In‑depth explainer on Movement, the Move‑based settlement and yield layer for stablecoin payments and remittances in emerging markets, covering its tech stack, USDCx, RWA yield, licensed rails, partners, risks and long‑term outlook.

+12 sources across the wider coverage universe

Movement pivots toward global payments and remittances, securing licensed rails across the US, Canada and EU while repurchasing 19% of investor-allocated tokens in a major strategic shift2026-06

Movement pivots toward global payments and remittances, securing licensed rails across the US, Canada and EU while repurchasing 19% of investor-allocated tokens in a major strategic shift2026-06 a16z reveals stablecoin usage shifting from transfers to real-world payments, signaling maturation of onchain finance as adoption expands beyond trading and capital movement2026-04

a16z reveals stablecoin usage shifting from transfers to real-world payments, signaling maturation of onchain finance as adoption expands beyond trading and capital movement2026-04 Real-world finance is moving onchain, but most DeFi infrastructure isn’t ready for institutional finance. Tokenized assets, lending, and payments need trusted settlement and seamless capital movement Here’s how USDC + CCTP on Pharos make it possible 🧵2026-03

Real-world finance is moving onchain, but most DeFi infrastructure isn’t ready for institutional finance. Tokenized assets, lending, and payments need trusted settlement and seamless capital movement Here’s how USDC + CCTP on Pharos make it possible 🧵2026-03 Enry’s Island unveils “Enry’s Island Adventures”: Venture capital becomes a videogame and launches the “Strap” movement on Kickstarter.2026-04

Enry’s Island unveils “Enry’s Island Adventures”: Venture capital becomes a videogame and launches the “Strap” movement on Kickstarter.2026-04 STBL CEO Avtar Sehra heads to CNBC Converge to outline how stablecoins and tokenization will reshape global finance, as onchain systems redefine value issuance and movement2026-04

STBL CEO Avtar Sehra heads to CNBC Converge to outline how stablecoins and tokenization will reshape global finance, as onchain systems redefine value issuance and movement2026-04 Movement goes live on M1 mainnet with USDCx, a native USDC stablecoin built on Circle's xReserve2026-03

Movement goes live on M1 mainnet with USDCx, a native USDC stablecoin built on Circle's xReserve2026-03

Movement: The Stablecoin Settlement and Yield Layer For Emerging Markets

Built on the Move programming language, Movement is a blockchain network that aims to be a global settlement and yield layer for stablecoins, targeting cross‑border payments, remittances, and dollar savings products for emerging markets. Originally launched as an Ethereum Layer 2 powered by a Move virtual machine, the project has pivoted toward regulated stablecoin infrastructure, native dollar yield, and real‑world payment rails, positioning itself as connective tissue between onchain finance and the global financial system.

What Movement Is – And What It Is Not

Movement sits at the intersection of blockchain infrastructure, regulated payments, and stablecoin‑denominated yield, and it is important to distinguish this protocol from other uses of the word “movement” in crypto and politics. In technical terms, Movement is a network of blockchains built on the Move language and the MoveVM, designed to provide safe, expressive smart contracts specialized for financial applications. The network’s current narrative is tightly focused: it wants to be the place “where money lives,” offering a stack that combines stablecoin settlement, money markets, curated yield vaults, and access to licensed off‑chain payment rails.

This scope differentiates Movement from the broader “Web3 movement” that advocates for user‑owned internet infrastructure, or from political movements such as Donald Trump’s MAGA coalition that deploy the term “movement” as a branding tool rather than a technical descriptor. Political movements might invoke sound money or Bitcoin as part of a campaign narrative, but they are not protocols in themselves, and they lack the deterministic settlement guarantees that a network like Movement attempts to provide. Similarly, “price movement” is a core concept in market reporting, capturing short‑term volatility in assets like BTC, ETH, or governance tokens, yet this is an analytic lens rather than a piece of infrastructure. Understanding these distinctions is useful for a crypto news audience, because coverage often shifts fluidly between social movements, price movements, and the Movement Network protocol.

Where Movement is distinctive is in its attempt to fuse stablecoins, yield, and compliant off‑chain rails into a single integration surface for fintechs and neobanks operating in emerging markets. The project explicitly targets use cases where users need access to dollar‑denominated savings, low‑cost remittances, and real‑world asset (RWA) yield, but are either excluded from or underserved by the legacy banking system. In doing so, Movement is betting that the next phase of crypto adoption will be driven less by speculative trading or high‑frequency “price movement” and more by everyday payments and dollar savings embedded inside consumer apps.

From Ethereum Layer 2 to Specialized Settlement Layer

The first iteration of Movement was framed as “Ethereum’s first layer 2 on the MoveVM,” positioning it as an alternative virtual machine (AltVM) rollup in the increasingly crowded Ethereum scaling landscape. In that model, Movement was a network of Ethereum‑secured blockchains that used MoveVM to execute contracts while maintaining compatibility with the Ethereum Virtual Machine (EVM), allowing developers to bridge assets and logic between environments. The Move language, originally developed at Meta for the Diem project, gave Movement a resource‑oriented programming model designed to improve safety and expressivity for financial applications when compared with Solidity.

As the Layer 2 boom accelerated, however, competition among rollups intensified, with many teams vying for liquidity and developer mindshare. Industry reporting has noted that Movement’s on‑chain activity declined over time, prompting the team to explore a pivot toward operating its own Layer 1 and to rethink how it differentiated itself from generic scaling solutions. Simultaneously, the broader market for L2 tokens grew more saturated, and users became less willing to experiment with new chains purely for marginal gas savings. In that environment, an altVM alone was not a compelling enough story.

The inflection point came when the team behind Movement decided to lean fully into stablecoin payments, cross‑border remittances, and yield as its core mission. Public statements describe this as a deliberate strategic shift: the company secured access to licensed payment rails in the United States, Canada, and the European Union, and rebranded Movement as the global settlement and yield layer for stablecoins. Reporting from industry news outlets framed this pivot as a response to the “layer‑2 boom losing momentum,” with Movement redirecting its roadmap toward the roughly 685 billion‑dollar remittance market serving low and middle‑income countries. In other words, the project moved from competing as yet another L2 to trying to own a specific application vertical: regulated stablecoin payments and yield for emerging markets.

