Deep explainer on Pakistan’s fast-evolving crypto scene, from new virtual asset laws and banking reforms to Trump-linked stablecoins, USDT promos, high grassroots adoption and the country’s role mediating U.S.–Iran tensions.

+13 sources across the wider coverage universe

State Bank of Pakistan lifts 8-year crypto ban, authorizes bank accounts for licensed VASPs2026-04

State Bank of Pakistan lifts 8-year crypto ban, authorizes bank accounts for licensed VASPs2026-04 Pakistan to allow Binance to explore 'tokenisation' of up to $2 billion of assets to boost liquidity and attract investors. The MOU agreement comes as Pakistan accelerates the rollout of a formal crypto regulatory framework and explores blockchain-based distribution of government-owned assets.2025-12

Pakistan to allow Binance to explore 'tokenisation' of up to $2 billion of assets to boost liquidity and attract investors. The MOU agreement comes as Pakistan accelerates the rollout of a formal crypto regulatory framework and explores blockchain-based distribution of government-owned assets.2025-12 Pakistan, Nigeria, Turkey, Japan... why emerging markets are turning to crypto2023-05

Pakistan, Nigeria, Turkey, Japan... why emerging markets are turning to crypto2023-05 Trump's World Liberty Financial partners with Pakistan Crypto Council to advance Blockchain and DeFi as Pakistan prepares crypto legalization2025-04

Trump's World Liberty Financial partners with Pakistan Crypto Council to advance Blockchain and DeFi as Pakistan prepares crypto legalization2025-04 Pakistan’s Finance Ministry will allocate 2,000 MW of surplus power for Bitcoin mining and AI centers, offering tax incentives to attract foreign firms2025-05

Pakistan’s Finance Ministry will allocate 2,000 MW of surplus power for Bitcoin mining and AI centers, offering tax incentives to attract foreign firms2025-05 Michael Saylor says he's open to advising Pakistan on its national crypto strategy2025-06

Michael Saylor says he's open to advising Pakistan on its national crypto strategy2025-06

Pakistan at the Crossroads of Crypto, Banking, and Geopolitics

Pakistan is a large South Asian economy and increasingly important crypto market where new virtual asset rules, high grassroots adoption, and fragile macro fundamentals intersect with U.S.–Iran tensions, dollar stablecoins, and evolving banking policy. For crypto investors and builders, it has become a test case for how an emerging-market state tries to harness digital assets while managing capital controls, sanctions risk, and religiously informed financial norms.

Pakistan’s journey from de facto crypto ban to a regulated, banked virtual-asset sector has unfolded in parallel with a broader digital transformation agenda and an unusual form of “crypto diplomacy” that has drawn in U.S. President Donald Trump’s stablecoin startup and placed Islamabad at the center of delicate U.S.–Iran negotiations. At home, regulators have created the Pakistan Crypto Council (PCC) and the Pakistan Virtual Assets Regulatory Authority (PVARA), passed the Virtual Assets Act 2026, and reversed a long‑standing banking prohibition that had walled crypto firms off from rupee payment rails. Abroad, Pakistan is now frequently ranked among the world’s top grassroots adopters of crypto, especially for retail usage and stablecoin flows, even as the State Bank of Pakistan insists that Bitcoin and other tokens remain outside the definition of legal tender. For market participants, Pakistan therefore offers both an opportunity and a caution: a large, young, digitally savvy population and strong remittance base, but also political volatility, complex regulatory layering, regional war risk, and close scrutiny from multilateral lenders and Western capitals.

Pakistan in Brief: From Frontier Economy to Digital Testbed

Geography, demographics, and development profile

Understanding Pakistan’s crypto trajectory first requires situating the country in its broader economic and geopolitical context. Pakistan is a populous state of more than 245 million people, making it one of the world’s largest countries and a major node in South Asia’s demography and trade. It straddles strategic routes between the Middle East, Central Asia, and the Indian Ocean, which shapes everything from its energy dependence on Gulf oil to its role as a potential corridor for overland and maritime trade. The economy is classified as lower‑middle‑income, with a large agricultural base, a sizable manufacturing sector, and growing services, including information technology and business process outsourcing. Chronic structural issues—such as fiscal deficits, narrow tax bases, and periodic balance‑of‑payments crises—have led Pakistan to rely recurrently on IMF programs and lender‑of‑last‑resort support.

In macro projections, the IMF has recently penciled in real GDP growth around \(3.6\%\) and consumer price inflation of roughly \(7.2\%\) for Pakistan, underscoring a modest recovery but continued price pressures. Such figures matter in crypto debates because persistent inflation and exchange‑rate volatility can drive households and small businesses to seek alternative stores of value and more stable currency exposure, including via Bitcoin or dollar‑linked stablecoins. At the same time, international financial institutions keep a close eye on capital flows, banking stability, and anti‑money‑laundering standards, which pushes Pakistani regulators toward relatively conservative, compliance‑oriented crypto rules. The country’s geography also embeds it in security and energy dilemmas: conflicts in the Persian Gulf, where much of its imported fuel originates, can quickly transmit into domestic inflation spikes and foreign‑exchange stress, conditions under which crypto prices and narratives often gain prominence.

Pakistan’s political system combines elected institutions with a powerful military establishment and a judiciary that has periodically intervened in civilian politics. This hybrid governance environment affects crypto policy in subtle ways. On one hand, it allows technocratic actors in the finance ministry, central bank, and digital‑policy bodies to push coherent regulatory agendas and engage with multilateral standard‑setters. On the other, it exposes policymaking to sudden shifts driven by coalition changes, security crises, or diplomatic realignments, such as those involving the United States, China, or Gulf monarchies. This mixture of strategic importance, macro fragility, and institutional pluralism makes Pakistan an instructive case for analysts of digital assets in emerging markets.

Banking system, financial inclusion, and digital payments

Pakistan’s banking system is bank‑centric but shallow when measured against advanced economies, with relatively low levels of private credit to GDP and significant segments of the population remaining unbanked or underbanked. Commercial banks are dominated by a mix of state‑owned institutions and large private players, supervised by the State Bank of Pakistan (SBP), the central bank that also manages monetary policy, exchange‑rate interventions, and payment systems. Traditional branch networks are complemented by microfinance banks and mobile money operators, but access gaps remain, especially in rural areas and among women. These gaps are crucial to the crypto story: when conventional banking is limited, alternative channels—from hawala networks to mobile wallets and, increasingly, crypto rails—become more attractive for moving and storing value.

The government has pushed for greater digitization of payments and expansion of fintech services, partly to improve tax collection and reduce leakages, and partly to foster financial inclusion and entrepreneurship. The Pakistan Digital Authority (PDA), created under the Digital Nation Pakistan Act 2025, serves as a central node for digital policy, data, and AI governance, and is now working with the DFINITY Foundation to build sovereign, AI‑native infrastructure for national‑scale applications. This includes a planned Pakistan‑specific “subnet” on DFINITY’s Internet Computer platform, intended to host tamper‑resistant software and public‑sector systems independent of foreign cloud providers. For crypto, this digital modernization agenda creates both opportunity and complexity: opportunity in the sense that robust digital ID, payments, and cloud infrastructure can support compliant virtual‑asset services; complexity because data‑sovereignty and security concerns may impose stricter localization and governance requirements on exchanges and wallets.

Remittances, hawala, and the dollar shortage problem

One of Pakistan’s defining macro features is its heavy reliance on remittances from a large diaspora, particularly in the Gulf, Europe, and North America. Workers’ remittances and compensation of employees constitute a significant share of current transfers, and over recent years personal remittances received have often hovered around the high single digits of GDP. World Bank data show that remittances as a percentage of GDP for Pakistan have remained elevated over a long period, underscoring their importance for household consumption, investment, and foreign‑exchange earnings. These flows act as a stabilizing force in times of export weakness or capital‑account stress, but they also expose Pakistan to regulatory changes in sending countries and to frictions in traditional money‑transfer channels.

Historically, a substantial portion of remittances has moved through informal mechanisms such as hawala or hundi, where a network of brokers (hundiwallahs) settle obligations via netting and trust rather than via formal banking channels. A Georgetown Law analysis of remittances notes Pakistan’s hawala system as a prominent example of such informal networks and argues that governments should reduce remittance costs and expand domestic banking networks to draw flows into regulated channels. For Pakistani authorities, crypto presents both a threat and an opportunity in this context. On one hand, unregulated crypto rails could replicate or even amplify the opacity of hawala, complicating AML/CFT efforts and undermining correspondent banking relationships. On the other, regulated, blockchain‑based remittance corridors and stablecoins could lower transfer costs, increase transparency, and integrate informal flows into the formal economy.

