Comprehensive explainer on Mt. Gox’s rise, 2014 collapse, legal rehabilitation, creditor repayments, market impact, and lasting lessons for Bitcoin custody, governance, exchanges, and crypto markets.

+6 sources across the wider coverage universe

From Mt. Gox to Hyperliquid: How crypto trading finally solved the trust problem2026-04

From Mt. Gox to Hyperliquid: How crypto trading finally solved the trust problem2026-04 Mt. Gox moves 10,306 BTC, worth about $731M, to a new wallet after two months of inactivity2026-06

Mt. Gox moves 10,306 BTC, worth about $731M, to a new wallet after two months of inactivity2026-06 Several Mt. Gox creditors claim they've received JPY repayments through PayPal after posting testimonials on the subreddit.2023-12

Several Mt. Gox creditors claim they've received JPY repayments through PayPal after posting testimonials on the subreddit.2023-12 Mt. Gox drops a $2.4B Bitcoin bomb—24,000 BTC moved to mystery wallet as Bitcoin hits $100K rocket zone.2024-12

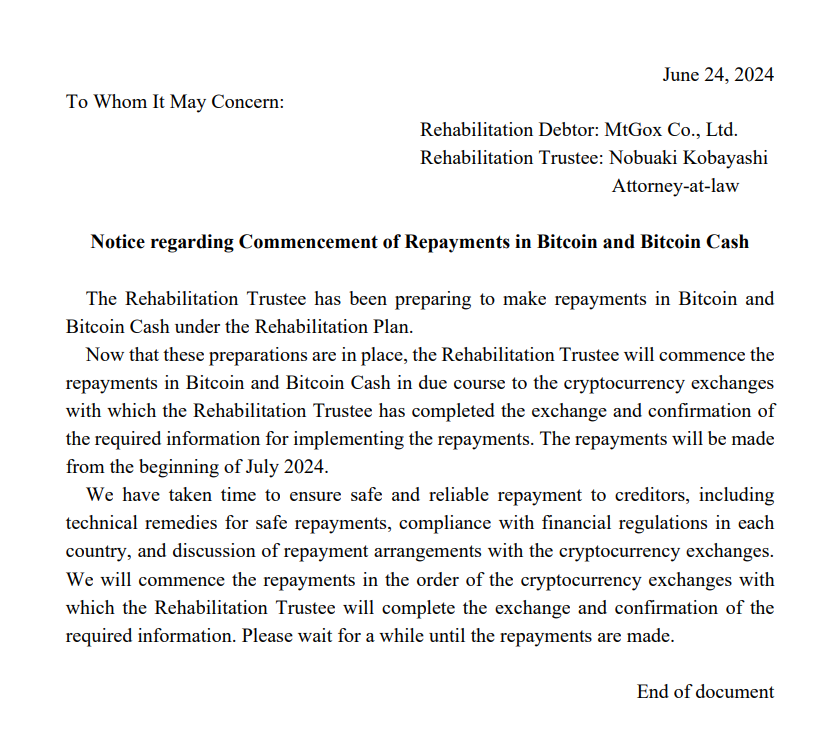

Mt. Gox drops a $2.4B Bitcoin bomb—24,000 BTC moved to mystery wallet as Bitcoin hits $100K rocket zone.2024-12 Mt. Gox to distribute Bitcoin, Bitcoin Cash repayments starting beginning of July 2024.2024-06

Mt. Gox to distribute Bitcoin, Bitcoin Cash repayments starting beginning of July 2024.2024-06- Mt. Gox creditors receive optimistic signal as repayment data updated; Fiat payments already arriving, crypto repayments expected soon.2024-04

Mt. Gox: How One Exchange Shaped Bitcoin’s Past, Present, and Future

Once the dominant venue for Bitcoin trading, the Tokyo-based exchange Mt. Gox became a byword for both early crypto exuberance and catastrophic failure, after losing hundreds of thousands of BTC and collapsing in 2014. Its story, from origins as a hobbyist project to handling over 70% of global Bitcoin volume and then imploding into years of litigation and delayed creditor repayments, continues to shape how markets think about custody, regulation, forks, and systemic risk in crypto today. The gradual distribution of roughly 140,000 BTC to creditors more than a decade later, combined with ongoing debates about “recovery forks” and distressed-claim investing, keeps Mt. Gox at the center of conversations about Bitcoin’s supply dynamics and governance. As exchanges, custodians, and decentralized trading venues evolve, the Gox saga remains an anchor for understanding why “not your keys, not your coins” is more than a slogan and why exchange risk is still a defining feature of crypto markets.

Origins: From Card Trading Site to Bitcoin’s Dominant Exchange

The early Bitcoin landscape

To understand Mt. Gox, it is necessary to situate it in the very small, very fragile Bitcoin ecosystem of the early 2010s. Bitcoin itself was launched in 2009, but for the first several years liquidity was thin, infrastructure rudimentary, and most trading took place among hobbyists on forums like BitcoinTalk or via informal over-the-counter arrangements. There were no large, regulated global exchanges, and basic functions such as price discovery, fiat on-ramps, and secure wallet custody were all experimental and often improvised. In this environment, the first entities to offer even semi-reliable BTC–fiat markets could grow extremely quickly, because they occupied a critical chokepoint between nascent crypto assets and the traditional financial system.

Mt. Gox emerged into this vacuum and rapidly became the default venue for anyone who wanted to buy or sell BTC using traditional currencies. By early 2014, the exchange was reportedly handling over 70% of all Bitcoin transactions worldwide, a level of dominance that no single centralized exchange has matched since in BTC spot trading. This concentration meant that Mt. Gox effectively anchored global BTC price discovery; shocks to its operations immediately translated into volatility across the entire market. The broader crypto ecosystem had yet to diversify into a complex network of spot, derivatives, and DeFi venues, which made Mt. Gox’s operational health almost synonymous with the health of the Bitcoin market itself. In hindsight, this degree of centralization around a single venue with weak internal controls represented a systemic risk that was poorly understood at the time.

From Magic: The Gathering to Bitcoin

The very name “Mt. Gox” hints at how accidental its rise into a systemically important crypto institution really was. The domain was originally registered by programmer Jed McCaleb in 2007 as an acronym for “Magic: The Gathering Online eXchange,” intended as a site where users could trade cards from the popular collectible card game. Although this original card platform never developed into a large business, McCaleb later repurposed the domain as an online interface for trading Bitcoin, launching the exchange in 2010 when BTC was still an obscure experiment. That origin story underscores a theme that recurs throughout Gox’s history: systems that were not designed with institutional-scale risk management in mind were gradually stretched to carry billions of dollars of value.

In 2011, McCaleb sold the site to French developer Mark Karpelès, who relocated operations to Tokyo and began building Mt. Gox into what would become the central hub of Bitcoin liquidity. Under Karpelès, the platform expanded its fiat integrations and attracted a global user base who often treated their Gox account balance as a de facto bank account for BTC and fiat currencies. At the time, the distinction between an exchange wallet and a personal wallet was poorly appreciated outside of core cypherpunk circles, and many users were content to leave their holdings in exchange custody indefinitely. The combination of rapid user growth, evolving code, and a single dominant custodian created conditions where latent security weaknesses could accumulate unnoticed, even as the notional value of assets under management skyrocketed.

The rise to systemic importance

As Bitcoin’s price climbed from cents to double digits and beyond, Mt. Gox became a magnet for speculative capital and arbitrage strategies. By early 2014, when BTC traded in the hundreds of dollars, Mt. Gox’s share of global volume made it the primary reference for BTC price quotations across media and market data services. This prominence was reinforced by liquidity feedback loops: traders went where the liquidity was, which further deepened the order book and kept spreads tighter than on smaller venues. For many mainstream journalists and new retail participants, “the Bitcoin price” was effectively synonymous with “the Mt. Gox price.”