Movement Versus Other “Movements” In Crypto And Politics

The word “movement” carries heavy cultural and political baggage, and the crypto industry frequently deploys it metaphorically. At events like the Web3 Summit, for example, speakers talk about a movement to “reclaim the internet for the people,” using decentralized protocols as tools for user sovereignty, censorship resistance, and programmable money. This rhetorical framing matters because it shapes how regulators, investors, and the public perceive crypto technologies: as either speculative instruments or as part of a broader social project.

In parallel, political actors, especially in the United States, describe their campaigns as movements. Donald Trump’s repeated references to the “MAGA movement” exemplify this trend, and his endorsements of down‑ballot candidates often frame them as warriors for that movement, not just individual politicians. While this may seem far removed from a protocol like Movement, there is a subtle connection: as political movements begin to engage with crypto policy, stablecoins, and Bitcoin, the regulatory environment that projects like Movement operate in can shift quickly. Campaign rhetoric about “crypto freedom” or “protecting Bitcoin” can translate into concrete laws governing stablecoins, money transmitter licenses, and cross‑border capital flows.

The upshot for readers is that when news headlines mention “the movement,” context is everything. Some articles will be about asset price movement, others about social or political movements, and others about the Movement Network protocol itself. This explainer focuses on the last of these, but it is useful to keep the broader semantic landscape in mind when parsing coverage that spans Trump, stablecoin payments, yield strategies, and Web3 infrastructure in a single news cycle.

Movement pivots toward global payments and remittances, securing licensed rails across the US, Canada and EU while repurchasing 19% of investor-allocated tokens in a major strategic shift

$38M of post-listing market-maker damage is the context that makes the 4.2% supply buyback matter; Movement is cleaning up cap-table overhang while asking fintechs to trust it as settlement plumbing. KAST’s 18k verified users and Sorted’s 500k downloads give the stack a distribution wedge, but remittance winners need local cash-out, fraud controls, support and corridor liquidity before 278ms blocks matter. USDCx gives them a cleaner Circle-backed dollar leg than wrapped stablecoins; TRON’s USDT moat is habit plus liquidity, so the bar is weekly flows in Mexico/Nigeria/Pakistan, not partner logos.

Readers click Movement stories primarily when framed as institutional stablecoin settlement infrastructure — the highest-engagement headline is about DeFi readiness gaps for institutions, not Movement's own blockchain mechanics, revealing that the audience bets on the stablecoin rails thesis more than on MOVE the token.↗

Architecture: Move, Modular Chains, And Settlement

At the technical core of Movement is the Move programming language and the MoveVM, which together form a virtual machine optimized for financial use cases. Move is a resource‑oriented language in which assets are represented as linear types that cannot be duplicated or accidentally destroyed, an architecture that aims to prevent entire classes of bugs common in Solidity contracts. The language supports fine‑grained access control and formal verification, making it attractive for building money markets, stablecoin protocols, and other financial primitives where safety and predictability are paramount. Movement leverages these properties to position itself as a safer settlement layer for high‑value flows like remittances and institutional stablecoin balances.

Movement’s network design is modular and multi‑chain. Early technical documentation and independent research describe it as a network of interconnected blockchains built using the same architecture and relying on the MoveVM, with compatibility bridges to the EVM. Rather than a single monolithic chain, Movement envisions a fabric of application‑specific or region‑specific chains that share common tooling and security assumptions. This approach mirrors broader trends in modular blockchain design, where execution, settlement, and data availability can be separated or recombined depending on the use case.

Security in this model is layered. On the onchain side, Movement relies on Move’s safety guarantees and rigorous audits of core protocols such as its canonical money market. On the off‑chain side, the project integrates with licensed payment partners that handle fiat custody, KYC/AML, and compliance in jurisdictions like the US, Canada, and the EU. This dual structure allows Movement to offer an end‑to‑end pipeline where value can originate in bank accounts, move through stablecoins on Movement’s chains, earn yield via onchain RWAs, and eventually be redeemed back into fiat, all while remaining within regulated perimeters for key touchpoints.

MoveVM Versus EVM: Why Language Choice Matters For Money

The Ethereum Virtual Machine was designed for general‑purpose smart contracts with a strong bias toward transparency: every transaction is public, every contract’s state is inspectable, and the language ecosystem has evolved around Solidity and EVM‑compatible variants. This model has been enormously successful, but it also has drawbacks when applied to complex financial systems. Re‑entrancy attacks, mis‑implemented token standards, and unsafe upgrade patterns have all led to multi‑million dollar exploits in the EVM world.

Move, by contrast, was explicitly designed as “a language for money.” Its resource model treats assets as first‑class citizens with strong guarantees about ownership and conservation, making it easier to encode invariants like “this coin cannot be spent twice” or “this vault cannot mint new tokens without appropriate collateral.” Formal verification tools built around Move allow developers to prove these invariants mathematically before deploying contracts, an appealing property for protocols like Movement that want to handle remittances and institutional stablecoin flows.

Movement’s use of MoveVM also helps it differentiate from other stablecoin‑focused chains that remain fully EVM‑based. While Move introduces a learning curve for Solidity developers, it offers a new design space for financial applications that require complex state machines, programmable access control, or fine‑grained tracking of multi‑asset portfolios. This is particularly relevant for yield products built on tokenized T‑bills, AAA‑rated CLOs, and structured lending pools, where ensuring the correct accounting of cash flows is critical. Movement’s bet is that a safer, more expressive VM will ultimately be an asset for builders of onchain financial infrastructure.

Toward A Dedicated Settlement Layer

As Movement repositioned away from being yet another Ethereum rollup, it leaned into the narrative of being a dedicated settlement and yield layer for stablecoins. Its mainnet, often referred to as M1 in official releases, hosts native assets like USDCx, and serves as the base for DeFi protocols that build money markets, DEXs, and vaults around that stablecoin. The team’s public communications emphasize that USDCx is natively issued on Movement, not bridged from another chain, eliminating a class of bridge‑related risks such as those seen when cross‑chain infrastructure sunsets or suffers liquidity shortfalls.

Movement’s architecture is increasingly slanted toward being the “middle layer” between local fiat payments systems and diverse onchain ecosystems. The introduction of intent‑based cross‑chain routing via NEAR Intents, discussed below, further reinforces this role: Movement is the place where yield and stablecoin balances ultimately live, even if user funds originate on other chains like Ethereum, Tron, or Polygon. In this sense, the network’s architecture is as much about connectivity and settlement finality as it is about throughput or gas fees.