The dollar shortage is a recurring theme in Pakistan’s macro narrative. Limited export diversification, energy imports priced in dollars, and external debt obligations often strain foreign‑exchange reserves, prompting periodic currency devaluations and restrictions on capital outflows. Retail users seeking dollar exposure have sometimes turned to unofficial markets, including cash dollars, gold, or offshore bank accounts, when accessible. Crypto, particularly dollar‑pegged stablecoins like USDT, has emerged globally as a digital alternative for such hedging and dollar access, and Pakistan is no exception. The combination of remittance dependence, hawala traditions, and FX bottlenecks makes stablecoins especially salient in Pakistan’s crypto ecosystem, as discussed in later sections.

Why this backdrop matters for crypto

Together, these structural features—large youth population, relatively low financial inclusion, significant remittances, and repeated FX crunches—create fertile ground for crypto adoption. Chainalysis’s 2025 Global Crypto Adoption Index places Pakistan among the top countries worldwide in grassroots crypto usage, alongside India, the United States, Vietnam, and Brazil, with the Asia‑Pacific region as a whole recording a \(69\%\) year‑over‑year increase in on‑chain activity. Crucially, Chainalysis emphasizes not only centralized exchange volumes but also decentralized and peer‑to‑peer usage, suggesting that users in Pakistan employ crypto across a spectrum of activities from speculation to savings and informal payments.

However, the same factors also make regulators cautious. Heavy reliance on remittances and external financing means Pakistan cannot easily afford to alienate international banks or run afoul of the Financial Action Task Force (FATF) and IMF expectations on AML/CFT and capital‑flow management. The central bank’s historical position that cryptocurrencies are not legal tender, and that banks must not deal directly in them, reflects this sensitivity. The policy challenge has therefore been to craft a framework that channels crypto activity into licensed, supervised entities without cutting off innovative use cases or driving users further into informal or offshore venues.

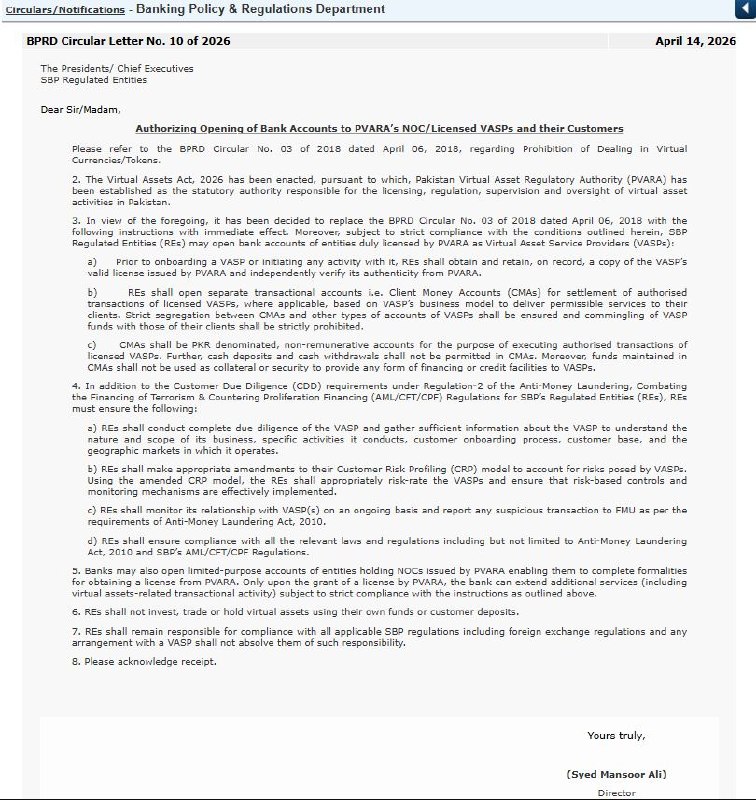

State Bank of Pakistan lifts 8-year crypto ban, authorizes bank accounts for licensed VASPs

State Bank of Pakistan just killed its 2018 crypto prohibition with BPRD Circular No. 10 — banks can now open dedicated rupee-only Client Money Accounts for VASPs licensed by the newly-created PVARA under the Virtual Assets Act 2026. Heavy guardrails though: no cash deposits, no interest, no use as collateral, and banks themselves remain banned from trading or holding any virtual assets. Enhanced due diligence and full AML compliance are mandatory, making this a carefully regulated thaw for one of the world's biggest crypto-using populations rather than a green light to go wild.

Readers clicked Pakistan stories not for retail adoption but for state-level crypto statecraft — the pattern shows a country deploying digital assets as a diplomatic instrument to buy influence with the Trump orbit, attract foreign capital, and offset IMF austerity with mining revenue.↗

Building a Crypto Policy Framework

From informal ban to cautious engagement

Pakistan’s early stance on crypto was broadly prohibitive. In 2018 the State Bank of Pakistan issued a circular instructing regulated financial institutions not to provide services to individuals or entities dealing in cryptocurrencies, effectively cutting local crypto exchanges and brokerages off from the formal banking system. While the circular did not criminalize individual holding or peer‑to‑peer trading per se, the inability to access bank accounts in rupees meant that most formalized platforms either shut down, moved offshore, or operated in a grey zone using informal payment intermediaries. This period formed the backdrop for Pakistan’s high level of grassroots crypto adoption despite weak domestic infrastructure, as users turned to global exchanges, over‑the‑counter brokers, and P2P platforms that were often beyond the reach of domestic regulators.

At the same time, Pakistani authorities were under pressure to improve AML/CFT controls and exit FATF’s “grey list,” which further constrained their appetite for embracing unregulated digital assets. The SBP repeatedly emphasized that virtual currencies and tokens were not recognized as legal tender and that existing banking laws prohibited institutions from dealing in them. This stance aligned with cautious positions in several other emerging markets and was meant to prevent potential misuse of crypto for illicit purposes, tax evasion, or capital flight. However, it also fostered a disconnect between on‑the‑ground adoption and formal regulation, a gap that became increasingly untenable as the scale of domestic crypto activity and the global prominence of the sector grew.

Over time, policymakers began to experiment with more nuanced approaches. Pilot projects in blockchain for land records, identity, and supply‑chain management signaled that the government recognized the underlying technology’s utility even as it continued to restrict open crypto markets. Advisory committees and inter‑agency working groups, involving the finance ministry, SBP, the Securities and Exchange Commission of Pakistan (SECP), and other federal bodies, started exploring frameworks for digital assets that could balance innovation with oversight. It was within this context that the Pakistan Crypto Council (PCC) and later the Pakistan Virtual Assets Regulatory Authority (PVARA) emerged.

The Pakistan Crypto Council and early policy experiments

Formally announced by the finance ministry in late February 2025 and launched in March of that year, the Pakistan Crypto Council is a regulatory body tasked with developing policy, infrastructure, and regulation for blockchain technology and digital assets. The PCC operates under the Ministry of Finance but draws input from the SBP, SECP, and other agencies, with a mandate that includes advising on legal frameworks, supporting pilot projects, and engaging with industry stakeholders. This institutionalization of crypto policy represented a shift from ad hoc, primarily prohibitive stances toward a more structured, consultative approach.

The PCC’s creation coincided with Pakistan’s recognition that crypto was not a niche phenomenon that could simply be banned away. Chainalysis data showing Pakistan near the top of global adoption rankings reinforced the idea that large numbers of citizens were already interacting with crypto, whether regulators liked it or not. In that environment, the PCC’s role included mapping existing usage patterns, identifying risks, and proposing regulatory pathways for exchanges, custodians, and other virtual asset service providers (VASPs). The council also served as a bridge between Pakistan’s domestic policy debate and international regulatory conversations, such as those taking place at the FATF, the Basel Committee, and IOSCO.

