In‑depth explainer on initial coin offerings (ICOs): what they are, how they work, history from Ethereum’s 2014 sale to today’s post‑hype market, legal risks, ICO vs IEO/IDO, onchain fundamentals, recent case studies and the outlook for future token launches.

+30 sources across the wider coverage universe

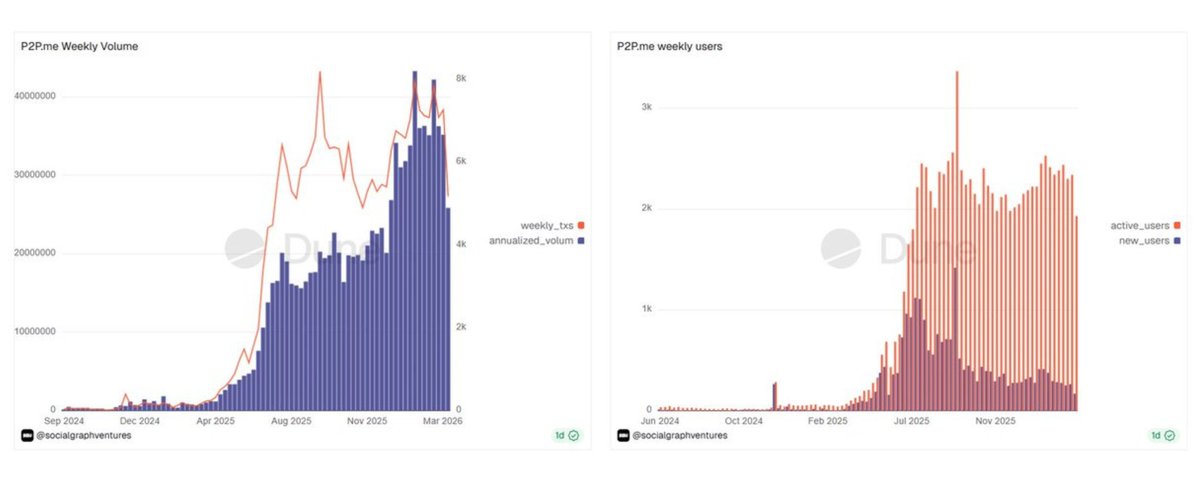

Social Graph breaks down onchain ICO fundamentals via P2P.me, highlighting retention, over 100% NRR cohorts, and zero-CAC growth as key signals for early-stage token underwriting2026-03

Social Graph breaks down onchain ICO fundamentals via P2P.me, highlighting retention, over 100% NRR cohorts, and zero-CAC growth as key signals for early-stage token underwriting2026-03 Tally shuts down after canceling its planned ICO, concluding that DAO governance tooling is not a viable venture-backed business in today’s crypto market despite facilitating over $1B in payments and securing $80B in on-chain value.2026-03

Tally shuts down after canceling its planned ICO, concluding that DAO governance tooling is not a viable venture-backed business in today’s crypto market despite facilitating over $1B in payments and securing $80B in on-chain value.2026-03 Mike Dudas alleges Trove ran an ICO scam by keeping 9.4 million dollars raised under false pretenses while the token’s value collapsed from a 20 million to about 1.4 million dollar FDV within minutes, calling for anyone who takes money from the project to be publicly shamed and outed.2026-01

Mike Dudas alleges Trove ran an ICO scam by keeping 9.4 million dollars raised under false pretenses while the token’s value collapsed from a 20 million to about 1.4 million dollar FDV within minutes, calling for anyone who takes money from the project to be publicly shamed and outed.2026-01 Hyperliquid’s HIP-6 adapts Uniswap-style continuous clearing auctions to a CLOB, fixing ICO pricing games and thin order books.2026-02

Hyperliquid’s HIP-6 adapts Uniswap-style continuous clearing auctions to a CLOB, fixing ICO pricing games and thin order books.2026-02 Miles Deutscher shared his 2026 crypto outlook, predicting stronger institutional dominance, 50%+ stablecoin supply growth, AI and RWA resurgence, an ICO renaissance, and Bitcoin ending the year higher, with real revenue-generating protocols outperforming pure speculation.2026-01

Miles Deutscher shared his 2026 crypto outlook, predicting stronger institutional dominance, 50%+ stablecoin supply growth, AI and RWA resurgence, an ICO renaissance, and Bitcoin ending the year higher, with real revenue-generating protocols outperforming pure speculation.2026-01 Cap ICO Registrations Opened2026-02

Cap ICO Registrations Opened2026-02

Initial Coin Offerings (ICOs): A Complete Guide for the Post‑Hype Era

An initial coin offering (ICO) is a way for a crypto project to raise capital by selling newly issued digital tokens, usually in exchange for ETH, BTC or stablecoins, often before the underlying network or product is fully live. In practice, ICOs sit somewhere between crowdfunding and early‑stage venture funding, but with onchain tokens instead of shares, global distribution instead of local cap tables, and a long history of both transformative innovation and speculative PUMP cycles.

What Is An ICO?

At its core, an ICO is a fundraising event in which a project issues a blockchain‑based token to early supporters, typically through a smart contract that accepts established cryptoassets and automatically allocates the new tokens. The project usually publishes a white paper describing its vision, technology and token economics, then opens a sale window during which investors can contribute assets like ETH or USDC in exchange for the new token at a set or dynamically discovered price. Unlike an IPO, investors do not receive equity in a legal entity; instead, they receive tokens that may confer usage rights, governance votes, or claims over future cash flows, depending on the design. This basic mechanism is flexible enough to support payments tokens, governance tokens, onchain game assets and more, which explains why ICOs became a dominant launch model in early Ethereum culture.

