Deep dive on Florida’s crypto, stablecoin, Bitcoin reserve and AI landscape, covering tax perks, fintech sandbox, state stablecoin law, CBDC pushback, Ponzi crackdowns, and OpenAI litigation shaping this pivotal U.S. jurisdiction.

+11 sources across the wider coverage universe

CFTC secures $1.3M penalty and trading ban against Florida resident in commodity pool fraud case, reinforcing crackdown on market abuse2026-04

CFTC secures $1.3M penalty and trading ban against Florida resident in commodity pool fraud case, reinforcing crackdown on market abuse2026-04 Florida passes first US state-level stablecoin bill, SB 314, creating a regulatory framework for payment stablecoin issuers aligned with federal GENIUS Act standards and enhancing consumer protections2026-03

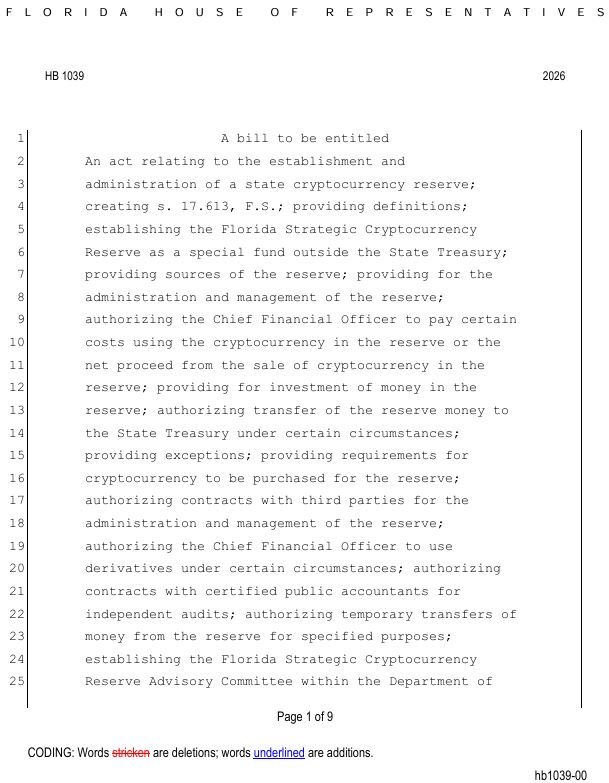

Florida passes first US state-level stablecoin bill, SB 314, creating a regulatory framework for payment stablecoin issuers aligned with federal GENIUS Act standards and enhancing consumer protections2026-03 Florida lawmakers renew push to launch State Bitcoin Reserve. On Tuesday, Florida lawmakers introduced another bill for the creation of a strategic Bitcoin reserve, less than a year after two attempts were shelved.2026-01

Florida lawmakers renew push to launch State Bitcoin Reserve. On Tuesday, Florida lawmakers introduced another bill for the creation of a strategic Bitcoin reserve, less than a year after two attempts were shelved.2026-01 Why Not!

Crypto investors behind the $PATRIOT memecoin fund a 15-foot golden “Don Colossus” statue of President Trump, awaiting installation at his Doral golf resort in Florida.2026-02

Why Not!

Crypto investors behind the $PATRIOT memecoin fund a 15-foot golden “Don Colossus” statue of President Trump, awaiting installation at his Doral golf resort in Florida.2026-02 Florida bill proposes creating a state-run strategic crypto reserve that would primarily hold Bitcoin, potentially making it a formal part of Florida’s financial assets by mid-2026.2026-01

Florida bill proposes creating a state-run strategic crypto reserve that would primarily hold Bitcoin, potentially making it a formal part of Florida’s financial assets by mid-2026.2026-01 Andrew Tate struggles to pump memecoin amid Florida criminal inquiry2025-03

Andrew Tate struggles to pump memecoin amid Florida criminal inquiry2025-03

Florida’s Evolving Role in Crypto, Stablecoins, and AI Regulation

Among U.S. states, Florida has emerged as a high‑impact laboratory for cryptocurrency, stablecoins, and artificial intelligence, combining a low‑tax environment with aggressive, often experimental regulation. Over the past few years the Sunshine State has launched a financial technology sandbox, pursued the first state‑level stablecoin framework aligned with the federal GENIUS Act, moved to block central bank digital currencies in its commercial law, welcomed political campaigns funded with Bitcoin, and simultaneously become a stage for billion‑dollar Ponzi‑style crypto frauds and high‑stakes legal battles against OpenAI. This explainer traces how Florida’s tax profile, regulatory architecture, enforcement actions, and political identity—shaped heavily by Donald Trump and Governor Ron DeSantis—are converging to define one of the most consequential jurisdictions for crypto, stablecoins, “Bitcoin reserve” strategies, and AI‑driven finance in the United States.

Florida as a Strategic Nexus for Crypto, AI, and Power

Florida’s importance to the crypto and AI conversation is not just a function of its sunshine and beaches. It is now one of the largest state economies in the U.S., a magnet for wealth migration, and a center of gravity for both national Republican politics and global tourism. Those factors combine to make it a natural hub for new financial experiments, from Bitcoin‑backed treasuries to AI‑assisted trading, and for the legal and political fights that inevitably follow. For market participants assessing jurisdictional risk, Florida has become impossible to ignore.

Analysts and industry guides routinely rank Florida among the most crypto‑friendly U.S. jurisdictions, citing its absence of a state income tax, its willingness to experiment with digital‑asset payments for state fees, and regulatory signals that treat many crypto businesses more lightly than traditional money transmitters. At the same time, Florida is home to some of the highest‑profile crypto enforcement stories in the country, including the HyperFund “Bitcoin Rodney” case and other Ponzi‑like schemes targeting retirees and church communities. This juxtaposition of permissive policy and robust enforcement reflects a broader pattern: the state encourages innovation, but it is also prepared to punish what it sees as abuse of that freedom.

Florida’s emerging role in AI regulation adds another layer. Its attorney general has sued OpenAI and Sam Altman on consumer‑protection and product‑liability theories and launched a criminal investigation tying ChatGPT to a campus shooting, while also driving new criminal penalties for AI‑generated child sexual abuse material. These initiatives are framed in moral and almost philosophical terms—arguing that AI should “advance mankind, not destroy it”—and they resonate with similar rhetoric around bitcoin as a “freedom money” alternative to centralized control. The result is an environment where crypto and AI are debated not only as technologies or asset classes, but as symbols in a broader struggle over sovereignty, surveillance, and political identity.

