Deep dive explainer on RAAC’s gold- and real-estate-backed DeFi stack, covering pmUSD’s IONau collateral, RWf(x) mechanics, Curve and Frax integrations, RAACLend and iREET, community tools like RAAC Bots and Squid Pass, and the key risks and outlook for this RWA-first protocol.

RAAC opens $1.135M bond for tokenized real estate token $IREET, with 45-day lockup timed to RAACLend debut2026-04

RAAC opens $1.135M bond for tokenized real estate token $IREET, with 45-day lockup timed to RAACLend debut2026-04 Curve Finance gauge vote live: RAAC allocates to pmUSD gauge with veCRV, vlCVX, sdCRV holders eligible to vote.2026-04

Curve Finance gauge vote live: RAAC allocates to pmUSD gauge with veCRV, vlCVX, sdCRV holders eligible to vote.2026-04 $iREET launches, enabling up to 25%+ $CRV APR on tokenized real estate via RAAC protocol2026-04

$iREET launches, enabling up to 25%+ $CRV APR on tokenized real estate via RAAC protocol2026-04 RAAC's gold-backed stablecoin doing up to 27% APR while the rest of crypto argues about altseasons and still focuses on speculation...

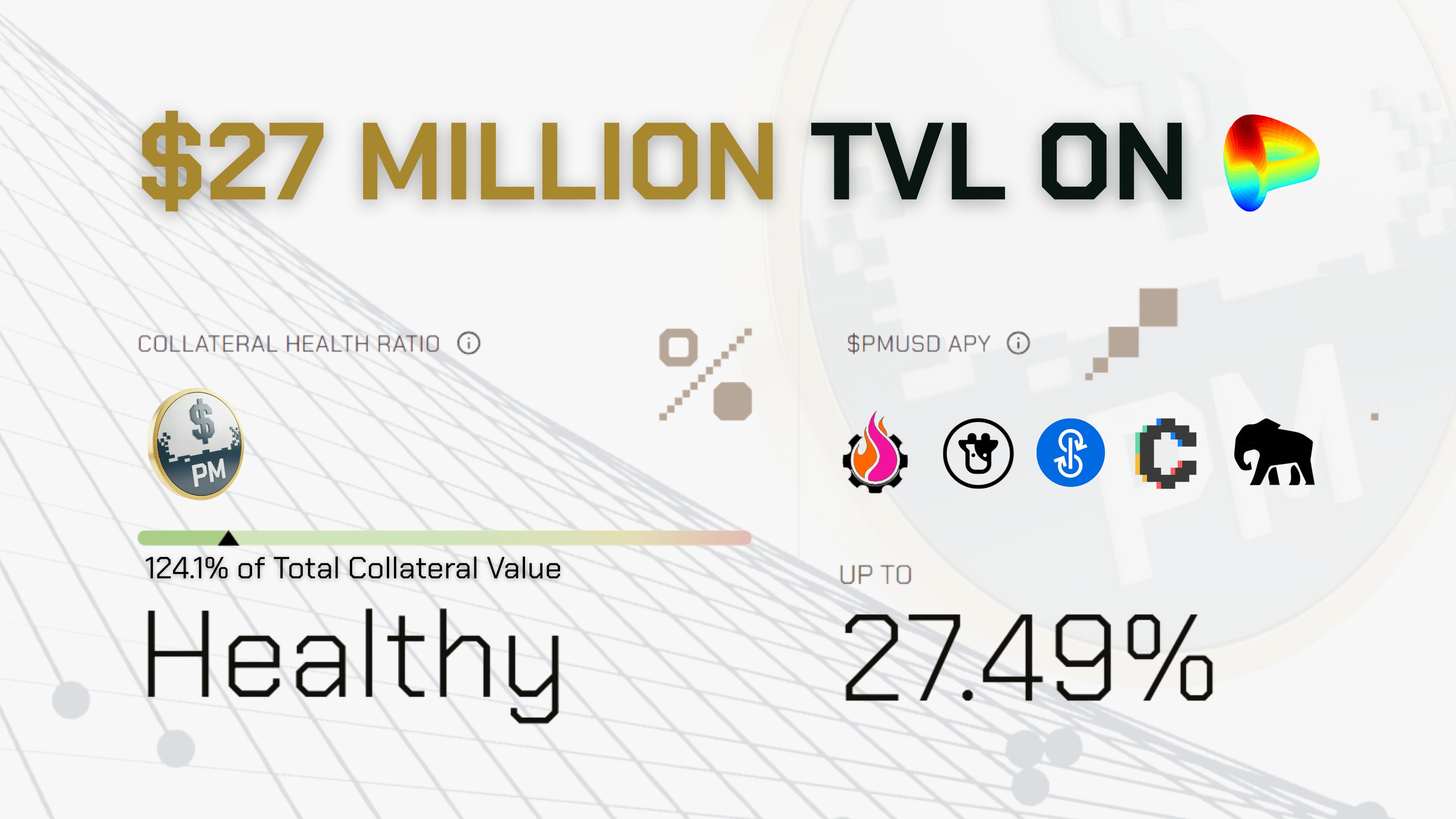

$pmUSD on Curve: $27M TVL in less than 2 months, and growing.2026-02

RAAC's gold-backed stablecoin doing up to 27% APR while the rest of crypto argues about altseasons and still focuses on speculation...

$pmUSD on Curve: $27M TVL in less than 2 months, and growing.2026-02 RAAC announces tentative agreement with a physical gold exchange provider to facilitate pmUSD redemptions, which is expected to begin the first week of July or even sooner.2026-05

RAAC announces tentative agreement with a physical gold exchange provider to facilitate pmUSD redemptions, which is expected to begin the first week of July or even sooner.2026-05 This Thursday December 18th, RAAC is officially launching its gold-backed stablecoin $pmUSD!

The launch is via a bond sale on Apebond, where $1M pmUSD will be available with a reward going from 2 to 5%!

This means: for every $1 USDT / USDC you deposit, you receive up to $1.05 pmUSD after the locking period. On top of that, this sale also marks the start of the RAAC points program, and participating in this sale will grant the biggest point multiplier of the program!

Finally, this sale is private for the RAAC Bots holder, the Llamas and the ApeBond premium users!

Follow RAAC on X for additional details!2025-12

This Thursday December 18th, RAAC is officially launching its gold-backed stablecoin $pmUSD!

The launch is via a bond sale on Apebond, where $1M pmUSD will be available with a reward going from 2 to 5%!

This means: for every $1 USDT / USDC you deposit, you receive up to $1.05 pmUSD after the locking period. On top of that, this sale also marks the start of the RAAC points program, and participating in this sale will grant the biggest point multiplier of the program!

Finally, this sale is private for the RAAC Bots holder, the Llamas and the ApeBond premium users!

Follow RAAC on X for additional details!2025-12

RAAC: Gold, Real Estate, and the DeFi RWA Stack

Real Asset Acquisition Corp (RAAC) is a decentralized finance ecosystem that brings tokenized real-world assets—starting with in-situ gold reserves and U.S. real estate—on-chain to back yield-bearing stablecoins, lending markets, and structured products, with its flagship gold-backed stablecoin pmUSD at the center of the design. By combining regulated commodity tokenization, DeFi-native stablecoin engineering, and deep integrations with protocols like Curve and Frax, RAAC is positioning itself as an RWA-first alternative to purely fiat- or crypto-backed stablecoin systems.