A defining feature of ICOs is their global and permissionless character. As long as the sale contract is deployed on a public chain like Ethereum, anyone with compatible crypto and a wallet can usually participate, subject to any geographic or KYC restrictions the team imposes. This stands in contrast to traditional venture capital, where early rounds are limited to a small group of accredited investors and institutions. In an ICO, thousands of retail participants might contribute, creating a large, globally distributed community from day one; empirical work suggests that a typical ICO has around 4,700 contributors, indicating how broad these offerings can be compared with conventional seed rounds. That broad access has been both a strength—allowing ordinary users to get in early—and a weakness, because unsophisticated investors can be lured into opaque, high‑risk offerings they do not fully understand.

The rise of ICOs is tightly linked to Ethereum and the concept of programmable, onchain contracts. Ethereum’s ERC‑20 standard made it trivial to create new fungible tokens and to wire up a sale contract that automatically handled allocation and refunds, eliminating much of the operational friction that would have accompanied a global token sale on Bitcoin. Ethereum itself was launched via an ICO in 2014, raising roughly \$18.3 million worth of BTC by selling ETH at an average price of around \$0.31, and that event became the canonical template for subsequent token launches. The fact that some Ethereum ICO participants who invested only a few hundred dollars later saw positions worth millions—one address is reported to have turned \$245 into 790.17 ETH, now valued in the low seven figures—cemented the narrative that ICOs could be life‑changing asymmetrical bets if investors picked the right projects early.

Over time, the ICO label has stretched to cover a wide range of practices, from carefully structured, regulated token offerings on major exchanges to informal “fair launches” conducted directly from a meme‑coin minting platform. In the public markets, the term still broadly signals a primary token sale that precedes or coincides with a token’s initial listing and onchain liquidity. However, as the market has matured, many teams now prefer alternative branding such as “token generation event,” “public sale” or “community launch,” both to distance themselves from the more toxic episodes of 2017 and to reflect new technical designs that differ from classic ICOs. For investors, the important point is not the label, but the underlying mechanics, rights and risks attached to the token.

“Everything is a meme now,” says VD, comparing modern IPOs and AI stocks to ICO-era crypto as investors price stories, sentiment, and consensus over present-day fundamentals

$33M of first-day volume and $21.8M OI on Trade.xyz’s SpaceX pre-IPO perp makes this more than a vibes take. ICOs financialized roadmaps; Hyperliquid-style pre-IPO perps financialize cap tables before the equity exists in public markets, giving retail a 24/7 liquidation market for venture narratives. If Anthropic/OpenAI/SPCX-style listings all get perp curves before bankers price the book, crypto rails become the mempool for Wall Street consensus.

Readers click ICO content as a fraud-accountability beat first and a capital-formation innovation beat second — the top two stories pit a new platform promising to 'democratize' ICOs against founders literally spending raise proceeds on luxury real estate, revealing that audiences are stress-testing whether the 2026 ICO renaissance can structurally separate itself from the 2017 playbook.↗

A Short History: From Ethereum To The ICO Boom And Beyond

The first ICO is generally traced back to July 2013, when the Mastercoin project (later Omni) raised funds by selling a new token layered on top of Bitcoin. That experiment foreshadowed a key insight: you could use a base blockchain for secure settlement while issuing new assets that represented speculative claims on future protocol development. Yet it was Ethereum, launched via its own ICO in 2014, that provided the full toolkit—Turing‑complete smart contracts, fungible token standards and developer‑friendly tooling—that allowed token sales to proliferate. Ethereum’s successful sale validated the idea that an open‑source project could bootstrap a new smart‑contract network by selling its native asset to a global audience years before the network reached full production.

By 2017, ICOs had become the defining phenomenon of crypto’s first major bull run beyond Bitcoin. Thousands of projects launched token sales on Ethereum, collectively raising billions of dollars in a short span, often with little more than a white paper and a website. Academic and policy analyses from this period describe ICOs as a new form of blockchain‑based crowdfunding, offering firms a way to raise corporate capital directly from the public in exchange for digital tokens that might function as utilities, payment instruments, or claims on future assets. Many of these offerings were structured to emphasize “utility” and avoid explicit promises of profit sharing, reflecting the industry’s growing awareness that tokens might be treated as securities under existing law.

The boom had predictable consequences. On the positive side, ICOs democratized access to early‑stage projects, allowing global communities to fund infrastructure, DeFi protocols, and Web3 applications that might have struggled to secure traditional venture capital. Ethereum‑native categories like decentralized exchanges, lending protocols and onchain games trace their origins to teams that leveraged token sales to fund development and bootstrap usage. On the negative side, the low entry barriers and speculative mania attracted outright scams and poorly conceived projects, many of which disappeared after raising funds, leaving investors with illiquid or worthless tokens. Regulators in multiple jurisdictions, including the United States and the European Union, began issuing warnings and taking enforcement actions, reshaping the landscape.

The subsequent bear market, often described as the “post‑ICO winter,” saw a sharp drop in both the number and total value of ICOs. Empirical reviews show that after the peak years, aggregate ICO volumes fell significantly as investor sentiment cooled and enforcement risk rose. At the same time, the crypto ecosystem itself evolved. The rise of automated market makers, onchain liquidity mining and yield farming during the DeFi “summer” shifted attention from one‑off token sales to ongoing incentive programs, while new launch models such as initial exchange offerings (IEOs) and initial DEX offerings (IDOs) emerged as alternatives that promised better curation or capital efficiency. Even within Ethereum’s own ecosystem, some of the most successful later‑stage projects opted for “fair launches,” airdrops or slow‑roll token distributions rather than classic ICOs, in part to avoid regulatory overhang and in part to align more closely with community ethos.