The presence of Donald Trump in Palm Beach and the prominence of Governor Ron DeSantis amplify this dynamic. Mar‑a‑Lago became a focal point of national controversy after the FBI’s search for classified documents, energizing a Florida‑based narrative that federal institutions are weaponized against conservative figures. DeSantis has built on that energy by casting the Biden administration’s interest in a U.S. central bank digital currency (CBDC) as a threat to financial freedom, while seeking to attract Bitcoiners, stablecoin issuers, and AI entrepreneurs as part of a broader “free state” brand. For crypto and AI builders, understanding Florida means understanding a jurisdiction where political symbolism and legal structure are tightly intertwined.

CFTC secures $1.3M penalty and trading ban against Florida resident in commodity pool fraud case, reinforcing crackdown on market abuse

$1.3M clawback on $1.5M solicited — near dollar-for-dollar recovery is rare for CFTC pool fraud cases (compare that to the $128M Brazilian nationals scheme where the ordered penalties are basically uncollectable). Forging an actual CFTC commissioner's signature on a fake license to sell "guaranteed 3.75% monthly" to 32 immigrants is old-school securities fraud wearing a commodity wrapper. Same playbook runs in DeFi yield farms daily, just without the physical paperwork — the CFTC can chase Matos because there's a name and a Florida address attached. Permissionless fraud is harder to settle.

Florida readers click hardest on the tension between DeSantis-era crypto libertarianism and the institutional reality check — Bitcoin reserve bills die, memecoins get investigated, and the stablecoin law that passed drew immediate surveillance comparisons to the CBDC ban DeSantis championed.↗

Regulatory Foundations: Tax, Sandboxes, and Money Transmission

Florida’s core appeal to crypto holders and founders begins with its tax and corporate profile. Unlike high‑tax coastal states, Florida does not levy a state income tax on individuals, which means realized crypto gains generally escape state‑level income taxation, even though they remain fully taxable at the federal level. For Bitcoiners pursuing a “Bitcoin reserve” strategy—accumulating BTC as a long‑term store of value and periodically realizing gains—this can materially alter after‑tax outcomes compared with jurisdictions like New York or California, where state income taxes can exceed ten percent. Coupled with relatively low corporate taxes and a cost of living that remains competitive with large coastal metros, this has helped draw both individual traders and crypto‑native companies.

Tax friendliness is only part of the story. Florida has also moved to position itself as a regulatory sandbox for financial technology, including crypto and blockchain projects. The state enacted a Financial Technology Sandbox, codified at Florida Statutes § 559.952, that took effect at the start of 2023 and was promoted as a tool to “solidify Florida as a crypto‑friendly state.” Under this sandbox framework, qualifying companies can test innovative financial products and services in a controlled environment with certain regulatory requirements relaxed or modified, subject to oversight by the Office of Financial Regulation (OFR). Although the statute is technology‑neutral, blockchain‑based payments, digital wallets, and other crypto‑adjacent services are explicitly contemplated within its scope, giving startups an avenue to experiment without immediately bearing the full weight of money‑transmission or banking regulation.

Tax Profile and Economic Incentives for Crypto

For a crypto‑savvy audience, Florida’s personal tax policy is particularly salient. Because the state lacks a personal income tax, there is no separate state capital gains regime; crypto trades that would generate state tax obligations in New York, for example, generate none in Florida. This does not change federal tax treatment—taxpayers must still report crypto disposals and pay federal income and capital gains taxes—but the absence of a state layer can be decisive for high‑volume traders or long‑term holders finally realizing large Bitcoin gains. Some wealth planners now explicitly recommend residency in states like Florida or Wyoming as part of a holistic Bitcoin reserve strategy, in which clients hold BTC as a quasi‑treasury asset and manage dispositions with an eye to minimizing the combined tax drag.

Beyond individual taxation, Florida has signaled a willingness to integrate crypto into public finance workflows. Under Governor DeSantis, the state proposed a pilot program that would allow businesses to pay certain state fees in digital currencies, effectively testing crypto rails as a medium for state‑level obligations. Public reporting indicated that DeSantis expected Florida businesses to “soon” be able to pay state fees in crypto, reinforcing his broader narrative that Florida would be on the front line of financial innovation. Although the scale of such programs remains modest, they underscore the state’s willingness to treat digital assets as a legitimate transactional medium rather than a purely speculative asset class.

Crypto tax and compliance guides also point to Florida’s treatment of crypto businesses under its money‑transmission laws as part of its crypto‑friendly profile. One such analysis notes that Florida has exempted certain crypto businesses from money transmission licenses, though the details turn heavily on the precise nature of the service (custody, exchange, or payments processing) and on evolving regulatory interpretations. For founders, this means that while Florida may require fewer licenses than some states for non‑custodial services or purely software‑based wallets, the picture is far from uniform. Given the interplay with federal obligations under the Bank Secrecy Act and FinCEN guidance, serious operators still treat Florida as a jurisdiction that demands high‑caliber legal advice rather than a regulatory free‑for‑all.

Fintech Sandbox and Money Services Regulation

The fintech sandbox is one of Florida’s most explicit tools for signaling openness to crypto and blockchain experimentation. By statute, eligible firms can request a waiver or relaxation of specific Florida financial regulations for a limited period, during which they test a product with a defined number of consumers, transaction limits, and disclosure requirements. For a startup building, for example, a crypto‑collateralized lending product or an AI‑driven robo‑advisor that rebalances a user’s Bitcoin and stablecoin portfolio, the sandbox can reduce initial compliance burdens while the viability and risks of the service are evaluated. Regulators remain involved, and consumer protections are not suspended, but the framework consciously moves away from a “license first, innovate later” posture.

This sandbox exists alongside Florida’s broader Money Services Businesses (MSB) regime, under which money transmitters, payment instruments sellers, and similar entities must generally be licensed and subject to anti‑money‑laundering obligations. The state’s new stablecoin framework, discussed later, grafts directly onto this MSB architecture by creating a special category for “qualified payment stablecoin issuers.” Consequently, even where sandbox relief is available, companies planning to operate at scale with customer funds—or to issue or redeem tokens that function as money—must think in terms of MSB licensing, ongoing OFR examination, and, for larger operations, eventual federal oversight.

The sandbox also serves a signaling function to federal and out‑of‑state stakeholders. When a state like Florida brands itself as a place where crypto and AI‑driven finance can be trialed in a supervised but flexible environment, it encourages founders who might otherwise gravitate to offshore jurisdictions to consider building domestically. In turn, this can attract conferences, venture capital, and specialist service providers, reinforcing a local ecosystem. For investors, the existence of a sandbox does not guarantee that any given project is safe or compliant, but it can indicate that regulators are aware of and engaged with the activity rather than blindly hostile.

