drawn down via card transactions. If collateral values fall or debts are not repaid, positions may be liquidated or constrained according to protocol parameters. Importantly, Ether.Fi positions Cash as non‑custodial: users retain control over their wallets and collateral onchain, rather than depositing assets into a traditional custodian. This aligns with the broader neobank narrative, in which Ether.Fi aims to replicate the simplicity of mainstream banking apps while preserving the self‑sovereignty and transparency of onchain finance.

- 01neobank pivot viability↗

Multiple headlines across DeFi Bank vision, Cash Visa card, hotel booking, and US card rollout accumulated the highest aggregate clicks, showing readers are uncertain whether a restaking protocol can credibly become consumer banking infrastructure.

- 02LRT TVL race↗

The surge past $3.5B TVL and side-by-side comparison charts pulled readers tracking which liquid restaking token—eETH, ezETH, or rsETH—captures dominant EigenLayer yield share before the market consolidates.

- 03blue-chip DeFi integrations↗

Partnerships with Aave, Ethena, Derive, Fluid, and Plume attracted readers using weETH's integration depth as a proxy for whether the token achieves durable liquidity across DeFi rather than remaining siloed.

- 04ETHFI airdrop disappointment

Season 2 claims going live alongside widespread complaints about the claim process drew readers who had farmed points and expected outsized rewards, revealing a gap between points-farming incentives and actual token distribution.

- 05institutional restaking scale↗

The $3B ETHGas preconfirmation deal and Plasma $500M vault partnership attracted readers tracking whether EtherFi can lock in institutional capital at a scale that forecloses competitor catch-up.

- 06frontend security breach

The frontend compromise warning drew readers questioning whether a non-custodial protocol retains meaningful attack surface through its own UI—and what that means for a protocol positioning itself as consumer banking.

Ether.Fi as an Onchain Neobank

The term “neobank” typically evokes mobile‑first fintechs that offer checking accounts, cards, and budgeting tools on top of regulated banking partners. Ether.Fi’s claim to be the leading onchain neobank reframes this model around smart contracts, liquid staking, and non‑custodial asset ownership. Rather than holding users’ deposits off‑chain and extending loans from a centralized balance sheet, Ether.Fi routes user assets directly into onchain staking, vaults, and RWA products, while coordinating card credit through collateralized positions.

The migration of Ether.Fi’s consumer stack to Optimism’s OP Mainnet underscores this neobank positioning. In announcing the move, Ether.Fi highlighted that more than 70,000 active cards, over 300,000 accounts, and more than 200 million dollars in TVL would be operating directly on OP Mainnet, with expectations of increased cashback rewards, native stablecoin support, and deeper onchain liquidity as a result. By embedding card operations and user balances on a scalable Ethereum layer‑2, Ether.Fi aims to reduce transaction costs, enable real‑time reward distribution, and integrate card spending more tightly with DeFi strategies.

Independent analyses of crypto card adoption trends place Ether.Fi alongside competitors such as Tria and KAST, noting that transaction data from these programs illustrates how stablecoins and tokenized dollars are increasingly used for everyday spending and quasi‑banking functions. Ether.Fi’s differentiation lies in combining this with restaking yield and DeFi vaults; card users are not simply spending from a static balance but from a collateral base that can generate returns in ETH, USD‑pegged assets, or other tokenized exposures. This turns the traditional bank account plus credit card stack into an onchain portfolio plus collateralized card model.

At the interface level, Ether.Fi’s app aims to abstract away some of the complexity of DeFi. Users onboarding via the neobank front end can see balances in intuitive categories—cash‑like assets, staked positions, vault allocations, and card credit—while the underlying contracts handle bridging, staking, and restaking. For more advanced users, the same interface exposes granular controls over vault choices, cross‑chain deployments, and collateral management. This dual‑mode design is critical for any attempt to move DeFi beyond niche usage, and it is where Ether.Fi’s branding as a neobank intersects with its technical ambitions in staking and blockspace markets.