Yet beneath the surface, there were already signs of strain. Integrating with banking partners was difficult for a lightly regulated crypto exchange headquartered in Japan but serving a mostly global customer base, leading to periodic delays in fiat withdrawals and mounting backlogs during periods of intense trading. Operationally, Mt. Gox was still in many respects run like a startup rather than a systemically important financial-market infrastructure. Internal controls, segregation between hot and cold wallets, and basic accounting of BTC balances were reportedly weak or ad hoc, with much of the critical infrastructure dependent on a small team and custom code. This discrepancy between external systemic importance and internal organizational maturity set the stage for a series of security incidents that would both expose and amplify the exchange’s vulnerabilities.

From Mt. Gox to Hyperliquid: How crypto trading finally solved the trust problem

16 validators force-settled JELLY positions at $0.0095 during a $12M exploit — same emergency lever any CEX risk desk pulls, just fewer people at the table. Even at $200B/month volume and 24 validators now, the node code is closed-source, price oracles aggregate CEX data under validator control, and there's no public governance framework. Custody moved off exchanges but the crisis playbook still reads like Binance's incident response manual.

Readers treat large BTC wallet movements as a real-time repayment oracle — the most-clicked stories are either 'transfer happened, repayment imminent?' or 'creditors actually received funds,' revealing that after a decade of delays, the community has learned to decode on-chain signals as the only reliable update ahead of official announcements.↗

The 2011 Hacks and Bitcoin’s First “Lehman Moment”

User database leak and rising security concerns

The first major wake-up call regarding Mt. Gox’s security posture came in mid-June 2011, when some users reported that BTC had gone missing from their accounts. Around the same time, the exchange’s user database—containing usernames, email addresses, and hashed passwords—was reportedly leaked and posted online, giving attackers the raw material needed to attempt account takeovers against any customer who reused credentials across services. Although password hashing provided some protection, the leak vividly illustrated how a centralized exchange represented a single point of failure for both assets and personal data. For the broader Bitcoin community, which had largely focused on the cryptographic robustness of the Bitcoin protocol itself, this was a reminder that security bottlenecks in surrounding infrastructure could be just as consequential.

Mt. Gox reported that in June 2011, around 25,000 BTC were stolen from 478 user accounts, an amount worth roughly 400,000 USD at the time but now representing a much larger notional value. The incident prompted a mixture of outrage and anxious introspection on BitcoinTalk and other community forums, where some posters began questioning whether the ongoing price run-up from under 1 USD to nearly 30 USD might be a bubble that could be punctured by an exchange failure. Community threads from early June 2011 capture a growing sense of unease, with users asking whether the rally was sustainable and pointing to Mt. Gox’s operational issues as a potential systemic risk. In that context, the events of June 19–20, 2011, would take on almost mythic significance as Bitcoin’s first brush with systemic collapse induced by a critical exchange.

The flash crash to one cent

On June 19–20, 2011, an attacker obtained credentials associated with a Mt. Gox administrator or auditor account and used them to manipulate trading on the platform in an unprecedented way. According to later reconstructions, the attacker logged into Mt. Gox’s internal system and used privileged access to move a large amount of BTC into their control, then placed massive sell orders that dumped those coins onto the order book at any available price. With order matching proceeding normally, the sudden wave of supply overwhelmed existing bids, causing the displayed price of BTC on Mt. Gox to plunge from around 17 USD to as low as 0.01 USD in a matter of minutes. This “flash crash” reverberated across the entire crypto ecosystem, as data sites reported Bitcoin trading for a penny and some observers speculated that the experiment might effectively be over.

In practice, the broader market quickly realized that the crash was driven by fraudulent internal activity rather than a genuine collapse in demand for BTC. Mt. Gox halted trading, investigated the incident, and ultimately rolled back all of the trades associated with the attack, restoring user balances to their pre-crash state and treating the episode as if it had never happened from an accounting perspective. However, the need for such a rollback highlighted a disquieting reality: although Bitcoin’s blockchain was immutable, the balances that most users saw and relied upon were mediated by centralized databases controlled by exchanges. When those databases could be altered retroactively in response to an incident, the effective finality and neutrality of user holdings depended less on cryptography than on the decisions of a single exchange operator. This dissonance between the philosophy of decentralized money and the practice of centralized custody would become a recurring theme in later crises.

Early technical mishaps and lost coins

The 2011 flash crash and account compromises were not isolated incidents. Over the early years, Mt. Gox reportedly suffered from a series of technical mishaps that led to further BTC losses or operational disruptions. One notable example involves around 2,609 BTC that were accidentally sent to an output script that could never be spent, effectively rendering the coins permanently inaccessible. The misconfiguration, which created a script that could never satisfy the required conditions for spending, meant that those bitcoins were, for all practical purposes, destroyed. This type of mistake underscored the complexity of handling Bitcoin at scale, where errors in address generation or script construction could lead to irreversible loss of funds.

These early technical failures underscored a pattern: Mt. Gox functioned as both a software experiment and a financial exchange, but its rapid growth outpaced its ability to develop institutional-grade engineering practices. The same platform that was handling the majority of global BTC trades was also prone to bugs, inadequate testing, and operational shortcuts that would be unacceptable in traditional capital markets. Because there were few alternatives with comparable liquidity, traders and investors largely tolerated these issues, even as they amplified volatility and created a sense that Bitcoin markets were fragile and easily disrupted. The lessons of 2011—that exchange security was a critical weak link and that centralized trading venues could abruptly fail—were heard but not fully internalized by the broader community.

The 2014 Meltdown: Missing Bitcoins and Bankruptcy

Mounting withdrawal problems and loss of confidence

By 2013, Bitcoin’s price had risen to the hundreds of dollars, and Mt. Gox was processing immense trading volumes, but operational stress was becoming increasingly apparent. Users began reporting delays in both BTC and fiat withdrawals, sometimes waiting weeks or months to move funds off the exchange. These delays were partly attributable to banking friction, as financial institutions grew wary of servicing a high-profile, lightly regulated crypto business whose legal status was often unclear. However, they also reflected deeper issues within Mt. Gox’s own accounting and wallet management systems, which were later alleged to have lost track of how many coins the exchange actually controlled.

Over time, the withdrawal bottlenecks eroded market confidence. A persistent discount began to emerge between the price of BTC on Mt. Gox and that on other exchanges, reflecting the perceived risk that coins trapped on Gox might never be withdrawn. Traders like Arthur Hayes, who would later found the derivatives exchange BitMEX, reportedly attempted to arbitrage this discrepancy by buying discounted BTC on Mt. Gox and simultaneously shorting or selling BTC at higher prices on other venues, betting that withdrawals would eventually resume and the spread would close. This strategy was highly profitable for those able to manage the operational and counterparty risk, but it also relied on the assumption that Mt. Gox remained solvent and would ultimately honor withdrawals. As would become clear in early 2014, that assumption was fatally flawed.

Discovery of the massive shortfall and suspension of operations

In February 2014, Mt. Gox abruptly suspended BTC withdrawals, citing “suspicious activity” and technical issues related to transaction malleability, a quirk in the Bitcoin protocol that can allow transaction IDs to be altered under certain conditions. The exchange claimed that this quirk made it difficult to reconcile its internal records with blockchain data, leading it to temporarily halt withdrawals while it investigated. However, as days stretched into weeks, it became apparent that the situation was far more serious than a mere software glitch. Other exchanges continued operating normally despite the same protocol behavior, and users grew increasingly alarmed as their funds remained inaccessible with little transparency from the company.