What RAAC Is Trying To Build

RAAC describes itself as a DeFi lending and borrowing ecosystem that opens participation in tokenized real-world assets (RWAs) to a broad on-chain audience. The core idea is to transform traditionally illiquid or institutional-only assets—such as gold reserves or subsidized U.S. rental housing—into programmable collateral that can support stablecoins, liquidity pools, and credit markets on public blockchains. Instead of treating RWAs as a niche add-on, RAAC makes them the primary source of backing for its products, beginning with the Precious Metal USD (pmUSD) stablecoin and expanding into tokenized real estate through RAACLend and the iREET asset. This design attempts to marry the perceived stability of physical assets with the composability and capital efficiency of DeFi.

At a high level, RAAC’s architecture has two flagship verticals. The first is RWf(x), a fork of the f(x) Protocol that mints stablecoins against tokenized commodities such as gold and other precious metals. Within RWf(x), pmUSD is the first production stablecoin, backed by tokenized in-situ gold reserves supplied by I-ON Digital Corp via its ION.au digital security. The second vertical is RAACLend, a protocol for on-chain borrowing against tokenized real estate and other low-volatility assets represented as NFTs, with exposure initially focused on U.S. properties participating in the Housing Choice Voucher Program (HCVP). These verticals are coordinated and incentivized by a broader RAAC ecosystem that includes the RAAC token (for governance and value capture), the iREET real-estate-linked token, and community access tools such as RAAC Bots NFTs and a points program meant to culminate in a future token generation event.

The project is built around a network of institutional partners. RAAC works with I-ON Digital Corp, a listed “tokenized gold” provider, to source and tokenize large in-situ gold reserves that become the underlying collateral for pmUSD. I-ON’s ION.au token is designed as an institutional-grade, legally compliant digital security that represents fractional claims on audited gold reserves and is priced against the London Bullion Market Association (LBMA) spot gold rate. RAAC also collaborates with Curve Finance to deploy deep liquidity pools for pmUSD and related assets, making Curve the core routing layer for its stablecoin ecosystem, and has joined the Chainlink BUILD program to use Chainlink’s Proof of Reserve (PoR) infrastructure for real-time collateral attestations. More recently, RAAC has entered into a strategic partnership with Frax Finance to pair pmUSD with frxUSD and build deep, RWA-backed stablecoin pools connecting gold collateral and U.S. Treasury bill-backed stablecoins.

RAAC’s strategy is unapologetically yield-focused but attempts to root that yield in off-chain economic activity rather than purely reflexive token incentives. Rental income from subsidized housing, discounted gold reserves, and traditional fixed-income instruments are all envisaged as the ultimate sources of cash flows that can support stable coin yields and lending returns. To bootstrap usage and liquidity, RAAC has used mechanisms familiar to DeFi veterans—bond sales via ApeBond, Curve gauge incentives, airdrop whitelisting, and a points program—but the stated long-term ambition is to have pmUSD and iREET yields anchored in real-world income streams rather than solely protocol emissions. In this sense, RAAC can be understood as part of the broader RWA movement in DeFi, but with a relatively concentrated initial bet on gold and U.S. real estate as foundational pillars.

Curve Finance gauge vote live: RAAC allocates to pmUSD gauge with veCRV, vlCVX, sdCRV holders eligible to vote.

Interesting development for Curve's governance. The RAAC allocation to pmUSD gauge shows liquidity focus shifting. Key levels on $CRV are $0.58 support and $0.65 resistance - we're currently testing the 20 EMA on daily. Volume is declining, which isn't ideal for a sustained move. If we break $0.65 with conviction, next target is $0.72. Lose $0.58 and we're likely retesting the $0.52 lows. Watching how veCRV holders react to this vote - could impact token velocity.

Readers engage RAAC most when tangible yield numbers on physical assets (27% APR on gold, 25%+ CRV on real estate) are delivered inside Curve ecosystem primitives they already trust — the click signal is not RWA curiosity in the abstract, but familiar DeFi flywheel mechanics applied to hard assets.↗

Tokenizing Gold: ION.au, RWf(x), and pmUSD

The ION.au Gold Rail

The most distinctive building block in RAAC’s design is its integration with I-ON Digital Corp, a regulated provider of tokenized gold claims whose flagship product, ION.au, is a gold-backed digital security secured by in-situ mineral reserves. I-ON pioneered a model in which audited gold reserves still in the ground are digitized into securities, offering fractional ownership with institutional-grade compliance and custody frameworks. Each IONau token represents one-thousandth of a troy ounce of in-situ gold, with pricing tied to daily LBMA gold spot rates and settlement infrastructure designed for institutional trust and mark-to-market accounting. The idea is to transform what would otherwise be dormant geological value into on-chain capital, usable as collateral for a variety of financial structures, including stablecoins and collateralized borrowing.

For RAAC, IONau serves as the underlying commodity reference that feeds into its RWf(x) tokenization system. The flow is roughly: physical in-situ gold reserves are audited and structured into ION.au digital securities; those securities are then bridged into TokenBlender contracts, which mint a base token representing claims on the IONau collateral; and RWf(x) uses that base token as collateral to mint pmUSD. RAAC’s own materials often describe this path using the “Instruxi tokenization engine,” an architecture that takes gold and other commodities, wraps them into ERC‑20 tokens, and then routes them into RAAC’s vaults as eligible collateral. While much of this infrastructure is behind-the-scenes from the average user’s perspective, it is critical in determining the legal and risk profile of pmUSD, because any failure in the chain from physical reserves to digital securities to tokenized claims ultimately impacts pmUSD’s solvency.

IONau is positioned as more than a static gold representation; I-ON promotes it as a “next-generation digital gold instrument” that can generate yield, provide liquidity, and power stablecoin issuance across a variety of DeFi integrations, including RAAC’s pmUSD and other gold-backed stablecoins such as Goldfish’s GGBR. The company emphasizes that its architecture enables scalable minting, transparent collateralization, and revenue-producing deployment strategies, with real-time connectivity between TradFi capital and DeFi liquidity rails. For pmUSD holders, this means that the token they are using is indirectly backed by regulated gold securities rather than unregulated gold tokens or purely off-chain claims, although the fact that the reserves are in-situ, rather than vaulted bullion, introduces a different risk profile than physically deliverable tokenized gold.

pmUSD: A Gold-Backed, USD-Pegged Stablecoin

RAAC’s flagship stablecoin, Precious Metals USD (pmUSD), is built on top of the IONau collateral rail and is designed as a gold-referenced, USD-pegged digital dollar. pmUSD is minted by RAAC’s RWf(x) module as the fToken in a fork of the f(x) Protocol, using tokenized gold collateral as backing. RAAC describes pmUSD as “the original gold-backed dollar brought on-chain,” aiming to provide a more conservative collateral base than fiat-backed or fund-backed DeFi stablecoins while still maintaining composability with DeFi protocols. The stablecoin is intended to hold a soft peg of 1 pmUSD to 1 USD, while the collateral is denominated in discounted gold value to provide a margin of safety.