The Stablecoin Stack: USDCx, Money Markets, And Yield

Movement’s value proposition hinges on a tightly integrated stack of stablecoins, money markets, and curated yield products. The foundational asset is USDCx, a natively issued stablecoin on Movement that is fully backed 1:1 by USDC. Unlike bridged stablecoins that lock collateral on another chain and issue synthetic claims, USDCx is minted and redeemed through a direct relationship with the USDC issuer and its banking partners, according to public statements. This design aims to combine the familiarity and regulatory moat of USDC with the performance and cost advantages of the Movement chain.

The launch press release for USDCx emphasizes several core properties: no bridges or opaque wrapping, near‑zero transaction fees on Movement, and a focus on everyday payments, remittances, and financial access for consumers in the Global South. On day one, USDCx integrated into a range of ecosystem protocols, including lending markets, DEXs, aggregators, and institutional custody solutions like Fireblocks and MPC Vault. This breadth of integration is crucial, because it makes USDCx not just a payment token but also a composable building block for DeFi yield, collateralization, and treasury management.

To make the role of USDC and USDCx concrete, it is helpful to compare them conceptually.

| Feature | USDC on Ethereum | USDCx on Movement M1 |

|---|---|---|

| Issuance | Native ERC‑20 on Ethereum | Native stablecoin on Movement, backed 1:1 by USDC |

| Transfer Fees | Subject to Ethereum gas prices | Near‑zero fees on Movement mainnet |

| Primary Use Cases | Trading, DeFi collateral, treasury | Payments, remittances, savings, onchain yield |

| Trust Model | Regulated issuer, Ethereum security | Same issuer backing plus Movement chain security |

| Bridge Dependency | None for Ethereum | No external bridge; integration at issuance layer |

The table underscores Movement’s strategy: rather than competing with USDC, it extends USDC’s reach into emerging markets and low‑cost payments by offering a specialized execution environment and settlement layer.

MovePosition: Canonical Money Market As Load‑Bearing Infra

On top of USDCx, Movement has designated MovePosition as its canonical lending and borrowing market, selected through a formal RFP process. In Movement’s own framing, a canonical money market is “load‑bearing infrastructure,” because yield strategies, structured products, and payments rails all build on top of it. MovePosition allows users to supply and borrow assets, establishing onchain interest rates and creating the base layer of liquidity that other protocols can plug into.

By running an RFP rather than arbitrarily anointing a partner, Movement signaled that the design, risk management, and resilience of this money market were subject to scrutiny. Official communications stress that MovePosition had demonstrated robustness during periods of elevated redemption activity, a key test for any lending platform that wants to support real‑world users rather than purely speculative leverage. For Movement’s target demographic—emerging‑market neobanks and their customers—this resilience matters: a failure in the canonical money market could cascade into losses for savings products and remittance flows that sit on top of it.

Economically, MovePosition supplies yield to other components of the stack. When users deposit USDCx into money markets, they receive interest‑bearing tokens that represent their share of the pool; those tokens can then be used as building blocks in vaults or structured products. This composability is standard in DeFi, but Movement’s twist is to couple it with RWAs and regulated payment rails so that dollar yield has a clearer link to traditional fixed income instruments like T‑bills and CLOs.

Canopy: Yield Curation And Vault Infrastructure

If MovePosition is the base yield engine, Canopy is the curation and distribution layer. Described as the “vault interface partners use to offer savings products to their users,” Canopy is deployed on Movement and connects eligible users to independent yield providers who manage underlying strategies. Users deposit USDC into Canopy vaults and receive yield‑bearing receipt tokens in return, while curators allocate capital across multiple providers to optimize risk‑adjusted returns.

Canopy’s design acknowledges that most neobanks and fintechs do not want to become full‑time DeFi strategy managers. Instead, they want a plug‑and‑play way to offer dollar savings with competitive yield, regulatory‑friendly backing, and clear reporting. By centralizing the curation function in an infrastructure layer, Movement allows different yield providers—such as Yuzu Money and Avant—to occupy specific parts of the risk spectrum. This is akin to an investment platform that offers a menu of conservative, moderate, and aggressive funds, except that the underlying assets are tokenized and onchain.

Public messaging from Movement and Canopy has emphasized sustainability and conservative risk management rather than eye‑catching APYs. That posture reflects hard lessons from the last cycle, where unsustainably high yields on algorithmic stablecoins led to spectacular collapses. In contrast, Canopy’s early partners are rooted in real‑world asset strategies, lending to creditworthy institutions, and tokenized short‑duration credit instruments, which produce yields that track traditional interest rate markets.

Yuzu Money, Avant, Oro, Zoth: Real‑World Asset Yield

Among the Day‑1 yield providers integrated into Canopy, Yuzu Money occupies the conservative end of the spectrum. Yuzu is a “Yield‑as‑a‑Service” platform that connects curated onchain strategies to neobanks and fintechs, and it already powers a meaningful share of EtherFi’s liquidUSD (Earn) vault product. Its flagship offering on Movement is Yuzu Prime, a conservative tier that targets around 7% APY through a portfolio that blends U.S. Treasury bills, AAA‑rated collateralized loan obligations (CLOs), and overcollateralized lending via platforms such as Maple Finance. While yields will vary over time, the important point is structural: Yuzu Prime is backed by identifiable, investment‑grade assets, not purely by leverage or reflexive token incentives.

For Movement users holding USDC on the network, Yuzu Prime offers a yield option that is explicitly differentiated from high‑risk or algorithmic strategies. The vault is USD‑denominated, backed by real‑world assets, and designed to satisfy compliance requirements that regulated partners such as neobanks must navigate. This makes it a plausible candidate for dollar savings accounts in emerging markets, where local banks may be unstable or offer negative real yields due to inflation.

Other partners fill different niches. Avant Protocol focuses on treasury and yield products that have weathered periods of heavy redemptions, making it suitable for institutions with shorter liquidity horizons. Oro brings tokenized gold vaults and physical redemption infrastructure, giving Movement’s partners a way to offer gold‑backed savings products alongside dollar stablecoins. Zoth contributes institutional‑grade RWA yield infrastructure that packages investment‑grade assets into tokenized products, broadening the menu of yields available on Movement. Together, these providers allow Movement to present a more complete yield curve, spanning conservative dollar savings to more diversified portfolios.