Ether.fi commits $3B in ETH to ETHGas in exclusive three-year preconfirmation deal

Ether.fi is routing roughly $3 billion in ETH — about 40% of its 2.8 million staked ETH under management — into ETHGas' blockspace marketplace over a three-year term. The deal locks ether.fi into ETHGas' High Performance Staking Service and grants ETHGas exclusive use of its preconfirmation platform for the duration. This dwarfs ETHGas' previous $800M in total validator commitments from its Polychain-led seed round and gives the blockspace futures market its largest single supply-side anchor. For ether.fi stakers, it's a bet that preconfirmation yield on top of existing restaking returns justifies concentrating this much liquidity with one infrastructure partner.

DeFi Vaults, Bridge Security, and Systemic Risk

As Ether.Fi’s AUM has grown, so too has its potential impact on DeFi stability. The protocol’s Liquid vaults, cross‑chain bridges, and participation in rescue mechanisms such as DeFi United all illustrate how large restaking platforms now sit at the center of systemic risk and risk mitigation.

The design of Liquid vaults reflects a trade‑off between automation and transparency. On the one hand, Ether.Fi advertises Liquid as a way for users to earn on their eETH without having to manually research and manage DeFi strategies, with smart contracts handling allocation, auto‑compounding, and rebalancing. On the other hand, this layering means that end‑users may be exposed to protocols they have not individually vetted, and to complex interactions between interest rates, liquidity incentives, and collateral risks. Ether.Fi and independent analytics providers therefore emphasize metrics such as total value locked, average APY, and revenue sources for Liquid, as well as publishing strategy details and contract addresses.

Bridge security is another focal point. Because weETH is designed to be used on multiple chains, Ether.Fi relies on cross‑chain messaging infrastructure such as LayerZero to move tokens between networks. Following high‑profile bridge exploits elsewhere in DeFi, Ether.Fi has undertaken security hardening measures, including pinning decentralized validation network configurations and raising thresholds so that every inbound message must be independently verified by four separate DVNs before being accepted on the destination chain. These changes increase redundancy and reduce single‑point‑of‑failure risks, at the cost of some latency and complexity.

The project’s response to the Kelp rsETH incident offers a case study in cross‑protocol risk management. When vulnerabilities in another restaking token raised fears of contagion, Ether.Fi announced that its Liquid vaults were unaffected and that users would not see drawdowns, emphasizing architectural separation between rsETH and its own collateral stack. It then temporarily paused certain bridge flows and re‑opened them only after implementing additional safeguards, framing the process as a proactive move to “unlock safer yields” while preserving user confidence. Such decisions highlight a broader shift in DeFi narratives: large protocols are no longer only optimizing yields, but also explicitly managing systemic risk and reputational spillovers.

Ether.Fi’s involvement in collaborative initiatives such as DeFi United and Fluid’s aWETH Redemption Protocol reinforces this theme. In the wake of the rsETH exploit, Ether.Fi was among the protocols backing a coordinated plan to direct recovered or unlocked ETH into a joint effort to restore rsETH backing and contain systemic fallout, effectively pledging part of its influence and liquidity to stabilize a peer asset. Likewise, by partnering with Lido, 1inch, 0x, Kyber, and Fluid to create an escape hatch for Aave’s frozen WETH positions, Ether.Fi helped process more than 136 million dollars in redemptions within two days, reducing concentration risk and unlocking trapped liquidity. These actions reflect not just altruism but enlightened self‑interest: as a major restaking provider, Ether.Fi’s long‑term value is tied to the health of the broader Ethereum and DeFi ecosystem.

