In crypto, “metals” spans tokenized bullion, strategic commodities and 24/7 derivatives on gold, silver, uranium and more. This explainer covers how metals move onchain, key platforms, DeFi integration gaps, and the macro forces shaping their future.

+6 sources across the wider coverage universe

Tezos backs Metals platform bringing gold, uranium, and rare earth assets onchain, enabling investors to access critical materials driving AI and industrial growth2026-04

Tezos backs Metals platform bringing gold, uranium, and rare earth assets onchain, enabling investors to access critical materials driving AI and industrial growth2026-04 Hyperliquid HIP-3 surpasses $2B in open interest as tokenized equities displace metals2026-04

Hyperliquid HIP-3 surpasses $2B in open interest as tokenized equities displace metals2026-04 Pyth launches 24/7 indices for US stocks, oil and metals, enabling round-the-clock trading across perps, prediction markets and tokenized assets2026-06

Pyth launches 24/7 indices for US stocks, oil and metals, enabling round-the-clock trading across perps, prediction markets and tokenized assets2026-06 Most tokenized RWAs just sit onchain: bonds and metals have huge tokenized caps but minimal DeFi use, while DeFi-native assets like reinsurance and private credit see far higher onchain utilization.2026-05

Most tokenized RWAs just sit onchain: bonds and metals have huge tokenized caps but minimal DeFi use, while DeFi-native assets like reinsurance and private credit see far higher onchain utilization.2026-05 Gold suffered its worst single-day crash in over 40 years, with ~$3T wiped from precious metals, while Bitcoin held above ~$82k—fueling a thesis that capital may rotate from crowded gold trades into BTC over the next few months as macro liquidity improves.2026-02

Gold suffered its worst single-day crash in over 40 years, with ~$3T wiped from precious metals, while Bitcoin held above ~$82k—fueling a thesis that capital may rotate from crowded gold trades into BTC over the next few months as macro liquidity improves.2026-02 A Tennessee man accused of stealing over $11M in XRP from Nancy Jones, widow of country music legend George Jones, has countersued, claiming entitlement to the crypto, cash, and precious metals after allegedly managing and growing the assets during their relationship.2026-01

A Tennessee man accused of stealing over $11M in XRP from Nancy Jones, widow of country music legend George Jones, has countersued, claiming entitlement to the crypto, cash, and precious metals after allegedly managing and growing the assets during their relationship.2026-01

Metals in Crypto: Tokenization, Derivatives, and the New Onchain Commodity Stack

In crypto markets, the term metals usually refers to digital instruments that track the price or ownership of physical commodities such as gold, silver, platinum, palladium, uranium, and rare earth elements, delivered via blockchains rather than vault receipts or futures accounts. These products range from fully backed tokenized bullion to leveraged perpetual futures and 24/7 indices, tying one of the oldest asset classes in finance to the infrastructure of onchain markets.

Although physical metals markets have been institutionalized for more than a century, many of their core processes—vault custody, over-the-counter trading, and limited market hours—still resemble a pre-digital era. This makes metals a natural proving ground for real‑world asset tokenization, where blockchain rails promise instant settlement, composability with DeFi, fractional ownership, and around‑the‑clock trading of what were once daylight-only assets. At the same time, metals occupy a unique place in investor psychology as both industrial inputs and macro hedges, creating interesting interactions with crypto’s own narratives around “digital gold,” risk-on speculation, and decentralized store-of-value. The result is a rapidly evolving landscape in which tokenized metals, perpetual futures, and oracle-powered indices are beginning to reshape how both retail and institutions access commodity exposure, even as most onchain metals still sit idle rather than being deeply integrated into DeFi.

What “Metals” Means in Crypto

From Bullion Vaults to Blockchains

To understand metals in a crypto context, it helps to begin with how metals are traded in traditional finance. For most of modern history, exposure to gold, silver and other precious metals has been obtained through a mixture of physical bullion, allocated or unallocated accounts with banks, exchange‑traded futures, and more recently exchange‑traded funds (ETFs). Despite incremental innovation, the structural features of the market—centralised vaults, reliance on intermediaries, regional trading hours, and settlement cycles that can stretch over days—have changed relatively little since the late nineteenth century. Even today, much of the global bullion trade is mediated through OTC dealers and clearing systems whose operational rhythms predate the internet.

Blockchain-based metals products attempt to retrofit this legacy infrastructure with a digital layer that is native to crypto. Tokenized metals create a digital representation of a specific quantity of physical metal, held in a secure vault and linked to a token that can move across wallets and smart contracts with the same ease as a stablecoin. In the canonical model, each token corresponds to a unit of metal—such as one troy ounce of gold—stored with a custodian, with transparency provided through attestations, audits, and sometimes onchain proofs of reserve. Crucially, these instruments are designed not merely as synthetic trackers of price, but as claims on actual bars or coins, giving token holders legal or contractual redemption rights.

However, “metals” in crypto is a broader category than spot tokenization alone. It also encompasses perpetual futures (or “perps”) that reference metal prices but are settled purely in stablecoins or crypto, options and structured products whose payoff depends on metal indices, and increasingly, baskets or indices that combine metals with equities or other assets in a single onchain instrument. Pyth’s 24/7 indices for gold and silver, built from live oracle price feeds, exemplify this expanded universe, providing reference rates that can be embedded in perps, prediction markets, structured vaults, and tokenized asset products. The term therefore spans the whole spectrum from fully collateralized real‑world assets to purely synthetic derivatives anchored in offchain prices.

Categories of Metal-Linked Crypto Instruments

At a high level, metal-linked crypto instruments can be grouped into several functional categories, each with different risk profiles and use cases. The first is tokenized spot metals, where a blockchain token represents title to a fixed amount of metal locked in a vault, typically on a one‑for‑one basis. These instruments are closest in spirit to traditional allocated bullion accounts, but with programmability and global transferability layered on top. Projects in this category aim to bridge the stability and familiarity of physical metals with the composability of DeFi, allowing gold or silver to be posted as collateral, lent into money markets, or swapped instantly against stablecoins.

The second category consists of synthetic exposure products, most notably perpetual futures contracts that reference metal prices but are collateralized and settled in crypto or stablecoins rather than in the underlying metal itself. Protocols such as Ostium offer RWA perps on gold, silver, oil and other assets, allowing traders to go long or short XAU/USD or XAG/USD in a self-custodial environment with leverage and real‑time funding rates. Centralized venues like Coinbase have also listed metals perps alongside stock perps, with stock and metals perpetuals generating over 1.5 billion dollars in trading volume within their first two months, highlighting demand for synthetic exposure to real‑world assets on 24/7 rails. These instruments are attractive for active traders but do not confer any claim on physical metal.

A third category is index-based and basket products, where metals are combined with other assets into a single composite measure or token. Pyth Indices, for example, construct proprietary 24/7 benchmarks for metals such as gold and silver, as well as U.S. equities and oil, which can be used as underlyings for onchain derivatives, structured vaults, or tokenized index products. These indices draw on the same oracle infrastructure used for spot price feeds but apply defined methodologies and basket weights to compute continuous benchmarks, mirroring what index providers have long done in equities and bonds. As more institutions bring their proprietary data onchain, including premium FX and metals feeds, these basket products are likely to proliferate.

Finally, there is a nascent but conceptually distinct category of metal‑adjacent RWAs, such as tokens linked to mining revenue, royalties, or financing vehicles for new extraction projects. While not metal claims per se, these instruments provide exposure to the economics of metal production and can be tokenized much like other private credit or specialty finance assets. They may ultimately intersect with DeFi in similar ways to tokenized Treasuries or reinsurance contracts, but they currently remain niche relative to spot tokenization and synthetic perps.