Crypto in State Payments and Campaign Finance

Florida’s openness to crypto is visible not only in administrative policy but also in political fundraising and campaign messaging. As early as 2023, reporting indicated that Governor DeSantis was preparing to accept cryptocurrency donations to his political committees, with a high‑profile Miami fundraiser intended as a launch point. That choice placed him alongside a small but growing group of U.S. politicians who see accepting Bitcoin or other digital assets as both a fundraising tool and a signal of alignment with tech‑savvy, anti‑establishment voters. The move was especially pointed given Miami’s aggressive branding under then‑Mayor Francis Suarez as a “crypto capital,” with city‑branded tokens and promotional campaigns aimed at luring blockchain companies.

Parallel to campaign contributions, Florida has flirted with crypto in state operations. DeSantis’s proposal for businesses to pay state fees in digital currencies suggested a willingness to use crypto not only as a symbol but as an operational medium for government collections. While such programs are rarely frictionless—volatility, custody, and vendor integration all pose challenges—they demonstrate a reiterating theme: Florida’s top leadership wants to be seen not merely as regulating crypto, but as using it. For holders pursuing a Bitcoin reserve strategy, this kind of state acceptance can be psychologically significant, reinforcing the idea that BTC is converging toward a parallel monetary system in which even governments participate.

At the same time, the integration of crypto into campaign finance raises familiar concerns. Issues of transparency, foreign influence, and compliance with Federal Election Commission guidelines around in‑kind contributions and valuation are all intensified when the asset is volatile and programmable. Florida’s experiments therefore serve as live test cases for how American democracy will handle digital money in its own bloodstream. For a crypto news audience, Florida offers both regulatory signals and political theater on this front, foreshadowing how national races might be funded in an increasingly tokenized economy.

Florida’s State‑Level Stablecoin Framework

One of the most consequential developments for digital assets in Florida is the state’s attempt to craft a comprehensive stablecoin regime aligned with emerging federal law. The legislative centerpiece is the Payment Stablecoin framework, advanced through Senate Bill 314 and its House counterpart, House Bill 175, which together seek to regulate “qualified payment stablecoin issuers” as a specific category within the state’s money services laws. The design is explicitly modeled on the federal Guiding and Establishing National Innovation for U.S. Stablecoins Act, known as the GENIUS Act, which aims to create a nationwide framework for payment stablecoin issuance.

SB 314, as analyzed by the Florida Senate, would revise the Florida Control of Money Laundering in Money Services Business Act to expressly include payment stablecoins and prohibit any person from engaging in the activities of a qualified payment stablecoin issuer without being appropriately licensed or exempt. The bill defines such issuers as a distinct category of money services business and outlines the procedures for registration with the Office of Financial Regulation, including application requirements and prudential standards. Although SB 314 itself was ultimately laid on the table in favor of the House companion, its language and analysis shaped the framework that would eventually pass.

House Bill 175, whose analysis describes it as implementing a state regulatory framework “pursuant to” the federal GENIUS Act, carries forward these concepts and specifies the concrete requirements for payment stablecoin issuers operating in Florida. Together, these measures amount to America’s first fully fleshed‑out state‑level stablecoin statute linked to an explicit federal template, making Florida a national pace‑setter in this area.

Origins and Alignment with the GENIUS Act

The GENIUS Act at the federal level lays out a regime for “permitted payment stablecoins,” requiring issuers to meet standards around capital, liquidity, risk management, and marketing, and to operate under the supervision of federal banking regulators such as the Federal Reserve or the Office of the Comptroller of the Currency. Its basic philosophy is that tokens referencing the U.S. dollar and intended for everyday payments should be issued only by well‑regulated entities holding high‑quality, liquid reserves, and that such issuers should be subject to rigorous supervision comparable to banks. By aligning closely with this framework, Florida is signaling that it does not intend to become a haven for unregulated dollar‑pegged tokens; instead, it wants to harmonize state oversight with emerging federal norms.

The Senate analysis of SB 314 makes this explicit, stating that the bill is “substantially similar” to the GENIUS Act and that it creates a state regulatory framework to regulate payment stablecoin issuers as money services businesses or trust companies. The House analysis of HB 175 echoes this framing, noting that issuers must comply with prudential requirements consistent with the GENIUS Act and that the Office of Financial Regulation will be responsible for implementing and enforcing these standards at the state level. By tying its regime so directly to a federal statute, Florida both reduces legal uncertainty for issuers who might otherwise face divergent state and federal rules, and positions itself as a cooperative partner rather than an outlier jurisdiction.

This coordination extends to oversight thresholds. Under SB 314’s analysis, an issuer whose consolidated total issuance reaches \(10\) billion dollars is required to transition to federal oversight unless a waiver is obtained, effectively capping the size of purely state‑regulated stablecoin programs. This mechanism ensures that Florida can facilitate smaller or emerging stablecoin issuers under its own MSB framework while automatically escalating systemic players into the federal orbit envisioned by the GENIUS Act. For a crypto audience, the message is that Florida is open for stablecoin business—but only for those ready to live under bank‑like scrutiny as they scale.

Licensing, Reserves, and Prudential Requirements

The operational core of Florida’s stablecoin regime lies in its licensing and reserve mandates. Effective October 1, 2026, HB 175 requires that any entity wishing to be a “qualified payment stablecoin issuer” must either obtain a money services business license that specifically covers such issuance or, if it is organized as a trust company, obtain a certificate of approval from the Office of Financial Regulation. The OFR must then review applications and issue written approvals or denials, anchoring the stablecoin space firmly within the state’s existing licensing apparatus.

Once licensed, issuers must comply with stringent prudential requirements. The House analysis specifies that qualified payment stablecoin issuers must maintain identifiable reserves equal to at least 100 percent of outstanding payment stablecoins, mirroring the 1:1 reserve principle embedded in the GENIUS Act. These reserves must be held in highly liquid, low‑risk instruments such as cash and short‑term Treasuries, and must be segregated so that, in the event of insolvency, stablecoin holders can be made whole from the reserve pool. Marketing and disclosure obligations aim to prevent misrepresentation of reserve composition or redemption rights, addressing concerns raised by past controversies around stablecoin backing.

In practice, this means that a Florida‑licensed payment stablecoin cannot behave like an unregulated offshore token that promises dollar parity while actually holding a mix of commercial paper, risky loans, or opaque investments. Instead, it must resemble a narrow‑bank instrument, with conservative reserves and transparent governance. Regular reporting to OFR, along with examination powers, gives the state tools to verify compliance and intervene if red flags appear. For users and DeFi protocols that might integrate such a token, the Florida license can serve as a due‑diligence signal—though it does not substitute for independent assessment of smart‑contract risks or counterparty exposures.