Later that month, Mt. Gox filed for bankruptcy protection in Tokyo, disclosing that it had lost approximately 850,000 BTC, including 750,000 BTC belonging to customers and 100,000 BTC owned by the company itself. The missing coins, worth hundreds of millions of dollars at the time and tens of billions at later prices, represented one of the largest single losses of digital assets in history. The company suggested that the loss had been ongoing for years, potentially due to a long-running security breach that allowed hackers to siphon coins progressively from the exchange’s wallets. The revelation that what many users had treated as a secure custodial account was in fact deeply undercollateralized was a shock to the community and triggered widespread media coverage painting Bitcoin as unsafe and poorly regulated.

Aftermath and partial recovery of funds

In the months following the bankruptcy filing, investigators and the court-appointed trustee began piecing together Mt. Gox’s actual asset position. They discovered that a substantial portion of the missing BTC—around 200,000 coins—remained in old-format wallets that the company had somehow failed to account for properly. These coins were transferred to secure storage under the control of the bankruptcy estate, forming the core of the assets that would eventually be available for distribution to creditors. Even so, the net loss remained enormous: in total, Mt. Gox is estimated to have lost over 750,000 BTC belonging to customers and approximately 100,000 BTC of its own holdings, for a total shortfall in excess of 850,000 BTC.

For Bitcoin’s reputation, the collapse was a major blow. Mainstream coverage often conflated Mt. Gox’s failure with a failure of the Bitcoin protocol itself, even though the underlying blockchain continued to function as designed throughout the crisis. For those inside the ecosystem, however, the lesson was more nuanced. The episode highlighted the need for due diligence on custodial infrastructure, the dangers of concentration risk around a single exchange, and the importance of separating the security model of Bitcoin’s protocol from that of centralized intermediaries. It also set in motion a long-running legal saga in Japan, as creditors sought to recover as much value as possible from the remaining assets and to determine whether they would be compensated in fiat terms based on BTC’s 2014 price or in kind with BTC and related forked assets such as Bitcoin Cash.

From Bankruptcy to Civil Rehabilitation: The Long Road for Creditors

Bankruptcy proceedings and the “Tokyo whale”

In the years immediately following Mt. Gox’s 2014 bankruptcy, the proceedings were initially structured as a traditional liquidation under Japanese law. The court appointed attorney Nobuaki Kobayashi as trustee to manage the exchange’s remaining assets, which included the roughly 200,000 BTC that had been recovered along with associated Bitcoin Cash after the 2017 hard fork. Under the original bankruptcy framework, creditors’ claims were denominated in Japanese yen based on the price of BTC at the time of the bankruptcy filing, meaning that any subsequent appreciation in BTC price would accrue to the estate rather than to creditors directly. As Bitcoin’s price rose dramatically in subsequent years, this created a situation where the estate was massively “overcollateralized” in BTC terms relative to the yen value of creditor claims.

The trustee began selling portions of the recovered BTC and BCH on the market to raise fiat currency for potential distributions and to cover administrative costs. These large sales, which took place intermittently from 2017 onward, attracted intense attention from traders, who dubbed Kobayashi the “Tokyo whale” and attempted to correlate major BTC price declines with on-chain movements from trustee-controlled wallets. Some analysts argued that these sales contributed to downward pressure on BTC during parts of the 2018 bear market, although the extent of their impact relative to broader macro and crypto-specific factors remains debated. Regardless, the optics of a court-appointed trustee selling BTC at levels far below later highs, while creditors were locked into claims valued at 2014 prices, fueled growing frustration and calls for a different legal mechanism that would allow creditors to benefit more directly from the assets’ appreciation.

Shift to civil rehabilitation

In response to creditor lobbying and changing perceptions of fairness, the Tokyo District Court issued an order in June 2018 to commence civil rehabilitation proceedings for Mt. Gox, replacing the previous bankruptcy framework. Under Japan’s Civil Rehabilitation Act, a distressed company can be reorganized, with a court-supervised plan designed to maximize recoveries and allow a measure of creditor input into how assets are distributed. For Mt. Gox, this transition meant that creditors could seek to be repaid in BTC and related crypto assets rather than being locked into a fixed yen valuation corresponding to BTC’s much lower 2014 price. The court’s order laid out deadlines for filing rehabilitation claims, submission of asset inventories, and proposals for a rehabilitation plan.

The announcement of civil rehabilitation was widely interpreted as a victory for creditors and as a recognition of the unique nature of crypto assets, whose value had multiplied many times since the original bankruptcy filing. It also significantly extended the timeline for final resolution, as the transition required recalculating claims, collecting additional documentation, and designing a distribution framework compatible with both Japanese law and the technical realities of Bitcoin transfers. The rehabilitation trustee, still Nobuaki Kobayashi, now had to maintain custody of the remaining BTC and BCH while crafting a plan that balanced fairness among different classes of creditors, including those whose claims had been traded on secondary markets, and addressed questions such as whether interest or damages would be paid.

Rehabilitation plan and categories of repayment

Over the following years, the rehabilitation process produced a series of draft plans and court filings outlining how the remaining assets would be allocated. A key document, the draft amended rehabilitation plan, specified that certain proposed forms of intermediate repayment would not in fact be implemented, reflecting evolving judgments about the most practical and equitable distribution mechanisms. Instead, the plan focused on several main categories of repayment: so‑called “base repayment” in BTC and/or fiat, “early lump-sum repayment” for creditors willing to accept a reduced amount in exchange for faster settlement, and “intermediate repayment” that would be contingent on remaining assets and legal outcomes. The trustee communicated deadlines for creditors to file proofs of rehabilitation claims, respond to proposed terms, and select preferred payout methods.

Despite the complexity, a basic structure emerged: of the approximately 200,000 BTC recovered, around 140,000 BTC were earmarked for redistribution to rehabilitation creditors, with the remainder reserved for fees and other obligations. Analysis by firms such as Coin Metrics estimated that only a portion of this 140,000 BTC—perhaps around 65,000 BTC—would ultimately go to individual creditors in the form of BTC, with the rest used for fiat-equivalent payments, claims by larger entities, and other settlement types. Repayments were to be facilitated in part through partnerships with exchanges such as Kraken, Bitstamp, and Bitbank, which would receive BTC on behalf of creditors and credit it to their accounts, reducing operational overhead for the trustee and leveraging existing exchange infrastructure. For many creditors, this structure represented a chance to recover a meaningful share of their lost BTC, albeit after an extraordinarily long wait and with considerable uncertainty about the final timing and amount.