NEAR Intents: Cross‑Chain Yield Without Bridges

One of Movement’s more technically ambitious integrations is with NEAR Intents, a system developed by Defuse Labs that abstracts away the complexity of moving funds across multiple blockchains. Instead of requiring users to manually bridge assets, select networks, and manage gas tokens, NEAR Intents allows them to simply state their goal—such as “earn stablecoin yield on Movement”—and lets an open network of automated solvers handle the routing. These solvers scan more than twenty connected chains, find the fastest and cheapest route, and execute the necessary transactions in the background.

For partners offering yield products on Movement, this means they can accept eligible deposits from any connected chain without changing how their applications work. A user on Tron, Ethereum, or Polygon can deposit their preferred asset, and the intent engine will route it such that the final balance arrives on Movement, where it is converted into the appropriate stablecoin and put to work earning yield. Importantly, the users are not exposed to the complexities of bridges, wrapped assets, or gas management; they interact with a familiar neobank interface, and the cross‑chain machinery runs underneath.

This design responds to a real pain point in DeFi. Bridging protocols have historically supported dozens of networks, but over time some of these bridges have been sunset, leaving users to navigate recovery processes that can involve burning tokens on one chain, paying fixed fees on another, and initiating manual settlements. By shifting to an intent‑based model, Movement and NEAR Intents aim to reduce the operational burden on users, while still providing access to multi‑chain liquidity. For a user in Nigeria or Pakistan who is not crypto‑native, this abstraction can be the difference between engaging with stablecoin yield or abandoning the process altogether.

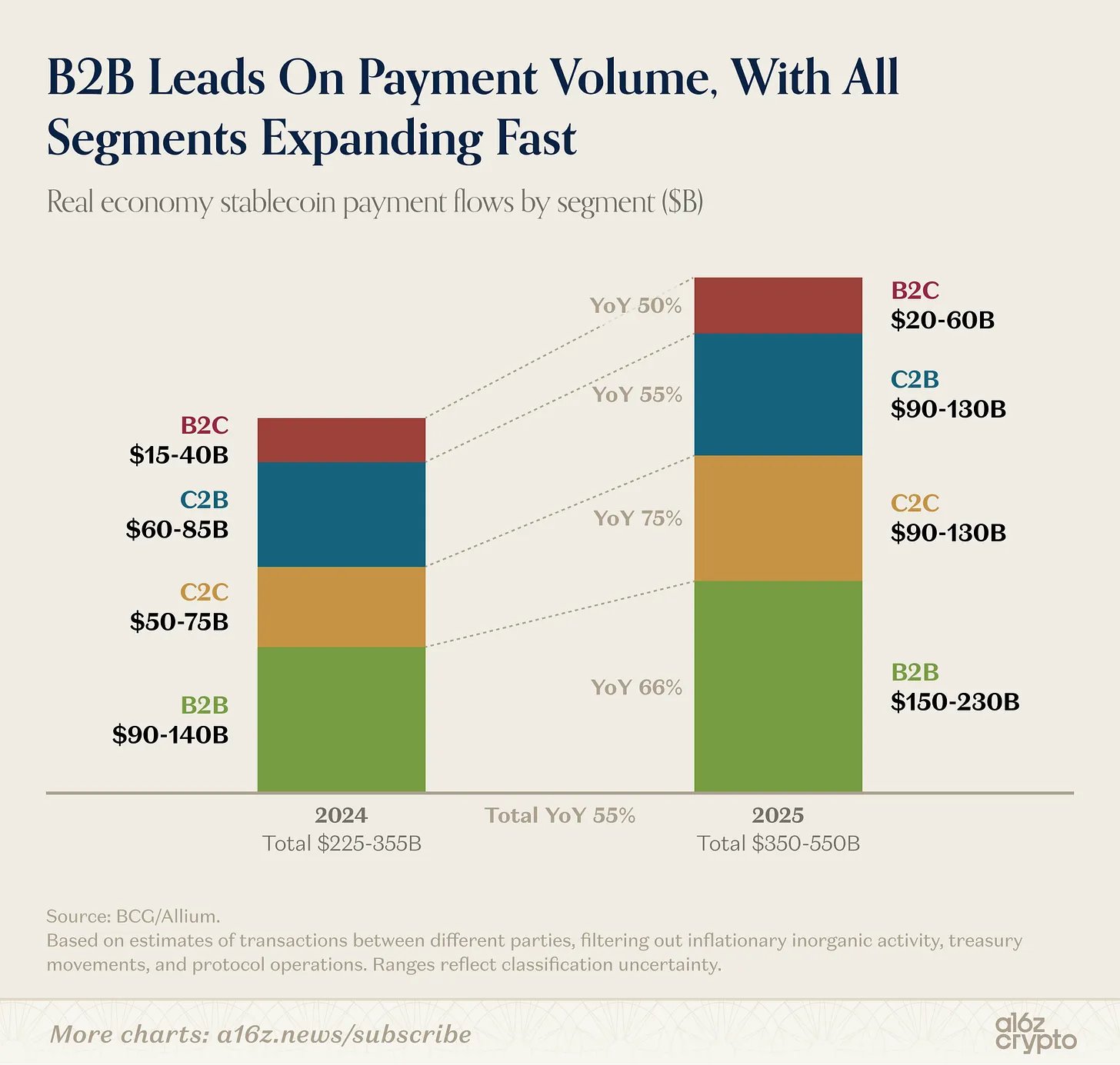

a16z reveals stablecoin usage shifting from transfers to real-world payments, signaling maturation of onchain finance as adoption expands beyond trading and capital movement

Cross-border stablecoin share collapsed from ~50% to ~25% of payment volume in two years — the 2022 remittance thesis is dead, replaced by domestic rail integration like BRLA + PIX hitting $400M/month. C2B transactions doubled to 284.6M in 2025 (128% YoY), the volume regime where merchant adoption stops being a curiosity and starts compounding. Asia owns 66% of payment volume while US/EU regulatory frameworks debate over a shrinking minority of actual flow.

- 01institutional DeFi infrastructure gap↗

The dominant click driver was the argument that most DeFi infrastructure cannot handle institutional capital flows, positioning USDC + CCTP settlement as the credible solution — readers are evaluating whether the category is real, not just Movement itself.

- 02stablecoin real-world payment adoption↗

a16z data showing stablecoin usage migrating from crypto transfers to everyday payments gave readers an external validation signal that the market Movement is targeting is actually materialising.