According to RAAC’s whitepaper, pmUSD is backed by tokenized in-situ gold reserves that are discounted by 80% relative to the real-time spot gold price when used for collateral calculations. Put differently, only 20% of the LBMA-marked value of the underlying gold is counted for minting purposes, which results in a stated reserve ratio of approximately 5:1 between gold value and pmUSD supply. This can be expressed schematically as \[ \text{EffectiveCollateralValue} = 0.2 \times \text{SpotGoldValue} \] and \[ \text{ReserveRatio} = \frac{\text{SpotGoldValue}}{\text{pmUSDSupply}} \approx 5. \] By over-collateralizing in this way, RAAC aims to protect pmUSD holders from downside moves in the gold price and from potential discounts associated with the in-situ nature of the reserves, though this does not eliminate all risk.

The pmUSD system is designed so that the net 1x long exposure to gold is split into two components: the stablecoin pmUSD and a leveraged gold position (in the original f(x) design, xGOLD) that absorbs most of the gold price volatility. RAAC’s twist is that, rather than offering that leveraged gold exposure to the public as a separate token, it internalizes the position, keeping the volatility-bearing side of the structure within the protocol. The goal is to present pmUSD as a relatively stable, USD-linked asset, while RAAC itself manages the risk associated with changes in collateral value. Minting pmUSD is not permissionless; it is controlled via manager-only silo multisigs, reflecting the protocol’s current centralized governance model for collateral management and system operations.

RWf(x), Peg Defense, and Proof of Reserves

pmUSD’s stability mechanics combine the RWf(x) collateral structure with a pegging mechanism based on a Peg Stability Module (PSM) that uses sUSDS as a reference stablecoin. In the RWf(x) silo, pmUSD is minted against TokenBlender base tokens linked to IONau collateral, while a corresponding xPM-like position (analogous to the leveraged gold token in f(x)) absorbs changes in collateral price, keeping pmUSD’s net asset value aligned as closely as possible with a dollar target. This design seeks to decouple pmUSD’s price from short-term gold volatility, so that pmUSD behaves more like a dollar stablecoin than a gold tracker, even though its backing ultimately derives from gold reserves.

The primary peg defense mechanism, as described by Pharos Watch’s risk profile, is a PSM in which arbitrageurs can swap pmUSD into sUSDS at a fixed face value of 1 USD when pmUSD trades at a discount on-chain. When pmUSD falls below peg in secondary markets, arbitrageurs can purchase discounted pmUSD, route it through the one-way PSM to receive sUSDS at a face value of 1, and thereby realize a profit while shrinking pmUSD supply and supporting its price. Swaps are one-directional and pause if the sUSDS reserve falls below 20% of PSM assets, which creates a guardrail but also introduces dependence on the health and liquidity of sUSDS and the Sky Protocol ecosystem more broadly. This external dependency is flagged by Pharos as a meaningful risk factor, because a failure in sUSDS or Sky could impair pmUSD’s peg defense even if the gold collateral remained intact.

To address transparency concerns, RAAC uses real-time Proof of Reserves via Chainlink’s PoR framework and data sourced from Instruxi to track collateral backing pmUSD. The pmUSD static profile on Pharos notes that Chainlink PoR and Instruxi Reserve data are used to attest to the presence of TokenBlender base tokens and underlying IONau holdings in RAAC’s RWf(x) treasury. This is augmented by I-ON’s own claims that IONau operates within a regulated custody framework and provides daily LBMA-based pricing. In principle, this combination should allow independent observers to verify both that pmUSD is sufficiently collateralized by tokenized gold claims and that those claims correspond to audited in-situ reserves, although practical verification still requires trust in I-ON’s audits and the correctness of the PoR feeds.

Liquidity, Curve Integration, and Yield

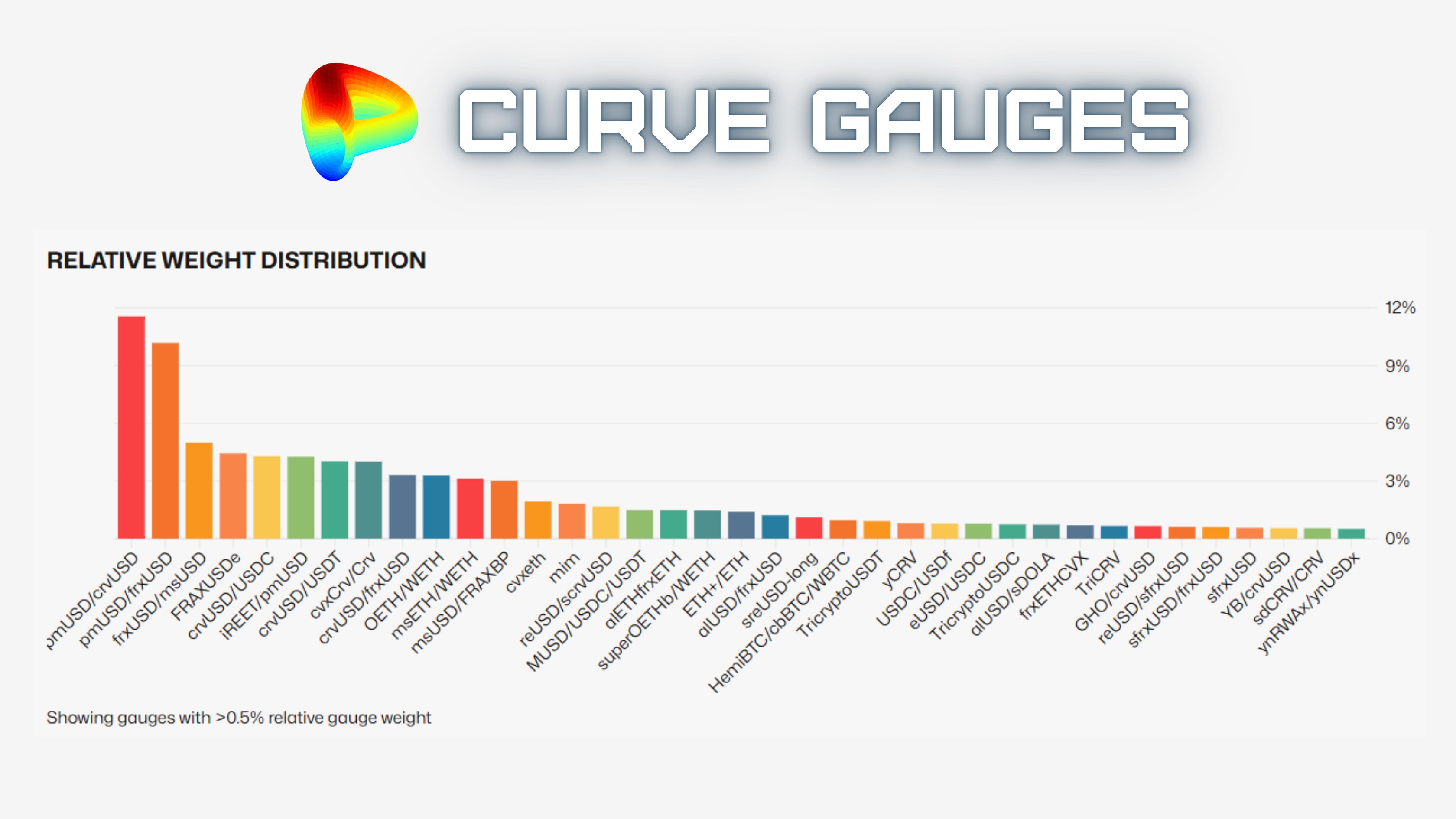

From launch, RAAC has prioritized deep on-chain liquidity for pmUSD, primarily through a strategic collaboration with Curve Finance. RAAC has announced that it is deploying over 100 million dollars’ worth of pmUSD liquidity to Curve and positioning Curve as the core infrastructure layer for its stablecoin and RWA ecosystem, using Curve’s factory pools and gauge system to route much of pmUSD’s trading volume and yield opportunities. A dedicated Curve pool hosts pmUSD liquidity, and a gauge proposal has been introduced and passed to add a gauge for an iREET/pmUSD pool on Ethereum mainnet, enabling tokens associated with RAAC’s real estate strategy to earn Curve incentives alongside pmUSD. The combination of pmUSD pools and iREET/pmUSD pools creates a network of routes through which users can move between gold-backed stablecoins, real estate exposure, and other DeFi assets.