One of the PCC’s distinctive features has been its openness to integrating Islamic finance perspectives into crypto policy design. Given that a significant portion of Pakistan’s financial system and political discourse is informed by Shariah principles, any framework for digital assets must grapple with questions around speculation (maysir), uncertainty (gharar), and interest (riba). While there is no single Islamic jurisprudential view on cryptocurrencies, the PCC and associated advisory bodies have explored how tokenized assets, profit‑and‑loss sharing instruments, and asset‑backed stablecoins might be structured to align with Islamic ethics, an issue that would later become more explicit in PVARA’s mandate.

The Virtual Assets Ordinance 2025 and birth of PVARA

The next major step came in July 2025, when the government issued the Virtual Assets Regulatory Authority Ordinance, creating the Pakistan Virtual Assets Regulatory Authority as an independent regulator for virtual assets. This ordinance, a form of presidential decree, gave PVARA initial powers to license and supervise VASPs, set conduct rules, and coordinate on AML/CFT matters. The creation of a dedicated authority reflected both the scale of crypto activity and the desire to avoid overstretching existing regulators like the SBP and SECP, whose mandates already spanned banking, securities, and insurance.

PVARA’s initial remit included overseeing exchanges, custodial wallets, and other intermediaries dealing in “virtual assets,” a broad category that encompasses cryptocurrencies, tokens, and certain forms of digital representations of value. The authority was tasked with designing regulations that would ensure consumer protection, market integrity, and systemic stability while facilitating innovation and aligning with both international standards and Islamic finance principles. From the outset, PVARA’s leadership and staff interacted closely with the PCC and other agencies, creating an ecosystem of overlapping but complementary bodies focused on different aspects of digital‑asset oversight.

However, ordinances are by nature temporary and must be ratified by Parliament to gain lasting statutory force. Over the next year, debates unfolded over how far Pakistan should go in legitimizing crypto, under what conditions banks should be allowed to interact with VASPs, and how to structure safeguards against money laundering, terrorism financing, and sanctions evasion. These discussions were influenced not only by domestic considerations but also by Pakistan’s evolving diplomatic relationships and the increasing involvement of external actors, including U.S. political figures and global crypto firms, as explored in later sections.

The Virtual Assets Act 2026: from ordinance to statute

Parliament’s passage of the Virtual Assets Act 2026 marked the conversion of the earlier ordinance into a full legislative framework and cemented PVARA’s status as a statutory authority. The Act formally established PVARA as the body responsible for licensing, regulating, and supervising VASPs operating in Pakistan and endowed it with powers to create rules aimed at transparency, investor protection, and market integrity. It also explicitly equipped the authority with tools to combat money laundering, terrorist financing, and other illicit activities involving virtual assets, thereby aligning Pakistan’s approach more closely with FATF recommendations.

Under the new law, VASPs are required to obtain a license from PVARA, comply with AML/CFT obligations such as customer due diligence and suspicious transaction reporting, and adhere to prudential and conduct standards. PVARA, in turn, is empowered to carry out inspections, impose fines, suspend or revoke licenses, and coordinate with domestic and foreign regulators. The Act signals that virtual assets are to be integrated into Pakistan’s regulatory perimeter, rather than existing in a legal vacuum, even as they remain excluded from the category of sovereign legal tender.

A critical consequence of the Virtual Assets Act was its enabling role in the reversal of the SBP’s 2018 banking ban. By creating a clear licensing regime for VASPs and a dedicated supervisory authority, the law provided the central bank with a framework within which it could permit regulated banks to serve crypto firms without compromising on prudential and AML/CFT standards. The linkage between PVARA’s licensing decisions and SBP’s banking rules is a central axis of Pakistan’s new crypto architecture.

Legal tender, Shariah finance, and the “grey area”

Despite these advances, Pakistan has not gone so far as to recognize Bitcoin or other cryptocurrencies as legal tender. The SBP has reiterated that digital currencies are not legal tender in Pakistan, and existing banking laws continue to bar institutions from directly dealing in them. This means that, even under the Virtual Assets Act, crypto remains a distinct asset class rather than a parallel currency, and its use in everyday commerce is mediated by intermediaries and constrained by regulatory norms.

The distinction between regulated virtual assets and legal tender is particularly important in an Islamic finance context. Some Shariah scholars in Pakistan have expressed concerns that unbacked, highly volatile cryptocurrencies could amount to gambling or excessive uncertainty, which would conflict with Islamic principles. Others, however, argue that cryptocurrencies are a legitimate form of property (mal) and can be permissible if used in ethical ways and backed by real economic activity. PVARA’s mandate to align its framework with Islamic finance standards indicates that such debates are not purely academic; they influence how products are structured, how leverage and derivatives are treated, and how stablecoins or tokenized assets might be designed to satisfy Shariah boards.

For everyday users, the result is a “grey area” in which holding and trading crypto through licensed platforms is increasingly normalized, but the boundary between acceptable investment, speculation, and quasi‑currency use remains contested. Merchants may be hesitant to accept direct crypto payments due to legal and tax uncertainties, while individuals may use stablecoins informally for savings or cross‑border transfers without clear guidance on their status. This ambiguity creates space for innovation but also for regulatory arbitrage and consumer confusion, themes that recur in discussions of Pakistan’s crypto markets.

Opening the Banking Pipes: Reversal of the 2018 Ban

What the 2018 banking prohibition did in practice

The SBP’s 2018 circular barring banks from servicing crypto‑related businesses had far‑reaching practical consequences. Without access to rupee accounts, local exchanges struggled to comply with AML/CFT standards, manage fiat on‑ and off‑ramps, or maintain transparent operations. Many platforms shut down, relocated abroad, or pivoted to informal payment channels, essentially shifting risk from supervised intermediaries to a more opaque ecosystem of peer‑to‑peer brokers and cash‑based transfers. The ban also discouraged mainstream financial institutions and fintechs from experimenting with blockchain or tokenization projects that could touch crypto markets, out of fear of regulatory backlash.

At the same time, the prohibition did not eliminate demand. Retail users continued to access global exchanges using foreign bank accounts, e‑money services, or third‑party payment processors. Others turned to P2P marketplaces, where local buyers and sellers matched fiat and crypto transactions bilaterally, often using bank transfers disguised as unrelated payments. This parallel market limited the authorities’ visibility into crypto flows and hindered their ability to enforce consumer protection or address fraud. The longer the ban persisted, the more apparent it became that a purely exclusionary approach was neither sustainable nor conducive to broader financial‑sector development.

The new SBP circular and its limitations

Against this backdrop, the SBP’s decision to lift the 2018 banking ban and allow licensed banks to serve crypto firms under strict conditions represents a fundamental policy pivot. The central bank issued a circular reversing the earlier prohibition and permitting banks to open accounts for virtual asset service providers, provided those entities are licensed by PVARA under the Virtual Assets Act 2026. This move transforms crypto firms from pariahs to regulated clients within the formal financial system, albeit with ongoing constraints.

The new framework enables banks to provide basic financial services—such as current accounts in Pakistani rupees, payment processing, and fiat custody—for PVARA‑licensed VASPs, while mandating comprehensive due diligence and risk‑management practices. Banks must verify that a prospective crypto client holds a valid PVARA license, assess its business model and risk profile, and monitor transactions for suspicious activity, reporting such cases to regulators as required. They are also obliged to maintain updated risk assessments for each VASP and engage in ongoing monitoring, reflecting the dynamic nature of crypto markets and associated risks.

However, the SBP has drawn a firm line on banks’ own exposure to digital assets. Under the new rules, banks are explicitly barred from investing in, trading, or holding cryptocurrencies using either their own capital or customer deposits. Their role is limited to facilitating fiat payment rails and providing custody of rupee funds linked to licensed crypto activity. Client funds must be held in segregated, non‑interest‑bearing accounts denominated in Pakistani rupees, and the commingling of customer and company funds is strictly prohibited. This ensures that banks do not assume market risk from crypto price fluctuations or expose depositors to speculative losses, while still allowing them to earn fee‑based income from servicing VASPs.

Compliance expectations for banks and VASPs

The regulatory trade‑off embedded in this framework is clear: Pakistan is willing to re‑bank the crypto sector as long as both banks and VASPs operate within a tightly supervised, AML‑compliant perimeter. For banks, this means upgrading their transaction‑monitoring systems to handle the peculiarities of crypto‑linked flows, such as large, rapid movements between exchanges, fiat ramps, and stablecoin wallets. It also implies closer collaboration with PVARA, including information‑sharing and joint inspections when necessary. For VASPs, licensing by PVARA is not a one‑time formality but an ongoing relationship involving audits, reporting, and adherence to evolving regulatory standards.