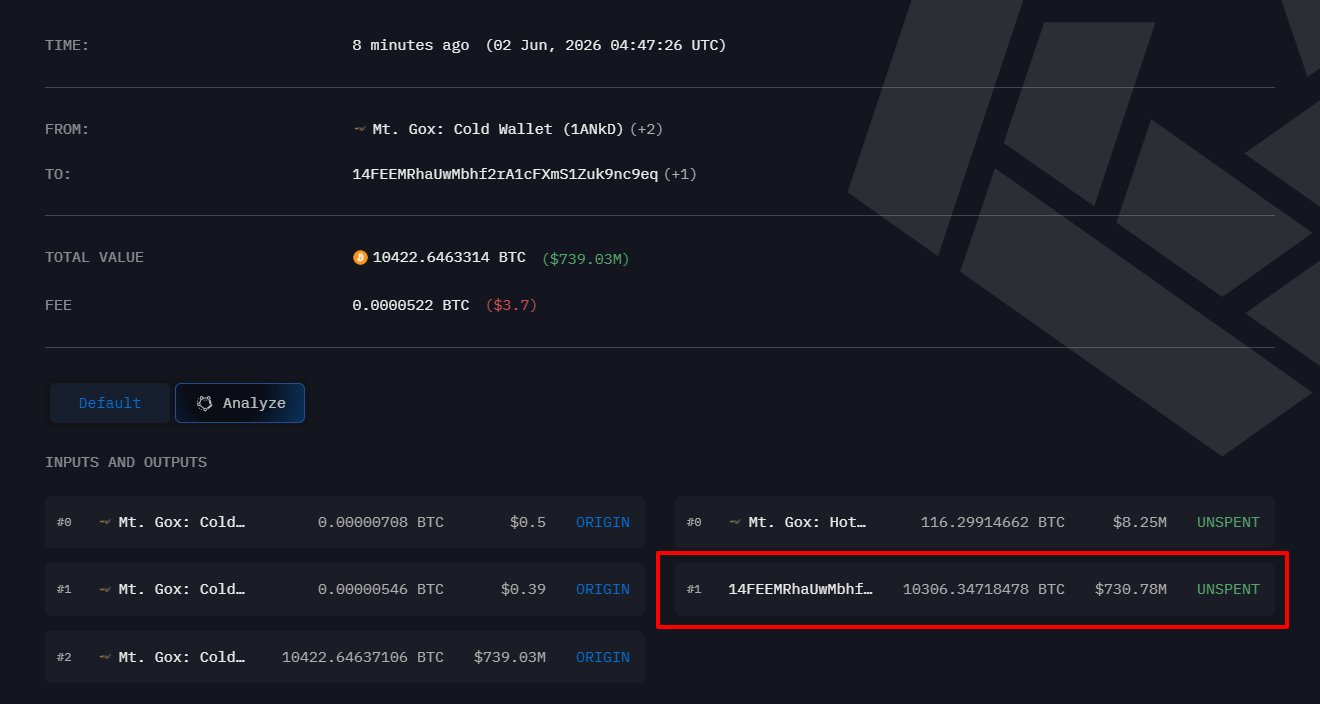

Mt. Gox moves 10,306 BTC, worth about $731M, to a new wallet after two months of inactivity

Mt. Gox moved 10,306 BTC, about $731M when flagged, to a new wallet for its first major movement in roughly two months. The transfer looks like wallet reshuffling for now, with OnchainLens calling the destination likely Mt. Gox's own wallet rather than an exchange deposit. The market still watches these moves because Mt. Gox-related BTC is the classic creditor-repayment overhang: movement alone is not selling, but exchange flows would change the risk fast.

- 01Creditor repayments finally arriving↗

After 10+ years of waiting, stories confirming actual fiat and crypto distributions — JPY via PayPal, Bitstamp processing — drove the single highest-clicked headline, signaling readers want proof of payment, not promises.

- 02Massive BTC wallet transfer alerts↗

Multiple high-click headlines tracked individual transfers of $700M–$2.9B, as readers treated each on-chain move as a potential signal that sell pressure or distributions were imminent.

- 03Market price impact of BTC overhang↗

With billions in BTC still held, readers repeatedly engaged with whether large transfers would crash the market — and were relieved when analysis showed price stability despite the moves.

- 04Perpetual repayment deadline extensions↗

Two separate deadline-extension stories drew clicks, reflecting creditor frustration at the cycle of delayed timelines stretching from 2024 through 2026.

- 05Institutional acquisition of bankruptcy claims↗

Vivek Ramaswamy's Strive pursuing 75,000 BTC worth of Mt. Gox claims framed the bankruptcy estate as a live supply-dynamics play, attracting readers tracking corporate Bitcoin treasury strategies.

- 06DEX trust vs. centralized exchange failure

The 'Mt. Gox to Hyperliquid' framing drew readers using the collapse as a benchmark for how far crypto infrastructure has evolved in handling custody and counterparty risk.

Deadlines, Delays, and the Start of Repayments

Extensions of repayment deadlines

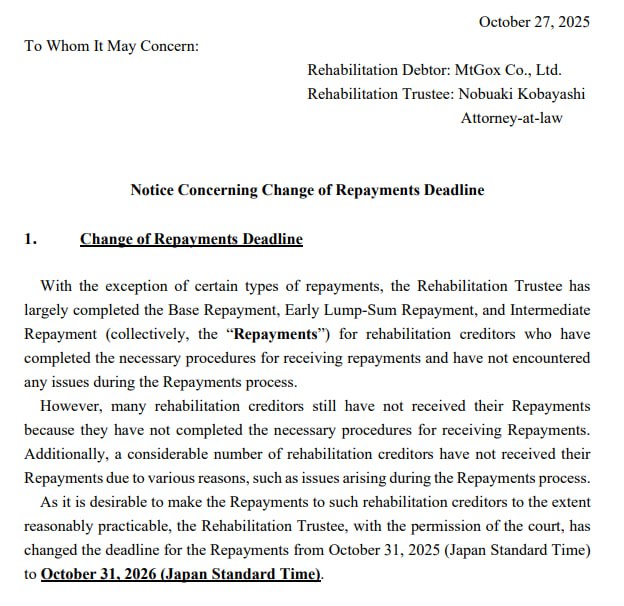

Over time, the schedule for Mt. Gox repayments has been repeatedly extended, reflecting the administrative complexity of verifying claims, complying with regulatory requirements across different jurisdictions, and ensuring secure transfer of large BTC amounts. An announcement on the official Mt. Gox website confirmed that the deadlines for base repayment, early lump-sum repayment, and intermediate repayment were postponed from October 31, 2025, to October 31, 2026. This extension effectively gave the trustee an additional year to complete distributions, while also providing more time for creditors to complete necessary selection and registration procedures. The communication noted that rehabilitation creditors who failed to complete selection and registration by the deadline would not be able to receive the relevant repayments, highlighting the importance of administrative follow-through in a process already stretched out over more than a decade.

These extended timelines have been a source of frustration for many original Gox customers, some of whom lost access to their BTC in 2014 and have been waiting ever since for resolution. However, they also reflect the practical constraints involved in securely moving and distributing billions of dollars worth of digital assets. Each batch of repayments must be carefully coordinated with exchanges, subjected to compliance checks such as anti-money-laundering and sanctions screening, and executed in a way that minimizes operational risk. The extension to 2026 also interacts with broader market narratives, as traders speculate about when large tranches of BTC might hit the market and how that timing intersects with halving cycles, macroeconomic conditions, and evolving ETF demand.

Onset of actual repayments and early distributions

Despite the long delays, there have been tangible signs that the rehabilitation process has moved from planning to execution. By mid‑2020s, reports indicated that thousands of creditors had received at least partial repayments, whether in fiat, BTC, or BCH, as the trustee began implementing parts of the approved plan. Official statements and third‑party analyses suggested that around 19,500 creditors had been repaid at least in part, while the trustee continued to hold a significant BTC balance—on the order of tens of thousands of coins—for remaining obligations and future distributions. In some cases, exchanges such as Bitstamp publicly confirmed that they had begun the process of crediting BTC to Mt. Gox creditors who chose them as the distribution venue, reinforcing that the theoretical repayment plan was becoming a concrete reality.