By the mid‑2020s, the ICO market had entered what many commentators call a post‑hype, structurally smaller phase. Data from CryptoRank indicates that in Q2 2026, combined fundraising via ICOs, IEOs and IDOs totaled only about \$58 million, an 85% decline from the previous quarter and the lowest quarterly figure in five years. The number of public sales reportedly fell from 105 in Q1 to a much smaller figure in Q2, underscoring how selective both founders and investors have become about public launch events in an environment dominated by stablecoins, RWAs and institutionally backed protocols. Instead of hundreds of loosely vetted ICOs, the market features fewer but more scrutinized offerings, such as the Monad MON token sale on Coinbase, which is framed as a regulated public token sale open to users in over 80 countries, including the United States. This transition reflects broader shifts: regulatory pressure, investor fatigue with pure PUMP narratives, and a growing emphasis on real onchain fundamentals.

How ICOs Actually Work: Mechanics, Tokens And Smart Contracts

Although designs vary, most ICOs share a common lifecycle: design, disclosure, launch, distribution and listing. In the design phase, a team defines the token’s purpose, supply, allocation and vesting schedule. Tokens can represent access rights (for example, staking to use a service), governance votes over protocol decisions, or claims on protocol revenue, although many ICOs still emphasize “utility” to sidestep securities classifications. The team decides how many tokens will exist, what portion will be sold to the public, what portion will be reserved for the team and early investors, and over what timeline locked allocations will vest. Well‑designed tokenomics aim to balance near‑term liquidity with long‑term incentives, ensuring that insiders cannot dump immediately while community members have enough float to trade and participate meaningfully.

Disclosure revolves around the white paper or litepaper, which sets out the project’s technical architecture, roadmap, business model, token economics and governance. Early in the ICO era, white papers often blended technical detail with aspirational promises, sometimes without clear implementation plans or credible team backgrounds. As the market has matured, serious projects have moved toward more sober documentation, including risk disclosures, legal analyses, and onchain dashboards that allow prospective participants to evaluate usage metrics and protocol behavior even before the token launch. For sophisticated investors, a modern ICO pitch often includes not only a narrative about decentralization and utility, but also empirical evidence such as user retention, onchain revenue and cohort‑level net revenue retention, echoing the metrics used in traditional SaaS and fintech investing.

The launch phase is where smart contracts take center stage. On Ethereum, an ICO typically involves deploying an ERC‑20 token contract and a sale contract that receives funds and allocates tokens according to predefined rules. The contract might implement a fixed‑price sale, a capped raise, a bonding curve, or an auction mechanism such as a Dutch or continuous clearing auction. Participants send ETH or stablecoins to the contract during the sale window; after the sale concludes, they either claim their allocated tokens or receive a refund if caps were exceeded or thresholds not met. Mistakes in these contracts can be costly. A recent example involves a 2016 ICO whose smart contract contained a bug that locked up roughly \$2 million worth of ETH for nine years, until a whitehat developer crafted an exploit to rescue the funds and return them to their rightful owners. That episode illustrates both the power of immutable onchain code and the need for rigorous audits before inviting the public into a sale.

Distribution and listing mark the transition from primary issuance to secondary trading. Once tokens are distributed, the team or third parties typically provide initial liquidity on DEXs or arrange centralized exchange listings so that market participants can buy and sell the token freely. Liquidity provision and pricing strategy can vary widely. In some ICOs, the team seeds a DEX pool with a portion of raised funds and tokens, letting the AMM set prices; in others, the initial listing happens on a centralized exchange that acts as market maker. More recently, designs like Hyperliquid’s HIP‑6 proposal adapt ideas from AMM‑style liquidity to an order‑book environment by using continuous clearing auctions for permissionless token launches, aiming to improve price discovery and reduce the timing games and thin order books that plagued some earlier ICOs. The mechanics of this transition matter greatly for early investors, because poorly managed listings can result in extreme volatility and rapid PUMP‑and‑dump dynamics that erode trust and long‑term engagement.

Behind these mechanical steps lies a more subtle layer of incentive engineering. Because ICO tokens often trade immediately and can be used as collateral or yield‑bearing assets across DeFi, there is constant tension between short‑term speculation and long‑term protocol health. Projects must decide how aggressively to incentivize early liquidity and onchain activity with token emissions, knowing that excess rewards may attract mercenary capital but not sticky users. The fact that some Ethereum ICO wallets remained dormant for over a decade before moving—one “OG” participant reportedly invested \$12,000 in the Ethereum ICO, receiving 38,800 ETH now worth tens of millions of dollars, and only started selling in size years later—highlights how long the tail of ICO‑driven capital allocation can be. ICO design is therefore not just about the sale window; it is about shaping token supply, governance and incentives over the full lifecycle of a protocol.

- 01new ICO platform legitimacy↗

Delphi Labs hiring a CEO and Cobie launching Sonar signal institutional actors trying to rehabilitate the ICO model, which readers tracked as a credibility referendum on whether professional rails can fix retail-extraction dynamics.

- 02founder fund misuse receipts

Bankera luxury real estate, the Trove $9.4M false-pretenses allegation, and Edel Finance's 30% self-snipe hidden behind wallet mazes drew readers hunting accountability evidence — not general scam warnings but named perpetrators and documented wallets.

- 03ICO pricing mechanics reform↗

Hyperliquid's HIP-6 continuous clearing auction fix and Social Graph's P2P.me underwriting framework attracted readers interested in whether structural rule changes — not just trust — can prevent launch-day pricing games and thin order books.

- 04SEC enforcement outcomes↗

Quantstamp's $28.35M settlement and the Dragonchain case being dropped in the same news cycle gave readers a concrete before/after on regulatory risk, making enforcement resolution more clickable than enforcement initiation.

- 05Ethereum OG whale sell pressure↗

Multiple dormant 2014 ICO wallets moving tens of millions of ETH to exchanges created a recurring 'original sin' narrative where early capital formation directly becomes present-day price headwinds.