CBDC Opposition and Surveillance Debates

Florida’s embrace of regulated payment stablecoins exists alongside an explicit political and legal hostility to central bank digital currencies. In 2023, Governor DeSantis announced a “first‑in‑the‑nation” legislative proposal to amend Florida’s Uniform Commercial Code to explicitly prohibit the use of any federally adopted CBDC as money under state law, as well as any CBDC issued by a foreign reserve or sanctioned central bank. The press release framed CBDCs as tools for financial surveillance and potential weaponization of the banking system, arguing that Floridians needed protection from such centralized digital cash. DeSantis also called on “likeminded states” to adopt similar UCC amendments, aiming to build a multi‑state firewall against CBDCs.

This stance has important implications for the state’s stablecoin policy. Critics note that, in order to satisfy money‑laundering, sanctions, and consumer‑protection mandates, highly regulated payment stablecoins may employ monitoring and transaction‑blocking tools that resemble some of the surveillance capabilities associated with CBDCs. Florida’s own stablecoin bill, by tying issuers into the MSB regime and aligning them with GENIUS Act requirements for risk management and compliance, effectively endorses a model in which private issuers act as gatekeepers, collecting detailed user data and potentially freezing or blocking transactions. Newsroom commentary has therefore described the state’s stablecoin push as “charting risky waters” that echo, at least in functional terms, some of the very tools denounced in the CBDC debate.

For Bitcoin maximalists in Florida, this tension underscores the appeal of a Bitcoin reserve strategy. In contrast to permissioned stablecoins and hypothetical CBDCs, on‑chain Bitcoin held in self‑custody is resistant to both corporate blacklists and centralized transaction filters. Florida’s legal architecture does not directly criminalize self‑custodial BTC holdings, and its tax advantages make such holdings relatively attractive. Yet the state’s eagerness to regulate intermediaries—whether stablecoin issuers or AI platforms like OpenAI—signals that any interface between individuals and the broader financial system will be subject to intensifying oversight. For crypto participants, the central question becomes how to balance the convenience of regulated instruments like Florida‑licensed stablecoins with the censorship resistance of base‑layer Bitcoin.

- 01DeSantis anti-CBDC positioning↗

His Twitter Spaces Bitcoin endorsement and CBDC ban framed Florida as the ideological frontline of the federal vs. state crypto sovereignty fight, driving high curiosity clicks.

- 02Bitcoin reserve bills collapse↗

Readers engaged with the gap between legislative ambition and political reality as HB 487 and SB 550 were withdrawn despite repeated attempts across multiple sessions.

- 03Andrew Tate memecoin inquiry

The collision of a polarizing celebrity, a pump-and-dump dynamic, and a criminal investigation made this the single highest-clicked angle on the topic.

- 04State stablecoin framework passage↗

Florida becoming the first US state to pass a stablecoin bill drew readers tracking whether state-level regulation could outpace federal gridlock.

- 05Crypto Ponzi enforcement↗

Multiple Florida-based fraud cases — including a $328M scheme and a CFTC commodity pool penalty — signaled the state as both a crypto hub and a fraud magnet.

- 06Stablecoin surveillance contradiction↗

Critics noting that SB 314's compliance framework mirrored the surveillance architecture DeSantis banned under the CBDC blockade created a pointed irony readers clicked to unpack.

Enforcement, Ponzi Schemes, and Investor Protection

No discussion of Florida’s crypto landscape is complete without addressing its role in some of the highest‑profile enforcement actions and Ponzi‑style scandals of the current cycle. The state’s demographic composition—home to many retirees and high‑net‑worth individuals—combined with its reputation as a lightly regulated, opportunity‑rich environment, has made it a fertile ground both for legitimate innovation and for fraudsters leveraging buzzwords like “Bitcoin” and “AI” to lure victims. Federal agencies, including the Department of Justice and the Commodity Futures Trading Commission, have repeatedly targeted Florida‑based actors in cases involving unregistered offerings, commodity pool fraud, and unlicensed money transmission.

Perhaps the most emblematic case for a crypto audience is the HyperFund scandal. In an indictment unsealed in early 2024, federal prosecutors charged Sam Lee, based in Dubai, with one count of conspiracy to commit securities fraud and wire fraud for allegedly orchestrating a cryptocurrency‑based investment scheme that raised approximately 1.89 billion dollars from investors worldwide. Prosecutors allege that HyperFund, also known by related brand names, operated as a classic Ponzi scheme in which earlier participants were paid “rewards” using funds from new recruits, under the guise of a sophisticated crypto mining and trading operation. Promotional materials reportedly dangled high, regular returns that were economically implausible absent continuous inflows of new capital.

The HyperFund “Bitcoin Rodney” Plea

Florida enters the HyperFund story through one of its most visible promoters, Rodney Burton, known in crypto circles as “Bitcoin Rodney.” In June 2026, the U.S. Department of Justice announced that Burton had pled guilty to a single count of conspiracy to operate an unlicensed money transmitting business in connection with the HyperFund scheme. The plea, entered in the U.S. District Court for the District of Maryland, acknowledged that Burton helped investors move money into and out of the HyperFund ecosystem without the necessary money‑transmission licenses, in violation of federal law. A sentencing hearing was scheduled for July 23, 2026, underscoring that even promoters who are not the architects of a scheme can face serious criminal exposure.

Media coverage emphasized Burton’s identity as a “Florida man,” reinforcing a broader stereotype of the state as both a playground and a cautionary tale for crypto speculation. In practice, his case illustrates several legal and practical lessons. First, operating or facilitating a crypto‑based investment program that accepts and disperses customer funds can trigger money‑transmission obligations, even if the program’s core activities are framed as “staking,” “mining,” or other technical services rather than traditional remittances. Second, the use of Bitcoin or other cryptocurrencies as the nominal asset does not immunize a scheme from being characterized as a securities offering or a Ponzi; what matters is the economic reality and the representations to investors. Third, affiliation with a charismatic brand or influencer culture—whether built around “Bitcoin Rodney” or similar figures—can mask the absence of genuine, verifiable underlying activity.

For Florida‑based investors, the HyperFund case is a reminder that the state’s friendly posture toward innovation does not translate into a guarantee of safety. The presence of a local promoter, a Florida address, or even social proof from community members is not a substitute for rigorous due diligence. From a policy perspective, the case demonstrates why Florida’s legislators have been keen to bring certain digital‑asset activities squarely within the MSB and stablecoin licensing framework: without clear legal channels for regulated operators, the void is more easily filled by Ponzi schemes masquerading as sophisticated crypto finance.

Other Ponzi and Commodity Fraud Cases Involving Floridians

HyperFund is not an isolated episode. Florida law enforcement and federal agencies have pursued multiple cases involving Ponzi‑like structures targeting vulnerable populations, often with a crypto or high‑yield investment twist. One notable example highlighted in official communications involves Brian Shane Haigler, described as a Florida man accused of running a Ponzi scheme that defrauded dozens of elderly and retired church members out of their life savings. While not all of these schemes are purely crypto‑based, they often use the language of modern finance—referencing blockchain, algorithmic trading, or AI‑driven strategies—to lend a veneer of sophistication to what are, in economic terms, simple recycling of new investors’ funds.