eETH opens for public minting with EigenLayer points

- 2024-03milestone

ETHFI token launches; Season 1 airdrop distributed

- 2024-07governance

Season 2 airdrop claims go live amid widespread user complaints

- 2024-11exploit

Frontend compromised; users warned to exercise caution

DeFi Bank and Ether.fi Cash Visa card announced for US market

- 2025-04milestone

Aave v3 EtherFi Instance launches isolated weETH market

Ether.fi commits $3B ETH to ETHGas in three-year preconfirmation deal

EtherFi allocates $100M exclusively into Plume RWA Nest Vault

OP Mainnet Migration and Multi‑Chain Strategy

Ether.Fi’s migration to OP Mainnet is a significant strategic move that touches technological, economic, and competitive dimensions. Prior to the migration, many Ether.Fi interactions ran on Ethereum mainnet, where gas costs and throughput can be constraints for consumer‑grade banking experiences. By relocating much of its user activity to Optimism’s layer‑2 network, Ether.Fi aims to achieve lower fees and higher transaction throughput while still anchoring security to Ethereum.

In its migration announcement, Ether.Fi reported bringing more than 70,000 active cards, over 300,000 accounts, and more than 200 million dollars in TVL to OP Mainnet. It framed the move as unlocking the “next phase” of its neobank roadmap, including richer cashback programs, native stablecoin support, and deeper onchain liquidity for its products. Because Optimism is EVM‑compatible, Ether.Fi can deploy smart contracts that closely mirror their mainnet counterparts, while bridging core assets like ETH, eETH, and stablecoins into the L2 environment. The result is a unified experience where card swipes, vault deposits, and collateral adjustments can all happen with low‑cost, near‑instant transactions.

At the same time, multi‑chain deployments introduce new categories of risk. Smart contract bugs or misconfigurations on L2 can affect large user cohorts; bridge failures can isolate or strand assets; and differences in sequencer or governance models can create nuanced trust assumptions compared to Ethereum mainnet. Ether.Fi’s OP Mainnet rollout therefore drew comparisons with previous banking system migration incidents, where software issues have caused prolonged outages and user frustration. In this context, the protocol’s emphasis on gradual migration, clear communication, and contingency planning takes on added importance.

Strategically, the move to OP Mainnet also intersects with competition among Ethereum L2s for marquee applications and TVL. Ether.Fi is a high‑profile win for Optimism’s ecosystem, contributing to one of the largest TVL surges in OP Mainnet’s history and reinforcing its narrative as an onchain economy for payments, DeFi, and consumer apps. For Ether.Fi, the choice of Optimism—rather than alternative L2s like Base or Arbitrum—as the primary home for its card and neobank logic signals a view on where its users and partners are likely to congregate, even as the protocol continues to interact with other chains via bridges and DeFi integrations.

Institutional Adoption, RWAs, and the Plume Partnership

One of the most consequential developments in Ether.Fi’s evolution has been its push into real‑world assets (RWAs) and institutional‑grade yield. This has been crystallized in its partnership with Plume, an onchain finance platform focused on institutional assets, to launch a flagship RWA Vault backed by a 100‑million‑dollar allocation from Ether.Fi.

The Plume RWA Vault is designed to bring institutional‑grade real‑world asset yield to Ether.Fi’s user base, which the partners describe as holding more than 6 billion dollars in deposits across Ether.Fi’s various products. Rather than relying solely on onchain lending and trading fees, the vault channels capital into a structured portfolio of traditional financial instruments, such as overcollateralized credit pools, AAA‑rated collateralized loan obligations (CLOs), and broad bond market ETFs managed by asset issuers with more than 10 trillion dollars under management. These exposures are then tokenized and standardized via Plume’s “Nest Vaults,” creating onchain shares that encode off‑chain yield streams.

For Ether.Fi users, the key promise is access to yield profiles that historically have been available mainly to institutional or high‑net‑worth investors, but in a form that remains non‑custodial and composable. Eligible users can access the Plume RWA Vault directly from within the Ether.Fi interface, allocating a portion of their assets into structured RWA strategies while maintaining onchain ownership and the ability to monitor positions transparently. In theory, this can smooth overall portfolio volatility by mixing crypto‑native and traditional yield, although it also introduces new layers of legal, regulatory, and counterparty risk associated with off‑chain borrowers and securities.