- 062026 mega-raise valuations↗

Monad at $2.5B FDV, megaETH raising toward $1B, and Pump.fun's planned $1B retail ICO at a $4B valuation gave readers a specific number-anchored argument about whether this cycle's raises are structurally different from 2017 or just larger.

ICOs, IEOs, IDOs And Other Launch Formats

As ICOs ran into legal and reputational headwinds, the industry experimented with new launch formats that preserve some benefits of token sales while addressing perceived shortcomings. Initial exchange offerings, or IEOs, move the sale onto a centralized exchange platform. In an IEO, the exchange vets the project, manages KYC/AML checks, hosts the sale, and often handles initial listing and market making after the sale ends. For projects, this can reduce operational overhead and lend credibility, since the exchange is staking its brand on the token. For investors, IEOs can provide a more streamlined user experience and some degree of gatekeeping, although due diligence standards still vary widely.

Initial DEX offerings, or IDOs, arose from the growth of DeFi and AMMs. Rather than working with a centralized exchange, the project lists its token directly on a DEX at or around the time of a public sale, often using liquidity pool mechanics to set the initial price and enable immediate trading. IDOs are typically more permissionless than IEOs and can be highly accessible for onchain‑native users, but they also suffer from the same front‑running, bot activity and short‑term PUMP dynamics that affect other DeFi markets. Many IDOs double as liquidity bootstrapping events, where the sale proceeds are used to seed long‑term liquidity pools, aligning the token’s tradability with its funding.

The relationship between ICOs, IEOs and IDOs is more evolutionary than binary. All three are forms of primary token distribution; the differences lie in who hosts the sale, how price discovery works and what safeguards exist around investor protection and compliance. Some projects run hybrid models, with a private token sale to institutions, an IDO for DeFi users and a subsequent IEO or listing on a centralized exchange for broader reach. Others adopt non‑sale models entirely, relying on airdrops to early users or “fair launches” where tokens are only earned through onchain participation rather than purchased. The memecoin ecosystem, especially on platforms like Pump.fun, has introduced yet another template: hyper‑fast, retail‑driven token launches with minimal documentation, tiny initial valuations and explicit embrace of speculative PUMP culture. These are not ICOs in the classic sense, but they compete for attention and liquidity in the same early‑stage token arena.

Recent developments suggest further innovation in launch mechanisms, especially around fair price discovery and anti‑bot protections. Hyperliquid’s HIP‑6 proposal, for instance, adapts Uniswap‑style continuous clearing auctions to a central limit order book, enabling permissionless token launches that clear orders at a single price over multiple blocks, reducing the advantage of being first in the mempool. This responds directly to issues seen in earlier ICOs and IDOs, where gas wars, sniping bots and thin order books made it hard for ordinary participants to get a fair allocation at a stable price. Other experiments include whitelisted allowlists with per‑wallet caps, quadratic allocations favoring smaller wallets, and sale structures that redirect unsold tokens to community treasuries rather than insider pools, as seen in the Monad MON sale where any remaining tokens from the \(7.5\%\) public allocation are slated for ecosystem development. For investors evaluating a token launch today, understanding these mechanics is at least as important as understanding the headline valuation.

Legal And Regulatory Considerations

From a legal perspective, the central question around ICOs is whether a given token sale amounts to an offering of securities. In the United States, this analysis typically turns on the Howey test, which asks whether there is an investment of money in a common enterprise with a reasonable expectation of profits to be derived from the efforts of others. The U.S. Securities and Exchange Commission has issued guidance framing many ICOs as investment contracts under this test, especially where tokens were sold prior to network launch with heavy marketing of potential price appreciation and little immediate utility. The SEC’s 2019 framework for digital asset analysis lists numerous factors that point toward a token being a security, including centralization of development, reliance on managerial efforts, and a primary focus on secondary market trading.

In Europe, ICO regulation has historically been fragmented across member states, with some jurisdictions treating certain tokens as financial instruments and others applying lighter‑touch regimes more akin to crowdfunding. A 2021 briefing paper for the European Parliament described ICOs as a novel way to raise corporate capital but highlighted significant risks around fraud, market manipulation and consumer protection. Since then, the EU’s Markets in Crypto‑Assets (MiCA) regulation has moved toward a more unified framework for cryptoasset issuance and service providers, although implementation details and their impact on token launches are still evolving. Other jurisdictions, including Switzerland, Singapore and certain offshore hubs, have issued guidance classifying tokens into payment, utility and asset (or security) categories, each with distinct regulatory expectations.

One practical consequence of this patchwork is an increasing preference for “regulated ICOs” or exchange‑hosted sales that explicitly comply with securities or crowdfunding laws in at least one major jurisdiction. The Monad MON token sale on Coinbase illustrates this trend: it is framed as the first regulated public token sale hosted by the exchange since 2018, open in over 80 countries including the U.S., with structured disclosures and allocation rules. For teams, working through a regulated platform may reduce enforcement risk but also imposes constraints on token design, marketing language, and target markets. For investors, participation in such sales may involve KYC/AML checks and geographic restrictions, but the trade‑off is potentially higher standards of due diligence and recourse.

Despite these shifts, unregulated or lightly regulated ICOs persist, especially in more permissive jurisdictions and among smaller, purely onchain projects. Enforcement actions have tended to focus on high‑profile or egregious cases, creating what critics describe as a regime of “regulation by enforcement,” where many projects operate in legal gray zones until they attract sufficient scale or public attention. This has implications for both founders and investors. Teams may structure tokens with minimal explicit profit promises and emphasize decentralized governance, hoping to stay on the right side of the Howey test, but substance matters more than form. Investors, meanwhile, need to recognize that many ICO tokens come with no legal claim on revenues or assets, and that disclosure standards can fall far short of what is expected in public equity markets.