- 03licensed payment rails pivot↗

Movement securing money-transmitter licenses across the US, Canada and EU while simultaneously repurchasing 19% of investor tokens was a credibility-and-commitment signal that pulled readers wanting evidence the pivot is real, not just a rebrand.

- 04USDCx M1 mainnet launch↗

The launch of a native USDC-backed stablecoin on Movement's own mainnet was the concrete product milestone readers used to judge whether the payments pivot had shipped anything tangible.

- 05Stableyard payments ecosystem bet↗

Movement's investment in Stableyard signalled that the network is building an end-to-end stablecoin payments stack, not just a chain — readers tracked it as a gauge of how much of the stack Movement intends to own.

Payments, Remittances, And Emerging Markets

The decision to focus on stablecoin payments and remittances places Movement at the center of a broader secular trend: the maturation of stablecoins from trading tools into everyday money. In the early years of DeFi, stablecoins like USDC and USDT were primarily used for arbitrage, liquidity provision, and as safe havens during market volatility. Today, research and reporting from major industry players suggest that an increasing share of stablecoin volume is tied to real‑world payments, merchant transactions, and cross‑border payroll, signaling a shift toward utility beyond pure capital movement. Circle, for example, has emphasized that payment interoperability and real‑world use cases are now core to its strategy for Global USDC adoption.

Remittances are a natural target for stablecoin rails. The World Bank estimates that annual remittance flows to low and middle‑income countries are on the order of hundreds of billions of dollars; Movement cites a figure of roughly 685 billion dollars as its target market segment. Traditional remittance channels often impose high fees, slow settlement times, and inconvenient cash pickup mechanisms, especially in regions with weak banking infrastructure. Stablecoins, by contrast, can move value globally in minutes, settle irreversibly onchain, and be held in self‑custodial wallets or converted into local currency through fintech apps.

Movement’s infrastructure is designed to slot into this landscape as a backend settlement layer that fintechs and neobanks can build on. Instead of each startup needing to secure money transmitter licenses in the US, Canada, or the EU, Movement works with licensed payment providers that already have those permissions and exposes their capabilities through APIs and onchain integrations. Builders can then focus on user experience, local distribution, and compliance in their home markets, while relying on Movement to move dollars across borders as stablecoins and to provide yield on idle balances.

Licensed Rails And Compliance As Competitive Advantage

One of Movement’s key differentiators is its access to licensed payment rails across major jurisdictions, secured through partnerships rather than direct licensing in every geography. According to public statements, the company has secured access to rails in the United States, Canada, and the European Union, enabling compliant movement of funds between bank accounts and onchain stablecoins. This setup allows a neobank in, say, West Africa or Southeast Asia to build cross‑border products that tap into US or EU banking systems without itself becoming a money transmitter in those regions.

The technical framework Movement has built around these rails is designed to reduce settlement times and lower the cost of moving money across borders. Instead of relying on correspondent banking systems and pre‑funded settlement accounts—a model that ties up capital and introduces counterparty risk—Movement routes value through stablecoins, with onchain settlement providing transparency and near‑real‑time finality. Licensed partners handle fiat custody and compliance at the edges, while Movement’s network serves as the neutral, programmable middle layer.

Compliance remains a central concern. Each licensed partner operates under its own program terms and underwriting standards, meaning that not all users or geographies will be eligible for every product. Know‑your‑customer checks, anti‑money‑laundering routines, and transaction monitoring continue to apply, even as the underlying settlement rail shifts from SWIFT messages to blockchain transactions. For regulators, this hybrid model offers a path to embracing stablecoin efficiency without abandoning consumer protection frameworks. For Movement, it offers a way to differentiate from purely permissionless chains that lack integrated compliance tooling.

Neobanks, Wallets, And On‑The‑Ground Integrations

Movement’s success will be measured not by the technical elegance of its stack but by the depth of its integrations with consumer‑facing applications. Several partners are already live and building on the network, spanning neobanks, wallets, yield providers, and tokenization platforms. KAST, for instance, has onboarded more than 18,000 verified users across over 160 countries through Movement‑powered products, suggesting early traction among globally distributed users.

Sorted Wallet illustrates Movement’s focus on accessibility. It is a non‑custodial crypto wallet built for feature phones with over 500,000 downloads across 160 countries and active users in Kenya, Nigeria, Tanzania, and Pakistan; the Movement Network Foundation participated in Sorted’s seed round alongside major industry players. By integrating with Movement, Sorted can offer stablecoin savings and payments to users who may not own smartphones, bridging a gap that many crypto projects overlook. This matters because in many emerging markets, feature phones remain a primary access point to digital services.

Other ecosystem participants play more specialized roles. Avant provides yield and treasury products, Yuzu Money curates conservative dollar yield, Oro tokenizes gold vaults with physical redemption, and Zoth brings institutional‑grade RWA strategies to the network. Collectively, they allow fintechs in corridors such as the US‑Mexico remittance route, West Africa, Southeast Asia, and the Gulf to plug into Movement once and receive an integrated stack of payments, treasury, savings, and liquidity services. This “single integration layer” pitch is a key part of Movement’s appeal to builders who want to offer stablecoin products without assembling dozens of separate vendor relationships.

Stableyard And DopePay: The Experience Layer For Stablecoin Commerce

Infrastructure only matters if it translates into usable experiences for end users and merchants. Recognizing this, Movement made a strategic investment in Stableyard, a full‑stack stablecoin commerce layer whose mission is to “make stablecoins move like money.” Stableyard focuses on the end‑to‑end experience of paying with and accepting stablecoins, offering merchant tools, checkout flows, and a consumer‑facing app. Movement’s investment is not purely financial; the two organizations plan to coordinate on routing merchant introductions, integrating Stableyard’s checkout as a payment surface for Movement‑native apps, and connecting Stableyard to Movement’s largest ecosystem applications.

Stableyard’s consumer app, DopePay, showcases what this experience layer looks like at the edge. In public teasers, DopePay is framed as an app where users can scan a QR code, tap their phone, and pay with stablecoins without worrying about wallet switching or chain selection. Social posts emphasize zero‑percent fees for paying with crypto and compatibility with local QR standards, suggesting that DopePay aims to be a bridge between existing POS infrastructure and onchain settlement. Movement has amplified these messages, describing DopePay as “one app for every payment, built on Movement,” underscoring its role as a flagship consumer experience.