Independent commentators have noted that pmUSD liquidity on Curve grew to around 27 million dollars in less than two months after launch, with the associated pools offering double-digit APRs driven by trading fees, CRV emissions, and external incentives from RAAC and partner protocols. Reports of yields in the 11–33% APR range on pmUSD liquidity provision have circulated in DeFi communities, particularly during the early phase of RAAC’s liquidity mining campaigns. RAAC has also run bond sales via ApeBond, offering pmUSD at a discount or with bonus rewards to early participants, with one flagship one-million-dollar pmUSD bond reportedly selling out and delivering a 5% bonus to depositors after a lockup period. These programs have been framed by RAAC as part of a broader points system designed to reward early adopters with multipliers toward a future RAAC token generation event, further boosting effective yields for participants willing to speculate on future governance token value.

Beyond Curve, RAAC’s partnership with Frax Finance is a key avenue for pmUSD utility. Frax has described pmUSD pairing with frxUSD as a core route in new T-bill- and RWA-backed stablecoin pools, with the intention of establishing one of the deepest such pools in DeFi. The collaboration spans not only Curve-based pools but also prospective integrations of pmUSD into FraxSwap and FraxLend, where it could function as collateral or as a base asset in lending markets. In this architecture, pmUSD becomes a gold-collateralized leg in a broader “RWA stablecoin stack” that also includes frxUSD, which itself is backed by U.S. Treasury bills and other reserve assets, creating layered exposure to different forms of real-world collateral.

pmUSD Risk Profile and Market Behavior

Despite the overcollateralization and peg-defense mechanics, pmUSD is not risk-free. Pharos Watch classifies pmUSD as a centrally governed, real-world-asset-backed stablecoin with manager-only minting and system operations controlled via authorized silo multisigs. The protocol’s contracts allow for issuer or admin freeze controls, and Pharos notes that pmUSD’s peg defense is meaningfully dependent on external systems such as the sUSDS-based PSM and the Sky Protocol’s health. This centralized control structure may be necessary for handling regulated collateral and complex RWA arrangements, but it introduces governance and counterparty risk that differs from more decentralized crypto-backed stablecoins.

Market behavior has underscored some of these risks. Public price data from aggregators such as CoinGecko have shown pmUSD trading below its intended 1 USD peg during periods of stress, including episodes where the token traded around 0.76 USD, far beneath its target. While such deviations may reflect temporary liquidity imbalances, confidence shocks, or friction in the arbitrage mechanisms, they indicate that pmUSD does not yet behave like a fully hardened, fiat-backed stablecoin in all conditions. For a gold-backed stablecoin whose raison d’être is stability grounded in hard assets, sustained or repeated depegs would be particularly problematic, since they would erode the core value proposition of combining real-asset backing with DeFi composability.

The nature of the underlying collateral also raises unique issues. In-situ gold reserves are inherently less liquid and harder to enforce claims against than vaulted bullion or cash equivalents, making recovery in extreme scenarios more complex even if legal rights are well-defined. RAAC’s decision to discount the collateral by 80% when calculating minting capacity is a recognition of this risk, but it does not by itself resolve questions about how quickly or completely collateral could be monetized in a crisis, particularly if both DeFi markets and commodity markets were under stress at the same time. Users must therefore consider pmUSD less as a direct claim on deliverable gold and more as a structured product backed by gold-linked securities, governance processes, and a web of external providers.

A simplified comparison with other asset-backed tokens helps illustrate where pmUSD sits in the landscape:

| Feature | pmUSD (RAAC) | Fiat-backed stablecoin (e.g., USDC) | Gold token (e.g., PAXG) |

|---|---|---|---|

| Primary backing | Tokenized in-situ gold (IONau via TokenBlender) | Cash and cash equivalents in regulated accounts | Allocated vaulted bullion |

| Target unit | 1 USD peg, gold-referenced | 1 USD peg | 1 troy ounce or fraction of gold |

| Peg mechanism | RWf(x) structure plus sUSDS-based PSM | Direct redemption and arbitrage via issuers | Direct gold redemption (fees apply) |

| Governance | Centralized, manager-only minting, admin controls | Centralized corporate issuer | Centralized issuer, gold custodian |

| On-chain composability | Designed for DeFi pools and lending | Widely integrated across DeFi | Moderate; often less integrated |

| Regulatory exposure | RWA securities plus DeFi protocol risk | Fiat regulation, money transmitter regimes | Commodities and securities considerations |

This table is schematic rather than exhaustive, but it illustrates pmUSD’s hybrid nature: it combines elements of RWA securitization, gold-linked exposure, centralized governance, and DeFi-native peg mechanics in a way that is distinct from both traditional fiat-backed stablecoins and pure gold tokens.

$iREET launches, enabling up to 25%+ $CRV APR on tokenized real estate via RAAC protocol

RAAC controls 4.1% of all Curve voting power through accumulated $CVX — that's the entire engine behind the 25%+ APR. Strip away the CRV emissions subsidy and you're looking at maybe 5-7% from actual rental yield on the underlying properties, which is standard cap rate territory for tokenized RE. The Convex flywheel bootstrapping RWA liquidity is a clever play, but every protocol that's leaned on directed gauge emissions eventually faces the same cliff when TVL outpaces incentive budgets — ask Frax how that math works at scale. Borrowing crvUSD against iREET collateral adds composability, but the liquidation mechanics on illiquid tokenized property NFTs during a drawdown are an unsolved problem that no amount of Chainlink price feeds will fully derisk.

- 01pmUSD gold stablecoin yield↗

Concrete APR figures (2–27%) on a gold-backed stablecoin with live TVL milestones gave readers a yield story with physical-asset backing, rare in 2024–25 DeFi.

- 02Curve gauge and veCRV integration↗

Gauge votes involving veCRV, vlCVX, and sdCRV holders pulled in the existing Curve voter base who saw pmUSD as a new bribe-worthy incentive route.

- 03iREET tokenized real estate launch↗

A $1.135M bond with a 45-day lockup timed to RAACLend's debut framed real estate tokenization as a concrete yield product, not a whitepaper concept.

- 04ION partnership and FT coverage↗

A $200M gold tokenization deal picked up organically by the Financial Times gave RAAC mainstream financial press legitimacy that DeFi-native projects rarely achieve.

- 05Frax liquidity flywheel deal↗

Pairing pmUSD with frxUSD inside FraxSwap and FraxLend signaled a two-protocol liquidity commitment that readers interpreted as structural depth, not a one-sided promo.