The partnership also reflects a broader thesis articulated by Ether.Fi’s venture arm: that RWA tokenization is shifting from hype to infrastructure. Ether.Fi Ventures has argued that RWAs should not be viewed as a single asset class but as a new financial infrastructure stack, where the visible token in a user’s wallet is only the tip of a system that includes stablecoins, Treasuries, custody, compliance, and liquidity plumbing underneath. In this framing, platforms like Plume and Ether.Fi are building shared rails through which institutional asset managers can connect directly to onchain neobanks and earn platforms, bypassing some of the fragmented intermediaries of traditional finance.

From an ecosystem perspective, Ether.Fi’s move into RWAs narrows the perceived gap between DeFi and regulated finance. Users who hold eETH and weETH for Ethereum staking yield can now toggle into RWA vaults within the same interface, potentially combining crypto‑denominated returns with dollar‑denominated fixed income. At the same time, institutional asset issuers gain access to a new distribution channel: onchain retail and prosumer users who want “institutional‑grade yield” without leaving the comfort of a crypto‑native app. How regulators, auditors, and risk managers respond to this blending will be a central storyline in the coming years.

Fluid rolls out $1B-cap aWETH Redemption Protocol with Lido Finance, EtherFi, and 1inch to reduce systemic DeFi risk and unlock trapped ETH liquidity on Aave

stETH depeg in 2022 proved the failure mode — looped LST collateral on Aave can't unwind through DEX liquidity when everyone hits exits at once. Routing aWETH redemptions atomically to Lido/EtherFi issuer queues via Fluid bypasses the AMM slippage cascade entirely. $1B cap vs $2B+ wstETH/weETH collateral on Aave v3 is partial coverage, but atomic unwind capacity shifts the game theory of a depeg event.

weETH routes through multiple contract layers across chains; the dedicated weETH bridge security hardening post indicates a prior vulnerability surface that required post-launch remediation rather than pre-launch prevention.

- CentralizationMedium

EtherFi holds withdrawal key custody for the majority of deposited ETH during the current non-permissionless validator phase; institutional restaking agreements capped at protocol-defined limits reduce operator diversity.

The Ether.fi Cash Visa card and neobank model place the protocol at the intersection of DeFi and consumer finance, inviting potential scrutiny from banking regulators and Visa network compliance requirements that do not apply to pure restaking protocols.

weETH participates in looped leverage strategies on Aave and Fluid; the DeFi United rsETH coordination—which EtherFi joined—demonstrates that LRT liquidity crises can require emergency multi-protocol bailouts to prevent cascading unwinding.

EigenLayer AVS slashing is not fully activated as of mid-2025; once live, eETH restakers face additional penalty exposure layered on top of standard Ethereum validator slashing risk, with no socialized insurance fund disclosed.

Renzo, Kelp, Puffer, and Bedrock compete directly for LRT market share; ezETH supply on L2s already exceeds eETH's L2 footprint according to clicked headlines, signaling that EtherFi does not hold a dominant position outside mainnet.

Governance, Token Incentives, and Business Model

While Ether.Fi’s smart contracts handle much of the protocol’s day‑to‑day logic, governance and incentive design are critical to how the system evolves. Ether.Fi’s revenue model, token incentives, and governance processes together shape how risk and rewards are distributed among users, node operators, and developers.

As noted earlier, Ether.Fi’s baseline economics allocate 90 percent of staking rewards to stakers, 5 percent to node operators, and 5 percent to the protocol treasury, with no additional management fees beyond Ethereum gas costs. This aligns incentives in a relatively straightforward way: stakers are the primary beneficiaries of validator performance; node operators are compensated for reliable uptime and honest behavior; and the protocol retains a modest but meaningful share to fund operations and growth. Any additional fee income from DeFi strategies, RWA vaults, or card products can be layered on top of this base, either accruing to the treasury or being shared with users through enhanced yields or reward programs.