CrowdfundInsider’s analysis of Pakistan’s new framework underscores how these rules could benefit consumers and local businesses by enabling safer, more accessible crypto services, but also notes that practical challenges remain in implementation and supervisory capacity. Ensuring that smaller banks and fintechs have the tools and expertise to evaluate crypto risks is non‑trivial, especially in a context where many have limited historical exposure to the sector. There is also the question of how PVARA and SBP will coordinate if a licensed VASP faces a liquidity crunch, security breach, or mass customer complaint; mechanisms for crisis management and resolution will be tested over time.

Reactions from markets and industry

Market reaction to the lifting of the banking ban has been broadly positive. News outlets highlighted Pakistan’s decision to end a seven‑ to eight‑year prohibition and ranked the country among top global crypto adoption hubs, emphasizing the potential for a more regulated and integrated digital‑asset market. Islamic finance commentators have welcomed the prospect of bringing crypto activity under Shariah‑sensitive oversight, particularly through PVARA’s mandate to align with Islamic standards. Domestic entrepreneurs view the banking opening as a chance to launch compliant exchanges, custodians, and fintech products tailored to local needs, from remittance‑linked wallets to SME financing platforms.

Internationally, global exchanges and service providers have taken note. Binance, for example, launched a Pakistan‑specific campaign titled “Game of Referrals,” offering \(25{,}000\) USDT in token vouchers to users who invite friends and family to sign up and trade during a limited period in June 2026, with rewards distributed via a leaderboard of top referrers. Such promotions underscore how major offshore platforms see Pakistan as a growth market now that local users can more easily link bank accounts to crypto activity. They also raise regulatory questions about cross‑border offerings, taxation of promotional rewards, and consumer protection in a landscape where the most visible brands are often foreign.

Pakistan’s position among regional competitors

In regional context, Pakistan’s shift aligns it more closely with a group of Asian jurisdictions that have moved from bans or severe restrictions toward more permissive but regulated environments. Chainalysis’s data show that the Asia‑Pacific region is the fastest‑growing area for on‑chain crypto activity, with a \(69\%\) year‑over‑year increase in value received, led by India, Pakistan, and Vietnam. While heavyweight hubs like Singapore and Hong Kong compete on institutional and wholesale markets, Pakistan’s niche is more on the retail and remittance side, where its large diaspora, mobile penetration, and informal finance traditions give it unique characteristics.

By allowing banks to serve licensed VASPs but prohibiting direct crypto investment on their balance sheets, Pakistan’s model resembles that of other emerging markets that aim to minimize systemic risk while capturing some fintech upside. Compared with outright bans, this approach is more attractive to legitimate operators and reduces the incentives for users to seek offshore workarounds. Compared with fully open regimes, it retains strong levers for AML/CFT control and macroprudential oversight. Over time, Pakistan’s ability to refine this balance, and to harmonize PVARA’s rules with those of SBP, SECP, and international partners, will determine whether it can sustain its position as a major crypto‑adoption hub without destabilizing its financial system.

- 01emerging-market crypto escape valve↗

The highest-clicked story framed Pakistan alongside Nigeria, Turkey, and Japan as countries where currency instability and remittance costs make crypto a rational hedge, not a speculative toy.

- 02Trump World Liberty Financial diplomacy↗

Two separate WLF-Pakistan MOU stories combined for 166 clicks, signaling readers tracking how a US presidential crypto venture became a foreign-policy handshake.

- 03Bitcoin mining on surplus power↗

Pakistan's offer of 2,000 MW of stranded electricity plus tax incentives pitched mining as an industrial-policy story, not just a crypto story, drawing readers interested in state-backed hash rate.

- 04Saylor and US advisory interest

Michael Saylor publicly offering to advise Pakistan on national crypto strategy validated the country's pivot as credible to a US Bitcoin-maximalist audience.

- 05Binance tokenisation MOU↗

A government-to-exchange deal to tokenise up to $2B of state assets attracted readers who see sovereign tokenisation as a liquidity unlock with systemic implications.

- 06PVARA licensing framework↗

Pakistan opening its new regulator to globally licensed firms and 40 million existing users signalled a frontier-market on-ramp story with real scale.

Adoption on the Ground: Users, Use Cases, and Platforms

Pakistan in global crypto adoption rankings

Empirical data from blockchain analytics firms confirm Pakistan’s status as a leading adopter of crypto on a per‑capita and income‑adjusted basis. Chainalysis’s 2025 Global Crypto Adoption Index ranks Pakistan in the top tier of countries worldwide, alongside India, the United States, Vietnam, and Brazil, when measuring grassroots adoption across centralized services, DeFi protocols, and peer‑to‑peer markets. When the data are adjusted purely for population size, some Eastern European countries move to the top, but Pakistan remains a standout case in the Global South, illustrating how large numbers of users have integrated crypto into their financial lives despite regulatory ambiguity.

The composition of Pakistan’s crypto usage likely mirrors global emerging‑market patterns: a mix of speculative trading, longer‑term holding of Bitcoin and large‑cap altcoins, use of stablecoins as synthetic dollar savings, and participation in P2P marketplaces to move funds domestically and across borders. Retail dominance does not preclude the presence of more sophisticated actors; local trading groups, arbitrageurs, and even small OTC desks have emerged to serve affluent clients and businesses. However, systematic data on institutional participation remain limited, especially given the historically hostile banking environment prior to the 2026 reforms.

Exchanges, P2P markets, and offshore platforms

Before the lifting of the banking ban, most Pakistani users interacted with crypto via offshore exchanges and P2P platforms, often using informal payment methods. International exchanges such as Binance have been particularly prominent, offering localized user interfaces, Urdu language support, and targeted marketing campaigns. Binance’s Pakistan‑exclusive USDT referral program, with reward boxes of \(3\)–\(6\) USDT per referral and a \(5{,}000\) USDT pool for top referrers, exemplifies how global platforms tailor promotions to capture market share among Pakistani users. These campaigns improve onboarding but can also encourage speculative trading by inexperienced users drawn by short‑term incentives.

P2P marketplaces, sometimes integrated into large exchanges’ interfaces and sometimes operating independently, have allowed users to match with local buyers or sellers who accept bank transfers, mobile money, or cash in exchange for crypto. Such markets are attractive in environments with limited formal on‑ramps but carry their own risks, including counterparty default, fraud, and legal uncertainty. They also challenge regulators’ ability to monitor flows, since they often involve small, fragmented transactions executed outside licensed VASPs. As local exchanges and brokers obtain PVARA licenses and secure banking relationships, policy makers hope to shift more volume into supervised channels, but P2P will likely remain important for users who prefer anonymity or live in regions with weak bank coverage.

Stablecoins, USDT, and everyday dollar access

Stablecoins play a central role in Pakistan’s crypto ecosystem, mirroring trends across much of the Global South. Tether’s USDT, the dominant dollar‑pegged stablecoin globally, functions as a de facto digital dollar for traders and savers, offering a liquid unit of account and medium of exchange denominated in a currency that many view as more stable than the local rupee. Promotions like Binance’s USDT‑denominated referral rewards reinforce this centrality, since they encourage users to hold and transact in USDT rather than immediately converting all balances back into rupees.

For individuals facing currency devaluation or difficulty accessing physical dollars, stablecoins provide a convenient way to hold value, make cross‑border payments, or participate in global markets without opening foreign bank accounts. For remittance corridors, sending USDT from a worker in Dubai to a family in Lahore can be cheaper and faster than traditional wire transfers, especially if both sides are comfortable using exchanges or wallets. However, this also raises regulatory concerns about unrecorded capital flows, potential misuse for illicit purposes, and consumer exposure to stablecoin issuer risk, including questions about reserves and redemption. Pakistan’s evolving framework has yet to fully resolve how stablecoins will be categorized and overseen, especially those issued abroad and accessed through offshore platforms.

In parallel, new entrants like World Liberty Financial’s USD1 stablecoin—tied to a controversial but high‑profile U.S. political figure—have added geopolitical nuance to the stablecoin landscape, as discussed later. For now, USDT and similar tokens remain dominant in trading pairs and P2P markets, but regulatory and diplomatic developments could reshape this equilibrium.