- 06RAAC Bots NFT membership mint↗

A free-mint genesis collection with gated access to the pmUSD bond sale created FOMO around membership utility, not just speculative NFT flipping.

Real Estate On-Chain: RAACLend, iREET, and Tokenized Property Income

RAACLend’s Real Estate Thesis

Parallel to its gold-backed stablecoin vertical, RAAC is building RAACLend as a protocol for on-chain borrowing against tokenized real estate and other low-volatility assets. RAACLend focuses initially on U.S. rental properties participating in the Housing Choice Voucher Program (HCVP), a federal subsidy program that provides government-backed rental payments to landlords on behalf of eligible tenants. Because rental income in HCVP is partially or largely backed by the U.S. government, such properties can exhibit relatively stable cash flows, making them attractive as a foundation for income-generating, RWA-backed crypto products. RAACLend’s goal is to translate these stable, off-chain rental flows into tokenized instruments that can support DeFi lending, yield strategies, and portfolio diversification.

According to RAAC’s whitepaper, RAACLend uses tokenized real-world assets, such as real estate, as collateral to mint stablecoins and structure credit exposures in a manner analogous to how RWf(x) uses tokenized gold. Each independent silo in the RAAC ecosystem is a self-contained vault that tokenizes a single asset class—examples ranging from gold and farmland to oil, data, or water—mints a branded stablecoin or credit token against that asset, and deploys the resulting tokens into RAAC products and external DeFi protocols to earn yield. In the context of RAACLend, underlying real estate is assessed, regularly valued, and then packaged into tokenized claims that can be used to mint or back tokens like iREET, which represent diversified exposure to the net asset value and income streams of the properties.

By emphasizing properties in the HCVP, RAACLend aims to anchor its returns in revenues that are relatively insensitive to typical crypto market cycles, because the primary payor is a government subsidy rather than a purely market-driven tenant base. This is pitched as an antidote to the volatility of on-chain yields that are often funded mostly by emissions or speculative trading. In principle, rent checks from HCVP-supported properties flow into a real estate operating entity, which then passes through returns, net of expenses and debt service, to token holders and protocol treasuries, providing the economic basis for yields paid out in iREET, pmUSD, or other RAAC-linked instruments. The challenge is to construct legal and operational structures that can reliably route these cash flows into on-chain instruments without creating regulatory vulnerabilities or operational bottlenecks.

iREET: Synthetic Real Estate Exposure and Bonds

The primary token through which RAACLend packages real estate exposure is iREET, a synthetic representation of real estate within the RAAC ecosystem. iREET is described as offering diversified exposure to the net asset value of real properties that have been tokenized and onboarded into RAACLend structures. Simply holding iREET is marketed as a way to gain exposure to a basket of underlying U.S. properties without directly owning or managing them, in a manner similar to a real estate investment trust (REIT) but implemented as an on-chain asset with DeFi composability rather than a listed security. The token can potentially be used as collateral, paired in liquidity pools (for example, with pmUSD), or held as a yield-bearing asset whose returns ultimately derive from property income and value appreciation.

RAAC’s whitepaper notes that the protocol charges a 2% minting fee denominated in iREET tokens, which are sent to the RAAC treasury when stablecoins or other credit exposures are minted against real estate collateral. This means that demand for borrowing or structured products backed by real estate translates into protocol-level accumulation of iREET, aligning RAAC’s treasury and governance token holders with the growth of RAACLend’s underlying property book. The value of the real estate is determined by regular appraisals or valuation processes, and the overcollateralization of loans or stablecoins backed by that real estate is adjusted accordingly. In effect, iREET functions both as an exposure token for investors and as a fee-capture and risk-absorption mechanism for the protocol.

RAAC has used bond offerings to bootstrap liquidity and distribution for iREET. One of the notable initiatives has been the opening of a roughly 1.135 million dollar bond for iREET, structured with a 45-day lockup period aligned with the planned debut of RAACLend’s mainnet lending platform. In this setup, users deposit stablecoins or other accepted assets into a bond contract, receive iREET at a discount or with a bonus after the lockup, and thereby finance the acquisition or refinancing of underlying properties while gaining leveraged exposure to the RAACLend thesis. The bond design closely mirrors the pmUSD bond structure RAAC used for its gold-backed stablecoin, which had a one-million-dollar cap and rewarded depositors with a 5% bonus after a lockup, and which reportedly sold out, delivering an extra 10% in rewards to RAAC Bot NFT holders as an additional incentive.

Curve Finance again plays a central role in making iREET liquid. A gauge proposal on Curve’s DAO has been advanced and accepted to add a gauge for an iREET/pmUSD pool on Ethereum mainnet, which enables liquidity providers in that pool to earn CRV emissions and potentially other stacked incentives from RAAC and partner protocols. RAAC has promoted opportunities for veCRV, vlCVX, and sdCRV holders to vote on allocations to pmUSD and iREET pools, shaping the emissions that flow to these pairs and potentially boosting yields into the 20–25% APR range for early participants, depending on CRV prices and bribe dynamics. By pairing iREET with pmUSD, RAAC effectively builds a “real assets square” on Curve, where a gold-backed stablecoin trades directly against a real estate-linked token, with CRV incentives rewarding users who take both sides of the trade.

Real Estate Risk and the HCVP Angle

Tokenizing real estate introduces a different constellation of risks than tokenizing gold. While gold prices are volatile but globally observable and liquid, real estate valuations depend on appraisals, local market conditions, and idiosyncratic property-level factors. RAACLend attempts to mitigate some of this by focusing on properties participating in the Housing Choice Voucher Program, where rental income is at least partially backed by government vouchers, reducing tenant default risk and smoothing cash flows. Nevertheless, property management risk, maintenance costs, vacancy periods, regulatory changes in housing policy, and interest rate fluctuations can materially impact net operating income and property valuations, which in turn affect the leverage capacity and risk profile of iREET and any stablecoins minted against real estate collateral.

Because iREET is a synthetic representation rather than a direct, legally enforceable share of a REIT-like entity for most users, the legal claim chain from the token to the underlying property income may be more complex than in traditional securities structures. RAAC’s documentation emphasizes compliant structuring on the gold side through IONau, but the precise legal form of real estate claims and how they flow through to token holders remains an area where investors must perform careful due diligence. If RAACLend relies on SPVs or trusts to hold properties and then issues on-chain claims against those entities, jurisdictional and securities law questions will arise, especially for users in tightly regulated markets.

Another important dimension is liquidity. Even if iREET trades actively on Curve and other DEXs, the underlying real estate is highly illiquid. If a large number of token holders sought to exit at once, secondary market liquidity could dry up long before properties could be sold or refinanced, potentially leading to sharp discounts to net asset value. In that sense, DeFi’s instant exit option and real estate’s slow exit reality are structurally in tension. RAAC’s approach of starting with bond-like lockups and controlled distribution may alleviate some of the immediate liquidity mismatch, but over time, systemic risk could emerge if leverage builds against iREET or if large positions are concentrated in a few wallets.

On the other hand, if RAACLend can successfully route HCVP-backed rental income into iREET yield streams, it would represent a meaningful step toward making subsidized housing cash flows investable via DeFi rails, which is a novel and potentially socially impactful use case. In such a scenario, iREET would not only reflect property values but also function as a conduit for predictable, policy-driven rental income into decentralized capital markets.