The gradual nature of these repayments is deliberate. Analysis by Coin Metrics emphasized that distributions would be spread across multiple exchanges, including Kraken, Bitstamp, and Bitbank, and executed over time rather than in a single lump sum. This structure is explicitly designed to reduce the likelihood of severe short‑term market disruption by avoiding a sudden injection of a large number of coins into a single venue’s order book. Rather than a single “Mt. Gox dump,” the market is more likely to experience a series of moderate inflows as individual creditors decide whether to hold, sell, or otherwise deploy their recovered BTC. This staggered approach, combined with the diversification of recipient exchanges, reflects lessons learned not only from Mt. Gox’s own history but also from later episodes where large on‑chain movements by centralized entities triggered volatility.

Large Wallet Movements and Market Reactions

Monitoring Mt. Gox wallets on‑chain

Even before meaningful volumes of BTC were actually distributed to creditors, Mt. Gox–linked wallets became a focal point for on‑chain analysts and traders. Blockchain intelligence platforms such as Arkham and others track large addresses known to be associated with the Mt. Gox estate and flag significant transfers as potential precursors to creditor repayments. For example, one widely reported event saw Mt. Gox move approximately 10,306 BTC, worth around 730–739 million USD at then‑prevailing prices, from a cold wallet to an unmarked address, prompting headlines and social‑media speculation about imminent distributions. In another instance, the exchange shifted roughly 13,265 BTC, placing 12,000 BTC back into cold storage and moving the remainder in a manner that market participants interpreted as internal rebalancing rather than outright selling.

In yet another episode, Mt. Gox transferred around 500 BTC, valued at roughly 35 million USD, to unidentified addresses; although relatively small compared with earlier transfers, the move coincided with a noticeable BTC price pullback, reinforcing the perception that any Mt. Gox activity could resonate with markets. Data cited in that coverage indicated that, at the time, Mt. Gox still held approximately 44,905 BTC worth over 3.1 billion USD, a fraction of its original holdings but still a sizeable stash whose eventual fate remained closely watched. These on‑chain movements illustrate the broader phenomenon of “address watching” in crypto, where transparent ledger data allows markets to anticipate, and sometimes overreact to, the actions of large holders long before any actual trades hit centralized exchange order books.

Price responses to transfer news

Market reactions to Mt. Gox–related transfers have varied, but they often manifest as short‑term volatility spikes and narrative‑driven trading. When Mt. Gox moved over 32,000 BTC—worth about 2.2 billion USD at the time—to new wallet addresses, Bitcoin’s price reportedly fell under 68,000 USD, dropping around 2% over 24 hours and contributing to a broader market slide amid other macro factors. Another reported transfer of about 500 BTC coincided with a roughly 4.4% decline in BTC price from an intraday peak near 73,300 USD to below 69,150 USD. In both cases, traders debated how much of the price move could be attributed to Mt. Gox versus other contemporaneous drivers such as macroeconomic news, ETF flows, or liquidations in derivatives markets.

Importantly, analysts often emphasize that wallet transfers alone do not constitute sell pressure unless the coins are sent to exchange deposit addresses and actually liquidated. Mt. Gox movements to intermediate wallets, or to custody arrangements established for the purpose of distribution to creditors, may never translate into concentrated market selling if a substantial share of creditors chooses to hold their BTC or sell gradually. Coin Metrics and other research firms have argued that, relative to the overall size and liquidity of the BTC market, the roughly 140,000 BTC earmarked for creditors—and the smaller subset likely to be actively sold—represent a manageable inflow, particularly when spread across multiple venues and time periods. As markets have matured and liquidity deepened, headline‑driven fear about a single “Mt. Gox dump” has given way to more nuanced assessments that distinguish between address activity, distribution mechanics, and actual realized selling.

Interplay with broader market narratives

The timing of Mt. Gox transfers and repayments also intersects with broader Bitcoin narratives about halving cycles, ETF adoption, and macro‑driven demand. When headlines link “Mt. Gox moves X billion in Bitcoin” with short‑term pullbacks, it is tempting to attribute causality, but a fuller picture often reveals overlapping factors, from funding‑rate resets in perpetual futures to profit‑taking after new all‑time highs. Market coverage from mainstream outlets has periodically framed BTC price weakness as driven by fears that Mt. Gox creditors might rush to sell their recovered coins, highlighting estimates that distributions could total around 8–9 billion USD in BTC. At the same time, some analysts point out that many creditors are long‑time Bitcoin holders who have already held through multiple cycles and may be inclined to keep at least a portion of their recovered BTC rather than immediately exiting.

The presence of sophisticated funds buying Mt. Gox claims at a discount adds another layer. If distressed‑asset funds or specialized vehicles aggregate large volumes of claims with the explicit goal of building a strategic BTC treasury, their eventual behavior may be closer to that of long‑term allocators than to short‑term sellers. Recent coverage has described entities aiming to acquire tens of thousands of BTC worth of Mt. Gox claims as part of a broader strategy to build sizable Bitcoin reserves and pursue “alpha” strategies relative to spot BTC returns. In such scenarios, the net effect of Mt. Gox distributions could be a reallocation of coins from a diverse, somewhat passive creditor base into the hands of professional asset managers who may opt for structured hedging or lending rather than outright liquidation. The market impact of Mt. Gox, in other words, depends not just on the volume of BTC released but on who ultimately controls it and how they integrate it into their broader portfolio strategies.

Hard Forks, Recovery Proposals, and Bitcoin Governance

The idea of a “Mt. Gox recovery fork”

Beyond its immediate market effects, Mt. Gox continues to surface in debates about Bitcoin’s governance and the ethics of altering the ledger to address theft or loss. Over the years, various commentators and stakeholders have floated the idea of a “Mt. Gox recovery fork,” a hypothetical protocol change that would reassign some portion of the stolen coins back to creditors by invalidating or redirecting the outputs associated with the theft. The concept mirrors earlier controversies in crypto history, most notably the 2016 Ethereum DAO fork, where the community opted to roll back the chain to reverse an exploit, creating a schism between Ethereum and Ethereum Classic. In the Bitcoin context, such a move is far more contentious, given the protocol’s strong cultural emphasis on immutability and resistance to arbitrary changes.

Recent coverage has noted that even Mt. Gox’s former CEO has at times proposed some form of code modification or hard fork aimed at recovering tens of thousands of hacked BTC, arguing that modern Bitcoin’s economic majority might prefer to see those coins returned to victims rather than left idle in addresses under the control of thieves. However, these ideas have consistently met with strong pushback from core developers, miners, and many community members who view any retroactive ledger reassignment as a dangerous precedent. Their argument is that if social consensus can be marshaled to alter the UTXO set for one high‑profile case, it becomes more difficult to reject similar demands in future disputes, whether they involve scams, regulatory interventions, or politically motivated confiscations.

BIP‑style proposals and cleanup mechanisms

Against this backdrop, some technical proposals have reportedly explored less invasive approaches, such as “cleanup” mechanisms that might allow coins provably lost or dormant for extremely long periods to be reassigned under carefully constrained conditions. References to concepts like a “BIP‑54 cleanup block” in recent discourse suggest attempts to formalize such ideas within Bitcoin’s improvement proposal process, though none have been adopted into Bitcoin’s mainline consensus rules. The crux of the debate is whether any on‑chain mechanism should exist to reinterpret ownership based on off‑chain information, such as court orders or evidence of theft, or whether Bitcoin’s security model must remain strictly indifferent to anything but possession of private keys and adherence to consensus rules.