Another emerging issue is the intersection of ICOs with broader policy debates around stablecoins, money laundering and consumer protection. As regulators scrutinize major stablecoin issuers and payments firms re‑enter the crypto conversation, policymakers are re‑evaluating the boundaries between speculative investment and payment infrastructure. In a market increasingly dominated by stablecoins and tokenized RWAs, the case for utility‑only tokens that are primarily used for speculation may face tougher questions. Projects that raise via ICOs while also touching regulated sectors such as lending, derivatives or tokenized securities must navigate overlapping regimes, further increasing the importance of competent legal advice and transparent communication.

Ethereum ICO raises ~$18M at $0.31/ETH

- 2017-10launch

Dragonchain raises $20M in ICO

Quantstamp conducts unregistered token sale

Quantstamp settles with SEC for $28.35M

Ethereum ICO whale offloads $47M ETH, contributing to 10% price drop

- 2026-04regulatory

SEC drops case against Dragonchain after years of litigation

Cobie's Sonar ICO platform launches with Plasma's $50M raise at $500M valuation

- 2026-07launch

Pump.fun announces $1B retail ICO at $4B valuation on July 12

Investor Perspective: Risks, Rewards And PUMP Dynamics

For investors, ICOs sit at the far end of the risk spectrum. On the upside, they offer access to early‑stage tokens at valuations that can look trivial if the protocol later becomes core infrastructure, as Ethereum’s ICO famously demonstrated. Stories of ICO participants turning a few hundred dollars into seven‑figure positions after a decade of holding—such as the wallet that invested \$245 in 2014 and later moved 790.17 ETH worth roughly \$1.79 million, a reported \(7,303\times\) return—continue to captivate crypto audiences and sustain the allure of “getting in early.” On the downside, most ICOs do not become the next Ethereum, and a large share of tokens never recover their ICO price once secondary trading begins, especially if insiders sell aggressively or the product fails to gain traction.

One structural risk is information asymmetry. Project teams typically know far more about their own roadmap, technical debt and governance plans than public participants. White papers and pitch decks can be selectively optimistic, and onchain data may be sparse if the ICO precedes mainnet launch. Even when projects share detailed roadmaps, execution risk remains high, particularly for ambitious layer‑one or DeFi protocols that must compete for developers, liquidity and users in a crowded landscape. The ICO format amplifies this asymmetry because tokens often trade shortly after launch, allowing insiders with superior information to exit into retail demand during the initial PUMP, sometimes before meaningful fundamentals exist.

Scams and misrepresentations are another concern. During the 2017–2018 boom, numerous ICOs raised funds on false or exaggerated claims, disappeared without delivering a product, or diverted proceeds to insiders rather than development. Contemporary controversies echo this pattern in more sophisticated form. Allegations around certain ICO‑style raises include accusations that teams kept the vast majority of funds while the token’s fully diluted valuation collapsed in minutes, or that insiders used complex wallet routing and liquidity position strategies to conceal large allocations and dump on retail buyers. Even when such cases do not rise to the level of outright fraud, they highlight the need for careful scrutiny of token distribution, lockups and onchain behavior.

Technical and operational risks also loom large. Poorly written smart contracts can lock or misallocate funds, as seen in the 2016 ICO contract where about \$2 million in ETH remained inaccessible for nine years until a whitehat exploit rescued it. Projects that attempt complex pre‑deposit or bonding mechanisms can run into issues with bots, gas spikes and user experience, as illustrated by MegaETH’s attempt to run a large‑scale pre‑deposit campaign that reportedly suffered from technical failures, unintended deposits and operational chaos, culminating in the cancellation of a planned \$1 billion raise. Such failures do not just hurt investors in the specific sale; they can sour sentiment toward the entire category, contributing to broader declines in ICO fundraising volumes.

Market structure adds further layers of risk. ICO tokens often launch into highly speculative environments where leverage, derivatives and PUMP‑driven narratives amplify volatility. The emergence of memecoin launchpads like Pump.fun and onchain casinos of leverage has trained a new generation of traders to chase ultra‑short‑term pumps rather than multi‑year fundamentals. In this context, ICO tokens can become targets for pump‑and‑dump schemes, insider “sniping” and coordinated shilling campaigns, regardless of their underlying quality. Traders may pile into a pre‑launch perpetual or onchain IOU token, as in the case of highly anticipated launches branded as “the biggest ICO ever,” only to see post‑launch reality fail to match pre‑launch hype.

Despite these risks, ICOs continue to attract investors who specialize in early‑stage, high‑volatility opportunities and who believe they can distinguish signal from noise. The more sophisticated among them emphasize rigorous due diligence: assessing the team’s track record, evaluating the technical architecture, modeling token flows, and increasingly, analyzing onchain metrics from testnets, early beta products or adjacent ecosystems. Some funds use Dune dashboards and other analytics tools to study DAU/MAU ratios, cohort retention, protocol revenue and net revenue retention before committing to a sale, treating the ICO as a growth‑stage funding round rather than a pure speculative bet. For retail investors, learning from this playbook—while keeping position sizes modest relative to portfolio—may be the most realistic path to engaging with ICOs without being dominated by PUMP narratives.

Onchain Fundamentals And The Shift Beyond Hype

A striking difference between the peak ICO era and today’s market is the role of onchain data in underwriting early‑stage tokens. In 2017, many ICOs launched before there was any product to use; today, a growing share of serious projects aim to build live, onchain products first, then use a token sale to decentralize ownership and fund scaling. This shift allows investors to review real usage metrics: transaction counts, active addresses, protocol revenue, and behavioral cohort analyses that mirror Web2 analytics. For example, Social Graph’s analysis of P2P.org’s onchain ICO fundamentals highlighted retention curves, over 100% net revenue retention in certain cohorts, and organic user growth with effectively zero customer acquisition cost, framing the token sale as a way to share in an already functioning onchain business rather than a speculative bet on a hypothetical product.