Tezos backs Metals platform bringing gold, uranium, and rare earth assets onchain, enabling investors to access critical materials driving AI and industrial growth

Gold tokenization is a >$1B solved problem across PAXG, XAUT, and VNXAU - this announcement adds nothing on that leg. xU3O8 is the unusual one: retail has no path to physical uranium, Cameco and Kazatomprom gatekeep spot, and non-proliferation rules make legal title harder to assemble than for precious metals. Trilitech going custody-first matches Paxos's gold playbook, but Paxos never attempted uranium. Rare-earth-for-AI framing is mostly narrative dress - China controls ~60-80% of actual supply, and a token doesn't fix the physical bottleneck.

Readers click metals-in-crypto stories not for yield or DeFi composability — but to validate that the category is real: the two highest-clicked stories are both legitimacy signals (a NASDAQ-parent oracle deal and a state law), while the 'tokenized metals sit unused onchain' story also got heavy traffic, revealing an audience actively stress-testing whether metals tokenization has substance beyond market-cap headlines.↗

Tokenized Metals: Turning Bullion into Bits

How Tokenized Metals Work

Tokenized metals typically follow a “digital twin” model: for each token minted, a corresponding quantity of physical metal is held in custody with a vault or bullion provider. When a user acquires a token—whether on a centralized exchange, via a Web3 interface, or in a DeFi pool—they are effectively acquiring a claim to that underlying metal, subject to the terms set by the issuer. Onchain, the token behaves like any other fungible asset, transferable between wallets and smart contracts, while offchain, the issuer maintains records that link the token supply to specific bars, lots, or pooled holdings.

This linkage is enforced through a combination of contractual arrangements and transparency mechanisms. Many tokenized metal issuers publish regular attestations confirming that the total metal held in custody matches or exceeds the outstanding token supply, sometimes augmented with serial-numbered bar lists or vault audit reports. In some cases, these proofs are brought onchain via oracle networks, allowing smart contracts to check collateralization ratios programmatically. Chainlink, for example, has outlined designs in which secure data feeds can attest to the existence and quantity of vaulted metals backing tokenized assets, reducing reliance on purely offchain trust.

Redemption is a critical component of the model. Some issuers allow token holders to redeem their tokens for physical metal, subject to minimum lot sizes and shipping or fabrication fees, effectively turning the blockchain token into a digital warehouse receipt. Others permit cash redemption at the prevailing spot price, functioning more like an ETF. The existence of a robust redemption mechanism helps keep token prices anchored to the underlying metal, as arbitrageurs can profit whenever the token trades at a premium or discount large enough to justify redemption costs.

Yet tokenized metals also introduce new risk layers compared to directly holding bullion. Token holders must trust that the issuer is solvent, that vault records are accurate, that legal claims would be enforceable in a dispute, and that smart contract controls cannot be abused to freeze or seize tokens. These counterparty and governance risks are structurally different from those in decentralized, collateral‑only protocols like DEXs or lending markets, and they are one reason why many DeFi users remain cautious about integrating tokenized metals deeply into composable financial circuits.

Key Projects and Blockchains

While Ethereum remains the largest base layer for tokenized assets broadly, newer platforms are positioning themselves as specialized homes for RWAs in general and metals in particular. Tezos has emerged as a notable hub through the launch of Metals.io, a web application built by Trilitech, Tezos’ R&D arm, that brings tokenized gold, uranium, and rare earth metals onchain. Metals.io enables users to buy, own, and trade digital representations of these strategic resources, with the aim of making access to critical materials driving AI and industrial growth as seamless as interacting with any other crypto asset. The project started with uranium but has expanded its remit as part of a broader vision for onchain access to real-world metals markets, supported and promoted in the Tezos ecosystem.

In practice, Metals.io functions as a front-end to a set of token contracts and custody arrangements that link Tezos-based tokens to underlying physical assets. By integrating with other Tezos DeFi primitives, such as DEXs and lending platforms, these metal tokens can potentially be swapped, collateralized, or pooled for liquidity in the same way as native Tezos tokens. Trilitech frames this as part of a “Tezos RWA boom,” in which tokenized commodities, including metals, are used to grow onchain activity and attract both crypto-native and traditional investors. The choice of uranium and rare earth metals alongside gold underscores a thesis that metals are not only stores of value but also key inputs into the AI and energy transitions.

Outside Tezos, there is a broader landscape of tokenized metals spanning permissioned and permissionless environments. Several centralized exchanges and custodians issue gold-backed tokens on mainline networks, which can be listed on CEX order books while also being accessible to DeFi users via self-custodial wallets. Institutional-grade custodians such as Anchorage Digital, which provides regulated support for a wide array of crypto assets, are beginning to link their custody frameworks to onchain markets like Hyperliquid, hinting at a future where institutions may hold tokenized RWAs, including metals, in qualified custody while trading them on decentralized venues. As more banks and market infrastructures experiment with tokenization, including government-backed initiatives, the range of custodial models for tokenized metals is likely to broaden.

Market Size and Growth

Tokenized metals sit within the larger universe of tokenized real‑world assets, a segment that has grown from a curiosity to a multi‑billion dollar market in just a few years. According to data compiled by a16z crypto, the total market capitalization of tokenized RWAs surpassed 30 billion dollars recently and has held around 34 billion dollars, excluding stablecoins, after being below 3 billion dollars as recently as mid‑2024. That represents roughly a tenfold expansion in under two years, a pace of growth that is noteworthy even by crypto standards. Though the overall figure is still small compared with global financial markets, it is already comparable to a mid‑sized regional bank or a large university endowment.