For a merchant in, say, Lagos or Manila, this stack could mean accepting stablecoin payments from international customers, settling in USDCx on Movement, and either holding that balance to earn yield or converting to local currency through integrated off‑ramps. For a user, it could mean paying a local QR code with stablecoins from any chain, routed via NEAR Intents to Movement in the background, with the merchant receiving value in their preferred denomination. If executed well, this approach could make stablecoin payments feel as seamless as mainstream mobile money apps, while exposing users to new investment and savings opportunities.

Governance, Economics, And The Investment Lens

Any serious explainer for a crypto news audience must tackle governance and token economics, even when details are evolving. Movement’s native token, typically referenced as MOVE, follows a familiar pattern for L1/L2 networks: it is used for paying transaction fees, participating in network governance, and potentially securing the network through staking or other consensus mechanisms. Independent research has framed Movement’s tokenomics as part of a broader ecosystem strategy in which MOVE captures some of the value generated by stablecoin settlement, DeFi activity, and integration with external partners.

The pivot from a generic L2 to a stablecoin settlement layer has implications for token value. On one hand, focusing on payments and remittances could stabilize fee revenue and decouple it from speculative trading cycles, as stablecoin transfers and yield flows tend to be less volatile than NFT minting or leveraged trading. On the other hand, stablecoin users are often fee‑sensitive and may not tolerate high gas costs, putting downward pressure on per‑transaction revenue. Movement’s near‑zero‑fee positioning for USDCx transfers suggests that the network is prioritizing volume and ecosystem growth over maximizing immediate fee capture.

For investors, Movement represents exposure to several overlapping narratives: the rise of stablecoin payments, the growth of RWA tokenization, and the search for sustainable, dollar‑denominated yield. Retail users can interact with Movement primarily through stablecoins and savings products, treating it more like a fintech backend than a speculative betting platform. Institutional investors, by contrast, might evaluate MOVE as a governance and fee‑capture token, while also considering direct investment opportunities in ecosystem participants like Yuzu, Stableyard, or Sorted Wallet.

Stablecoin Yield: Sources, Risks, And Sustainability

Stablecoin yield on Movement draws from both onchain and off‑chain sources. On the onchain side, money markets like MovePosition generate interest from borrowers who supply collateral to gain leverage or manage short‑term liquidity needs. On the off‑chain side, RWA vaults like Yuzu Prime invest user funds into portfolios of short‑duration U.S. Treasury bills, highly rated CLOs, and overcollateralized loans to institutions vetted by platforms like Maple Finance. In an environment of higher global interest rates, these instruments can produce mid‑single to low‑double‑digit yields without relying on reflexive token rewards.

However, no yield is free of risk. Treasury bills carry interest rate risk and, in extreme scenarios, sovereign credit risk; CLOs add tranche‑specific credit and liquidity risk; and overcollateralized loans can still default if collateral assets crash or counterparties behave maliciously. Onchain wrappers introduce additional smart contract risk, oracle risk, and governance risk, as changes in protocol parameters or misaligned incentives can impact the safety of the vaults. For Movement’s users, especially those in emerging markets where financial literacy about structured products may be limited, these risks must be clearly disclosed and managed.

Movement’s communications around yield emphasize stress‑testing under “real redemption pressure” and the importance of conservative strategies for regulated partners. Avant is highlighted as having weathered periods of elevated redemptions, implying that its liquidity management and risk controls have been tested in practice. Yuzu Prime is explicitly described as the low‑to‑medium risk slot in the Canopy lineup, in contrast to more aggressive strategies that may emerge later. This framing aligns with a post‑2022 industry norm that prioritizes sustainability and transparency over headline APYs, especially for products that aspire to be the onchain equivalents of savings accounts or money market funds.

Investment Case: Comparing Movement To Alternatives

From an investment standpoint, Movement can be compared to several categories of alternatives. On one axis, it competes with traditional bank accounts and remittance services; on another, with other stablecoin‑oriented chains and DeFi protocols. The table below offers a high‑level conceptual comparison.

| Dimension | Traditional Bank / Remittance | Generic DeFi on Ethereum | Movement Stablecoin Stack |

|---|---|---|---|

| Settlement Speed | 1–3 days (SWIFT, correspondent banks) | Minutes, subject to gas | Near‑instant on Movement mainnet |

| Fees | 3–10% for remittances typical | Variable gas plus protocol fees | Near‑zero transfer fees; yield vault fees apply |

| Access Requirements | Local ID, bank account | Crypto‑native, wallet, gas | Neobank or wallet interface; KYC with partners |

| Yield On Dollars | Low, often below inflation | Variable, often higher risk | RWA‑backed, curated via Canopy and partners |

| Regulatory Perimeter | Fully regulated | Varies; often gray area | Hybrid: licensed rails plus permissionless settlement |

| User Experience | Familiar, but slow and fragmented | Complex, bridge‑intensive | Abstracted via intents, QR payments, and local apps |

For users in emerging markets, Movement’s value proposition is that it can deliver dollar‑denominated yield and low‑cost remittances in a single interface, powered by stablecoins and onchain infrastructure. For investors, the key question is whether Movement can achieve sufficient scale and regulatory clarity to make its token and ecosystem sustainably valuable, especially in a crowded market where other networks are chasing similar goals.

Real-world finance is moving onchain, but most DeFi infrastructure isn’t ready for institutional finance. Tokenized assets, lending, and payments need trusted settlement and seamless capital movement Here’s how USDC + CCTP on Pharos make it possible 🧵

$9B in tokenized treasuries sitting on-chain and most of it is dead capital — minted, custodied, earning yield, but not composable with the DeFi stack it lives on. Pharos pairing CCTP across 20+ chains with Centrifuge's JTRSY/JAAA distribution is attacking the right layer, but every institutional chain keeps recreating permissioned walled gardens that fragment liquidity instead of deepening it. Cross-jurisdictional compliant settlement — not just fast finality on a single L1 — remains the gap nobody's closed, and bolting KYC onto existing DeFi primitives won't get us there.

Movement launches M1 mainnet (initial)

Token-dumping scandal, market-maker controversy

Movement pivots from Layer-2 to Layer-1 positioning

USDCx native stablecoin launches on M1 mainnet

Movement acquires Canopy vault infrastructure

Licensed payment rails secured in US, Canada, EU; 19% investor token repurchase announced

Movement invests in Stableyard for stablecoin payments experience layer

NEAR Intents integration enables cross-chain yield settlement on Movement

Movement In The Broader Crypto And Socio‑Political Context

Movement’s evolution mirrors larger shifts in crypto. The last decade has seen Bitcoin move from cypherpunk experiment to macro asset, DeFi move from curiosity to multi‑billion‑dollar ecosystem, and stablecoins move from exchange settlement assets to tools for payroll, commerce, and savings. In parallel, political and social movements have begun to engage with crypto themes: some embrace Bitcoin as a hedge against monetary debasement, others criticize crypto as speculative or destabilizing. As these narratives collide, protocols like Movement find themselves at the intersection of technology, finance, and politics.