Regulators have also targeted Florida residents in commodity pool and derivatives‑related frauds that intersect with the broader digital‑asset market. Newsroom coverage has noted, for instance, a CFTC enforcement action resulting in a 1.3 million dollar penalty and trading ban against a Florida resident involved in commodity pool fraud, reinforcing the message that Florida is not a safe harbor for market abuse merely because some activity occurs online or uses novel assets. These cases often involve misrepresentations about trading expertise, hidden losses, and the misuse of customer funds—risks that are magnified when victims are encouraged to send cryptocurrency, which can be more difficult to recover than fiat transfers once dissipated.

Against this backdrop, Florida’s image as a “crypto‑friendly” state must be understood in nuanced terms. The same factors that attract genuine entrepreneurs—openness, a large retiree population, sunbelt lifestyle, and a history of permissive real‑estate and financial cultures—also attract opportunists. For serious projects, the existence of this enforcement environment means that associating with Florida comes with reputational as well as legal responsibilities. For investors, it underscores the need to distinguish between regulated, properly licensed operations (such as future Florida‑qualified stablecoin issuers) and loosely structured programs that rely on personality‑driven marketing and vague promises.

Lessons for Investors and the “Bitcoin Reserve” Mindset

The recurring theme of Ponzi schemes and unlicensed businesses in Florida highlights an important conceptual distinction for crypto participants: the difference between holding a volatile asset like Bitcoin as a long‑term reserve and chasing yields through opaque intermediaries that simply reference Bitcoin. A Bitcoin reserve strategy, in its purest form, involves accumulating BTC, holding it in self‑custody or with a transparent qualified custodian, and accepting its price volatility in exchange for long‑term, censorship‑resistant value storage. By contrast, many of the schemes that have imploded in Florida and elsewhere promised to “smooth out” or “enhance” Bitcoin returns through proprietary trading, mining pools, or AI‑driven strategies without providing verifiable evidence of their operations.

HyperFund and the Haigler‑type Ponzi schemes show how dangerous this search for yield can be when combined with the psychological allure of “easy” crypto gains. For Florida residents—some of whom may have relocated to the state precisely to enjoy the fruits of successful crypto investments—these cases underscore the importance of skepticism toward any program that offers high, stable returns disconnected from transparent, market‑based risk. They also illustrate why Florida’s regulators have emphasized prudential requirements and licensing for entities that take custody of customer funds or issue money‑like tokens: by insisting on 100 percent reserves for payment stablecoins and clear MSB licensing for transmissions, the state is trying to build a perimeter between regulated finance and Ponzi‑style opportunism.

In practical terms, investors using Florida as a base should distinguish between three layers of risk: protocol‑level risk (for example, potential bugs in Bitcoin or Ethereum itself), intermediary risk (the solvency and honesty of exchanges, lenders, or stablecoin issuers), and regulatory risk (the possibility that an activity is deemed unlawful or that enforcement actions disrupt operations). Florida’s recent history shows that while protocol‑level risk is relatively low for blue‑chip chains, intermediary and regulatory risks are significant, especially where yields appear too good to be true. A conservative Bitcoin reserve approach that minimizes intermediary dependencies may align better with Florida’s combination of tax advantages and enforcement realities than more leveraged, yield‑seeking strategies.

Florida passes first US state-level stablecoin bill, SB 314, creating a regulatory framework for payment stablecoin issuers aligned with federal GENIUS Act standards and enhancing consumer protections

It's like Florida is already gaining its ground on crypto . They are giving an open hand to stablecoins issuers.

Florida’s AI and OpenAI Battles

Parallel to its crypto initiatives, Florida has thrust itself into the center of the national debate over artificial intelligence and platform responsibility. The state’s attorney general, James Uthmeier, has pursued both civil and criminal actions against OpenAI, the company behind ChatGPT, arguing that the firm misrepresented the safety of its AI systems and may bear responsibility for downstream harms ranging from self‑harm and child exploitation to a deadly campus shooting. These moves are being closely watched not only by AI developers but also by crypto and DeFi builders, because they hint at how U.S. courts and regulators might treat complex, algorithm‑driven systems that mediate financial decisions.

In a high‑profile civil action, Florida’s attorney general sued OpenAI and CEO Sam Altman, asserting consumer‑protection, product‑liability, and tort claims based on allegations that the company overstated its safety guardrails and failed to warn users about the risks of relying on ChatGPT. According to legal summaries, the complaint argues that ChatGPT is unreasonably dangerous because it can generate harmful content, give advice that encourages lawbreaking or self‑harm, and produce false or defamatory statements, all while being marketed as a reliable assistant. By invoking product‑liability theories traditionally applied to tangible goods, Florida is testing whether AI models can be treated as “products” with design defects, rather than mere speech tools protected by broad immunities.

The FSU Shooting and Criminal Investigation

The stakes rose further when Florida announced a criminal investigation into OpenAI and ChatGPT in connection with a shooting at Florida State University. In an official news release, Attorney General Uthmeier stated that the Office of Statewide Prosecution had launched a criminal probe after reviewing chat logs between ChatGPT and the gunman, Phoenix Ikner, who opened fire at FSU. The release emphasized that Florida prosecutors are examining whether OpenAI could bear criminal responsibility for ChatGPT’s role in the incident, and whether the platform’s interactions with the shooter amounted to aiding and abetting under Florida law.

A televised press conference elaborated on this theory. Uthmeier asserted that for months prosecutors had been investigating harms suffered by Floridians—including increases in self‑harm and suicides among children using ChatGPT—and instances where individuals used the platform to engage in criminal activity such as child pornography. He noted that under Florida law, anyone who intentionally “aids, abets, or otherwise assists” in the commission of a crime and that crime is committed can be treated as a principal in the first degree. By connecting this doctrine to ChatGPT’s outputs, Florida is exploring whether a generative AI system can ever satisfy the mental‑state and causation requirements for such liability.

The same press conference highlighted Florida’s broader campaign against AI‑facilitated child sexual abuse material. Uthmeier pointed to a case in which a predator received a 135‑year prison sentence for possessing CSAM, some of which was AI‑generated, and another defendant facing 100 criminal charges including dozens of counts related to AI‑generated CSAM. He also noted that in March 2026 he had joined Governor DeSantis for the signing of HB 1159, which increased the penalty for using AI to create child sexual abuse material to a second‑degree felony. These moves position Florida at the forefront of efforts to criminalize specific uses of generative AI and to treat synthetic imagery as legally equivalent to traditional exploitative content.