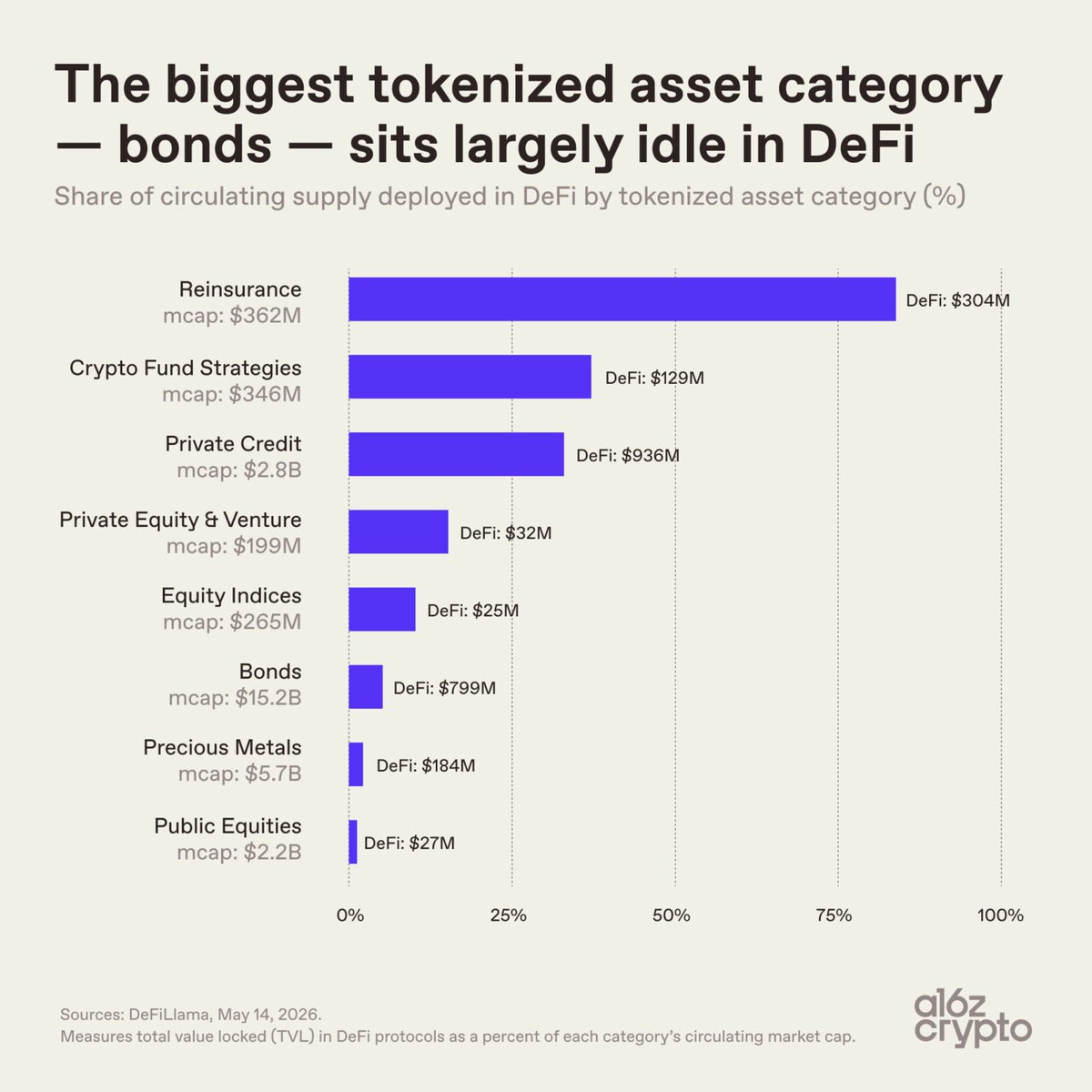

Within this RWA universe, government debt and commodities have been among the fastest to scale. Tokenized U.S. Treasuries and commodities together now account for roughly two‑thirds of the total onchain RWA market, having both reached the one‑billion‑dollar mark in two to three years and then continued to expand. Bonds are by far the largest category, at approximately 15.2 billion dollars in market cap, but commodities—where tokenized metals sit alongside tokenized energy products—are disproportionately important in shaping the public imagination around what tokenization can do. As a long‑established asset class with liquid offchain markets and clear pricing, metals have served as a natural testbed.

Despite this growth, utilization inside DeFi remains modest. Only about five percent of tokenized bonds are actively deployed in DeFi protocols, representing roughly 800 million dollars of supply, while tokenized precious metals exhibit similarly low usage rates. In contrast, specialized assets such as reinsurance tokens, with market caps in the low hundreds of millions, see more than eighty percent of their supply deployed in DeFi, and private credit tokens have utilization rates around one‑third. This divergence suggests that while metals have achieved meaningful scale in terms of tokenized capitalization, their integration into permissionless financial primitives is still at an early stage.

Forward‑looking projections underscore how early the market remains. Major institutions such as McKinsey, ARK Invest, Boston Consulting Group (in partnership with Ripple), and Standard Chartered project that the tokenized assets market could reach between 2 and 30 trillion dollars by the early 2030s, implying growth of more than one hundred times from today’s roughly 30‑billion‑dollar baseline. While these figures cover all RWAs, not just metals, they imply that if tokenized commodities maintain even a modest share of the RWA market, tokenized metals could grow by orders of magnitude. The limiting factors are therefore less about addressable market size and more about legal, operational, and composability constraints that currently keep most tokenized metals in a “buy and hold” mode rather than fully embedded in DeFi.

To make these contrasts more concrete, the following table illustrates how metal-related tokenized assets sit within the broader RWA landscape:

| RWA Category | Approx. Onchain Market Cap | Approx. % Deployed in DeFi | Notes on Metals Linkage |

|---|---|---|---|

| Government Bonds | ≈ 15.2B USD | ≈ 5% | Often paired with tokenized commodities in RWA portfolios |

| Commodities (incl. metals) | ≥ 1B USD and growing | Low, similar to bonds | Includes tokenized gold and other metals |

| Reinsurance Tokens | ≈ 362M USD | ≈ 84% | DeFi‑native structured RWAs, no direct metals exposure |

| Private Credit | Hundreds of millions USD | ≈ 33% | Some potential for mining‑linked deals |

This snapshot highlights that metals are significant enough to matter for tokenization narratives, yet still underutilized relative to their potential as building blocks in composable finance.

Metals Perpetuals and Derivatives Onchain

Perpetual Futures on Gold, Silver and Beyond

Alongside spot tokenization, one of the most active areas for metals in crypto is the rise of perpetual futures referencing metal prices. Perpetuals, or “perps,” are futures contracts without a fixed expiry date; instead, they use a funding rate mechanism to keep the contract price anchored to a reference index over time. In crypto, perps have long been the dominant instrument for trading BTC and ETH with leverage, and the same structure is now being applied to real‑world assets, including metals.

Ostium exemplifies this trend as a decentralized protocol purpose‑built for RWA perps. Rather than trading BTC/USD, users can open long or short positions on XAU/USD (gold), XAG/USD (silver), crude oil benchmarks, major FX pairs, or equity indices, all collateralized and settled in USDC stablecoins. When a trader opens a gold perp on Ostium, the protocol consults a real‑time oracle price feed for gold—linked to the underlying spot market—to determine the entry price, and it continuously marks the position to market as prices move, crediting or debiting the trader’s margin balance accordingly. Positions can remain open indefinitely, subject only to liquidation if the value of collateral falls below maintenance thresholds, making RWA perps functionally similar to crypto perps in user experience.

As of May 2026, Ostium reported offering seventy‑one trading pairs, including a wide range of commodity markets such as gold, silver, U.S. and U.K. crude oil, copper, platinum, and palladium, as well as major FX pairs, global equity indices, U.S. single stocks, and several ETFs, including a uranium-focused fund. This breadth effectively turns Ostium into an onchain multi‑asset derivatives venue, where metals coexist with macro assets under a unified margin and liquidation engine. For metals traders, this opens possibilities that would be difficult to replicate in traditional broker accounts, such as cross‑margining long gold against short equity index positions, or using crypto collateral to trade industrial metals around the clock.

Centralized exchanges have moved in parallel. Coinbase, for example, has highlighted that trading volume across its stock and metals perpetuals exceeded 1.5 billion dollars within just two months of launch, despite these being relatively new product lines. Coinbase’s marketing also emphasizes the contrast between traditional markets—open only around 30 percent of the week—and crypto perps, which are available 24/7, enabling continuous exposure management and speculation. This positioning suggests that metals perps are not just a niche add‑on but part of a broader push by centralized crypto venues to become “always-on” gateways to real-world markets.

Other derivatives platforms, such as GMX and Hyperliquid, have also added metals futures and are experimenting with institutional partnerships. GMX has noted that gold and silver trade continuously across global futures and OTC markets, implying that traders in these assets are less exposed to overnight gap risk than in assets with more limited trading hours, though onchain liquidity can still be a constraint. Hyperliquid’s HIP‑3 markets, initially focused on perpetuals for various assets, have generated more than 200 billion dollars in cumulative volume since launching in late 2025, with institutional-grade custody via Anchorage Digital helping to attract professional traders. While tokenized equities and crypto still dominate volumes, metals are an important component in diversifying product suites and establishing RWA credentials.

Indices, Oracles and 24/7 Pricing

The expansion of metals derivatives onchain depends critically on high-quality, continuous price data. Unlike purely onchain assets, where prices are determined by DEX order books or AMM curves, metals and other RWAs require oracles to bring offchain market data into smart contracts. Two broad trends stand out: the rise of specialized RWA indices and the involvement of major market data providers in onchain oracle networks.

Pyth Network has been a central actor in this shift. Initially known for crypto price feeds, Pyth has moved toward an “always-on market data platform” that can provide real-time pricing across U.S. equities, oil, metals, and thematic baskets, with indices constructed from its underlying price feeds. Pyth Indices are proprietary 24/7 products with defined baskets and methodologies, including specific indices for gold and silver that run continuously rather than being limited to exchange hours. These indices are co-developed with established index providers such as MarketVector, a VanEck company, marrying traditional index expertise with onchain delivery mechanisms.