Price movement remains the lens through which many observers view crypto. Tokens spike and crash based on macro data, protocol announcements, and, occasionally, rumors of insider selling or “token dumping.” Projects must now respond quickly to community concerns about onchain activity in team or investor wallets, publishing updates that clarify whether transfers are part of scheduled liquidity provisioning or something more concerning. This context matters for Movement as well; the team has at times had to reassure the market that transfers tied to bridge contracts or infrastructure provisioning did not represent token dumping, but rather operational actions in support of new products.

Meanwhile, the “Web3 movement” continues to push for more user control over data and value flows. At conferences like Web3 Summit, speakers highlight how decentralized networks can unbundle banking, media, and identity, shifting power from centralized intermediaries to users. Movement’s focus on emerging markets, feature‑phone wallets, and stablecoin‑based savings aligns with this ethos, even if its architecture remains anchored in partnerships with licensed financial institutions. The tension between decentralization and compliance is not going away; instead, it is becoming the defining design challenge for protocols that want to reach mainstream users.

Political movements, including Trump’s MAGA coalition, increasingly treat crypto as a wedge issue or fundraising tool. Campaigns discuss Bitcoin mining jobs, stablecoin regulation, and central bank digital currencies as part of their platforms, signaling that crypto policy is no longer niche. For Movement, which aspires to serve users in jurisdictions with volatile politics and capital controls, the evolution of U.S. and EU stablecoin laws will be critical. If major economies adopt clear, supportive frameworks for dollar‑backed stablecoins, networks like Movement could operate with greater certainty. If, instead, regulators clamp down on non‑bank stablecoin issuers or impose restrictive cross‑border rules, Movement’s model would need to adapt.

Risks, Challenges, And Open Questions

No explainer would be complete without tackling the risks and challenges facing Movement. On the regulatory front, the treatment of stablecoins remains unsettled in many jurisdictions. The European Union’s Markets in Crypto‑Assets Regulation (MiCA) introduces new categories for e‑money tokens and asset‑referenced tokens, imposing capitalization, disclosure, and supervision requirements on issuers. In the United States, competing legislative proposals would either bring stablecoin issuance under bank‑like charters or create bespoke licenses. Movement’s decision to work through licensed partners gives it some flexibility, but those partners themselves must navigate evolving rules in multiple jurisdictions.

Emerging markets add another layer of complexity. Governments facing dollarization pressure may be wary of apps that enable residents to hold dollar stablecoins and earn yield, especially if this undermines local monetary policy or capital controls. Banks and incumbents may lobby against stablecoin‑based fintechs, arguing that they pose systemic risks or facilitate illicit flows. Movement’s ability to operate in these environments will depend on its partners’ relationships with regulators, its own transparency about flows, and the perceived benefits to local economies.

Technically, Movement must manage the usual risks of blockchain infrastructure: smart contract bugs, consensus failures, and cross‑chain exploits. Its reliance on Move reduces certain categories of bugs but does not eliminate risk entirely. Integrations with NEAR Intents, RWA providers, and complex vault strategies introduce additional attack surfaces. A failure in any part of this stack—say, a bug in a vault contract, a misconfigured solver network, or a failure in a custody provider’s systems—could erode trust not just in a single product but in Movement’s brand as a settlement and yield layer.

Operationally, cross‑chain infrastructure has shown that sunsets and migrations can be painful. Bridging providers that once supported dozens of chains have had to consolidate, and users are sometimes left with stranded assets that require manual recovery processes, as seen when KelpDAO sunset bridging for rsETH across twenty networks and instituted a manual burn‑and‑redeem procedure with fixed fees. Movement’s intent‑based approach aims to mitigate these user‑experience pitfalls, but the underlying economics—liquidity provisioning, solver incentives, and security guarantees—must be robust to avoid similar headaches.

Competition is intense. Other ecosystems are also targeting emerging‑market payments and dollar savings, including Tron with its dominance in USDT transfers, Solana with high‑throughput USDC payments, and specialized chains like Celo that brand themselves as “mobile‑first” stablecoin platforms. Centralized players like Circle are investing heavily in payment interoperability, treasury products, and merchant tools around USDC. In this context, Movement’s differentiation—MoveVM safety, integrated RWA yield, licensed rails via partners, and user‑friendly intent routing—must be both real and recognized by builders and users.

Finally, the macro environment matters. In a world of high interest rates, tokenized T‑bills and CLOs offer attractive yields; in a low‑rate world, the spread between onchain yields and bank deposits narrows, making it harder to justify the added complexity and risk of DeFi. Political shifts can also affect stablecoins; a future administration hostile to crypto could impede bank partnerships or limit stablecoin issuance, while a friendly administration could accelerate adoption. Movement operates within these larger currents, and its long‑term trajectory will reflect both its own execution and the broader evolution of the crypto and regulatory landscape.

MoveVM is a newer execution environment with less battle-testing than EVM; M1 mainnet only launched in early 2026, meaning smart-contract surface area is largely unaudited at scale.

A market-maker token-dumping scandal preceded the Layer-1 pivot, and the 19% investor-token repurchase implies historically concentrated allocations that created structural sell pressure.

Actively securing money-transmitter licenses in the US, Canada and EU reduces regulatory exposure but also subjects Movement to ongoing compliance obligations and potential enforcement actions as a licensed payments entity.

The pivot away from a general-purpose Layer-2 toward a stablecoin settlement layer risks cannibalising existing DeFi liquidity integrations before the payments ecosystem reaches sufficient depth.

Movement has undergone at least two major strategic repositionings — Ethereum L2 to L1, then L1 to stablecoin settlement layer — compressing the window for ecosystem developers to build with confidence on a stable roadmap.

The token-dumping scandal and subsequent investor-allocation repurchase indicate persistent overhang risk; MOVE price remains sensitive to any on-chain treasury or team wallet movement.