Supporters of recovery‑style proposals often emphasize fairness and victim restitution, arguing that allowing stolen coins to remain in limbo indefinitely undermines public trust and creates windfalls for criminals. Opponents counter that Bitcoin’s core value proposition lies precisely in its refusal to make such judgments and that any formalized cleanup mechanism would invite pressure from states, corporations, and interest groups to weaponize protocol changes for narrower agendas. The Mt. Gox case functions as a powerful reference point because the magnitude of the theft is large enough to be economically significant and emotionally resonant, yet small enough relative to total supply that it does not obviously justify a radical departure from long‑standing norms. The ongoing stalemate illustrates how contentious and path‑dependent Bitcoin governance remains, with Mt. Gox serving as a recurring test of whether the community prioritizes social justice or protocol purity when they appear to conflict.

Mt. Gox as a governance case study

Regardless of whether any recovery fork ever gains meaningful traction, the Mt. Gox saga has already shaped how Bitcoiners think about governance. It has reinforced a distinction between protocol‑level guarantees, which are intentionally minimal, and ecosystem‑level responses such as legal action, insurance, and voluntary restitution. While Bitcoin’s base layer offers no built‑in mechanism for reversing fraudulent transactions, victims can and do pursue relief through courts, bankruptcy proceedings, and negotiated settlements, as Mt. Gox creditors have done for more than a decade. This multi‑layered response—protocol neutrality paired with off‑chain legal processes—has become a template for thinking about other large‑scale losses, from exchange hacks to protocol‑level bugs in other blockchains.

The Mt. Gox recovery debates also highlight the growing role of miners, full‑node operators, and large custodians as de facto governance stakeholders. Any hard fork or consensus change aimed at addressing the Gox theft would require broad coordination among these actors, and their reluctance to entertain such changes reinforces the de facto veto power of conservative consensus. At the same time, the fact that such proposals are even discussed in public forums indicates that governance in Bitcoin is not purely ossified; rather, it is a living process in which extreme events like Mt. Gox are periodically revisited as stress tests of the system’s values. For observers and participants alike, watching how the community responds to these proposals offers insight into Bitcoin’s evolving notion of what is—and is not—up for social renegotiation.

Mt. Gox moved 10,423 BTC after eight months of silence, fueling concerns but no signs of actual selling yet. Analysts say transfers alone are not sell pressure unless coins hit exchanges.

Ahhh it was mtgox all along, gotcha

Mt. Gox launched by Jed McCaleb as Bitcoin exchange

Hacker crashes BTC from $17 to $0.01 via compromised auditor account

Mt. Gox suspends trading, files for bankruptcy; 850,000 BTC reported lost

Civil rehabilitation plan approved, replacing liquidation with creditor repayment process

Bitcoin and Bitcoin Cash repayments to creditors begin via Bitstamp and Kraken

Repayment deadline extended to October 2024, then again to October 2026

Trustee moves $2.9B in BTC for first time in five years amid creditor distribution activity

Creditors report JPY repayments via PayPal; $4B+ BTC still held by trustee

Lessons for Custody, Exchanges, and Market Structure

“Not your keys, not your coins” becomes mainstream

One of the most enduring legacies of Mt. Gox is the popularization of the mantra “not your keys, not your coins,” the idea that users who leave assets on centralized exchanges effectively relinquish control and accept counterparty risk. While this principle was understood within early cypherpunk circles, the Gox collapse dramatically illustrated it for a wider audience. Hundreds of thousands of BTC that customers believed they “owned” were in fact IOUs from a single exchange whose internal wallets had been steadily drained by hackers over several years. When the music stopped, those IOUs were suddenly worth far less than face value, subject to court proceedings, and payable—if at all—over a timeline measured in decades.

In response, a growing share of Bitcoin users began adopting self‑custody solutions such as hardware wallets and multisignature arrangements, reducing their reliance on centralized exchanges for long‑term storage. Wallet providers and educational initiatives emphasized the practical steps needed to generate, back up, and secure private keys, translating abstract cryptographic concepts into user‑friendly products and guidance. At the same time, exchanges faced mounting pressure to improve their own custody practices, including segregating customer funds from operational wallets, using cold storage with multi‑party controls, and undergoing independent security audits. Although subsequent failures like those of FTX and Celsius showed that custodial risk never fully disappeared, Mt. Gox ensured that exchange trust was no longer taken for granted and that self‑custody remained a core part of Bitcoin’s culture.

Evolution of centralized exchanges and proof‑of‑reserves

The failures exposed by Mt. Gox and later collapses catalyzed a wave of innovation in exchange design, risk management, and transparency. Many major platforms introduced more formalized wallet segregation, distinguishing between hot wallets used for day‑to‑day operations and cold wallets whose private keys are kept offline and governed by strict access controls. Some exchanges began publishing partial proof‑of‑reserves attestations, leveraging cryptographic techniques to demonstrate that they hold on‑chain assets at least equal to the sum of user liabilities, without revealing individual account balances. While proof‑of‑reserves remains imperfect—especially when liabilities can be hidden off‑balance‑sheet—it reflects an effort to harness the transparency of blockchains themselves to compensate for opaque corporate structures.

In parallel, regulators in multiple jurisdictions tightened oversight of custodial exchanges, requiring licensing, capital buffers, and compliance programs that more closely resemble those of traditional financial institutions. These regulatory responses, though uneven across countries, were informed in part by the optics of Mt. Gox, which showcased what could go wrong when large amounts of public savings were concentrated in an unregulated offshore entity. As later headlines described a trajectory “from Mt. Gox to Hyperliquid,” the implicit message was that the crypto industry has gradually evolved from informal, trust‑me exchanges to more robust platforms that blend technical safeguards with legal accountability. Nevertheless, the persistence of new exchange failures demonstrates that Mt. Gox was not a one‑off anomaly but rather an early, visible data point in a longer learning curve.

Rise of non‑custodial and hybrid trading venues

Mt. Gox also indirectly boosted interest in non‑custodial trading models, where users maintain control of their wallets and private keys while interacting with order books or automated market makers. Decentralized exchanges (DEXs) on networks like Ethereum and other smart‑contract platforms allow users to swap tokens directly from self‑custodied wallets, eliminating the need to trust a centralized operator with large balances. While Bitcoin itself has not developed DEX infrastructure to the same extent as some other chains, cross‑chain bridges, derivatives protocols, and newer layer‑two designs are exploring ways to bring more trust‑minimized trading to BTC holders.

Hybrid models have emerged as well, combining centralized order matching with on‑chain settlement or segregated custody, so that even if an operator fails, user funds remain recoverable on‑chain. These architectures draw a direct line back to the realization that placing all trust in a single off‑chain ledger, as Mt. Gox customers did, is antithetical to Bitcoin’s promise of self‑sovereign money. By tying exchange solvency more closely to the transparent state of public blockchains and by reducing the amount of time and value exposed to centralized custody, the industry has sought to “solve the trust problem” that Mt. Gox so starkly exposed. The fact that Mt. Gox still functions as the benchmark reference point for discussions of exchange risk underscores how deeply its failure shaped the imagination of crypto builders and users.

Claims Trading, Arbitrage, and the Financialization of Mt. Gox

Distressed‑claim markets and institutional interest

As the Mt. Gox rehabilitation process dragged on and BTC’s price appreciated, a secondary market for bankruptcy claims emerged. Holders of claims—essentially the rights to receive a share of whatever assets the estate ultimately distributes—could sell them to third parties at a discount, effectively cashing out their position in exchange for immediate liquidity. Buyers, in turn, assumed the risk that distributions might be delayed or smaller than expected, in exchange for the potential upside if BTC prices rose further or legal outcomes proved favorable. This type of distressed‑asset trading is common in traditional bankruptcies, but in the case of Mt. Gox, it took on a distinctly crypto flavor: the underlying asset was not a factory or brand but a stockpile of BTC and forked coins whose market value fluctuated continuously.