The availability of such metrics enables a more nuanced conversation about value creation. Instead of asking only whether a token will PUMP after launch, investors can ask what drives sustainable demand for the token’s utility and governance rights. Does the protocol generate fees, and if so, are they denominated in ETH, stablecoins or the native token? Are there mechanisms, such as buy‑and‑burn or fee distribution, that tie token value to protocol performance, or is the token primarily a coordination and voting device? How concentrated is usage—do a handful of whales generate most of the volume, or is there a broad base of sticky users? Onchain analytics platforms make it increasingly possible to answer these questions empirically, even before a token exists, by studying smart contract interactions related to the underlying product.

This focus on fundamentals aligns with a broader market narrative about moving from hype to utility. Commentators have described the current phase of crypto as a “post‑hype” era in which speculative fervor coexists with growing regulatory scrutiny, stablecoin adoption and real‑world asset tokenization. In such an environment, ICOs that cannot demonstrate credible, onchain traction may struggle to attract serious capital, even if they can still excite segments of retail traders. At the same time, protocols that can point to billions in secured value, hundreds of millions in processed payments or sustained onchain cash flows can use ICO‑style launches to transition gradually from VC‑heavy cap tables to broader community ownership, as long as their token economics align incentives for both groups.

The rise of onchain data also has governance implications. Tokenholders can now monitor whether teams respect vesting schedules, how treasuries are managed, and whether governance proposals align with earlier promises. For example, Tally, a governance platform that facilitated over \$1 billion in payments and secured around \$80 billion in onchain value, ultimately decided to wind down after scrapping its planned ICO, concluding that the market for DAO tooling could not sustain a venture‑backed business in the current climate. That decision, made transparent via public communications, shows that not every protocol with strong onchain metrics will ultimately choose to launch a token; conversely, it underscores that token issuance is just one tool among many in the crypto entrepreneur’s kit.

For investors, the integration of onchain analytics into ICO due diligence is both an opportunity and a challenge. On the one hand, it reduces reliance on marketing and narratives by allowing independent verification of usage, liquidity and risk. On the other hand, it raises the technical bar for effective analysis, privileging those who can write queries, interpret complex dashboards and distinguish between genuine organic activity and wash trading or sybil farming. As a result, the ICO landscape is increasingly bifurcated between speculative retail flows drawn to simple PUMP narratives and more systematic capital that treats ICOs as one input into a broader, data‑driven investment process.

The SEC's active enforcement posture — Quantstamp settled for $28.35M and Dragonchain only escaped after years of litigation — signals that token sales without registered securities status remain high-exposure even years after the raise.

- Fraud / Founder MisconductHigh

Documented cases of ICO proceeds diverted to luxury real estate (Bankera), funds held under false pretenses collapsing token FDV from $20M to $1.4M in minutes (Trove), and self-sniping 30% of supply hidden across wallet mazes (Edel) demonstrate that fund misuse risk is structural, not anecdotal.

ICO launch mechanics create predictable extraction windows: bots front-run predeposit campaigns (megaETH), insiders snipe allocations before public clearing, and thin post-launch order books let small sells collapse FDV — Hyperliquid's HIP-6 is a direct market response to these failure modes.

Large-cap raises at multi-billion FDVs (Monad $2.5B, Pump.fun $4B) concentrate float at launch, making post-ICO liquidity shallow relative to implied valuation and amplifying the impact of early-investor unlocks.

- Smart ContractLow

Legacy ICO contracts from 2016 can trap funds for nearly a decade with no recovery path, as illustrated by a developer needing a whitehat exploit to rescue $2M locked for nine years; modern raises on audited infrastructure have materially lower contract risk.

Q2 2026 ranked as the worst ICO quarter on record by CryptoRank, and Tally's shutdown after canceling its ICO — despite facilitating $1B in payments — shows that product-market fit does not guarantee a viable token raise even in a declared renaissance.

Case Studies: Ethereum, Stuck Funds, MegaETH, Monad And Governance ICOs

Ethereum’s ICO remains the canonical success story. Conducted in 2014, the sale offered ETH at roughly \$0.31, raising about \$18.3 million worth of BTC to fund development of the then‑unbuilt smart‑contract platform. At the time, many considered the valuation high relative to Bitcoin’s more proven use case, and regulatory frameworks for such offerings were less formed than today. Nevertheless, the Ethereum Foundation deployed the funds to build a general‑purpose blockchain that became the backbone of DeFi, NFTs and most subsequent ICOs themselves. The fact that some early participants left their ICO allocations untouched for a decade—only recently moving or selling portions worth tens of millions of dollars—illustrates both the magnitude of the upside and the cultural norm of long‑term holding among certain OGs.

The 2016 ICO contract bug that locked up around \$2 million in ETH offers a cautionary counterpoint. Deployed on Ethereum’s early mainnet, the sale contract contained flawed logic that prevented contributors from withdrawing or transferring their tokens, effectively trapping user funds for nine years. Only in 2024 did a whitehat developer identify a way to exploit the bug to move the funds into a safe account under community oversight, subsequently returning 19.329 ETH to original contributors from both the 2016 sale and a separate 2018 ICO that had suffered similar issues. This saga underscores the permanence of smart contract bugs and the ethical complexity of “whitehat exploits” used to rescue funds—but from an ICO perspective, it highlights how critical contract audits and minimal‑complexity designs are when dealing with immutable onchain fundraising.