How Users And Builders Can Engage With Movement Today

For individual users, interacting with Movement will typically occur through a partner neobank, wallet, or app rather than through direct RPC calls or block explorers. A user might download a wallet like Sorted, complete a KYC process with a local neobank or fintech, and deposit local currency that is converted into USDC or USDCx via Movement’s licensed rails. Within that app, the user could choose to hold their balance as a cash‑like stablecoin, allocate some portion to a conservative savings vault such as Yuzu Prime, and use a card or QR payment interface to spend funds with merchants that accept stablecoin payments. From the user’s perspective, the complexity of MoveVM, NEAR Intents, and RWA tokenization is hidden behind familiar metaphors like “wallet,” “savings,” and “pay.”

Builders engage with Movement at several levels. At the lowest level, developers can write Move smart contracts to deploy new protocols on Movement’s chains, leveraging the language’s resource model and safety features. At a higher level, they can integrate existing infrastructure such as MovePosition, Canopy, USDCx, and NEAR Intents via SDKs and APIs, building products that tap into Movement’s liquidity and yield without re‑implementing core primitives. For example, a remittance startup might use Movement for cross‑border settlement while building a custom front‑end that integrates local identity verification, compliance checks, and fiat cash‑out options. A merchant‑focused startup could integrate Stableyard’s checkout components and DopePay’s QR payment flows to enable stablecoin acceptance at physical points of sale.

Developers and community members can also connect through Movement Global Hubs, a program designed to “level up Movement communities around the world.” While details vary by hub, the initiative generally includes local meetups, hackathons, education efforts around Move and DeFi, and support for builders exploring Movement as a platform. These hubs are particularly important in regions where Movement hopes to become a default backend for fintechs and wallets, as they help cultivate local expertise and user feedback.

For investors and institutions, engagement can range from direct participation in RWA vaults to strategic partnerships. Asset managers might view Movement as a distribution channel for tokenized fixed income products, while banks and payment processors might partner with Movement to extend their reach into emerging markets without building onchain capabilities from scratch. At the same time, institutions must perform rigorous due diligence on Movement’s governance, security, and regulatory posture, especially in light of past episodes in crypto where misaligned incentives or opaque structures led to losses.

Outlook

Movement’s trajectory encapsulates a broader pivot in crypto from infrastructure‑for‑its‑own‑sake to infrastructure in service of concrete financial use cases. By reorienting around stablecoin settlement, RWA‑backed yield, and licensed payment rails for emerging markets, the project has staked out a differentiated position in a crowded field of L1s and L2s. Its success will depend on execution across several dimensions: maintaining technical robustness in its Move‑based stack, scaling integrations with neobanks and wallets that reach real users, navigating regulatory change across multiple jurisdictions, and proving that its curated yield offerings can deliver sustainable, transparent returns.

If stablecoin usage continues to shift from speculative transfers toward real‑world payments, payroll, and savings, networks like Movement that specialize in settlement and yield for those flows could become increasingly important. Integration with intent‑based systems like NEAR Intents and experience layers like Stableyard and DopePay suggests that Movement understands the importance of invisible infrastructure and frictionless UX. At the same time, competition, regulation, and macroeconomic cycles will pose ongoing challenges.

For a crypto news audience, Movement is worth watching not just as a token chart, but as a case study in how blockchain projects adapt when initial narratives—such as “yet another Ethereum L2”—run out of steam. Its reinvention as a stablecoin settlement and yield layer for emerging markets reflects both the pressures of the market and the opportunities ahead as onchain finance moves closer to everyday life.

Latest Movement news

Movement pivots toward global payments and remittances, securing licensed rails across the US, Canada and EU while repurchasing 19% of investor-allocated tokens in a major strategic shifta16z reveals stablecoin usage shifting from transfers to real-world payments, signaling maturation of onchain finance as adoption expands beyond trading and capital movementReal-world finance is moving onchain, but most DeFi infrastructure isn’t ready for institutional finance. Tokenized assets, lending, and payments need trusted settlement and seamless capital movement Here’s how USDC + CCTP on Pharos make it possible 🧵Enry’s Island unveils “Enry’s Island Adventures”: Venture capital becomes a videogame and launches the “Strap” movement on Kickstarter.STBL CEO Avtar Sehra heads to CNBC Converge to outline how stablecoins and tokenization will reshape global finance, as onchain systems redefine value issuance and movementMovement goes live on M1 mainnet with USDCx, a native USDC stablecoin built on Circle's xReserveSources

- https://www.movementnetwork.xyz

- https://oakresearch.io/en/reports/protocols/movement-move-ethereum-s-first-layer2-movevm

- https://cryptonews.net/news/market/32953782/

- https://thedefiant.io/news/blockchains/movement-pivots-to-layer1-blockchain

- https://x.com/canopyxyz

- https://x.com/near_intents/status/2067265431468192144

- https://www.movementnetwork.xyz/article/movement-secures-money-transmitter-licenses-and-rebrands-as-the-global-settlement-and-yield-layer-for-stablecoins

- https://telemetr.io/es/channels/1968050683-heartysender/posts?cursor=ICg%3D

- https://secureshift.io/crypto-news/movement-pivots-to-stablecoin-payments-as-the-layer-2-boom-loses-momentum

- https://www.movementnetwork.xyz/article/yuzu-money-joins-movement-network-as-a-day-1-canopy-yield-provider

- https://www.movementnetwork.xyz/article/movement-invests-in-stableyard-to-build-the-end-to-end-experience-layer-of-stablecoin-payments

- https://www.movementnetwork.xyz/article/movement-integrates-near-intents-to-enable-cross-chain-yield-without-the-complexity

- https://x.com/KelpDAO/status/2068047308806385688

- https://x.com/movement_xyz/status/2054608962327081362

- https://www.circle.com/blog/payment-interoperability-the-missing-layer-for-global-money-movement

- https://www.globenewswire.com/news-release/2026/03/25/3262226/0/en/movement-launches-usdcx-the-native-usdc-backed-stablecoin-on-m1-mainnet.html

- https://www.movementnetwork.xyz/article/movement-selects-moveposition-as-its-canonical-money-market

- https://www.prnewswire.com/news-releases/movement-secures-licensed-payment-rails-access-in-the-us-canada-and-eu-commits-to-stablecoin-settlement-and-yield-infrastructure-for-emerging-markets-302787887.html

- https://www.movementnetwork.xyz/article/movement-global-hubs-global-program

- https://x.com/dopepayme

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…