The availability of such indices has tangible implications. Perps, prediction markets, and tokenized asset protocols can reference a Pyth metal index rather than a single exchange price, reducing susceptibility to idiosyncratic venue disruptions and smoothing intraday volatility. Moreover, having continuous indices that do not “sleep” on weekends aligns with the operational reality of crypto markets, where traders expect to adjust positions at any time. Euronext FX’s decision to deliver premium FX and metals data through the Pyth marketplace, as highlighted in recent coverage, illustrates how established trading venues view onchain distribution as a new channel for monetizing their data and reaching DeFi protocols.

Chainlink is pursuing a complementary path from the perspective of enterprise integrations. Beyond providing crypto price feeds, Chainlink has emphasized the role of its oracle network in attesting to and pricing tokenized metals, and NYSE‑parent Intercontinental Exchange (ICE) has tapped Chainlink to bring forex and precious metals data onchain. By doing so, ICE is effectively exporting parts of its data infrastructure into the Web3 ecosystem, enabling DeFi protocols, tokenized asset platforms, and even traditional institutions experimenting with blockchains to rely on regulated market data rather than ad hoc scrapes or low-quality feeds.

Together, these developments signal a convergence between commodities market data and DeFi’s programmable environment. Oracles transform metals from assets whose price is discovered exclusively in specialist venues into building blocks that can be referenced by any smart contract, whether for perps, collateral valuation, automated asset management, or structured payoff products. The challenge, as always in oracle design, is to maintain security, resilience, and economic incentives that minimize manipulation, particularly in less liquid or more opaque metals markets.

Liquidity, Leverage and Risk

Metals perps offer powerful tools, but they also introduce distinctive risk profiles for traders and protocols. One dimension is liquidity fragmentation. While the underlying gold and silver markets are deep and trade nearly continuously across global futures exchanges and OTC desks, onchain liquidity is often far thinner. A large order in a DEX-based gold perp could move its price significantly relative to the reference index, triggering liquidations or anomalous funding rates, especially in times of stress. Centralized venues like Coinbase mitigate this with internal market-making and cross-venue hedging, but DeFi protocols must rely on incentive structures and risk controls.

A second dimension is leverage and funding risk. Because perps are marginally collateralized, sudden moves in the underlying metal price can lead to rapid cascades of liquidations, particularly during events like the recent episode in which gold suffered its worst two-day decline in over a decade, wiping out approximately 2.5 trillion dollars in market value, or about eight percent over two sessions. In that instance, analysts attributed the crash to a mix of profit-taking after a lengthy rally, overheated sentiment, and overextended positioning, with the magnitude of the move being statistically rare for a mature asset. For onchain perps, such tail events stress liquidation engines and oracle systems; if funding rates flip sharply or oracles lag, traders can experience larger-than-expected losses.

There is also basis and weekend risk. Even though gold and silver trade nearly around the clock across venues, not all markets observe the same hours or liquidity profiles. Crypto perps trade 24/7, including weekends and public holidays when some traditional venues are closed or thin. When onchain markets move in response to crypto-wide sentiment during these periods, they can diverge from the eventual Monday opening levels of futures or spot markets, leading to basis gaps that must be arbitraged once traditional markets reopen. Traders who understand these dynamics can exploit them, but protocols must design funding rate mechanisms and circuit breakers that will behave robustly in such circumstances.

On the institutional side, products like Hyperliquid’s HIP-3 suite, supported by Anchorage Digital’s institutional custody, are beginning to bridge the gap between professional trading standards and onchain derivatives. By combining regulated custody, KYC processes, and high-throughput decentralized execution, such platforms aim to make metals and other RWA perps acceptable to proprietary trading firms and hedge funds that would previously have limited themselves to CME or OTC swaps for commodity exposure. Their growth, however, also intensifies competition for liquidity between centralized and decentralized venues, and between perps and spot tokenized metals, which may vie for the same pool of capital.

- 01TradFi oracle rails for metals↗

ICE parent backing Chainlink for forex and metals data onchain was the single highest-clicked story, signaling readers treat institutional data infrastructure as the credibility gate for the whole metals-tokenization thesis.

- 02State and sovereign endorsement↗

New Hampshire's law permitting state-level investment in crypto and precious metals and Hong Kong's multi-round tokenized bond program with explicit metals expansion plans read as green lights from real governments, not just DeFi natives.

- 03New perpetuals venues for metals↗

Ostium's palladium and platinum listings and Hyperliquid's HIP-3 crossing $2B open interest show readers tracking where actual price-discovery liquidity is forming for metals, not just custody.

- 04Exotic and strategic metals onchain↗

The Tezos-backed Metals.io pitch — uranium and rare earths alongside gold — tapped a distinct angle: AI and industrial demand, not just store-of-value, as the demand driver for tokenized commodity access.

- 05Tokenized metals DeFi utilization gap↗

The a16z-sourced finding that bonds and metals have large tokenized market caps but almost no DeFi activity attracted clicks precisely because it punctures the hype with data on actual usage.

- 06Gold crash Bitcoin rotation thesis↗

Gold's worst single-day drop in four decades coinciding with Bitcoin holding above $82K gave the BTC-as-digital-gold narrative a live test case readers wanted to examine.

Institutional and Regulatory Shifts Around Onchain Metals

Governments Experiment with Tokenized Metals

One of the most notable aspects of the metals‑onchain story is that it does not belong solely to crypto natives; governments and regulators are increasingly experimenting with tokenized instruments that include metals or pave the way for them. Hong Kong offers a prominent example. Authorities there have issued tokenized green bonds twice, in 2023 and 2025, and are preparing a third batch that will be structured as regular, recurring tokenized government bond offerings. As part of this push, Hong Kong has announced its intention to exempt stamp duty on transfers of tokenized ETFs and to promote tokenization in sectors such as precious metals, non-ferrous metals, and even solar panels. This signals a view of tokenization not merely as a novelty but as an infrastructure upgrade for capital markets.

If implemented at scale, such policies could turn Hong Kong into a regional hub for tokenized metals. Exempting stamp duty on tokenized ETF transfers could make onchain vehicles more cost-effective than their traditional, paper-based counterparts, particularly for high-frequency traders or market makers. Encouraging tokenization of precious and base metals also aligns with Hong Kong’s historic role as a gateway between global commodity markets and Chinese demand, suggesting that future onchain metals products could be tailored for both international and mainland investors. For crypto protocols, this creates opportunities to interface with regulated tokenized products through compliant wrappers or cross‑listing arrangements.

In the United States, regulatory dynamics are more fragmented, yet state-level experiments provide early signals. New Hampshire, for example, has passed a law explicitly allowing the state to invest in cryptocurrency and precious metals, as highlighted by Governor Kelly Ayotte. While this law is primarily about treasury investment policy rather than tokenization per se, it reflects a willingness by public entities to treat both crypto and metals as legitimate components of a diversified asset base. Should such states later embrace tokenized metals, they might hold onchain gold or silver as part of their reserves, setting a precedent for public sector adoption.

These governmental moves intersect with private sector innovation. In jurisdictions that explicitly recognize tokenized securities or commodities, issuers of metal-backed tokens can more confidently structure instruments that satisfy regulatory requirements while remaining composable with DeFi. Conversely, in areas without clear guidance, projects may adopt geofencing, permissioned access, or whitelisting to avoid regulatory risk, limiting the global fungibility of metal tokens. For crypto users, understanding this patchwork is important, as it shapes which instruments are available where and under what conditions.

Market Data Giants Move Onchain

Another axis of institutionalization is the participation of large market data providers in onchain ecosystems. As noted earlier, ICE has engaged Chainlink to deliver regulated FX and precious metals data into Web3 contexts, while Euronext’s FX business has partnered with Pyth to supply premium FX and metals data to the Pyth marketplace. These moves blur the lines between “crypto-native” and “TradFi-native” data sources, as the same ticker feeds used by banks and asset managers become accessible to smart contracts.