In recent years, specialized investment vehicles and funds have reportedly raised capital specifically to acquire large blocks of Mt. Gox claims, with some aiming to assemble exposure equivalent to tens of thousands of BTC. Their thesis hinges on a combination of factors: a belief that BTC’s long‑term price trajectory remains positive; confidence that the rehabilitation trustee will successfully distribute the earmarked coins; and an expectation that they can manage the timing and method of any eventual selling or hedging to maximize returns. For some funds, the goal is not merely to arbitrage the claims discount but to build a strategic Bitcoin treasury, effectively using the legal channel of bankruptcy claims as an avenue for large‑scale BTC acquisition without directly buying on the open market.

Arbitrage during the crisis and lessons learned

Arbitrage strategies linked to Mt. Gox date back to the crisis itself. As noted earlier, traders such as Arthur Hayes exploited price discrepancies between Mt. Gox and other exchanges during the 2013–2014 withdrawal crises, buying discounted BTC on Gox and selling at higher prices on more liquid venues in mainland China and elsewhere. These trades were inherently risky, relying on the assumption that Gox withdrawals would resume and that the trader would be able to extract the BTC needed to close the position. When withdrawals ultimately froze and the exchange collapsed, some arbitrageurs were left with unhedged positions or unrecoverable balances, revealing the danger of treating exchange IOUs as equivalent to on‑chain BTC.

The evolution from those early, operationally fragile arbitrage plays to today’s more structured distressed‑claim investing illustrates the increasing financialization of crypto. Instead of betting directly on the reliability of a single exchange, modern strategies often blend legal analysis, on‑chain monitoring, and macro views on BTC’s future. The market prices of Mt. Gox claims encapsulate aggregated expectations about both legal timelines and Bitcoin’s price path, turning a historical catastrophe into a tradable, quantifiable risk factor. For better or worse, the Gox saga has become not only a cautionary tale but also a platform for sophisticated financial engineering.

Interactions with broader Bitcoin supply dynamics

The existence of large pools of Mt. Gox‑linked claims and their aggregation by institutional players has implications for Bitcoin’s broader supply dynamics. If a single entity or small set of funds acquires claims representing, for example, tens of thousands of BTC, then the eventual distribution of those coins concentrates ownership in ways that differ from the original, more granular distribution among retail users. Depending on the strategies these funds pursue—such as long‑term holding, derivatives hedging, or participation in lending markets—the net effect could be to either dampen or amplify BTC’s effective circulating supply. A fund that lends its coins into centralized or DeFi lending platforms, for example, could increase leverage in the system, while one that simply holds in cold storage might effectively remove supply from short‑term circulation.

At the same time, the protracted nature of the Mt. Gox process means that markets have had years to incorporate expectations about these future flows into pricing. Analysts tracking on‑chain data, exchange balances, and derivatives positioning routinely incorporate Mt. Gox scenarios into their models, assessing, for instance, how the release of 65,000 BTC to individual creditors might compare with typical daily spot and derivatives volume. In a market where hundreds of thousands of BTC can trade in a single day across spot and perpetual futures, the incremental impact of Mt. Gox distributions may be more muted than sensational headlines imply, especially if a significant share of the coins end up in the hands of long‑term allocators. The financialization of Mt. Gox thus cuts both ways: it turns a messy, idiosyncratic bankruptcy into quantifiable supply‑and‑demand variables, but it also embeds the legacy of that collapse into the structural features of modern Bitcoin markets.

Cultural and Psychological Legacy

“Getting Goxxed” as a shared memory

Beyond legal and financial dimensions, Mt. Gox occupies a powerful place in Bitcoin’s cultural memory. The phrase “getting Goxxed” became shorthand for losing funds due to an exchange failure, and for many early adopters, the collapse was a personal trauma as well as a financial loss. Discussions on forums and social media in the years following the collapse often feature users reflecting on how being “Goxxed” changed their approach to risk, custody, and trust. Some described it as a painful but formative experience that drove them to learn self‑custody and to adopt a more skeptical stance toward centralized intermediaries. Others expressed long‑lasting resentment toward the exchange’s management and frustration with the pace of legal redress.

The 2011 flash crash to one cent holds a similarly mythic status. Retellings of the event—when a single stolen password reportedly allowed a hacker to crash BTC from around 17 USD to 0.01 USD on Mt. Gox within minutes—serve as a reminder of just how fragile the early market was and how closely price formation was tied to the internal security of a single venue. For newer participants who encounter these stories years later, they function as parables about vigilance and the difference between Bitcoin’s technological resilience and the vulnerability of human‑run institutions. The fact that Bitcoin survived both the 2011 hacks and the 2014 collapse, ultimately going on to reach successive all‑time highs, reinforces a narrative of antifragility: the system can be wounded, sometimes severely, but seems to adapt and grow stronger.

Influence on narratives of decentralization and regulation

Mt. Gox also plays a central role in debates about the appropriate balance between decentralization and regulation in crypto. Proponents of stronger regulatory frameworks often point to Gox as proof that leaving large financial intermediaries unregulated invites disaster, arguing that basic standards for capital adequacy, custody segregation, and disclosure might have prevented or at least mitigated the loss. They note that traditional securities and derivatives markets, while not immune to fraud and failure, have developed extensive infrastructures—clearinghouses, custodians, auditors—that make Mt. Gox‑style blow‑ups less likely at scale. From this perspective, integrating crypto exchanges more fully into existing regulatory regimes is seen as a path toward protecting retail investors and legitimizing digital assets as a mainstream asset class.

On the other side, decentralization advocates see Mt. Gox as evidence that relying on centralized intermediaries is fundamentally at odds with Bitcoin’s ethos. For them, the lesson is not that exchanges should be regulated into safety but that users should minimize reliance on exchanges altogether, using them only as transient on‑ramps and off‑ramps while keeping long‑term holdings in self‑custodied wallets. They argue that no amount of regulation can fully eliminate the risk of mismanagement, hacking, or political interference at centralized entities and that the only robust solution is to reduce the amount of trust placed in such entities in the first place. The persistence of Mt. Gox in both sides of this debate speaks to its symbolic power: it is invoked both as justification for greater state involvement and as a cautionary tale against trusting any single institution too much.

Mt. Gox as a benchmark for future crises

Finally, Mt. Gox serves as a benchmark against which subsequent crypto crises are measured. When FTX collapsed, commentators immediately drew parallels, highlighting both similarities—such as commingling of funds and opaque accounting—and differences, such as the presence of more sophisticated institutional participants and a larger, more diversified exchange landscape. Likewise, when other venues suffer hacks, partial failures, or withdrawal freezes, journalists and analysts often ask whether the episode is “another Mt. Gox” or something less systemic. In this way, Gox functions as a reference event, akin to how the collapse of Lehman Brothers became shorthand for systemic financial contagion in traditional markets.

The recurring use of Mt. Gox as a frame for interpreting new events reinforces its status as a foundational myth in crypto culture. It anchors the community’s sense of how bad things can get and how resilient the ecosystem can be in the aftermath. For Bitcoin specifically, the fact that its protocol continued functioning flawlessly through the Gox collapse has become a key talking point: the failure was in the exchange, not the chain. That distinction, repeatedly stressed in educational materials and industry commentary, owes much of its force to the memory of Mt. Gox and the determination not to let a single venue’s mismanagement define an entire asset class.

A single court-appointed trustee controls tens of thousands of BTC on behalf of ~127,000 creditors, making the entire repayment process dependent on one centralized actor and one jurisdiction.