Implications for Crypto, DeFi, and AI‑Driven Trading

For crypto and DeFi builders, Florida’s AI offensive is more than a distant headline. It suggests a regulatory philosophy under which algorithm designers and platform operators can be held responsible for downstream misuse of their systems, especially when they make optimistic safety claims or fail to implement robust guardrails. Many trading tools, portfolio optimizers, and yield‑strategy engines in DeFi already rely on AI or machine‑learning components, whether for price prediction, risk scoring, or user‑behavior analysis. If courts accept Florida’s framing of generative AI as a “product” with design defects, similar arguments could be made about AI‑assisted trading systems that encourage excessive leverage, misallocate funds, or mislead users about risks.

Moreover, Florida’s willingness to investigate OpenAI criminally under “aiding and abetting” theories raises questions about how far liability could extend in financial contexts. Could a developer of an AI bot that suggests yield‑farming strategies be accused of aiding and abetting fraud if users are steered into Ponzi‑like protocols? Could a company offering AI‑powered tax optimization for Bitcoin reserves be held liable if users employ the tool to evade reporting obligations? These scenarios remain hypothetical, but Florida’s actions signal that at least one major state is prepared to test the outer boundaries of such liability.

At the same time, Florida officials have framed their AI actions in optimistic terms, suggesting that strong enforcement can steer AI toward beneficial uses. Newsroom coverage of the OpenAI probe emphasizes themes like harnessing AI as a “supportive gale, not a tempest of demise,” and insisting that “AI should advance mankind, not destroy it.” This rhetoric mirrors the way some Florida politicians talk about Bitcoin and stablecoins—as tools for financial empowerment that must be channeled correctly rather than suppressed. For innovators, the message is dual: Florida is open to AI and crypto experimentation, but it expects builders to internalize safety, transparency, and user protection from the outset.

DeSantis signals crypto-friendly business posture

DeSantis announces CBDC ban legislation

DeSantis launches presidential campaign with pro-Bitcoin Twitter Spaces

Florida Bitcoin reserve bills HB 487 and SB 550 introduced

Florida Bitcoin reserve bills indefinitely postponed and withdrawn

- 2026-02regulatory

Florida lawmakers renew Bitcoin reserve push with new bill

Florida passes SB 314, first US state stablecoin regulatory framework

Politics, Campaigns, and the Narrative War over Digital Finance

Florida’s regulatory and enforcement posture cannot be separated from its political identity. The state functions as both a proving ground and a megaphone for national conservative politics, with Donald Trump’s residence at Mar‑a‑Lago and Ron DeSantis’s governorship shaping how issues like CBDCs, Bitcoin, and AI are framed in partisan terms. This politicization has practical consequences for crypto: it influences which bills advance, which enforcement actions receive resources, and how the public interprets the legitimacy of federal versus state oversight.

The FBI’s 2022 search of Mar‑a‑Lago for classified documents turned a Palm Beach property into a symbol of conflict between Trump and the Department of Justice, catalyzing narratives of a “grand conspiracy” against the former president among his supporters. For many in Florida’s conservative base, this episode reinforced distrust of federal institutions, including agencies that would likely administer any U.S. CBDC or oversee national stablecoin rules. DeSantis has tapped into this sentiment by styling himself as a bulwark against federal overreach in finance, casting CBDCs as instruments of surveillance and censorship while championing private digital assets as tools of self‑determination.

Campaigns Funded by Bitcoin and Crypto Narratives

Within this political environment, crypto has become both a fundraising mechanism and a cultural signal. DeSantis’s move to accept crypto donations during his national political campaigns sent a clear message that digital‑asset holders were part of his envisioned coalition, while also creating practical challenges around compliance and disclosures. Elsewhere in the state, congressional candidates have reportedly liquidated substantial Bitcoin holdings—on the order of hundreds of thousands of dollars—to bankroll their bids, illustrating how Bitcoin reserves accumulated during earlier bull markets are now being redeployed as political capital. For a crypto audience, Florida offers a live demonstration of Bitcoin’s evolution from speculative asset to war chest for real‑world endeavors.

Trump, for his part, has used his influence over Florida’s Republican apparatus to endorse candidates in state legislative races, from House District 87 to 94, often praising them as “America First patriots” advancing his agenda. These endorsements occur in a media environment where issues like CBDCs, stablecoins, and AI regulation are increasingly presented as proxies for deeper questions about sovereignty and the administrative state. It is not difficult to imagine a near‑future Florida race in which a candidate’s stance on state‑licensed stablecoins, Bitcoin treasury reserves, or the OpenAI lawsuit becomes a litmus test for ideological alignment.

Judicial Appointments and Long‑Term Regulatory Trajectories

Another lever of influence lies in judicial appointments. Newsroom coverage has highlighted Trump’s nomination of a young conservative judge, Kuntz, to a federal bench in Florida, raising questions about how decades‑long tenures might shape the interpretation of statutes touching on crypto, AI, and digital privacy. Federal courts in Florida will almost certainly hear cases involving the state’s stablecoin law, OpenAI litigation, and future disputes over Bitcoin custodians or DeFi platforms. The ideological leanings and interpretive philosophies of these judges—textualist, formalist, or otherwise—will profoundly affect how far state regulators can go in stretching traditional legal doctrines to address novel technologies.

For example, whether Florida can successfully apply product‑liability theories to AI systems, or treat stablecoin issuers like quasi‑banks under state law, may hinge on how federal judges balance innovation with civil‑liberties concerns. The intersection of state‑level CBDC bans and federal constitutional supremacy could likewise be litigated in Florida courts. Crypto participants considering Florida as a domicile for their projects must therefore think not only about statutes and regulations, but also about the judiciary that will interpret them over the coming decades.

Beyond Finance: Environment, Tourism, and Soft Power

Florida’s regulatory experiments do not stop at money and machines. The state’s decisions on environmental and cultural issues also shed light on its broader approach to balancing economic interests, global obligations, and public sentiment. A recent example comes from an unexpected corner: the conservation of giant manta rays.

In May 2026, the Florida Fish and Wildlife Conservation Commission (FWC) voted to adopt new rules governing the capture of giant manta rays, following criticism that the existing permitting framework was “broken.” Effective July 1, 2026, the revised rules ban international exports of giant manta rays for exhibition, meaning Florida will no longer permit the shipment of these or any federally threatened or endangered marine species captured for exhibition to facilities outside the United States. The commission cited new obligations under the Convention on International Trade in Endangered Species (CITES) as making such exports nearly impossible in any case.

At the same time, capture limits were dramatically reduced. Where up to three manta rays could previously be taken per year under a special permit, the new rules allow just one every two years, and future permits must be presented to the full commission for a public hearing and case‑by‑case approval rather than being rubber‑stamped administratively. Conservation advocates welcomed these changes as a meaningful shift, but noted that Florida remains the only state in the country that permits the capture of giant manta rays at all, and that the hoped‑for complete ban did not materialize. The result is a compromise between preserving research and education opportunities and tightening protections for a vulnerable species.