RAAC announces tentative agreement with a physical gold exchange provider to facilitate pmUSD redemptions, which is expected to begin the first week of July or even sooner.

RAAC Bots free-mint listed on MagicEden, August 7 mint date confirmed

pmUSD gold-backed stablecoin launched via $1M Apebond bond sale on December 18; points program begins

pmUSD $1M bond fully subscribed; whitepaper published

pmUSD reaches $27M TVL on Curve within two months of launch

Frax strategic partnership announced: pmUSD paired with frxUSD in FraxSwap and FraxLend pools

ION partnership for $200M gold tokenization covered organically by the Financial Times

iREET tokenized real estate token launches with $1.135M bond and up to 25%+ CRV APR via RAACLend

Physical gold redemptions for pmUSD expected to begin via tentative exchange provider agreement

RAAC In The DeFi Stack: Curve, Frax, Squid Pass, and Community Infrastructure

Curve Finance as Liquidity Backbone

Curve Finance has emerged as the central liquidity backbone for RAAC’s ecosystem. RAAC has announced a long-term strategic collaboration with Curve, committing to deploy over 100 million dollars in pmUSD liquidity and to make Curve its core infrastructure layer for stablecoin routing and RWA integrations. This manifests in multiple pools: stable pools for pmUSD versus other dollar-pegged assets, metapools where pmUSD inherits liquidity from established stablecoin baskets, and mixed-asset pools such as iREET/pmUSD that link real estate exposure with gold-backed liquidity. For RAAC, Curve’s dominance in stablecoin swaps and its gauge system for directing CRV emissions make it an ideal platform to bootstrap deep liquidity and attract sophisticated DeFi participants.

The Curve DAO’s governance process plays a key role in determining how attractive pmUSD and iREET pools will be for liquidity providers. Gauge proposals must be submitted and approved before pools earn CRV emissions; one such proposal for an iREET/pmUSD pool has already achieved quorum and unanimous support, indicating at least initial community openness to RAAC-linked assets. Once a gauge is active, veCRV, vlCVX, and sdCRV holders can vote on how much weight to allocate to pmUSD and iREET pools, with RAAC and its allies able to influence outcomes through bribes, partnerships, or strategic vote accumulation. This interplay between protocol teams and Curve’s governance is a familiar pattern in DeFi and is central to RAAC’s strategy of embedding pmUSD liquidity into what some call the “Curve flywheel.”

For users, the result is a set of opportunities to earn yield by providing liquidity to pmUSD pools and related pairs. In periods of strong incentives, APRs on pmUSD liquidity provision have been reported in the double digits, sometimes exceeding 25% when stacking CRV, partner incentives, and protocol-specific rewards such as RAAC points. However, these yields are partly a function of token incentives and gauge wars, which are inherently volatile and subject to governance dynamics, emissions schedules, and token price action. Over the long term, RAAC’s challenge will be to transition from “subsidized” Curve yields to sustainable, cash-flow-backed yields derived from gold and real estate income, without losing liquidity depth or community interest.

The Frax Partnership and RWA Stablecoin Stacks

RAAC’s partnership with Frax Finance adds another dimension to its integration into the DeFi stack. Frax has announced a strategic collaboration with RAAC to build Treasury bill- and RWA-backed stablecoin pools in DeFi, with pmUSD pairing with Frax’s dollar stablecoin frxUSD as a core route. The combined pool is intended to be one of the deepest T-bill- and RWA-based stablecoin pools in the space, mixing pmUSD’s gold-backed design with frxUSD’s exposure to short-duration U.S. government debt and other reserve assets. This arrangement effectively creates a composite RWA basket in which users can move between gold-linked and T-bill-linked stablecoins without leaving DeFi, while liquidity providers earn yields from trading fees and incentives.

Beyond Curve, the partnership envisions integrating pmUSD across Frax’s product suite, including FraxSwap and FraxLend. In FraxSwap, pmUSD could function as a base or quote asset in concentrated liquidity markets, while in FraxLend it could be listed as collateral or a borrowable asset, depending on risk assessments and governance decisions. Such integrations would deepen pmUSD’s utility beyond pure swap pairs, making it part of a broader RWA-based money market architecture that includes Frax’s suite of products like sfrxETH, frxETH, and other yield-bearing tokens. For RAAC, this offers a path to embed pmUSD within one of DeFi’s more established RWA-focused stablecoin systems, potentially enhancing its resilience and adoption.

This cross-pollination between RAAC and Frax reflects a broader trend in DeFi toward stacking multiple forms of RWA exposure. Rather than relying solely on crypto-backed overcollateralized loans or on opaque fiat reserves, protocols are increasingly combining gold, T-bills, real estate, and other off-chain assets to build diversified, yield-generating stablecoin portfolios. RAAC’s gold-backed pmUSD, paired with Frax’s T-bill-backed frxUSD, is one instantiation of this trend. If RAACLend’s real estate instruments such as iREET eventually become accepted collateral in FraxLend or similar platforms, the result could be a multi-layered architecture where gold, Treasuries, and rental income all back interlocking stablecoin and lending markets.

Media, Community, RAAC Bots, Llama Party, and Squid Pass

RAAC’s growth strategy is not purely technical; it also leans heavily on community-building, media partnerships, and access NFTs. One of the more distinctive elements is the introduction of RAAC Bots, a limited, free-mint membership NFT genesis collection that functions as more than a digital collectible. Holders of RAAC Bots have been given privileged access to early pmUSD bond sales on ApeBond, higher reward multipliers, and additional bonuses such as extra percentages on bond payouts when funding caps are filled. The RAAC Bots collection has been listed on the MagicEden launchpad with a formal mint date, underlining RAAC’s attempt to bridge the NFT and DeFi communities with a membership token that confers ongoing benefits in the RAAC ecosystem.

This membership layer is intertwined with a broader points and airdrop strategy. RAAC has publicly discussed whitelisting wallets across the Curve ecosystem and publishing airdrop eligibility checkers, rewarding early pmUSD liquidity providers and participants in bond sales with points that are expected to convert into allocations in a future RAAC token generation event. Integrations with Curve, Convex, StakeDAO, Yearn, and Gearbox have been highlighted as avenues through which users can earn RAAC points while farming pmUSD yields, further embedding RAAC into the existing DeFi yield-maximization culture. Live community events such as “Llama Party” streams, featuring the launch of RAAC and its products, have been used to announce milestones, explain tokenomics, and coordinate with other projects and influencers.

RAAC has also partnered with decentralized media infrastructure, integrating a Leviathan News headline feed directly into its Discord server and experimenting with $SQUID-powered headline streaming to keep its community informed about DeFi developments. This has overlapped with the use of Squid Pass credentials and related tools in some RAAC-aligned communities, connecting access to RAAC content, events, or rewards with broader on-chain media and reputation systems. In this configuration, RAAC is not just building financial primitives but is participating in an emerging stack that combines RWAs, DeFi protocols, NFT-based memberships, and decentralized news distribution.

At the same time, the reliance on Discord and other centralized social platforms introduces attack surfaces. There have been instances in which RAAC’s Discord server has reportedly been compromised, leading to warnings not to interact with suspicious links or announcements until verified. This risk is not unique to RAAC; Discord itself has suffered security incidents, including breaches via third-party customer support vendors that exposed usernames, emails, IP addresses, and even government ID images for some users who had submitted age-verification tickets. Such incidents highlight that even sophisticated DeFi protocols with robust on-chain architectures can have their communities targeted through off-chain channels, making user education and cautious operational practices essential.