For metals, this is particularly significant because reliable price discovery has historically depended on centralized venues, such as the London Bullion Market Association’s auctions or futures exchanges like COMEX. When those venues’ prices are streamed onchain through robust oracle networks, they become reference points not only for derivatives but also for the collateral valuation of tokenized metals, automated margining, and even decentralized credit scoring. A lending protocol could, for example, accept tokenized gold as collateral, using a Chainlink or Pyth price feed to compute loan‑to‑value ratios and margin calls in real time, thereby integrating metals into a broader onchain credit system.

The involvement of these data giants also has governance ramifications. It raises questions about who controls index methodologies, how updates are managed, what happens if offchain benchmarks change, and how disputes or outages are handled. In the long run, governance frameworks that recognize both the onchain DAO-like aspects of protocols and the contractual obligations of traditional data vendors will be necessary to ensure that metal-linked products remain reliable and legally sound. For now, the trend is incremental but clear: onchain metals are increasingly priced and benchmarked using the same data that underpins institutional markets.

Custody, Compliance and Institutional Access

Institutional participation in onchain metals hinges not only on data quality but also on custody and compliance. Anchorage Digital’s role as the institutional home for Hyperliquid illustrates how regulated custodians can serve as bridges between traditional institutions and decentralized markets. Since its launch, Hyperliquid’s HIP‑3 markets have generated over 200 billion dollars in cumulative volume, and Anchorage provides custody for the assets that institutions trade there, mitigating operational risks that would otherwise deter participation. While these volumes span multiple asset classes, metals perps constitute part of the product mix that draws professional traders.

For tokenized metals, the custody question is two‑layered: custodians must manage both the physical metal and the digital representation. Some issuers rely on established bullion banks or specialized vaulting firms for the physical layer, while partnering with digital custodians for the token layer. In a regulatory context, these arrangements must satisfy both commodity custody standards and crypto asset safeguarding requirements, which can vary by jurisdiction. Institutions subject to strict rules may prefer tokenized metals that are held in segregated accounts with recognized custodians and that fit within existing regulatory buckets, such as “collective investment schemes” or “digital securities.”

Compliance concerns extend to KYC/AML and market conduct. Tokenized metals that are freely transferable between pseudonymous addresses pose challenges for sanctions screening and anti-money-laundering obligations. As a result, some projects adopt permissioned architectures where only whitelisted entities can hold or transfer tokens, or they implement transfer restrictions at the smart contract level. Others rely on onchain analytics and monitoring to identify suspicious patterns. From an institutional perspective, having clear procedures and compliance tooling around tokenized metals is a precondition for adoption.

Ultimately, the institutionalization of onchain metals is not a binary switch but a gradient. At one end are fully permissionless, DeFi-centric products that maximize composability and global access; at the other are tightly controlled, institutional vehicles that happen to use blockchain for settlement but otherwise resemble traditional notes or funds. Metals as an asset class are likely to see offerings along the entire spectrum, and the balance between them will shape how deeply metals integrate into the broader crypto ecosystem.

Hyperliquid HIP-3 surpasses $2B in open interest as tokenized equities displace metals

Hyperliquid's permissionless HIP-3 futures market has blown past $2B in open interest — up roughly 190% from March and 800% year-to-date. Oil perpetuals still anchor the platform with Brent and WTI combining for over $1.1B, but tokenized equities like the S&P 500 and XYZ100 have added $500M and are now displacing precious metals as the second-largest asset class on the venue. Six of Hyperliquid's ten most active markets are RWA-linked, pulling around $3B in daily volume — about a third of all DEX volume. The 24/7 angle is the real draw: HIP-3 offers continuous price discovery for stocks and commodities while TradFi sleeps through weekends.

Metals versus Crypto: Safe Havens, Correlation and Rotation

Precious Metals as Traditional Safe Havens

Gold and silver have long been regarded as safe‑haven assets, sought out in times of macroeconomic turbulence, inflation fears, or geopolitical tension. Their appeal stems from a combination of physical scarcity, long historical track records as money or monetary anchors, and deep, globally integrated markets. When investors question the stability of fiat currencies or the solvency of financial intermediaries, allocating to gold is a well‑worn response, often executed via bullion, ETFs, or futures. This reputation stands in contrast to crypto assets, which are newer, more volatile, and often perceived as speculative technology investments rather than conservative stores of value.

In the context of crypto markets, this contrast has sometimes produced narratives of competition between “digital gold” (usually Bitcoin) and physical gold. Crypto advocates argue that Bitcoin combines scarcity with programmability and resistance to seizure in ways that surpass physical bullion, while critics note that crypto prices have historically been more correlated with risk-on assets like tech stocks than with traditional havens. Recent coverage has highlighted how, during periods of regulatory uncertainty, exchange hacks, or sharp drawdowns, precious metals can outperform crypto, reinforcing their traditional roles as stabilizers in portfolios.

At the same time, tokenization blurs some of these distinctions. When gold is represented as a token on a blockchain, it acquires some of the functional attributes of crypto—instant settlement, global transferability, composability—even as it retains the economic properties of metal. This means that investors can use gold tokens alongside stablecoins and crypto derivatives in their onchain strategies, for example by using tokenized gold as collateral in a lending protocol while maintaining exposure to its price. In this hybrid space, gold is no longer just a traditional safe haven; it becomes a programmable asset that lives in the same transactional layer as crypto.

Gold’s Crash and Bitcoin’s Resilience

The relationship between metals and crypto has been particularly salient during sharp market moves. One vivid example is the recent episode in which gold experienced one of its steepest price declines in modern history, with its market value falling by roughly 2.5 trillion dollars in a single day, amounting to about an eight percent drop over two trading sessions. Analysts cited by market commentary noted that such a move would be expected only once every hundreds of thousands of trading days under normal statistical assumptions, underscoring how extreme it was for an asset of gold’s maturity.

Commentary attributed the crash to a confluence of factors, including profit-taking after a prolonged rally of around sixty percent since 2022, overheated sentiment, and crowded positioning by large investors who had piled into gold as an inflation hedge. When momentum slowed and macro conditions shifted, these investors began to offload positions, triggering cascade effects across futures and ETF markets and leading to an abrupt evaporation of trillions in notional value. The episode served as a reminder that even venerable safe havens are not immune to volatility when positioning and leverage reach extremes.

What made this event particularly interesting from a crypto perspective was that during the same window, Bitcoin held above levels that, while volatile in their own right, suggested relative resilience compared with gold’s sudden slide. This fueled a thesis in some quarters that capital might rotate from crowded gold trades into Bitcoin as macro liquidity conditions improved, treating Bitcoin as an alternative or complement to physical gold for those seeking non‑sovereign stores of value. Whether such rotation materializes in a sustained way is an open question, but the juxtaposition complicates simplistic narratives about metals always being safer and crypto always being riskier.

For onchain metals products, episodes like this present both risks and opportunities. On the risk side, extreme gold moves can stress tokenization and derivatives infrastructures, as discussed earlier, especially if vault operations, redemption windows, or oracle feeds are disrupted. On the opportunity side, sharp dislocations can drive demand for 24/7 trading venues where investors can reposition outside of traditional market hours. Perps on Coinbase, GMX, Ostium, and similar platforms, as well as tokenized metals on Tezos or Ethereum, provide channels through which investors can adjust metal exposure dynamically in response to macro events or reallocate between metals and crypto.

Co-movement, Diversification and Portfolio Construction

Beyond specific episodes, the broader question for investors is how metals and crypto co‑move and what this implies for diversification. Historically, gold has exhibited low or negative correlation with equities in stressed environments, though correlations can vary over time depending on the macro regime. Crypto, particularly Bitcoin, has at times correlated with risk assets like technology stocks—especially during periods of abundant liquidity—but has also shown unique behavior around halving cycles or regulatory developments. The rise of tokenized metals and metal perps does not change these underlying economic drivers, but it makes it easier to express views and construct portfolios at higher frequency.