MegaETH’s attempted pre‑deposit campaign represents a more contemporary lesson in scale and operational risk. The project aimed to raise up to \$1 billion via a pre‑deposit mechanism, inviting users to send funds ahead of a formal token sale in exchange for preferential allocations. However, according to post‑mortems, technical issues, bot activity and misconfigured contracts led to unintended deposits and chaotic user experience, forcing the team to cancel the planned raise and unwind the process. While MegaETH remains a live project, the episode damaged trust and illustrated how difficult it can be to run very large, permissionless onchain fundraising events without battle‑tested infrastructure and clear, conservative parameters. In a market already wary of outsized raises with little track record, such missteps risk reinforcing the narrative that ICO‑scale fundraising is misaligned with genuine product‑market fit.

Monad’s MON token sale on Coinbase showcases a different approach: a regulated, exchange‑hosted public sale with clear allocation, pricing and geographic parameters. The sale offers \(7.5\%\) of the total 100 billion MON supply, or 7.5 billion tokens, at a fixed price of \$0.025, implying a \$2.5 billion fully diluted valuation. It is open for 5.5 days to participants in over 80 countries, including the U.S., with a fair‑allocation model that prioritizes smaller bidders and caps individual participation at \$100,000. Any tokens not sold in the public tranche are to be redirected to ecosystem development rather than returned to private allocations, addressing concerns about insiders reclaiming unsold supply. By running the sale through a major exchange with compliance infrastructure and transparent documentation, Monad is effectively merging the ICO concept with elements of a public equity offering, aiming to reduce both regulatory and reputational risk.

The story of Tally, the governance platform that ultimately decided not to proceed with an ICO and instead wind down operations, highlights the limits of tokenization as a business model. Tally helped DAOs administer governance, facilitating over \$1 billion in payments and safeguarding on the order of \$80 billion in onchain value. Despite this, the team concluded that demand for governance tooling was insufficient to justify a token sale or ongoing venture‑backed development, especially in a market skeptical of governance tokens without clear value capture. Rather than forcing a token into a model where it did not fit, they chose to sunset the platform, giving users time to migrate. For founders, this case illustrates that launching a token is not always the optimal path, even for protocols deeply integrated into the onchain economy; for investors, it is a reminder that the absence of an ICO can sometimes be a sign of discipline rather than a missed opportunity.

Taken together, these case studies illustrate the spectrum of ICO outcomes: from epoch‑defining success (Ethereum), through technical failure and eventual rescue (the 2016 contract bug), to operational missteps under intense market scrutiny (MegaETH), regulated evolution (Monad on Coinbase), and thoughtful abstention (Tally). For a crypto news audience, they reinforce a key point: ICOs are neither inherently good nor inherently bad. They are tools whose effectiveness depends on design quality, legal context, market conditions and, ultimately, on whether the underlying protocol delivers real, onchain value over time.

ICOs In Today’s Market: Volumes, Narratives And Platforms

In the mid‑2020s, ICOs coexist with a wider array of funding channels, from private venture rounds and onchain revenue financing to IDOs, airdrops and memecoin launches. Quantitatively, the category is a shadow of its 2017 peak. CryptoRank’s data showing only \$58 million raised via ICOs, IEOs and IDOs in Q2 2026, down 85% quarter‑on‑quarter, indicates how cautious both projects and investors have become about public token sales. The sharp drop in the number of public sales—from 105 in the preceding quarter to several dozen—is consistent with a market that has shifted attention toward established L1s, stablecoins, RWAs and real revenue‑generating protocols. This does not mean there is no appetite for early‑stage tokens; rather, it suggests that capital is more concentrated and selective.

Narratively, the ICO conversation has splintered. On one side, there is lingering fascination with high‑profile speculative bets: pre‑launch markets for tokens tied to major brands or protocols, leveraged trading on CEXs around rumored “biggest ICO ever” events, and the ever‑present prospect of 100× PUMPs. On the other side, there is a sober recognition—visible in commentary from market analysts and builders—that the era of easy ICO money with no product is over, at least for now. As Miles Deutscher and others have argued, the next phase of crypto growth is likely to feature stronger institutional dominance, substantial growth in stablecoin supply, and an outperformance of protocols with real, onchain revenues relative to pure speculation, even if an “ICO renaissance” eventually emerges within that more mature context.

Platform dynamics reinforce this bifurcation. On regulated exchanges, ICO‑like sales such as Monad’s MON offering are carefully curated, compliance‑driven and often oriented toward users who already trade major assets like ETH and BTC. On DeFi and onchain platforms, permissionless launchpads and memecoin factories make it trivial to spin up new tokens, often with little more than a logo and a ticker, tapping into retail flows chasing the next 1,000× PUMP. The Pump.fun ecosystem on Solana, for example, reduces token creation and initial liquidity to a web form and a small fee, blurring the line between “ICO” and spontaneous meme mint. While these launches rarely come with white papers or detailed tokenomics, they compete directly for attention and liquidity with more structured ICOs, especially in frothy market phases.

At the macro level, the shift to a post‑hype market also reflects regulatory and macroeconomic realities. Stablecoins—once a niche tool for traders—are now central to onchain and cross‑border payments, drawing heightened regulatory focus. As policymakers and central banks evaluate the systemic role of stablecoins and tokenized treasuries, speculative token launches must navigate a more scrutinized environment in which consumer protection and financial stability are front of mind. At the same time, higher interest rates in traditional markets raise the opportunity cost of holding non‑yielding speculative tokens, pushing investors toward protocols that can demonstrate sustainable yields derived from real activity rather than emissions‑driven farming. ICOs that can position themselves as gateways to such protocols, rather than as standalone casino chips, are better placed to attract durable capital.

Finally, onchain culture itself has matured. Early ICOs were often the only game in town for supporting new Ethereum‑based projects. Today, users and builders have multiple channels for participating in protocol growth: running validators, contributing to DAOs, providing liquidity to DEXs, building on top of core protocols, or earning airdrops through usage. ICOs are now one option among many for distributing value and risk. Some of the most anticipated events—such as large‑scale airdrops to long‑time users of DeFi platforms—do not involve raising new capital at all, but rather redistributing existing value to those who have contributed onchain. In this context, the role of ICOs is more specialized: they are best suited for protocols that require substantial up‑front capital, have clear token‑based value capture, and can make a credible case that public investors should share in that upside alongside private capital and contributors.