This pattern—incremental tightening without outright prohibition—parallels Florida’s approach to stablecoins and AI. Rather than banning private digital currencies or generative AI systems, the state has chosen to regulate them aggressively, setting boundaries (such as 100 percent reserve requirements or criminal penalties for AI‑generated CSAM) while allowing economic and technological activity to continue. In both arenas, Florida positions itself as a steward rather than a simple enforcer, seeking to shape how innovation unfolds without relinquishing the perceived benefits of being a hub for research, tourism, and commerce.

Golf, Conferences, and the Networking Layer of Crypto in Florida

Florida’s soft power in the crypto and AI world also flows through its social and cultural infrastructure. High‑end golf clubs, resort towns, and conference venues serve as informal networking hubs where founders, investors, and policymakers meet. A small but telling example is the Seminole Pro‑Member event in Florida, where Rory McIlroy and his father reportedly fired a blistering 63 to win the Pro‑Member tournament, joined by professional Shane Lowry in what was described as a gratifying team victory. Events like these attract wealthy attendees, including many with exposure to Bitcoin, crypto funds, or AI ventures, and provide fertile ground for deal‑making and narrative‑shaping.

Parallel to the golf circuit, Florida hosts recurring conferences devoted to reimagining finance and AI’s future. Promotional materials for such events speak of a “triumphant return” to the Sunshine State to “reprogram” finance and AI’s horizon, emphasizing Florida’s role as both a literal and symbolic launching point for new technological cycles. For crypto communities, the state’s beaches, favorable weather, and hospitality infrastructure make it an appealing location for hackathons, DAO meetups, and cross‑disciplinary gatherings focused on Bitcoin, stablecoins, and AI agents.

These soft‑power dynamics matter because they influence where talent clusters and how narratives about Bitcoin reserves, DeFi, and AI‑aligned regulation are formed. Founders who attend a Florida conference or golf outing may leave with a sense that Florida is not only a tax haven but a cultural home for their projects. That, in turn, shapes where companies incorporate, where they litigate disputes, and where they lobby for favorable treatment. For a crypto news audience, it is important to see Florida not just as a set of statutes, but as an ecosystem where laws, culture, and capital intersect.

Florida lawmakers renew push to launch State Bitcoin Reserve. On Tuesday, Florida lawmakers introduced another bill for the creation of a strategic Bitcoin reserve, less than a year after two attempts were shelved.

Let them keep trying harder 💪🏾

Florida has passed the first state stablecoin law (SB 314) aligned with the federal GENIUS Act, but Bitcoin reserve legislation failed twice, reflecting inconsistent follow-through on crypto-friendly rhetoric.

- MarketHigh

Florida-linked memecoin promotions tied to high-profile figures under criminal scrutiny (Andrew Tate inquiry) and the $PATRIOT token stunt illustrate elevated retail manipulation risk in the state's crypto ecosystem.

State-run Bitcoin reserve proposals would have concentrated sovereign crypto holdings under a single state treasury without clear custody or governance standards.

CFTC secured a $1.3M penalty and trading ban against a Florida resident in a commodity pool fraud case, and a $328M Ponzi scheme drew federal charges, indicating active enforcement exposure.

- LiquidityLow

No evidence of systemic DeFi liquidity crises specific to Florida-domiciled protocols; risk is concentrated in retail fraud schemes rather than protocol-level liquidity failure.

Practical Takeaways for Crypto and AI Participants in Florida

For builders, investors, and policymakers looking at Florida from the outside, the picture that emerges is complex. The state is simultaneously a haven for low‑tax Bitcoin reserve strategies, a pioneer in state‑level stablecoin regulation, a pugnacious antagonist of CBDCs and certain forms of AI, and a hot zone for Ponzi‑like schemes and aggressive enforcement. To make sense of this landscape, it helps to distill the key policy pillars and their practical implications.

One way to conceptualize Florida’s stance is to view it across four core domains: taxation, financial innovation, enforcement, and AI regulation. In taxation, Florida offers structural advantages by eliminating state income taxes on crypto gains, but this does not obviate federal obligations. In financial innovation, the fintech sandbox and upcoming stablecoin framework signal openness to experimentation, provided firms are willing to accept licensing and prudential oversight. In enforcement, the HyperFund case and other Ponzi prosecutions demonstrate a low tolerance for fraud, particularly where vulnerable populations are targeted. In AI, the OpenAI lawsuits and HB 1159 show a willingness to impose both civil and criminal liability for perceived safety failures and harmful content.

The table below summarizes these themes.

| Domain | Florida’s stance | Practical implications for crypto/AI actors |

|---|---|---|

| Taxation | No state income tax; crypto gains not taxed at state level; federal taxes still apply. | Attractive for Bitcoin reserve strategies; still need robust federal tax compliance. |

| Financial innovation | Fintech sandbox; pilot for paying state fees in crypto; state‑level stablecoin framework. | Encourages experimentation but ties stablecoins and MSBs into stringent licensing. |

| Enforcement | High‑profile prosecutions of HyperFund promoter and Ponzi operators; cooperation with DOJ/CFTC. | Fraud and unlicensed money transmission aggressively targeted; due diligence essential. |

| AI regulation | Civil and criminal actions against OpenAI; enhanced penalties for AI‑generated CSAM. | Signals potential liability for AI‑driven financial tools and content moderation duties. |

From this matrix, several practical lessons follow. First, for crypto companies considering Florida as a base, the state’s advantages are most pronounced for non‑custodial, software‑centric models that can leverage the sandbox and tax environment without triggering intensive MSB or stablecoin issuer obligations. A developer of non‑custodial Bitcoin wallets or decentralized protocols that never take possession of user funds may benefit substantially from Florida domicile, provided federal securities and commodities laws are respected. Conversely, an aspiring stablecoin issuer or centralized exchange should assume that Florida will require full licensing, 1:1 reserves, and regulatory reporting, and should budget accordingly.

Second, for individuals and funds employing a Bitcoin reserve strategy, Florida is attractive but demands discipline. Holding BTC for the long term with periodic, well‑planned realizations can align well with the absence of state income taxes. However, chasing yield through opaque lending programs or offshore platforms lacking clear licensure can expose investors to both loss and potential entanglement in enforcement actions, especially if they recruit others into such schemes. The HyperFund case illustrates how even promoters who may not see themselves as orchestrators can be swept into charges of unlicensed money transmission.