In an onchain context, investors can create portfolios that combine stablecoins, tokenized bonds, tokenized metals, and crypto assets within a single wallet, using DeFi protocols to manage leverage and yield. For example, a user might hold tokenized Treasuries and gold tokens for defensive exposure, while employing a modest amount of leverage via metals perps or crypto perps to implement tactical trades. Automated strategies could dynamically adjust allocations based on realized volatility, funding rates, or oracle‑derived signals, exploiting differences in how metals and crypto respond to macro data releases or policy announcements.

These possibilities illustrate why composability is such a recurring theme in discussions of tokenized metals. The full promise of onchain metals is not merely that they exist as static tokens or tradeable perps, but that they can be woven into multi‑asset strategies that exploit their differing risk-return characteristics. Achieving this in practice, however, requires solving the utilization and integration challenges described next.

Hong Kong issues first tokenized green bond

Gold's worst single-day crash in 40+ years; Bitcoin holds ~$82K

New Hampshire signs law permitting state investment in crypto and precious metals

Ostium lists palladium (XPD) and platinum (XPT) perpetuals

Hong Kong issues second tokenized green bond; plans metals tokenization expansion

Pyth launches 24/7 index feeds covering metals, oil, and US equities

Tezos backs Metals.io launch with gold, uranium, and rare earth tokenization

ICE parent (NYSE) taps Chainlink to bring forex and precious metals data onchain

Metals Powering the Physical World and the AI Economy

Uranium, Rare Earths and Strategic Metals

While gold and silver dominate the popular imagination, a significant part of the onchain metals story revolves around strategic and industrial metals—materials whose value is tied less to safe‑haven narratives and more to their essential roles in modern technology, energy systems, and defense. Uranium, for instance, underpins nuclear power generation, which is experiencing renewed interest as governments seek low‑carbon baseload energy sources. Rare earth elements meanwhile are critical for high-performance magnets, batteries, and various components in electronics and renewable energy infrastructure.

Metals.io’s decision to focus on uranium and rare earths alongside gold reflects this shift in emphasis. Rather than simply reproducing traditional bullion products, Metals.io positions itself as a gateway to the materials that drive AI, data centers, electric vehicles, and industrial automation. For crypto investors, exposure to such metals can be a way to play macro themes around electrification and digital infrastructure without directly holding equities in mining companies or industrial firms. The onchain format further allows these exposures to be integrated into DeFi strategies, used as collateral, or traded against crypto assets, creating a bridge between digital growth narratives and physical resource constraints.

From a regulatory and operational standpoint, tokenizing strategic metals can be more complex than tokenizing gold. Supply chains may involve multiple jurisdictions, export controls, and specialized storage or handling requirements. Nonetheless, the economic incentives are strong: many of these metals have historically been difficult for ordinary investors to access directly, with exposure limited to specialist funds or equity proxies. Tokenization promises to democratize access while providing new liquidity channels for producers and intermediaries.

From Railroads to Data Centers: Industrial Demand

Metals are also central to the physical infrastructure of the economy, from railroad tracks and bridges to power grids and semiconductor fabrication plants. A recent conversation about the AI and innovation transformation of a 200‑year‑old railroad company, for example, highlighted how industrial firms are using AI and machine vision to modernize train inspections, with sophisticated algorithms analyzing high-resolution images of trains traveling at speed to detect defects in real time. While this discussion was not directly about metals, it underscores the broader context: heavy industries built on steel, copper, and other metals are themselves becoming data-intensive and digitally managed.

As AI workloads proliferate in data centers and as electrification expands in transport and industry, demand for certain metals such as copper, lithium, cobalt, and rare earths is expected to remain structurally robust. For crypto markets, this matters because tokenized metals and metal derivatives offer a way to express views on these macro trends without leaving the onchain environment. Investors who are bullish on the AI “picks and shovels” trade can allocate to tokenized uranium or rare earths via platforms like Metals.io, while managing macro hedges or cross‑asset exposure using DeFi tools.

The convergence of industrial demand and digital trading infrastructure also suggests longer‑term possibilities. In principle, a mining company could issue tokenized claims on future metal production, using onchain markets to pre‑sell output or raise working capital, with repayments linked to realized production or price performance. Such arrangements would treat metals not merely as static collateral but as part of dynamic financing ecosystems, potentially improving capital access for producers while giving investors more granular exposure. Although these models remain largely experimental, the underlying idea aligns with trends in tokenized private credit and specialty finance.

Why Crypto Investors Care About Industrial Commodities

For crypto investors, industrial metals can serve several roles. They can be macro hedges against inflation and supply shocks, thematic plays on AI and green energy transitions, or simply diversifying assets whose price dynamics differ from those of cryptocurrencies. Tokenized metals allow these roles to be filled within the same operational environment as crypto trading, avoiding the frictions of moving capital between brokerages, banks, and exchanges.

Furthermore, the risk profile of industrial metals is distinct from that of Bitcoin or Ethereum. Metals prices are influenced by global growth, technological change, regulatory shifts (for example around nuclear power or environmental standards), and geopolitics. Crypto prices, while increasingly tied to macro liquidity and institutional flows, are also driven by idiosyncratic factors such as protocol upgrades, regulatory enforcement actions, and speculative cycles. Combining the two can mitigate some risks while introducing others, making thoughtful risk management essential.

Crypto’s ethos of open access and programmability resonates with the need to allocate capital to critical infrastructure and resources. If tokenized metals and related RWAs can be structured in ways that are transparent, secure, and compliant, they could enable new forms of participation in the physical economy, from retail investors funding small‑scale mining projects to DAOs hedging their treasury exposures with strategic metals. The key is ensuring that the abstractions created by tokenization remain tied to real economic activity rather than drifting into purely speculative instruments detached from the underlying metals.

DeFi and Composability: Why Most Tokenized Metals Still Sit Idle

Utilization Gaps between Metals and DeFi-Native RWAs

Despite the conceptual appeal of metals as DeFi collateral or portfolio components, the reality is that most tokenized metals—and tokenized RWAs more broadly—are not yet deeply integrated into composable finance. As noted earlier, only about five percent of tokenized bond supply is currently used inside DeFi protocols, with precious metals exhibiting similar underutilization. In contrast, reinsurance tokens, which represent specialized financial contracts rather than widely held sovereign instruments, have about eighty‑four percent of their supply deployed in DeFi, and private credit tokens see about one‑third utilization.

Several reasons help explain this discrepancy. First, many tokenized metals are issued under legal structures that limit their transferability or restrict their use in permissionless protocols, either to comply with securities regulations or to satisfy the risk appetites of issuers and custodians. These constraints can make it difficult for DeFi protocols to integrate metal tokens trustlessly, as they must handle potential blacklisting, transfer restrictions, or freeze functions that are at odds with fully decentralized designs.

Second, there is a path dependence in DeFi composability: early collateral types such as ETH, wrapped BTC, and stablecoins became standards around which protocols were built, while newer RWAs, including metals, arrived later and must overcome established conventions. Lending protocols, for example, may be reluctant to add exotic collateral types without long historical data, particularly if they fear that liquidations would be difficult during stress. Metals are liquid in traditional markets, but onchain markets may not yet offer sufficient depth or arbitrage capacity to guarantee robust liquidation.

Third, there is the issue of user demand. Many crypto participants still approach DeFi primarily as a way to lever up on crypto-native assets or to earn yield on stablecoins. Metals, by contrast, are more commonly used by macro investors, commodity traders, or wealth managers, groups that are only gradually entering DeFi. Until these constituencies become more comfortable with onchain workflows, demand for using tokenized metals as composable building blocks rather than mere buy-and-hold instruments may remain limited.

What True Composability Could Look Like

If these barriers are addressed, tokenized metals could occupy diverse roles within DeFi architectures. In lending markets, for instance, tokenized gold could serve as a relatively low‑volatility collateral asset, sitting between stablecoins and crypto in the risk spectrum. Borrowers might post tokenized gold to obtain stablecoins or leverage their exposure to metals, while lenders would gain exposure to the metal’s price and yield from interest payments. Automated rebalancing strategies could adjust loan‑to‑value ratios based on volatility and correlation measures, making metals integral to dynamic risk management.