Remittances, savings, and inflation hedging

One of the most promising but complex use cases for crypto in Pakistan is remittances. As noted earlier, remittances constitute a large share of GDP and are vital for many households’ livelihoods. Traditional channels, such as bank wires and money‑transfer operators, can be slow and expensive, especially for small‑ticket transfers. Crypto remittances, by contrast, allow senders to convert local currency into stablecoins or major cryptocurrencies, transmit them over a blockchain, and have recipients cash out through local exchanges or P2P brokers, often at lower cost and higher speed.

Academic work on remittances suggests that governments should both reduce the cost of sending money and expand domestic banking networks to maximize developmental benefits. Crypto can potentially contribute to both objectives, but only if integrated into a regulated framework that ensures consumer protection and linkages with domestic financial services, such as savings accounts, credit, and insurance. Without such integration, crypto remittances risk staying within an informal, speculative loop, offering short‑term cost savings but little long‑term financial deepening.

Beyond remittances, crypto also serves as a savings vehicle and inflation hedge for some Pakistanis. When domestic inflation erodes purchasing power and the rupee depreciates, holding Bitcoin or dollar‑linked stablecoins can appear attractive as an alternative store of value. This behavior is evident in many emerging markets, where periods of macro stress often correlate with spikes in crypto trading volumes and stablecoin adoption. The flip side is that crypto prices are themselves highly volatile, particularly for non‑stablecoin assets, and sudden market downturns can wipe out savings for households that lack diversification or financial literacy. Regulators therefore face a balancing act between enabling access and preventing predatory practices.

Risks for retail users

For retail users in Pakistan, the risks associated with crypto are multifaceted. Market volatility remains the most obvious: Bitcoin and other cryptocurrencies can experience double‑digit percentage swings within days, exposing leveraged traders and even unleveraged holders to significant drawdowns. Stablecoins mitigate price volatility but introduce counterparty and regulatory risk. Hacks, phishing attacks, and scams are pervasive, and users unfamiliar with private key management or security best practices can easily lose funds.

Regulatory risk is another factor. Although Pakistan has moved toward a more permissive framework, policy reversals or sudden enforcement actions remain possible, particularly in response to external pressure or domestic political shifts. Users who rely heavily on offshore platforms face additional uncertainty, since foreign regulators could intervene in those platforms’ operations or restrict services in certain jurisdictions. Consumer‑protection frameworks in Pakistan are still evolving, and mechanisms for redress in cases of fraud or platform insolvency are limited, especially when dealing with non‑licensed entities.

Education and transparent communication will be critical if Pakistan is to harness crypto’s benefits for inclusion and innovation while minimizing harm. This includes not only technical literacy but also understanding of tax obligations, reporting requirements, and the difference between regulated and unregulated service providers. PVARA, PCC, and industry players all have roles to play in this domain.

Pakistan to allow Binance to explore 'tokenisation' of up to $2 billion of assets to boost liquidity and attract investors. The MOU agreement comes as Pakistan accelerates the rollout of a formal crypto regulatory framework and explores blockchain-based distribution of government-owned assets.

“The MoU establishes a framework for exploring potential collaboration on the tokenization and blockchain-based distribution of Pakistan’s real-world and sovereign assets, including government bonds, treasury bills, commodity reserves and other federally owned assets,” the finance ministry said. “Subject to applicable laws, policies and regulatory approvals, the initiative may involve assets of up to USD 2 billion, with the objective of enhancing liquidity, transparency and international market accessibility.”

Crypto Diplomacy: Trump, Iran, and Pakistan’s New Leverage

The World Liberty Financial USD1 stablecoin arrangement

Perhaps the most unusual aspect of Pakistan’s crypto story is its intersection with high‑stakes geopolitics and U.S. domestic politics. In January, Zach Witkoff, the young CEO of World Liberty Financial (WLF), a crypto finance firm co‑founded by U.S. President Donald Trump, signed an agreement in Islamabad with Pakistan’s finance minister that would allow WLF’s USD1 stablecoin to be used for Pakistan’s cross‑border transactions. The agreement is non‑binding and exploratory, according to reporting, but it carries potentially significant implications given its association with a sitting U.S. president and the prospect of integrating a privately issued dollar stablecoin into a sovereign payments framework.

A Central Banking article describes how Pakistan’s central bank would integrate USD1 into the country’s payment systems, enabling its use in certain cross‑border flows while presumably maintaining oversight mechanisms. The optics of Witkoff’s visit underscored its political weight: media reports noted that Pakistan’s top civilian and military leaders gathered in an ornate building in Islamabad to welcome him, creating an atmosphere more akin to a state visit than a routine fintech MoU. The fact that the deal did not involve immediate large‑scale financial commitments did little to dampen speculation about its strategic significance.

For Pakistan, the attraction of such a partnership lies partly in access to a dollar‑denominated digital instrument that could facilitate trade and remittances without relying exclusively on traditional correspondent banking channels, which are vulnerable to sanctions and de‑risking. For Trump and his associates, it offers a chance to promote a signature crypto project on the global stage and reinforce their narrative of financial innovation and strength. However, the entanglement of a sovereign payment system with a politically connected private stablecoin also raises concerns about conflicts of interest, regulatory capture, and long‑term dependence on a product tied to a specific administration.

Pakistan’s mediation role between Washington and Tehran

The WLF deal did not occur in a vacuum; it is intertwined with Pakistan’s role as a mediator between the United States and Iran during a period of heightened tensions. Reports indicate that Pakistan has hosted talks between U.S. and Iranian officials, with its leadership mediating over issues such as the blockade of the Strait of Hormuz and broader regional security. Senior figures like Pakistan’s army chief and prime minister have engaged with U.S. counterparts, and Trump has publicly thanked Pakistan’s leadership for their diplomatic efforts, highlighting the country’s evolving role in U.S. Middle East policy.

Media coverage has coined terms like “crypto diplomacy” and “biplomacy” to describe how Pakistan’s engagement with WLF and the broader Trump circle has helped it gain a seat at the table in U.S.–Iran negotiations, with 35‑year‑old crypto entrepreneur Bilal Bin Saqib portrayed as a key navigator of these ties. Bilal, who serves as chairman of PVARA and CEO of the PCC, has been cast as a bridge figure connecting Pakistan’s technocratic elite, global crypto networks, and Trump’s inner circle. While such narratives may exaggerate any one individual’s influence, they underscore how digital assets have become entangled with high‑level diplomacy and strategic bargaining.

Pakistan’s mediation role is not purely symbolic. The closure or reopening of the Strait of Hormuz directly affects its energy imports, inflation trajectory, and external balances. Successful de‑escalation can relieve pressure on fuel prices and currency markets, while failure risks compounding economic stress. Pakistan thus has material incentives to facilitate dialogue and leverage any channels available—including those opened through crypto partnerships—to encourage compromise.

Market reactions: Bitcoin, risk sentiment, and headlines

Crypto markets have reacted in real time to developments in Pakistan‑mediated talks and related announcements. Coverage from financial news outlets has highlighted episodes where Bitcoin’s price surged amid optimistic updates from Pakistani leaders on Iran peace talks, with one report noting BTC climbing above \(64{,}000\) USD after Prime Minister Shehbaz Sharif’s positive comments on progress. Conversely, reports of talks stalling or U.S. threats to blockade the Strait of Hormuz have coincided with risk‑off sentiment and declines in major crypto assets, including Bitcoin and XRP, as investors reassessed geopolitical risk.

These episodes illustrate how Pakistan, once a marginal player in global markets, has become a conduit through which macro and geopolitical signals are transmitted into crypto prices. Traders increasingly watch headlines from Islamabad alongside those from Washington, Tehran, or Riyadh when gauging near‑term volatility. While it would be overstated to claim that Pakistan alone drives crypto markets, its role as a mediator in a critical energy chokepoint and as a partner in high‑profile stablecoin initiatives ensures that its moves are priced into broader sentiment.

From a structural perspective, such linkages reinforce the notion that crypto is not decoupled from geopolitical realities. The value proposition of Bitcoin as “digital gold” or a hedge against political turmoil is dynamically tested by events like Middle East conflicts, sanctions regimes, and diplomatic breakthroughs. Pakistan’s actions contribute to this ongoing test and shape narratives about crypto as both a hedge and a risk asset.