Tens of thousands of BTC distributed to creditors who have waited over a decade create real liquidation risk, though multiple large transfers in 2024–2025 passed without measurable price impact, suggesting the market has largely priced in the overhang.

Mt. Gox's collapse — triggered by years of undetected theft from a single exchange with no proof-of-reserves or external audit — remains the canonical example of exchange counterparty risk in crypto.

The civil rehabilitation process spans Japanese bankruptcy law, cross-border creditor eligibility checks across dozens of countries, and exchange compliance requirements at distribution partners like Bitstamp and Kraken, creating persistent procedural delays.

Remaining holdings of roughly 34,000–35,000 BTC represent a known but concentrated liquidity event; distributions are staggered through exchange partners rather than dumped on-chain, moderating spot impact.

Conclusion

The Mt. Gox saga encapsulates almost every major theme in Bitcoin’s evolution: rapid innovation outpacing governance and risk management, the dangers of centralization in a system designed for decentralization, and the complex interplay between protocol guarantees and human institutions. From its origins as a repurposed card‑trading site through its rise to handling over 70% of global BTC volume, Mt. Gox illustrates how a small, informal project can accidentally become systemically important when it sits at the nexus of liquidity and infrastructure in a young market. Its catastrophic collapse—triggered by years of undetected wallet drain and culminating in the disappearance of roughly 850,000 BTC—exposed the fragility of relying on a single, opaque custodian for what many users mistakenly believed were trustless digital assets.

In the decade since, the long, winding road of bankruptcy, civil rehabilitation, and delayed creditor repayments has highlighted both the strengths and limitations of using traditional legal systems to resolve disputes involving crypto assets. On‑chain transparency has allowed markets to monitor Mt. Gox wallet movements in real time, while court‑supervised processes have slowly translated a pile of coins into structured claims and repayment categories, mediated by exchanges such as Bitstamp and Kraken. Along the way, Mt. Gox has shaped debates about Bitcoin governance, inspiring controversial proposals for recovery forks and cleanup mechanisms that test the community’s commitment to immutability. It has also spurred concrete improvements in custody practices, the rise of self‑custody culture, and the development of more robust centralized and decentralized trading venues.

Most importantly, Mt. Gox has left a deep psychological imprint on the crypto community. The phrase “getting Goxxed” remains a cautionary reference point, reminding users that holding BTC on an exchange is fundamentally different from holding BTC in a personal wallet. At the same time, the fact that Bitcoin not only survived but flourished after Mt. Gox collapsed has become part of a broader story about the resilience of decentralized protocols in the face of institutional failure. As the final chapters of the rehabilitation process play out and the remaining coins are gradually distributed, Mt. Gox will continue to serve as both a warning and a guide: a warning about the costs of ignoring custodial risk and a guide to how crypto can evolve, structurally and culturally, to better align its infrastructure with its foundational ideals.

Outlook

Looking ahead, the remaining Mt. Gox repayments and their integration into global markets will likely be gradual rather than explosive. With repayment deadlines now extended to late 2026 and distributions structured across categories such as base and early lump‑sum repayments, the trustee has considerable room to manage flows in a way that minimizes market disruption. The roughly 140,000 BTC allocated for creditors, and the smaller portion expected to be actively sold, represent a modest fraction of daily global BTC trading volume, especially when spreads and derivative liquidity are taken into account. While individual transfer events may continue to produce headline‑driven volatility, the market’s growing sophistication and the diversification of liquidity across multiple exchanges and instruments make a single “Gox dump” moment increasingly unlikely.

At the same time, Mt. Gox will remain part of Bitcoin’s governance and cultural landscape. Proposals for recovery forks or cleanup mechanisms are unlikely to gain broad consensus in the near term, but they will continue to surface whenever large‑scale thefts or losses prompt calls for protocol‑level intervention. The community’s responses to such proposals will reveal how firmly committed Bitcoin remains to its ethos of immutability and how willing it is to tolerate pockets of unresolved injustice in the name of that principle. On the infrastructure side, the memory of Mt. Gox will continue to motivate improvements in custody, transparency, and user education, reinforcing the distinction between BTC held on centralized platforms and BTC held in self‑custodied wallets. For a crypto news audience, Mt. Gox will thus remain both a living story—shaping markets through ongoing creditor distributions—and a historical touchstone, against which future crises, reforms, and innovations will inevitably be measured.

Latest Mt. Gox news

From Mt. Gox to Hyperliquid: How crypto trading finally solved the trust problemMt. Gox moves 10,306 BTC, worth about $731M, to a new wallet after two months of inactivityMt. Gox moved 10,423 BTC after eight months of silence, fueling concerns but no signs of actual selling yet. Analysts say transfers alone are not sell pressure unless coins hit exchanges. Mt. Gox delays creditor repayments by another year to October 2026, citing incomplete eligibility procedures despite repaying 19,500 creditors and still holding 34,689 BTC.

Mt. Gox delays creditor repayments by another year to October 2026, citing incomplete eligibility procedures despite repaying 19,500 creditors and still holding 34,689 BTC. Vivek Ramaswamy’s Strive secures $750M to build Bitcoin treasury, acquire Mt. Gox claims, and deploy alpha strategies aiming to outperform BTC, signaling aggressive moves to impact supply dynamics.

Vivek Ramaswamy’s Strive secures $750M to build Bitcoin treasury, acquire Mt. Gox claims, and deploy alpha strategies aiming to outperform BTC, signaling aggressive moves to impact supply dynamics. Vivek Ramaswamy’s Strive aims to build a Bitcoin reserve by acquiring 75,000 Bitcoins (~$8 billion) from Mt. Gox bankruptcy claims.

Vivek Ramaswamy’s Strive aims to build a Bitcoin reserve by acquiring 75,000 Bitcoins (~$8 billion) from Mt. Gox bankruptcy claims.Sources

- https://trustwallet.com/blog/cryptocurrency/mt-gox-explained

- https://www.facebook.com/cryptosrus/posts/15-years-ago-bitcoin-crashed-to-001on-june-19-2011-a-compromised-mt-gox-account-/1636960601769102/

- https://www.instagram.com/reel/DYCSujfib3C/

- https://www.mtgox.com

- https://www.cybereason.com/blog/malicious-life-podcast-the-fall-of-mt.-gox-part-1

- https://x.com/CoinDesk/status/2068052445603967461

- https://www.facebook.com/cointelegraph/posts/-history-on-this-day-12-years-ago-mt-gox-collapsed-after-losing-850k-btc-marking/1230785915894901/

- https://www.mtgox.com/d/04y7ivbnz5gw.pdf

- https://es.tradingview.com/news/cointelegraph:22f58f8e9094b:0-mt-gox-moves-739m-in-bitcoin-from-cold-wallets-arkham/

- https://x.com/RoundtableSpace/status/1826202941948051689

- https://www.mtgox.com/img/pdf/20180622_announcement_en.pdf

- https://www.facebook.com/bloombergbusiness/posts/bitcoin-is-under-pressure-again-on-concerns-about-possible-sales-of-the-token-by/899037395415688/

- https://coinmetrics.substack.com/p/state-of-the-network-issue-268

- https://en.wikipedia.org/wiki/Mt._Gox

- https://phemex.com/news/article/arthur-hayes-reflects-on-early-bitcoin-arbitrage-and-founding-bitmex-66431

- https://cryptonews.net/news/bitcoin/30027186/

- https://www.coinspeaker.com/mt-gox-transfers-35m-bitcoin-unknown-addresses/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…