Conclusion

Viewed in historical perspective, ICOs were both a product of and a catalyst for Ethereum’s early growth. They provided a capital formation mechanism that matched the ethos and technical affordances of programmable blockchains: global, permissionless, and natively digital. Millions of people around the world gained exposure to early‑stage crypto projects without going through traditional financial institutions, and some of those bets, most notably Ethereum’s own ICO, delivered extraordinary returns to long‑term holders. At the same time, the lack of mature regulation, the ease of token creation and the intoxicating narrative of quick riches yielded a wave of scams, half‑baked projects and poorly structured offerings that burned many participants and attracted justified regulatory scrutiny.

Today’s ICO landscape is more nuanced. Pure ICO volumes are far below their peak, and the term itself has lost some of its marketing appeal as projects experiment with IEOs, IDOs, airdrops and other launch models. Yet the underlying idea—a primary token sale to bootstrap a protocol or network—remains alive, now embedded in more complex and often more compliant architectures. Regulated exchange‑hosted sales such as Monad’s MON offering show that ICO‑like events can coexist with securities law and investor protection regimes, while DeFi‑native innovations like HIP‑6 signal that onchain communities are still actively solving the microstructure problems that plagued earlier launches.

For investors and builders alike, the lesson is that structure matters. Token design, legal framing, smart contract implementation, allocation rules and post‑launch liquidity strategy all shape whether an ICO is a fair mechanism for aligning a project with its community or a short‑lived PUMP followed by disillusionment. In an environment where onchain data is widely available and sophisticated players scrutinize fundamentals such as user retention, protocol revenue and treasury management, it is harder for hollow narratives to sustain themselves over time. The most durable ICOs are likely to be those that treat the token sale as one step in a long‑term decentralization and value‑creation plan, rather than as an exit opportunity for insiders.

Ultimately, ICOs are best understood not as a monolithic phenomenon but as one expression of crypto’s broader experiment with programmable capital. They sit at the intersection of investment, technology and community building, leveraging blockchains’ ability to represent and trade ownership stakes in open networks. Whether they deserve a central place in the next phase of crypto’s evolution will depend less on branding and more on execution: on whether upcoming generations of ICOs can marry onchain transparency with sound economics, regulatory clarity and genuine product‑market fit, in a market that is increasingly unforgiving of empty promises.

Outlook

Looking ahead, the future of ICOs is likely to be cyclical but structurally different from the 2017 peak. Analysts who anticipate an “ICO renaissance” generally envision one embedded in a more institutional, fundamentals‑driven market, where tokens represent claims on real cash flows, RWAs or critical infrastructure rather than purely speculative narratives. In such a setting, ETH and other base assets will remain the primary collateral and funding currencies for launches, but investors will expect clear explanations of how token value links to protocol economics, not just vague allusions to network effects.

Regulatory trajectories will play a decisive role. If clearer paths emerge for compliant token offerings—whether under securities, crowdfunding or bespoke cryptoasset regimes—more high‑quality teams may choose public token sales over opaque private rounds. Conversely, if enforcement actions continue to treat most ICOs as illicit securities offerings, the center of gravity may shift further toward private capital and airdrops, with ICOs remaining a niche tool in more permissive jurisdictions. Parallel innovations in launch mechanics, from fair auctions to improved anti‑bot protections and data‑driven allocations, will determine whether retail participants can access early‑stage tokens on terms that feel meaningfully fair, rather than as exit liquidity for insiders and high‑frequency traders.

For a crypto news audience tracking the intersection of onchain innovation and market structure, the key is to view each ICO not as a generic event but as a specific design choice within a broader ecosystem. The same underlying technologies that enabled early ICO PUMP cycles also enable transparent treasuries, verifiable token flows and accountable governance. Whether the next wave of ICOs leans more toward speculative excitement or sustainable value creation will depend on how builders and investors use those tools—and on whether they remember the lessons coded into Ethereum’s success, the scars of 2017’s excess, and the quiet discipline of projects that chose not to launch a token at all.

Latest ICO news

Sources

- https://globaladvisoryexperts.com/what-is-an-initial-coin-offering-ico-and-how-does-it-work/

- https://www.europarl.europa.eu/RegData/etudes/BRIE/2021/696167/EPRS_BRI(2021)696167_EN.pdf

- https://www.sciencedirect.com/science/article/abs/pii/S235267342030069X

- https://trustswap.com/blog/crypto-fundraising-models-explained

- https://coincodex.com/ico/ethereum/

- https://www.sec.gov/about/divisions-offices/division-corporation-finance/framework-investment-contract-analysis-digital-assets

- https://cryptorank.io/insights/analytics/q2-2026-the-worst-ico-quarter

- https://pmc.ncbi.nlm.nih.gov/articles/PMC8591750/

- https://x.com/DecryptMedia/status/2061478636109099365

- https://cryptonews.net/news/ethereum/32945054/

- https://x.com/socialgraphvc/status/2038001062662050245

- https://www.bitget.com/news/detail/12560605319919

- https://x.com/lookonchain/status/2054716297666335035

- https://www.youtube.com/watch?v=NyhR_KyQ22U

- https://x.com/HYPERDailyTK/status/2027273017987154034

- https://x.com/milesdeutscher/status/2010749591462051987

- https://www.cryptopolitan.com/tally-winds-down-after-scrapping-ico-plans/

- https://www.bitget.com/news/detail/12560605087738

- https://ourcryptotalk.com/news/monad-mon-token-sale-begins-on-coinbase

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…