Domestic debates on sovereignty and alignment

Within Pakistan, the WLF deal and broader crypto diplomacy have sparked debates about sovereignty, alignment, and the appropriate balance between courting U.S. favor and maintaining strategic autonomy. Critics worry that integrating a Trump‑linked stablecoin into national payments could give undue leverage to one political faction in the United States and entangle Pakistan’s financial infrastructure with the fortunes of a particular administration. They also question whether reliance on a privately issued dollar token could complicate relationships with other partners, including China and Gulf states, or expose Pakistan to political pressure if future U.S. policymakers take a different stance.

Proponents counter that Pakistan must pragmatically seize opportunities to modernize its financial system and diversify access to dollar liquidity, particularly in the face of repeated IMF programs and vulnerability to sanctions. They argue that PVARA, SBP, and other institutions can build safeguards into any stablecoin integration, such as limits on usage, clear redemption mechanisms, and contingency plans in case of issuer default. Some view the WLF engagement as a bargaining chip that strengthens Pakistan’s hand in negotiations over aid, trade, and security cooperation.

These debates mirror global discussions about the role of U.S. dollar stablecoins in emerging markets, including concerns about monetary sovereignty, capital‑flow volatility, and regulatory dependence on U.S. agencies. Pakistan’s case is distinctive mainly because of the direct involvement of a sitting U.S. president’s business venture and the explicit linkage to geopolitical negotiations.

Long-term implications for sanctions and compliance

From a compliance perspective, Pakistan’s embrace of a Trump‑linked stablecoin and its broader crypto diplomacy raise complex questions about sanctions, FATF standards, and relationships with Western regulators. On one hand, closer alignment with U.S. political and business interests could reduce the risk of unilateral sanctions and improve access to dollar‑based instruments, provided Pakistan adheres to Washington’s expectations on security and AML/CFT. On the other, any perception that Pakistan is facilitating sanctions evasion by third parties, such as Iran or non‑state actors, via crypto rails could trigger scrutiny or punitive measures.

PVARA’s mandate to address money laundering and terrorist financing, and the Virtual Assets Act’s emphasis on aligning with international standards, suggest that Pakistani regulators are keenly aware of these risks. The authority’s challenge will be to demonstrate that its oversight of stablecoin usage and cross‑border flows meets or exceeds FATF expectations, including travel‑rule implementation and beneficial‑ownership transparency. For crypto businesses and investors, Pakistan’s trajectory on these issues will be a key determinant of how sustainable and scalable its virtual‑asset ecosystem becomes.

Pakistan Crypto Council founded; Bilal Bin Saqib named CEO

Bilal Bin Saqib brokers Pakistan-Trump orbit introductions, WLF MOU signed

Pakistan announces 2,000 MW surplus power allocation for Bitcoin mining and AI

Binance signs MOU with Pakistan for tokenisation of up to $2B in state assets

Pakistan hosts US-Iran nuclear talks; crypto diplomacy credited as enabling access

Parliament passes Virtual Assets Act, formally establishing PVARA

State Bank of Pakistan lifts eight-year ban, authorises banks to serve PVARA-licensed VASPs

Institutions and Infrastructure: PVARA, PCC, PDA, and Sovereign Cloud

Mandate and governance of PVARA

The Pakistan Virtual Assets Regulatory Authority sits at the center of the country’s new crypto regime. As established under the Virtual Assets Ordinance 2025 and later codified in the Virtual Assets Act 2026, PVARA is responsible for licensing VASPs, issuing rules and guidance, and supervising compliance with regulatory requirements. Its remit covers a wide range of entities, including exchanges, custodians, brokers, and certain wallet providers, and it is empowered to enforce AML/CFT standards, consumer‑protection norms, and prudential safeguards.

PVARA’s governance structure aims to balance independence with coordination. While it is an autonomous authority, it operates within a broader ecosystem that includes the Finance Ministry, SBP, SECP, and other agencies with stakes in financial stability and market integrity. Regular inter‑agency committees and memoranda of understanding facilitate information‑sharing and joint decision‑making, especially on issues such as bank‑VASPs relationships, securities‑token classification, and cross‑border cooperation. PVARA also engages with international bodies and foreign regulators to exchange best practices and stay aligned with evolving standards.

One of the authority’s notable features is its explicit mandate to ensure that its framework is compatible with both international norms and Islamic finance principles. This dual alignment is non‑trivial, as global standards often originate in secular financial traditions and may not directly address Shariah‑specific concerns. PVARA’s work therefore involves dialogue with Shariah scholars, Islamic banks, and religious authorities to determine how crypto products and practices can be structured in ethically permissible ways. This could include, for example, restrictions on interest‑bearing lending or leverage for certain products, or requirements that stablecoins be backed by Shariah‑compliant reserves.

The role of the Pakistan Crypto Council

The Pakistan Crypto Council, although distinct from PVARA, complements its work by serving as a policy and industry liaison body. Established under the Finance Ministry but with participation from SBP, SECP, and other agencies, the PCC’s functions include conducting research, consulting stakeholders, and proposing regulatory reforms. It can be seen as both a think tank and a coordination mechanism, helping to ensure that crypto policy is informed by market realities and technological developments.

Under the leadership of figures like Bilal Bin Saqib, the PCC has emphasized the potential of blockchain and digital assets not only for trading but also for real‑economy applications, such as supply‑chain transparency, digital identity, and tokenized financing. It has also played a role in shaping Pakistan’s external messaging on crypto, promoting the country as a responsible yet forward‑looking jurisdiction that seeks to harness innovation for inclusive growth. This positioning has been important in conversations with international partners, including multilateral institutions and foreign investors, who are wary of jurisdictions perceived as crypto wild‑west environments.

Bilal Bin Saqib as “crypto navigator”

Bilal Bin Saqib, a British Pakistani businessman and philanthropist born in 1990, occupies a unique place in this ecosystem. He has served as chairman of PVARA and CEO of the PCC since 2025, effectively bridging regulatory and policy roles. Media portrayals depict him as a “crypto navigator” or “crypto bro” who has helped steer Pakistan into Trump’s orbit and secure a seat at the negotiating table in U.S.–Iran talks. While such labels may be caricatured, they reflect the reality that charismatic, globally networked individuals often play outsized roles in shaping emerging‑market crypto agendas.

Bilal’s dual identity as a diasporic entrepreneur and domestic regulator gives him credibility with both international investors and Pakistani institutions. He has championed initiatives that position Pakistan as a regional crypto hub, emphasizing its young, tech‑savvy population and rapid adoption rates. At the same time, his proximity to political power and involvement in high‑profile deals, such as the WLF stablecoin arrangement, have attracted scrutiny from those concerned about conflicts of interest or the politicization of regulatory decisions. How PVARA manages such perceptions and maintains institutional integrity will influence long‑term confidence in Pakistan’s regulatory regime.

Pakistan Digital Authority and DFINITY’s Internet Computer

Beyond financial regulation, Pakistan is investing in digital infrastructure that could underpin both public services and private‑sector innovation, including in crypto and Web3. The Pakistan Digital Authority, established under the Digital Nation Pakistan Act 2025, serves as the country’s central authority for digital policy, data governance, and AI strategy. In partnership with the DFINITY Foundation, PDA has announced plans to create a dedicated Pakistan “subnet” on DFINITY’s Internet Computer (ICP), described as a sovereign cloud designed to host tamper‑resistant software, national‑scale applications, and AI‑powered systems that can operate independently of foreign cloud infrastructure.

This partnership includes not only infrastructure deployment but also a National Messenger application for private, verifiable communications, access to an AI development platform called Caffeine, and capacity‑building initiatives that provide \(1{,}500\) Caffeine licenses for building applications. DFINITY has also committed to establishing a local presence in Pakistan, signaling long‑term collaboration and technical engagement. For the crypto industry, these developments are relevant in several ways. They suggest that Pakistan may seek to host critical digital‑asset infrastructure, including perhaps elements of PVARA’s supervisory systems or national KYC/AML databases, on sovereign cloud platforms. They also indicate an openness to decentralized or blockchain‑inspired architectures in public‑sector IT.

At the same time, data‑sovereignty and security concerns may lead to stricter regulatory expectations around where VASPs store customer data, how they manage keys, and which cloud or hosting providers they may use. Firms looking to operate in Pakistan will need to keep abreast of PDA’s guidelines and any sector‑specific rules that emerge from the intersection of data protection, AI ethics, and financial regulation.