In terms of incentives, Ether.Fi has made extensive use of points and token‑based loyalty structures. Staking reviews and governance proposals emphasize that users can earn Ether.Fi points and EigenLayer points in addition to base rewards, with points at times implying double‑digit effective yields when valued according to secondary market expectations. These programs are subject to change and often tied to speculative narratives around future token distributions or governance rights. For the Cash card, Ether.Fi also uses its ETHFI token as part of membership tier requirements, with higher tiers such as Luxe and Pinnacle unlockable by staking specified amounts of ETHFI or accumulating points through activity.

Governance itself mixes onchain and off‑chain mechanisms. For large institutional relationships, such as Nexus Mutual’s proposal to allocate between 6,585 and 14,000 ETH into weETH, detailed forum discussions, risk assessments, and periodic reviews are expected, including scheduled calls with the Ether.Fi team to discuss updates, concerns, and additional staking opportunities. For protocol‑internal decisions, such as bridge parameters, vault configurations, or response strategies to ecosystem incidents, Ether.Fi has tended to act quickly through its core contributor team, later publishing post‑mortems or blog posts that explain changes and invite feedback. Over time, one can expect more of these levers to be formalized into token‑holder voting or structured governance frameworks, particularly as the protocol’s footprint in blockspace markets and RWA channels expands.

The business model that emerges from these pieces is multi‑segment. For retail and prosumer users, Ether.Fi offers a suite of free or low‑fee services—staking, vaults, and a cashback card—funded by protocol reward shares, card economics, and partner incentives. For institutions, it offers access to large‑scale validator capacity, blockspace preconfirmation markets, and distribution for structured products such as the Plume RWA Vault. The challenge will be balancing these constituencies so that institutional deals, like the 3‑billion‑dollar ETHGas agreement, reinforce rather than undermine user trust and yield sustainability.

Positioning in the Restaking and Neobank Landscape

Ether.Fi operates in two overlapping competitive arenas: liquid staking/restaking on Ethereum and crypto‑enabled neobanking. Comparing it to typical liquid staking protocols and to other crypto card providers helps clarify what is distinctive about its model.

Traditional liquid staking protocols, such as those that issue basic LSTs without restaking or consumer banking features, focus primarily on maximizing staking efficiency and DeFi composability. They take in ETH, run validators, and return a liquid token that represents staked ETH plus base rewards. In contrast, Ether.Fi’s eETH and weETH are explicitly designed as liquid restaking tokens, with integrated hooks into EigenLayer and other AVSs, and with downstream uses in strategy vaults, RWA products, and credit lines. This means Ether.Fi’s tokens sit at the center of a thicker stack of financial relationships than many first‑generation LSTs.

On the neobank side, competitors such as Tria or KAST typically combine stablecoin balances, basic yield, and card programs, but may rely on centralized custody or require users to sell crypto into fiat before spending. Ether.Fi’s Cash program instead uses onchain collateral and self‑custodial wallets, with card users effectively drawing against credit lines backed by staked, yield‑earning crypto. This mirrors margin‑backed credit cards in traditional finance but implemented via smart contracts and liquid restaking tokens.

The following simplified table compares Ether.Fi’s positioning with a generic liquid staking protocol and a generic crypto card provider. The table abstracts away many nuances but highlights key structural differences.

| Dimension | Ether.Fi | Typical Liquid Staking Protocol | Typical Crypto Card Provider |

|---|---|---|---|

| Core asset | ETH, stablecoins, BTC via LRTs (eETH, weETH, eUSD, eBTC) | ETH via LST (e.g., staked ETH) | Fiat or stablecoins held custodially |

| Staking model | Liquid staking plus restaking into AVSs | Liquid staking only | Usually none (off‑chain banking relationships) |

| Yield sources | ETH staking, restaking, DeFi vaults, RWA products | ETH staking plus limited DeFi integrations | Bank interest, card interchange, sometimes simple yield |

| User custody | Non‑custodial; user controls keys and contracts | Often non‑custodial, but narrower front end | Frequently custodial, with user balances on provider ledger |

| Card model | Credit line backed by onchain collateral (eETH/weETH) | Often no native card, or prepaid debit via partners | Credit or debit, funded by selling crypto or fiat balances |

| Network footprint | Ethereum mainnet, OP Mainnet, multi‑chain via weETH bridges | Ethereum mainnet, sometimes L2 and sidechains | Primarily off‑chain, with limited onchain interaction |

| Institutional partnerships | Validator liquidity (ETHGas), RWA vaults (Plume) | Validator relationships, some institutional staking | Card networks, banks, but little onchain institutional finance |