In decentralized exchanges, metals could form part of multi‑asset liquidity pools that provide cross‑asset exposure and fee income. A pool comprising stablecoins, tokenized Treasuries, and tokenized gold, for example, could approximate a conservative portfolio while still earning trading fees from rebalancing. Structured products, such as vaults that sell covered calls on tokenized gold or implement volatility harvesting strategies on gold perps, could offer yield‑enhancing alternatives to traditional metal ETFs, with transparent, auditable logic onchain.

More ambitiously, metals could be embedded in DAO treasury management frameworks. DAOs with long time horizons might allocate a share of their reserves to tokenized metals as a hedge against crypto drawdowns, with governance policies specifying target allocations and rebalancing rules. Smart contracts could automatically rebalance between crypto, stablecoins, and metals based on pre‑agreed triggers, reducing the need for ad hoc human intervention during crises. Such designs would operationalize long‑standing debates about diversification and risk management in decentralized organizations.

Building the Plumbing: Oracles, Bridges and Legal Wrappers

Realizing these possibilities requires robust infrastructure across several layers. On the oracle side, protocols such as Chainlink and Pyth must continue to expand and secure their metals price feeds, ensuring low latency, high reliability, and resistance to manipulation. This includes drawing from multiple exchanges and OTC venues, implementing aggregation logic, and establishing economic incentives for data providers that align with DeFi’s security needs. For metal tokens that rely on proofs of reserve or vault attestations, oracles may also play roles in verifying physical holdings, allowing DeFi protocols to monitor collateralization status in near real time.

Bridging is another key challenge. As tokenized metals proliferate across multiple chains—Ethereum, Tezos, L2s, and appchains—users and protocols must be able to move exposure across ecosystems without introducing undue risk. Native issuance on multiple chains, canonical bridges controlled by issuers, or third‑party cross‑chain messaging frameworks are all being explored, each with different trust models. Failures or hacks in bridges have been among the most costly incidents in DeFi history, so designing secure pathways for metal tokens is crucial to avoid undermining confidence in tokenized RWAs more broadly.

Finally, legal wrappers must evolve to reconcile onchain composability with offchain regulation. Tokenized metals may be structured as warehouse receipts, investment fund units, structured notes, or bespoke contractual rights, each with distinct legal implications. For DeFi protocols integrating these tokens, understanding the legal nature of the underlying claims is important, as it affects bankruptcy risk, regulatory treatment, and the ability to enforce rights in court. Standardization efforts, whether driven by industry consortia, regulators, or major custodians, could help create interoperable frameworks that make it easier for DeFi to incorporate metal tokens consistently.

Pyth launches 24/7 indices for US stocks, oil and metals, enabling round-the-clock trading across perps, prediction markets and tokenized assets

Over 125 first-party publishers plus MarketVector governance matters for mark-price risk: an oil perp at 3am Sunday cannot lean on its own venue book without inviting reflexive liquidation wicks. Coinbase using AI10, Defense10, China10 and Tech100 while Kraken, dYdX and Nado plug into the oil index pushes Pyth closer to CME CF-style benchmark plumbing than a generic oracle feed. If these references become collateral and settlement inputs, weekend TradFi gaps start hitting DeFi risk engines before Monday’s cash open.

Tokenized metals pricing depends entirely on oracle feeds (Chainlink, Pyth); a manipulated price feed can trigger mass liquidations on metals perps without any underlying custody failure.

Physical metal backing requires trusted custodians — unlike crypto-native collateral, there is no on-chain proof of reserve that cannot be faked at the auditor layer, making the entire category dependent on off-chain institutional trust.

The a16z RWA dataset shows metals have among the largest tokenized market caps but among the lowest on-chain DeFi utilization rates, meaning exit liquidity in a stress event is shallow relative to headline TVL.

U.S. state-level signals (New Hampshire) and Hong Kong's bond programs are positive, but no federal U.S. framework exists for tokenized commodity securities, leaving custody and transfer rules ambiguous for institutional participants.

Gold's sharp single-day selloff demonstrated that tokenized metals inherit macro-commodity volatility in full; perpetuals on metals amplify this with leverage, and thin on-chain order books can gap far worse than the spot market.

- Counterparty / legalMedium

The XRP-precious-metals theft lawsuit illustrates that off-chain claims over metals held alongside crypto create contested legal ownership that blockchain provenance alone cannot resolve.

Case Study: Metals.io, Tezos and the RWA Boom

Trilitech and Tezos’s RWA Strategy

Metals.io provides a concrete example of how a particular blockchain ecosystem is approaching tokenized metals as part of a broader RWA strategy. Developed by Trilitech, the London-based R&D hub for Tezos, Metals.io is positioned as a platform for buying, owning, and trading tokenized gold, uranium, and rare earth metals. Rather than targeting only gold, the project explicitly emphasizes “critical metals” that are central to AI, clean energy, and advanced manufacturing, aligning its narrative with secular macro themes. This emphasis was highlighted at TezDev, the ecosystem’s flagship conference, where the platform was framed as a way to bring gold and strategic metals into a modern, 24/7, accessible market built on Tezos.

From Tezos’s perspective, Metals.io serves several strategic purposes. It showcases the chain’s capabilities for asset tokenization, including smart contract features, formal verification tools, and potentially lower transaction costs relative to congested L1s. It also creates a new class of assets that can plug into Tezos-native DeFi protocols, attracting users and liquidity. Moreover, by focusing on tokenized commodities rather than purely speculative tokens, the Tezos community can position itself in policy conversations about the productive uses of blockchains in capital markets, potentially appealing to regulators and institutions.

Trilitech’s involvement underscores the importance of dedicated development organizations in driving RWA adoption. Whereas tokenized metals on Ethereum may be issued by third-party custodians with loose ties to the underlying protocol community, Metals.io is deeply integrated into Tezos’s roadmap and narrative. This alignment can be advantageous for coordination, standard setting, and cross‑protocol integration, although it also concentrates influence over how metals are represented and used on the chain.

User Experience and Market Design

Though detailed technical documentation is still evolving, Metals.io appears designed to abstract much of the complexity of tokenized asset operations away from end users. Through a web interface, users can deposit fiat or stablecoins, acquire metal tokens representing specific quantities of gold, uranium, or rare earths, and manage their holdings within a unified dashboard. Onchain, these tokens conform to Tezos token standards, enabling them to be transferred, traded on DEXs, or integrated into other dApps as those opportunities arise.

Market design choices for platforms like Metals.io involve trade‑offs between liquidity, price discovery, and regulatory constraints. One question is whether prices are set primarily by onchain order books, AMM curves, or offchain RFQ systems integrated with professional market makers. Another is how redemption works: can users redeem tokens for physical metal, cash, or only trade them for other onchain assets? The platform’s positioning around critical metals suggests that physical redemption may be more complex than for gold, given the specialized storage and regulatory requirements for uranium and some rare earths, which may push the design toward cash-settled redemptions or secondary market liquidity rather than widespread physical delivery.

Tezos’s broader RWA push, combined with Metals.io, also raises interesting possibilities around cross‑asset integration. For instance, a Tezos-based lending protocol might accept Metals.io tokens as collateral, or a DEX might list trading pairs between tokenized metals and stablecoins, enabling organic price discovery. Over time, structured products could emerge on Tezos that reference metals prices, such as vaults that generate yield by selling options on tokenized gold or diversified baskets combining metals with other RWAs. The key determinant of whether these emerge will be user demand and the willingness of developers to navigate legal and operational complexities.

Competition and Differentiation

Metals.io does not operate in a vacuum; it competes for attention and liquidity with tokenized metals on other chains, metals perps on DEXs like Ostium and GMX, and centralized offerings from exchanges such as Coinbase. Each of these has different strengths. Spot tokenization platforms provide direct ownership claims and appeal to long‑term holders, while perps cater to short‑term traders seeking leverage and hedging tools. Centralized exchanges offer deep liquidity and fiat onramps but may constrain composability, while DeFi protocols offer permissionless access but must overcome liquidity and UX hurdles.