Toward an integrated digital and financial stack

Taken together, PVARA, PCC, and PDA represent an attempt to build an integrated digital and financial stack that can support both traditional and crypto‑native services. PVARA focuses on the financial‑regulatory perimeter, ensuring that virtual asset activities are supervised and compliant. PCC provides policy research and stakeholder coordination. PDA builds the underlying digital infrastructure and data‑governance framework. If these institutions can coordinate effectively, Pakistan could develop a relatively coherent environment in which digital ID, payments, cloud hosting, and virtual asset services interoperate, potentially enabling novel applications such as programmable remittances, tokenized government bonds, or AI‑driven compliance tools.

However, institution‑building is a long‑term process, and the risk of fragmentation, turf battles, or politicization is real. Clear delineation of mandates, robust legal frameworks, and transparent accountability mechanisms will be essential to avoid regulatory arbitrage and ensure that innovation does not outpace safeguards. For crypto market participants, understanding this institutional landscape is as important as tracking token prices or user metrics.

Sectoral Perspectives: Trading, DeFi, NFTs, and Real-World Assets

Trading and derivatives patterns

While hard data on Pakistan‑specific trading volumes are limited, regional patterns and anecdotal evidence suggest that spot and derivatives trading form the backbone of its crypto activity. Retail traders typically engage in spot buying and selling of Bitcoin, Ethereum, and popular altcoins, often on offshore exchanges with leveraged products. The availability of perpetual futures and options on major platforms enables Pakistani users to speculate on price movements, hedge positions, or pursue arbitrage strategies. Such activities are attractive in an environment where local capital markets are relatively shallow and access to sophisticated derivatives is limited in traditional finance.

Under PVARA’s oversight, local exchanges that emerge or formalize will face decisions about whether to offer derivatives products and how to structure leverage in a Shariah‑compliant and prudentially sound way. Authorities may initially restrict derivatives offerings to professional clients or require robust margining and risk controls. They may also discourage or ban certain highly leveraged products, especially those perceived as purely speculative or akin to gambling. For now, the largest derivatives volumes will likely remain on global platforms, but over time local players could carve out niches, particularly if they can offer smoother integration with rupee banking and tax reporting.

DeFi experiments and regulatory concerns

Decentralized finance (DeFi) is another area where Pakistani users participate, largely through global protocols such as decentralized exchanges (DEXs), lending platforms, and yield‑farming schemes. DeFi’s permissionless nature allows users with internet access and a crypto wallet to interact with sophisticated financial instruments without intermediaries. This has obvious appeal in a context where traditional financial inclusion is limited. However, it poses severe regulatory challenges, as PVARA and SBP have little direct visibility or control over smart contracts hosted on global blockchains.

Regulators may respond by focusing on “on‑ramps” and “off‑ramps”—the points where fiat and crypto meet—rather than trying to directly supervise DeFi protocols. Licensed VASPs could be required to monitor clients’ DeFi interactions, impose limits on certain activities, or provide warnings about risks. Policymakers will also need to consider how DeFi fits into Islamic finance frameworks, as many DeFi products involve interest‑bearing lending, complex derivatives, or liquidity pools that may not align with Shariah principles. Pakistani innovators could see an opportunity here to build Shariah‑compliant DeFi primitives, such as profit‑sharing pools or asset‑backed tokens, that are tailored to domestic norms.

NFTs, gaming, and creative industries

Non‑fungible tokens (NFTs) and blockchain‑based gaming offer another vector for crypto adoption in Pakistan, particularly among younger demographics. Pakistani artists, musicians, and game developers can use NFTs to monetize digital creations, access global audiences, and experiment with new business models. While NFT hype has cooled globally since its 2021 peak, the underlying concept of verifiable digital ownership continues to find niche applications in art, collectibles, and in‑game assets.

From a regulatory perspective, NFTs raise questions about consumer protection, securities classification, and intellectual‑property rights. PVARA and SECP will need to determine when an NFT constitutes a mere digital collectible and when it amounts to a tokenized security or investment contract. They will also have to coordinate with cultural and IP authorities to address issues such as unauthorized minting of copyrighted works. For the most part, NFT activity in Pakistan is likely to remain modest in scale compared with trading and stablecoin usage, but it can play a role in broader Web3 ecosystem development and creative‑economy growth.

Tokenized real-world assets and Islamic finance

Tokenization of real‑world assets (RWAs), such as real estate, commodities, or infrastructure projects, is a promising area for Pakistan given its need for investment and the prevalence of Islamic finance. Tokenized sukuk (Islamic bonds), for example, could allow fractional ownership of Shariah‑compliant financing structures, making it easier for retail investors and diaspora members to participate in infrastructure funding. Asset‑backed tokens representing shares in agricultural commodities, solar‑energy projects, or SME receivables could also align with Islamic finance principles that emphasize linkage to real economic activity.

Implementing such tokenization projects will require careful design and regulatory clarity. PVARA and SECP will need to define how tokenized RWAs are classified, how custody and transfer are managed, and how disputes are resolved. Land and property registries may need modernization to support token‑linked ownership records. Islamic scholars will need to evaluate the permissibility of specific structures. Nonetheless, if executed well, tokenization could help channel crypto‑era tools into productive investment rather than mere speculation.

Illicit finance, scams, and enforcement

No discussion of crypto in Pakistan would be complete without acknowledging the risks of illicit finance and fraud. The same attributes that make crypto attractive for inclusion and innovation—pseudonymity, global reach, and low barriers to entry—also make it appealing for money laundering, tax evasion, and scams. Pakistan’s history with hawala and informal finance heightens concerns that crypto could become a digital extension of existing opaque channels if not properly regulated.

PVARA’s statutory powers to tackle money laundering and terrorism financing are designed to address such risks. Licensing requirements, know‑your‑customer (KYC) obligations, and suspicious‑transaction reporting aim to create a supervised perimeter within which most legitimate activity occurs. However, enforcement capacity will be tested by the speed of innovation and the global nature of crypto. Cooperation with foreign regulators, investment in blockchain analytics tools, and public‑education campaigns about common scams will be crucial. For users, vigilance remains essential, as fraudsters often exploit regulatory uncertainty and technological complexity to deceive.

Pakistan is exploring a rupee-backed stablecoin to expand financial access and modernize payments, aiming to boost remittances and digital inclusion under new crypto regulatory frameworks.

Good luck holding this

The Virtual Assets Act and PVARA are newly established; licensing rules, Sharia compliance requirements, and capital standards are still being operationalised, creating near-term uncertainty for entrants.

All DeFi and crypto activity is being funnelled through a single state regulator (PVARA) with politically connected founders, concentrating gatekeeping power and creating single-point-of-failure risk.

Banking access for licensed VASPs was only restored after an eight-year ban, meaning fiat on/off-ramp infrastructure is nascent and liquidity depth remains untested at scale despite 40 million claimed users.

Pakistan's crypto diplomacy is explicitly entangled with the Trump administration and US-Iran mediation; a change in US political alignment or regional escalation could directly affect regulatory goodwill and investment flows.

- Smart-contract / TechnicalLow

Current activity is dominated by exchange licensing, mining, and government MOUs rather than native DeFi protocols, so smart-contract exploit risk is minimal in this phase.

Pakistan remains under an IMF programme with persistent rupee depreciation and high inflation, which drives adoption demand but also creates capital-control pressure that could snap back against open crypto flows.

Banking, Payments, and Stablecoins in Practice

How banks can serve licensed VASPs

With the SBP’s reversal of the 2018 ban, Pakistani banks can now serve PVARA‑licensed VASPs under defined conditions. Practically, this means banks can provide rupee accounts, payment processing, and settlement services to exchanges, brokers, and custodians, enabling smoother fiat‑crypto flows. Banks must, however, implement robust customer due diligence, assess the VASP’s governance and compliance systems, and monitor transactions for suspicious patterns. They are also required to ensure that client funds related to crypto activity are held in segregated accounts and are not mixed with the VASP’s own operating funds.

This arrangement transforms the business landscape for both banks and VASPs. Banks gain a new category of clients that can generate fee income and drive transaction volumes, particularly in payments and treasury services. VASPs benefit from access to reliable banking, which improves user experience and reduces reliance on informal payment intermediaries. Over time, competition among banks to serve high‑quality VASPs could lead to specialized products, such as escrow services for OTC trades, corporate accounts for crypto‑native businesses, or settlement solutions for tokenized assets.