In sum, RAAC’s community stack blends financial incentives, NFT memberships, points systems, media integrations, and social events into a cohesive, if complex, growth engine. Whether this engine ultimately converts early speculative energy into durable, RWA-backed usage will depend on how well RAAC can deliver on its gold and real estate theses while maintaining trust and security in both its on-chain and off-chain interfaces.

RAACLend is a newly launched lending protocol and pmUSD is an early-stage stablecoin; neither has a long live-production track record to stress-test under adverse market conditions.

Physical gold backing for pmUSD redemptions depends on a single unnamed exchange provider agreement that was still 'tentative' as of mid-2025, creating a single point of failure for the peg mechanism.

Tokenizing real estate (iREET) and gold (pmUSD) for DeFi yield likely triggers securities and commodity regulations across multiple jurisdictions, and the ION partnership's FT coverage increases regulatory visibility.

pmUSD reached $27M TVL within two months of launch, but bond-sale lockup structures and reliance on Curve gauge incentives mean liquidity is incentive-dependent and could exit rapidly if CRV rewards compress.

Gold price volatility affects the collateral value underlying pmUSD; a sharp gold drawdown could stress the peg before the physical redemption mechanism is fully operational.

A confirmed Discord compromise was publicly flagged, indicating the project's community infrastructure has been targeted by threat actors, a common precursor to phishing attacks on holders.

Risk, Regulation, and Operational Considerations

Market and Collateral Risks: Gold and Real Estate

RAAC’s choice of gold and U.S. real estate as foundational collateral introduces both diversification benefits and new risks. Gold has historically been seen as a store of value and a hedge against fiat debasement, but its price is volatile on shorter timeframes, and the specific form of gold backing pmUSD—in-situ reserves—adds idiosyncratic risk related to extraction feasibility, jurisdiction, and geological uncertainty. RAAC attempts to mitigate this by heavily discounting collateral values when minting pmUSD, using only 20% of LBMA spot value, resulting in a 5:1 reserve ratio. Nonetheless, severe and prolonged declines in gold prices, legal disputes over reserve ownership, or operational failures at the level of I-ON’s tokenization could all stress the system, especially if they coincided with DeFi market turmoil.

Real estate collateral in RAACLend and iREET structures is subject to a different risk set. Interest rate cycles can dramatically affect capitalization rates, borrowing costs, and property valuations, while local policy changes can influence housing demand and landlord obligations. RAAC’s focus on properties in the Housing Choice Voucher Program is a bet on the stability of U.S. federal housing subsidies, but changes in budget priorities, program rules, or administrative efficiency could affect the regularity and magnitude of rental payments. Moreover, property management quality, maintenance expenditures, and neighborhood-level developments can all impact net operating income, feeding into iREET’s economic underpinnings and the safety of any stablecoins or credit instruments backed by real estate collateral.

Correlation between gold and real estate is not necessarily low in macro stress scenarios. A sharp rise in real yields, for instance, could simultaneously weigh on gold prices and compress real estate valuations, hitting both pillars of RAAC’s collateral stack at once. While RAAC’s structures may be overcollateralized and diversified at the protocol level, users who hold concentrated positions in pmUSD and iREET could find themselves exposed to a complex mix of commodity, interest rate, and housing market risk that is not always transparent in token price charts. For institutional users, this may be acceptable as part of a broader allocation strategy, but for retail users seeking “stable” yield, it demands a level of macro awareness that is not always prevalent in DeFi.

Smart Contract, Oracle, and Counterparty Risk

Beyond market risk, RAAC’s architecture is exposed to the usual spectrum of smart contract and oracle vulnerabilities that accompany any complex DeFi protocol. The RWf(x) implementation is a fork of the f(x) Protocol 1.0, with modifications such as internalizing the leveraged gold position (xGOLD) rather than offering it to the public. Forking a mature protocol can bring battle-tested code but also the risk of misconfigurations or unanticipated interactions in the new environment. Given that pmUSD minting, PSM operations, and collateral accounting are all heavily on-chain, any bug, mispriced oracle, or permissioning error could have systemic consequences for the stablecoin’s solvency and peg.

Oracle risk is particularly salient. Gold prices and IONau valuations must be accurately reflected in on-chain positions for RAAC’s reserve and leverage calculations to remain correct. I-ON’s IONau instruments rely on daily LBMA spot pricing, while RAAC uses Chainlink Proof of Reserve and Instruxi Reserve data to attest to collateral holdings. If either the LBMA price feeds or the Chainlink PoR mechanisms were to be compromised, manipulated, or delayed, pmUSD could become either undercollateralized or unnecessarily constrained, leading to loss of confidence or missed opportunities. Similarly, in RAACLend, real estate valuations and rental income assumptions must be translated into token economics via models that are only as good as their inputs.

Counterparty risk extends to I-ON Digital Corp, custodians, legal entities holding real estate, and any off-chain service providers involved in tokenization, custody, or compliance. While I-ON emphasizes that IONau is an institutional-grade security with a regulated custody framework, holders of pmUSD ultimately rely on I-ON’s continued solvency and regulatory compliance, as well as RAAC’s ability to enforce claims against IONau collateral in adverse conditions. In the real estate vertical, RAACLend must trust property managers, valuation agents, and legal counsel to maintain assets and contracts in good standing. This web of off-chain counterparties is intrinsic to any RWA protocol but can be at odds with DeFi’s aspirations for trust minimization.

Governance, Centralization, and Regulatory Questions

Pharos Watch’s assessment that pmUSD uses a centralized governance model, with manager-only minting and admin freeze controls, points to a deliberate design choice by RAAC to prioritize managed risk over permissionless expansion. While this may be necessary for handling regulated collateral and complex RWA structures, it creates a single point of governance failure and raises questions about how power will be distributed once RAAC’s own governance token is fully launched. RAAC’s whitepaper notes that the $RAAC token will coordinate components such as RWf(x), the RAACLend index, and distributions, indicating an intent to layer in protocol-level governance. However, the path and timeline toward meaningful decentralization remain unclear, and in the interim, users must accept a high degree of trust in the current operators.

Regulatory considerations loom large over RAAC’s model. IONau is explicitly described as a digital security, with fractional ownership rights in gold reserves and institutional-grade compliance. This implies that, at least on the gold side, RAAC’s collateral base is squarely within securities law frameworks, even if pmUSD itself is presented as a stablecoin. Depending on jurisdiction, regulators may view pmUSD as a derivative of a security, a form of deposit-like instrument, or something else entirely. The involvement of real estate, including HCVP-backed properties, adds another layer of potential regulatory scrutiny related to securities, investment company rules, and tax treatment.

RAAC’s founder has publicly called for DeFi to collaborate with “suitcoiners”—a shorthand for traditional finance actors entering the space—while maintaining core decentralization principles. This encapsulates RAAC’s balancing act: it seeks to work with regulated entities like I-ON and engage traditional housing markets, yet it operates through smart contracts, yield farming, and NFT-based membership systems that are native to DeFi culture. The more deeply RAAC integrates with TradFi, the more it may face demands for KYC, restrictions on access for certain jurisdictions, and constraints on how its tokens can be marketed or used. How RAAC navigates this tension will significantly shape its long-term viability.