This comparison underscores Ether.Fi’s ambition to straddle both infrastructure and consumer finance. It attempts to be a core staking and blockspace liquidity provider to Ethereum while also presenting itself as a checking account, investment platform, and credit card all rolled into one onchain application. That breadth creates both opportunity—cross‑selling, ecosystem influence—and risk, because failures in one layer can reverberate through others.

Practical Considerations for Users

For users considering Ether.Fi, the platform’s integrated design is both a strength and a source of complexity. A typical journey might begin with depositing ETH into the Stake product to obtain eETH or weETH. That weETH could then be deployed into a Liquid vault to earn additional yield, pledged as collateral for the Cash card to enable spending, or allocated into the Plume RWA Vault to gain exposure to institutional‑grade fixed‑income strategies. Each step layers on new forms of risk and reward, all mediated by smart contracts and market dynamics.

The non‑custodial architecture means that users are responsible for their own wallets, private keys, and transaction management. While Ether.Fi’s user interface aims to abstract away many technical details, underlying operations—such as approving token spends, bridging assets, or managing collateral ratios—still require basic DeFi literacy. Mistakes such as signing malicious transactions, misconfiguring collateral settings, or ignoring liquidation warnings can have irreversible consequences. This is particularly salient for the Cash product, where failing to manage credit lines within protocol parameters could result in collateral liquidation or loss of access to credit.

Smart contract and protocol risk are also central. Ether.Fi’s contracts have been deployed on Ethereum mainnet and OP Mainnet and are subject to audits and public scrutiny, but no onchain system is free from the possibility of bugs or economic exploits. Similarly, Liquid vault strategies rely on other DeFi protocols; a failure or exploit in those dependencies could translate into losses for vault depositors, even if Ether.Fi’s own contracts perform as intended. The same applies to cross‑chain bridges used by weETH—security hardening measures such as four‑of‑four DVN validation reduce risk but cannot eliminate it.

Restaking introduces a further layer of systemic considerations. Because eETH and weETH may be used to secure additional AVSs beyond Ethereum itself, adverse events in those services—such as slashing, misbehavior penalties, or governance failures—could impact restaked capital. While restaking promises higher aggregate yields, it also links Ether.Fi’s deposit base to an evolving and relatively experimental risk surface. Users should therefore be cautious about treating restaking yields as “free” incremental return; they are compensation for real, if sometimes opaque, additional risks.

Regulatory and tax implications round out the picture. Ether.Fi’s headquarters in the Cayman Islands and its availability in jurisdictions like the USA, UK, and EEA are subject to compliance obligations that may shift as regulators clarify rules around staking, stablecoins, RWAs, and crypto‑backed credit. Users may face local tax obligations on staking rewards, vault yields, or card cashback, and should seek professional advice where needed. Moreover, eligibility for products such as the Plume RWA Vault may depend on jurisdiction, accreditation status, or KYC/AML requirements. As with any cross‑border financial product stack, the convenience of a unified interface does not erase the underlying legal and regulatory complexity.

Outlook

Ether.Fi embodies several of the most important trends in Ethereum and DeFi today: liquid restaking, onchain neobanking, RWA integration, and institutional blockspace markets. Its rapid growth—from a liquid staking startup founded in 2022 to a self‑styled leading onchain neobank with billions in AUM, tens of thousands of cardholders, and a three‑billion‑dollar validator liquidity deal—illustrates how quickly the frontier of crypto financial infrastructure is moving.