Binance’s Pakistan-focused USDT campaign

Binance’s Pakistan‑exclusive USDT referral campaign exemplifies how global exchanges intend to capitalize on these regulatory shifts. The promotion offers \(25{,}000\) USDT in token vouchers to Pakistani users who invite friends to sign up and make their first trades, with both referrer and referee receiving rewards ranging from \(3\) to \(6\) USDT per successful referral, and an additional \(5{,}000\) USDT allocated to the top \(50\) referrers via a leaderboard. The campaign runs over a defined period in June 2026 and distributes rewards through Binance’s Rewards Hub.

Such targeted campaigns serve multiple purposes. They accelerate user acquisition at a time when banking access lowers friction for fiat deposits and withdrawals. They encourage social diffusion of crypto usage, as existing users onboard friends and family. They also entrench USDT as a default stablecoin in Pakistani users’ mental models, since rewards are denominated in USDT and participants are nudged to hold or trade in it. For regulators, these campaigns highlight the need to monitor cross‑border marketing and ensure that users understand the risks associated with trading and stablecoin holding.

USD1 versus incumbent dollar tokens

World Liberty Financial’s USD1 stablecoin enters this landscape as a politically charged competitor to incumbents like USDT and USDC. Whereas USDT is issued by a private company with global reach but limited direct ties to any one government, USD1 is associated with a sitting U.S. president’s startup and is being positioned as a stablecoin integrated into sovereign payment systems like Pakistan’s. This integration could provide USD1 with a unique distribution channel and aura of official backing, even if its legal status remains that of a private token.

For Pakistani users and institutions, the key questions will revolve around trust, liquidity, and interoperability. Does USD1 maintain a credible reserve and redemption mechanism? How easily can it be converted into other stablecoins, fiat currencies, or assets? What are the legal recourses in case of disputes or issuer failure? How does its use intersect with U.S. regulatory jurisdiction and potential sanctions? PVARA and SBP will need to formulate clear guidelines on how USD1 can be used, if at all, by licensed VASPs and banks, and under what risk‑management frameworks.

Integration with domestic payment rails

Integrating crypto and stablecoins with domestic payment rails is a technical and policy challenge. Pakistan has been developing instant‑payment systems and expanding digital‑wallet usage, and banks now face the task of linking these rails with PVARA‑licensed VASPs without compromising security or compliance. Potential models include API‑based connectivity between banks and exchanges, direct settlement via central‑bank‑operated systems, or the use of tokenized deposits that represent claims on bank balances and can be transferred on blockchain networks.

The WLF arrangement suggests one possible pathway, where a stablecoin is plugged into central‑bank payment infrastructure for specific cross‑border use cases. However, broader integration will require harmonization of messaging standards, reconciliation processes, and risk controls. Regulators will also need to consider how to treat on‑chain transactions in legal terms—are they final settlement events, or do they require off‑chain confirmation? How are disputes resolved in cases of technical failure or fraud? These questions are not unique to Pakistan but acquire local flavor due to its institutional architecture and legal traditions.

Opportunities for fintech and neobanks

The convergence of crypto regulation, banking reform, and digital‑infrastructure development opens opportunities for fintech firms and neobanks in Pakistan. Startups can build products that sit at the intersection of fiat and crypto, such as wallets that allow users to hold both rupees and stablecoins, apps that facilitate low‑cost remittances using regulated VASPs as back‑end providers, or platforms that offer Shariah‑compliant investment products using tokenized assets. Neobanks can differentiate themselves by offering crypto‑friendly accounts, educational content, and integrated spending tools, subject to regulatory approval.

Nonetheless, competition will be intense, not only among domestic players but also from global platforms with deep pockets and established brands. Regulatory clarity, partnerships with banks, and alignment with PVARA’s licensing requirements will be critical differentiators. Fintechs that ignore compliance in pursuit of rapid growth may find themselves shut out of the banking system or subject to enforcement actions. Those that navigate the regulatory landscape successfully could help translate Pakistan’s high crypto adoption into broader financial inclusion and innovation.

Macro, Markets, and Systemic Risk

Growth, inflation, and IMF projections

From a macro perspective, Pakistan’s crypto trajectory cannot be separated from its broader economic outlook. The IMF projects real GDP growth of around \(3.6\%\) and consumer price inflation near \(7.2\%\), figures that point to modest recovery but continued structural challenges. Debt pressures, fiscal deficits, and external‑financing needs will keep the country engaged with multilateral lenders and susceptible to conditionality related to financial‑sector reforms, capital‑flow management, and AML/CFT frameworks. Crypto regulation will therefore be scrutinized not only domestically but also by external partners concerned about financial stability and illicit finance.

Inflation dynamics also influence crypto demand. When price levels rise and the rupee depreciates, households seek stores of value that can preserve purchasing power, whether in dollars, gold, or digital assets. Crypto offers a novel vector for such hedging, but it can also exacerbate volatility if large inflows and outflows interact with fragile banking and FX markets. Policymakers will need to monitor whether crypto usage intensifies in periods of macro stress and how it affects the transmission of monetary policy and capital controls.

Energy prices, Middle East tensions, and external balances

Pakistan’s external balances are highly sensitive to energy prices, particularly oil imports from the Gulf. Tensions in the Middle East, including threats or disruptions to the Strait of Hormuz, can quickly translate into higher fuel costs, inflation, and pressure on foreign‑exchange reserves. Media reports note that rising Middle East tensions have strained Pakistan’s economy, pushing fuel prices higher, intensifying inflation, and raising concerns about remittance flows. In such scenarios, crypto markets often experience heightened volatility, as investors reassess global risk and the potential for sanctions, war, or supply‑chain disruptions.

Pakistan’s role as mediator between the U.S. and Iran means that its diplomatic successes or failures can themselves influence expectations about energy prices and regional stability. When negotiations go well, risk assets, including Bitcoin and equities, may rally on expectations of reduced conflict and smoother trade. When talks stall or threats escalate, safe‑haven flows may move into assets like gold or, paradoxically, into Bitcoin if it is perceived as a hedge against geopolitical chaos. For Pakistan’s domestic economy, the key question is whether crypto channels amplify or cushion these shocks.

Crypto as hedge, risk asset, or both

The dual nature of crypto—as both a speculative risk asset and a potential hedge against inflation or political instability—complicates macro risk analysis. In Pakistan, this duality is evident in how Bitcoin and stablecoins are used: some actors speculate aggressively on price moves, while others use stablecoins for savings or remittances. Market reactions to Pakistan‑related geopolitical news, such as Bitcoin surging above \(64{,}000\) USD after positive Iran‑talks updates, highlight its risk‑asset behavior, closely tied to global sentiment. At the same time, anecdotal evidence suggests that in periods of local financial stress, Pakistani users increase crypto holdings as a way to diversify away from rupee exposure.

For policy makers and investors, the key is to recognize that crypto’s role may shift depending on the timeframe and shock type. Over short horizons, it may trade like a high‑beta tech stock, sensitive to liquidity conditions and risk appetite. Over longer horizons, in contexts of persistent inflation or currency devaluation, it may function as a partial hedge. Stablecoins, meanwhile, straddle the line between cash equivalent and credit instrument, depending on the robustness of their reserves and regulatory treatment. Pakistan’s challenge is to harness the potential hedging functions without letting speculative excesses or regulatory gaps destabilize its financial system.

Capital controls, regulatory arbitrage, and financial stability

Pakistan, like many emerging markets, uses capital‑flow measures and prudential tools to manage its external accounts and protect against sudden stops. Crypto poses a challenge to such controls, as it enables cross‑border value transfers that are harder to monitor and regulate than traditional channels. If residents use crypto to move large amounts of capital abroad in response to economic or political shocks, this could exacerbate pressure on the rupee and reserves. Conversely, if crypto is used to bring in capital or remittances through regulated channels, it could support external stability.

PVARA’s licensing regime and SBP’s banking rules are designed to reduce regulatory arbitrage by channelling major flows through supervised VASPs and banks. However, enforcement will be an ongoing task, especially given the persistence of P2P markets and offshore platforms. Pakistan will likely need to invest in blockchain analytics, cross‑border cooperation, and targeted enforcement against unlicensed operators. It may also explore positive incentives, such as tax or fee advantages, for using regulated channels over informal ones.