Security Hygiene: Discord Compromises and User Protection

As noted earlier, RAAC’s reliance on Discord and other centralized communication channels introduces additional risk vectors that are not captured in smart contract audits. There have been episodes where RAAC’s Discord server was reportedly compromised, prompting warnings from observers and the team itself not to engage with links, DMs, or announcements that had not been verified through official channels. Such incidents are common in DeFi, where attackers routinely attempt to hijack server permissions, impersonate team members, or exploit bots to distribute malicious links.

These project-specific incidents take place against a broader backdrop of platform-level vulnerabilities. Discord has experienced security breaches via third-party support vendors, exposing names, Discord usernames, email addresses, IP addresses, and even images of government IDs for users who had appealed age determinations or undergone identity verification. Victims of such breaches can face increased risk of phishing, SIM swapping, and targeted social engineering, especially in crypto communities where wallet addresses, investment activity, and social graphs are often public. For RAAC users, this means that protecting their accounts and being skeptical of unsolicited messages is as important as understanding on-chain risk.

Best practices in this context include never signing transactions or approvals from links received via DMs, always verifying contract addresses through official websites or reputable aggregators, and using hardware wallets to isolate high-value assets. When interacting with RAAC’s pmUSD bonds, iREET offerings, or liquidity pools, users should rely on URLs announced through verified channels and double-check on-chain addresses against multiple sources, including RAAC’s documentation and well-known DeFi dashboards. Given the complexity of RAAC’s structures and the relatively high yields on offer, the protocol is likely to be an attractive target for both smart contract exploits and social engineering campaigns, making multi-layered operational security essential.

Outlook

RAAC sits at the intersection of several powerful trends in crypto: the rise of real-world assets as collateral, the maturation of stablecoin engineering, the deepening of Curve and Frax as RWA infrastructure hubs, and the convergence of DeFi, NFTs, and decentralized media. Its gold-backed stablecoin pmUSD leverages a novel in-situ gold tokenization rail via I-ON’s IONau digital security, overcollateralized through an RWf(x) structure and defended with a PSM, then routed into deep liquidity on Curve and, increasingly, into Frax’s RWA pools. Parallel efforts in RAACLend and iREET aim to bring subsidized U.S. real estate income into DeFi, tokenizing HCVP-backed rental streams into tradable and composable assets. If these verticals can be operationalized at scale, RAAC could emerge as a significant player in an RWA-dominated phase of DeFi.

At the same time, RAAC’s trajectory is far from riskless. pmUSD has already exhibited peg volatility, and its structure introduces dependencies on gold prices, I-ON’s tokenization apparatus, Chainlink PoR, the Sky Protocol’s sUSDS, and RAAC’s own centralized governance. Real estate tokenization via iREET and RAACLend confronts the perennial challenges of property management, valuation, liquidity, and complex legal structuring, all while being layered into an on-chain environment that expects instant settlement and composability. Community-driven growth mechanisms—RAAC Bots, points programs, Squid-powered media feeds, Llama Party events—can be powerful bootstrapping tools but also risk overemphasizing speculative yield and airdrop farming at the expense of sustainable, RWA-backed demand.

Looking forward, several milestones will be important to watch for anyone following or participating in RAAC’s ecosystem. On the gold side, the move from purely on-chain pmUSD markets to facilitated redemptions through physical gold exchange providers—an initiative RAAC has signaled through tentative agreements—will be a critical test of how directly pmUSD connects to tangible metal. If users can reliably convert pmUSD into deliverable gold or gold-linked financial products, the token’s positioning as a “gold-backed dollar” will be substantially strengthened. On the real estate side, the full launch of RAACLend, the scaling of iREET issuance, and the demonstration of consistent, rental-income-backed yields will determine whether RAAC can make good on its promise to channel stable off-chain cash flows into DeFi.

Finally, RAAC’s integration into the broader DeFi stack—through Curve gauges, Frax RWA pools, and potentially inclusion as collateral in major lending markets—will influence its systemic importance and risk profile. A pmUSD that is deeply embedded in multiple protocols and used as a base asset in high-leverage strategies can enhance capital efficiency but also amplify contagion risk if something goes wrong at the collateral or governance level. For now, RAAC represents an ambitious and sophisticated attempt to fuse gold, real estate, and DeFi into a unified RWA platform. Whether it ultimately becomes a cornerstone of an RWA-heavy crypto economy or a cautionary tale about the complexity of marrying TradFi assets with permissionless systems will depend on execution, transparency, and the protocol’s ability to maintain both economic and social trust over time.

Latest RAAC news

Curve Finance gauge vote live: RAAC allocates to pmUSD gauge with veCRV, vlCVX, sdCRV holders eligible to vote.$iREET launches, enabling up to 25%+ $CRV APR on tokenized real estate via RAAC protocolRAAC announces tentative agreement with a physical gold exchange provider to facilitate pmUSD redemptions, which is expected to begin the first week of July or even sooner.This Thursday December 18th, RAAC is officially launching its gold-backed stablecoin $pmUSD!

The launch is via a bond sale on Apebond, where $1M pmUSD will be available with a reward going from 2 to 5%!

This means: for every $1 USDT / USDC you deposit, you receive up to $1.05 pmUSD after the locking period. On top of that, this sale also marks the start of the RAAC points program, and participating in this sale will grant the biggest point multiplier of the program!

Finally, this sale is private for the RAAC Bots holder, the Llamas and the ApeBond premium users!

Follow RAAC on X for additional details! RAAC and Frax have formed a strategic partnership to establish deep T-bill and RWA-backed stablecoin pools in DeFi, with pmUSD paired as a core route alongside frxUSD. This collaboration aims to reinforce a liquidity flywheel and expand pmUSD's utility across Frax's product suite, including FraxSwap and FraxLend.

RAAC and Frax have formed a strategic partnership to establish deep T-bill and RWA-backed stablecoin pools in DeFi, with pmUSD paired as a core route alongside frxUSD. This collaboration aims to reinforce a liquidity flywheel and expand pmUSD's utility across Frax's product suite, including FraxSwap and FraxLend. The RAAC $pmUSD vault sold out, earning depositors a bonus 10%

The RAAC $pmUSD vault sold out, earning depositors a bonus 10%Sources

- https://pmusd.raac.io

- https://raac.io

- https://iondigitalcorp.com

- https://www.curve.finance/dex/ethereum/pools/factory-stable-ng-652/swap

- https://x.com/DeFi_Dad/status/2039752707829813547

- https://x.com/fraxfinance/status/2016534107778400619

- https://www.youtube.com/watch?v=GbXATeFfkRA

- https://www.coingecko.com/en/coins/precious-metals-usd

- https://blog.raac.io

- https://x.com/leviathan_news/status/1950785418737119645

- https://pharos.watch/stablecoin/pmusd-precious-metals/

- https://ngntipkolamrenang.twstalker.com/AungPhyo2281

- https://docs.raac.io/whitepaper-q1.pdf

- https://www.curve.finance/dao/ethereum/proposals/

- https://x.com/thedefiedge/status/2027414495602086273

- https://x.com/Raacfi/status/2003094392890953992

- https://x.com/Raacfi

- https://x.com/RegnumAurum/status/1937903906035769557

- https://x.com/LlamaQuestNFTs

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…