Looking ahead, much will depend on how three vectors evolve. First, the restaking ecosystem must demonstrate that it can deliver sustainable, non‑circular rewards without introducing destabilizing correlated risks. Ether.Fi’s role in coordinated risk‑management initiatives, such as DeFi United and the aWETH Redemption Protocol, suggests an awareness that large restaking providers now share responsibility for ecosystem stability as well as for yield generation. Second, the RWA and institutional yield thesis must prove itself through transparent performance, robust legal structuring, and regulatory clarity. The Plume partnership positions Ether.Fi at the forefront of this experiment, but scaling integrated onchain/off‑chain portfolios will test both platforms’ operational and governance models.

Third, the onchain neobank model must compete not only with other crypto cards and DeFi wallets, but with regulated fintechs and traditional banks that are slowly integrating digital asset rails. Ether.Fi’s OP Mainnet migration, self‑custodial card, and integrated vaults give it a differentiated entry in this race, but they also raise the bar for security, user experience, and compliance. Success will require pairing low‑friction interfaces with transparent disclosures and robust risk controls, so that users can understand what underlies their yield and card limits.

If Ether.Fi can balance these forces—leveraging its validator base and institutional deals to support user yields, while maintaining non‑custodial principles and contributing to systemic resilience—it will likely remain a central reference point in discussions of Ethereum restaking and onchain banking. For crypto users, Ether.Fi is an early glimpse of a world where the line between “bank account,” “investment portfolio,” and “staking rig” blurs, and where the infrastructure of institutional finance becomes increasingly programmable, transparent, and accessible from a wallet on a phone.

Latest Ether.Fi news

OP Mainnet logs largest TVL surge in history as Etherfi migrates $200M, bringing 70K cards and 300K users to Optimism to scale real-world crypto paymentsEther.fi commits $3B in ETH to ETHGas in exclusive three-year preconfirmation dealFluid rolls out $1B-cap aWETH Redemption Protocol with Lido Finance, EtherFi, and 1inch to reduce systemic DeFi risk and unlock trapped ETH liquidity on AaveEther.fi re-enables weETH bridging via LayerZero across all chains with liquid minting and redemption, boosting security by increasing DVNs to four and tightening rate limitsAave alongside EtherFi, KelpDAO, and Compound propose unlocking ETH frozen by Arbitrum Security Council, aiming to channel funds into DeFi United to restore rsETH backing after April exploitCrypto card competition heats up in 2026 as Tria, EtherFi and KAST battle traditional neobanks with stablecoin payments and onchain banking featuresSources

- https://www.ether.fi

- https://www.ether.fi/app/weeth

- https://x.com/ether_fi/status/2048051089497329876

- https://phemex.com/news/article/ether-fi-secures-3-billion-validator-liquidity-deal-with-ethgas-73433

- https://www.ether.fi/blog/ether-fi-is-now-on-op-mainnet

- https://www.prnewswire.com/news-releases/etherfi-allocates-100m-exclusively-into-plume-rwa-vault-302791339.html

- https://stacymuur.substack.com/p/crypto-cards-in-2026-tria-vs-etherfi

- https://www.ether.fi/blog/weeth-bridge-security-hardening

- https://thedefiant.io/news/defi/defi-protocols-launch-joint-escape-hatch-for-aave-eth-lenders-and-loopers

- https://x.com/etherfi_VC/status/2059352774253613236

- https://www.bullish.com/us/digital-assets/weeth-wrapped-eeth

- https://x.com/ether_fi/status/2045901462623133865?lang=en

- https://x.com/ether_fi/status/2045901462623133865

- https://forum.nexusmutual.io/t/rfc-stake-idle-eth-on-enzyme-vault-to-ether-fi/1464

- https://www.spendnode.io/crypto-cards/ether-fi/

- https://www.coininterestrate.com/platforms/ether-fi/

- https://defillama.com/protocol/ether.fi-liquid

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…