Tezos’s bet is that a tightly integrated, RWA‑friendly ecosystem can carve out a differentiated niche where tokenized metals are not just financial curiosities but part of a broader industrial and macro narrative. This differentiation may hinge on factors such as transaction costs, regulatory clarity in jurisdictions where Tezos is particularly active, and the success of complementary RWA projects that share infrastructure or user bases. Ultimately, the metals segment of the Tezos ecosystem will live or die by its ability to attract sustained usage, not just initial launch hype.

Risks, Challenges and Open Questions

Counterparty and Custody Risk

Tokenized metals bring with them an inherent layer of counterparty risk that is distinct from, say, holding native crypto assets like ETH or BTC. Holders must trust that the issuer maintains sufficient physical metal in secure storage, that audits and attestations are accurate, and that in the event of insolvency or legal disputes, token holders’ claims would be honored in line with expectations. For gold, where vaulting and custody practices are well-established, these risks may be manageable, but for more specialized metals, the custody chain could involve multiple intermediaries and regulatory regimes.

Even for gold, history offers examples of mismanagement or mismatches between claims and underlying assets in traditional bullion banking. Tokenization does not magically eliminate such risks; it simply wraps them in a new technical interface. For DeFi protocols that might consider metal tokens as collateral, these counterparty exposures are hard to quantify, especially if legal documentation is complex or jurisdiction-specific. There is thus a tension between the desire for permissionless, trust-minimized systems and the reality that tokenized RWAs inherently reintroduce offchain trust.

Market Microstructure and Liquidity Fragmentation

Another set of challenges revolves around market microstructure. Onchain metals trade across a patchwork of centralized and decentralized venues, each with its own liquidity pools, order book depth, and pricing conventions. Perps on Coinbase or Hyperliquid may have relatively deep liquidity and tight spreads, whereas a small DEX on a more niche chain might exhibit large slippage even for modest orders. Arbitrage between these venues, and between onchain and offchain markets, is possible but requires capital, speed, and operational sophistication.

This fragmentation can lead to inconsistent pricing and episodic dislocations, particularly during stress events or outside traditional trading hours. For protocol designers, the question is how to construct robust systems that can withstand such fragmentation. Should lending protocols apply higher haircuts to metal collateral? Should perps implement dynamic funding rate caps tied to realized basis? How should oracle designers handle outliers or venue outages in their price aggregation? These are research and engineering questions as much as market ones.

Legal, Tax and Regulatory Uncertainty

Legal and regulatory frameworks for tokenized metals are still evolving. In some jurisdictions, a tokenized metal claim might be treated similarly to a warehouse receipt or ETF share; in others, it might fall into uncharted territory, potentially triggering securities regulation, commodity regulation, or both. Tax treatment is also a concern: investors must understand whether gains on tokenized metals are taxed like gains on physical metals, like securities, or in some hybrid manner, and whether the location of the vault or issuing entity affects this.

For DeFi protocols, these uncertainties manifest as jurisdictional risk. Developers and DAO participants may face regulatory scrutiny if authorities view certain tokenized metal activities as unauthorized investment products or as offering unregistered securities or derivatives. Cross‑border issues complicate matters further: a protocol accessible globally may have users in dozens of jurisdictions with conflicting rules. While some of these challenges are generic to RWAs, metals add specific wrinkles around export controls, sanctions, and trade regulations, especially for strategic materials.

Open questions remain about the extent to which tokenized metals will be integrated into regulated financial market infrastructures. Will central securities depositories or commodity clearinghouses adopt blockchain rails for settlement? Will regulators mandate particular standards for metal token custody, auditing, and disclosure? How will cross‑listing between onchain and offchain venues be handled? The answers will shape the contours of the metals‑onchain landscape for years to come.

Outlook

Metals occupy a distinctive intersection between the physical and digital economies, and their emerging presence on blockchains highlights both the promise and the complexity of tokenizing real‑world assets. In the near term, growth is likely to continue along two main vectors. First, spot tokenization of gold and other metals will expand as more issuers and custodians experiment with digital twins, particularly in jurisdictions like Hong Kong that actively promote tokenized markets and in ecosystems like Tezos that prioritize RWAs. Second, derivatives platforms—both centralized and decentralized—will keep broadening their catalogues of metals perps and index products, fueled by 24/7 oracle data from networks such as Pyth and Chainlink.

Yet the full potential of onchain metals will only be realized if they move beyond being passive tokens that largely sit in wallets or exchange accounts. Integrating metals into DeFi’s composable architecture—as collateral, as components of structured products, and as elements of diversified onchain portfolios—will require advances in legal structuring, oracle security, liquidity provisioning, and risk management. It will also depend on the gradual convergence of traditional commodity market participants, regulators, and crypto-native builders around standards that balance innovation with investor protection.

For crypto news audiences, metals represent an important lens on the broader tokenization narrative. They invite questions about how blockchains can interface with centuries-old markets, about whether “digital gold” will coexist or compete with gold onchain, and about how AI, electrification, and industrial policy will shape demand for strategic metals that may themselves be tokenized. As infrastructure matures and experiments like Metals.io, Ostium’s RWA perps, and institutional partnerships with oracles and custodians evolve, metals are likely to become a more familiar and integral part of the crypto market conversation—sometimes as hedges, sometimes as speculative vehicles, and increasingly as programmable building blocks in a global, 24/7 financial system.

Latest Metals news

Tezos backs Metals platform bringing gold, uranium, and rare earth assets onchain, enabling investors to access critical materials driving AI and industrial growthHyperliquid HIP-3 surpasses $2B in open interest as tokenized equities displace metalsPyth launches 24/7 indices for US stocks, oil and metals, enabling round-the-clock trading across perps, prediction markets and tokenized assetsMost tokenized RWAs just sit onchain: bonds and metals have huge tokenized caps but minimal DeFi use, while DeFi-native assets like reinsurance and private credit see far higher onchain utilization.Gold suffered its worst single-day crash in over 40 years, with ~$3T wiped from precious metals, while Bitcoin held above ~$82k—fueling a thesis that capital may rotate from crowded gold trades into BTC over the next few months as macro liquidity improves.A Tennessee man accused of stealing over $11M in XRP from Nancy Jones, widow of country music legend George Jones, has countersued, claiming entitlement to the crypto, cash, and precious metals after allegedly managing and growing the assets during their relationship.Sources

- https://chain.link/article/tokenized-metals-onchain

- https://www.pyth.network/blog/24-7-finance-needs-24-7-price-infrastructure-introducing-pyth-indices

- https://x.com/CoinbaseMarkets/status/2056570485031268465

- https://x.com/tezos/status/2062097060887961817

- https://metals.io

- https://x.com/GMX_IO/status/2042576914854940700

- https://www.anchorage.com/insights/anchorage-digital-is-the-institutional-home-for-hyperliquid

- https://x.com/WuBlockchain/status/1941396712272322701

- https://www.facebook.com/KellyAyotteForNH/posts/new-hampshire-is-once-again-first-in-the-nation-just-signed-a-new-law-allowing-o/1231536788344143/

- https://www.techflowpost.com/en-US/article/31736

- https://thedefiant.io/news/blockchains/metals-io-brings-tokenized-gold-uranium-and-rare-earth-metals-to-tezos

- https://x.com/OstiumLabs/status/1945540768355197124

- https://a16zcrypto.com/posts/article/tokenized-asset-rwa-market-data-charts/

- https://www.ostium.com/blog/perps-on-rwas-best-dex-for-rwa-perpetuals-2026-guide?tag=Crypto

- https://www.youtube.com/watch?v=ucuRE76BtyQ

- https://www.binance.com/en/square/post/31366046356250

- https://www.youtube.com/watch?v=oxz8OGG_-LU

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…