Third, for AI‑driven crypto tools—such as bots that recommend trading strategies, AI tax assistants, or generative‑AI interfaces to DeFi protocols—Florida’s actions against OpenAI should be read as an early signal. Builders should document and implement safety measures, provide clear risk disclosures, and avoid overstating the reliability or “intelligence” of their systems. They should also monitor developments in the OpenAI litigation to understand how Florida courts interpret product‑liability, negligence, and aiding‑and‑abetting claims in the context of AI outputs. What happens in those cases could inform best practices for AI‑enhanced financial products nationwide.

Finally, for policymakers, Florida offers both inspiration and caution. Its stablecoin framework illustrates how a state can harmonize with federal initiatives like the GENIUS Act to provide clarity for issuers and users. Its CBDC opposition raises questions about the balance between state and federal authority over money. Its aggressive AI enforcement highlights the challenge of holding global technology companies accountable for localized harms. States following in Florida’s footsteps will need to decide which aspects of this model to emulate and which to temper.

Conclusion

Florida occupies a unique and increasingly central place in the evolving story of crypto, stablecoins, Bitcoin reserves, and AI regulation. On the one hand, it offers tangible advantages to digital‑asset holders and builders: a tax environment that favors long‑term Bitcoin accumulation, a fintech sandbox that signals openness to innovation, and a pioneering stablecoin framework that promises legal clarity for dollar‑pegged tokens aligned with federal standards. On the other hand, it has become the site of severe enforcement actions against Ponzi‑style schemes like HyperFund, the nation’s most assertive state‑level legal campaign against OpenAI, and a political theater in which CBDCs and AI are cast as potential instruments of surveillance and control.

This duality is not accidental. Florida’s leaders seek to position the state as both a laboratory and a bulwark—a place where new forms of money and intelligence can flourish, but only within boundaries that reflect local values of individual autonomy, skepticism of federal power, and concern for vulnerable populations. The state’s manta ray regulations, its golf and conference culture, and its targeted AI and CSAM statutes all point to a regulatory style that prefers incremental tightening and visible moral framing over technocratic neutrality. For crypto and AI innovators, this means that operating in Florida requires both technical excellence and narrative fluency: projects must not only comply with formal rules but also fit within the stories Florida tells about freedom, responsibility, and progress.

Looking ahead, Florida’s decisions will reverberate far beyond its borders. Its stablecoin law will test how well state and federal frameworks can coordinate around GENIUS‑style regimes; its CBDC stance may shape national debates about the proper role of central banks in digital money; its OpenAI litigation could influence how courts see algorithmic systems across domains, including finance. In each case, Florida is forcing hard questions about who controls digital infrastructure, who bears responsibility when it fails, and how much trust citizens should place in both markets and the state. For a crypto news audience, watching Florida is less about tracking a single jurisdiction and more about observing a microcosm of the global struggle over the future of money and intelligence.

Outlook

Florida is likely to remain a high‑variance environment for crypto, stablecoins, and AI over the coming years. As the state‑level stablecoin framework comes into force, issuers will either rise to the challenge of full‑reserve, highly supervised operations or decamp to friendlier jurisdictions, providing a real‑world test of whether rigorous regulation and innovation can coexist. The outcome of the OpenAI civil and criminal proceedings will either validate Florida’s expansive theories of AI liability or prompt legislative recalibration, with knock‑on effects for AI‑driven trading, compliance, and consumer‑facing tools. Politically, the state’s role as a Republican stronghold and Trumpian power center ensures that CBDCs, Bitcoin reserves, and AI narratives will continue to be weaponized in national debates, influencing federal policymaking and electoral strategies.

For now, crypto and AI participants should treat Florida neither as a simple paradise nor as a minefield, but as a sophisticated, evolving ecosystem. Those who understand its tax advantages, regulatory expectations, enforcement history, and political narratives will be best positioned to harness its opportunities while avoiding its hazards. As finance and intelligence become increasingly programmable, Florida’s experiment will help determine whether decentralized technologies can truly thrive within—and sometimes against—the structures of a modern U.S. state.

Latest Florida news

CFTC secures $1.3M penalty and trading ban against Florida resident in commodity pool fraud case, reinforcing crackdown on market abuseFlorida passes first US state-level stablecoin bill, SB 314, creating a regulatory framework for payment stablecoin issuers aligned with federal GENIUS Act standards and enhancing consumer protectionsFlorida lawmakers renew push to launch State Bitcoin Reserve. On Tuesday, Florida lawmakers introduced another bill for the creation of a strategic Bitcoin reserve, less than a year after two attempts were shelved.Why Not!

Crypto investors behind the $PATRIOT memecoin fund a 15-foot golden “Don Colossus” statue of President Trump, awaiting installation at his Doral golf resort in Florida.Florida bill proposes creating a state-run strategic crypto reserve that would primarily hold Bitcoin, potentially making it a formal part of Florida’s financial assets by mid-2026. Florida moves to scrap capital gains tax on Bitcoin, XRP, and stocks, aiming to boost crypto investment.

Florida moves to scrap capital gains tax on Bitcoin, XRP, and stocks, aiming to boost crypto investment.Sources

- https://wifpr.wharton.upenn.edu/50-state-review-of-cryptocurrency-and-blockchain-regulation/

- https://www.politico.com/newsletters/florida-playbook/2023/08/25/desantis-00112944

- https://x.com/DecryptMedia/status/2067278219074531715

- https://www.flsenate.gov/Session/Bill/2026/314/Analyses/2026s00314.pre.aeg.PDF

- https://www.flsenate.gov/Session/Bill/2026/175/Analyses/h0175z.IBS.PDF

- https://www.jdsupra.com/legalnews/florida-ag-sues-openai-over-chatgpt-7607108/

- https://www.myfloridalegal.com/newsrelease/attorney-general-james-uthmeier-launches-criminal-investigation-openai-chatgpt

- https://www.youtube.com/watch?v=7JO9utWlcaA

- https://www.justice.gov/criminal/case/hyperfund-and-associated-cases

- https://www.flsenate.gov/Session/Bill/2026/314

- https://www.flgov.com/eog/news/press/2023/governor-ron-desantis-announces-legislation-protect-floridians-federally-controlled

- https://www.sidley.com/en/insights/newsupdates/2025/07/the-genius-act-a-framework-for-us-stablecoin-issuance

- https://www.facebook.com/UnitedStatesSecretServiceOfficial/posts/brian-shane-haigler-spent-seven-years-building-a-criminal-network-the-secret-ser/1242379078068068/

- https://www.worldanimalprotection.us/latest/blogs/manta-ray-capture-florida/

- https://www.facebook.com/rockbottomgolf/posts/rory-and-his-dad-win-the-seminole-memberguest-/1393918066108533/

- https://coinledger.io/blog/crypto-friendly-states

- https://fortune.com/2021/12/09/florida-governor-ron-desantis-businesses-fees-crypto/

- https://en.wikipedia.org/wiki/FBI_search_of_Mar-a-Lago

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…